Embed Size (px)

Citation preview

Nuffield International Contemporary Scholars Conference New Zealand - March 2011

Brazilian Agriculture DevelopmentIn a Global Perspective

Milton SuzukiBayer CropScience

Development and Field Trial - Latin America

Latin America Agriculture Potential1.

2.

3.

4.

Brazilian Agriculture Overview

Opportunities

Challenges

Content

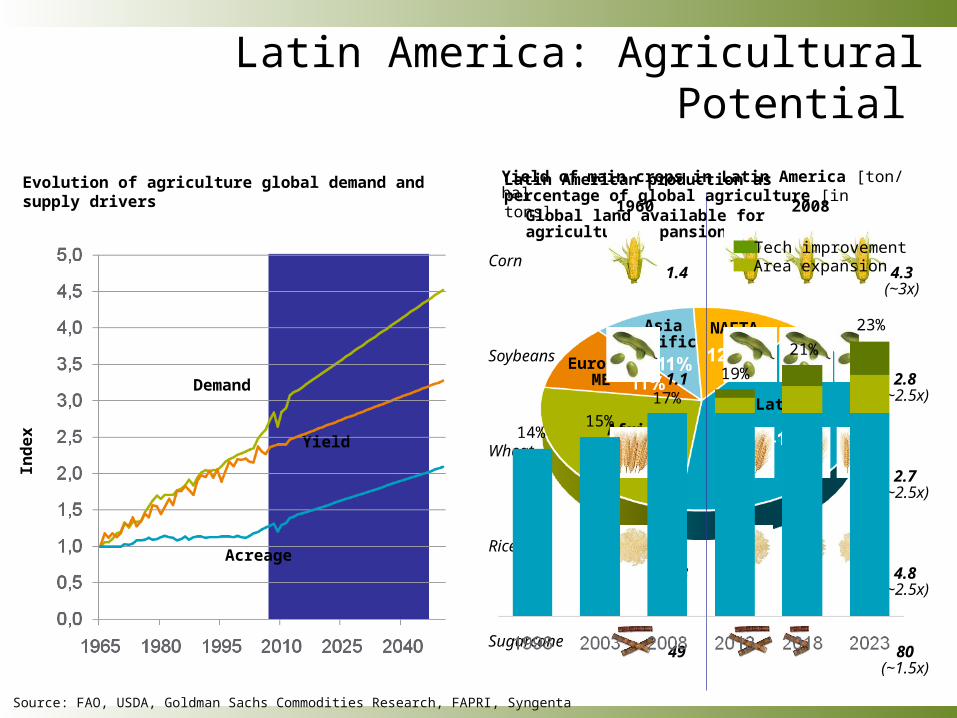

Latin America: Agricultural Potential

Evolution of agriculture global demand and supply drivers

Global land available for agriculture expansion

LatAm

Europe/ ME

Asia PacificNAFTA

Africa

Ind

ex

Demand

Yield of main crops in Latin America [ton/ ha]

Corn

Soybeans

1960

1.4

1.1

Wheat

1.1

Rice

1.8

Sugarcane49

2008

4.3(~3x)

2.8(~2.5x)

2.7(~2.5x)

4.8(~2.5x)

80(~1.5x)

Yield

Acreage

Source: FAO, USDA, Goldman Sachs Commodities Research, FAPRI, Syngenta

Latin American production as percentage of global agriculture [in tons]

