Embed Size (px)

Citation preview

Resources and Energy Quarterly September 2016

Further Information

For more information on data or government initiatives please access the report from the Department’s website at:

www.industry.gov.au/oce

Chapter Authors

Macroeconomic outlook: Kristy Krautler and Ana Porta Cubas

Resources and energy overview: Marco Hatt and Kieran Bernie

Steel, iron ore and nickel: Monica Philalay

Metallurgical and thermal coal: Gayathiri Bragatheswaran

Oil and gas: Nikolai Drahos

Uranium: Mark Gibbons

Gold and copper: Joseph Moloney

Aluminium, alumina, bauxite and zinc: Thuong Nguyen

Acknowledgements

The authors would like to acknowledge the contributions of:

Mark Cully

Tim Bradley

Ross Lambie

Nicole Thomas

David Whitelaw

Laura Ling

Katya Golobokova

Cover image source: Shutterstock

Error! No text of specified style in document.OCE Report Template 1

© Commonwealth of Australia 2016

ISSN 1839-5007 [ONLINE]

Vol. 5, no. 5

This work is copyright. Apart from any use as permitted under the Copyright Act 1968, no part may be reproduced or altered by any process without prior written permission from the Australian Government. Requests and inquiries concerning reproduction and rights should be addressed to:

Department of Industry, Innovation and Science, GPO Box 9839, Canberra ACT 2601 or by emailing [email protected]

Creative Commons Licence

With the exception of the Coat of Arms, this publication is licensed under a Creative Commons Attribution 3.0 Australia Licence.Creative Commons Attribution 3.0 Australia Licence is a standard form license agreement that allows you to copy, distribute, transmit and adapt this publication provided that you attribute the work.

A summary of the licence terms is available from: http://creativecommons.org/licenses/by/3.0/au/deed.en

The full licence terms are available from: http://creativecommons.org/licenses/by/3.0/au/legalcode

The Commonwealth’s preference is that you attribute this publication (and any material sourced from it) using the following wording:Source: Licensed from the Commonwealth of Australia under a Creative Commons Attribution 3.0 Australia Licence.

Error! No text of specified style in document.OCE Report Template 2

ContentsForward

Executive summary

Macroeconomic outlook

Resource and energy overview

Steel

Iron ore

Metallurgical coal

Thermal coal

Gas

Oil

Uranium

Gold

Aluminium, alumina and bauxite

Copper

Nickel

Zinc

Trade summary charts

Appendix

Error! No text of specified style in document.OCE Report Template 3

ForewordPrices for most construction and steel making raw materials continued to grow in the last three months — despite expectations of decline — because of unexpectedly resilient demand from China’s construction sector and unforeseen supply disruptions.

The speculative activity in China’s commodity futures markets that led to high spot price volatility in the first half of 2016 has tapered off. This was supported by measures to reduce speculative trading, including increased commission fees, margin requirements and trading restrictions. Commodity prices should therefore better reflect market fundamentals going forward.

China’s economy — and its demand for construction raw materials — is slowing as it transitions away from investment-led growth to consumption-led growth. While any slowdown in the short term remains sensitive to government policy and stimulus measures, the likelihood of significant increases in demand from China for resource commodities is limited.

Australia’s suppliers are well-placed to satisfy demand for resources and energy over the next fifteen months, despite difficult operating conditions. In particular, production of most bulk commodities is forecast to increase, even as prices decline. As a result, Australia’s earnings from resources and energy exports are forecast to increase by 12 per cent to $176 billion in 2016–17.

Mark CullyChief EconomistDepartment of Industry, Innovation and Science

Error! No text of specified style in document.OCE Report Template 4

1. Macroeconomic Outlook

1.1 World economy

World economic conditions were generally softer in the June quarter of 2016. Europe experienced better-than-expected growth, while growth in the United States was weak. Productivity growth in most advanced economies remains slow. Global industrial activity and trade have also been lacklustre. In July, the volume of world trade fell 0.9 per cent year-on-year.

Poor trade outlooks and the continued uncertainty following the Brexit have led the International Monetary Fund (IMF) to make downward revisions to economic growth forecasts. The global economic growth outlook was marked down by 0.1 percentage point to 3.1 per cent in 2016 and 3.4 per cent in 2017. This is attributed to a weakened outlook for advanced economies, which are forecast to grow by 1.8 per cent in 2016 and 2017. The outlook remains unchanged for emerging markets and developing countries, at 4.1 per cent in 2016 and 4.6 per cent in 2017.

A number of ongoing risks continue to keep global economic prospects low. These include continued uncertainty for Europe and the United Kingdom following the recent Brexit referendum, China’s continued reliance on borrowing to increase growth, and weak trade patterns coupled with growing protectionist sentiment around the world.

1.2 Outlook for key economies

China’s outlook remains steady despite weak private investment

Chinese growth remained unchanged in the June quarter, growing 6.7 per cent, year-on-year. Despite steady growth figures, investment and new construction has slowed as the stimulus from earlier in the year fades. The outlook for residential construction is discussed in Box 1. Private fixed asset investment grew only 2.1 per cent from January to July, due to weak non-state firm investment which fell by 1.0 per cent year-on-year.

In an effort to stimulate growth through private investment, the Chinese Government has made cost cutting a key policy goal. By financing local government debt, the central government intends to help boost revenues so local governments can cut business taxes. In addition to the central bank reducing financing costs, the labour ministry has lowered social pension payment obligations for business. The shift from business taxes to value-added taxes reduces the burden for business by 500 billion yuan (US$75 billion) a year. This should significantly cut business costs and encourage private non-state firm investment, allowing the economy to pursue growth in areas outside the housing market.

Figure 1.1: World trade volumes vs world trade values

Recent data suggests that while state-firm investment is weak, investment growth remains strong for state-owned enterprises. Competition with state firms and restricted access to some markets, particularly in the services

Error! No text of specified style in document.OCE Report Template 5

sector, is preventing private investment from taking full advantage of these reforms.

China’s imports from the rest of the world performed unexpectedly well in August, rising 1.5 per cent year-on-year, marking the first increase in 22 months. The rise was largely attributed to a stockpiling of resources as Chinese producers are expecting commodity prices may start to pick up in some areas. This follows a better-than-expected result for China’s manufacturing activity in August with the official index of manufacturing activity reaching 50.4 indicating the sector is expanding. These positive indicators for both imports and manufacturing may indicate domestic demand is improving.

Box 1.1: The outlook for the Chinese housing sector

The Chinese housing sector has experienced marked growth since its liberalisation in the late 1990s, when the government decision to abolish employer-allocated housing spurred a residential construction boom. Much of this growth in the sector has continued to be policy driven, and there are questions about the future sustainability of growth in the absence of policy interventions. Any slowdown in housing construction poses risks for exports of commodities used in construction, including iron ore, metallurgical coal and copper. Australia is highly dependent on the Chinese demand for construction raw materials—over 80 per cent of Australia’s iron ore exports go to China.

Chinese governments have traditionally been highly involved in modulating demand in the housing sector, including managing differences in demand between cities. One of the Central Government’s five goals for 2016 was to reduce housing inventories and stabilise the housing market. In early 2016, it undertook a number of steps, most notably lowering interest rates and business taxes in cities other than the more desirable cities of Beijing, Shanghai, Guangzhou and Shenzhen. The Central Bank also eased lending standards, lowering the necessary mortgage down-payment for first homes from 25 to 20 per cent and from 40 to 30 per cent for second home buyers. These stimulus measures resulted in a spike in construction completions growth in early 2016, following a decline post 2012.

The future growth of the Chinese housing sector is uncertain. The Chinese Central Government is focussed on moving from investment to consumption-led growth, and earlier this year stated no excessive stimulus would be required to achieve their growth targets in the immediate future. Additionally, the housing market has now matured and there is oversupply in the less desirable smaller and inland cities. It is therefore likely that the Chinese government will provide only a light touch in modulating housing construction in the medium term. As a result, the current uptick in China’s construction activity and commodity demand is unlikely to be sustained, which will place downward pressure on commodity export volumes over the outlook period. The outlook is sensitive to Central Government policy, and could change if the Government decides to once again stimulate housing demand through monetary and fiscal measures.

Figure 1.2: Floor space of completed residential buildings, annual growth

Error! No text of specified style in document.OCE Report Template 6

However, weakness in exports (which dropped 2.8 per cent year-on-year in August) and overcapacity in many sectors will continue to be a challenge for China’s economic transition.

China’s economic growth outlook remains steady from previous forecasts at 6.6 per cent for 2016 and 6.2 per cent in 2017. The growth forecast for 2016 falls within the government’s target of between 6.5 and 7.5 per cent.

1.3 Indian manufacturing continues to grow strongly

India’s GDP growth slowed to 7.1 per cent year-on-year in the June quarter. Strong growth in government spending and net exports were offset by slowdowns in both private consumption and investment growth. Consumption growth dropped to 6.7 per cent year-on-year, compared to the previous quarter result of 8.3 per cent. Private investment fell by 3.1 per cent year-on-year.

Sectors that contributed to lower-than-expected growth include mining and construction. Mining sector output declined by 0.4 per cent due to falls in the production of crude oil and natural gas. This is a significant drop for the mining sector, compared to previous growth of 8.3 per cent in the same quarter last year. Growth in construction slowed to 1.5 per cent, compared to growth of 5.6 per cent in same quarter last year.

Manufacturing continued to grow strongly. The sector grew 9.1 per cent in the June quarter year-on-year. This result was also reflected in the official index of factory activity which reached 52.6 in August, the highest level since July 2015. The index measures manufacturing performance with a result above 50 indicating that the sector is expanding.

