Embed Size (px)

DESCRIPTION

Magazine for newly qualified acountants who have studied a CCAB qualification.

Citation preview

FUTURE PERFECTNewly qualifieds: seize the day, says Reed Finance’s Peter Sherlock

MAKING STRIDES We focus on four women who are making headway in accountancy

THE VOICE OF ALL NQs

GoING STATESIDE CIMA and the American dream

ALL THE NEws yOu NEEd

Pages 4 and 6

HOmE swEET HOmE Page 11

CGT and your home

THREE FANTAsTICE-REAdERs

musT BE wON!

see page 3

CHANGES AFooTIFRS: Five things to look out for

P16

P8

Contact usemail:

[email protected]: @pqmagazinefacebook: pqmag.com

call: 020 7216 6427

MAY 2013

P20

P14

Take your ACCA or

CIMA qualification

further with an MBA*

UKBA HIGHLY TRUSTED

SPONSOR

LONDON SCHOOLOF BUSINESS & FINANCE

ACHIEVE MORE. BECOME MORE.

*The awarding body for the MBA/MSc course will be one of LSBF’s partner universities,

however, awarding bodies are subject to change from time to time. The School’s obligations

shall be discharged by providing tuition leading to a recognised MBA/MSc award by a recognised

awarding body. The student shall have no claim based on changes to the awarding bodies.

The MBA/MSc programmes are subject to approval of association and programmes of study.

www.LSBF.org.uk/NQ

020 3535 1410

Combine accounting and advanced business skills

Gain two globally recognised qualifications

Full-time, part-time and online study options

Boost your career and earning potential

u

u

u

u

Full-time Part-time Online

ENQUIRE TODAY!

002_LSBF.indd 3 07/05/2013 15:20

Three NOOK Simple Touch e-readers to give away

Welcome to the latest issue of NQ magazine – our second of 2013. We want to make sure we are giving you what you want, and feel we should offer an incentive – and that incentive is the NOOK Touch! All you need to do is tell us what subjects you would like to see featured in a forthcoming issue and tell us where – apart from this one and the cover – you can see a NOOK Touch. You could suggest a feature on interview skills, CPD, international standards – simply send your ideas (and the page number when you’ve found the Touch!) to [email protected]. Head up your email ‘NQ magazine ideas’.

In this issue we also home in on NQ salaries and opportunities. Our friends at Reed Accountancy explain that the very nature of what the professional accountant has to bring to the table is changing. You may need to get outside your comfort zone to put yourself at the heart of the business. Technical skills are no longer enough, and as we say on page 18, you can’t be a zombie!

We hope we have the balance of technical and people stories about right. Kaplan Financial’s Bruce Cowie, for example, explains the five major changes we have seen recently in the world of IFRSs, and we have four women who have all made it to the top in their chosen area.

Enjoy the read and do tell us what you want to see. Graham Hambly, Editor ([email protected])

Everything AccountingFrom Auditing & Fraud to IFRS... Our knowledge is your power

FREE sample chapter minibook featuring the above titles at http://tinyurl.com/d58rwyh OR scan on the QR code

www.wiley.com/go/accounting

@wiley_finance #wileyknowledge #knowyourpower

NQ Readers SAVE 30%*

*Quote code ANQ20 when ordering at www.wiley.com

EDITOR’S COMMENTS

Addictionpage 10

COMMENT

ADDITIONAL CONTENTS

Addiction – Sage advice for CABA on dealing with addiction Page 10

People skills – Why developing ‘inter-personal’ skills is vital for your career Page 18

Auditor reporting – Changes are in the pipeline for audit reporting. We explain all Page 22

4 NQ Magazine May 2013

NEWS

A game of cat and mouseHMRC cannot win its war on tax avoidance claims the Public Accounts Committee, and it appears the blame is being laid at the door of the Big 4 firms.

The PAC recently published its 44th report of this session on tax avoidance: the role of large accountancy firms. Chair of the committee Margaret Hodge said: “Our inquiry has exposed the continuing weakness of HMRC in its efforts to deal with tax avoidance. It is engaged in a never-ending game of cat and mouse. Among those ranged against it are the Big 4 accountancy firms, which earn £2bn each year from their tax work in the UK.

“They employ nearly 9,000 people just to provide tax advice to companies and wealthy individuals, much of which is aimed at minimising the tax paid. Between them they boast 250 transfer pricing specialists whereas HMRC has only 65 people working in this area.

“The firms declare that their focus is now on acceptable tax planning and not aggressive tax avoidance. These protestations of innocence fly in the face of the fact that the firms continue to sell complex tax avoidance schemes with as little as 50% chance of succeeding if challenged in court.

“The large accountancy firms are in a powerful position in the tax world and have an unhealthy cosy relationship with government. They second staff to the Treasury to advise on formulating tax legislation.

“When those staff return to their firm, they have the very inside knowledge and insight to be able to identify loopholes in the new legislation and advise their clients on how to take advantage of them. The poacher, turned gamekeeper for a time, returns to poaching.

“This is a ridiculous conflict of interest, which should be banned in a code of conduct for tax advisers, as we have recommended to the Treasury and HMRC.”

Where are all the women?

Female partners in the top 50 accountancy firms are still rare creatures, according to statistics put together by Accountancy.

Just 10 of the top 50 accountancy firms have 20% (or more) women partners. Firms such as Frank Hirth and Mercer & Hole are

leading the way.The concern will be with

firms such as BDO (12%), Mazars (9.5%) and Johnston Carmichael (6.7%).

When it comes to the Big 4, Ernst & Young head the rest with female partners totalling 17%. The rest hover around the 14%–15% range.

European politicians appear to have decided to water down the plans for a more highly regulated audit industry.

Out then goes the proposals for mandatory audit rotation every six years. The Legal Affairs Committee has said that quoted companies should switch auditors every 14 years instead. However, companies will be able to hold on to the same auditor

for up to 25 years if they ensure certain safeguards are in place to ensure independence.

The committee also dismissed a ban on auditors carrying out non-audit work for clients. This would have had serious implications for the Big 4 and could have forced them to break-up their operations.

The reforms will now go back to member states for more discussion.

