Embed Size (px)

Citation preview

Technical University Hamburg-HarburgInstitute of Marketing and InnovationProf. Dr. Christian LüthjeProject Seminar IIWinter Semester 2010/11

Novel-Lemonade

Market analysis for organic lemonades and recommendations for the

market launch of a B12 enriched organic lemonade

Authors:

Martin Brücher

Date:

27.01.2011

Executive Summary

This report presents the key findings and outcomes from the Innovation Marketing

project; which aims at the analysis and determination of the market potential for the

Novel-Lemonade, an innovative drink developed by Benjamin Bürgel. This report also

intends to provide useful recommendations for a successful market entrance

strategy.

To achieve the project goals, a situation analysis was executed gaining insights in

the market, competition, and customers. Furthermore, the market analysis indicates

high market growth of 35% for the organic lemonade segment, which also

corresponds to rising consumption trends towards health and sustainability. The

organic lemonade market is, in addition, highly competitive; consisting on the

dominant players and a number of small start-up companies. Following the latter, the

competition is given mainly amongst direct competitors such as Bionade and Now,

but also between wider competitors like Aloha and Vitamalz.

Compared to its competitors, the novel lemonade has a high competency in its

healthy benefits. Hence, the main target customers are health and sustainability

conscious consumers aged above 25, who demand quality and pleasure, and are

willing to pay more for premium products.

The blind tasting study serves to determine the lemonade’s strengths and weakness

with regards to customer expectation and satisfaction of the taste and smell. The

results show various areas of improvement; including the strong malty smell and the

sweet and unbalanced taste.

The section concerning the marketing mix provides essential recommendations for its

components, namely product, place, price, and promotion; based on the key findings

of the situation analysis. Healthiness and indulgence are suggested to be the key

positioning factors for the product itself and its branding. Increasing the fruitiness and

reducing the malty taste can improve the flavor. For cost efficiency reasons, standard

reusable glass bottles and standard labels should be used.

Cooperation with the “Verband korrekter Getränkehersteller e.V.” and its distribution

network helps placing the product; the same as to have the contracted brewery

located in the middle of Germany and, to start the actual sales in Hamburg. The

benchmarking analysis against the established competitors and a calculation of the

estimated pricing structure set the recommended retail price at 0.79€ for a 0.33L

bottle and at 0.99€ for a 0.5L bottle.

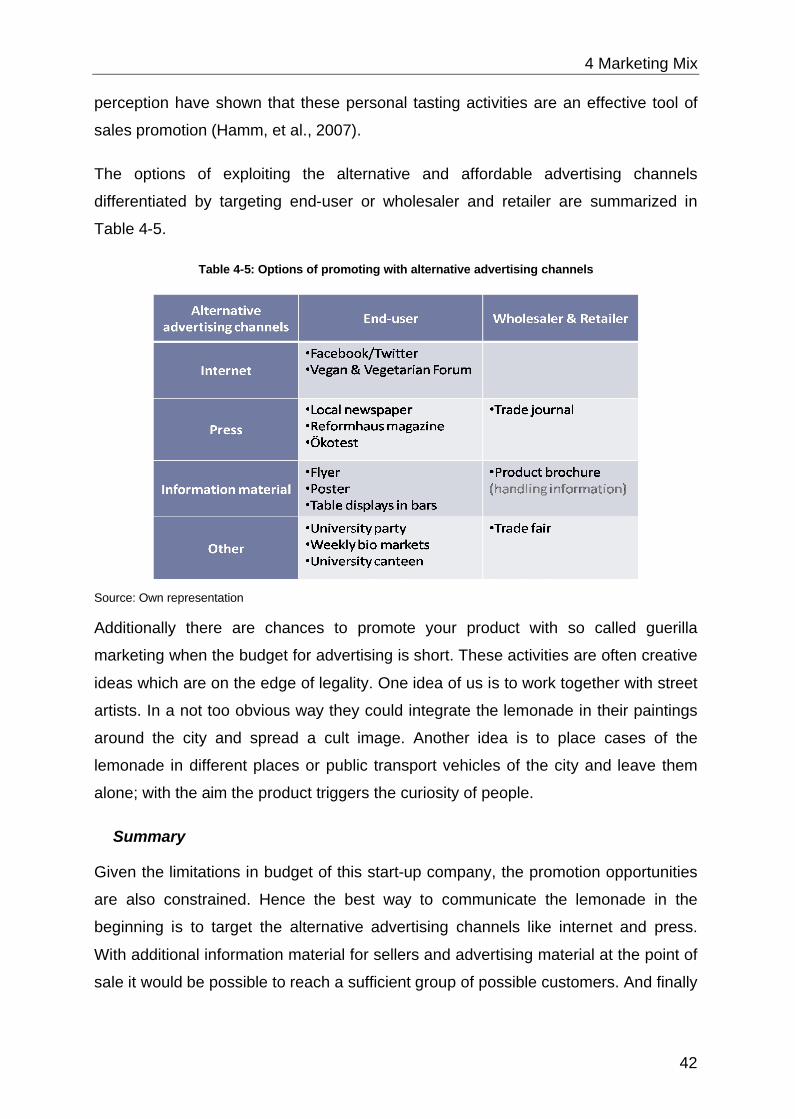

In addition, this report provides a low cost proposition for promotion channels; such

as the internet and press. Places such as weekly organic markets, trade fairs and

university are interesting opportunities to promote the product.

Finally, the last section of the report provides key next steps as a roadmap to

successfully bring the Novel-Lemonade to the market.

I

Table of Contents

List of Abbreviations............................................................................................... III

List of Figures.......................................................................................................... IV

List of Tables ............................................................................................................ V

1 Introduction .......................................................................................................... 11.1 Goal of this report .......................................................................................... 11.2 The Founder .................................................................................................. 11.3 The Product ................................................................................................... 2

2 Situation Analysis ................................................................................................ 42.1 Market Analysis.............................................................................................. 4

2.1.1 Market growth and size ....................................................................... 52.1.2 Market Trends ..................................................................................... 62.1.3 Key success Factors ........................................................................... 72.1.4 Summary ............................................................................................. 7

2.2 Market Potential ............................................................................................. 82.3 Competitive Analysis...................................................................................... 9

2.3.1 Definition of Competition ..................................................................... 92.3.2 Competitive Products .......................................................................... 92.3.3 Competitive Companies .................................................................... 102.3.4 Selection Process.............................................................................. 112.3.5 Further Competitors .......................................................................... 14

2.4 Target Customer Analysis............................................................................ 162.4.1 Main Target Group: Vegetarians, Vegans, and LOHAS ................... 162.4.2 Secondary Target Group: Young Customers (aged below 25).......... 18

3 Blind Taste Study ............................................................................................... 193.1 Products....................................................................................................... 193.2 Survey.......................................................................................................... 203.3 Study............................................................................................................ 203.4 Results......................................................................................................... 213.5 Summary...................................................................................................... 21

4 Marketing Mix ..................................................................................................... 234.1 Product......................................................................................................... 23

4.1.1 Product strategy ................................................................................ 234.1.2 Packaging.......................................................................................... 254.1.3 Summary ........................................................................................... 27

4.2 Place............................................................................................................ 284.2.1 Beverage distribution in Germany ..................................................... 284.2.2 Points of sale..................................................................................... 294.2.3 Location of production and sales area............................................... 33

II

4.2.4 Distribution system............................................................................ 354.2.5 Summary ........................................................................................... 36

4.3 Price............................................................................................................. 364.3.1 Market prices..................................................................................... 364.3.2 Production ......................................................................................... 374.3.3 Costs and profit ................................................................................. 38

4.4 Promotion..................................................................................................... 39

5 Conclusion.......................................................................................................... 445.1 Self Analysis ................................................................................................ 445.2 Recommendations ....................................................................................... 44

6 List of References .............................................................................................. 45

7 Appendix ............................................................................................................. 497.1 Details about Vitamin B12............................................................................ 497.2 Competitive products ................................................................................... 547.3 Blind Tasting Questionnaire......................................................................... 577.4 Blind Tasting Comments .............................................................................. 587.5 E-mail contact: Ökotest................................................................................ 58

III

List of Abbreviations

ADHD Attention Deficit Hyperactivity Disorder

AfG Alkoholfreie Getränke (non-alcoholic beverages)

BK Bionade Kräuter

EU European Union

F Feminine

FMCG Fast Moving Consumer Goods

FMSG Fast Moving Sustainable Goods

GFK Gesellschaft für Konsumforschung

LOHAS Lifestyle of Health and Sustainability

LPG Liquefied Petroleum Gas

M Masculine

N/A Non-Applicable

NL Novel-Lemonade

NMI Natural Marketing Institute

VEBU Vegetarierbund Deutschland

WAFG Wirtschaftsvereinigung Alkoholfreie Getränke e.V.

IV

List of Figures

Figure 2-1: Sales percentage of beverage industry in Germany................................. 4

Figure 2-2: Non-alcoholic beverages.......................................................................... 5

Figure 2-3: Portfolio of main competitors.................................................................. 13

Figure 2-4: Age distribution of lemonade buyers in Germany................................... 17

Figure 4-1: Beverage distribution in Germany .......................................................... 29

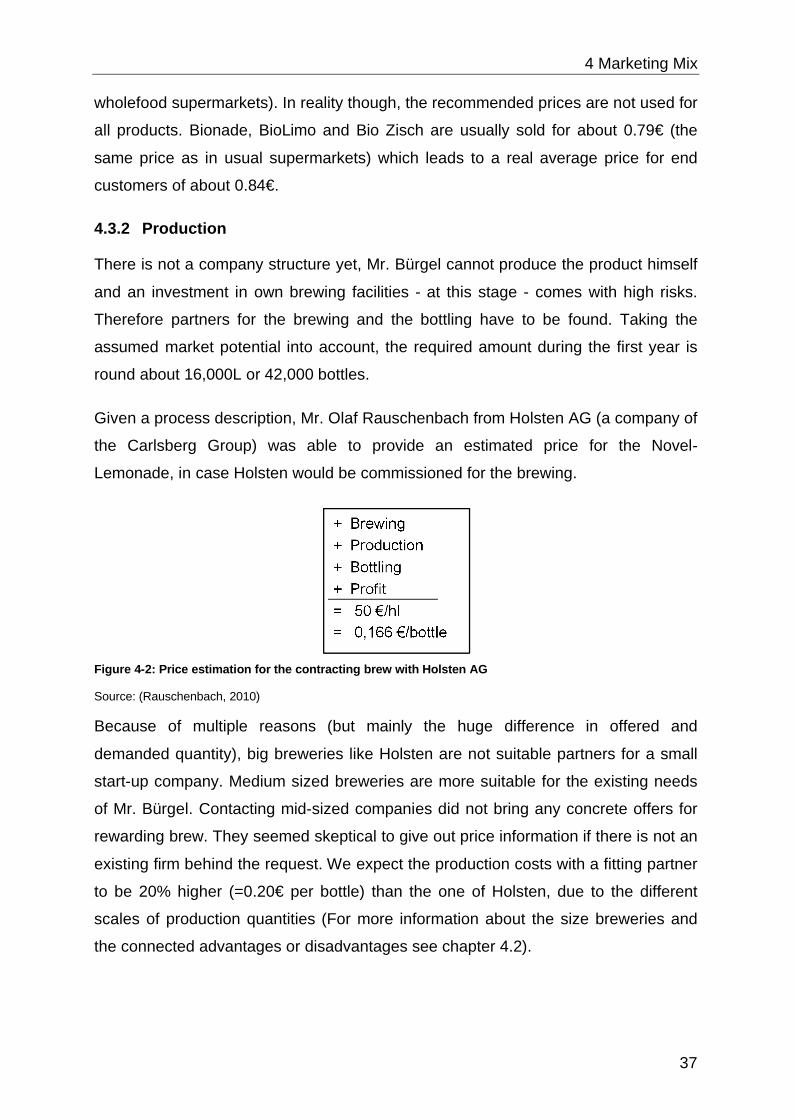

Figure 4-2: Price estimation for the contracting brew with Holsten AG..................... 37

Figure 7-1: Table for the Comparison of competitive products ................................. 56

