Embed Size (px)

Citation preview

1/37 International Capital Markets Day - Grupa LOTOS S.A. - Gdańsk November 27th 2013 1/40

INTERNATIONAL CAPITAL MARKETS DAY

GRUPA LOTOS S.A.

GDAŃSK

NOVEMBER 27TH 2013

2/37 International Capital Markets Day - Grupa LOTOS S.A. - Gdańsk November 27th 2013 2/40

STRATEGIC OVERVIEW

PAWEŁ OLECHNOWICZ

CHIEF EXECUTIVE OFFICER, GRUPA LOTOS S.A.

PRESIDENT OF THE MANAGEMENT BOARD OF GRUPA LOTOS S.A.

3/37

YME exit route : settlement with SBM

Heimdal package acquisition

expanded upstream portfolio (14 licenses)

crude oil production doubled (~10 000 bbl/d)

2/3 of deferred tax asset unlocked by 2016

Milestone for B8 Project development (financing)

EXECUTIVE SUMMARY

UP

ST

RE

AM

D

OW

NS

TR

EA

M

FIN

AN

CIA

LS

Outperforming in challenging macro environment

Operational excellence confirmed by Solomon Associates Study

Coker unit (DCU) project

Pre-feasibility study of the petrochemical project with Grupa Azoty

Steadily decreasing level of indebtedness

net debt down to 5.5 bn PLN

61% gearing ratio (net debt / equity)

New CAPEX solely focused on the core business areas

4/37

GLOBAL PRODUCT DEMAND – OUTLOOK UNTIL 2015

(’000 boe/d)

Source: JBC

5/37

= B8

THE AGREEMENT OF PIR AND LOTOS PETROBALTIC FOR B8 PROJECT

6/37

Significant improvement of EBIT margin : LPG and naphtha

Cost synergies : e.g. energy cost savings

PETROCHEMICAL COMPLEX IN GDAŃSK

STRATEGIC DETERMINANTS OF THE PROJECT

Deficit of raw materials for the production of petrochemicals

Opportunities of enlarging products portfolio

A significant deficit in international trade in chemicals

Demand for highly processed products and innovative installations

Labor market : new jobs

Cooperation with PIR

Grupa LOTOS S.A.

Grupa Azoty S.A.

The Polish economy

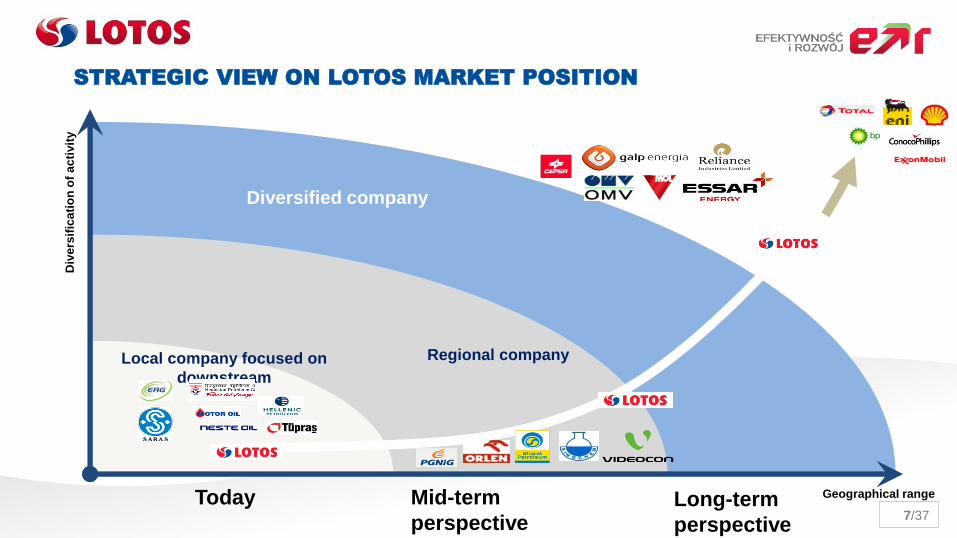

7/37

STRATEGIC VIEW ON LOTOS MARKET POSITION D

ive

rsif

ica

tio

n o

f a

cti

vit

y

Geographical range

Local company focused on

downstream

Regional company

Diversified company

Today Mid-term

perspective Long-term

perspective

8/37

Value creation : over PLN 1bn worth of brand

Downstream : LOTOS refinery’s capacity extension by 75% (up to 10.5m tpa)

Wholesale : 34% domestic fuel market share (trading in 62 countries)

Retail : over 400 service stations in Poland (8.4% market share)

Exploration and production : international upstream operations

Key strategic focus : value-creation in well balanced E&P portfolio of assets

STRONG MANAGEMENT TEAM

Stable and experienced Management Board

9/37 International Capital Markets Day - Grupa LOTOS S.A. - Gdańsk November 27th 2013 9/40

FINANCIAL SEGMENT

MARIUSZ MACHAJEWSKI

CHIEF FINANCIAL OFFICER, GRUPA LOTOS S.A.