14%15%

17%

19%

21%

23%

Tech improvementArea expansion

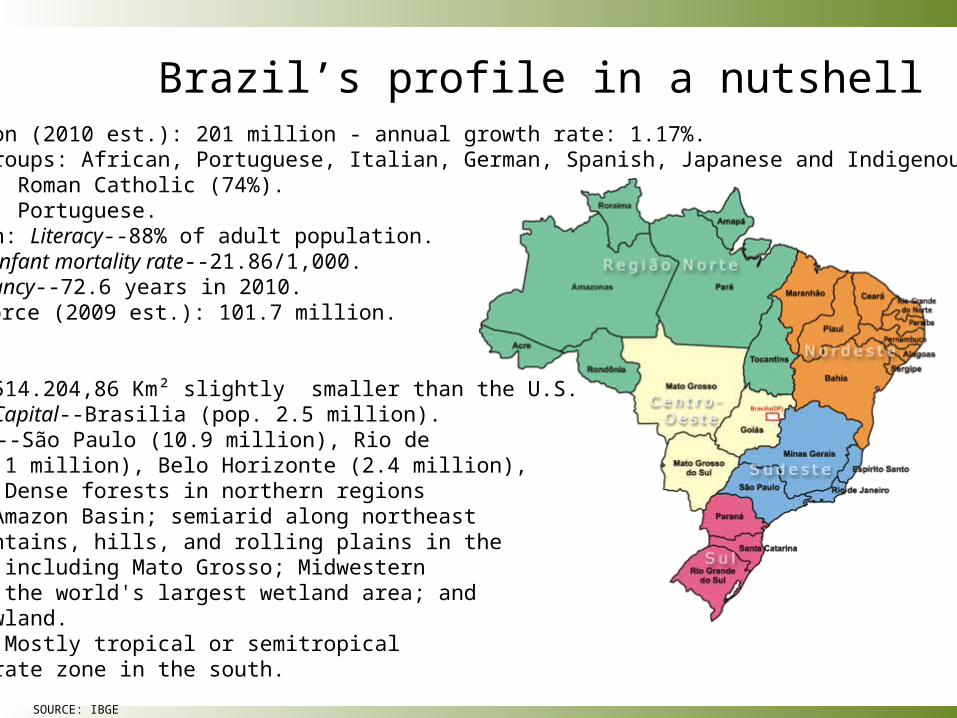

People Population (2010 est.): 201 million - annual growth rate: 1.17%. Ethnic groups: African, Portuguese, Italian, German, Spanish, Japanese and Indigenous peoples, Religion: Roman Catholic (74%). Language: Portuguese. Education: Literacy--88% of adult population. Health: Infant mortality rate--21.86/1,000. Life expectancy--72.6 years in 2010.

Work force (2009 est.): 101.7 million.

Geography Area: 8.514.204,86 Km² slightly smaller than the U.S. Cities: Capital--Brasilia (pop. 2.5 million). Other cities--São Paulo (10.9 million), Rio de Janeiro (6.1 million), Belo Horizonte (2.4 million), Terrain: Dense forests in northern regions including Amazon Basin; semiarid along northeast coast; mountains, hills, and rolling plains in the southwest, including Mato Grosso; Midwestern savannahs; the world's largest wetland area; and coastal lowland. Climate: Mostly tropical or semitropical with temperate zone in the south.

