Embed Size (px)

Citation preview

NYP/Q DSRIP PPS – Finance Meeting

Page 1

Meeting Purpose:

1. Discuss current status of DSRIP deliverables for Finance.

# Topic

Document

Responsible Person

1. Welcome & Purpose of Meeting

Chris

2. Audit Updates

NYS I.A. (October 6th

, 2016)

Amanda

3.

(2) At-Risk Network Partners

Visiting Nurse Service of New York

Lexington Hearing and Speech Center

Follow-Up Plan - VNSNY.docx

Follow-Up Action Plan - Lexington.docx

Daniel

4.

Equity Updates

EIP

EPP

Amanda

5. Revenue & Expense Trend Updates

Revenue & Expense Forecast.xlsx

Amanda

6.

ACTION ITEM:

VBP Baseline Assessment (PowerPoint)

Value Based Payment (VBP) Survey Results [Final].pptx

Daniel

7. Partner Incentive Distribution #3 Amanda

8.

Next Steps:

Engage At-Risk Partners and execute follow-up plan

Finalize distribution checklist for payment #3 partner

incentives

All

Meeting Title: NYP/Q DSRIP Finance Meeting :

Finance Progress Overview

Meeting

Date: November 1

st, 2016

Facilitator(s): Amanda Simmons/Daniel Notarnicola Meeting

Time: 1:00 PM – 2:00 PM

Attendees: Finance Committee

Chair : Christopher Caulfield

NYP/Q 56-45 Main Street K.W Board Room

NYP/Q DSRIP PPS – Finance Meeting

Page 2

9. Questions / Adjourn All

Financial Sustainability Follow-Up Evaluation Plan:

Lexington Hearing & Speech Center:

1. Confirm with the provider that the reported financial numbers are accurate, and that the

metrics have, indeed, identified a financial challenge.

2. Inquire about the availability of mid-year consolidated financials that can be used to

supplement the trend being reviewed.

3. Gain an understanding as to why this provider is setting off key financial risk indicators

and if there is any visible trend.

4. NO visible risk indicator trend:

a. Activity flagged initially may indicate an outlier performance.

i. Partner requires no immediate intervention.

5. YES visible risk indicator trend:

a. Detective

i. Partner will go through a monitoring program that will assess financials on

a 6-month basis in order to isolate risk occurrence.

b. Corrective

i. Reconcile partner DSRIP funding receipts with funds flow model to

identify any possible discrepancies.

ii. Identify potentials for engaging in additional projects to maximize funds

flow.

iii. Identify alternative funding sources; e.g. grants.

iv. Seek alternative providers that could fulfill the project goals.

c. Report findings to the Finance Committee and solicit advice on the

implementation of one of the above strategies or an alternative one.

Financial Sustainability Follow-Up Evaluation Plan:

Visiting Nurse Service of New York:

1. Confirm with the provider that the reported financial numbers are accurate, and that the

metrics have, indeed, identified a financial challenge.

a. Current notes show that 2015 financials for VNSNY were unaudited.

Confirmation needs to be obtained that the status here has been updated to

“audited”

2. Inquire about the availability of mid-year consolidated financials that can be used to

supplement the trend being reviewed.

3. Gain an understanding as to why this provider is setting off key financial risk indicators

and if there is any visible trend.

4. NO visible risk indicator trend:

a. Activity flagged initially may indicate an outlier performance.

i. Partner requires no immediate intervention.

5. YES visible risk indicator trend:

a. Detective

i. Partner will go through a monitoring program that will assess financials on

a 6-month basis in order to isolate risk occurrence.

b. Corrective

i. Reconcile partner DSRIP funding receipts with funds flow model to

identify any possible discrepancies.

ii. Identify potentials for engaging in additional projects to maximize funds

flow.

iii. Identify alternative funding sources; e.g. grants.

iv. Seek alternative providers that could fulfill the project goals.

c. Report findings to the Finance Committee and solicit advice on the

implementation of one of the above strategies or an alternative one.