Despite slowing growth in the June quarter, the forecast for India’s economy remains robust. Economic growth will be supported by a number of structural reforms, including the passing of a bill introducing a national Goods and Services Tax (GST) which is expected to commence in April 2017. It is expected this reform will add between 0.8 per cent and 1.7 per cent to economic growth following implementation in April 2017. The Indian economy is expected to grow by 7.4 per cent in both 2016 and 2017.

Figure 1.3: China’s imports and manufacturing activity

Figure 1.4: India’s construction and manufacturing gross value added

1.4 Japan’s exports remain weak amidst an appreciating yen

Japan’s economy grew 0.6 per cent year-on-year in the June quarter. Net exports and business investment remained weak as a higher yen hurt exporters, and businesses remained cautious. Japan remained in deflation, with consumer prices falling 0.5 per cent year-on-year in July. Meanwhile, industrial production fell 3.8 per cent year-on-year.

At the Bank of Japan’s September meeting, the governor chose not to further lower the -0.1 per cent interest rate on bank deposits. The governor noted that ultra-low long-term interest rates were hurting the investment returns of insurance and pension companies and damaging business sentiment.

Error! No text of specified style in document.OCE Report Template 7

The Japanese Government has announced stimulus measures of 13.5 trillion yen (US$13 billion) in the form of cash payouts to low-income earners and infrastructure spending. In doing so, the government hopes to encourage greater spending to reverse the trend of deflation and encourage economic growth.

These measures have supported an appreciation of the yen, which make Japan’s exports more expensive for other countries. Exports fell 14 per cent year-on-year in July, marking the tenth month in a row for falling exports. As a result, the IMF’s growth forecast for Japan in 2016 has been reduced by about 0.2 percentage points to 0.3 per cent.

A delay in the increase of the consumption tax from April 2017 to October 2019 has improved growth prospects for Japan in 2017. However, any benefit to growth will be moderated by a higher yen that continues to hurt exports.

1.5 South Korea faces increased competition from Chinese manufacturing

South Korea’s economy picked up in the June quarter, growing 3.1 per cent year-on-year. Both private consumption and investment increased, though exports growth remained soft due to weak global demand.

Slowing demand from China has also hurt South Korean exporters. As Chinese manufacturers move up the value chain and produce higher quality goods, this could result in increased competition for South Korean exports in the future.

Figure 1.5: Growth in Japan’s exports

Figure 1.6: South Korea’s trade price indices

In an effort to stimulate growth, the South Korean government announced an 11 trillion won (US$10 billion) supplementary budget in August. The stimulus package is intended to help reduce the negative impact of corporate restructuring on the job market and complement the rate cut from the Bank of Korea in June.

South Korea’s economy is forecast to grow by 2.7 per cent in 2016, and 2.9 per cent in 2017. An unexpectedly sharp slowdown in China remains the biggest risk for South Korea, as China accounts for one quarter of South Korean exports. A planned restructuring of major industries may also lead to higher unemployment in the short run, and growing household debt could constrain private consumption.

1.6 United States shows gradual improvement

The United States (US) economy grew by 1.2 per cent year-on-year in the June quarter—the slowest in three years—although other economic indicators suggest stronger economic conditions. In particular, the labour market continues to show improvement.

Error! No text of specified style in document.OCE Report Template 8

US interest rates remain low with the Federal Reserve choosing not to increase interest rates at their September meeting. However, we expect a rate increase to be announced later in 2016.

An increase in the real US interest rate is generally associated with falling commodity prices (when denominated in US dollars) and an increase in the value of the US dollar. While a decline in commodity prices is negative for Australia’s commodity export revenue, an increase in the value of the US dollar is positive. These two effects are expected to broadly cancel out when considering the impact on Australian dollar commodity export revenues.

The US economy is forecast to grow by 2.2 per cent in 2016 and 2.5 per cent in 2017. Conditions in the US labour market are expected to remain relatively strong and should continue to support growth of consumption. This is likely to offset the ongoing weakness in overall business investment.

Figure 1.7: Unemployment rate and growth in personal incomes in the US

1.7 Europe faces uncertainty following Brexit decision

Economic growth in the European Union was 0.4 per cent in the June quarter, 1.8 per cent year-on-year. Economic growth is forecast to average 1.8 per cent in 2016, before increasing slightly to 1.9 per cent in 2017.

Heightened uncertainty following the United Kingdom’s (UK) decision to leave the European Union (EU) is putting downward pressure on growth. The UK’s decision is unlikely to have significant implications outside the EU. However, the decision led to the IMF downgrading growth prospects for the UK by 0.2 per cent in 2016 and 0.9 per cent in 2017.

Continued global uncertainties, weakening exports, and low consumer confidence are expected to continue to put pressure on the growth outlook. Fiscal constraints or reluctance to increase fiscal stimulus will put greater pressure on the European Central Bank to provide additional support to increase inflation and boost growth. In September, the Bank left rates unchanged, but the market continues to expect there will be further stimulus announced, most likely in December.

Error! No text of specified style in document.OCE Report Template 9

Table 1.1: Key world macroeconomic assumptions

Per cent 2013 2014 2015 2016 a 2017 a

Economic growth b

Advanced economies 1.2 1.9 1.9 1.8 1.8United States 1.5 2.4 2.4 2.2 2.5Japan 1.4 0.0 0.5 0.3 0.1European Union 28 0.3 1.4 2.0 1.8 1.9

Germany 0.4 1.6 1.5 1.6 1.2France 0.7 0.6 1.3 1.5 1.2United Kingdom 2.2 3.1 2.2 1.7 1.3

South Korea 2.9 3.3 2.6 2.7 2.9New Zealand 1.7 3.0 3.4 2.0 2.5Chinese Taipei 2.2 3.9 0.7 1.5 2.2

Emerging economies 4.9 4.6 4.0 4.1 4.6Non-OECD Asia 6.9 6.8 6.6 6.4 6.3

South East Asia d 5.1 4.6 4.8 4.8 5.1China e 7.7 7.3 6.9 6.6 6.2India 6.6 7.2 7.6 7.4 7.4

Latin America & Caribbean 3.0 1.3 0.0 –0.4 1.6Middle East 2.1 2.6 2.3 2.9 3.3

World c 3.3 3.4 3.1 3.1 3.4

Inflation rate b

United States 1.5 2.2 0.1 1.1 1.8Notes: a Assumption; b Change from previous period; c Weighted using 2012 purchasing power parity (PPP) valuation of country gross domestic product by IMF; d Indonesia, Malaysia, Philippines, Thailand and Vietnam; e Excludes Hong Kong Source: IMF (2016) World Economic Outlook

Error! No text of specified style in document.OCE Report Template 10

2. Resources and energy overview

2.1 Revisions to the outlook

The value of Australia’s resources and energy exports is forecast to increase by 12 per cent to $176 billion in 2016–17, revised up from the previous forecast of $163 billion. The upward revision in export values reflects revisions to the underlying price forecasts, not volumes.

This set of forecasts has been prepared against a backdrop of slightly higher prices than in the June quarter. The increase in prices primarily reflects unexpected persistence in the effects from the housing stimulus in China, in addition to weather and infrastructure related supply disruptions.

The most material revisions to the outlook for 2016–17 have been made to metallurgical coal and iron ore. The price of metallurgical coal has been revised up from US$85 a tonne to US$118 in 2016–17, adding $8 billion to Australia’s resource and energy export earnings over the year. The price of iron ore has been revised up from US$43 a tonne (FOB Australia) to US$47 a tonne adding US$4.7 billion to export revenues.

However, the recent price increases in metallurgical coal and iron ore are driven by temporary factors. The price of both commodities is expected to decline from current levels over the outlook period to the end of 2017.

Figure 2.1: Export earnings

2.2 Market summary

Conditions for Australian producers remained challenging in the first half of 2016, despite some lift in commodity prices driven by increased activity in China’s construction sector. Australia’s production of LNG and bulk commodities is forecast to increase over the outlook period as significant investments in new capacity undertaken over the last decade begin to deliver additional output. As a result, export earnings are forecast to increase by 12 per cent in 2016–17, to $176 billion.

2.3 Prices

Resource and energy commodity prices unexpectedly continued to grow since the release of June edition of the Resources and Energy Quarterly. While prices remain well below their mining boom peaks, most commodity spot prices are now higher than they were a year ago.

A resurgence in demand from China’s residential construction sector has supported higher prices for raw construction materials such as iron ore, metallurgical coal, copper and zinc; while the consolidation of China’s domestic coal mines has driven increased seaborne demand for thermal and metallurgical coal. Recent spikes in coal prices were also supported by production disruptions in Queensland. Gold prices also rose, fuelled by increased global economic uncertainty.

Error! No text of specified style in document.OCE Report Template 11

Prices for Australia’s resource and energy commodity exports reached 13 month highs in August 2016. Prices for bulk commodities and base metals both increased, although the increase was most pronounced in the bulks. The RBA commodity price index (non-rural component) increased 16 per cent in the first 8 months of the year in US dollar terms. However, an appreciation in the value of the Australian dollar has seen the index increase by only 11 per cent in Australian dollar terms.

Bulk commodity prices are generally forecast to remain relatively flat or fall slightly over the next 15 months, as weaker consumption growth compounds the effect of ample supply. The outlook for metals is slightly more positive, largely as a result of a relatively stronger consumption forecast. Prices for energy commodities are forecast to increase slightly over the outlook period, but excess capacity on the supply-side is likely to continue to constrain the pace and extent of any increases.

