Embed Size (px)

Citation preview

NEWS RELEASE November 6, 2013

ENDEAVOUR MINING ANNOUNCES POSITIVE FEASIBILITY STUDY FOR HOUNDÉ GOLD PROJECT IN BURKINA FASO

November 6, 2013 – Endeavour Mining Corporation (“Endeavour”) (TSX:EDV, ASX:EVR, OTCQX:EDVMF) announces the results of a positive NI 43-101 compliant Feasibility Study (“FS”) of its Houndé Gold Project, an open pit gold mine with an initial life of mine (“LOM”) of over 8 years. The FS will be presented to the government of Burkina Faso as part of the on-going permitting process.

(All amounts in US dollars unless otherwise indicated) Houndé FS Highlights, on a 100% basis, include:

Average annual production of 178,000 gold ozs per year over an 8.1 year LOM, with total LOM production of 1.44 million ozs.

An average gold recovery of 93.3% via a SAG/ball mill (SABC) grinding circuit followed by gravity/CIL plant capable of treating 3.0 million tonnes per annum (Mtpa) of ore (nameplate capacity: 9,000 tpd).

Owner operated open pit mining and Proven and Probable reserve of 25 million tonnes with an average grade of 1.95 g/t Au.

Initial start-up capital of $315 million (including working capital, import duties, and contingency). LOM sustaining capital of $62 million, and $26 million of rehabilitation and closure costs.

Forecast LOM direct cash cost of $636/oz (excluding royalties) and all-in sustaining cost of $775/oz (including royalties and rehabilitation and closure).

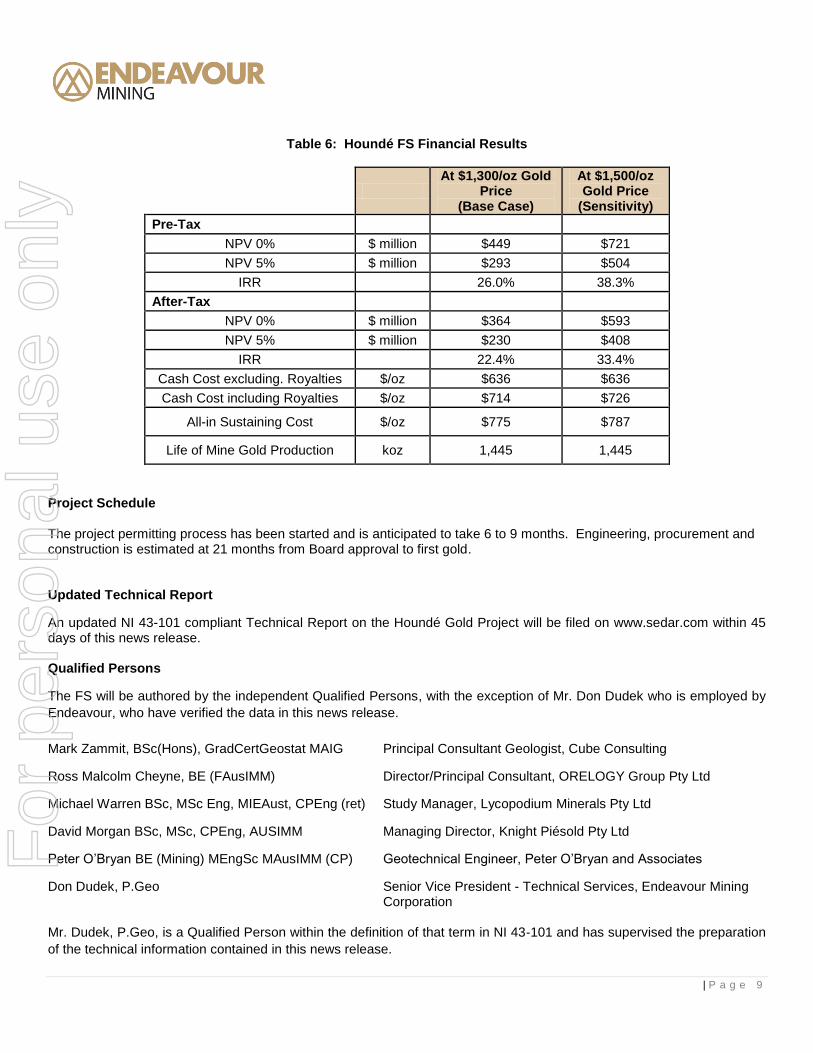

The project yields, on an after-tax basis:

At $1,300/oz Gold Price

(Base Case)

At $1,500/oz Gold Price

(Sensitivity)

NPV 0% $ million $364 $593

NPV 5% $ million $230 $408

IRR % 22.4% 33.4%

For additional information, contact:

Doug Reddy Senior Vice President – Business Development

+1 604 609 6114 [email protected]

UK/Europe: Bobby Morse Buchanan

+44 20 7466 5000 [email protected]

Endeavour Mining Corporation Regatta Office Park Windward 3, Suite 240, PO Box 1793 West Bay Road, Grand Cayman KY1-1109, Cayman Islands

Tel: +1 345 946 7603 Fax: +1 345 946 7604

www.endeavourmining.com

A Cayman Islands exempted company with limited liability.