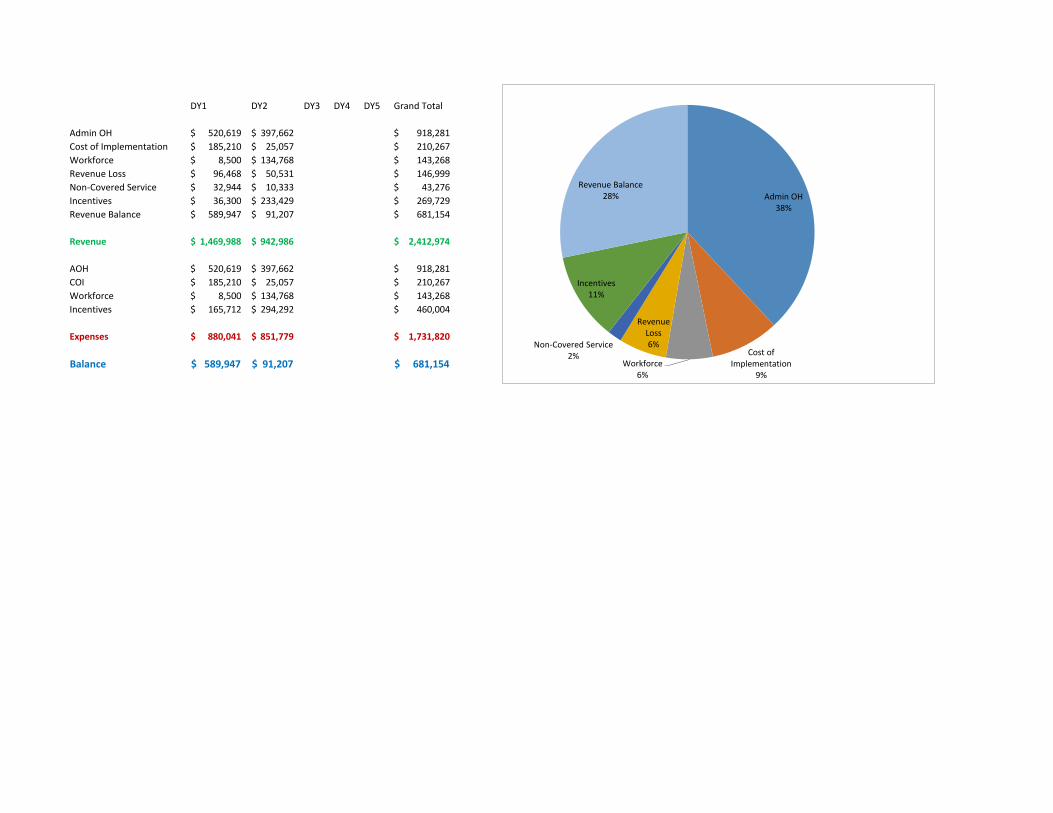

DY1 DY2 DY3 DY4 DY5 Grand Total

Admin OH 520,619$ 397,662$ 918,281$

Cost of Implementation 185,210$ 25,057$ 210,267$

Workforce 8,500$ 134,768$ 143,268$

Revenue Loss 96,468$ 50,531$ 146,999$

Non-Covered Service 32,944$ 10,333$ 43,276$

Incentives 36,300$ 233,429$ 269,729$

Revenue Balance 589,947$ 91,207$ 681,154$

Revenue 1,469,988$ 942,986$ 2,412,974$

AOH 520,619$ 397,662$ 918,281$

COI 185,210$ 25,057$ 210,267$

Workforce 8,500$ 134,768$ 143,268$

Incentives 165,712$ 294,292$ 460,004$

Expenses 880,041$ 851,779$ 1,731,820$

Balance 589,947$ 91,207$ 681,154$

Admin OH 38%

Cost of Implementation

9%

Workforce 6%

Revenue Loss 6% Non-Covered Service

2%

Incentives 11%

Revenue Balance 28%

Revenue & Expense Forecast

April 1, 2015 -

March 31, 2016

April 1, 2016 -

March 31, 2017

April 1, 2017 -

March 31, 2018

April 1, 2018 -

March 31, 2019

April 1, 2019 -

March 31, 2020

Month DY1 DY2 DY3 DY4 DY5

April -$ 369,789.82$

May -$ 112,921.80$

June -$ 115,451.78$

July -$ 151,266.75$

August -$ 57,824.39$

September -$ 44,524.12$

October 302,360.27$

November 31,398.01$

December 57,335.99$

January 49,764.83$

February 332,645.87$

March 106,536.12$

Grand Total 880,041.09$ 851,778.66$ -$ -$ -$

April 1, 2015 -

March 31, 2016

April 1, 2016 -

March 31, 2017

April 1, 2017 -

March 31, 2018

April 1, 2018 -

March 31, 2019

April 1, 2019 -

March 31, 2020

Month DY1 DY2 DY3 DY4 DY5

April -$

May -$

June 1,102,491.00$

July -$ 367,497.09$

August -$ 575,489.00$

September -$

October -$

November -$

December -$

January 367,497.00$

February -$

