Embed Size (px)

Citation preview

1

Northern California | 2012

Mike Kamm, CEO Cassidy Turley

Northern California

Introduction

Discover The State of Real Estate / 2012

Cassidy Turley

3,400 professionals

940 agents

60 US offices

455M SF under management on behalf of corporate, institutional

and private investors

25,000

corporate services locations

Discover The State of Real Estate / 2012

High Profile Hires

Discover The State of Real Estate / 2012

High Profile Hires

Discover The State of Real Estate / 2012

Santana Row Move

Kevin Thorpe Chief Economist

Cassidy Turley

Featured Speaker

Discover The State of Real Estate / 2012

World GDP Grows by 4.1% in 2012

Canada

Brazil

UK

Eurozone

Russia

India

China

Japan

GDP, 2012, Year-over-year % change

Source: IMF, The Economist

Mexico

2.5%

3.6%

1.7%

3.8%

3.6%

9.1%

2.1%

7.5%

-0.3%

Discover The State of Real Estate / 2012

U.S. Bank Exposure to Euro-zone

% of Tier 1 Capital

0

10

20

30

40

50

60

70

80

90

Portugal,Ireland,Italy Greece,Spain

All Claims(Entire Eurozone)

16.8%

76.7%

Private

Public

Banks

Source: Capital Economic, BIS

Exposure to Peripheral

Countries

Exposure to entire

Euro-zone

Discover The State of Real Estate / 2012

Source: CBO, Moody’s

Total of $4 trillion needed for long-run sustainability, 2012-2021

The Budget Control Act of 2011

Discover The State of Real Estate / 2012

DJIA Predicts Presidency When DJIA is up, Incumbent wins 100% of the time

Source: Bloomberg

Harry S.

Truman

1945

Dwight D. Eisenhower

1953

Ronald Regan

1983

Bill Clinton

1995

George W. Bush

2003

FDR

1936

FDR

1940

Discover The State of Real Estate / 2012

Historical Average

Still Deleveraging Household Debt-to-GDP

Source: Federal Reserve Board

Discover The State of Real Estate / 2012

Source: U.S. Census Bureau

Slow Recovery Continues…

Real GDP, % Chg

Potential GDP = 2.7%

Discover The State of Real Estate / 2012

Unemployment will stay high, but…

Source: BLS

Discover The State of Real Estate / 2012

Multifamily Hotel

Retail

Industrial

Office

Downturn Recovery Upturn Mature Downturn Weak demand

Vacancy not falling

Improving Demand

Falling Vacancy

Strong Demand

Tight Vacancy

Historic, demand,

vacancy, rents

Absorption Q1 – Q3 2011

Vacancy

YoY Chg

Rents Yoy

Chg

Sales

Yoy %Chg

Office +38.1 M -90 bps +$0.18 +57.1%

Industrial +71.6 M -50 bps -$0.07 +76.2%

Retail +247 K +10 bps -$0.06 +108.1%

Multifamily +122.7 units -170 bps +$21.00 +57.3%

CRE Fundamentals Improving

Discover The State of Real Estate / 2012 16

When will we reach normalcy?

Source: Cassidy Turley Research

Absorption vs. Available Office Space

49.5 M SF Historical Absorption

0

200

400

600

800

1000

1200

2011 2012 2013 2014 2015

Mil

lio

ns, s.f

.

Empty Office Space Equilibrium

Discover The State of Real Estate / 2012

NABE’s Consensus Forecast Annual Forecasts made in November 2011

2011 Forecast 2012 Forecast

Median Five

Lowest

Five

Highest Median

Five

Lowest

Five

Highest

Real GDP, % change, Q4/Q4 1.7 1.2 2.0 2.4 0.9 3.8

CPI, % change, Q4/Q4 3.4 1.3 3.9 2.0 0.7 3.9

Personal Consumption Expenditures

Price Index less food energy, % chg,

Q4/Q4

1.9 1.4 2.3 1.8 0.9 2.8

Civilian Unemployment Rate, % annual

average 9.0 9.0 9.1 8.9 8.1 9.5

Federal Funds Target, % year-end 0.125 0.103 0.126 0.125 0.103 0.341

10-Yr Treasury Note Yield, % year-end 2.73 2.15 3.53 2.70 2.18 4.03

Foreign Exchange Rate, US$ per Euro,

December Average 1.37 1.22 1.43 1.37 1.11 1.47

Housing Starts, millions of units 0.60 0.57 0.74 0.66 0.60 0.96

Home Prices, FHFA, % change, Q4/Q4 -2.5 -6.2 1.8 0.9 -3.6 4.8

Oil Prices, $ per barrel, December

Average 92.0 78.7 97.0 94.8 79.6 110.6

S&P 500 Index, December 31 1294.4 1178.0 1391.2 1380.0 1202.6 1604.8

“While we still expect that economic

activity and labor market conditions

will improve gradually over time, the

pace of progress is likely to be

frustratingly slow.”