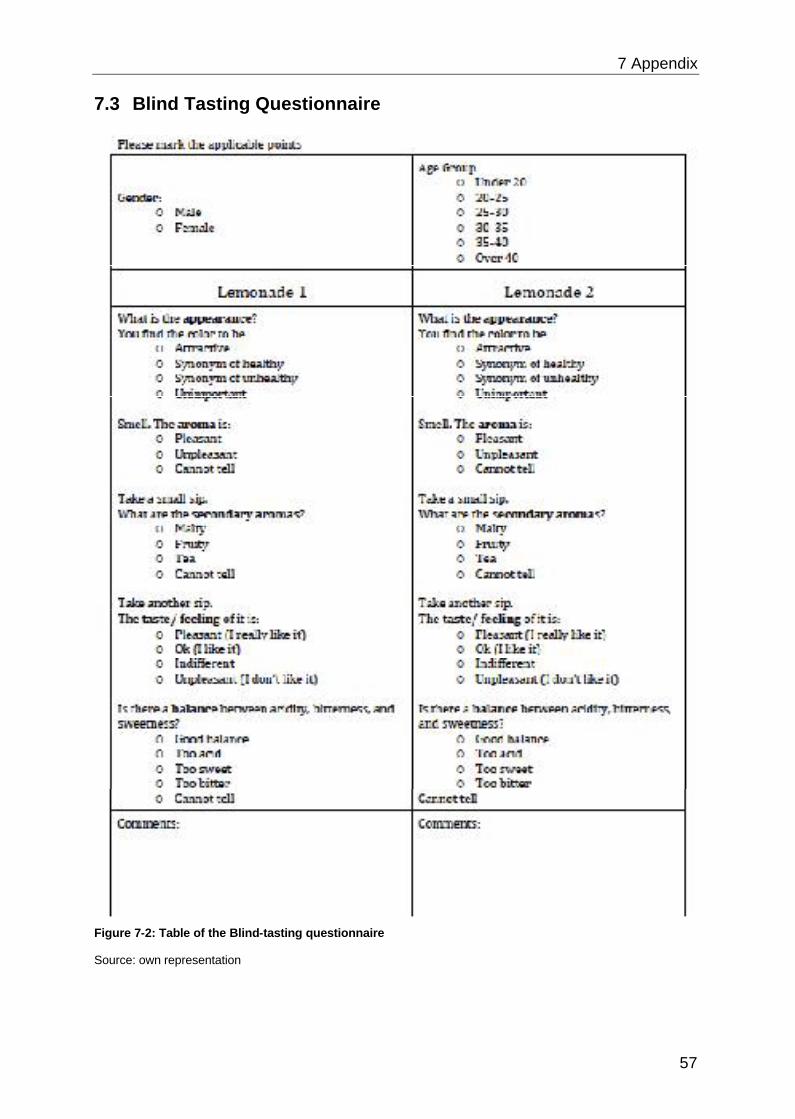

Figure 7-2: Table of the Blind-tasting questionnaire ................................................. 57

V

List of Tables

Table 1-1: Products of fermentation with different organisms..................................... 3

Table 2-1: Summary of criteria used for the calculation of the “Healthiness value” .. 12

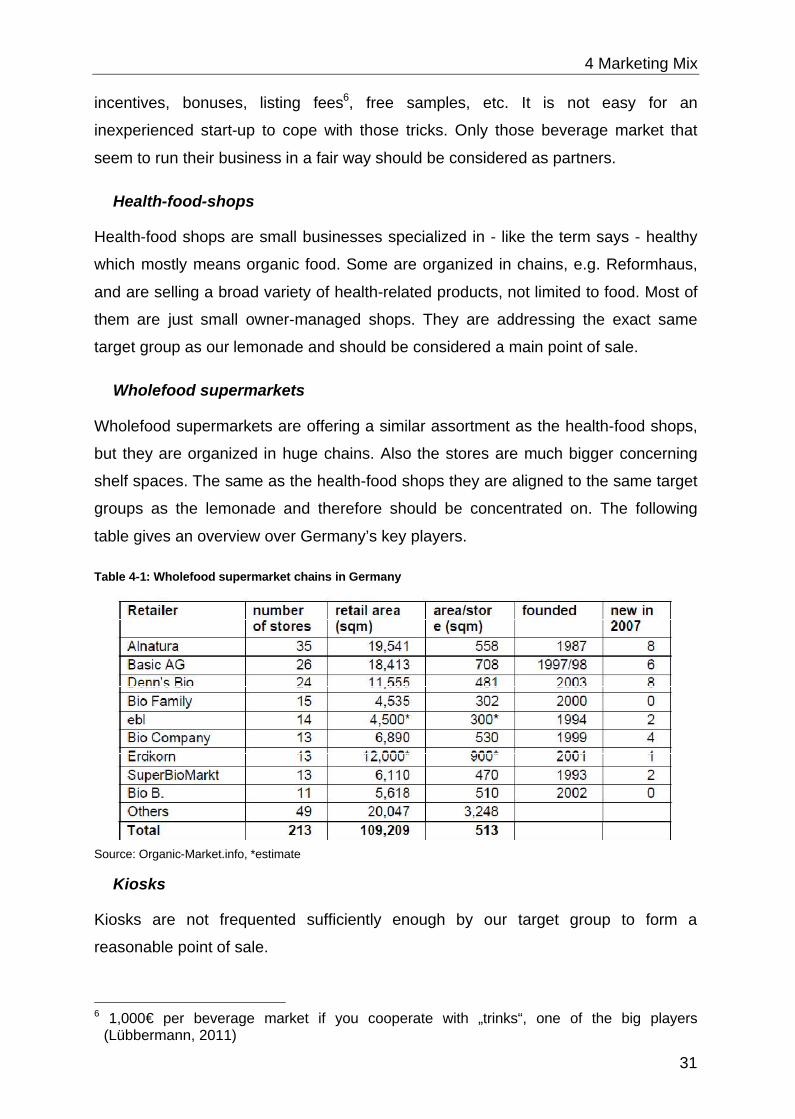

Table 4-1: Wholefood supermarket chains in Germany............................................ 31

Table 4-2: Summary of points of sale ....................................................................... 33

Table 4-3: Sizes of breweries in Germany................................................................ 34

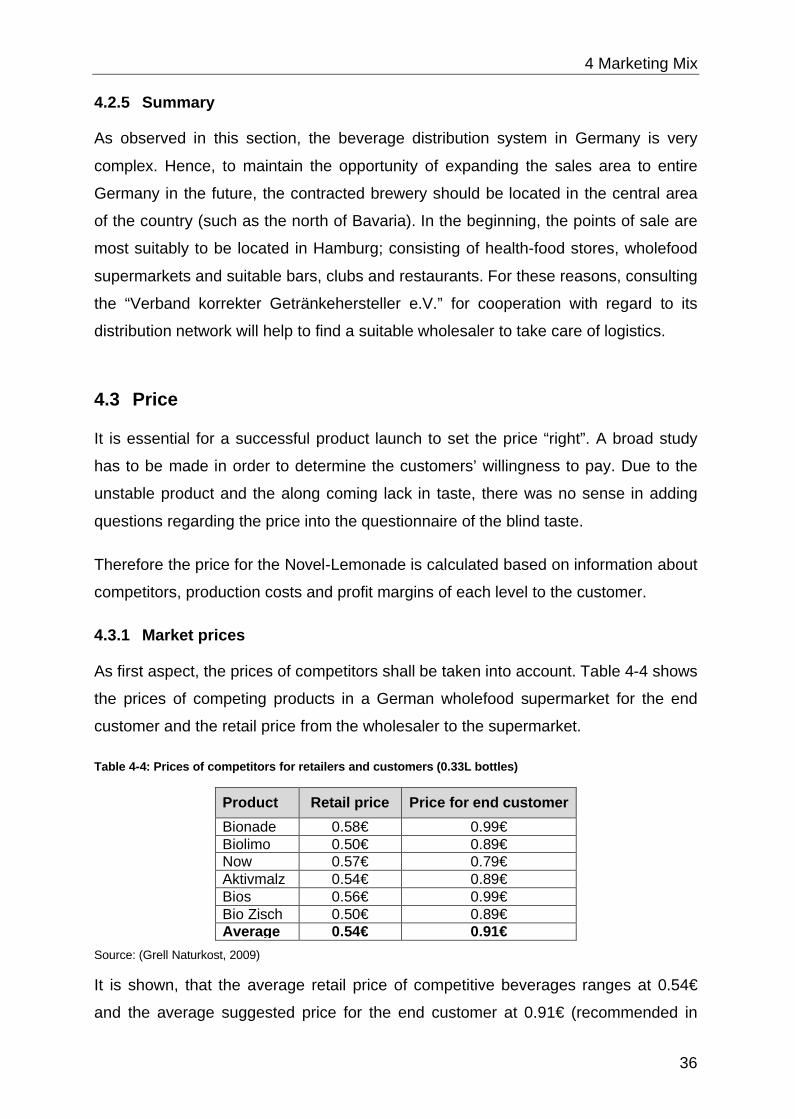

Table 4-4: Prices of competitors for retailers and customers (0.33L bottles) ............ 36

Table 4-6: Options of promoting with alternative advertising channels..................... 42

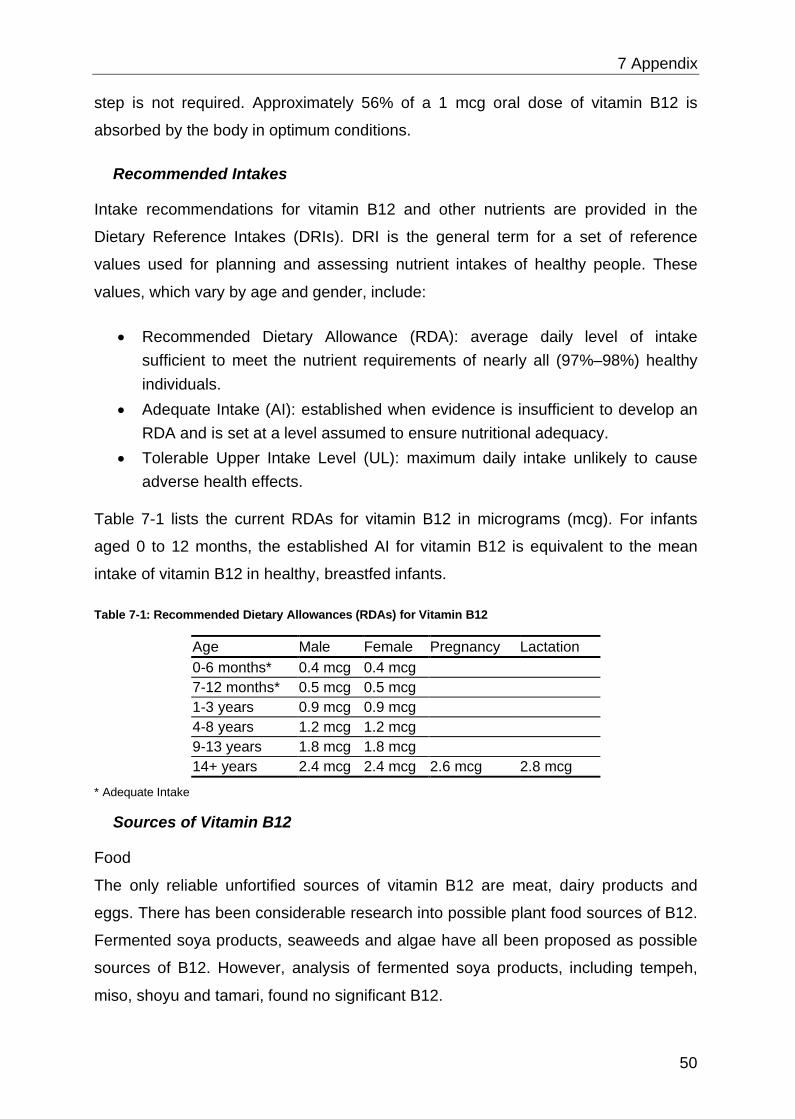

Table 7-1: Recommended Dietary Allowances (RDAs) for Vitamin B12................... 50

Table 7-2: Selected Food Sources of Vitamin B12 ................................................... 51

Table 7-3: Summary of competitive products ........................................................... 54

Table 7-4: Comments reported in the dedicated boxes of the questionnaire............ 58

1 Introduction

1

1 Introduction

1.1 Goal of this report

The goal of this report is to determine the possible market potential of the innovative

non-alcoholic beverage product of Benjamin Bürgel and to give a recommendation

about how to enter the market successfully. Therefore a marketing concept is

developed - based on conclusions drawn from the market situation - containing

information about the product, the price, the place and the promotion.

This report is carried out in the framework of the “Project seminar II – Innovation

marketing” in the winter term of 2010/2011 at the Institute of Marketing and

Innovation of the Technical University Hamburg-Harburg. The head of this Institute is

Prof. Dr. Christian Lüthje, the project is mentored by Stephanie Toth.

1.2 The Founder

1 Introduction

2

1.3 The Product

What is the Novel-Lemonade?

The traditional concept of lemonade consists of a lemon-flavored beverage, typically

made from lemons (citrons), sugar and water. However, in recent times the name has

been adopted to refer to different types of beverages. The French term lemonade

has come to mean “soft drink” in many countries, regardless of the flavor.

The Novel-Lemonade is also not a lemon-flavored beverage, yet it is produced form a

natural resource. In the case of the product for this study, the natural resource is

barley. The Novel-Lemonade is carbonized, acquiring this characteristic from the

process of fermentation to which the barley is subject to produce the lemonade drink.

