Embed Size (px)

Citation preview

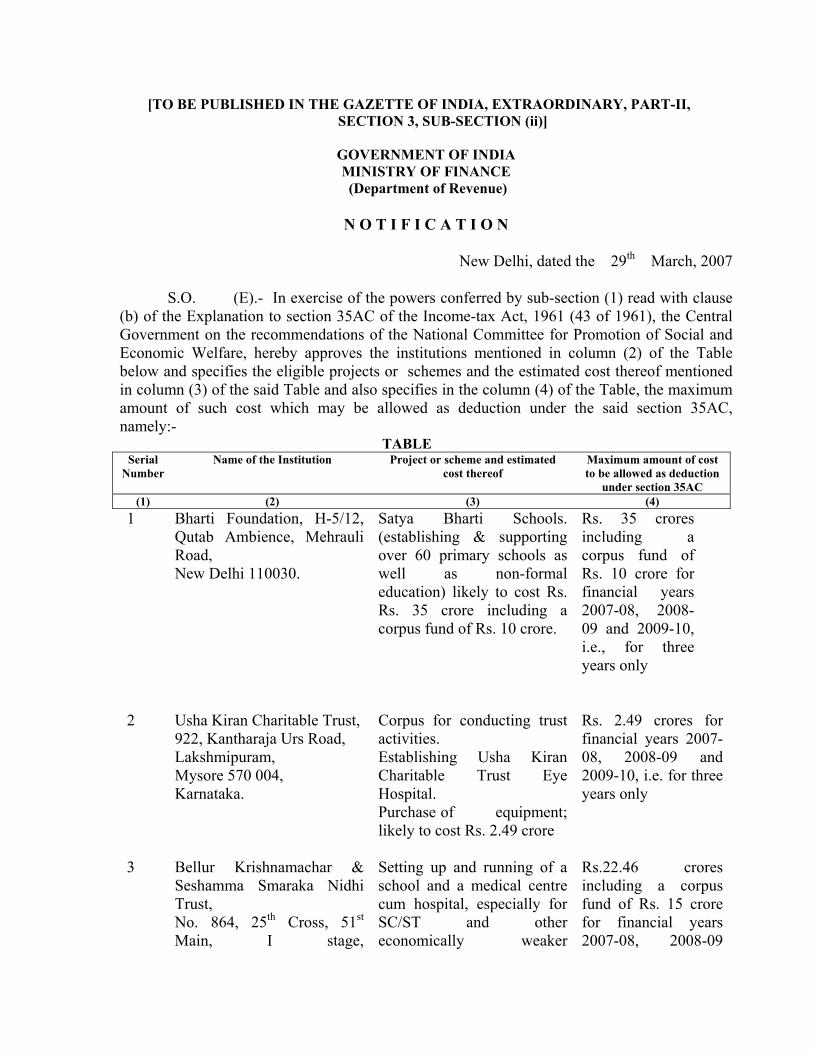

[TO BE PUBLISHED IN THE GAZETTE OF INDIA, EXTRAORDINARY, PART-II, SECTION 3, SUB-SECTION (ii)]

GOVERNMENT OF INDIA MINISTRY OF FINANCE (Department of Revenue)

N O T I F I C A T I O N

New Delhi, dated the 29th March, 2007

S.O. (E).- In exercise of the powers conferred by sub-section (1) read with clause

(b) of the Explanation to section 35AC of the Income-tax Act, 1961 (43 of 1961), the Central Government on the recommendations of the National Committee for Promotion of Social and Economic Welfare, hereby approves the institutions mentioned in column (2) of the Table below and specifies the eligible projects or schemes and the estimated cost thereof mentioned in column (3) of the said Table and also specifies in the column (4) of the Table, the maximum amount of such cost which may be allowed as deduction under the said section 35AC, namely:-

TABLE Serial

Number Name of the Institution Project or scheme and estimated

cost thereof Maximum amount of cost to be allowed as deduction

under section 35AC (1) (2) (3) (4)

1 Bharti Foundation, H-5/12, Qutab Ambience, Mehrauli Road, New Delhi 110030.

Satya Bharti Schools. (establishing & supporting over 60 primary schools as well as non-formal education) likely to cost Rs. Rs. 35 crore including a corpus fund of Rs. 10 crore.

Rs. 35 crores including a corpus fund of Rs. 10 crore for financial years 2007-08, 2008-09 and 2009-10, i.e., for three years only

2 Usha Kiran Charitable Trust, 922, Kantharaja Urs Road, Lakshmipuram, Mysore 570 004, Karnataka.

Corpus for conducting trust activities. Establishing Usha Kiran Charitable Trust Eye Hospital. Purchase of equipment; likely to cost Rs. 2.49 crore

Rs. 2.49 crores for financial years 2007-08, 2008-09 and 2009-10, i.e. for three years only

3 Bellur Krishnamachar & Seshamma Smaraka Nidhi Trust, No. 864, 25th Cross, 51st Main, I stage,

Setting up and running of a school and a medical centre cum hospital, especially for SC/ST and other economically weaker

Rs.22.46 crores including a corpus fund of Rs. 15 crore for financial years 2007-08, 2008-09

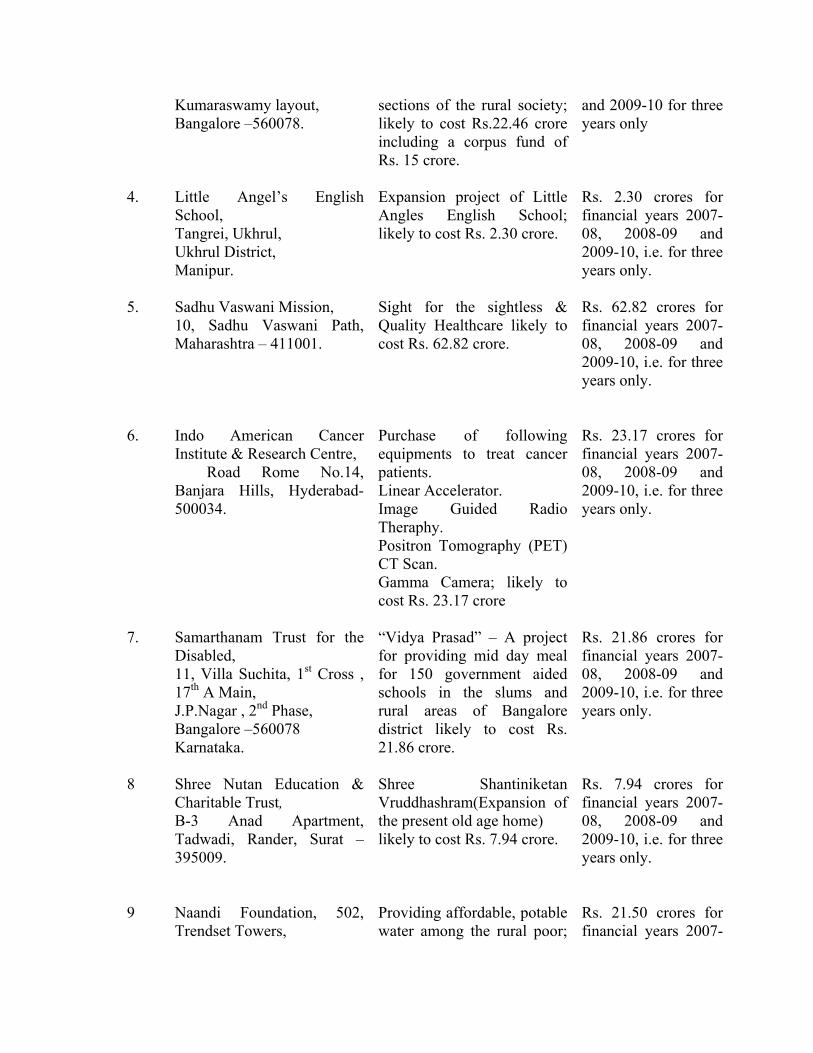

Kumaraswamy layout, Bangalore –560078.

sections of the rural society; likely to cost Rs.22.46 crore including a corpus fund of Rs. 15 crore.

and 2009-10 for three years only

4. Little Angel’s English School, Tangrei, Ukhrul, Ukhrul District, Manipur.

Expansion project of Little Angles English School; likely to cost Rs. 2.30 crore.

Rs. 2.30 crores for financial years 2007-08, 2008-09 and 2009-10, i.e. for three years only.

5. Sadhu Vaswani Mission, 10, Sadhu Vaswani Path, Maharashtra – 411001.

Sight for the sightless & Quality Healthcare likely to cost Rs. 62.82 crore.

Rs. 62.82 crores for financial years 2007-08, 2008-09 and 2009-10, i.e. for three years only.

6. Indo American Cancer Institute & Research Centre, Road Rome No.14, Banjara Hills, Hyderabad-500034.

Purchase of following equipments to treat cancer patients. Linear Accelerator. Image Guided Radio Theraphy. Positron Tomography (PET) CT Scan. Gamma Camera; likely to cost Rs. 23.17 crore

Rs. 23.17 crores for financial years 2007-08, 2008-09 and 2009-10, i.e. for three years only.

7.

Samarthanam Trust for the Disabled, 11, Villa Suchita, 1st Cross , 17th A Main, J.P.Nagar , 2nd Phase, Bangalore –560078 Karnataka.

“Vidya Prasad” – A project for providing mid day meal for 150 government aided schools in the slums and rural areas of Bangalore district likely to cost Rs. 21.86 crore.

Rs. 21.86 crores for financial years 2007-08, 2008-09 and 2009-10, i.e. for three years only.

8 Shree Nutan Education & Charitable Trust, B-3 Anad Apartment, Tadwadi, Rander, Surat – 395009.

Shree Shantiniketan Vruddhashram(Expansion of the present old age home) likely to cost Rs. 7.94 crore.

Rs. 7.94 crores for financial years 2007-08, 2008-09 and 2009-10, i.e. for three years only.

9 Naandi Foundation, 502, Trendset Towers,

Providing affordable, potable water among the rural poor;

Rs. 21.50 crores for financial years 2007-

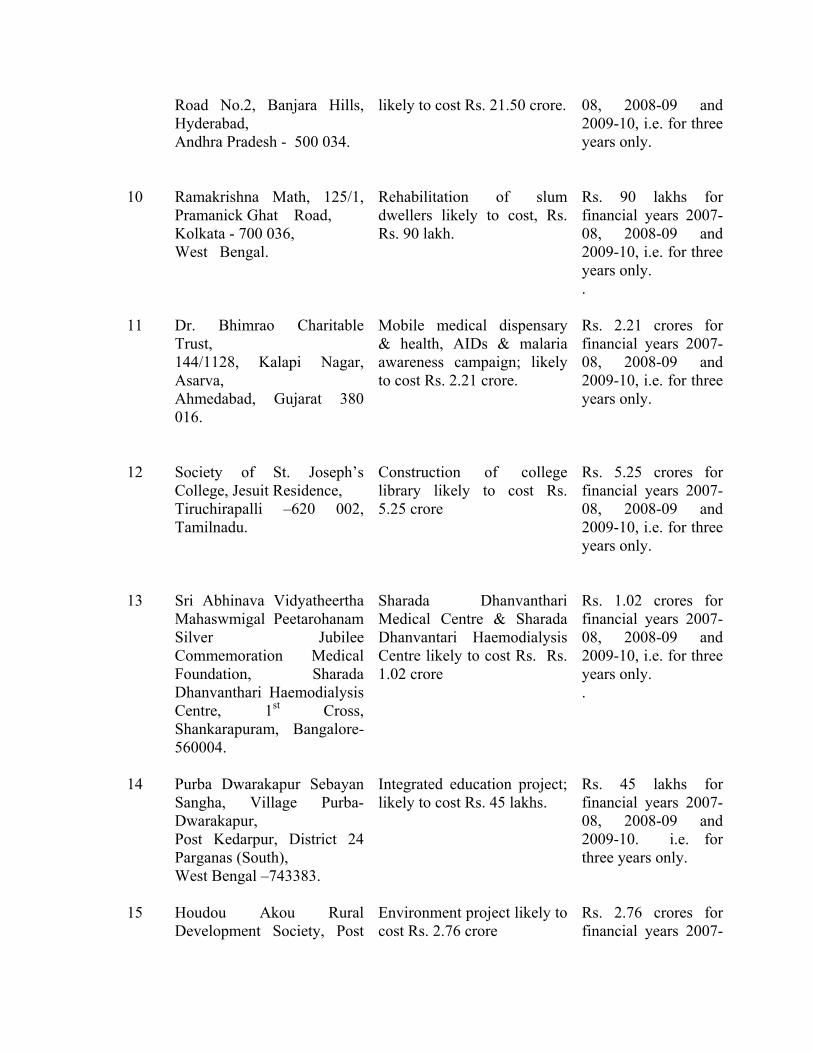

Road No.2, Banjara Hills, Hyderabad, Andhra Pradesh - 500 034.

likely to cost Rs. 21.50 crore.