Auditors win reprieve

020 8408 9999www.walkerdendle.co.uk

Find us on Facebook, Twitter and LinkedIn

DEPENDABILITY

Walker Dendle Financial Recruitment has become established as a leading

recruiter of professional permanent and temporary finance staff in Surrey and

the surrounding area for over 12 years, filling a diverse range of part qualified

finance and accounting roles across financial and management accountants to

commercial accounting and analysis to finance business partnering.

We continually focus on adapting and refining our service to suit you, offering sound and

knowledge based careers advice to part qualifieds seeking their next, all-important job move.

For more information about the range of career openings available though Walker Dendle

Financial Recruitment, please contact:

Permanent Division [email protected]

Temporary & Contract Division [email protected]

Walker Dendle Financial Recruitment

Swan House, 51 High Street, Kingston, Surrey KT1 1LQ

AT WAlkeR DenDle We hAve mAny DiFFeRenT AbiliTieS.

ouR RePuTATion FoR DePenDAbilTy SeTS uS APART.

6 NQ Magazine May 2013

NEWS

What are NQs worth?The Reed Finance Salary Guide 2013 is hot off the press. It explains that organisations are striving to align their finance functions within the main heart of their business. That means finance professionals are increasingly being asked what other skills and experience they have beyond their core technical skills.

Candidates who are able to provide prospective employers with credible evidence of past successful business partnering, for example, will in the short-term stand out from the competition, say Reed Finance.

Compliance and risk management will continue to be an important discipline in 2013, as will corporate governance, so candidates with these skills sets and experience will be in high

demand over the next 12 months, especially in regulated industries such as financial services.

The survey covers financial services, pharmaceuticals, banking, manufacturing, FMCG, retail

and leisure, property and construction, energy and utilities, technology and communications, creative and media, public sector and business services. Phew!

Reed Finance’s Salary Guide & Market Insight 2013

FMCG Financial Public Sector Services

Central London £45,464-£60,618 £48,431-£64,575 £40,459-£53,945

South Coast £27,328-£38,000 £29,112-£35,000 £24,320-£33,995

South Wales £29,203-£40,816 £31,109-£43,481 £25,988-£36,323

Midlands £30,487-£37,371 £32,477-£39,810 £27,131-£33,257

East Anglia £32,873-£39,846 £32,019-£42,447 £29,254-£35,460

North West £32,317-£40,397 £34,427-£43,034 £28,759-£35,950

North East £27,836-£34,000 £29,653-£34,949 £24,772-£29,196

Scotland £30,121-£40,160 £32,087-£42,781 £26,805-£35,739

Northern Ireland £29,943-£39,925 £31,898-£42,531 £26,647-£35,530

(our table is a snapshot: more industries and regional salaries are online at www.reedglobal.com)

Reed Finance’s Salary Guide & Market Insight 2013reedglobal.com

Highest number of business start-upsLondon

Lowest numberof business start-ups

65.0

Milton Keynes 50.1

Aberdeen47.7

Stoke23.2

Mansfield21.7

Sunderland16.8

START-UP CITIESBusiness start-ups by region

London

38.6

29.0

65.0

South Midlands38.3

Yorkshire & Humber30.5

22.0

32.0

31.5

Northern Ireland & Scotland33.2

32.3

Cities with the...

Salary Guide and Market Insight 2013

CFO jobs: keep it in the familyChief Finance Officers appointed from within a company have longer, more stable tenures and are associated with better returns than CFOs hired from outside, says the Curzon Partnership.

An analysis of FTSE100 CFOs over the past five years shows that internally appointed CFOs have an average tenure of 6 years, which is 30% longer than the average of just 4.6 years for CFOs appointed externally.

The return on assets for

businesses with internally appointed CFOs is a third better, at 9.5%, than the 7.1% for companies that hire their CFOs from outside.

Curzon’s James Colhoun was not surprised. He said: “Internally bred CFOs know the company, its markets and its culture far better than an outsider. The best CFOs will not only understand the right strategy to improve returns and properly exploit the businesses assets but, crucially, they will know how best to deliver that strategy.”

The ACCA has introduced an interactive checklist of competencies that business leaders require from aspiring finance professionals.

The Competency Framework is a fantastic tool for newly qualifieds. The specially constructed website will help those filling out job applications to understand what competences sitting their exams have given them – some of which they might not even know they have!

The 10 key competencies for complete finance professionals are:1) Professionalism & ethics.2) Governance, risk and control.3) Stakeholder relationship

management.4) Strategy and innovation.5) Leadership and management.6) Corporate reporting.7) Sustainable management accounting.8) Financial management.9) Audit and assurance.10) Taxation.

You can find the ACCA’s Competency Framework at: http://competencyframework.accaglobal.com

Are you a competent accountant? – ACCA

Executive recruitment specialists

Time for your next step

At Reed Finance, over a quarter

of our roles are ideal for newly

qualified accountants.

To discuss your next step,

Änd your nearest branch here.

reedglobal.com/finance

@ReedFinanceJobs

For all the latest jobs where you are

@ReedFinance

For all our latest Finance news

Reed Finance

For news, views, jobs and discussion

Stay in touch with us:

8 NQ Magazine May 2013

REED FINANCE

This is an exciting time for newly qualified accountants – the finance function within

an organisation changed irrevocably during the downturn and in most businesses has a much broader remit than in pre-recessionary days. Since then, finance professionals have increasingly found themselves acting more in a ‘business partner’ capacity which demands additional skill sets not typically associated with traditional finance professionals, as well as having increased influence and involvement in wide ranging areas of their business.

This blurring of the lines between finance and business management, between the tasks typically performed by CFOs and those by COOs, has

given a number of experienced finance professionals a widely sought-after opportunity to develop beyond financial management into business management and leadership – a shift in emphasis that is here to stay.

As organisations strive to more closely align their finance functions within the main heart of their business, finance professionals at every level are increasingly being asked what other skills and experience they have beyond their core technical skills. Candidates who are able to provide prospective employers with credible evidence of past successful business partnering, for instance, will in the short term at least, stand out clearly from the competition.

For new and recently qualified accountants, this broader scope of the finance function presents an exciting opportunity to forge an interesting and challenging career path.

