Embed Size (px)

Citation preview

NORTH YORKSHIRE COUNTY COUNCIL

EXECUTIVE

22 February 2011

QUARTERLY PERFORMANCE AND BUDGET MONITORING REPORT

Joint Report of the Chief Executive and Corporate Director – Finance and Central Services

1.0 Purpose of Report 1.1 To bring together performance, personnel and financial information for

the third quarter of 2010/11 within the Performance Management and Improvement Framework.

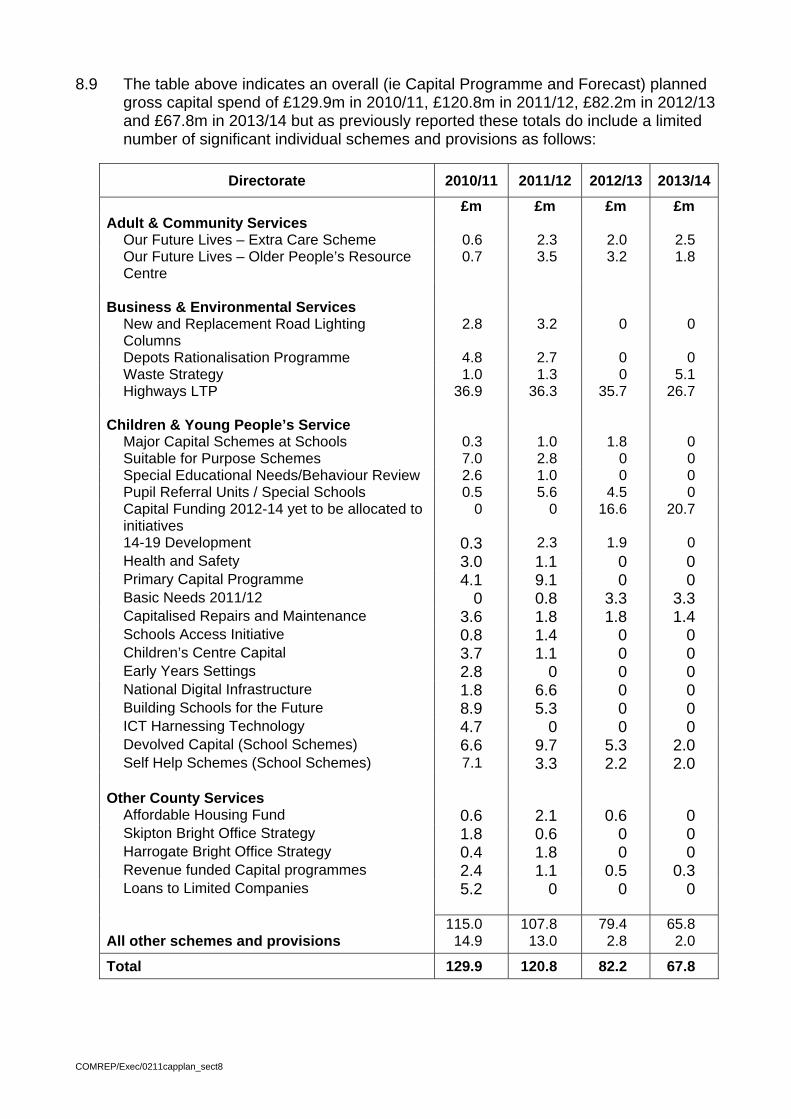

2.0 Contents 3.0 Background 4.0 Performance

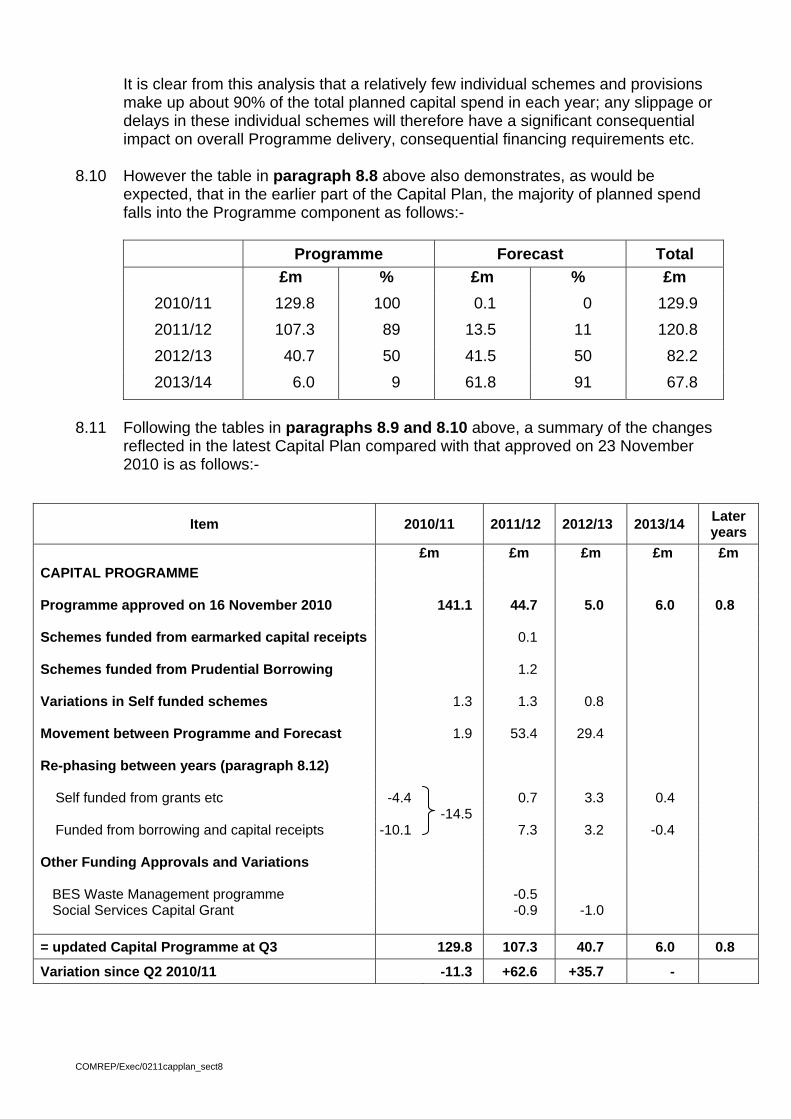

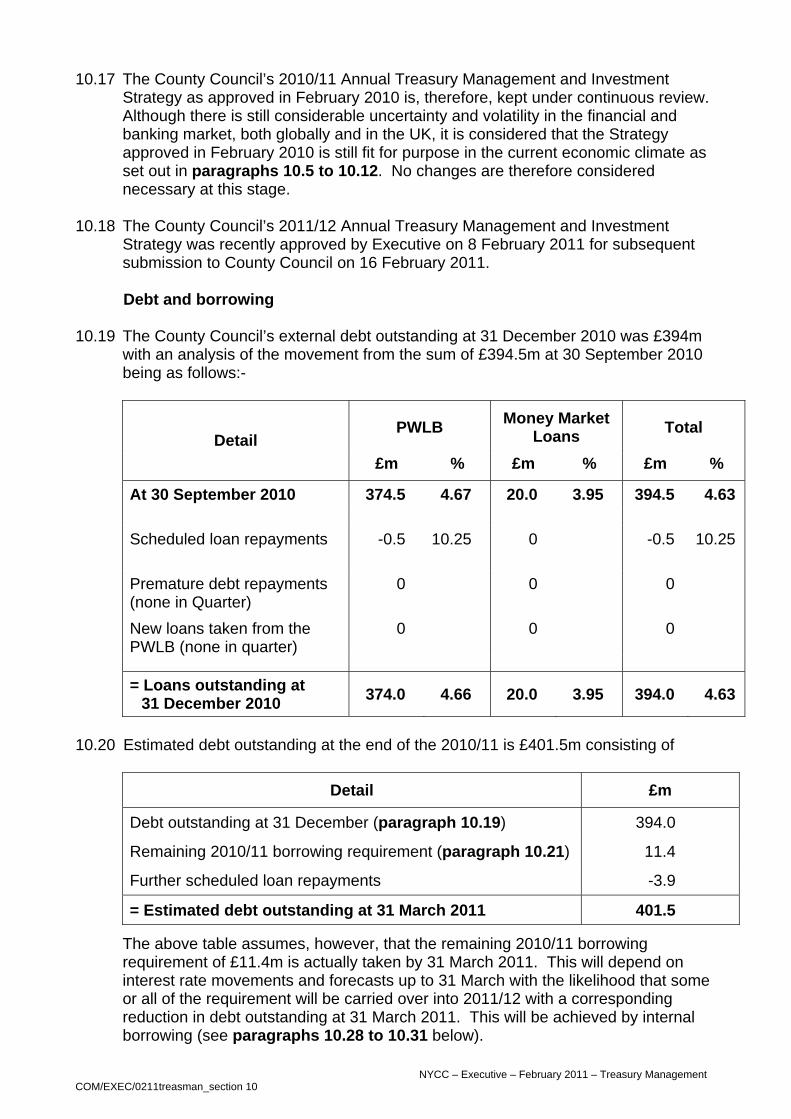

Annex A Top Level Performance Indicator Results 5.0 Citizens’ Panel

6.0 Human Resources Performance Data

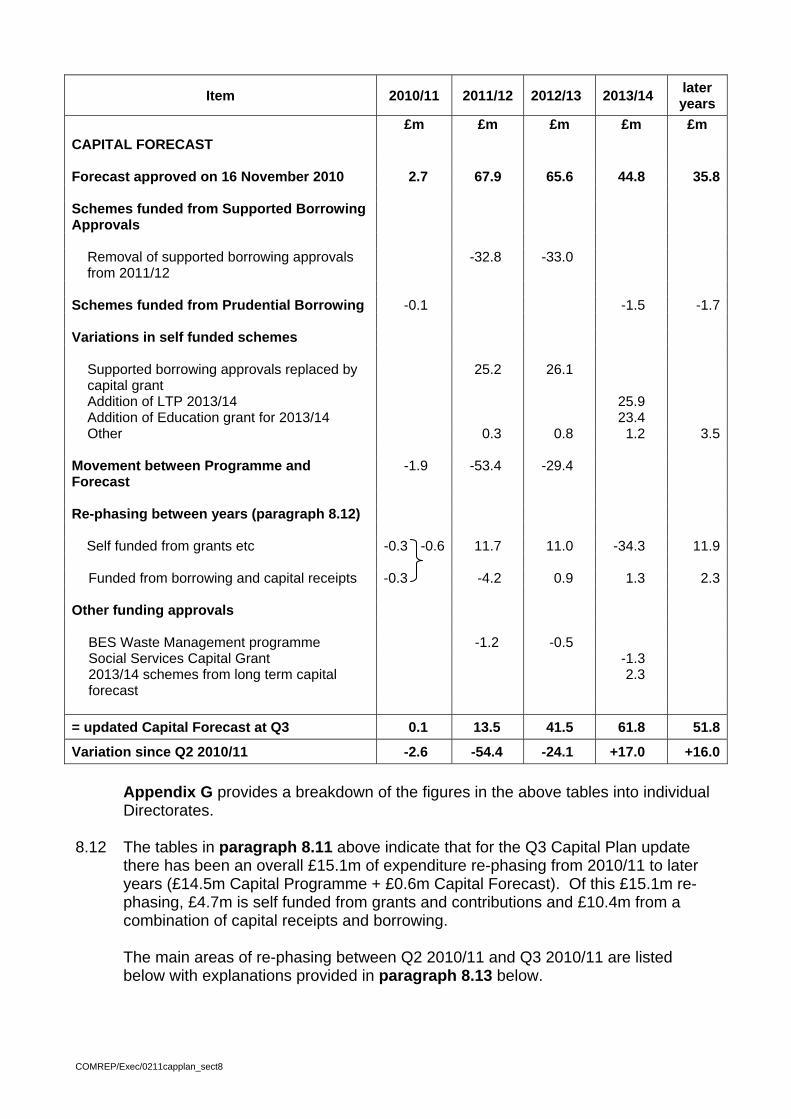

Annex B Performance Framework 2010/11 – Qtr 3

7.0 Revenue 2010-11 Annex C Revenue Budget Appendices

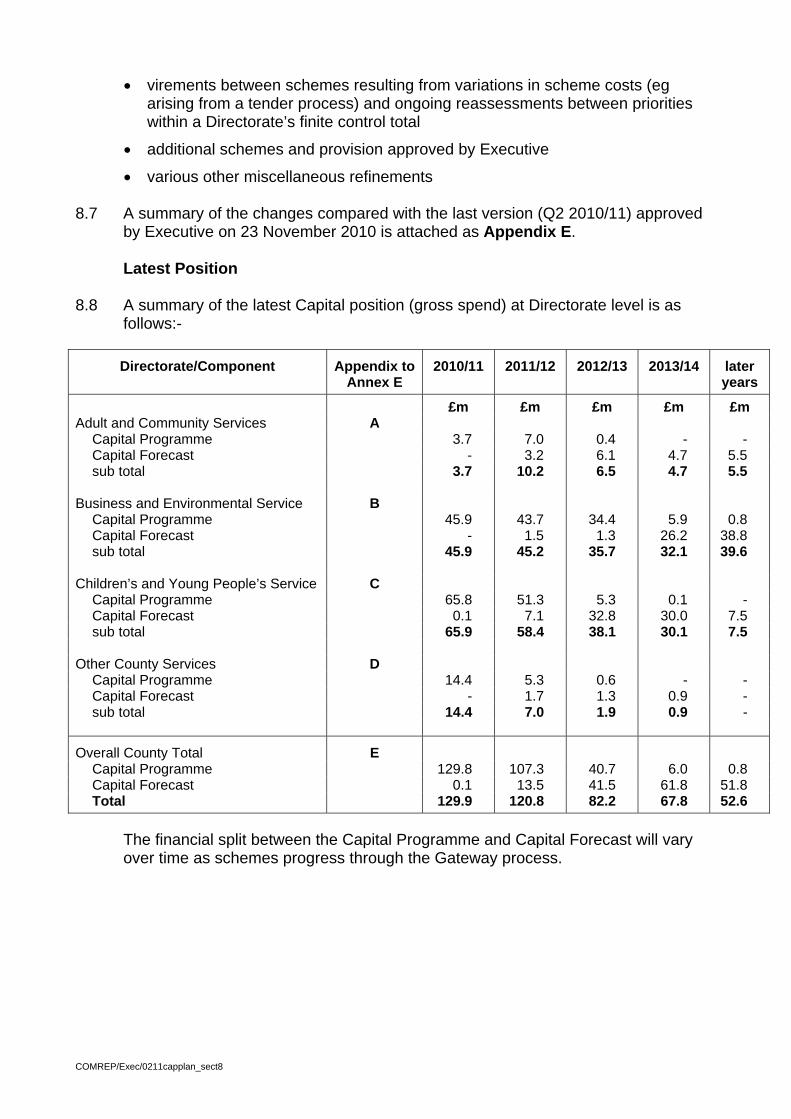

8.0 Capital Expenditure and Financing

Annex D Capital Plan Appendices 9.0 Budget Savings

Annex E 10.0 Annual Treasury Management Annex F 11.0 Legal Implications 12.0 Consultation and Responses 13.0 Conclusions and Recommendations

E/2011/25

3.0 Background 3.1 The Council plan sets out the priorities that have been set to achieve the

County Council’s corporate objectives. Quarterly monitoring reports track progress and provide the information needed to adjust priorities or investment and spending plans.

4.0 Performance

Last October the Secretary of State for Communities and Local Government announced the ending of the National Indicator Set and central control over LAA targets. He announced that the Government would establish a single list of all data that central government asks of local government. Work on developing the single list is under way and the Government intends that the list will take effect from April 2011 and be reviewed annually thereafter.

4.1 In November the Government announced the abolition of the Care Quality Commission’s annual score for adult social care and the current annual performance assessment system. The Department of Health is consulting on a new sector-led performance assessment system which it intends to introduce in 2001/12. The Government has also announced that Ofsted’s annual assessment of children’s services will end as soon as a suitable legislative opportunity can be identified, although it will still be in place for 2011, and possibly 2012.

4.3 Since the last quarterly report the annual assessment of Adult Social Care

by CQC has been announced with the award of an overall grade of ‘excellent’ and a detailed report on this was presented to the Executive on 1 February 2011. Ofsted’s annual judgement on children’s services was announced in December, with an overall grade of ‘Performing Well’ and the very large majority of services, settings and institutions judged to be good or excellent. The Youth Justice Service has been inspected by HM Inspectorate of Probation and the report published in January 2011 noted the county’s work with young offenders as well above average in the three key areas and overall judged to be a ‘very creditable set of findings’.

4.4 While this report highlights particular areas of improved performance and

potential concern this is in the context of the County Council’s services being rated by external inspection as performing well or excellently. This is achieved thanks to the many services that consistently deliver excellent performance through sustained focus and effort over time.

4.5 In preparing this quarterly report a range of performance data relating to

each service area has been monitored as well as the Key Performance Indicators presented in Annex A. The annex shows target achievement, a comparison against the previous reporting period and where available the quartile position compared to all county councils. The information needs to be considered in the round – for example a decline in performance between quarters may not be a cause for concern if the indicator is still on or above target.

4.6 Particular areas of improved performance to note are: a. The number of visits to the website is well ahead of target with 1.5

million visits so far this year. A major factor in the Q3 performance was use of the website to access information during the bad weather and the promotion and popularity of the ice station weather cameras.

b. The number of people receiving an ‘At Home’ library service has

continued to rise and is ahead of target. c. The number of adult social care clients receiving Self Directed Support

has risen significantly, building on good performance last year, and is ahead of target.

d. The number of people killed or seriously injured in road traffic accidents

continues to reduce with the Q3 outturn of 366 keeping ahead of the target for the quarter of 467.

4.7 Areas of potential concern noted in the last report to the Executive were:

a. SEN final statements issued within 26 weeks (excluding exceptions) has dropped back slightly to 95.4% in Q3 but this is still more than 10% above last year’s performance.

b. The upward trend in number of moves of placements experienced by

looked after children last year has been reversed and the Q3 figure has maintained the improvement.

4.8 Recommendation

(a) Note performance in the third quarter.

Annex A

Top Level Performance Indicator Results

KEYTarget achieved

Top quartile

Result within 10% of target Above the median

X Target not achievedBelow the median

Bottom quartile

Above the median

Below the median

Bottom Quartile

Improving

No change

Getting worse

Top Quartile

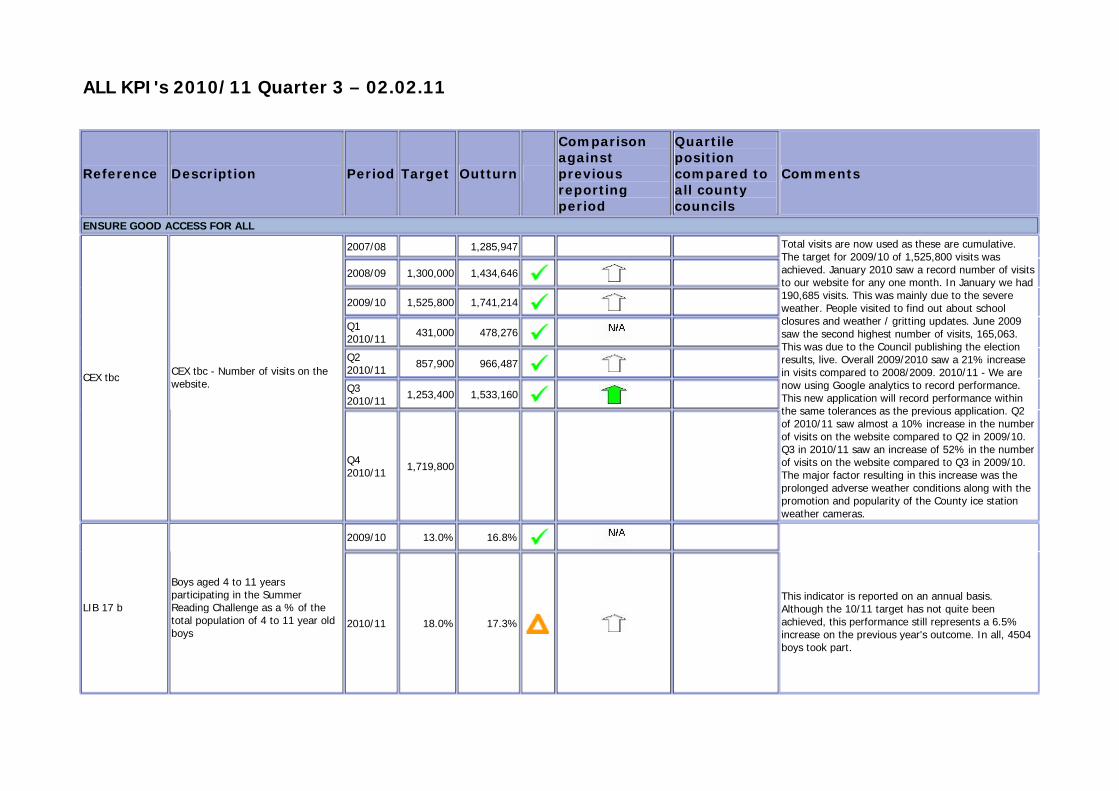

ALL KPI's 2010/11 Quarter 3 – 02.02.11

Reference Description Period Target Outturn

Comparison against previous reporting period

Quartile position compared to all county councils

Comments

ENSURE GOOD ACCESS FOR ALL

2007/08 1,285,947 2008/09 1,300,000 1,434,646 2009/10 1,525,800 1,741,214 Q1 2010/11 431,000 478,276 Q2 2010/11 857,900 966,487 Q3 2010/11 1,253,400 1,533,160

CEX tbc CEX tbc - Number of visits on the website.

Q4 2010/11 1,719,800

Total visits are now used as these are cumulative. The target for 2009/10 of 1,525,800 visits was achieved. January 2010 saw a record number of visits to our website for any one month. In January we had 190,685 visits. This was mainly due to the severe weather. People visited to find out about school closures and weather / gritting updates. June 2009 saw the second highest number of visits, 165,063. This was due to the Council publishing the election results, live. Overall 2009/2010 saw a 21% increase in visits compared to 2008/2009. 2010/11 - We are now using Google analytics to record performance. This new application will record performance within the same tolerances as the previous application. Q2 of 2010/11 saw almost a 10% increase in the number of visits on the website compared to Q2 in 2009/10. Q3 in 2010/11 saw an increase of 52% in the number of visits on the website compared to Q3 in 2009/10. The major factor resulting in this increase was the prolonged adverse weather conditions along with the promotion and popularity of the County ice station weather cameras.

2009/10 13.0% 16.8%

LIB 17 b

Boys aged 4 to 11 years participating in the Summer Reading Challenge as a % of the total population of 4 to 11 year old boys

2010/11 18.0% 17.3%

This indicator is reported on an annual basis. Although the 10/11 target has not quite been achieved, this performance still represents a 6.5% increase on the previous year's outcome. In all, 4504 boys took part.

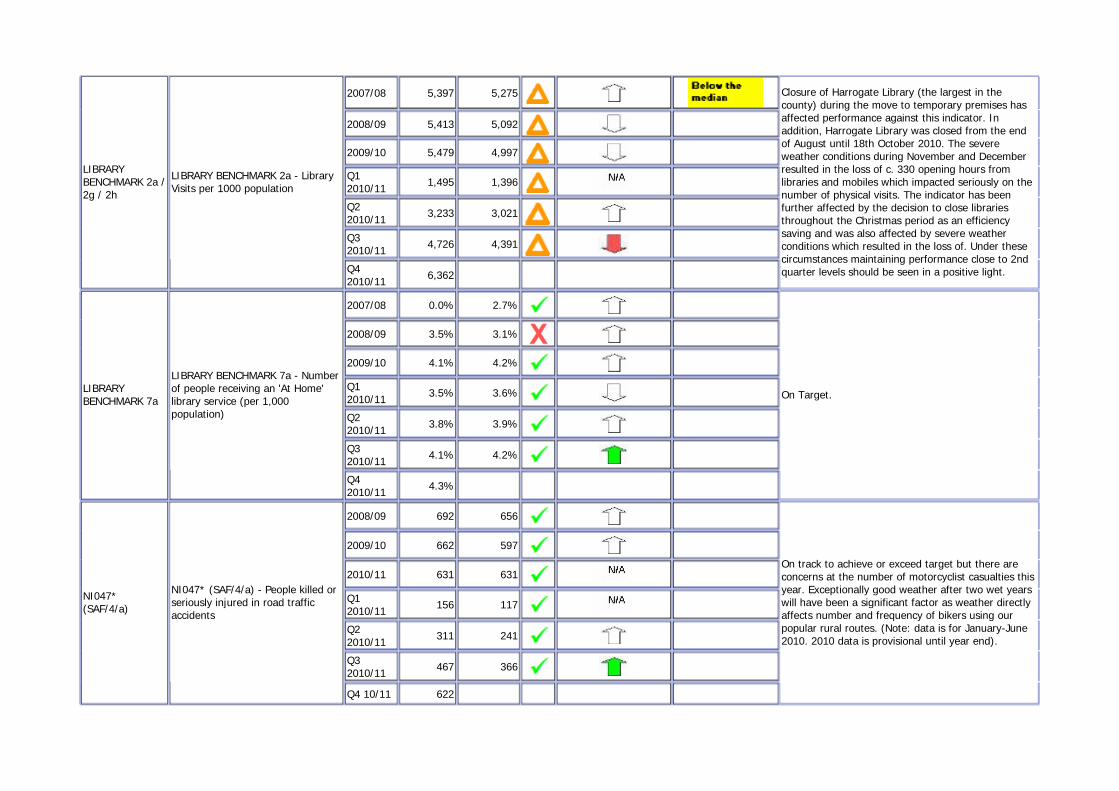

2007/08 5,397 5,275 2008/09 5,413 5,092 2009/10 5,479 4,997 Q1 2010/11 1,495 1,396 Q2 2010/11 3,233 3,021 Q3 2010/11 4,726 4,391

LIBRARY BENCHMARK 2a / 2g / 2h

LIBRARY BENCHMARK 2a - Library Visits per 1000 population

Q4 2010/11 6,362

Closure of Harrogate Library (the largest in the county) during the move to temporary premises has affected performance against this indicator. In addition, Harrogate Library was closed from the end of August until 18th October 2010. The severe weather conditions during November and December resulted in the loss of c. 330 opening hours from libraries and mobiles which impacted seriously on the number of physical visits. The indicator has been further affected by the decision to close libraries throughout the Christmas period as an efficiency saving and was also affected by severe weather conditions which resulted in the loss of. Under these circumstances maintaining performance close to 2nd quarter levels should be seen in a positive light.