-Chairman Bernanke

"If the economy is growing only 1.5

percent to 2 percent and you get a

fiscal drag of 1.3 percent — that's

the difference between a growth

recession and effectively zero

growth.”

-Nouriel Roubini, NYU

"The economy is struggling to avoid

recession…There are a number of

things coming together with regards

to fiscal policy that makes early next

year look very iffy .”

-Mark Zandi, Moody’s Analytics

Discover The State of Real Estate / 2012 18

Reasons for optimism

Source: Federal Reserve Board

Historical Avg: 12.1

HH debt is affordable debt

Discover The State of Real Estate / 2012

Consumer Confidence Index

Gas prices

spike $4

Disaster in

Japan

Debt ceiling

debate begins

S&P

Downgrade

US GDP nearly

contracts in Q1 European Debt

Crisis Worsens

Couldn’t catch a break in 2011

Source: The Conference Board, Cassidy Turley Research

Discover The State of Real Estate / 2012

Reasons for optimism Corporate Profits, $ tril

• Corporate profits up

• Job growth hits 200k

• Auto sales rebounding

• Confidence is rebounding

• Exports strong

• ISM Index back up

Source: Census Bureau, Cassidy Turley

Discover The State of Real Estate / 2012

Source: Moody’s

10-Yr Sovereign Debt Yields, %

What to Watch: Italian Bonds

Discover The State of Real Estate / 2012

What to Watch: Copper

Source: DOW Jones AIG, NSA

Copper Prices

Discover The State of Real Estate / 2012

Northern California

Includes four major metros:

• San Jose-Sunnyvale-Santa Clara

• San Francisco-San Mateo-Redwood city

• Oakland-Fremont-Hayward

• Sacramento Arden-Arcade-Roseville

Discover The State of Real Estate / 2012

Northern California

Midwest Economy • GDP $2.4 Trillion • Total Employment 29,778,000 • Unemployment Rate 8.8%

Economic Snapshot

• Total Employment

3.6 million

• GDP

$477.5 Billion

• Population

8.4 million

• Unemployment Rate:

9.8% Job Sectors

Discover The State of Real Estate / 2012

Northern California Employment

Source: Bureau of Labor Statistics

Is 2011 the first year of the

next tech boom?

Discover The State of Real Estate / 2012

-1,700

-1,000

1,200

2,700

5,100

5,400

6,600

17,100

18,000

-5,000 0 5,000 10,000 15,000 20,000

Government

Financial Activities

Other Service

Information

Leisure and Hospitality

Trade, Transportation and Utilities

Goods-Producing

Educational and Health Services

Prof. & Bus. Services

Employment Growth/Decline by Industry Northern California, Nov 2011 vs. Year-ago

Source: Bureau of Labor Statistics

Discover The State of Real Estate / 2012

Job Growth in NorCal Markets

Y/Y Percent Change: Nov 11 over Nov 10

Source: Bureau of Labor Statistics

+28,400 jobs

+14,800 jobs

+7,200 jobs

+3,000 jobs

Discover The State of Real Estate / 2012

-4

-3

-2

-1

0

1

2

3

4

5N

ew

Yo

rk, N

Y

Se

att

le, W

A

Ho

us

ton

, TX

Da

lla

s, T

X

Sa

n J

os

e-S

ilic

on

Va

lle

y

Sa

n F

ran

cis

co

, C

A

Au

sti

n,

TX

Ph

ila

de

lph

ia, P

A

Sa

n M

ate

o C

ou

nty

, C

A

Wa

sh

ing

ton

DC

Oa

kla

nd

-Ea

st

Ba

y, C

A

Sa

cra

me

nto

, CA

Cle

ve

lan

d, O

H

Sa

int

Lo

uis

, M

O

Ve

ntu

ra C

ou

nty

, C

A

Po

rtla

nd

, M

E

Ind

ian

ap

olis

, IN

We

stc

he

ste

r, N

Y

Lo

s A

ng

ele

s,

CA

Ch

ica

go

, IL

Mil

lio

ns, s

.f.