And finally, the Novel-Lemonade is naturally enriched with vitamins and flavonoids,

which are indispensible for the optimum performance and health of the human body.

What is fermentation?

Fermentation is an anaerobic (in absence of oxygen) process present in nature.

During this process, complex molecules are oxidized to produce an organic

compound.

The primary industrial advantage of fermentation is the conversion of grape juice into

wine, barley into beer and carbohydrates into carbon dioxide to produce bread. It is

to mention that fermentation serves other general purposes:

� The enrichment of the diet trough the development of a variety of textures,

aromas and flavors;

� The preservation of important amounts of nutrients by means of lactic acid,

ethanol, acetic acid and alkaline fermentations;

� The enrichment of the food substrates with proteins, amino acids, essential

fatty acids and vitamins;

� And detoxification.

1 Introduction

3

In brewing, fermentation typically involves conversion of carbohydrates to alcohols

and carbon dioxide or organic acids, using yeasts, bacteria or a combination of both.

Nonetheless, brewing specifically refers to the process of steeping.

What drinks can be produced out of fermentation?

As mentioned before, fermentation is mainly utilized to produce alcoholic beverages,

such as wine or beer. Nevertheless, depending on the organism employed in the

fermentation process different products can be obtained from the brewing process.

The table below summarizes some of the products associated to a specific type of

organism employed in the fermentation process.

Table 1-1: Products of fermentation with different organisms

Commercial Product Organism Product of fermentation

Beer & Wine Saccharomycescerevisiae Alcohol

Rivella Lactobacillus reuteri Lactic acid

Posca Acetobacteraceti Acetic Acid

Bionade Gluconobacteroxydans Gluconic Acid

Source: Own representation

However, these are not the only organisms that can be used in the process of

fermentation and this is where our product stands. The addition of streptomycin as

the organism present in the fermentation produces, between others, Vitamin B12,

which is indispensible for the proper function of multiple activities in the body. For

further information about B12 please see the appendix.

What are the advantages of the Novel-Lemonade over other lemonades?

2 Situation Analysis

4

2 Situation Analysis

This chapter provides information about the current situation of market, competitors

and target customers of the Novel-Lemonade.

2.1 Market Analysis

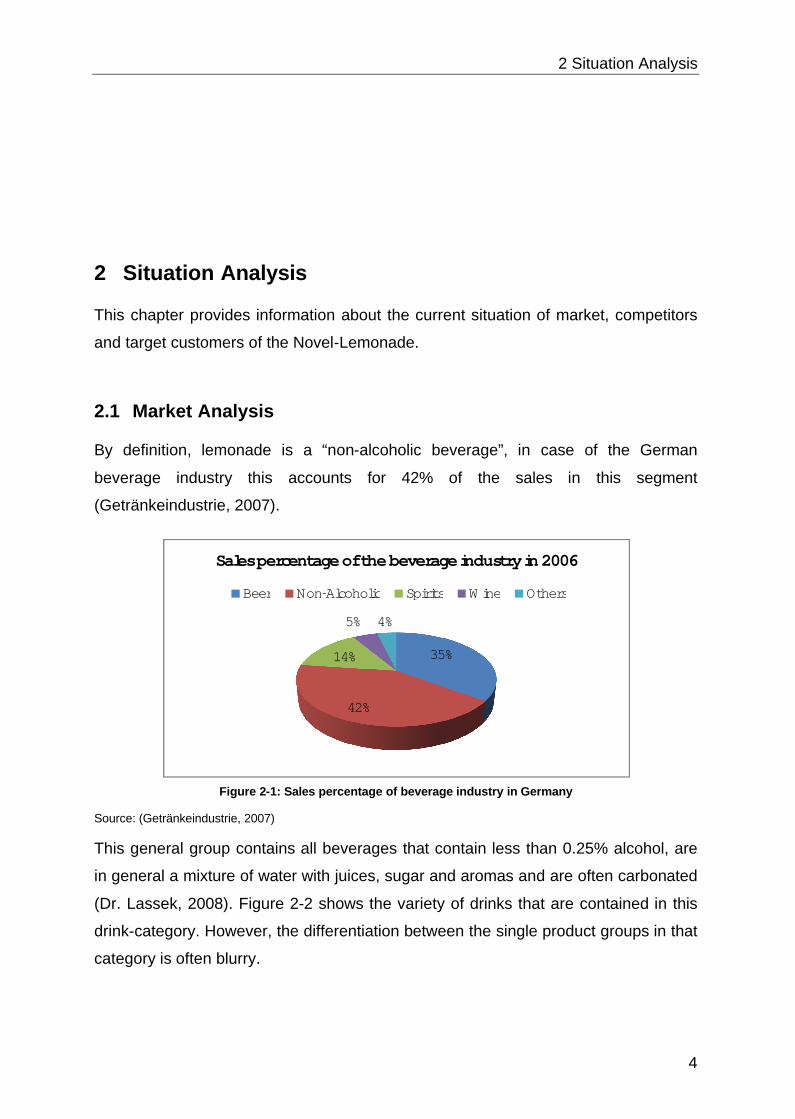

By definition, lemonade is a “non-alcoholic beverage”, in case of the German

beverage industry this accounts for 42% of the sales in this segment

(Getränkeindustrie, 2007).

Figure 2-1: Sales percentage of beverage industry in Germany

Source: (Getränkeindustrie, 2007)

This general group contains all beverages that contain less than 0.25% alcohol, are

in general a mixture of water with juices, sugar and aromas and are often carbonated

(Dr. Lassek, 2008). Figure 2-2 shows the variety of drinks that are contained in this

drink-category. However, the differentiation between the single product groups in that

category is often blurry.

35%

42%

14%

5% 4%

Sales percentage of the beverage industry in 2006

Beer Non-Alcoholic Spirits Wine Others

2 Situation Analysis

5

Figure 2-2: Non-alcoholic beverages

Source: Own representation in dependence on (Zarnkow, et al., 2010)

2.1.1 Market growth and size

The German soft drinks market is large but fairly mature. However, the market has

not shown any signs of contraction. The value of soft drink market is projected to

stagnate for the next five years, neither growing nor shrinking to a great extent

(Business Monitor International, 2008). However, the particular sector that is of

highest growth is the ‘new segment’ which offers healthy benefits for consumers. This

segment includes energy drinks, vitamin water, oxygenated water, smoothies, and

organic lemonades. It accounts for almost one-fifth of the total non-alcoholic

beverage sales. According to GFK, the growth for this new segment is 35% per year

(Axel Springer, 2009). From the information available, we estimate the market size of

Bio-lemonade to be around 60 Million Euro or 0.8% of the non-alcoholic drink market

(7.2 billion Euros). For the Novel-Lemonade which offers functional benefit of vitamin

B12, it could attract the potential customers who are vegetarian or vegan.

Vegetarians are estimated to be 7.38 million, which is 9% of the total population of

Germany (Institut Produkt und Markt, 2009).

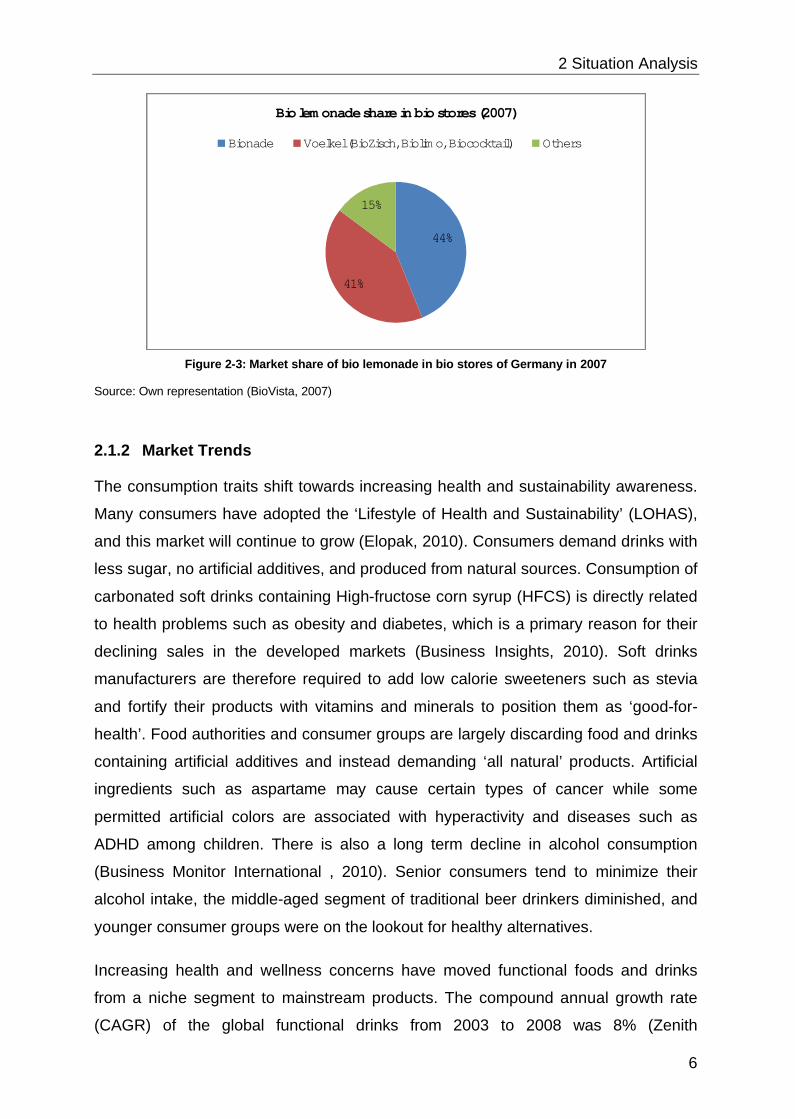

Considering the market share for organic lemonades, the major player is Bionade,

which had a market share of 43.9% in 2007, and Voelkel, the company that produces

BioLimo accounts for 41.3% of the market (BioVista, 2007). The organic market is

highly competitive, with the major players mentioned previously and a wave of small

start-up companies. The in-depth analysis of competitors can be found in section 2.2.

Non-alcoholic beverages

Juices Smoothies Mineral water

Bitter lemonades Ice Tea Energy

drinks Cola Drinks Lemonades& Sherbet

2 Situation Analysis

6

Figure 2-3: Market share of bio lemonade in bio stores of Germany in 2007

Source: Own representation (BioVista, 2007)

2.1.2 Market Trends

The consumption traits shift towards increasing health and sustainability awareness.

Many consumers have adopted the ‘Lifestyle of Health and Sustainability’ (LOHAS),

and this market will continue to grow (Elopak, 2010). Consumers demand drinks with

less sugar, no artificial additives, and produced from natural sources. Consumption of

carbonated soft drinks containing High-fructose corn syrup (HFCS) is directly related

to health problems such as obesity and diabetes, which is a primary reason for their

declining sales in the developed markets (Business Insights, 2010). Soft drinks

manufacturers are therefore required to add low calorie sweeteners such as stevia

and fortify their products with vitamins and minerals to position them as ‘good-for-

health’. Food authorities and consumer groups are largely discarding food and drinks

containing artificial additives and instead demanding ‘all natural’ products. Artificial

ingredients such as aspartame may cause certain types of cancer while some

permitted artificial colors are associated with hyperactivity and diseases such as

ADHD among children. There is also a long term decline in alcohol consumption

(Business Monitor International , 2010). Senior consumers tend to minimize their

alcohol intake, the middle-aged segment of traditional beer drinkers diminished, and

younger consumer groups were on the lookout for healthy alternatives.

Increasing health and wellness concerns have moved functional foods and drinks

from a niche segment to mainstream products. The compound annual growth rate

(CAGR) of the global functional drinks from 2003 to 2008 was 8% (Zenith

44%

41%

15%

Bio lemonade share in bio stores (2007)

Bionade Voelkel (BioZisch, Biolimo, Biococktail) Others

2 Situation Analysis

7

International, 2009). Naturalness, functional benefits, and indulgence are the

emerging trends in new product development and will continue to be a key driver of

formulation launches (Business Insights, 2010). Sustainability and ethical concerns

also affect requirements for packaging materials. There is an increasing regulatory

pressure concerning return of the bottles, recycling, and using biodegradable

materials (Business Insights, 2010).

2.1.3 Key success Factors

� Healthy and functional benefits continue to be the crucial factors determining consumption decisions. Qualities such as all-natural, low-calories, sugar-free, and functional benefits all help grow sales (Mintel International, 2010).

� Flavor is very essential. Health conscious customers will not buy the product if it does not taste good (New Zealand Trade and Enterprise, 2008).

� The healthy products need to be packaged in a trendy and ‘cool’ way, and be as sustainable as possible. Packaging and label design are important in attracting the customer to try the product for the first time and they contribute to the total customer satisfaction with the product.