08, 2008-09 and 2009-10, i.e. for three years only.

10 Ramakrishna Math, 125/1, Pramanick Ghat Road, Kolkata - 700 036, West Bengal.

Rehabilitation of slum dwellers likely to cost, Rs. Rs. 90 lakh.

Rs. 90 lakhs for financial years 2007-08, 2008-09 and 2009-10, i.e. for three years only. .

11 Dr. Bhimrao Charitable Trust, 144/1128, Kalapi Nagar, Asarva, Ahmedabad, Gujarat 380 016.

Mobile medical dispensary & health, AIDs & malaria awareness campaign; likely to cost Rs. 2.21 crore.

Rs. 2.21 crores for financial years 2007-08, 2008-09 and 2009-10, i.e. for three years only.

12 Society of St. Joseph’s College, Jesuit Residence, Tiruchirapalli –620 002, Tamilnadu.

Construction of college library likely to cost Rs. 5.25 crore

Rs. 5.25 crores for financial years 2007-08, 2008-09 and 2009-10, i.e. for three years only.

13 Sri Abhinava Vidyatheertha Mahaswmigal Peetarohanam Silver Jubilee Commemoration Medical Foundation, Sharada Dhanvanthari Haemodialysis Centre, 1st Cross, Shankarapuram, Bangalore-560004.

Sharada Dhanvanthari Medical Centre & Sharada Dhanvantari Haemodialysis Centre likely to cost Rs. Rs. 1.02 crore

Rs. 1.02 crores for financial years 2007-08, 2008-09 and 2009-10, i.e. for three years only. .

14 Purba Dwarakapur Sebayan Sangha, Village Purba- Dwarakapur, Post Kedarpur, District 24 Parganas (South), West Bengal –743383.

Integrated education project; likely to cost Rs. 45 lakhs.

Rs. 45 lakhs for financial years 2007-08, 2008-09 and 2009-10. i.e. for three years only.

15 Houdou Akou Rural Development Society, Post

Environment project likely to cost Rs. 2.76 crore

Rs. 2.76 crores for financial years 2007-

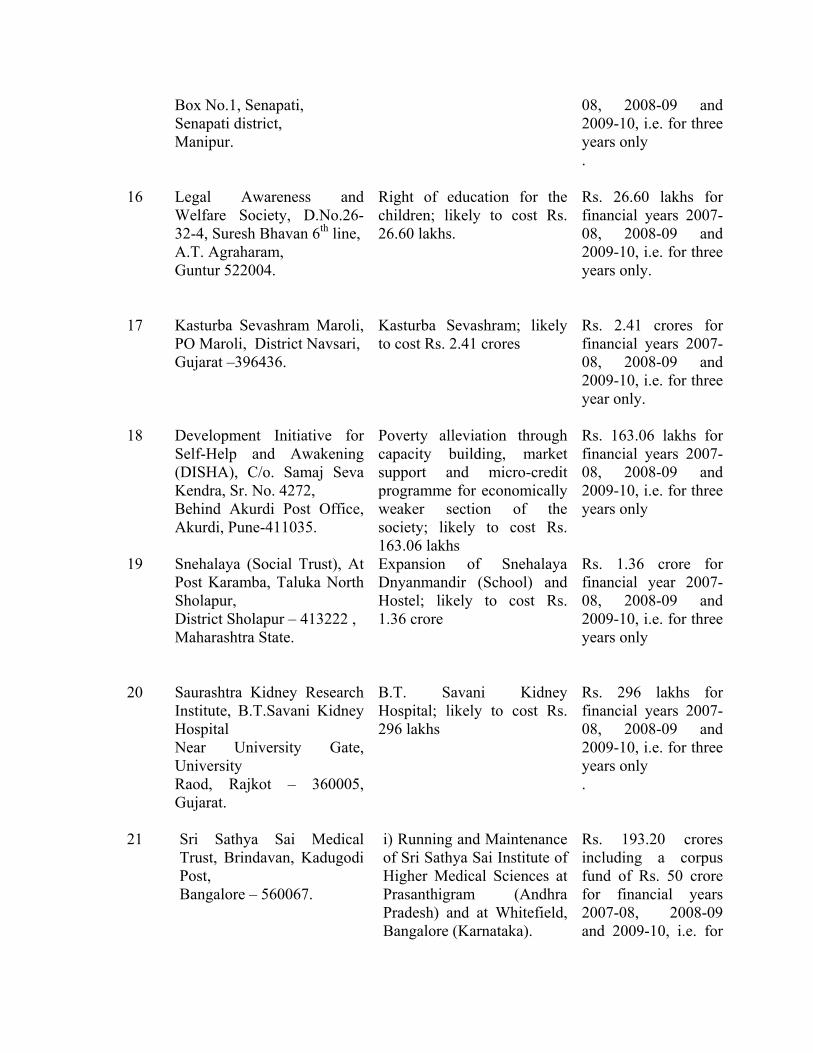

Box No.1, Senapati, Senapati district, Manipur.

08, 2008-09 and 2009-10, i.e. for three years only .

16 Legal Awareness and Welfare Society, D.No.26-32-4, Suresh Bhavan 6th line, A.T. Agraharam, Guntur 522004.

Right of education for the children; likely to cost Rs. 26.60 lakhs.

Rs. 26.60 lakhs for financial years 2007-08, 2008-09 and 2009-10, i.e. for three years only.

17 Kasturba Sevashram Maroli, PO Maroli, District Navsari, Gujarat –396436.

Kasturba Sevashram; likely to cost Rs. 2.41 crores

Rs. 2.41 crores for financial years 2007-08, 2008-09 and 2009-10, i.e. for three year only.

18 Development Initiative for Self-Help and Awakening (DISHA), C/o. Samaj Seva Kendra, Sr. No. 4272, Behind Akurdi Post Office, Akurdi, Pune-411035.

Poverty alleviation through capacity building, market support and micro-credit programme for economically weaker section of the society; likely to cost Rs. 163.06 lakhs

Rs. 163.06 lakhs for financial years 2007-08, 2008-09 and 2009-10, i.e. for three years only

19 Snehalaya (Social Trust), At Post Karamba, Taluka North Sholapur, District Sholapur – 413222 , Maharashtra State.

Expansion of Snehalaya Dnyanmandir (School) and Hostel; likely to cost Rs. 1.36 crore

Rs. 1.36 crore for financial year 2007-08, 2008-09 and 2009-10, i.e. for three years only

20 Saurashtra Kidney Research Institute, B.T.Savani Kidney Hospital Near University Gate, University Raod, Rajkot – 360005, Gujarat.

B.T. Savani Kidney Hospital; likely to cost Rs. 296 lakhs

Rs. 296 lakhs for financial years 2007-08, 2008-09 and 2009-10, i.e. for three years only .

21 Sri Sathya Sai Medical Trust, Brindavan, Kadugodi Post, Bangalore – 560067.

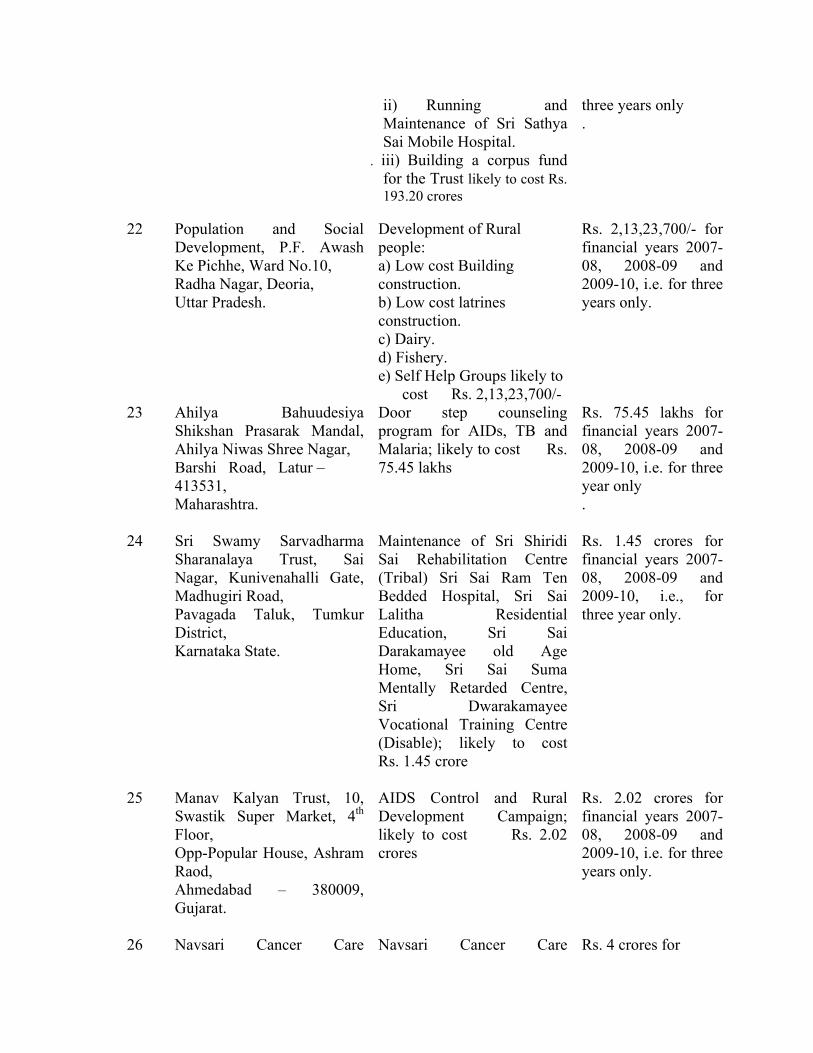

i) Running and Maintenance of Sri Sathya Sai Institute of Higher Medical Sciences at Prasanthigram (Andhra Pradesh) and at Whitefield, Bangalore (Karnataka).

Rs. 193.20 crores including a corpus fund of Rs. 50 crore for financial years 2007-08, 2008-09 and 2009-10, i.e. for

ii) Running and Maintenance of Sri Sathya Sai Mobile Hospital.

. iii) Building a corpus fund for the Trust likely to cost Rs. 193.20 crores

three years only .

22 Population and Social Development, P.F. Awash Ke Pichhe, Ward No.10, Radha Nagar, Deoria, Uttar Pradesh.

Development of Rural people: a) Low cost Building construction. b) Low cost latrines construction. c) Dairy. d) Fishery. e) Self Help Groups likely to

cost Rs. 2,13,23,700/-

Rs. 2,13,23,700/- for financial years 2007-08, 2008-09 and 2009-10, i.e. for three years only.

23 Ahilya Bahuudesiya Shikshan Prasarak Mandal, Ahilya Niwas Shree Nagar, Barshi Road, Latur – 413531, Maharashtra.

Door step counseling program for AIDs, TB and Malaria; likely to cost Rs. 75.45 lakhs

Rs. 75.45 lakhs for financial years 2007-08, 2008-09 and 2009-10, i.e. for three year only .

24 Sri Swamy Sarvadharma Sharanalaya Trust, Sai Nagar, Kunivenahalli Gate, Madhugiri Road, Pavagada Taluk, Tumkur District, Karnataka State.

Maintenance of Sri Shiridi Sai Rehabilitation Centre (Tribal) Sri Sai Ram Ten Bedded Hospital, Sri Sai Lalitha Residential Education, Sri Sai Darakamayee old Age Home, Sri Sai Suma Mentally Retarded Centre, Sri Dwarakamayee Vocational Training Centre (Disable); likely to cost Rs. 1.45 crore

Rs. 1.45 crores for financial years 2007-08, 2008-09 and 2009-10, i.e., for three year only.

25 Manav Kalyan Trust, 10, Swastik Super Market, 4th Floor, Opp-Popular House, Ashram Raod, Ahmedabad – 380009, Gujarat.

AIDS Control and Rural Development Campaign; likely to cost Rs. 2.02 crores

Rs. 2.02 crores for financial years 2007-08, 2008-09 and 2009-10, i.e. for three years only.

