Embed Size (px)

Citation preview

Selected Issues when Advising

the U.S. Buyer in Private

Company Acquisitions

Allan J. Ritchie, JD, LLM, MBA, CS

OBA Institute 2015 – Hot Topics in Corporate Law

February 5, 2015

Westin Harbour Castle, Toronto

The information presented is for general discussion purposes only and does not constitute legal advice for any

specific situation. Please contact any of the presenters if you have need for any specific legal advice.

About Loopstra Nixon LLP

Loopstra Nixon is a full-service Canadian business and public law firm

dedicated to serving clients involved in business and finance, litigation and

dispute resolution, municipal, land use planning and development, and

commercial real estate. Major financial institutions, insurance companies,

municipal governments, and real estate developers along with corporate

organizations and individuals are among the wide range of clients we are

proud to serve.

www.loopstranixon.com www.loopstranixon.com

Presenter Biography

Allan has particular expertise executing international business transactions on behalf of foreign entities

entering the North American market and domestic entities seeking global opportunities. He also serves a

number of foreign law firms as Canadian agent counsel. In 2015 Lexpert Magazine named Allan one of

"Canada's Leading Canada/US Cross Border Lawyers to Watch", in recognition of his growing

international business practice.

Allan holds the unique distinction of being the youngest lawyer ever certified by the Law Society of Upper

Canada as a Specialist in Corporate and Commercial Law.

Allan J. Ritchie, Partner

E-mail: [email protected]

Tel: (416) 748-4754

Allan became a partner of the firm in 2010 after

several years with the Toronto office of a United

States based, global law firm.

He is licensed to practice law in Canada and the

United States and manages a global corporate

finance and commercial law practice.

The State of the Union

Purchased by US Buyers:

More available for sale, at lowest price since before the 2008/09 Global Financial Crisis …

Outline of Today’s Presentation

Four Quick Structural Questions

Most Common U.S. Entities

Canadian Entity Options for U.S. Clients

Principles of the Canada - U.S. Tax Treaty

Branch Operations

Standard Corporate Structures

Hybrid Structures

CCPC Status

Trade Regulation (Competition Act / Investment Canada Act)

