Embed Size (px)

Citation preview

GOVERNMENT SERVICE INSURANCE SYSTEMSOCIAL INSURANCE FUND

NOTES TO FINANCIAL STATEMENTS(All amounts in Philippine Peso unless otherwise stated)

1. GENERAL INFORMATION

The Government Service Insurance System (GSIS) is a government financial institution, organized and created to administer the System’s funds and implement the laws that govern the social security and insurance benefits of all government employees. The GSIS maintains its officially registered address at the Government Financial Center, Roxas Boulevard, Pasay City, which is also its Home Office. It has 15 Regional Offices, 25 Branch Offices, 19 Satellite Offices and 5 District Offices strategically located in various cities and municipalities of the country.

The GSIS was created by the Congress of the Philippines through the passing of Commonwealth Act No.186 on November 14, 1936. Its primary objective is to promote the welfare of the employees of the government through an insurance system that will protect its members against adverse economic effects resulting from death, disability and old age.

On May 31, 1977, Presidential Decree No. 1146, otherwise known as “Revised Government Service Insurance Act of 1977,” was issued by then President Ferdinand E. Marcos. On June 24, 1997, Republic Act (RA) No. 8291 otherwise known as, “The Government Service Insurance System Act of 1997”, was enacted into law, enhancing the social security coverage of the GSIS.

Pursuant to Section 34 of RA 8291, all contributions payable under Section 5 thereof, together with the earnings and accruals thereon shall constitute the GSIS Social Insurance Fund (SIF). The said Fund shall be used to finance the benefits administered by the GSIS under RA 8291. As such, the Social Insurance Fund (SIF) serves as the core fund of the GSIS, as distinguished from the other funds that the GSIS is mandated to administer.

The accompanying consolidated financial statements of the GSIS were authorized for issue by the GSIS management represented by the President and General Manager and the Senior Vice President – Controller Group on April 30, 2009.

2. CHANGE IN FINANCIAL STATEMENTS PRESENTATION

The GSIS Board of Trustees, in its Resolution No. 180, dated November 5, 2008, has approved the change in financial statements presentation of the GSIS Social Insurance Fund to conform to the format prescribed under Philippine Accounting Standards (PAS) 26 and International Financial Reporting Standards (IFRS) for pension funds.

PAS 26 prescribes measurement and disclosure principles for the reports of retirement benefit plans, under either defined contribution plan or defined benefit plan. The standard requires that for defined benefit plans, the financial statements shall contain a

9

statement of net assets available for benefits and a statement of changes in net assets available for benefits. The format in the disclosure and presentation of actuarial information, however, may vary (i.e. can be included as a statement of changes in the actuarial present value of promised retirement benefits; or in a disclosure in the notes to financial statements; or contained in a separate actuarial report).

The financial reporting format prescribed under PAS 26 is used for the reporting period December 31, 2008.

The financial statements for the Social Insurance Fund consist of the following:

Statement of Net Assets Statement of Changes in Net Assets Statement of Changes in Net Worth Cash Flow Statement Notes to Financial Statements

In compliance with PAS 27 which requires the preparation and presentation of consolidated financial statements for a group of entities under the control of a parent, and the applicable rules and regulations issued by the Commission on Audit, the Financial Statements of the GSIS Subsidiaries now form part of the GSIS Financial Statements for Social Insurance Fund for the year December 31, 2008 with 2007 as its transition date.

The adoption of PAS 27 involved the following steps/procedures:

The carrying amount of GSIS’ investment in each subsidiary and the GSIS portion of equity of each subsidiary are eliminated;

Intragroup balances, transactions, income and expenses are eliminated in full;

The accounts for both GSIS and those of the Subsidiaries were combined line by line by adding together like items of assets, liabilities, equity, income and expenses;

Minority interests in the profit or loss of consolidated subsidiaries for the reporting period are identified; and

Minority interests in the net assets of consolidated subsidiaries are identified separately from the GSIS’ net assets.

Basis of Consolidation

The consolidated financial statements include the financial statements of the GSIS and its subsidiaries as at December 31, 2008. Subsidiaries are consolidated from the date on which control is transferred to the Group and cease to be consolidated from the date on which control is transferred out of the Group. Consolidated financial statements are prepared using uniform accounting policies for like transactions and other events in similar circumstances. Inter-company balances and transactions, including intra-group profits and losses are eliminated.

10

The GSIS Subsidiaries and its percentage of ownership as at December 31, 2008 are as follows:

Subsidiaries Percentage of Ownership

GSIS Family Bank (GFB) 99.55%

GSIS Properties, Inc. (GPI) 100.00%

Meat Packing Corp. of the Philippines (MPCP) 100.00%

GSIS Mutual Fund Inc. (GMFI) 57.48%

Meat Packing Corporation of the Philippines, however, is not included in the consolidation. It is now in the process of liquidation, thus, equity method is used in recording GSIS’ investments in the subsidiary.

3. UPDATE ON GSIS NEW COMPUTERIZED SYSTEM

3.1 Integrated loans, membership, acquired assets and accounts management system (ILMAAAMS)

The ILMAAAMS is designed to handle and process all data requirements in four major areas that form the core of GSIS operations: membership, loans origination and administration, acquired assets, and accounts management. Its main objective is to have a concrete grasp on the concept of “one member view”. The system facilitates the automatic posting of financial data to the members’ accounts on a transaction level. As a result, the GSIS has drastically quickened the pace by which it administers membership accounts from loans processing to the identification of delinquent members – by integrating its financial requirements in all processes of loan granting, premium billing, and loan and premium collection.

ILMAAAMS can integrate with the general ledger system of the Financial Information (FI-GL). Transactions like loan granting and collections, premium billing and collections etc. are automatically reflected in the general ledger. There is seamless communication between these two systems.

At present, posting periods from January 1997 to December 2008 in the SAP are still open due to the on-going updating of members’ accounts.