Brazil’s profile in a nutshell

SOURCE: IBGE

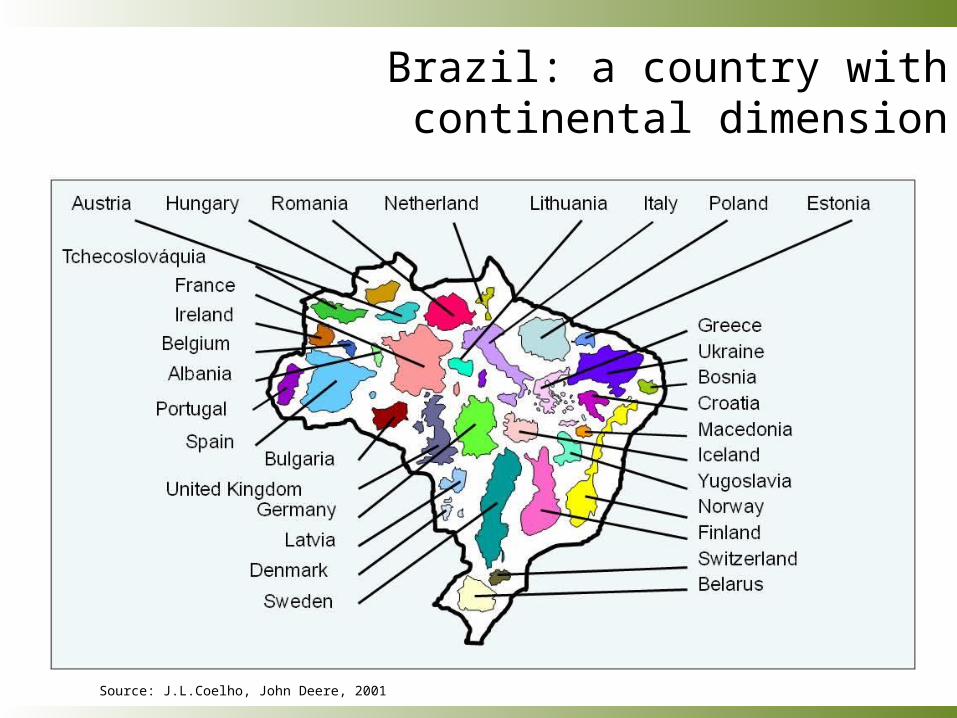

Brazil: a country with continental dimension

Source: J.L.Coelho, John Deere, 2001

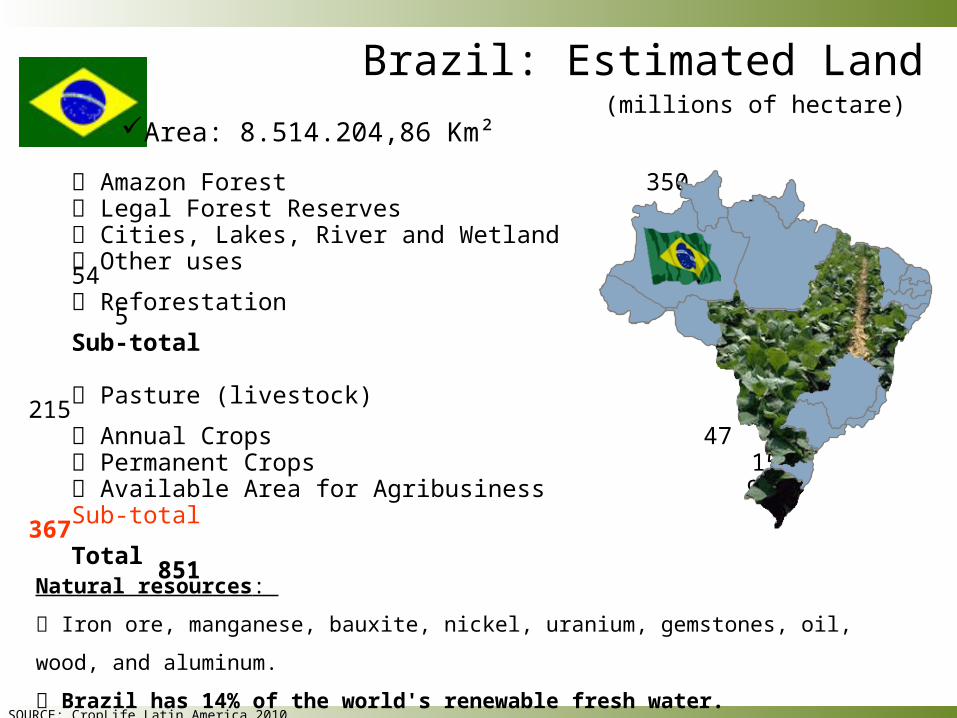

Amazon Forest 350 Legal Forest Reserves 55 Cities, Lakes, River and Wetland 20 Other uses 54 Reforestation 5 Sub-total 484

Pasture (livestock) 215 Annual Crops 47 Permanent Crops 15 Available Area for Agribusiness 90 Sub-total 367 Total 851

Brazil: Estimated Land(millions of hectare)

SOURCE: CropLife Latin America 2010

Area: 8.514.204,86 Km²

Natural resources:

Iron ore, manganese, bauxite, nickel, uranium, gemstones, oil, wood, and aluminum.

Brazil has 14% of the world's renewable fresh water.

Agriculture is a major sector of the Brazilian economy, and is key for economic growth and foreign exchange.

Agriculture accounts for about 5.5% of GDP (25% when including agribusiness) and 36% of Brazilian exports.

Brazil enjoyed a positive agricultural trade balance of US$55 billion in 2009.

Brazil is the world's largest producer of sugarcane, coffee, tropical fruits, frozen concentrated orange juice (FCOJ), and has the world's largest commercial cattle herd (50% larger than that of the U.S.) at 170 million head.

Brazil is also an important producer of soybeans (second to the United States), corn, cotton, cocoa, tobacco, and forest products.

The remainder of agricultural output is in the livestock sector, mainly the production of beef and poultry (second to the United States), pork, milk, and seafood.

Brazil: Agriculture outlook

SOURCE: state.gov.