Figure 2.2: Commodity price movements

Also putting downward pressure on US dollar denominated commodity prices is the growing potential for the US Federal Reserve to raise interest rates. However, with the Australian dollar expected to decline from an US interest rate hike, Australian dollar commodity revenues are likely to be relatively unaffected by any such decision.

Risks to commodity prices over the outlook period remain linked to developments in China, where the full effect of efforts to remove excess production capacity in the thermal coal and steelmaking sectors remains unclear. In the near term, commodity price risks are also likely to depend on uncertainty surrounding the resilience of recent growth in the Chinese construction sector. More generally, commodity prices are expected to remain sensitive to the pace of the broader economic transition occurring within the Chinese economy.

Outside China, uncertainty about prospects for economic growth and the consequences of recent developments in Europe are also likely continue to influence commodity price risks.

2.4 Consumption

Consumption of commodities used in construction—including iron ore, metallurgical coal and copper—continues to be supported by a resurgence in demand from China’s residential construction sector. In the first seven months of 2016, the volume of newly started residential floor space in China grew 13 per cent year-on-year, largely as a result of increases associated with government stimulus measures introduced earlier in the year.

However, the uptick in China’s construction activity is unlikely to persist, and the use of commodities in the sector is forecast to decline over the outlook period. Despite a modest draw down in inventories in the first half of 2016, the residential property market remains oversupplied. Efforts by the Chinese Government to reduce excess steelmaking capacity may also see some reduction in demand for iron ore and metallurgical coal.

Error! No text of specified style in document.OCE Report Template 12

In general, metals consumption is forecast to increase over the next 15 months, driven by investments in electricity infrastructure and growing demand for household appliances. Growth in metals consumption will continue to be concentrated in emerging economies, and remains sensitive to changes in economic conditions.

Growth in global energy consumption is also expected to be driven by increased consumption in developing economies. However, the prospects for trade in energy commodities are mixed. Global thermal coal imports are forecast to decline in 2016 and 2017, as India reduces its dependence on imports and demand growth in China eases. In contrast, global imports of LNG are forecast to increase strongly, growing to 288 million tonnes in 2017, supplied by increased export capacity in Australia and the United States.

2.5 Production

Lower commodity prices have caused global production growth to slow markedly in recent years, with producers deferring or cancelling investment in additional capacity to reduce costs.

Although the price recovery in the first half of 2016 delivered some support to producers, the generally subdued outlook for prices means producers are likely to remain under financial pressure in the near-term.

In general, global bulk commodities markets are likely to remain well-supplied over the outlook period as major investments undertaken over the last decade reach full production capacity. However, there may be some tightness in global coal supply in the near-term due to production constraints in Indonesia and further declines in the volume of exports from the United States.

Production volumes for metals commodities are also generally expected to grow over the next 15 months. Gold production is forecast to increase, supported by further growth in recycled supply. Copper supply is also expected to grow, as additional supply from new investments in Peru and Kazakhstan offsets declines elsewhere.

In contrast, world nickel production is forecast to fall over the remainder of 2016 as a result of shut-downs in the Philippines. Nickel production is forecast to increase again in 2017 in line with returning capacity in the Philippines and Indonesia.

Markets for energy commodities are expected to remain well-supplied over the outlook period due to additional LNG production associated with new projects, and elevated stocks of crude oil and petroleum products.

2.6 Australia’s exploration, production and exports

Exploration

Although higher than a year ago, the price of most of Australia’s mineral commodities have declined considerably from their mining boom peaks. With the notable exception of gold, this has reduced the incentive for further minerals exploration. Similarly, the incentive for further petroleum exploration

Error! No text of specified style in document.OCE Report Template 13

has been dampened by weak oil prices. The Brent oil price increased in the first half of 2016, but remains less than half of what it was three years ago.

Mineral exploration expenditure increased 3 per cent year-on-year in the June quarter, growing to $354 million. However, petroleum exploration expenditure declined by 59 per cent year-on-year, to reach $283 million for the June quarter.

Figure 2.3 Australia’s exploration expenditure

Figure 2.4: Mineral exploration expenditure by state and territory

Figure 2.5: Mineral exploration by deposit type

Figure 2.6: Minerals exploration, metres drilled

The decline was most pronounced in the onshore sector, which recorded a 76 per cent year-on-year fall, to $59 million. Offshore exploration fell by 51 per cent year-on-year to $224 million, accounting for a larger share of the absolute decline.

The increase in mineral exploration expenditure in the June quarter was almost entirely attributable to increased gold exploration, which rose 40 per cent year-on-year, to reach $157 million. Gold prices have held up much better than most other mineral commodities in recent years with margins supporting further exploration.

A smaller contribution to increased mineral exploration was from copper, which increased 15 per cent year-on-year in the June quarter, to $32 million. Exploration for other mineral commodities continued to decline in the June quarter.

Mineral exploration expenditure increased in South Australia (up 62 per cent to $19 million), Victoria (up 27 per cent to $8 million), New South Wales (up 22 per cent to $31 million) and Western Australia (up 11 per cent to $228 million). This was partially offset by lower exploration expenditure in all other states and territories.

Mineral exploration expenditure targeting existing deposits increased 9 per cent year-on-year to $250 million, while expenditure at new deposits declined 9 per cent, to $104 million.

The generally subdued outlook for growth in commodities prices make increases in exploration expenditure over the outlook period unlikely.

Capital expenditure

The environment for investment in new mining projects remains challenging due to lower prices and tighter access to finance. Private capital expenditure in the mining sector declined by 30 per cent in 2015–16, to $53 billion. This was the lowest level in five years, although it remains well above levels observed prior to the onset of the mining boom. In the 10 years to 2002–03, annual capital expenditure in the mining sector averaged only $7.7 billion, around 14 per cent of current levels.

Error! No text of specified style in document.OCE Report Template 14

However, the pace of decline in mining investment is expected to slow. Mining businesses are planning capital expenditure of $42 billion in 2016–17, 22 per cent lower than in 2015–16.

Figure 2.7: Year-on-year change in petroleum exploration

Figure 2.8: Private mining capital expenditure

Employment

Employment in the mining sector declined in the September quarter, falling 9 per cent year-on-year to 222,300 people. The largest fall in occurred in Queensland, where employment contracted 11 per cent year-on-year to 61,100 people. Employment is likely to decline further over the outlook period as major projects move into the less labour-intensive production phase.

Production

The outlook for Australia’s production of bulk commodities remains generally positive, despite challenging conditions facing most producers. Production of iron ore is forecast to grow over the next year, supported by additional supply from the Roy Hill, Nammuldi and Jimblebar projects. Domestic production of metallurgical coal is also forecast to increase in 2016–17, as production returns to normal following outages in May. In contrast, thermal coal production is forecast to remain relatively flat over the next 9 months, as closures and suspensions just outweigh the effect of increasing production at a number of remaining mines.

Metals production is largely expected to increase over the outlook period, led by growth in gold, copper and alumina. Gold production is forecast to increase to 293 tonnes in 2016–17, mainly as a result of higher expected ore grades and additional supply from the new Matilda mine. Production of copper is also forecast to increase, in line with the expansion of the Olympic Dam project and additional output from the Mount Lyell mine. In contrast, Australia’s nickel production is forecast to decline over the outlook period, as lower mined output compounds the effect of falling refined production.

The outlook for Australia’s energy commodities is mixed. LNG production is forecast to continue to increase in line with growth in export capacity, supported by additional supply from the Gorgon project and stronger coal seam gas production on the east coast. In contrast, uranium production is forecast to decline over the outlook period. Oil production is also expected to fall in 2016–17 as natural decline outweighs increased condensate production.

Figure 2.9: Mining sector employment

Figure 2.10: Quarterly mining sector employment by state

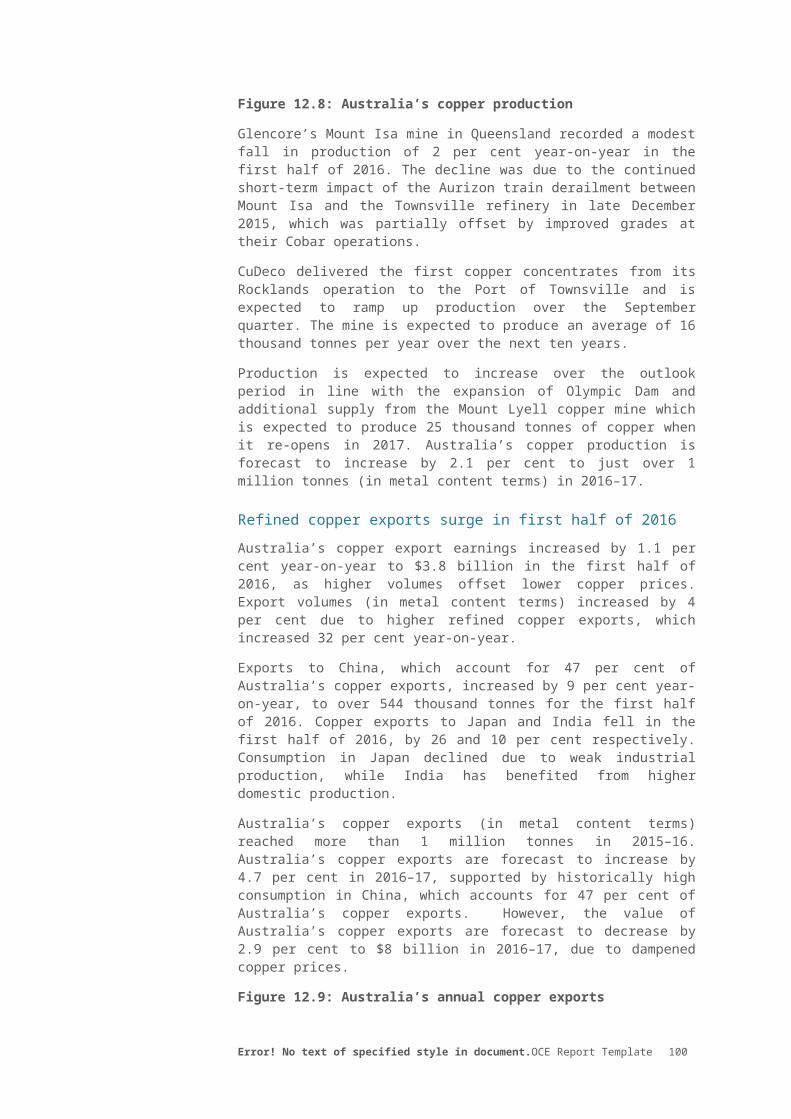

Exports

The volume of Australia’s exports of resources and energy commodities generally increased year-on-year in the June quarter 2016, as growth in

Error! No text of specified style in document.OCE Report Template 15

exports of iron ore, metallurgical coal, gold, copper and LNG contrasted with declines in thermal coal, alumina, and crude oil.

