Embed Size (px)

Citation preview

RevenuePaper.nt.gov.au

DEPARTMENT OFTREASURY AND FINANCE

Northern Territory RevenueDiscussion PaperNovember 2017

ii | Northern Territory Revenue Discussion Paper

November 2017 | 1

ǀǀContents

1 ObjectivesoftheNorthernTerritoryRevenueDiscussionPaper 2

2 Consultationprocess 4

3 StructureandlimitationsofNorthernTerritoryrevenuesources 5

4 KeyfiscalandeconomicchallengesfacingtheNorthernTerritory 9

5 NorthernTerritoryown-sourcerevenue 12

6 Payroll tax 18

7 Property taxes 23

8 Gamblingtaxes 31

9 Motorvehicletaxes 36

10 Insuranceduty 40

11 Bankingtaxes 42

12 Mineralroyalties 44

13 Petroleumroyalties 51

14 Otherown-sourcerevenuebases 55

15 Recentstatetaxationreforms 57

2 | Northern Territory Revenue Discussion Paper

1 ObjectivesoftheNorthernTerritoryRevenueDiscussion Paper

1.1 WhyareweconsultingthecommunityabouttheTerritory’smain own-sourcerevenues?TheNorthernTerritoryreceivesthemajorityofitsrevenuefromtheCommonwealthGovernment,moresothantheotherstatesandterritories,boththroughGSTdistributionandtiedgrants.

Nevertheless,theimportanceoftheTerritoryhavingarobust,efficient,stableown-sourcerevenuebasehasneverbeenmoreapparentthanthroughthe2017BudgetperiodwhensignificantchangesinGSTrevenue,whicharebeyondthecontroloftheTerritory,substantiallyimpactedonGovernment’sabilitytoplananddeliveressentialservices.

TheTerritoryGovernmentwillcontinuetolobbytheAustralianGovernmenttoensuretheTerritoryreceivesitsfairshareoftheGST,alongwithcontinuingthedebatearoundnationaltaxreform.

Inthemeantime,itisimportanttheTerritoryconsidersimprovingitsown-sourcerevenuebase.TaxesandroyaltiesraisedbytheTerritorydirectlyassisttoprovideessentialgovernmentservicessuchashospitalsandhealthcare,policeandemergencyservices,education,familysupportandvitalinfrastructure.Fundingrequirementsfortheseservices,especiallyhealthandeducation,willcontinuetogrow,placingincreasingfiscalpressureontheTerritory.

Consequently,TerritorytaxesandroyaltiesmustprovidethefundingrequiredtocontinuetoprovidethequalitygovernmentservicesTerritoriansexpectanddeserve.Wemustraiserevenueinasustainablemannerthatdoesnotundulyimpedeinvestmentandbusinessdecisions,reducesredtapeandcomplianceeffort,andprovidesgovernmentwithstabilityandcertaintytoplanandbudget.

AnexaminationofTerritorytaxesandroyaltiesisnotsimplyaboutloweringorraisingtaxesorroyalties,orintroducingnewtaxesorabolishingcurrenttaxes.Itisaboutdevelopingtaxandroyaltysystemsthatraiseenoughrevenuetofundservicesandinfrastructurewhilebeingfairandefficient.BalancingtheseobjectivesisimportantinassistingtheTerritorytogrowandprosper.

1.2 ObjectivesandfiscalstrategyTheTerritoryGovernment’sfiscalstrategyinrespectofitsrevenuerequirementsistomaintainacompetitivetaxenvironmentthatencouragesinvestment,createsjobsandattractsbusinesstotheTerritory,whileraisingsufficientrevenuetocontributetofundinggovernmentservicedelivery.

Accordingly,Territorytaxesandroyaltiesneedto:

• deliversufficientrevenuenowandintothefuturetoallowGovernmenttodeliverservicesandinfrastructuretoTerritorians

• beasefficientandfairaspossible,makingsureeveryonecontributestothedevelopmentoftheTerritory,havingregardtotheircapacitytodoso

• beassimpleaspossibletominimisecomplianceandadministrationcosts

• beasstableandpredictableaspossiblesoGovernmentcanplanandbudgetforthefuture

• supportjobcreationandnotactasabarriertoinvestmentintheTerritorybyremainingcompetitivewiththeotherjurisdictions.

November 2017 | 3

TheseprinciplesarethefundamentalareasonwhichGovernmentwishestoengagewiththecommunitytodiscusstheTerritory’staxesandroyalties.

1.3 NatureoftheDiscussionPaperThisDiscussionPaperwillallowTerritorianstohavetheirsayonthefuturedevelopmentoftheTerritory’staxandroyaltypolicies.ThepaperprovidesasummaryoftheTerritory’staxandroyaltysystems,settingoutpolicyobjectives,alongwitheconomicefficienciesandinefficienciesofthecurrent system.

Thepaperalsoprovidesarangeofreformoptionsthatcouldbeconsidered,inordertoassistinstimulatingcommunityinputtogovernmentpolicy.TheseoptionsarenotrecommendationsanddonotreflectanypolicyproposaloftheGovernment.

4 | Northern Territory Revenue Discussion Paper

2 Consultationprocess

TheGovernmentencouragesinterestedpartiestomakeawrittensubmissionregardingthisDiscussionPaper.ThesesubmissionswillassistGovernmenttoprepareitstaxationandroyaltypolicies,considertheneedandappropriatenessforreform,andfeedintothedevelopmentofrevenueoptionsaspartofitsBudgetprocesses.

Inadditiontoseekingwrittensubmissions,publicconsultationwithinterestgroups,peakbodiesandthebroadercommunitywillaccompanytheDiscussionPaper.Thedatesofpublicconsultationwillbereleasedshortly.

2.1 KeydatesNovember2017: DiscussionPaperreleasedforconsultation

NovembertoJanuary2017: Engagementwithindustryandpeakbodies,publicinformationsessions

28February2018: Closingdateforwrittensubmissions

Anychangestothesedates,alongwithupdatesontimingofconsultationprocesses,willbeadvised on RevenuePaper.nt.gov.au

2.2 SubmissionsSubmissions can be lodged via the following methods:

Email: [email protected]

Mail: DepartmentofTreasuryandFinance Revenue Discussion Paper GPOBox154 DARWINNT0801

Hand delivery: DepartmentofTreasuryandFinance Revenue Discussion Paper Level14,CharlesDarwinCentre 19TheMall DARWINNT0801

AllsubmissionswillbepubliclyavailableandpublishedtothewebsiteRevenuePaper.nt.gov.au,unlessyouspecificallyrequestotherwiseinyoursubmission.

November 2017 | 5

3 StructureandlimitationsofNorthernTerritoryrevenue sources

3.1 NorthernTerritorysourcesofrevenueTheTerritory’stotalrevenuecomprises30percentown-sourcerevenueand70percentCommonwealthrevenue.Bycontrast,thesplitforotherjurisdictionsisabout55percentown-sourcerevenueand45percentCommonwealthrevenue.

TheTerritory’sown-sourcerevenueprimarilycomprisestaxesandroyalties,butalsoincludesfeesandcharges,rentandtenancyincome,interestanddividendrevenue,andprofitandlossonthedisposalofassets.Own-sourcerevenueprovidesfiscalautonomytotailorinfrastructureandservicestomeetajurisdiction’sneeds.

CommonwealthrevenueprovidedtotheTerritorycomprises:

• goodsandservicestax(GST),whichaccountsforabouthalfoftotalTerritoryrevenue

• tiedpayments,whichaccountforabout20percentoftotalTerritoryrevenue.

ThedifferenceintheimportanceofCommonwealthrevenuetotheTerritoryisdemonstratedinChart3.1,whichshowsstateandterritoryrevenuesbysource.

Chart3.1:StateandTerritoryRevenuesbySource,2015-16

Source:Commonwealth2015-16FinalBudgetOutcome;stateandterritory2015-16annualfinancialreportsor2016-17mid-yearreports

• TheTerritoryreceivesmostofitsrevenuefromtheCommonwealth,moresothantheotherstatesandtheAustralianCapitalTerritory.

• LikeotherstatesandtheAustralianCapitalTerritory,theTerritoryhaslimitedpowerstoimposeonlyanarrowrangeoftaxesandroyalties.

• ChangestoGSTdistribution,whichprovideshalfoftheTerritory'srevenue,havealargeimpactontheTerritory'sBudget.

0

20

40

60

80

100%

NSW Vic QldWA SA TasACT NT TotalOwn-source revenue GST Tied Commonwealth payments

6 | Northern Territory Revenue Discussion Paper

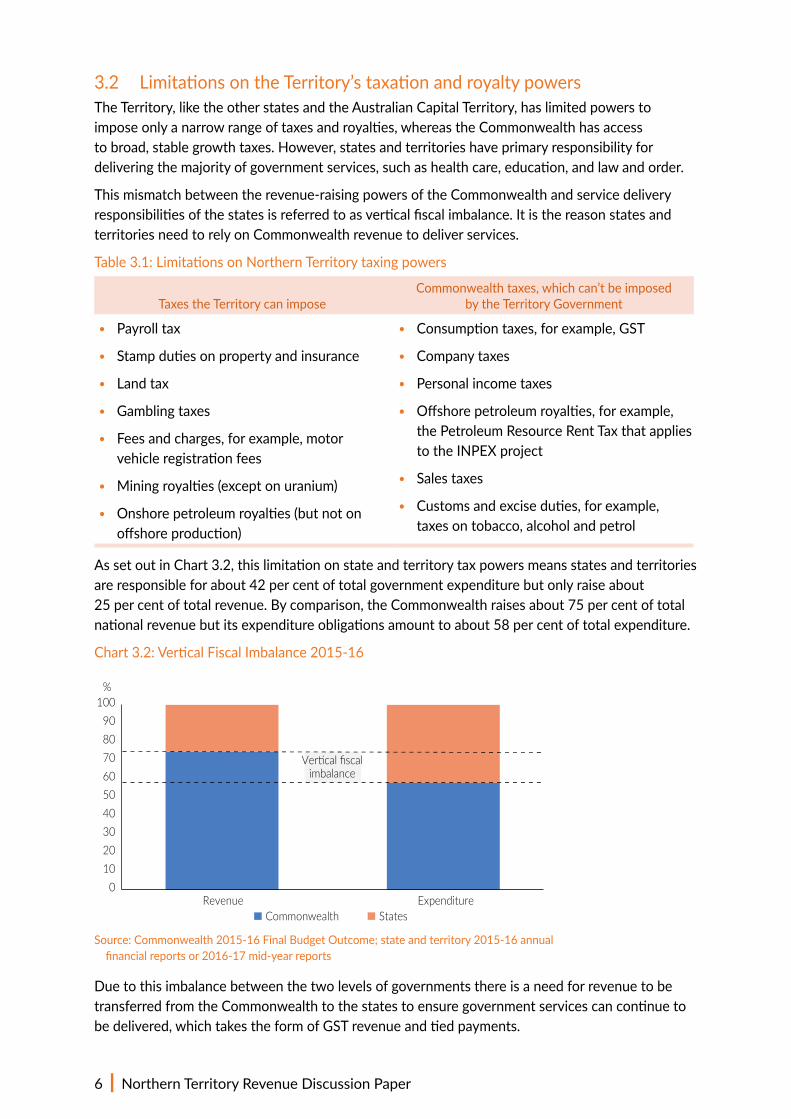

3.2 LimitationsontheTerritory’staxationandroyaltypowersTheTerritory,liketheotherstatesandtheAustralianCapitalTerritory,haslimitedpowerstoimposeonlyanarrowrangeoftaxesandroyalties,whereastheCommonwealthhasaccesstobroad,stablegrowthtaxes.However,statesandterritorieshaveprimaryresponsibilityfordeliveringthemajorityofgovernmentservices,suchashealthcare,education,andlawandorder.

Thismismatchbetweentherevenue-raisingpowersoftheCommonwealthandservicedeliveryresponsibilitiesofthestatesisreferredtoasverticalfiscalimbalance.ItisthereasonstatesandterritoriesneedtorelyonCommonwealthrevenuetodeliverservices.

Table3.1:LimitationsonNorthernTerritorytaxingpowers

Taxes the Territory can imposeCommonwealthtaxes,whichcan’tbeimposed

by the Territory Government

• Payroll tax

• Stampdutiesonpropertyandinsurance

• Land tax

• Gamblingtaxes

• Feesandcharges,forexample,motorvehicleregistrationfees

• Miningroyalties(exceptonuranium)

• Onshorepetroleumroyalties(butnotonoffshoreproduction)

• Consumptiontaxes,forexample,GST

• Company taxes

• Personal income taxes

• Offshorepetroleumroyalties,forexample,the Petroleum Resource Rent Tax that appliestotheINPEXproject

• Sales taxes

• Customsandexciseduties,forexample,taxesontobacco,alcoholandpetrol

AssetoutinChart3.2,thislimitationonstateandterritorytaxpowersmeansstatesandterritoriesareresponsibleforabout42percentoftotalgovernmentexpenditurebutonlyraiseabout25percentoftotalrevenue.Bycomparison,theCommonwealthraisesabout75percentoftotalnationalrevenuebutitsexpenditureobligationsamounttoabout58percentoftotalexpenditure.

Chart3.2:VerticalFiscalImbalance2015-16

Source:Commonwealth2015-16FinalBudgetOutcome;stateandterritory2015-16annualfinancialreportsor2016-17mid-yearreports

DuetothisimbalancebetweenthetwolevelsofgovernmentsthereisaneedforrevenuetobetransferredfromtheCommonwealthtothestatestoensuregovernmentservicescancontinuetobedelivered,whichtakestheformofGSTrevenueandtiedpayments.

0102030405060708090

100

Revenue ExpenditureCommonwealth States

Vertical fiscalimbalance

%

November 2017 | 7

3.3 ConstraintsonCommonwealthrevenuetotheTerritory3.3.1 Constraints to the GSTGSTisaconsumptiontaxand,becauseithasamuchbroaderbasethanmostothertaxes,isconsideredaneconomicallyefficienttax.However,theGSTcouldprovidegreaterrevenuetostatesand territories.

