Embed Size (px)

Citation preview

NUCLEAR POWER

BOOKLETS

APRIL 2016 | YEAR 3 | No. 6 | ISSN 2358-5277

NUCLEAR POWER

DIRECTOR Carlos Otavio de Vasconcellos Quintella TECHNICAL STAFF Editorial Coordination Felipe Gonçalves Authors Felipe Gonçalves Renata Hamilton de Ruiz

PRODUCTION STAFF Operational Coordination Simone Corrêa Lecques de Magalhães Desktop Publishing Bruno Masello and Carlos Quintanilha [email protected]

FIRST FOUNDING PRESIDENT Luiz Simões Lopes PRESIDENT Carlos Ivan Simonsen Leal VICE-PRESIDENTS Sergio Franklin Quintella, Francisco Oswaldo Neves Dornelles and Marcos Cintra Cavalcanti de Albuquerque BOARD OF DIRECTORS President Carlos Ivan Simonsen Leal Vice-Presidents Sergio Franklin Quintella, Francisco Oswaldo Neves Dornelles and Marcos Cintra Cavalcanti de Albuquerque Members Armando Klabin, Carlos Alberto Pires de Carvalho e Albuquerque, Ernane Galvêas, José Luiz Miranda, Lindolpho de Carvalho Dias, Marcílio Marques Moreira and Roberto Paulo Cezar de Andrade Deputies Antonio Monteiro de Castro Filho, Cristiano Buarque Franco Neto, Eduardo Baptista Vianna, Gilberto Duarte Prado, Jacob Palis Júnior, José Ermírio de Moraes Neto and Marcelo José Basílio de Souza Marinho. TRUSTEE COUNCIL President Carlos Alberto Lenz César Protásio Vice-President João Alfredo Dias Lins (Klabin Irmãos e Cia) Members - Alexandre Koch Torres de Assis, Angélica Moreira da Silva (Brazilian Federation of Banks), Ary Oswaldo Mattos Filho (EDESP/FGV), Carlos Alberto Lenz Cesar Protásio, Carlos Moacyr Gomes de Almeida, Eduardo M. Krieger, Fernando Pinheiro e Fernando Bomfiglio (Souza Cruz S/A), Heitor Chagas de Oliveira, Jaques Wagner (State of Bahia), João Alfredo Dias Lins (Klabin Irmãos & Cia), Leonardo André Paixão (IRB - Brasil Resseguros S.A.), Luiz Chor (Chozil Engenharia Ltda.), Marcelo Serfaty, Marcio João de Andrade Fortes, Orlando dos Santos Marques (Publicis Brasil Comunicação Ltda.), Pedro Henrique Mariani Bittencourt (Banco BBM S.A.), Raul Calfat (Votorantim Participações S.A.), Ronaldo Mendonça Vilela (Trade Union of Private Insurance, Capitalization and Reinsurance Companies of the States of Rio de Janeiro and Espírito Santo), Sandoval Carneiro Junior (DITV - Dept. Vale Technology Institute)

and Tarso Genro (State of Rio Grande do Sul). Deputies - Aldo Floris, José Carlos Schmidt Murta Ribeiro, Luiz Ildefonso Simões Lopes (Brookfield Brasil Ltda.), Luiz Roberto Nascimento Silva, Manoel Fernando Thompson Motta Filho, Roberto Castello Branco (Vale S.A.), Nilson Teixeira (Banco de Investimentos Crédit Suisse S.A.), Olavo Monteiro de Carvalho (Monteiro Aranha Participações S.A.), Patrick de Larragoiti Lucas (Sul América Companhia Nacional de Seguros), Rui Barreto (Café Solúvel Brasília S.A.), Sérgio Lins Andrade (Andrade Gutierrez S.A.), and Victório Carlos De Marchi (AMBEV).

EXECUTIVE BOARD Carlos Otavio de Vasconcellos Quintella RESEARCH COORDINATION Lavinia Hollanda COORDINATION OF INSTITUTIONAL RELATION Luiz Roberto Bezerra COORDINATION OF TEACHING AND R&D Felipe Gonçalves OPERATIONAL COORDINATION Simone Corrêa Lecques de Magalhães RESEARCHERS Bruno Moreno R. de Freitas Camilo Poppe de Figueiredo Muñoz Mariana Weiss de Abreu Michelle Bandarra Mônica Coelho Varejão Rafael da Costa Nogueira Renata Hamilton de Ruiz INTERN Júlia Febraro F. G. da Silva ADMINISTRATIVE ASSISTANT Ana Paula Raymundo da Silva CONSULTANT Paulo César Fernandes da Cunha

PRAIA DE BOTAFOGO, 190, RIO DE JANEIRO - RJ - POSTAL CODE 22250-900 OR POSTAL BOX 62.591 - POSTAL CODE 22257-970 - TELEPHONE (21) 3799-5498 - WWW.FGV.BR

Institution of technical and scientific, educational, and charitable nature created on December 20, 1944 as a private legal entity with the purpose of fully acting in all scientific matters, and emphasizing in the field of social sciences: administration, law and economy, thus contributing to the country’s social and economic development.

Preface

José Luiz Alquéres A history of development and use of nuclear power in Brazil is a history with ups and downs. However, it allows us a great learning and some lessons. The first lesson is that using any form of power - in the case of nuclear even more - is a matter of the society. Cabinets should not make this decision, neither support obscure “strategic reasons” for its development. This is a type of power that requires a long construction cycle, major investments and exceptional care in safety. Even after many of its implementation, as we saw in Germany, it can be discontinued by political and emotional factors. Hence the need for a public opinion supporting it, evidently after a deep discussion on the advantages and disadvantages of its adoption. This did not happen in Brazil, neither in most countries that explore it - which explains the sarcastic conclusion of The Economist’s specialized article “... nuclear power seems to be destined for implementation only in authoritarian countries and not the democratic ones” published recently. The second lesson is that it should not be installed near large and medium agglomerations of people as Angra dos Reis, for example. Reduced losses in power transmission, which was a claimed ‘advantage’,

stopped being considered after the tragedy in Fukushima. In my opinion, 6 to 10 plants concentrations should be installed in areas apart from current federation units and inside the national territories, protected by the strictest security codes of our armed forces. The third lesson is that uranium mining and plants construction and operation should be opened for national or foreign investors, being restricted to the so-called ‘fuel cycle’ federal monopoly and the property and storage of waste. The fourth lesson - and confirmation - is that the Brazilian history building, operating, training staff and managing safety is excellent. We were capable of recovering Angra 1, the former Westinghouse technology “firefly plant”, transforming it into an efficient plant. It was also noted in the same line that Angra 2 - the first one of the Brazil-Germany agreement - stood out many years in the global reliability ranking. It is also recognized that we know how to train high quality professionals. Such efforts and characteristics seem lost or forgotten nowadays, but YES we can! Here in this brief introduction to FGV Energia Special Booklet that deeply discusses

and will mark nuclear power situation point in Brazil, I understand that the fifth and last topic should emphasize the right moment to make decisions instead of postponing it.

Many of the nuclear power problems came from ups and downs, postponements, legal suspensions (sometimes disregarding technical factors), discontinuation of financial resources, and other factors, which made 4 to 5 years works last over 30 years.

After analyzing the relevant factors and discussing pros and cons in the National Congress, in mid 1994, when I was the president of Eletrobras and a member of its Board of Directors, I faced Angra 2 peculiar situation: after years of interruption in works, the barriers that prevented its conclusion were finally solved.

In fact, contrary to the lesson above, showing that it is better to install nuclear plants in points of reduced urban density, there was Angra 2 work in a region that grew without the due planning in the almost fifteen-year in which works were stopped.

Anyway, new investments were made for special alarms measures, expansion of the drainage capacity through roads and safer

operation strategies - which provided the necessary tranquility to authorize the continuation of the work, thus “saving” billions of resources already invested and not putting the population at risk.

We were in the interim between the final months of the term of a President of the Republic and the new term of the President elected. The theme was destined to be suspended until the new Government decided to resume it - which could take time. However, power demand was growing (which in fact grew even more with the success of Real Plan, as was noted later). Given this scenario, I understood to be relevant - and received authorization from the Board of Directors of the company - submitting a Letter of Eletrobras to Furnas authorizing the remobilization of the site and the immediate resumption of works. Naturally, along with Dr. Ronaldo Fabrício, President of that large company.

The work was no longer interrupted and, today, besides being an essential generator of our system, it reaches full performance in similar units according to parameters defined and assessed by WANO (World Association of Nuclear Operators) - a Brazilian technical capacity certificate in the nuclear field.

José Luiz Alquéres - Performed or will perform roles in the Board of Directors. President or Director of large companies as Eletrobras, Light, MDU Brasil, EDP, Angra Partners, Cia. Bozano Simonsen, ALSTOM, Signatura Lazard-Freres, Banco Credit Lyonnais, Rio Bravo, CEMIG and others. Former president of ACRJ (Commercial Association of Rio de Janeiro). Former National Secretary of Energy and Director of BNDESPAR. Honorary Vice-President of the Global Board of Energy and philanthropist.

Prologue

Leonam dos Santos Guimarães There are 67 nuclear plants currently in construction around the world: 23 in China, 9 in Russia, 6 in India, 5 in the USA, 4 in South Korea, 4 in the United Arab Emirates, 2 in Japan, 2 in Belarus, 2 in Ukraine, 2 in Pakistan, 2 in Slovakia, 2 in Taiwan, 1 in Argentina, 1 in Finland, 1 in France, and 1 in Brazil. The United Kingdom recently launched the construction of 2 other plants. The power of these new units represents 18% of increase to the power installed of the 439 plants in operation, which currently generate 12% of the electricity produced in the world. Forty-five new plants started to operate over the past 10 years. This shows the competitiveness of nuclear generation in terms of production costs. However, two reasons explain why the number of nuclear plants being built is not a lot higher: construction costs and public acceptance. But, there is an important connection between both causes. Public acceptance does not prevent new projects in many important countries as the number of plants in construction shows. The biggest problem is the growing capital investment cost and the difficulties to structure projects to fund these long-term maturation

investments. However, numbers show a greater distance between these costs in the West and the East where most new constructions are located. Some forms allow this distance to be reduced and to address matters related to nuclear power competitiveness. But matters involving public acceptance are at least partially responsible for the underlying problem of construction costs in the Western world. If Fukushima imposed more obstacles for public acceptance and; therefore, for generation costs as well, what can the nuclear industry do about it? The first point to be noted is that public opinion and political support level for nuclear power is basically local. There are major differences from country to country, but we know that even in countries with significant acceptance of nuclear power it varies considerably per region. We also know that, even in countries with strong antinuclear feeling there is an important acceptance in regions around nuclear facilities. It would be wrong to conclude that support for nuclear power in these regions is exclusively because of jobs associated to such

facilities. Familiarity with technology and plants themselves simply accepted as part of everyday life in the region is much more important. This is the main reason why nuclear power is not publicly accepted in other places. Its distance from the society in general leads to a misunderstand and susceptibility to negative images spread so successfully by antinuclear people. This Nuclear Power Booklet, launched by FGV Energia, is a major contribution for the society’s better understand of the important role played by nuclear power generation in Brazil and the world. It introduces reasons why the nuclear option is part of the solution for the global challenge of energy transition, necessary to face climatic changes, and the national challenge of hydrothermal transition of the Brazilian electricity sector in the 21st century.

Nuclear technologies and its risks are discussed and a panoramic view of nuclear power in the world is provided. Considerations on the business model to expand nuclear generation in Brazil are also given proposing improvements to be considered for the structuring of future projects. The Booklet also provides a better understanding of several facets of the future energy and nuclear generation problem by lay readers, but is also a source of useful information for those who already have any involvement in this industrial sector. Such an understanding contributes significantly for public acceptance and consequently reduced nuclear electricity costs, so as to allow its expansion to levels that are compatible with the decarbonization needs of the global power matrix.

Leonam dos Santos Guimarães - Doctor in Naval and Ocean Engineering by USP and Master in Nuclear Engineering by University of Paris XI. Director of Planning, Management and Environment at Eletrobras Eletronuclear, member of the Permanent Nuclear Power Advisory Group of the Director-General of the International Atomic Energy Agency - IAEA, member of the Council of Representatives of the World Nuclear Association - WNA, member of the Business Council of Electricity of FIRJAN/CIRJ and Vice-President of the Latin American Section of the American Nuclear Society. He was the Commercial and Technical Director of Amazônia Azul Tecnologias de Defesa SA - AMAZUL, President Assistant of Eletrobras Eletronuclear and Coordinator of the Nuclear Propulsion Program of the Navy Technology Center in São Paulo - CTMSP.

Acknowledgements We would like to thank the collaboration of all nuclear professionals who helped us preparing this booklet. This work only became possible thanks to the contribution and support of those who provided us their time to talk and give interviews sharing their views, knowledge and experiences in the sector with us. On behalf of FGV Energia, we thank Antonio Barroso, Antonio Müller, Carlos Leipner, Drausio Atalla, João Moreira, João Roberto de Mattos, José Luiz Alquéres, Leonam dos Santos Guimarães, Marcio Zimmermann, Otavio Mielnik, Paulo Berquó, Roberto Travassos, Ronaldo Fabrício, Thiago Almeida and Werner Stratmann, and other professionals who were also present during the preparation of this booklet. We take this opportunity to show our gratitude to our colleagues at FGV Energia who helped us having a more complete and multidisciplinary view on the nuclear sector through daily exchanges of knowledge.