March -$

Grand Totals 1,469,988.00$ 942,986.09$ -$ -$ -$

EXPENSE

REVENUE

$-

$50,000.00

$100,000.00

$150,000.00

$200,000.00

$250,000.00

$300,000.00

$350,000.00

$400,000.00

DY1 DY2

$-

$200,000.00

$400,000.00

$600,000.00

$800,000.00

$1,000,000.00

$1,200,000.00

DY1 DY2

10/27/2016 CONFIDENTIAL

Revenue & Expense Forecast

April 1, 2015 -

March 31, 2016

April 1, 2016 -

March 31, 2017

April 1, 2017 -

March 31, 2018

April 1, 2018 -

March 31, 2019

April 1, 2019 -

March 31, 2020

Month DY1 DY2 DY3 DY4 DY5

April 77,613.29$

May 85,205.19$

June 36,758.15$

July 107,551.10$

August 51,877.41$

September 38,656.47$

October 202,490.27$

November 31,273.01$

December 679.33$

January 26,402.61$

February 166,415.78$

March 93,358.03$

Grand Total 520,619.03$ 397,661.61$ -$ -$ -$

April 1, 2015 -

March 31, 2016

April 1, 2016 -

March 31, 2017

April 1, 2017 -

March 31, 2018

April 1, 2018 -

March 31, 2019

April 1, 2019 -

March 31, 2020

Month DY1 DY2 DY3 DY4 DY5

April (14,563.17)$

May 13,862.65$

June 7,995.00$

July 5,947.65$

August 5,946.98$

September 5,867.65$

October 99,870.00$

November 125.00$

December 56,656.66$

January 14,279.22$

February 14,279.22$

March -$

Grand Total 185,210.10$ 25,056.76$ -$ -$ -$

EXPENSE : Administrative Overhead

EXPENSE : Cost of Implementation

$-

$50,000.00

$100,000.00

$150,000.00

$200,000.00

$250,000.00

DY1 DY2

$(40,000.00)

$(20,000.00)

$-

$20,000.00

$40,000.00

$60,000.00

$80,000.00

$100,000.00

$120,000.00

DY1 DY2

10/27/2016

All expenses are reflected in GL290 file exported from Lawson General Ledger System

