Embed Size (px)

Citation preview

Northern Territory Petroleum Royalty Reforms

Key Directions

Discussion Paper

November 2014

Discussion Paper – Petroleum Royalty Reforms

Consultation

Comments are sought from interested stakeholders on the issues in this Discussion Paper. The Northern Territory Department of Treasury and Finance (DTF) is seeking written feedback on the key directions that are outlined and stakeholders are invited to provide any other relevant feedback. All submissions will be closely analysed by DTF in developing petroleum royalty reforms.

Written submissions received by DTF will be treated as public unless the documentation is clearly marked as “CONFIDENTIAL”.

Non-confidential comments and submissions may be made publicly available and DTF may quote from or refer to this material in reports that it prepares. DTF will not provide access to a confidential submission or commercially sensitive information unless access accords with the Information Act.

Any views or opinions expressed in the Discussion Paper should not be taken to represent the final settled views of either DTF or the Northern Territory Government.

Written submissions will be accepted until Friday 30 January 2015. Comments should be sent by email to [email protected] or by post to:

Director Revenue DevelopmentDepartment of Treasury and FinanceGPO Box 154DARWIN NT 0801

Enquiries can also be directed to the Director Revenue Development at (08) 8999 5453 or to the email address above.

An electronic copy of this Discussion Paper can be found at: http://www.treasury.nt.gov.au/TaxesRoyaltiesAndGrants/Pages/default.aspx

Guiding Questions

Questions that stakeholders may consider in responding to this Discussion Paper include:

1. Do you agree that the current petroleum royalty regime is in urgent need of reform?

2. If petroleum royalty reform is needed:

Option 1 – Should all new petroleum projects, and existing producers who have elected to opt-in, be subject to a profit-based royalty regime, thereby establishing a consistent royalty treatment for the Territory’s mineral and petroleum resources?

Option 2 – Should reform instead be limited to inserting comprehensive administrative provisions in the existing Petroleum Act or Petroleum Regulations, with the current ad valorem royalty rate of 10 per cent of gross value at the wellhead retained?

2

Discussion Paper – Petroleum Royalty Reforms

Secondary questions in relation to Options 1 and 2 include whether the petroleum royalty regime:

(i) should have closer regard to a petroleum producer’s ability to pay by only imposing royalty on profitable ventures?

(ii) should recognise the significant up-front costs of new petroleum ventures by allowing the carry forward and deduction of these costs in future years?

3. What other matters should be considered in relation to Options 1 and 2 to ensure that any reforms are workable and have no unintended consequences?

Are there any technical issues that you wish to raise at this stage?

3

Discussion Paper – Petroleum Royalty Reforms

Background

This Discussion Paper is designed to highlight the key directions for possible petroleum royalty reforms in the Territory. The questions in relation to the options are designed to assist stakeholders in preparing their submissions to DTF. Further targeted consultation may occur if it is necessary for DTF to clarify or explore points raised in submissions.

Following consultation, DTF will develop its recommendations to the Government. This will include a recommendation as to whether to prepare exposure draft legislation and an explanatory statement of the reforms, potentially to be released for comment by the second half of 2015.

Issues

The purpose of this Paper is to canvass views about applying the Territory’s profit-based mineral royalty system to petroleum. This would involve reforming the Petroleum Act, with consequential changes to the Mineral Royalty Act, with the intention of providing a more transparent, equitable and efficient royalty framework to encourage greater exploration, investment and petroleum production.

This is in keeping with the Territory’s key objectives to help stimulate development of petroleum and ensuring a fair sharing of revenue from the extraction of non-renewable resources. The Territory recognises that it competes both domestically and internationally in relation to oil and gas exploration and subsequent investment decisions.

At the very least, reforms should consider how to improve the administration of petroleum royalties in the Territory, provide for greater consistency between royalty payers and obtain an optimum return from the ownership of its resources for the benefit of Territorians.

Introduction

Although land may be leased or owned by a person, the ownership of non-renewable onshore resources, and limited offshore resources in coastal waters, remains with the Territory on behalf of the community. Although a significant part of the Territory is covered by exploration permits, the Territory remains largely under-explored and its full resource potential is yet to be realised.

Exploration and extraction of these resources is not undertaken by the Territory Government but instead by the private sector at considerable risk and potential for significant rewards. In return for the right to extract the Territory’s resources, on behalf of the community, the Government receives compensation or consideration known as a royalty. Unlike taxes, royalties are designed to compensate the Territory for the depletion or loss of its non-renewable resources.

Importantly, it should be noted that exploration does not necessarily lead to further development and production. In under-developed regions where there is limited infrastructure, substantial capital costs may deter private investment.

4

Discussion Paper – Petroleum Royalty Reforms

The economics of oil and gas projects in the Territory are impacted by the Territory’s remoteness and the high cost of the infrastructure that is required. The royalty regime is only one relevant factor in deciding whether to invest large capital amounts in a project with long lead times and many potential years of production. Royalties are unrelated to environmental and other broader regulatory matters administered by the Department of Mines and Energy.

There is also an ongoing need to balance development objectives with ensuring a fairer return to the community. If royalty collections are low, then the Territory is effectively foregoing an important source of revenue by selling community resources cheaply.

In contrast with mineral royalties, due to much petroleum production occurring offshore and outside coastal waters, petroleum royalties do not currently represent a significant portion of the Territory’s revenue. Petroleum royalties will remain at such a level in the short to medium term until new onshore projects commence and/or existing projects increase production.