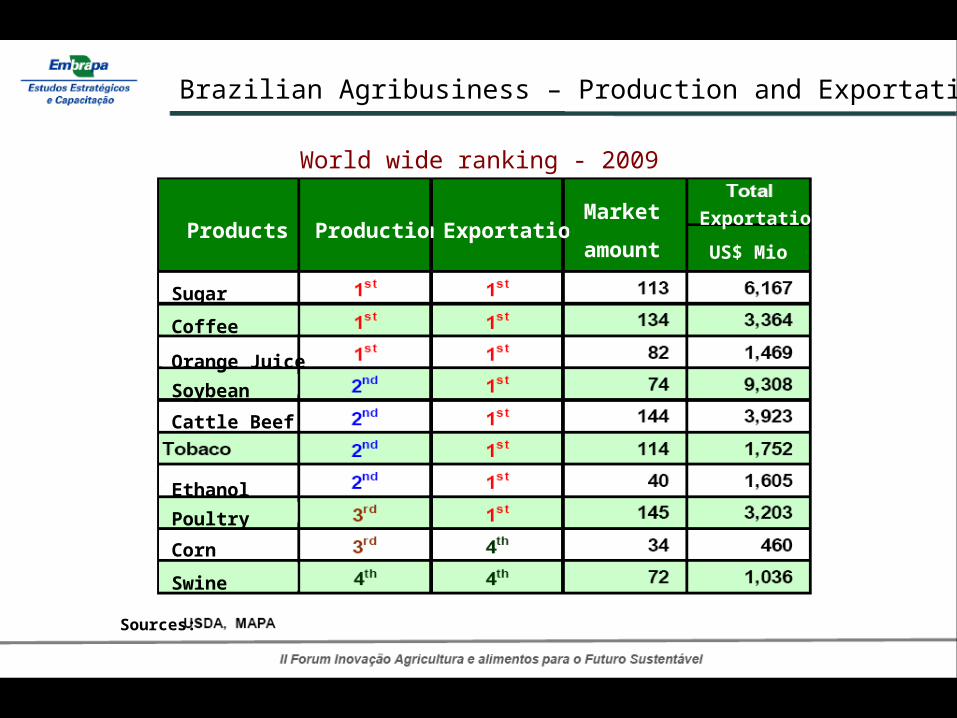

Brazilian Agribusiness – Production and Exportation

Products

Sources:

Production ExportationMarket

amount

Exportation

US$ Mio

World wide ranking - 2009

Sugar

Coffee

Soybean

Poultry

Swine

Orange Juice

Cattle Beef

Ethanol

Corn

Brazil: The Opportunity, Still a Challenge

?

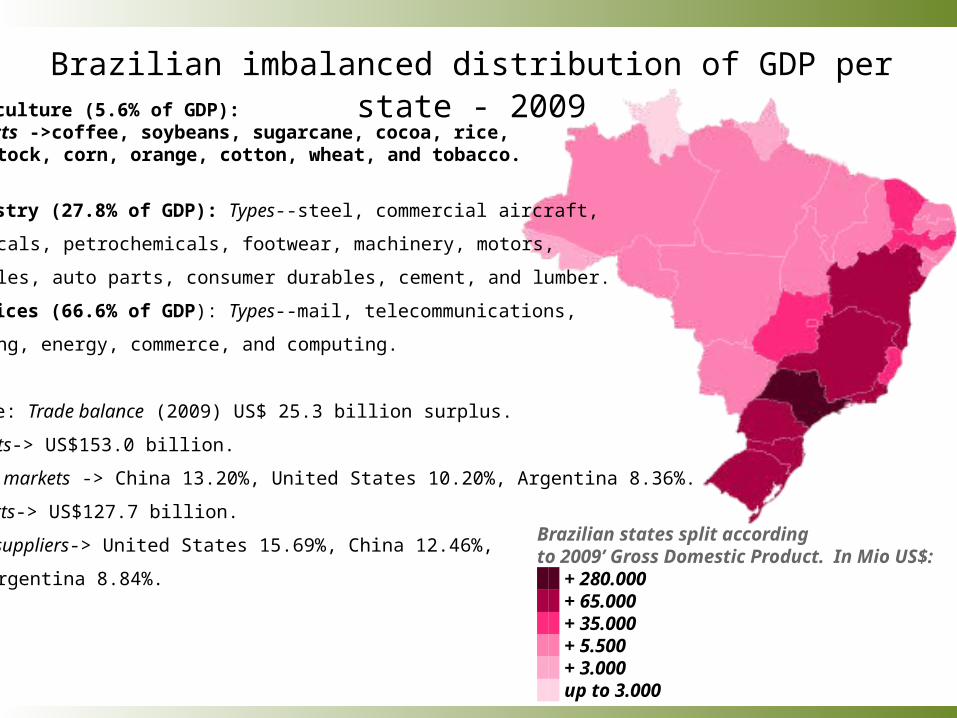

Brazilian states split according to 2009’ Gross Domestic Product. In Mio US$: ██ + 280.000██ + 65.000██ + 35.000██ + 5.500██ + 3.000██ up to 3.000

Brazilian imbalanced distribution of GDP per state - 2009Agriculture (5.6% of GDP): Products ->coffee, soybeans, sugarcane, cocoa, rice, livestock, corn, orange, cotton, wheat, and tobacco.

