Embed Size (px)

Citation preview

Worldwide news and intelligence for the chemical industry chemweek.com

IHS Chemical WeekWorldwide news and intelligence for the chemical industry chemweek.com

IHS Chemical WeekNovember 18/25, 2013 As Seen In

Shale brings petrochemical investment back to US

The US unconventional oil and gas supply surge is moving downstream as investments ramp up, providing a boon for US chemical makers. The margin benefit is already being felt. The supply impact is modest today but will accelerate as projects come onstream the next few years.

Shale sparks US petchem renaissance

chemweek.com IHS Chemical Week, November 18/25, 2013 |

Cheap energy and feedstocks have quickly reset the competitive balance for US petrochemical makers. With natural gas

available at a fraction of the cost of its oil equiv-alent, the United States is again one of the world’s lowest-cost petrochemical producers.

“Manufacturers can make ethylene in the United States for less than half of what it costs in Europe, Asia, and Latin America,” says Ste-phen Pryor, president of ExxonMobil Chemical. The advantage has reversed the fortunes of US chemical makers, he says.

Although petrochemicals, particularly ethane-based ethylene and its derivatives, are some of the strongest beneficiaries, the impact will be felt across the US economy. The impact of unconventional energy, in the form of new supplies of shale oil and gas, is expected to add 2.0–3.2%/year to US GDP through 2025, ac-

cording to a study from IHS. The rate of GDP in-crease builds rapidly and peaks at 3.2% in 2016. In the context of a $13–15-trillion US economy, this 2016 peak equates to an increase in GDP of $500–600 billion, IHS estimates.

While the GDP growth rates and capital in-vestment peak early, gains in chemical produc-tion and broader industrial production will con-tinue unabated through the forecast period.

By 2015, lower natural gas prices and higher activity will lift industrial production by 2.8%. By 2025, industrial production will be 3.9% higher, according to IHS. Chemicals will out-perform thanks to their energy intensity and use of natural gas feedstocks. IHS estimates that unconventional energy lifted organic chemical production by 1.5% in 2012. That figure ramps up to 4.9% in 2015, 7.1% in 2020, and 9.5% in 2025. The figures for resins are 1.7% in 2012,