3.2 Financial information system (FIS)

The FIS is designed to capture the recording of all the financial transactions from the source or feeder systems. These feeder systems have implementation environments different from that of the FIS subsystems. Financial data from various feeder systems are either automatically extracted and uploaded to FIS through interface program or generated in excel format following a Systems Applications and Programs (SAP)-

11

prescribed template with pre-defined accounting entries and manually uploaded to FIS through an upload program. The following are the different feeder systems and a brief description on how accounting data are captured and fed to the FIS:

a. Technistock portfolio management system (TPMS)

The TPMS is a portfolio management solution which was customized to fit the back-office portfolio requirements of the Investment Management Office. It captures transactions involving equities as well as local and foreign fixed-income securities. It also handles accruals, maturities, amortizations of bond and premiums and mark-to-market valuations of equities. The system generates a SAP-prescribed template with predefined accounting entries in excel format for batch uploading to FIS.

b. Human resources information system (HRIS)

The payroll system of the GSIS is processed through HRIS. The system generates the payroll file with predefined accounting entries in excel format. The file is saved in a specified storage directory, and extracted for batch uploading to FIS.

c. Real and other properties owned and acquired (ROPOA) and Leasing manager

The ROPOA Manager is a system used for monitoring and recording the acquisition, administration and disposition of acquired assets. For financial recording purposes, the system is capable to do the following:

Creation of records for new acquired assets upon tagging of loans in default in the Customer Mortgage Loan (CML) module of ILMAAAMS;

Seamless interface with Leasing Manager for the creation of rental record and accrual of rental receivables;

Generation of report on gain or loss on valuation;

Tagging of acquired assets as disposed upon cash or installment sale; and

Automatic creation of interface file for FIS to book newly acquired assets, gain or loss on valuation, disposal and closing of corresponding rental receivables upon cash or installment sale.

The Leasing Manager, on the other hand, is a system that creates the records for the accrued rental receivables on occupied properties that were previously covered by cancelled deed of conditional sale (DCS) and occupied foreclosed properties after the expiration of the redemption period. For financial recording purposes, the system is capable to do the following:

12

Creation of property record, lease contract and tenant record;

Monthly accrual of rental receivables;

Generation of statement of account on rental receivables;

Posting of rental payments from cash desk (CD) module as well as those collected through Claims and Loans Interdependency Program (CLIP);

Stoppage of rental receivable upon conclusion of sale; and

Automatic creation of interface file for FIS to book accrued rental receivable, rental payments collected or “CLIPped”, and closing of rental receivables upon disposition of acquired assets.

Both systems generate file with predefined accounting entries in excel format. The file is saved in a specified storage directory and extracted for batch uploading to FIS.

d. Claims and pensions administration system (CPAS)

CPAS is a comprehensive application system that will consolidate all information and processing requirements of members’ claim, pension, retirement and dividend under the new open system platform - SAP.

The CPAS is designed to provide online facility for inquiry, processing and computation of life, retirement and survivorship claims. It can integrate with the general ledger system of the FIS. Completed transactions of claims and pensions will be automatically reflected in the general ledger. The CPAS Project will be implemented in 2009.

At present, all social insurance claims and pensions are uploaded to FIS through manually-prepared templates based on the monthly abstract of disbursed claims extracted by the Information Technology Services Group (ITSG) from the mainframe.

The GSIS is still in a transition period due to the recent implementation of the new systems, thus the financial statements for CY2008 were prepared manually based on the readily available data from the SAP and feeder systems.

4. RECORDING OF COLLECTIONS AND DISBURSEMENTS IN FIS 4.1 Collections

a. Collections thru the Financial information - Cash desk (FS-CD) facility of ILMAAAMS

13

Effective October 13, 2008, all collections pertaining to loans and contributions were processed thru the FS-CD of ILMAAAMS where transactions are automatically recorded simultaneously in the general ledger and subsidiary ledger.

b. Collections thru the Cash receipts and management system (CRMS)

All collections pertaining to Social Insurance (SI) accounts not covered by the FS-CD, investments and other miscellaneous transactions are processed thru the CRMS. Collections done thru the CRMS are uploaded to FIS through the use of templates.

c. Collections covered by Letter of authority (LOAs)

All collections pertaining to investment maturities and interests and all fund transfers from other bank accounts are covered by LOAs. Collections that are covered by LOAs are uploaded to FIS through manually prepared templates based on the manually processed LOAs.

Effective December 2008, all LOAs covering incoming collections are prepared in the SAP where transactions are automatically recorded in the FI-GL.

4.2 Disbursements

All disbursements pertaining to investments, payroll and other miscellaneous transactions from January to May 2008 were uploaded to Financial Information System (FIS) through manually prepared templates based on the manually-processed disbursement vouchers and LOAs.

In June 2008, the Accounts Payable (AP) Module, one of the subsystems of the FIS was implemented. The subsystem provides automated support in processing the miscellaneous disbursements of the GSIS. It generates disbursement checks and provides accounting information.

Effective October 2008, all LOAs covering miscellaneous disbursements and fund transfers to other bank accounts are prepared in the SAP where transactions are automatically recorded in the FI-GL.

5. GSIS RATIONALIZATION PROGRAM

In 2008, the GSIS underwent a major change in its corporate structure. The rationalization was a direct offshoot to the implementation of the new computerized systems in the GSIS operational processes.

As the GSIS geared towards full automation, a lot of units were rendered irrelevant and a number of employees previously engaged in paper-based transactions were left in operational limbo. There was an overlapping of functions. As a result, the GSIS has offered the GSIS Retirement Incentive Program (GRIP) to solve its “redundancy

14

problem” and to be able to hire people with expertise and necessary skills and talents that will improve the overall productivity and operational efficiency of the System. There were 790 GSIS employees who availed of the retirement program. In the light of the implementation of the FIS, the accounting function was centralized in the Home Office; hence the accounting divisions in the Field Offices were abolished.

The GSIS has applied the so-called “scrap and build” scheme wherein certain executive positions that have been vacated were dissolved and converted into multiple lower-rank positions. The cost of keeping many of these created positions virtually equaled the cost of paying the few executive positions that were vacated.

The GSIS Corporate Rationalization has been approved in a series of board resolutions, as follows:

Board Resolution No. 197, dated December 3, 2008; Board Resolution No. 70, dated May 14, 2008; and Board Resolution No. 62, dated April 23, 2008.

6. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

6.1 Basis of preparation of financial statements

The accompanying financial statements for the Social Insurance Fund (SIF) have been prepared in accordance with the Philippine Accounting Standards (PAS)/Philippine Financial Reporting Standards (PFRS) and the generally accepted insurance principles and reporting practices prescribed by the Insurance Commission.

The financial statements are prepared on historical cost basis, except for certain financial instruments and investment property which are carried at fair values.

6.2 Centralized deposit and funding system or “One-bank account” policy

Under the centralized deposit and funding system, all collections are deposited to a centralized collection account and all disbursements are funded through the same account, which is maintained in the Home Office.