Industry (27.8% of GDP): Types--steel, commercial aircraft,

chemicals, petrochemicals, footwear, machinery, motors,

vehicles, auto parts, consumer durables, cement, and lumber.

Services (66.6% of GDP): Types--mail, telecommunications,

banking, energy, commerce, and computing.

Trade: Trade balance (2009) US$ 25.3 billion surplus.

Exports-> US$153.0 billion.

Major markets -> China 13.20%, United States 10.20%, Argentina 8.36%.

Imports-> US$127.7 billion.

Major suppliers-> United States 15.69%, China 12.46%,

and Argentina 8.84%.

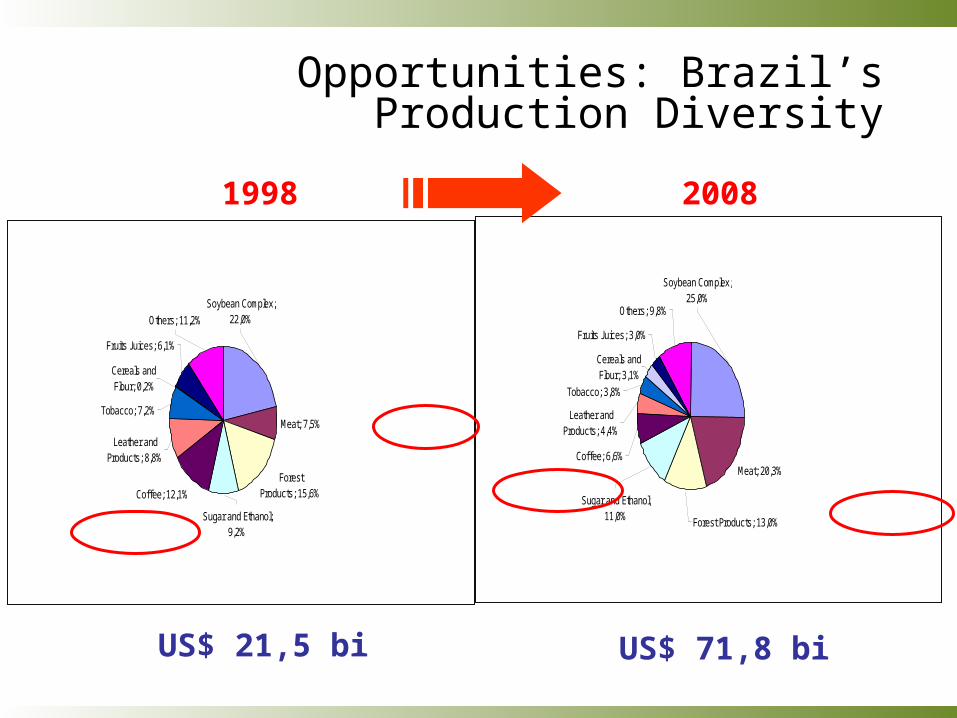

Opportunities: Brazil’s Production Diversity

1998 2008

US$ 21,5 bi US$ 71,8 bi

Meat; 7,5%

Coffee; 12,1%