RENATA HAMILTON DE RUIZ Researcher of FGV Energia FELIPE GONÇALVES Coordinator of Teaching and R&D

Table of Contents 11 WHY TALKING ABOUT NUCLEAR POWER?

23 NUCLEAR TECHNOLOGY

37 SAFETY AND RELIABILITY

47 NUCLEAR POWER IN THE WORLD

57 PERSPECTIVES FOR BRAZIL

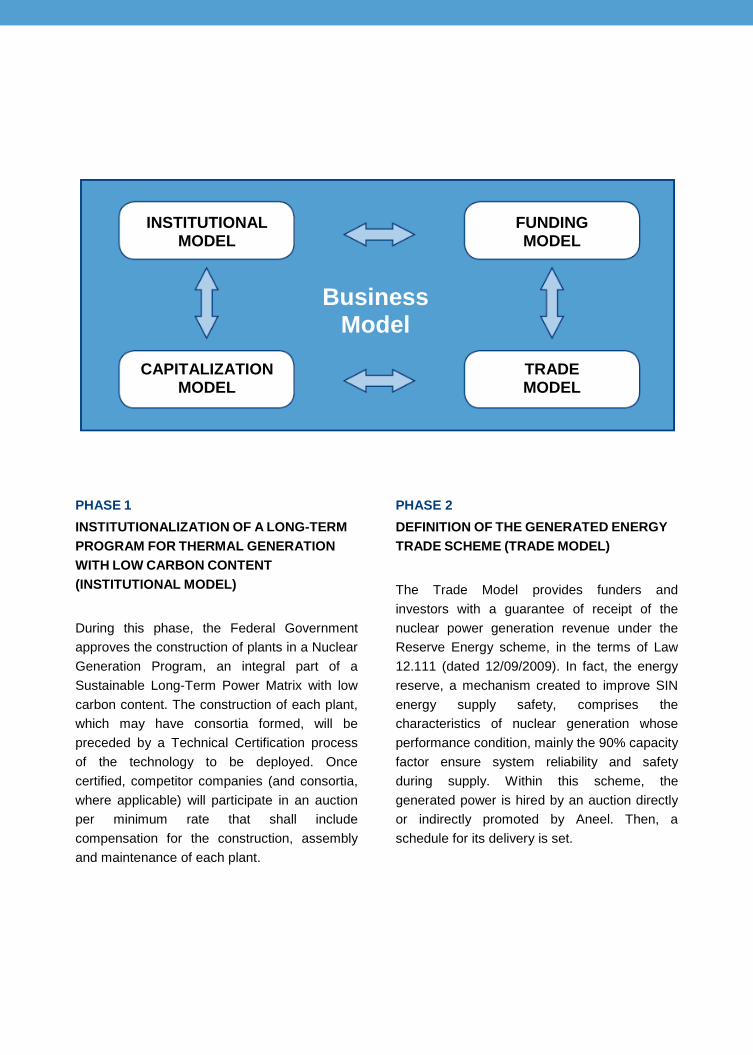

68 BUSINESS MODEL FOR NUCLEAR GENERATION IN BRAZIL

74 FINAL CONSIDERATIONS

76 LIST OF ACRONYMS

78 BIBLIOGRAPHY

Why talking about Nuclear Power? After five years of the greatest earthquake every recorded in the history of Japan, which led to a sequence of events culminating in the partial melting of reactors’ core in Fukushima plant, it is possible to have a distance from emotional visions and bring to debate the challenges and opportunities of nuclear power participation in the composition of the Brazilian power matrix. Despite the feeling of insecurity commonly associated with nuclear power, this is the fourth largest source generating electricity in the world behind coal, natural gas and hydroelectricity [1]. Today, we have 442 nuclear reactors generating power in 30 countries and 66 new reactors being built, notably in countries as China, USA, Russia and members of the European Union [2]. Brazil is one of the few countries that dominates the nuclear fuel cycle and has one of the largest uranium reserves in the world at the same time [3]. In spite of this, this industry is being

developed at a slow pace in the country amid an energy planning focused on the expansion of renewable sources and due to the lack of society’s knowledge regarding the real risks and benefits associated to nuclear power, in addition to regulatory barriers hindering the participation of the private sector in the financing of new plants. People who live near nuclear plants tend to accept more this source once they receive more information on its operation and plants’ safety [4]. Thus, introducing nuclear

The National Interconnected System (SIN) is expected to reduce the power inventory regularization capacity from 6.5 to 4.7 months between 2002 and 2017.

power neutrally becomes the main goal of this FGV Energia booklet, explaining the opportunities and risks of this source to the society, as well as pointing out the challenges and potentials to expand the nuclear industry in Brazil. Analyses and surveys presented herein were made through bibliographic technical research and based on the opinion of different experts selected to represent the different views of the sector. THE NEW PARADIGM OF THE NATIONAL INTERCONNECTED SYSTEM The Brazilian electricity sector has predominantly hydro generator park and in order to ensure continuous meeting of the demand, it depends on power plants with regularization reservoirs so that the confluences

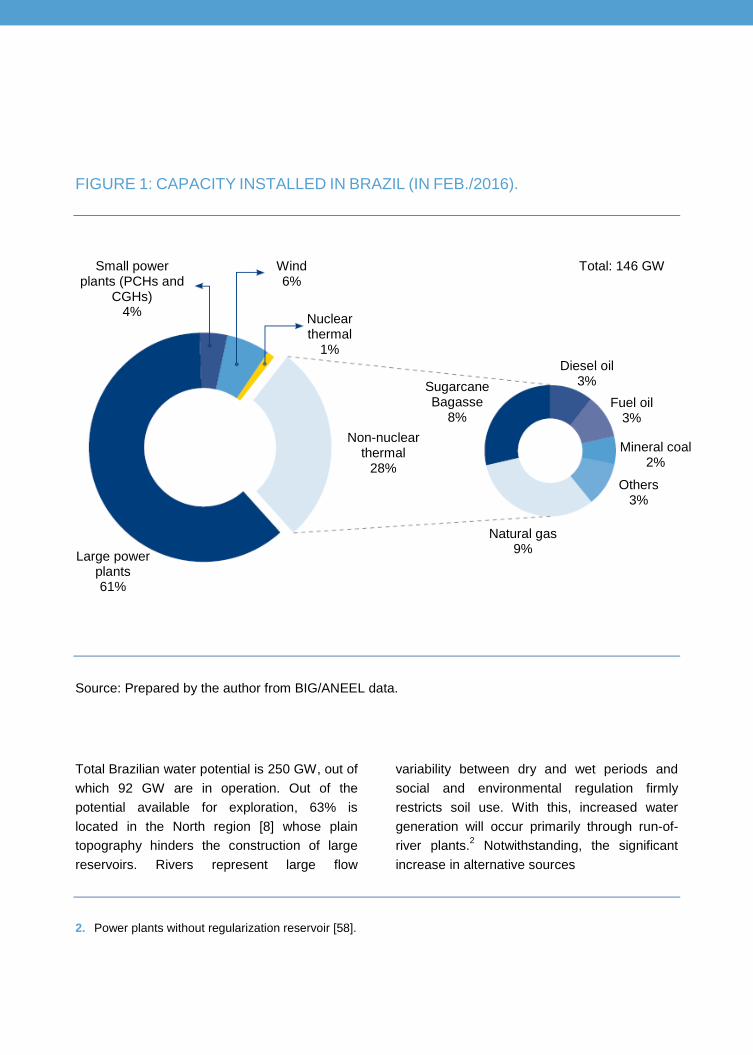

of the wet season can be stored and used in power generation in the dry season. Brazil has a total installed capacity of 146 GW [5], out of which over 60% correspond to large power plants.1 However, the National Electric System Operator (ONS) points out that new power plants with multiannual regularization reservoirs did not come into operation since the end of the 90s [6]. The National Interconnected System (SIN) is expected to reduce the power inventory regularization capacity from 6.5 to 4.7 months between 2002 and 2017 [7]. According to ONS 2014 Energy Operation Plan (PEN), the gradual loss of SIN power plants regularization capacity against the load growth has impacted the results of metrics commonly used to plan the energy operation, such as deficit risks, expected value of non-supplied energy and marginal operation costs [6].

1. Those with installed capacity above 30 MW and reservoir area greater than 3 km2.

FIGURE 1: CAPACITY INSTALLED IN BRAZIL (IN FEB./2016).

Source: Prepared by the author from BIG/ANEEL data. Total Brazilian water potential is 250 GW, out of which 92 GW are in operation. Out of the potential available for exploration, 63% is located in the North region [8] whose plain topography hinders the construction of large reservoirs. Rivers represent large flow

variability between dry and wet periods and social and environmental regulation firmly restricts soil use. With this, increased water generation will occur primarily through run-of-river plants.2 Notwithstanding, the significant increase in alternative sources

2. Power plants without regularization reservoir [58].

Small power plants (PCHs and

CGHs) 4%

Wind 6%

Nuclear thermal

1%

Non-nuclear thermal

28%

Large power plants 61%

Total: 146 GW

Sugarcane Bagasse

8%

Diesel oil 3%

Fuel oil 3%

Mineral coal 2%

Others 3%

Natural gas 9%

as solar and wind power, which have the burden of their intermittency. The Ten-Year Expansion Plan (PDE) 2024 expects the installed capacity of wind plants to reach 24,000 MW while the solar power should reach 7,000 MW by 2024, when they should have a participation of 11.6% and 3.3% in total installed capacity, respectively [9]. Brazilian thermal plants - except for the two Angra nuclear plants - play a supplementary role, that is, they were contracted to meet priority power demands in the dry period, on average 4 months per year. Since these plants are planned to operate outside the basis, triggering them above the plan greatly increases the Marginal Cost of Operation (CMO) of the SIN. The 2013 water crisis made thermal plants operate continuously, which besides causing an impact on the rate increased maintenance and operation costs for agents and reduced equipment reliability. Thermal generation has nearly quadrupled in 3 years, and in June, 2015, more than 30% of all energy generated in Brazil came from thermal sources3 [10]. The lack of a long-term energy strategy strengthens the current structure and only

prioritizes supplementary generation, which compromises the energy diversity. In fact, the energy policy should have background aspects (related to general medium and long-term strategies) and immediate management aspects (related to the economic policy and social Government policy conduction) [11]. Since the electricity matrix progress should maintain the hydroelectricity expansion trend with low or no multiannual regularization and growing entry of intermittent sources, the long-term energy policy should still be accountable of the analysis of thermal sources diversity available to ensure supply security. Currently, 27% of Brazilian thermal plants use sugar cane bagasse as fuel, which is a renewable source impacted by crops seasonality. Another 32% of thermal potential should be moved by natural gas whose consumption tend to grow over the next years although the national production is still not capable to meet the demand. In this context, nuclear generation may play an important role for being a cheap thermal source capable of operating in the basis, thus allowing power plants reservoirs main function to be the regulation of intermittent renewable sources.

3. According to CCEE data, thermal generation in January, 2012 was 4,252 MW on average, and increased to

15,771 MW on average in January, 2015. In June, 2012, thermal generation represented only 14% of the total generated.

Nuclear power has great potential not only to ensure energy safety, but also economic safety (competitive costs and long-term fuel availability) and environmental safety - once fossil fuels are still the major responsible for the emission of greenhouse gas (GHG) in the atmosphere. Another relevant topic is the cost associated to the expansion of the transmission system because the generation potential through

renewable sources should be distant from load centers. In this sense, PEN 2014 notes that the continued transmission expansion, particularly in regional interconnections, is of paramount importance allowing the import and export of large energy blocks between regions. SIN transmission lines, which today have more than 125 thousand kilometers in extension, have a high installation and maintenance cost and end up increasing the final power rate for consumers.4

Capacity Factors The Capacity Factor is the ration between energy produced in fact by a plant and its nominal production capacity. According to data from the Ministry for Mines and Energy (MME) [12], the average capacity factor of Brazilian power plants has been dropping in the last few years: from 57% in 2012 to 52% in 2013 and 49% in 2014. The capacity factor of wind plants in 2014 was 38%, while the capacity factor of Angra 1 and 2 nuclear plants was 88% in the same year. Which means that, in Brazil, a nuclear plant generates more than twice as much energy than a wind plant with the same installed capacity. In addition, the energy generated by a nuclear plant rarely suffers unpredictable fluctuations, and thus have capacity to provide energy from the basis, which should be continuous, cheap and highly reliable.

4. Costs of SIN installations are remunerated through Time of Use of the Transmission System Pricing (TUST)

charged from basic network users.

Intermittent sources still pose other technical challenges for SIN operation once they may lead to increased variations in frequency during disturbances, thus exceeding safe limits. An adequacy of strategies and control practices adopted to operate the transmission system will be necessary. As presented, it is noted a new paradigm of SIN, which should have adjustments in operation and control models, as well as in the expansion planning process where the choice of technologies consider costs and risks of the future matrix composition together.