ARBN 153 067 639

EDV EVR Toronto Stock Exchange

Australian Securities Exchange

For

per

sona

l use

onl

y

| P a g e 2

Neil Woodyer, CEO, stated

“Houndé is a strong gold project with potential to produce approximately 180,000 ozs per year at an all-in sustaining cost

of under $800 per ounce. At a $1,300 gold price, Houndé has an attractive after-tax IRR of 22% illustrating strong cash

flow generation. The project also benefits from excellent infrastructure, our current Agbaou mine building expertise, and

our Burkina Faso operating experience at Youga. While work continues on obtaining the Houndé mining permit, we are

evaluating how best to integrate Houndé into Endeavour’s production growth plans.”

Management Conference Calls – November 13 and 14, 2013 Endeavour’s Management previously scheduled two conference calls to discuss the Q3/2013 operating and financial

results on November 13 and 14, 2013. During these calls, Management will also discuss highlights from the Houndé FS.

Details for the conference calls can be found in a news release on November 4, 2013.

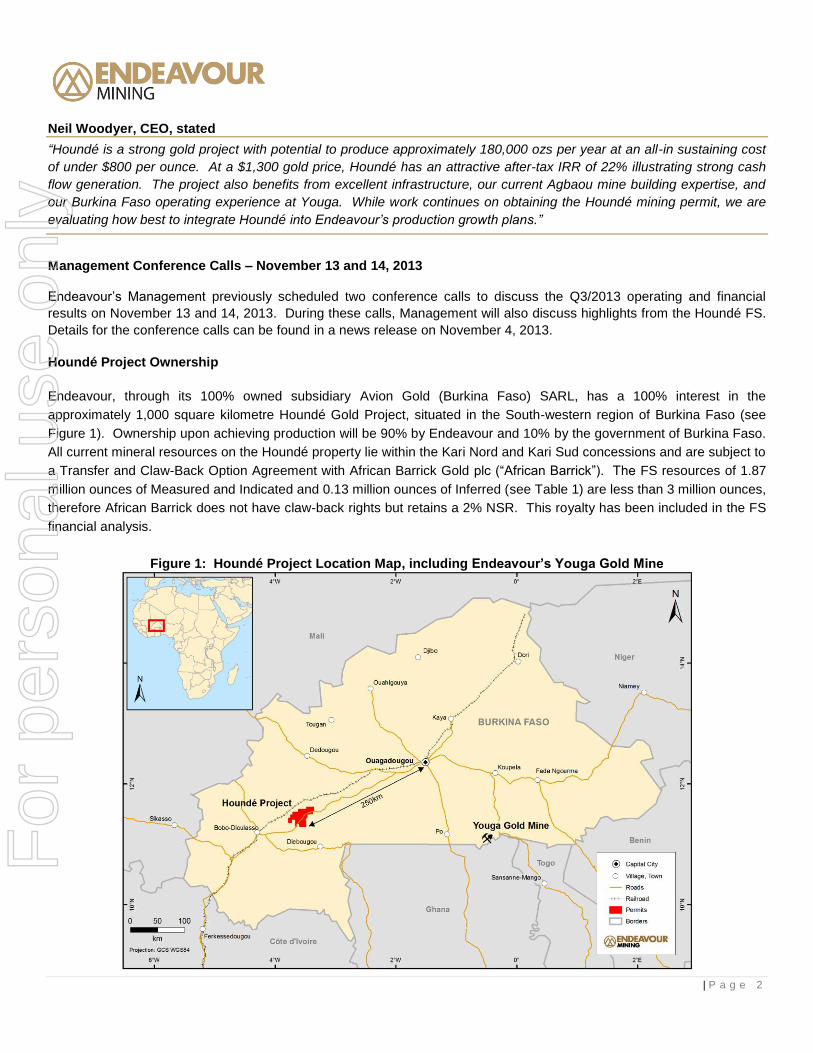

Houndé Project Ownership

Endeavour, through its 100% owned subsidiary Avion Gold (Burkina Faso) SARL, has a 100% interest in the

approximately 1,000 square kilometre Houndé Gold Project, situated in the South-western region of Burkina Faso (see

Figure 1). Ownership upon achieving production will be 90% by Endeavour and 10% by the government of Burkina Faso.

All current mineral resources on the Houndé property lie within the Kari Nord and Kari Sud concessions and are subject to

a Transfer and Claw-Back Option Agreement with African Barrick Gold plc (“African Barrick”). The FS resources of 1.87

million ounces of Measured and Indicated and 0.13 million ounces of Inferred (see Table 1) are less than 3 million ounces,

therefore African Barrick does not have claw-back rights but retains a 2% NSR. This royalty has been included in the FS

financial analysis.

Figure 1: Houndé Project Location Map, including Endeavour’s Youga Gold Mine

For

per

sona

l use

onl

y

| P a g e 3

Houndé FS Summary

The Houndé Project FS focuses on the Vindaloo group of deposits that are located approximately 250 km South-west of

Ouagadougou, the capital city of Burkina Faso. The deposits are approximately 2.7 km from a paved highway and as

close as 200 metres from a 225 kV power line that extends from Côte d’Ivoire through to Ouagadougou (see Figure 2).

The nearby town of Houndé has a population of approximately 22,000. A rail line that extends to the port of Abidjan, Côte

d’Ivoire lies approximately 25 km west of the deposit area.