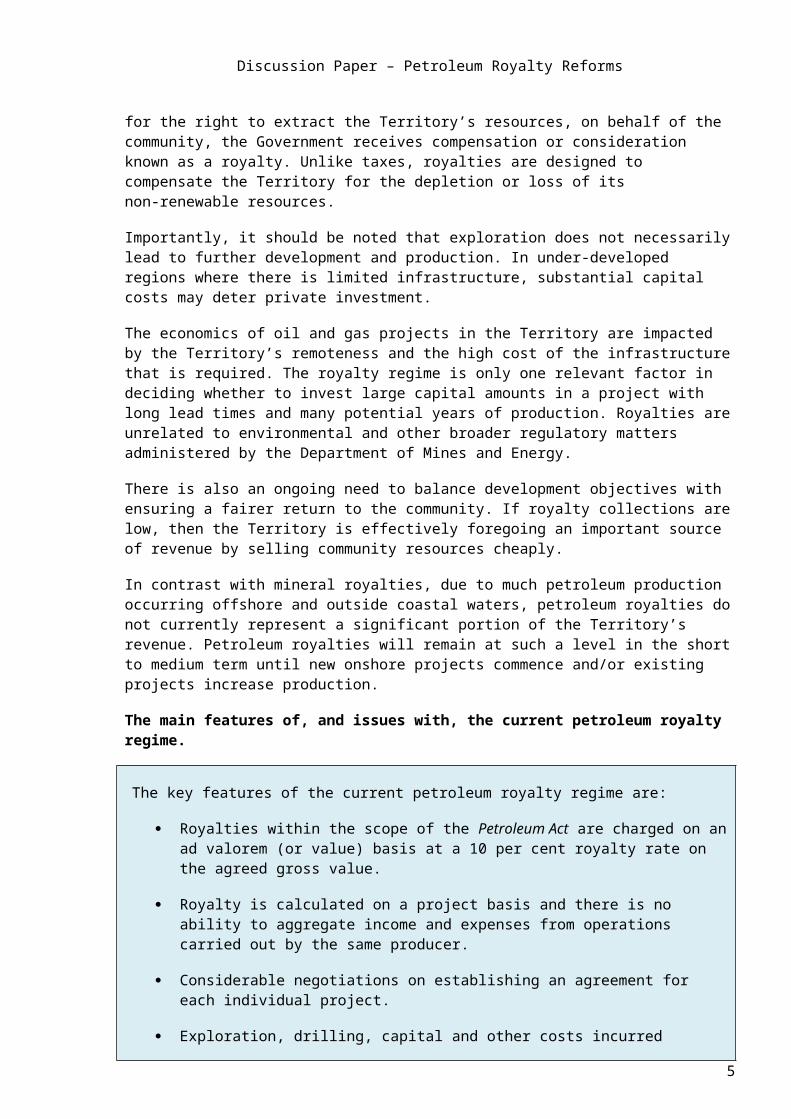

The main features of, and issues with, the current petroleum royalty regime.

The key features of the current petroleum royalty regime are:

Royalties within the scope of the Petroleum Act are charged on an ad valorem (or value) basis at a 10 per cent royalty rate on the agreed gross value.

Royalty is calculated on a project basis and there is no ability to aggregate income and expenses from operations carried out by the same producer.

Considerable negotiations on establishing an agreement for each individual project.

Exploration, drilling, capital and other costs incurred upstream of the wellhead are not recognised. Similarly, abandonment costs (such as mothballing and rehabilitation expenditure) are not deductible.

Royalty not directly affected by profitability therefore, royalty will be payable as soon as production commences (regardless of the quality, size and location of the production fields).

Administrative arrangements also by way of agreement rather than by legislation.

An overview of the administrative arrangements relating to the establishment, calculation and collection of royalties under the Petroleum Act is set out in the Appendix.

Valuation and deductions

Petroleum royalty is imposed under the Petroleum Act at a rate of 10 per cent of the agreed gross value of the petroleum produced at the wellhead. This is because it is at the wellhead that ownership of the petroleum passes from the Territory to the producer. The Petroleum Act requires gross value to be calculated in accordance with individual agreements with producers.

5

Discussion Paper – Petroleum Royalty Reforms

In the absence of an agreement, royalties will be imposed pursuant to a binding determination by the Treasurer (being the Minister responsible for administering the royalty provisions within the Petroleum Act). This absence of a legislative valuation process causes market uncertainty and is one of the barriers to explorers/potential producers being able to forecast the likely economic return of a project.

The general basis underpinning the notion of gross value at the wellhead is that it is determined by the price received by producers for any petroleum sold when it is first extracted (i.e. at the top of the well casing). However, the oil and gas industry has significantly changed in the period since the relevant petroleum legislation came into force such that most producers no longer market petroleum products for sale at the wellhead. Instead, petroleum can be disposed of at different points in the production and transport chain.

As a result, with no direct sales (i.e. arm’s length sales or comparable sales) of petroleum at the wellhead, gross value must be calculated according to the net-back or work-back method or other acceptable valuation methods. Currently, these valuation methods are negotiated on a project by project basis. For example, gross value at the wellhead may be ascertained by determining the commercial value of the petroleum at the first point of sale and then subtracting certain expenditure directly attributable to post-wellhead production/processing, maintenance for the purposes of post-wellhead production/processing or the sale and marketing of petroleum up to the first point of sale.

Limitation of net-back methodology and allowable deductions

As there is no legislative underpinning for determining gross value of the petroleum produced at the wellhead under a net-back methodology, this process is dependent upon the adoption of reasonable administrative guidelines and the negotiation of proper outcomes under the written agreement between the Territory and petroleum producers.

Only essential post-wellhead production costs are deductible from the sale price, such as processing, transport and storage costs. This is provided that the costs are incurred before the first point of sale. However, costs incurred upstream of the wellhead are not deductible. Examples of non-deductible costs are exploration and drilling costs and the lifting costs of bringing petroleum to the surface.

By contrast, under a net value or profit-based approach, there may be considerable room for allowing deductions in relation to some exploration or drilling costs, or costs of bringing petroleum to the surface. Such an approach may better reflect the significant pre-production costs of the petroleum extraction industry.

The limitations of the net-back approach coupled with the inherent nature of the ad valorem royalty scheme mean that generally, a limit on post-wellhead costs up to 50 per cent of the gross sales value for petroleum will be incorporated into the agreements and implemented in determining gross value at the wellhead.