The value of Australia’s exports increased in line with generally higher volumes, to reach $40 billion for the June quarter, led by strong year-on-year growth in earnings from exports of gold, iron ore and LNG.

The outlook for Australia’s resources and energy exports remains broadly positive, with export earnings forecast to increase 12 per cent in 2016–17, to $176 billion. The strongest growth in export earnings is expected to come from LNG, which is forecast to increase 41 per cent, from $17 billion in 2015–16 to $23 billion in 2016–17, supported by additional production at the Gorgon project and new capacity coming online on the east coast.

Continued growth in the volume of most bulk commodities exports is also expected to contribute to higher export earnings over the outlook period. The value of Australia’s exports of iron ore are forecast to increase 13 per cent, to reach $54 billion in 2016–17.

Figure 2.11 Australia’s resources and energy export earnings

Figure 2.12: Australia’s major resources and energy commodity exports

Error! No text of specified style in document.OCE Report Template 16

Table 2.1: Outlook for Australia’s resources and energy commodities

unit 2013–14 2014–15 2015–16 2016–17 f Per cent change

Value of exports

Resources and energy A$m 194,881 171,971 157,130 175,782 12.2

– real b A$m 205,500 178,286 160,682 175,782 9.7

Energy A$m 71,455 66,831 59,500 72,629 22.1

– real b A$m 75,348 69,285 60,845 72,629 19.4

Resources A$m 123,426 105,140 97,630 103,153 6.2

– real b A$m 130,152 109,001 99,837 103,153 3.8Notes: b In current financial year Australian dollars; f ForecastSource: ABS (2016) International Trade in Goods and Services, 5368.0; Department of Industry, Innovation and Science (2016)

Table 2.2: Australia’s resources and energy commodity exports, selected commodities

Volume Value

unit 2015–16 2016–17 f Per cent change 2015–16 2016–17 f Per cent change

Alumina kt 17,676 18,158 2.7 5,995 6,006 0.2Aluminium kt 1,441 1,399 -2.9 3,237 3,669 13.3Copper kt 1,055 1,056 0.1 8,124 7,992 –1.6Gold t 306 306 -0.2 15,674 16,277 3.8Iron ore Mt 786 851 8.2 47,766 53,570 12.2Nickel kt 216 178 -17.6 2,477 2,134 –13.8Zinc kt 1,509 921 -38.9 2,621 2,321 –11.5LNG Mt 37 51 39.6 16,557 23,357 41.1Metallurgical coal Mt 188 189 0.6 19,533 26,400 35.2Thermal coal Mt 200 204 1.6 14,698 14,167 –3.6Oil kbd 241 235 -2.6 5,467 5,776 5.7Uranium t 7,837 7,225 -7.8 959 917 –4.4Notes: f ForecastSource: ABS (2016) International Trade in Goods and Services, 5368.0; Department of Industry, Innovation and Science (2016)

Error! No text of specified style in document.OCE Report Template 17

3. Steel

3.1 Market overview

Global steel production is forecast to decline by 0.7 per cent to 1,605 million tonnes in 2016 and then increase by 0.8 per cent in 2017 to 1,618 million tonnes, broadly unchanged from the June quarter forecast.

The pace of decline in China’s steel production is expected to pick up as the effects of stimulus measures and housing policies implemented at the start of the year wane, and capacity cuts take effect. Steel production is forecast to continue to grow strongly in India, supported by trade restrictions and ambitious plans for infrastructure projects. Despite sharp falls in 2016, anti-dumping measures in the US and the EU are expected to support steel production growth in 2017, while production growth is expected to remain subdued in Japan and South Korea.

3.2 Steel production and consumption

China steel production forecast to fall in 2016 and 2017

Despite declining steel production in early 2016, China’s steel production increased by 1.5 per cent year-on-year in the three months to August due to growth in both domestic consumption and exports. Steel production in China is forecast to decline by 1.0 per cent in 2016 and by 2.5 per cent in 2017.

Production in 2016 has been revised up slightly. Higher than expected steel production was incentivised by stronger demand from the construction sector, which put upward pressure on steel prices, following stimulus measures implemented earlier in the year.

There are signs of slowing momentum in China’s construction sector, which accounts for 73 per cent of domestic steel use. Newly started residential buildings (in terms of floor space) grew 6 per cent year-on-year in the three months to August, in contrast to 18 per cent year-on-year growth earlier in the year in the three months to May.

China’s export growth remained strong in the three months to August, up 7 per cent year-on-year. Export growth was largely driven by the Philippines, Thailand and Vietnam. Partially offsetting this was steel products exports to the US, which fell by 69 per cent year-on-year through 2016 to July, dampened by anti-dumping measures.

Figure 3.1: Annual growth in world steel production

Figure 3.2: China’s steel consumption and residential construction

Overcapacity in the Chinese steel sector remains a key issue. Mandated capacity cuts are behind schedule, with firms and local governments reluctant to reduce steel capacity due to higher steel prices and concerns of mass unemployment.

Error! No text of specified style in document.OCE Report Template 18

Nevertheless, the central government has reaffirmed its commitment to achieving the 45 million tonne reduction target for the year, in part motivated by its case for being granted market economy status in the World Trade Organisation. In late August, the National Development and Reform Commission dispatched inspectors to steel producing provinces to monitor progress and ensure the completion of planned capacity cuts.

However, even if the annual target is achieved, it is unclear the extent to which capacity cuts will translate to a reduction in production, if higher prices encourage production growth at remaining plants.

There are moderate risks to the outlook though to 2017. A faster pace of capacity closures and increasingly stringent environmental regulations to lower emissions and improve local air quality present a downside risk to the outlook. On the upside, there is the possibility of further stimulus measures to boost the domestic construction industry.

India’s steel production forecast to grow in 2016 and 2017

Growth in India’s steel production accelerated to 7 per cent year-on-year in the three months to July, as major producers continued to ramp up production at newly commissioned plants or utilisation rates of existing capacity increased.

Increased steel production has been supported by a range of policy measures to protect the domestic industry. In March 2016, safeguard duty was extended on some steel products for two years, and in August 2016, the minimum import price mechanism was extended until October, and an anti-dumping tax levy on hot-rolled flat steel was imposed for six months. The effect of these measures are reflected in substantially reduced steel imports, down 26 per cent year-on-year in the three months to July.

Figure 3.3: China’s exports of iron and carbon steel products, by destination

Figure 3.4: India’s monthly steel production and imports, year-on-year change

The forecast for steel production in India remains unchanged, growing at 6 per cent in 2016 and 7 per cent in 2017. Growth in steel production will be supported by government policy targeting the expansion and improvement of both infrastructure and the manufacturing industry. The forecast for India’s consumption growth remains at 8 per cent in 2017.

Japan’s steel production forecast to be steady through outlook period

In contrast to the declines seen in the first quarter of 2016, Japan’s steel production increased 1.1 per cent year-on-year in the three months to July, despite soft domestic demand indicators, supported by higher exports and lower import competition.

The trend of international competition displacing Japan’s domestic steel production observed earlier in the year has eased, with steel exports up 2.6 per cent year-on-year in May and June, while imports were down 1.5 per cent

Error! No text of specified style in document.OCE Report Template 19

over the same period. On the domestic front, industrial production was down 1.7 per cent in the June quarter, while housing starts barely grew at 0.3 per cent.

Japan’s steel production forecasts have remained broadly unchanged for 2016 and 2017, at around 104 million tonnes.

South Korea’s steel production adversely affected by global overcapacity in ship building

South Korea’s steel production decreased 2.7 per cent year-on-year in the four months to July, because of weak demand from China and falling demand from South Korea’s ship building and automobile industry. South Korea’s ship building industry is a large consumer of steel, and has been weakened by soft global demand. South Korea’s automobile production has declined as a result of labour strikes and falling domestic sales due to the end of a temporary consumption tax cut in June.

South Korea’s steel production is forecast to decline by slightly more than previously forecast, down 2.7 per cent in 2016, due to a larger than expected decline in the first seven months of 2016. Steel production is forecast to moderately increase by 0.9 per cent in 2017.

Figure 3.5: Japan’s monthly steel production, exports and imports, year-on-year change

Figure 3.6: South Korea’s monthly steel production and vehicle production, year-on-year change

US steel production forecast to grow in 2017

US steel production fell by 0.2 per cent year-on-year in the three months to July, because of subdued domestic demand conditions. The Dodge construction index was down 11 per cent and industrial production was down 1.1 per cent year-on-year in the three months to July. The fall in production occurred despite a decline in imports of 8 per cent year-on-year in the three months to July, as a result of high anti-dumping duties on hot-rolled, cold-rolled and corrosion resistant steel products.