This cash management policy is adopted to manage efficiently the cash in bank and to strengthen the monitoring and control of cash flows.

6.3 Cash and cash equivalents

Cash includes cash on hand and in banks. Cash equivalents are short - term and highly liquid investments with original maturity of less than three months, are readily convertible into cash. These include special savings deposits and time deposits.

6.4 Contributions and premiums receivable

Pursuant to Section 5 of RA 8291, it shall be mandatory for all the covered members of the GSIS to pay monthly contributions based on the members’ Monthly Compensation

15

(MC), as follows: nine per cent thereof payable by the member and 12 per cent payable by the employer. The premium contributions are remitted directly to the GSIS within the first ten days of the month following the month to which the contributions apply.

Based on the monthly billing reports, premium contributions are set-up in the books as Premiums Receivable and correspondingly presented as additions to net assets. Upon actual receipt of remittances, the receivable account is adjusted accordingly.6.5 Loans and accounts receivable

Loans and accounts receivables are stated net of deferred income or provision for estimated uncollectible accounts.

a. Provision for probable losses is established for estimated losses on the principal portion of business loans and receivable accounts based on management’s evaluation if the accounts are collectible.

b. Allowance for doubtful accounts/bad debts is established for estimated losses on the interest income portion of business loans and receivable accounts.

6.6 Investments

Investments are classified according to the following categories at initial recognition based on the purpose for which they are acquired.

a. Held for trading (HFT) or Fair value through profit or loss (FVPL)

These are financial assets acquired principally for the purpose of generating profit from short-term fluctuations in price or dealer’s margin.

These are initially recorded at cost and are revalued at fair values every reporting date. Any difference between the cost and the fair value is recorded as appreciation or depreciation of the fair value of investments in the statement of changes in net assets. Investments in equity securities - stocks traded are classified as HFT or FVPL and as such, these are recorded at cost and are revalued every month-end.

b. Held-to-maturity investments (HTM)

These are financial assets with fixed or determinable payments and fixed maturities. They are carried at amortized cost using the effective interest method and are classified as non-current assets.

Investments in Foreign Currency and Peso Denominated Bonds are classified as Held to Maturity and as such, these are recorded at cost, duly adjusted periodically through the amortization of premiums or discounts.

c. Available-for-sale (AFS)

16

AFS financial assets are acquired and held indefinitely for long-term capital appreciation or are not classified as (a) loans and receivables (b) held-to-maturity investments or (c) financial assets of fair value thru profit and loss. These assets are initially recognized at cost and are subsequently valued at fair values. Any difference between the cost and the fair value is recorded as appreciation or depreciation of the fair value of investments in the statement of changes in net assets. d. Investments in subsidiaries

The System practices the equity method in accounting for investments in shares of stocks in which it holds at least 20 per cent ownership or where it has the ability to exercise significant influence over the companies’ operating and financial affairs.

The equity method is a method of accounting whereby the investment is initially recognized at cost and adjusted thereafter for the post-acquisition change in the net investors’ share of the net assets of the investee.

e. Investments in non-traded stocks

Non-traded stocks are valued at cost, net of allowance for impairment in value.

6.7 Investment property

Investment property pertains to land or a building or part of a building or both, held to earn rentals or for capital appreciation or both.

These consist of real properties that are previously the subject of mortgage loan, individual real estate loan, commercial-industrial loan, lease-purchase agreement, or deed of conditional sale, which are either foreclosed or cancelled or dacioned by former owners in favor of the System.

a. Fair valuation model

In compliance with Philippine Accounting Standard (PAS) 40, the GSIS applies fair value model consistently on its investment property, whereby the assets are initially recorded at cost (consisting of the purchase price and any directly attributable expenditures), then subsequently valued at fair values.

Gains or losses from changes in fair values are recognized during the period in which they occur.

b. Selling price

In November 2007, the GSIS Board of Trustees thru Board Resolution No. 167 approved the computation of the new selling price of acquired housing units and lots for disposition by applying the higher of 70 per cent of the current market

17

values (CMV) of the said acquired properties; and book value plus 50 per cent of the rental receivables of the acquired property.

6.8 Property and equipment

These assets are recognized and recorded in accordance with PAS 16.

Depreciation is computed in conformity with the provisions of COA Circular No. 2003-007 dated December 11, 2003. The COA Circular provides the revised estimated useful life in computing depreciation for government property, and equipment effective January 1, 2004. The major changes involve the following:

Depreciation is computed on a straight-line method based on the estimated useful life of 20 to 30 years for buildings and a residual value of ten per cent of the acquisition cost/appraised value thereof.

Prior to CY 2004, the salvage value for building was computed at five per cent of its cost while useful life is estimated at 50 years. For land improvements, depreciation was computed at five per cent residual value and useful life of five years.

In October 2004, the above circular was amended by COA Circular No. 2004-003 which prescribes that the resulting adjustment from the change in the depreciation computation shall be charged to the current depreciation expense and that past depreciation expense need not be adjusted.

Computer equipment is carried at cost less salvage value of ½ per cent of the cost of the equipment. Depreciation is computed on a straight-line method over estimated life of five years.

In September 2008, the Asset Accounting (AA) Module, one of the FIS subsystems was implemented. The subsystem is designed to manage and supervise all GSIS’ assets which are used in the normal business operations. These assets include, but are not limited to, land and land improvement, building and building improvement, information technology (IT) resources, construction in progress, furniture, equipment and fixtures, and asset under construction (AUC).

The AA module provides an efficient and effective system of recording assets in the financial book of accounts from asset acquisition, transfers, retirements, and depreciation postings. It also serves as a subsidiary ledger to the financial information - general ledger (FI-GL), providing detailed information on asset transactions.

6.9 Revenue recognition

The major sources of operating revenues of the Fund are investment income, interest income from loans, rental income from investment property and other income.

The GSIS uses the accrual method in recognizing revenues.

a. Service loans

18

The full implementation of ILMAAAMS and FIS facilitates the accurate computation and recording of interest for each loan and timely distribution of collection to the proper loan account. The system computes interests in advance on eCard cash advance, emergency loans, emergency loans assistance and pension loans for the entire term of the loan upon granting and are made part of the loan amortization. This is recorded as deferred interest income and recognized as earned upon collection.

b. Housing loans Accrual of interest on housing loans, Real estate loans (REL) and Deeds of conditional sale (DCS)

The system accurately computes and records interest on REL and DCS and timely distributes collections to the proper loan account.