ENERGY DEMAND IN BRAZIL FOR THE NEXT YEARS Total energy consumption has decreased due to increased rates (ordinary, extraordinary readjustments and rate flags) and the weakening of the economy - industrial consumption reduced 4.8% in 2015 compared to 2014 [13]. These results led the Energy Research Company (EPE) to review its projections. Estimates for the next years were reduced, but even with the 1.8% reduction in total electricity consumption in 2015 [13], an average growth of 4.3% per year was estimated for the quadrennium 2016-2020 [14] .

EPE expects consumption more than triple reaching 197 MW on average in 2050 [15], which represents an average growth of 3.1% per year. This forecast is considered optimistic as it considers that the country will have an economic growth above the global projection, thus achieving an average GDP annual increase from 3.6 to 4% in 2013-2050. Such an estimate considers the development of energy efficiency programs, distributed renewable generation, demand and storage management. Thus, electricity supplied for consumers through the network must be reliable and cheap and may supply power whenever necessary - as in the case of low renewable generation, for example. Another factor to be considered is the increased electric and hybrid cars fleet, which should represent 60% of the national fleet estimated in 130 million vehicles by 2050. In addition, the public transport network of subway and urban trains also moved by electricity should be expanded

as well. To ensure electric vehicles represent a lower environmental impact than internal combustion vehicles, the power matrix must be clean and do not depend on fossil fuels. To favor the resumption of economic and industrial production growth in Brazil, the supply of reliable and cheap energy must be ensured. In 2013, 78% of the entire electricity generated in the world came from thermal sources [16], which have both characteristics. With current technologies and the operation model of the country’s power sector, it is still not possible to fully rely on renewable sources, which was demonstrated with the water crisis Brazil went through. A thermal basis generation could help to control the levels of hydraulic reservoirs keeping them always above the safety levels.5 Out of the thermal sources capable of operating in the basis, the only one capable of ensuring continuous energy supply without issuing GHG is the nuclear source.

5. This also favored the multiple uses of water - human consumption, power generation, sanitation, irrigation,

navigation, etc. - avoiding cuts in water supply for the population, as it happened in some cities of the State of São Paulo during the water crisis.

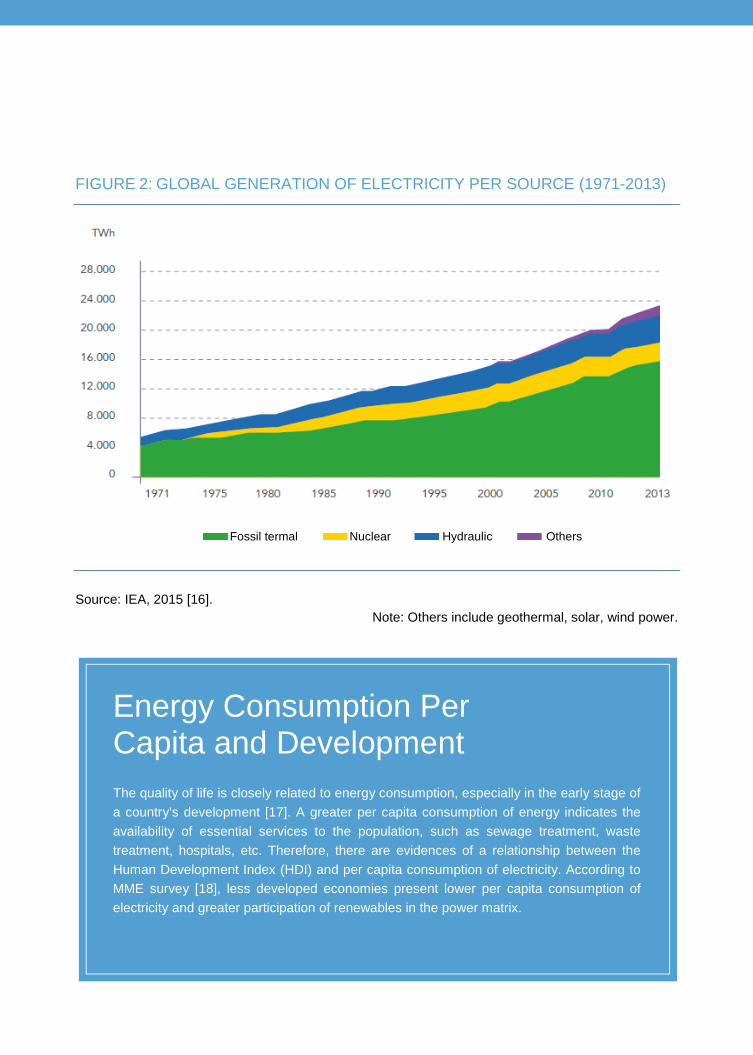

FIGURE 2: GLOBAL GENERATION OF ELECTRICITY PER SOURCE (1971-2013)

Source: IEA, 2015 [16].

Note: Others include geothermal, solar, wind power.

Energy Consumption Per Capita and Development The quality of life is closely related to energy consumption, especially in the early stage of a country’s development [17]. A greater per capita consumption of energy indicates the availability of essential services to the population, such as sewage treatment, waste treatment, hospitals, etc. Therefore, there are evidences of a relationship between the Human Development Index (HDI) and per capita consumption of electricity. According to MME survey [18], less developed economies present lower per capita consumption of electricity and greater participation of renewables in the power matrix.

Fossil termal Nuclear Hydraulic Others

In Brazil, social inequality is still strong. The Southeast region, for example, has a per capita consumption of energy two times higher than the Northeast region, meaning that the Northeast region has fewer access to basic services. Even in the Southeast, region with the highest consumption in the country, per capita consumption was 2,900 kWh in 2013 [19], still much below 4,000 Kwh per person per year considered as the division between developed countries and developing countries. Improvements in life expectation, education and income of the population can be made only with access to power. The availability of power is a pre-requisite for this improvement, not a consequence [17].

FIGURE 3: RELATION BETWEEN HDI AND PER CAPITA

CONSUMPTION OF ELECTRICITY (2004)

Source: InterAcademy Council, 2007 [20]

Hum

an D

evel

opm

ent I

ndex

(HD

I)

Argentina Poland

Brazil

México

China

India South Africa

Pakistan

Zambia

Republic of Niger

Australia

Japan; France; The Netherlands; Italy; United Kingdom; Germany; Israel; South Korea

Russian Federation; Saudi Arabia

Kuwait

EUA Canada Norway

Electricity consumption (kWh per person per year)

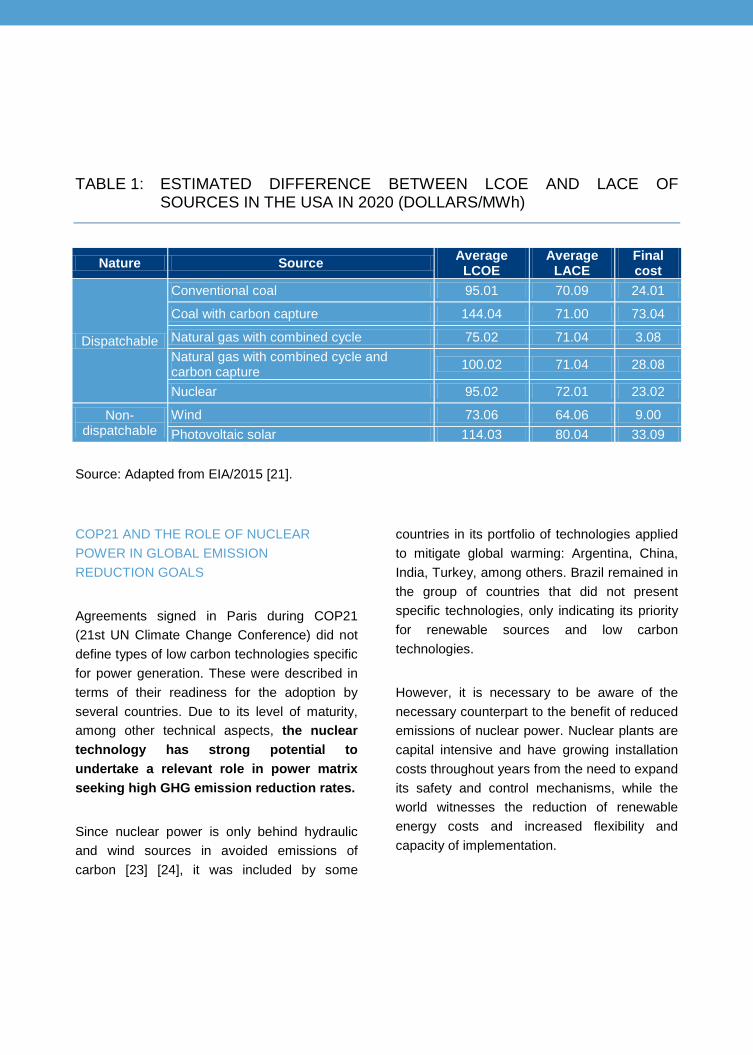

LEVELIZED COSTS OF ENERGY Projects of nuclear plants are characterized by the high volume of capital applied in the construction step offset by lower operation costs and a long period of useful life - approximately 60 years for the new models of reactors. Such an offset makes the nuclear technology have a levelized competitive cost when compared to other technologies for energy generation in the basis. The levelized cost of energy (LCOE) gives a value closer to the real cost per kWh of the plant construction and operation throughout its life cycle, thus representing the average revenue required, per unit of energy generated so that investments in construction, operation, maintenance and capital costs can be recovered. Specific circumstances of each country influence LCOE calculation, such as the access to fuels, availability of resources and market regulations. However, LCOE does not distinguish the nature of energy offer, that is, does not take into account if the technology can be implemented or not.6 The offer of a non-storable technology that depends on climatic factors does not have the same

value for the system of other that can be implemented at any time. Aiming to compare the costs of implementable and non-implementable technologies was prepared by EIA (US Energy Information Administration), the levelized avoided cost of energy (LACE), a measure of the cost to meet the load if the project assessed could not contribute with energy. That is, the lack of a source in question would result in increased costs when demanding the implementation of more expensive sources [11] [21] [22]. LCOE (cost) comparison with LACE (benefit) allows to check if project costs exceed or not its advantages. According to EIA estimates [21] for differente sources in the USA, nuclear power has an average cost of US$ 23.2 per MWh, below coal thermal , natural gas thermal with carbon capture and photovoltaic solar. This type of calculation should be adapted for Brazilian conditions, so that the bodies responsible for the power industry planning could have a broader vision on different sources, remembering that the main advantage of nuclear power is clean implementable generation, without competing with renewable sources.

6. A technology is implementable when it can be triggered when the system operator requires [58].

TABLE 1: ESTIMATED DIFFERENCE BETWEEN LCOE AND LACE OF

SOURCES IN THE USA IN 2020 (DOLLARS/MWh)

Nature Source Average LCOE

Average LACE

Final cost

Dispatchable

Conventional coal 95.01 70.09 24.01

Coal with carbon capture 144.04 71.00 73.04

Natural gas with combined cycle 75.02 71.04 3.08 Natural gas with combined cycle and carbon capture 100.02 71.04 28.08

Nuclear 95.02 72.01 23.02

Non-dispatchable

Wind 73.06 64.06 9.00 Photovoltaic solar 114.03 80.04 33.09

Source: Adapted from EIA/2015 [21]. COP21 AND THE ROLE OF NUCLEAR POWER IN GLOBAL EMISSION REDUCTION GOALS Agreements signed in Paris during COP21 (21st UN Climate Change Conference) did not define types of low carbon technologies specific for power generation. These were described in terms of their readiness for the adoption by several countries. Due to its level of maturity, among other technical aspects, the nuclear technology has strong potential to undertake a relevant role in power matrix seeking high GHG emission reduction rates. Since nuclear power is only behind hydraulic and wind sources in avoided emissions of carbon [23] [24], it was included by some

countries in its portfolio of technologies applied to mitigate global warming: Argentina, China, India, Turkey, among others. Brazil remained in the group of countries that did not present specific technologies, only indicating its priority for renewable sources and low carbon technologies. However, it is necessary to be aware of the necessary counterpart to the benefit of reduced emissions of nuclear power. Nuclear plants are capital intensive and have growing installation costs throughout years from the need to expand its safety and control mechanisms, while the world witnesses the reduction of renewable energy costs and increased flexibility and capacity of implementation.

Nuclear Technology The operation of a nuclear plant can be compared to the operation of a traditional thermal plant, where a heat source transforms water into steam, which makes a turbine couple to an electric generator rotate at a high pressure. The main difference between traditional and nuclear thermal plants is the heat source. In traditional plants, the heat comes from fuel burning - coal, natural gas, diesel oi, biomass, among others - while the heat of a nuclear plant is obtained through a fission reaction.7 Both processes produce waste that potentially cause an impact on the environment. In the case of traditional thermal plants, whose capture technologies have high cost, gases8 and particulate materials are emitted. On the

other hand, the by-product of fission reactions is a set of radioactive materials that can be reprocessed or stored for long periods until radioactivity decays.

7. Fission is the process in which the nucleus of fissile atoms is split (unstable atoms that break easily) after

being hit by neutrons at high speed. It releases large amounts of energy in the form of heat. 8. Thermal plants heat generation process is responsible for the release of gases as sulfur dioxide (SO2), carbon

monoxide (CO), carbon dioxide (CO2) and nitrogen oxides (NOx) into the atmosphere, thus contributing to global warming and acid rains.