Office Sector: Net Absorption 2011

NorCal all over the Top 10

Source: Cassidy Turley Research

Discover The State of Real Estate / 2012

Is this tech boom sustainable?

This time it’s different

• Real businesses with real products

• More global – 2 billion internet users

today

• Huge growth potential in China &

other emerging economies

• 77% of the world has a cell –

5.3b of repeat demand

• NASDAQ not outpacing DJIA like it did

in the 90s

Late 90s all over again

• Too frothy

• Tech salaries growing too fast

• Venture capitalists have no where

else to put their money

• Fledging firms commanding huge

IPOs again

• Investors still don’t get technology

Discover The State of Real Estate / 2012

36,500

78,500

106,450

84000

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

2012 2013 2014 2015

0

20,000

40,000

60,000

80,000

100,000

120,000

Cassidy Turley

Moody's

Average

Source: Moody’s, Cassidy Turley

Northern California Job Growth Forecast

Strong Years Lie Ahead

Discover The State of Real Estate / 2012

Employment Forecast

Market 2012 2013 2014 2015

Oakland-East Bay 9.3 16.5 19.1 15.8

Sacramento 5.4 14.0 17.4 14.9

San Jose 12.6 15.7 18.9 15.8

San Francisco 12.6 19.8 22.6 18.5

Northern

California 40.0 66.0 78.9 65.0

Northern California, 000’s

Source: Cassidy Turley

Discover The State of Real Estate / 2012

Tech drove the bus in 2011

Top Office/R&D Leases in 2011

Tenant RSF Tenant RSF Tenant RSFFacebook, Inc. 1,029,000 Affymetrix, Inc. 201,052 Zynga 117,280

Google, Inc. 700,328 Atmel 194,000 Siemens 114,583

Sony 456,795 Dreamworks 193,000 Cavium Networks 113,381

Hewlett Packard 393,776 Wilson, Sonsini, etal 184,000 Healthnet 113,078

Linkedin, Inc 393,195 Jabil Circuits 181,656 Cepheid 110,217

Google, Inc. 387,939 Micro Semi Corp. 179,232 Abbott Labs 110,000

Apple, Inc. 377,927 TeleNav, Inc 175,000 Magma Design 109,450

Synopsys, Inc. 340,000 Intevac 169,795 Apple, Inc. 108,712

Motorola Mobility 317,166 Theranos 137,000 Covington & Burling 108,315

Hitachi 300,000 Symantec Corporation 136,377 Pillsbury, Winthrop, Shaw 107,447

Logitech, Inc. 263,543 Google, Inc. 135,656 Avid Technology 106,460

University Of The Pacific 260,843 SAP America, Inc. 135,080 Riverbed Technology 103,985

Avaya 257,155 Bristol-Myers Squibb 133,123 C8 Medisensors 102,114

Dell Computers 240,823 Flextronics 130,455 Perfect World 100,000

Microsoft Corporation 237,121 Celestica 128,250 Omnicell 99,880

Apple, Inc. 215,481 Silicon Image 128,154 NVIDIA 99,800

PolyCom, Inc. 212,863 Farella, Braun, & Martel 121,000 Microchip Technology/SST 98,423

