Embed Size (px)

Citation preview

Ocean Carrier Issues and Perspectives Shifting International Trade Routes, January 23 rd

Introduction

Dean Rodin

Managing Director – Maersk Line Caribbean Sea Cluster

page 2

Maersk Line at a glance

• 596 vessels with a capacity of 2.6m TEU

transporting 8.5m FFE generating a total

revenue of USD 27bn in 2012

• Enabling global growth with a total value of

goods transported estimated at USD 650bn in

2012

• 31,000 employees (incl. 6,000 sea farers) in

362 office locations globally, serving 67,000

customers world wide Note: Based on 2012-data. Total number of vessels as of Q2 2013 incl. multipurpose vessels. Value of shipping

goods estimated as Maersk Line capacity market share (15%) of total value of global container imports by sea

Source: Alphaliner, Maersk Line, Seabury

Maersk Line trade routes

page 3

page 4

Liner Shipping is today a

Commoditized Industry and Low

Cost is the Key to Success

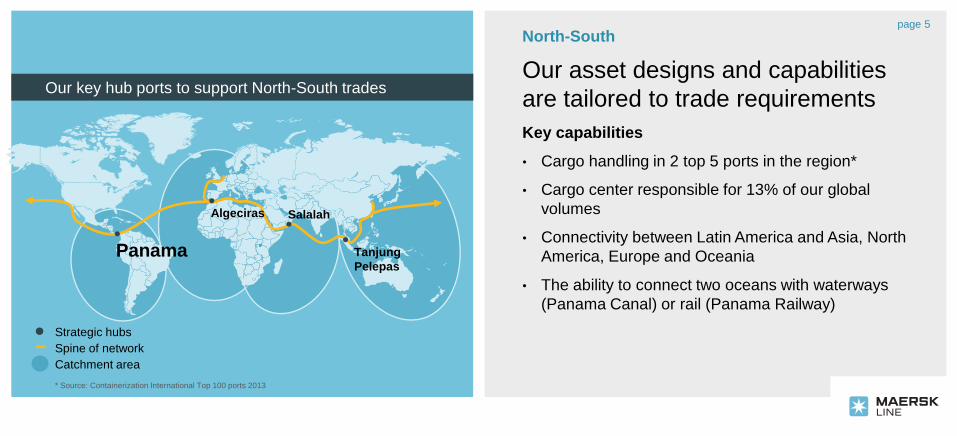

Key capabilities

• Cargo handling in 2 top 5 ports in the region*

• Cargo center responsible for 13% of our global

volumes

• Connectivity between Latin America and Asia, North

America, Europe and Oceania

• The ability to connect two oceans with waterways

(Panama Canal) or rail (Panama Railway)

Salalah

Tanjung

Pelepas Panama

Algeciras

Catchment area

Spine of network

Strategic hubs

North-South

Our key hub ports to support North-South trades

Our asset designs and capabilities

are tailored to trade requirements

* Source: Containerization International Top 100 ports 2013

page 5

Network Optimization is a game

changer

Growing with the market

• Maersk Line adjusts its network and deployment

regularly to ensure cost and environmental

efficiency

• Effects on deployment changes are felt across the

Maersk Line network

• These changes have to make sense from a

financial, environmental and commercial

perspective

Source: Maersk Line

page 6

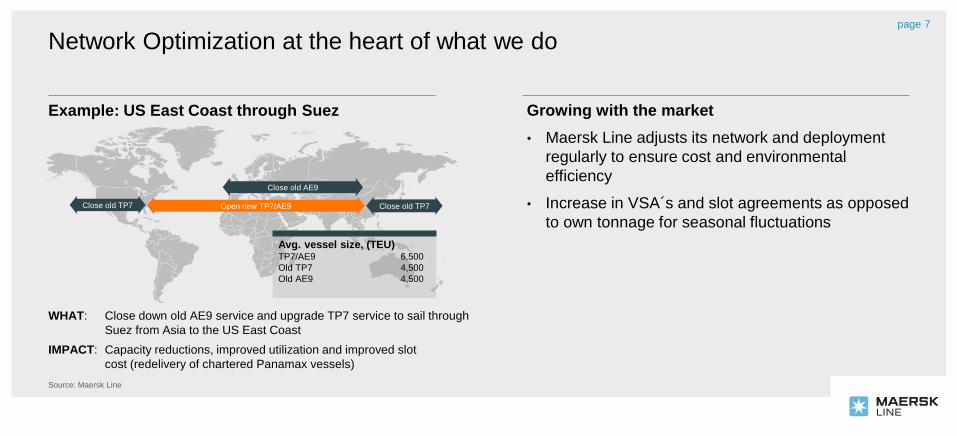

Source: Maersk Line

Close old TP7 Close old TP7

Close old AE9

Open new TP7/AE9

Example: US East Coast through Suez

WHAT: Close down old AE9 service and upgrade TP7 service to sail through

Suez from Asia to the US East Coast

IMPACT: Capacity reductions, improved utilization and improved slot

cost (redelivery of chartered Panamax vessels)