Other Applications of Radioactive Materials Radioactive materials are not necessarily harmful for human beings. They fulfill a series of other functions in addition to power generation and can be used in medicine, agriculture and industry. Radioisotopes9 are used to sterilize equipment and as radioactive markers to detect pollutants dispersed into the environment. In medicine, several conditions are diagnosed and treated using radioactive materials. X-rays are an electromagnetic radiation form and, in other examinations, small dosages of radioisotopes are used in patients as contrasts to facilitate the identification of tumors. Radiotherapy, which is used to treat cancer, also uses radioactive isotopes. In agriculture, radioisotopes are used in pests control helping in the sterilization of insects, which is a technique being studied by Oswaldo Cruz Foundation (FIOCRUZ) and the Institute for Energy and Nuclear Research (IPEN) to be used in the control of the mosquito Aedes aegypti in Brazil. Radiation is also used in food preservation preventing the proliferation of fungi and microbes, without affecting the quality or leave residues.

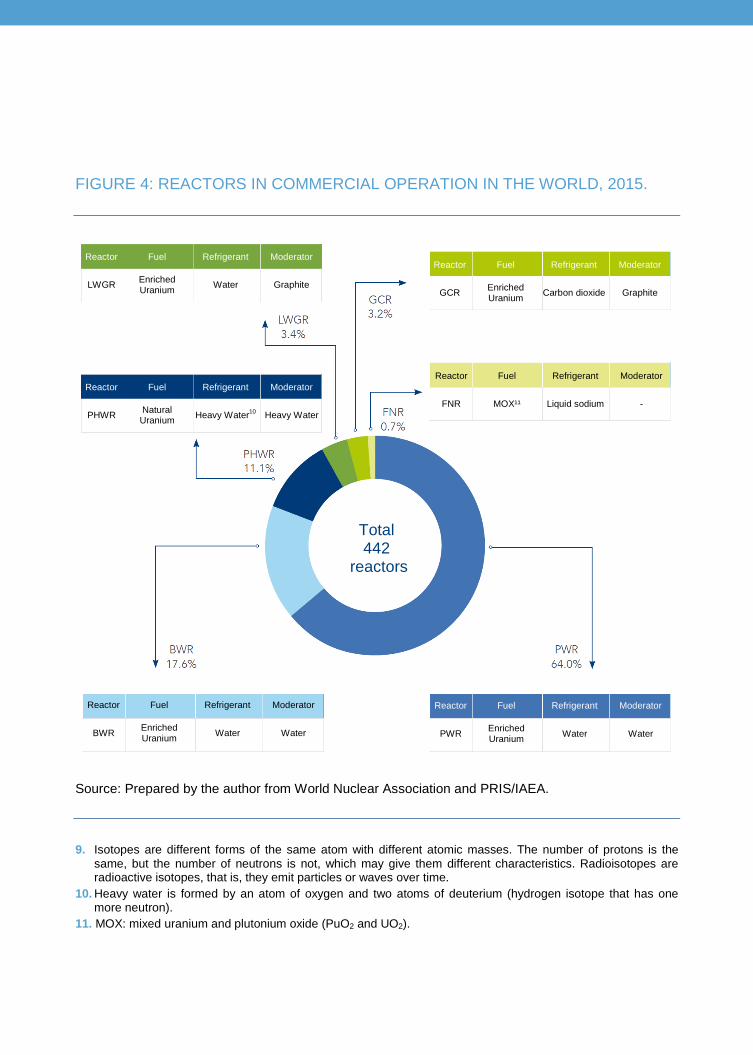

TECHNICAL ASPECTS There are several types of nuclear reactors, but the most common ones currently are the LWR (light water reactor) in which water is used as a heat transport fluid and moderator of fission reactions. Light water reactors represent over 80% of all reactors currently in operation. This category of reactors can be subdivided into BWR (boiling water reactor) and PWR (pressurized water reactor).

PWR is the most used in the world. It is used in Angra I and II, and Angra III plants, which is still being built. It is also used in ships and submarines powered by nuclear propulsion. Others models currently operated nowadays are: PHWR (pressurized heavy water reactor), LWGR (light water graphite-moderated reactor), GCR (gas-cooled reactor), and FNR (fast neutron reactor).

FIGURE 4: REACTORS IN COMMERCIAL OPERATION IN THE WORLD, 2015.

Source: Prepared by the author from World Nuclear Association and PRIS/IAEA. 9. Isotopes are different forms of the same atom with different atomic masses. The number of protons is the

same, but the number of neutrons is not, which may give them different characteristics. Radioisotopes are radioactive isotopes, that is, they emit particles or waves over time.

10. Heavy water is formed by an atom of oxygen and two atoms of deuterium (hydrogen isotope that has one more neutron).

11. MOX: mixed uranium and plutonium oxide (PuO2 and UO2).

Reactor Fuel Refrigerant Moderator

LWGR Enriched Uranium Water Graphite

Reactor Fuel Refrigerant Moderator

GCR Enriched Uranium Carbon dioxide Graphite

Reactor Fuel Refrigerant Moderator

PHWR Natural Uranium Heavy Water10 Heavy Water

Reactor Fuel Refrigerant Moderator

FNR MOX¹¹ Liquid sodium -

Reactor Fuel Refrigerant Moderator

BWR Enriched Uranium Water Water

Reactor Fuel Refrigerant Moderator

PWR Enriched Uranium Water Water

Total 442

reactors

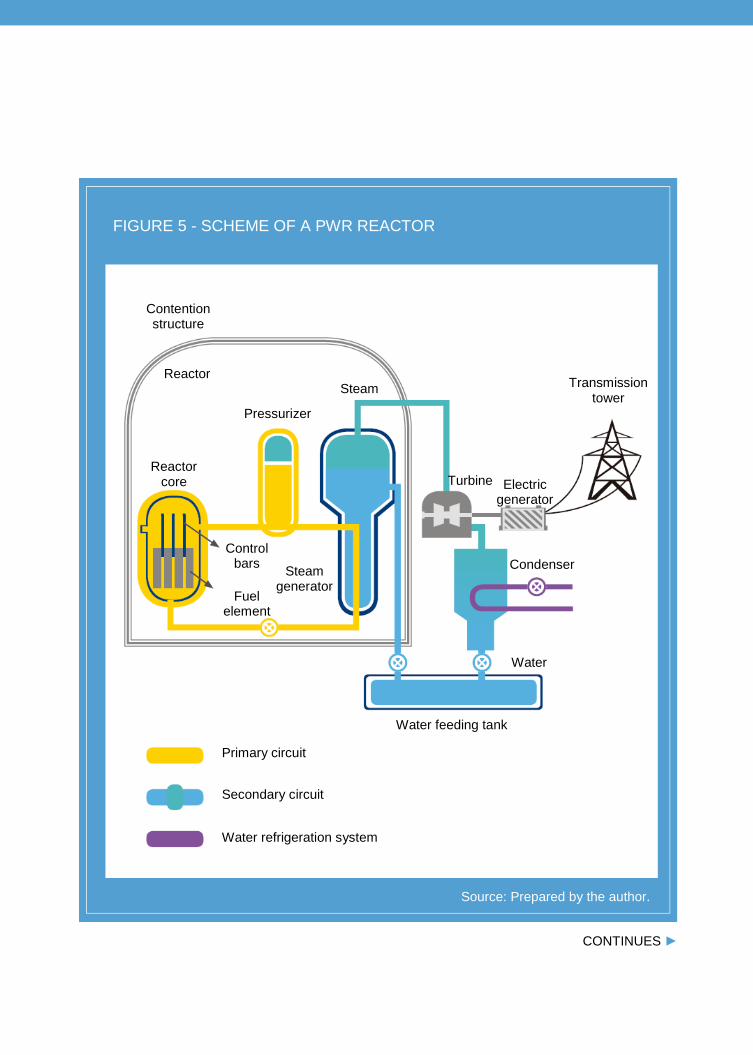

Operation of a Nuclear Reactor PWR (pressurized water reactor): Radioactive fuel is enriched uranium, which is inside the reactor core. It is hit by neutrons at high speed and its atoms undergo fission. A chain reaction12 is established when the fission rate remains constant, which occurs when neutrons speed is not very high. Therefore, a moderator element is used around the fuel for neutrons to lose kinetic energy before reaching the uranium. In PWR reactors, the water fulfills this role. Control bars are made of materials capable of absorbing neutrons and are inserted or removed from within the core in order to control the speed of reactions or interrupt them when necessary. The atomic nucleus division reaction emits heat that heats the water of the primary system, the one in direct contact with the reactor core. In steam generator, this hot water pressurized water exchanges heat (without mixing) with water from the secondary system, heating and transforming it into steam with lower pressure. The steam is responsible for moving the turbine-generator set, which generates electricity. I n PWR reactor, each water circulation system is independent, which increases the safety of the plant as a whole once the radioactive material only circulates in the primary system. Furthermore, there is a containment structure around the core usually made of concrete and steel that protects the reactor from external factors and avoids radiation leaks in case there is an internal failure. A pressurizer controls water pressure in the primary system, thus preventing water from vaporizing despite the very high temperature. The condenser in the secondary system cools the steam and puts it back into circulation.

CONTINUES ►

12. After being hit by neutrons, the uranium nucleus is divided into two or more nuclei. Other neutrons are

released in this process and they hit atoms close that also release other neutrons. This continuous reaction without the need to introduce new external neutrons is called chain reaction.

FIGURE 5 - SCHEME OF A PWR REACTOR

Source: Prepared by the author.

Contention structure

Reactor

Pressurizer

Steam

Reactor core

Control bars

Fuel element

Steam generator

Turbine Electric generator

Condenser

Water

Water feeding tank

Transmission tower

Primary circuit

Secondary circuit

Water refrigeration system

CONTINUES ►

CONTINUED ▼

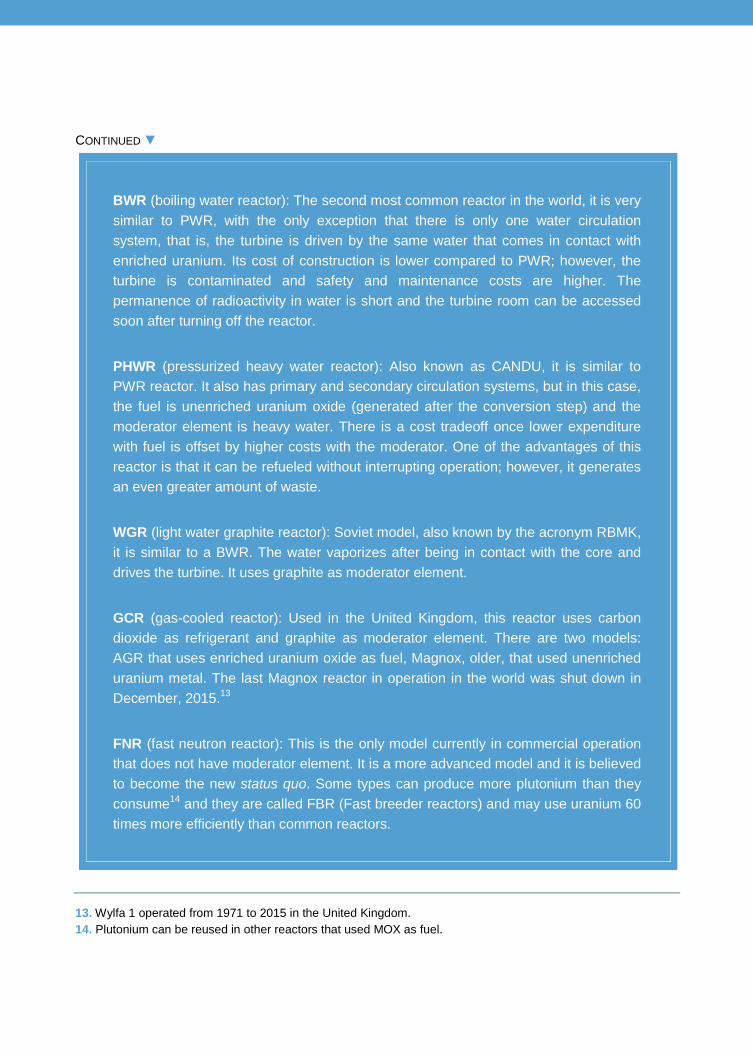

BWR (boiling water reactor): The second most common reactor in the world, it is very similar to PWR, with the only exception that there is only one water circulation system, that is, the turbine is driven by the same water that comes in contact with enriched uranium. Its cost of construction is lower compared to PWR; however, the turbine is contaminated and safety and maintenance costs are higher. The permanence of radioactivity in water is short and the turbine room can be accessed soon after turning off the reactor. PHWR (pressurized heavy water reactor): Also known as CANDU, it is similar to PWR reactor. It also has primary and secondary circulation systems, but in this case, the fuel is unenriched uranium oxide (generated after the conversion step) and the moderator element is heavy water. There is a cost tradeoff once lower expenditure with fuel is offset by higher costs with the moderator. One of the advantages of this reactor is that it can be refueled without interrupting operation; however, it generates an even greater amount of waste. WGR (light water graphite reactor): Soviet model, also known by the acronym RBMK, it is similar to a BWR. The water vaporizes after being in contact with the core and drives the turbine. It uses graphite as moderator element. GCR (gas-cooled reactor): Used in the United Kingdom, this reactor uses carbon dioxide as refrigerant and graphite as moderator element. There are two models: AGR that uses enriched uranium oxide as fuel, Magnox, older, that used unenriched uranium metal. The last Magnox reactor in operation in the world was shut down in December, 2015.13 FNR (fast neutron reactor): This is the only model currently in commercial operation that does not have moderator element. It is a more advanced model and it is believed to become the new status quo. Some types can produce more plutonium than they consume14 and they are called FBR (Fast breeder reactors) and may use uranium 60 times more efficiently than common reactors.