Steel production in the US is forecast to remain stable in 2016 at 79 million tonnes, lower than previously forecast due to weaker than expected domestic demand. The forecast for 2017 remains unchanged, with steel production increasing 3.4 per cent, supported by ongoing import duties.

Steel production in the EU continues to decline in 2016, forecast to grow in 2017

EU steel production continued to fall—down 5 per cent in the three months to July—because of international competition.

Steel imports increased 21 per cent year-on-year in the first five months of 2016, while steel exports decreased 9 per cent. As a result, the EU has implemented 37 anti-dumping duties on steel products over the past year, and is scheduled to rule on preliminary anti-dumping duties on plate and hot

Error! No text of specified style in document.OCE Report Template 20

rolled coil from China in November 2016. In addition, the potential for the EU to further pursue policies to protect domestic steelmakers has increased following the United Kingdom’s decision to leave the EU, as the United Kingdom has historically lead a small minority of countries that opposed trade restrictions.

Domestic demand conditions have been soft in the first half of 2016. Industrial production increased 1.3 per cent in the first half of the year compared to a year earlier, while construction remained broadly stable.

With steel production falling further than previously anticipated, the forecast for EU steel production in 2016 has been revised down to 160 million tonnes, a 3.5 per cent decline. The forecast for 2017 remains unchanged, for growth of 2.5 per cent, supported by improving demand conditions.

Figure 3.7: United States monthly steel production, inventory and imports, year-on-year change

Figure 3.8: European Union monthly steel production, exports and imports, year-on-year change

Australia’s steel exports fall in the June quarter due to a decrease in exports to the US

Australia’s steel production in 2015–16 increased by 4.8 per cent to 5 million tonnes, while apparent steel consumption (steel production plus imports less exports) increased 0.9 per cent. Australia represents 0.3 per cent of global steel production.

Australia’s imports of crude steel declined 53 per cent year-on-year in the June quarter to 415,000 tonnes, while unit values declined 66 per cent. Imports from Japan were down 94 per cent to 22,000 tonnes, while imports from China increased 3 per cent to 77,000 tonnes.

Australia’s exports of crude steel declined 15 per cent year-on-year in the June quarter to 205,000 tonnes. The fall in exports was primarily due to a fall in exports to the US—Australia’s largest steel export market. Exports to the US were down 97 per cent year-on-year in the June quarter by 92,000 tonnes, as a result of subdued demand and a preliminary ruling on hot-rolled steel products from Australia under an anti-dumping investigation.

Final determinations on hot-rolled steel products from Australia, amongst other countries, were affirmed in August by the US Department of Commerce. As a result, Australian steel producers could face dumping margins of 29 per cent, up from 23 per cent in the preliminary ruling, and Australian steel could potentially become uncompetitive in the US market. The impact on Australian steel exports will depend on whether new arrangements can be made with US importers, and whether Australian steel exports can be redirected to other markets in an environment of global oversupply in the steel sector.

Figure 3.9: Australia’s steel exports

Figure 3.10: Australia’s quarterly steel imports, production and apparent consumption

Error! No text of specified style in document.OCE Report Template 21

Error! No text of specified style in document.OCE Report Template 22

Table 3.1: World steel consumption

Million tonnes 2014 2015 2016 f 2017 f Per cent change

European Union 28 162 167 171 175 2.9

United States 122 109 112 118 5.2

Brazil 28 24 16 14 –11.7

Russia 49 45 41 39 –3.0

China 740 698 677 664 –2.0

Japan 73 68 67 66 –1.5

South Korea 58 58 57 56 –1.5

India 84 88 92 99 7.7

World steel consumption 1,663 1,611 1,598 1,610 0.8

Notes: f Forecast Source: Bloomberg (2016) World Steel Association; Department of Industry, Innovation and Science (2016)

Table 3.2: World steel production

Million tonnes 2014 2015 2016 f 2017 f Per cent change

European Union 28 169 166 160 164 2.5

United States 88 79 79 81 3.4

Brazil 34 33 29 27 –6.7

Russia 71 71 70 70 –0.7

China 823 801 793 773 –2.5

Japan 111 105 104 104 –0.5

South Korea 72 70 68 68 0.9

India 87 90 95 102 7.0

World steel production 1,670 1,616 1,605 1,618 0.8

Notes: f Forecast Source: Bloomberg (2016) World Steel Association; Department of Industry, Innovation and Science (2016)

Error! No text of specified style in document.OCE Report Template 23

4. Iron ore

4.1 Market overview

Australia’s iron ore export volumes are forecast to increase by 8 per cent to reach 851 million tonnes in 2016–17, supported by operational improvements and the ramp up of production at new mines and expansions. Export earnings are forecast to increase by 12 per cent to $54 billion in 2016–17, revised up from the previous forecast of $49 billion. The revision reflects persistently high prices in the September quarter.

However, the iron ore price is forecast to decline later in 2016 and average 6 per cent lower in 2017, at US$45 a tonne (FOB Australia).

4.2 Prices

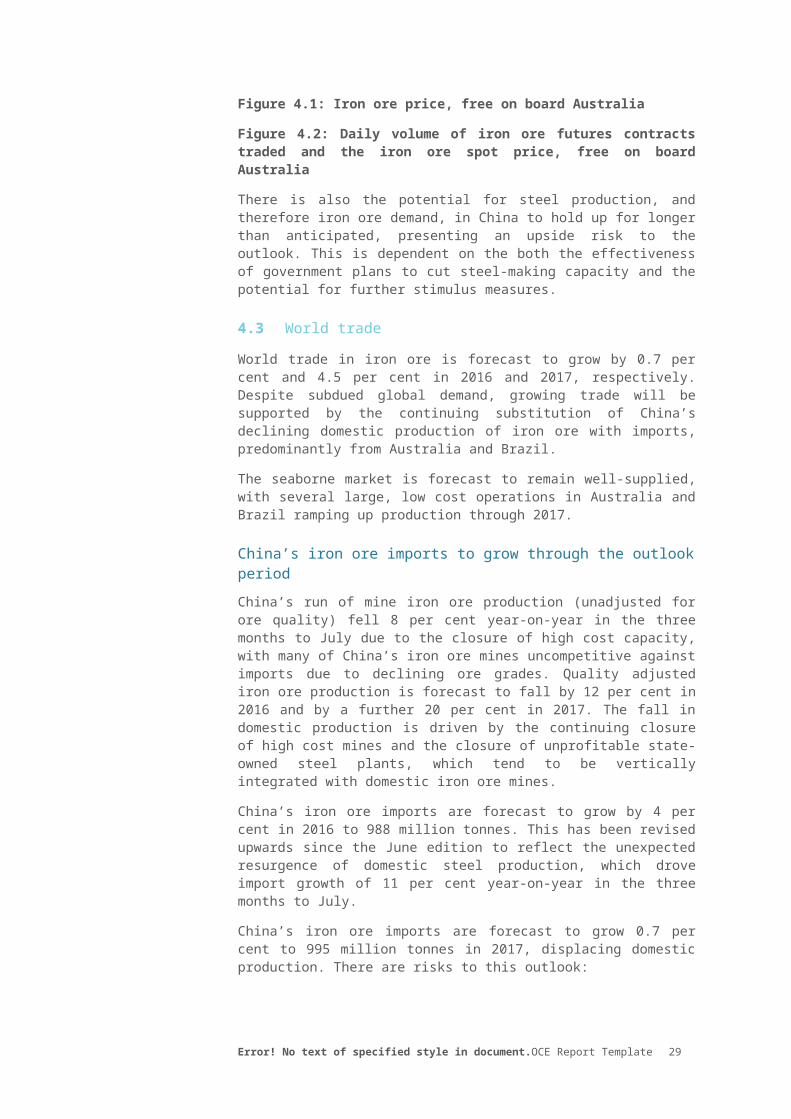

The iron ore spot price (FOB Australia) unexpectedly rallied through July and August to average US$54 a tonne, up 14 per cent year-on-year. As a result, the forecast has been revised up, to average US$49 for 2016 as a whole. However, the price is still expected to decline, and the forecast of US$45 a tonne in 2017 remains unchanged.

Higher iron ore prices since the June edition have been supported by strong demand from China’s steel sector, underpinned by stimulus-driven resurgence of the construction sector.

The speculative activity on the Dalian Commodities Exchange that contributed to high volumes being traded and high spot price volatility in the first half of the year has tapered off. This was supported by measures to reduce speculative trading, including increased commission fees, margin requirements and trading restrictions.

As a result of reduced speculative activity, the iron ore price going forward will likely better reflect market fundamentals of slow consumption growth, and further growth in production volumes at low costs.

Risks to the outlook are considered moderate. In particular, the price outlook remains sensitive to the amount of loss making that producers in the market may tolerate. Additionally, there remains the potential for producers to further cut costs enabling them to operate profitably at lower market prices.

Figure 4.1: Iron ore price, free on board Australia

Figure 4.2: Daily volume of iron ore futures contracts traded and the iron ore spot price, free on board Australia

There is also the potential for steel production, and therefore iron ore demand, in China to hold up for longer than anticipated, presenting an upside risk to the outlook. This is dependent on the both the effectiveness of government plans to cut steel-making capacity and the potential for further stimulus measures.