Avg. vessel size, (TEU) TP7/AE9 6,500

Old TP7 4,500

Old AE9 4,500

Network Optimization at the heart of what we do page 7

Growing with the market

• Maersk Line adjusts its network and deployment

regularly to ensure cost and environmental

efficiency

• Increase in VSA´s and slot agreements as opposed

to own tonnage for seasonal fluctuations

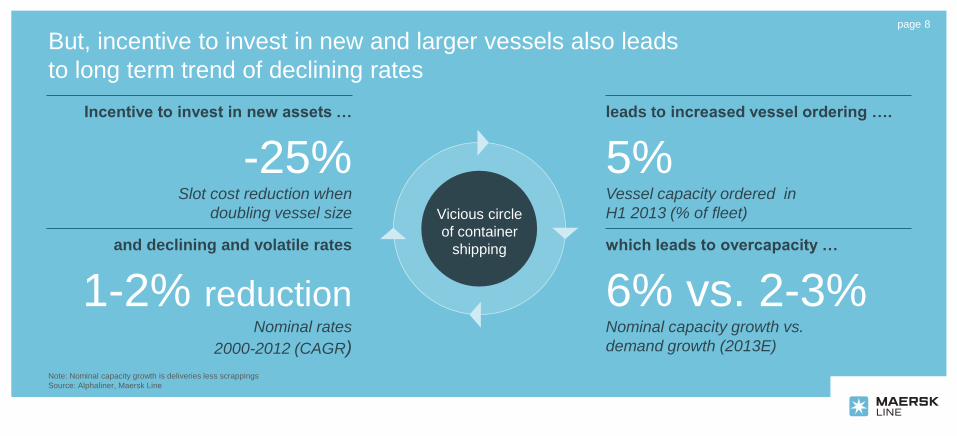

Incentive to invest in new assets … leads to increased vessel ordering ….

and declining and volatile rates which leads to overcapacity …

But, incentive to invest in new and larger vessels also leads

to long term trend of declining rates

-25% Slot cost reduction when

doubling vessel size

5% Vessel capacity ordered in

H1 2013 (% of fleet)

6% vs. 2-3% Nominal capacity growth vs.

demand growth (2013E)

1-2% reduction Nominal rates

2000-2012 (CAGR)

Note: Nominal capacity growth is deliveries less scrappings

Source: Alphaliner, Maersk Line

Vicious circle

of container

shipping

page 8

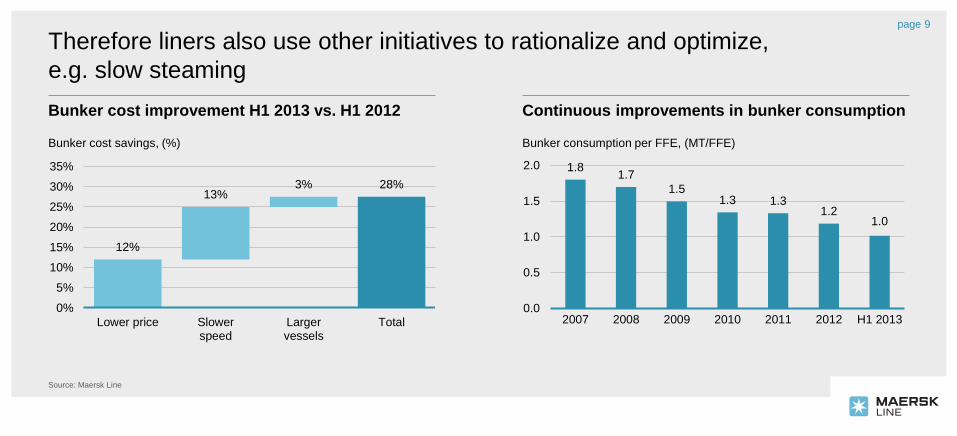

Therefore liners also use other initiatives to rationalize and optimize,

e.g. slow steaming

Source: Maersk Line

1.8 1.7

1.5 1.3 1.3

1.2 1.0

0.0

0.5

1.0

1.5

2.0

2007 2008 2009 2010 2011 2012 H1 2013

Continuous improvements in bunker consumption

Bunker consumption per FFE, (MT/FFE)