Employment Issues

Cross-Border Opinions

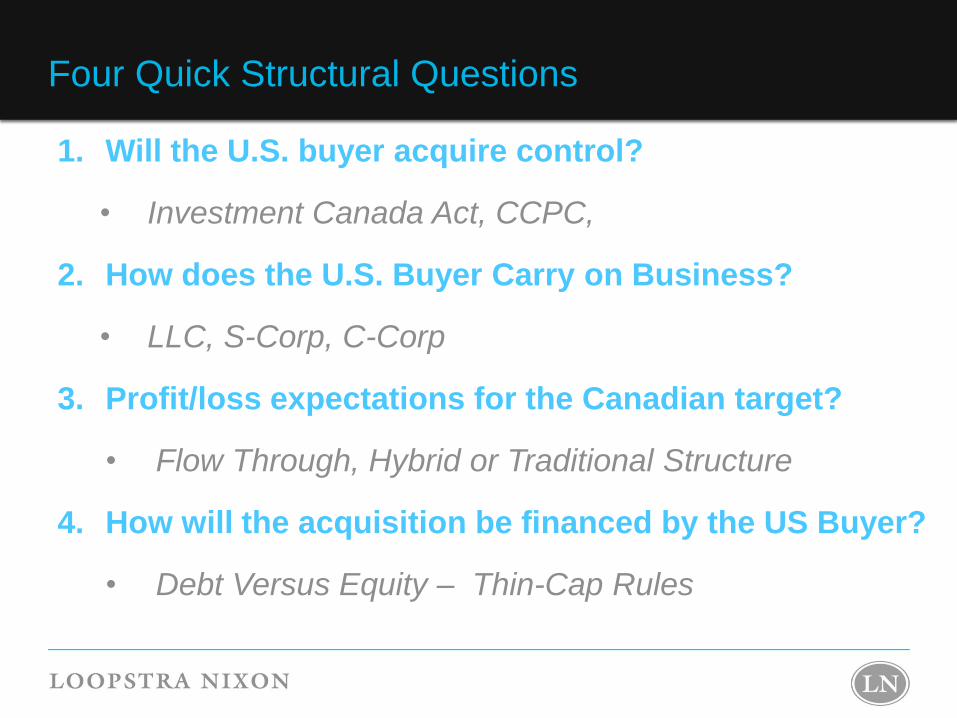

Four Quick Structural Questions

1. Will the U.S. buyer acquire control?

• Investment Canada Act, CCPC,

2. How does the U.S. Buyer Carry on Business?

• LLC, S-Corp, C-Corp

3. Profit/loss expectations for the Canadian target?

• Flow Through, Hybrid or Traditional Structure

4. How will the acquisition be financed by the US Buyer?

• Debt Versus Equity – Thin-Cap Rules

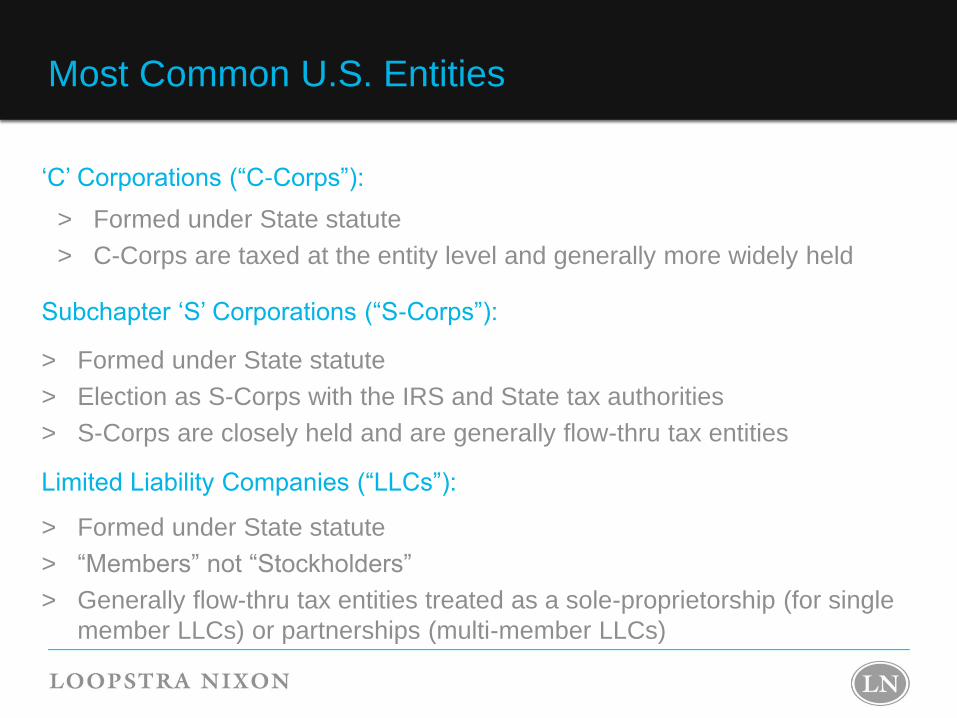

Most Common U.S. Entities

> Formed under State statute

> C-Corps are taxed at the entity level and generally more widely held

‘C’ Corporations (“C-Corps”):

Subchapter ‘S’ Corporations (“S-Corps”):

> Formed under State statute

> Election as S-Corps with the IRS and State tax authorities

> S-Corps are closely held and are generally flow-thru tax entities

Limited Liability Companies (“LLCs”):

> Formed under State statute

> “Members” not “Stockholders”

> Generally flow-thru tax entities treated as a sole-proprietorship (for single

member LLCs) or partnerships (multi-member LLCs)

Canadian Entity Options for U.S. Clients

> Require 25-50% Canadian resident directors (not B.C., N.S., N.B., P.E.I.)

> Limited liability

Provincial or Federal Business Corporations

Foreign Registered Branch

> Registration with Canada Revenue Agency

> Registration as an ‘Extra-Provincial’ entity where applicable

> Unlimited liability for Canadian operations

> Branch tax applies on after tax profits

Unlimited Liability Companies (“ULCs”):