Error! No text of specified style in document.OCE Report Template 24

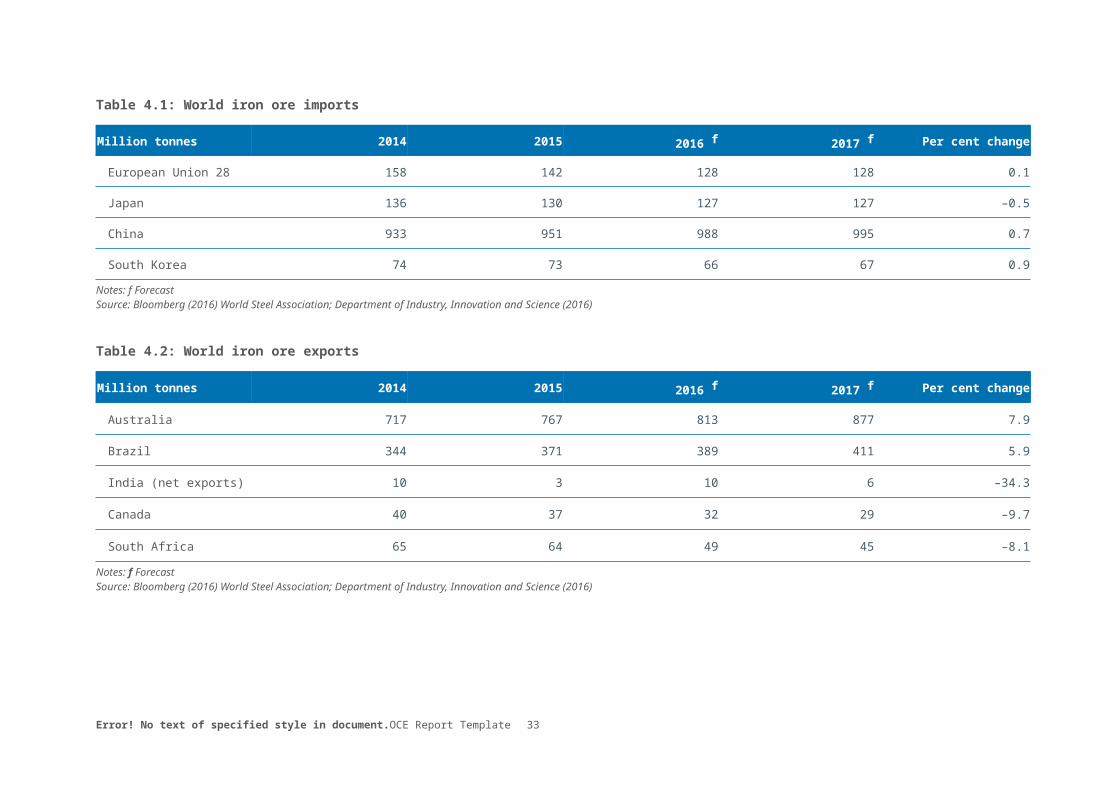

4.3 World trade

World trade in iron ore is forecast to grow by 0.7 per cent and 4.5 per cent in 2016 and 2017, respectively. Despite subdued global demand, growing trade will be supported by the continuing substitution of China’s declining domestic production of iron ore with imports, predominantly from Australia and Brazil.

The seaborne market is forecast to remain well-supplied, with several large, low cost operations in Australia and Brazil ramping up production through 2017.

China’s iron ore imports to grow through the outlook period

China’s run of mine iron ore production (unadjusted for ore quality) fell 8 per cent year-on-year in the three months to July due to the closure of high cost capacity, with many of China’s iron ore mines uncompetitive against imports due to declining ore grades. Quality adjusted iron ore production is forecast to fall by 12 per cent in 2016 and by a further 20 per cent in 2017. The fall in domestic production is driven by the continuing closure of high cost mines and the closure of unprofitable state-owned steel plants, which tend to be vertically integrated with domestic iron ore mines.

China’s iron ore imports are forecast to grow by 4 per cent in 2016 to 988 million tonnes. This has been revised upwards since the June edition to reflect the unexpected resurgence of domestic steel production, which drove import growth of 11 per cent year-on-year in the three months to July.

China’s iron ore imports are forecast to grow 0.7 per cent to 995 million tonnes in 2017, displacing domestic production. There are risks to this outlook:

• On the upside, the pace of closures of China’s iron ore mines is subject to government policy and could occur faster than expected; and

• On the downside, small-scale iron ore mines in China are able to restart operations relatively quickly in response to a recovery in price, and as a result, reductions may not occur as rapidly as currently anticipated.

India’s iron ore production forecast to grow through outlook period

India’s iron ore production grew 43 per cent year-on-year in the June quarter, supported by the lifting of some mining restrictions. However, production caps in the states of Odisha and Goa continue to constrain growth.

India’s production of iron ore is forecast grow by 25 per cent in 2016 and 4 per cent in 2017 to meet higher domestic demand. The domestic steel industry has been buoyed by ambitious infrastructure projects and policies to expand the manufacturing sector, along with protection from international competition through import duties.

Increased domestic production has resulted in decreased iron ore imports, down 67 per cent year-on-year in the first five months of 2016. Over the same

Error! No text of specified style in document.OCE Report Template 25

period, there was a substantially large growth in exports, primarily to China, up 485 per cent to 6 million tonnes. However, this export growth has been from a low base, and with relatively small, high cost mines and growing domestic consumption, India is not expected to become a major exporter of iron ore.

Figure 4.4: China’s quarterly iron ore production and imports

Figure 4.5: India’s monthly iron ore exports and imports

Australia and Brazil to increase share of global trade

Australia and Brazil are forecast to increase their share of global seaborne trade in 2017 to 58 per cent and 27 per cent, respectively. Export growth in both countries will be supported by the ramping up of production at new, low cost mines and expansions of existing operations at the end of 2016 and through 2017. The additional supply from Australia and Brazil will put downward pressure on prices over the outlook period.

Production growth in Brazil is expected to be largely underpinned by Vale’s S11D expansion project, currently in its final stages of development. S11D is expected to produce 75 million tonnes of high quality iron ore annually, with more than half of production planned to be exported to Asia. Vale has indicated that the mine will ramp up production over a period of four years, slower than previously expected.

Export growth from Australia and Brazil is also expected to be supported by a growing preference from China’s steel mills for higher grade ore to reduce emissions, as operations face more stringent environmental regulations. In contrast to an average proven reserve grade of 34 per cent iron content in China, the average reserve grade in Australia and Brazil is approximately 58 per cent and 53 per cent, respectively, with even higher grades at particular deposits. For example, Vale’s S11D deposit has an estimated reserve grade of 67 per cent, and BHP Billiton’s Jimblebar deposit has an estimated reserve grade of 63 per cent.

4.4 Australia’s exploration, production and exports

Exploration activity

Iron ore exploration expenditure in Australia remained relatively steady year-on-year in the June quarter 2016 following over three years of declines. However, for 2015–16 as a whole, iron ore exploration expenditure declined 35 per cent, as a result of cost cutting activities and the substantial falls in prices, which reduced the feasibility of new iron ore projects and reduced incentives to explore.

A recovery in iron ore exploration expenditure in the next few years remains unlikely, given that iron ore prices are forecast to remain low.

Figure 4.6: Share of total iron ore exports

Figure 4.7: Forecast iron ore production and cash costs in 2017

Error! No text of specified style in document.OCE Report Template 26

Australia’s export volumes forecast to grow in 2016–17

Australia’s iron ore production grew 9 per cent year-on-year to 218 million tonnes in the June quarter, while exports grew 6 per cent to 202 million tonnes. Production and exports growth were supported by continued ramping up of Hancock Prospecting’s Roy Hill mine, expansions of existing operations, and favourable weather conditions. For 2015–16 as a whole, Australia’s iron ore exports increased by 5 per cent to 786 million tonnes.

Australia’s iron ore production is forecast to increase 4.8 per cent to 891 million tonnes in 2016–17, supported by operational improvements and further ramp up of production. While ramp up at Roy Hill has been slower than expected due to technical issues at the ore processing plant, production is still expected to reach nameplate capacity of 55 million tonnes in early 2017. Rio Tinto’s Nammuldi Incremental Tonnes project is expected to start production in the December quarter 2016, doubling capacity to 10 million tonnes. In addition, improved utilisation rates and the installation of a new crusher at BHP Billiton’s Jimblebar hub is expected to add to production. Beyond the outlook period, Rio Tinto has confirmed a US$338 million investment to complete the development of the Silvergrass mine, expected to have an annual capacity of 20 million tonnes.

There are minimal risks to the outlook. Australia’s largest iron ore companies, Rio Tinto, BHP Billiton, Fortescue Metals Group and Hancock Prospecting—which are forecast to represent a combined 92 per cent of total production in 2016–17—all have low cost operations and are expected to remain competitive at prices below US$50 a tonne.

Australia’s export values revised to 12 per cent growth in 2016–17

Despite increased volumes, the value of Australia’s iron ore exports decreased 13 per cent to $48 billion in 2015–16, as a result of lower prices.