Lycopodium Minerals Pty Ltd. was the FS study lead consultant with a focus on study coordination, metallurgy,

infrastructure design and process plant design. Cube Consulting completed an updated Mineral Resource estimate.

Knight Piésold Pty. Ltd. carried out pit and site geotechnical reviews, completed a water balance study and designed the

tailings storage facility, water harvest dam and the water storage dam along with mine site drainage control elements.

Orelogy Group Pty Ltd completed the mine plan and Mineral Reserve.

Mine environmental and social impact assessments (“ESIA”) were completed under the lead of Genivar Inc. with

SOCREGE and INGRID collecting social and environmental data, respectively. INGRID also completed an additional

environmental and social study on the project’s water supply. Knight Piésold provided high level oversight over all of these

studies.

Copies of the FS and ESIA will be presented to the government of Burkina Faso on November 7, 2013.

The Vindaloo zones are hosted by Proterozoic-age, Birimian Group, intensely sericite- and silica-altered mafic intrusions

and similarly-altered, strongly foliated and altered intermediate to mafic volcaniclastics and occasionally sediments. The

mineralization is often quartz stockwork-style and is weakly to moderately pyritic. The Vindaloo trend has been drill tested

for a distance of approximately 7.7 kilometres along strike and up to 350 metres depth. The intrusion-hosted zones range

up to 70 metres in true thickness and average close to 20 metres true thickness along a 1.2 km section of the zone called

Vindaloo Main. Volcanic- and sediment-hosted zones are generally less than 5 m wide. The entire mineralized package

strikes north-northeast and dips steeply to the west to vertical. The mineralization remains open both along strike and to

depth.

During Q4/2012 and Q1/2013, Endeavour completed 40,534 metres of drilling in 358 holes with a specific goal of

upgrading the Inferred in-pit Mineral Resources to Indicated Mineral Resources and some Indicated Mineral Resources to

Measured Mineral Resources. Endeavour’s drilling in conjunction with previous drilling comprise a drill database of 751

core and RC holes totalling 103,677 metres that supported the creation of an updated, in-pit Mineral Resources

statement, which is summarized in Table 1.

For

per

sona

l use

onl

y

| P a g e 4

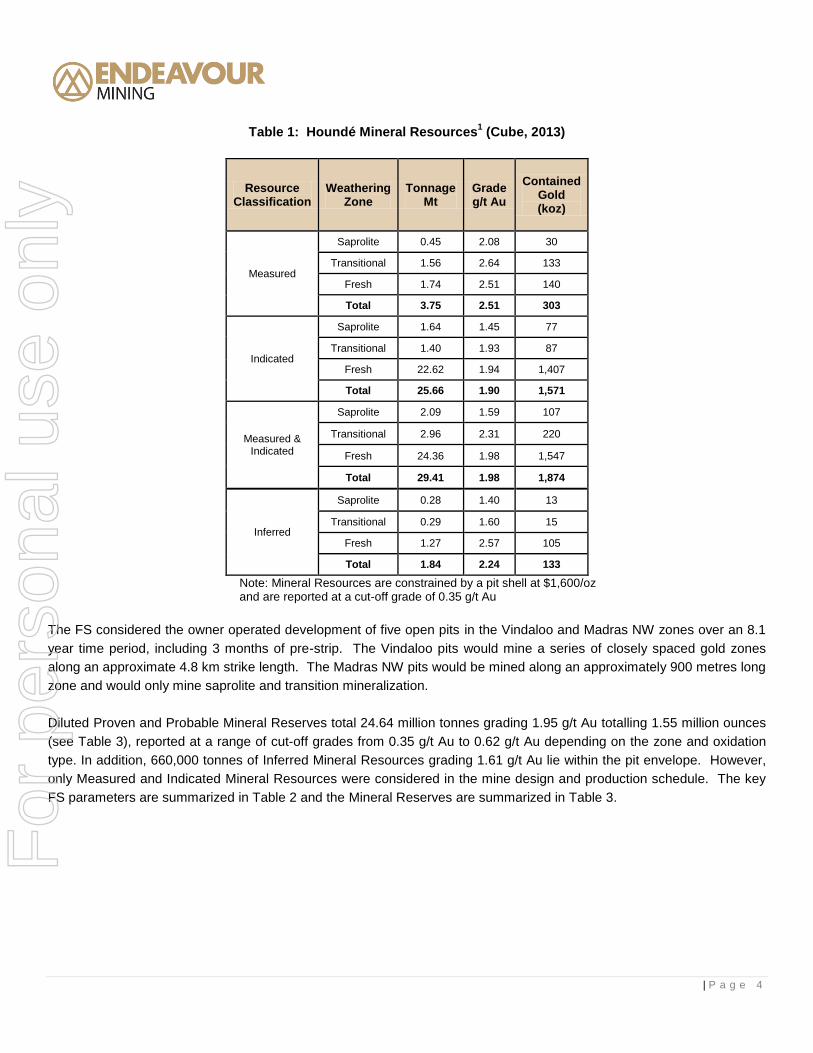

Table 1: Houndé Mineral Resources1 (Cube, 2013)

Resource Classification

Weathering Zone

Tonnage Mt

Grade g/t Au

Contained Gold (koz)