No Cost of Implementation expenses for March ‘16

No Workforce expenses for March ‘16

No Revenue Loss cleared the GL during March ‘16 CONFIDENTIAL

Revenue & Expense Forecast

April 1, 2015 -

March 31, 2016

April 1, 2016 -

March 31, 2017

April 1, 2017 -

March 31, 2018

April 1, 2018 -

March 31, 2019

April 1, 2019 -

March 31, 2020

Month DY1 DY2 DY3 DY4 DY5

April 22,500.00$

May -$

June 72,000.00$

July 40,268.00$

August

September

October

November

December

January 4,083.00$

February 4,083.00$

March 334.00$

Grand Total 8,500.00$ 134,768.00$ -$ -$ -$

April 1, 2015 -

March 31, 2016

April 1, 2016 -

March 31, 2017

April 1, 2017 -

March 31, 2018

April 1, 2018 -

March 31, 2019

April 1, 2019 -

March 31, 2020

Month DY1 DY2 DY3 DY4 DY5

April 50,530.84$

May

June

July

August

September

October

November

December

January

February 96,467.99$

March -$

Grand Total 96,467.99$ 50,530.84$ -$ -$ -$

EXPENSE : Workforce

EXPENSE : Revenue Loss

$-

$10,000.00

$20,000.00

$30,000.00

$40,000.00

$50,000.00

$60,000.00

$70,000.00

$80,000.00

DY1 DY2

$-

$20,000.00

$40,000.00

$60,000.00

$80,000.00

$100,000.00

$120,000.00

DY1 DY2

10/27/2016

All expenses are reflected in GL290 file exported from Lawson General Ledger System

No Cost of Implementation expenses for March ‘16

No Workforce expenses for March ‘16

No Revenue Loss cleared the GL during March ‘16 CONFIDENTIAL

Revenue & Expense Forecast

April 1, 2015 -

March 31, 2016

April 1, 2016 -

March 31, 2017

April 1, 2017 -

March 31, 2018

April 1, 2018 -

March 31, 2019

April 1, 2019 -

March 31, 2020

Month DY1 DY2 DY3 DY4 DY5

April 10,332.57$

May

June

July

August

September

October

November

December

January

February 25,199.84$

March 7,743.70$

Grand Total 32,943.54$ 10,332.57$ -$ -$ -$

April 1, 2015 -

March 31, 2016

April 1, 2016 -

March 31, 2017

April 1, 2017 -

March 31, 2018

April 1, 2018 -

March 31, 2019

April 1, 2019 -

March 31, 2020

Month DY1 DY2 DY3 DY4 DY5

April 223,376.29$

May 13,853.96$

June (1,301.37)$

July (2,500.00)$

August

September

October

November

December

January

February 31,200.04$

March 5,100.39$

Grand Total 36,300.43$ 233,428.88$ -$ -$ -$

EXPENSE : Incentives

EXPENSE : Non-Covered Services

$-

$5,000.00

$10,000.00

$15,000.00

$20,000.00

$25,000.00

$30,000.00

DY1 DY2

$(50,000.00)

$-

$50,000.00

$100,000.00

$150,000.00

$200,000.00

$250,000.00

DY1 DY2

10/27/2016

All expenses are reflected in GL290 file exported from Lawson General Ledger System

No Cost of Implementation expenses for March ‘16

No Workforce expenses for March ‘16

No Revenue Loss cleared the GL during March ‘16 CONFIDENTIAL

Type Payment # Description Month/Year NYP/Q CY Amount Received Anticipated Amount Variance Notes

Grant Grant 1 Grant Payment #1 Pre DSRIP 2015 500,000$ 500,000$

Grant Grant 2 Grant Payment #2 Pre DSRIP 2015 1,299,999$ 1,299,999$

DSRIP DY1-1 Project Plan Payment Jun-15 2016 1,102,491$ 1,102,491$

DSRIP DY1-2 DY1 Q1 & Q2 Jan-16 2016 367,497$ 367,497$

DSRIP DY1-3 DY1 Q3 & Q4 Jul-16 2016 367,497$ 367,497$

EIP DY1 Emblem (Health Insurance Plan) Aug-16 2016 127,950$ 149,270$ 21,320$ EIP PPM rate issue NYS - MCO ; pending adjustment

EIP DY1 Empire (Amerigroup) Aug-16 2016 447,539$ 447,539$

Payment received Sept 2016 - need confirmation on

amount

EIP DY1 Fidelis Oct-16 2016 305,165$ Contracts executed - pending payment

EIP DY1 Health First Oct-16 2016 757,571$ Contracts executed - pending payment

EIP DY1 MetroPlus Oct-16 2016 179,286$ Contracts executed - pending payment

EIP DY1 United Oct-16 2016 196,998$ Contracts executed - pending payment

EIP DY2-1 Emblem (Health Insurance Plan) Oct-16 2016 74,635$

EIP DY2-1 Empire (Amerigroup) Oct-16 2016 223,770$

EIP DY2-1 Fidelis Oct-16 2016 152,583$

EIP DY2-1 Health First Oct-16 2016 378,786$

EIP DY2-1 MetroPlus Oct-16 2016 89,643$

EIP DY2-1 United Oct-16 2016 98,499$

DSRIP DY2-1 DY2 Q1 & Q2 Jan-17 2017 906,854$

EPP DY1 Emblem (Health Insurance Plan) Jan-17 2017 99,513$ Pending DOH release of EPP data - Guess January 2017