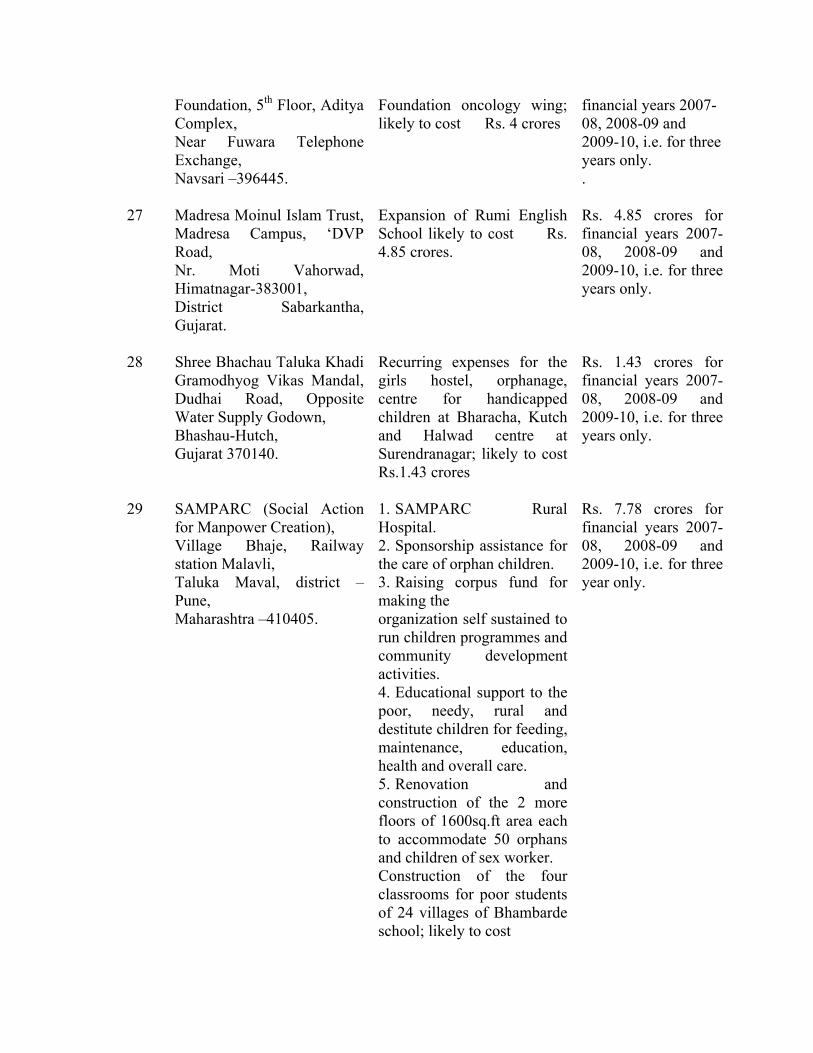

26 Navsari Cancer Care Navsari Cancer Care Rs. 4 crores for

Foundation, 5th Floor, Aditya Complex, Near Fuwara Telephone Exchange, Navsari –396445.

Foundation oncology wing; likely to cost Rs. 4 crores

financial years 2007-08, 2008-09 and 2009-10, i.e. for three years only. .

27 Madresa Moinul Islam Trust, Madresa Campus, ‘DVP Road, Nr. Moti Vahorwad, Himatnagar-383001, District Sabarkantha, Gujarat.

Expansion of Rumi English School likely to cost Rs. 4.85 crores.

Rs. 4.85 crores for financial years 2007-08, 2008-09 and 2009-10, i.e. for three years only.

28 Shree Bhachau Taluka Khadi Gramodhyog Vikas Mandal, Dudhai Road, Opposite Water Supply Godown, Bhashau-Hutch, Gujarat 370140.

Recurring expenses for the girls hostel, orphanage, centre for handicapped children at Bharacha, Kutch and Halwad centre at Surendranagar; likely to cost Rs.1.43 crores

Rs. 1.43 crores for financial years 2007-08, 2008-09 and 2009-10, i.e. for three years only.

29 SAMPARC (Social Action for Manpower Creation), Village Bhaje, Railway station Malavli, Taluka Maval, district –Pune, Maharashtra –410405.

1. SAMPARC Rural Hospital. 2. Sponsorship assistance for the care of orphan children. 3. Raising corpus fund for making the organization self sustained to run children programmes and community development activities. 4. Educational support to the poor, needy, rural and destitute children for feeding, maintenance, education, health and overall care. 5. Renovation and construction of the 2 more floors of 1600sq.ft area each to accommodate 50 orphans and children of sex worker. Construction of the four classrooms for poor students of 24 villages of Bhambarde school; likely to cost

Rs. 7.78 crores for financial years 2007-08, 2008-09 and 2009-10, i.e. for three year only.

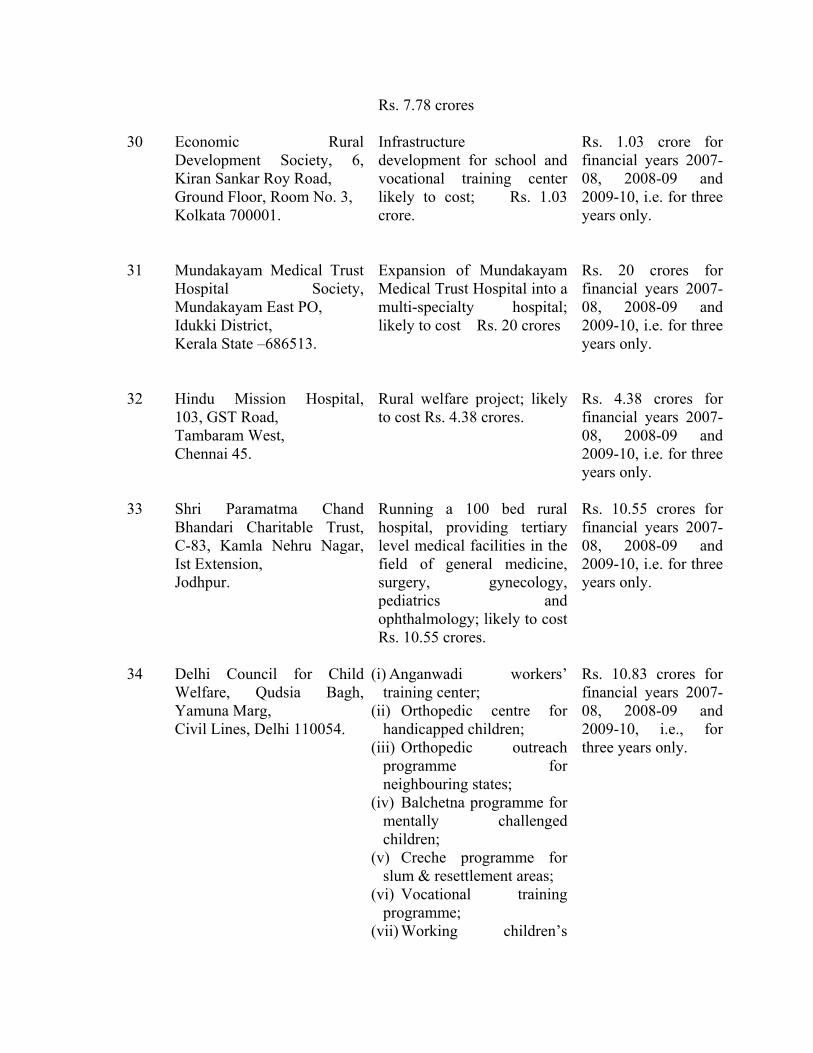

Rs. 7.78 crores

30 Economic Rural Development Society, 6, Kiran Sankar Roy Road, Ground Floor, Room No. 3, Kolkata 700001.

Infrastructure development for school and vocational training center likely to cost; Rs. 1.03 crore.

Rs. 1.03 crore for financial years 2007-08, 2008-09 and 2009-10, i.e. for three years only.

31 Mundakayam Medical Trust Hospital Society, Mundakayam East PO, Idukki District, Kerala State –686513.

Expansion of Mundakayam Medical Trust Hospital into a multi-specialty hospital; likely to cost Rs. 20 crores

Rs. 20 crores for financial years 2007-08, 2008-09 and 2009-10, i.e. for three years only.

32 Hindu Mission Hospital, 103, GST Road, Tambaram West, Chennai 45.

Rural welfare project; likely to cost Rs. 4.38 crores.

Rs. 4.38 crores for financial years 2007-08, 2008-09 and 2009-10, i.e. for three years only.

33 Shri Paramatma Chand Bhandari Charitable Trust, C-83, Kamla Nehru Nagar, Ist Extension, Jodhpur.

Running a 100 bed rural hospital, providing tertiary level medical facilities in the field of general medicine, surgery, gynecology, pediatrics and ophthalmology; likely to cost Rs. 10.55 crores.

Rs. 10.55 crores for financial years 2007-08, 2008-09 and 2009-10, i.e. for three years only.

34 Delhi Council for Child Welfare, Qudsia Bagh, Yamuna Marg, Civil Lines, Delhi 110054.

(i) Anganwadi workers’ training center;

(ii) Orthopedic centre for handicapped children;

(iii) Orthopedic outreach programme for neighbouring states;

(iv) Balchetna programme for mentally challenged children;

(v) Creche programme for slum & resettlement areas;

(vi) Vocational training programme;

(vii) Working children’s

Rs. 10.83 crores for financial years 2007-08, 2008-09 and 2009-10, i.e., for three years only.

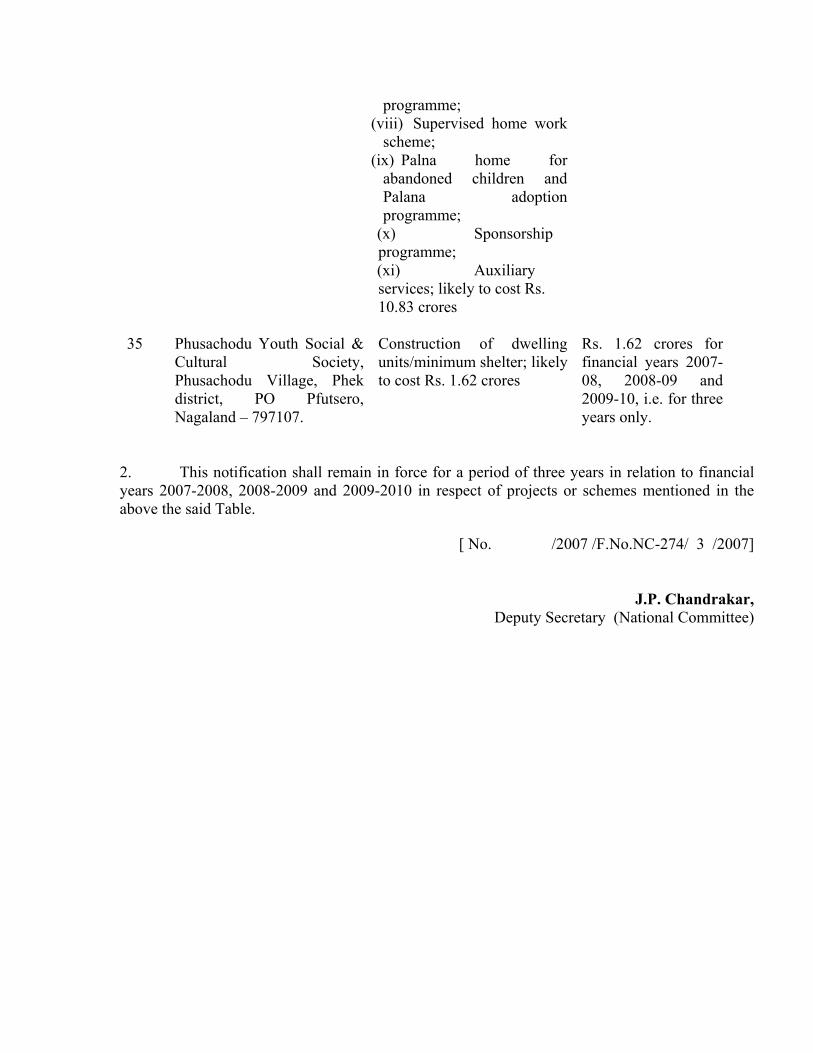

programme; (viii) Supervised home work

scheme; (ix) Palna home for

abandoned children and Palana adoption programme;

(x) Sponsorship programme; (xi) Auxiliary services; likely to cost Rs. 10.83 crores

35 Phusachodu Youth Social &

Cultural Society, Phusachodu Village, Phek district, PO Pfutsero, Nagaland – 797107.