2007/08 0.0% 2.7% 2008/09 3.5% 3.1% 2009/10 4.1% 4.2% Q1 2010/11 3.5% 3.6% Q2 2010/11 3.8% 3.9% Q3 2010/11 4.1% 4.2%

LIBRARY BENCHMARK 7a

LIBRARY BENCHMARK 7a - Number of people receiving an 'At Home' library service (per 1,000 population)

Q4 2010/11 4.3%

On Target.

2008/09 692 656 2009/10 662 597 2010/11 631 631 Q1 2010/11 156 117 Q2 2010/11 311 241 Q3 2010/11 467 366

NI047* (SAF/4/a)

NI047* (SAF/4/a) - People killed or seriously injured in road traffic accidents

Q4 10/11 622

On track to achieve or exceed target but there are concerns at the number of motorcyclist casualties this year. Exceptionally good weather after two wet years will have been a significant factor as weather directly affects number and frequency of bikers using our popular rural routes. (Note: data is for January-June 2010. 2010 data is provisional until year end).

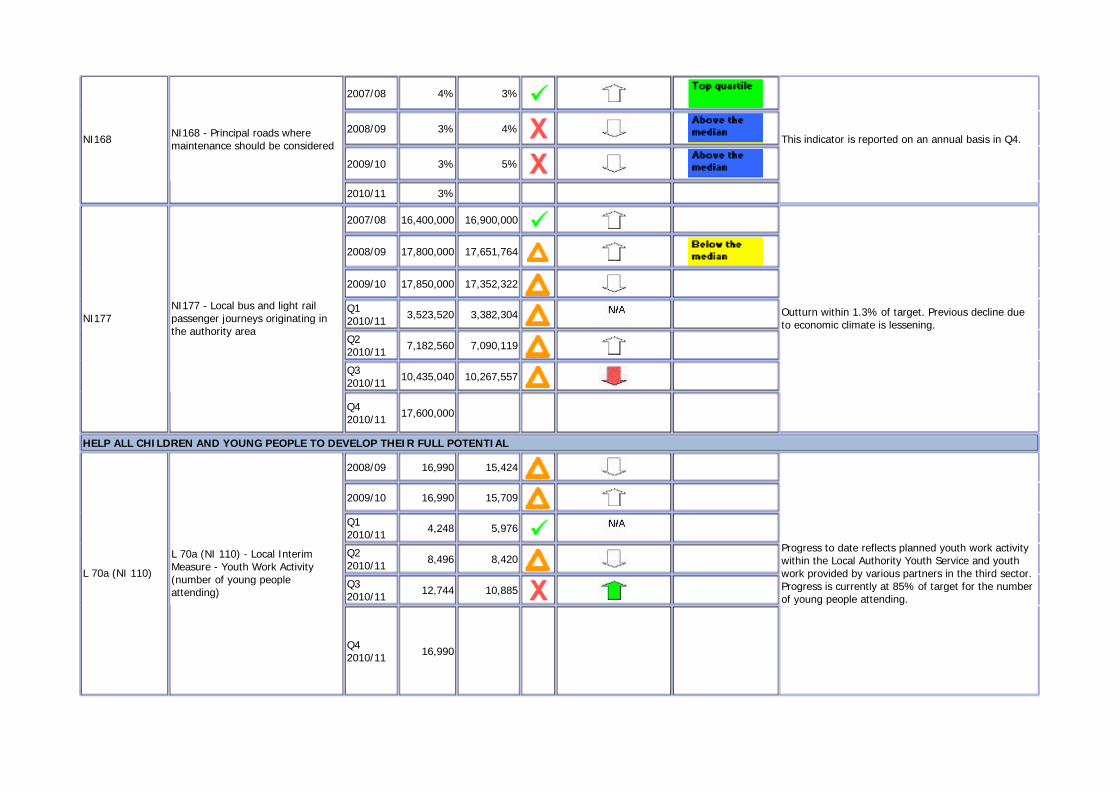

2007/08 4% 3% 2008/09 3% 4% 2009/10 3% 5%

NI168 NI168 - Principal roads where maintenance should be considered

2010/11 3%

This indicator is reported on an annual basis in Q4.

2007/08 16,400,000 16,900,000

2008/09 17,800,000 17,651,764 2009/10 17,850,000 17,352,322 Q1 2010/11 3,523,520 3,382,304 Q2 2010/11 7,182,560 7,090,119 Q3 2010/11 10,435,040 10,267,557

NI177 NI177 - Local bus and light rail passenger journeys originating in the authority area

Q4 2010/11 17,600,000

Outturn within 1.3% of target. Previous decline due to economic climate is lessening.

HELP ALL CHILDREN AND YOUNG PEOPLE TO DEVELOP THEIR FULL POTENTIAL

2008/09 16,990 15,424 2009/10 16,990 15,709 Q1 2010/11 4,248 5,976 Q2 2010/11 8,496 8,420 Q3 2010/11 12,744 10,885

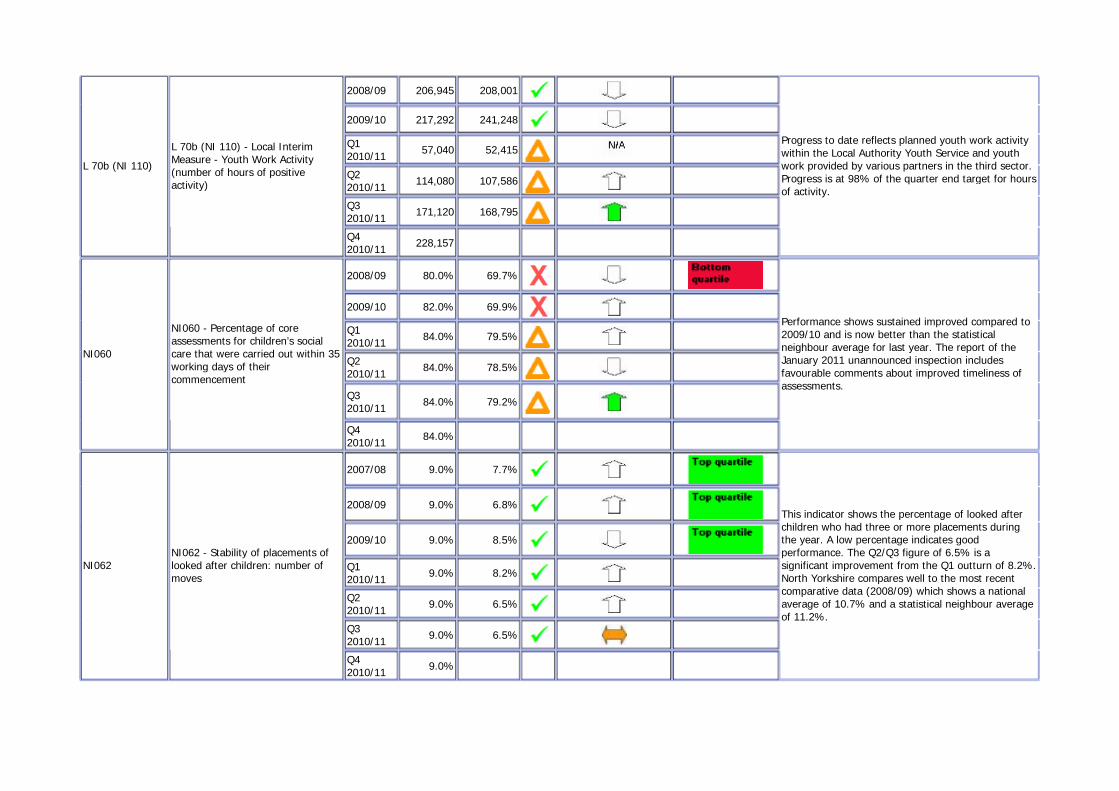

L 70a (NI 110)

L 70a (NI 110) - Local Interim Measure - Youth Work Activity (number of young people attending)

Q4 2010/11 16,990

Progress to date reflects planned youth work activity within the Local Authority Youth Service and youth work provided by various partners in the third sector. Progress is currently at 85% of target for the number of young people attending.

2008/09 206,945 208,001 2009/10 217,292 241,248 Q1 2010/11 57,040 52,415 Q2 2010/11 114,080 107,586 Q3 2010/11 171,120 168,795

L 70b (NI 110)

L 70b (NI 110) - Local Interim Measure - Youth Work Activity (number of hours of positive activity)

Q4 2010/11 228,157

Progress to date reflects planned youth work activity within the Local Authority Youth Service and youth work provided by various partners in the third sector. Progress is at 98% of the quarter end target for hours of activity.

2008/09 80.0% 69.7% 2009/10 82.0% 69.9% Q1 2010/11 84.0% 79.5% Q2 2010/11 84.0% 78.5% Q3 2010/11 84.0% 79.2%

NI060

NI060 - Percentage of core assessments for children’s social care that were carried out within 35 working days of their commencement

Q4 2010/11 84.0%

Performance shows sustained improved compared to 2009/10 and is now better than the statistical neighbour average for last year. The report of the January 2011 unannounced inspection includes favourable comments about improved timeliness of assessments.

2007/08 9.0% 7.7% 2008/09 9.0% 6.8% 2009/10 9.0% 8.5% Q1 2010/11 9.0% 8.2% Q2 2010/11 9.0% 6.5% Q3 2010/11 9.0% 6.5%

NI062 NI062 - Stability of placements of looked after children: number of moves

Q4 2010/11 9.0%

This indicator shows the percentage of looked after children who had three or more placements during the year. A low percentage indicates good performance. The Q2/Q3 figure of 6.5% is a significant improvement from the Q1 outturn of 8.2%. North Yorkshire compares well to the most recent comparative data (2008/09) which shows a national average of 10.7% and a statistical neighbour average of 11.2%.

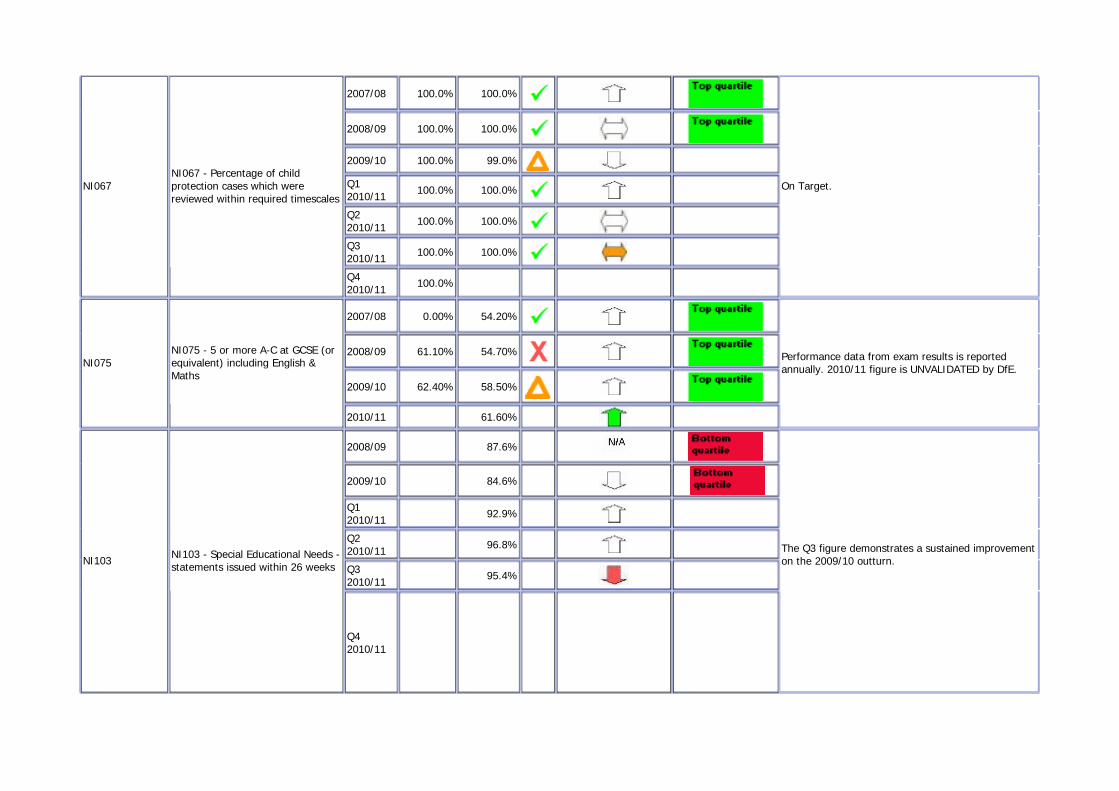

2007/08 100.0% 100.0% 2008/09 100.0% 100.0% 2009/10 100.0% 99.0% Q1 2010/11 100.0% 100.0% Q2 2010/11 100.0% 100.0% Q3 2010/11 100.0% 100.0%

NI067 NI067 - Percentage of child protection cases which were reviewed within required timescales

Q4 2010/11 100.0%

On Target.

2007/08 0.00% 54.20% 2008/09 61.10% 54.70% 2009/10 62.40% 58.50%

NI075 NI075 - 5 or more A-C at GCSE (or equivalent) including English & Maths

2010/11 61.60%

Performance data from exam results is reported annually. 2010/11 figure is UNVALIDATED by DfE.

2008/09 87.6% 2009/10 84.6% Q1 2010/11 92.9% Q2 2010/11 96.8% Q3 2010/11 95.4%

NI103 NI103 - Special Educational Needs - statements issued within 26 weeks

Q4 2010/11

The Q3 figure demonstrates a sustained improvement on the 2009/10 outturn.

2007/08 4.4% 3.8%

2008/09 4.1% 4.8% 2009/10 3.6% 4.5% Q1 2010/11 3.3% 4.2% Q2 2010/11 3.3% 5.3% Q3 2010/11 3.3% 4.3%

NI117* (CYP/7/a)

NI117* (CYP/7/a) - The percentage of 16 to 18 year olds who are not in education, employment or training (NEET).

Q4 2010/11 3.3%

Target, set 3 years prior, is unrealistic due to present climate. Data accuracy has continued to improve since 2009-10. Currently showing as second in comparison with statistical neighbours. Data available quarterly but can be miss-leading as the annual target comes from the average for the 3 months Nov/Dec/Jan when the cohort is most settled and representative of the real situation, (i.e. it is always high in the Summer through to November due to school leavers settling into their post 16 destination).

HELP PEOPLE LIVE IN SAFE COMMUNITIES

2008/09 1.20 1.38 2009/10 1.10 1.13 Q1 2010/11 0.27 0.21 Q2 2010/11 0.54 0.58 Q3 2010/11 0.81

NI019 NI019 - Rate of proven re-offending by young offenders

Q4 2010/11 1.06

Reporting is one quarter behind. Baseline = Jan-Mar 05 cohort. 374 young people in the cohort, with 140 re-offending (37.4%) with a total of 452 further offences (an average of 1.21 further offences per member of the cohort). The rate of re-offending was significantly reduced in the final quarter of 2009/10, leading to at 1.13 a better 2009/10 outturn than anticipated. The 2010/11 Q2 offending figures are not due to be finalised and submitted to the Youth Justice Board (YJB) until 31.01.11. The unfinalised position at 2010/11 Q2 is an average number of offences per cohort member of 0.58.

IMPROVE HEALTH AND WELLBEING AND GIVE PEOPLE EFFECTIVE SUPPORT

2007/08 32.0% 40.2% 2008/09 35.0% 40.9% 2009/10 40.0% 45.7%

ACS 2 ACS 2 - The percentage of people receiving intensive support who are helped to live at home.

2010/11 45.0%

ACS has continued to perform well in this indicator as a result of a continuous drive to reduce residential placements and wherever possible support people in their own home or through community based services.

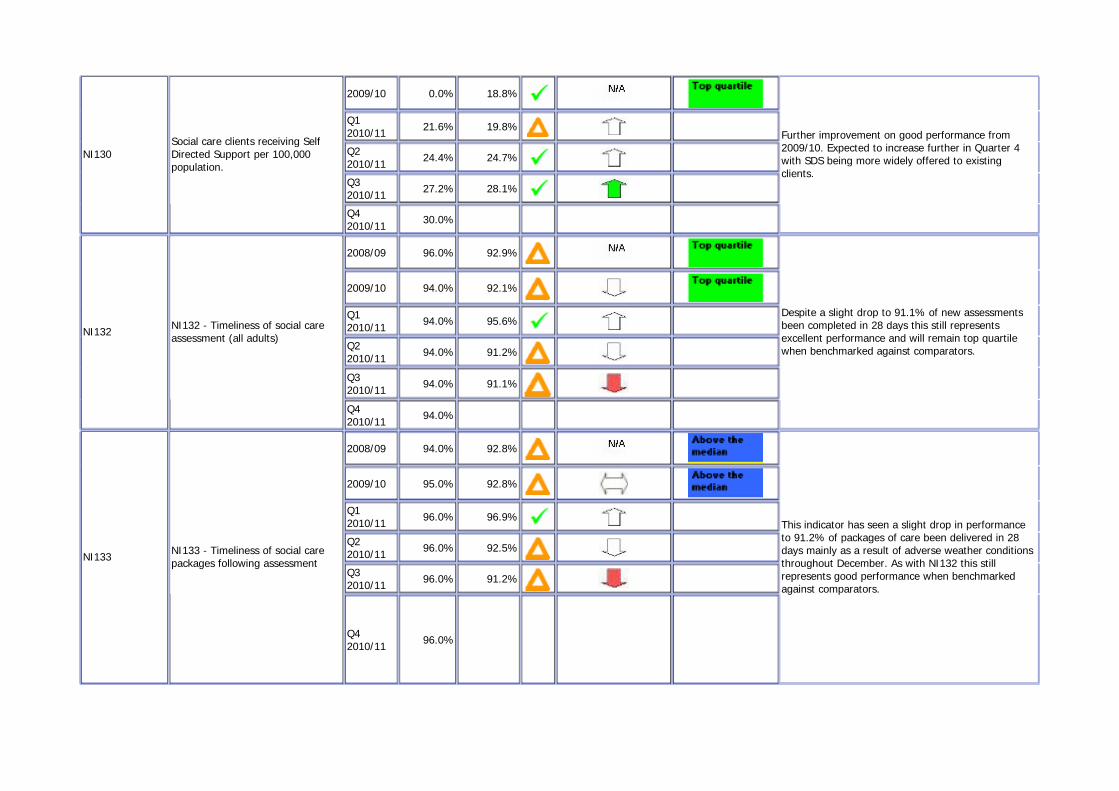

2009/10 0.0% 18.8% Q1 2010/11 21.6% 19.8% Q2 2010/11 24.4% 24.7% Q3 2010/11 27.2% 28.1%

NI130 Social care clients receiving Self Directed Support per 100,000 population.

Q4 2010/11 30.0%

Further improvement on good performance from 2009/10. Expected to increase further in Quarter 4 with SDS being more widely offered to existing clients.

2008/09 96.0% 92.9% 2009/10 94.0% 92.1% Q1 2010/11 94.0% 95.6% Q2 2010/11 94.0% 91.2% Q3 2010/11 94.0% 91.1%

NI132 NI132 - Timeliness of social care assessment (all adults)

Q4 2010/11 94.0%

Despite a slight drop to 91.1% of new assessments been completed in 28 days this still represents excellent performance and will remain top quartile when benchmarked against comparators.

2008/09 94.0% 92.8% 2009/10 95.0% 92.8% Q1 2010/11 96.0% 96.9% Q2 2010/11 96.0% 92.5% Q3 2010/11 96.0% 91.2%

NI133 NI133 - Timeliness of social care packages following assessment

Q4 2010/11 96.0%

This indicator has seen a slight drop in performance to 91.2% of packages of care been delivered in 28 days mainly as a result of adverse weather conditions throughout December. As with NI132 this still represents good performance when benchmarked against comparators.

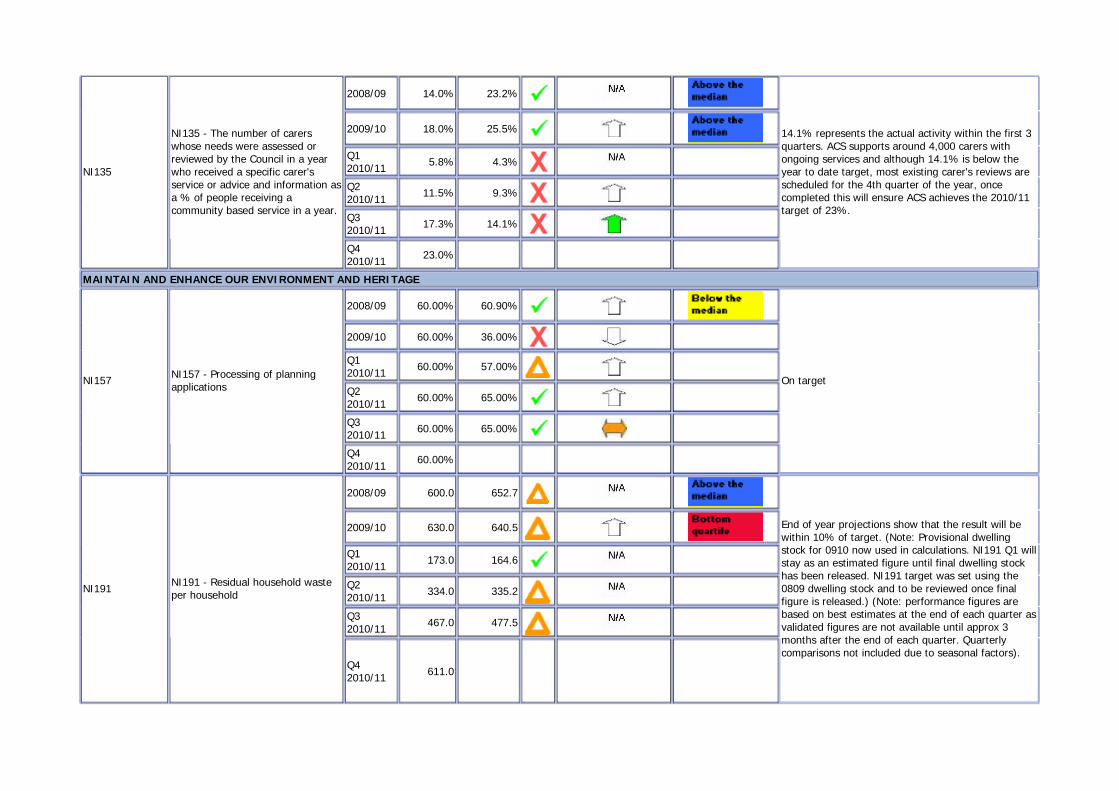

2008/09 14.0% 23.2% 2009/10 18.0% 25.5% Q1 2010/11 5.8% 4.3% Q2 2010/11 11.5% 9.3% Q3 2010/11 17.3% 14.1%

NI135

NI135 - The number of carers whose needs were assessed or reviewed by the Council in a year who received a specific carer's service or advice and information as a % of people receiving a community based service in a year.

Q4 2010/11 23.0%

14.1% represents the actual activity within the first 3 quarters. ACS supports around 4,000 carers with ongoing services and although 14.1% is below the year to date target, most existing carer's reviews are scheduled for the 4th quarter of the year, once completed this will ensure ACS achieves the 2010/11 target of 23%.

MAINTAIN AND ENHANCE OUR ENVIRONMENT AND HERITAGE

2008/09 60.00% 60.90% 2009/10 60.00% 36.00% Q1 2010/11 60.00% 57.00% Q2 2010/11 60.00% 65.00% Q3 2010/11 60.00% 65.00%

NI157 NI157 - Processing of planning applications

Q4 2010/11 60.00%

On target

2008/09 600.0 652.7 2009/10 630.0 640.5 Q1 2010/11 173.0 164.6 Q2 2010/11 334.0 335.2 Q3 2010/11 467.0 477.5

NI191 NI191 - Residual household waste per household

Q4 2010/11 611.0

End of year projections show that the result will be within 10% of target. (Note: Provisional dwelling stock for 0910 now used in calculations. NI191 Q1 will stay as an estimated figure until final dwelling stock has been released. NI191 target was set using the 0809 dwelling stock and to be reviewed once final figure is released.) (Note: performance figures are based on best estimates at the end of each quarter as validated figures are not available until approx 3 months after the end of each quarter. Quarterly comparisons not included due to seasonal factors).

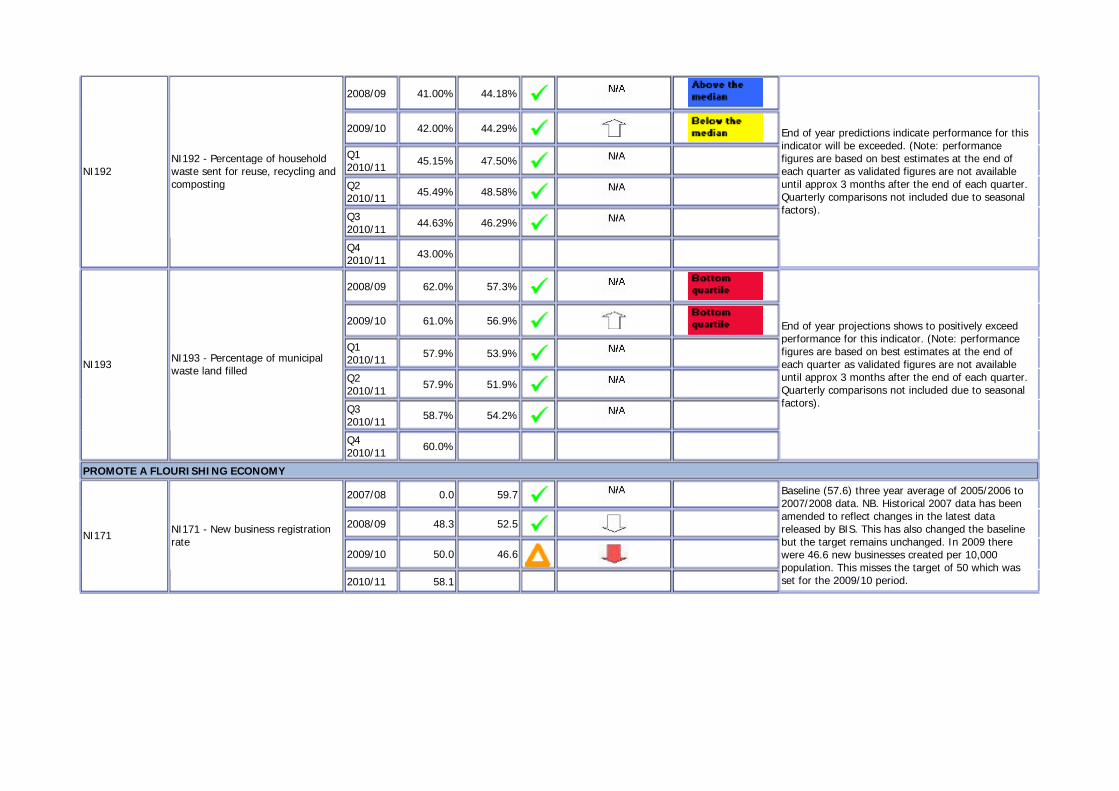

2008/09 41.00% 44.18% 2009/10 42.00% 44.29% Q1 2010/11 45.15% 47.50% Q2 2010/11 45.49% 48.58% Q3 2010/11 44.63% 46.29%

NI192 NI192 - Percentage of household waste sent for reuse, recycling and composting

Q4 2010/11 43.00%

End of year predictions indicate performance for this indicator will be exceeded. (Note: performance figures are based on best estimates at the end of each quarter as validated figures are not available until approx 3 months after the end of each quarter. Quarterly comparisons not included due to seasonal factors).