This limitation is required to ensure that deductions do not exceed sale values and that the Territory will always receive a royalty on petroleum production. This is because the nature of a net-back methodology sits uncomfortably within a scheme intended to be an ad valorem

6

Discussion Paper – Petroleum Royalty Reforms

royalty and instead can lead to quasi profit-based or net value outcomes but without the guidance of a robust legislative scheme.

Overall, the 10 per cent rate on agreed gross value of the petroleum produced at the wellhead is effectively an average equivalent ad valorem rate of about 5 to 6 per cent on the actual sales at the first point of sale.

Timing of royalty payments over life of project

Under the existing petroleum royalty scheme, producers are required to pay royalties as soon as a project commences production. This is notwithstanding the large capital start-up costs producers would have incurred and is regardless of whether the project is profitable. As a result, the Territory may be missing out on the benefits from marginal fields that currently are not developed due to potential investors deciding that a project is not feasible after royalty is imposed.

Administration frameworks

The Department of Mines and Energy issues titles under the Territory’s petroleum legislation for the right to produce petroleum within the Territory. When a person obtains a title or licence they must undertake to pay royalties. The Territory Revenue Office is responsible for administering both mining and petroleum royalties.

The Petroleum Act has limited administrative and compliance provisions to support the collection of royalties. For example, the Petroleum Act does not detail the requirements for making payment and lodging returns and has no administrative review provisions (i.e. objection and appeal rights against assessments) if disputes arise. It also provides little guidance for determining appropriate deductions for allowable post-wellhead costs.

This lack of legislative detail creates uncertainty for both producers and the Territory Revenue Office as to when and how royalty liabilities are to be met. Accordingly, a project by project approach to settling petroleum royalty arrangements in the Territory is currently necessary.

This framework has significant compliance limitations, may be less attractive to investors due to the uncertainty for prospective producers and is less transparent than a more comprehensive, up to date legislative scheme.

Establishing all mining and petroleum royalties under a single profit-based scheme would streamline regulation and provide certainty and equity. The administrative arrangements under the Mineral Royalty Act are more robust and transparent than the Petroleum Act.

Furthermore, Royalty Guidelines issued by the Mineral Royalty Secretary assist royalty payers in understanding and meeting their mineral royalty obligations. These Guidelines can be found at: http://www.treasury.nt.gov.au/TaxesRoyaltiesAndGrants/Royalties/Mineral-Royalty/Pages/Mineral-Royalty-Guidelines.aspx

The Mineral Royalty Act also contains rules which limit the amount of transfer pricing that multi-national miners can engage in. Rules also address the increasing integration and centralisation of operational management and administration functions at the royalty payer’s head office. Bringing petroleum royalty under the ambit of the Mineral Royalty Act would ensure that the transfer pricing rules also apply to new petroleum projects, limiting the scope for manipulation of petroleum royalty obligations.

7

Discussion Paper – Petroleum Royalty Reforms

Unconventional Gas

A difficulty that would be eliminated by a single profit-based scheme is the uncertainty as to which royalty regime applies to unconventional processes such as coal seam methane and underground gasification, which are akin to petroleum production but relate to a mineral resource.

The petroleum industry has traditionally involved the recovery of oil and gas through conventional means. This has involved drilling wells and lifting the oil and gas out of the ground for processing and transportation to the marketplace. Recent advances in technology and exploration and extraction techniques have resulted in the discovery of, and the ability to recover natural gas from, new sources such as shale rock and coal.

While the chemical makeup of this gas is the same as conventional gas, shale gas and coal seam gas are commonly referred to as ‘unconventional gas’. This is due to the innovative techniques used to recover these resources, particularly horizontal drilling and hydraulic fracturing (fracking). Increased discoveries of and access to unconventional gas has resulted in estimates of the Territory’s gas reserves being revised upwards and substantial growth is expected to continue.

A move by the Territory to a profit-based petroleum royalty, consistent with the Territory’s regime for miners, would clarify the royalty treatment for unconventional gas and ensure that arrangements are robust with respect to new technologies and innovative techniques. The environmental impacts of fracking and the effectiveness of mitigation measures are beyond the scope of the Discussion Paper.

Profit-based royalty regime – Mineral Royalty Act

The key features of the current mineral royalty regime are:

20 per cent royalty rate on the net value as prescribed by legislation.

A uniform scheme for all royalty payers regardless of the type of minerals produced.

Greater deductibility of certain exploration, pre-production, production and rehabilitation costs.

Royalty losses can be carried forward and accumulated until offset against profits.

Accelerated semi-annual deduction of capital costs, with an uplift factor based on the 10 year bond rate plus 2 per cent, which recognises the depreciation of mining assets as well as the cost of financing.

Changes in profitability over a mine’s life impacts on royalty such that less or no royalty is collected at commencement, with greater royalty being collected when a mine matures. Also there is a stronger growth in royalty revenues in times of high mineral prices than under an ad valorem scheme but the opposite result in times of low mineral prices.

Consistent treatment of projects and avoids the need for lengthy negotiations on establishing an agreement for each new project.

Administrative arrangements also specified in the legislation.

8

Discussion Paper – Petroleum Royalty Reforms

Although a move by the Territory to a profit-based petroleum royalty would differ from the approach of the other states, it would be consistent with the Territory’s regime for miners.

The Mineral Royalty Act establishes a profit-based regime that uses the ‘net value’ of a mine’s production to calculate royalty. It has been in place in the Territory and applied to numerous mining companies since 1982. The regime allows for the deduction of a range of costs associated with the operation of a mine. The regime also recognises the cost of capital expenditure through a deduction that recognises the depreciation of mining assets.

The Commonwealth imposes a profit-based resource rent tax on petroleum, although onshore petroleum producers are able to credit in full the royalties paid to state and territory governments. The Commonwealth’s scheme, however, attempts to tax “super profits” and, accordingly, the rate is higher (40 per cent of taxable profits) and the deductions allowed to be claimed by producers are wider and more significant when compared to those allowed under the Mineral Royalty Act.