13. Wylfa 1 operated from 1971 to 2015 in the United Kingdom. 14. Plutonium can be reused in other reactors that used MOX as fuel.

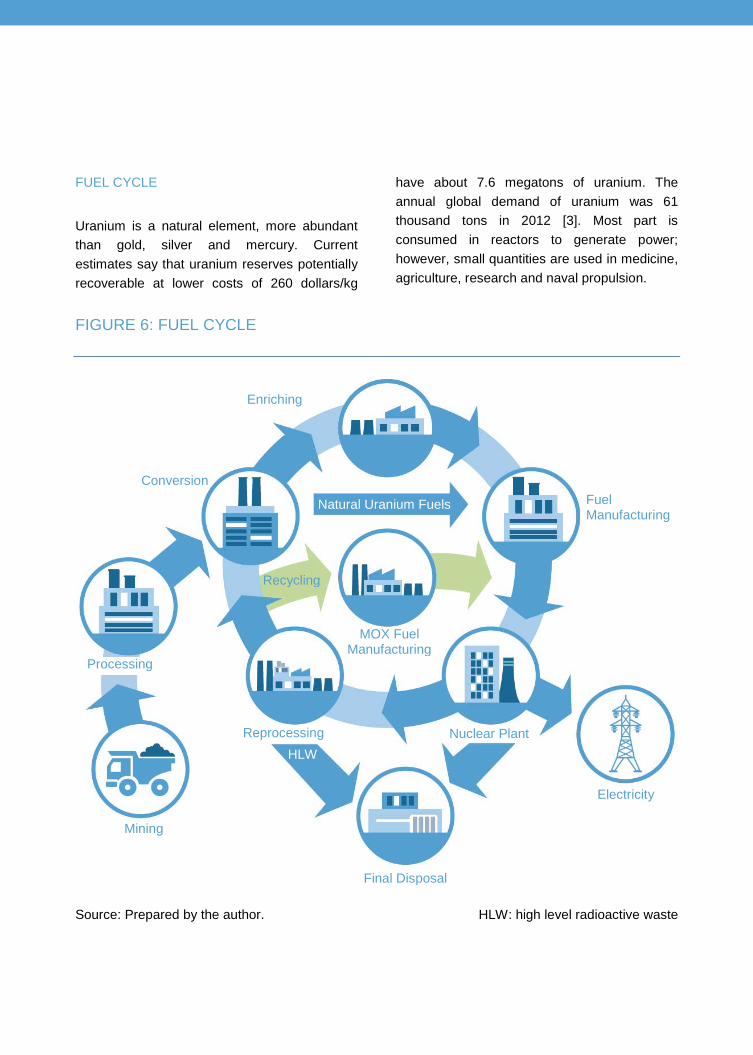

FUEL CYCLE Uranium is a natural element, more abundant than gold, silver and mercury. Current estimates say that uranium reserves potentially recoverable at lower costs of 260 dollars/kg

have about 7.6 megatons of uranium. The annual global demand of uranium was 61 thousand tons in 2012 [3]. Most part is consumed in reactors to generate power; however, small quantities are used in medicine, agriculture, research and naval propulsion.

FIGURE 6: FUEL CYCLE

Source: Prepared by the author. HLW: high level radioactive waste

Enriching

Conversion

Reprocessing

Mining

Processing

Recycling

HLW

Natural Uranium Fuels

MOX Fuel Manufacturing

Final Disposal

Fuel Manufacturing

Nuclear Plant

Electricity

Mining: In general, uranium mining is very similar to common mining. Uraninite, mainly comprised by uranium oxide, is usually found associated to other ores and radioactive uranium concentration is very low. The only mine being currently explored in Brazil is Caetité mine in the State of Bahia. Santa Quitéria mine (State of Ceará) is in the licensing phase. Processing: Uranium is removed from ore, purified and concentrated into a yellow cake (U3O8). This step, as well as mining, is also conducted by INB (Nuclear Industries of Brazil) in Caetité. Conversion: Uranium oxide (U3O8) is transformed into uranium dioxide (UO2), which can already be used in reactors that do not use enriched uranium. The remainder of the uranium dioxide is then converted into uranium hexafluoride gas (UF6) to be enriched. Only some countries15 operate plants in commercial scale to convert uranium. Currently, the uranium used in Angra I and II is converted in France; however, Brazil already masters the technology: there is a small conversion facility at pilot scale and USEXA (Uranium Hexafluoride Production Unit) is being implemented in the city of Iperó, State of São Paulo. Enriching: In nature, uranium fissionable isotope (235U) is found in a concentration of approximately 0.07% while the remainder is not fissionable (238U). Enriching is to increase the

radioactive isotope concentration for 3% to 5% so that it can be used in most reactors in the world. Most part of the uranium used in Brazil is enriched by the group URENCO16; however, FCN (Nuclear Fuel Factory) has plans to expand its enriching scale. Its unit in Resende, State of Rio de Janeiro, uses the ultracentrifugation technique, in which UF6 gas is added to a centrifuge that, by rotating, separates uranium hexafluoride molecules according to their mass difference. The final products of this step are enriched uranium and depleted uranium. Reconversion and manufacturing of fuel elements: Enriched UF6 gas is then reconverted into solid UO2, which is then sintered17 to form fuel pellets.18 These pellets usually have 1 cm in diameter and 1.5 cm high and are organized in rods to be used in the reactor. Use: To refuel Angra I, 10.5 million pellets are necessary. Part of the uranium is transformed into plutonium during nuclear fission, and part of it also undergoes fission and generates power. After 12-36 months, part of the fuel used should be replaced. It is temporarily stored in pools (once water isolates radiation and absorbs heat) until the material reaches levels sufficiently low of radiation, which usually lasts a few months. Then, the fuel may follow two paths: reprocessing or final disposal.

Reprocessing: Some countries have the fuel used reprocessed. Reprocessing allows to separate enriched uranium without fission and plutonium, which can be recycled and transformed into new fuel. This significantly reduces the amount of waste sent for final disposal and reduces the demand of mined uranium to the nature, but it can facilitate the manufacturing of atomic bombs. A few countries as China, France, India, Japan, Russia and United Kingdom reprocess fuel and adopt the so-called nuclear fuel “closed cycle”.

Final disposal: Countries as the United States, Brazil and many other that adopt the “open cycle” do not reprocess its atomic waste. There are no final disposal facilities for nuclear waste yet, which is not characterized as a problem. Most countries have not made a decision about their cycle and keeps waste in “temporary” storage facilities (designed to last dozens and even hundreds of years) in a form that can be reprocessed in the future and used in more modern reactors being developed.

15. As Canada, China, France, Russia, United Kingdom and USA. 16. This group operates enrichment plants in Germany, the Netherlands, USA and United Kingdom. 17. The sintering process involves heating the material to a temperature near its melting point so that particles are

united by fusing adjacent surfaces without changing its physical state. In the case of uranium, this temperature exceeds 1400 °C.

18. Each uranium pellet that has nearly 1 cm3 of volume produces the same quantity of energy that 800 kg of coal, 150 gallons of oil and 480m3 of natural gas [49].

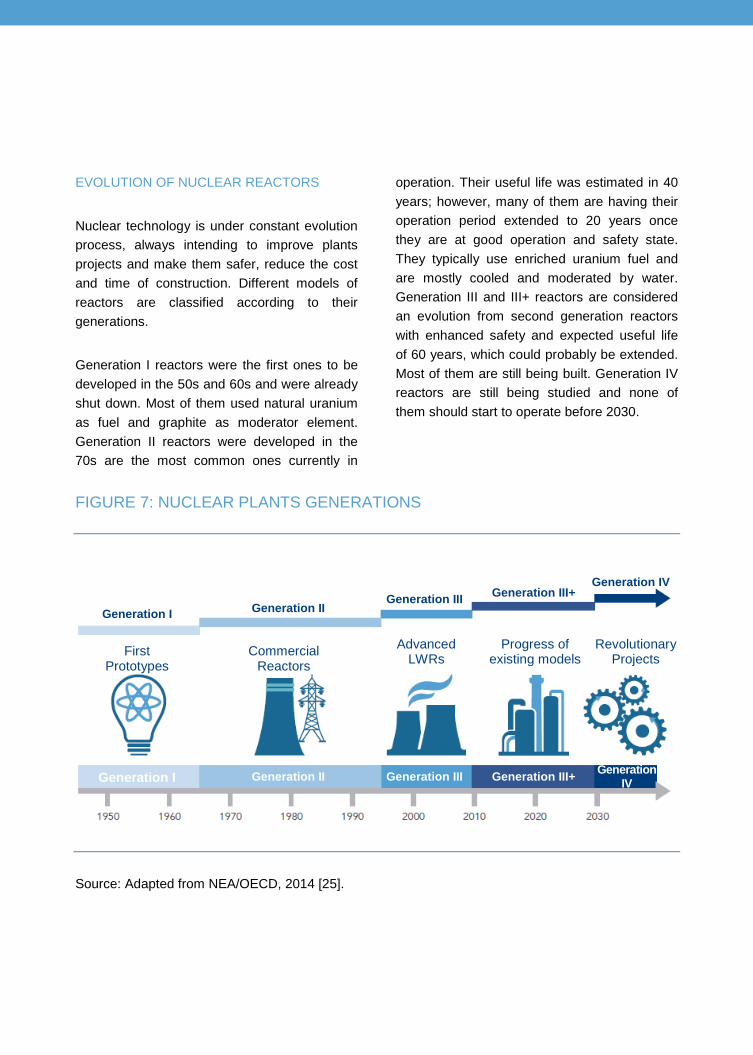

EVOLUTION OF NUCLEAR REACTORS Nuclear technology is under constant evolution process, always intending to improve plants projects and make them safer, reduce the cost and time of construction. Different models of reactors are classified according to their generations. Generation I reactors were the first ones to be developed in the 50s and 60s and were already shut down. Most of them used natural uranium as fuel and graphite as moderator element. Generation II reactors were developed in the 70s are the most common ones currently in

operation. Their useful life was estimated in 40 years; however, many of them are having their operation period extended to 20 years once they are at good operation and safety state. They typically use enriched uranium fuel and are mostly cooled and moderated by water. Generation III and III+ reactors are considered an evolution from second generation reactors with enhanced safety and expected useful life of 60 years, which could probably be extended. Most of them are still being built. Generation IV reactors are still being studied and none of them should start to operate before 2030.

FIGURE 7: NUCLEAR PLANTS GENERATIONS

Source: Adapted from NEA/OECD, 2014 [25].

Generation I Generation II Generation III Generation III+

Generation IV

First Prototypes

Commercial Reactors

Generation I Generation II Generation III Generation III+

Advanced LWRs

Progress of existing models

Generation IV

Revolutionary Projects

Generation III+ reactors, the most advanced one available in the market, incorporate “passive” safety systems, that is, in case of accidents or malfunction of the plant they are activated regardless of the human action or supply of electricity, unlike “active” mechanisms (as hydraulic pumps, fans and diesel generators) that usually need operators to work.

Passive safety systems only depend on natural physical phenomena as gravity, convection and materials strength to temperature variation, and are automatically activated whenever required. In addition, Generation III+ reactors have a modular construction structure that reduces cost and time of construction.

Some Generation III/III+ Models ABWR (advanced BWR) developed by GE-Hitachi. There are four operating units in Japan being reviewed after Fukushima, and others being built in Japan, and planned in the United Kingdom, Taiwan and Lithuania. The American Westinghouse’s AP1000 whose majority owner is currently Toshiba is based on the PWR model and have units being built in China and USA, and other are being planned in China and India. KEPCO’s APR1400, South Korean company, is also based on the PWR model. The first unit started to commercially operate in the country in January, 2016. Units are being built in the United Arab Emirates. EPR (European PWR) from Areva, whose largest shareholder is the French Government. Units are being built in China, Finland and France, and others are being planned in the United Kingdom and India. Rosatom’s VVER-1200, the Russian nuclear state company, based on the PWR model. Units are being built in Russia. ESBWR (simplified and economic BWR) from GE-Hitachi. Some units are under planning phase in the United States.

Some Generation IV models already had their prototypes tested, but substantial research and development efforts are still required.

GENERATION IV PERSPECTIVES The nuclear technology is in constant evolution and seeks to assimilate what has been learned from past experiences. New Generation IV reactors respond very well to criticisms made to the nuclear regarding the generation of waste, environmental impacts, proliferation of nuclear weapons and accident probability. Unlike Generation III/III+ that only carry improvements from traditional Generation II reactor models, Generation IV discontinues this type of technology with mechanisms entirely different from previous ones. Generation IV is being developed based on four goals [25]: • Sustainability: more efficient use of fuel and

reduced generation of nuclear waste. • Safety and reliability: reduction in accident

risks and greater efficiency. • Economic competitiveness: reduction in

construction and operation costs by simplifying models.