Sugar and Ethanol; 9,2%

Forest Products; 15,6%

Tobacco; 7,2%

Others; 11,2%

Fruits Juices; 6,1%

Cereals and Flour; 0,2%

Leather and Products; 8,8%

Soybean Complex; 22,0%

Meat; 20,3%

Fruits Juices; 3,0%

Others; 9,8%

Cereals and Flour; 3,1%

Tobacco; 3,8%

Leather andProducts; 4,4%

Coffee; 6,6%

Sugar and Ethanol; 11,0% Forest Products; 13,0%

Soybean Complex; 25,0%

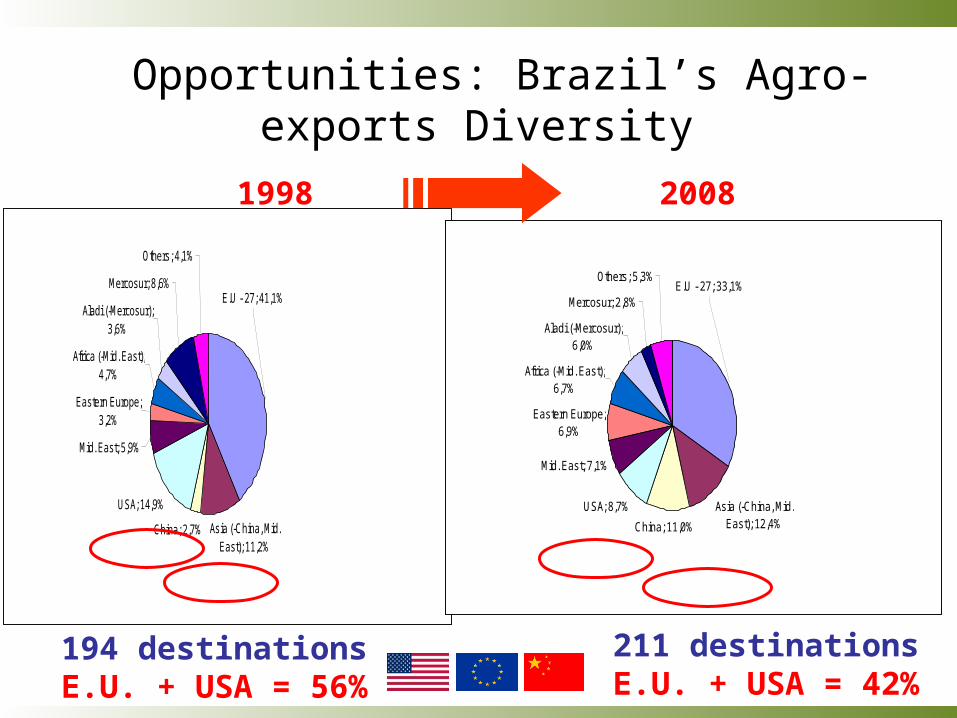

Opportunities: Brazil’s Agro-exports Diversity

Asia (-China, Mid. East); 11,2%

China; 2,7%

USA; 14,9%

Mid. East; 5,9%

Eastern Europe; 3,2%

Africa (-Mid. East); 4,7%

Aladi (-Mercosur); 3,6%

Mercosur; 8,6%

Others; 4,1%

E.U - 27; 41,1%

Asia (-China, Mid. East); 12,4%China; 11,0%