Intuit 210,000 Biomarin Pharmaceutical 120,338 Guidewire 97,674

Twitter 205,903 Zazzle 119,730 Keker & Van Nest, LLP. 97,034

NanoSolar 203,807 Sun Edison 118,741 Qualcomm Inc. 96,780

Discover The State of Real Estate / 2012

Tech drove the bus in 2011

Top Office/R&D Leases in 2011

Tenant RSF Tenant RSF Tenant RSFBox.Net 96,562 NetSuite 79,589 C3 68,409

Sephora 91,666 Capital Region Financial 77,748 American Medical Systems 68,366

Apple, Inc. 91,195 Ebay, Inc. 75,432 Juniper Networks, Inc. 68,000

ST Microelectronics, Inc. 91,008 Huawei Technologies 75,000 Phillips 67,000

Sedgwick,Detert, etal 89,076 Siemens 75,000 Santa Clara Cty Valley Trans. 67,000

Ironport 88,412 Tellabs 74,453 Symantec Corp. 67,000

DropBox 87,500 AAA 73,696 Codexis Inc. 66,080

NXP Semiconductor USA 86,602 Sungevity 73,100 National Instruments 66,000

Ariba 86,000 Micron Technologies 72,486 Google, Inc. 65,856

Altierre Corp. 85,637 Enphase 72,000 Farallon Capital Mgmt 65,553

Evalve 84,643 Loral Space Systems 71,972 First Republic Bank 65,506

Quantum Corporation 83,877 Verizon 71,484 Pharmacyclics, Inc. 64,776

KPMG 82,771 Fluor 70,047 Ubiquiti Networks 64,512

Northrup Grumman 82,574 Epicor Software 70,000 Geometrics, Inc. 64,100

24 Hour Fitness 81,500 Pac-12 70,000 Dolby Laboratories 63,379

Comerica Bank 81,213 Intematix Corporation 69,752 Pisces Inc. 63,000

Goodby, Silverstein etal 81,065 Innovative Molding 69,000 Huawei Technologies 62,522

Financial Engines, Inc 80,995 SeaMicro 68,608 EBay 62,281

Good Technology Inc. 80,302 Sonic Mfg Technologies 68,600 Triple Ring Technologies 62,020