• Resistance to proliferation and physical

safety: reinforced physical protection against terrorist attacks and technology that does not allow the development of atomic weapons.

Generation IV reactors will operate at higher temperatures than the current ones, and heat can be reused (process known as cogeneration) for other purposes besides electricity generation, such as in industrial processes including steelmaking and petrochemical, and desalination of water. Some Generation IV models already had their prototypes tested. However, in order to become profitable substantial research and development efforts are still required. Generation IV reactors are expected to start operating at commercial scale as of 2030. Almost all Generation IV rectors being studied may operate with closed fuel cycle, that is, reuse reprocessed used fuel. They all use uranium in different compositions, and SCFR model also enables the use of plutonium generated by current light water reactors. In the case of VHTR and MSR models, there is the possibility to use thorium, a new promising fuel.

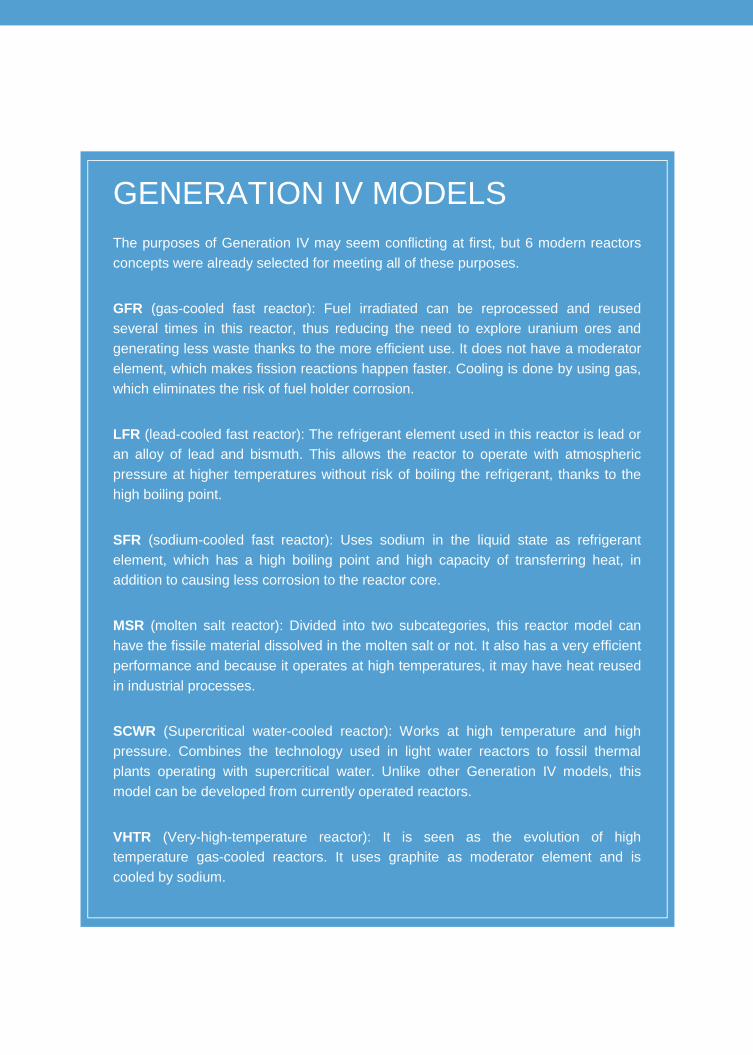

GENERATION IV MODELS The purposes of Generation IV may seem conflicting at first, but 6 modern reactors concepts were already selected for meeting all of these purposes. GFR (gas-cooled fast reactor): Fuel irradiated can be reprocessed and reused several times in this reactor, thus reducing the need to explore uranium ores and generating less waste thanks to the more efficient use. It does not have a moderator element, which makes fission reactions happen faster. Cooling is done by using gas, which eliminates the risk of fuel holder corrosion. LFR (lead-cooled fast reactor): The refrigerant element used in this reactor is lead or an alloy of lead and bismuth. This allows the reactor to operate with atmospheric pressure at higher temperatures without risk of boiling the refrigerant, thanks to the high boiling point. SFR (sodium-cooled fast reactor): Uses sodium in the liquid state as refrigerant element, which has a high boiling point and high capacity of transferring heat, in addition to causing less corrosion to the reactor core. MSR (molten salt reactor): Divided into two subcategories, this reactor model can have the fissile material dissolved in the molten salt or not. It also has a very efficient performance and because it operates at high temperatures, it may have heat reused in industrial processes. SCWR (Supercritical water-cooled reactor): Works at high temperature and high pressure. Combines the technology used in light water reactors to fossil thermal plants operating with supercritical water. Unlike other Generation IV models, this model can be developed from currently operated reactors. VHTR (Very-high-temperature reactor): It is seen as the evolution of high temperature gas-cooled reactors. It uses graphite as moderator element and is cooled by sodium.

Safety and Reliability The lack of information leads people to treat nuclear power with more apprehension than compared to other sources of energy. In fact there are risks related to nuclear power, as well as there are risks related to all types of energy generating sources. However, people feel that the nuclear risk is associated to nuclear explosions and thermal effects, which were not relevant in any nuclear accident, including Chernobyl and Fukushima [26]. In addition, the concentration of radioactive uranium (235U) does not exceed 5% in a plant, thus it cannot be compared to atomic bombs where this concentration does not reach 90%. Besides safety, other factors causing estrangement are the generation of waste and possible environmental impacts from nuclear generation. These risks are not as high as they are believed to be, especially if considering the most modern models of reactors.

Misinformation about these issues may eventually affect the Brazilian nuclear development, thus causing a series of economic and environmental harm to the country.

Transformation of Nuclear Weapons into Fuel There are concerns that power generation from nuclear sources encourages the use of uranium for military purposes. However, most part of the uranium used today in nuclear plants comes from the dismantling of nuclear weapons. Highly enriched uranium (concentration of up to 90% of radioactive uranium) can be mixed with natural uranium to produce lightly enriched uranium (concentration from 3% to 5% of radioactive uranium), which can be used in power generation reactors. This source has been annually replacing almost 8,850 tons of uranium oxide produced in mines and represented 13% to 19% of the global uranium needs for the generation of power in 2013. The program “Megatons to Megawatts”, for example, was signed by the USA and Russia in 1993. It lasted 20 years and led Russia to impoverish 500 tons of warheads and military arsenal and sell them so that the US would use in civil reactors [27].

SAFETY Accidents in nuclear plants are seen as the most serious than other types of accidents with similar levels of damages to the society and the environment [28]. In fact, accidents related with the operation of nuclear plants happened in the past, but the nuclear industry improves after each

occurrence by introducing new technologies to make plants safer. The first reactors in the USA and in other countries were built in remote areas and did not have containment structure around the reactor. The industry expansion made reactors to be installed closer to consumption centers, which led to a constant improvement process of the safety measures [26].

Nuclear Accidents and Technology Evolution Accidents occurred in nuclear plants operation encouraged companies from the sector to improve and enhance even more the safety levels of plants in operation and new plants projects. Nuclear accidents are rare and one accident gives rise to reduced probability of new future occurrences. 1979 - Three Mile Island (USA) Reactor 2 of this plant was partially meltdown due to failures in a valve of the cooling system and data interpretation mistakes that led operators to try and shut down the automatic safety systems. Radioactive gases were released to the outside, but at very low levels. Each person exposed received lower radiation than in a radiography [59]. Reactor 1 of this plant continues operating until nowadays. Such an accident made human errors to be considered in the assessment of risks and the following safety measures to be adopted [29]: • Control rooms project was improved and included ergonomic improvements and

presentation of ambiguous data for better interpretation of operators. • Periodic training of operators in real-size simulators. • Automatic safety systems cannot suffer interferences from operators during the first

phase of a potential accident. • Creation of INPO (Institute of Nuclear Reactors Operators) in the USA to promote

best practices.

CONTINUES ►

CONTINUED ▼

1986 - Chernobyl (URSS, current region of Ukraine) The four Chernobyl nuclear complex reactors were LWGR (RBMK in the Russian acronym), model only used in the Soviet Union. Safety mechanisms responsible for the reactor 4 automatic shutdown had been turned off to conduct a test. The system was unstable and explosions happened due to increased pressure inside the reactor. Such explosions destructed the reactor building - that did not follow the same safety measures already implemented globally - releasing large quantities of radioactive material to the outside. Thousands of people were evacuated from the surroundings and a 30 km-radius area was isolated.19 Other three reactors of this plant continued operating until 1991, 1996 and 2000. This accident was very specific of this family of reactors, but still taught a few lessons [29] [30] [31]: • The reactor containment is essential to limit the consequences of nuclear accidents;

therefore, it was necessary to protect it from elements that during the accident may hinder it (as hydrogen explosions, high temperatures, etc.);

• As low as the possibility of an accident is, creating prevention matters to reduce the

impact on the external environment in case of accident is necessary; • After the accident, URSS made changes to all RBMK reactors in operation, making

them more stable; • Measures adopted after such accident make a new occurrence as this one be

virtually impossible. Lessons from this accident led to improvements in Generation III/III+ reactors, such as passive safety systems.

19. Almost 2,800 km2. As comparison, Sobradinho UHE flooded area, the largest reservoir in Brazil, is 4,214 km2

and approximately 60 thousand people were displaced for the construction of this reservoir.

2011 - Fukushima Daiichi (Japan)

An earthquake measuring 9 on the Richter scale (the largest earthquake in the history of the country) [26] caused two tsunamis, one of them 15 m high. Only the earthquake and tsunami caused more than 19 thousand deaths. Eleven reactors were operating in the region and they were all turned off automatically and were not damaged. However, the tsunami damaged Fukushima Daiichi diesel generators, responsible for keeping the cooling system in operation. Four reactors of this plant had increased pressure because of the temperature, which caused the explosions.

Emissions from the nuclear accidents did not reach levels that may cause irreparable damage to the environment or human health (even for workers involved in emergency cases), according to a report of the World Health Organization (WHO) [32]. Still, the Fukushima accident hindered the public acceptance of nuclear power in several countries [28], but on the other hand brought great learnings to the nuclear industry [26] [33] [34] [35]:

• There were no records of natural phenomena in this magnitude in Japan and the plant was designed to withstand earthquakes and tsunamis of smaller scale. To avoid this type of occurrence, safety measures for accidents should be planned even though they seem unlikely.

• Improvement of buildings attached to plants the same way as the reactor building.

• Japan had three different agencies dedicated to the nuclear sector regulation, being one of them linked to the ministry responsible for promoting the nuclear power (METI). The lack of coordination among these agencies hindered the reaction to accident and this model was reviewed in 2012, thus leading to the creation of a single independent agency responsible for the regulation and control of the sector.

• Many countries revised their regulatory framework, in order to allow a faster reaction of plants operators and/or the Government in case of accidents.

The passive safety mechanisms of generation III/III+ were not operating in Fukushima reactors yet, which were launched in the 70s. Reactors currently being built will not go through a similar accident.

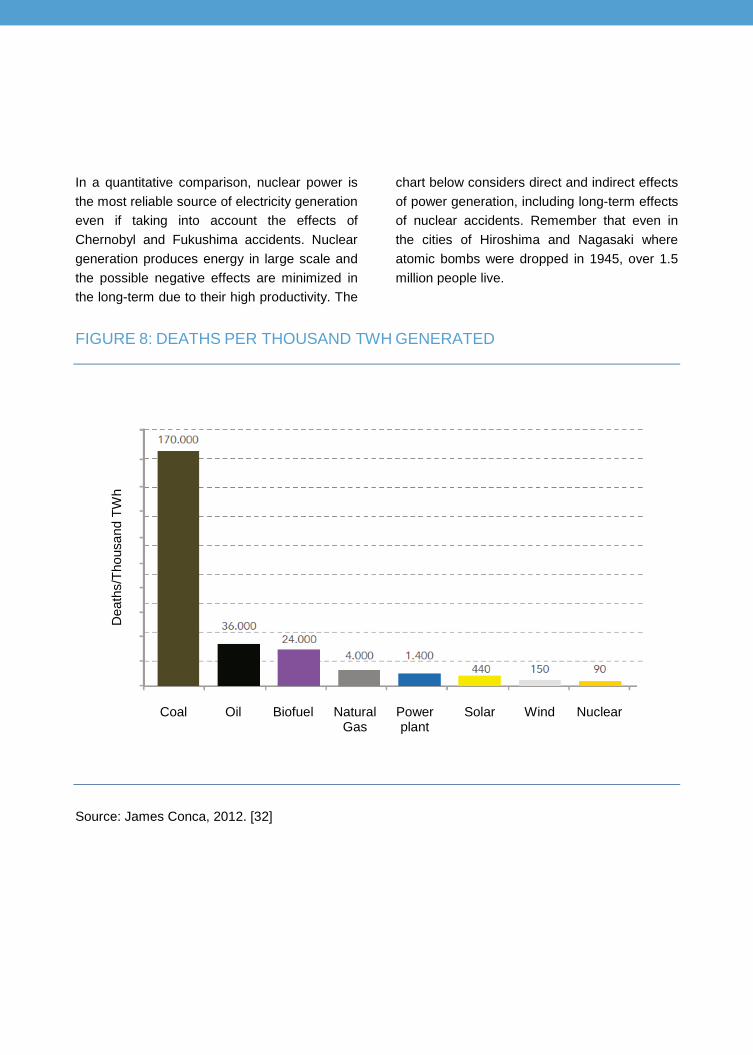

In a quantitative comparison, nuclear power is the most reliable source of electricity generation even if taking into account the effects of Chernobyl and Fukushima accidents. Nuclear generation produces energy in large scale and the possible negative effects are minimized in the long-term due to their high productivity. The

chart below considers direct and indirect effects of power generation, including long-term effects of nuclear accidents. Remember that even in the cities of Hiroshima and Nagasaki where atomic bombs were dropped in 1945, over 1.5 million people live.