� Distribution channels are also of high importance. Selecting and gaining access to the right distribution channels that are effective in reaching the target customers means higher sales and profits. The options for places to sell the products include organic shops, supermarkets, discounters, bars and restaurants. Organic food is sold through all distribution channels in Germany -in conventional supermarkets and discounters as well as in a rapidly increasing number of organic supermarkets. About half of these are organized in chains, the other half are still independently owned (New Zealand Trade and Enterprise, 2008). More information regarding the distribution channels can be found in section 4.2.1.

2.1.4 Summary

Organic lemonade in Germany has the market size of around 60 Million Euro. It is

part of the fastest growing segment of non-alcoholic drink, the ‚new segment‘, with

the growth rate of 35%. The competitiveness in the market is high with the

dominance of some key players and waves of small companies. The major players in

health food stores are Bionade (43.9% market share) and Voelkel (41.3% market

share). The market trend shows rising health and sustainability awareness. The key

success factors are flavor, health and functional benefits, trendy and sustainable

packaging, and right distribution channels.

2 Situation Analysis

8

2.2 Market Potential

To calculate the market potential (MP), we have to define the number of customer

(N), the price (P) and the yearly quantity consumed per point of sale (Q). The market

potential can then be calculated using the following formula:

� � = � � � � �

The following numbers used in the calculation are derived from our analysis and

assumptions that are explained in Chapter 4 Marketing Mix.

2 Situation Analysis

9

2.3 Competitive Analysis

2.3.1 Definition of Competition

The goal of this chapter is to obtain a detailed description and definition of

competitive products and companies. Due to the fact, that brewed lemonades are

rather new to the market, there is not a clear segment, nor are there many products

like e.g. Bionade (regarding the production-process). Therefore, the term competitor

has to be defined specifically in regards to the Novel-Lemonade.

In this report, different criteria of the products themselves and of the companies

behind each product where used to gain knowledge about competing drinks. This is a

very theoretical approach, only taking numerical facts into account. But another very

important aspect is the customer perception of the Novel-Lemonade in comparison to

other products, because it is subjective. Therefore a detailed survey about the

perceived images and properties of competitors has to be made.

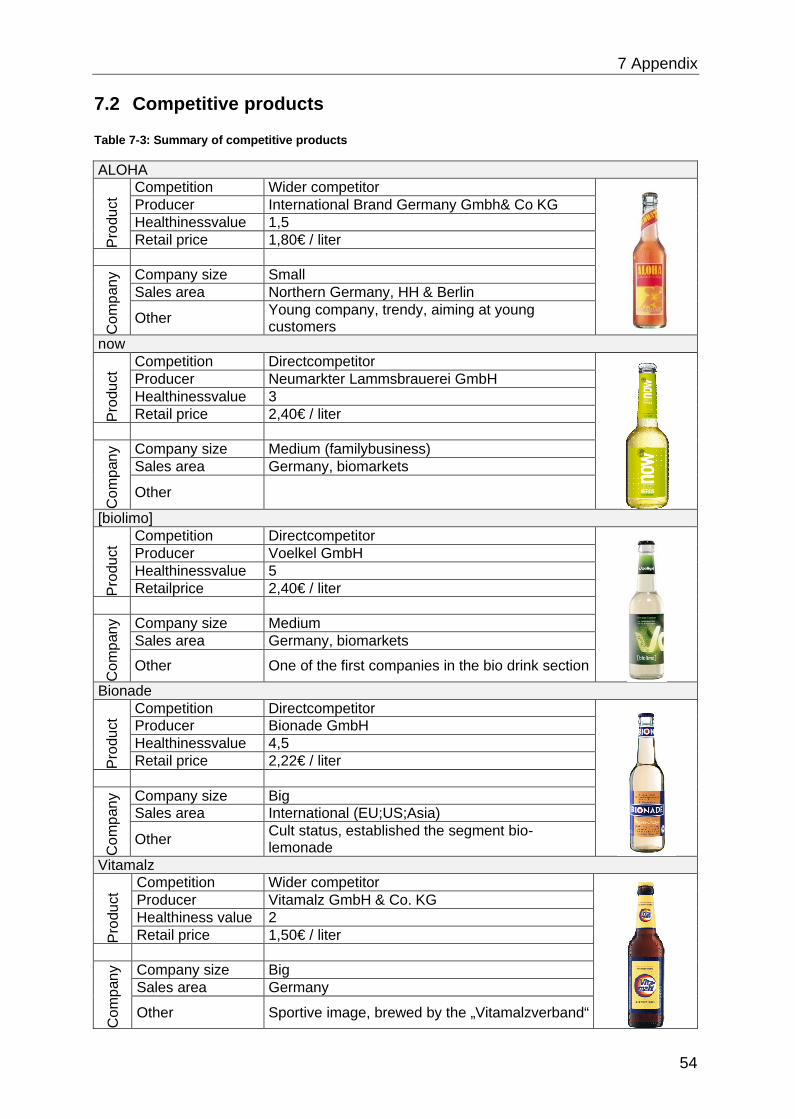

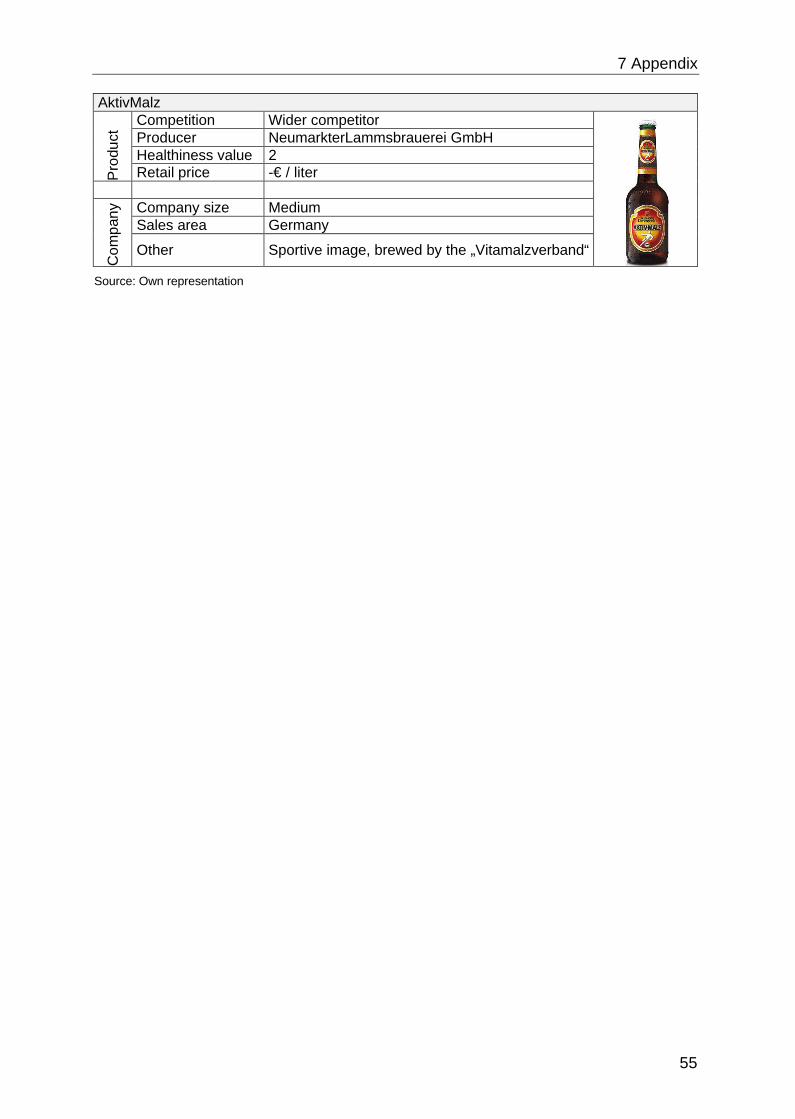

2.3.2 Competitive Products

The Pioneer in the segment of bio-lemonades is Bionade. Referring to the European

Patent Office, the production process of Bionade has the international patent WO

95/22911 (European patent office EP000000748168B11; German patent office

DE000004406087C12), naming the end product of this process “alcohol-free

refreshing drink”. Terms like “Lemonade” or “Bio-Lemonade” are not mentioned at all.

Henning Alberts, working in the marketing department of Bionade, states:

“…Bionade is competing with all products in the non-alcoholic beverages market…”

(Alberts, 2010)

This underlines the vague differentiation between products in the non-alcoholic

beverages segment.

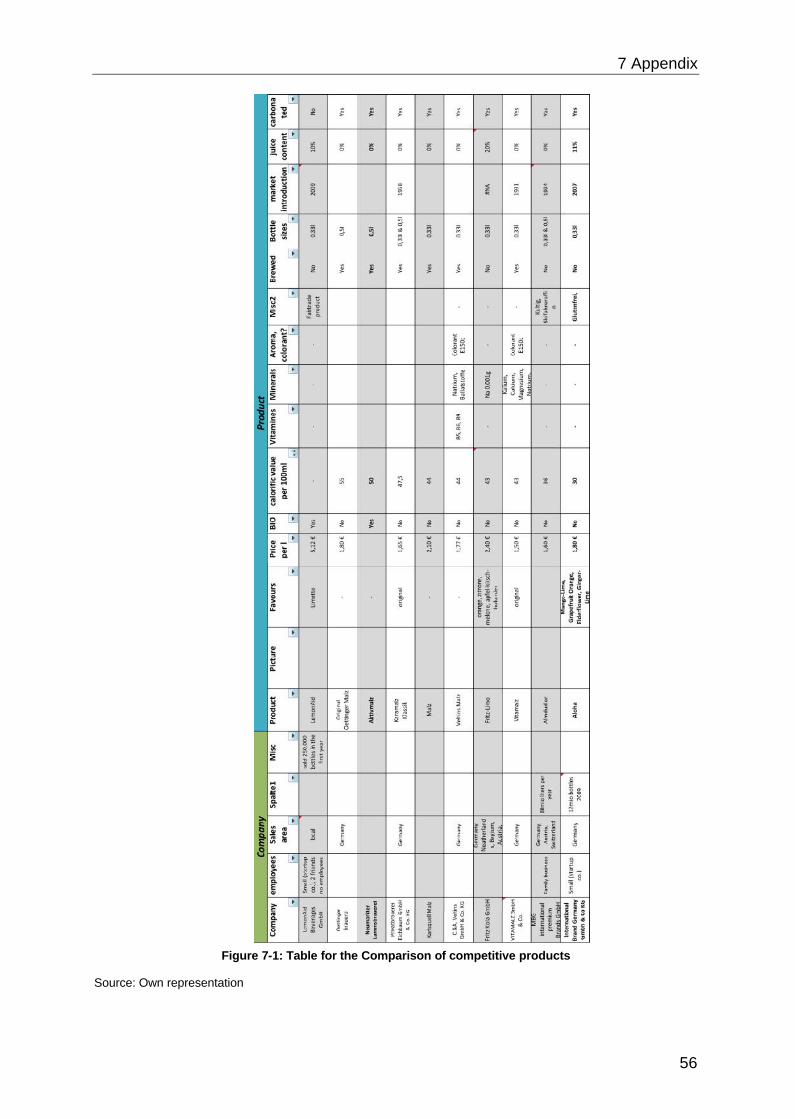

For this approach a table was created collection as much information as possible

from drinks on the market (see Figure 7-1 in the appendix). The chosen products are

1 (Leipold, 1990)2 (Leipold, 1990)

2 Situation Analysis

10

mainly lemonades, malt beers3 and bio-lemonades. The product criteria, collected in

the table, are the following:

� Available flavors� Price per liter� Bio certification (yes or no)� Caloric value per 100ml� Contained vitamins, minerals, aromas and colorant� Year of market introduction� Juice content� Carbonization (yes or no)� Production process (brewed lemonade or mixture)

Using this table as a basis, the competition for our product was derived. (For details

see the Chapter 2.3.4.)

Properties of the drink

From the customers perspective it does not matter how the product is produced in

first line, because the process is not adding any customer value, as long as major

product requirements of the specific customer are met. If the drink has e.g. a BIO

certification it does not make a difference if it is a fermented drink or a mixture (there

might be a difference in the taste, but this is a subjective criteria depending on the

individual customer).

2.3.3 Competitive Companies

Size

Another way to figure out possible competitors is to look closer at the companies

instead of just at their products. In this approach the focus would be the size of the

company; is the investigated company a big global player or also just a small, maybe

even a start-up company? In consideration of no artificial flavors and conservatives,

the product “The Spirit of Georgia” is going slightly into the same direction as the

Novel-Lemonade, but already due to the fact that it is a Coca Cola product, it makes

no sense to include such a lemonade to the competitors.

3 Malt beers have been considered because the taste of the Novel-Lemonade has a slight malty scent.

2 Situation Analysis

11

Sales area

Another important aspect is the sales area. Competitors can be lemonades that are

not exactly fulfilling the same ideologies regarding biological ingredients, but focusing

on the same sales area. An example for this is Aloha, which is calling itself a

“Surfsoda”. But it is also a small company distributing its products mainly in the North

of Germany and so can be seen as a competitor. In contrast to this example there

are some other lemonades having the same attributes but being distributed in other

parts of Germany and therefore targeting another sales area, which is why they are

not considered being a real competitor.