A-10 Networks 79,803 NovaSolar 68,441 Solution Set 61,980

Discover The State of Real Estate / 2012

Tech drove the bus in 2011

Top Office/R&D Leases in 2011

Tenant RSF Tenant RSFKovio 61,656 Cable Connection 55,138

MediaTek 61,518 Supracor, Inc. 55,124

Taleo Corp 61,089 Aecom Technology Corp 55,000

Stanford 61,081 Catholic Healthcare 55,000

Williams Sonoma 60,000 Palo Alto Medical Found. 55,000

Google, Inc. 59,617 Ascentool, Inc. 54,440

Apple, Inc. 59,075 AT&T 53,284

Apple, Inc. 58,979 Coverity 53,025

Zynga 58,728 Apple, Inc. 52,661

Responsys 58,388 Neuropace 52,528

Fish & Richardson 58,260 Gilead Sciences 52,416

Actuate 58,069 Nitinol Devices 52,200

Reel Solar 57,850 Goodby, Silverstein etal 51,931

MediVation 57,172 BioNovo 51,472

LinkedIn 57,120 Aptimus 51,429

Kabam 57,096 Zurich American Insurance 51,115

Wells Fargo Insurance 57,081 NIKU 51,063

Netflix 56,698 RIM 50,478

Finisar Corporation 56,156 Model N 50,473

John Wiley And Sons 55,770 Apple, Inc. 50,159

Discover The State of Real Estate / 2012

Rents surge…driven by tech

16%17%

-5% 0% 5% 10% 15% 20%

Sacramento, CA Phoenix, AZ

Oakland-East Bay, CASan Diego, CA Baltimore, MD

Atlanta, GA Dallas, TX

San Jose-Silicon Valley, CAUnited States

Denver, COWashington DC

Suburban VABoston-Cambridge, MA

Saint Louis, MONew York, NY

San Francisco, CA San Mateo County, CA

Office Rents, 2011 vs. 2010 % chg

Discover The State of Real Estate / 2012

Bay Area Office Market

Market Vacancy

Q4-10

Vacancy

Q4-11

Net

Absorption

Average

Asking

Rate

Rent YOY

%Change

Marin County 20.3% 13.7% 638K $2.46 1%

San Francisco 14.5% 11.0% 2.9M $3.18 16%

San Mateo County 16.7% 13.2% 1.1M $3.16 17%

Santa Clara County 18.2% 14.1% 2.5M $2.53 -3%

East Bay 17.0% 17.1% -152K $1.96 -4%

Bay Area Total 16.5% 13.8% 7.0M $2.59 5%

Full Service

Rates

Discover The State of Real Estate / 2012

Bay Area R&D Market

Market Vacancy

Q4-10

Vacancy

Q4-11

Net

Absorption

Average

Asking

Rate

Rent YOY

%Change

San Mateo County 14.5% 12.1% 474K $2.14 -3%

East Bay 23.5% 21.1% 780K $0.79 -9%

Santa Clara County 17.6% 14.6% 3.3M $1.24 15%

Bay Area Total 18.3% 15.4% 4.5M $1.20 7%

NNN Rates

Discover The State of Real Estate / 2012

Bay Area Warehouse Market

Market Vacancy

Q4-10

Vacancy

Q4-11

Net

Absorption

Average

Asking

Rate

Rent YOY

%Change

San Francisco 5.1% 5.1% 2K $0.75 -8%

San Mateo County 10.4% 10.0% 142K $0.72 -1%

East Bay 10.0% 9.9% 244K $0.37 2%

Santa Clara County 9.3% 9.1% -3K $0.44 -1%

Bay Area Total 9.3% 9.2% 384K $0.49 -2%

NNN Rates

Discover The State of Real Estate / 2012

Bay Area Retail Market

Shopping

Centers* Vacancy

Q4-10

Vacancy

Q4-11

Net

Absorption

Average

Asking

Rate

Rent YOY

%Change

San Francisco 7.1% 5.7% 51K $3.03 -7%

San Mateo County 3.4% 2.9% 106K $2.21 0%

East Bay 7.6% 6.5% 728K $1.74 -2%

North Bay 5.7% 4.7% 181K $1.67 -3%

Santa Clara County 7.2% 6.7% 346K $2.08 -6%

Bay Area Total 6.8% 5.9% 1.4 M $1.89 -5%

NNN Rates *Excluding Malls

Discover The State of Real Estate / 2012

Bay Area Office Net Absorption

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

Q1-1

0

Q2-1

0

Q3-1

0

Q4-1

0

Q1-1

1

Q2-1

1

Q3-1

1

Q4-1

1

Mil

lio

ns, s

.f.