Measured

Saprolite 0.45 2.08 30

Transitional 1.56 2.64 133

Fresh 1.74 2.51 140

Total 3.75 2.51 303

Indicated

Saprolite 1.64 1.45 77

Transitional 1.40 1.93 87

Fresh 22.62 1.94 1,407

Total 25.66 1.90 1,571

Measured & Indicated

Saprolite 2.09 1.59 107

Transitional 2.96 2.31 220

Fresh 24.36 1.98 1,547

Total 29.41 1.98 1,874

Inferred

Saprolite 0.28 1.40 13

Transitional 0.29 1.60 15

Fresh 1.27 2.57 105

Total 1.84 2.24 133

Note: Mineral Resources are constrained by a pit shell at $1,600/oz and are reported at a cut-off grade of 0.35 g/t Au

The FS considered the owner operated development of five open pits in the Vindaloo and Madras NW zones over an 8.1

year time period, including 3 months of pre-strip. The Vindaloo pits would mine a series of closely spaced gold zones

along an approximate 4.8 km strike length. The Madras NW pits would be mined along an approximately 900 metres long

zone and would only mine saprolite and transition mineralization.

Diluted Proven and Probable Mineral Reserves total 24.64 million tonnes grading 1.95 g/t Au totalling 1.55 million ounces

(see Table 3), reported at a range of cut-off grades from 0.35 g/t Au to 0.62 g/t Au depending on the zone and oxidation

type. In addition, 660,000 tonnes of Inferred Mineral Resources grading 1.61 g/t Au lie within the pit envelope. However,

only Measured and Indicated Mineral Resources were considered in the mine design and production schedule. The key

FS parameters are summarized in Table 2 and the Mineral Reserves are summarized in Table 3.

For

per

sona

l use

onl

y

| P a g e 5

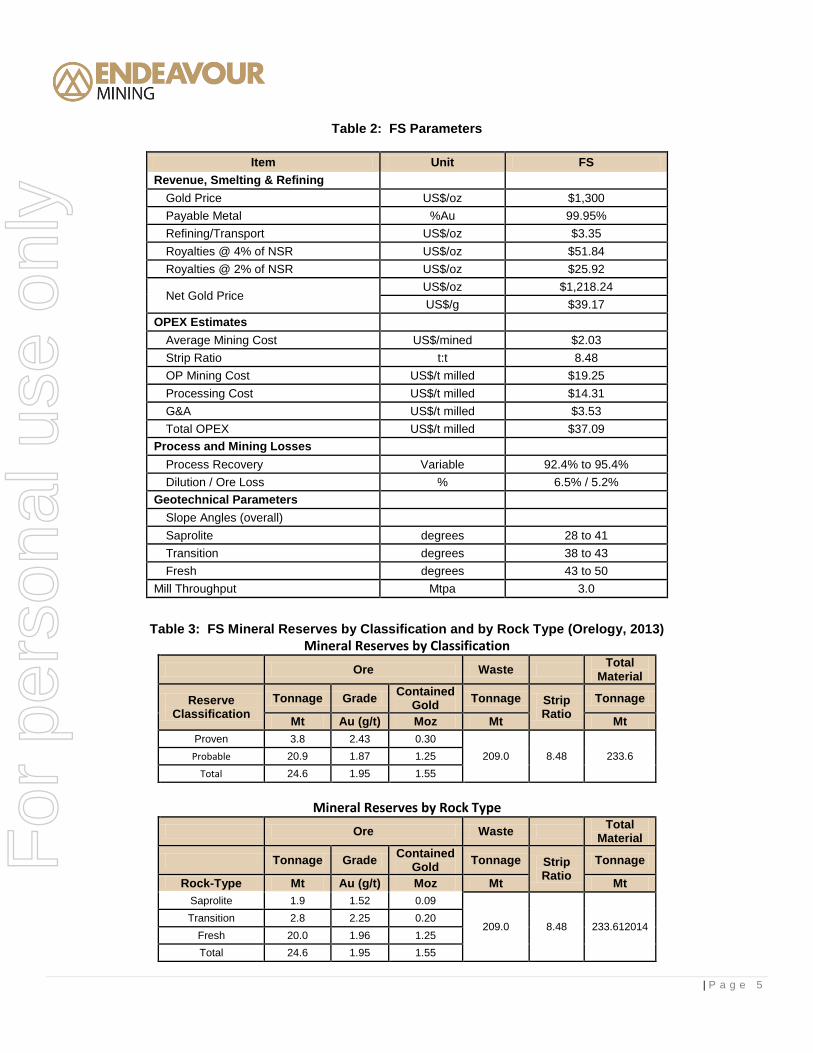

Table 2: FS Parameters

Item Unit FS

Revenue, Smelting & Refining

Gold Price US$/oz $1,300

Payable Metal %Au 99.95%

Refining/Transport US$/oz $3.35

Royalties @ 4% of NSR US$/oz $51.84

Royalties @ 2% of NSR US$/oz $25.92

Net Gold Price US$/oz $1,218.24

US$/g $39.17

OPEX Estimates

Average Mining Cost US$/mined $2.03

Strip Ratio t:t 8.48

OP Mining Cost US$/t milled $19.25

Processing Cost US$/t milled $14.31

G&A US$/t milled $3.53

Total OPEX US$/t milled $37.09

Process and Mining Losses

Process Recovery Variable 92.4% to 95.4%

Dilution / Ore Loss % 6.5% / 5.2%

Geotechnical Parameters

Slope Angles (overall)