2008/09 62.0% 57.3% 2009/10 61.0% 56.9% Q1 2010/11 57.9% 53.9% Q2 2010/11 57.9% 51.9% Q3 2010/11 58.7% 54.2%

NI193 NI193 - Percentage of municipal waste land filled

Q4 2010/11 60.0%

End of year projections shows to positively exceed performance for this indicator. (Note: performance figures are based on best estimates at the end of each quarter as validated figures are not available until approx 3 months after the end of each quarter. Quarterly comparisons not included due to seasonal factors).

PROMOTE A FLOURISHING ECONOMY

2007/08 0.0 59.7 2008/09 48.3 52.5 2009/10 50.0 46.6

NI171 NI171 - New business registration rate

2010/11 58.1

Baseline (57.6) three year average of 2005/2006 to 2007/2008 data. NB. Historical 2007 data has been amended to reflect changes in the latest data released by BIS. This has also changed the baseline but the target remains unchanged. In 2009 there were 46.6 new businesses created per 10,000 population. This misses the target of 50 which was set for the 2009/10 period.

5.0 CITIZENS’ PANEL UPDATE 5.1 The current Citizens’ Panel was reviewed by the Corporate and

Partnerships Overview and Scrutiny Committee on 31st January 2011. A separate paper on the results of this review is on the agenda.

5.2 A number of topics have been proposed for the next survey including

awareness of adult safeguarding issues and services, minerals and waste planning and communication with the council. However, these will be reviewed as a result of the Scrutiny Committee recommendations.

5.3 RECOMMENDATION

To consider the separate paper on the scrutiny review of the Citizens’ Panel.

NYCC – Executive October 2010 Quarterly Monitoring Report/2

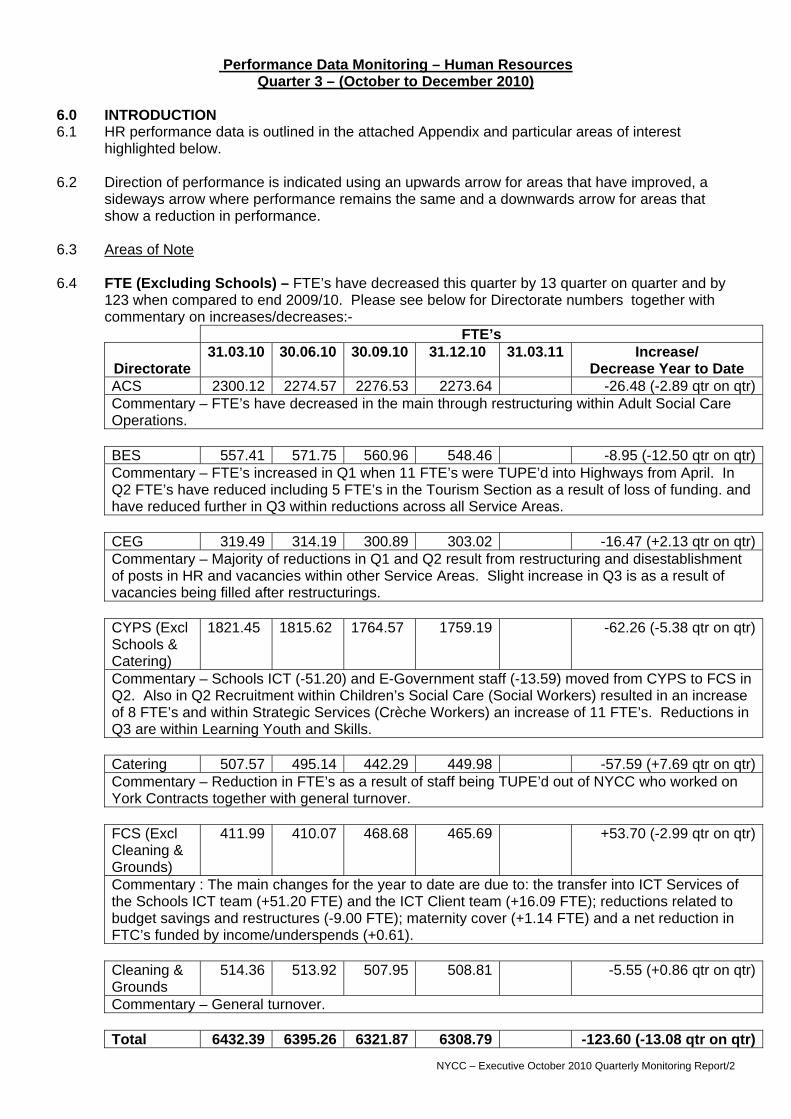

Performance Data Monitoring – Human Resources Quarter 3 – (October to December 2010)

6.0 INTRODUCTION 6.1 HR performance data is outlined in the attached Appendix and particular areas of interest

highlighted below. 6.2 Direction of performance is indicated using an upwards arrow for areas that have improved, a

sideways arrow where performance remains the same and a downwards arrow for areas that show a reduction in performance.

6.3 Areas of Note 6.4 FTE (Excluding Schools) – FTE’s have decreased this quarter by 13 quarter on quarter and by

123 when compared to end 2009/10. Please see below for Directorate numbers together with commentary on increases/decreases:-

FTE’s

Directorate 31.03.10 30.06.10 30.09.10 31.12.10 31.03.11 Increase/

Decrease Year to Date ACS 2300.12 2274.57 2276.53 2273.64 -26.48 (-2.89 qtr on qtr)Commentary – FTE’s have decreased in the main through restructuring within Adult Social Care Operations.

BES 557.41 571.75 560.96 548.46 -8.95 (-12.50 qtr on qtr)Commentary – FTE’s increased in Q1 when 11 FTE’s were TUPE’d into Highways from April. In Q2 FTE’s have reduced including 5 FTE’s in the Tourism Section as a result of loss of funding. and have reduced further in Q3 within reductions across all Service Areas.

CEG 319.49 314.19 300.89 303.02 -16.47 (+2.13 qtr on qtr)Commentary – Majority of reductions in Q1 and Q2 result from restructuring and disestablishment of posts in HR and vacancies within other Service Areas. Slight increase in Q3 is as a result of vacancies being filled after restructurings.

CYPS (Excl Schools & Catering)

1821.45 1815.62 1764.57 1759.19 -62.26 (-5.38 qtr on qtr)

Commentary – Schools ICT (-51.20) and E-Government staff (-13.59) moved from CYPS to FCS in Q2. Also in Q2 Recruitment within Children’s Social Care (Social Workers) resulted in an increase of 8 FTE’s and within Strategic Services (Crèche Workers) an increase of 11 FTE’s. Reductions in Q3 are within Learning Youth and Skills.

Catering 507.57 495.14 442.29 449.98 -57.59 (+7.69 qtr on qtr)Commentary – Reduction in FTE’s as a result of staff being TUPE’d out of NYCC who worked on York Contracts together with general turnover.

FCS (Excl Cleaning & Grounds)

411.99 410.07 468.68 465.69 +53.70 (-2.99 qtr on qtr)

Commentary : The main changes for the year to date are due to: the transfer into ICT Services of the Schools ICT team (+51.20 FTE) and the ICT Client team (+16.09 FTE); reductions related to budget savings and restructures (-9.00 FTE); maternity cover (+1.14 FTE) and a net reduction in FTC’s funded by income/underspends (+0.61).

Cleaning & Grounds

514.36 513.92 507.95 508.81 -5.55 (+0.86 qtr on qtr)

Commentary – General turnover.

Total 6432.39 6395.26 6321.87 6308.79 -123.60 (-13.08 qtr on qtr)

NYCC – Executive February 2010 Quarterly Monitoring Report/2

6.5 FTE’s are continuing to decrease slowly with more after 31st March 2011 as on-going restructurings across the Authority take effect in Quarter 4 and into 2011/12. 6.6 In addition to the above the following data illustrates changes taking place within the workforce in

response to savings requirements:-

• Vacancies – This quarter has seen a further rise in vacancies from 439 last quarter to 511 this quarter. This is expected as posts are held vacant as part of restructuring in order to maximise redeployment opportunities for staff under notice of redundancy and save budget.

• Leavers – Turnover has increased again this quarter compared to the same quarter last year

by 126 (full workforce). The projected turnover this year is 11.27% compared to 9.72% during 2009/10. A proportion of this relates to fixed term contracts expiring and not being renewed. Voluntary leavers (non-schools) have also increased this quarter when compared to the same quarter last year. The percentage of employees leaving with less than 12 months service has increased this quarter due to an increased volume of fixed term contracts of less than 12 months. Involuntary Leavers - The reported number of redundancies (non-schools workforce) this quarter is 11. The number of employees on redeployment (staff actively seeking alternative posts under notice of redundancy) is 56.

• Starters – The number has decreased again this quarter compared to the same quarter last

year with 199 reported this quarter compared to 279 last year. • Internal Movements – The quarter has seen an increase in internal movements due to

restructuring activity which will continue to increase. 6.7 Age Profile Full Workforce – The average age for the whole workforce has remained static for

this quarter but the average for the non-schools workforce has increased to 45.5. Workforce Aged Up to 25 – Non-Schools – This has remained static at 610 employees at the end of this quarter.

6.8 Attendance Management – Absence levels improved this quarter and the projected outturn is

now slightly lower than for 2009/10 (7.15 days compared to 7.21 days in 09/10). Absence levels for the same quarter last year were higher due to the swine flu pandemic and other winter viruses which do not appear to have had the same impact this quarter. Substantial numbers of staff are now affected by specific restructuring which historically tends to reduce absence.

6.9 Key Developments/Area for Expansion during Quarter 3 6.10 Removal of the Default Retirement Age (DRA) - From October 2011 the DRA will be removed which means that employers will no longer be able to rely on the DRA of age 65 to justify a dismissal for a compulsory retirement age, and will therefore be unable to issue new notifications of retirement using the DRA on or after 6.4.11. Employers have the option to retain a DRA, but must be able to objectively justify the reason for this as it may be open to challenge on discrimination grounds. Alternatively, employers can have no DRA. NYCC is currently considering how to respond to this legislation. 6.11 RECOMMENDATION 6.12 Executive is recommended to:

a) Note the performance within the report and the Appendix. Justine Brooksbank - Assistant Chief Executive – HR & OD – 26 January 2011 - JB/JML

Annex B Performance Framework

2010/11 – Qtr 3

Performance Report - 2010/11 AppendixPerformance Improvement Plans

2009

/201

0

Qua

rter

1

Qua

rter

2

Qua

rter

3

Qua

rter

4

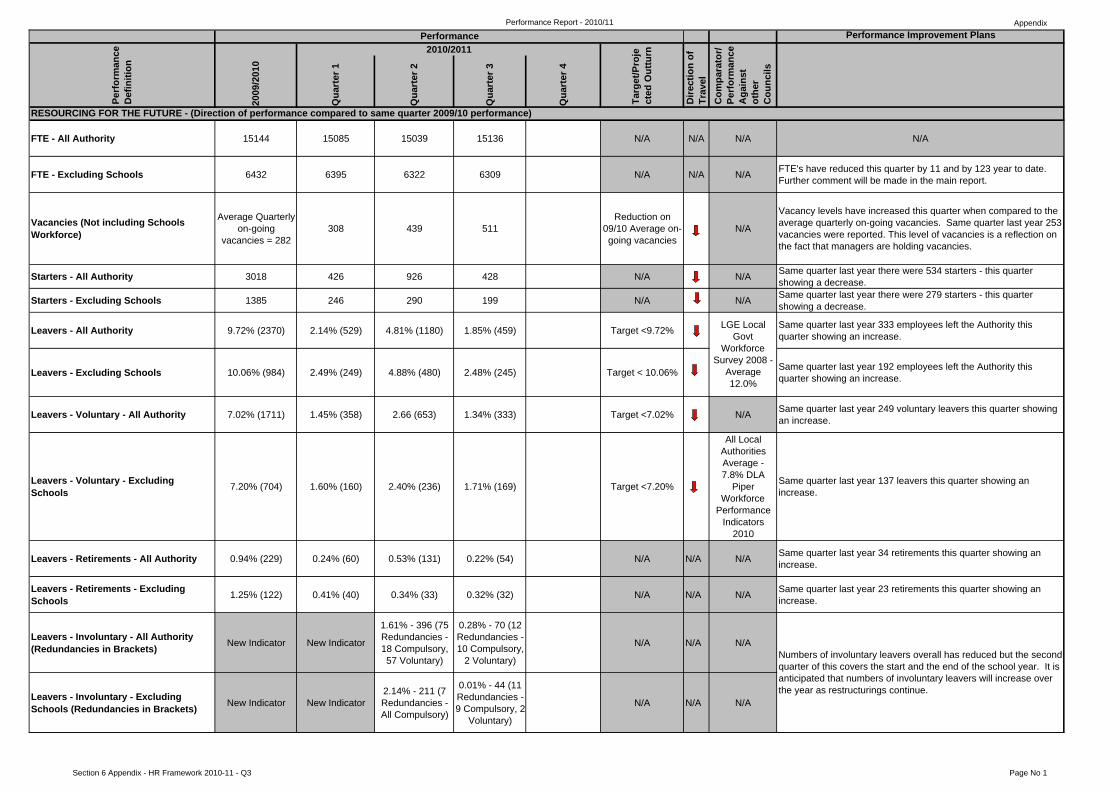

FTE - All Authority 15144 15085 15039 15136 N/A N/A N/A N/A

FTE - Excluding Schools 6432 6395 6322 6309 N/A N/A N/A FTE's have reduced this quarter by 11 and by 123 year to date. Further comment will be made in the main report.

Vacancies (Not including Schools Workforce)

Average Quarterly on-going

vacancies = 282308 439 511

Reduction on 09/10 Average on-going vacancies

N/A

Vacancy levels have increased this quarter when compared to the average quarterly on-going vacancies. Same quarter last year 253 vacancies were reported. This level of vacancies is a reflection on the fact that managers are holding vacancies.

Starters - All Authority 3018 426 926 428 N/A N/A Same quarter last year there were 534 starters - this quarter showing a decrease.

Starters - Excluding Schools 1385 246 290 199 N/A N/A Same quarter last year there were 279 starters - this quarter showing a decrease.

Leavers - All Authority 9.72% (2370) 2.14% (529) 4.81% (1180) 1.85% (459) Target <9.72% Same quarter last year 333 employees left the Authority this quarter showing an increase.

Leavers - Excluding Schools 10.06% (984) 2.49% (249) 4.88% (480) 2.48% (245) Target < 10.06% Same quarter last year 192 employees left the Authority this quarter showing an increase.

Leavers - Voluntary - All Authority 7.02% (1711) 1.45% (358) 2.66 (653) 1.34% (333) Target <7.02% N/A Same quarter last year 249 voluntary leavers this quarter showing an increase.

Leavers - Voluntary - Excluding Schools 7.20% (704) 1.60% (160) 2.40% (236) 1.71% (169) Target <7.20%

All Local Authorities Average - 7.8% DLA

Piper Workforce

Performance Indicators

2010

Same quarter last year 137 leavers this quarter showing an increase.

Leavers - Retirements - All Authority 0.94% (229) 0.24% (60) 0.53% (131) 0.22% (54) N/A N/A N/A Same quarter last year 34 retirements this quarter showing an increase.

Leavers - Retirements - Excluding Schools 1.25% (122) 0.41% (40) 0.34% (33) 0.32% (32) N/A N/A N/A Same quarter last year 23 retirements this quarter showing an

increase.

Leavers - Involuntary - All Authority (Redundancies in Brackets) New Indicator New Indicator

1.61% - 396 (75 Redundancies - 18 Compulsory, 57 Voluntary)

0.28% - 70 (12 Redundancies - 10 Compulsory,

2 Voluntary)

N/A N/A N/A

Leavers - Involuntary - Excluding Schools (Redundancies in Brackets) New Indicator New Indicator

2.14% - 211 (7 Redundancies - All Compulsory)

0.01% - 44 (11 Redundancies - 9 Compulsory, 2

Voluntary)

N/A N/A N/AD

irect

ion

of

Trav

el

LGE Local Govt

Workforce Survey 2008 -

Average 12.0%

RESOURCING FOR THE FUTURE - (Direction of performance compared to same quarter 2009/10 performance)

Numbers of involuntary leavers overall has reduced but the second quarter of this covers the start and the end of the school year. It is anticipated that numbers of involuntary leavers will increase over the year as restructurings continue.

Performance

Targ

et/P

roje

cted

Out

turn2010/2011

Perf

orm

ance

D

efin

ition

Com

para

tor/

Perf

orm

ance

A

gain

st

othe

r C

ounc

ilsSection 6 Appendix - HR Framework 2010-11 - Q3 Page No 1

Performance Report - 2010/11 AppendixPerformance Improvement Plans

2009

/201

0

Qua

rter

1

Qua

rter

2

Qua

rter

3

Qua

rter

4

Dire

ctio

n of

Tr

avel

Performance

Targ

et/P

roje

cted

Out

turn2010/2011

Perf

orm

ance

D

efin

ition

Com

para

tor/

Perf

orm

ance

A

gain

st

othe

r C

ounc

ils

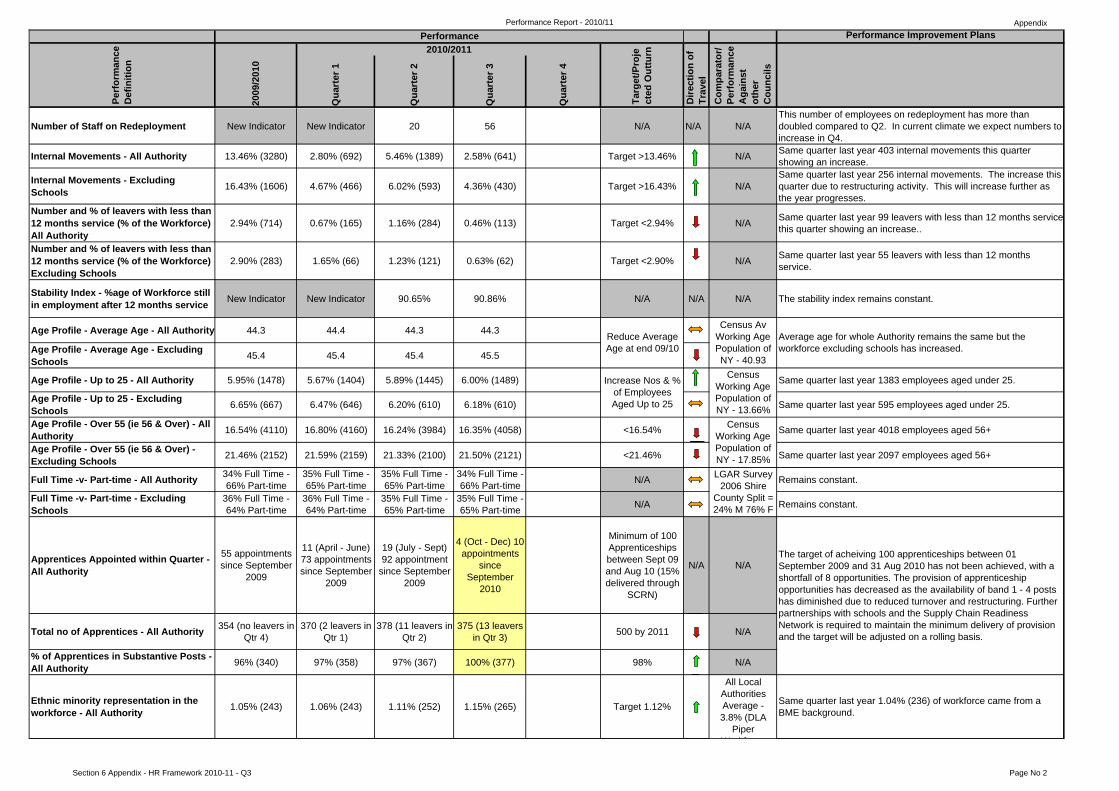

Number of Staff on Redeployment New Indicator New Indicator 20 56 N/A N/A N/AThis number of employees on redeployment has more than doubled compared to Q2. In current climate we expect numbers to increase in Q4.

Internal Movements - All Authority 13.46% (3280) 2.80% (692) 5.46% (1389) 2.58% (641) Target >13.46% N/A Same quarter last year 403 internal movements this quarter showing an increase.

Internal Movements - Excluding Schools 16.43% (1606) 4.67% (466) 6.02% (593) 4.36% (430) Target >16.43% N/A

Same quarter last year 256 internal movements. The increase this quarter due to restructuring activity. This will increase further as the year progresses.

Number and % of leavers with less than 12 months service (% of the Workforce) -All Authority

2.94% (714) 0.67% (165) 1.16% (284) 0.46% (113) Target <2.94% N/A Same quarter last year 99 leavers with less than 12 months service this quarter showing an increase..

Number and % of leavers with less than 12 months service (% of the Workforce) -Excluding Schools

2.90% (283) 1.65% (66) 1.23% (121) 0.63% (62) Target <2.90% N/A Same quarter last year 55 leavers with less than 12 months service.

Stability Index - %age of Workforce still in employment after 12 months service New Indicator New Indicator 90.65% 90.86% N/A N/A N/A The stability index remains constant.

Age Profile - Average Age - All Authority 44.3 44.4 44.3 44.3

Age Profile - Average Age - Excluding Schools 45.4 45.4 45.4 45.5

Age Profile - Up to 25 - All Authority 5.95% (1478) 5.67% (1404) 5.89% (1445) 6.00% (1489) Same quarter last year 1383 employees aged under 25.

Age Profile - Up to 25 - Excluding Schools 6.65% (667) 6.47% (646) 6.20% (610) 6.18% (610) Same quarter last year 595 employees aged under 25.

Age Profile - Over 55 (ie 56 & Over) - All Authority 16.54% (4110) 16.80% (4160) 16.24% (3984) 16.35% (4058) <16.54% Same quarter last year 4018 employees aged 56+

Age Profile - Over 55 (ie 56 & Over) - Excluding Schools 21.46% (2152) 21.59% (2159) 21.33% (2100) 21.50% (2121) <21.46% Same quarter last year 2097 employees aged 56+

Full Time -v- Part-time - All Authority 34% Full Time - 66% Part-time

35% Full Time - 65% Part-time

35% Full Time - 65% Part-time

34% Full Time - 66% Part-time N/A Remains constant.

Full Time -v- Part-time - Excluding Schools

36% Full Time - 64% Part-time

36% Full Time - 64% Part-time

35% Full Time - 65% Part-time

35% Full Time - 65% Part-time N/A Remains constant.

Apprentices Appointed within Quarter - All Authority

55 appointments since September

2009

11 (April - June) 73 appointments since September

2009

19 (July - Sept) 92 appointment

since September 2009

4 (Oct - Dec) 10 appointments

since September

2010

Minimum of 100 Apprenticeships between Sept 09 and Aug 10 (15% delivered through

SCRN)

N/A N/A

Total no of Apprentices - All Authority 354 (no leavers in Qtr 4)

370 (2 leavers in Qtr 1)

378 (11 leavers in Qtr 2)

375 (13 leavers in Qtr 3) 500 by 2011 N/A

% of Apprentices in Substantive Posts - All Authority 96% (340) 97% (358) 97% (367) 100% (377) 98% N/A

Ethnic minority representation in the workforce - All Authority 1.05% (243) 1.06% (243) 1.11% (252) 1.15% (265) Target 1.12% Same quarter last year 1.04% (236) of workforce came from a

BME background.

Census Working Age Population of NY - 13.66%

All Local Authorities Average - 3.8% (DLA

Piper W kf

Census Av Working Age Population of NY - 40.93

The target of acheiving 100 apprenticeships between 01 September 2009 and 31 Aug 2010 has not been achieved, with a shortfall of 8 opportunities. The provision of apprenticeship opportunities has decreased as the availability of band 1 - 4 posts has diminished due to reduced turnover and restructuring. Further partnerships with schools and the Supply Chain Readiness Network is required to maintain the minimum delivery of provision and the target will be adjusted on a rolling basis.

Average age for whole Authority remains the same but the workforce excluding schools has increased.

LGAR Survey 2006 Shire

County Split = 24% M 76% F

Census Working Age Population of NY - 17.85%

Increase Nos & % of Employees Aged Up to 25

Reduce Average Age at end 09/10

Section 6 Appendix - HR Framework 2010-11 - Q3 Page No 2

Performance Report - 2010/11 AppendixPerformance Improvement Plans

2009

/201

0

Qua

rter

1

Qua

rter

2

Qua

rter

3

Qua

rter

4

Dire

ctio

n of

Tr

avel

Performance

Targ

et/P

roje

cted

Out

turn2010/2011

Perf

orm

ance

D

efin

ition

Com

para

tor/

Perf

orm

ance

A

gain

st

othe

r C

ounc

ils

Ethnic minority representation in the workforce - Excluding Schools 1.26% (110) 1.31% (114) 1.34% (115) 1.40% (121) Target 1.12% Same quarter last year 1.23% (105) of workforce came from a

BME background.