Australia’sGSTrateis10percent,oneofthelowestamongdevelopedcountries.TheGSThassignificantexemptionsforfreshfood,health-relatedservices,education,childcareandutilitiesservices,whichbenefitconsumersbutreduceGSTrevenueandaddcomplexityandcoststobusiness.

Only49percentofAustralia’snationalconsumptionissubjecttoGST,comparedtotheOECDaverageconsumptiontaxationratioof56percent,or55percentinGermany,71percentinSwitzerlandand97percentinNewZealand.

Furthermore,sincetheintroductionofGSTinJuly2000,therehasbeenanotableshiftinconsumerspendingpatternsfromitemsthatattractGSTtothosethatareGST-exempt,notablyeducationandhealth-relatedservices.

TheseexemptionsandchangedconsumerhabitshaveresultedinamoderationinthegrowthofGSTcollections.IntheinitialyearsofGSTtheaverageannualgrowthrateofcollectionswasaround8.2percent.Morerecently,averageannualgrowthhasbeenaround3.9percent.

RegardlessofwhetherchangestoGSTwouldbeunanimouslysupportedbystates,thecurrentCommonwealthGovernmenthasmadeitcleartherewillbenochangetoGST–baseorrate–duringthistermofGovernment.

TheTerritoryfacesriskstoitsshareofGSTcollectionsasaresultofthefactorstakenintoaccountincalculatingstates’shares.

BesidesthegrowthintheamountofnationalGSTcollections,theotherparametersthatinfluencetheamountofGSTreceivedbytheTerritoryareGSTrelativitiesassessedbytheCommonwealthGrantsCommissionandtheTerritory’sshareofthenationalpopulation.

ThechallengesfacingtheTerritoryregardingpopulationgrowthareaddressedinChapter4.CombinedwithadeclineintheTerritory’sshareofnationalpopulation,asignificantreductionintheTerritory’sGSTrelativityin2017hadthesignificanteffectofreducingtheTerritory’sexpectedGSTreceiptsby$2billionovertheforwardestimates,withGSTrevenuenotexpectedtoreturnto2016-17levelsuntil2020-21.ThisissetoutinChart3.3below.

Chart3.3:VariationstoGSTrevenuesinceAugust2016Pre-ElectionFiscalOutlook

Source:NorthernTerritory2017-18BudgetPaperNo.2BudgetStrategyandOutlook

2800

3000

3200

3400

3600

3800

4000

2017 2018 2019 2020 2021

2016 Pre-ElectionFiscal Outlook

2017-18 Budget

($M)

Year ended June

8 | Northern Territory Revenue Discussion Paper

3.3.2 Constraints to tied Commonwealth paymentsTiedCommonwealthpaymentsareprovidedtosupporttheachievementofoutcomesinaparticularsector,deliveryofspecifiedprojectsortofacilitatenationalreforms.Theyaregenerallysubjecttoachievingdefinedmilestonesorperformancebenchmarksandareoftentimelimited.Assuch,theycannotbereliedonasaguaranteedongoingsourceofrevenueforthestates.

Inaddition,tiedpaymentsareoftenprovidedtopursueCommonwealthGovernmentpriorities,whichmaynotalwaysalignwiththeTerritory’spriorities.

TherehasbeenincreasinguncertaintyaroundCommonwealthfundinginrecentyearswiththeCommonwealthpreferringnottocommittofundingformostNationalPartnershipAgreementsbeyondonetotwoyears;reducingorterminatingNationalPartnerships;andintroducinginputcontrolsandgreaterlevelsofprescriptionthatimpactstates’autonomytodeliverservicesforwhichtheyareresponsible.

WithoutsustainableCommonwealthpayments,bothtiedandgeneralrevenueassistance,theTerritorywouldneedtoapplyahighertaxburdenonitscitizensorraisesignificantlevelsofdebtinordertomaintainexistingservicedeliverylevels.Alternatively,itwouldneedtoreducethelevelofservice delivery.

3.4 NationaltaxreformStatesandtheCommonwealthcontinuetoinvestigatearangeofCommonwealthandstatetaxandrevenuereformoptions,includingproposalstoshareCommonwealthpersonalincometaxrevenuewiththestates.Itishopedthisworkwillidentifyanappropriatemeasurethatwill:

• providestateswithaccesstoabroadrevenuebasethatgrowsinlinewiththeeconomy

• reducethenumberoftiedCommonwealthgrantstothestates,providingthemwithgreaterautonomyandreducingadministrativeburden

• createflexibilityforstatestomeettheirongoingexpenditureneeds.

November 2017 | 9

4 KeyfiscalandeconomicchallengesfacingtheNorthern Territory

4.1 KeyfiscalpressuresHealth,education,publicorderandsafety,andhousingandcommunityamenitiescomprisetwothirdsoftheTerritoryBudgetandaresubjecttothegreatestfiscalpressuresarisingfromgrowthinbothdemandandthecostofprovidingthoseservices.

TheTerritoryhasasmallpopulationdispersedoveralargelandmassthatisisolatedfromAustralia’smainpopulationcentres.Aboriginalpeople,whocomprisearound30percentoftheTerritory’spopulation,tendtoliveinmoreremoteareasandusemainstreamservicesmoreintensivelycomparedtothenon-Aboriginalpopulation.

ThesefactorsaffectboththedemandforandcostofgovernmentservicesandresultintheTerritoryneedingtospendmorethandoublepercapitaongovernmentservicesthantheaverageoftheotherjurisdictions.ThisisdemonstratedinTable4.1

Table4.1:Generalgovernmentoperatingexpensespercapita,2015-16($)

NT ACT TAS WA SA QLD VIC NSW

24009 12536 10448 11140 9976 10251 8725 9328

Source:ABS,GovernmentFinanceStatistics,Australia2015-16,April2017.ABS,AustralianDemographicStatistics,December 2016

ChangestotheleveloftiedCommonwealthpaymentsandthedeclininggrowthinGSTcollectionsarebothcontributingtothefiscalpressuresexperiencedbystates.Asaresult,Commonwealthfundingisnotexpectedtogrowinlinewithdemandforservices,particularlyhealthcareandeducation,overthemediumtolongterm.

Sincethe2014-15CommonwealthBudgettherehasbeensignificantuncertaintyaroundtheCommonwealth’sfuturefundingforhealthandeducation,withaproposaltomoveawayfromactivityorneeds-basedfundingtoaflatindexationarrangement.Indexationislikelytoresultinashortfallforjurisdictionswithhigherdemandgrowth,includingtheTerritory.Accordingly,theTerritoryisfacedwithsignificantfundinguncertaintyinthelongterm.

• TheTerritorydeliversthesamescopeofservicesasthoseprovidedbyotherstatesbutfaceshigherdemandandservicedeliverycosts.

• DemandfortheseservicesisexpectedtooutpaceCommonwealthfundinggrowthoverthemediumtolongterm.

• TheTerritorycontinuestoneedtoinvestinclosingthegapinoutcomesbetweenAboriginalandnon-AboriginalTerritorians.

• TheTerritoryhasasmall,openeconomythatissignificantlyinfluencedbymajorprojectsandcyclicalsectorssuchasminingandconstruction.Thisresultsingreaterrevenuevolatilitythan other states.

• LowpopulationgrowthmaynegativelyaffecttheTerritory’sshareofGST.

10 | Northern Territory Revenue Discussion Paper

Inaddition,inits2017-18Budget,theCommonwealthannouncedtheQualitySchoolsfundingandreformpackage2018-2027.Underthispackage,theleveloffundingforTerritorygovernmentschoolswillbelessthanundertheexistingarrangements.

Thesefiscalpressuresareexpectedtobefurthercompoundedby:

• challengingeconomicconditions

• theTerritory’spossibleexpenditurecommitmentsundertheNationalDisabilityInsuranceScheme

• costsofanyreformsundertakeninresponsetofindingsoftheRoyalCommissionintotheProtectionandDetentionofChildrenintheNorthernTerritory.

4.2 PopulationanddemographicchangeFiscalpressureswillbeinfluencedbydemographicchangeintheTerritory,withthemainfactorsbeing:

• thecontinuedhighproportionofthepopulationthatisAboriginalorwholiveinremoteareas

• slowoverallpopulationgrowthintheshorttomediumterm

• anageingpopulation.

AsatJune2016therewereapproximately10.4peopleofworkingage(15to64)foreveryonepersonaged65andoverintheTerritory,comparedtoaratioof4.3nationally.However,theTerritorypopulationisprojectedtoageinthefuture.AnolderpopulationbasecanimpactontheTerritorybudgetthroughincreaseddemandforservices,especiallyhealthcare,andareductioninthesizeofthepotentialtaxbase.

ItisexpectedthattheTerritory’spopulationgrowthwillcontinuetobeslowintheshortterm.ThisincludestheeffectofaproportionofresidentconstructionworkersdepartingtheTerritorywhentheINPEXprojecttransitionsfromtheconstructiontooperationalphase.

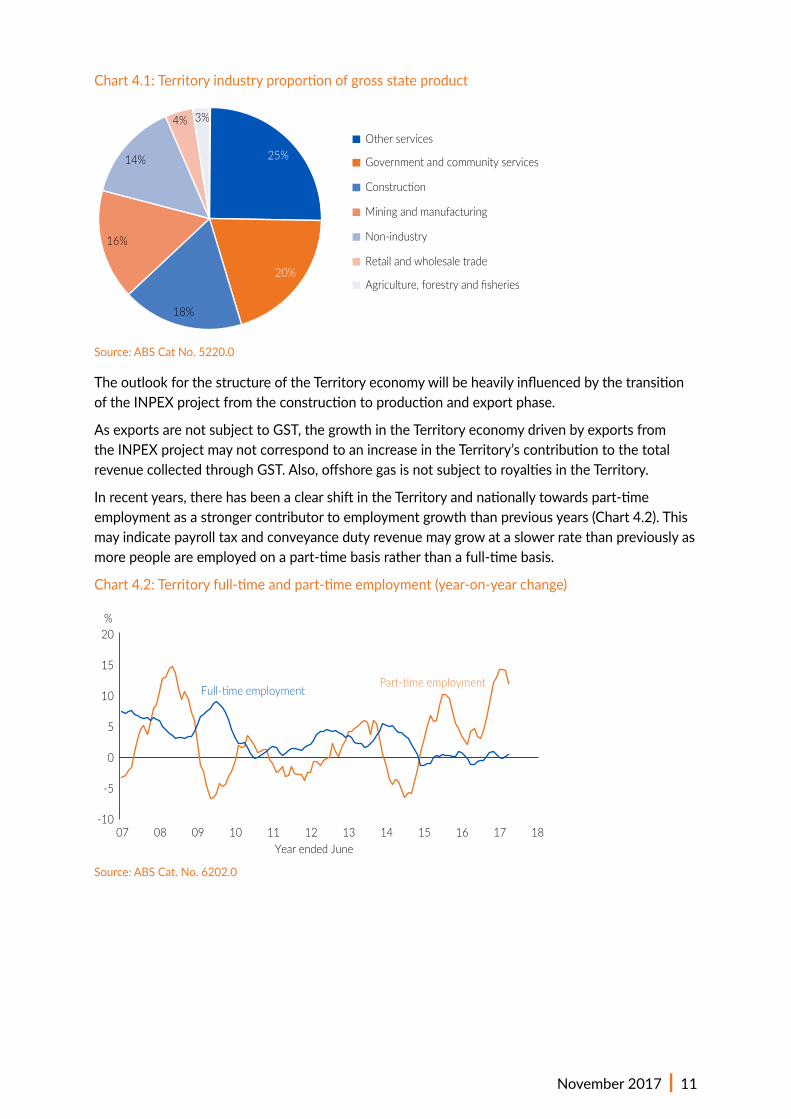

4.3 EconomyTheminingandconstructionsectorsaretwoofthelargestcontributorstoTerritorygrossstateproduct(GSP).Botharecyclicalindustries,whichleadstovariationsintheirlevelofcontributiontotheeconomy,whichcanexacerbatefiscalpressures.

TheminingandconstructionindustrieswerekeycontributorsofeconomicgrowthintheTerritoryduringtheminingboom.Futuregrowthprospectsfortheseindustriesisreliantonoverseasdemandandinvestment,andsubjecttomovementinglobalcommoditypricesandtheexchangerate.

November 2017 | 11

Chart4.1:Territoryindustryproportionofgrossstateproduct

Source:ABSCatNo.5220.0

TheoutlookforthestructureoftheTerritoryeconomywillbeheavilyinfluencedbythetransitionoftheINPEXprojectfromtheconstructiontoproductionandexportphase.

AsexportsarenotsubjecttoGST,thegrowthintheTerritoryeconomydrivenbyexportsfromtheINPEXprojectmaynotcorrespondtoanincreaseintheTerritory’scontributiontothetotalrevenuecollectedthroughGST.Also,offshoregasisnotsubjecttoroyaltiesintheTerritory.

Inrecentyears,therehasbeenaclearshiftintheTerritoryandnationallytowardspart-timeemploymentasastrongercontributortoemploymentgrowththanpreviousyears(Chart4.2).Thismayindicatepayrolltaxandconveyancedutyrevenuemaygrowataslowerratethanpreviouslyasmorepeopleareemployedonapart-timebasisratherthanafull-timebasis.

Chart4.2:Territoryfull-timeandpart-timeemployment(year-on-yearchange)

Source:ABSCat.No.6202.0

25%

20%

18%

16%

14%

4% 3%

Other services

Government and community services

Construction

Mining and manufacturing

Non-industry

Retail and wholesale trade

Agriculture, forestry and fisheries

-10

-5

0

5

10

15

20

07 08 09 10 11 12 13 14 15 16 17 18Year ended June

%

Part-time employmentFull-time employment

12 | Northern Territory Revenue Discussion Paper

5 NorthernTerritoryown-sourcerevenue

5.1 Componentsofown-sourcerevenueTerritoryown‑sourcerevenuepredominantlycomprisestaxesandminingrevenuebutalsoincludesfeesandcharges,rentandtenancyincome,interestanddividendrevenue,andprofitandlossonthedisposalofgovernmentassets.