Saprolite degrees 28 to 41

Transition degrees 38 to 43

Fresh degrees 43 to 50

Mill Throughput Mtpa 3.0

Table 3: FS Mineral Reserves by Classification and by Rock Type (Orelogy, 2013)

Mineral Reserves by Classification

Ore Waste Total

Material

Reserve Classification

Tonnage Grade Contained

Gold Tonnage Strip

Ratio

Tonnage

Mt Au (g/t) Moz Mt Mt

Proven 3.8 2.43 0.30

209.0 8.48 233.6 Probable 20.9 1.87 1.25

Total 24.6 1.95 1.55

Mineral Reserves by Rock Type

Ore Waste Total

Material

Tonnage Grade Contained

Gold Tonnage Strip

Ratio

Tonnage

Rock-Type Mt Au (g/t) Moz Mt Mt

Saprolite 1.9 1.52 0.09

209.0 8.48 233.612014 Transition 2.8 2.25 0.20

Fresh 20.0 1.96 1.25

Total 24.6 1.95 1.55

For

per

sona

l use

onl

y

| P a g e 6

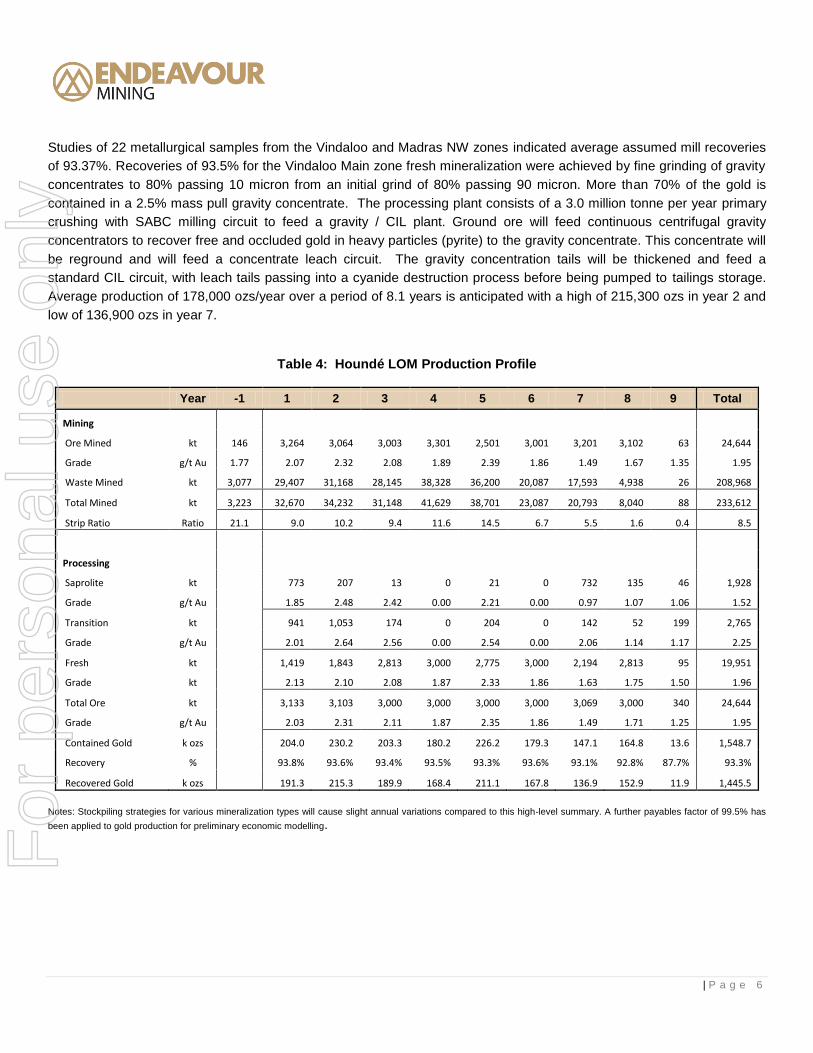

Studies of 22 metallurgical samples from the Vindaloo and Madras NW zones indicated average assumed mill recoveries

of 93.37%. Recoveries of 93.5% for the Vindaloo Main zone fresh mineralization were achieved by fine grinding of gravity

concentrates to 80% passing 10 micron from an initial grind of 80% passing 90 micron. More than 70% of the gold is

contained in a 2.5% mass pull gravity concentrate. The processing plant consists of a 3.0 million tonne per year primary

crushing with SABC milling circuit to feed a gravity / CIL plant. Ground ore will feed continuous centrifugal gravity

concentrators to recover free and occluded gold in heavy particles (pyrite) to the gravity concentrate. This concentrate will

be reground and will feed a concentrate leach circuit. The gravity concentration tails will be thickened and feed a

standard CIL circuit, with leach tails passing into a cyanide destruction process before being pumped to tailings storage.

Average production of 178,000 ozs/year over a period of 8.1 years is anticipated with a high of 215,300 ozs in year 2 and

low of 136,900 ozs in year 7.