Interest Income on housing loans, REL and DCS

In May 2007, the interest rate on housing loans was reduced to six per cent pursuant to “SAIS Program”. A grace period of three months (May to July 2007) was provided under this program. Hence, interests at six per cent for these three months based on the outstanding principal balance as of April 30, 2007 are capitalized and are made part of the new outstanding principal.

6.10 Foreign currency transactions and translations

a. Functional and presentation currency

The financial statements are measured and presented using the Philippine Peso, which is the System’s functional and presentation currency.

b. Foreign currency translations

Foreign currency income and expenses are translated into Philippine Pesos based on the Philippine Dealing System Weighted Average Rate (PDSWAR) exchange rate prevailing on transaction dates.

Foreign currency-denominated assets and liabilities are translated into Philippine Pesos based on PDSWAR prevailing at the end of the interim reporting period. At the end of the reporting year, foreign currency-denominated assets and liabilities are translated to Philippine Peso using the exchange rate provided by the Insurance Commission.

Gain or Loss from foreign exchange transactions and revaluation of foreign currency–denominated assets and liabilities are credited to or charged against current operations.

19

6.11 Administrative loading

Pursuant to Section 35, RA 8291, the Fund is allowed to disburse a maximum of 12 per cent of the annual revenues from all sources for administrative and operating expenses.

6.12 Claims and benefits

Regular disbursements of the Social Insurance Fund comprise the claims of members/pensioners involving the following:

Life insurance benefits claims which consist of policy maturities, cash surrender values, disability benefit, death benefit, accidental benefit, accidental death benefit, and funeral benefits;

Retirement Claims;

Monthly Old-Age Pension;

Monthly Survivorship Pension; and

Cash Gift to all entitled old-age pensioners

6.13 Actuarial reserves

Actuarial Reserve requirements for the mandated obligations of the System are computed monthly by the GSIS Actuarial Group based on certain assumptions which are in accordance with generally accepted principle of actuarial valuation. The actuarial reserves are set up / appropriated out of the accumulated earnings of the Social Insurance Fund. Any amount in excess of actuarial reserves requirements is presented as additional reserves for contingencies.

6.14 Non-admitted assets

Pursuant to Section 179 of the Insurance Code, certain assets are not allowed as Admitted Assets; hence, are presented as Non-Admitted Assets. These are furniture, fixtures and equipment; deposit and indent orders; supplies and materials in stock; prepaid expenses; income receivable; and such other assets proven to be of doubtful value.

Non-Admitted Assets include accrued interests on obligations of Department of Budget and Management (DBM) and other government agencies for unpaid and/or delayed remittances of social insurance premiums and rental receivable on occupied housing units with cancelled DCS and foreclosed REL. Since collection thereof is very low and the receivables are not readily realizable, the same were classified from admitted to non-admitted assets.

6.15 Related party transactions/agreements

20

Related party relationships exist when one party has the ability to control, directly or indirectly through one or more intermediaries, the other party or exercise significant influence over the other party in making financial and operating decisions. Such relationships also exist between and/or among entities which are under common control with the reporting enterprise, or between and/or among the reporting enterprises and their key management personnel, directors, or its stockholders. Transactions between related parties are accounted for at arm’s length prices or on terms similar to those offered to non-related entities in an economically comparable market.

PAS 24 provides additional guidance and clarity in the scope of the standard definitions and disclosures for related parties.

7. CASH AND CASH EQUIVALENTS

This account consists of the following:

2008 2007

Cash on hand and in banks 4,581,137,015 3,086,682,259

Cash equivalents 40,573,044,950 7,240,720,523

45,154,181,965 10,327,402,782

8. RECEIVABLES

This account consists of the following:

2008 2007

Contributions and premiums receivable 19,143,790,623 18,153,430,739

Other receivables 57,195,190,667 37,797,607,988

76,338,981,290 55,951,038,727

8.1 Contributions and premiums receivable

General Ledger (GL) and Subsidiary Ledger (SL) Discrepancies

At present, the SL balances of the contributions and premiums receivable are not yet fully reconciled with their GL balances due to the ongoing cleansing and updating of the members’ records. In the design of the Financial Information System (FIS), the reconciliation of the discrepancies between SL and GL balances of contributions and premiums receivable was taken into consideration by creating migration GL accounts (eight series) representing the Controller’s records and another GL accounts (one series) linked to

21

the SL. This was done to preserve the balances of the GL and SL upon migration to the FIS.

It will only be upon completion of the updating of members’ records that the final adjusting entry will be recorded to reconcile discrepancies between GL and SL balances of contributions and premiums receivable. The difference between SL and GL will be closed to the surplus adjustments account.

8.2 Other receivables

Other receivables account consists of the following:

2008 2007

Revenue receivable 33,235,076,787 26,854,128,760Notes receivable 21,143,238,859 7,249,094,589Accounts receivable for deficit cases - net 329,513,793 331,685,741Contingent asset disallowance 53,289,367 82,365,687Advances to contractors 16,437,718 16,623,327Cash advances 3,265,576 2,628,276Other receivable-agencies with MOA 1,310,747,885 1,963,971,930Other receivables-subsidiaries 368,541,390 423,144,247Sundry accounts receivable - net 735,079,292 873,965,431

57,195,190,667 37,797,607,988

The increase in Notes Receivable account of P13.894 billion or 192 per cent is primarily due to the installment sale of MERALCO shares in October 2008.