TaxationandminingroyaltiesareanimportantrevenuesourcefortheTerritory.In2016-17,own-sourcetaxationandminingroyaltiescontributedover$768millionofTerritoryrevenue.TaxationandroyaltyreceiptsarethesecondlargestrevenuesourcefortheTerritorybehindGSTgrants.

Themaincontributorstoown-sourcerevenuearetaxesonemployers(payrolltax)at$313millionoralmost40per cent,miningandpetroleumroyaltiesat$165million,or21percent,andtaxesonproperty(conveyancestampduty)at$105million,or14percent.ThisissetoutinChart5.1below.

Chart5.1Mainown-sourcerevenuecategories,2016-17

Source:DepartmentofTreasuryandFinance

• TheTerritoryleviessimilartaxesandroyaltiesastheotherstatesandtheAustralianCapitalTerritory.

• Territorytaxesandroyaltiesaregenerallyvolatileanddifficulttoforecast.

• Inaggregate,Territoryown-sourcerevenuesareamongthelowestinAustralia.

$313M

$165M

$105M

$72M

$70M

$43M

Payroll tax

Mining and petroleum royalties

Conveyance stamp duty

Gambling taxes

Motor vehicle taxes

Insurance duty

November 2017 | 13

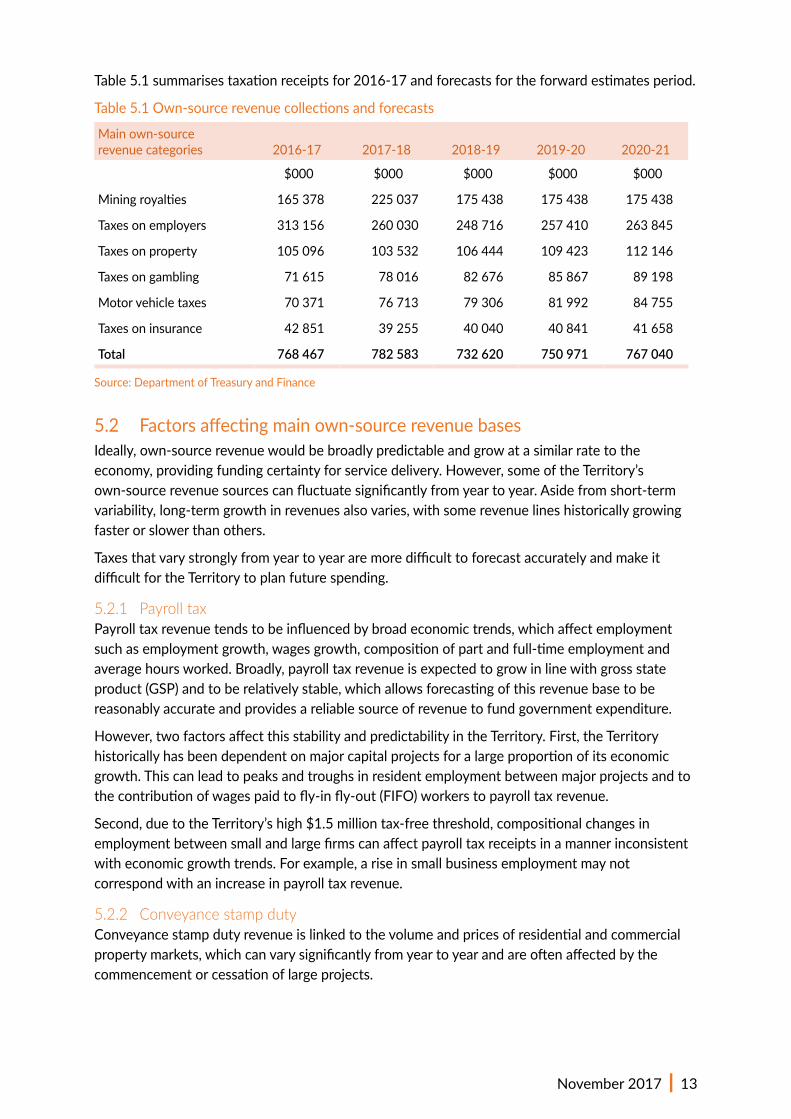

Table5.1summarisestaxationreceiptsfor2016-17andforecastsfortheforwardestimatesperiod.

Table5.1Own-sourcerevenuecollectionsandforecasts

Mainown-source revenuecategories 2016-17 2017-18 2018-19 2019-20 2020-21

$000 $000 $000 $000 $000

Miningroyalties 165378 225037 175438 175438 175438

Taxes on employers 313156 260 030 248716 257410 263845

Taxes on property 105096 103532 106444 109423 112146

Taxesongambling 71615 78 016 82 676 85867 89198

Motorvehicletaxes 70 371 76 713 79306 81992 84755

Taxes on insurance 42851 39255 40040 40841 41658

Total 768 467 782 583 732 620 750 971 767 040

Source:DepartmentofTreasuryandFinance

5.2 Factorsaffectingmainown-sourcerevenuebasesIdeally,own-sourcerevenuewouldbebroadlypredictableandgrowatasimilarratetotheeconomy,providingfundingcertaintyforservicedelivery.However,someoftheTerritory’sown-sourcerevenuesourcescanfluctuatesignificantlyfromyeartoyear.Asidefromshort-termvariability,long-termgrowthinrevenuesalsovaries,withsomerevenuelineshistoricallygrowingfasterorslowerthanothers.

TaxesthatvarystronglyfromyeartoyeararemoredifficulttoforecastaccuratelyandmakeitdifficultfortheTerritorytoplanfuturespending.

5.2.1 Payroll taxPayrolltaxrevenuetendstobeinfluencedbybroadeconomictrends,whichaffectemploymentsuchasemploymentgrowth,wagesgrowth,compositionofpartandfull-timeemploymentandaveragehoursworked.Broadly,payrolltaxrevenueisexpectedtogrowinlinewithgrossstateproduct(GSP)andtoberelativelystable,whichallowsforecastingofthisrevenuebasetobereasonablyaccurateandprovidesareliablesourceofrevenuetofundgovernmentexpenditure.

However,twofactorsaffectthisstabilityandpredictabilityintheTerritory.First,theTerritoryhistoricallyhasbeendependentonmajorcapitalprojectsforalargeproportionofitseconomicgrowth.Thiscanleadtopeaksandtroughsinresidentemploymentbetweenmajorprojectsandtothecontributionofwagespaidtofly-infly-out(FIFO)workerstopayrolltaxrevenue.

Second,duetotheTerritory’shigh$1.5milliontax-freethreshold,compositionalchangesinemploymentbetweensmallandlargefirmscanaffectpayrolltaxreceiptsinamannerinconsistentwitheconomicgrowthtrends.Forexample,ariseinsmallbusinessemploymentmaynotcorrespondwithanincreaseinpayrolltaxrevenue.

5.2.2 Conveyance stamp dutyConveyancestampdutyrevenueislinkedtothevolumeandpricesofresidentialandcommercialpropertymarkets,whichcanvarysignificantlyfromyeartoyearandareoftenaffectedbythecommencementorcessationoflargeprojects.

14 | Northern Territory Revenue Discussion Paper

Conveyancedutyreceiptsvaryyeartoyearduetolargeone-offreceiptsfromsignficantcommercialtransactions,suchasthesaleofminesorpastoralproperties.Forexample,in2014-15,afewlargecommercialtransactionssawconveyancestampdutyrevenueincreaseto$265millioncomparedto$142millioninthepreviousyearand$114millioninthesubsequentyear.

5.2.3 Mining and petroleum royalties MiningroyaltiesintheTerritoryaregenerallypayableunderaprofit-basedschemesetoutintheMineral Royalty Act.Onshorepetroleumroyaltyispayablebasedonthevalueofthepetroleumatthepointofextraction.

WithonlyasmallnumberofminersintheTerritory,materialchangestotheprofitabilityofasingleminercanhaveasignificanteffectonminingroyaltyreceipts.Accordingly,forecastingroyaltyreceiptsisreliantonadvicefromminingcompaniesandpetroleumproducersofestimatedliabilityandcommoditypricemovements,productionlevelsandthevalueoftheAustraliandollar.

5.3 Own-sourcerevenuestabilityInaggregate,theTerritory’sown-sourcerevenuescanbechallengingtoforecastaccurately,largelyasaresultofthevariabilityofconveyancedutyandroyalties,whichmakesitdifficultfortheGovernmenttobudgetandplanforthefuture.Althoughpayrolltaxisacomparativelystablesourceofrevenue,evensmallpercentagechangescanhaveasignificantimpactontotalrevenues,aspayrolltaxisthelargestcontributortoown-sourcerevenue.

Chart5.2:VariationsingrowthofTerritoryown-sourcerevenuecomponentsovertime

Source:DepartmentofTreasuryandFinance

5.4 Interstate comparisonsInterstatecomparisonsoftaxarrangements,includingthoseundertakenbytheCommonwealthGrantsCommission(CGC),PitcherPartnersandtheInstituteofPublicAffairs(IPA),haveoftenshownthattheTerritoryisthelowestorsecondlowesttaxingjurisdiction.

ThisisparticularlytrueforrecurrentbusinesstaxesbecausetheTerritoryistheonlyjurisdictionthatdoesnotimposealandtax.Althoughthismaybeanattractivearrangementformanybusinesses,itisunlikelytoencouragebusinessestomovetheirheadofficestotheTerritory.

-50-40-30-20-10

010203040%

Total taxation

Chan

ge fr

om p

revi

ous y

ear

Payroll tax Conveyance dutyYear ended June

Royalties

135%83%

08 09 10 11 12 13 14 15 16 17 08 09 10 11 12 13 14 15 16 17 08 09 10 11 12 13 14 15 16 17 08 09 10 11 12 13 14 15 16 17

November 2017 | 15

5.4.1 Taxation as a percentage of gross state productTaxationasapercentageofGSPisonewaytomeasurethegrossamountoftaxrevenuecollectedbyajurisdictioncomparedtothesizeofthatjurisdiction’seconomy.Basedon2015-16data(thelatestavailable),theTerritoryhadthelowesttaxtoGSPratioinAustralia.ThisissetoutinTable5.2.

Table5.2:TaxationasapercentageofGSP

JurisdictionTaxationasapercentage ofGSP(2015-16) Rank

NewSouthWales 5.5% 8

Victoria 5.3% 7

SouthAustralia 4.4% 6

AustralianCapitalTerritory 4.3% 5

Tasmania 4.1% 4

Queensland 4.0% 3

WesternAustralia 3.8% 2

Northern Territory 2.6% 1

Source:ABS,DepartmentofTreasuryandFinance

TherearesomelimitationswhencomparingtaxationasapercentageofGSP.IntheTerritory,somesectors(inparticular,theprocessingandexportofnaturalgasfromoffshorefields)contributeheavilytoGSPbutarenotdirectlysubjecttoTerritorytaxation(inthecaseofoffshoregas,thisistaxedbytheCommonwealth).ThispartlyexplainstheTerritory’slowtaxationtoGSPratio.

5.4.2 Taxation per capitaTaxationpercapitaisameasurethatcomparestaxationreceiptswithajurisdiction’spopulation.Itprovidesausefulindicationoftheoverallleveloftaxation.However,itdoesnottakeintoaccountthedistributionofwhopaystax.Onthismeasure,assetoutinTable 5.3,theTerritoryhadthesecondlowesttaxpercapitaratioin2015-16(thelatestavailabledata).

Table5.3:Taxationpercapita(2015-16)

Jurisdiction $ per capita Rank

AustralianCapitalTerritory 3919 8

NewSouthWales 3 880 7

WesternAustralia 3526 6

Victoria 3 280 5

Queensland 2605 4

SouthAustralia 2592 3

Northern Territory 2478 2

Tasmania 2 068 1

Allstates 3290

Source:ABS,DepartmentofTreasuryandFinance

16 | Northern Territory Revenue Discussion Paper

5.4.3 Commonwealth Grants Commission tax effort ratiosTheCGCassesseseachstate’srevenue-raisingeffortonanannualbasis.RevenueeffortistheratiooftheactualamountofrevenueastateraisestotheamountoftaxrevenuetheCGCassessescouldberaisedifthestateappliednationalaveragetaxratestoitstaxbase.

Underthisassessment,theTerritoryhasthelowesttotaltaxationeffort.Table5.4reflectsthisassessment.

Table5.4:CommonwealthGrantCommissionassessmentsofrevenueeffort(2017UpdateReport)

NSW Vic Qld WA SA Tas ACT NT NT Rank

Miningrevenue 100.8 47.7 105.6 99.0 81.0 56.2 n/a 129.2 7

Payroll tax 101.8 100.9 91.1 106.0 87.1 106.3 132.2 106.9 7

Stamp duty 100.0 104.9 86.7 113.1 105.8 88.7 88.9 105.0 6

Insurance tax 110.5 95.9 77.8 115.7 116.6 113.2 29.0 77.6 2

Motortaxes 121.2 81.3 104.4 100.2 80.5 72.9 111.0 65.5 1

Land tax 80.2 114.1 96.5 116.9 138.9 115.7 182.5 0.0 1

Total tax revenue 105.1 101.2 87.7 102.2 102.6 90.2 101.7 85.4 1

Total revenue 97.5 95.3 105.8 103.0 99.8 83.2 152.0 95.2 2

Source:CGC2017Update

5.4.4 Business tax costs modelsComparisonsofstateandterritorytaxesareundertakenbyarangeoffirms,peakbodiesandpolicyinstitutes.AcomparisonofstatetaxesbasedonthemethodologyoftworeasonablyrecentstatetaxmodelsindicatesthattheTerritorygenerallyhasthelowestbusinesstaxcosts.

Pitcher PartnersThePitcherPartners'StateTaxReview2014-15comparedtaxespayableandothercostsbysmalltomedium-sizedcompaniesineachstate.TheNorthernTerritory,AustralianCapitalTerritoryandTasmaniawerenotincludedintheoriginalanalysis.However,usingPitcherPartners'methodologyandupdatingitwith2017-18data,theanalysis(setoutinTable5.5)showsthattheTerritoryisgenerallyalowtaxingjurisdiction.