In comparison, states generally impose royalties on a value or per tonnage basis with very limited or no allowable deductions. State mineral royalty rates often vary depending on the commodity being recovered. For petroleum products, similar to the Territory, all states impose royalties on value at the wellhead with rates ranging between 10 and 12.5 per cent.

When comparing royalty regimes, a profit-based regime will always have a higher headline rate than a value based or volume based regime. Thus, on the surface, the 20 per cent rate on net profit imposed by the Mineral Royalty Act will appear high against the rates imposed interstate. However, offsetting the impact of a higher rate is a broader range of deductible operating, capital and exploration costs.

The Mineral Royalty Act allows various pre-production, exploration and development costs to be carried forward and claimed by miners as allowable deductions once production has commenced. Royalty is only imposed after prior year losses are fully absorbed. Furthermore, actual rehabilitation expenditure incurred subsequent to the cessation of mineral production may also be claimable.

The ad valorem rate equivalent will vary over the life of a mine, and a comparison of profit-based and ad valorem royalty schemes can only be reliably determined over a mine’s life or at least over a significant period of time. However, overall, the 20 per cent rate on net profit is effectively an average equivalent ad valorem rate of about 5 to 6 per cent.

The deductibility of exploration and development expenditure may be more significant for petroleum ventures. This is due to the larger scale, risk and the higher costs incurred during the early stages of a project.

It is widely considered that profit-based royalties are more equitable and efficient and do not unduly distort economic and investment decisions.1 Numerous countries have recently reviewed their royalty regimes and some are moving to profit-based royalties. Such regimes also provide greater returns where market conditions are favourable and profits increase.1 See, for example, Hogan, L and McCallum R, 2010 ‘Non-renewable resource taxation in Australia’, ABARE Report, Canberra, and the references cited therein. The report is available at http://taxreview.treasury.gov.au/content/html/commissioned_work/downloads/hogan_and_mccallum.pdf. A copy can also be obtained by contacting the Revenue Policy Division on (08) 8999 5453 or [email protected].

9

Discussion Paper – Petroleum Royalty Reforms

This avoids the situation encountered recently in other states, where the value based royalty rates have been increased to provide a better return to government. Unfortunately, these increases have generally occurred after the periods of high profitability enjoyed by miners or petroleum producers and now directly affect investment decisions when market conditions are less favourable.

Profit-based royalties only become payable when there is a greater capacity to pay, as the project is profitable, and do not deter marginal projects that would otherwise be uneconomic under the current wellhead value petroleum royalty regime. Table 1 compares the royalty regimes under the Mineral Royalty Act and Petroleum Act.

In comparison, the current wellhead value petroleum royalty regime is imposed as soon as production commences, regardless of whether a project is profitable. Charging royalty without having regard to a producer’s ability to pay acts as a disincentive when potential producers are making decisions regarding when and where to invest. For example, marginal projects may be profitable and economically feasible prior to the application of a value-based royalty but may no longer be so after the royalty is imposed.

In addition to increasing the Territory’s competitiveness against other jurisdictions seeking to attract investors to their respective oil and gas sectors, a neutral and consistent royalty regime with respect to all resources promotes economic efficiency by ensuring that available capital and labour is allocated to the most productive areas of the economy.

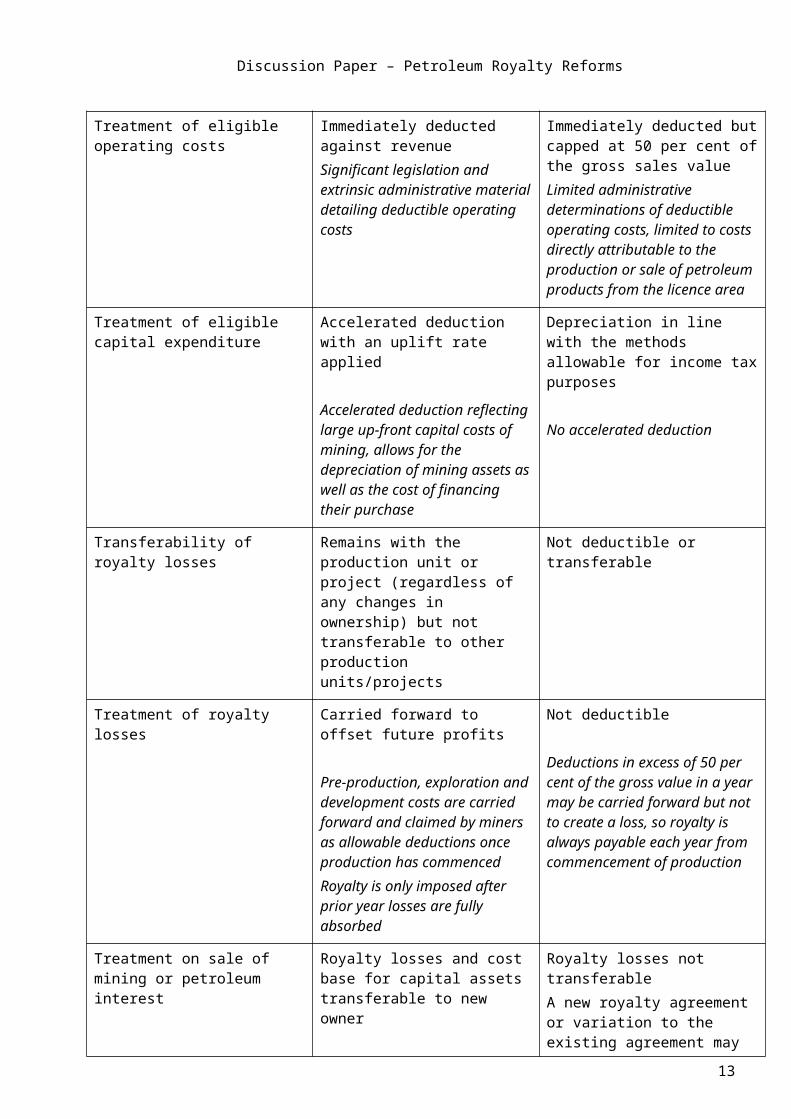

Table 1: Comparison of the Mineral Royalty Act and Petroleum Act

Key Feature Mineral Royalty Act Petroleum Act

Basis of royalty Project-based royalty Project-based royalty

Royalty rate 20 per cent* 10 per cent*

Rate calculation basis Gross sales value less deductible expenditure, capital allowance and carry forward losses