Ethnic Minority Representation in the Workforce + White Other - All Authority 2.99% (690) 2.96% (678) 3.00% (683) 3.02% (698) N/A N/A Same quarter last year 2.97% (675) of workforce came from a

BME and White Other Background.

Ethnic Minority Representation in the Workforce + White Other - Excluding Schools

3.99% (349) 4.00% (347) 4.07% (350) 4.10% (355) N/A N/A Same quarter last year 3.96% (339) of workforce came from a BME and White Other Background.

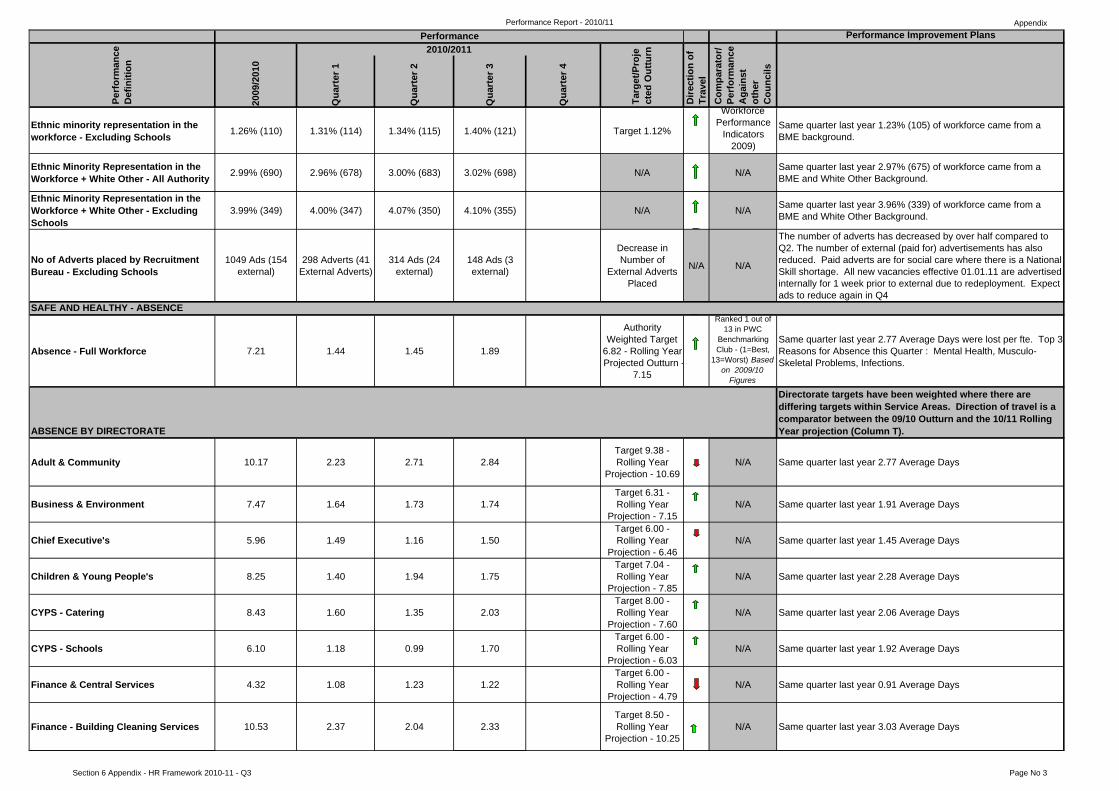

No of Adverts placed by Recruitment Bureau - Excluding Schools

1049 Ads (154 external)

298 Adverts (41 External Adverts)

314 Ads (24 external)

148 Ads (3 external)

Decrease in Number of

External Adverts Placed

N/A N/A

The number of adverts has decreased by over half compared to Q2. The number of external (paid for) advertisements has also reduced. Paid adverts are for social care where there is a National Skill shortage. All new vacancies effective 01.01.11 are advertised internally for 1 week prior to external due to redeployment. Expect ads to reduce again in Q4

Absence - Full Workforce 7.21 1.44 1.45 1.89

Authority Weighted Target

6.82 - Rolling Year Projected Outturn -

7.15

Ranked 1 out of 13 in PWC

Benchmarking Club - (1=Best,

13=Worst) Based on 2009/10

Figures

Same quarter last year 2.77 Average Days were lost per fte. Top 3 Reasons for Absence this Quarter : Mental Health, Musculo-Skeletal Problems, Infections.

Directorate targets have been weighted where there are differing targets within Service Areas. Direction of travel is a comparator between the 09/10 Outturn and the 10/11 Rolling Year projection (Column T).

Adult & Community 10.17 2.23 2.71 2.84Target 9.38 - Rolling Year

Projection - 10.69N/A Same quarter last year 2.77 Average Days

Business & Environment 7.47 1.64 1.73 1.74Target 6.31 - Rolling Year

Projection - 7.15N/A Same quarter last year 1.91 Average Days

Chief Executive's 5.96 1.49 1.16 1.50Target 6.00 - Rolling Year

Projection - 6.46N/A Same quarter last year 1.45 Average Days

Children & Young People's 8.25 1.40 1.94 1.75Target 7.04 - Rolling Year

Projection - 7.85N/A Same quarter last year 2.28 Average Days

CYPS - Catering 8.43 1.60 1.35 2.03Target 8.00 - Rolling Year

Projection - 7.60N/A Same quarter last year 2.06 Average Days

CYPS - Schools 6.10 1.18 0.99 1.70Target 6.00 - Rolling Year

Projection - 6.03N/A Same quarter last year 1.92 Average Days

Finance & Central Services 4.32 1.08 1.23 1.22Target 6.00 - Rolling Year

Projection - 4.79N/A Same quarter last year 0.91 Average Days

Finance - Building Cleaning Services 10.53 2.37 2.04 2.33Target 8.50 - Rolling Year

Projection - 10.25N/A Same quarter last year 3.03 Average Days

ABSENCE BY DIRECTORATE

Workforce Performance

Indicators 2009)

SAFE AND HEALTHY - ABSENCE

Section 6 Appendix - HR Framework 2010-11 - Q3 Page No 3

Performance Report - 2010/11 AppendixPerformance Improvement Plans

2009

/201

0

Qua

rter

1

Qua

rter

2

Qua

rter

3

Qua

rter

4

Dire

ctio

n of

Tr

avel

Performance

Targ

et/P

roje

cted

Out

turn2010/2011

Perf

orm

ance

D

efin

ition

Com

para

tor/

Perf

orm

ance

A

gain

st

othe

r C

ounc

ils

Absence - Short Term (1-7 Days) New Indicator New Indicator 23% 31% N/A N/A N/A

Absence - Medium Term (8-30 Days) New Indicator New Indicator 22% 20% N/A N/A N/A

Absence - Long Term (31+ Days) New Indicator New Indicator 55% 49% N/A N/A N/A

Average Length of Absence New Indicator New Indicator 4.20 Days 3.23 Days N/A N/A

All Local Authorities Average - 6.3 Days

(DLA Piper Workforce Performance Indicators

2010)

Average length of absence has reduced in line with the increase in number of short-term absences during the quarter.

Reported injuries, diseases & dangerous occurrences per 1000 employees per year

2.50 (61 Reportable Employee Incidents)

0.69 (17 Reportable Employee Incidents)

0.20 (5 Reportable Employee Incidents)

0.64 (16 Reportable Employee Incidents

Reduction on 09/10 Figure N/A

This is one of the measures of effectiveness of NYCC's health and safety procedures. It is based on the RIDDOR Regulations 1995 which requires the reporting of work-related accidents, diseases and dangerous occurrences.

Members Appeals (AC), Employment Tribunals (ET), Appeals Against Redundancy (AR) and Appeals Against Ill-Health (IHA)

8 AC 3 ET 2 AC 0 ET 0 AC 2 ET0 AC 1 ET 1 x

Attendance Appeal

N/A N/A N/AOne ET was held this quarter and the outcome is awaited. There was one manager appeal against attendance which was not upheld.

Number of Grievances/Apps of Resolving Issues at Work (RIAW)

5 RIAW Grievances - 32

Formal 7 Informal

1 RIAW Grievances - 4

Formal 2 Informal

3 RIAW Grievances - 2

Formal 4 Informal

0 RIAW Grievances - 4

Formal 3 Informal

N/A N/A N/A Number of grievances remain small compared to the workforce.

Union Membership (Excludes Teaching Staff)

Unison 19% : GMB 1.10%

Unison 20% : GMB 1.09%

Unison 20% : GMB 1.10%

Unison 20% : GMB : 1.12% N/A N/A N/A Slight increase in GMB membership this quarter.

Cost of Agency Staff as % of Total Pay Bill

£3.57m (1.33% Excluding

Teachers Pay Bill, 0.73% including

Teachers Pay Bill)

N/A N/A Comment will be made on an annual basis.

MODERNISATION AND CHANGE TO IMPROVEANNUAL STATISTICS

Short-term absence has increased this quarter with a reduction in long term absence.

Annual Report

ENGAGING WITH STAFF

Section 6 Appendix - HR Framework 2010-11 - Q3 Page No 4

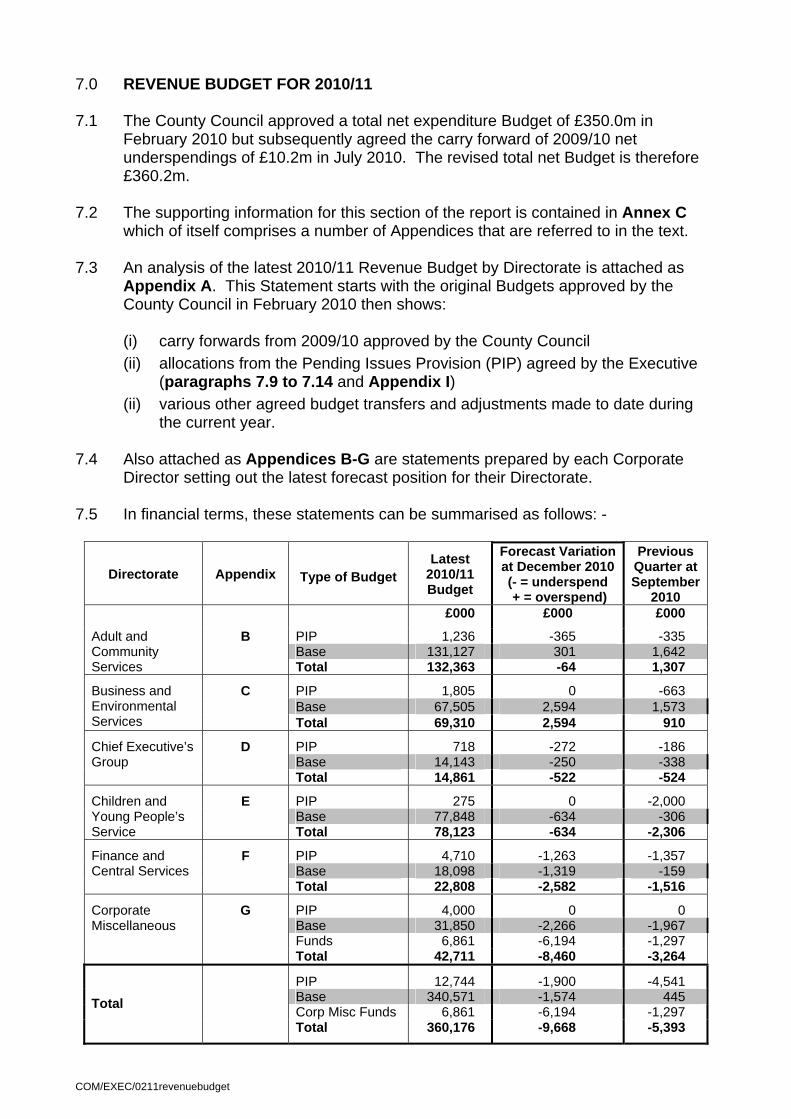

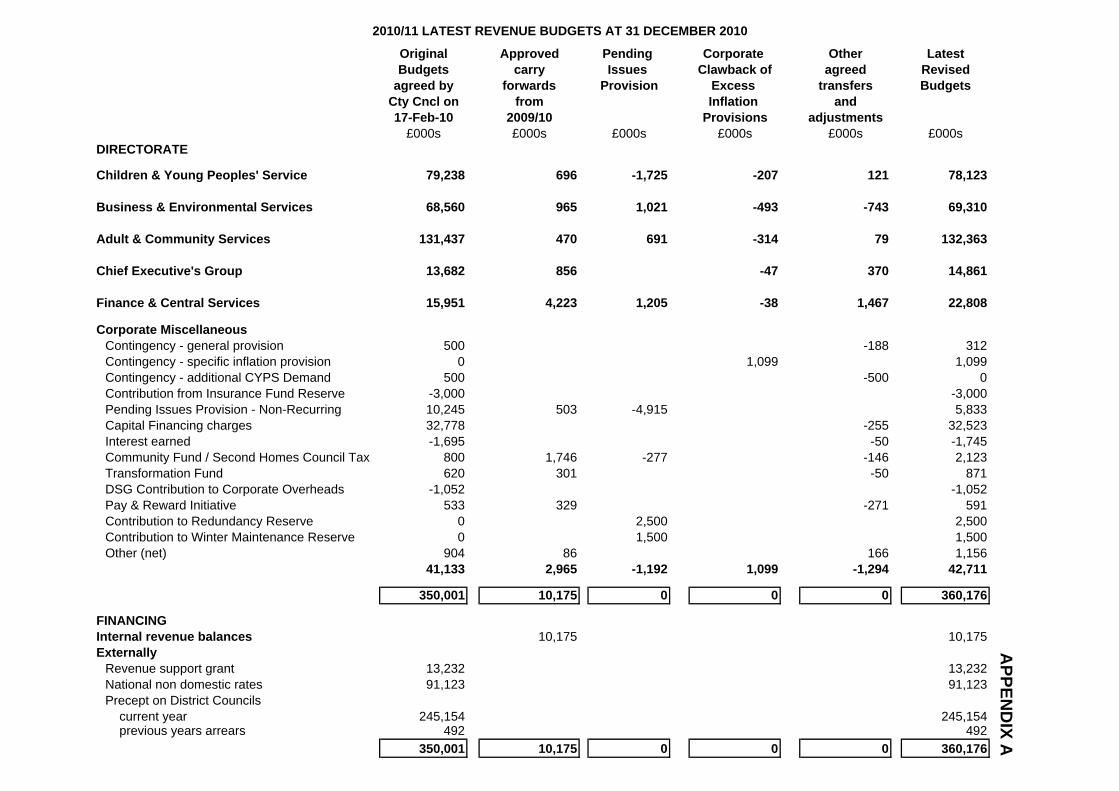

7.0 REVENUE BUDGET FOR 2010/11 7.1 The County Council approved a total net expenditure Budget of £350.0m in

February 2010 but subsequently agreed the carry forward of 2009/10 net underspendings of £10.2m in July 2010. The revised total net Budget is therefore £360.2m.

7.2 The supporting information for this section of the report is contained in Annex C

which of itself comprises a number of Appendices that are referred to in the text. 7.3 An analysis of the latest 2010/11 Revenue Budget by Directorate is attached as

Appendix A. This Statement starts with the original Budgets approved by the County Council in February 2010 then shows:

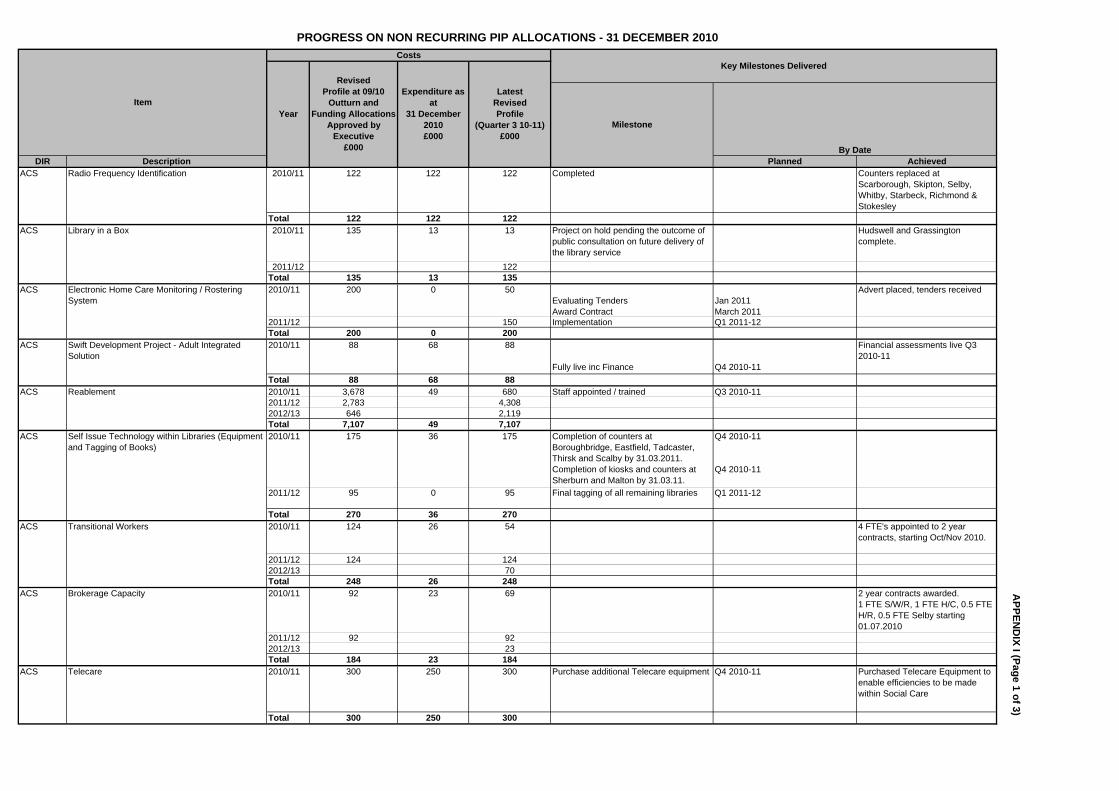

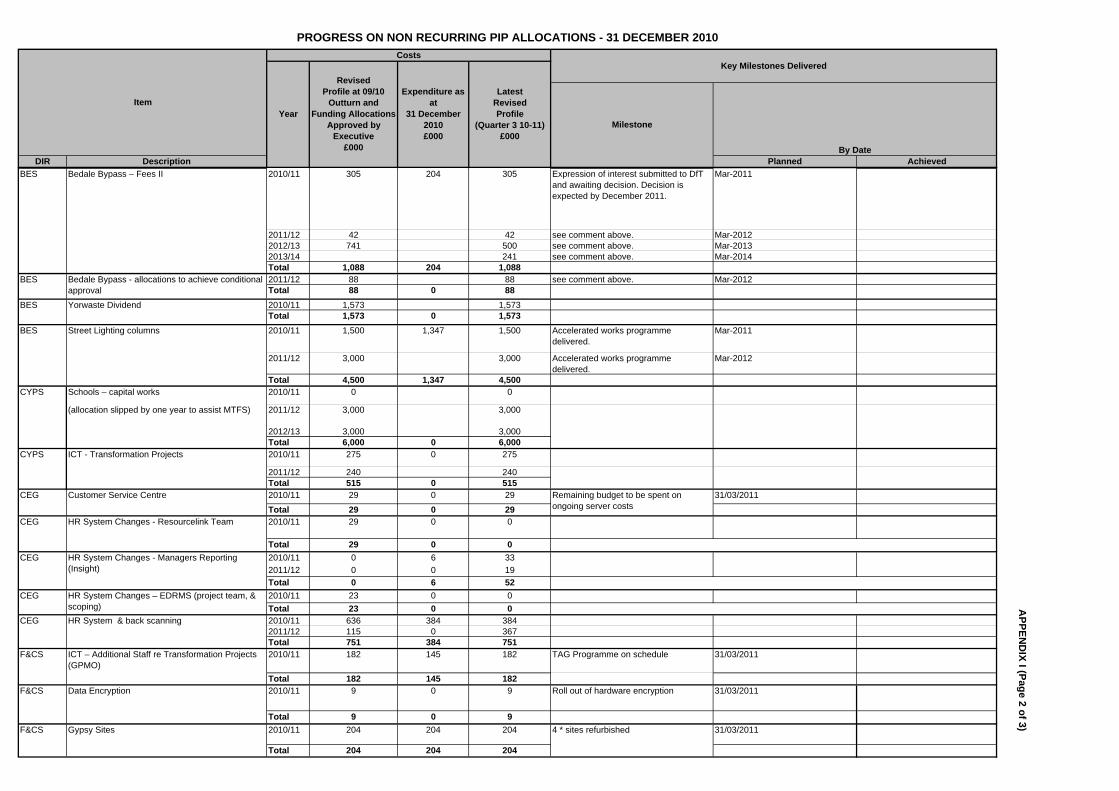

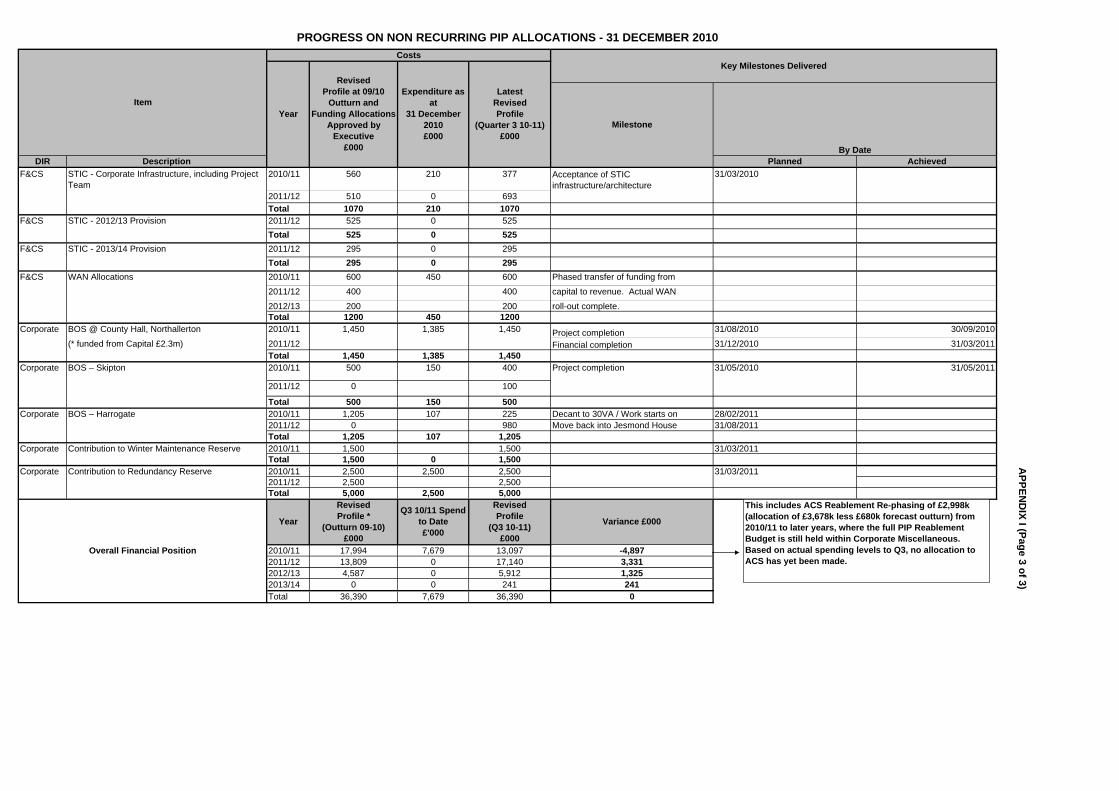

(i) carry forwards from 2009/10 approved by the County Council (ii) allocations from the Pending Issues Provision (PIP) agreed by the Executive

(paragraphs 7.9 to 7.14 and Appendix I) (ii) various other agreed budget transfers and adjustments made to date during

the current year. 7.4 Also attached as Appendices B-G are statements prepared by each Corporate

Director setting out the latest forecast position for their Directorate. 7.5 In financial terms, these statements can be summarised as follows: -

Directorate Appendix Type of Budget Latest

2010/11 Budget

Forecast Variation at December 2010 (- = underspend + = overspend)

Previous Quarter at September

2010 £000 £000 £000

B PIP 1,236 -365 -335 Base 131,127 301 1,642

Adult and Community Services Total 132,363 -64 1,307

C PIP 1,805 0 -663 Base 67,505 2,594 1,573

Business and Environmental Services Total 69,310 2,594 910

D PIP 718 -272 -186 Base 14,143 -250 -338

Chief Executive’s Group

Total 14,861 -522 -524

E PIP 275 0 -2,000 Base 77,848 -634 -306

Children and Young People’s Service Total 78,123 -634 -2,306

F PIP 4,710 -1,263 -1,357 Base 18,098 -1,319 -159

Finance and Central Services

Total 22,808 -2,582 -1,516

G PIP 4,000 0 0 Base 31,850 -2,266 -1,967 Funds 6,861 -6,194 -1,297

Corporate Miscellaneous

Total 42,711 -8,460 -3,264

PIP 12,744 -1,900 -4,541 Base 340,571 -1,574 445 Corp Misc Funds 6,861 -6,194 -1,297 Total

Total 360,176 -9,668 -5,393

COM/EXEC/0211revenuebudget

7.6 The following paragraphs explain the variances shown above.

Projected Variances

7.7 Comments on the forecast variance for each Directorate is as follows:-

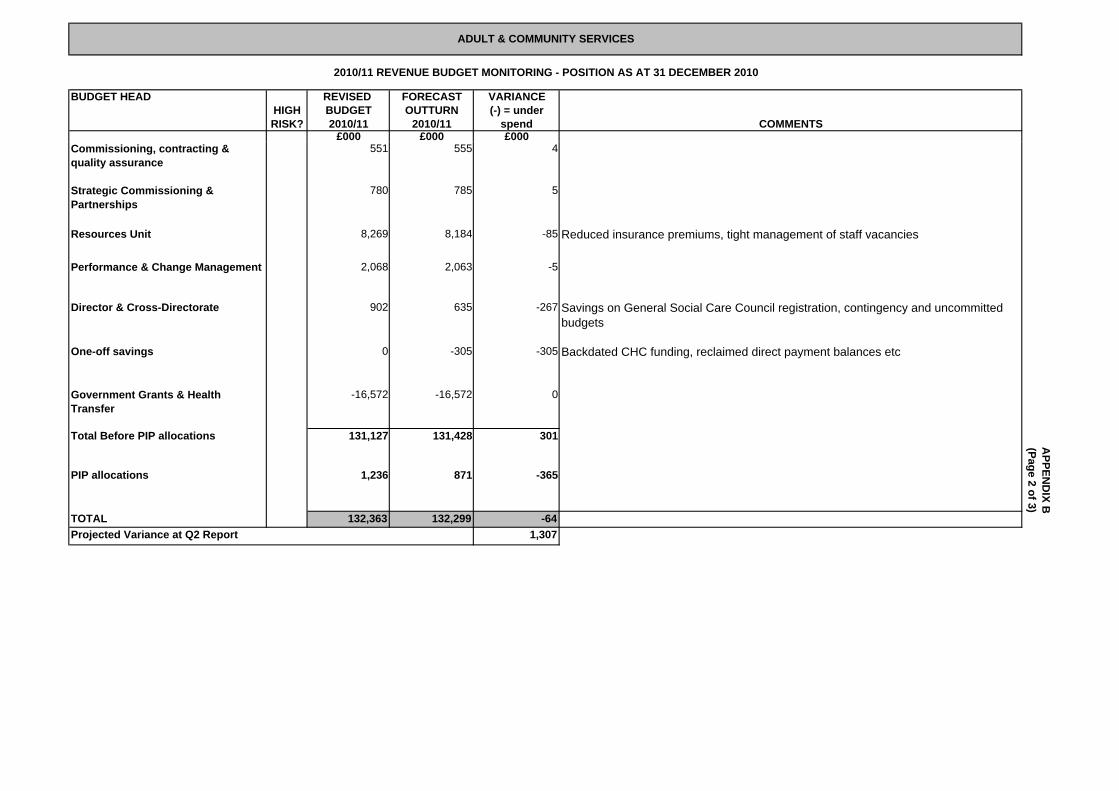

(a) Adult and Community Services Adults and Communities Services (ACS) has a revised budget of £132,363k which includes the one-off allocations of PIP monies. The projected expenditure included in Appendix B takes account of the current service pressures and trends and projects these to the financial year end. If these levels of service continue to run at the current levels, the outturn position at the 31st March is estimated to be £132,299k. The overall £64k underspend consists of £365k unspent PIP funding being carried forward to 2011/12 and a remaining £301k (0.2%) overspend against the base budget. Compared with the figures reported at Q2, and excluding the potential impact of ordinary residence cases (see below), this represents a reduction in the projected overspend of more than £1.3m reflecting the vigorous management action to reduce costs. The most significant pressure on the ACS budget continues to be the high levels of demand for social care services largely driven by demographic pressures, in particular the growth in the numbers of older people and people with learning disabilities requiring service. To offset these pressures a number of measures have been taken:- (i) a programme of efficiency savings over and above the VFM budget target

has been identified and ‘re-cycled’ into social care operations (ii) an intensive programme of service reviews has been initiated which has

already released significant cash savings (iii) linked to (ii) PIP monies are being used to increase the cost effectiveness

of service delivery through the development of re-ablement services and use of facilities such as telecare

(iv) a re-emphasis on rigorous ‘gatekeeping’ of services including senior

management approval of care packages, use of placement panels etc (v) concerted action to ensure external funding is maximised However one of the other major risks to the social care budget is the incidence of ordinary residence challenges. These are where social care clients, originally from other local authority areas, have moved to North Yorkshire and live in their own accommodation. Because of financial pressures local authorities are now seeking to argue that these individuals are ordinarily resident in North Yorkshire and therefore responsibility for funding their care falls to the County Council.