A thriving marketIt’s encouraging that demand for new and recently qualified accountants has remained resilient across most sectors during the last twelve months and continues to hold firm. As finance strengthens its position at the heart of most business operations, employers are increasingly looking to ‘grow their own’ finance experts by recruiting at a newly qualified level. This gives NQ level candidates the luxury of choice – albeit in a competitive jobs market

Finance takes centre stageAttaining NQ status opens the door to a host of new opportunities. Peter Sherlock looks at how you can make the most of them to achieve your career goals

9NQ Magazine May 2013

REED FINANCE

– in terms of their chosen working environment.

For those keen to forge a more rounded career path, in the new mould of ‘business partner’, there has been healthy demand among SMEs operating in a wide range of markets. Whilst at the more technical end of the spectrum there is particularly strong demand for candidates with corporate governance and compliance expertise to fill analyst roles in the financial services sector, following the huge drive to strengthen compliance in this sector. Across the board, compliance and risk management will continue to be an important discipline in 2013, as will corporate governance, so candidates with experience in this area will be in high demand.

Stability and satisfaction levelsOur recent REED Finance 2013 Salary and Market Insight report showed that the majority of finance professionals are very satisfied in their current roles, up 10% on the previous year – perhaps as a result of the perceived value of their work within the wider organisation. Against the backdrop of healthy demand for candidates in the sector, coupled with the increased importance of the finance function, it’s not surprising that the overwhelming majority (83%) also said they felt secure in their role.

● Peter Sherlock, Divisional Director at Reed Finance

NQ

reedglobal.com

Highest number of business start-upsLondon

Lowest numberof business start-ups

65.0

Milton Keynes 50.1

Aberdeen 47.7

Stoke23.2

Mansfield 21.7

Sunderland 16.8

START-UP CITIESBusiness start-ups by region

London

38.6

29.0

65.0

South Midlands38.3

Yorkshire & Humber 30.5

22.0

32.0

31.5

Northern Ireland & Scotland33.2

32.3

Cities with the...

Salary Guide and Market Insight 2013

POST QUALIFICATION: TIPS FOR SECURING YOUR DREAM ROLE● Be clear on your long-term goal It’s important to be focused in your search and think about how your first role post-qualification will lead to achieving your long-term goal. ● Take a long hard look at yourself Once you know the type of role/s that you are interested in applying for, you need to consider your strengths and weaknesses in the context of the role you are seeking. Businesses want long term potential with their NQ hires and will be typically looking for evidence of commercial acumen, communication skills, people management and potential for leadership in addition to the core financial management skills that are taken as a given at this level. Give some thought to how you

might be able to demonstrate a broader skill set and stand out against other candidates. ● Timing is everything It’s tempting to start the search as soon as you attain NQ status, but the timing may not be right. You will still be considered ‘newly qualified’ for up to 18 months post-qualification. For some candidates, six months spent sitting tight in your current role strengthening your CV by volunteering for projects that expose you to the broader business could give you the edge further down the line.

● To discuss your next step or for more advice from our expert consultants, find your nearest branch here.

Sherlock: “Exciting opportunity”

10 NQ Magazine May 2013

ADDICTION

Coping with addiction

I t’s worth noting from the outset that at the Chartered Accountants’ Benevolent Association we have

no evidence to suggest that there is a widespread problem with addiction among young accountants. During the past few years we have been contacted by no more than a handful of people with problems that fall into this category. However, those who have turned to us have often been in a very real state of distress and needed help.

What is addiction? According to the NHS Live Well website, “Addiction means not having control over doing, taking or using something harmful. You can't control how you use whatever you are addicted to and you become dependent on it to get through each day.”

How do you become addicted to something? The addiction arises as a result of physical or psychological changes. For example, someone who likes to gamble may feel so good after placing a winning bet that they have a desire to repeat the experience. Over time, that impulse grows until it becomes all-consuming. If a person has a similar relationship to a substance such as alcohol their body will become tolerant over time and the user will

need to consume increasing amounts to experience the same effect.

Some studies claim to show a genetic predisposition to addiction. However, the factors are just as likely to be environmental. As a young accountant under pressure both from exams and work, you may find yourself turning to something to cope that at first appears harmless but can develop into an issue.

How do you know when you are addicted? This will vary with the nature of your addiction but the key signs are that your behaviour becomes obsessive, that social relationships and work start to suffer as a result, and that you experience not just good feelings surrounding the activity but perhaps also a degree of guilt and shame.

So what can be done? It’s something of a cliché but on a personal level, the first step towards managing your addiction is admitting that there is a problem. Similarly, if you believe that someone you know is suffering from an addiction, then you should consider approaching them in a non-confrontational manner.

With this first step taken, if you call CABA, our qualified counsellors evaluate the nature of your problem

and the type of help that you may need. Often the first step is to encourage someone to visit their GP so that they can be properly assessed. Also, there are specialist groups such as Alcoholics Anonymous and Gamblers Anonymous who will provide assistance.

From a young accountant’s point of view, it is important to underline that all of this help, including any provided by CABA, is confidential. Also, it is worth underlining that the best time to seek help if you believe that you have an addiction problem is now. Research shows that the earlier the intervention, the easier and more successful the outcome.

● Wendy Saunders is Head of Development at the Chartered Accountants’ Benevolent Association

NQ

More information about CABA and its services can be found at www.caba.org.uk

NHS advice on addiction can be found at www.nhs.uk/Livewell/addiction

Help is at hand for young accountants whose addictive behaviour is starting to take over their lives, says CABA’s Wendy Saunders

Farnham office:

01252 718777 [email protected]

Weybridge office:

01932 901900 [email protected]

www.howett-thorpe.co.uk

For a career with added bite!

th

WEYBRIDG

E

OFFICE

NO

W O

PEN

added bite!

We’ll satisfy your hunger.