Construction of dwelling units/minimum shelter; likely to cost Rs. 1.62 crores

Rs. 1.62 crores for financial years 2007-08, 2008-09 and 2009-10, i.e. for three years only.

2. This notification shall remain in force for a period of three years in relation to financial years 2007-2008, 2008-2009 and 2009-2010 in respect of projects or schemes mentioned in the above the said Table.

[ No. /2007 /F.No.NC-274/ 3 /2007]

J.P. Chandrakar, Deputy Secretary (National Committee)

[TO BE PUBLISHED IN THE GAZETTE OF INDIA, EXTRAORDINARY, PART-II,

SECTION 3, SUB-SECTION (ii)] GOVERNMENT OF INDIA MINISTRY OF FINANCE (Department of Revenue)

N O T I F I C A T I O N

New Delhi, dated the March, 2007

S.O. (E).- Whereas by notification of the Government of India in the Ministry of

Finance (Department of Revenue), number S.O.698(E) dated the 3rd October, 1997, issued under sub-section (1) read with clause (b) of the Explanation to section 35AC of the Income-tax Act, 1961 (43 of 1961), the Central Government had specified at serial number 1, for Development of land and construction of 5000 houses, “Amrita Kuteeram” all over India by Mata Amritanandamayi Charitable Trust, Amritapuri P.O., Kollam District, Kerala-690525 as an eligible project or scheme for a period of three years beginning with assessment year 1998-1999, which was extended further vide notification number S.O.874(E) dated the 21st September, 2000 for a period of three years beginning with assessment year 2001-2002 and which was extended further vide notification number S.O.1257(E) dated the 30th October, 2003 for a period of three years beginning with assessment year 2004-2005;

And whereas vide notification number S.O.1257(E) dated the 30th October, 2003 the

estimated cost was enhanced from Rs.1400.00 lakhs to Rs.7400.00 lakhs; And whereas the said project or scheme is likely to extend beyond nine years;

And whereas the National Committee for Promotion of Social and Economic Welfare, being satisfied that the said project or scheme is being executed properly, made a further recommendation under sub-rule (5) of rule 11M of the Income-tax Rules, 1962 for specifying the said project or scheme for a further period of three years and amending the 5000 houses to 1,00,000 houses and enhancing the project cost from Rs.7400.00 lakhs to Rs. 300.00 crore;

Now, therefore, the Central Government, in exercise of the powers conferred by sub-

section (1) read with clause (b) of the Explanation to section 35AC of the Income-tax Act, 1961 (43 of 1961), -

(a) hereby specifies the scheme or project for development of land and construction of 5000 houses- “Amrita Kuteeram” all over India, which is being carried out by Mata Amritanandamayi Charitable Trust, Amritapuri P.O., Kollam District, Kerala-690525 as an eligible project or scheme for a further period of three years commencing from the financial year 2006-2007; and (b) further amends the said notification number S.O.698(E) dated the 3rd October, 1997, to the following effect, namely :-

(i) in the said notification, in the Table against serial number 1, in column (3), relating to Project or Scheme and estimated cost thereof for the figures and word “5000 houses”, the figures and word “1,00,000 houses” shall be substituted;

(ii) In the said notification, in the Table against serial number 1, in column (4),

relating to maximum amount of cost to be allowed as deduction under section 35 AC, for the letters, figures and word “Rs.7400.00 lakhs”, the letters, figures and word “Rs. 300.00 crores ” shall be substituted.

[ No. /2007 /F.No.NC-274/ 3 /2007]

J.P. Chandrakar, Deputy Secretary (National Committee)

[TO BE PUBLISHED IN THE GAZETTE OF INDIA, EXTRAORDINARY, PART-II, SECTION 3, SUB-SECTION (ii)]

GOVERNMENT OF INDIA MINISTRY OF FINANCE (Department of Revenue)

N O T I F I C A T I O N

New Delhi, dated the 29th March, 2007

S.O. (E).- Whereas by notification of the Government of India in the Ministry of

Finance (Department of Revenue), number S.O.81(E) dated the 24th October, 2005, issued under sub-section (1) read with clause (b) of the Explanation to section 35AC of the Income-tax Act, 1961 (43 of 1961), the Central Government had specified at serial number 7, for an integrated project on Water and Natural Resources Management; improving livelihood & quality of lives of the rural poor with reference to the forest and forest fringe dwellers in Uttar Pradesh and West Bengal by Programme Support Unit Foundation (PSU Foundation), 4- Rafi Ahmed Kidwai Marg, Cantonment, Lucknow 226002 as an eligible project or scheme for a period of three years beginning with financial years 2004-2005;

And whereas the said project or scheme is likely to extend beyond three years;

And whereas the National Committee for Promotion of Social and Economic Welfare, being satisfied that the said project or scheme is being executed properly, made a further recommendation under sub-rule (5) of rule 11M of the Income-tax Rules, 1962 for specifying the said project or scheme for a further period of three years;

Now, therefore, the Central Government, in exercise of the powers conferred by sub-

section (1) read with clause (b) of the Explanation to section 35AC of the Income-tax Act, 1961 (43 of 1961), hereby specifies the scheme or project for an integrated project on Water and Natural Resources Management; improving livelihood & quality of lives of the rural poor with reference to the forest and forest fringe dwellers in Uttar Pradesh and West Bengal which is being carried out by Programme Support Unit Foundation (PSU Foundation), 4- Rafi Ahmed Kidwai Marg, Cantonment, Lucknow 226002, without any change in the approved cost of Rs. 380.19 crores including a corpus fund of Rs.45.62 crores, as an eligible project or scheme for a further period of three years commencing from the financial year 2007-2008.

[No. /2007/ F.No. NC-274/03/2007]

J.P. Chandrakar, Deputy Secretary (National Committee)

[TO BE PUBLISHED IN THE GAZETTE OF INDIA, EXTRAORDINARY, PART-II,

SECTION 3, SUB-SECTION (ii)] GOVERNMENT OF INDIA MINISTRY OF FINANCE (Department of Revenue)

N O T I F I C A T I O N

New Delhi, dated the 29th March, 2007

S.O. (E).- Whereas by notification of the Government of India, in the Ministry of Finance (Department of Revenue) number S.O.402(E) dated the 3rd May, 1995, issued under sub-section (1) read with clause (b) of the Explanation to section 35AC of the Income-tax Act, 1961 (43 of 1961), the Central Government had specified at serial number 10, for Construction of swimming pool complex with facilities of boarding and lodging for the Swimmers and a modern gymnasium at Basavanagudi, Near National College, Bangalore and running by Basavanagudi Aquatic Centre, Shankar Prasad, Number 34, Shankar Mutt Road, Basavanagudi, Bangalore-560004, as an eligible project or scheme for a period of three years beginning with assessment year 1996-1997 which was extended further vide notification number S.O.919(E) dated the 29th December, 1997 for a period of three years beginning with assessment year 1999-2000 which was extended further vide notification number S.O.915(E) dated the 20th September, 2001 for a period of three years beginning with assessment year 2002-2003 and which was extended further vide notification number S.O.795(E) dated the 5th July, 2004 for a period of three years beginning with financial year 2004-2005;

And whereas the said project or scheme is likely to extend beyond twelve years;

And whereas the National Committee for Promotion of Social and Economic Welfare, being satisfied that the said project or scheme is being executed properly, made a further recommendation under sub-rule (5) of rule 11M of the Income-tax Rules, 1962 for specifying the said project or scheme for a further period of three years;

Now, therefore, the Central Government, in exercise of the powers conferred by sub-

section (1) read with clause (b) of the Explanation to section 35AC of the Income-tax Act, 1961 (43 of 1961), hereby specifies the scheme or project for Construction of swimming pool complex with facilities of boarding and lodging for the Swimmers and a modern gymnasium at Basavanagudi, Near National College, Bangalore and running which is being carried out by Basavanagudi Aquatic Centre, Shankar Prasad, Number 34, Shankar Mutt Road, Basavanagudi, Bangalore-560004, without any change in the approved cost of Rs.100.30 lakhs, as an eligible project or scheme for a further period of three years commencing from the financial year 2007-2008.

[F.No. -2007/ F.No. NC-274/03/2007]

J.P. Chandrakar, Deputy Secretary (National Committee)

[TO BE PUBLISHED IN THE GAZETTE OF INDIA, EXTRAORDINARY, PART-II,

SECTION 3, SUB-SECTION (ii)] GOVERNMENT OF INDIA MINISTRY OF FINANCE (Department of Revenue)

N O T I F I C A T I O N

New Delhi, dated the 29th March, 2007

S.O. (E).- Whereas by notification of the Government of India in the Ministry of

Finance (Department of Revenue), number S.O.96(E) dated the 11th February, 1999, issued under sub-section (1) read with clause (b) of the Explanation to section 35AC of the Income-tax Act, 1961 (43 of 1961), the Central Government had specified at serial number 9, for Providing free food and anti-Cancer drugs to poor cancer patients in General wards of Cancer Institute at Chennai, Tamilnadu by the Cancer Institute (WIA) Trust, East Canal Bank Road, Gandhi Nagar, Adyar, Chennai-600020, as an eligible project or scheme for a period of three years beginning with assessment year 1999-2000 which was extended further vide notification number S.O.920(E) dated the 20th September, 2001 for a period of three years beginning with assessment year 2002-2003 and which was extended further vide notification number S.O.130(E) dated the 2nd February, 2005 for a period of three years beginning with financial year 2004-2005;

And whereas the said project or scheme is likely to extend beyond nine years;

And whereas the National Committee for Promotion of Social and Economic Welfare, being satisfied that the said project or scheme is being executed properly, made a further recommendation under sub-rule (5) of rule 11M of the Income-tax Rules, 1962 for specifying the said project or scheme for a further period of three years;

Now, therefore, the Central Government, in exercise of the powers conferred by sub-

section (1) read with clause (b) of the Explanation to section 35AC of the Income-tax Act, 1961 (43 of 1961), hereby specifies the scheme or project for Providing free food and anti-Cancer drugs to poor cancer patients in General wards of Cancer Institute at Chennai, Tamilnadu which is being carried out by The Cancer Institute (WIA) Trust, East Canal Bank Road, Gandhi Nagar, Adyar, Chennai-600020, without any change in the approved cost of Rs. 650.00 lakhs as corpus fund only, as an eligible project or scheme for a further period of three years commencing from the financial year 2007-2008.

[F.No. /2007/ F.No. NC-274/03/2007]

J.P. Chandrakar, Deputy Secretary (National Committee)

[TO BE PUBLISHED IN THE GAZETTE OF INDIA, EXTRAORDINARY, PART-II,

SECTION 3, SUB-SECTION (ii)] GOVERNMENT OF INDIA MINISTRY OF FINANCE (Department of Revenue)

N O T I F I C A T I O N

New Delhi, dated the 29th March, 2007

S.O. (E).- Whereas by notification of the Government of India in the Ministry of

Finance (Department of Revenue), number S.O.839(E) dated the 24th July, 2003, issued under sub-section (1) read with clause (b) of the Explanation to section 35AC of the Income-tax Act, 1961 (43 of 1961), the Central Government had specified at serial number 4, for Baba Amte Centre for People’s Empowerment by Samaj Pragati Sahayog, Bagli, District Dewas, Madhya Pradesh-455227, as an eligible project or scheme for a period of three years beginning with assessment year 2004-2005;

And whereas the said project or scheme is likely to extend beyond three years; And whereas the National Committee for Promotion of Social and Economic Welfare, being satisfied that the said project or scheme is being executed properly, made a further recommendation under sub-rule (5) of rule 11M of the Income-tax Rules, 1962 for specifying the said project or scheme for a further period of three years;

Now, therefore, the Central Government, in exercise of the powers conferred by sub-

section (1) read with clause (b) of the Explanation to section 35AC of the Income-tax Act, 1961 (43 of 1961), hereby specifies the scheme or project for Baba Amte Centre for People’s Empowerment which is being carried out by Samaj Pragati Sahayog, Bagli, District Dewas, Madhya Pradesh-455227, without any change in the approved cost of Rs. 350.00 lakhs (corpus fund), as an eligible project or scheme for a further period of three years commencing from the financial year 2006-2007.