4.4% in 2015, 7.1% in 2020, and 8.1% in 2025.A massive wave of new petrochemical

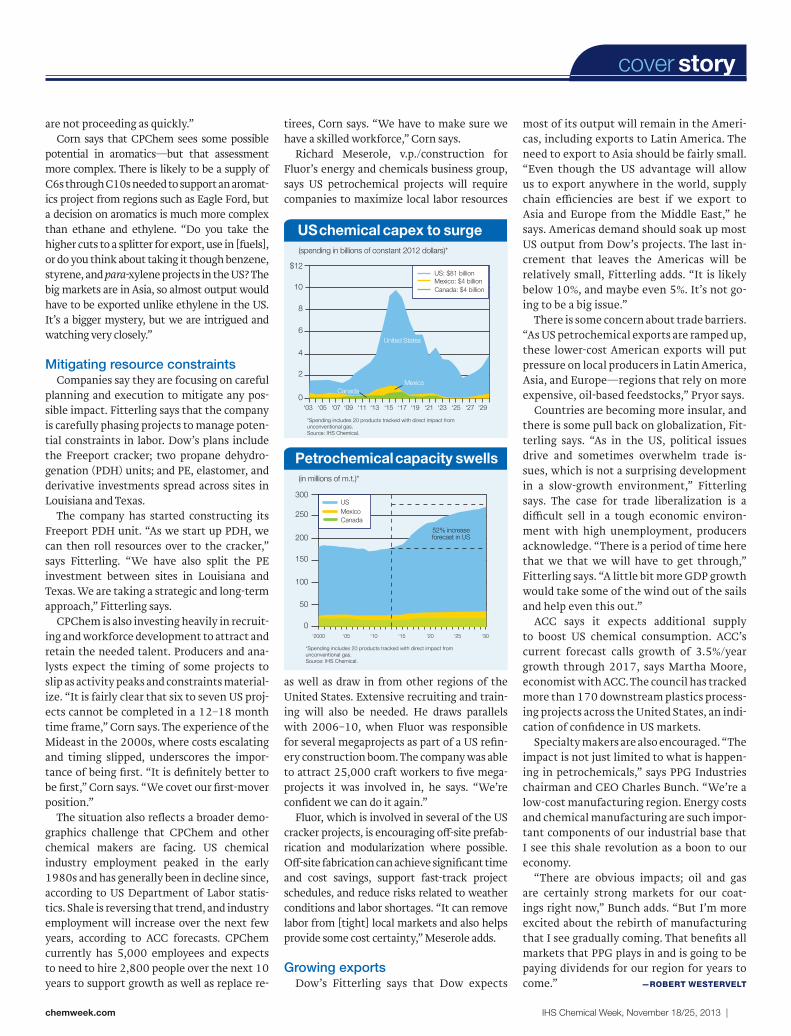

capacity—with investment exceeding more than $100 billion—will support this growth. “Chemicals investment activity is expected to peak in 2017 and will represent one of the larg-est expansions to ever occur in North America,” says Russell Heinen, senior director/chemical technology and analytics at IHS Chemical. Di-rect petrochemical investment between 2013 and 2030 for a group of 20 products impacted by shale will total $123 billion, Heinen says. The figure in constant 2012 dollars is roughly $90 billion. US spending peaks near $10 billion in 2017. Ethylene investment alone accounts for 34% of the spending over the period.

While the US has not added a cracker since 2000, industry has continued to build else-where. Between 2008 and 2013, global ethyl-

cover story

| IHS Chemical Week, November 18/25, 2013 chemweek.com

cover story

ene capacity increased by about 25 million m.t./year, mostly in the Mideast and Asia, bringing the total to 154 million m.t./year. For 2013–18, IHS Chemical projects another 37 million m.t./year of ethylene production capacity will be installed. “There’s continued growth in the Middle East, although not at the same rate as in the past,” Nick Vafiadis, senior director/global polyolefins and plastics at IHS Chemical says. “If you look at Asia, we’re seeing more and more of that capacity being skewed toward the coal-to-olefins technology. But the big change here is the return of North America to the scene.”

Total US capacity added because of shale is close to 100 million m.t. for the 20 products tracked, Heinen says. The likely peak, now estimated in 2018, is 18 million m.t. of additional capacity, far exceeding the previous peak in North America, Heinen says.

Upstream and midstream invest-ments are also surging, so feedstock supply should not be a constraint, with US natural gas liquids (NGLs) supply set to double by 2020. Since 2008, US NGLs produc-tion from natural gas processing has increased by over 500,000 bbl/day, reaching about 1.8 million bbl/day, according to IHS. “Because of the ongoing development of shale gas and tight oil resources, US NGL production is ex-pected to continue expanding rapidly over the next decade,” IHS says. “By 2020, total unconventional NGL production from natural gas processing is expected to reach about 3.8 million bbl/day, which represents an increase of 100% over current levels.”

Shale has created an abundance of indus-try’s principal feedstocks in the United States and has quickly reset competitiveness, Pryor says. “Just five years ago, the United States was losing ground in the export market. The country was on the verge of becoming a net importer of chemicals. But today, chemicals are once again America’s single biggest ex-port—larger than agriculture, automobiles, and aerospace.”

ExxonMobil Chemical has announced plans to build a 1.5-million m.t./year cracker at its Baytown, TX, site and two 650,000-m.t./year polyethylene (PE) plants. “We’re confident in positive permit decisions and expect con-struction to begin 2014, with target comple-tion late 2016,” Pryor says.