VICE PRESIDENT OF THE MANAGEMENT BOARD OF GRUPA LOTOS S.A.

10/37

Strategic goal for 2015

Wholesale market share (eop) Retail market share (eop)

10% 30%

Gearing ratio (net debt / equity)

40%

Key comments

Wholesale : exceeding the target

Retail : systematic growth

Gearing ratio : steadily improving

STRATEGIC UPDATE : DOWNSTREAM AND FINANCIALS

11/37

BITUMENS

New model

margin

New product yield(1)

less Ural price

Cost of gas from the natural gas grid

c. 3 USD/bbl

HSFO

Notes:

(1) Assuming 95% utilization rate.

All prices based on Thomson Reuters data source

(2) LPG price benchmarked to 50/50 mix of propane/butane prices

LESS

50% butane (2)

50% propane (2)

Yield structure in the old and new model

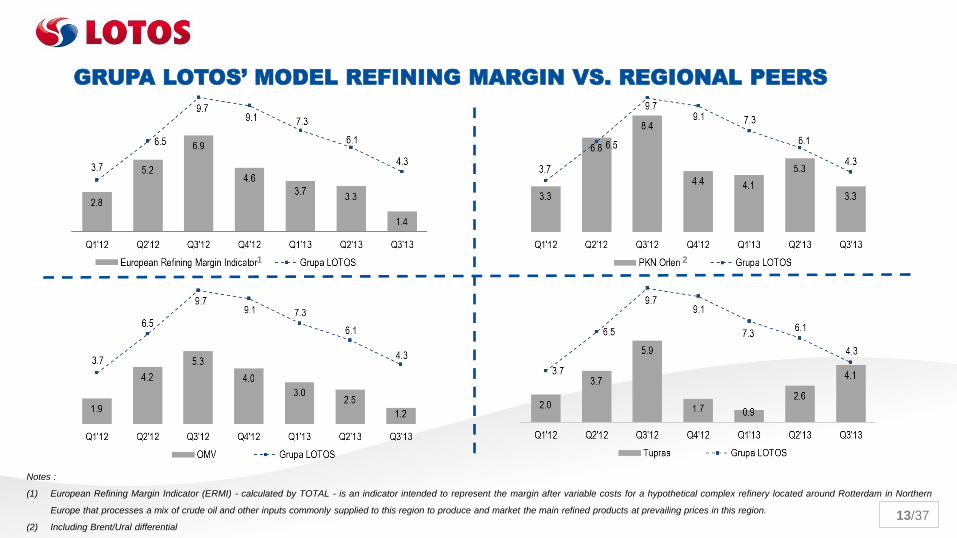

ADJUSTED MODEL REFINING MARGIN

12/37

Average quarterly model refining margin (USD/bbl)

(1)

Notes :

(1) New model refining margin beginning with the 3Q of 2012

New model refining margin assuming current product slate, influenced by the switch to the natural

gas grid and maintenance shutdown triggering energetic improvement

GRUPA LOTOS’ MODEL REFINING MARGIN

1

13/37

Notes :

(1) European Refining Margin Indicator (ERMI) - calculated by TOTAL - is an indicator intended to represent the margin after variable costs for a hypothetical complex refinery located around Rotterdam in Northern

Europe that processes a mix of crude oil and other inputs commonly supplied to this region to produce and market the main refined products at prevailing prices in this region.

(2) Including Brent/Ural differential

1

GRUPA LOTOS’ MODEL REFINING MARGIN VS. REGIONAL PEERS

2

14/37 International Capital Markets Day - Grupa LOTOS S.A. - Gdańsk November 27th 2013 14/40

UPSTREAM SEGMENT

ZBIGNIEW PASZKOWICZ

EXPLORATION AND PRODUCTION OFFICER, GRUPA LOTOS S.A.