I N D I V I D UA L F I N A N C I A L R E C RU I T M E N T

PQ Magazine 297x210.indd 1 16/04/2013 16:40

12 NQ Magazine May 2013

SELLING YOUR HOME

When you sell your home, it is strictly a chargeable disposal of a chargeable asset and therefore subject to Capital Gains Tax. This seems harsh,

however, as the main reason for buying the asset was to provide shelter for you and your family, not to make a profit. In many cases the proceeds have been reinvested in the next family home, so there is no cash available to pay any Capital Gains Tax, especially with all of those extra expenses of moving such as Stamp Duty Land Tax, solicitor’s and estate agent’s fees, plus all the decorating and new furniture.

So, if you sell the home that you have lived in the whole time that you have owned it there is no Capital Gains Tax to pay. The gain (or loss) is automatically exempt under Principal Private Residence (PPR) Relief.

The complications arise if you haven’t lived in, or occupied, your home the whole time; for example if you worked away and let it out or you went travelling for a few months and left it empty, asking neighbours to pop in and water the plants. And what if you used the spare room as your office, or if you own more than one house?

Well, a person together with their spouse/civil partner can only have one home, or PPR, and if you own more than one property you have to decide which one of them is your PPR. It must be a property that you do actually use as a home, even if it’s a country retreat that you live in at the weekends, or a flat in the city that you use during the week.

You then look at how that property has been used over the years that you owned it. The capital gain is deemed to accrue evenly over the period of ownership, and for any periods that you actually occupied the property, the same

proportion of the gain is exempt. Periods when you weren’t living in your PPR are also exempt if they fall into any period of ‘deemed occupation’.

The last three years that you own your PPR are always deemed occupation, provided the property was your PPR at some point.

The following are all deemed occupation if there is a period of actual occupation at some point both before and after the absences:◗ Cumulative periods of up to four years where you or your spouse/civil partner are employed elsewhere in the UK, or self-employed elsewhere in the UK or overseas;◗ Any periods in which you or your spouse/civil partner are employed overseas; and◗ Cumulative periods of up to three years absence for any reason.

The requirement to actually occupy the property after the absence can be waived if an employee working elsewhere is prevented from returning by his employer, so for example, there is no position available in your local office at the end

Liz Halford outlines the various taxes that come into play when a homeowner sells up

Selling your home: the tax implications

13NQ Magazine May 2013

SELLING YOUR HOME

of a secondment and you are offered a position elsewhere. You can potentially claim all of the above periods of deemed occupation on a PPR, provided you meet the conditions for each.

Any period not covered by actual or deemed occupation is chargeable to Capital Gains Tax. If during any of these chargeable periods the property was let out, there is an additional exemption that is automatically applied known as Lettings Relief. This will exempt the lower of:◗ The gain that is chargeable as a result of the let (ie. not covered by the PPR Relief);◗ The PPR Relief given on the property; and◗ £40,000.

The £40,000 limit applies per owner, so if a house is owned jointly by a husband and wife a maximum of £80,000 lettings relief will apply to the disposal.

PPR and lettings reliefs cannot cover parts of the property that have been used exclusively for business purposes as they are designed to cover your home, not your business assets. So if you have used 10% of your home exclusively as

a workshop, 10% of the gain for the periods that it was used as a workshop is chargeable. However, if at some point this area was used as part of your home, the workshop will still qualify for PPR during those periods and also the last three years as deemed occupation.

So, in summary, when you sell your house, PPR Relief will exempt any gains arising when:◗ You lived in the house, or◗ You were deemed to have lived in the house.Lettings Relief will exempt any gains arising while the property was let, if not already covered by PPR Relief, up to a maximum of £40,000.

As a result, the vast majority of taxpayers will be able to sleep soundly in their homes, safe in the knowledge that if they decide to move, CGT will not be a factor in the decision.

● Liz Halford is a tutor at Tolley Exam Training, part of LexisNexis. She can be contacted on 020 3364 4500 or [email protected]

NQ

14 NQ Magazine May 2013

IFRS

Five key changes to IFRSs

1. IAS 19 Employee benefits: actuarial gains/lossesProbably the most visible of the changes is in the treatment of actuarial gains/losses on defined benefit pension schemes. Previously companies have been able to opt for the “corridor and spread” approach under which gains and losses were not immediately recognised, resulting in pension deficits (and surpluses!) not being recognised on balance sheet in full. A classic example is British Airways (now part of IAG), who recognised a net pension asset of £878m on their balance sheet at 31/12/2011 whilst the notes to the accounts reveal a net deficit of £361m. The new standard requires the full recognition of all gains and losses immediately in Other Comprehensive Income, resulting in full on balance sheet recognition of all deficits and surpluses.

2. IAS 19 Employee benefits: the financing elements of the pension costThis change initially slipped under the radar, but will adversely affect the reported earnings of almost every entity with a funded defined benefit pension plan. Instead of reporting two components within the income statement, being the expected return on plan assets (finance income) and interest (at a rate based on bond yields) on the plan liabilities (finance costs), in future entities will report a single amount of interest (at the bond yield rate) on the opening net pension

liability (or asset). Impacts on reported earnings in the region of £20m to £70m will be relatively commonplace. Measures such as EBIT and EBITDA will not be affected, but there will be substantial changes to earnings per share.

3. IAS 19 Termination benefitsTermination benefits have been redefined in IAS 19. This change at first appears inconsequential: however, it will require companies to look at the terms of termination/restructuring arrangements to identify elements which are in substance remuneration arrangements rather than terminations. An example would be so called “golden handcuffs” offered to retain employee services in a rundown period. These will generally be spread over the retention period. In addition, the point at which the cost of voluntary redundancy schemes is recognised may change.

4. Identification of subsidiaries (IFRS 10)Subsidiaries will no longer be identified by considering voting power, and the concept of consolidated Special Purpose Entities introduced by SIC 12 is superseded. The revised definition of a subsidiary considers control over the key drivers of profit or loss, whether sourced by voting power or by contractual arrangements. The effect of this change will be the consolidation of some entities not currently consolidated and the omission from consolidation of

some currently consolidated. Careful re-examination of the accounting for many investments and collaboration arrangements will be required.

5. Identification of and accounting for joint ventures (IFRS 11)IAS 31 Joint ventures is replaced. The new standard defines joint arrangements as entities which are jointly controlled, with joint control being identified under principles that are consistent with IFRS 10. Joint arrangements are then distinguished between joint ventures and joint operations, based on the nature of the commercial relationship between the venturers and the joint arrangement.