Significant legislation and extrinsic administrative material to support the calculation of royalty

Gross value at the wellhead

Uncertainty as to calculation of gross royalty due to the lack of direct sales of petroleum at well headDependent upon agreements and ad hoc administrative decisions

Deductions Certain exploration, pre-production, production, rehabilitation and capital costs

Better reflects life of mine costs including pre-productionBetter aligns royalty payments with profitability of the mine

Certain post-wellhead field gathering, processing, storage, sales and marketing costs up to the first point of sale where a net-back method is used

Results in quasi net value approach under an ad valorem regime and requires payments of royalty from commencement of production

Key Feature (Continued) Mineral Royalty Act Petroleum Act

Treatment of eligible operating costs

Immediately deducted against Immediately deducted but capped at 50 per cent of the

10

Discussion Paper – Petroleum Royalty Reforms

revenueSignificant legislation and extrinsic administrative material detailing deductible operating costs

gross sales valueLimited administrative determinations of deductible operating costs, limited to costs directly attributable to the production or sale of petroleum products from the licence area

Treatment of eligible capital expenditure

Accelerated deduction with an uplift rate applied

Accelerated deduction reflecting large up-front capital costs of mining, allows for the depreciation of mining assets as well as the cost of financing their purchase

Depreciation in line with the methods allowable for income tax purposes

No accelerated deduction

Transferability of royalty losses Remains with the production unit or project (regardless of any changes in ownership) but not transferable to other production units/projects

Not deductible or transferable

Treatment of royalty losses Carried forward to offset future profits

Pre-production, exploration and development costs are carried forward and claimed by miners as allowable deductions once production has commencedRoyalty is only imposed after prior year losses are fully absorbed

Not deductible

Deductions in excess of 50 per cent of the gross value in a year may be carried forward but not to create a loss, so royalty is always payable each year from commencement of production

Treatment on sale of mining or petroleum interest

Royalty losses and cost base for capital assets transferable to new owner

Makes buy-outs and industry consolidation more attractive, allows economies of scale purchases

Royalty losses not transferableA new royalty agreement or variation to the existing agreement may need to be negotiated

* After deductions, both regimes are effectively equivalent to a true ad valorem rate of about 5 to 6 per cent (on net value of minerals or actual petroleum sales at first point of sale) over the life of a project.

Key Directions

11

Discussion Paper – Petroleum Royalty Reforms

There appear to be two main practical legislative options to reforming the Territory’s petroleum royalty regime. The options are:

Option 1

Option 1 would require all new petroleum projects, and existing producers who elect to opt-in, be subject to a profit-based royalty regime. This would involve the following main features:

adopting the substantive concepts, definitions and comprehensive administrative provisions in the Mineral Royalty Act.

royalty guidelines issued by the Mineral Royalty Secretary being modified to assist petroleum royalty payers in understanding and meeting their royalty obligations.

a 20 per cent royalty rate on the net value of production, which equates to an average ad valorem rate of about 5 to 6 per cent.

greater deductibility of certain exploration, pre-production and production costs and an accelerated deduction of uplifted capital costs.

losses can be carried forward and accumulated until offset against profits.

The benefits of Option 1 are that the reforms would:

establish a consistent regime for the Territory’s mineral and petroleum resources.

provide greater certainty through a more comprehensive, robust and transparent administrative and substantive framework for the Territory’s petroleum royalty regime, thereby avoiding the need for lengthy negotiations on establishing an agreement for each new project.

recognise the significant costs of new petroleum ventures by allowing the carry forward and deduction of a greater range of costs in future years.

be more equitable in terms of having closer regard to a petroleum producer’s ability to pay by only imposing royalty on profitable ventures with stronger growth in royalty revenues in times of high petroleum prices.

increase the integrity of the petroleum royalty base and minimise possible royalty avoidance such as through transfer pricing.

address royalty issues in relation to unconventional gas.

Option 2

Option 2 would limit reforms to inserting comprehensive administrative provisions in the existing Petroleum Act or Petroleum Regulations.

Option 2 would involve the following main features:

12

Discussion Paper – Petroleum Royalty Reforms

the retention of the current ad valorem royalty rate of 10 per cent of gross value at the wellhead.

adopting comprehensive administrative provisions into the petroleum legislation.

the retention of existing agreement or determination based arrangements for each petroleum project.

developing petroleum royalty guidelines where required.

continued application of the principles set out in the Petroleum Royalty Overview for the calculation of petroleum royalty.

multiple royalty schemes for a mine producing minerals and petroleum.

The benefits of Option 2 are that the reforms would:

provide greater certainty through a more comprehensive, robust and transparent administrative framework for the Territory’s petroleum royalty regime, thereby reducing the length of negotiations on establishing an agreement for each new project.

increase the integrity of the petroleum royalty base but not to the extent of Option 1.

13

Appendix

NORTHERN TERRITORY PETROLEUM ROYALTY OVERVIEW

Purpose

1. This Overview outlines the administrative arrangements relating to the establishment, calculation and collection of royalties under the Petroleum Act 1984 (NT) (the Act).

2. This Overview is for general guidance purposes only.

Introduction

3. Royalties are payments made to the Northern Territory Government (the Territory), as the owner of the petroleum, in consideration of a right granted to extract and remove petroleum and are calculated at the rate of 10 per cent of gross value at the wellhead on petroleum production. They are not a tax.