> Only available in B.C., Alberta, and Nova Scotia

> Unlimited Liability

> ‘Hybrid’ treatment may have benefits

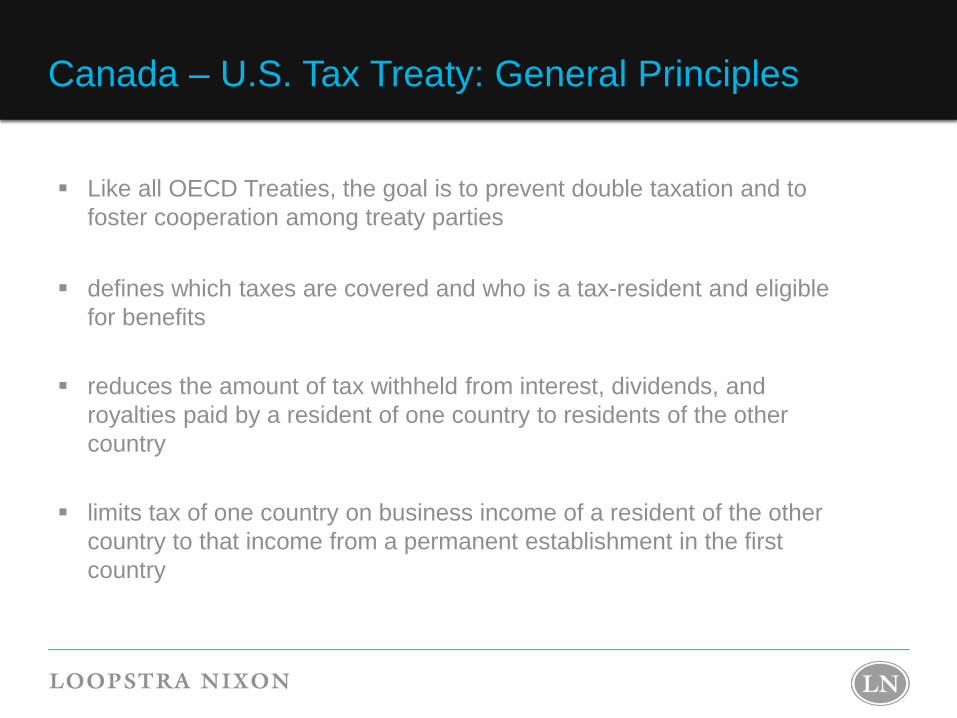

Canada – U.S. Tax Treaty: General Principles

Like all OECD Treaties, the goal is to prevent double taxation and to

foster cooperation among treaty parties

defines which taxes are covered and who is a tax-resident and eligible

for benefits

reduces the amount of tax withheld from interest, dividends, and

royalties paid by a resident of one country to residents of the other

country

limits tax of one country on business income of a resident of the other

country to that income from a permanent establishment in the first

country

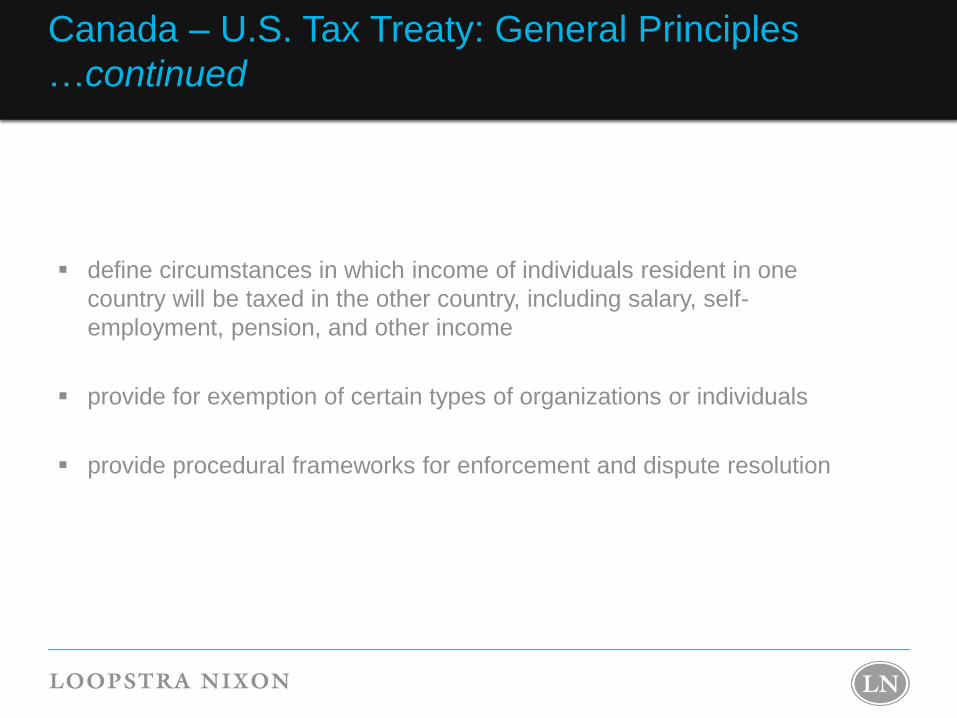

Canada – U.S. Tax Treaty: General Principles

…continued

define circumstances in which income of individuals resident in one