2.3.4 Selection Process

Taking all the perspectives mentioned before into account, we come to a selection of

competitors. For further examination of these potential competitors, it is necessary to

derive indices that would group the selected products and indicate where in

comparison the Novel-Lemonade is positioned.

In the search of indices, we focus on the aspects, which are important concerning a

bio-lemonade, the taste and the healthiness. In general, taste is the most important

selling feature for lemonades, but it is often a very subjective perception. Because of

this reason we developed a taste index based on three rough taste categories. The

first one is called “Lemonade”, which implies a really sweet, fruity and sour taste, the

second category is “Fermented”, which means the customer experience a moderate

sweetness combined with a slight bitterness and tea taste, and the third taste

category is “Malt drink”, which is associated with a strong malt taste and moderate

bitterness.

The Healthiness index consists of the indicators Bio certification, calories, added

sugar, vitamins and minerals. By means of a point system the indicators receive

different weights, which are derived from assumptions the customer would perceive

as more important concerning healthiness. Products get two points whenever they

have a Bio certification. As a boundary the average caloric value of the three market

leaders in the segment of non-alcoholic beverages (Coca-Cola, Fanta and Sprite) is

used, which is 40kcal per 100ml(Coca-Cola GmbH, 2010). Consequently, a product

which contains 40kcal and more gets no points, between 39kcal and 28kcal one point

and under 28kcal two points. The other three indicators are weighted less. Products

2 Situation Analysis

12

with additional added sugar receive no points, with fruit sugar half a point and with no

added sugar one point. For the indicators vitamins and minerals, the point structure

follows the same pattern. Whenever there is no significant amount indicated, the

product gets no points (We acknowledge an amount as significant as soon as the

company is actively advertising with it.). Indicated moderate amounts of minerals or

vitamins lead to half of a point and for significant amounts the product receives a full

point.

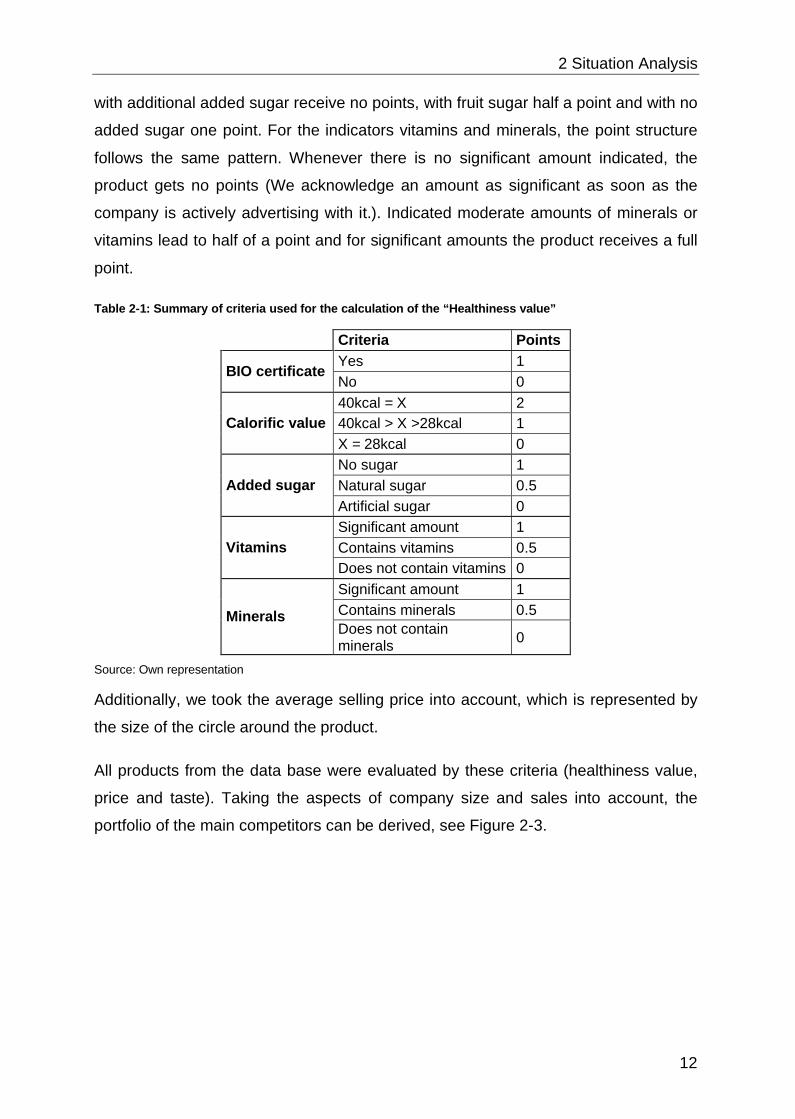

Table 2-1: Summary of criteria used for the calculation of the “Healthiness value”

Criteria Points

BIO certificate Yes 1No 0

Calorific value40kcal = X 240kcal > X >28kcal 1X = 28kcal 0

Added sugarNo sugar 1Natural sugar 0.5Artificial sugar 0

VitaminsSignificant amount 1Contains vitamins 0.5Does not contain vitamins 0

Minerals

Significant amount 1Contains minerals 0.5Does not contain minerals 0

Source: Own representation

Additionally, we took the average selling price into account, which is represented by

the size of the circle around the product.

All products from the data base were evaluated by these criteria (healthiness value,

price and taste). Taking the aspects of company size and sales into account, the

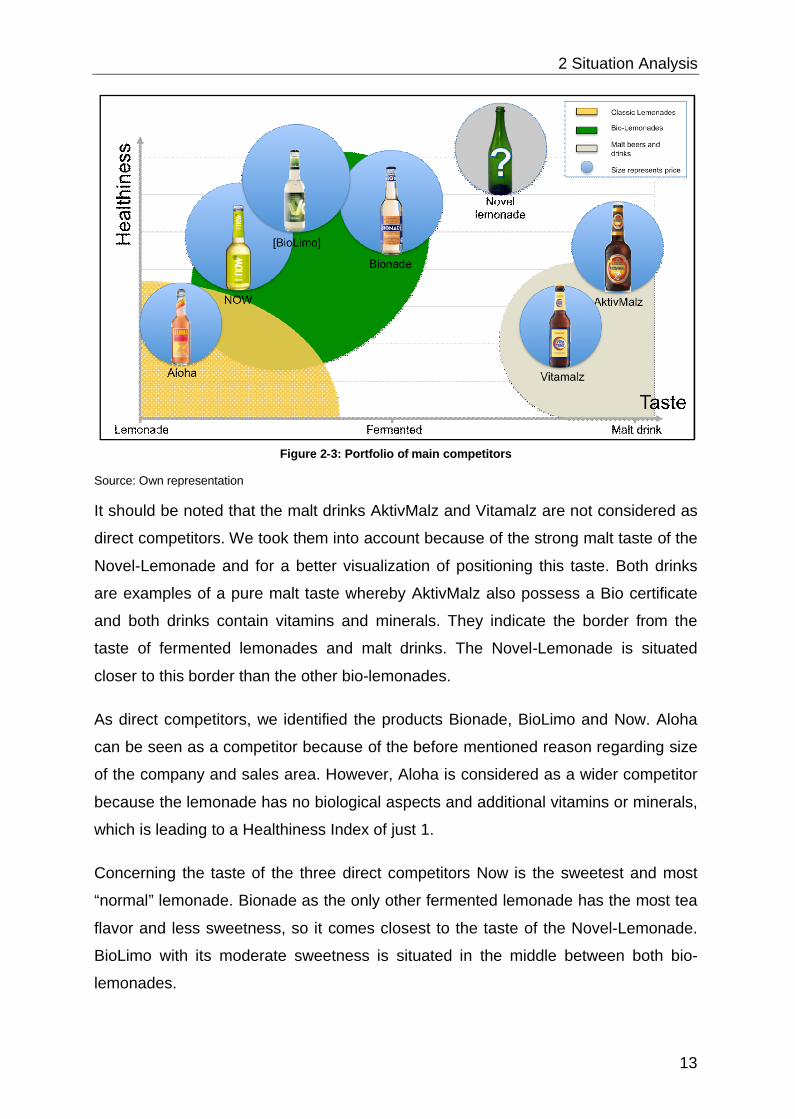

portfolio of the main competitors can be derived, see Figure 2-3.

2 Situation Analysis

13

Figure 2-3: Portfolio of main competitors

Source: Own representation

It should be noted that the malt drinks AktivMalz and Vitamalz are not considered as

direct competitors. We took them into account because of the strong malt taste of the

Novel-Lemonade and for a better visualization of positioning this taste. Both drinks

are examples of a pure malt taste whereby AktivMalz also possess a Bio certificate

and both drinks contain vitamins and minerals. They indicate the border from the

taste of fermented lemonades and malt drinks. The Novel-Lemonade is situated

closer to this border than the other bio-lemonades.

As direct competitors, we identified the products Bionade, BioLimo and Now. Aloha

can be seen as a competitor because of the before mentioned reason regarding size

of the company and sales area. However, Aloha is considered as a wider competitor

because the lemonade has no biological aspects and additional vitamins or minerals,

which is leading to a Healthiness Index of just 1.

Concerning the taste of the three direct competitors Now is the sweetest and most

“normal” lemonade. Bionade as the only other fermented lemonade has the most tea

flavor and less sweetness, so it comes closest to the taste of the Novel-Lemonade.

BioLimo with its moderate sweetness is situated in the middle between both bio-

lemonades.

2 Situation Analysis

14

The calculation of the Healthiness index for the three products shows that they are all

quite close together. All of them have a Bio certificate and indicate a moderate

amount of vitamins or minerals. “Now” with a healthiness value of 3.5 points has the

lowest index because of a medium high calorie amount. While Bionade with an index

of 4.5 points has the lowest amount of calories, BioLimo reaches a Healthiness Index

of 5 points due to its use of fruit sugar. The Novel-Lemonade achieves the highest

healthiness value with 6 points. This amount is reached by the estimations that the

product gets a Bio certification, has comparable calories as Bionade, contains

completely no added sugar and is rich in vitamin B12.

This analysis shows that the Novel-Lemonade would slightly outstand concerning the

healthiness in comparison to the three direct competitors, which are the most sold

bio-lemonades in the bio stores.

Direct Competitors

� Bionade� [biolimo]� Now

Wider Competitors

� Aloha� Vitamalz� Aktivmalz

2.3.5 Further Competitors

Additional to the before mentioned competitors, there is a trend of small start-up

companies in the beverage market which try to initiate social consume. Their goal is

to combine biological ingredients, fair trade and charity. An example for this trend is

LemonAid. Founded in 2008 by two entrepreneurs from Hamburg, LemonAid is

selling nowadays around 50.000 bottles per month. Sugar and lime juice are

imported from fair-trade cooperatives in developing countries. With the future return,

the company also wants to support projects in these countries. It might be the

beginning of a long-term trend. Being socially committed and not just a bio product

could be a competitive advantage. Until today this trend has not provided a

comparable product to Novel-Lemonade, concerning healthiness and the

fermentation process, but the beverage market is fast moving and there might be a

2 Situation Analysis

15

new competitor in the future who is more similar to it. In this regard, there are

reasons to consider the fair trade and charity aspects into the product concept to stay

competitive (Frommberg, 2010).

The selected companies (from the direct and the wider competition) only represent

the established players that already have a well-known brand name, developed

company structures and networks. Thereby, they have a significant advantage in

respect to market strength. It has to be pointed out though, that a wave of young

start-ups is flooding the non-alcoholic beverages market, with a variety of different

products (Reißmann, 2010) (Trentmann, 2010). They are mostly operating in their

direct regional surroundings, have small market shares and no national-wide known

brand name. Additionally, the majority of those drinks aims for customers of “classic”

lemonades and are not trying to enter the healthiness-oriented segment. This is why

none of them is chosen as competitor. Still the danger of many new small start-ups

has to be pointed out, because the customer is flooded with new drinks in bars and

the shelves of supermarkets, which makes a clear diversification even more

important.

2 Situation Analysis

16

2.4 Target Customer Analysis

Based on the analysis of the product and its position in terms of competitiveness in

the market, the customer that would likely purchase the product is analyzed. As a

Hamburg based start-up business, it makes sense to target customers who are

located primarily in the city of Hamburg and in a future step in some other big cities in

Germany.

2.4.1 Main Target Group: Vegetarians, Vegans, and LOHAS (aged above 25)

Having a product with outstanding healthiness characteristics and the vitamin B12

feature, the first obvious target customer would be vegetarians and vegans. It is

estimated that there are around 7.3 million vegetarians in Germany (Institut Produkt

und Markt, 2009) or around 9% of the total population. Vegetarians and vegans come

from all age, income, education and geographical boundaries. A typical characteristic

of them is that they can be loyal, enthusiastic customers who generate word-of-

mouth recommendations to other vegetarians and vegans.