Bunker cost improvement H1 2013 vs. H1 2012

12%

13% 3% 28%

Lower price Slowerspeed

Largervessels

Total

0%

5%

10%

15%

20%

25%

30%

35%

Bunker cost savings, (%)

page 9

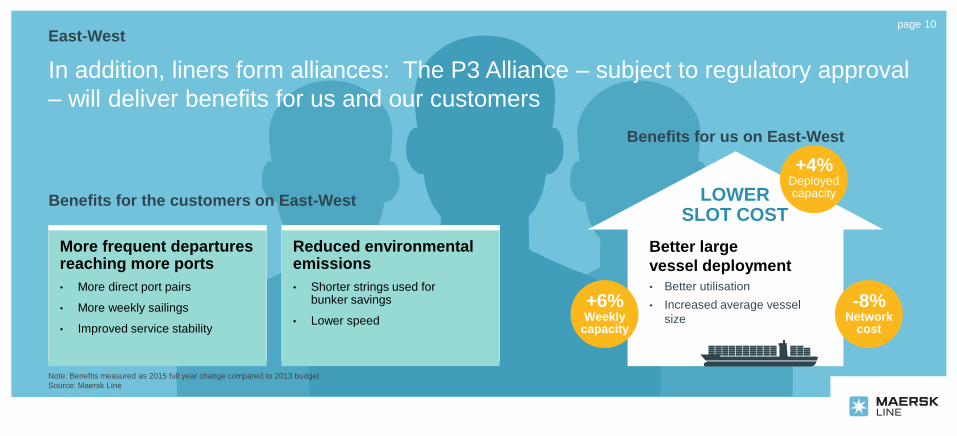

Better large

vessel deployment

• Better utilisation

• Increased average vessel

size

In addition, liners form alliances: The P3 Alliance – subject to regulatory approval

– will deliver benefits for us and our customers

East-West

Benefits for the customers on East-West

Benefits for us on East-West

LOWER SLOT COST

More frequent departures reaching more ports

• More direct port pairs

• More weekly sailings

• Improved service stability

Reduced environmental emissions

• Shorter strings used for bunker savings

• Lower speed

Note: Benefits measured as 2015 full year change compared to 2013 budget.