EPP DY1 Empire (Amerigroup) Jan-17 2017 298,359.22$ Pending DOH release of EPP data - Guess January 2017

EPP DY1 Fidelis Jan-17 2017 203,443$ Pending DOH release of EPP data - Guess January 2017

EPP DY1 Health First Jan-17 2017 505,047$ Pending DOH release of EPP data - Guess January 2017

EPP DY1 MetroPlus Jan-17 2017 119,524$ Pending DOH release of EPP data - Guess January 2017

EPP DY1 United Jan-17 2017 131,332$ Pending DOH release of EPP data - Guess January 2017

EIP DY2-2 Emblem (Health Insurance Plan) Apr-17 2017 74,635$

EIP DY2-2 Empire (Amerigroup) Apr-17 2017 223,770$

EIP DY2-2 Fidelis Apr-17 2017 152,583$

EIP DY2-2 Health First Apr-17 2017 378,786$

EIP DY2-2 MetroPlus Apr-17 2017 89,643$

EIP DY2-2 United Apr-17 2017 98,499$

DSRIP DY2-2 DY2 Q3 & Q4 Jul-17 2017 1,051,470$

EIP DY3-1 Emblem (Health Insurance Plan) Oct-17 2017 74,635$

EIP DY3-1 Empire (Amerigroup) Oct-17 2017 223,770$

EIP DY3-1 Fidelis Oct-17 2017 152,583$

EIP DY3-1 Health First Oct-17 2017 378,786$

EIP DY3-1 MetroPlus Oct-17 2017 89,643$

EIP DY3-1 United Oct-17 2017 98,499$

Grand Totals 4,212,973$ 12,042,600$ 21,320$

Will we get DY2 EPP in 2017??

Source of Revenue numbers is reconciliation cover page for DSRIP account.

Value Based Payment (V.B.P.)

Baseline & Readiness Network Assessment

September 2016

Purpose

Create a baseline assessment of the New York-Presbyterian/Queens PPS partner network to

include contracting status and a readiness assessment for moving to alternative payment

methodologies.

________________________________________________________________

Financial sustainability is an overall goal of the DSRIP program; therefore, the NYS DOH has

established milestones related to value based payment methodologies inclusive of a

comprehensive baseline assessment. The assessment was completed utilizing a survey

methodology for all network partners and is summarized in the below slide deck. This analysis

is inclusive of a baseline assessment of actual alternative payment models as well as a

readiness assessment for moving toward such models.

To ensure compliance with all local and federal regulations, all survey questions were not

specific to payer or contractual relationships but included general questions relating to

categories associated with value based payment arrangements.

The PPS’ collaborative model will utilize this analysis to focus on education, connectivity, and

quality analytics, which our network partners will be able to use to provide tools and resources

for individual teams to work with MCO’s in order to move towards risk based models.

2016 V.B.P. Survey 2

Governing Process

The VBP baseline assessment was completed by the Project Management Office

with reviews and approvals for publishing by the Finance Committee as well as

the Executive Committee.

Approvals of this assessment will be completed in October 2016.

Presentation Title 3

What is Value Based Payment (V.B.P.)?