There are now nine announced crackers in the United States, with several more under consid-eration (p. 23). The trend is now undeniable, but the idea just started to form in the second-half of

2010. “It was over three years ago that we start-ed to get a sense that this was real,” says James Fitterling, executive v.p./feedstocks and perfor-mance plastics for Dow Chemical. “At that time, there was enough information to know that gas would be available [from Marcellus and on the US Gulf Coast], and people were starting to talk about activating pipelines.” Since those initial considerations, and Dow’s announcement of a planned cracker in April 2011, other shale pro-

duction areas such as Bakken in North Dakota and rest of the “liquids fairway” down the US Rocky Mountains through Eagle Ford in south Texas proven more productive than expected.

“The US sits today with a propane export terminal in operation, gas prices have dropped below $4/million Btu, and ethane is in com-plete rejection,” Fitterling says. “You add all of those dynamics together and it is clear that this real,” Fitterling says. “We are very con-fident in these investments and it is all sys-tems go.” The company expects to secure final permitting in first-half 2014 for a planned 1.5-million m.t./year Freeport, TX cracker and meet an expected first-half 2017 start up. “Everything looks like it is falling right in line,” he adds.

Ron Corn, currently v.p./corporate plan-ning and development for Chevron Phillips Chemical (CPChem), says company officials started “noodling around with the idea” of a US cracker in July 2010.

Since 2000, CPChem’s spending had been focused on the Mideast, where the company built three major projects. The final proj-ect came online in early 2013. As planning started to wind down on Mideast projects in 2008–09, Corn says CPChem looked around the world for the next big project. “We looked at the Middle East, South America, and Asia, but we didn’t come up with any-thing that fully met our standards,” Corn says. “We kept looking, however, and, lo and behold, one of the best opportunities was

right in our back yard.” CPChem and the US chemical industry had

been hit hard by the 2008–09 recession, and the company had idled some capacity, includ-ing a smaller ethylene unit at Sweeny, TX. Hurricanes in 2008 and 2009 were also se-verely harmful and set the United States back. By summer 2010, however, it was clear that fortunes were shifting in the United States even though industry was still coping with

the impacts of the recession. US ethane-based capacity was

competitive again, and the com-pany decided to restart an eth-ylene plant at Sweeny that had been idled. “It had a pretty siz-able advantage even though it was our highest-cost and small-est cracker,” Corn says. “We started thinking, ‘Maybe this is the next place to build.’” Corn notes that ethane was 70–80 cts/gal, well above the mid-20-ct range today. “The scale of the

advantage wasn’t yet obvious from a pricing standpoint,” Corn says. “You could see what was coming, however, because of what US midstream activity was starting to look like. Sooner or later, it would affect NGLs’” supply and pricing in a more substantial way. CPChem also notes activity in its own midstream busi-ness, including a pipeline that gathers and col-lects NGLs in western Texas and New Mexico. “In 2005 and 2006, we had trouble keeping it full,” Corn says. “By 2009, it was full.”

The decision to build a cracker now looks so simple, but it was pretty radical at the time given the turmoil industry had just been through, Corn says. “One of the questions I asked my boss [in 2010] was, ‘Do you think we’ll get fired if we suggest this?’” The pro-posed cracker project received strong immedi-ate support all the way to the CPChem board.

Corn says it is difficult to assess just how long the United States will be advantaged, but it the advantage is likely to be durable. “Many have been humbled trying to predict the future in energy,” Corn says. “If you look at current trends and hydrocarbon potential, however, you have to be encouraged.”

The United States likely has a long runway on shale development, he adds. “Develop-ment of competing resources is not advancing as rapidly,” Corn says. “There is a variety of reasons for that, including issues around land rights, water availability, and trickier geology. But, even in some high-profile areas, such as Poland and China, shale exploration efforts

PRYOR: US production costs very competitive.

FITTERLING: Confident in US advantage.

CORN: Started reevaluating US prospects in 2010.

tirees, Corn says. “We have to make sure we have a skilled workforce,” Corn says.

Richard Meserole, v.p./construction for Fluor’s energy and chemicals business group, says US petrochemical projects will require companies to maximize local labor resources

as well as draw in from other regions of the United States. Extensive recruiting and train-ing will also be needed. He draws parallels with 2006–10, when Fluor was responsible for several megaprojects as part of a US refin-ery construction boom. The company was able to attract 25,000 craft workers to five mega-projects it was involved in, he says. “We’re confident we can do it again.”