[F.No. 2007/ F.No. NC-274/03/2007]

J.P. Chandrakar, Deputy Secretary (National Committee)

[TO BE PUBLISHED IN THE GAZETTE OF INDIA, EXTRAORDINARY, PART-II, SECTION 3, SUB-SECTION (ii)]

GOVERNMENT OF INDIA MINISTRY OF FINANCE (Department of Revenue)

N O T I F I C A T I O N

New Delhi, dated the 29th March, 2007

S.O. (E).- Whereas by notification of the Government of India in the Ministry of

Finance (Department of Revenue), number S.O.19(E) dated the 7th January, 2004, issued under sub-section (1) read with clause (b) of the Explanation to section 35AC of the Income-tax Act, 1961 (43 of 1961), the Central Government had specified at serial number 10, for Purchase of land, construction of Building for school, hostel, purchase of furniture/fixture books utensils etc. Establishment of one Military school and 20 cluster level coordination centers and running of the project by Netaji Azad Hind Fauj Smarak Nyas, 10196, Mata Mandir Gali, Jhandewalan, New Delhi 110055, as an eligible project or scheme for a period of three years beginning with assessment year 2004-2005;

And whereas the said project or scheme is likely to extend beyond three years;

And whereas the National Committee for Promotion of Social and Economic Welfare, being satisfied that the said project or scheme is being executed properly, made a further recommendation under sub-rule (5) of rule 11M of the Income-tax Rules, 1962 for specifying the said project or scheme for a further period of three years;

Now, therefore, the Central Government, in exercise of the powers conferred by sub-

section (1) read with clause (b) of the Explanation to section 35AC of the Income-tax Act, 1961 (43 of 1961), hereby specifies the scheme or project for Purchase of land, construction of Building for school, hostel, purchase of furniture/fixture books utensils etc. Establishment of one Military school and 20 cluster level coordination centers and running of the project which is being carried out by Netaji Azad Hind Fauj Smarak Nyas, 10196, Mata Mandir Gali, Jhandewalan, New Delhi 110055, without any change in the approved cost of Rs. 35.00 crores including a corpus fund of Rs.17.00 crores, as an eligible project or scheme for a further period of three years commencing from the financial year 2006-2007.

.

[No. /2007/ F.No. NC-274/03/2007]

J.P. Chandrakar, Deputy Secretary (National Committee)

[TO BE PUBLISHED IN THE GAZETTE OF INDIA, EXTRAORDINARY, PART-II, SECTION 3, SUB-SECTION (ii)]

GOVERNMENT OF INDIA MINISTRY OF FINANCE (Department of Revenue)

N O T I F I C A T I O N

New Delhi, dated the 29th March, 2007

S.O. (E).- Whereas by notification of the Government of India in the Ministry of

Finance (Department of Revenue), number S.O.1237(E) dated the 28th October, 2003, issued under sub-section (1) read with clause (b) of the Explanation to section 35AC of the Income-tax Act, 1961 (43 of 1961), the Central Government had specified at serial number 7, for Diagnostic camps and cataract eye surgeries under community ophthalmology programme by Free Ophthalmic Hospital’s Society’s K.B. Haji Bachooalli, Charitable Ophthalmic and E.N.T. Hospital, 58/60, Jahangir Mervanji Street, Poiba Wadi Parel, Mumbai 400012, as an eligible project or scheme for a period of three years beginning with assessment year 2004-2005;

And whereas the said project or scheme is likely to extend beyond three years;

And whereas the National Committee for Promotion of Social and Economic Welfare, being satisfied that the said project or scheme is being executed properly, made a further recommendation under sub-rule (5) of rule 11M of the Income-tax Rules, 1962 for specifying the said project or scheme for a further period of three years;

Now, therefore, the Central Government, in exercise of the powers conferred by sub-

section (1) read with clause (b) of the Explanation to section 35AC of the Income-tax Act, 1961 (43 of 1961), hereby specifies the scheme or project for Diagnostic camps and cataract eye surgeries under community ophthalmology programme which is being carried out by Free Ophthalmic Hospital’s Society’s K.B. Haji Bachooalli, Charitable Ophthalmic and E.N.T. Hospital, 58/60, Jahangir Mervanji Street, Poiba Wadi Parel, Mumbai 400012, without any change in the approved cost of Rs. 116.00 lakhs, as an eligible project or scheme for a further period of three years commencing from the financial year 2006-2007.

[No. /2007/ F.No. NC-274/03/2007]

J.P. Chandrakar, Deputy Secretary (National Committee)

[TO BE PUBLISHED IN THE GAZETTE OF INDIA, EXTRAORDINARY, PART-II, SECTION 3, SUB-SECTION (ii)]

GOVERNMENT OF INDIA MINISTRY OF FINANCE (Department of Revenue)

N O T I F I C A T I O N

New Delhi, dated the 29th March, 2007

S.O. (E).- Whereas by notification of the Government of India in the Ministry of Finance (Department of Revenue), number S.O.388(E) dated the 19th May, 1997, issued under sub-section (1) read with clause (b) of the Explanation to section 35AC of the Income-tax Act, 1961 (43 of 1961), the Central Government had specified at serial number 23, for School Adoption Scheme and Balwadi Project at Mumbai, Maharashtra by The Bombay Community Public Trust, Regent Chamber, 5th Floor, Nariman Point, Mumbai, as an eligible project or scheme for a period of three years beginning with assessment year 1998-1999 which was extended further vide notification number S.O.303(E) dated the 29th March, 2000 for a period of three years beginning with assessment year 2001-2002 and which was extended further vide notification number S.O.1373(E) dated the 27th November, 2003 for a period of three year beginning with assessment year 2004-2005;

And whereas the said project or scheme is likely to extend beyond nine years; And whereas the National Committee for Promotion of Social and Economic Welfare, being satisfied that the said project or scheme is being executed properly, made a further recommendation under sub-rule (5) of rule 11M of the Income-tax Rules, 1962 for specifying the said project or scheme for a further period of three years;

Now, therefore, the Central Government, in exercise of the powers conferred by sub-

section (1) read with clause (b) of the Explanation to section 35AC of the Income-tax Act, 1961 (43 of 1961), hereby specifies the scheme or project for School Adoption Scheme and Balwadi Project at Mumbai, Maharashtra, which is being carried out by The Bombay Community Public Trust, Regent Chamber, 5th Floor, Nariman Point, Mumbai, without any change in the approved cost of Rs. 300.00 lakhs, as an eligible project or scheme for a further period of three years commencing from the financial year 2006-2007.

[No. /2007/ F.No. NC-274/03/2007]

J.P. Chandrakar, Deputy Secretary (National Committee)

[TO BE PUBLISHED IN THE GAZETTE OF INDIA, EXTRAORDINARY, PART-II,

SECTION 3, SUB-SECTION (ii)] GOVERNMENT OF INDIA MINISTRY OF FINANCE (Department of Revenue)

N O T I F I C A T I O N

New Delhi, dated the 29th March, 2007

S.O. (E).- Whereas by notification of the Government of India in the Ministry of

Finance (Department of Revenue), number S.O.839(E) dated the 24th July, 2003, issued under sub-section (1) read with clause (b) of the Explanation to section 35AC of the Income-tax Act, 1961 (43 of 1961), the Central Government had specified at serial number 1, for Jagshanti Udayan Care Hostel for Women, by Udayan Care, 412 Sant Nagar, East of Kailash, New Delhi-110065, as an eligible project or scheme for a period of three years beginning with assessment year 2004-2005;

And whereas the said project or scheme is likely to extend beyond three years; And whereas the National Committee for Promotion of Social and Economic Welfare, being satisfied that the said project or scheme is being executed properly, made a further recommendation under sub-rule (5) of rule 11M of the Income-tax Rules, 1962 for specifying the said project or scheme for a further period of three years and enhancing the project cost from Rs. 210 lakhs to Rs. 310 lakhs including a corpus fund of Rs. 210 lakhs;

Now, therefore, the Central Government, in exercise of the powers conferred by sub-

section (1) read with clause (b) of the Explanation to section 35AC of the Income-tax Act, 1961 (43 of 1961), -

(a) hereby specifies the scheme or project for Jagshanti Udayan Care Hostel for Women, which is being carried out by Udayan Care, 412 Sant Nagar, East of Kailash, New Delhi-110065, as an eligible project or scheme for a further period of three years commencing from the financial year 2006-2007; and (b) further amends the said notification number S.O.839(E) dated the 24th July, 2003, to the following effect, namely :-

In the said notification, in the Table against serial number 1, in column (4),

relating to maximum amount of cost to be allowed as deduction under section 35 AC, for the letters, figures and words “Rs. 210 lakhs (corpus fund )”, the letters, figures and words “Rs. 310 lakhs including a corpus fund of Rs. 210 lakhs” shall be substituted. .

[No. / 2007/ F.No. NC-274/03/2007]

J.P. Chandrakar,

Deputy Secretary (National Committee)

[TO BE PUBLISHED IN THE GAZETTE OF INDIA, EXTRAORDINARY, PART-II, SECTION 3, SUB-SECTION (ii)]

GOVERNMENT OF INDIA MINISTRY OF FINANCE (Department of Revenue)

N O T I F I C A T I O N

New Delhi, dated the 29th March, 2007

S.O. (E).- Whereas by notification of the Government of India in the Ministry of

Finance (Department of Revenue), number S.O.97(E) dated the 11th February, 1999, issued under sub-section (1) read with clause (b) of the Explanation to section 35AC of the Income-tax Act, 1961 (43 of 1961), the Central Government had specified at serial number 2, for Digging of tube-wells for providing potable drinking water, repairing of schools, promotion/improvement of agricultural activities and providing medical facilities in various villages in Keonjhar District of Orissa by Tata Sponge Iron Limited, P.O. Joda, Distt. Keonjhar, Orissa, as an eligible project or scheme for a period of three years beginning with assessment year 1999-2000, which was extended further vide notification number S.O.1270(E) dated the 28th December, 2001 for a period of three years beginning with assessment year 2002-2003 which was extended further vide notification number S.O.794(E) dated the 5th July, 2004 for a period of three years beginning with financial year 2004-2005;

And whereas vide notification number S.O.1270(E) dated the 12th December, 2001 the

estimated cost was enhanced from Rs.10.00 lakhs to Rs.30.00 lakhs and vide notification number S.O.384(E) dated the 23rd March, 2005 the estimated cost was enhanced from Rs.30.00 lakhs to Rs.56.00 lakhs;

And whereas the said project or scheme is likely to extend beyond nine years;

And whereas the National Committee for Promotion of Social and Economic Welfare, being satisfied that the said project or scheme is being executed properly, made a further recommendation under sub-rule (5) of rule 11M of the Income-tax Rules, 1962 for specifying the said project or scheme for a further period of three years and enhancing the project cost from Rs.56.00 lakhs to Rs. 166.00 lakhs;

Now, therefore, the Central Government, in exercise of the powers conferred by sub-

section (1) read with clause (b) of the Explanation to section 35AC of the Income-tax Act, 1961 (43 of 1961), -

(a) hereby specifies the scheme or project for Digging of tube-wells for providing potable drinking water, repairing of schools, promotion/improvement of agricultural activities and providing medical facilities in various villages in Keonjhar District of Orissa, which is being carried out by Tata Sponge Iron Limited, P.O. Joda, Distt. Keonjhar, Orissa as an eligible project

or scheme for a further period of three years commencing from the financial year 2007-2008; and (b) further amends the said notification number S.O.97(E) dated the 11th February, 1999, to the following effect, namely :-

In the said notification, in the Table against serial number 2, in column (4), relating to maximum amount of cost to be allowed as deduction under section 35 AC, for the letters, figures and word “Rs.56.00 lakhs”, the letters, figures and word “Rs. 166.00 lakhs” shall be substituted.