USA; 8,7%

Mid. East; 7,1%

Eastern Europe; 6,9%

Africa (-Mid. East); 6,7%

Aladi (-Mercosur); 6,0%

Mercosur; 2,8%

Others; 5,3%E.U - 27; 33,1%

1998 2008

194 destinationsE.U. + USA = 56%

211 destinationsE.U. + USA = 42%

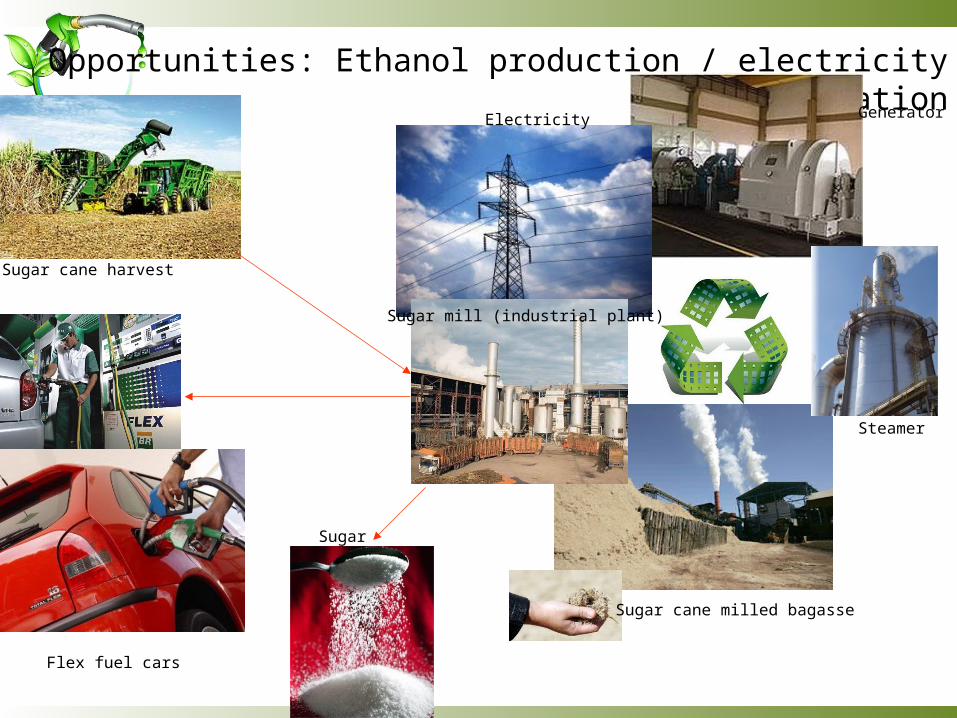

Opportunities: Ethanol production / electricity co-generation

Flex fuel cars

Sugar cane milled bagasse

Steamer

GeneratorElectricity

Sugar

Sugar cane harvest

Sugar mill (industrial plant)

Opportunities: Bio diesel

SOURCE: CropLife Latin America 2010

Issues and bottle necks

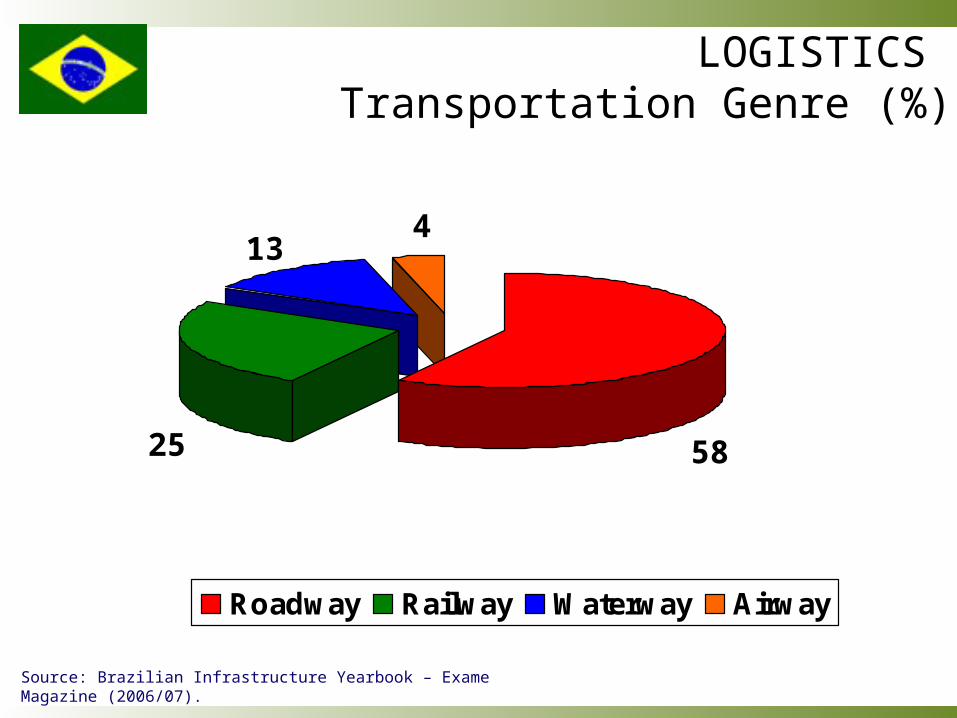

Source: Brazilian Infrastructure Yearbook – Exame Magazine (2006/07).

LOGISTICS Transportation Genre (%)