Table5.5:BusinesstaxationcostsusingPitcherPartners'StateTaxReviewmethodology(2017-18)

Scenario1:Businesswithpayrollsize$1225564 Scenario2:Businesswithpayrollsize$6010000Aggregatetaxesandcharges(purchaseof

property)Aggregatetaxesandcharges(renting)

Aggregatetaxesandcharges(purchaseof

property)Aggregatetaxesandcharges(renting)

State Total($) Rank Total($) Rank Total($) Rank Total($) Rank

NSW 175061 6 43076 4 1148548 6 370 810 3

VIC 142920 4 44717 5 884593 3 337 620 1

QLD 113 618 3 22 162 1 915890 4 357595 2

SA 75155 1 54864 6 569740 1 384990 4

WA 150678 5 41471 3 1045541 5 409203 5

NT 80 306 2 23 286 2 773572 2 424253 6

Source:DepartmentofTreasuryandFinance

November 2017 | 17

Inallscenariosbutone,theTerritoryisthesecondlowestbusinesstaxingjurisdiction(withtheexceptionoflargerbusinessesthatchoosetorentratherthanpurchasetheirpremises).ThislargelyreflectsthattheTerritorydoesnotimposealandtax.

Forasmallbusiness(scenario1),Territorytaxislowerbecauseabusinesswithapayrolloflessthan$1.5millionintheTerritorywouldbeexemptfrompayingpayrolltax.ThisisduetotheTerritory'srelativelyhighpayrolltaxtax-freethresholdcomparedtomostotherstates.

Foralargerbusiness(scenario2),theTerritoryrankedsecondforbusinessespurchasingtheirpremiseslargelyduetothefactlandtaxisnotimposed.ThisisoffsetbytherelativelyhighpayrolltaxpayablebyabusinessofthissizeintheTerritory.

Institute of Public Affairs (IPA)TheIPABusinessBearingtheBurden2012reportcomparedthetaxationcostsassociatedwithrunningarangeofbusinesssizesineachstate.ArangeofbusinesssizesareusedbasedontheparametersoftheWorldBank’sstandardcasestudycompany.

Table5.6:BusinesstaxationcostsusingIPABusinessBearingtheBurden2012methodology(2017-18)

Business size1

10% 50% 100% 200%Taxpaid($) Ranking Taxpaid($) Ranking Taxpaid($) Ranking Taxpaid($) Ranking

NSW 4201 7 117501 8 284561 8 622 222 7

Vic 2 027 3 97292 3 231 311 2 518545 1

Qld 3 032 6 98047 4 264048 4 546381 3

WA 1407 2 104591 6 272468 5 607651 5

SA 2572 4 109396 7 276993 6 615183 6

Tas 4988 8 100274 5 280 210 7 640083 8

ACT 2691 5 39638 1 216698 1 571226 4

NT 1 171 1 65568 2 234261 3 544500 2

Average 2 761 91538 257569 583224

1 Compared to World Bank case study company.Source:DepartmentofTreasuryandFinance

UsingtheIPAmethodologyfor2017-18,theTerritoryhasabelowaveragetaxpayableforeachbusiness.ThisisconsistentwiththeresultsusingthePitcherPartners'methodology,discussedabove.

18 | Northern Territory Revenue Discussion Paper

6 Payroll tax

6.1 PayrolltaxoverviewPayrolltaxisthemostsignificantsourceofTerritoryown-sourcetaxrevenue.In2016-17,Territorypayrolltaxrevenuewasabout$313million,orabout40 percentofown-sourcetaxandroyaltyrevenue.AsdiscussedinChapter5,itisalsooneofthemoreefficientandstabletaxes,althoughitcanbeheavilyinfluencedbymajorprojects.

PayrolltaxispayableintheTerritorywhenthetotalannualAustralianwagesofanemployerexceedstheTerritory’s$1.5milliontax-freethresholdamount.Thethresholdreducesproportionatelyifanemployerpayswagesinanotherstateorterritory.

Thethresholdamountisadeductionfromtaxablewages,whichoperatessobusinesseswithtotalAustralianwagesofupto$1.5millioninafinancialyeardonotpayanypayrolltax.

Thedeductionreducesby$1forevery$4inwagespaidbyanemployerabovethe$1.5millionthreshold.Thismeansanemployerwhopayswagesof$7.5millionormoredoesnotreceiveadeductionandpaystaxbasedontheirtotaltaxablewages.

Afterapplyingthededuction,payrolltaxiscalculatedattherateof5.5percentontaxablewagespaidbyanemployerforservicesrenderedbyemployeesintheTerritory.Payrolltaxisgenerallypaidmonthlyandcalculatedbasedonwagespaidinthepreviousmonth.

Payrolltaxappliestomostemployeeremunerationincludingwagesandsalaries,commissions,bonuses,allowances,employer-fundedsuperannuationbenefits,terminationpayments,mostleavepaymentsandthegrossed-upvalueoffringebenefits.

In2009,theTerritoryintroducedpayrolltaxlegislationharmonisedwiththatofmostotherstatesandtheAustralianCapitalTerritory.Asaresult,payrolltaxlegislationinterstatehasthesamerules.ThiswasdonetosimplifyadministrationandcomplianceandsignificantlyreduceredtapeforbusinessesoperatingintheTerritoryandotherjurisdictions.However,taxratesandthresholdsstilldifferbetweenjurisdictions.

• PayrolltaxisthelargestsourceofTerritoryown-sourcerevenue.

• PayrolltaxisthemoststableandpredictableTerritorytax,althoughitcanvarywiththecommencementandendoflargeprojects.

• Payrolltaxhaseconomicimpactssimilartoconsumptiontaxes,isanefficienttax,andhasrulesthatarelargelyharmonisedwiththeotherstates.

• Territorypayrolltaxhasahightax-freethresholdthatensuresmostlocalbusinessesdonotpaypayrolltax,coupledwitharelativelyhightaxrate.

• Reformstopayrolltaxmayfocusonrateandthresholdchanges,andshouldbalancetheinterestsofTerritorybusinesseswiththeimportanceofpayrolltaxasarevenuesource.

November 2017 | 19

6.2 WhopayspayrolltaxintheNorthernTerritory?ThepayrolltaxpolicysettingintheTerritoryisahightax-freethresholdthatmeansthemajorityofsmalllocalTerritorybusinessesdonothavetoregisterfororpaypayrolltax.Italsosignificantlyreducesthetaxpayablebyslightlylargerlocalbusinesses.

Payrolltaxisimposedonemployers.Althoughpayrolltaxisoftenregardedasa‘taxonjobs’andadisincentivetoemploy,studiesindicatethatpayrolltaxeshavesimilareconomicconsequencestoconsumptiontaxessuchastheGST,andgenerallydonotresultinlowerprofitsforbusinesses.

PayrolltaxisgenerallyseenasanefficientsourceofTerritoryrevenue,withrevenuegrowthwhenwagesandemploymentgrow.

6.2.1 Tax-free thresholdTheTerritory’shightax-freethresholdmeansthetaxbaseissmallerandahighertaxrateisrequiredtoachievethedesiredrevenueoutcome.Largerbusinesseswillhaveapayrolltaxliabilitywhileothers,includingsmallermarketcompetitors,willnot.Someemployerswithtaxablewagesclosetothe$1.5millionthresholdmayalsoperceivepayrolltaxasadisincentivetoengagingadditionalemployees.However,payrolltaxisonlypayableonthetaxablewagesthatexceedthetax-freethreshold.

ItisalsoimportanttorecognisethatTerritorytaxesareonlyareasonablysmallproportionofoverallbusinesscosts.Businessesconsiderallcostsarisingfromstartingorexpandingabusinessanddonotbasetheirlocationdecisionssolelyontaxconsiderations.

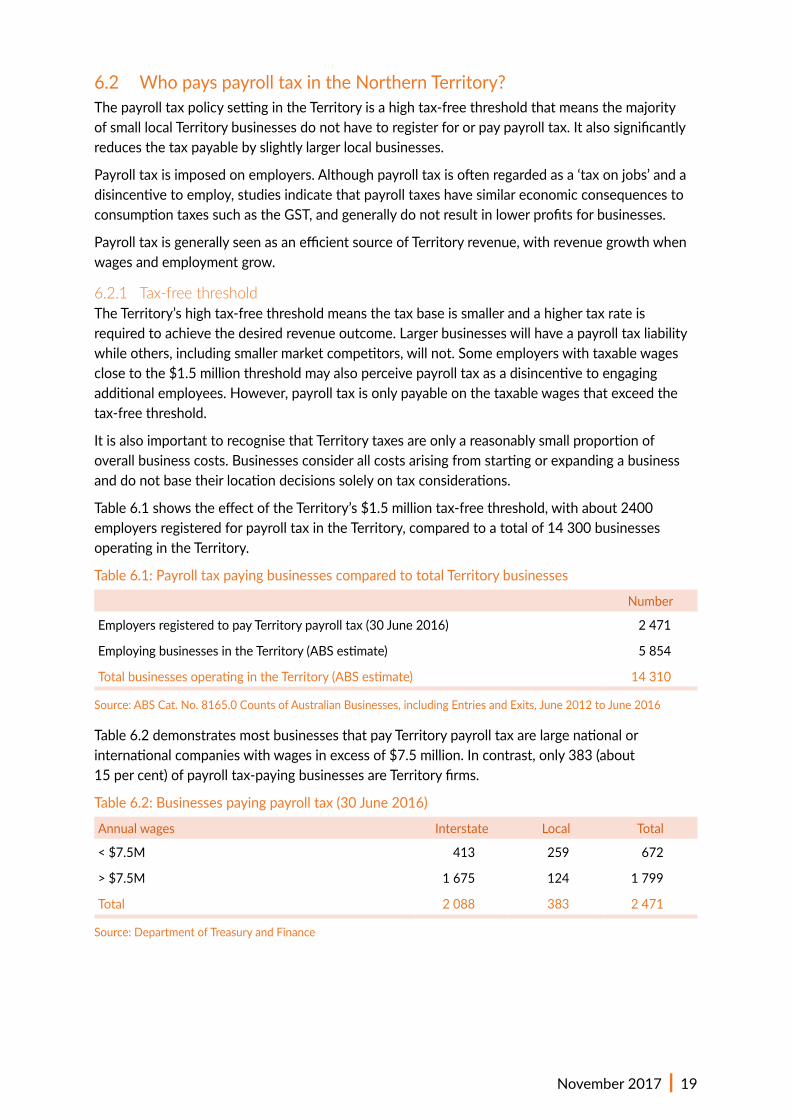

Table6.1showstheeffectoftheTerritory’s$1.5milliontax-freethreshold,withabout2400employersregisteredforpayrolltaxintheTerritory,comparedtoatotalof14300businessesoperatingintheTerritory.

Table6.1:PayrolltaxpayingbusinessescomparedtototalTerritorybusinesses

Number

EmployersregisteredtopayTerritorypayrolltax(30June2016) 2471

EmployingbusinessesintheTerritory(ABSestimate) 5854

TotalbusinessesoperatingintheTerritory(ABSestimate) 14 310

Source:ABSCat.No.8165.0CountsofAustralianBusinesses,includingEntriesandExits,June2012toJune2016

Table6.2demonstratesmostbusinessesthatpayTerritorypayrolltaxarelargenationalorinternationalcompanieswithwagesinexcessof$7.5million.Incontrast,only383(about15percent)ofpayrolltax-payingbusinessesareTerritoryfirms.

Table6.2:Businessespayingpayrolltax(30June2016)

Annualwages Interstate Local Total

<$7.5M 413 259 672

>$7.5M 1675 124 1799

Total 2 088 383 2471

Source:DepartmentofTreasuryandFinance

20 | Northern Territory Revenue Discussion Paper

6.2.2 ExemptionsWagespaidbymostnon-profitorganisationsrunforacharitablepurpose,religiousorpublicbenevolentinstitutions,someschoolsandeducationproviders,andhealthserviceprovidersareexemptfrompayrolltax.Exemptionsarealsoprovidedtobusinessesinrespectofwagespaidtoemployeesonmaternity,paternityandadoptionleaveorwhenvolunteeringasfirefightersandemergencyservicevolunteers.AsmostTerritorybusinessesarenotsubjecttopayrolltax,payrolltaxexemptionsprimarilybenefitlargeinterstateemployers.

6.3 Interstate comparisonTables6.3and6.4setoutacomparisonofthetaxratesandtax-freethresholdsofstatesandterritories,withTable6.4providingtheeffectivepayrolltaxrateatvariouswagelevelsforeachjurisdictionafterconsideringindividualstatethresholdsandtaxrates.

AsaresultoftheNorthernTerritory’shighthresholdandaveragepayrolltaxrate,theTerritoryimposeslowerthanaveragepayrolltaxesuptoabout$3millioninwages.However,forbusinesseswithabout$4millionormoreinwages,theTerritory’spayrolltaxschemehasaneffectivetaxrateabovethenationalaverage.

Table6.3:Stateandterritorypayrolltaxratesandannualthresholds

NSW Vic1 Qld2 WA3 SA4 Tas ACT NT3 Average

Threshold($M) 0.75 0.63 1.10 0.85 0.60 1.25 2.00 1.50 1.08

Rate(%) 5.45 4.85 4.75 5.50 4.95 6.10 6.85 5.50 5.49

1Arateof3.65 per centappliesforregionalVictorianemployers.2 Thresholdreducesaswagesincrease,sonoexemptionisprovidedforemployerswithwagesover$5.5million.3 Thresholdreducesaswagesincrease,sonoexemptionisprovidedforemployerswithwagesover$7.5million.4 Lowerrateof2.50 per centappliesforwagesfrom$0.6Mto$1Mandtherategraduallyincreasesto4.95 per centforwagesbetween$1Mand$1.5M.