[ No. /2007 /F.No.NC-274/ 3 /2007]

J.P. Chandrakar, Deputy Secretary (National Committee)

[TO BE PUBLISHED IN THE GAZETTE OF INDIA, EXTRAORDINARY, PART-II,

SECTION 3, SUB-SECTION (ii)] GOVERNMENT OF INDIA MINISTRY OF FINANCE (Department of Revenue)

N O T I F I C A T I O N

New Delhi, dated the 29th March, 2007

S.O. (E).- Whereas by notification of the Government of India in the Ministry of

Finance (Department of Revenue), number S.O.206(E) dated the 17th March, 1997, issued under sub-section (1) read with clause (b) of the Explanation to section 35AC of the Income-tax Act, 1961 (43 of 1961), the Central Government had specified at serial number 9, for running of Health Camps at rural areas of all Districts of Tamil Nadu by Singhvi Charitable Trust, 11, Ponnappa Lane, Triplicane, Chennai, TAMIL NADU-60005, as an eligible project or scheme for a period of three years beginning with assessment years 1997-1998 which was extended further vide notification number S.O.321(E) dated the 11th May, 1999 for a period of three years beginning with assessment year 2000-2001 which was extended further vide notification number S.O.613(E) dated the 7th June, 2002 for a period of three years beginning with assessment year 2003-2004 and which was extended further vide notification number S.O.137(E) dated the 3rd February, 2006 for a period of three years beginning with financial year 2005-2006;

And whereas vide notification number S.O. 321(E) dated the 11th May, 1999 the estimated cost was enhanced from Rs.147.00 lakhs to Rs.201.00 lakhs;

And whereas the said project or scheme is likely to extend beyond twelve years; And whereas the National Committee for Promotion of Social and Economic Welfare, being satisfied that the said project or scheme is being executed properly, made a further recommendation under sub-rule (5) of rule 11M of the Income-tax Rules, 1962 for specifying the said project or scheme for a further period of three years and enhancing the project cost from Rs.201.00 lakhs to Rs. 286.00 lakhs;

Now, therefore, the Central Government, in exercise of the powers conferred by sub-

section (1) read with clause (b) of the Explanation to section 35AC of the Income-tax Act, 1961 (43 of 1961), - (a) hereby specifies the scheme or project for running of Health Camps at rural areas of all Districts of Tamil Nadu, which is being carried out by Singhvi Charitable Trust, 11, Ponnappa Lane, Triplicane, Chennai, TAMIL NADU-60005 as an eligible project or scheme for a further period of three years commencing from the financial year 2007-2008; and (b) further amends the said notification number S.O.206(E) dated the 17th March, 1997, to the following effect, namely :-

In the said notification, in the Table against serial number 9, in column (4), relating to maximum amount of cost to be allowed as deduction under section 35 AC, for

the letters, figures and word “Rs.201.00 lakhs”, the letters, figures and word “Rs. 286.00 lakhs” shall be substituted.

[F.No. /2007/ F.No. NC-274/03/2007]

J.P. Chandrakar, Deputy Secretary (National Committee)

[TO BE PUBLISHED IN THE GAZETTE OF INDIA, EXTRAORDINARY, PART-II,

SECTION 3, SUB-SECTION (ii)] GOVERNMENT OF INDIA MINISTRY OF FINANCE (Department of Revenue)

N O T I F I C A T I O N

New Delhi, dated the 29th March, 2007

S.O. (E).- Whereas by notification of the Government of India, in the Ministry of Finance (Department of Revenue) number S.O.901(E) dated the 20th September, 2001, issued under sub-section (1) read with clause (b) of the Explanation to section 35AC of the Income-tax Act, 1961 (43 of 1961), the Central Government had specified at serial number 13, for Literacy project of running 2890 One Teacher Schools (OTS) at 2890 tribal areas in 6 States, by Friends of the Tribal Society, 19- Ganga Prasad Mukherjee Road, Kolkatta-700025, as an eligible project or scheme for a period of three years beginning with assessment year 2002-2003 and which was extended further vide notification number S.O.797(E) dated the 5th July, 2004 for a period of three years beginning with financial year 2004-2005;

And whereas the said project or scheme is likely to extend beyond six years; And whereas the National Committee for Promotion of Social and Economic Welfare, being satisfied that the said project or scheme is being executed properly, made a further recommendation under sub-rule (5) of rule 11M of the Income-tax Rules, 1962 for specifying the said project or scheme for a further period of three years and amending the project of running from 2890 schools to 8030 schools and enhancing the project cost from Rs.8.67 crore to Rs. 16.50 crore;

Now, therefore, the Central Government, in exercise of the powers conferred by sub- section (1) read with clause (b) of the Explanation to section 35AC of the Income-tax Act, 1961 (43 of 1961), - (a) hereby specifies the scheme or project for Literacy project of running 2890 One Teacher Schools (OTS) at 2890 tribal areas in 6 States, which is being carried out by Friends of the Tribal Society, 19- Ganga Prasad Mukherjee Road, Kolkatta-700025 as an eligible project or scheme for a further period of three years commencing from the financial year 2007-2008; and (b) further amends the said notification number S.O.901(E) dated the 20th September, 2001, to the following effect, namely :-

In the said notification, in the Table against serial number 13; (i) in column (3), relating to project or scheme and estimated cost thereof, for the figures and word “2890 schools”, the figures and word “8030 schools ” shall be substituted; (ii) in column (4), relating to maximum amount of cost to be allowed as deduction under section 35 AC, for the letters, figures and word “Rs.867.00 lakhs”, the letters, figures and word “Rs. 1650.00 lakhs” shall be substituted.

[F.No. / 2007/ F.No. NC-274/03/2007]

J.P. Chandrakar, Deputy Secretary (National Committee)

[TO BE PUBLISHED IN THE GAZETTE OF INDIA, EXTRAORDINARY, PART-II, SECTION 3, SUB-SECTION (ii)]

GOVERNMENT OF INDIA MINISTRY OF FINANCE (Department of Revenue)

N O T I F I C A T I O N

New Delhi, dated the 29th March, 2007

S.O. (E).- Whereas by notification of the Government of India in the Ministry of Finance (Department of Revenue), number S.O.198(E) dated the 12th March, 1998, issued under sub-section (1) read with clause (b) of the Explanation to section 35AC of the Income-tax Act, 1961 (43 of 1961), the Central Government had specified at serial number 3, for purchase of equipments and running of socio-economic promotion of cerebral palsied children and adults through education, institutional care, training and vocational guidance at Kothrud, Pune, Maharashtra, by “Savali” (Association for Mentally Retarded and Cerebral Palsy Children), Alankar Plot No.14, S.No.133, Kothrud, Pune-411029, as an eligible project or scheme for a period of three years beginning with assessment year 1998-1999 which was extended further vide notification number S.O.857(E) dated the 21st September, 2000 for a period of three years beginning with assessment year 2001-2002 and which was extended further vide notification number S.O.607(E) dated the 20th May, 2004 for a period of three year beginning with financial year 2003-2004;

And whereas the said project or scheme is likely to extend beyond nine years; And whereas the National Committee for Promotion of Social and Economic Welfare, being satisfied that the said project or scheme is being executed properly, made a further recommendation under sub-rule (5) of rule 11M of the Income-tax Rules, 1962 for specifying the said project or scheme for a further period of three years;

Now, therefore, the Central Government, in exercise of the powers conferred by sub-

section (1) read with clause (b) of the Explanation to section 35AC of the Income-tax Act, 1961 (43 of 1961), hereby specifies the scheme or project for purchase of equipments and running of socio-economic promotion of cerebral palsied children and adults through education, institutional care, training and vocational guidance at Kothrud, Pune, Maharashtra, which is being carried out by “Savali” (Association for Mentally Retarded and Cerebral Palsy Children), Alankar Plot No.14, S.No.133, Kothrud, Pune-411029, without any change in the approved cost of Rs. 71.21 lakhs, as an eligible project or scheme for a further period of three years commencing from the financial year 2006-2007.

[No. /2007/ F.No. NC-274/03/2007]

J.P. Chandrakar, Deputy Secretary (National Committee)

[TO BE PUBLISHED IN THE GAZETTE OF INDIA, EXTRAORDINARY, PART-II, SECTION 3, SUB-SECTION (ii)]

GOVERNMENT OF INDIA MINISTRY OF FINANCE (Department of Revenue)

N O T I F I C A T I O N

New Delhi, dated the 29th March, 2007

S.O. (E).- Whereas by notification of the Government of India in the Ministry of Finance (Department of Revenue), number S.O.844(E) dated the 17th October, 1995, issued under sub-section (1) read with clause (b) of the Explanation to section 35AC of the Income-tax Act, 1961 (43 of 1961), the Central Government had specified at serial number 14, for Running expenses for Mata Gujari Old Age Home-cum-Orphanage at Village Khanpur, District Ropar, Punjab by Nishkam Sikh Welfare Council, BF-33, Tagore Garden, New Delhi-110027, as an eligible project or scheme for a period of two years beginning with assessment year 1996-1997 which was extended further vide notification number S.O.259(E) dated the 27th March,1997, for a period of three year beginning with assessment year 1998-1999 which was extended further vide notification number S.O.924(E) dated the 20th September,2001, for a period of three year beginning with assessment year 2001-2002 and which was extended further vide notification number S.O.724(E) dated the 23rd June, 2004 for a period of three year beginning with financial year 2003-2004;

And whereas by notification number S.O.924(E) dated the 20th September, 2001 the estimated cost was enhanced from Rs.27.36 lakhs to Rs.99.00 lakhs and notification number S.O.724(E) dated the 23rd June, 2004 the estimated cost was enhanced from Rs.99.00 lakhs to Rs.159.00 lakhs;

And whereas the said project or scheme is likely to extend beyond twelve years; And whereas the National Committee for Promotion of Social and Economic Welfare, being satisfied that the said project or scheme is being executed properly, made a further recommendation under sub-rule (5) of rule 11M of the Income-tax Rules, 1962 for specifying the said project or scheme for a further period of three years;

Now, therefore, the Central Government, in exercise of the powers conferred by sub-

section (1) read with clause (b) of the Explanation to section 35AC of the Income-tax Act, 1961 (43 of 1961), hereby specifies the scheme or project for Running expenses for Mata Gujari Old Age Home-cum-Orphanage at Village Khanpur, District Ropar, Punjab, which is being carried out by Nishkam Sikh Welfare Council, BF-33, Tagore Garden, New Delhi-110027, without any change in the approved cost of Rs. 159.00 lakhs, as an eligible project or scheme for a further period of three years commencing from the financial year 2006-2007.

[No. /2007/ F.No. NC-274/03/2007]

J.P. Chandrakar, Deputy Secretary (National Committee)

[TO BE PUBLISHED IN THE GAZETTE OF INDIA, EXTRAORDINARY, PART-II, SECTION 3, SUB-SECTION (ii)]

GOVERNMENT OF INDIA MINISTRY OF FINANCE (Department of Revenue)

N O T I F I C A T I O N

New Delhi, dated the 29th March, 2007

S.O. (E).- Whereas by notification of the Government of India in the Ministry of

Finance (Department of Revenue), number S.O.591(E) dated the 20th August, 1997, issued under sub-section (1) read with clause (b) of the Explanation to section 35AC of the Income-tax Act, 1961 (43 of 1961), the Central Government had specified at serial number 13, for construction of building, equipment, furnishing and running of Hospital and Research Centre at Hojai, District Nagaon, Assam by Haji Abdul Majid Memorial Public Trust, P.O. Hojai, Village Gopal Nagar, District-Nagaon, Assam-782435, as an eligible project or scheme for a period of three years beginning with assessment year 1998-1999 which was extended further vide notification number S.O.1030(E) dated the 17th November, 2000 for a period of three years beginning with assessment year 2001-2002 and which was extended further vide notification number S.O.378(E) dated the 19th March, 2004 for a period of three years beginning with financial year 2003-2004;

And whereas the said project or scheme is likely to extend beyond nine years;

And whereas the National Committee for Promotion of Social and Economic Welfare, being satisfied that the said project or scheme is being executed properly, made a further recommendation under sub-rule (5) of rule 11M of the Income-tax Rules, 1962 for specifying the said project or scheme for a further period of three years;

Now, therefore, the Central Government, in exercise of the powers conferred by sub-

section (1) read with clause (b) of the Explanation to section 35AC of the Income-tax Act, 1961 (43 of 1961), hereby specifies the scheme or project for construction of building, equipment, furnishing and running of Hospital and Research Centre at Hojai, District Nagaon, Assam, which is being carried out by Haji Avdul Majid Memorial Public Trust, P.O. Hojai, Village Gopal Nagar, District-Nagaon, Assam-782435, without any change in the approved cost of Rs. 7593.00 lakhs, as an eligible project or scheme for a further period of three years commencing from the financial year 2006-2007.