Fluor, which is involved in several of the US cracker projects, is encouraging off-site prefab-rication and modularization where possible. Off-site fabrication can achieve significant time and cost savings, support fast-track project schedules, and reduce risks related to weather conditions and labor shortages. “It can remove labor from [tight] local markets and also helps provide some cost certainty,” Meserole adds.

Growing exportsDow’s Fitterling says that Dow expects

chemweek.com IHS Chemical Week, November 18/25, 2013 |

are not proceeding as quickly.” Corn says that CPChem sees some possible

potential in aromatics—but that assessment more complex. There is likely to be a supply of C6s through C10s needed to support an aromat-ics project from regions such as Eagle Ford, but a decision on aromatics is much more complex than ethane and ethylene. “Do you take the higher cuts to a splitter for export, use in [fuels], or do you think about taking it though benzene, styrene, and para-xylene projects in the US? The big markets are in Asia, so almost output would have to be exported unlike ethylene in the US. It’s a bigger mystery, but we are intrigued and watching very closely.”

Mitigating resource constraintsCompanies say they are focusing on careful

planning and execution to mitigate any pos-sible impact. Fitterling says that the company is carefully phasing projects to manage poten-tial constraints in labor. Dow’s plans include the Freeport cracker; two propane dehydro-genation (PDH) units; and PE, elastomer, and derivative investments spread across sites in Louisiana and Texas.

The company has started constructing its Freeport PDH unit. “As we start up PDH, we can then roll resources over to the cracker,” says Fitterling. “We have also split the PE investment between sites in Louisiana and Texas. We are taking a strategic and long-term approach,” Fitterling says.

CPChem is also investing heavily in recruit-ing and workforce development to attract and retain the needed talent. Producers and ana-lysts expect the timing of some projects to slip as activity peaks and constraints material-ize. “It is fairly clear that six to seven US proj-ects cannot be completed in a 12–18 month time frame,” Corn says. The experience of the Mideast in the 2000s, where costs escalating and timing slipped, underscores the impor-tance of being first. “It is definitely better to be first,” Corn says. “We covet our first-mover position.”

The situation also reflects a broader demo-graphics challenge that CPChem and other chemical makers are facing. US chemical industry employment peaked in the early 1980s and has generally been in decline since, according to US Department of Labor statis-tics. Shale is reversing that trend, and industry employment will increase over the next few years, according to ACC forecasts. CPChem currently has 5,000 employees and expects to need to hire 2,800 people over the next 10 years to support growth as well as replace re-

most of its output will remain in the Ameri-cas, including exports to Latin America. The need to export to Asia should be fairly small. “Even though the US advantage will allow us to export anywhere in the world, supply chain efficiencies are best if we export to Asia and Europe from the Middle East,” he says. Americas demand should soak up most US output from Dow’s projects. The last in-crement that leaves the Americas will be relatively small, Fitterling adds. “It is likely below 10%, and maybe even 5%. It’s not go-ing to be a big issue.”

There is some concern about trade barriers. “As US petrochemical exports are ramped up, these lower-cost American exports will put pressure on local producers in Latin America, Asia, and Europe—regions that rely on more expensive, oil-based feedstocks,” Pryor says.

Countries are becoming more insular, and there is some pull back on globalization, Fit-terling says. “As in the US, political issues drive and sometimes overwhelm trade is-sues, which is not a surprising development in a slow-growth environment,” Fitterling says. The case for trade liberalization is a difficult sell in a tough economic environ-ment with high unemployment, producers acknowledge. “There is a period of time here that we that we will have to get through,” Fitterling says. “A little bit more GDP growth would take some of the wind out of the sails and help even this out.”

ACC says it expects additional supply to boost US chemical consumption. ACC’s current forecast calls growth of 3.5%/year growth through 2017, says Martha Moore, economist with ACC. The council has tracked more than 170 downstream plastics process-ing projects across the United States, an indi-cation of confidence in US markets.