Source:Statelegislationandinformationavailableat31October2017

Table6.4:Effectivestateandterritorypayrolltaxratesatvariouswagelevels

Wages$M

NSW%

Vic%

Qld%

WA%

SA1

%Tas%

ACT%

NT%

Average%

1 1.36 1.82 0.00 0.93 1.98 0.00 0.00 0.00 0.76

2 3.41 3.33 2.67 3.57 3.47 2.29 0.00 1.72 2.56

3 4.09 3.84 3.76 4.45 3.96 3.56 2.28 3.44 3.67

4 4.43 4.09 4.30 4.88 4.21 4.19 3.43 4.30 4.23

5 4.63 4.24 4.63 5.15 4.36 4.58 4.11 4.81 4.56

10 5.04 4.55 4.75 5.50 4.65 5.34 5.48 5.50 5.10

20 5.25 4.70 4.75 5.50 4.80 5.72 6.17 5.50 5.30

1Notincludingthesmallbusinesspayrolltaxrebateprovidedtoeligibleemployerswithpayrollsupto$1.2million.Source:Statelegislationandinformationavailableat31October2017

November 2017 | 21

6.4 EmploymentincentivesSomestatesprovide,orhavepreviouslyprovided,short-termemploymentincentiveschemesthrough,orlinkedto,theirpayrolltaxschemes.AcurrentexampleistheNSWJobsActionPlan,whichprovidesapayrolltaxrebateforbusinesseswith50orlessfull-timeequivalent(FTE)employeesforeachpersonemployedinanewjobforaminimumoftwoyears.Othersimilarprogramshavevariouslytargetedincreasingemploymentbasedon:

• employersize,thatis,generallysmallerormediumbusinesses

• employerlocation,suchasregionalorremoteemployers,oremployersinareaswithhighlocalunemployment

• targetedemployees,suchaslong-termunemployed,retrenchedpersons,apprentices,youngpersons,residents(ratherthanFIFOemployees)andAboriginalemployees.

Asidefromtherangeoftheseschemes,thetaxsystemisgenerallynotconsideredthemosteffectivemechanismtoachieveemploymentobjectivesasitcannotaccuratelytargetgovernmentassistancetoparticulargroupsoractivitieswithoutaddingsignificantredtaperequirements.

Also,onlyasmallproportionofemployerspaypayrolltax,especiallyintheTerritorywherethemajorityoflocally-establishedbusinessesarenotsubjecttopayrolltax.Therefore,taxincentivesprovidenobenefittothesesmalleremployers.

Taxconcessionsmaydistorttheintendedoutcomeifanemployerhiresbasedonlocalityratherthanbusinessefficiencyordismissesalong-servingemployeetoreceiveorretainaconcessionprovidedforaneweremployee.

6.5 PotentialreformoptionsGiventhedesirabilityofmaintainingharmonisedpayrolltaxlegislationacrossthestates,thekeyreformoptionsavailableareeitheralterationstothepayrolltaxrateof5.5percentorthe$1.5milliontax-freethreshold.

TheGovernmentisinterestedindiscussingwhatisrequiredtoensuretheTerritorypayrolltaxschemeiseffectiveandsupportiveofTerritorybusinesses,balancedwithitbeingaveryimportantrevenuesource.Thisincludessubmissionsinrespectoftheappropriatenessofthecurrentpolicysettingofahightax-freethresholdtoreducetheimpactofpayrolltaxonlocalbusinesses,balancedwitharelativelyhigherpayrolltaxrate.

Adjusting the payroll tax rateIntermsoffiscalimpact,each0.1percentchangeinthepayrolltaxratewouldleadtoa$5to6 million per annum changeintotalrevenue.

Adjusting the tax-free threshold Areformoptionmayincludeloweringthetax-freethresholdsoanumberofsmallerbusinessescommencepayingpayrolltax.Itisestimatedthatloweringthetax-freethresholdto$1millionwouldraiseabout$11million,whileloweringthethresholdto$600000(equaltoSouthAustralia’sthreshold,thelowestinAustralia)wouldraiseadditionalrevenueofabout$24 million.Thesewouldleadtoabout150to450additionalemployers,respectively,payingpayrolltaxcomparedtothecurrent2500registeredemployers.

22 | Northern Territory Revenue Discussion Paper

Incomparison,increasingthetax-freethresholdwouldreducethenumberofemployersthatpaypayrolltaxatthecostofareductioninpayrolltaxrevenue.However,theindividualsavingsforeachbusinesswouldbemoderate.Thecostofincreasingthethresholdto$1.75millionwouldbeabout$4millionperannumandthecostofraisingthethresholdto$2millionwouldbeabout$7millionperannum.Thesethresholdincreaseswouldonlyremove50to100employersfromthetax base.

Introduce new employee incentivesPayrolltaxconcessionsorrebatescouldbeprovidedforemployersthatemployworkersinnewjobsforaminimumperiodoftime(forexample,atleasttwoyears)ortargetedatparticularcategoriesofemployeroremployee.Forexample,payrolltaxincentivescouldbedesignedtoencourageemploymentoflocalworkersratherthaninterstateorFIFOarrangementsinordertobenefittheTerritoryandregionaleconomies,althoughitmayincuradditionaltaxforbusinesses.

However,ingeneral,theremaybelimitationstotheeffectivenessandefficiencyofpayrolltaxemployeeincentiveschemes.Anysuchincentiveneedstocarefullyconsiderwhetherthetaxsystemisthemostappropriatemethodfordeliveringassistance.

Reduce exemptionsPayrolltaxexemptionsforcertainorganisationsortypesofemployeesresultinrevenueforgoneofabout $30 million.

Removingexemptionsmightincreasethesimplicity,efficiencyandequityofthepayrolltaxsystem,aswellasprovidingasignificantadditionalsourceofrevenuefortheTerritory.However,asthebulkoftheseexemptionsareprovidedtocharitableorganisations,removingtheexemptionsmaybeinconsistentwithgovernmentandcommunityobjectives.

Ontheotherhand,thereisacasetobemadethattheprovisionofassistanceisalwaysmoreefficientlyprovidedthroughagrantandpaymentframework,ratherthantaxconcessions.First,thisrecognisesthattaxconcessionsprovidenoassistancetosmallerorganisationsbelowthetax-freethresholdorthosemainlyrelyingonvolunteers.Italsoallowsagovernmenttobettertargetparticulartypesofcharitiesorensuretheefficientallocationofresources.

Discussion questionsQ6.1 Arethecurrentbroadpolicysettingsforpayrolltax,focussedonahightax-free

thresholdtominimisetheliabilityofsmallerlocalbusinesses,appropriate?

Q6.2 Shouldadjustmentsbemadetothepayrolltaxrateorthreshold?Whatrevenueneutraloptionscouldbepursued,suchasloweringthethresholdinordertolowerthepayrolltaxrate?

Q6.3 DoesthecurrentpayrolltaxsystemencouragebusinessestoemploylocalworkersratherthanFIFOworkers?Shouldit?Ifso,how?

Q6.4 Whatotherimprovementstothepayrolltaxsystemcouldbeconsidered?

Q6.5 IfadjustmentstothepayrolltaxsystemwouldreducetherevenuereceivedbyGovernment,whatmeasuresshouldbetakentocompensate?

November 2017 | 23

7 Property taxes

7.1 ConveyancedutyoverviewIn2016-17,theTerritorycollected$105millioninconveyanceduty,orabout14percentofown-sourcetaxandroyaltyrevenue.

ConveyancedutyisderivedfromdirectandindirecttransfersofdutiablepropertyintheTerritory.Dutiablepropertyisrealestate(land,buildingsandotherfixtures),miningtenementsincludingexplorationrights,andbusinessassetsincludingplantandequipment,intellectualproperty,statutorylicencesandgoodwill.

DutyintheTerritoryiscalculatedbyaprogressiverateonthewholevalueoftheproperty.Forpropertywithadutiablevalueof:

• lessthan$525000,therateisdeterminedbyaformulathatrangesfromaminimumof1.5to4.95percent

• between$525000andlessthan$3million,therateis4.95percent

• between$3millionand$5million,therateis5.75percent

• $5millionormore,therateis5.95percent.

Arangeofexemptionsfromconveyancedutyalsoapplyandconcessionsareavailableforfirsthomebuyers,seniorsandNorthernTerritoryPensionerandCarerConcessioncardholdersandfornewlybuiltprincipalplacesofresidence.

7.2 ConveyancedutycollectionsConveyancedutycollectionsareaffectedbybothpropertyvaluesandtransactionvolumes,whichcanvaryfromyeartoyearandresultinvolatility.Forexample,significantdutycanresultfromasmallnumberofverylargecommercialtransactionsinasingleyear.

• ConveyancestampdutytaxisanimportantTerritoryown-sourcerevenue.

• Stampdutyisdifficulttoforecastaccuratelyasitisaffectedbypropertypricesandsalevolumes,aswellaslargecommercialtransactionsinanotherwisesmallmarket.

• Annualpropertytaxesaregenerallyregardedasastableandeffectivetaxbase.However,annuallandtaxesinotherstatesarenotasefficientastheycouldbe.

24 | Northern Territory Revenue Discussion Paper

Chart7.1:Territorydutycollectionsandtransactionvolumesatselectedvalueranges(2016-17)

Note:Excludesduty-exempttransactions.Source:DepartmentofTreasuryandFinance

AsdetailedinChart7.1,althoughtherearemanytransactionsforpropertiesvaluedbelow$400000,relativelylittlestampdutyiscollectedduetothecombinationoflowerpropertyvaluesandlowerdutyrates.Atvaluesof$400000to$600000,substantialdutyiscollectedbothduetohighervaluesandvolumes,asthisvaluerangecorrespondstotheDarwinmedianhouseprice.Incontrast,therearefarfewertransactionswithavalueof$1millionormorebutsignificantdutyiscollectedduetohighervaluesanddutyrates.

7.3 ConveyancedutydesignissuesAsatransaction-basedtax,conveyancedutyhasbeencriticisedbecauseitaddstothecostoftransfersandcanpotentiallydelayorpreventtransactionsfromoccurring.

Asatransactionaltax,stampdutyimposesahigherlevelofoveralltaxationonindividualswhotransferpropertymorefrequently.StampdutyispartlymitigatedintheTerritorybyanumberofhomebuyerconcessionsandexemptionsforcorporatereconstructionstoassistwithbusinessrestructures.Dutyreliefisalsoprovidedtofirsthomebuyerstoensurestampdutydoesnotdetertheirentryintothehousingmarket.Furtherdetailsontheseconcessionsareprovidedlaterinthischapter.

Stampduty,inthatitincreasespurchasecosts,isonlyonefactoraffectingadecisiontopurchaseproperty.Otherfactorsincludeeconomicconditions,suchasemploymentopportunities,rentalorbusinessinvestmentreturns,andpersonalfactors,suchasthelocationoffamilyandtheavailabilityofhealth,educationandrecreationalservices.

Stampdutyalsohassomedesignbenefits.Stampdutyisonlypaidwhenpropertyispurchased,meaningthetimingofthetaxliabilitywillgenerallyalignwithataxpayer’sabilitytopay(thatis,whenthetaxpayerhasenoughfundstobuytheproperty),orbecapitalisedintoamortgage.Incomparison,recurrentpropertytaxesmaybelesssensitivetothetaxpayer’scapacitytopay.

Stampdutymayalsoimprovemarketstabilitybyaddingtransactioncostsandincreasingthecapitalgainsrequiredbeforeprofitscanbemadeonpropertyinvestment,whichmaydampenspeculativeinvestmentactivity.Aspropertyvaluesandinvestmentdecisionsareaffectedbyawiderangeofvariables,itisdifficulttoevaluatestampduty’seffectonmarketdemand.Somestateshavenonethelessintroducedspecificduties,particularlysurchargesonforeignbuyers,toattempttoaffectdemand-sidemarketconditions.

0246810121416$M

0100200300400500600700Number

< 10

0

100-

200

200-

300

300-

400

400-

500

500-

600

600-

700

700-

800

800-

900

900-

1 00

0

1 00

0-3

000

3 00

0-5

000

5 00

0-10

000

10 0

00-2

0 00

0

20 0

00-3

0 00

0

30 0

00-5

0 00

0

> 50

000

Stam

p du

ty c

olle

cted

Tran

sacti

on v

olum

e

Property value ($000)Transaction volume (count) Stamp duty revenue ($)

November 2017 | 25

Table7.1Foreignbuyersurcharges

NSW VIC QLDSA

(1January2018)WA

(1January2019)

8% 7% 3% 4% 4%

Source:Statelegislationandinformationavailableat31October2017

TheTerritorydoesnotimposeadutysurchargeonforeignbuyersofresidentiallandandforeigninvestmentinresidentialpropertyintheTerritoryisextremelylimited.AlthoughadutysurchargecouldbeimposedonforeignbuyersintheTerritory,itisunlikelytohaveanymaterialeffectonTerritoryrevenuesorrealestatemarketactivity.

7.4 StampdutyeffortintheTerritory–interstatecomparisonTheTerritoryhasrelativelyhighstampdutyrateswhencomparedtomoststates,otherthanVictoria.However,thereisnoannualpropertyorlandtaxintheTerritory.

Somestateshavedifferentdutyratesforcommercialtransactions.InSouthAustraliaandtheAustralianCapitalTerritory,thisreflectsabroaderreformagendatoexemptcommercialtransactionsfromstampduty.

TheTerritorychargescomparativelyhighstampdutyratesoverall,butthesizeofthedifferenceintaxratesvarieswithpropertyvalues.TheTerritory’staxonmedian-valueresidentialpropertiesiscomparativelymuchhigherthantheratesimposedinterstate.Thetaxonhigh-valuetransactionsisalsomorethanthestateaverage,particularlysincetaxrateswereincreasedfrom5.45toamaximumof5.95percenton1July2017.

TheTerritory’shighstampdutyrateissimilarlyreflectedinCommonwealthGrantCommission’s(CGC)assessmentsoftaxeffort.

Table7.2CGCassessedeffort–transferstampduty

NSW Vic Qld WA SA Tas ACT NT Average

2015-16 100.0 104.9 86.7 113.1 105.8 88.7 88.9 105.0 100.0

Source:CGC2017Update

7.5 Stamp duty home buyer concessionsTheeffectoftheTerritory'srelativelyhighstampdutyonTerritoryhomebuyersispartlyoffsetbyanumberofhomeincentiveschemes.