Source: Maersk Line

+4% Deployed capacity

-8% Network

cost

+6% Weekly

capacity

page 10

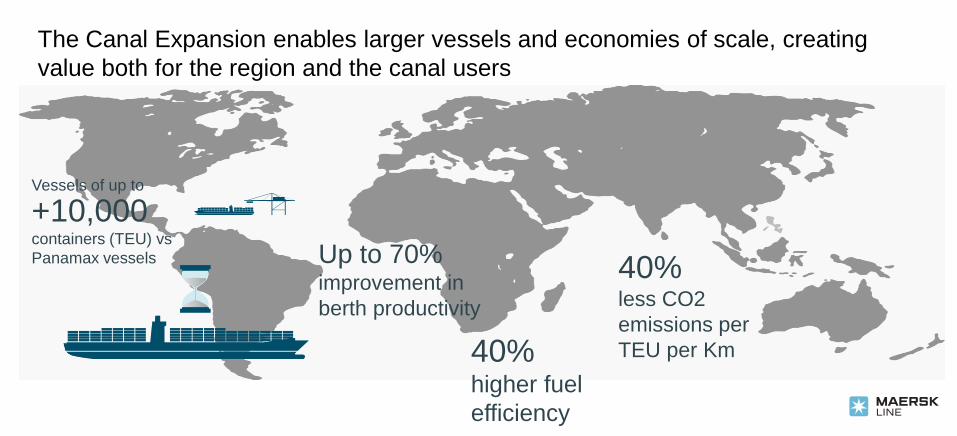

The Canal Expansion enables larger vessels and economies of scale, creating

value both for the region and the canal users

Up to 70% improvement in

berth productivity

Vessels of up to

+10,000

containers (TEU) vs

Panamax vessels

40% higher fuel

efficiency

40% less CO2

emissions per

TEU per Km

page 12

To encourage larger vessels get

deployed through the canal, conditions

must support same

• Infrastructure

• Cost competitiveness

• Demand growth

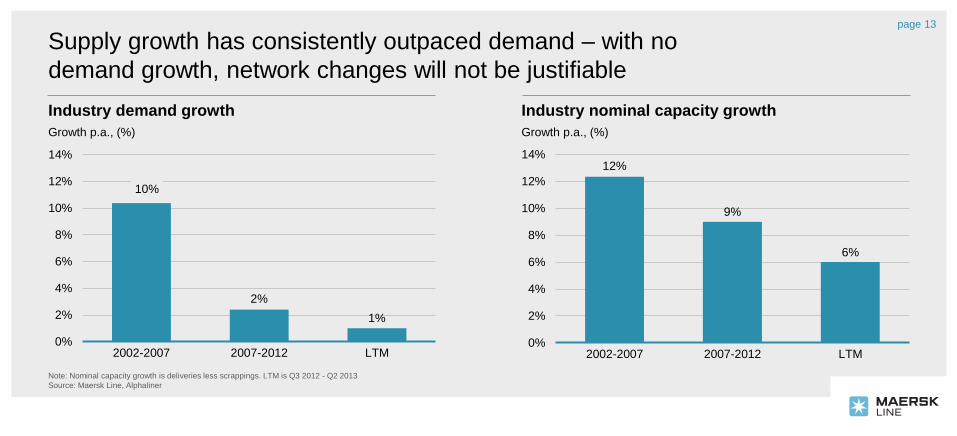

12%

9%

6%

0%

2%

4%

6%

8%

10%

12%

14%

2002-2007 2007-2012 LTM

10%

2%

1%

0%

2%

4%

6%

8%

10%

12%

14%

2002-2007 2007-2012 LTM

Industry demand growth

Note: Nominal capacity growth is deliveries less scrappings. LTM is Q3 2012 - Q2 2013

Source: Maersk Line, Alphaliner

Growth p.a., (%)

Industry nominal capacity growth

Growth p.a., (%)

page 13

Supply growth has consistently outpaced demand – with no

demand growth, network changes will not be justifiable

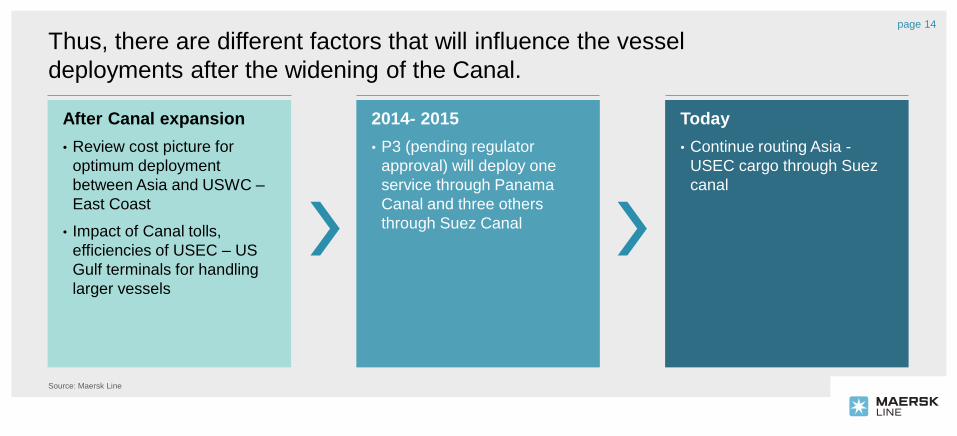

Thus, there are different factors that will influence the vessel

deployments after the widening of the Canal.

Source: Maersk Line

After Canal expansion

• Review cost picture for

optimum deployment

between Asia and USWC –

East Coast

• Impact of Canal tolls,

efficiencies of USEC – US

Gulf terminals for handling

larger vessels

Today

• Continue routing Asia -

USEC cargo through Suez

canal

2014- 2015

• P3 (pending regulator

approval) will deploy one

service through Panama

Canal and three others

through Suez Canal

page 14

Thank you

![T82 - Ocean Carrier Booking: Outbound Process Port to Portsapidp/012002523100005931022015E/... · Send Booking to Ocean Carrier [NWBC]; SAP TM Menu: NWBC Freight Order Management](https://img.pdfslide.us/doc/110x75/5a9f7b9c7f8b9a62178cc80d/t82-ocean-carrier-booking-outbound-process-port-to-port-sapidp012002523100005931022015esend.jpg)