Specialty makers are also encouraged. “The impact is not just limited to what is happen-ing in petrochemicals,” says PPG Industries chairman and CEO Charles Bunch. “We’re a low-cost manufacturing region. Energy costs and chemical manufacturing are such impor-tant components of our industrial base that I see this shale revolution as a boon to our economy.

“There are obvious impacts; oil and gas are certainly strong markets for our coat-ings right now,” Bunch adds. “But I’m more excited about the rebirth of manufacturing that I see gradually coming. That benefits all markets that PPG plays in and is going to be paying dividends for our region for years to come.” —RObERT WEsTERvELT

cover story

*Spending includes 20 products tracked with direct impact from unconventional gas. Source: IHS Chemical.

US chemical capex to surge

$12

10

8

6

4

2

0‘03 ‘05 ‘07 ‘09 ‘11 ‘13 ‘15 ‘17 ‘19 ‘21 ‘23 ‘25 ‘27 ‘29

(spending in billions of constant 2012 dollars)*

United States

CanadaMexico

US: $81 billionMexico: $4 billionCanada: $4 billion

US MexicoCanada

*Spending includes 20 products tracked with direct impact from unconventional gas. Source: IHS Chemical.

Petrochemical capacity swells

300

250

200

150

100

50

0‘05‘2000 ‘10 ‘15 ‘20

52% increaseforecast in US

‘25 ‘30

(in millions of m.t.)*

For the first decade of this century, it was easy to say how many ethylene projects were under development in North Amer-

ica because there were none. Now, however, it is easy to lose track. The number could change at any moment, as the recent announcement by Odebrecht shows.

On 14 November, the Brazilian engineer-ing and construction firm said that it may build an ethane cracker and three polyethyl-ene (PE) plants in West Virginia, a project the company calls the Appalachian Shale Cracker Enterprise, or Ascent. Odebrecht would op-erate the utilities, while its affiliate Braskem would manage production and sales. At CW press time, Hanhwa Chemical confirmed that it plans to participate in a US cracker. Hanwha Chemical brings to ten the number of an-nounced cracker projects in North America. Several others are under consideration.

Behind this surge in capacity is, of course, the shale gas revolution. With ethane prices in North America at historic lows, margins for ethane crackers have risen to record highs, notes Nick Vafiadis, senior director/global polyolefins and plastics at IHS Chemi-cal. “Right now, if you’re using ethane, it costs about 12–13 cents/lb to make a pound of eth-ylene—very, very low,” Vafiadis says. Only the Mideast has lower costs.

With so many new ethane crackers com-ing online, the cost of production in North America will increase considerably, but the region’s advantage over Asia and Eu-rope will remain significant and sus-tainable, says Vafiadis (graph).

The project slateIronically, cheap feedstock will be

a windfall for North America’s first new ethylene plant, Braskem Idesa’s Etileno XXI. The $3.2-billion proj-ect, which includes a 1.05-million m.t./year ethane cracker and three PE plants, was approved in 2008, be-fore the shale gale struck. Construc-tion began at Coatzacoalcos in 2012. Braskem says the project is about 50% com-plete, with production to begin in 2015.

Other projects have not yet broken ground. Chevron Phillips Chemical (CPChem) is

well along, having received its greenhouse gas permit from EPA in January and air permits

chemweek.com IHS Chemical Week, November 18/25, 2013 |

New North American crackers come online beginning in 2015

ethylene capacity—aim to start up in 2017.Dow Chemical was another early mover, in

April 2011 presenting plans for a 1.5-million m.t./year ethane cracker as part of its $4-bil-lion US Gulf Coast investment plan. Both the cracker and a propane dehydrogenation (PDH) unit are to be built at Freeport, TX. Dow says it is in the final stages of permitting and expects to begin construction in the second quarter of 2014. Fluor is managing construction.