Other receivables - subsidiaries

Other receivables-subsidiaries account consists of the following:

2008 2007

Due from Bangko Sentral ng Pilipinas 20,941,645 25,164,221Due from other banks 11,707,712 30,610,560Sales contract receivable 18,395,913 8,197,077Other assets 317,496,120 359,172,389

368,541,390 423,144,247

22

9. INVESTMENTS

This account consists of the following:

2008 2007

Financial securities 179,874,367,445 198,397,244,691Loans – net 122,866,606,555 125,855,725,578Investment property 26,273,028,467 23,969,501,391

329,014,002,467 348,222,471,660

9.1 Financial securities

Financial securities account consists of the following:

2008 2007

ROP notes and bonds – Held to maturity 107,463,707,147 89,010,872,380ROP bills 24,907,207,476 21,481,553,619Externally managed funds - global 24,014,881,155 -Externally managed funds - domestic 5,141,899,817 6,444,649,437Stocks - traded - AFS 4,267,457,282 14,666,478,660Investment in bonds and other debt instruments 3,866,611,085 5,175,618,663Investment in joint venture 1,275,317,941 975,317,941Stocks - non-traded 921,681,100 921,681,100Investment in subsidiaries 762,808,146 762,808,146Stocks - traded – Held for trading 429,983,804 918,664,745Asset participation certificate 181,257,354 551,600,000STI placements - BSP - 34,000,000,000Other investments - subsidiaries 6,641,555,138 23,488,000,000

179,874,367,445 198,397,244,691

a. Investment in externally managed funds - global

The Board of Trustees in its resolution no. 155 dated October 25, 2007 approved the hiring of ING Investment Management (ING IM) and Credit Agricole Asset Management (CAAM) as global fund managers of GSIS with the following objectives:

Assist the GSIS to invest in global financial instruments through sufficient diversification among asset classes and geographically; and

Provide GSIS with consistent investment returns with capital preservation and sufficient liquidity over a three-year period.

23

b. Foreign-currency denominated Republic of the Philippines (ROP) bonds

The foreign-currency denominated ROP bonds in the total amount of P58.387 billion were reclassified from HFT or FVPL to HTM.

Due to the current financial crisis resulting in market volatility, the Philippine Financial Reporting Standard Council (PFRSC) has approved last October 29, 2008 the immediate adoption of the amendments to PAS 39, reclassification of financial assets from HFT to HTM.

The Bangko Sentral ng Pilipinas (BSP) came out with the Guidelines on the Reclassification of Financial Assets between categories under Circular Nos. 626 and 628 dated October 23 and 31, 2008, respectively. BSP allowed financial institutions to look back anytime between July 1, 2008 and November 14, 2008 for the purpose of selecting the effective date of their reclassification.

GSIS has selected the date August 31, 2008 to reclassify its FCY ROPs from HFT to HTM, resulted in a net unrealized gain of P0.539 billion.

9.2 Loans - net

The total loans financed by the Fund consist of the following:

2008 2007

Consolidated loans 56,284,297,406 44,360,545,786Salary loans 19,223,207,405 30,340,974,859Policy loans 14,786,620,440 15,029,972,934Real estate loans 9,745,080,544 10,499,207,847Government loans 6,371,007,803 6,293,973,426eCard plus cash advance loan 5,090,752,378 6,156,104,292Deeds of conditional sale 3,034,998,762 3,155,499,579Private loans 2,955,023,616 2,922,463,919Emergency/calamity loans 1,999,915,481 1,119,491,486Summer one month 1,451,624,139 2,675,319,482Pension loan 1,325,666,478 1,262,362,129Emergency loan assistance 543,517,291 910,608,847Lease purchases 160,016,846 160,016,846Stock purchase loans 41,043,549 44,353,094Educational assistance loans 31,889,936 32,438,993Loans receivable-subsidiaries - 703,835,241eCard cash advance loan (178,055,519) 188,556,818

122,866,606,555 125,855,725,578

General Ledger (GL) and Subsidiary Ledger (SL) Discrepancies

24

At present, the SL balances of service loans and interest receivable are not yet fully reconciled with their GL balances due to the ongoing cleansing and updating of the individual loan accounts.

In the design of the FIS, the reconciliation of the discrepancies between SL and GL balances of loans and interest receivable was taken into consideration by creating migration GL accounts (eight series) representing the Controller’s records and another GL accounts (one series) linked to the SL. This was done to preserve the balances of the GL and SL upon migration to the FIS.

It will only be upon completion of the updating of members’ loan accounts that the final adjusting entry will be recorded to reconcile discrepancies between GL and SL balances of loans and interest receivable. The difference between SL and GL will be closed to the surplus adjustments account.

As at December 31, 2008, the summary of the SL balances based on SAP-ILMAAAMS data for service and housing loans and the GL balances for the same showed the following:

GL SL Difference Over/(Under) % to GL

Service loansConso-loan 56,284,297,406 59,320,604,560 (3,036,307,154) (5.39)

Salary loan 19,223,207,405 25,574,318,403 (6,351,110,998) (33.04)

Policy loans 14,786,620,440 19,003,901,008 (4,217,280,568) (28.52)eCard cash advance/ eCard plus cash advance loan

4,912,696,859 5,834,824,157 (922,127,298) (18.77)

Emergency/Calamity loan/ Emergency loan assistance 2,543,432,772 5,458,986,520 (2,915,553,748) (114.63)

Summer one month salary loan 1,451,624,139 1,135,843,176 315,780,963 (21.75)

99,201,879,021 116,328,477,824 (17,126,598,803) (17.26)

Housing loansReal estate loans 9,745,080,544 14,536,939,613 (4,791,859,069) (49.17)Deeds of conditional sale 3,034,998,762 4,828,945,881 (1,793,947,119) (59.11)

12,780,079,306 19,365,885,494 (6,585,806,188) (51.53)

111,981,958,327 135,694,363,318 (23,712,404,991) (21.18)

9.3 Investment property

As of December 31, 2008, Investment property is broken down as follows:

2008 2007

25

Cancelled deeds of conditional sale/ (Mass housing) 14,611,671,110 14,727,394,969

Foreclosed real estate loans 161,498,118 161,498,118

Other investment property 11,499,859,239 9,080,608,304

26,273,028,467 23,969,501,391

The investment property of the GSIS earned P2.999 billion in 2008 and P1.862 billion in 2007, primarily from the capital appreciation, disposition and rental of the property.