VICE PRESIDENT OF THE MANAGEMENT BOARD OF GRUPA LOTOS S.A.

15/37

Poland

Lithuania

Norway

Poland:

– offshore: development of existing

fields and full exploration of the

Baltic Sea

– onshore: cooperation with PGNIG

Norway:

– offshore: exploration, development

and production activities

Lithuania:

– onshore: full development of the

licenses held

2015 – production potential 24 kboe/d

LOTOS E&P STRATEGY

16/37

2013

B3 field: PG-1 unmanned rig revamped, back

in production in October 2013

continued production from B3 field until 2026

the first seismic campaign since 2009 - 2D

and 3D seismic 1200 km²

2 new licenses

2015-2014

B8 field development, first oil in 4Q 2015,

production potential: 3.5 million t, cooperation

with PIR

B4/B6 gas fields – preparation and launching

the development together with CalEnergy,

production potential: 4 billion m3 gas

drilling exploration campaign

seismic to be realised in 2013

POLAND: THE INTENSIFICATION OF WORKS IN THE BALTIC SEA

17/37

drilling rig purchase – plan 2014

operation to a water depth of >120 m

implementation of horizontal wells

to be used for exploration and production

activities

exploration target: prospective resources of 30 million toe

POLAND: FULL EXPLORATION OF THE BALTIC SEA

18/37

3 producing, 3 development fields, 1 HUB

5.000+ boe/d production net

14 licenses / operator in Fulla development

$ 175.8m acquisition price

$ 80m (45%) of the acquisition costs financed on

a non-cash basis (using the tax shield)

required approvals from Norwegian authorities:

– Ministry of Petroleum and Energy (MPE)

– Ministry of Finance (MoF)

Heimdal – reserves and resources net

2P 2C prospective resources

NORWAY: HEIMDAL ACQUISITION

19/37

2/3 of the tax assets unlocked in 2013 – 2016

recovery of acquisition cost by late 2014/early 2015

cooperation with experienced Partners:

Statoil, Centrica, Total

risk diversification

building up strong E&P industry position within NCS

access to areas with high potential for the discovery of

resources

doubling production

Positive

effects

Heimdal = new begining

NORWAY: HEIMDAL TRANSACTION RESULTS

20/37

Dated as of 01.01.2013

mm boe Poland Norway Lithuania

35.2

8.4

22.0

+16%

2P reserves = 65.6 mn boe

30.1

0.3

31.0

+102%

Poland Norway Lithuania

2C reserves = 61.4 mn boe

RESERVES AFTER HEIMDAL TRANSACTION

21/37

4.7 5.7

9.4 10.4

24.0

0

5

10

15

20

25

30

2011 2012 2013 2014 2015

dai

ly p

rod

uct

ion

(kb

oe

/d)

+5.1 - B8

+2 - other PL (onshore)

+ 0.5 - Lithuania

+6 - acquisition

total investments in LOTOS E&P 2011-2015 3.9 billion PLN

daily p

rod

ucti

on

(kb

oe/d

)

*kboe/d

Strategy implementation plan

2015 – PRODUCTION POTENTIAL 24 KBOE/D

22/37

production potential 24 kboe/d in 2015

full exploration of the Baltic Sea licenses

onshore presence in Poland

stable position and growth potential in Norway

solving the problem with YME

an active participant in the international market

a modern and dynamic organization with a

highly qualified staff

SUMMARY

23/37 International Capital Markets Day - Grupa LOTOS S.A. - Gdańsk November 27th 2013 23/40

OPERATING SEGMENT

MAREK SOKOŁOWSKI

CHIEF OPERATION OFFICER, GRUPA LOTOS S.A.

VICE PRESIDENT OF THE MANAGEMENT BOARD OF GRUPA LOTOS S.A.