When selecting vegetarian foods, consumers consider availability, taste, convenience

and price. In a study of 20,000 households by the Soyfoods Association of America,

taste was the primary consideration while purchasing, with cost ranking the second

and fat content the third. Vegetarians and vegans are usually having a strong

relationship to each other and establish communities. In Germany, the

Vegetarierbund Deutschland (VEBU) is the main organization for vegetarians and

vegans.

There is a strong consumer movement focused on health, environment, personal

development, social responsibility and sustainable living. This target group is called

LOHAS (Lifestyle of Health and Sustainability). In the German market, the number of

LOHAS consumer has reached 28% of the population in 2008 (Elopak, 2010) and

this number is expected to continue to rise in the future. Therefore this group is the

ideal target customer, apart from vegetarians and vegans, who have a special benefit

of the B12 feature due to their diet.

While current LOHAS consumers are usually slightly older, aged 40+ with family,

there is a strong indication that younger people are getting into this new lifestyle.

Angela Kuhnert from Bionade stated that “while the buyers of traditional soft drinks

2 Situation Analysis

17

are between 14 to 35 years old, Bionade’s buyers are between two to above 90

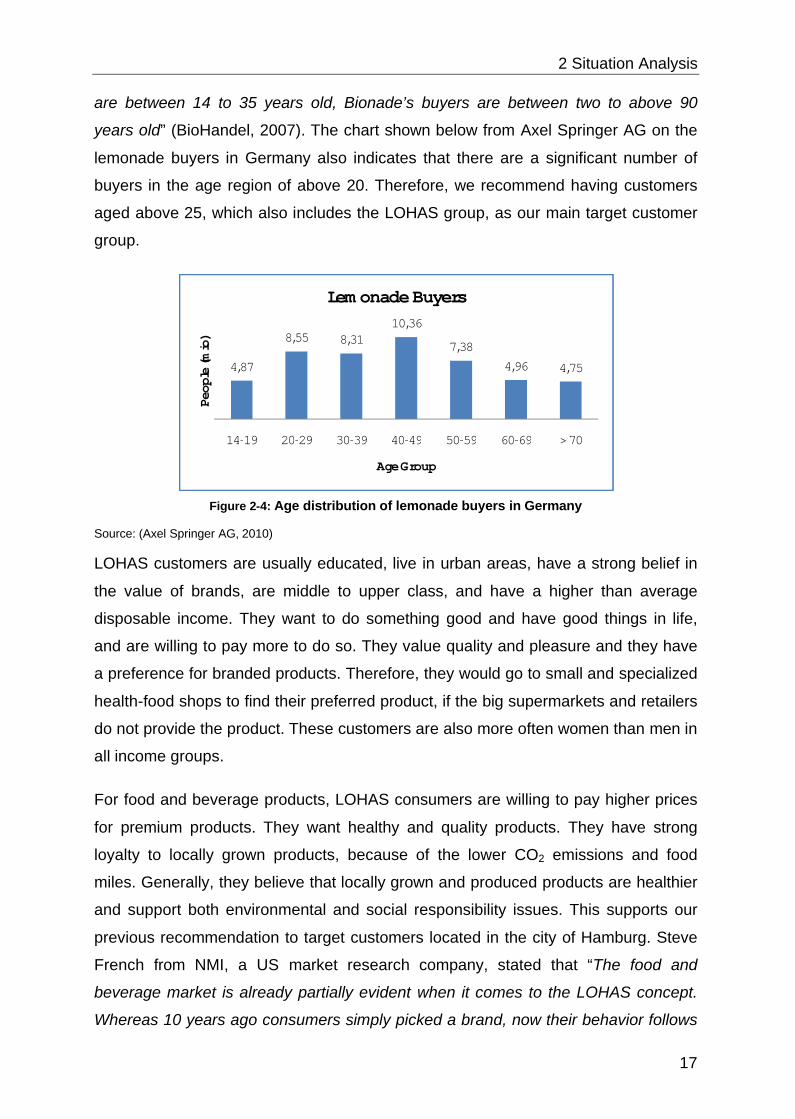

years old” (BioHandel, 2007). The chart shown below from Axel Springer AG on the

lemonade buyers in Germany also indicates that there are a significant number of

buyers in the age region of above 20. Therefore, we recommend having customers

aged above 25, which also includes the LOHAS group, as our main target customer

group.

Figure 2-4: Age distribution of lemonade buyers in Germany

Source: (Axel Springer AG, 2010)

LOHAS customers are usually educated, live in urban areas, have a strong belief in

the value of brands, are middle to upper class, and have a higher than average

disposable income. They want to do something good and have good things in life,

and are willing to pay more to do so. They value quality and pleasure and they have

a preference for branded products. Therefore, they would go to small and specialized

health-food shops to find their preferred product, if the big supermarkets and retailers

do not provide the product. These customers are also more often women than men in

all income groups.

For food and beverage products, LOHAS consumers are willing to pay higher prices

for premium products. They want healthy and quality products. They have strong

loyalty to locally grown products, because of the lower CO2 emissions and food

miles. Generally, they believe that locally grown and produced products are healthier

and support both environmental and social responsibility issues. This supports our

previous recommendation to target customers located in the city of Hamburg. Steve

French from NMI, a US market research company, stated that “The food and

beverage market is already partially evident when it comes to the LOHAS concept.

Whereas 10 years ago consumers simply picked a brand, now their behavior follows

4,87

8,55 8,3110,36

7,384,96 4,75

14-19 20-29 30-39 40-49 50-59 60-69 > 70

Peop

le(m

io)

Age Group

Lemonade Buyers

2 Situation Analysis

18

a pre-and post consumption pattern, such as where is the product from, what are the

ingredients, where are they from, how can they recycle the packaging, etc. This has

opened up opportunities to answer these questions through their product and

packaging.” (Elopak, 2010)

However, the significance of younger customer in lemonade market cannot be

neglected. Therefore, in the next section we will provide explanations on our

secondary target customer: customers aged below 25.

2.4.2 Secondary Target Group: Young Customers (aged below 25)

As stated before, Bionade as our main competitor states, that their target customers

are aged between two to above 90 years old and there is also a significant number of

young lemonade buyers in the chart provided in the previous section. Therefore, it is

also important to understand these young customers’ buying behavior and

characteristics.

This segment is still relatively small for the bio market, which means that the

customers would normally buy from normal supermarkets and retailers, rather than

going to health-food shops. Despite that, Bionade has proven successfully combining

the “bio” and youthful lifestyle orientation in the brand. One success factor is that

Bionade has managed to attract buyers by its appearance. Successful examples

show that advertising and packaging have features like “tasty”, “trendy” and “simple”

(easy to carry). Brand identities, advertising, packaging and retail outlet design have

an initial impact to develop customer’s curiosity of the product. Good taste, however,

would be the ultimate deciding factor to retain customer’s loyalty of the brand.

A Recent study from BioHandel (2007) stated that almost 78% of young customers

think of taste as the most important buying motive, followed by price (55.1%), and

habit/lifestyle (43.6%). Therefore, if the taste of the product can convince these

young customers, this target group would have a potential market opportunity, even

at a higher price. There is also a changing trend from the basic positive values to the

direction of more organic/bio awareness of young people.

3 Blind Taste Study

19

3 Blind Taste Study

The purpose of this section is to determine what characteristics of the Novel-

Lemonade compel with the general expectations of the future customer; as well as

the areas in which the product needs to be improved in order to meet the customers’

requirements in terms of smell, taste and general satisfaction when drinking the

Novel-Lemonade.

To achieve this purpose, we designed a blind tasting study. This includes the

comparison of the Novel-Lemonade against a selected competitor and, coupled with

a brief questionnaire; provides the most relevant information about the positioning of

the product in the customers preferences when compared to similar alternatives.

The evaluation of the product by the target market has been one of the major

concerns of this project. However, the delay in obtaining the pointed permissions

from the German Health Ministry for a public tasting, the delay in the delivery of

irreplaceable pieces of the brewing equipment and electricity problems during the

brewing process previous to the study, resulted in a very constraint blind tasting

study. Therefore the results are not representative, due to the scarcity of the sample.

3.1 Products

The volume of Novel-lemonade available for tasting was close to 1.8 liters of a sweet

“flavor”. It can be described as natural (no added flavoring) lemonade.

Since the study was designed to compare the Novel-Lemonade against an existing

product in the market, the group decided to benchmark our product against the

market leader within the defined segment, namely Bionade. This selection for the

tasting study also relies on the relative similarity of the products given that they are

both fermented. The herbal flavor of the Bionade Kräuter was thought to be

comparable to the expected tea-like flavor of the Novel-Lemonade.

3 Blind Taste Study

20

3.2 Survey

The survey comprehended two general questions, five questions per product and two

open boxes for additional comments from the participants.

There are several purposes the survey was designed to fulfill. In addition to the

information about the product, we yearned for confirmation that the target market

perceived the product the way it was conceived.

The first two questions, age and gender, served the purpose of fairness to the

sample - similar male and female participants - and to identify the preferences of the

sample, age being the distinguishing factor. It is well known that taste preferences

and the sensorial perception change during the different life stages(Mojet, et al.,

2001).

The second group of questions regarded the perception of the different features of

the product as well as the overall experience of the product in the eyes of the

participants. These questions included the perception of the appearance, the primary

(smell) and secondary (flavor) aromas, the acceptance of the taste/feeling and the

balance between the three of the five basic tastes (savory, sweet, sour, bitter and

salty) in the Novel-Lemonade.

Finally, the comment boxes added to the survey were an instrument to acquire as

much information as possible of the tasting experience. It serves to provide a more

detailed explanation of the answers given or as tool to suggest improvements subject

to personal tastes.

3.3 Study

The study was executed within the Technical University Hamburg-Harburg (TUHH).

Personnel from different departments allocated in buildings D and E participated in

the study.

The participants were approached by the team, briefly informed of what was the

purpose of the survey as well as what was demanded from them. To those who

agreed on participating, a printed copy of the questionnaire was provided,

accompanied by two small glasses (20ml) each containing one of the trial products.

3 Blind Taste Study

21

The Novel-Lemonade was always the first product to be evaluated by the participants

in order to avoid influenced participants being misled by other products features and

evade biased comments.

The participants were then asked to read the questionnaire and fill in their responses,

marking the responses from the ones provided that would best fit into the perception

of the different aspects of the drink. Participants were invited to add any further

comments they considered appropriate for the improvement of the product.

3.4 Results

3.5 Summary

Different areas of improvement were identified from exercising the blind tasting study.

There are additional highlights mentioned here that were extracted from the

recommendations provided in the comment boxes in the survey itself (please refer to

appendix Blind Tasting Comments in Table 7-4).

From the results we can settle upon the reduction of the strong malty smell of the

Novel-Lemonade. The impressions provided in the answers to the survey and in the

comment boxes is that the smell is unpleasant and rather misleading, since in few

cases it was associated to honey and the utter taste of the Novel-Lemonade is

completely different form this.

Another clear conclusion is the enhancement of the healthiness quality; this should

be achieved by providing a better balance of the basic tastes in the Novel-Lemonade.

Some participants (24%) perceived the product to be too sweet, even when the

natural sugar content is similar to that found in the benchmark Bionade.

3 Blind Taste Study

22

As a result, the question that arose in this regard is the suitability of sweetness to the

overall taste of the final product. “Would it be suitable to shift the ultimate taste of the

Novel-Lemonade towards a more fruity and refreshing product?” “Would it rather be

shifted towards a more settled and herbal flavor?” These questions must be

answered in the future preferably in collaboration with a food and drink taste

development expert.

Finally, we can deduct from the comments and the answers to the questionnaire, that

the flavor of the Novel-Lemonade should transmit a clear impression. This argument

is supported both on the “cannot tell” answers in the questionnaire, and on the

comments provided as feedback during the tasting study. It is important that the

overall product experience causes a favorable impression in the customers’ sensorial

memory; otherwise, the success of the product might be severely hampered.

4 Marketing Mix

23

4 Marketing Mix

Considering the findings of market, competitor, target customer analysis and the blind

taste study, the following suggestions for the marketing mix can be derived.

4.1 Product

The branding strategy and characteristics of the lemonade and its packaging greatly

determine consumer total product experience and satisfaction as well as differentiate

the product from the competitors. According to the market analysis, the key criteria

for success are taste, naturalness, healthiness and functional benefits. Our potential

target consumer group belongs to the age over 25 with health and sustainability

consciousness. The following section provides recommendations for the product

based on market trends, target customers analysis and analogies from Innocent Ltd..

4.1.1 Product strategy

“Healthiness and Indulgence” are suggested to be the key elements of the product

positioning and brand strategy. This means to provide healthy and functional

benefits, which are demanded by an increasing number of customers (Eickmeier,

2009) as well as to leave consumers with pleasurable experiences when drinking the

lemonade. It is highly important to ensure that the product and brand are completely

in synchrony for complete consistency.