Table 4: Houndé LOM Production Profile

Year -1 1 2 3 4 5 6 7 8 9 Total

Mining

Ore Mined kt 146 3,264 3,064 3,003 3,301 2,501 3,001 3,201 3,102 63 24,644

Grade g/t Au 1.77 2.07 2.32 2.08 1.89 2.39 1.86 1.49 1.67 1.35 1.95

Waste Mined kt 3,077 29,407 31,168 28,145 38,328 36,200 20,087 17,593 4,938 26 208,968

Total Mined kt 3,223 32,670 34,232 31,148 41,629 38,701 23,087 20,793 8,040 88 233,612

Strip Ratio Ratio 21.1 9.0 10.2 9.4 11.6 14.5 6.7 5.5 1.6 0.4 8.5

Processing

Saprolite kt 773 207 13 0 21 0 732 135 46 1,928

Grade g/t Au 1.85 2.48 2.42 0.00 2.21 0.00 0.97 1.07 1.06 1.52

Transition kt 941 1,053 174 0 204 0 142 52 199 2,765

Grade g/t Au 2.01 2.64 2.56 0.00 2.54 0.00 2.06 1.14 1.17 2.25

Fresh kt 1,419 1,843 2,813 3,000 2,775 3,000 2,194 2,813 95 19,951

Grade kt 2.13 2.10 2.08 1.87 2.33 1.86 1.63 1.75 1.50 1.96

Total Ore kt 3,133 3,103 3,000 3,000 3,000 3,000 3,069 3,000 340 24,644

Grade g/t Au 2.03 2.31 2.11 1.87 2.35 1.86 1.49 1.71 1.25 1.95

Contained Gold k ozs 204.0 230.2 203.3 180.2 226.2 179.3 147.1 164.8 13.6 1,548.7

Recovery % 93.8% 93.6% 93.4% 93.5% 93.3% 93.6% 93.1% 92.8% 87.7% 93.3%

Recovered Gold k ozs 191.3 215.3 189.9 168.4 211.1 167.8 136.9 152.9 11.9 1,445.5

Notes: Stockpiling strategies for various mineralization types will cause slight annual variations compared to this high-level summary. A further payables factor of 99.5% has

been applied to gold production for preliminary economic modelling.

For

per

sona

l use

onl

y

| P a g e 7

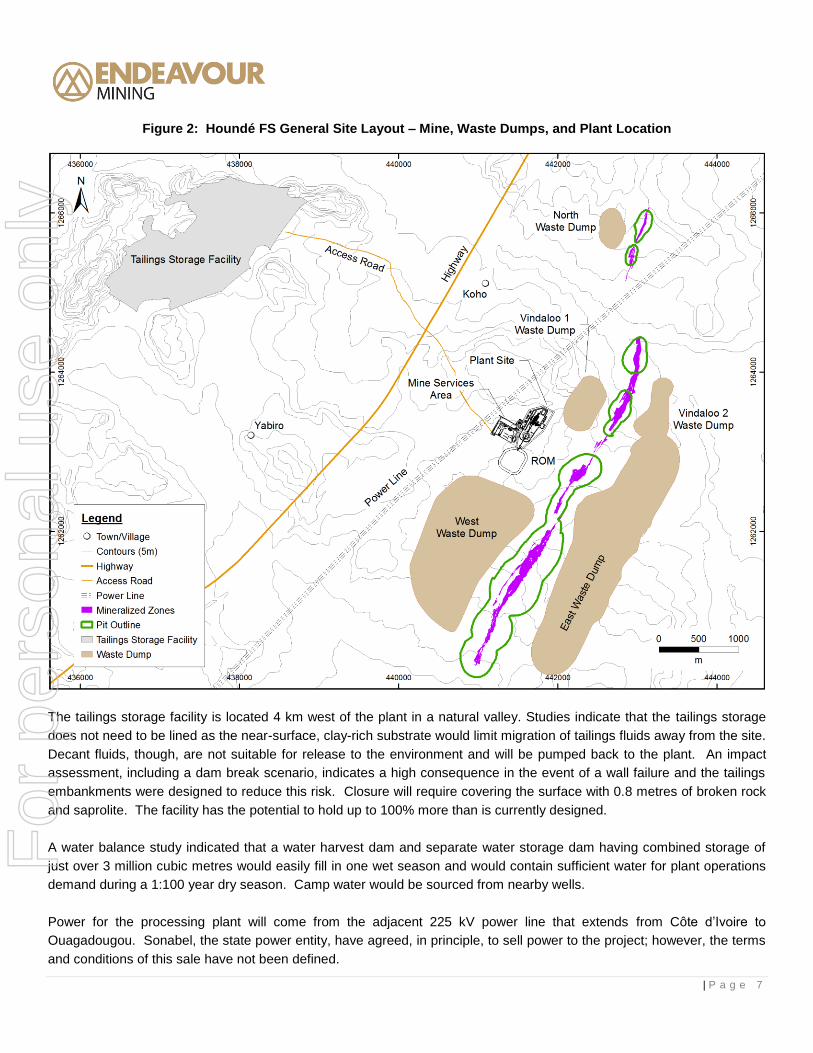

Figure 2: Houndé FS General Site Layout – Mine, Waste Dumps, and Plant Location

The tailings storage facility is located 4 km west of the plant in a natural valley. Studies indicate that the tailings storage

does not need to be lined as the near-surface, clay-rich substrate would limit migration of tailings fluids away from the site.