24/37

2008 → 2010→ 2012

Refinery Utilization 1Q → 3Q → 2Q

Energy Intensity Index (EII™ ) 1Q → 1Q → 1Q

Personnel Index 4Q → 3Q → 2Q

Personnel Cost Indicator 3Q → 1Q → 1Q

Mechanical Availability 3Q → 1Q → 2Q

Maintenance Index 2Q → 1Q → 1Q

Maintenance Cost Efficiency Index (MEI™) 2Q → 1Q → 1Q

Return on Investment 1Q → 1Q → 2Q

LOTOS REFINERY IN SOLOMON STUDIES

25/37

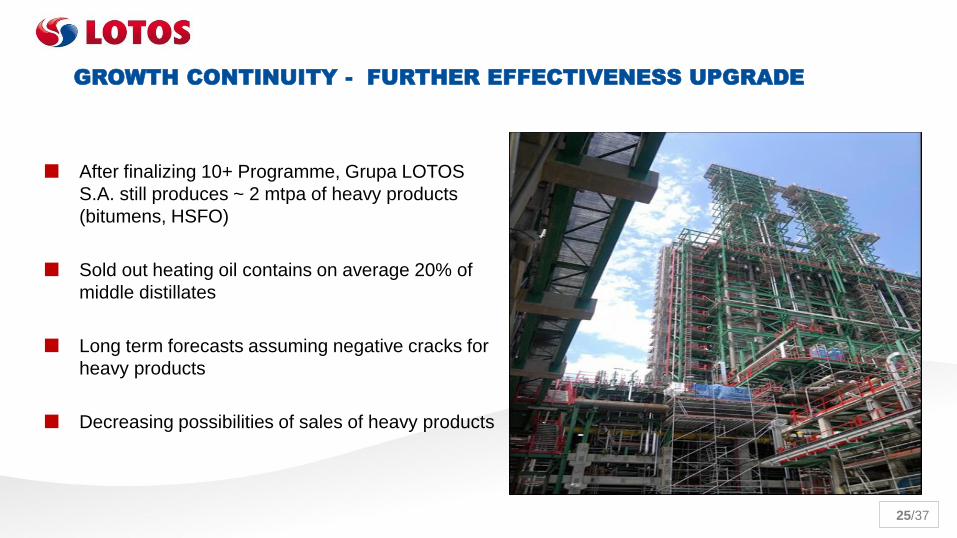

GROWTH CONTINUITY - FURTHER EFFECTIVENESS UPGRADE

After finalizing 10+ Programme, Grupa LOTOS

S.A. still produces ~ 2 mtpa of heavy products

(bitumens, HSFO)

Sold out heating oil contains on average 20% of

middle distillates

Long term forecasts assuming negative cracks for

heavy products

Decreasing possibilities of sales of heavy products

26/37

Very low low very high

IRR

NPV

Una

ttrac

tive

at

trac

tive

CHP*

DCU*

IGCC*

Size of the bubble – relative CAPEX for the project

CAPEX for the project EUR 400 – 500m

Higher utilization rate of the existing units

(HDS and MHC)