These changes will mean that investors will no longer have the facility to manipulate accounting treatment by the use of legal entity structures, and that there will be no choice of accounting treatments. A key effect of the changes will be that proportional consolidation will no longer be an available accounting treatment for joint ventures. Where an entity is defined as a joint venture, equity accounting will be mandatory thus making the treatment the same as associates.

● Bruce Cowie, Head of Financial Reporting, Kaplan Hawksmere

A raft of amends to IFRSs took effect from 1 January 2013, but which are the key ones? Bruce Cowie highlights some of the headline changes

To find out what Kaplan Hawksmere offer, or if you have any specific requirements then please get in touch. Email [email protected] or call 0845 833 3212.

Why not attend one of Kaplan Hawksmere’s FREE Finance CPD webinars? Just use code NQWEB and click here to book.

NQ

Register today for your FREE TICKET using code: ICPA13 at www.accountex.co.uk

ACCOUNTEX2013

THE NATIONAL ACCOUNTANCY EXHIBITION AND CONFERENCE

6 / 7 JUNE 2013 ExCeL, LONDON

SUPPORTED BY

Limited stands still available, for more information please email [email protected]

p� 120 + FREE SEMINARS RUN BY INDUSTRY EXPERTS

p� INTERACTIVE WORKSHOPS

p� PROFESSIONAL DEVELOPMENT

p� 100 INDUSTRY SUPPLIERS ALL UNDER ONE ROOF

p� STAY AHEAD IN AN EVER CHANGING INDUSTRY

p� COMPLETELY FREE TO ATTEND WHEN YOU REGISTER IN ADVANCE

The UK’s largest event for Accountants in practice

and in businessAccountex offers unparalleled opportunities

for Financial Professionals to gain expert

insight and education in a live environment.

Supported by all the major Accountancy

Associations with 100 exhibiting companies,

12 seminar theatres and workshops this is the

must attend annual event for any leading

professional in the Accounting Profession.

16 NQ Magazine May 2013

CGMA

A year of success

CIMA’s tie-up with the AICPA is proving a game-changer for management accountants across the globe

I t has been a little over a year since the launch of the Chartered Global Management Accountant

(CGMA) designation changed the international landscape of the accounting profession. The designation was established by a joint venture between two of the world’s leading accounting bodies, the Chartered Institute of Management Accountants (CIMA) and the American Institute of CPAs (AICPA), in January 2012. Since its launch, it has become the most prominent management accounting credential in the US, with more than 38,000 finance professionals now holding the designation. They are part of a global community of over 129,000 CGMA business experts.

The new designation has also attracted more students to CIMA, with 2012 a record-breaking year that saw more than 29,000 new students joining. This growth was fuelled by the institute’s wider geographic footprint and the additional opportunities

created by the partnership with the AICPA.

CIMA Chief Executive Charles Tilley said: “The CGMA designation has elevated the profession of management accounting. It recognises those with the discipline and skill required to drive strong business performance in uncertain economic times.

“It is a global designation which demonstrates expertise in areas such as effective decision-making, risk management and operational efficiency.”

He added: “With the designation your value is known all around the world. It opens more doors, and presents more opportunities, than any other professional business qualification. It allows you to showcase your expertise in management accounting to the global market.

“It has been a great experience for CIMA to work with the AICPA. The relationship allows us to complement each other’s skills and specialties, and

ensure that we are meeting the needs of a global membership base. We continue to learn from each other every day and look forward to a long and successful partnership.” NQ

CIMA Chief Executive Charles Tilley

�ĐĐŽƵŶƟŶŐ

dĂdžĂƟŽŶ

&ŝŶĂŶĐŝĂů

DĂŶĂŐĞŵĞŶƚ

�ĂƉŝƚĂů

DĂƌŬĞƚƐ

ZĞŐƵůĂƚŽƌLJ

Θ�ZŝƐŬ

&ŝŶĂŶĐŝĂů�Θ��ŽŵŵĞƌĐŝĂů�

�ǁĂƌĞŶĞƐƐ

/ŵƉƌŽǀŝŶŐ�WĞƌƐŽŶĂů

�īĞĐƟǀĞŶĞƐƐ

�ŽŶƟŶƵĞ�LJŽƵƌ�ƉƌŽĨĞƐƐŝŽŶĂů�ĚĞǀĞůŽƉŵĞŶƚ�ũŽƵƌŶĞLJ�ǁŝƚŚ�<ĂƉůĂŶ�,ĂǁŬƐŵĞƌĞ�

0845 833 3212

ƚƌĂŝŶŝŶŐΛŬĂƉůĂŶŚĂǁŬƐŵĞƌĞ�ĐŽ�ƵŬ

ǁǁǁ�ŬĂƉůĂŶŚĂǁŬƐŵĞƌĞ�ĐŽ�ƵŬ

������ΛŬĂƉůĂŶŚĂǁŬƐŵĞƌĞ

FREE �W��t��/E�Z^hƐĞ�ƉƌŽŵŽ�ĐŽĚĞ�EYt���ƚŽ�Ŭ

<ĂƉůĂŶ�,ĂǁŬƐŵĞƌĞ�ƐƉĞĐŝĂůŝƐĞ�ŝŶ�ƚŚĞ�ĚĞůŝǀĞƌLJ�ŽĨ�ĮŶĂŶĐĞ�ĂŶĚ�ŵĂŶĂŐĞŵĞŶƚ�ƚƌĂŝŶŝŶŐ��KƵƌ�ƐƵďũĞĐƚ�ŵĂƩĞƌ�

ĞdžƉĞƌƚƐ�ǁŝůů�ĞƋƵŝƉ�LJŽƵ�ǁŝƚŚ�ƚŚĞ�ůĂƚĞƐƚ�ŬŶŽǁůĞĚŐĞ �ƐŬŝůůƐ�ĂŶĚ�ƚĞĐŚŶŝƋƵĞƐ�ƚŽ�ŚĞůƉ�LJŽƵ�ƉƌŽŐƌĞƐƐ�ŝŶ�LJŽƵƌ�ĐĂƌĞĞƌ�

tŚLJ�ŶŽƚ�ĂƩĞŶĚ�ŽŶĞ�ŽĨ�ŽƵƌ�&Z����W��ǁĞďŝŶĂƌƐ��&ŝŶĚ�ŽƵƚ�ŵŽƌĞ�Ăƚ�ǁǁǁ�ŬĂƉůĂŶŚĂǁŬƐŵĞƌĞ�ĐŽ�ƵŬ�ǁĞďŝŶĂƌƐ

18 NQ Magazine May 2013

PEOPLE SKILLS

Don’t be a zombie!