ThelargestprogramistheFirstHomeOwnerDiscount,whichprovidesstampdutyassistanceforfirsthomebuyerswhopurchaseanestablishedhomeintheTerritoryuptothevalueof$650000.Itisafullstampdutyconcessionontheinitial$500000valueofthehome,whichequatestoastampdutysavingofupto$23928.60.

TheTerritoryalsoprovidesaSenior,PensionerandCarerConcession,whichisastampdutydiscountofupto$10000toseniors(aged60yearsorover)orholdersofaNorthernTerritoryPensionerandCarerConcessionCard,forthepurchaseofahomevaluedupto$750000,orvacantlandvaluedupto$385000.

Finally,theTerritoryprovidesaPrincipalPlaceofResidenceRebate,whichisa$7000stampdutyconcessionfornon-firsthomebuyerswhopurchaseorbuildanewhome.

26 | Northern Territory Revenue Discussion Paper

Althoughnotataxconcession,theTerritoryalsoprovidesaFirstHomeOwnerGrantof$26000forfirsthomebuyersthatpurchaseorconstructanewhome.

Togetherthesestampdutyconcessions(andgrant)provideassistanceandresultinrevenueforgone,ofover$24millionperannum,whichissetoutinTable7.3.

Table7.3Homebuyerstampdutyconcessionsandotherincentives

Concession typeAnnualrevenueforgone

$M

FirstHomeOwnerDiscount 13.2

Senior,PensionerandCarerConcession 0.6

PrincipalPlaceofResidenceRebate 0.3

FirstHomeOwnerGrant 10.0

Total cost 24.1

Source:DepartmentofTreasuryandFinance

7.6 PotentialstampdutyreformoptionsIncrease stamp duty ratesAnincreaseinstampdutyrateswouldgenerategreaterGovernmentrevenuesandfundgovernmentservicedelivery.

AnyconsiderationofraisingstampdutyratesshouldtakeintoaccounttheTerritory’srelativelyhighstampdutyrateswhencomparedtothenationalaverage.

Nonetheless,theTerritory’soveralltaxationbaseislimitedandintheabsenceofanalternativeformoftaxation,increasingstampdutyrates(orreducingconcessions)isoneofthefewoptionsavailabletoGovernmenttoraiseadditionalrevenue.

Reform/reduce stamp duty ratesStampdutyisaprogressivetax,withratesincreasingasthevalueofthepropertybeingtransferredincreases.Otherthanatverylowvalueranges,theTerritory’sstampdutyrateishighwhencompared to stamp duty rates interstate.

Onereformoptionistoreducetaxrates.ThiscouldgenerallyimprovetheefficiencyoftheTerritory’staxationsystembutwouldresultinsubstantialreductionsinrevenue.

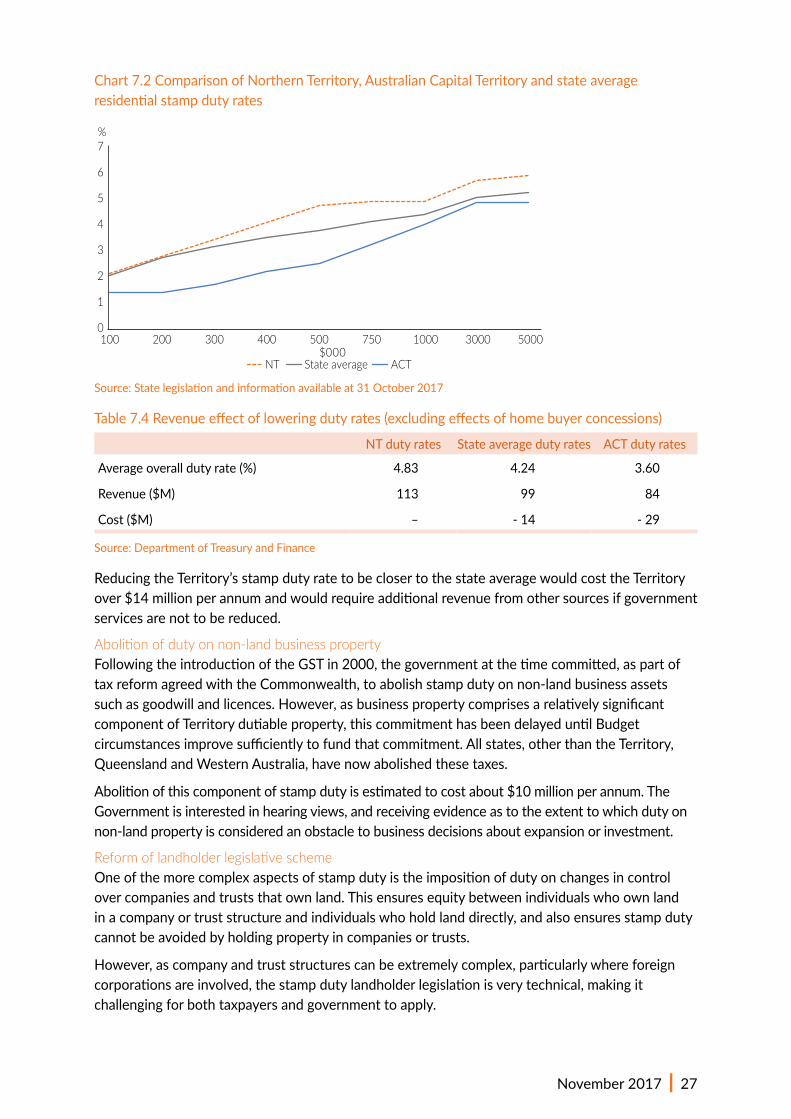

Chart7.2andTable7.4illustratetheeffectonTerritoryrevenuefromaligningtheTerritory’sdutyrateswiththelowerdutyratesintheAustralianCapitalTerritory,orbyadoptingtheaverageofduty rates imposed interstate.

November 2017 | 27

Chart7.2ComparisonofNorthernTerritory,AustralianCapitalTerritoryandstateaverageresidentialstampdutyrates

Source:Statelegislationandinformationavailableat31October2017

Table7.4Revenueeffectofloweringdutyrates(excludingeffectsofhomebuyerconcessions)

NT duty rates Stateaveragedutyrates ACTdutyrates

Averageoveralldutyrate(%) 4.83 4.24 3.60

Revenue($M) 113 99 84

Cost($M) – -14 -29

Source:DepartmentofTreasuryandFinance

ReducingtheTerritory’sstampdutyratetobeclosertothestateaveragewouldcosttheTerritoryover$14millionperannumandwouldrequireadditionalrevenuefromothersourcesifgovernmentservices are not to be reduced.

Abolition of duty on non-land business propertyFollowingtheintroductionoftheGSTin2000,thegovernmentatthetimecommitted,aspartoftaxreformagreedwiththeCommonwealth,toabolishstampdutyonnon-landbusinessassetssuchasgoodwillandlicences.However,asbusinesspropertycomprisesarelativelysignificantcomponentofTerritorydutiableproperty,thiscommitmenthasbeendelayeduntilBudgetcircumstancesimprovesufficientlytofundthatcommitment.Allstates,otherthantheTerritory,QueenslandandWesternAustralia,havenowabolishedthesetaxes.

Abolitionofthiscomponentofstampdutyisestimatedtocostabout$10millionperannum.TheGovernmentisinterestedinhearingviews,andreceivingevidenceastotheextenttowhichdutyonnon-landpropertyisconsideredanobstacletobusinessdecisionsaboutexpansionorinvestment.

Reform of landholder legislative schemeOneofthemorecomplexaspectsofstampdutyistheimpositionofdutyonchangesincontrolovercompaniesandtruststhatownland.Thisensuresequitybetweenindividualswhoownlandinacompanyortruststructureandindividualswhoholdlanddirectly,andalsoensuresstampdutycannotbeavoidedbyholdingpropertyincompaniesortrusts.

However,ascompanyandtruststructurescanbeextremelycomplex,particularlywhereforeigncorporationsareinvolved,thestampdutylandholderlegislationisverytechnical,makingitchallengingforbothtaxpayersandgovernmenttoapply.

100 200 300 400 500 750 1000 3000 5000$000

ACTNT State average

0

1

2

3

4

5

6

7%

28 | Northern Territory Revenue Discussion Paper

Althoughsomeofthiscomplexityisunavoidable,thecurrentlegislationcouldpossiblybereformedto make it easier to understand and apply.

Governmentisinterestedinwhetherindustryconsidersthistobeapriorityareaforreform.

Reform of corporate reconstruction exemptionsDutyexemptionsexisttoallowforcorporatereconstructionstoallowfortransfersofpropertywithincorporategroupsandfacilitatebusinessrestructures.However,toensuretheseprovisionsarenotexploitedfortaxavoidance,thecurrentprovisionsarerelativelytechnicalandhavearangeofspecificcriteriathatmustapplybeforetheconcessionisapplied.

Theseprovisionscouldbeexpandedtoallowforabroaderrangeoftransactionstobeexempted.Forexample,theprovisionscurrentlydonotapplytoassetsheldinunittruststructures.However,ascorporatereconstructionsarerelativelyrare,viewsaresoughtastowhethersuchreformswouldbeusefulinpracticeorareapriority.

7.7 AnnualpropertytaxesAnalternativetostampdutyisanannualtaxonlandownership.Arecurrentlandtaxisgenerallychargedontheunimprovedvalueoftheland(thatis,thelandvalueexcludingbuildingsandimprovements),andisnotdependentontransactionsinvolvingtheland.Recurrenttaxesonlandareregardedasefficientbecauselandisvaluableandimmobile,meaningthetaxcannotbeavoidedbychangesinthebehaviourofthelandowner.Previoustaxationreformreviewsinterstatehavenotedoveralleconomicefficiencycouldbeimprovedifstatesandterritoriesweretofocusonbroad-basedrecurrenttaxesonland.

Recurrentpropertytaxesincreasethecostsofowningland.Thiscanencouragelandlordstodevelopandutiliselandtowardsitsbesteconomicuse,anddiscouragepracticessuchaslandbanking.Taxesonunimprovedlandvaluesarealsodesirablefromarevenuestabilityperspective,asunimprovedlandvaluesarenotreliantonthestateoftherealestatemarket,thatis,priceandsalesvolumes.

OtherthantheTerritory,allstatesandtheAustralianCapitalTerritoryhavesomeformofrecurrentpropertytaxinadditiontolocalgovernmentrates,generallycalledalandtax.TheTerritorydoesnotimposeanykindoflandtax.

Althoughpropertytaxesaresaidtobeefficient,thelandtaxescurrentlyinplaceinotherstatessufferdesigninefficiencies,suchas:

• taxfreethresholdsthatexcludelowervaluelandholdingsfromthetaxbase

• significantexemptionsforparticularlanduses,specificallyprincipalplaceofresidence(forexample,thefamilyhome)andfarmingland,whichremovealargeportionoftheresidentiallandbaseandhighvaluelandholdingsfromthelandtaxbase

• progressiveratestructures,wheremorevaluablelandistaxedatahigherrate,whichmeanspropertyholdingsneedtobeaggregatedtoassessowners’liabilitytotax.Suchaggregationisadministrativelycomplexandcostlyandcancauseanincentiveforownerstoholdtheirlandindifferentformsofownershipvehiclesinanattempttoreducetheirlandtaxliability.

Incontrast,localgovernmentsacrossAustraliaimposebroad-basedlandtaxesintheformoflocalgovernmentrates.Thesetaxesmostlydonothavetheaboveinefficienciesandareconsideredtobeamongthemostefficienttaxesagovernmentcanimpose.

November 2017 | 29

Othertypesofrecurrentpropertytaxationinterstateincludetheimpositionofvariousmiscellaneouslevies,feesandcharges.Thisincludesregionallevies,suchasemergencyservicesleviesormetropolitanparkinglevies,leviesonforeignownersofland,andleviesonvacantresidentialland.Therateoflandtaxvariessignificantlyineachjurisdiction,asillustratedinTable7.5.

Table7.5Summaryoflandtaxratesandthresholds

NSW VIC QLD WA SA TAS ACT

Fixedcomponent($) 100 275 500 300 – 50 –

Minimumthreshold($000) 549 250 600 300 353 25 –

Maximumthreshold($000) 3357 3 000 5000 11 000 1 176 350 275

Minimumrate(%) 1.60 0.20 1.00 0.25 0.50 0.55 0.41

Maximumrate(%) 2.00 2.25 1.75 2.67 3.70 1.50 1.23

Source:Statelegislationandinformationavailableat31October2017

Theamountofrevenuethatcanberaisedineachjurisdictionthroughalandtaxvariesaccordingtothetaxrateandthresholds,butisalsodependentontheamount,valueanduseoflandinthatjurisdiction.

Assessmentsofeachjurisdiction’slandtaxcapacityaremadeannuallybytheCGC.HavingregardtotheTerritory’spopulation,theTerritoryisassessedashavingbelowaveragelandtaxcapacity,butcouldraise$72millionannuallyifstateaveragepolicywasimposed.

7.8 Potentialreform–introduceanannualpropertytaxAnannualbroad-basedpropertytaxwithnotax-freethresholdsandalowtaxratewouldbeverysimilarto,andhavethesameincidenceas,localgovernmentrates.Duetotheirsimilarities,itispossiblethatexistinglocalgovernmentsystemscouldbeleveragedtoallowanannualpropertytaxtobeimplementedintheTerritorytominimiseadministrativecosts.

Intermsofpossiblerevenueraisedundersuchamodel,theunimprovedcapitalvalueofrateablelandintheDarwin,Palmerston,Litchfield,AliceSpringsandKatherinelocalgovernmentareasisabout$21billion.Atataxrateof0.5percent,whichisroughlyequivalenttothelevelofratesimposedbylocalgovernments,thiswouldraise$105million,broadlyequivalenttoTerritorystampdutyrevenuein2016-17.

Introductionofanannualpropertytaxwouldprovideadditionalrevenuethatcouldfundgovernmentservices.Itmayalsoprovideanopportunitytofundothertaxreform,suchasreducingconveyanceorinsurancestampduty.Othertaxreviews,suchastheAustralia’sFutureTaxSystemReview,haverecommendedthatamovetoreducestampdutiesfundedbyannualpropertytaxeswouldresultinimprovementsinstateandterritorytaxationsystems.