10. PROPERTY AND EQUIPMENT – NET

The property and equipment account consists of the following:

Land and land

improve- ments

Building andimprove-

ments

Real estate

apprecia-tion

Technology (IT)

resources

Construc-tion in

progressFFE -

Subsidiary TotalCost

January 1, 2008 486,988,528 4,014,468,195 69,781,103 1,815,410,612 36,237,805 50,660,687 6,473,546,930

Additions - 71,878,178 - 259,804,217 359,531,123 10,338,559 701,552,077

Adjustments - (110,613) - 7,912,136 (92,569,946) (165,274) (84,933,697)Derecognition in books(due to donations/sale) - - - (22,066,557) - (1,260,830) (23,327,387)

December 31, 2008 486,988,528 4,086,235,760 69,781,103 2,061,060,408 303,198,982 59,573,142 7,066,837,923

Accumulated Depreciation

January 1, 2008 185,393,050 1,167,362,088 - 1,042,545,897 - 32,347,009 2,427,648,044

Depreciation Charges during the year 407,205 142,084,607 - 169,058,354 - 5,823,711 317,373,877

Derecognition in the books – (due to donations/sale of unserviceable units)

- - - 19,859,901 - (1,225,416) 18,634,485

Adjustments 157,013 (1,613) - - (187,624) (32,224)

December 31, 2008 185,957,268 1,309,445,082 - 1,231,464,152 - 36,757,680 2,763,624,182

Net Book Value – December 31, 2008 301,031,260 2,776,790,678 69,781,103 829,596,256 303,198,982 22,815,462 4,303,213,741

Net Book Value – December 31, 2007 301,595,478 2,847,106,107 69,781,103 772,864,715 36,237,805 18,313,678 4,045,898,886

11. OTHER ASSETS

26

The Other assets account consists of the following:

2008 2007

Discontinued operationsLand 43,048,600 43,048,600Building 2,975,410 2,975,410Paintings and tapestries 18,566,310 16,693,267

64,590,320 62,717,277

12. SOCIAL INSURANCE CLAIMS PAYABLE

Social insurance claims payable account pertains to the claims on retirement and life insurance benefits due to members as at December 31, 2008 but which remained unpaid as of year-end broken down as follows:

2008 2007

Claims and benefits payableRetirement claims 2,784,448,463 387,089,954Life insurance claims 1,738,692,401 634,472,676Survivorship 44,619,450 50,494,105 Funeral 6,309,144 -Other social insurance benefits-scholarship program 12,000,000 111,239,242

4,586,069,458 1,183,295,977

Dividends payable 967,886,097 1,063,824,019

5,553,955,555 2,247,119,996

Dividends payable

The GSIS Board of Trustees under Resolution No. 206 dated December 17, 2008 declared an annual cash dividend of P950 million to Compulsory Life Insurance Policy Holders, chargeable against the surplus of the Social Insurance Fund.

13. DEFERRED CREDITS

Deferred credits account consists of the following:

2008 2007

27

Unrealized income 7,955,262 286,395,648

Undistributed collections 311,334 311,334

8,266,596 286,706,982

14. OTHER LIABILITIES

This account consists of the following:

2008 2007

Funds held in trust 1,082,397,308 894,095,905Due to Philam asset management 33,831,476 17,753,632Leasehold liability 4,221,855 4,221,855Sundry accounts payable 1,893,063,917 2,822,422,395Other liabilities – subsidiaries 1,626,554,297 1,202,729,532

4,640,068,853 4,941,223,319

14.1 Funds held in trust

2008 2007

DBM payments to Philippine Health Insurance Corporation (PHIC) 408,875,850 408,875,850

FHIT-Bidder's Deposits – ROPOA 144,102,799 33,356,097

FHIT-(developer) 166,379,057 166,379,057

GSIS Employee Loyalty Incentive Plan (ELIP) Retirement fund 96,057,740 96,057,740Others (retention fee of contractor/Bid Security/Performance Bond/Rental Deposit/Cash collateral) 266,981,862 189,427,161

1,082,397,308 894,095,905

14.2 Sundry accounts payable

28

The account consists of the following:

Accrued employees’ benefits - in compliance with PAS 19; Administrative and operating expenses already incurred but not yet paid as of

balance sheet date; Goods already delivered and services already rendered but not yet paid as of

balance sheet date; Unpaid bank service fee on eCrediting transactions; Negative loan balance for refund; and Custody fee.

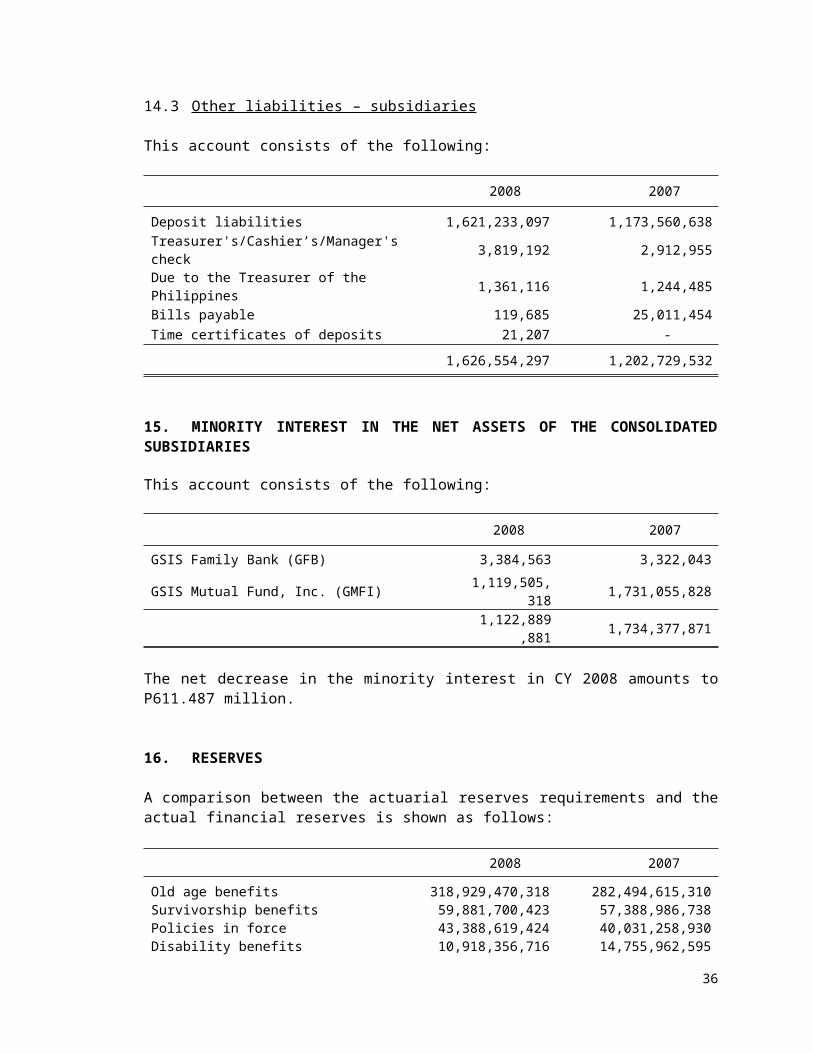

14.3 Other liabilities – subsidiaries

This account consists of the following:

2008 2007

Deposit liabilities 1,621,233,097 1,173,560,638Treasurer's/Cashier’s/Manager's check 3,819,192 2,912,955Due to the Treasurer of the Philippines 1,361,116 1,244,485Bills payable 119,685 25,011,454Time certificates of deposits 21,207 -

1,626,554,297 1,202,729,532

15. MINORITY INTEREST IN THE NET ASSETS OF THE CONSOLIDATED SUBSIDIARIES

This account consists of the following:

2008 2007

GSIS Family Bank (GFB) 3,384,563 3,322,043

GSIS Mutual Fund, Inc. (GMFI) 1,119,505,318 1,731,055,828

1,122,889,881 1,734,377,871

The net decrease in the minority interest in CY 2008 amounts to P611.487 million.