Middle distillates production oriented

Solving all problems of heavy residue

Increase of the refining margin – estimated

for 2 USD/bbl

Source: Purvin & Gertz * DCU – Delayed Coking Unit

IGCC – Integrated Gasification Combined Cycle

CHP – Combined Heat and Power

ALTERNATIVE SCENARIOS POSITIONING – RATIONALE BEHIND DCU

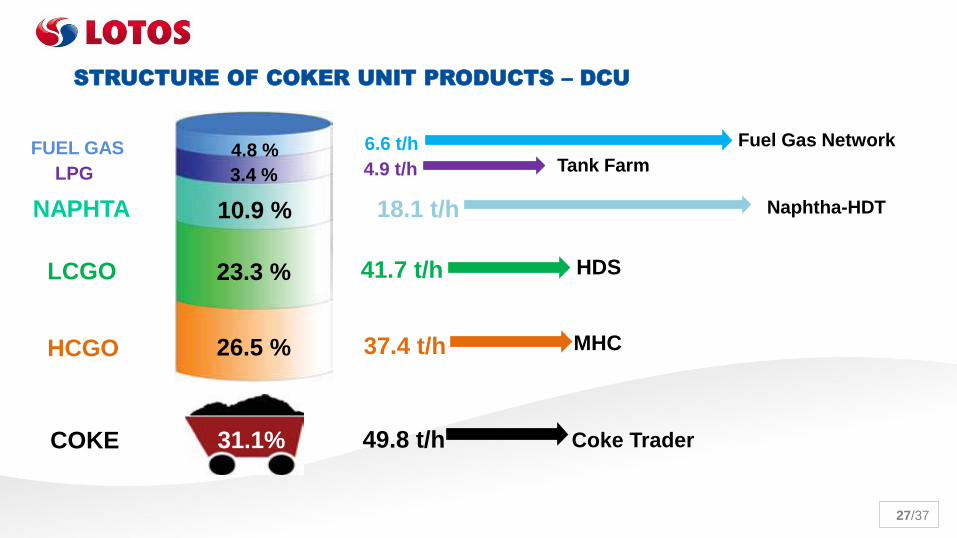

27/37

31,1 %

26.5 %

23.3 %

10.9 %

3.4 %

4.8 % FUEL GAS

NAPHTA

LPG

LCGO

HCGO

COKE

41.7 t/h HDS

37.4 t/h MHC

49.8 t/h Coke Trader

18.1 t/h Naphtha-HDT

Fuel Gas Network 6.6 t/h

4.9 t/h Tank Farm

31.1%

STRUCTURE OF COKER UNIT PRODUCTS – DCU

28/37

Product yield following implementation of DCU (% product)

Decrease of the heavy

products’ share in the total

output

Increased level of middle

distillates

Residual Coke appearing

following the finalization of the

project

+8pp

-12pp

Notes:

1) Gasoline + Naphtha + LPG

2) Diesel + Jet Fuel + LHO

3) HSFO + Bitumens + Slacks

1) 2) 3)

DCU – SIGNIFICANT IMPROVEMENT OF PRODUCTS YIELD

29/37

Increase of hydrogen available in the

refinery – by recovery from refining gases -

increase of refining margin

Replacing high margin products (used in

refinery fuel gas) with natural gas

CAPEX ~ PLN 100m

NPV PLN 400 – 500m:

Payback period: 2 years (after completion

of the project)

Additional annual production from HRU (k tons)

+50%

+4%

+7%

Product sales volume increase thanks to HRU

HYDROGEN RECOVERY UNIT

30/37 International Capital Markets Day - Grupa LOTOS S.A. - Gdańsk November 27th 2013 30/40

MARKETING SEGMENT

MACIEJ SZOZDA

CHIEF COMMERCIAL OFFICER, GRUPA LOTOS S.A.

VICE PRESIDENT OF THE MANAGEMENT BOARD OF GRUPA LOTOS S.A.

31/37

Main achievements Future goals

LOTOS TANK AND AIR BP JOIN VENTURE

DOMESTIC MARKET DEVELOPMENT IN

FUELS AND LUBRICANTS

RETAIL MARKET SHARE INCREASE

NEW IMPORTANT DESTINATIONS IN

LUBRICANTS’ SALE

PETROL STATION NETWORK EXPANSION

IN DOMESTIC MARKET

10% SHARE IN RETAIL MARKET IN 2015

SUSTAINABLE SALES GROWTH IN ALL

PRODUCTS

INVESTMENTS IN DOMESTIC LOGISTICS

INFRASTRUCTURE

32/37

LOTOS AIR BP

33/37

DECEMBER 2013 – 451 petrol stations

2012

Domestic retail consumption (mln m3)

2013

(5.8%)

14.7 13.9

2012

LOTOS Group share in retail market

2013

0.6 pp

8.0%

Forecast

Forecast

8.6%

RETAIL MARKET IN POLAND

34/37

27.1% 27.9%

2012 2013

LOTOS Group share

in the domestic lubricants market

0.8 pp

Strong expansion of LOTOS Group in the

lubricants export.

Our products are available in more than 50

countries in Europe and around the world.

Forecast

LUBRICANTS AND PLASTICIZERS MARKET

35/37

LOGISTICS

Key projects

Logistic assets’ optimization

LOTOS Terminale – fuel terminals integration and development – operational

concentration in one functional structure

Fuel storage effectiveness improvement

Marine terminal investment at Martwa Wisła

Creating trans shipment availability in the nearest district

Export and import channels diversification

Intermediaries’ costs elimination

36/37

Yemen Vietnam

Venezuela

V.A.E

Uzbekistan

USA

Ukraine

Tunesia

Turkey

Togo

Tansania

Tadschikistan

South Africa

Sudan Senegal

Sweden Russia

Romania

Portugal

Poland

Philippines

Peru

Panama

Norway

Nigeria

Morocco

Mauretania

Madagascar

Liberia

Kirgisistan

Kasachstan

Israel

Italy

Ireland

Iraq

Indonesia

Guinea

Greece

Great Britain

Germany

Fr. Guyana

France

Finland

Egypt

Cote d‘Ivoire

Chile

Belarus

Argentinia

Algeria

Alaska

Afghanistan

EXPORT TO 62 COUNTRIES ALL AROUND THE WORLD

37/37

Thank You