Australia’s iron ore export earnings are forecast to increase 12 per cent to $54 billion in 2016–17, revised up from the previous forecast of $49 billion because of persistently high prices in the September quarter

Figure 4.8: Australia’s iron ore production

Figure 4.9: Australia’s quarterly iron ore export volumes and values

Error! No text of specified style in document.OCE Report Template 27

Table 4.1: World iron ore imports

Million tonnes 2014 2015 2016 f 2017 f Per cent change

European Union 28 158 142 128 128 0.1

Japan 136 130 127 127 –0.5

China 933 951 988 995 0.7

South Korea 74 73 66 67 0.9

Notes: f ForecastSource: Bloomberg (2016) World Steel Association; Department of Industry, Innovation and Science (2016)

Table 4.2: World iron ore exports

Million tonnes 2014 2015 2016 f 2017 f Per cent change

Australia 717 767 813 877 7.9

Brazil 344 371 389 411 5.9

India (net exports) 10 3 10 6 –34.3

Canada 40 37 32 29 –9.7

South Africa 65 64 49 45 –8.1

Notes: f ForecastSource: Bloomberg (2016) World Steel Association; Department of Industry, Innovation and Science (2016)

Table 4.3: Iron ore outlook

Error! No text of specified style in document.OCE Report Template 28

unit 2014 2015 2016 f 2017 f Per cent change

World

Prices b

Iron ore c

– nominal US$/t 88.0 50.3 48.5 44.8 –7.5

– real d US$/t 89.0 50.8 48.5 44.1 –8.9

2013–14 2014–15 2015–16 2016–17 f Per cent change

Australia

Production

Iron and steel gs Mt 4.57 4.74 4.97 4.73 –4.7

Iron ore Mt 680.1 786.6 850.3 891.3 4.8

Exports

Iron and steel gs Mt 0.57 0.92 0.77 0.88 15.0

– nominal value A$m 616 719 601 666 10.7

– real value h A$m 650 745 615 666 8.3

Iron ore Mt 651.4 747.7 786.3 851.0 8.2

– nominal value A$m 74,671 54,519 47,766 53,570 12.2

– real value h A$m 78,740 56,521 48,846 53,570 9.7

Notes: b fob Australian basis c Spot price, 62 per cent iron content basis; d In current calendar year US dollars; g Crude steel equivalent. Crude steel is defined as the first solid state of production after melting. In ABS Australian Harmonized Export Commodity Classification, crude steel equivalent includes most items from 7206 to 7307, excluding ferrous waste and scrap and ferroalloys; h In current Australian financial year dollars; s Estimate; f ForecastSource: ABS (2016) International Trade in Goods and Services, 5368.0; World Steel Association (2016); AME Group (2016); Company Reports;Department of Industry, Innovation and Science (2016)

Error! No text of specified style in document.OCE Report Template 29

5. Metallurgical coal

5.1 Market summary

Global metallurgical coal prices rallied to four year highs in the September quarter, driven by increased import demand from China and production disruptions in Australia.

Australia’s coal production is expected to recover as weather and infrastructure returns to normal and other mines ramp up production. In addition, while prices are forecast to decline from early 2017, the recent price spike is expected to see 2016–17 prices average higher than 2015–16 prices. As a result, Australia’s export earnings are forecast to increase by 35 per cent in 2016–17.

5.2 Prices

Spot prices rally to 4 year highs

Australian hard prime coking coal spot prices started rallying from the beginning of the June quarter, hitting US$100 a tonne in late April. The rally has gained momentum since late July, with spot prices in mid September reaching US$210, a four year high. The rally has been longer and sharper than forecast in the June edition of the Resources and Energy Quarterly, because of larger than expected import demand from China and a number of supply disruptions.

Government-mandated coal mine closures and weather related supply disruptions in China’s main coal producing region of Shanxi have supported the recent surge in metallurgical coal prices. These supply constraints were further exacerbated by wet weather related production disruptions in Australia and increased demand from China’s steel sector, compounding the impact on price. Production at Anglo America’s Capcoal operation in Queensland was disrupted due to prolonged industrial action and geological issues. Infrastructure disruptions also contributed with a derailment on the train line to the Abbott Point port, a major coal export terminal with an annual capacity of 50 million tonnes.

Prices in the September quarter averaged US$133 a tonne, the highest since December quarter 2013. Low volatility pulverised coal injection (PCI) and semi–soft coking coal prices also increased, but not at the same magnitude as hard coking coal.

Figure 5.1: 2016 surge in metallurgical coal prices to four year high

Figure: 5.2 Benchmark contract prices for Australian metallurgical coal

Benchmark contract prices for the September quarter were settled between Australian metallurgical coal producers and Japanese steel producers at US$92.50 a tonne. This is 10 per cent higher than the June quarter, but relatively unchanged year-on-year. Due to the large increases in metallurgical

Error! No text of specified style in document.OCE Report Template 30

coal prices it is likely that a December quarter contract price will not be settled in advance of the December quarter, as per usual.

Australian benchmark metallurgical coal contract prices are forecast to decline 2.6 per cent to average US$99 a tonne in 2016, and to increase 8 per cent to average US$108 a tonne in 2017. The forecast for increasing prices is partly attributable to continued supply constraints, in late 2016, early 2017.

5.3 World trade

World metallurgical coal trade is forecast to increase 3.3 per cent to 285 million tonnes in 2016, driven by increased import demand from China and India. Similar trade levels are forecast for 2017, where declining metallurgical coal demand for steel production in China will be offset by increasing import demand from India.

China’s metallurgical coal imports grew in the first half of 2016

China’s metallurgical coal imports are forecast to increase 8 per cent to 52 million tonnes in 2016. China’s metallurgical coal imports increased 11 per cent year-on-year in the first seven months of 2016, supported by Government-mandated coal mine capacity closures as the Government seeks to reduce the coal industry to a more sustainable size. Increased imports were also driven by infrastructure constraints brought on by bad weather in China’s Shanxi province, which is China’s biggest coal producing region. Reports indicate that there was a shortage of railway wagons available for transport of metallurgical coal in the June quarter, as a result of increased haulage of thermal coal resulting from a surge in electricity generation needs over China’s summer.

Higher coal imports were also supported by demand from China’s steel sector, which was boosted by the Government’s stimulus package from earlier in the year. China’s steel production increased 2 per cent year-on-year in the three months to July, driven by stronger demand from the construction sector.

Figure 5.3: Major metallurgical coal importers

Figure 5.4: China and India's monthly metallurgical coal imports

China’s metallurgical coal import demand in 2017 will be highly dependent on the resilience of its construction sector and its appetite for steel. Imports are forecast to decline 5 per cent to 50 million tonnes in 2017, in line with declining domestic steel production. However, there is some upside risk as to the magnitude of the rate of decline of China’s coal capacity cuts, especially given the Government’s concerns relating to the recent price spikes.

India’s metallurgical coal imports are forecast to increase

India’s metallurgical coal imports increased 1.8 per cent year-on-year in the first half of 2016. Imports are forecast to increase 3.9 per cent to 53 million tonnes in 2016, driven by increased steel production. Reports indicate that China’s strong interest in coking coal has caught Indian steel makers by

Error! No text of specified style in document.OCE Report Template 31

surprise, with price-sensitive end users prepared to pay higher prices to secure supply, at the beginning of the price rally.

In 2017, India’s metallurgical coal imports are forecast to increase 4 per cent to 55 million tonnes. Government policies are expected to continue to discourage steel imports, which increases the need for more metallurgical coal to support local production, given India’s very small domestic coking coal reserves. In an attempt to secure affordable imports, Coal India (the country’s largest coal producer) continues to seek coal reserves abroad. The state-owned company’s board recently approved the signing of a Memorandum of Understanding with South Africa’s state-owned African Exploration Mining and Finance Corporation, to explore and potentially exploit South Africa’s metallurgical coal reserves.

Japan’s metallurgical coal imports are forecast to remain stable in 2016 and 2017

Japan’s metallurgical coal imports increased 3.1 per cent year-on-year in the first six months of 2016, aided by higher steel production in the June quarter. Imports in 2017 are forecast to stay broadly the same as 2016, at 50 million tonnes.

Error! No text of specified style in document.OCE Report Template 32

Table 5.1: World metallurgical coal trade

2014 2015 s 2016 f 2017 f Per cent change

Metallurgical coal imports

European Union 28 45 42 42 43 2.5

Japan 51 50 50 50 –0.3

China 62 48 52 50 –5.0

South Korea 33 37 38 38 0.0

India 52 51 53 55 4.0

Metallurgical coal exports

Australia 186 186 184 188 2.4

Canada 31 28 26 24 –5.0

United States 54 42 32 30 –6.0

Russia 21 18 20 22 7.0

World trade 292 276 285 285 0.2Notes: f Forecast; s EstimateSource: IEA (2015) Coal Information 2015; Department of Industry, Innovation and Science (2016)

Error! No text of specified style in document.OCE Report Template 33

5.4 World exports

North America’s metallurgical coal exports continue to decline

Metallurgical coal exports from the US declined 30 per cent year-on-year in the first six months of 2016. Overall, exports for 2016 are forecast to decline 24 per cent to 32 million tonnes. The decline in coal prices in recent years has put pressure on many US coal producers, leading to mine closures and capacity cuts, which in turn have affected exports.

In addition to weak coal prices, US metallurgical coal export competitiveness has been affected by distance to major markets and an appreciating US dollar. US metallurgical coal exports are forecast to decline a further 6 per cent in 2017 to 30 million tonnes, as the attractiveness of coal exports relative to competitors is likely to continue to decline. This reflects the expectation of a further appreciation in the US exchange rate towards the end of 2016 and into 2017, with expectations of interest rate hikes by the US Federal Reserve.

Figure 5.5: Major metallurgical coal exporters

Canada’s metallurgical coal exports declined 11 per cent year-on-year in the first six months of 2016, reflecting mine closures and a downgraded coal mining labour force on the back of sustained lower prices before the rally. Metallurgical coal exports are expected to stay low for the remainder of 2016, estimated to be 26 million tonnes, 7 per cent lower than 2015. Exports in 2017 are forecast to decline a further 5 per cent to 24 million tonnes.