16. RESERVES

29

A comparison between the actuarial reserves requirements and the actual financial reserves is shown as follows:

2008 2007

Old age benefits 318,929,470,318 282,494,615,310Survivorship benefits 59,881,700,423 57,388,986,738Policies in force 43,388,619,424 40,031,258,930Disability benefits 10,918,356,716 14,755,962,595Burial benefits 2,568,096,718 3,108,173,582Contingencies 1,700,667,353 1,771,167,122Actuarial reserves requirements 437,386,910,952 399,550,164,277Surplus appropriated to additional reserves for contingencies 6,162,877,946 9,849,936,887

Total reserves 443,549,788,898 409,400,101,164

The reserves for policies in force are computed using the mean reserve formula. This formula assumes that the entire premium for the calendar year was paid at the beginning of that policy year. The amount presented above is net of P2.576 billion representing the net deferred premiums for 2008.

17. LOANS AND INVESTMENT REVENUE – NET

This consists of the following:

2008 2007

Revenue from loansInterest on conso loans 6,145,029,749 4,188,448,690 Interest on salary loans 3,008,571,976 6,891,561,943 Interest on policy loans 1,284,309,972 1,883,655,265 Interest on eCard plus cash advances 698,756,211 459,223,051 Interest on real estate loans 443,177,636 805,297,716 Interest on emergency/calamity loans 357,943,573 288,355,903 Interest on SOS loans 278,714,331 1,002,071,085 Interest on deeds of conditional sale 187,565,614 552,030,761 Interest on emergency loan assistance 171,660,235 367,508,207 Interest on pension loans 168,606,815 128,319,762 Interest on eCard cash advances 140,752,792 679,830,647 Interest on private loans 18,678,201 97,308,575 Interest on government and government guaranteed loans 485,991,472 298,075,447 Service revenue 458,947,455 376,376,162 Surcharge on loans in arrears 105,041,469 591,450,769 Interest revenue from loans – subsidiaries 1,175,623,435 1,544,771,798

15,129,370,936 20,154,285,781

Revenue from investments

30

Gain on sale of stocks 9,221,355,361 10,595,433,264(Loss)/Gain on sale of bonds (457,362,100) 85,304,852

8,763,993,261 10,680,738,116

Net appreciation/(depreciation) in FV of investmentsUnrealized gain(loss) – Held for trading 187,123,950 (8,966,276,792)

Interest on investmentsInterest on ROP notes and bonds 6,387,885,228 8,874,390,380Interest on ROP bills 1,409,298,257 1,250,525,067Interest on Asset Participation Certificates 29,154,327 47,537,194

7,826,337,812 10,172,452,641

2008 2007

Gain/(loss) on forex 5,579,746,574 (390,324,546)Dividend on stocks 607,280,714 301,641,082Externally managed funds – domestic - 444,649,437Other investment revenue 2,979,221,089 2,453,685,291(Loss)/Gain on revenue from investments - subsidiaries (1,288,890,561) 626,429,422

7,877,357,816 3,436,080,686

Investment expensesInterest expenses 878,068,776 1,414,797,735Investment fees and others 45,774,405 28,911,428 Expenses on eCard 38,508,995 85,834,094 Foreclosure expenses 8,750,861 136,234,084 Bad debts expenses - 6,713,963Impairment loss - 527,181,540

971,103,037 2,199,672,844

23,683,709,802 13,123,321,807

Revenue from investment propertyGain on valuation of investment property 2,813,566,294 1,771,874,934 Gain on disposition of investment property 110,198,972 16,600,847Rental of investment property 75,549,036 73,740,545

2,999,314,302 1,862,216,326

41,812,395,040 35,139,823,914

18. OTHER REVENUE This account consists of the following:

2008 2007

31

GSIS fees and commissionsMarketing commission 1,098,675,080 1,042,593,659Administration fee 979,166,878 680,185,635Management fee 182,941,745 216,008,464

2,260,783,703 1,938,787,758Interest on receivables – agencies with MOA 228,629,079 49,933,757Revenue from rental 104,759,883 96,835,510Interest on savings deposits 20,341,158 29,973,164Refund of gratuity 771,252 55,506Gain/(Loss) on disposition of assets 4,966 66,013,252Others 61,308,567 409,115,800

2,676,598,608 2,590,714,747

GSIS fees and commissions revenues

The Social Insurance Fund, being the administrator of the General Insurance Fund (GIF) which consists of the General Insurance business, Optional Life Insurance (OLI) business and Pre-Need (PN) business, and Employees Compensation Insurance Fund (ECF), charges the latter funds administration fees, marketing commissions, and management fees, as follows:

Ten per cent Administration Fee based on the three Businesses’ respective gross income;

Twenty per cent Marketing Commission based on gross premium earned of the GI and the OLI businesses; and

Ten per cent Management fee on ECF premium collections.