The competitive features of our lemonade are its naturalness, healthiness, and

functional benefits. The product contains all-natural organic ingredients with no sugar

added in the process. These organic and ‘no added sugar’ features are

unquestionably appealing to the growing number of health conscious consumers.

Functional benefits from Vitamin B12 attract customers who have a particular need

for it, particularly, vegetarians and vegans. These healthy benefits are the key

competitive advantage that the Novel-Lemonade has over its current competitors.

4 Marketing Mix

24

The unique selling point of the product, vitamin B12 and naturalness, should be

emphasized in all aspects of branding and marketing strategy, e.g. brand name, label

design, selling places and promotion materials.

Flavor is a crucial factor. The majority of LOHAS customers consider taste as the

most important buying criteria in addition to naturalness and healthiness. They

demand products that have good taste, pleasant smell and provide functional

benefits to their health. The blind tasting results indicate that flavor and smell of the

Novel-Lemonade are an area of improvement. Based on the results, we suggest the

lemonade to be less sweet and malty, and increase fruitiness to make it more

refreshing. The smell has to be less pungent and enhanced with tea flavors. In

addition, it is crucial to keep consistency in the quality of the lemonade, including

consistency in flavor. Product line extensions by introducing new flavors could be

considered later on in order to satisfy customer needs for a greater variety.

AN

ALO

GY-

Inno

cent

Innocent is the UK’s leading smoothie brand that dominates the smoothies market

with a 73% share (Turner, 2008). They create the product from their principle, to

produce ‘natural drinks that taste good and do you good.’ Innocent ensures that there

is a good product at the heart of business, and believe that good reality and brand

image will follow. Before starting their business, they bought £500 worth of fruit,

turned it into smoothies and sold them from a stall at a music festival in London.

People were asked to put their empty bottles in a 'yes' or 'no' bin depending on

whether they thought the three entrepreneurs should quit their jobs to make

smoothies. At the end of the festival, the 'yes' bin was full, with only three cups in the

'no' bin, so they resigned from their works and started the business (Tryhorn, 2009).

Innocent also ensures that the product and brand are coherent. The brand is infused

with curiosity, fun and compassion. Innocent has put large effort to distance itself from

the corporate image and instead build a pure and student image as can be seen from

its witty packaging, Fruit towers premises, and grass covered vans. This alternative

image turns out to be an effective marketing ploy in a world increasingly disillusioned

with Americanization and corporate power.

4 Marketing Mix

25

AN

ALO

GY-

Inno

cent

Sustainability is Innocent’s core brand value. As the company continues to reassess

its carbon footprint, its ultimate aims are to become not an FMCG but an FMSG, with

the S standing for ‘Sustainable’. Innocent’s ‘Sustainability Squad’ is built around the

principle to procure ethically, reduce and offset carbon emissions, recycle and give

something back through charitable giving. Its fruit suppliers have to meet minimum

International Labor Organization standards and premium rates are paid to Rainforest

Alliance-accredited or local farms. Electricity comes from green renewable sources.

Fleet vehicles are powered either by bio fuels, LPG or hybrid. CO2 emissions are

measured each month and are offset by 120% to be carbon negative across the

business (Growingbusiness, 2007). It also recently introduced bottles that are 100%

recyclable.

4.1.2 Packaging

There are many important decisions to make concerning the bottle: reusability,

material, size, shape and bottle cap. These decisions are strategic, since it is not

possible to change the type of bottle that is used overnight; mainly, because there is

much capital tied up in the bottles and the cases. Also, the decision about the bottle

characteristics affects the feasible distribution channels.

First of all it needs to be decided if the bottle should be one-way or reusable. This

decision affects the shape and the material of the bottle. Furthermore, Germany has

very strict regulations (Verpackungsverordnung, 2010) about bottle deposit. Since the

lemonade is carbonated it must be sold in a returnable bottle, regardless of whether it

is sold in a glass or plastic bottle and whether it is a one-way or reusable bottle.

There is a trend that beverages are increasingly sold in one-way plastic bottles.

Almost 90% of the sold drinks for home use are filled in these bottles nowadays4.

Nevertheless for organic lemonades with LOHAS, vegetarians and vegans as a

target group, the drinks should be filled in reusable glass bottles. On the one hand it

actually is more environmentally friendly and, on the other hand, it shows that the

company cares for issues like these which are also important for the target group.

Furthermore, in restaurants and bars it is the only way to sell drinks. Another

important fact that supports the decision to use a glass bottle is the extended shelf-

life (time of permanency) in comparison to plastic bottles which are not 100% airtight.

4 Statistic of WAFG, which is not available for the public

4 Marketing Mix

26

The lemonade, especially placed in health-food shops, might not be a fast moving

product, is dependent on a preferably long time of permanency. A collection of more

reasons that support the use of a glass bottle can be found here (Leonhardt, et al.,

2010).

For the sales in restaurants, bars and clubs the 0.33L bottle is the most common

size. If sold in shops and stores, 0.5L bottles are more favorable to some customers

and should be provided as well.

Reusable glass bottles are available in a huge variety of shapes on the German

beverage market. It would be desirable to have a “designer bottle” to show the

uniqueness of the product, but it is much more cost-efficient to select the standard

bottle. It is easier for logistic purposes and for finding a bottler who is capable of filling

the bottles. The glass will be transparent so that the lemonade is shown it its natural

color. The 0.33L bottle usually is a longneck bottle and comes with a crown cap. For

the 0.5L bottle a screw cap is more convenient.

To point out the importance of this decision some interesting financial figures are

given. (Lübbermann, 2011)

� Cost of the cheapest standard bottle case: ca. 3.00€

Deposit for a bottle case in the store: 1.50€

� Cost of the cheapest standard bottle: ca. 0.12€

Deposit for a bottle: 0.08€

This means that with every case of lemonade sold, the company is losing money at

first. A huge investment is necessary in the beginning to buy cases and bottles. That

is the reason why by all means standard bottles and cases should be used.

There are two ways to reduce the financial loss. Including a bigger margin for the

company or increasing the deposit for the bottles. The 0.08€ deposit per bottle is the

legal minimum but it can be increased by the company, e.g. to 0.15€ per bottle. This

would be an alternative to avoid a higher selling price for the customer.

Finally, the label for the bottle has to be defined. It should be a standard label

concerning size and material. Every other option would be too expensive and also

not usable in some bottling facilities. There are many regulations that have to be

4 Marketing Mix

27

followed to comply with legal issues. Detailed information about batch number and

ingredients has to be on the label and there are many formalities like font size that

have to be considered. We strongly recommend seeking the advice of an expert in

order to cope with those issues. The image and unique selling point of the product

should be expressed on the label. This includes mentioning and graphically

emphasizing the ‘vitamin B12’, ‘no added sugar’ and the “Bio label”. The nutritional

facts should also show amount of vitamin B12, natural sugar in addition to standard

information.

Bio

labe

l

To use this label, manufacturers need to be annually certified

by one of the registered certification agencies. At least 95%

of the agricultural ingredients contained in processed

products must come from organic production (Bio-Siegel

Information Centre, 2006). The remaining ingredients of

agricultural origin must be listed in Annex VI Part C of the EU

Regulation on Organic Farming. The list of ingredients has to be printed on the

label. The certification costs depend on the produced amount of lemonade. For the

first year, it will probably be beyond a certain limitation and cost 300€ flat rate

(Lübbermann, 2011).

The criteria to qualify for the Bio label are not very high and, past industry

experiences show that it is generously issued by the certification agencies, which

means that the actual value of this label should not be overestimated. The

consumers mostly do not know about this fact and trust the label (EARSANDEYES

GmbH, 2006 p. 27) though, which is why we definitely recommend using the Bio

label. There is a great variety of organic labels with different requirements. A

summary and a list of certification agencies can be found in the article by Richter

(2005 p. 7 ff.).

4.1.3 Summary

Healthiness and indulgence are recommended as key features for product

positioning and branding. Healthiness and functional benefits are the competitive

features of our product; therefore, they should be emphasized in all aspects of brand

strategy. Flavor is one of the most important buying criteria that largely determine

consumer experience with the product. Based on the tasting results, we suggest the

product to be less sweet and malty in taste, fruitier and less pungent in smell, and

4 Marketing Mix

28

enhanced with flavors. The bottle should be a standard glass bottle having the sizes

of 0.33L and 0.5L. We also suggest using a standard label in term of size and

material, which should graphically express the brand image and the unique selling

point of the product, including Bio label and mentioning of the vitamin B12 content.

With regards to batch number, ingredients, and other formalities, consulting an expert

is recommended.

4.2 Place

This chapter includes several explanations about possible points of sale and the

distribution channels that should be targeted. Furthermore, the sales area has to be

defined given its close connection to the decision about the location of production.

4.2.1 Beverage distribution in Germany

In order to propose the suitable points of sale, it is necessary to take a closer look at

the whole distribution system of beverages in Germany. The customers can buy

drinks in discounters, supermarkets, beverage markets, kiosks and, of course, for

immediate consumption in bars, restaurants, clubs, etc. Especially organic

lemonades are also available in health-food shops and wholefood supermarkets.

From the perspective of the manufacturer those points of sale are not necessarily the

ultimate customers. Usually, beverage sales are organized in multi-level distribution

systems, with slight differences depending on the final point of sale. In most cases

the manufacturer sells the beverages to a wholesaler. If the beverage is sold in a

restaurant, bar or club, there is usually one more level in between, a local trader. If

not, the wholesaler mostly sells directly to the supermarket or beverage market. It

depends on the received bulk and on the size of the customer whether a local trader

is required or not.

4 Marketing Mix

29

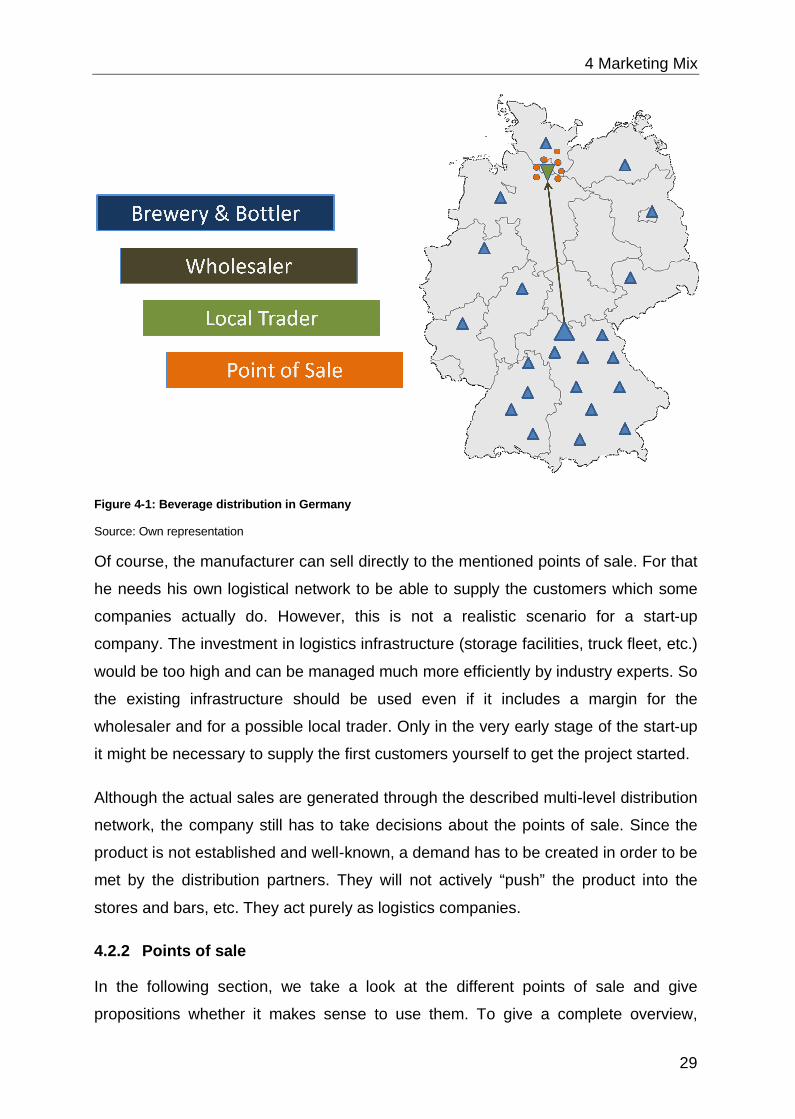

Figure 4-1: Beverage distribution in Germany

Source: Own representation

Of course, the manufacturer can sell directly to the mentioned points of sale. For that

he needs his own logistical network to be able to supply the customers which some

companies actually do. However, this is not a realistic scenario for a start-up

company. The investment in logistics infrastructure (storage facilities, truck fleet, etc.)

would be too high and can be managed much more efficiently by industry experts. So

the existing infrastructure should be used even if it includes a margin for the

wholesaler and for a possible local trader. Only in the very early stage of the start-up

it might be necessary to supply the first customers yourself to get the project started.