4. Royalties are collected under the Act.

5. The Territory’s royalty regime encourages present and future exploration and development of petroleum resources. At the same time, it compensates the Northern Territory community for allowing the private extraction of the Northern Territory’s non-renewable resources.

6. The Department of Mines and Energy issues titles under Territory petroleum legislation for the right to produce petroleum within the territorial boundary of the Northern Territory (including coastal waters). When titleholders (commonly known as licence holders or licensees) obtain a title, they undertake to pay royalties. This Overview outlines the royalty requirements and sets out the obligations of the licensees in this regard.

7. The payment of royalties is governed by Division 5 of Part III of the Act,2 coupled with a legally enforceable written agreement between a licensee and the Treasurer (as the responsible Minister for administering the royalty provisions of the Act) on behalf of the Territory or, in the absence of a legally enforceable agreement, a binding determination made by the Treasurer. A failure to pay royalties can result in cancellation of a retention licence or production licence.

8.

8. The annual royalty return required to be lodged provides the Commissioner of Territory Revenue with information to enable calculation of the royalty, including the gross value of the petroleum and any applicable allowable deductions.

Substances subject to the Act

9. Subject to the terms of the Act, royalties are payable on all petroleum (in the sense described in the Act) except for a substance which, in its naturally occurring state, is not recoverable from a well by conventional means.

10. “Petroleum” is defined as:

2 Section 119(2) of the Petroleum Act (being a transitional or savings provision) expressly ensures that Division 5 of Part III of the Petroleum Act applies to a lease granted or renewed under the now repealed Petroleum (Prospecting and Mining) Act 1954 (NT) which is continued in force (as if the law remained the same as it was at the time immediately before the Petroleum Act commenced operation on 15 October 1984).

(i) any naturally occurring hydrocarbon, whether in gaseous, liquid or solid state;

(ii) any naturally occurring mixture of hydrocarbons, whether in gaseous, liquid or solid state;

(iii) any naturally occurring mixture of one or more hydrocarbons, whether in gaseous, liquid or solid state, and one or more of the following: hydrogen-sulphide, nitrogen, helium and carbon dioxide or any combination thereof; and

(iv) any petroleum as defined in (i), (ii) or (iii) that has been returned to a natural reservoir.

Royalties

11. Royalties on petroleum within the scope of the Act are charged on an ad valorem basis (not a profit-based or net value approach) which is applied to the recovery of all petroleum within the boundary of the geographical area of the Northern Territory (including coastal waters) that is subject to a retention licence or production licence (described as the “licence area” in the Act).

12. The inherent nature of the Territory’s petroleum royalty scheme is that petroleum products (“petroleum”) have a value at the wellhead and that a royalty will always be payable on petroleum production under the ad valorem scheme.

13. Under the Act, royalty applies to petroleum derived from the licence area. Ring-fencing principles apply and each of the licensee’s operations are treated independently, for royalty purposes, from all of the licensee’s other operations (including operations on distinct and separate licence areas). Accordingly, the accounts from the individual field or project the subject of a retention licence or production licence may not be mixed with the accounts for activities outside the field or project. There is no ability to aggregate income or revenue and expenses from all operations carried on by the licensee within the Northern Territory.

14. The licensee(s) is/are the royalty payer for the purposes of the Act. Accordingly, the licensee is responsible for the lodgement of royalty returns and payment of royalties.

Ad valorem royalty15. The imposition and assessment of royalty on petroleum recovered in the Northern Territory is

governed by the Act coupled with a legally enforceable written agreement or, in the absence of a legally enforceable agreement, a binding determination made by the Treasurer.

16. Under section 84 of the Act, royalty is payable to the Territory and liability for royalty is a joint and several liability of the licensee(s).

17. Under section 84, the royalty rate is 10 per cent of gross value at the wellhead.3 The term “wellhead” has a well-established common business usage or practice in the Australian (and, indeed the world) petroleum recovery industry.4 The term refers to the top of the well casing and/or equipment at the top of the well casing, including outlets and values, designed to control the production of petroleum (commonly known in the industry as the “Christmas tree” being an assembly of valves mounted on the casing head through which petroleum is produced. The Christmas tree also contains valves for testing the well and for shutting it down if necessary).

18. The point at which a licensee is required to bring to account the gross value of the petroleum for the purposes of calculating the royalty in respect of, or determining the consequent royalty implications arising from the recovery of the petroleum from, the relevant area of the retention licence or production licence is fixed by the terms of section 84(1) of the Act (see also section 84(5) of the Act). The precise time at which the gross value of the petroleum has

3 There is provision to reduce the royalty in exceptional circumstances such as if the production becomes uneconomic at the fixed rate (section 86).4 See BHP Petroleum Pty Ltd v Balfour (Unreported, Supreme Court of Victoria, Marks J, 8 February 1985); BHP Petroleum Pty Ltd v Balfour (1994) 180 CLR 474; Schroeder v Terra Energy Ltd 565 N.W.2d 887,890 (Mich. App. 1997).

15

to be determined is at the wellhead (see also sections 5(1) (definition of “well”) and 6(2) of the Act).

19. For the purposes of calculating the amount of royalty payable, petroleum is deemed not to have been produced in the period to which the royalty calculation relates if, during that period, that petroleum is unavoidably lost, returned to the natural reservoir, flared or vented in accordance with good oilfield practice or used by the licensee for the purposes of approved mining operations or any incidental purposes (including the heating and lighting of the dwellings of employees engaged by the licensee in connection with the work of production and the heating and lighting of buildings maintained to provide social amenities for those employees, workers and their families).

Methods for determining gross value

20. There are generally three methods used to determine “gross value at the wellhead”. First, the most desirable method is to refer to the actual arm’s length sales to unrelated parties of the petroleum at the wellhead. The second method, used only when there is no actual sales of petroleum at the wellhead, is comparable sales (i.e. sales comparable in time, quality, quantity and availability of market outlets). The third method, used only when actual sales or comparable sales are not available, is the net-back or work-back method;5 i.e. subject to one qualification or limitation (refer to paragraph 26), the subtraction of reasonable post-wellhead costs from the actual sales price/market value (i.e. the arm’s length price achieved or achievable between unrelated parties) at the first point of sale.