COM/EXEC/0211revenuebudget

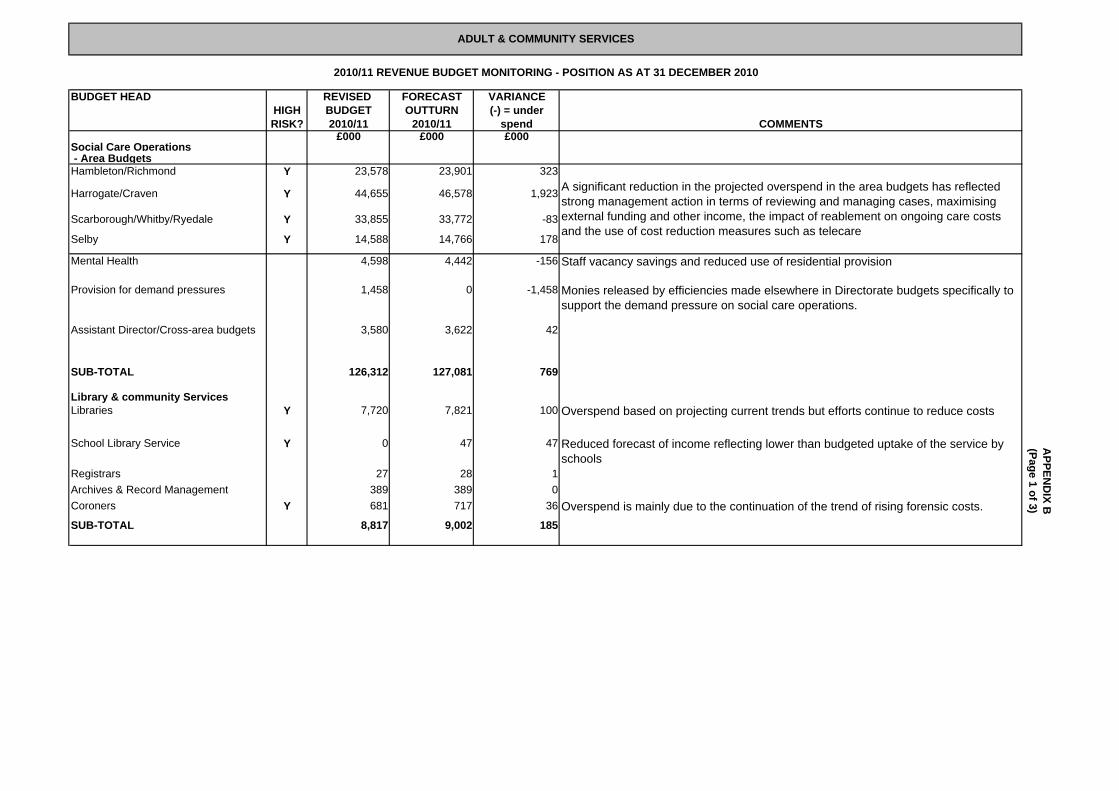

Where cases have been decided the financial impact is included in the main projections but in addition a number of other cases are currently in dispute and the possible ongoing impact on the base budget of these is included as a memo item in Appendix B. It should be emphasised that these are just the cases currently in process but the total costs of all the potential cases would be very significantly higher. Work is ongoing to identify the potential liability for NYCC. Elsewhere the main concern is within the Libraries and Community Services unit. On the core library service a projected overspend of £100k is a result of a number of factors but in particular the decision not to reduce the mobile fleet at this point in time although this was identified as one of the budget savings for the service and the budget reduced accordingly. On the School Library Service, compared to the position at Q2, there has been a small reduction in the projected overspend reflecting downwards pressure on the costs of the operation. Further discussions are taking place with CYPS to discuss the long term funding of the service.

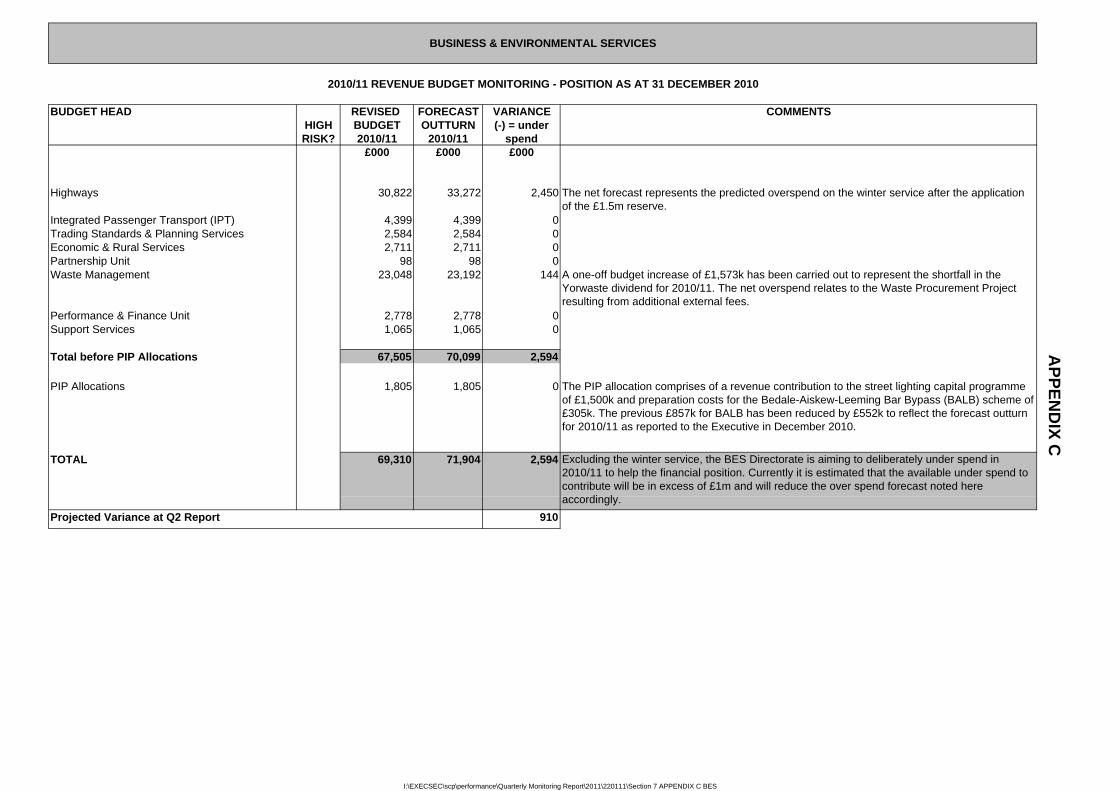

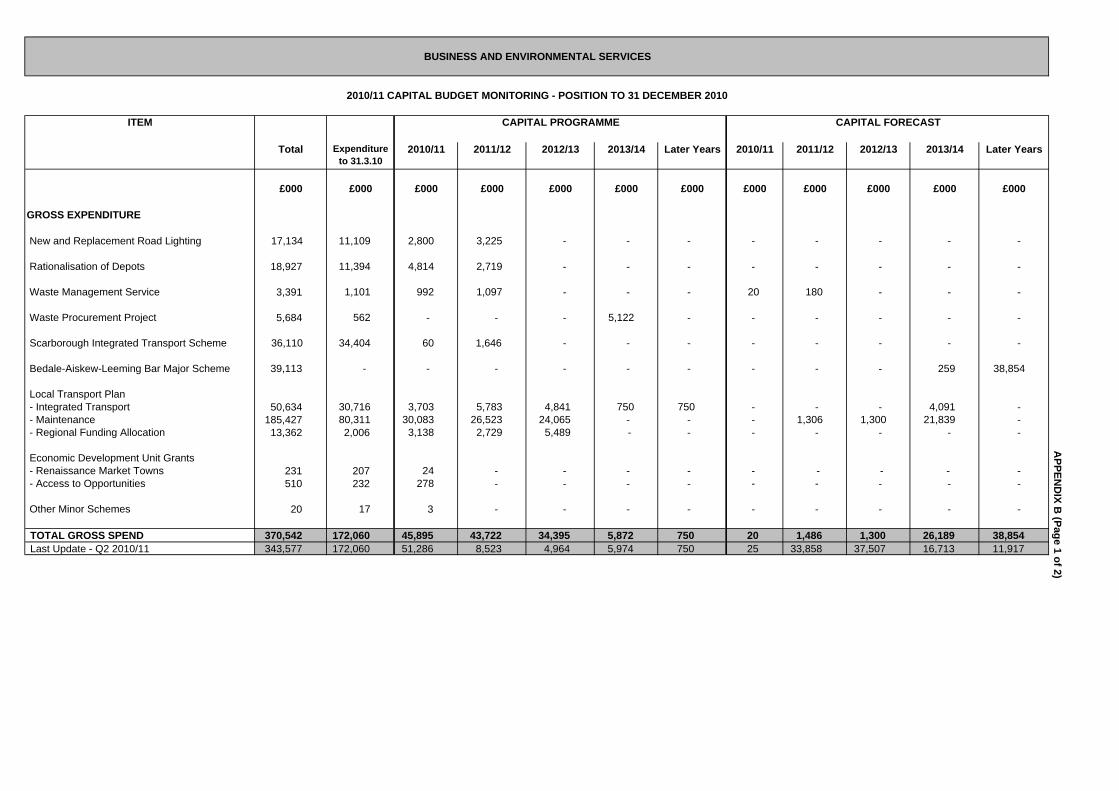

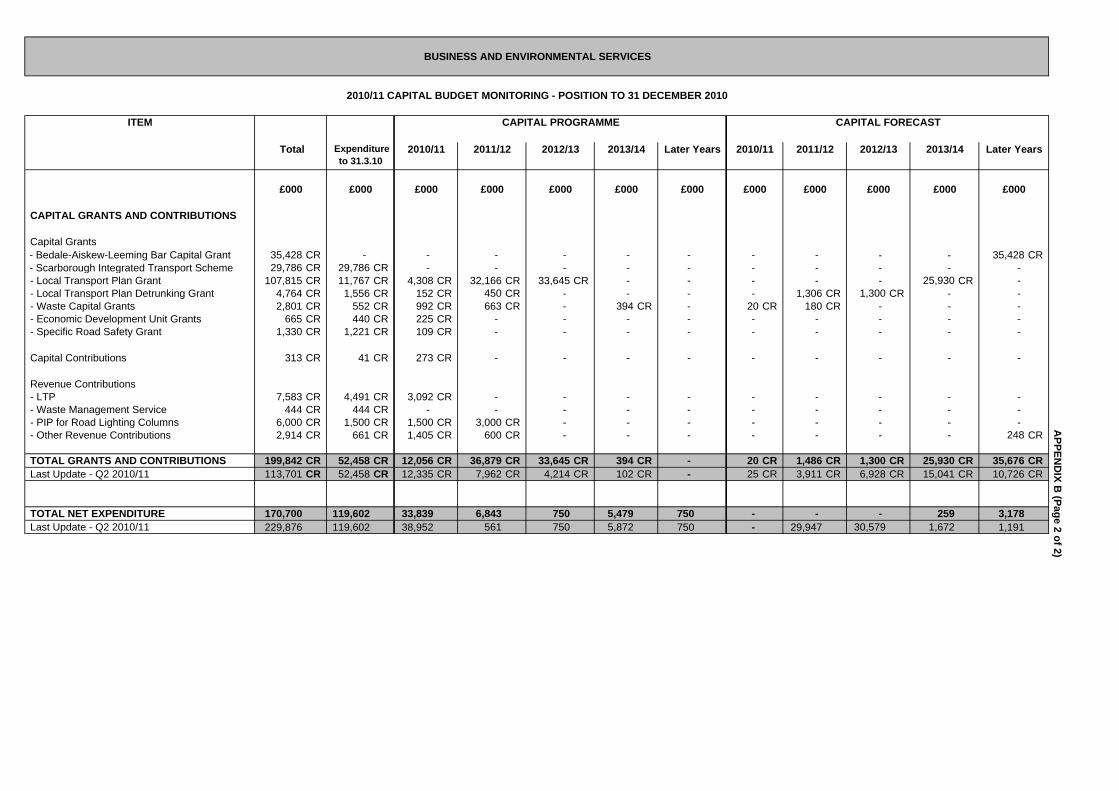

(b) Business and Environmental Services

The forecast position is an overspend of £2,594k, of which the winter service accounts for £2,450k after the application of the Reserve of £1,500k referred to below. However, excluding the winter service, BES is aiming to deliberately under spend in 2010/11 to help the overall financial position of the County Council, whilst recognising that there are other cost pressures which the Directorate is looking to contain within existing resources. Currently it is estimated that the available underspend to contribute will be in excess of £1m and will reduce the above overspend forecast accordingly. This approach will reduce the potential claim on the GWB for the ‘overspend’ on the winter service (see paragraph 7.19 et seq). The overspend for the winter service is due to weather conditions experienced during this season as at 23 January 2011. The forecast is subject to change as the season continues. The winter service Reserve was fully utilised last financial year but as part of the Q1 report the Executive approved a contribution of £1.5m to re-establish the Reserve, - however as indicated above this will be fully utilised in 2010/11. Based on expenditure incurred in the current and previous winters the longer term aim is to build the Reserve to £2.5m. The Directorate continues to prioritise highway maintenance works to deal with damage to the network resultant from severe winter conditions experienced in 2009/10. A works package of £10.5m is in place funded from both revenue and capital budgets. The total estimate of damage remaining from 2009/10 is £23m but it should be noted however that the value of additional damage resulting from 2010/11 winter conditions is yet to be quantified indicating that further funding from future budgets will be directed to the repair efforts. The remaining net overspend forecast of £144k relates to additional external fees for the waste procurement project.

COM/EXEC/0211revenuebudget

The Q2 report noted an over spend of £1,573k due to the loss of Yorwaste dividend for 2010/11. A budget transfer of £1,573k (increase for BES) has been effected from Corporate Miscellaneous (PIP) in Q3 to fund this shortfall. Further assessments of the Waste Management budget have been carried out which confirm the position reported to the Executive at Q2. The forecast position on the waste budget is subject to change given its volatile nature albeit this should diminish as the financial year progresses; close monitoring of the position will continue. Forecast expenditure on the PIP funded Bedale-Aiskew-Leeming Bar Bypass (BALB) scheme for 2010/11 is £305k. This is £552k below the PIP allocation this year.

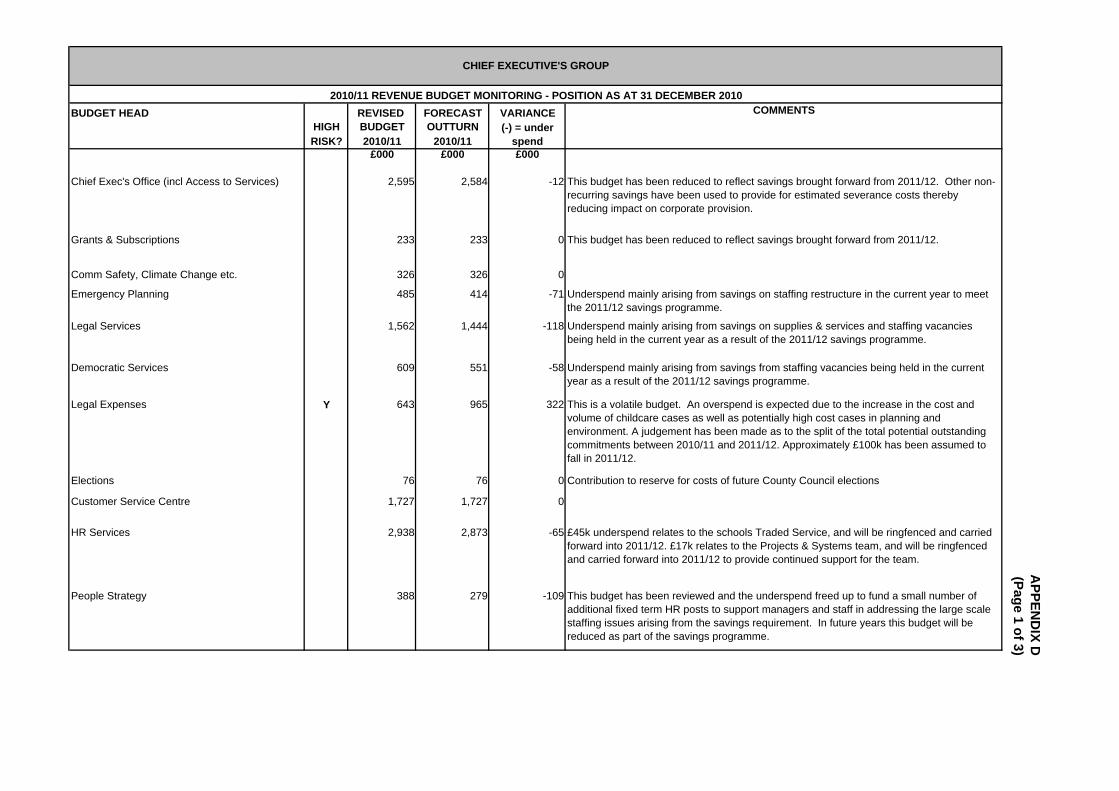

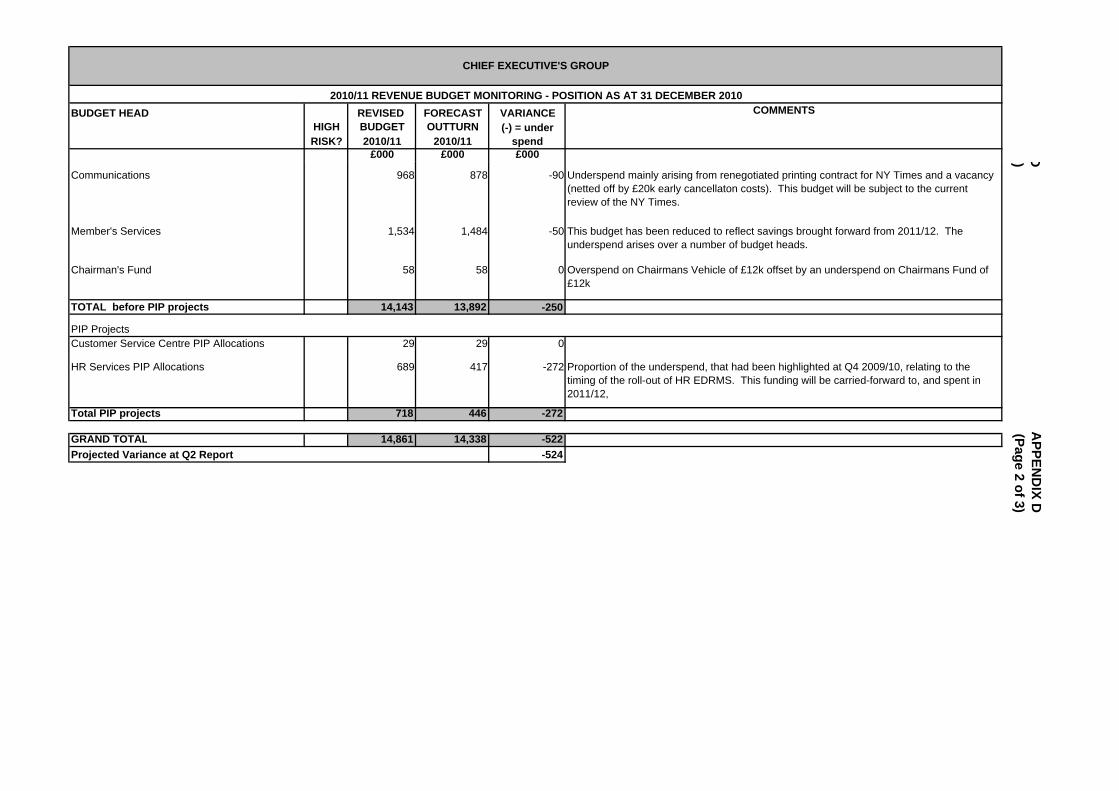

(c) Chief Executive’s Group

The forecast net underspend on Chief Executive’s Group at Q3 is £522k. Once adjusted for the reprofiling of one-off projects funded by the PIP (£272k) the effective forecast underspend against base Budget is £250k. The budgets for Chief Executive’s Office, Grants & Subscriptions and Members Services have been reduced by £100k to reflect savings within the CEG programme that have been brought forward from 2011/12. A large proportion of the forecast saving is due to staffing vacancies in the current year as managers seek to hold vacancies as part of the savings strategy. Savings have been used to provide for severance costs (thereby reducing the impact on any corporate fund for severance) and to support one-off activity that will allow HR services to implement change which will deliver further savings in later years. The Legal Expenses budget continues to be volatile and is forecast to overspend due to a number of potentially high cost court cases. A judgement has been made as to whether the total potential outstanding commitments will fall in 2010/11 or 2011/12. Approximately £100k has been assumed to fall in 2011/12. Although no expenditure is expected against the Elections budget in 2010/11, funding will be put into a reserve to contribute to the costs of the next County Council Elections.