[No. /2007/ F.No. NC-274/03/2007]

J.P. Chandrakar, Deputy Secretary (National Committee)

[TO BE PUBLISHED IN THE GAZETTE OF INDIA, EXTRAORDINARY, PART-II,

SECTION 3, SUB-SECTION (ii)] GOVERNMENT OF INDIA MINISTRY OF FINANCE (Department of Revenue)

N O T I F I C A T I O N

New Delhi, dated the March, 2007

S.O. (E).- Whereas by notification of the Government of India in the Ministry of

Finance (Department of Revenue), number S.O.602(E) dated the 12th August, 1993, issued under sub-section (1) read with clause (b) of the Explanation to section 35AC of the Income-tax Act, 1961 (43 of 1961), the Central Government had specified at serial number 12, for Medical care to old persons Leprosy and cancer patients, provision of home to old persons rehabilitation of destitute old women, conducting eye camps by Helpage India, Helpage India, C-14. Qutab Institutional Area, New Delhi-110016 as an eligible project or scheme for a period of two years beginning with assessment year 1994-1995 which was extended further vide notification number S.O.405(E) dated the 3rd May, 1995 for a period of three years beginning with assessment year 1996-1997 which was extended further vide notification number S.O.220(E) dated the 16th March, 1998 for a period of three years beginning with assessment year 1999-2000 which was extended further vide notification number S.O.553(E) dated the 20th June, 2001 for a period of three year beginning with assessment year 2002-2003 which was extended further vide notification number S.O.82(E) dated the 24th January, 2005 for a period of three years beginning with financial year 2004-2005;

And whereas by notification number S.O.17(E) dated the 11th January, 1994 the

estimated cost was enhanced from Rs.12.95 lakhs to Rs.1295.00 lakhs notification number S.O.No.510(E) dated the 26th May, 2000 estimated cost was enhanced from Rs.1295.00 lakhs to Rs.2000.00 lakhs and notification number S.O.1046(E) dated the 18th October, 2001 the estimated cost was enhanced from Rs.2000.00 lakhs to Rs.4000.00 lakhs and notification number S.O.82(E) dated the 24th January, 2005 the estimated cost was enhanced from Rs.4000.00 lakhs to Rs.6500.00 lakhs;

And whereas the said project or scheme is likely to extend beyond fourteen years; And whereas the National Committee for Promotion of Social and Economic Welfare, being satisfied that the said project or scheme is being executed properly, made a further recommendation under sub-rule (5) of rule 11M of the Income-tax Rules, 1962 for specifying the said project or scheme for a further period of three years;

Now, therefore, the Central Government, in exercise of the powers conferred by sub-

section (1) read with clause (b) of the Explanation to section 35AC of the Income-tax Act, 1961

(43 of 1961), hereby specifies the scheme or project for Medical care to old persons Leprosy and cancer patients, provision of home to old persons rehabilitation of destitute old women, conducting eye camps which is being carried out by Helpage India, Helpage India, C-14. Qutab Institutional Area, New Delhi-110016, without any change in the approved cost of Rs. 6500.00 lakhs, as an eligible project or scheme for a further period of three years commencing from the financial year 2006-2007.

[F.No. /2007/ F.No. NC-274/03/2007]

J.P. Chandrakar, Deputy Secretary (National Committee)

[TO BE PUBLISHED IN THE GAZETTE OF INDIA, EXTRAORDINARY, PART-II,

SECTION 3, SUB-SECTION (ii)] GOVERNMENT OF INDIA MINISTRY OF FINANCE (Department of Revenue)

N O T I F I C A T I O N

New Delhi, dated the 29th March, 2007

S.O. (E).- Whereas by notification of the Government of India in the Ministry of

Finance (Department of Revenue), number S.O.973(E) dated the 14th December, 1995, issued under sub-section (1) read with clause (b) of the Explanation to section 35AC of the Income-tax Act, 1961 (43 of 1961), the Central Government had specified at serial number 9, for Construction, furnishing and running of South Block of Ashram Saravana Old Age Home and Eye-cum-General Hospital at Ramanayyapeta Village, Near Kakinada Town by Association for the Care of the Aged, House No. 8-14-1, Mahalakshmi Nilayam, Gandhi Nagar, Kakinada-4 as an eligible project or scheme for a period of three years beginning with assessment year 1996-1997 which was extended further vide notification number S.O.427(E) dated the 19th May, 1998 for a period of two years beginning with assessment year 1999-2000 which was extended further vide notification number S.O.631(E) dated the 5th July, 2000 for a period of three years beginning with assessment year 2001-2002 which was extended further vide notification number S.O.534(E) dated the 9th May, 2003 for a period of three year beginning with assessment year 2004-2005;

And whereas the said project or scheme is likely to extend beyond eleven years; And whereas the National Committee for Promotion of Social and Economic Welfare, being satisfied that the said project or scheme is being executed properly, made a further recommendation under sub-rule (5) of rule 11M of the Income-tax Rules, 1962 for specifying the said project or scheme for a further period of three years;

Now, therefore, the Central Government, in exercise of the powers conferred by sub-

section (1) read with clause (b) of the Explanation to section 35AC of the Income-tax Act, 1961 (43 of 1961), hereby specifies the scheme or project for Construction, furnishing and running of South Block of Ashram Saravana Old Age Home and Eye-cum-General Hospital at Ramanayyapeta Village, Near Kakinada Town which is being carried out by Association for the Care of the Aged, House No. 8-14-1, Mahalakshmi Nilayam, Gandhi Nagar, Kakinada-4, without any change in the approved cost of Rs. 9.70 lakhs, as an eligible project or scheme for a further period of three years commencing from the financial year 2006-2007.

[F.No. /2007/ F.No. NC-274/03/2007]

J.P. Chandrakar,

Deputy Secretary (National Committee)

[TO BE PUBLISHED IN THE GAZETTE OF INDIA, EXTRAORDINARY, PART-II, SECTION 3, SUB-SECTION (ii)]

GOVERNMENT OF INDIA MINISTRY OF FINANCE (Department of Revenue)

N O T I F I C A T I O N

New Delhi, dated the 29th March, 2007

S.O. (E).- Whereas by notification of the Government of India in the Ministry of

Finance (Department of Revenue), number S.O.604(E) dated the 20th May, 2004, issued under sub-section (1) read with clause (b) of the Explanation to section 35AC of the Income-tax Act, 1961 (43 of 1961), the Central Government had specified at serial number 10, for Establishment and running of the school and hospital by H.B.S. Trust, (Human Benefits Services Trust) 21-C First Floor, Ratanada, Jodhpur-342001 (Rajasthan) as an eligible project or scheme for a period of three years beginning with financial year 2003-2004 ;

And whereas the said project or scheme is likely to extend beyond three years;

And whereas the National Committee for Promotion of Social and Economic Welfare, being satisfied that the said project or scheme is being executed properly, made a further recommendation under sub-rule (5) of rule 11M of the Income-tax Rules, 1962 for specifying the said project or scheme for a further period of three years;

Now, therefore, the Central Government, in exercise of the powers conferred by sub-

section (1) read with clause (b) of the Explanation to section 35AC of the Income-tax Act, 1961 (43 of 1961), hereby specifies the scheme or project for Establishment and running of the school and hospital which is being carried out by H.B.S. Trust, (Human Benefits Services Trust) 21-C First Floor, Ratanada, Jodhpur-342001 (Rajasthan), without any change in the approved cost of Rs. 937.74 lakhs (including a corpus fund of Rs.500.00 lakhs), as an eligible project or scheme for a further period of three years commencing from the financial year 2006-2007.

[F.No. /2007/ F.No. NC-274/03/2007]

J.P. Chandrakar, Deputy Secretary (National Committee)

[TO BE PUBLISHED IN THE GAZETTE OF INDIA, EXTRAORDINARY, PART-II, SECTION 3, SUB-SECTION (ii)]

GOVERNMENT OF INDIA MINISTRY OF FINANCE (Department of Revenue)

N O T I F I C A T I O N

New Delhi, dated the 29th March, 2007

S.O. (E).- Whereas by notification of the Government of India in the Ministry of

Finance (Department of Revenue), number S.O.28(E) dated the 10th January, 2001, issued under sub-section (1) read with clause (b) of the Explanation to section 35AC of the Income-tax Act, 1961 (43 of 1961), the Central Government had specified at serial number 2, for Tribal Welfare Project – construction of building for dispensary, schools, hostel, small scale industries, technical training/vocational training institute, cultural hall, Ashram complex, residential quarters, water tank etc. at Gangpur, District Navsari, Gujarat by Bharat Sevashram Sangha, 211, Rash Behari Avenue, Calcutta-700019, as an eligible project or scheme for a period of three years beginning with assessment year 2001-2002 and which was extended further vide notification number S.O.897(E) dated the 5th August, 2003 for a period of three years beginning with assessment year 2004-2005 ;

And whereas the said project or scheme is likely to extend beyond six years; And whereas the National Committee for Promotion of Social and Economic Welfare, being satisfied that the said project or scheme is being executed properly, made a further recommendation under sub-rule (5) of rule 11M of the Income-tax Rules, 1962 for specifying the said project or scheme for a further period of three years;

Now, therefore, the Central Government, in exercise of the powers conferred by sub-

section (1) read with clause (b) of the Explanation to section 35AC of the Income-tax Act, 1961 (43 of 1961), hereby specifies the scheme or project for Tribal Welfare Project – construction of building for dispensary, schools, hostel, small scale industries, technical training/vocational training institute, cultural hall, Ashram complex, residential quarters, water tank etc. at Gangpur, District Navsari, Gujarat, which is being carried out by Bharat Sevashram Sangha, 211, Rash Behari Avenue, Calcutta-700019, without any change in the approved cost of Rs. 277.00 lakhs, as an eligible project or scheme for a further period of three years commencing from the financial year 2006-2007.

[F.No. /2007/ F.No. NC-274/03/2007

J.P. Chandrakar, Deputy Secretary (National Committee)

[TO BE PUBLISHED IN THE GAZETTE OF INDIA, EXTRAORDINARY, PART-II, SECTION 3, SUB-SECTION (ii)]

GOVERNMENT OF INDIA MINISTRY OF FINANCE (Department of Revenue)

N O T I F I C A T I O N

New Delhi, dated the 29th March, 2007

S.O. (E).- Whereas by notification of the Government of India in the Ministry of

Finance (Department of Revenue), number S.O.839(E) dated the 22nd November, 1994, issued under sub-section (1) read with clause (b) of the Explanation to section 35AC of the Income-tax Act, 1961 (43 of 1961), the Central Government had specified at serial number 8, for Construction of building of 80 beded General Hospital in an area of 16,449 Sq. ft. with equipment and furniture at Talab Tillo Road, Jammu by BEE ENN Charitable Trust, Talab Tillo Road, Jammu-180002, as an eligible project or scheme for a period of three years beginning with assessment year 1995-1996 which was extended further vide notification number S.O.214(E) dated the 17th March, 1997 for a period of three years beginning with assessment year 1998-1999 which was extended further vide notification number S.O.1029(E) dated the 17th November, 2000 for a period of three years beginning with assessment year 2001-2002 and which was extended further vide notification number S.O.1244(E) dated the 30th October, 2003 for a period of three year beginning with assessment year 2004-2005;

And whereas the said project or scheme is likely to extend beyond twelve years;

And whereas the National Committee for Promotion of Social and Economic Welfare, being satisfied that the said project or scheme is being executed properly, made a further recommendation under sub-rule (5) of rule 11M of the Income-tax Rules, 1962 for specifying the said project or scheme for a further period of three years;

Now, therefore, the Central Government, in exercise of the powers conferred by sub-

section (1) read with clause (b) of the Explanation to section 35AC of the Income-tax Act, 1961 (43 of 1961), hereby specifies the scheme or project for Construction of building of 80 beded General Hospital in an area of 16,449 Sq. ft. with equipment and furniture at Talab Tillo Road, Jammu which is being carried out by BEE ENN Charitable Trust, Talab Tillo Road, Jammu-180002, without any change in the approved cost of Rs. 238.88 lakhs, as an eligible project or scheme for a further period of three years commencing from the financial year 2006-2007.