5.5 Australia’s production and exports

Australia’s metallurgical coal production was an estimated 48 million tonnes in the June quarter, up 11 per cent quarter-on-quarter, but down 7 per cent year-on-year. Australia’s metallurgical coal production is estimated to have declined 4.2 per cent to 186 million tonnes in 2015–16, as a result of disruptions hampering production at mines in Queensland.

Production trends varied across companies and mines. Vale’s Carborough Downs mine suffered production disruptions due to geological instability and roof fall events associated with the restart of operations after a longwall move in May 2016. This reduced the mine’s June quarter production by 66 per cent year-on-year. In contrast, although Australian miner Yancoal suffered financial losses in 2015–16 due to lower prices and reduced output, construction work on stage 2 of its Moolarben mine went ahead. Coal from its new underground mine was extracted in April.

Australia’s metallurgical coal production in 2016–17 is forecast to increase 3.4 per cent to 192 million tonnes, as overall production returns to normal. Continued production disruptions are affecting metallurgical coal production at a number of mines, including Anglo American’s Capcoal operation. Production at the operation has been hampered by prolonged industrial action and geological instability, with longwall moves curtailing output at the Grasstree underground mine. There is also likely to be a gradual decline in production by financially distressed coal producer, Peabody Energy, who

Error! No text of specified style in document.OCE Report Template 34

plans to reduce its Australian metallurgical coal production by more than half by 2021.

However, these declines are expected to be outweighed by increases in production across the board for the remainder of the year. Increased mine production is expected at large mines such as Whitehaven’s Maules Creek mine (a thermal and semi-soft coking coal mine), which achieved higher than expected production rates in the June quarter and is expected to ramp up production in 2016–17. Anglo American’s Grosvenor mine achieved first coal earlier than scheduled, and the sale of the mine is unlikely to cause much disruption to production, with plans to eventually become a 7.5 million tonne per annum operation.

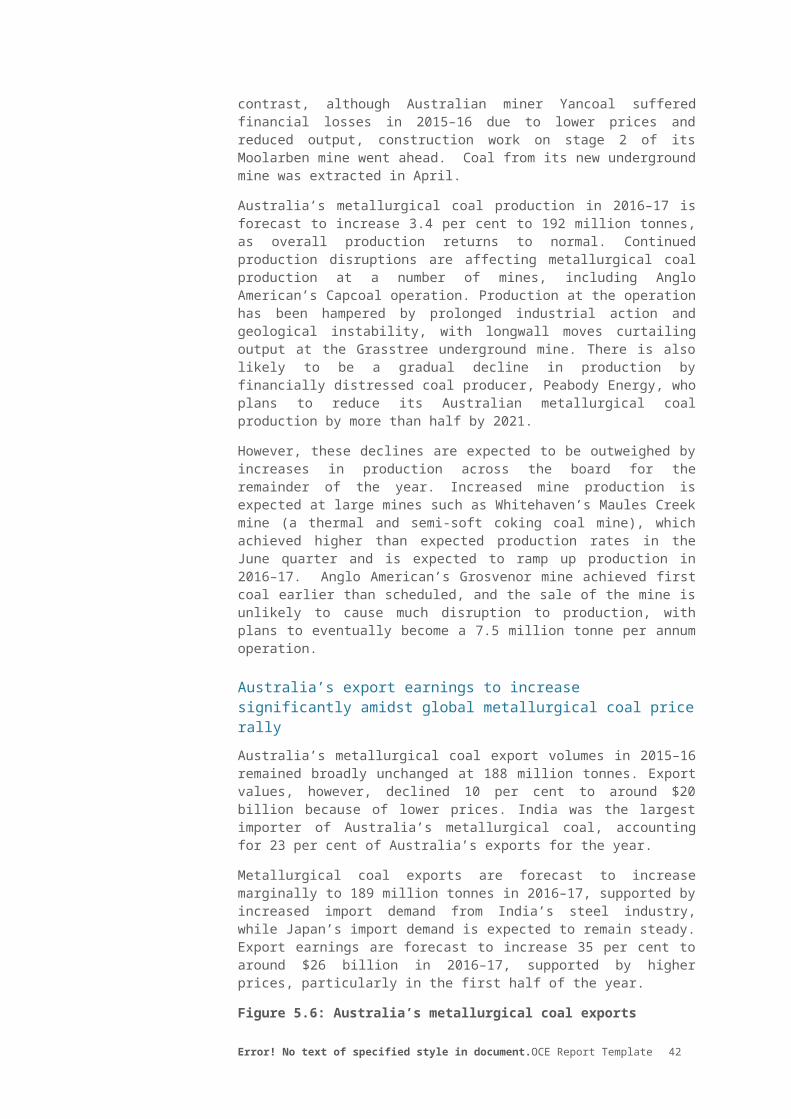

Australia’s export earnings to increase significantly amidst global metallurgical coal price rally

Australia’s metallurgical coal export volumes in 2015–16 remained broadly unchanged at 188 million tonnes. Export values, however, declined 10 per cent to around $20 billion because of lower prices. India was the largest importer of Australia’s metallurgical coal, accounting for 23 per cent of Australia’s exports for the year.

Metallurgical coal exports are forecast to increase marginally to 189 million tonnes in 2016–17, supported by increased import demand from India’s steel industry, while Japan’s import demand is expected to remain steady. Export earnings are forecast to increase 35 per cent to around $26 billion in 2016–17, supported by higher prices, particularly in the first half of the year.

Figure 5.6: Australia’s metallurgical coal exports

Error! No text of specified style in document.OCE Report Template 35

Table 5.2: Australia’s metallurgical coal outlook

Units 2014 2015 2016 f 2017 f Per cent change

Contract prices d

– nominal US$/t 125.5 102.1 99.4 107.5 8

– real e US$/t 126.8 103.0 99.4 105.9 7

Units 2013–14 2014–15 2015–16 2016–17 f Per cent change

Australia

Production Mt 183.1 194.1 186 192.3 3.4

Export volume Mt 180 188 188 189 0.6

– nominal value A$m 23,254 21,813 19,533 26,400 35

– real value h A$m 23,979 22,114 19,533 25,817 32

Notes: f Forecast; s Estimate d Contract price assessment for high-quality hard coking coal; e In current calendar year US dollars; h In current financial year Australian dollarsSource: ABS (2016) International Trade in Goods and Services, 5368.0; Department of Industry, Innovation and Science (2016)

Error! No text of specified style in document.OCE Report Template 36

6. Thermal coal

6.1 Market summary

Thermal coal prices rose further than anticipated in the September quarter to two year highs, driven by government mandated cuts to supply in China, weather-related supply disruptions in Indonesia and increased demand attributed to high temperatures through China’s summer. Continued capacity cuts in China are likely to maintain upward pressure on prices over the outlook period. However, Australia’s export values are expected to stay steady over the outlook period, with higher prices offsetting a small decline in export volumes.

6.2 Prices

Prices spike on the back of capacity cuts in China

Thermal coal spot prices recovered in the September quarter, counter to the downward trend since early 2011. Australia’s benchmark Newcastle free on board (FOB) spot price reached over US$70 a tonne in mid-September, the highest in over two years. Benchmark coal prices in the third quarter increased across the board relative to the previous quarter and year. The Newcastle FOB spot price increased 29 per cent to US$66 a tonne, up from US$51 a tonne in the previous quarter.

Increases in thermal coal prices can largely be attributed to increased Chinese demand for imports, driven by the government-mandated closure of coal mine capacity and a spike in electricity demand over China’s hot summer. Weather-related production disruptions and mine closures in Indonesia (the world’s largest thermal coal exporter) over the same period also placed upward pressure on prices.

The current contract price covering the 2016 Japanese fiscal year (JFY, April 2016–March 2017) is US$61.60 a tonne Newcastle FOB. The JFY 2017 benchmark price, to be negotiated early next year, is forecast to increase to US$64 a tonne, given the expectation of continued capacity closures in China. However, there are uncertainties surrounding the extent and timing of these closures, given they are having a significant impact on prices and import costs for Chinese consumers. A likely slowdown in closures of coal mines, combined with a decline in India’s import growth, are expected to support a gradual decline in spot prices in late 2016 and early 2017, and ease upward pressure on the benchmark price.

Figure 6.1: Thermal coal spot prices

Figure 6.2: JFY thermal coal contract prices

6.3 World trade

World thermal coal trade is forecast to decline to 1.0 billion tonnes in 2016, supressed by a decline in demand in India and developed economies. Global trade in 2017 is forecast to remain broadly unchanged from 2016.

Error! No text of specified style in document.OCE Report Template 37

6.4 World imports

China’s thermal coal imports bounce back in 2016

China’s thermal coal imports have been in decline since 2014. This can be attributed to China’s slowing economic growth and its focus on lowering carbon emissions and air pollution levels, consistent with the transition from an industrial economy to a less energy intensive services economy.

Against this trend, China’s imports of thermal coal increased by 0.2 per cent year-on-year in the first seven months of 2016. This was largely driven by cuts in coal mine capacity as part of the government’s supply-side reforms, and also by increased import demand because of high summer temperatures. Total industry and residential electricity consumption over the warmer months of May to August was up 7 per cent year on year, and thermal coal imports between May and July were up 14 per cent year-on-year.

Reports indicate that by the end of July, China had cut 38 per cent of the 250 million tons of coal capacity it pledged to reduce in 2016. The Government is committed to meeting its annual target, however this may be ambitious given the current price rally, which may encourage a restart of closed capacity or at least slow the rate of future closures. On balance, China’s imports are expected to remain stable over the year, an upwards revision from the June edition, where Chinese thermal coal imports were expected to decline in 2016.