Decant fluids, though, are not suitable for release to the environment and will be pumped back to the plant. An impact

assessment, including a dam break scenario, indicates a high consequence in the event of a wall failure and the tailings

embankments were designed to reduce this risk. Closure will require covering the surface with 0.8 metres of broken rock

and saprolite. The facility has the potential to hold up to 100% more than is currently designed.

A water balance study indicated that a water harvest dam and separate water storage dam having combined storage of

just over 3 million cubic metres would easily fill in one wet season and would contain sufficient water for plant operations

demand during a 1:100 year dry season. Camp water would be sourced from nearby wells.

Power for the processing plant will come from the adjacent 225 kV power line that extends from Côte d’Ivoire to

Ouagadougou. Sonabel, the state power entity, have agreed, in principle, to sell power to the project; however, the terms

and conditions of this sale have not been defined.

For

per

sona

l use

onl

y

| P a g e 8

Project staff will include approximately 470 people, not including catering and cleaning staff and miscellaneous

contractors with 41 international and African expatriates and 430 Burkinabe employees. A camp to house 130 senior staff

will be installed with the remaining employees living in the nearby communities.

The ESIA, which has a goal of being IFC compliant, outlines Endeavour’s responsibilities to the well-being of the people

and the environment during the development, operation and closure of the Houndé gold project. The project will require

the acquisition of 2,096 ha of land. Several major land owners own the bulk of the land, however, numerous subsistence

farmers rent portions of the land from the land owners. Compensation mechanisms for the land, buildings, trees and crops

are part of the ongoing permitting process. Typical concerns, as a result of the project development include changes to

quality of life, loss of livelihood, environmental degradation, potential for jobs, potential health issues, increase in traffic

etc. Permitting is expected to take between six to nine months to complete.

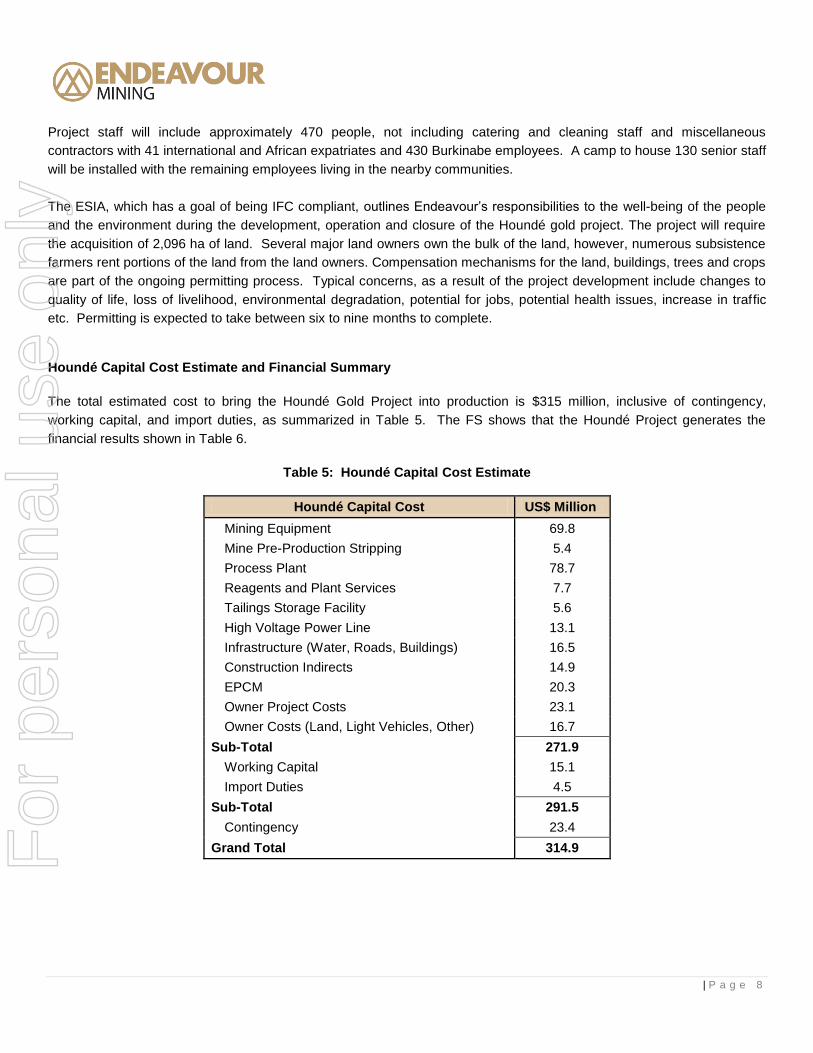

Houndé Capital Cost Estimate and Financial Summary

The total estimated cost to bring the Houndé Gold Project into production is $315 million, inclusive of contingency,

working capital, and import duties, as summarized in Table 5. The FS shows that the Houndé Project generates the

financial results shown in Table 6.