T he life of a newly qualified accountant is not an easy one. I remember attitudes shifting

pretty much the moment I got my final results. Expectations seemed to move even faster than my charge out rate and suddenly I was an engagement manager, with all the associated pressures that entailed. I was lucky, in that I’d been given some great training in preparation, and had some great managers to learn from, but it was still a daunting experience. The thing that got me through was people skills.

Fast forward 12 years and I’m still

seeing individuals at my clients, in both financial and non-financial fields, who seem to think that the intellect that got them in the door is all that they need to get them up the ladder. I often find myself training or coaching these people because the reality is very different. Your qualification is the price of admission to the party: what makes you successful is how you cope with the different personalities and situations that you find when you get there.

The stand-out individuals in any organisation, be they finance or non

finance professionals, are always those with great people skills, and these skills can fit nicely into the four categories of emotional intelligence: self awareness; self management; social awareness; and relationship management.

Self awareness is about personal understanding. As a newly qualified the world is at your feet, you have a range of career directions that you can take, but you won’t take the right route unless you understand what’s really important to you. What do you really value, what motivates you, what causes you stress and why? Reflect on your experiences and you can work these things out and start to manage those emotions and the situations that lead to them. Know yourself and what drives you and it’s easier to stay on track.

I often think about self management as the way you manage the stress of increasing expectations. People with good self management are great at prioritising what really matters

Gareth Batterbee argues that developing ‘inter-personal’ skills is as vital as your qualifi cation when it comes to progressing your career

19NQ Magazine May 2013

PEOPLE SKILLS

so that their time in the office is as productive as possible. It’s not only time management, but it’s also about counting to 10 when the part qualified team member you’re now managing gets something wrong for the fourth time today, or when your manager drops yet more “urgent” work on you at 4pm on a Friday. If you can manage your emotions and your “state” then you can be a more effective professional. Think how much more respect you have for the manager who never blows their top, but instead gives you clear critical feedback that helps you improve.

Social awareness is something that the stereotypical accountant is not blessed with, but even those of us who are fully functioning members of society still face challenges in this area. The biggest challenge for the accountant is always to put yourself in the other person’s shoes, particularly when that individual isn’t a finance

person. When someone explained to me how intimidating they found their auditors it dawned on me that while I was worried about getting it wrong or over budget, the client staff I was dealing with were even more terrified: after all, I was potentially telling their boss that they weren’t doing their job right. Practice empathy and your interactions with people in the office and beyond will improve.

All these other elements feed into your ability to manage relationships. If you can hold back on your reactions, assess how the other person is feeling through listening and watching their body language, then you can choose the way you want the relationship to develop.

The good news is that all of these skills can be learnt. Some people may be naturals, but the rest of us can get there with practise. So the next time you’ve got some “soft” skills training, think of it as learning about how to deal

NQ

Gareth Batterbee specialises in personal, management and leadership development training at Kaplan Hawksmere. To find out what we offer or if you have any specific requirements then please get in touch. Email [email protected] or call 0845 833 3212.

To attend a FREE CPD webinar just use code NQWEB and click here to book.

with “hard to handle” people and see what you can learn. It may make the difference for your next client win – or promotion.

● Gareth Batterbee, Learning Development Lead, Kaplan Hawksmere

20 NQ Magazine May 2013

WOMEN IN ACCOUNTANCY

Real role modelsNQ magazine takes a look at four women’s very different paths to success

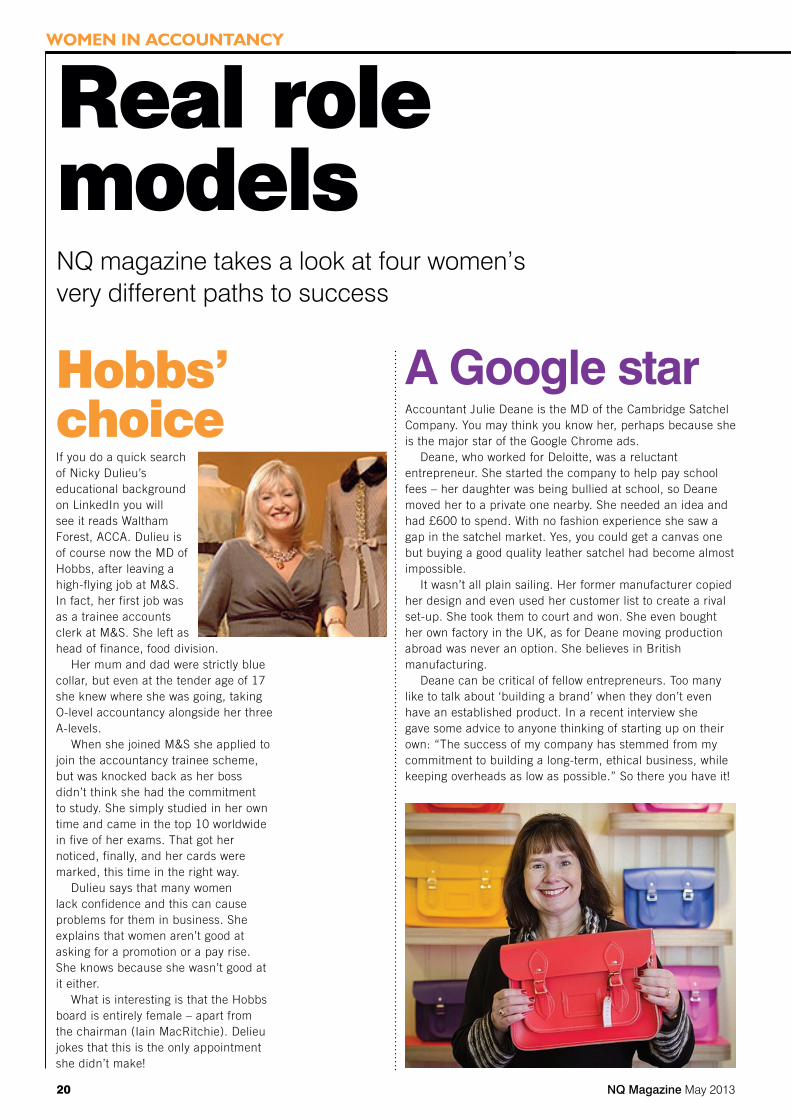

A Google starAccountant Julie Deane is the MD of the Cambridge Satchel Company. You may think you know her, perhaps because she is the major star of the Google Chrome ads.