[F.No. /2007/ F.No. NC-274/03/2007]

J.P. Chandrakar,

Deputy Secretary (National Committee)

[TO BE PUBLISHED IN THE GAZETTE OF INDIA, EXTRAORDINARY, PART-II, SECTION 3, SUB-SECTION (ii)]

GOVERNMENT OF INDIA MINISTRY OF FINANCE (Department of Revenue)

N O T I F I C A T I O N

New Delhi, dated the 29th March, 2007

S.O. (E).- Whereas by notification of the Government of India in the Ministry of

Finance (Department of Revenue), number S.O.224(E) dated the 16th March, 1994, issued under sub-section (1) read with clause (b) of the Explanation to section 35AC of the Income-tax Act, 1961 (43 of 1961), the Central Government had specified at serial number 3, for World Memorial Fund T.B. Project-Four mobile teams at Sikkim, Himachal Pradesh, Surat and Delhi by The Memorial Fund for Disaster Relief India, C/o The Delhi Cheshire Home, Okhla road, New Delhi, as an eligible project or scheme for a period of two years beginning with assessment year 1994-1995 which was extended further vide notification number S.O.297(E) dated the 14th April, 1995 for a period of three years beginning with assessment year 1996-1997 which was extended further vide notification number S.O.916(E) dated the 29th December, 1997 for a period of three years beginning with assessment year 1999-2000 which was extended further vide notification number S.O.566(E) dated the 20th June, 2001 for a period of three years beginning with assessment year 2002-2003 and which was extended further vide notification number S.O.132(E) dated the 22nd February, 2005 for a period of three year beginning with financial year 2004-2005;

And whereas by notification number S.O.566(E) dated the 20th June, 2001 the estimated cost was enhanced from Rs.40,41,600 to Rs.338.19 lakhs;

And whereas the said project or scheme is likely to extend beyond fifteen years; And whereas the National Committee for Promotion of Social and Economic Welfare, being satisfied that the said project or scheme is being executed properly, made a further recommendation under sub-rule (5) of rule 11M of the Income-tax Rules, 1962 for specifying the said project or scheme for a further period of three years;

Now, therefore, the Central Government, in exercise of the powers conferred by sub-

section (1) read with clause (b) of the Explanation to section 35AC of the Income-tax Act, 1961 (43 of 1961), hereby specifies the scheme or project for World Memorial Fund T.B. Project-Four mobile teams at Sikkim, Himachal Pradesh, Surat and Delhi which is being carried out by The Memorial Fund for Disaster Relief India, C/o The Delhi Cheshire Home, Okhla road, New Delhi, without any change in the approved cost of Rs. 338.19 lakhs, as an eligible project or scheme for a further period of three years commencing from the financial year 2007-2008.

[F.No. 37 -2007/ F.No. NC-274/03/2007]

J.P. Chandrakar, Deputy Secretary (National Committee)

[TO BE PUBLISHED IN THE GAZETTE OF INDIA, EXTRAORDINARY, PART-II,

SECTION 3, SUB-SECTION (ii)] GOVERNMENT OF INDIA MINISTRY OF FINANCE (Department of Revenue)

N O T I F I C A T I O N

New Delhi, dated the 29th March, 2007

S.O. (E).- Whereas by notification of the Government of India in the Ministry of

Finance (Department of Revenue), number S.O.1273(E) dated the 9th December, 2002, issued under sub-section (1) read with clause (b) of the Explanation to section 35AC of the Income-tax Act, 1961 (43 of 1961), the Central Government had specified at serial number 11, for Shraddha Rehabilitation Foundation- Centre for mentally ill destitute. Garnet, Behind Shanti Ashram, Borivli (W), Mumbai-400003, by Shraddha Rehabilitation Foundation, Garnet, Behind Shanti Ashram, Borivli (W), Mumbai-400 003, as an eligible project or scheme for a period of three years beginning with assessment year 2003-2004 and which was extended further vide notification number S.O.1598(E) dated the 14th November, 2005 for a period of three years beginning with financial year 2005-2006;

And whereas the said project or scheme is likely to extend beyond six years;

And whereas the National Committee for Promotion of Social and Economic Welfare, being satisfied that the said project or scheme is being executed properly, made a further recommendation under sub-rule (5) of rule 11M of the Income-tax Rules, 1962 for specifying the said project or scheme for a further enhancing the project cost from Rs.43.30 lakhs to Rs. 150.00 lakhs;

Now, therefore, the Central Government, in exercise of the powers conferred by sub- section (1) read with clause (b) of the Explanation to section 35AC of the Income-tax Act, 1961 (43 of 1961), - (a) hereby specifies the scheme or project for Shraddha Rehabilitation Foundation, Centre for mentally ill destitute. Garnet, Behind Shanti Ashram, Borivli (W), Mumbai-400003, which is being carried out by Shraddha Rehabilitation Foundation, Garnet, Behind Shanti Ashram, Borivli (W), Mumbai-400 003; and (b) further amends the said notification number S.O.1273(E) dated the 9th December, 2002, to the following effect, namely :-

In the said notification, in the Table against serial number 11, in column (4), relating to maximum amount of cost to be allowed as deduction under section 35 AC, for the letters, figures and word “Rs.40.30 lakhs”, the letters, figures and word “Rs. 150.00 lakhs” shall be substituted.

[F.No /2007/ F.No. NC-274/03/2007]

J.P. Chandrakar,

Deputy Secretary (National Committee)

[TO BE PUBLISHED IN THE GAZETTE OF INDIA, EXTRAORDINARY, PART-II, SECTION 3, SUB-SECTION (ii)]

GOVERNMENT OF INDIA MINISTRY OF FINANCE (Department of Revenue)

N O T I F I C A T I O N

New Delhi, dated the March, 2007

S.O. (E).- Whereas by notification of the Government of India in the Ministry of

Finance (Department of Revenue), number S.O.371(E) dated the 23rd March, 2005, issued under sub-section (1) read with clause (b) of the Explanation to section 35AC of the Income-tax Act, 1961 (43 of 1961), the Central Government had specified at serial number 1, for Development of educational infrastructure at Sangroli district Nanded Community Health Services, Rural Development project by Sanskrit Samvardhan Mandal, Sharadanagar, Sangroli, district Nanded-431731, as an eligible project or scheme for a period of three years beginning with financial year 2004-2005;

And whereas the said project or scheme is likely to extend beyond three years;

And whereas the National Committee for Promotion of Social and Economic Welfare,

being satisfied that the said project or scheme is being executed properly, made a further recommendation under sub-rule (5) of rule 11M of the Income-tax Rules, 1962 for specifying the said project or scheme for a further period of three years;

Now, therefore, the Central Government, in exercise of the powers conferred by sub-

section (1) read with clause (b) of the Explanation to section 35AC of the Income-tax Act, 1961 (43 of 1961), hereby specifies the scheme or project for Development of educational infrastructure at Sangroli district Nanded Community Health Services, Rural Development project which is being carried out by Sanskrit Samvardhan Mandal, Sharadanagar, Sangroli, district Nanded-431731, without any change in the approved cost of Rs. 8.11 lakhs, as an eligible project or scheme for a further period of three years commencing from the financial year 2007-2008.

[F.No /2007/ F.No. NC-274/03/2007]

J.P. Chandrakar, Deputy Secretary (National Committee)

[TO BE PUBLISHED IN THE GAZETTE OF INDIA, EXTRAORDINARY, PART-II, SECTION 3, SUB-SECTION (ii)]

GOVERNMENT OF INDIA MINISTRY OF FINANCE (Department of Revenue)

N O T I F I C A T I O N

New Delhi, dated the March, 2007

S.O. (E).- Whereas by notification of the Government of India in the Ministry of

Finance (Department of Revenue), number S.O.839(E) dated the 24th July, 2003, issued under sub-section (1) read with clause (b) of the Explanation to section 35AC of the Income-tax Act, 1961 (43 of 1961), the Central Government had specified at serial number 16, for Animal Husbandary and Natural Resources by Foundation for Ecological Security, National Dairy Development Board Building, Safdarjung Enclave, New Delhi-110029, as an eligible project or scheme for a period of three years beginning with assessment year 2004-2005;

And whereas the said project or scheme is likely to extend beyond three years;

And whereas the National Committee for Promotion of Social and Economic Welfare,

being satisfied that the said project or scheme is being executed properly, made a further recommendation under sub-rule (5) of rule 11M of the Income-tax Rules, 1962 for specifying the said project or scheme for a further period of three years;

Now, therefore, the Central Government, in exercise of the powers conferred by sub-

section (1) read with clause (b) of the Explanation to section 35AC of the Income-tax Act, 1961 (43 of 1961), hereby specifies the scheme or project for Animal Husbandary and Natural Resources which is being carried out by Foundation for Ecological Security, National Dairy Development Board Building, Safdarjung Enclave, New Delhi-110029, without any change in the approved cost of Rs.875.21 lakhs, as an eligible project or scheme for a further period of three years commencing from the financial year 2006-2007.

[F.No. 37 -2007/ F.No. NC-274/03/2007]

J.P. Chandrakar, Deputy Secretary (National Committee)

[TO BE PUBLISHED IN THE GAZETTE OF INDIA, EXTRAORDINARY, PART-II, SECTION 3, SUB-SECTION (ii)]

GOVERNMENT OF INDIA MINISTRY OF FINANCE (Department of Revenue)

N O T I F I C A T I O N

New Delhi, dated the 29th March, 2007

S.O. (E).- Whereas by notification of the Government of India in the Ministry of

Finance (Department of Revenue), number S.O.461(E) dated the 5th April, 2004, issued under sub-section (1) read with clause (b) of the Explanation to section 35AC of the Income-tax Act, 1961 (43 of 1961), the Central Government had specified at serial number 8, for Welfare programmes in the field of Health, education, environment etc. by SNS Foundation, 1, Sri Aurobindo Marg, New Delhi-110016, as an eligible project or scheme for a period of three years beginning with financial year 2004-2005;

And whereas the said project or scheme is likely to extend beyond three years;

And whereas the National Committee for Promotion of Social and Economic Welfare,

being satisfied that the said project or scheme is being executed properly, made a further recommendation under sub-rule (5) of rule 11M of the Income-tax Rules, 1962 for specifying the said project or scheme for a further period of three years and enhancing the project cost from Rs.810.00 lakhs to Rs. 1000.00 lakhs;

Now, therefore, the Central Government, in exercise of the powers conferred by sub- section (1) read with clause (b) of the Explanation to section 35AC of the Income-tax Act, 1961 (43 of 1961), - (a) hereby specifies the scheme or project for Welfare programmes in the field of Health, education, environment etc., which is being carried out by SNS Foundation, 1, Sri Aurobindo Marg, New Delhi-110016, as an eligible project or scheme for a further period of three years commencing from the financial year 2007-2008; and (b) further amends the said notification number S.O.461(E) dated the 5th April, 2004, to the following effect, namely :-

In the said notification, in the Table against serial number 13, in column (4), relating to maximum amount of cost to be allowed as deduction under section 35 AC, for the letters, figures and word “Rs.810.00 lakhs”, the letters, figures and word “Rs. 1000.00 lakhs” shall be substituted.

[F.No. 37 -2007/ F.No. NC-274/03/2007]

J.P. Chandrakar,

Deputy Secretary (National Committee)

[TO BE PUBLISHED IN THE GAZETTE OF INDIA, EXTRAORDINARY, PART-II,

SECTION 3, SUB-SECTION (ii)] GOVERNMENT OF INDIA MINISTRY OF FINANCE (Department of Revenue)

N O T I F I C A T I O N

New Delhi, dated the 29th March, 2007

S.O. (E).- Whereas by notification of the Government of India in the Ministry of

Finance (Department of Revenue), number S.O.212(E) dated the 1st April, 1999, issued under sub-section (1) read with clause (b) of the Explanation to section 35AC of the Income-tax Act, 1961 (43 of 1961), the Central Government had specified at serial number 2, for Construction of buildings, purchase of books, vehicles, equipments, furnishing and running of “Valley for the Disabled” Project at Ayikudy, Shencottah Taluk, Tirunelveli District of Tamil Nadu by Amar Seva Sangam, Post Box No.1, Sulochana Gardens, 7-4-104B, Tenkasi Road, Ayikudi-627852, Tamilnadu, as an eligible project or scheme for a period of three years beginning with assessment year 1999-200 which was extended further vide notification number S.O.572(E) dated the 20th June, 2001 for a period of three years beginning with assessment year 2002-2003 and which was extended further vide notification number S.O.1608(E) dated the 14th November, 2005 for a period of two years beginning with financial year 2005-2006;