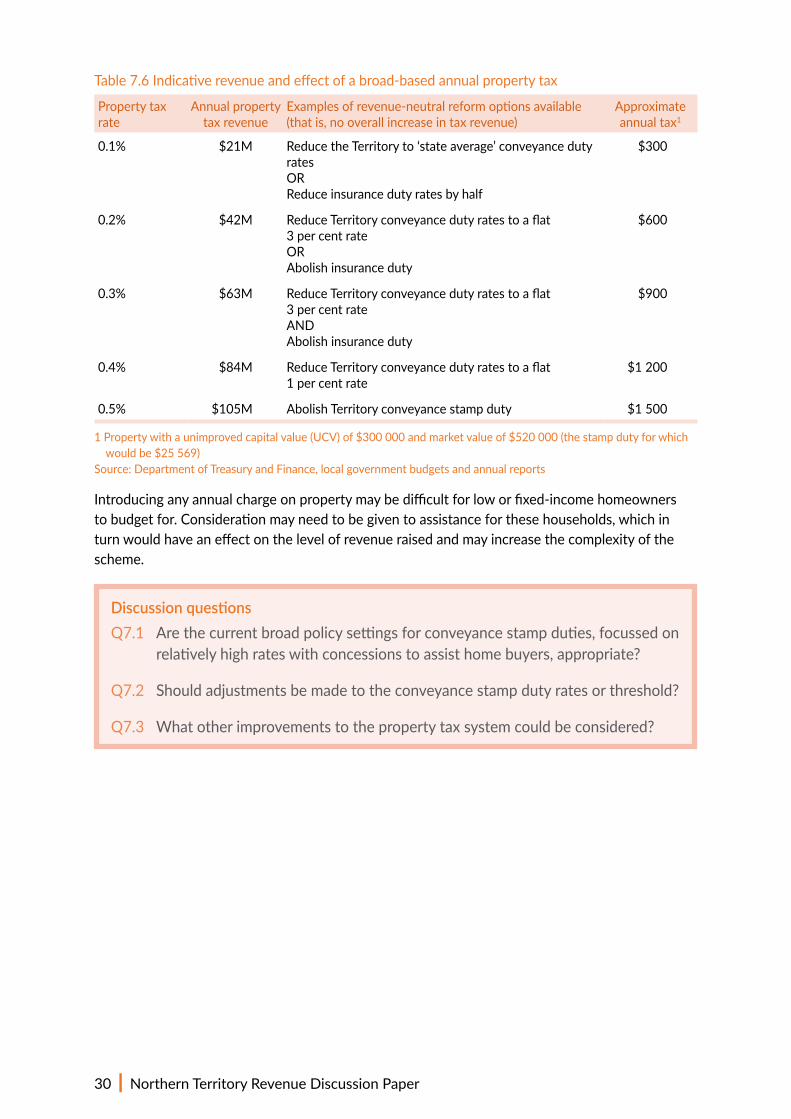

Table7.6setsoutindicativerevenue,theapproximateannualtaxpayablebyatypicalDarwinhomeandexamplesofothertaxreformthatcouldbefunded.

30 | Northern Territory Revenue Discussion Paper

Table7.6Indicativerevenueandeffectofabroad-basedannualpropertytax

Property tax rate

Annualpropertytax revenue

Examplesofrevenue-neutralreformoptionsavailable(thatis,nooverallincreaseintaxrevenue)

Approximateannual tax1

0.1% $21M ReducetheTerritoryto‘stateaverage’conveyancedutyratesORReduceinsurancedutyratesbyhalf

$300

0.2% $42M ReduceTerritoryconveyancedutyratestoaflat3 per cent rateORAbolishinsuranceduty

$600

0.3% $63M ReduceTerritoryconveyancedutyratestoaflat3 per cent rateANDAbolishinsuranceduty

$900

0.4% $84M ReduceTerritoryconveyancedutyratestoaflat1 per cent rate

$1 200

0.5% $105M AbolishTerritoryconveyancestampduty $1500

1Propertywithaunimprovedcapitalvalue(UCV)of$300000andmarketvalueof$520000(thestampdutyforwhichwouldbe$25569)

Source:DepartmentofTreasuryandFinance,localgovernmentbudgetsandannualreports

Introducinganyannualchargeonpropertymaybedifficultforloworfixed-incomehomeownerstobudgetfor.Considerationmayneedtobegiventoassistanceforthesehouseholds,whichinturnwouldhaveaneffectonthelevelofrevenueraisedandmayincreasethecomplexityofthescheme.

Discussion questionsQ7.1 Arethecurrentbroadpolicysettingsforconveyancestampduties,focussedon

relativelyhighrateswithconcessionstoassisthomebuyers,appropriate?

Q7.2 Shouldadjustmentsbemadetotheconveyancestampdutyratesorthreshold?

Q7.3 Whatotherimprovementstothepropertytaxsystemcouldbeconsidered?

November 2017 | 31

8 Gamblingtaxes

8.1 GamblingtaxoverviewGamblingtaxesarethefourthlargestcontributortotheTerritory’sown-sourcerevenue.In2017-18,gamblingtaxrevenueisforecasttobe$78million,upfrom$72millionin2016-17.Thismainlycomprisescommunitygamingmachinetaxof$32million,communitybenefitlevyof$12million,lotterytaxof$23million,bookmakertaxof$5millionandcasinotaxesof$4million.

Generally,gamblingactivitiesaretaxedathighrates.Thisisbecausegamblingactivitiesareoftenrestrictedbyregulation,withfewersuppliersthaninnormalcompetitivemarkets.Asaresult,industryparticipantsfacerestrictedcompetitionfromwhichtheycanextracthigherprofits.Thesehigherprofitsarealsoknownasmonopolyprofitsoreconomicrent.

Taxesoneconomicrentaregenerallyregardedasbeingaveryefficientformoftaxation.However,determininganappropriateleveloftaxationischallengingduetotheneedtobalancetherevenuethatcanberaisedfromgamblingtaxeswiththeregulatoryrolegovernmentplaysinlimitingsocialharmfromproblemgambling.

Furthermore,giventhesocialcostsassociatedwithgambling,thereisastrongcommunityexpectationforgovernmentstocollectareasonableshareofprofits,intheformoftaxes,fromgamblingactivities.

Intermsoftaxpolicyprinciples,gamblingtaxesaresomewhatregressive.Thisisbecauselowincomeearnerstendtospendproportionatelymoreoftheirincomeongamblingactivitiesincludinglotteriesandgamingmachines.

Gamblingtaxesarereasonablystraightforwardtoadminister,withlimitedcompliancecostsforbusinessafterotherregulatorycompliancerequirementsarefactoredin.Despitethissimplicityandtherelativestabilityofgamblingtaxcollection,therearetax-baserisksinrelationtobookmakertax,whicharedetailedlaterinthischapter.

TheNorthernTerritory2015GamblingPrevalenceandWellbeingSurveybytheNorthernTerritoryGovernmentandMenziesSchoolofHealthResearchfoundthatTerritoryadultpopulationgamblingparticipationdeclinedsignificantlybetween2005and2015,otherthanonlinegamblingonracingandsports.Thismayindicatelimitedscopeforgrowthingamblingtaxrevenues.

• TheTerritoryimposesseveralkindsofgamblingtaxes,includinglotteries,electronicgamingmachinetaxes,bookmakertaxandcasinotaxes.

• Communitygamingmachinetaxespaidbyclubsandhotelswererecentlyincreasedinthe2017-18Budget.

• Bookmakertaxesmayshifttobeingbasedonthelocationofthepersonplacingthebet,dependingonthereformsinterstate.

• Duetoexistingcontractualagreementswithoperators,thereislimitedscopetoreformothergamblingtaxes,suchascasinotaxes,inthenearterm.

32 | Northern Territory Revenue Discussion Paper

8.2 GamblingintheTerritoryGamblingintheTerritoryinvolvesElectronicGamingMachines(EGMs,colloquiallyknownaspokermachinesor‘pokies’),tablegamingincasinos,NTKenoandlotteries.Gamblingalsoincludesbetsplacedoneventssuchashorseracingorsportsbetting.

Pokies,tablegames,lotteries,andNTKenotypicallyphysicallytakeplaceintheTerritory,whilebettingonevents,andinparticularsportsbetting,canoccuronlinewiththebetsbeingplacedremotelybybothlocalandinterstatecustomers.TotheextenttheonlinebookmakersandbettingexchangecompaniesarelocatedintheTerritory,taxesarecurrentlypaidtotheTerritoryregardlessofwherethecustomersare.

8.3 TaxesoncommunitygamingmachinesCommunitygamingmachinetaxisamonthlytaxbasedonthegrossprofits,thatis,playerlosses,fromgamingmachinesinhotelsandclubs.ATerritorywide-caplimitsthetotalnumberofcommunitygamingmachinesto1852.Limitsinthenumberofgamingmachinesalsoapplyforeachvenue,being55forclubsand20forhotels.

From1July2017,communitygamingmachinetaxisimposedonclubsandhotelsatmarginalratesrangingfrom12.91percentto42.91percent,withrecentreformloweringthethresholdsatwhichthosemarginalratesareimposed.From1July2018,hotelswillbesubjecttofurtherchangestorates and thresholds.

8.4 CommunitybenefitsHotelsandthecasinosarealsosubjecttoa10percentcommunitybenefitlevyinadditiontogamingmachinetaxes,withrevenuefromthatlevycontributing$11milliontotheCommunityBenefitFundin2016-17.TheCommunityBenefitFundprovidesgrantstooffsetgaming-relatedharmandimprovecommunitywelfare.

Clubsarenotsubjecttothecommunitybenefitlevyinrecognitionthatclubsarenot-for-profitandalreadyprovidearangeofbenefitstothecommunity.

Clubshavesignificantdiscretioninthemannerandamountofcommunitybenefitstheyprovide.Thelevelofcontributionstothecommunityvarysignificantlyfromclubtoclubandyeartoyear.

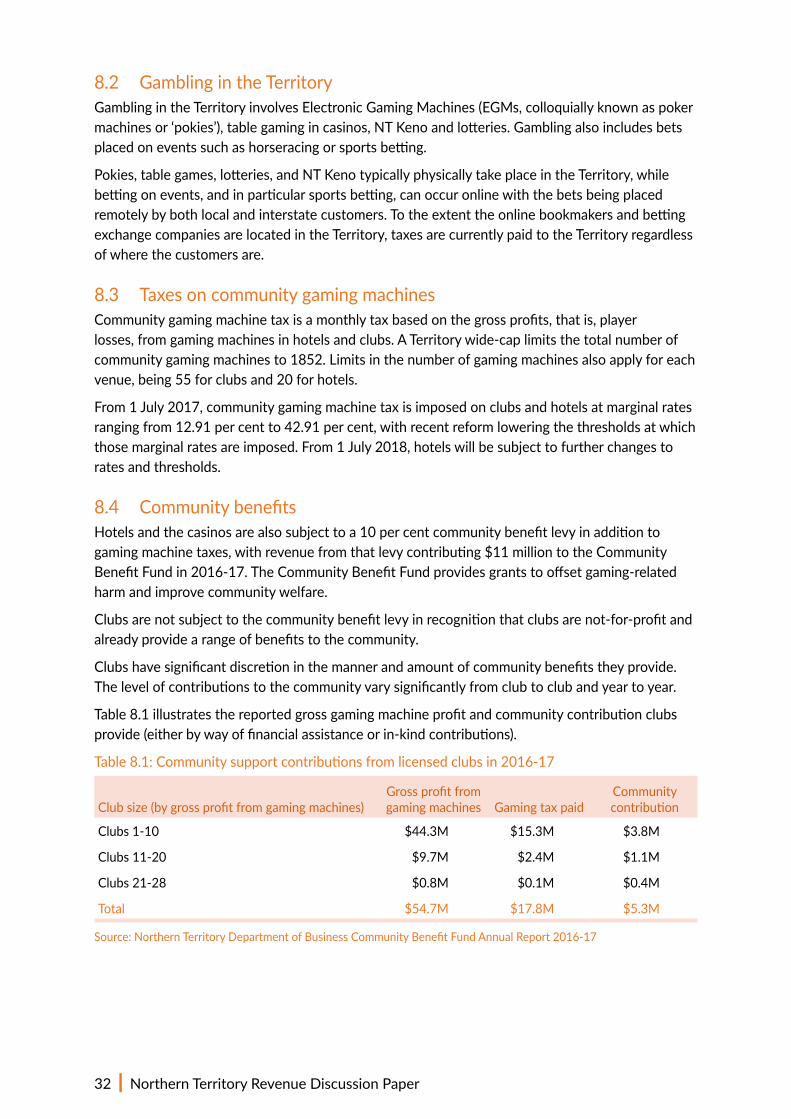

Table8.1illustratesthereportedgrossgamingmachineprofitandcommunitycontributionclubsprovide(eitherbywayoffinancialassistanceorin-kindcontributions).

Table8.1:Communitysupportcontributionsfromlicensedclubsin2016-17

Clubsize(bygrossprofitfromgamingmachines)Grossprofitfromgamingmachines Gamingtaxpaid

Community contribution

Clubs1-10 $44.3M $15.3M $3.8M

Clubs11-20 $9.7M $2.4M $1.1M

Clubs21-28 $0.8M $0.1M $0.4M

Total $54.7M $17.8M $5.3M

Source:NorthernTerritoryDepartmentofBusinessCommunityBenefitFundAnnualReport2016-17

November 2017 | 33

8.5 Casino taxesTherearetwocasinosintheTerritory,SKYCITYinDarwinandLassetersinAliceSprings.Casinosarelicensedtooperatepokies,whichareadditionaltotheTerritory-widecaponmachinenumbersapplicabletoclubsandhotels.Territorycasinosarealsorequiredtoprovideadditionalactivitiesincludingtablegames,aswellasrestaurantsandotherfacilities.Thisindirectlylimitsthenumberofpokiesbyrequiringfloorspacetobeputtootheruses.SKYCITYalsooperatesNTKeno,whichisbroadcasttoothervenuesunderlicensingarrangements.