Deane, who worked for Deloitte, was a reluctant entrepreneur. She started the company to help pay school fees – her daughter was being bullied at school, so Deane moved her to a private one nearby. She needed an idea and had £600 to spend. With no fashion experience she saw a gap in the satchel market. Yes, you could get a canvas one but buying a good quality leather satchel had become almost impossible.

It wasn’t all plain sailing. Her former manufacturer copied her design and even used her customer list to create a rival set-up. She took them to court and won. She even bought her own factory in the UK, as for Deane moving production abroad was never an option. She believes in British manufacturing.

Deane can be critical of fellow entrepreneurs. Too many like to talk about ‘building a brand’ when they don’t even have an established product. In a recent interview she gave some advice to anyone thinking of starting up on their own: “The success of my company has stemmed from my commitment to building a long-term, ethical business, while keeping overheads as low as possible.” So there you have it!

Hobbs’ choiceIf you do a quick search of Nicky Dulieu’s educational background on LinkedIn you will see it reads Waltham Forest, ACCA. Dulieu is of course now the MD of Hobbs, after leaving a high-flying job at M&S. In fact, her first job was as a trainee accounts clerk at M&S. She left as head of finance, food division.

Her mum and dad were strictly blue collar, but even at the tender age of 17 she knew where she was going, taking O-level accountancy alongside her three A-levels.

When she joined M&S she applied to join the accountancy trainee scheme, but was knocked back as her boss didn’t think she had the commitment to study. She simply studied in her own time and came in the top 10 worldwide in five of her exams. That got her noticed, finally, and her cards were marked, this time in the right way.

Dulieu says that many women lack confidence and this can cause problems for them in business. She explains that women aren’t good at asking for a promotion or a pay rise. She knows because she wasn’t good at it either.

What is interesting is that the Hobbs board is entirely female – apart from the chairman (Iain MacRitchie). Delieu jokes that this is the only appointment she didn’t make!

21NQ Magazine May 2013

WOMEN IN ACCOUNTANCY

NQ

Making experience countIt is fair to say that Kirstin Baker is a career civil servant. She can also safely be described as an all-rounder, with probably one of the best CVs in central government.

Baker started her working life at the Foreign Office, liaising with the European Commission and specialising in competition policy. She has also worked in the European Secretariat in Cabinet Office, and gradually over time worked more on financial and economic issues.

Baker then decided she wanted to work at the Treasury and eventually got the chance to work on secondment on the 2004 Spending Review.

The most turbulent time in Baker’s career (to date) was when she became the Head of the Northern Rock Shareholding Team in 2008, just after it was nationalised. It was a time of real crisis and meant she was working late into the night and every weekend for quite some time.

Then she decided it was time to get an accountancy qualification – and in two short years was CIMA qualified. This is something she did off her own bat and being a qualified accountant had an immediate effect as it opened the door to her current role – she is the new Finance and Commercial Director at HM Treasury.

Sam’s the girlSam Smith is a unique woman – she is the only woman to run a stockbroker, finnCap. The KPMG trained accountant joined private client broker JM Finn straight after qualifying. That meant at the tender age of 23 she was thrown in at the deep end, putting clients with money together with companies needing funds.

Less than 10 years later she was leading the management buyout in 2007 to set up finnCap. The shy girl from West Sussex has some outspoken views about women and glass ceilings. Basically, she seems to think they are a myth, and that women are largely to blame for their own absence from an industry full of male egos. In the past she has endured ‘animal noises’ on the London Commodity Exchange, but her answer was to give them a quick remark back and ‘bang’ – you are on a level.

Smith believes a lot of women don’t have the confidence to get to the top of finance, and perhaps not the vision, either. For her quotas are not the answer. Instead, she believes that what needs to be created is a talent pool who want to knock down the City’s door. To this end she is heavily involved in mentoring projects and organisations aimed at helping to encourage more young women into business.

22 NQ Magazine May 2013

AUDITOR REPORTING

Katherine Bagshaw explains the changes in the pipeline for the audit report

Auditor reporting has always been a difficult issue. It doesn’t take a professional

accounting qualification to realise that there are a fair amount of soft numbers, judgements and guesses that go into a set of accounts. That, combined with human error, means that they are never going to be wholly ‘right’ or ‘wrong’. So the idea that auditors provide an opinion on the truth and fairness of financial statements (or on their ‘fair presentation’ if you come from the US) is well-understood, widely accepted and an exceptionally long-standing and tenacious notion. It is not

going away any time soon. But it has never been quite enough.

UK audit reports in 1985 were a few short lines giving what is now called the ‘binary’, or ‘pass/fail’ opinion. Over the last 25 years, they have become longer. Regulatory reform usually follows in the wake of a series of corporate collapses, and there have been many collapses and several rounds of reform. Regulators must regulate, and improving the audit report, always after extensive consultation, has resulted over the years in more and more paragraphs explaining what auditors have done, and what they have not

done. Requirements for auditors to report on corporate governance statements accelerated this process and audit reports for large listed entities are now complex. While all of this boilerplating probably has helped educate the investing public and reduce the expectations gap a little, the opinion is still the first and only thing many investors will look at.