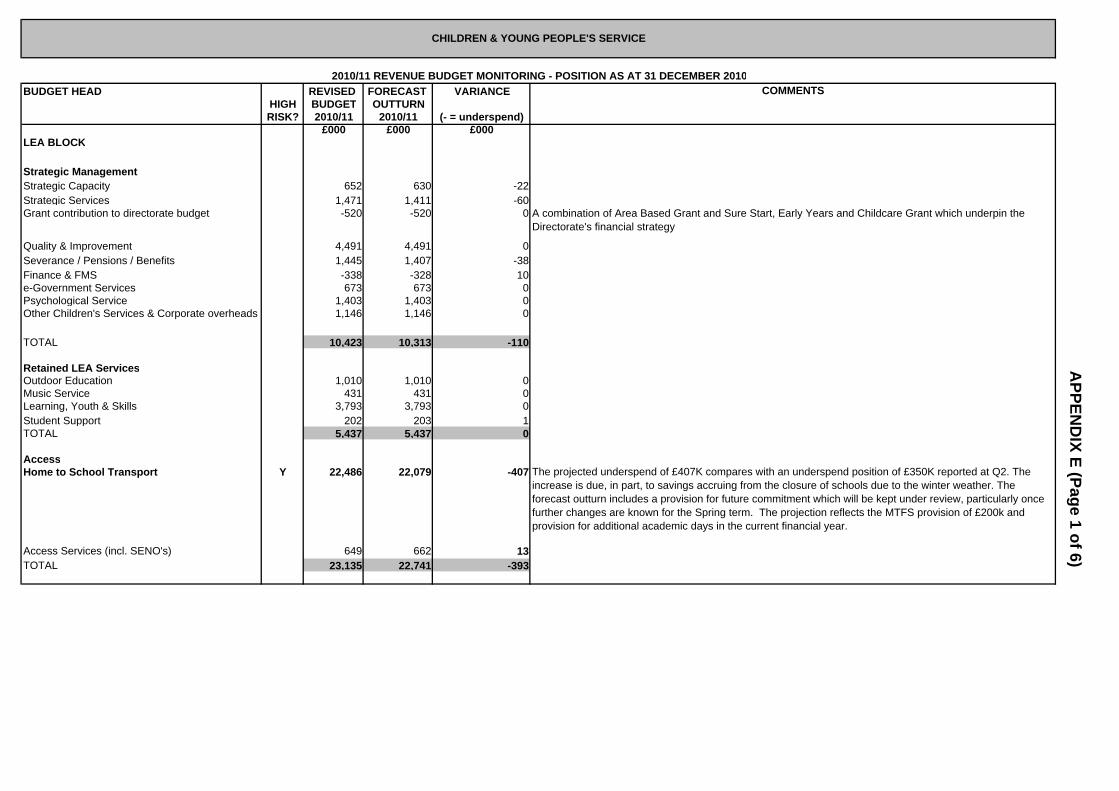

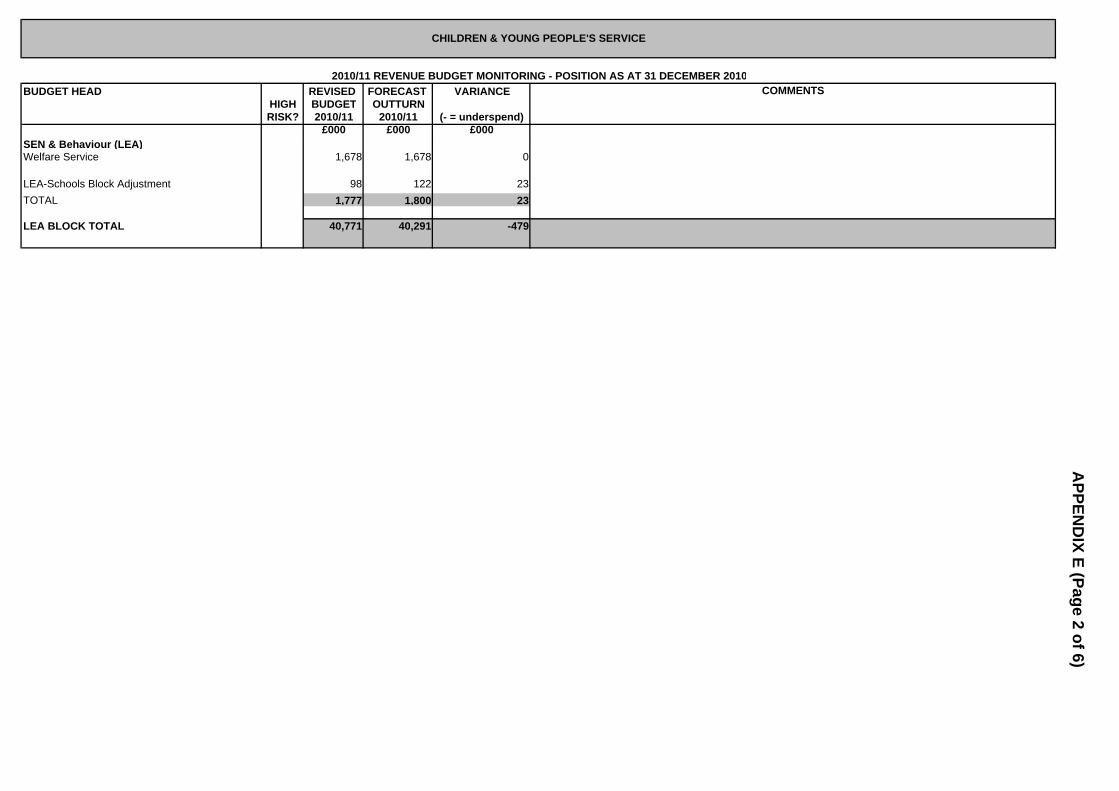

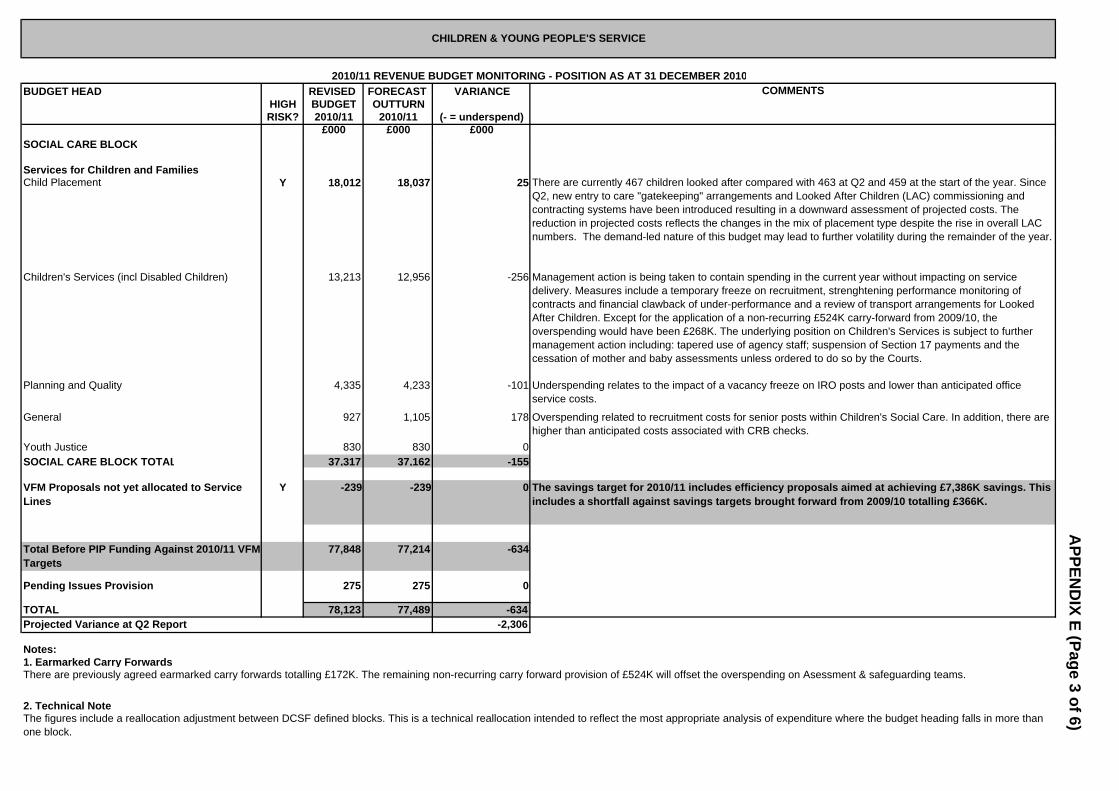

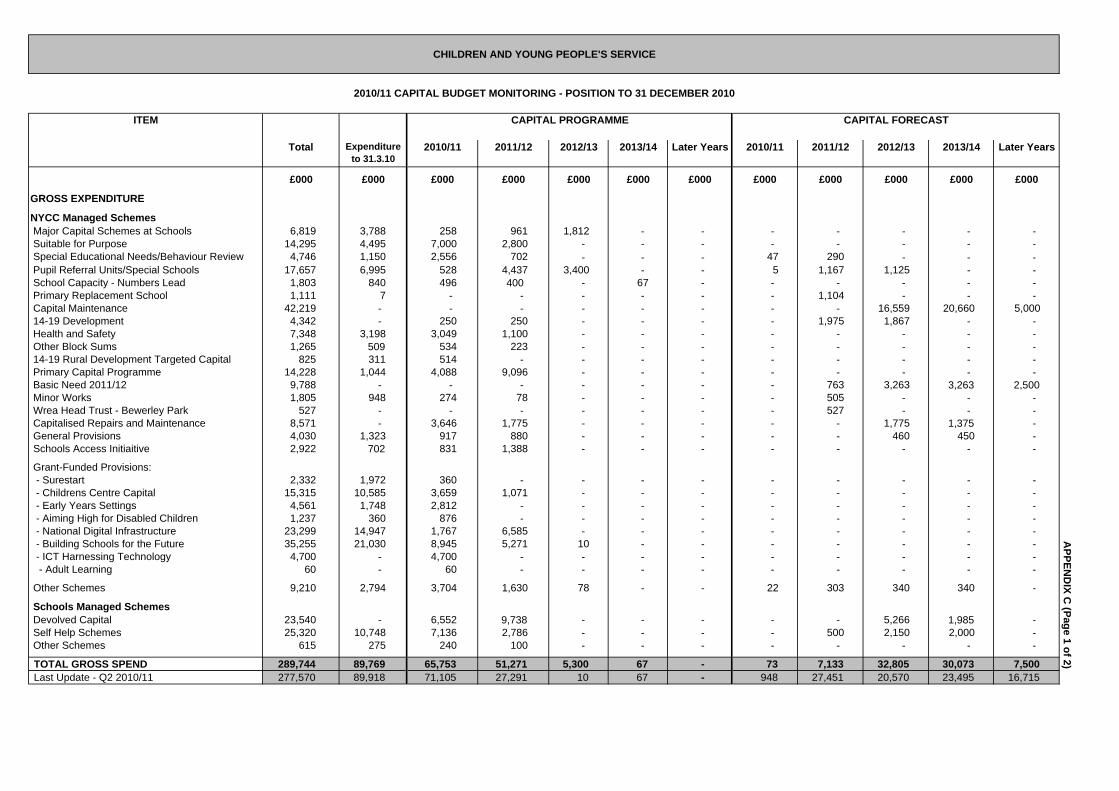

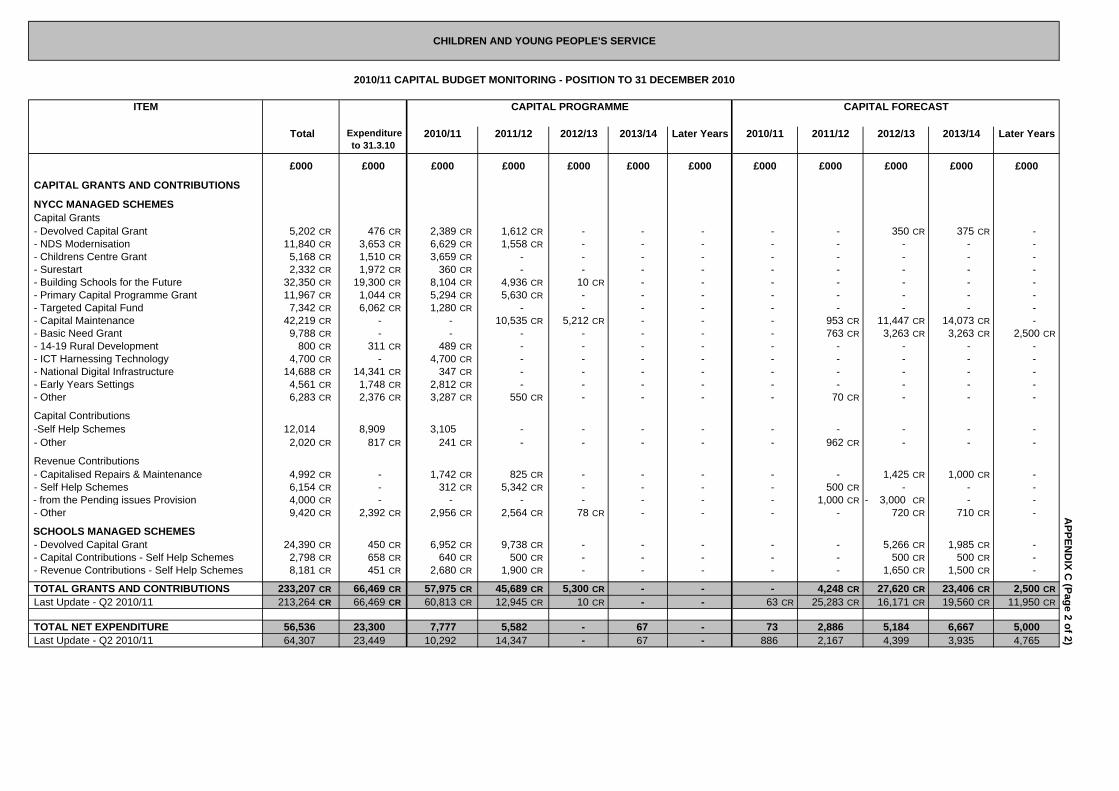

(d) Children and Young People’s Service

(i) Local Authority Block Overall the projected underspending at Q3 is £634k compared with a forecast underspend at Q2 of £306k – representing an increase in underspending of £328k. These projections exclude the non-recurring £2m PIP originally agreed for capital investment and subsequently earmarked to support CYPS Revenue budgets up to Q2. The Directorate has decided in Q3 not to use this allocation in 2010/11 for revenue purposes and it has therefore been re-phased into 2011/12 for investment in Directorate co-location which is needed to secure efficiency savings via integration.

COM/EXEC/0211revenuebudget

The latest assessment of spending against Children’s Social Care budgets indicates that management action has helped to contain costs in the current year. Overall, these measures have helped to reduce the projected overspending of £584k at Q2 to a projected overspend of £369k – a reduction of £215k. In particular, new “gatekeeping” arrangements around children entering the care system have had a significant impact. There are currently 467 looked after children which represents an increase of 4 compared with Q2 and an increase of 8 compared to the commencement of the year. While overall numbers have increased, changes in the way children’s needs are matched to placement type are reflected by a mix of care which represents better value for money. The Children’s Social Care budget – excluding placements and services for disabled children – is showing an overspend of £268k. However, after the application of the entire £524k earmarked reserve for non-recurring social care costs this shows an underspend of £256k within the headline figure above. This reduced call on the reserve for 2010/11 is due to management action to reduce spending in Assessment & Safeguarding teams. This includes: a temporary freeze on all recruitment; restriction of Children in Need payments, and; cessation of the use of agency staff, balancing the need to address the underlying budgetary position and manage child welfare risks. However there may be additional non-recurring and recurring pressures on this budget in 2011/12. The projected underspend on Home to School Transport is £407k compared with £350k at Q2 – an increase in underspending of £57k. While the daily rate of contract prices has increased by over £900 a day, reflecting the network changes from September, this is offset by savings accruing from school closures due to winter weather. £300k of this underspend has already been offered up as a recurring MTFS saving from 2011/12. The CYPS MTFS savings strategy equals £7,386k: a significant financial challenge to the Directorate. As part of the savings strategy CYPS will use some reserves carried forward from previous years and specifically earmarked to achieve the cash targets before recurring savings are implemented in full from 1 April 2011. Therefore the current projection, will deliver the full £7.386m savings plus £300k recurring from 2011/12, which is reflected in the outturn underspend in 2010/11. In addition a Home to School Transport contingency of £300k has been set aside to deal with one off issues and the latest position suggests that this will not be called on during 2010/11.

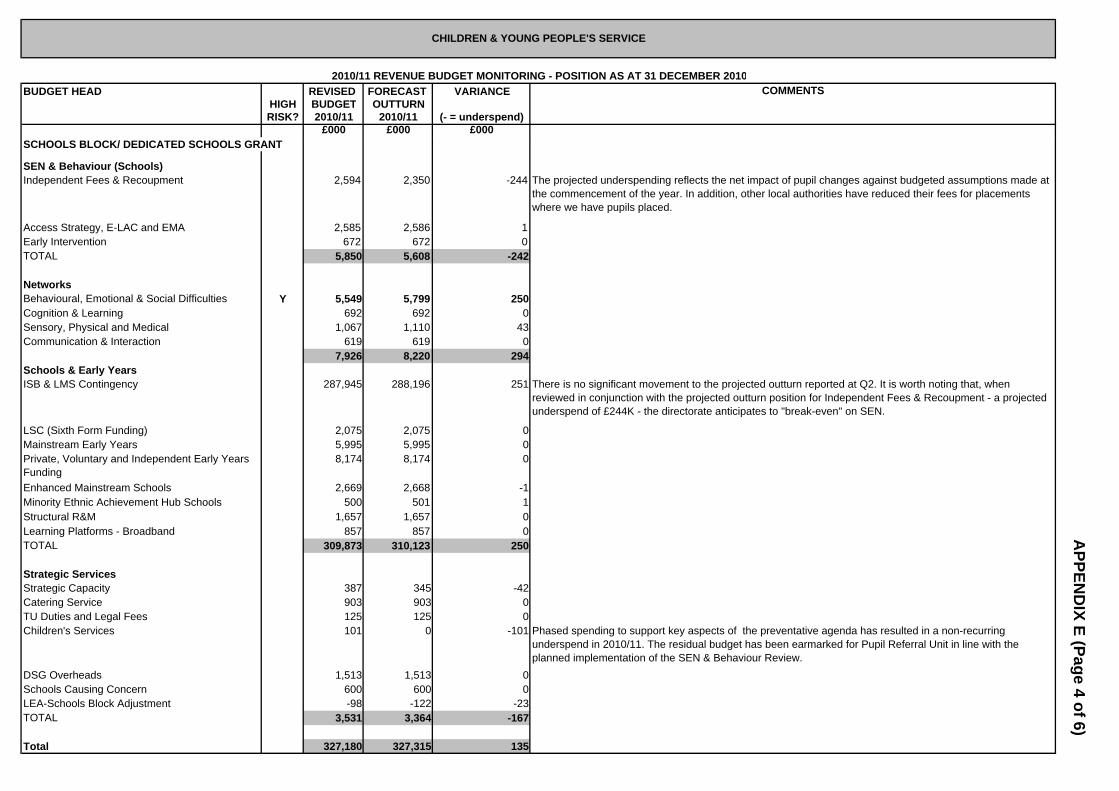

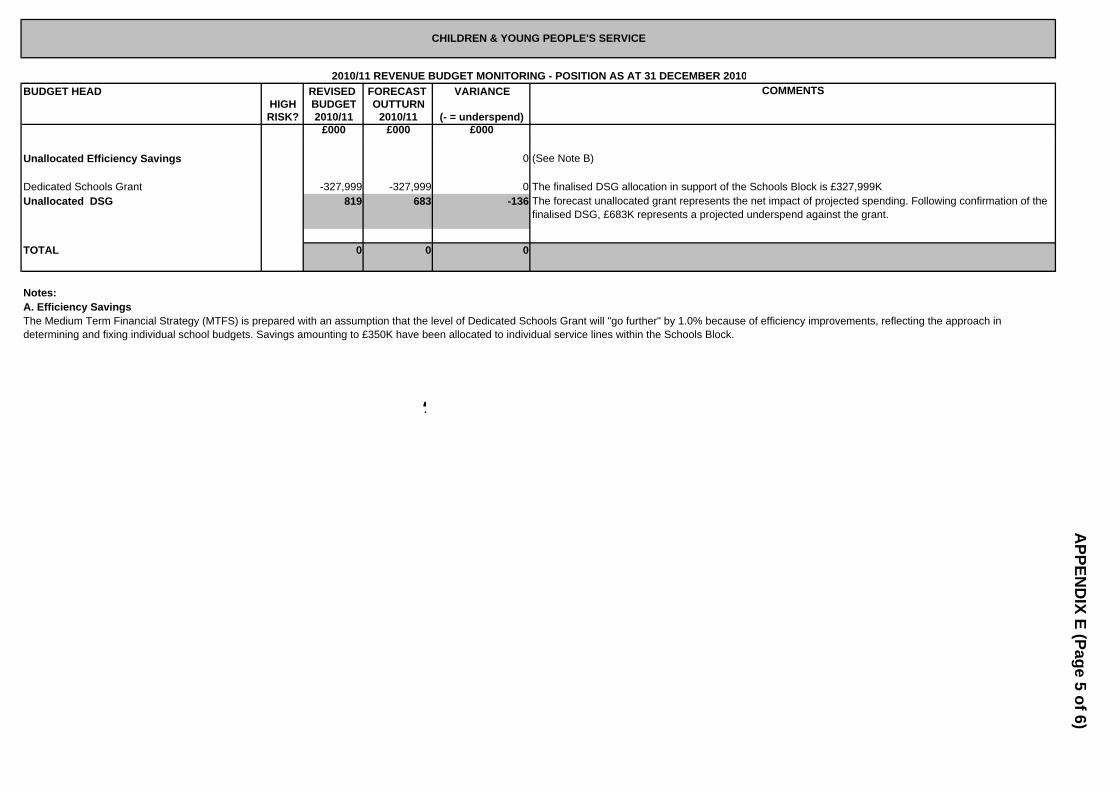

(ii) Schools Block Dedicated Schools Grant (DSG) is used to fund the Schools Block. Currently, there is a projected net overspend on the Schools Block of £136k which, if confirmed, would reduce the unallocated DSG to £683k. This represents a small contingency (0.2%) in relation to a ring-fenced grant of £328m.

COM/EXEC/0211revenuebudget

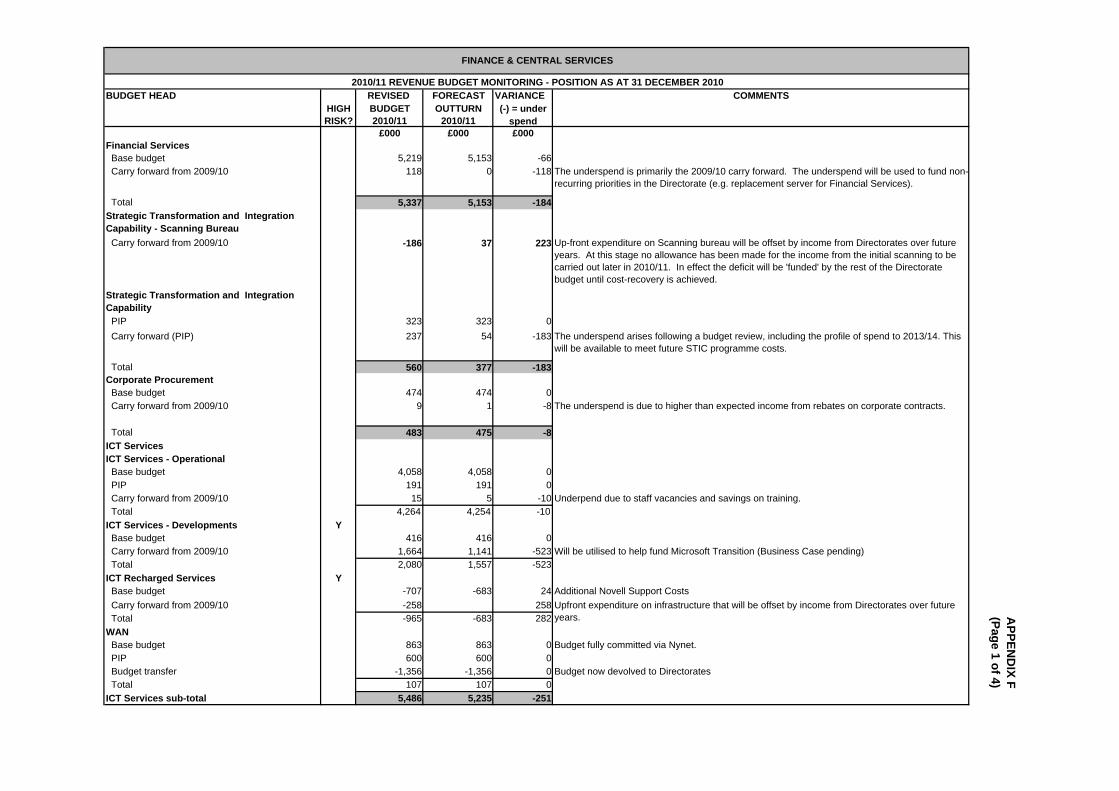

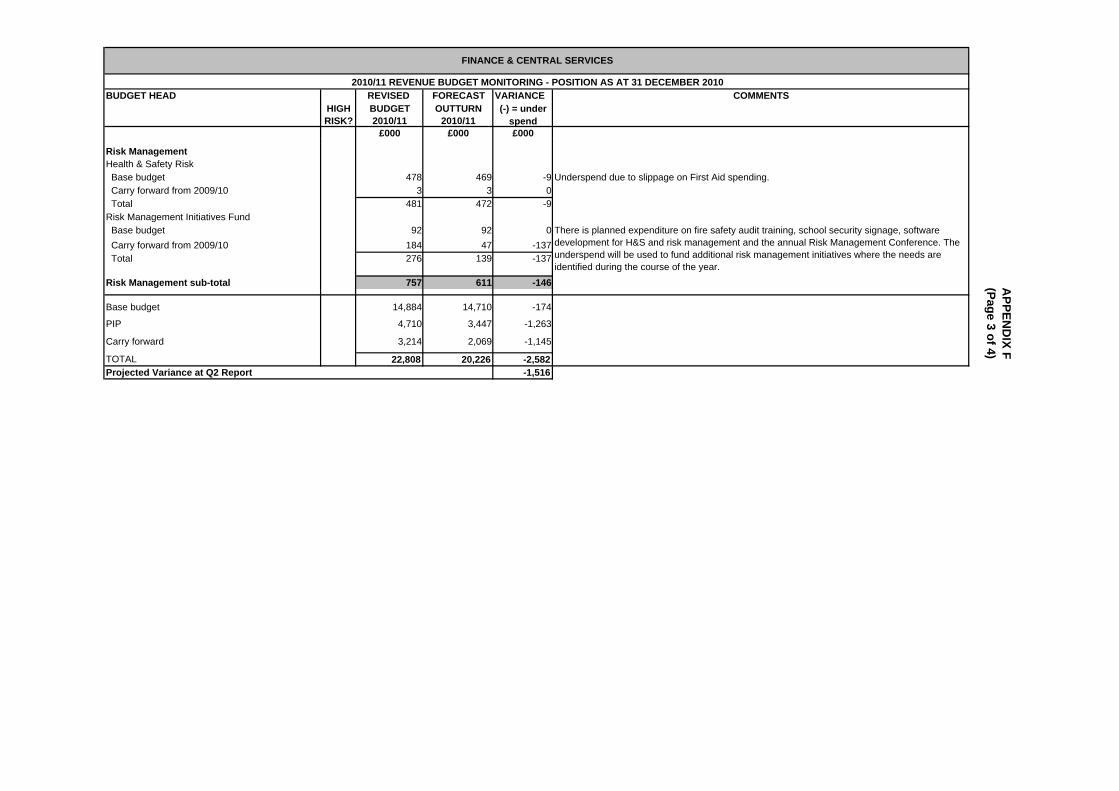

(e) Finance and Central Services

There is an overall forecast underspend of £2,582k of which £174k relates to recurring base budget provision; of the remainder £1,263k relates to PIP funded projects (primarily Harrogate BOS) and £1,145k relates chiefly to committed property and ICT related projects for which funds have been specifically allocated. These projects have either been delayed or in the case of ICT ‘stopped’ pending the outcome of a strategy review. The main items making up this sum are: (i) a potential underspend against Financial Services of £184k mainly due to

the carry-forward from 2009/10; this will be used to fund non-recurring priorities within the Directorate (eg replacement of server for Oracle Financials)