19. PERSONAL SERVICES

This account consists of the following:

2008 2007

Salaries and wages 1,245,788,205 1,440,583,431Statutory expenses 690,106,275 842,772,613Allowances 491,828,777 598,489,501Fringe benefits 448,236,024 464,473,389Bonus/Awards 311,586,642 388,124,961

3,187,545,923 3,734,443,895

20. OPERATING EXPENSES

This account consists of the following:

32

2008 2007

Separation pay 1,644,405,835 136,340,697Depreciation and amortization expense 368,221,726 357,468,309Electric and water consumption 127,619,557 143,201,474Assets and facilities maintenance expense 122,449,946 157,755,974Public relations and advertisement 120,234,894 129,763,725Retainer's and consultants 99,803,265 103,142,809Communication services 84,425,133 132,767,648Insurance expense 83,033,394 90,917,973Overtime expenses 80,039,345 32,373,828Auditing expenses 78,563,877 72,155,215Computer expenses 71,258,530 125,649,426Office supplies expenses 65,940,078 187,946,230Education, training and scholarship 42,667,692 46,957,686

2008 2007

Traveling expenses 33,358,679 66,559,722Contractual services 31,929,565 76,868,564Rental expenses 25,759,689 51,463,339Provision for income tax 21,688,790 10,961,911Representation expenses 16,820,370 20,093,666Athletic and cultural expenses 15,320,604 11,318,707Taxes and licenses 14,721,706 17,048,853Discretionary expenses 14,063,674 10,214,548Fuel and gasoline consumption 13,135,192 14,974,978Contributions-others 2,921,748 2,329,715Medical supplies expenses 2,155,423 2,482,426Extra remuneration 966,873 5,977,785

33

Library books and materials 395,857 717,442Amortization expenses - 6,544,308Miscellaneous expenses 137,089,657 77,036,740 3,318,991,099 2,091,033,698

Separation pay increased by P1.508 billion or 1,106 per cent while personal services decreased by P0.546 billion or 15 per cent. The increase in separation pay and decrease in personal services are primarily due to the 790 GSIS employees who availed of the GSIS Retirement Incentive Program (GRIP) in 2008.

GSIS was able to finance the retirement pay out of the savings from the approved budget for CY 2008.

21. MINORITY INTEREST IN THE NET (LOSS)/INCOME OF THE CONSOLIDATED SUBSIDIARIES This account consists of the following:

2008 2007

GSIS Family Bank (GFB) 293,078 497,914

GSIS Mutual Fund, Inc. (GMFI) (545,615,537) 186,438,128

(545,322,459) 186,936,042

22. OTHER (DEDUCTIONS)/ ADDITIONS

This account consists of the following:

2008 2007

Decrease in non-admitted assets/ Increase in income/surplus 952,063,227 (2,028,690,199)

Increase in minority interest in the changes in the equity of the consolidated subsidiaries 66,165,531 (1,734,377,871)

Decrease in unrealized (loss)/gain – Available-for-sale (13,401,533,025) 8,686,394,026

34

Decrease in proceeds(payment) from issuance (redemption) of capital stock – net (160,527,264) 1,750,533,435

Decrease in surplus adjustments (44,998,028) 632,875 Decrease in contingent surplus (29,161,579) 82,371,917 Decrease in appraisal surplus - 72,994,538 Decrease in donation surplus - 11,677,212

(12,617,991,138) 6,841,535,933

22.1 Non-admitted assets

The Non-admitted assets account consists of the following:

2008 2007

Furniture, fixtures and equipment - net 387,568,807 355,055,970Loans and investment 304,511,943 309,511,943Prepaid expenses 55,601,461 1,021,050,796Medicines and other medical supplies 25,829,774 25,861,006Supplies and materials in stock 19,721,103 31,136,359Deposit and Indent orders 9,416,609 9,639,472Educational assistance loan 7,244,209 7,244,209Contingent asset - deficit cases 4,367,914 6,825,292Suspense account 98,077,809 98,077,809Others 262,365,152 262,365,152

1,174,704,781 2,126,768,008

22.2 Minority interest in the changes in the equity of the consolidated subsidiaries due to Other (deductions)/additions

For CY 2008, the increase of P66 million in minority interest in the changes in the equity of the consolidated subsidiaries consists of the following:

2008 2007

GSIS Family Bank (GFB) (230,558) 3,322,043

GSIS Mutual Fund, Inc. (GMFI) (65,934,973) 1,731,055,828

35

(66,165,531) 1,734,377,871

23. CONTINGENT LIABILITIES

At present, there are lawsuits and claims against the GSIS that are either awaiting decisions by the courts or are subject to settlement agreements. In the opinion of Management and its legal counsels, the contingent liability or loss arising there from, under the Social Insurance Fund amounts to at least P781.381 million. Reserve for Contingencies has been set for the same amount.

Additional Reserve for contingencies2008 2007

Cases involving the Housing and Real Property Development Group 725,366,465 833,433,464

Cases involving the Administration Group 53,107,825 88,607,825Cases involving the Field Operations Group 2,907,037 9,045,537

Cases involving the Social Insurance Group - 36,394

781,381,327 931,123,220

24. RELATED PARTY TRANSACTIONS

The GSIS, in its regular conduct of business, has transactions with its subsidiaries. GFB acts as conduit for its short-term placement with the BSP. While waiting for longer tenor instruments providing better yields, GSIS places its investible funds with BSP through GFB.

As at December 31, 2008, the total short-term placements of the GSIS through GFB amounted to P5.340 billion. These funds are invested overnight to BSP. Maturities of the overnight placements are credited back to GSIS investment account with the Union Bank of the Philippines (UBP) via Real-Time Gross Settlement (RTGS).

25. ADMINISTRATIVE LOADING

For CY 2008, the administrative loading of the Fund is 6.97 per cent which is well below the allowable limit of 12 per cent.

26. EXEMPTION FROM TAX

36

Pursuant to Section 39 of RA 8291, the GSIS, its assets, revenues including all accruals thereto, and benefits paid are exempted from all taxes, assessments, fees, charges or duties of all kind.

27. EVENTS AFTER THE BALANCE SHEET DATE

On March 30, 2009, the GSIS experienced the first crash of its database management system software or the IBM-DB2 software, in its unstable, corrupted state. The second incident occurred on April 2, 2009. The GSIS experienced eight system crashes in two months. About 90 per cent of the GSIS’ operations were adversely affected by the crash. Thousands of loans and claims of GSIS members could not be processed, membership records could not be updated, transactions could not be recorded, and a sizeable data in the GSIS database were either corrupted or lost temporarily. During system crashes, the G-W@PS kiosks were rendered off-line. The GSIS has suffered at least P5 billion in actual damages as a result of the system crashes.

On June 3, 2009, the GSIS filed a civil case against IBM Corporation, IBM Philippines and Questronix Corporation as it asked the court to order these companies to pay the GSIS the amount of P100 million in damages.

The GSIS has implemented various measures for data recovery and upgraded its back-up systems. The GSIS has assured all its members and pensioners that the integrity of all its data has not been compromised. For every step of a process, records are preserved and kept in perpetual storage. The GSIS is currently implementing migration to Oracle database system software.

37