Aspartofacasinolicence,operatorsenterintoataxagreementwiththeGovernment.Casinotaxratesaresetoutintheagreements,withtaxessubjecttoreviewbyGovernmentonthetermssetoutintheagreements.SKYCITY’snexttaxreviewisin2025(andthenevery10years),whereasLasseters’reviewisin2022(andthenevery10years).

Thesetaxreviewsmusttakeintoaccounttheprofitabilityofthecasinos,gamblingharm,conductofthecasinosandthecasinos’investmentinthelocaleconomy,suchasthroughexpansion,refurbishment,communitysponsorshipandsupport,andtheprovisionofnon-gamblingentertainment,retailanddiningfacilities.Thereislimitedscopetoamendcasinotaxarrangementsoutsidetheagreementreviewclauses.

Presently,differenttaxratesapplytothegrossprofitsofeachtypeofgamblingactivityundertakenatSKYCITYandLasseterscasinos.ThesearesummarisedinTable8.2below.

Table8.2:Comparisonofcasinotaxes

Casino Poker machines Tablegamesandcommissionplay Keno

SKYCITY 15%plus10%community benefitlevy

RateequivalenttotheGSTrate 10%

Lasseters 11%1plus10%communitybenefitlevy

RateequivalenttotheGSTrate TaxpaidbySKYCITY

1Increasingto13 per centin2018,15 per centin2019and20 per cent in 2022.Source:CasinoOperatorsAgreements

8.6 LotterytaxCurrently,theTattsGrouppayslotterytaxbasedonnetprofitsoflotteriesphysicallysoldintheTerritoryandonlinethroughtheinternetlotterylicencegrantedbytheTerritorytoTatts Group.

Lotterytaxisbasedonanexclusive20-yearlicenceandagreementbetweentheTerritoryandTatts,negotiatedin2012.Toreflectthemonopolyrightsassociatedwiththeseagreements,andthegenerallackofseparatecommunityinvestmentincomparisonwithcasinosorothercommunitygamingvenues,lotterytaxratesaremuchhigherthanotherformsofgamingtax.Aslotterytaxesaresetbyagreement,reformoptionsarelimited.

8.7 WageringtaxWageringtaxispaidbyUBETinrelationtototalisator(‘tote’)wageringthoughTerritoryoutlets,clubsandpubs,andatracecourses.In2015,UBETwasgrantedalong-termexclusivelicencetooperatetotewageringintheTerritoryforaperiodof20years.

34 | Northern Territory Revenue Discussion Paper

AlthoughthetermsofthatagreementreducedtheamountofwageringtaxpayabletotheTerritorybyUBET,itresultedinUBETprovidingsustainable,long-termfundingtotheracingindustrythroughthepeakbodiesThoroughbredRacingNTandtheDarwinGreyhoundAssociation.Thesebodiesreceivesignificantfixedannualfunding,monthlypaymentsbasedonfixedpricebettingrevenue,aquarterlyindustryfundingpackage,andracingandregionalmarketingsupportfees.Thesepaymentssignificantlyreducetheamountofindustryassistancegovernmentwouldotherwiseprovidetotheracingsector.

Duetothe20-yearexclusivityagreementcurrentlyinplacewithUBET(until2035),taxreformoptionsarelimited.

8.8 BookmakertaxandbettingexchangetaxAlthoughonlinebookmakershavearelativelysmallphysicalpresenceintheTerritory,theynonethelesscontributetotheTerritoryeconomy.Onlinebookmakersandbettingexchangesemployabout380Territoriansandprovideabout$42millioninbroadereconomicbenefitsincludingtaxes,sponsorships,productfees,rentandAboriginalemploymentprograms.

Bookmakersandbettingexchangespaytaxatarateof10percentongrossprofits,cappedatamaximumof500000revenueunits(currently$575000).Bookmakerspaidabout$5.4millioninbookmakertaxin2016-17.

TheTerritory’sbookmakertaxcapwassetindirectresponsetotaxcompetitionfromotherstates.Asaresult,bookmakersremainedintheTerritorybutatthecostofasignificantreductioninTerritorytaxrevenue.Aslongascurrentinterstatetaxcompetitionremains,thereislimitedabilityfortheTerritorytoadjustbookmakertaxrates.

However,oneareathatcouldbeexaminedisaligningthetreatmentofbetsmadeinrelationtosportingevents.Currently,bookmakertaxesareleviedongrossprofitsinrelationtobetsmadeonhorse,trottingandgreyhoundraces.Betsonothereventsarespecificallyexcludedincalculatinggrossmonthlyprofitfortaxpurposes.Asaresult,bookmakersprimarilyfocusedonbettinginrelationtosportingeventspaylowerbookmakertax.

Thereasonforthisinconsistencyislargelyhistoric,asgamblingonothersportingeventswasmuchlowerinthe1990sandTerritorygamblingtaxonothersportingeventswasrelativelylowpriortobeingremovedtomakewayfortheintroductionoftheGST.Expandingthetaxtoincludesportingevents could raise up to $1.1 million per annum.

Morerecently,otherstateshaveexpressedinterestinapoint-of-consumptiontaxonbookmakersbasedonthelocationofthepersonplacingthebet,ratherthanthelocationofthebookmaker.SouthAustraliacommencedapoint-of-consumptiontaxon1July2017,andimposesa15percenttaxonthenetwageringrevenueofallbettingcompaniesfrombetsplacedbycustomerslocatedinSouthAustralia.Thisnewtaxisexpectedtoraiseabout$10 millionperannumfortheSouthAustralianGovernment.

WesternAustraliaissettointroduceasimilartaxfrom1January2019anditsracingindustrywillbecompensatedforanydirectfinancialimpactsrelativetothecurrenttaxscheme.Themeasureisexpectedtoraiseover$20millionperannumfortheWesternAustralianGovernment.

November 2017 | 35

Incomparison,theTerritorywouldraiseonlyabout$1to$2millionifitfollowedtheSouthAustralianapproach,whereasmorethan$5millioninbookmakertaxwascollectedin2016-17.Althoughapoint-of-consumptiontaxhasadvantagesforotherstategovernments’taxrevenues,itpresentsachallengefortheTerritory,asmostbetsareplacedbyconsumersresidinginotherjurisdictions.

Otherissuesincludedesigningtaxestoavoiddoubletaxation,ensuringanewtaxcanbeeffectivelyimplementedbybookmakers,andrecognisingthepaymentofGSTandproductfeespaidtosportingbodies.

TheTerritoryopposestheintroductionofpoint-of-consumptiontaxes.However,giventhemovesbyotherstates,theTerritoryhasadvocated,throughtheCouncilofFederalFinancialRelations,thatanyintroductionofapoint-of-consumptiontaxshouldbethroughaunifiednationaltaxscheme,eitherthroughconsistentstatetaxescollectedbyasinglejurisdictionorbymeansofaCommonwealthtax.Suchamodelwouldreducetheadministrativeandcomplianceburdenthatwouldariseunderdivergentstatetaxmodels.

Discussion questionsQ8.1 Arethecurrentbroadpolicysettingsforgamblingtaxesappropriate?

Q8.2 Aregamblingtaxcollectionsatanappropriatelevel?Ifnot,howshouldgamblingprofitsbebetterdistributedbetweengamblingoperatorsandtheTerritory?

Q8.3 IfanygamblingtaxadjustmentswouldreducetherevenuereceivedbyGovernment,whatmeasuresshouldbetaken,orothersourcesofrevenueconsidered,tocompensate?

36 | Northern Territory Revenue Discussion Paper

9 Motorvehicletaxes

9.1 MotorvehicletaxoverviewTherearetwomainTerritorytaxesimposedonmotorvehicles.Stampdutyisimposedonthetransferofownershipofamotorvehicle(motorvehicleduty)andfeesarealsopayableontheregistrationorrenewalofregistrationofamotorvehicle.

In2016-17,theTerritoryreceivedabout$70millioninmotorvehicletaxesoralmost10per cent ofown-sourcetaxandroyaltyrevenue.Thistotalcomprised$48millioninmotorvehiclefees($28millionfromlightvehicleregistrationsand$20millionfromheavyvehicleregistrations)and$22 million in motor vehicle duty.

Motorvehicletaxesarearelativelyefficientandstableformofrevenue.Motorvehicleregistrationfees,imposedperiodicallyandatlowerrates,aremoreefficientthanmotorvehicleduty,whichisimposedonatransactionalbasis.

Itisrecognisedthatmotorvehiclecostsareasignificantcomponentofhouseholdexpenditure.AustralianGovernmenttaxes,compulsorymotoraccidentinsuranceandothercostssuchascouncilparkingfees,eachincreasethecostofowningamotorvehicle.

9.2 MotorvehicledutyMotorvehicleownersarerequiredtopaystampdutyontheissueortransferofamotorvehiclecertificateofregistration.Stampdutyisleviedonthevalueorpurchasepriceofthevehicleatarateof$3per$100orpartthereof.ThisincludesvehicleaccessoriesandadditionalequipmentatthetimetheapplicationforregistrationortransferismadeaswellasanyGSTpayable.

DutyispayableattheMotorVehicleRegistryatthetimetheapplicationforregistrationortransferismade,withapplicationtobemadewithin14daysofapersonbecomingtheownerofthevehicle.

Duetomotorvehicleduty’srelativelylowrate,itsinfluenceontaxpayerbehaviourislikelytobelimited.Forexample,anadditional$150indutywouldbepayablebyaTerritoriandecidingbetweena$25000and$30000car.Comparedwiththecostofthecar,thestampdutyisunlikelytobeamajorfactorindecidingbetweenthetwochoices.

Totheextentthatithasaneffectonbehaviour,stampdutyismorelikelytodeterapersonfromregisteringchangeofownershipofamotorvehicle(asthisiswhenthedutyispaid)ratherthanthesaleorunderlyingchangeinownershipofavehicle.

• TheTerritoryimposesmotorvehicledutywhenownershipofavehiclechanges,andalsochargessix-monthlyorannualregistrationfees.

• TheTerritory’sstampdutyrateandregistrationfeesareamongthelowestinAustralia.ThiscontributestothetotalcostofregistrationofTerritoryvehiclesbeingbelowthenationalaverage.

• AustralianGovernmenttaxes,compulsorymotoraccidentinsuranceandothercostsincreasethecostofowningamotorvehiclefarmorethanTerritorytaxes.

November 2017 | 37

9.3 MotorvehicleregistrationfeesTerritorymotoristsarealsorequiredtopayasix-monthlyorannualfeetoregistertheirvehiclesforuseon-road.Vehicleregistrationhelpstoensuretheroadworthinessofmotorvehiclesandpromotestheirsimpleandreliableidentificationandproofofownership.

RegistrationfeesintheTerritoryarecollectedontheregistrationofbothlightandheavyvehicles.HeavyvehicleregistrationfeesaredeterminednationallybytheStandingCouncilonTransportandInfrastructure,andareadjustedinJulyeachyear.

LightvehicleregistrationfeesaredeterminedbytheTerritoryandvaryaccordingtoadifferentialscalebasedonenginecapacityandnumberofcylinders.Feesareexpressedinrevenueunits,whichmeansmotorvehicleregistrationfeesincreaseinlinewithinflation.

Althoughnottaxationrevenue,compulsorymotoraccidentcoveraddstothetotalcostofowningavehicle.MotoraccidentinsurancepremiumsintheTerritoryaresetbytheMotorAccidentsCompensationCommissionandfundno-faultinsurancetoroaduserswhoareinjuredordieasaresultofanaccident.Premiumsarebasedonensuringlikelycompensationclaimscanbemetandaresubjecttoactuarialreviewannually.IntheTerritory,premiumsareaffectedbyhighercostsassociatedwiththeTerritory’ssmallpopulationbaseandhighincidenceofroadaccidentcasualties.Nonetheless,Territorymotoraccidentpremiumsarearoundtheaverageoftheotherstates.

9.4 Interstate comparisonTheTerritory’sstampdutyrateandmotorvehicleregistrationfeesareamongthelowestinAustralia.Intermsofstampduty,incomparisonwiththeTerritory’sflat3percentrate,otherjurisdictionsapplyvariousprogressiveratescalesandoftenapplydifferentratesforpassengerandcommercialvehicles.Forexample,forpassengervehiclesaboveacertainvaluethreshold(rangingfromover$40000inTasmaniato$65000inVictoria),higherratesofbetween4percentand6.5percentmayapplyinterstate.

AnumberofmotorvehicledutyexemptionsapplyintheTerritoryandinterstate,includingwhenregistrationistransferredbetweenjurisdictions,agriculturalorprimaryproductionvehicles,vehiclesownedbycharities,andtradingstockofmotorvehicledealers.Someenthusiastvehicles,caravansandtrailersmayalsobeexempt.IntheAustralianCapitalTerritory,agreenvehicleratingschemeapplies,whichprovidesforconcessionalratesofdutybasedonlowervehiclecarbondioxide emissions per kilometre.

Formotorvehicleregistrationfees,somestatescalculatefeesbasedongrossvehiclemassandtareweightandsomebasedonenginecapacityandnumberofcylinders.Somestatesalsoimposeemergencyservicelevies,trafficimprovementlevies,roadrescuefeesandroadsafetycontributionfees.AscanbeseeninTable9.1,whichcomparesarangeofpopularlightvehicles,theTerritory’smotorvehicleregistrationfeesareamongthelowestinAustraliaandcontributetotheTerritory’stotalcostofregistrationgenerallybeingbelowthenationalaverage.

38 | Northern Territory Revenue Discussion Paper

Table9.1:Motorvehicleregistrationcostscomparison

Vehicle NSW VIC QLD WA SA TAS ACT NT Avg

2017ToyotaCorolla/Hyundaii30

Registrationfee($) 358 290 310 301 123 200 366 179 266

Compulsoryinsurance,othercharges($)

638 510 435 421 648 377 700 559 536

Total registration cost ($) 996 801 746 721 771 577 1 066 738 802

Ranking1

Registrationfee 7 4 6 5 1 3 8 2

Total costs 7 6 4 2 5 1 8 3

2017ToyotaHiluxSR5

Registrationfee($) 513 290 310 474 454 200 532 179 369

Compulsoryinsurance,othercharges($)