country will be taxed in the other country, including salary, self-

employment, pension, and other income

provide for exemption of certain types of organizations or individuals

provide procedural frameworks for enforcement and dispute resolution

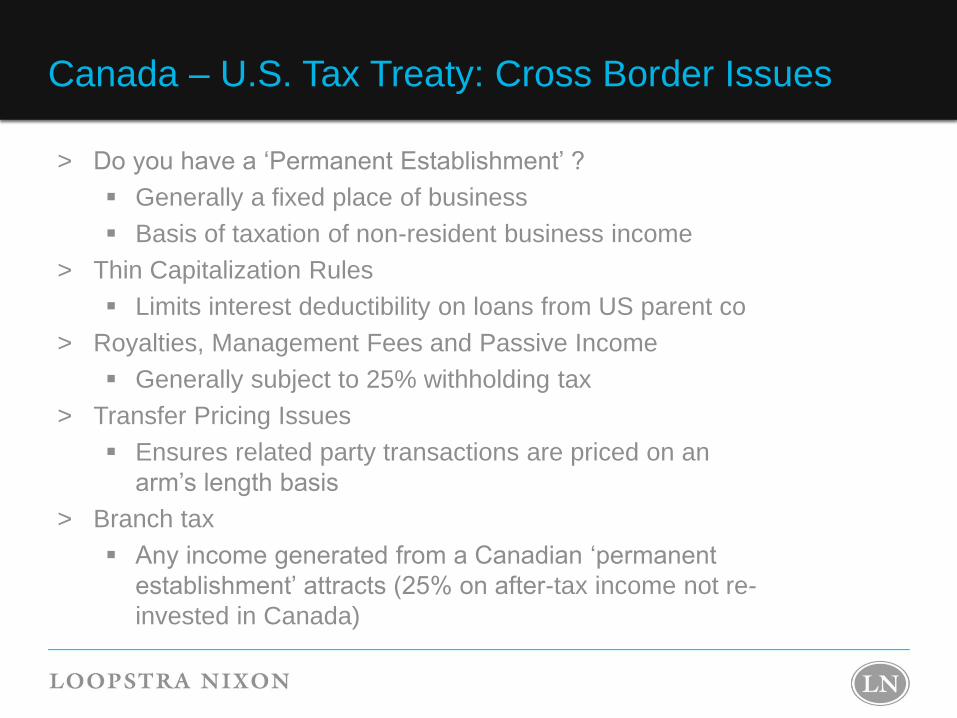

Canada – U.S. Tax Treaty: Cross Border Issues

> Do you have a ‘Permanent Establishment’ ?

Generally a fixed place of business

Basis of taxation of non-resident business income

> Thin Capitalization Rules

Limits interest deductibility on loans from US parent co

> Royalties, Management Fees and Passive Income

Generally subject to 25% withholding tax

> Transfer Pricing Issues

Ensures related party transactions are priced on an

arm’s length basis

> Branch tax

Any income generated from a Canadian ‘permanent

establishment’ attracts (25% on after-tax income not re-

invested in Canada)