21. Where there is no sale of petroleum at the wellhead or comparable sales, to enhance administrative simplicity and to negate or minimise the potential for difficulties and uncertainties in valuing the petroleum at that precise point of time, a general practice has been adopted to determine the gross value of the recovered petroleum by taking the value at the point where the value of the petroleum can be independently established (this is generally the first point of sale) and deducting from this value, post-wellhead costs directly attributable to the production of petroleum from the licence area.

22. Depending on the specific circumstances, an alternative method or formula (other than the methodologies stated above), the application of which results in an amount that fairly reflects the gross value concept and simplifies royalty calculations, may also be considered.

23. To allow for an alternative method to be considered as part of the agreement process, a written application or claim should be made to the Commissioner of Territory Revenue setting out a statement of reasons to establish and substantiate to the Commissioner that the alternative method accurately represents the gross value of the petroleum produced (or to be produced) from a licence area. The reasons should be sufficiently explicit to identify and direct the Commissioner’s attention to the particular aspects upon which it is contended that the amount should be determined as the gross value of petroleum for the purposes of the Act.

24. In circumstances where the sale or transaction involves a transfer pricing arrangement between related parties, the licensee must establish and substantiate an alternate value for petroleum royalty purposes. Generally, the alternate value should be determined in conformity with the concepts, principles and rules identified and described in the Mineral Royalty Act 1982 (NT).

25. The Commissioner of Territory Revenue considers parties to be related where they are “related bodies corporate”, as defined in section 50 of the Corporations Act 2001 (Cth). This includes companies in a parent/subsidiary relationship and subsidiaries of the same parent company.

5 The authorities of Oil Basins Limited v BHP Petroleum Pty Limited [1988] VicSC 247 and Australian Energy Limited v Lennard Oil NL (Unreported, QSC, MacPherson J, 6 February 1985); [1986] 2 Qd R 216 support that it is appropriate to ascertain the wellhead gross value by using the net-back approach; i.e. it is an appropriate method of deducing from actual downstream sales the gross value at the point of production upstream of those actual sales (see also Bob Jane T-Marts Pty Ltd v Commissioner of Taxation [1999] FCA 415 at [92]-[93]; Howell v Texaco Inc 112 P.3d 1154, 1159 (Okla. 2004); Ramming v Natural Gas Pipeline Company of America 390 F.3d 366, 372 (5th, Cir. 2004)).

16

Deductible post-wellhead costs under a net-back method

26. As the royalties on petroleum within the scope of the Act are charged on an ad valorem basis (not a profit-based or net value approach), where a net-back method is used, generally a limit on post-wellhead costs up to 50 per cent of the gross value for petroleum production will be incorporated into the written agreement or determination. Any deduction in excess of this limit may be carried forward to the next royalty period without adjustment for inflation. This limitation acknowledges the inherent nature of the petroleum royalty scheme and ensures that deductions will never exceed sales value and that the Territory will always receive a royalty on production under the ad valorem scheme.

27. While revenue and costs are calculated on a field by field basis, depending on its specific circumstances, “post-wellhead costs” are normal operating costs which are reasonable in amount and are directly attributable to the production, maintenance for the purpose of production or the marketing or sale of petroleum products from the licence area. These will generally include field gathering costs (i.e. costs of running the petroleum from the well(s) into processing facilities), processing, storage and pipeline tariffs or transportation costs (i.e. costs of transporting the petroleum to the refinery or the first point of sale).

28. Labour, office and management costs are generally deductible if the work was performed solely in the Northern Territory and was directly attributable to the petroleum operations conducted on the licence area.

29. In relation to field production assets (i.e. assets located on the licence area) used for petroleum production, deductions will generally be allowed for depreciation in conformity with the income tax treatment of the asset and any gain or loss on the sale of eligible field assets will be included as part of the allowable deduction calculation.

Non-deductible costs under a net-back method

30. The concept or notion of “gross value” clearly prohibits the deduction of pre-wellhead costs such as exploration costs (i.e. costs incurred in exploring and prospecting for petroleum and outlays on plant and other items of capital equipment required to develop petroleum from a well), lifting costs (being the costs of bringing petroleum to the surface), reservoir maintenance costs and overhead costs relating to pre-wellhead activities.

31. Where a field or project ceases production as a result of a permanent shut down or a field or project ceases production and its operation is placed in care and maintenance for an indefinite period (as a result of a temporary shut down), mothballing costs (however described such as care and maintenance or abandonment costs) - even if mothballing costs may be required to maintain plant and gathering systems to facilitate the safe re-commencement of production at some future period of time - are considered not to be directly attributable to the production of petroleum from the field. Consequently, that expenditure is not eligible to be claimed as post-wellhead costs.

32. Similarly, deferred or post-production rehabilitation expenditure (i.e. expenditure incurred subsequent to the cessation of production and, accordingly, not directly attributable to the production of petroleum from the field) is not eligible to be claimed as post-wellhead costs.

33. In addition, any gains/losses from foreign exchange dealings and asset revaluation adjustments will not be recognised for royalty purposes.

Royalty agreements with the Treasurer

34. For the purposes of entering into a written agreement with the Treasurer under section 84 of the Act and to ensure that any future royalty (in relation to petroleum produced from an area that is subject to a retention licence or production licence) is correctly accounted for and paid in a timely manner, it is important that a prospective licensee notifies, and commences discussions with, the Territory Revenue Office (being the office responsible for administration and enforcement of the royalty provisions of the Act), when an application for a retention licence or a production licence is submitted to the Department of Mines and Energy.