(ii) a planned overspend of £223k relating to the Scanning Bureau which will

be offset by income from Directorates over future years (iii) following a project review, a ‘managed’ £183k underspend on the core

STIC budget for system infrastructure. This will be available to meet future STIC programme costs

(iv) a forecast net underspend on ICT Services of £251k primarily relating to

the phasing of development projects (£523k) offset by £282k planned overspend on infrastructure investment (eg servers and storage) that will be offset by contributions from Directorates in future years

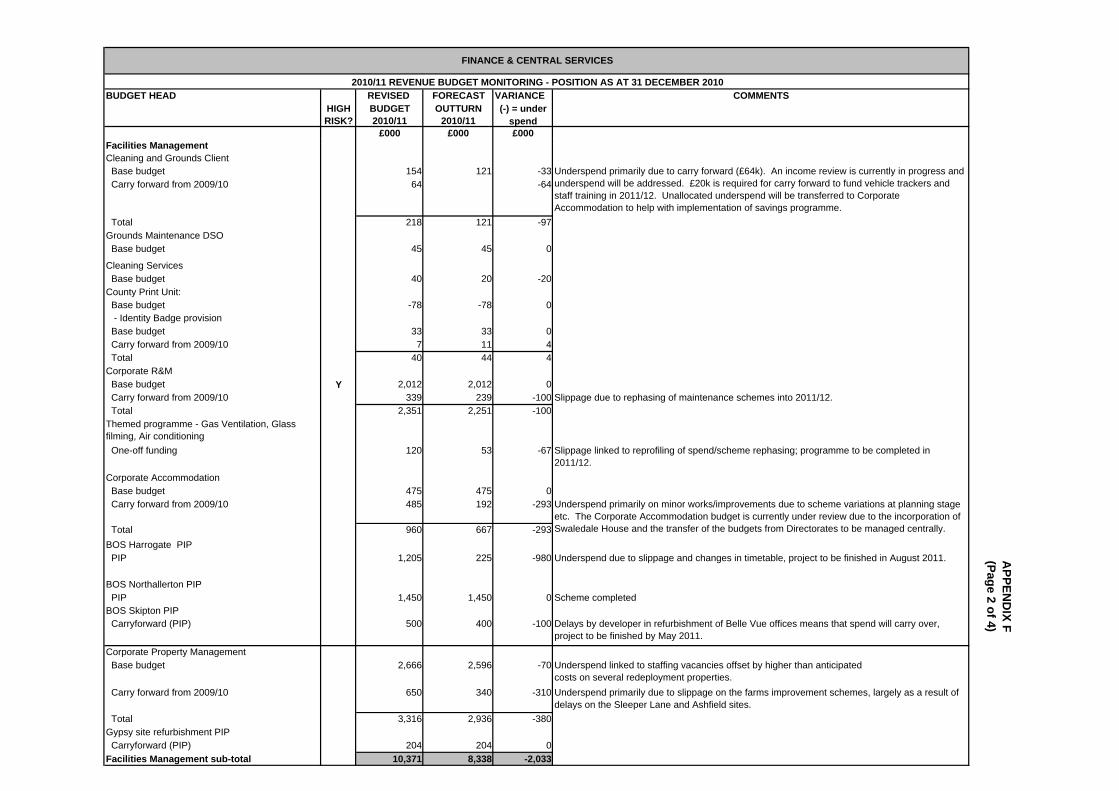

(v) a forecast underspend of £100k on Corporate Repairs and Maintenance

due to rephasing of maintenance schemes into 2011/12 following the bad weather in November/January period

(vi) a forecast underspend of £293k primarily on minor improvements against

the Corporate Accommodation budget due to individual on site scheme delays

(vii) a forecast underspend of £980k on Harrogate BOS due to scheme

rephasing. This PIP funding will be carried forward to fund the completion of the scheme in 2011/12. Also in the light of the pending financial scenario a review of some aspects of the scheme is in hand to ensure there is no long term over-capacity of office accommodation in the Harrogate area (this review embraces a number of CYPS properties in Harrogate and offices in Ripon)

(viii) a forecast underspend of £100k on Skipton BOS due to delays in the

refurbishment. This funding will be carried forward to fund the completion of the scheme in early 2011/12

(ix) a forecast underspend of £380k on Corporate Property Management.

The underspend comprises staffing vacancies (linked to 2011/12 Budget savings), delays on Farms Minor Improvements offset by the contract management setup costs relating to the new Gypsy sites management agreement

COM/EXEC/0211revenuebudget

(x) £137k of the Risk Management Initiatives budget is currently unspent in

cash terms. This budget is used to fund corporate risk management initiatives (eg for Vehicle Driving skills, Radon investigations, First Aid training) and, there are a number of ‘earmarked’ commitments that will utilise this balance in 2011/12

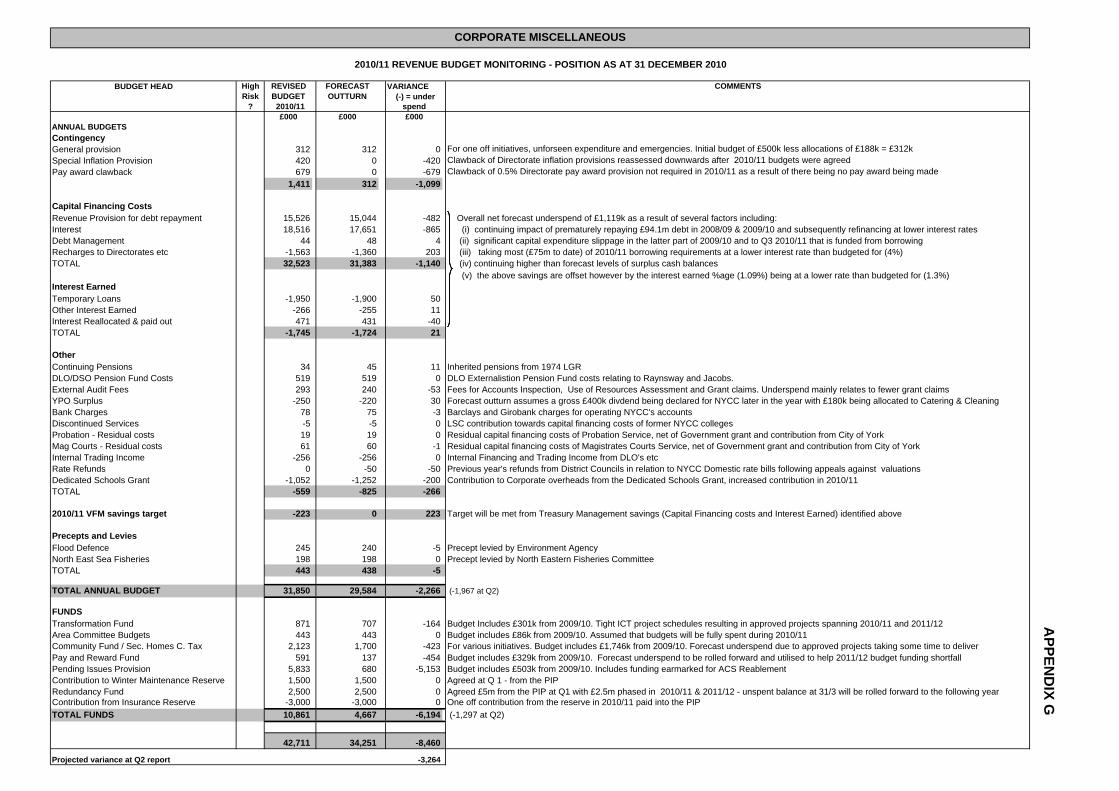

(f) Corporate Miscellaneous

Although a bottom line underspend of £8,460k is forecast at Q3, a significant element of this relates to Funds which are set up to manage one off issues across a number of financial years. If these are excluded (because year end balances are carried forward) the variation (ie underspending) on annual budgets is £2,266k. This latter figure comprises (i) Treasury Management (TM) savings of £1,119k (£1,036k at Q2) which

are covered in more detail in the separate TM section of this Quarterly Report but relate principally to the continuing effects of premature debt repayment, capital expenditure slippage and taking most of the 2010/11 borrowing needs at below budgeted interest rates. Offset against these savings however is the £223k VFM target for the range of corporately held budgets so the net underspend on this group of items is forecast to be £896k.

(ii) clawback of £1,099k from Directorate budgets relating to inflationary

(contracts) and pay award provisions made as part of last year’s budget process that are no longer required.

(iii) other net underspends totalling £271k.

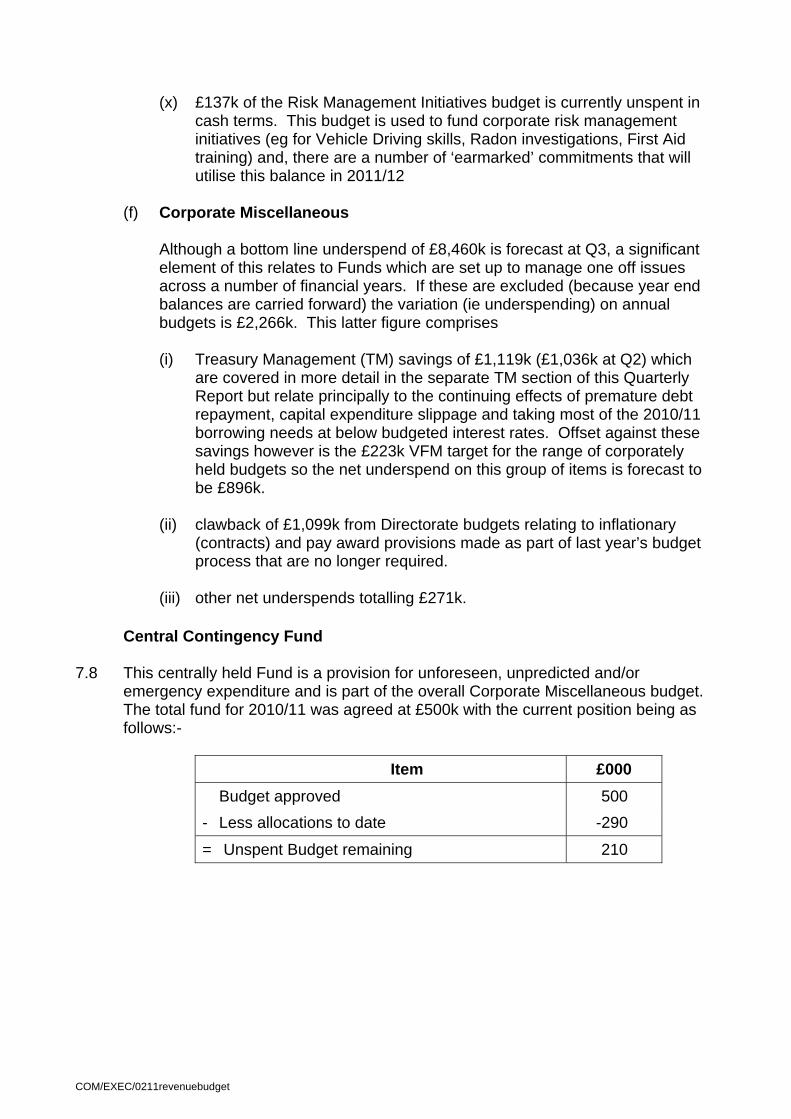

Central Contingency Fund 7.8 This centrally held Fund is a provision for unforeseen, unpredicted and/or

emergency expenditure and is part of the overall Corporate Miscellaneous budget. The total fund for 2010/11 was agreed at £500k with the current position being as follows:-

Item £000 Budget approved 500

- Less allocations to date -290

= Unspent Budget remaining 210

COM/EXEC/0211revenuebudget

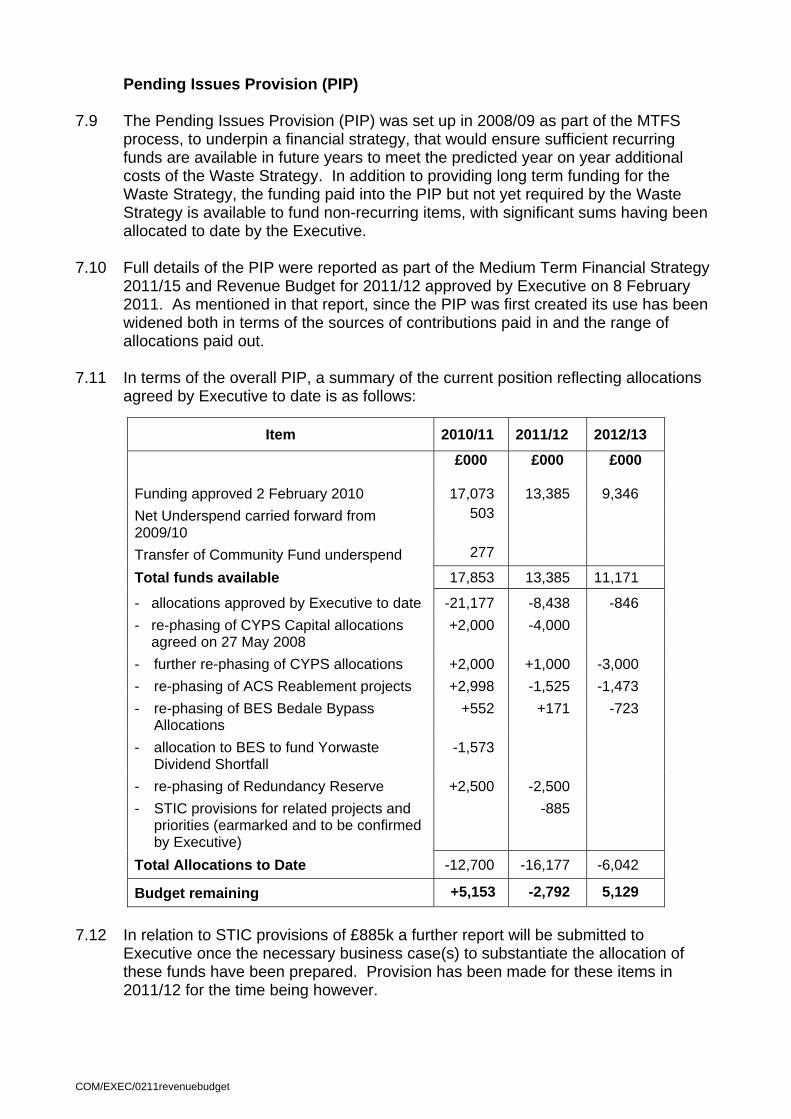

Pending Issues Provision (PIP) 7.9 The Pending Issues Provision (PIP) was set up in 2008/09 as part of the MTFS

process, to underpin a financial strategy, that would ensure sufficient recurring funds are available in future years to meet the predicted year on year additional costs of the Waste Strategy. In addition to providing long term funding for the Waste Strategy, the funding paid into the PIP but not yet required by the Waste Strategy is available to fund non-recurring items, with significant sums having been allocated to date by the Executive.

7.10 Full details of the PIP were reported as part of the Medium Term Financial Strategy

2011/15 and Revenue Budget for 2011/12 approved by Executive on 8 February 2011. As mentioned in that report, since the PIP was first created its use has been widened both in terms of the sources of contributions paid in and the range of allocations paid out.

7.11 In terms of the overall PIP, a summary of the current position reflecting allocations

agreed by Executive to date is as follows:

Item 2010/11 2011/12 2012/13

£000 £000 £000 Funding approved 2 February 2010 17,073 13,385 9,346 Net Underspend carried forward from 2009/10

503

Transfer of Community Fund underspend 277

Total funds available 17,853 13,385 11,171

- allocations approved by Executive to date -21,177 -8,438 -846 - re-phasing of CYPS Capital allocations

agreed on 27 May 2008 +2,000 -4,000

- further re-phasing of CYPS allocations +2,000 +1,000 -3,000 - re-phasing of ACS Reablement projects +2,998 -1,525 -1,473 - re-phasing of BES Bedale Bypass

Allocations +552 +171 -723

- allocation to BES to fund Yorwaste Dividend Shortfall

-1,573

- re-phasing of Redundancy Reserve +2,500 -2,500 - STIC provisions for related projects and

priorities (earmarked and to be confirmed by Executive)

-885

Total Allocations to Date -12,700 -16,177 -6,042

Budget remaining +5,153 -2,792 5,129 7.12 In relation to STIC provisions of £885k a further report will be submitted to

Executive once the necessary business case(s) to substantiate the allocation of these funds have been prepared. Provision has been made for these items in 2011/12 for the time being however.

COM/EXEC/0211revenuebudget

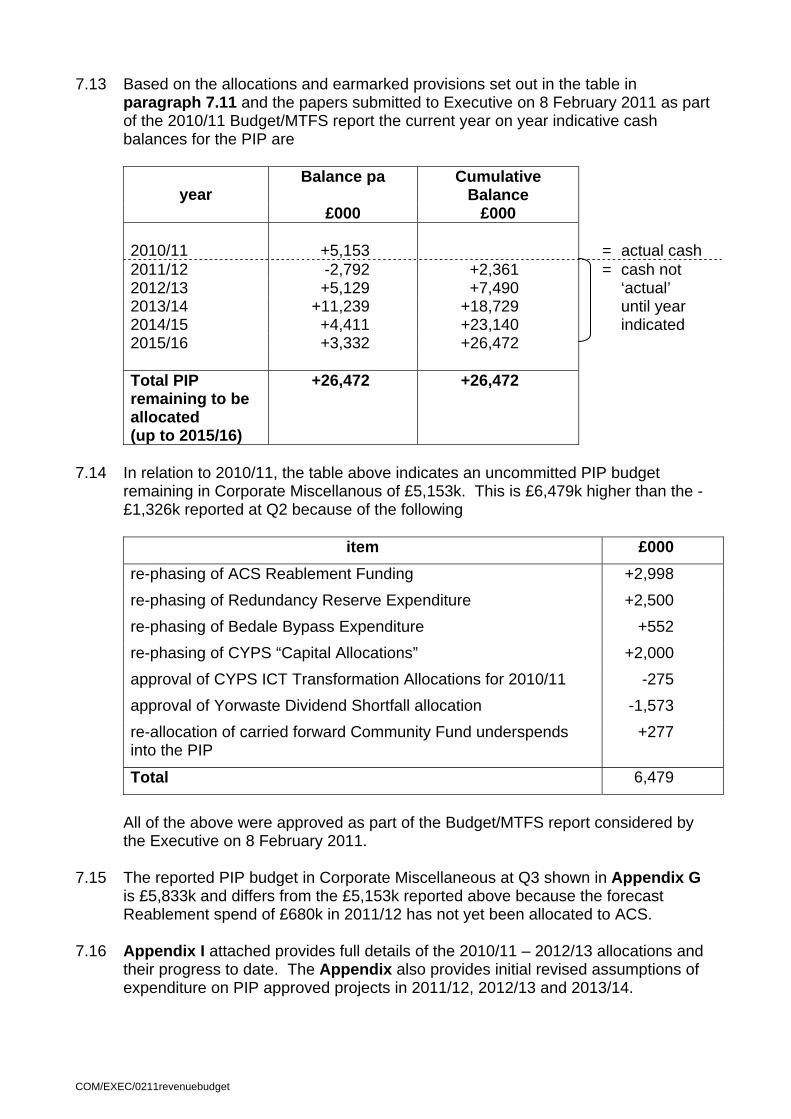

7.13 Based on the allocations and earmarked provisions set out in the table in paragraph 7.11 and the papers submitted to Executive on 8 February 2011 as part of the 2010/11 Budget/MTFS report the current year on year indicative cash balances for the PIP are

Balance pa Cumulative

Balance

year £000 £000

2010/11 +5,153 = actual cash 2011/12 -2,792 +2,361 = cash not 2012/13 +5,129 +7,490 ‘actual’ 2013/14 +11,239 +18,729 until year 2014/15 +4,411 +23,140 indicated 2015/16 +3,332 +26,472 Total PIP remaining to be allocated (up to 2015/16)

+26,472 +26,472

7.14 In relation to 2010/11, the table above indicates an uncommitted PIP budget

remaining in Corporate Miscellanous of £5,153k. This is £6,479k higher than the -£1,326k reported at Q2 because of the following

item £000

re-phasing of ACS Reablement Funding +2,998 re-phasing of Redundancy Reserve Expenditure +2,500 re-phasing of Bedale Bypass Expenditure +552 re-phasing of CYPS “Capital Allocations” +2,000 approval of CYPS ICT Transformation Allocations for 2010/11 -275 approval of Yorwaste Dividend Shortfall allocation -1,573 re-allocation of carried forward Community Fund underspends into the PIP

+277

Total 6,479

All of the above were approved as part of the Budget/MTFS report considered by

the Executive on 8 February 2011. 7.15 The reported PIP budget in Corporate Miscellaneous at Q3 shown in Appendix G

is £5,833k and differs from the £5,153k reported above because the forecast Reablement spend of £680k in 2011/12 has not yet been allocated to ACS.

7.16 Appendix I attached provides full details of the 2010/11 – 2012/13 allocations and

their progress to date. The Appendix also provides initial revised assumptions of expenditure on PIP approved projects in 2011/12, 2012/13 and 2013/14.

COM/EXEC/0211revenuebudget

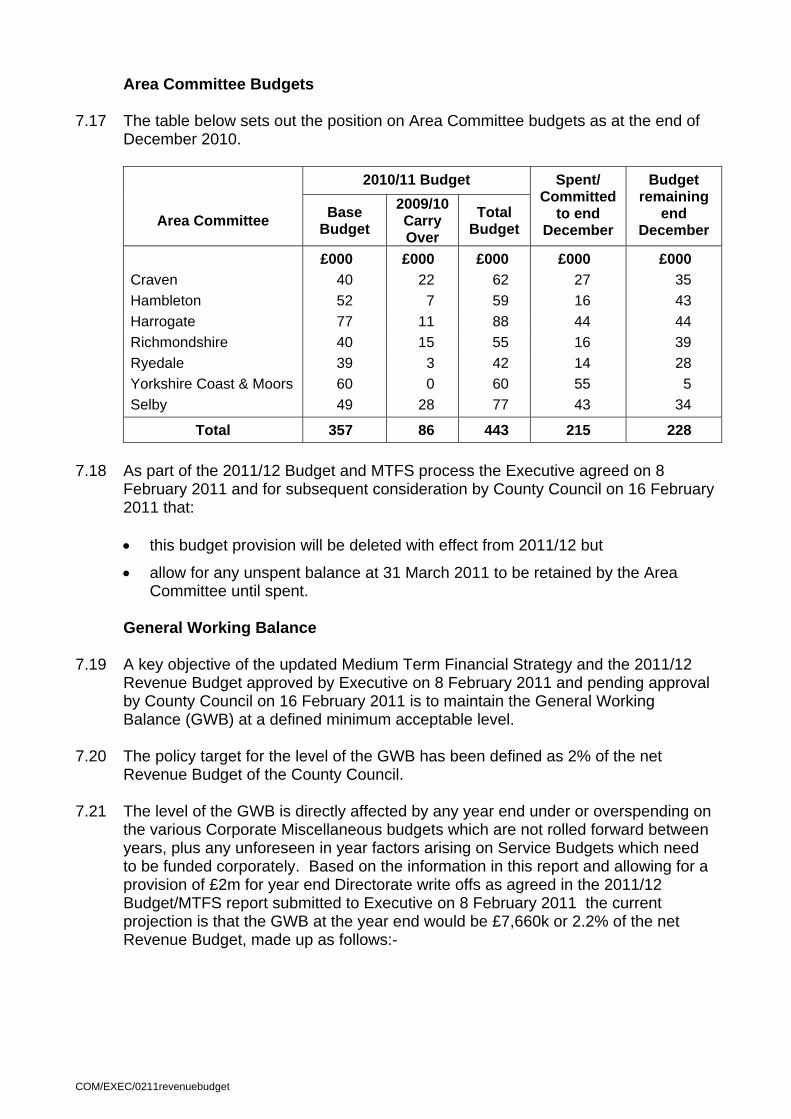

Area Committee Budgets 7.17 The table below sets out the position on Area Committee budgets as at the end of

December 2010. 2010/11 Budget

Area Committee Base Budget

2009/10Carry Over

Total Budget

Spent/ Committed

to end December

Budget remaining

end December

£000 £000 £000 £000 £000 Craven 40 22 62 27 35 Hambleton 52 7 59 16 43 Harrogate 77 11 88 44 44 Richmondshire 40 15 55 16 39 Ryedale 39 3 42 14 28 Yorkshire Coast & Moors 60 0 60 55 5 Selby 49 28 77 43 34

Total 357 86 443 215 228 7.18 As part of the 2011/12 Budget and MTFS process the Executive agreed on 8

February 2011 and for subsequent consideration by County Council on 16 February 2011 that:

• this budget provision will be deleted with effect from 2011/12 but

• allow for any unspent balance at 31 March 2011 to be retained by the Area Committee until spent.