Table 5: Houndé Capital Cost Estimate

Houndé Capital Cost US$ Million

Mining Equipment 69.8

Mine Pre-Production Stripping 5.4

Process Plant 78.7

Reagents and Plant Services 7.7

Tailings Storage Facility 5.6

High Voltage Power Line 13.1

Infrastructure (Water, Roads, Buildings) 16.5

Construction Indirects 14.9

EPCM 20.3

Owner Project Costs 23.1

Owner Costs (Land, Light Vehicles, Other) 16.7

Sub-Total 271.9

Working Capital 15.1

Import Duties 4.5

Sub-Total 291.5

Contingency 23.4

Grand Total 314.9

For

per

sona

l use

onl

y

| P a g e 9

Table 6: Houndé FS Financial Results

At $1,300/oz Gold

Price (Base Case)

At $1,500/oz Gold Price

(Sensitivity)

Pre-Tax

NPV 0% $ million $449 $721

NPV 5% $ million $293 $504

IRR 26.0% 38.3%

After-Tax

NPV 0% $ million $364 $593

NPV 5% $ million $230 $408

IRR 22.4% 33.4%

Cash Cost excluding. Royalties $/oz $636 $636

Cash Cost including Royalties $/oz $714 $726

All-in Sustaining Cost $/oz $775 $787

Life of Mine Gold Production koz 1,445 1,445

Project Schedule The project permitting process has been started and is anticipated to take 6 to 9 months. Engineering, procurement and construction is estimated at 21 months from Board approval to first gold. Updated Technical Report

An updated NI 43-101 compliant Technical Report on the Houndé Gold Project will be filed on www.sedar.com within 45 days of this news release. Qualified Persons

The FS will be authored by the independent Qualified Persons, with the exception of Mr. Don Dudek who is employed by

Endeavour, who have verified the data in this news release.

Mark Zammit, BSc(Hons), GradCertGeostat MAIG Principal Consultant Geologist, Cube Consulting

Ross Malcolm Cheyne, BE (FAusIMM) Director/Principal Consultant, ORELOGY Group Pty Ltd

Michael Warren BSc, MSc Eng, MIEAust, CPEng (ret) Study Manager, Lycopodium Minerals Pty Ltd

David Morgan BSc, MSc, CPEng, AUSIMM Managing Director, Knight Piésold Pty Ltd

Peter O’Bryan BE (Mining) MEngSc MAusIMM (CP) Geotechnical Engineer, Peter O’Bryan and Associates

Don Dudek, P.Geo Senior Vice President - Technical Services, Endeavour Mining Corporation Mr. Dudek, P.Geo, is a Qualified Person within the definition of that term in NI 43-101 and has supervised the preparation

of the technical information contained in this news release.

For

per

sona

l use

onl

y

| P a g e 1 0

About Endeavour Mining Corporation

Endeavour is a gold producer delivering growth. Endeavour owns three gold mines producing more than 300,000 ounces

per year in Mali, Ghana and Burkina Faso. Endeavour’s annual gold production is forecast to exceed 400,000 ounces per

year during 2014, including the start-up of production at the Agbaou Gold Mine in Cote d’Ivoire scheduled for Q1 2014. In

addition, in November 2013 a Feasibility Study for the Houndé Project in Burkina Faso was completed showing potential

for approximately 180,000 ozs per year over 8 years.

Endeavour Mining Corporation is listed on the TSX (symbol EDV) and ASX (symbol EVR), and also trades on the OTCQX

(symbol EDVMF).

On behalf of Endeavour Mining Corporation

Neil Woodyer Chief Executive Officer

1Mineral resources which are not mineral reserves do not have demonstrated economic viability. The estimate of mineral resources may be materially

affected by environmental, permitting, legal, title, taxation, socio-political, marketing, or other relevant issues. The quantity and grade of reported Inferred resources in this estimation are uncertain in nature and there has been insufficient exploration to define these Inferred resources as an Indicated or Measured mineral resource and it is uncertain if further exploration will result in upgrading them to an Indicated or Measured mineral resource category.

This news release contains "forward-looking statements" including but not limited to, statements with respect to Endeavour's plans and operating performance, the estimation of mineral reserves and resources, the timing and amount of estimated future production, costs of future production, future capital expenditures, and the success of exploration activities. Generally, these forward-looking statements can be identified by the use of forward-looking terminology such as "expects", "expected", "budgeted", "forecasts" and "anticipates". Forward-looking statements, while based on management's best estimates and assumptions, are subject to risks and uncertainties that may cause actual results to be materially different from those expressed or implied by such forward-looking statements, including but not limited to: risks related to the successful integration of acquisitions; risks related to international operations; risks related to general economic conditions and credit availability, actual results of current exploration activities, unanticipated reclamation expenses; changes in project parameters as plans continue to be refined; fluctuations in prices of metals including gold; fluctuations in foreign currency exchange rates, increases in market prices of mining consumables, possible variations in ore reserves, grade or recovery rates; failure of plant, equipment or processes to operate as anticipated; accidents, labour disputes, title disputes, claims and limitations on insurance coverage and other risks of the mining industry; delays in the completion of development or construction activities, changes in national and local government regulation of mining operations, tax rules and regulations, and political and economic developments in countries in which Endeavour operates. Although Endeavour has attempted to identify important factors that could cause actual results to differ materially from those contained in forward-looking statements, there may be other factors that cause results not to be as anticipated, estimated or intended. There can be no assurance that such statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Accordingly, readers should not place undue reliance on forward-looking statements. Please refer to Endeavour's most recent Annual Information Form filed under its profile at www.sedar.com for further information respecting the risks affecting Endeavour and its business.

For

per

sona

l use

onl

y