17

35. Subject to all of the particular circumstances of the prospective field or project and the ultimate views and consent of the Treasurer, the terms of any legally enforceable written agreement between a licensee and the Treasurer will generally align with the principles set out in this Overview and may include:

(1) an appropriate or reliable net-back method or approach to determine the gross value of all the petroleum recovered at the wellhead from the actual downstream sales value of petroleum or, in the alternative, value added products such as LNG; and

(2) relevant deductible post-wellhead costs (including capital costs) directly attributable to the production of petroleum from the field or project - which are reasonable in amount (i.e. the amount expended must represent the fair and realistic value of the activities carried out).

Lodgement of royalty returns

36. Annual royalty returns are required to be lodged in circumstances where the production of petroleum has commenced. The returns are to be lodged within three months after the expiration of a royalty year or such longer period as the Commissioner of Territory Revenue permits.

37. The licensee must ensure that:

(1) information relating to its field or project is accurate and up to date; and

(2) completed and signed returns are lodged with the Commissioner of Territory Revenue covering all details set out in the return together with working papers supporting the royalty calculations.

38. For convenience, a template royalty return will shortly be made available by the Territory Revenue Office.

Records required when royalty return lodged39. To facilitate the audit and assessment process, the following is a list of some of the

information required to be submitted with the royalty return:

(1) a statement showing -

a) the quantity; and

b) gross value as determined in accordance with section 84 of the Act;

of all petroleum produced from the licence area and in respect of which royalty is payable under the Act;

(2) the licensee’s method of determining the quantity and gross value;

(3) a list of expenditure claimed (if applicable);

(4) an explanation for any increase/decrease in revenue or expenditure in comparison with the amounts declared in the previous royalty return; and

(5) any other relevant information which may facilitate the audit of the royalty return.

Audit and assessment of royalty

40. The terms of the Act coupled with the agreement or Treasurer’s determination depend upon the issuance and delivery of an assessment by the Commissioner of Territory Revenue stating the amount of royalty payable by the licensee.

41. An assessment is made of the royalty payable. A licensee’s liability for royalty is not determined until an assessment has been issued.

42. To make an assessment, an audit may be conducted to verify information disclosed in the royalty return.

18

43. The audit may be carried out on the licensee’s licence area or premises, or the licensee may be requested to provide further information to substantiate the royalty return. To facilitate the audit process, licensees need to ensure that all records requested by the Commissioner of Territory Revenue or a person appointed or authorised by the Commissioner (“authorised officer”) are submitted and available for examination in a timely manner.

44. Once the audit is completed, an assessment is issued incorporating any necessary adjustments arising from the audit.

45. The Commissioner of Territory Revenue has the ability to issue amended assessments in certain circumstances.

Authorised officer’s powers in conducting an audit46. Under the Act and the terms of an agreement, for the purposes of the administration and

enforcement, an authorised officer is permitted to, amongst other things:

(1) gain access to the licence area or premises where records are kept;

(2) inspect, examine, make and retain copies of documents or records;

(3) test a device referred to in section 84(5) of the Act and make and retain records associated with or produced by the device;

(4) require a person to produce records; and

(5) require a person to answer questions and provide information.

Your rights in respect of an audit47. In relation to the audit process you should expect:

(1) the authorised officer to be professional and courteous;

(2) the audit to be completed in a timely manner;

(3) your affairs to be treated with strict confidentiality;

(4) to be given a receipt for records or other materials the authorised officer removes from your premises;

(5) to be given an opportunity to discuss any aspect of the findings with the authorised officer;

(6) to be given the opportunity to explain the reasons for any irregularities and discrepancies; and

(7) to receive an explanation of the results or findings.

Your obligations in respect of an audit48. Throughout the audit, you are obliged to:

(1) disclose any discrepancies, errors and undeclared royalty liabilities;

(2) provide the authorised officer reasonable assistance and facilities;

(3) provide complete and honest answers and explanations to questions;

(4) provide prompt, full and free access to all relevant information, records, documents, data and systems as required; and

(5) ensure accounting records and books of accounts are properly kept and complete.

Payment of royalty

49. Provisional royalty payments are generally made monthly. However, further payments may be made at the end of the royalty year.

50. Payment of royalty is generally required to be made:

19

(1) in the case of monthly provisional payments (which are to be accompanied by a statement), not later than 15 days after the commencement of each month;

(2) in the case of a residual payment (i.e. the difference between the sum of the monthly payments and the total amount calculated as payable in the royalty return) for a royalty year, at the same time the royalty return is lodged, which must be within three months of the end of the royalty year; and

(3) in the case of any shortfall between royalty assessed in an assessment and the sum of the monthly provisional payments and residual payment, on the date specified in the notice of assessment (generally within 30 days of the issue of the assessment).

Unpaid royalties and interest charges51. Royalties not paid by the due date incur an interest charge. The interest rate is fixed at

0.33 per cent per day.

52. Interest charges apply in all cases upon the amount of royalty from time to time remaining unpaid, to be computed from the time such royalty became payable until it is paid. In exceptional circumstances, some or all of the interest may be remitted.

Record keeping requirements

53. Licensees are required to maintain proper and accurate records relating to petroleum recovered and which substantiate details contained in royalty returns. The records are to be kept at the licence area or at some other place in Australia as agreed between the licensee and the Commissioner of Territory Revenue.

54. The Commissioner of Territory Revenue or any authorised officer is to have access to accounts, books, documents and other records relating to the field or project.

Confidentiality

55. Information collected by the Commissioner of Territory Revenue or any authorised officer for the purposes of royalty is used only for the purpose of administering and enforcing the royalty provisions of the Act.

56. The confidentiality of this information is strictly maintained and any disclosure will only be made if consistent with the confidentiality requirements, or when required or authorised by law.

Grant ParsonsCommissioner of Territory Revenue

Date of Issue: 3 March 2014

For further information please contact the Territory Revenue Office:

GPO Box 154Darwin NT 0801Email: [email protected]

Phone: 1300 305 353Fax: 08 8999 5577Website: www.revenue.nt.gov.au

20