In February 2012, Formosa Plastics com-mitted to a $2-billion project for Point Comfort, TX, that includes a roughly 1.2-million m.t./year ethane cracker, a PDH plant and a low-density PE plant. Permit-ting is still in process with both TCEQ and EPA, says a spokesperson. The company hopes to begin construction in late 2014, and to begin operations in early 2017.

OxyChem and Mexichem (Tlalnepantla, Mexico) began studying a 550,000-m.t./year cracker project in early 2012. On 31 October, they announced a 50-50 jv, Ingle-side Ethylene, to build the plant at Oxy-Chem’s Ingleside, TX, facility. OxyChem has completed front-end engineering and design (FEED), received draft permits from TCEQ, and applied for permits from EPA. The com-pany expects to award EPC by year’s end, with construction to begin in mid-2014 and operations in the first quarter of 2017. Oxy-Chem will run the cracker, and Mexichem will use the product to make vinyl chloride monomer at existing facilities.

Sasol is in the FEED stage of a $5–7-bil-lion cracker project that will be built at Lake Charles, LA. The 1.5-million m.t./year ethyl-ene plant will be part of a mammoth $16–21

billion investment that includes not only the downstream production of ethylene oxide, alcohols, ethoxylates, octene, hexene, and PE, but also a world-scale gas-to-li quids facility.

All of these crackers are destined for the US Gulf Coast, but the produc-tivity of the Marcellus Shale region in the Northeast has created unusual opportunities for investment. The Odebrecht project, set squarely atop the Marcellus Shale, is one example, but it follows in the footsteps of Shell’s proj-ect, a 1.5-million m.t./year cracker and

three 500,000-m.t./year PE units announced in 2011. Shell has chosen a site at Monaca, PA, and begun taking bids for ethane supply. The com-pany has hired a Linde-Bechtel alliance for FEED, which is expected to begin in early 2014.

—CLAY bOsWELL

cover story

from TCEQ in August. The project includes a 1.5-million m.t./year ethane cracker at its Cedar Bayou facility, at Baytown, TX, and two 500,000-m.t./year PE units at Old Ocean, TX. CPChem committed financing in October. In July, the company hired a joint venture be-tween JGC and Fluor to handle the engineer-ing, procurement, and construction (EPC) of

the ethane cracker, and, in September, CP-Chem hired Gulf Coast Partners, a partner-ship between Technip and Zachry Industrial, to manage EPC for the PE facilities.

ExxonMobil aims to build a 1.5-million m.t./year ethane cracker in Baytown that will feed two new 650,000-m.t./year PE lines at its nearby Mont Belvieu Plastics Plant. The

company filed for permits from EPA and TCEQ in May 2012 and hopes for a positive decision by early 2014. Assuming all goes well, the company will begin construction in 2014 and start the plant up in 2016.

Six projects—6.25 million m.t./year of

Source: IHS Chemical.

North America’s advantage

Jan.2000

Jan.‘01

Jan.‘02

Jan.‘03

Jan.‘04

Jan.‘05

Jan.‘06

Jan.‘07

Jan.‘08

Jan.‘09

Jan.‘10

Jan.‘11

Jan.‘12

Jan.‘13

Jan.‘14

Jan.‘15

Jan.‘16

(Ethylene cash cost, in $/m.t.)

0

200

400

600

800

1,000

1,200

1,400

$1,600

US Gulf Coast - purity ethaneSoutheast Asia - naphthaWestern Europe - naphtha

New cracker projects in North Americain thousands of m.t./year

CompANy LoCATIoN CApACITy oNSTreAm

Braskem Idesa Coatzacoalcos 1,050 2015

CpChem Baytown, TX 1,500 2017

Dow Chemical Freeport, TX 1,500 2017

exxonmobil Chemical Baytown, TX 1,500 2016

Formosa plastics point Comfort, TX 1,200 H1 2017

odebrecht/Braskem parkersburg, WV 1,500 NA

oxyChem/mexichem Ingleside, TX 550 Q1 2017

Sasol Lake Charles, LA 1,500 2017

Shell Chemicals monaca, pA 1,500 NA

NA: not announced Source: Companies, Chemical Week