Although the actual sales are generated through the described multi-level distribution

network, the company still has to take decisions about the points of sale. Since the

product is not established and well-known, a demand has to be created in order to be

met by the distribution partners. They will not actively “push” the product into the

stores and bars, etc. They act purely as logistics companies.

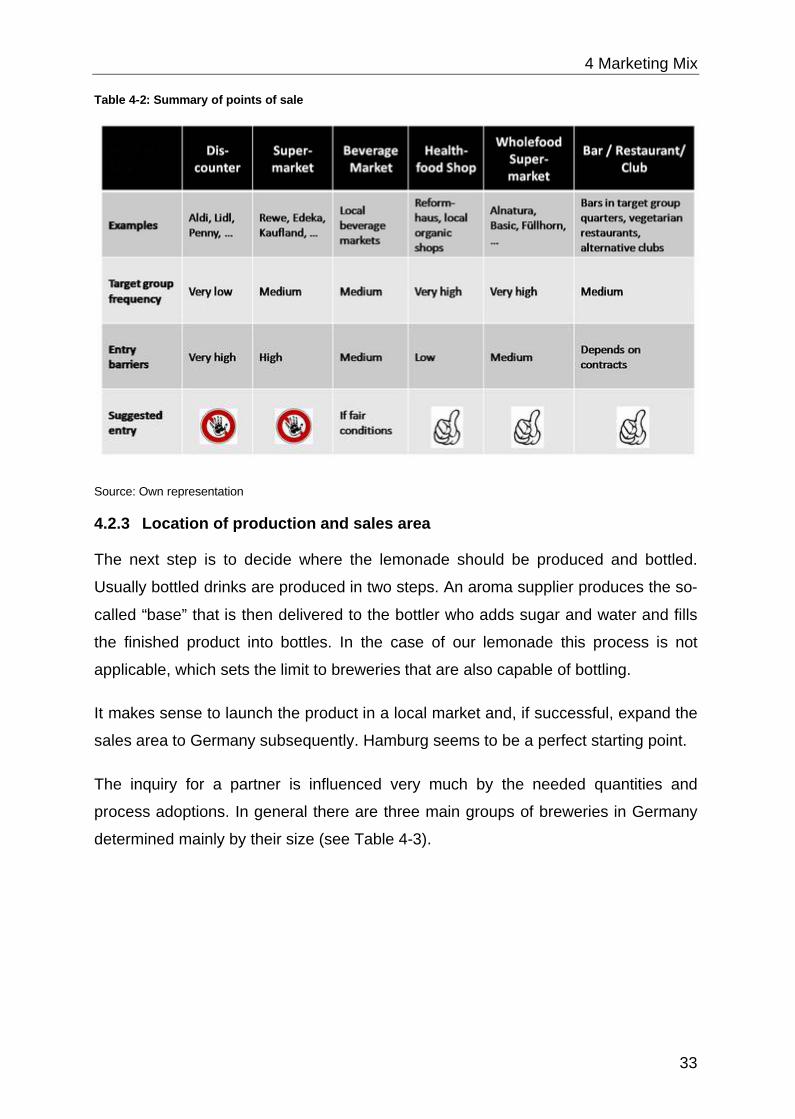

4.2.2 Points of sale

In the following section, we take a look at the different points of sale and give

propositions whether it makes sense to use them. To give a complete overview,

4 Marketing Mix

30

which is very important to understand the beverage business, all points of sale are

examined. As described before, it is required to find your way into those points of

sale by your own initiative. Firstly, the opportunities for take-away purchase are

listed.

Discounters

Discounters are very popular in Germany and register increasing beverage sales

annually. That is the most important reason for the decreasing multi-cycle quota of

bottles. However, it is not realistic to use discounters as a distribution channel at all.

They are limited to very few products in their shelves, and need to be extremely fast

moving. The lemonade will not be one of those products due to its comparatively high

price. Also there are so-called listing fees to place the product in the assortment of

the discounter in the first place. Given the fact that our described target group is not

consistent with the target group of discounters, it would be questionable if substantial

sales could be realized.

Supermarkets

Supermarkets are quite similar to discounters when it comes to listing fee issues.

REWE asked for 2.4 million € listing fees plus price discounts between 5% and 8%

when Bionade was first interested in being listed in their assortment (Weiguny, 2009

S. 189). Our inquiries5 have shown that supermarkets are mostly not willing to

support “small” products or that it is at least very hard to convince them. They should

not be considered in this phase of the start-up.

Beverage markets

Beverage markets are a German phenomenon, in other countries sales are mostly

generated in supermarkets. It has become more and more difficult for beverage

markets to survive and they are rapidly losing their market share. Nevertheless, those

markets are an elegant way to sell greater bulks of a beverage since the customer

usually comes by car and uses special shopping carts to carry whole cases of drinks.

It is said that those markets are making money not through their sales but through

their smart purchasing. They are asking their suppliers to provide all sorts of

5 Inquiries at Edeka, REWE, Teegut and Budnikowsky

4 Marketing Mix

31

incentives, bonuses, listing fees6, free samples, etc. It is not easy for an

inexperienced start-up to cope with those tricks. Only those beverage market that

seem to run their business in a fair way should be considered as partners.

Health-food-shops

Health-food shops are small businesses specialized in - like the term says - healthy

which mostly means organic food. Some are organized in chains, e.g. Reformhaus,

and are selling a broad variety of health-related products, not limited to food. Most of

them are just small owner-managed shops. They are addressing the exact same

target group as our lemonade and should be considered a main point of sale.

Wholefood supermarkets

Wholefood supermarkets are offering a similar assortment as the health-food shops,

but they are organized in huge chains. Also the stores are much bigger concerning

shelf spaces. The same as the health-food shops they are aligned to the same target

groups as the lemonade and therefore should be concentrated on. The following

table gives an overview over Germany’s key players.

Table 4-1: Wholefood supermarket chains in Germany

Source: Organic-Market.info, *estimate

Kiosks

Kiosks are not frequented sufficiently enough by our target group to form a

reasonable point of sale.

6 1,000€ per beverage market if you cooperate with „trinks“, one of the big players (Lübbermann, 2011)

4 Marketing Mix

32

In the following points of sale the beverage is consumed immediately and therefore

mostly sold in single units.

Bars, restaurants and clubs

Bars, restaurants and clubs often have contracts with beverage manufacturers. The

manufacturers provide them with credits and interior accessories (bar signs,

umbrellas, bar equipment, etc.). In return the bars have long-term contracts with the

manufacturers and are allowed to sell just their drinks. This means that they have to

be approached individually and even if it takes a great effort, these channels should

not be disregarded. They have a great potential, also as a multiplier considering

promotion. Most of the drinks that started as start-ups, got popular through the sales

in clubs and bars. There probably are locations that are visited more frequently by

our target group than others and, these definitely should be addressed at first. As an

example there are vegetarian restaurants, alternative clubs and bars in certain areas

of a city where the target groups tends to live.

Additionally the canteens of Hamburg’s universities, managed by the

Studierendenwerk Hamburg, should be regarded as a point of sale.

The points of sale, their characteristics and our recommendations are summarized in

the following table.

4 Marketing Mix

33

Table 4-2: Summary of points of sale

Source: Own representation

4.2.3 Location of production and sales area

The next step is to decide where the lemonade should be produced and bottled.

Usually bottled drinks are produced in two steps. An aroma supplier produces the so-

called “base” that is then delivered to the bottler who adds sugar and water and fills

the finished product into bottles. In the case of our lemonade this process is not

applicable, which sets the limit to breweries that are also capable of bottling.

It makes sense to launch the product in a local market and, if successful, expand the

sales area to Germany subsequently. Hamburg seems to be a perfect starting point.

The inquiry for a partner is influenced very much by the needed quantities and

process adoptions. In general there are three main groups of breweries in Germany

determined mainly by their size (see Table 4-3).

4 Marketing Mix

34

Table 4-3: Sizes of breweries in Germany

Size Big Medium Small

ExampleHolstenOettingerKrombacher

KneitingerBischofshofCeller Bier

Brauhaus Johannes AlbrechtMälzer's Brau- u. Tafelhaus

Sales area International / National Regional (national) LocalCooperation Difficult Realistic DifficultQuantities Very high high smallPrice & Service Good Good insufficient

Source: Own representation

After contacting multiple breweries, it resulted, that small breweries are not suitable

for cooperation. They mainly belong to hotels or restaurants and brew only for the

demand there. Usually those breweries are not able to either provide the bottling or

sufficient quantities.

Big players can realize all process steps and even give support in regard of logistics

and distribution. Their facilities offer a high efficiency and thereby a good price. The

scale of those companies on the other side also generates difficulties. E.g. the

minimum amount that the Holsten AG will accept for a contractor is one charge at the

size of 2,000hl, which is delivered in just about 14 days (Rauschenbach, 2010).

Additionally the requirements for a contract are very high; because these companies

cannot risk that their brewing equipment to infiltration of foreign organisms. As a

consequence a lot of detailed information (possible conflict with patent & secrecy) is

needed and even adjustments of the brewing process of the Novel-Lemonade might

be needed.

Mid-sized breweries seem to be the best fitting partners for the given conditions.

They are able to perform the brewing processes as well as bottling and labeling.

The decision about the location of production is strategic since it is difficult to switch it

afterwards. For that reason, a location in the central area or of Germany should be

chosen. In that way it is no problem to extend the sales area in the future. Due to

cultural development in Germany it turns out, that the scenery of breweries in

Germany is not homogeneous. In 2008 Germany had 1,319 breweries, with 628 of

them located in Bavaria (Statistisches Bundesamt, 2008). The reason for such a

large amount is that in Bavaria a huge variety of mid-sized breweries is located and

makes it a predestined area for partner companies.

4 Marketing Mix

35

4.2.4 Distribution system

After production, bottling and labeling, which is done by a contracted brewery in a

probably monthly rhythm, a wholesaler transports the goods to his storage facilities or

directly to a local trader. The local trader supplies bars, restaurants and clubs in

shorter intervals on demand. The same is valid for wholefood-supermarkets and

health-food shops that are directly supplied by the wholesaler.

Verb

and

korr

ekte

rGet

ränk

eher

stel

lere

.V.

It would make sense to use an existing distribution network

to save the work of organizing it yourself. Therefore we

recommend cooperating with the network of the “Verband

korrekter Getränkehersteller e.V.”. It is located in Hamburg

and can be described as a cooperation of some mostly

Hamburg-based beverage producers that try to run their

businesses in a fair and sustainable way. So far, the

members of the network are: Viva con Aqua, Premium

Cola, LemonAid, ChariTea, BierBier, Karl Mölle Getränke

and Hermann-Kola. Their aim is cooperating with regard to distribution and sharing

of information, ideas and contacts. Our product and company fits perfectly into this

network. Especially for a start-up, the network’s experiences would help to get the

company on the right way.

As described earlier, the wholesaler and local traders are, in the case of an unknown

product, not promoting it so much to their customers. For that reason, our company

has to convince the different points of sale itself. Usually salesmen are used in order

to acquire new customers. There is one company we are using here as an analogy,

that provides a new approach.

AN

ALO

GY

Prem

ium

Col

a

In this concept, literally everybody can participate in the company’s success. The

system is easy. People go into bars and promote the product. If they successfully

set up a deal, they receive a certain amount of money per bottle (0.04€) which is

sold in that bar as an incentive. In return, they have to undertake the task of

customer care.

4 Marketing Mix

36

4.2.5 Summary

As observed in this section, the beverage distribution system in Germany is very

complex. Hence, to maintain the opportunity of expanding the sales area to entire

Germany in the future, the contracted brewery should be located in the central area

of the country (such as the north of Bavaria). In the beginning, the points of sale are

most suitably to be located in Hamburg; consisting of health-food stores, wholefood

supermarkets and suitable bars, clubs and restaurants. For these reasons, consulting

the “Verband korrekter Getränkehersteller e.V.” for cooperation with regard to its

distribution network will help to find a suitable wholesaler to take care of logistics.

4.3 Price

It is essential for a successful product launch to set the price “right”. A broad study

has to be made in order to determine the customers’ willingness to pay. Due to the

unstable product and the along coming lack in taste, there was no sense in adding

questions regarding the price into the questionnaire of the blind taste.

Therefore the price for the Novel-Lemonade is calculated based on information about

competitors, production costs and profit margins of each level to the customer.

4.3.1 Market prices

As first aspect, the prices of competitors shall be taken into account. Table 4-4 shows

the prices of competing products in a German wholefood supermarket for the end

customer and the retail price from the wholesaler to the supermarket.

Table 4-4: Prices of competitors for retailers and customers (0.33L bottles)