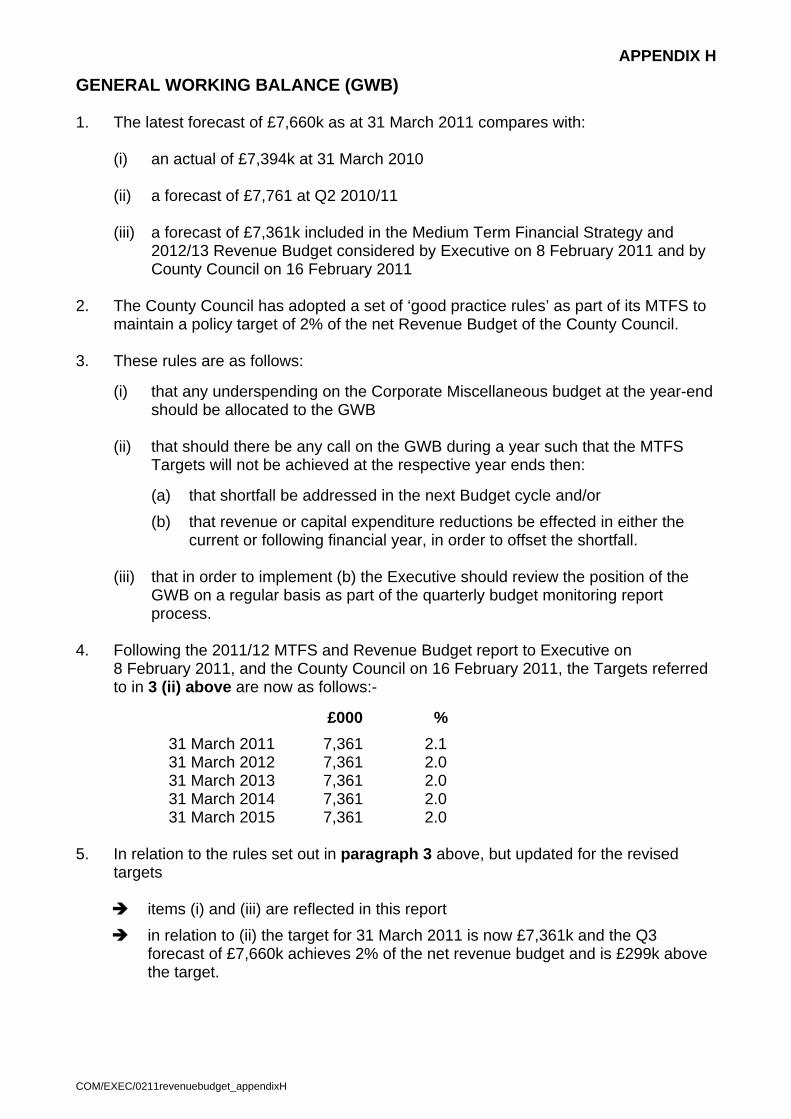

General Working Balance

7.19 A key objective of the updated Medium Term Financial Strategy and the 2011/12

Revenue Budget approved by Executive on 8 February 2011 and pending approval by County Council on 16 February 2011 is to maintain the General Working Balance (GWB) at a defined minimum acceptable level.

7.20 The policy target for the level of the GWB has been defined as 2% of the net

Revenue Budget of the County Council. 7.21 The level of the GWB is directly affected by any year end under or overspending on

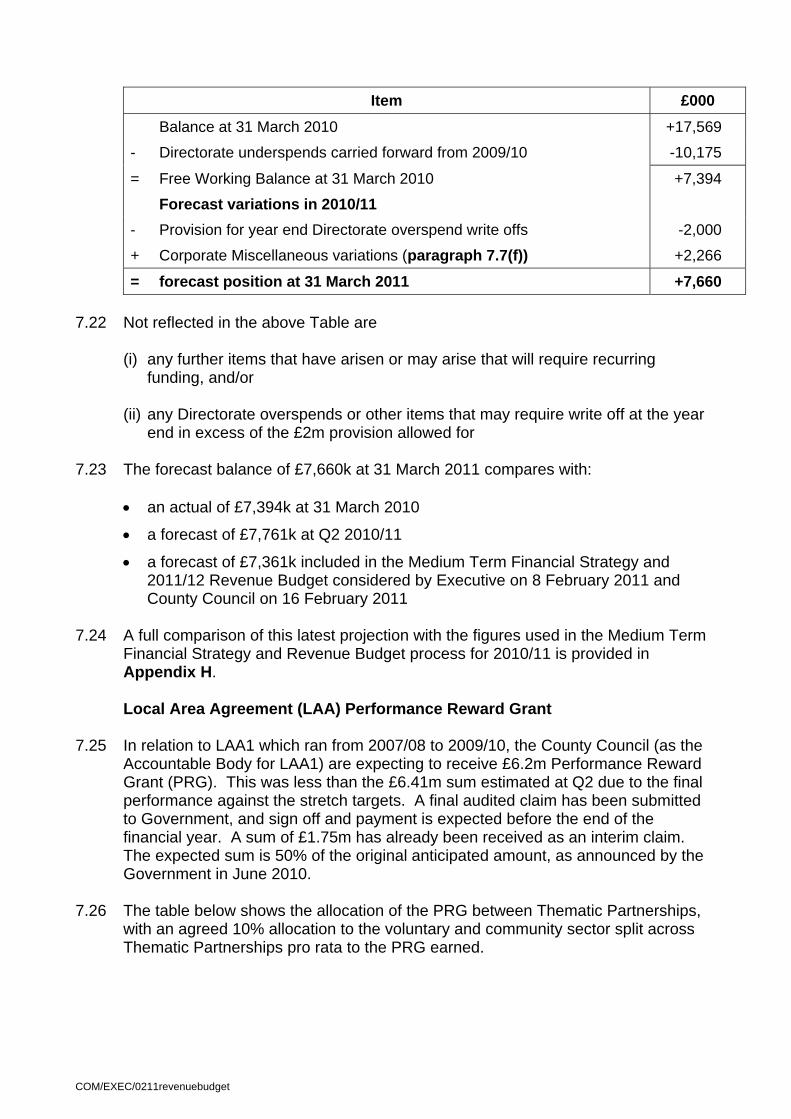

the various Corporate Miscellaneous budgets which are not rolled forward between years, plus any unforeseen in year factors arising on Service Budgets which need to be funded corporately. Based on the information in this report and allowing for a provision of £2m for year end Directorate write offs as agreed in the 2011/12 Budget/MTFS report submitted to Executive on 8 February 2011 the current projection is that the GWB at the year end would be £7,660k or 2.2% of the net Revenue Budget, made up as follows:-

COM/EXEC/0211revenuebudget

Item £000 Balance at 31 March 2010 +17,569

- Directorate underspends carried forward from 2009/10 -10,175

= Free Working Balance at 31 March 2010 +7,394

Forecast variations in 2010/11

- Provision for year end Directorate overspend write offs -2,000

+ Corporate Miscellaneous variations (paragraph 7.7(f)) +2,266

= forecast position at 31 March 2011 +7,660 7.22 Not reflected in the above Table are

(i) any further items that have arisen or may arise that will require recurring funding, and/or

(ii) any Directorate overspends or other items that may require write off at the year

end in excess of the £2m provision allowed for

7.23 The forecast balance of £7,660k at 31 March 2011 compares with:

• an actual of £7,394k at 31 March 2010

• a forecast of £7,761k at Q2 2010/11

• a forecast of £7,361k included in the Medium Term Financial Strategy and 2011/12 Revenue Budget considered by Executive on 8 February 2011 and County Council on 16 February 2011

7.24 A full comparison of this latest projection with the figures used in the Medium Term

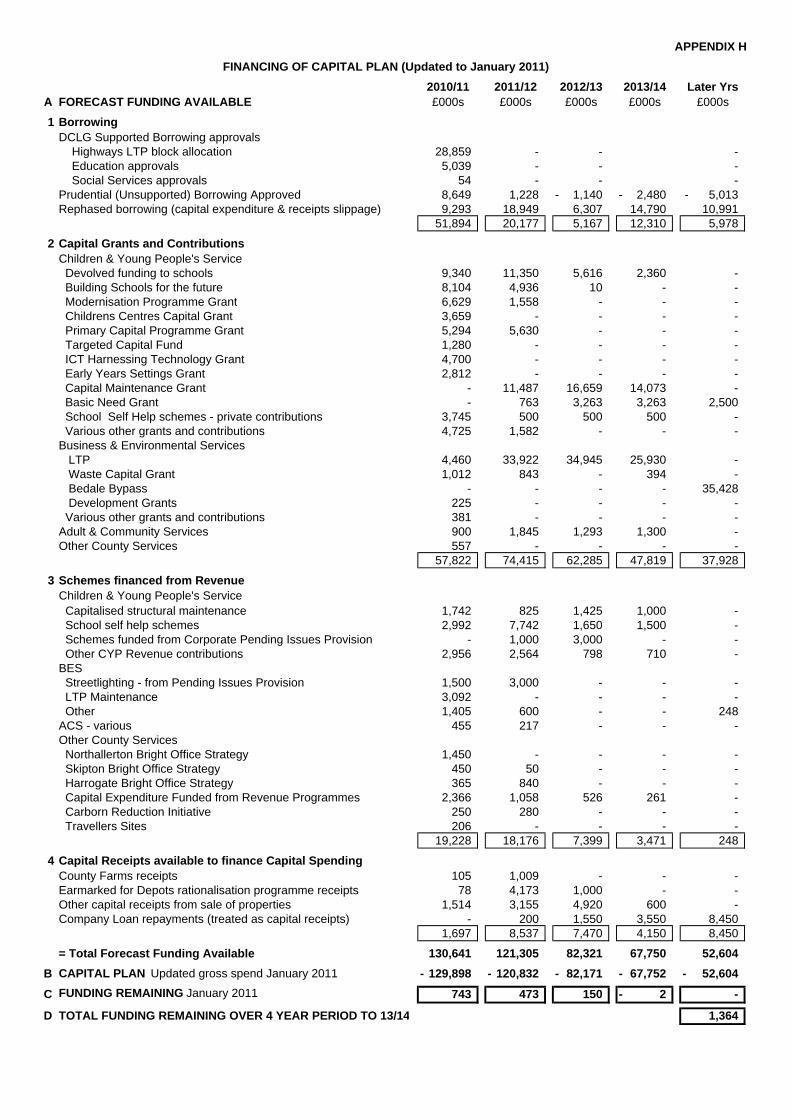

Financial Strategy and Revenue Budget process for 2010/11 is provided in Appendix H.

Local Area Agreement (LAA) Performance Reward Grant 7.25 In relation to LAA1 which ran from 2007/08 to 2009/10, the County Council (as the

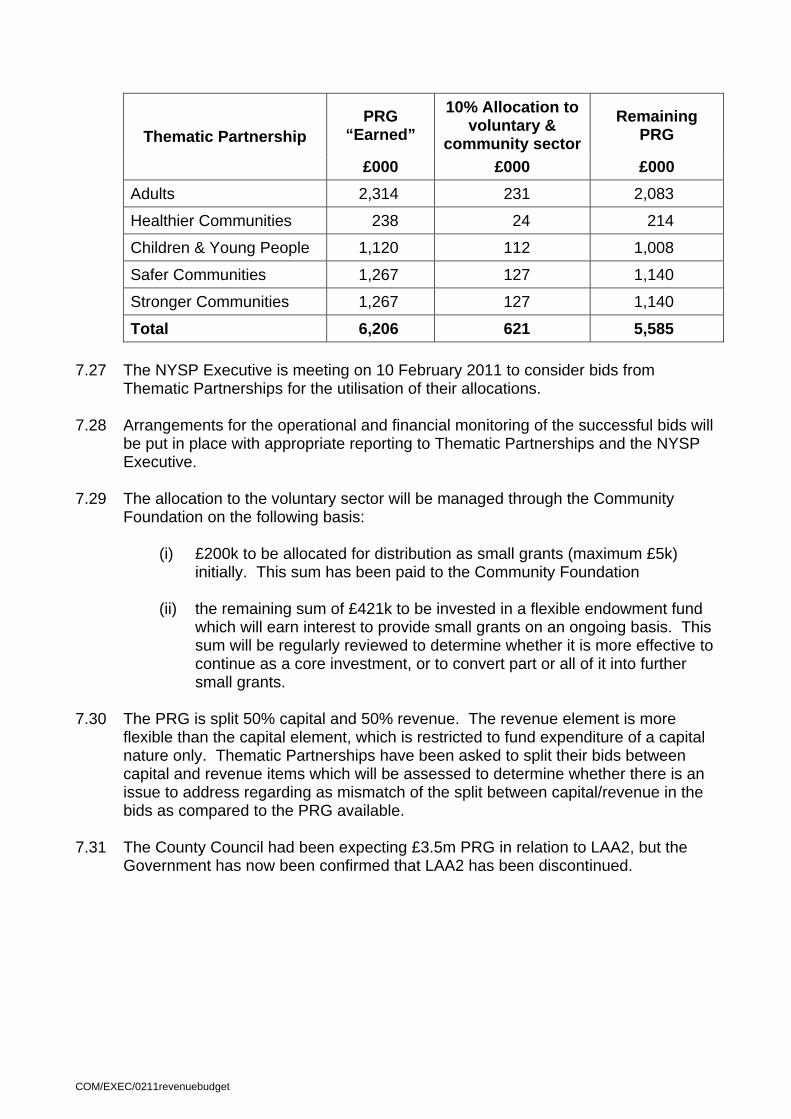

Accountable Body for LAA1) are expecting to receive £6.2m Performance Reward Grant (PRG). This was less than the £6.41m sum estimated at Q2 due to the final performance against the stretch targets. A final audited claim has been submitted to Government, and sign off and payment is expected before the end of the financial year. A sum of £1.75m has already been received as an interim claim. The expected sum is 50% of the original anticipated amount, as announced by the Government in June 2010.

7.26 The table below shows the allocation of the PRG between Thematic Partnerships,

with an agreed 10% allocation to the voluntary and community sector split across Thematic Partnerships pro rata to the PRG earned.

COM/EXEC/0211revenuebudget

PRG “Earned”

10% Allocation to voluntary &

community sector Remaining

PRG Thematic Partnership

£000 £000 £000 Adults 2,314 231 2,083

Healthier Communities 238 24 214

Children & Young People 1,120 112 1,008

Safer Communities 1,267 127 1,140

Stronger Communities 1,267 127 1,140

Total 6,206 621 5,585 7.27 The NYSP Executive is meeting on 10 February 2011 to consider bids from

Thematic Partnerships for the utilisation of their allocations. 7.28 Arrangements for the operational and financial monitoring of the successful bids will

be put in place with appropriate reporting to Thematic Partnerships and the NYSP Executive.

7.29 The allocation to the voluntary sector will be managed through the Community

Foundation on the following basis:

(i) £200k to be allocated for distribution as small grants (maximum £5k) initially. This sum has been paid to the Community Foundation

(ii) the remaining sum of £421k to be invested in a flexible endowment fund

which will earn interest to provide small grants on an ongoing basis. This sum will be regularly reviewed to determine whether it is more effective to continue as a core investment, or to convert part or all of it into further small grants.

7.30 The PRG is split 50% capital and 50% revenue. The revenue element is more

flexible than the capital element, which is restricted to fund expenditure of a capital nature only. Thematic Partnerships have been asked to split their bids between capital and revenue items which will be assessed to determine whether there is an issue to address regarding as mismatch of the split between capital/revenue in the bids as compared to the PRG available.

7.31 The County Council had been expecting £3.5m PRG in relation to LAA2, but the

Government has now been confirmed that LAA2 has been discontinued.

COM/EXEC/0211revenuebudget

7.32 RECOMMENDATIONS

That the Executive (i) notes the latest position for Directorate budgets as summarised in paragraph

7.5 (ii) notes the consequential forecast position of the General Working Balance as

detailed in paragraph 7.21

COM/EXEC/0211revenuebudget

ANNEX C

REVENUE BUDGET APPENDICES

Appendix A 2010/11 Latest Revenue Budgets Appendix B Adult and Community Services Appendix C Business and Environmental Services Appendix D Chief Executive’s Group Appendix E Children and Young People’s Service Appendix F Finance and Central Services Appendix G Corporate Miscellaneous Appendix H General Working Balance Appendix I Pending Issue Provision (PIP) Monitoring Statement

COM/EXEC/0211revenuebudget

2010/11 LATEST REVENUE BUDGETS AT 31 DECEMBER 2010

Original Approved Pending Corporate Other LatestBudgets carry Issues Clawback of agreed Revised

agreed by forwards Provision Excess transfers BudgetsCty Cncl on from Inflation and17-Feb-10 2009/10 Provisions adjustments

£000s £000s £000s £000s £000s £000sDIRECTORATE

Children & Young Peoples' Service 79,238 696 -1,725 -207 121 78,123

Business & Environmental Services 68,560 965 1,021 -493 -743 69,310

Adult & Community Services 131,437 470 691 -314 79 132,363

Chief Executive's Group 13,682 856 -47 370 14,861

Finance & Central Services 15,951 4,223 1,205 -38 1,467 22,808

Corporate MiscellaneousContingency - general provision 500 -188 312Contingency - specific inflation provision 0 1,099 1,099Contingency - additional CYPS Demand 500 -500 0Contribution from Insurance Fund Reserve -3,000 -3,000Pending Issues Provision - Non-Recurring 10,245 503 -4,915 5,833Capital Financing charges 32,778 -255 32,523Interest earned -1,695 -50 -1,745Community Fund / Second Homes Council Tax 800 1,746 -277 -146 2,123Transformation Fund 620 301 -50 871DSG Contribution to Corporate Overheads -1,052 -1,052Pay & Reward Initiative 533 329 -271 591Contribution to Redundancy Reserve 0 2,500 2,500Contribution to Winter Maintenance Reserve 0 1,500 1,500Other (net) 904 86 166 1,156

41,133 2,965 -1,192 1,099 -1,294 42,711

350,001 10,175 0 0 0 360,176

FINANCINGInternal revenue balances 10,175 10,175Externally

Revenue support grant 13,232 13,232National non domestic rates 91,123 91,123Precept on District Councils current year 245,154 245,154 previous years arrears 492 492

350,001 10,175 0 0 0 360,176

APPEN

DIX A

BUDGET HEAD REVISED FORECAST VARIANCEHIGH BUDGET OUTTURN (-) = underRISK? 2010/11 2010/11 spend

£000 £000 £000Social Care Operations - Area BudgetsHambleton/Richmond Y 23,578 23,901 323

Harrogate/Craven Y 44,655 46,578 1,923

Scarborough/Whitby/Ryedale Y 33,855 33,772 -83

Selby Y 14,588 14,766 178

Mental Health 4,598 4,442 -156 Staff vacancy savings and reduced use of residential provision

Provision for demand pressures 1,458 0 -1,458 Monies released by efficiencies made elsewhere in Directorate budgets specifically to support the demand pressure on social care operations.

Assistant Director/Cross-area budgets 3,580 3,622 42

SUB-TOTAL 126,312 127,081 769

Library & community ServicesLibraries Y 7,720 7,821 100 Overspend based on projecting current trends but efforts continue to reduce costs

School Library Service Y 0 47 47 Reduced forecast of income reflecting lower than budgeted uptake of the service by schools

Registrars 27 28 1Archives & Record Management 389 389 0Coroners Y 681 717 36 Overspend is mainly due to the continuation of the trend of rising forensic costs.SUB-TOTAL 8,817 9,002 185

ADULT & COMMUNITY SERVICES

2010/11 REVENUE BUDGET MONITORING - POSITION AS AT 31 DECEMBER 2010

COMMENTS

A significant reduction in the projected overspend in the area budgets has reflected strong management action in terms of reviewing and managing cases, maximising external funding and other income, the impact of reablement on ongoing care costs and the use of cost reduction measures such as telecare

APPEN

DIX B

(Page 1 of 3)

BUDGET HEAD REVISED FORECAST VARIANCEHIGH BUDGET OUTTURN (-) = underRISK? 2010/11 2010/11 spend

£000 £000 £000

ADULT & COMMUNITY SERVICES

2010/11 REVENUE BUDGET MONITORING - POSITION AS AT 31 DECEMBER 2010

COMMENTS

Commissioning, contracting & quality assurance

551 555 4

Strategic Commissioning & Partnerships

780 785 5

Resources Unit 8,269 8,184 -85 Reduced insurance premiums, tight management of staff vacancies

Performance & Change Management 2,068 2,063 -5

Director & Cross-Directorate 902 635 -267 Savings on General Social Care Council registration, contingency and uncommitted budgets

One-off savings 0 -305 -305 Backdated CHC funding, reclaimed direct payment balances etc

Government Grants & Health Transfer

-16,572 -16,572 0

Total Before PIP allocations 131,127 131,428 301

PIP allocations 1,236 871 -365

TOTAL 132,363 132,299 -641,307Projected Variance at Q2 Report

APPEN

DIX B

(Page 2 of 3)

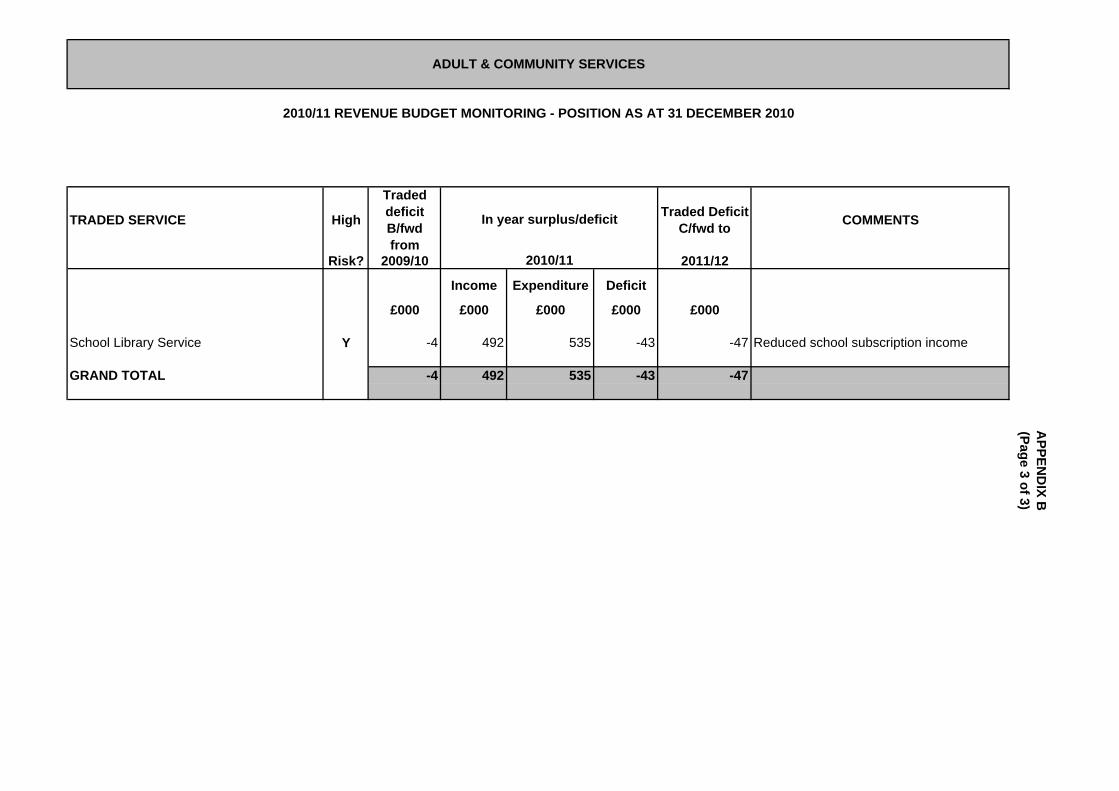

TRADED SERVICE High

Traded deficit B/fwd from

Traded Deficit C/fwd to COMMENTS

Risk? 2009/10 2011/12

Income Expenditure Deficit

£000 £000 £000 £000 £000

School Library Service Y -4 492 535 -43 -47 Reduced school subscription income

GRAND TOTAL -4 492 535 -43 -47

In year surplus/deficit

2010/11

ADULT & COMMUNITY SERVICES

2010/11 REVENUE BUDGET MONITORING - POSITION AS AT 31 DECEMBER 2010

APPEN

DIX B

(Page 3 of 3)

BUDGET HEAD REVISED FORECAST VARIANCEHIGH BUDGET OUTTURN (-) = underRISK? 2010/11 2010/11 spend

£000 £000 £000

Highways 30,822 33,272 2,450 The net forecast represents the predicted overspend on the winter service after the application of the £1.5m reserve.

Integrated Passenger Transport (IPT) 4,399 4,399 0Trading Standards & Planning Services 2,584 2,584 0Economic & Rural Services 2,711 2,711 0Partnership Unit 98 98 0Waste Management 23,048 23,192 144 A one-off budget increase of £1,573k has been carried out to represent the shortfall in the

Yorwaste dividend for 2010/11. The net overspend relates to the Waste Procurement Project resulting from additional external fees.

Performance & Finance Unit 2,778 2,778 0Support Services 1,065 1,065 0

Total before PIP Allocations 67,505 70,099 2,594

PIP Allocations 1,805 1,805 0 The PIP allocation comprises of a revenue contribution to the street lighting capital programme of £1,500k and preparation costs for the Bedale-Aiskew-Leeming Bar Bypass (BALB) scheme of £305k. The previous £857k for BALB has been reduced by £552k to reflect the forecast outturn for 2010/11 as reported to the Executive in December 2010.

TOTAL 69,310 71,904 2,594

910

BUSINESS & ENVIRONMENTAL SERVICES

2010/11 REVENUE BUDGET MONITORING - POSITION AS AT 31 DECEMBER 2010

Excluding the winter service, the BES Directorate is aiming to deliberately under spend in 2010/11 to help the financial position. Currently it is estimated that the available under spend to contribute will be in excess of £1m and will reduce the over spend forecast noted here accordingly.

COMMENTS

Projected Variance at Q2 Report

APPEN

DIX C

I:\EXECSEC\scp\performance\Quarterly Monitoring Report\2011\220111\Section 7 APPENDIX C BES

BUDGET HEAD REVISED FORECAST VARIANCEHIGH BUDGET OUTTURNRISK? 2010/11 2010/11

£000 £000 £000

Chief Exec's Office (incl Access to Services) 2,595 2,584 -12

Grants & Subscriptions 233 233 0

Comm Safety, Climate Change etc. 326 326 0

Emergency Planning 485 414 -71

Legal Services 1,562 1,444 -118

Democratic Services 609 551 -58

Legal Expenses Y 643 965 322

Elections 76 76 0

Customer Service Centre 1,727 1,727 0

HR Services 2,938 2,873 -65

People Strategy 388 279 -109

Underspend mainly arising from savings on supplies & services and staffing vacancies being held in the current year as a result of the 2011/12 savings programme.

Underspend mainly arising from savings from staffing vacancies being held in the current year as a result of the 2011/12 savings programme.