Discover The State of Real Estate / 2012

Panelists

Office

Mike Moran Managing Partner

R&D

Erik Hallgrimson Partner

Industrial

Jeff Starkovich Managing Partner

Retail

Matt Kircher Managing Partner

Investments

Bob Gilley Managing Director

Discover The State of Real Estate / 2012

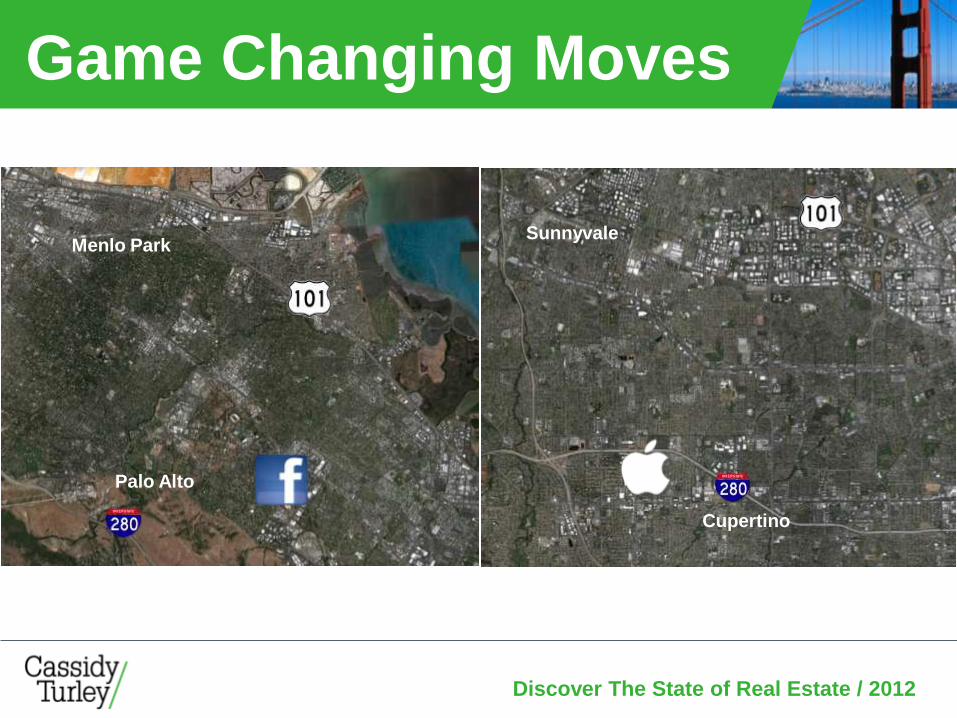

Game Changing Moves

Mountain View

Sunnyvale

Palo Alto

Menlo Park

Cupertino

Sunnyvale

Discover The State of Real Estate / 2012

Game Changing Moves

Mountain View

Sunnyvale

SoMa

Mid-Market

Discover The State of Real Estate / 2012

Pre-1996

±250SF/Employee

Circa 2007

±200SF/Employee

Circa 2011

±150SF/Employee

The Evolution of the Work Space

Discover The State of Real Estate / 2012

Everything has Changed Key Bay Area Industries/Companies

MEDIA

• Craigslist

• Wikipedia

• IDC

• Blogger

• Future Networks

• World Press

FINANCIAL

• Franklin

• Visa

• E-Trade

• Intuit

• Schwab

• Barclays

• JP Morgan

LEGAL

• Tech Legal

• Intellectual Capital

• IP Practice

• Patent Specialties

• IPO

• M&A Practice

Discover The State of Real Estate / 2012

Everything has Changed Key Bay Area Industries/Companies

TECHNOLOGY

• Media

• Cloud

• Social Networking

• Wireless

• Software Dev.

• Sales Subscription

LIFE SCIENCES

• Genentech

• Bayer

• Novartis

• Amgen

• Gilead

AUTO (Tech)

• GM (On-Star)

• Renault (Nissan)

• Ford (Palo Alto)

• Tesla

• VW-Audi-Bentley

• Google (autocars)

Discover The State of Real Estate / 2012

What is an R&D building?

Discover The State of Real Estate / 2012

What is an R&D building?