Despite the fact that much of the report currently reads defensively, it is instructive to remember how much opposition there was to many changes that now look innocuous. Some considered that the mere mention of the word ‘fraud’ would result in more litigation, others thought that trying to explain an audit-a fairly complex and lengthy process – in a few lines in the audit report, was both pointless and likely to result in more misunderstandings, not less.

We are where we are and overall, investors remain unhappy. They do not want to lose the pass/fail opinion but they want more detail about the audit and the company, and they think auditors ought to provide it. In the USA, there is a Management Discussion and Analysis (MDA) for some entities and there were suggestions that auditors might produce an ‘Auditor Discussion and Analysis’. French and other European auditors have for many years published a report on issues that arose during the audit. These reports are not exemplary but they do prove that auditors in some parts of the world are able to say a great deal more than UK auditors do at present.

Investors do not really want to hear more from directors – they want to know what keeps auditors awake at night. They want to know what auditors think are the most significant risks, and they want to know what auditors did about them. But who says what is important and the arguments are convoluted: some assert that auditors cannot and should not provide any ‘new’ or ‘original’ information about a company. Original information is for directors to provide, auditors merely report on what directors have said. If auditors and directors do report on the same areas, what happens if they say different things about the same issue? This is exactly what some investors appear to want because they do not trust directors, but it seems that auditors are not wholly trusted either. Whose version are investors going to

Auditor reporting: Don’t be defensive

23NQ Magazine May 2013

AUDITOR REPORTING

believe? How are they going to resolve the issue?

There have been proposals for significant changes to auditor reporting before. Real-time reporting and narrative reporting have been discussed for at least a decade but it seems that there is now sufficient will and momentum for meaningful change to take place, and fairly soon. The Financial Reporting Council (FRC) issued an exposure draft in February 2013 proposing that auditors of entities reporting under the UK Corporate Governance Code entities should be required to:1 ◗ describe the risks which had the greatest effect on audit strategy with regard to the allocation of resources and audit effort; ◗ explain how materiality was applied, disclosing materiality and performance materiality levels; ◗ summarise the scope of the audit including the response to the matters above.

These proposals are based on the Autumn 2012 changes to FRC requirements for: ◗ auditors to communicate information about significant audit judgments to audit committees; ◗ audit committees to report on their activities to the board and boards to describe the work of the audit committee in the annual report; and◗ auditors to report if the board’s disclosures do not appropriately address the matters they have communicated.

Risks having the greatest effect on audit strategy would not necessarily be all of the ‘significant risks’ auditors identify but they are likely to be risks that have been communicated to the audit committee.

While it is inevitable that where nothing changes, auditors will report the same matters several years running, investors are concerned that auditors will copy each other across different entities, examples given in any guidance, and that disclosures will quickly be reduced to more boilerplate. Auditors are concerned about how regulators will approach any risk reported to the audit committee but not included in the audit report. There is a real risk that everything reported to the audit committee will be reported in the audit report, which is not the intention. The instinct of regulators, and indeed nervous auditors, is to encourage and include more rather than less as the safer option. Both will have to resist that tendency if the proposals are to work.

There are also concerns about the subtle behavioural aspects of the proposed requirements. If auditors are required to include in the audit report matters previously reported to the audit committee, rightly or wrongly, it is likely to make them think about what and how they report to the audit committee in the first place.

Similar proposals are being developed internationally by The International Auditing and Assurance Standards Board (IAASB).2 It is

suggesting that auditors of listed entities should be required to report key audit matters in the audit report, i.e. matters that were of ‘most significance’ in the audit of the financial statements. In all cases they will be a ‘selection of matters communicated with those charged with governance’.3

While IAASB’s proposed changes to external audit reporting requirements will be restricted to audits of listed entities, the effect of these changes on ISA 2604 will apply to all entities. Papers presented to recent IAASB meetings will require all auditors to discuss with those charged with governance: ◗ significant risks identified by the auditor and the auditor’s responses to them; and◗ significant transactions outside the entity’s normal course of business, or transactions that otherwise appear to be unusual, the auditor’s understanding of the business rationale for such transactions and the audit approach to them.

It seems very likely that these proposals will go ahead in some form both in the UK and internationally. The European Commission and The Public Company Accounting Oversight Board (PCAOB)5 in the USA have published similar proposals.

Audit reports for smaller entities should not be affected by these changes but it seems likely that the proposed broadened scope of what is reported to those charged with governance will affect smaller audits.

It remains to be seen what auditors report, how regulators react and whether investors are satisfied. But it will make audit reports more interesting, at least for a while.

The views expressed in this article are the author’s own.

NQ

1. For periods commencing on or after 1st October 2012 – i.e. for 2013 audits www.frc.org.uk/News-and-Events/FRC-Press/Press/2013/February/FRC-consults-on-proposals-to-improve-the-auditor’s.aspx 2. www.ifac.org/auditing-assurance/auditor-reporting-iaasbs-1-priority3. www.frc.org.uk/News-and-Events/FRC-Press/Press/2013/February/FRC-consults-on-proposals-to-improve-the-auditor’s.aspx4. ISA 260 Communication with Those Charged with Governance5. The US auditing standard-setter for listed entity audits

Katharine Bagshaw is a specialist in UK and international auditing standards. She qualified with Ernst & Young and has written and lectured for over twenty years on ISAs. For three years she acted as auditing examiner for the ACCA and she wrote some of the first UK training materials on ISAs in the mid-1990s. Since 2000 Katharine has worked for the ICAEW on ISA-related projects, now on a part-time basis. She managed ICAEW’s ISA implementation work when ISAs were introduced into the UK in 2005, and the move to clarified ISAs in 2010.

Katharine sits on IFAC’s SMP Committee.She is the author of numerous publications and webinars on ISAs, including Audit and Assurance Essentials for Professional Accountancy

Examinations, published in February 2013. www.amazon.co.uk/Katharine-Bagshaw/e/B0034NLG6C For a free sample chapter and table of contents just input this URL – http://goo.gl/h8463 or scan the QR code below using your smartphone.

examiner for the ACCA and

Katharine sits on IFAC’s SMP Committee.She is the author of numerous publications and webinars on ISAs, including Audit and Assurance Essentials for Professional Accountancy

Examinations, published in