FIGURE 8: DEATHS PER THOUSAND TWH GENERATED

Source: James Conca, 2012. [32]

Dea

ths/

Thou

sand

TW

h

Coal Oil Biofuel Natural Gas

Power plant

Solar Wind Nuclear

Air pollution is now the most serious environmental issue to be discussed.

ENVIRONMENTAL IMPACTS Air pollution is now the most serious environmental issue to be discussed. According to the World Health Organization, the inhalation of particulate matter causes 3.7 million premature deaths in the world annually [37]. Countries as India and China, which are growing at high rates and whose energy consumption has been increasing considerably, generate most of their electricity through fossil thermal plants. Local atmospheric pollution and GHG emission are making these countries look to change their power matrix, thus prioritizing clean sources, including nuclear. Recent studies of the Intergovernmental Panel on Climate Change (IPCC) and the International Energy Agency (IEA) have been setting nuclear as one of the key technologies to reduce GHG emissions [38]. In the case of fossil sources, GHG emissions come mainly from fuel burning. In nuclear generation, as well as in renewable generation, most part of emissions occur before operation, that is, during the installation and assembly phases. Nuclear plants require a high initial

investment to acquire components, systems and structures; however, when considering the entire lifecycle of these plants, emissions per MWh are comparable (and in some cases lower) to solar and wind sources [23]. If the electricity generated by clean sources as nuclear, hydroelectric and other renewable ones, was generated through a combination of coal, oil and natural gas20, 6 billion extra tons of GHG would have been issued only in 2011 [39]. In addition, nuclear plants occupy relatively small spaces and does not require deforestation and expropriation of areas, and do not significantly alter the environment in which they are installed. Itaipu power plant, for example, the biggest power plant in Brazil, has a 1,359 km2 reservoir of flooded area for an installed capacity of 14,000 MW. Angra 1 and 2 nuclear plants occupy an area of 3.5 km2 and have an installed capacity of 1,990 MW. Itaipu production index is 10.4 MW/km2 while Angra center’s is 570 MW/km2. This is one of the major advantages in nuclear power as it can be installed in small areas relatively close to consumption centers.

20. Proportional to the respective participations in the global power matrix.

By-products are generated in all steps of the uranium cycle classified as low, medium or high radioactivity.

One of the greatest environmental impacts caused by a nuclear plant is the release of heat21, which can be dissipated through steam towers (which may cause small heat islands around the plant) or exchanges of heat with colder water of a body of water nearby, as is the case of the Angra complex plants. WASTE Another factor related to the operation of nuclear plants is the generation of radioactive waste. By-products are generated in all steps of the uranium cycle classified as low, medium or high radioactivity. Processing and storage in special barrels at the own nuclear center is recommended for the first two, mainly formed by clothes, rags used to clean the plant, water

and tools. Fifty years ago, when radioactive material began to be handled, experiences with this type of residue were successful. High radioactivity waste contained in used fuel was temporarily stored in borate22 water pools, which inhibit the chain reaction and absorb the heat released. Unlike waste generated in other human activities (as the industrial production, urban exhaustion or the generation of power by fossil sources) which are often released in waters or the atmosphere without supervision, the nuclear waste is constantly monitored. After proper decay of the nuclear fuel used, it can be sent for final disposal or reprocessing.

21. Approximately 35% of the heat released by the fission is converted to electricity, while the equivalent to 65%

of the heat should be dissipated. Gas engines, for example, release almost 80% of the heat generated by combustion in the environment.

22. Mixed with Boron.

Countries that adopt the nuclear fuel open cycle reduce the volume of waste after the decay time they are kept in pools, which are solidified along with other materials resulting in glass bars. Vitrification facilitates transport and storage, thus reducing possible impacts on the environment. Currently, one of the alternatives most considered for the final disposal of high radioactivity waste after vitrification is storage in geological stable structures with more than 500 m deep. Comparing a coal generation plant to a nuclear plant we are able to have a new perspective of the losses associated with the nuclear waste. Considering facilities with 1,300 MW of installed

capacity (Angra 3 size), the annual average of fuel consumption in a coal plant is 3.3 million tons, while a nuclear plant consumes only 32 tons of enriched uranium [40]. In the USA, for example, 2,200 tons of nuclear waste are estimated to be generated annually, small compared to the 115 million annual tons of waste generated in factories and coal generators in the country [41]. It turns out that the waste from a coal plant are released in the air and technologies of capture are still expensive and not widely used. On the other hand, all nuclear waste is stored in controlled conditions and once it still a great potential for power generation, it could be recycled and used for Generation IV reactors in the future.

Nuclear Power in the World In 2010, the nuclear industry was living the so-called “nuclear renaissance” with a growing number of reactors in construction. Interest in the technology has increased due to the need to meet the growing energy consumption globally, with a power basis while it would obey the new environmental standards for GHG emissions and had stable costs23 [42]. Facility to install a nuclear plant close to consumption centers and its high efficiency, mainly regarding the small area occupied, make it a good alternative for developing countries as it is capable of producing power in large scale for large urban centers. However, the Fukushima nuclear accident, in March, 2011, interrupted this global nuclear expansion trend once it had a strong impact in the public acceptance of this source [28], and thus some countries changed their nuclear programs and regulatory policies. Another factor that slowed nuclear expansion was the

2008/2009 economic crises that not only reduced energy consumption in affected countries, but also made the financing capacity of credit institutions to decrease [42]. However, five years after Fukushima, the nuclear industry is

23. In traditional thermal plants, fuel is the main component in generation cost. In nuclear plants, fuel price

represents a small part of the energy final cost and most part of costs is fixed [57]. Thus, the final price of MWh is kept relatively stable throughout the plant operation.

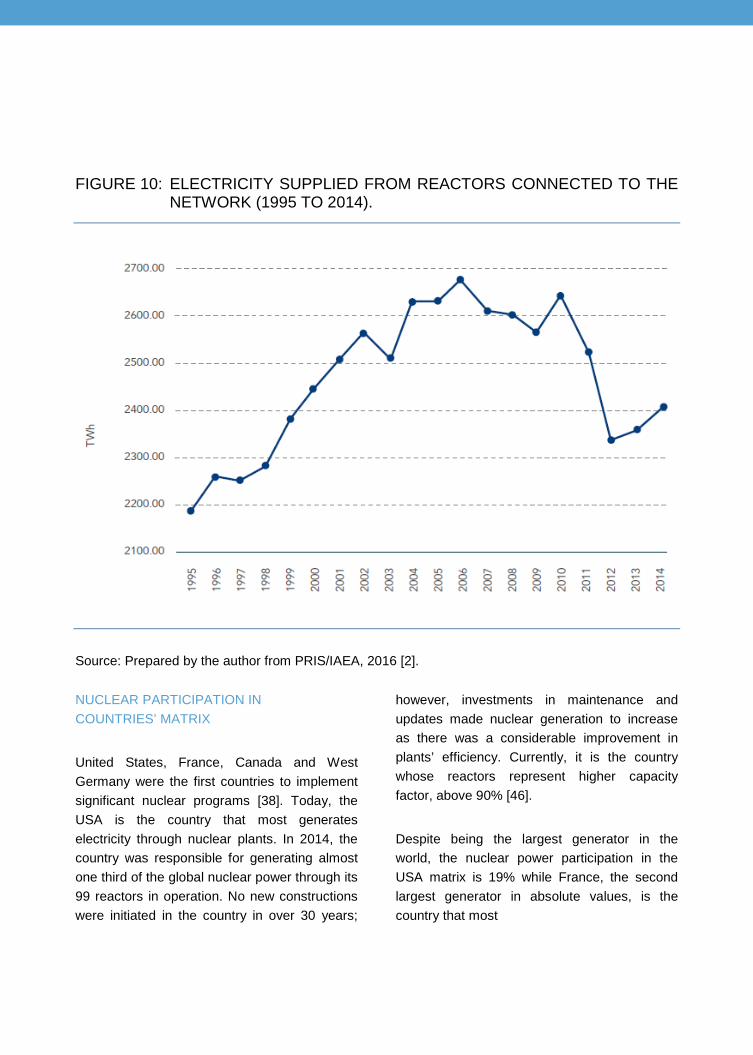

resuming its growth with new plants in different phases of planning and construction. In March, 2016, 66 new reactors are being built in Europe, Asia and the Americas [2]. Currently, 442 nuclear reactors are in commercial operation in 30 countries24 in five continents with a total installed capacity of 384 GW and average capacity factor of 76% [2]. Taking into account the regional power grids and power export, even more countries use nuclear power in their matrices. Italy and Denmark, for example, despite not having reactors operating in their territories obtain almost 10% of their electricity from nuclear sources [43]. Global generation by nuclear sources had a reduction of 10.8% from 2010 to 2012, mainly due to the temporary shut down for tests of all Japanese reactors, which sum over 40 and the anticipated decommissioning of the 8 oldest German reactors in 2011. However, power generation resumed growth as of 2012, albeit

moderately. In 2013, nuclear generation represented almost 11% of the entire power matrix in the world being the 4th source to generate more electricity, after coal, gas thermal and power plants. Japan reconnected two of its nuclear reactors in 201525 and Government projections estimate that 20 to 22% of the electricity generated in the country will be obtained through nuclear source in 2030, a level similar to those obtained before the accident [44]. Besides the reactors in commercial operation, over 240 research reactors are operating in 56 countries and others are being built. They are generally used to produce radioisotopes for medicine and industry26 [45]. In Brazil, we have 4 research reactors in operation located in the States of Rio de Janeiro (IEN - Nuclear Engineering Institute), São Paulo (IPEN - Nuclear and Energy Research Institute), and Minas Gerais (CDTN - Nuclear Technology Development Center).

24. Countries that currently have nuclear plants in commercial operation are: South Africa, Germany, Argentina,

Armenia, Belgium, Brazil, Bulgaria, Canada, China, South Korea, Slovakia, Slovenia, Spain, United States, Finland, France, The Netherlands, Hungary, India, Iran, Japan, Mexico, Pakistan, United Kingdom, Romania, Russia, Czech Republic, Sweden, Switzerland and Ukraine.

25. Sendai 1 and 2. 26. See box “OTHER APPLICATIONS OF RADIOACTIVE MATERIALS” on page 24

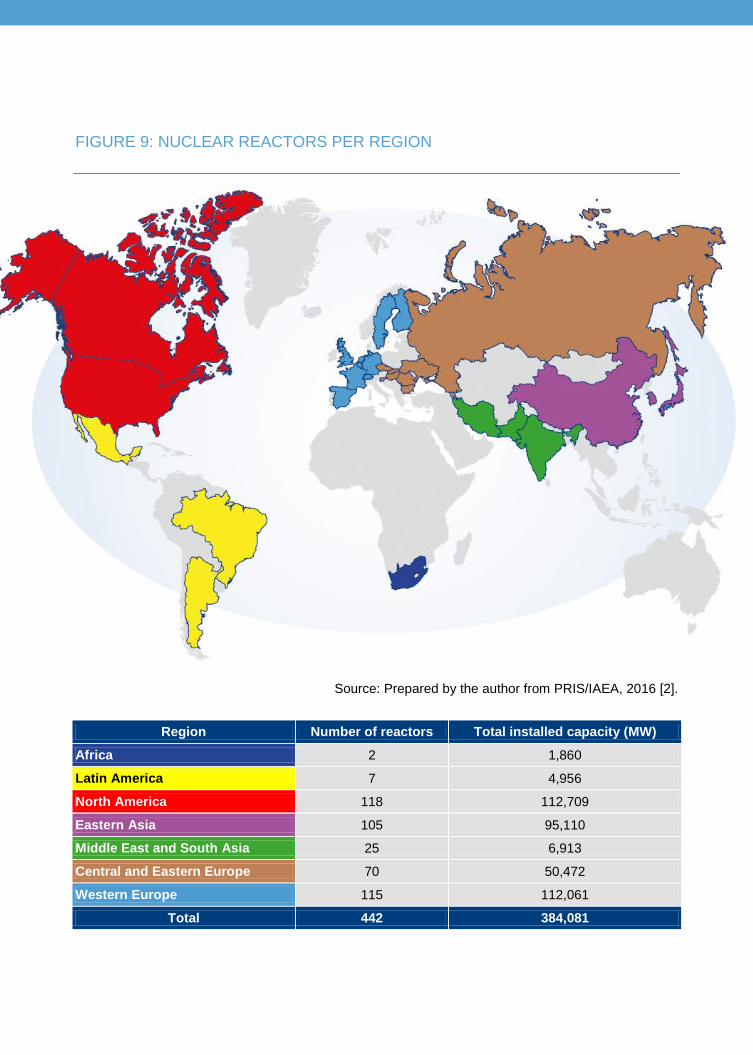

FIGURE 9: NUCLEAR REACTORS PER REGION

Source: Prepared by the author from PRIS/IAEA, 2016 [2].