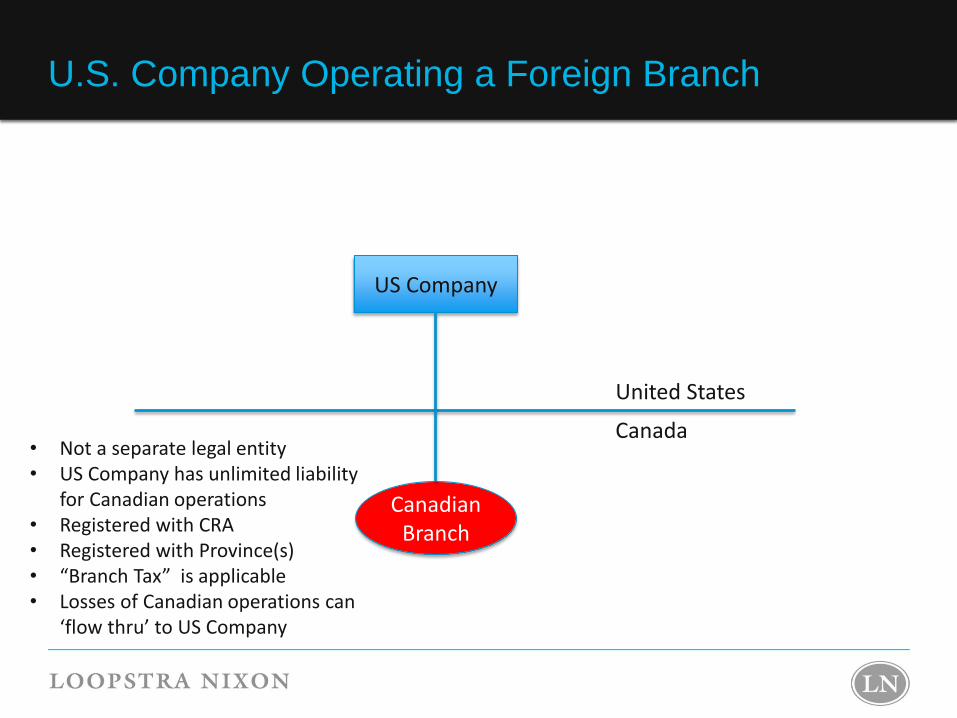

U.S. Company Operating a Foreign Branch

US Company

Canadian Branch

Canada

United States

• Not a separate legal entity • US Company has unlimited liability

for Canadian operations • Registered with CRA • Registered with Province(s) • “Branch Tax” is applicable • Losses of Canadian operations can

‘flow thru’ to US Company

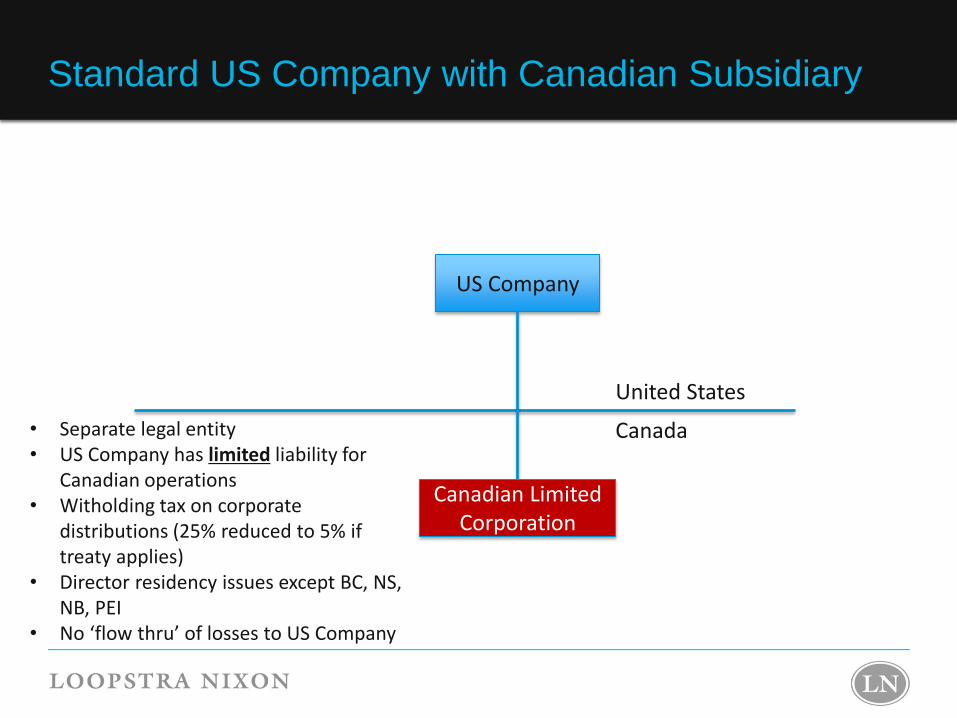

Standard US Company with Canadian Subsidiary

US Company

Canada

United States

• Separate legal entity • US Company has limited liability for

Canadian operations • Witholding tax on corporate

distributions (25% reduced to 5% if treaty applies)