Roadway Railway Waterway Airway

58

4

25

13

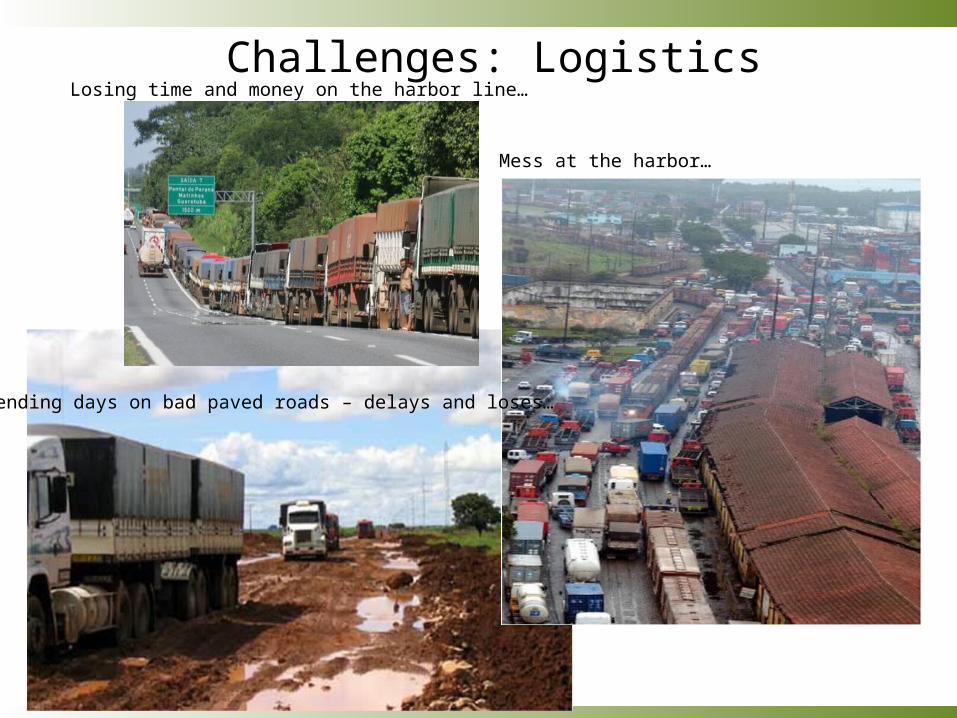

Challenges: Logistics Losing time and money on the harbor line…

Mess at the harbor…

Spending days on bad paved roads – delays and loses…

Challenges: Logistics

Santos’ harbor (BR) occupies position #41 world wide in container movement

Challenges: Logistics

Folha de São Paulo says: Worse logistic takes out US$3,9 billion from agribusiness

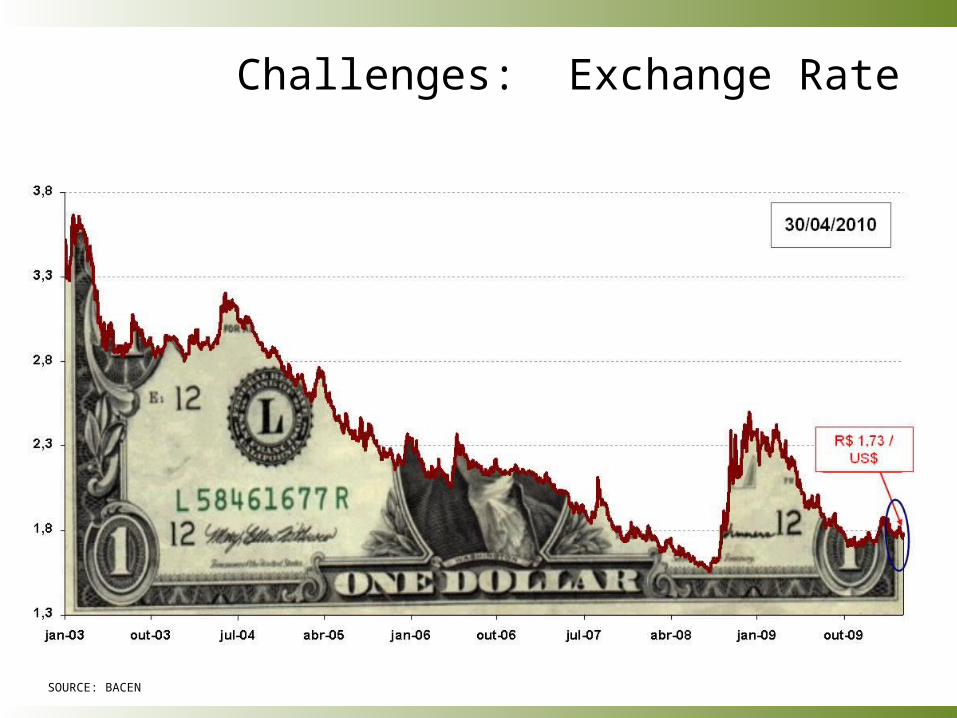

Challenges: Exchange Rate

SOURCE: BACEN

In sum, yes Brazil is not only...

Carnival party Soccer/football Amazon forest

It also is...

food feed fuel

Latin America has the potential to be a global efficient supplier of food, fiber, feed and renewable energies.

Investment & enablement of

technology

Investment in human capital & infrastructure

Business-oriented policies