Embed Size (px)

Citation preview

Objective 10.0-10.03Teen Living

Money Management

Money Management10.00 Analyze strategies for managing

money to achieve financial stability.10.01 Identify sources of income and

types of spending. 10.02 Record factors that influence

spending. 10.03 Explore ways to manage money.

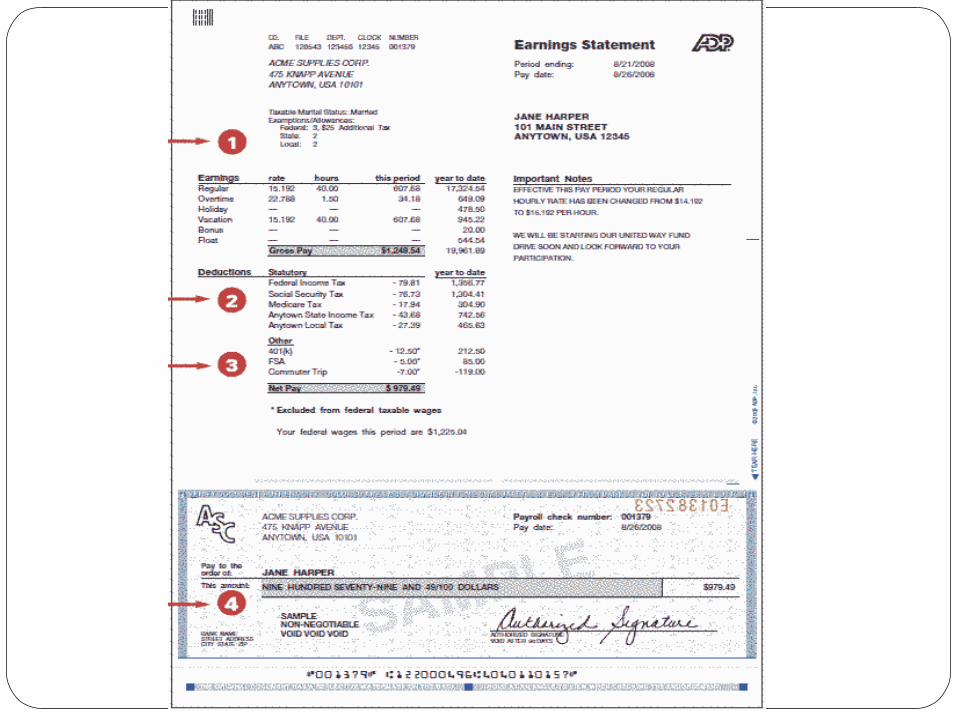

IncomeThe amount of money someone earns and has

available to spend Net Income: the amount of money available

after taxes are taken outGross: Before taxes taken out—MUCH higherA salaried employee earns the same amount

of money each month regardless of the hours worked. Teachers! (Anyone being paid a fixed amount of money for the their work, irregardless of the hours spent.)

PaycheckPaid by check: you must ENDORSE it by

signing your name on the back of the check to cash or deposit it.

Direct deposit: your money goes straight into your checking or savings account. (This can be good once you have this set up, but not good if you need your money deposited by a specific time on a particular day.)

DeductionsThe amount of money taken out of your

paycheck for taxes, insurance, other items.

Checking AccountComes with a register ( booklet for

recording each check amount, date, number, and to whom the check goes)

Record the amount of the check in the check register immediately

Any check that you have written, but does not appear on the bank statement is still outstanding, and has to be considered to reconcile your account correctly

Reconciling a bank statement means your check register must match the bank statement

Savings AccountsKeep money safe and pays you interest on

the moneyWhen choosing a place to open a savings

account, be aware of any fees the bank may charge you.

Automatic Teller Machines (ATM)

Enables customers to withdraw money from their account at any time of day or night, even when the bank is not open. (You must have a card that is connected to a bank account.) The money is taken out of your checking or savings account, depending on which you choose.

Safety: Look around you. Protect your PIN number. After using the ATM, lock your doors and leave quickly

Credit CardsThe grace period is the amount of time before a

finance charge is added to the balance or amount owed.

Use wisely! If your parents provide you with their credit card in case of an emergency, save it for unexpected car repairs, etc.

DO NOT CHARGE: two packs of gum; dinner out for all your friends; two blouses you want, but do not need.

Debit CardUsed instead of writing a check. Money

comes out of a checking account or savings account. You already have the money in the bank

LoansMake regular payments toward the cost of

the item bought on “time,” usually for items that cost a lot of money: house, car, college education. Otherwise you should save your money, until you can pay cash.

CreditLook for the lowest annual percentage rateInterest: amount charged to let you use

money you do not have, to buy things. EX. Purchase $450.00 stereo paying for it

over the course of a year. Final cost is $525.00. The extra $75.00 is interest.

Avoid Impulse BuyingPurchasing something that you did not

intend to buyThink about your purchases before buying.

Is it a need or a want? Is it a fad? Will there be a newer, better item in a few weeks?

Follow a specific listImpulse items are at the checkout

Advertising Make consumers aware of their choicesEvaluate advertising by remembering that MOST

celebrity endorsers are paid by the manufacturer to appear in the ad.

Designed to attract attention and promote sales, NOT help consumers make wise decisions about the product

Slogans or songs are designed to make consumers remember the ad: Alka-Seltzer (plop-plop, fizz-fizz); Burger King (have it your way); Big Mac (Two all beef patties…can you think of any?)

Advertisers typically use internet websites, yellow pages, store windows, and point-of-sale (place where item is sold)

Defective ItemsNormally, return the item to the store

where it was purchasedConsumer’s right to redress means that

you have the right to a refund or replacement when products do not work properly

Product LabelingUse this to get SOME information about the

product. It will not contain all the information about the product

BudgetIs a plan for spending and saving moneyIncludes costs for food (all food, including

trips to restaurants, fast food, lunch room)Anything on which you spend money is an

EXPENSEA written or printed record of what you

purchase is called a RECEIPT. These can be used to help you set up your budget

Consumer’s Rights1. Right to be heard 2. Right to be informed 3. Right to redress/recourse (Explain what

this means)4. Right to safety 5. Right to choose/selection 6. Right to consumer education

![FCV1100L Installation Manual C2 12[1].10.03](https://img.pdfslide.us/doc/110x75/5468197fb4af9f443f8b5767/fcv1100l-installation-manual-c2-1211003.jpg)