Discover The State of Real Estate / 2012

Recent Bankruptcies…

Discover The State of Real Estate / 2012

Tenants on the rise…

Discover The State of Real Estate / 2012

Bay Area Warehouse Landscape

Discover The State of Real Estate / 2012

Sublease Q3-Q4

Added 400K Added 400K Down No Impact Flat

East Bay Warehouse

Net Absorption Conundrum

Discover The State of Real Estate / 2012

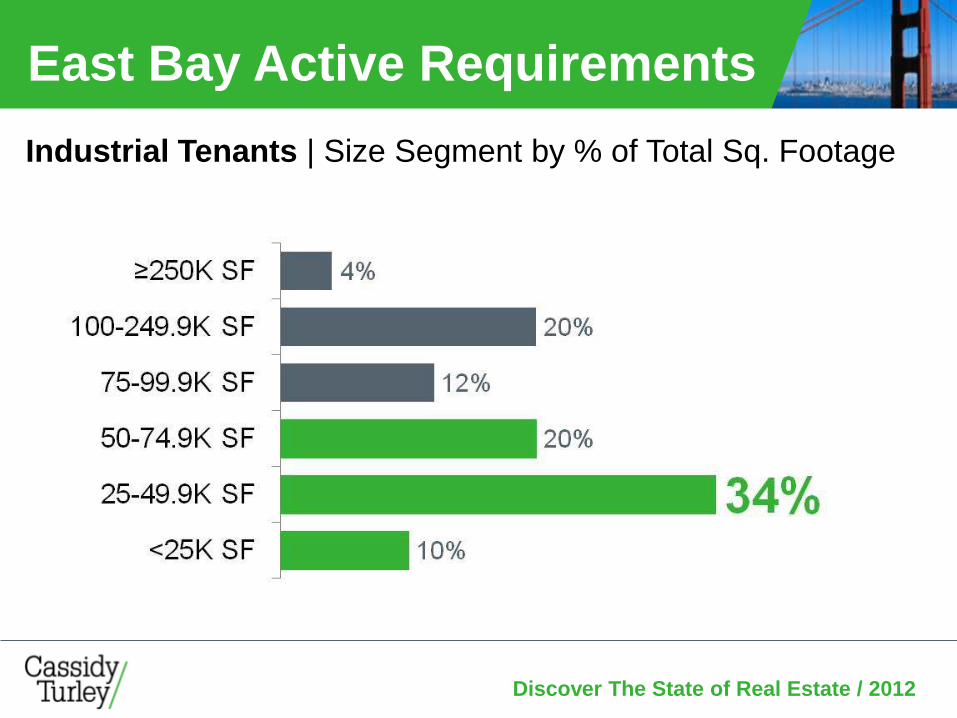

East Bay Active Requirements

Industrial Tenants | Size Segment by % of Total Sq. Footage

Discover The State of Real Estate / 2012

City Target Metreon

Discover The State of Real Estate / 2012

1 2

3 4

5 6 8

7

9 10

11

Mountain View

Fremont

Milpitas

North San Jose

Santa Clara

Sunnyvale

Tenant RSF Rate NNN

1 Motorola 80,669 $3.37

2 Rambus 30,963 $3.19

3 Financial Engines 80,995 $3.09

4 Microsoft 237,121 $2.59

5 Hewlett Packard 393,776 $2.86

6 Motorola 236,444 $2.74

7 Synopsys, 340,000 $3.80

8 Omnicell 99,880 $3.13

9 Micron Technologies 72,486 $0.72

10 NovaSolar 68,441 $0.65

11 Ascentool 54,440 $0.52

A Tale of Two Cities Silicon Valley Office/R&D Tenant Trends in 2011

Discover The State of Real Estate / 2012

Silicon Valley Tenant Tracking

By Search Area

Total Requirements

0 10 20 30 40

South SMC

Mt. View-Palo Alto-Menlo Park

Sunnyvale-Santa Clara

West Valley

San Jose

Milpitas-Fremont

Unknown

Square Footage (Millions)

0 1 2 3

South SMC

Mt. View-Palo Alto-Menlo Park

Sunnyvale-Santa Clara

West Valley

San Jose

Milpitas-Fremont

Unknown

Discover The State of Real Estate / 2012

Silicon Valley Tenant Tracking

By Size Segment

100,000 - 199,999 SF 17 2,210,000

60,000 - 79,999 SF

810,000 81,00010

20,000 - 39,999 SF 15 400,000 26,667

Location Requirements SF

Total 85 9,022,000 106,141≥200,000 SF 13 4,100,000 315,385

8 540,000 67,500

40,000 - 59,999 SF 21 945,000 45,000

130,000

80,000 - 99,999 SF

Avg Deal Size

Discover The State of Real Estate / 2012

$0.25

$0.30

$0.35

$0.40

$0.45

$0.50

$0.55

$0.60

0%

2%

4%

6%

8%

10%

12%

14%

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Vacancy Avg Asking NNN

East Bay Warehouse Vacancy & Average Asking Rate (NNN) Trend

Vacancy Falls

Below 8%

Discover The State of Real Estate / 2012

Office Development Pipeline

2.4M

0.7

2.9

4.4

BTS

Spec.

BTO

Likely Development Next 24 Mos (Million SF)

8.1M Square Feet

3.9M

1.8M

Discover The State of Real Estate / 2012

Bay Area Warehouse Development Trend | Square Feet in Millions

Discover The State of Real Estate / 2012

2012 Major Shopping Centers

1

2

3

4

5

6

7

8

9

10

Discover The State of Real Estate / 2012

Bay Area Office Underwriting

San Francisco Silicon Valley Secondary Markets

Core Funds (7-10 Yr Hold)

Returns

Going-in Cap 5-6% 6-6.5% 7-8%

Unleveraged IRR 7-8% 8-10% 9-12%

Leveraged IRR 8-9.5% 10-12% 12-15%

Underwriting

Exit Cap 7-7.5% 7.5-8% 8-8.5%

Rent Growth

2012 10% 10% 3-4%

2013 10% 10% 3-4%

2014 5% 5% 3-4%

2015+ 3% 3% 3%

Institutional Investors

Discover The State of Real Estate / 2012

Bay Area Office Underwriting

Institutional Investors

San Francisco Silicon Valley Secondary Markets

Value-Add Funds (3-5 Yr Hold)

Returns

Leveraged IRR 13-15% 15-18% 17-20%

Underwriting

Exit Cap 6-7% 7-7.5% 8-8.5%

Rent Growth

2012 15% 15% 5-10%

2013 15% 15% 5-10%

2014 10% 10% 5-10%

2015+ 3% 3% 3%

Discover The State of Real Estate / 2012

Select Recent Institutional Deals

PROJECT SQ.FT. PRICE

• Central Research Park, Sunnyvale 468,953 $132M

• Sobrato Portfolio, Silicon Valley 789,033 $88.8M

• 360 Spear St, San Francisco 154,950 $85.0M

• Capmark Portfolio, Silicon Valley 539,095 $66.6M

• 625 Second St, San Francisco 136,906 $56.4M

• MachineWorks Bldg, Portland OR 114,396 $41.1M

Discover The State of Real Estate / 2012

2012 Forecast Book

Discover The State of Real Estate / 2012

Web Video Available Friday!

68

Northern California | 2012