• Director residency issues except BC, NS, NB, PEI

• No ‘flow thru’ of losses to US Company

Canadian Limited Corporation

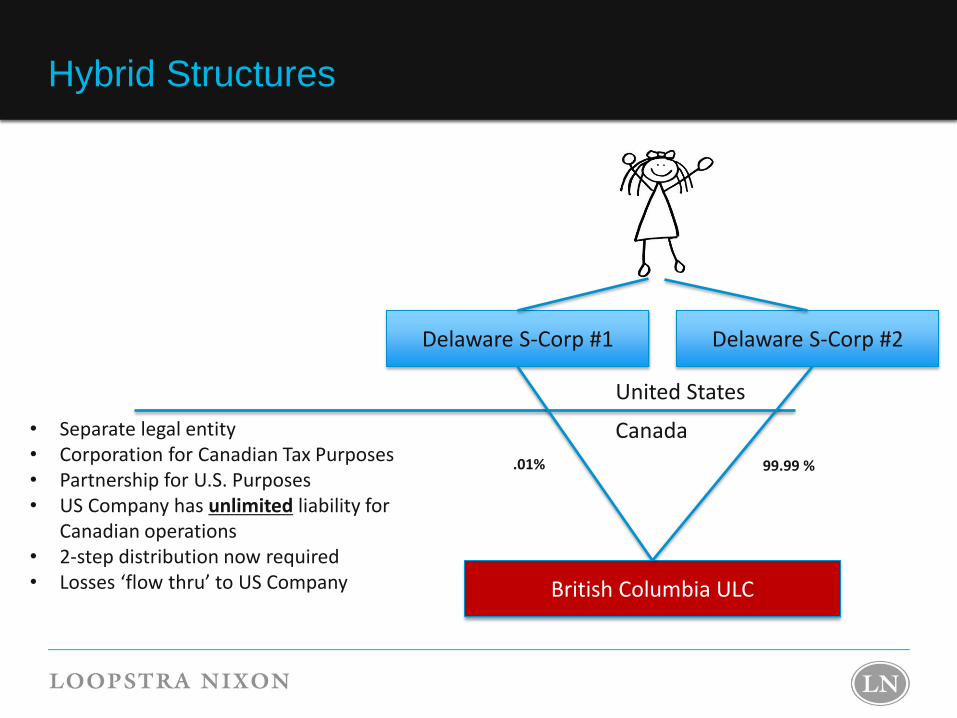

Hybrid Structures

Delaware S-Corp #1

Canada

United States

• Separate legal entity • Corporation for Canadian Tax Purposes • Partnership for U.S. Purposes • US Company has unlimited liability for

Canadian operations • 2-step distribution now required • Losses ‘flow thru’ to US Company British Columbia ULC

Delaware S-Corp #2

.01% 99.99 %

Canadian Controlled Private Corporation Status

Make sure U.S. investors know how much their ‘American-ness’ will cost them.

What is a CCPC

In order to qualify as a CCPC the company must not be controlled,

directly or indirectly in any manner whatever, by public

corporations, non-residents or a combination of the two.

CCPC Benefits that will fall away

Small business deduction

Enhanced SRED credits (refundable)

Life time capital gains exemption

Deferral of taxable benefit from exercise of stock options

Pitfalls

Option agreements, contingent or otherwise will terminate CCPC

status (be careful with minority investments)

Trade Regulation

Pre-Merger Notification (Competition Act)

Transaction size threshold C$86 million for 2015

Combined assets or revenues with affiliates threshold C$400 million

Investment Canada Act

Transaction threshold of C$369 million for 2015 for WTO Investors

must be of ‘net benefit to Canada’

‘Cultural Sector’ investment review threshold at C$5 million

ALL acquisitions of control by US Investors require a Investment

Canada Act Notification within 30 days of the investment

Employment Law

“They’re entitled to what?!”

Absence of ‘at-will’ employment.

Impact of universal health care.

Parental leave entitlements.

Employee v. Independent Contractor

Enforceability of Restrictive Covenants

Human Rights Tribunal

Mandatory Workplace Safety

Insurance Regime

Cross-Border Opinions

Three options when you are asked to provide a cross border opinion:

Independent Opinions: US Counsel provides a separate opinion and

neither Canadian nor US opinion refer to each other.

Co-Dependant Opinions: Canadian counsel’s opinion refers to the

US Counsel’s opinion, but does not repeat its conclusions on US

Matters. US Counsel’s opinion is addressed to Canadian Counsel

and the seller.

Umbrella Opinions: US Counsel’s opinion is addressed only to

Canadian counsel and Canadian Counsel expresses its reliance on

the US opinion and repeats its conclusions.

Questions?