Region Number of reactors Total installed capacity (MW)

Africa 2 1,860

Latin America 7 4,956

North America 118 112,709

Eastern Asia 105 95,110

Middle East and South Asia 25 6,913

Central and Eastern Europe 70 50,472

Western Europe 115 112,061

Total 442 384,081

FIGURE 10: ELECTRICITY SUPPLIED FROM REACTORS CONNECTED TO THE

NETWORK (1995 TO 2014).

Source: Prepared by the author from PRIS/IAEA, 2016 [2]. NUCLEAR PARTICIPATION IN COUNTRIES’ MATRIX United States, France, Canada and West Germany were the first countries to implement significant nuclear programs [38]. Today, the USA is the country that most generates electricity through nuclear plants. In 2014, the country was responsible for generating almost one third of the global nuclear power through its 99 reactors in operation. No new constructions were initiated in the country in over 30 years;

however, investments in maintenance and updates made nuclear generation to increase as there was a considerable improvement in plants’ efficiency. Currently, it is the country whose reactors represent higher capacity factor, above 90% [46]. Despite being the largest generator in the world, the nuclear power participation in the USA matrix is 19% while France, the second largest generator in absolute values, is the country that most

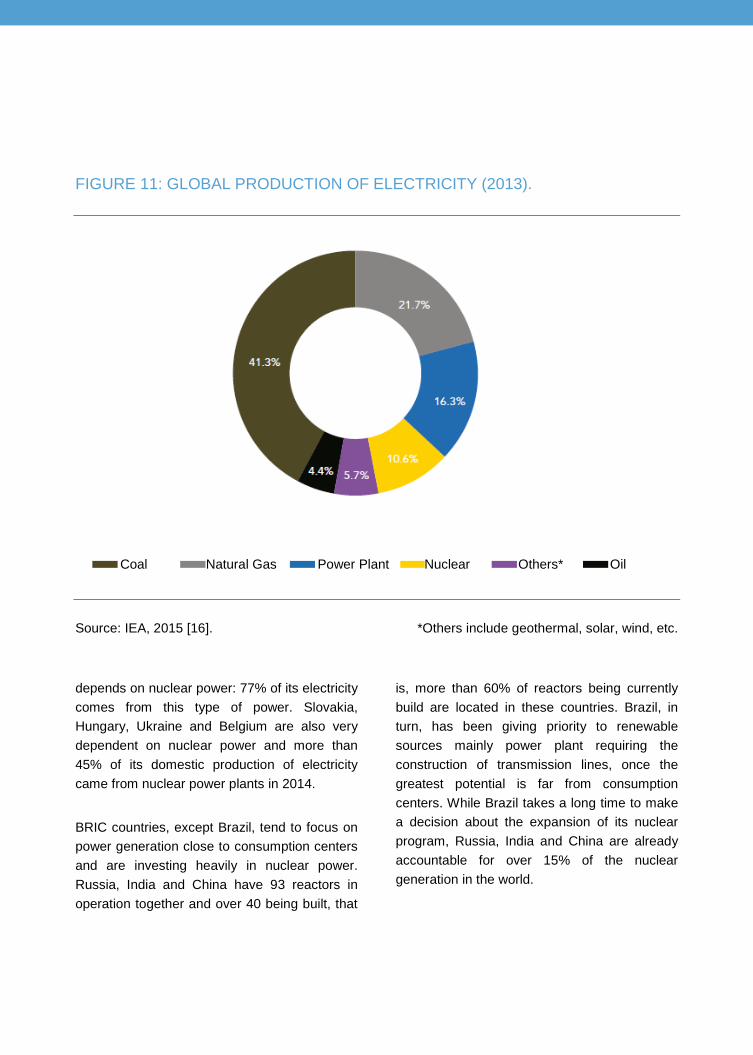

FIGURE 11: GLOBAL PRODUCTION OF ELECTRICITY (2013).

Source: IEA, 2015 [16]. *Others include geothermal, solar, wind, etc. depends on nuclear power: 77% of its electricity comes from this type of power. Slovakia, Hungary, Ukraine and Belgium are also very dependent on nuclear power and more than 45% of its domestic production of electricity came from nuclear power plants in 2014. BRIC countries, except Brazil, tend to focus on power generation close to consumption centers and are investing heavily in nuclear power. Russia, India and China have 93 reactors in operation together and over 40 being built, that

is, more than 60% of reactors being currently build are located in these countries. Brazil, in turn, has been giving priority to renewable sources mainly power plant requiring the construction of transmission lines, once the greatest potential is far from consumption centers. While Brazil takes a long time to make a decision about the expansion of its nuclear program, Russia, India and China are already accountable for over 15% of the nuclear generation in the world.

Coal Natural Gas Power Plant Nuclear Others* Oil

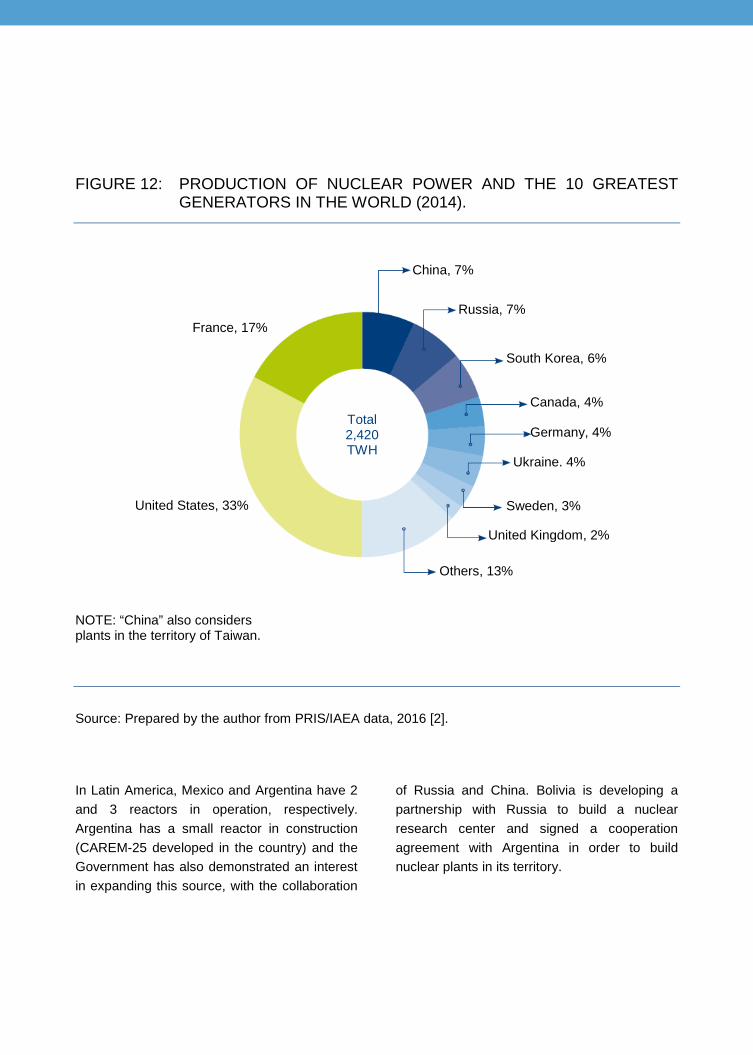

FIGURE 12: PRODUCTION OF NUCLEAR POWER AND THE 10 GREATEST

GENERATORS IN THE WORLD (2014).

NOTE: “China” also considers plants in the territory of Taiwan. Source: Prepared by the author from PRIS/IAEA data, 2016 [2]. In Latin America, Mexico and Argentina have 2 and 3 reactors in operation, respectively. Argentina has a small reactor in construction (CAREM-25 developed in the country) and the Government has also demonstrated an interest in expanding this source, with the collaboration

of Russia and China. Bolivia is developing a partnership with Russia to build a nuclear research center and signed a cooperation agreement with Argentina in order to build nuclear plants in its territory.

France, 17%

United States, 33%

China, 7%

Russia, 7%

South Korea, 6%

Canada, 4%

Germany, 4%

Ukraine. 4%

Sweden, 3%

United Kingdom, 2%

Others, 13%

Total 2,420 TWH

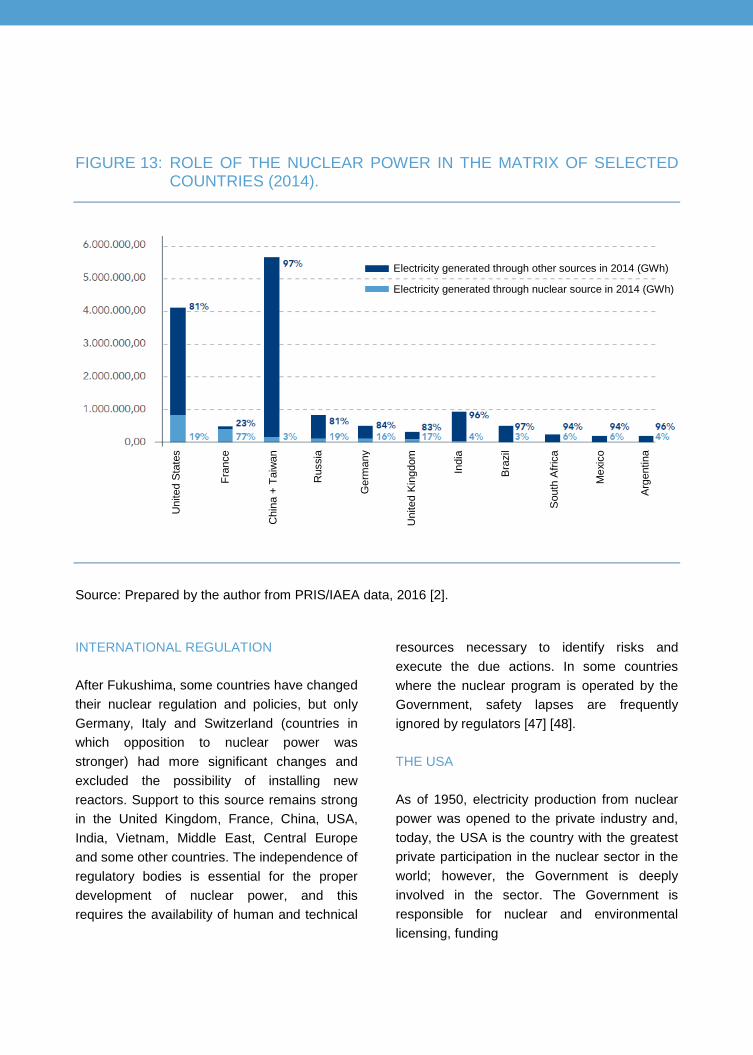

FIGURE 13: ROLE OF THE NUCLEAR POWER IN THE MATRIX OF SELECTED

COUNTRIES (2014).

Source: Prepared by the author from PRIS/IAEA data, 2016 [2].

INTERNATIONAL REGULATION

After Fukushima, some countries have changed their nuclear regulation and policies, but only Germany, Italy and Switzerland (countries in which opposition to nuclear power was stronger) had more significant changes and excluded the possibility of installing new reactors. Support to this source remains strong in the United Kingdom, France, China, USA, India, Vietnam, Middle East, Central Europe and some other countries. The independence of regulatory bodies is essential for the proper development of nuclear power, and this requires the availability of human and technical

resources necessary to identify risks and execute the due actions. In some countries where the nuclear program is operated by the Government, safety lapses are frequently ignored by regulators [47] [48].

THE USA

As of 1950, electricity production from nuclear power was opened to the private industry and, today, the USA is the country with the greatest private participation in the nuclear sector in the world; however, the Government is deeply involved in the sector. The Government is responsible for nuclear and environmental licensing, funding

Electricity generated through other sources in 2014 (GWh)

Electricity generated through nuclear source in 2014 (GWh)

Uni

ted

Stat

es

Fran

ce

Chi

na +

Tai

wan

Rus

sia

Ger

man

y

Uni

ted

Kin

gdom

Indi

a

Bra

zil

Sou

th A

frica

Mex

ico

Arg

entin

a

R&D, energy planning and, since 1982, assumed the responsibility for waste generated in the country’s nuclear plants. The private sector is generally responsible for building and operating plants. Almost all reactors in operation in the country belong to private owners. Nuclear power regulation in the USA is prepared by NRC (Nuclear Regulatory Commission), an independent Government agency (belonging to the Government, but that has autonomy). It is directed by 5 Commissioners with terms of five years, chosen

by the President of the Republic and approved by the Senate. It was established in 1974 and is responsible for the regulation and licensing of the entire nuclear activity in the country. Aiming at accelerating the new plants installation process, NCR created a technology certificate in 2003 meaning that the reactor model approved after an extensive analysis can be built anywhere in the USA (after specific assessment of the place), thus requiring only a Combined Construction and Operating License.27

27. Combined Construction and Operating License (COL)