National healthcare strategy used by healthcare systems to promote quality and

value of health care services utilizing non fee for service payment methodologies

focused to quality based outcomes. Goals include:

Shift from pure volume-based payment (Fee-for-Service) to those that are

outcome related

Implement pay for performance programs that reward improvements in

quality metrics & aligns risks of all parties

Establish methodologies that align with the complexity of the patient base

as well as the offerings of the system with the strategies of the managed

care organization

Engage multiple facets of the healthcare system to encourage quality

based outcomes by assigning levels of risk

Establish data reporting & warehousing mechanisms for tracking and

ongoing performance reporting

2016 V.B.P. Survey 4

Survey Categories

I. Organization Type

II. Current Value/Equity Payment Arrangements

III. V.B.P. Model Preferences

IV. Current V.B.P. Aligned Medicaid Managed Care Organization (M.C.O.)

Strategies

V. Readiness to convert 90% of Medicaid revenue sources to a V.B.P.

methodology

VI. Training Topic Interest Areas

The following slides summarize the data compiled by category &

organization type.

2016 V.B.P. Survey 5

Organization Types

2016 V.B.P. Survey 6

0 2 4 6 8 10 12 14 16 18 20

Outpatient Behavioral Health (Art 31 & Art 32)

Article 28 Diagnostic & Treatment Centers

Article 16 Clinics (OPWDD)

Private Practice Provider – Primary Care

Private Practice Provider – Specialty Care

Hospital Article 28 Outpatient Clinics

Inpatient Home Care Agency

Licensed Hospice

Long-Term Acute Care Hospital

Nursing Home/SNF

Non-licensed CBO

Article 36 Certified Home Health Agency

4. Type of Organization

Results

All network partners were sent the VBP survey

(35) unique partners provided responses

(40) organization types reported

- Some partners counted their business operations among multiple

classifications

Nursing Homes/Skilled Nursing Facilities represented 45% of the total

responses

2016 V.B.P. Survey 7

Current Value/Equity Payment Arrangements

2016 V.B.P. Survey 8

0 5 10 15 20 25

Yes

No

N/A

Results

34% of the partner reporting population indicated, YES, to current

arrangements

62% of the partner reporting population indicated, NO, to current arrangements

PPS Opportunities:

- Education to increase familiarity with VBP concepts

- Growth opportunity to introduce unique VBP concepts

2016 V.B.P. Survey 9

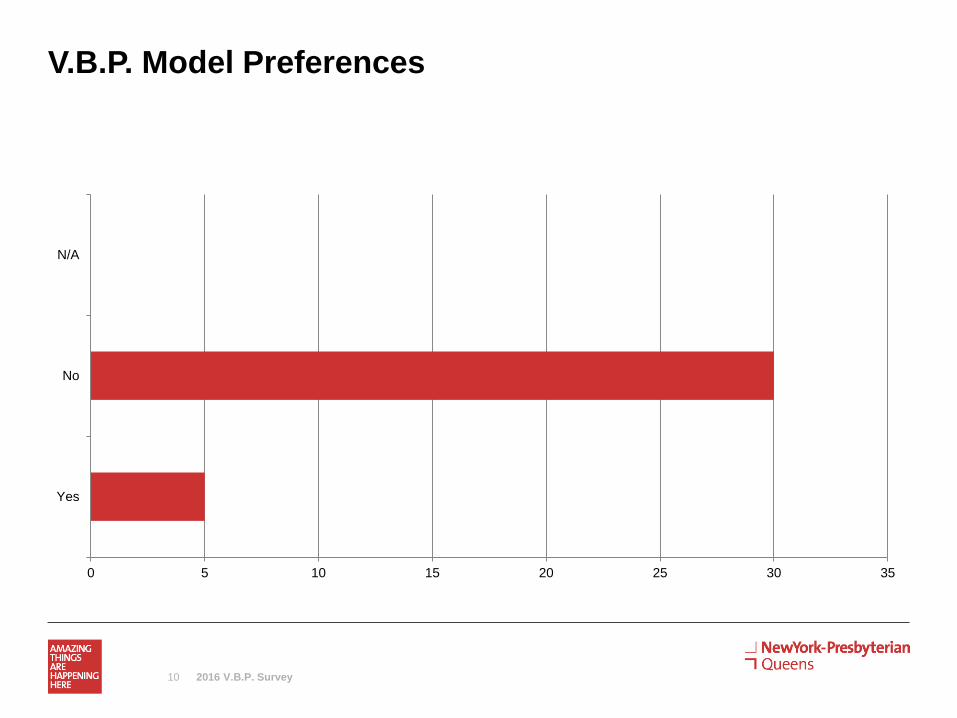

V.B.P. Model Preferences

2016 V.B.P. Survey 10

0 5 10 15 20 25 30 35

Yes

No

N/A

Results

85% indicated NO preference to any specific V.B.P. model

15% indicated YES to a preference of a specific V.B.P. model

PPS Opportunities:

- Education of unique types of VBP arrangements in the local market

- Alignment of education with the findings from the Rapid Cycle Evaluation

Unit

- Engagement with MCO’s for discussions of concepts that align with

population strategies

2016 V.B.P. Survey 11

Current V.B.P. Aligned Medicaid Managed Care

Organization (M.C.O.) Strategies

2016 V.B.P. Survey 12

0 5 10 15 20 25 30

Yes

No

N/A

Results

80% indicated No to having any current V.B.P. Aligned Medicaid Managed

Care Organization (M.C.O.) Strategies

20% indicated YES to having any current V.B.P. Aligned Medicaid Managed

Care Organization (M.C.O.) Strategies

PPS Opportunities:

- Incorporation of multiple provider / payer strategies by network partners

- Lessons learned among network partners for VBP arrangements

2016 V.B.P. Survey 13

Readiness to convert 90% of Medicaid revenue sources

to a V.B.P. methodology

2016 V.B.P. Survey 14

0 2 4 6 8 10 12 14

Confident our organization is ready for the change

Slightly confident our organization is ready for the change

No confidence that our organization is ready for the change

Unsure of our readiness

Results

37% Unsure

34% Slightly confident

25% Confident

PPS Opportunities:

- Provide basic education models for partner network

- Partner with Medicaid MCO’s to roll-out any existing educational programs

for VBP

- Utilize Rapid Cycle Evaluation Unit quality analysis to provide partners

baseline quality assessments

2016 V.B.P. Survey 15

Training Topic Interest Areas

2016 V.B.P. Survey 16

0 5 10 15 20 25 30 35

Overall education of VBP options

Alignment of VBP with DSRIP programs

Quality based outcome analytics

MCO sponsored learning collaborative aligned with their benefit plans

National trends of value based payment methodologies

Maximizing IT tools for VBP scenarios

Other

Results

(3) Highest Requested Topics:

- Overall Education (85%)

- Quality Based Outcome Analytics (85%)

- I.T. Tool Maximization (80%)

PPS Opportunities:

- High interest in education of VBP models

- Utilization of Rapid Cycle Evaluation Unit data analytics for quality reporting

2016 V.B.P. Survey 17

Existing V.B.P. Arrangements Within NewYork-

Presbyterian/Queens PPS Network

2016 V.B.P. Survey 18

99.5%

3.0%

65.0%

0.0%

40.0%

0.49%

1%

0%

0%

60%

0%

0%

0%

0.90%

0%

0%

0%

0%

0%

0%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

1. All care for total population

2. All care for total population

3. Acute and Chronic Bundles

4. Acute and Chronic Bundles

5. All care for total population

Level 3 VBP

Level 2 VBP

Level 1 VBP

Level 0 VBP

Next Steps

Receive approvals from Finance & Executive Committees

Establish an educational program for value based payment opportunities

Await VBP NYS DOH updates to all deliverables

Align VBP data needs with the Rapid Cycle Evaluation Unit (in development)

Establish communication channels specific to VBP utilizing website,

Healthstreams, or Performance Logic

Presentation Title 19

Summary

Thank you to all our network partners that provided us with responses

- Any questions regarding what was discussed or for copies of anything

presented, please feel free to contact:

2016 V.B.P. Survey 20

Sadia Choudhury

Director

DSRIP PMO Office

E-Mail: [email protected]

Daniel M. Notarnicola

Financial Analyst

DSRIP PMO Office

E-Mail: [email protected]

![Microsoft PowerPoint - NYP talk.ppt [Read-Only]](https://img.pdfslide.us/doc/110x75/5589527ad8b42aea0b8b45d6/microsoft-powerpoint-nyp-talkppt-read-only.jpg)