Embed Size (px)

Citation preview

North Central Regional Training August 20-23, 2013

1

Financial and Grants Management 101 Basics

1

Bonnie JanickiSenior Grants OfficerOffice of Grants ManagementCNCS

You need to know . . .The information in this workshop is based on

CNCS and Federal laws, rules, and regulations; CNCS grant terms and provisions; and generally accepted

accounting and financial principles and practices.

Some state commissions, national grantees, or parent organizations may impose

additional requirements.

North Central Regional Training August 20-23, 2013

2

Welcome . . . Introduction of trainer and CNCS staff Program types represented

Senior Corps, AmeriCorps, SIF, NCB, 9/11, MLK Questions

As we go . . . ask clarifying questions and provide your experiences

Questions at the end as time permits We will do a small group activity

North Central Regional Training August 20-23, 2013

3

Workshop Flow

4North Central Regional Training August 20-23, 2013

Workshop Objectives Review basic Corporation for National

and Community Service facts Develop knowledge about effective

financial and grants management Discuss challenges and opportunities for

financial management growth Explore ways to enhance and improve

current practices North Central Regional Training

August 20-23, 20135

National Service Grantees Senior Corps

Foster Grandparents, Senior Companion, RSVP

AmeriCorps National Capacity Building Program Social Innovation Fund 9/11 Day of Service and Remembrance MLK Day of Service

North Central Regional Training August 20-23, 2013

6

See Handout 1

ActivityBasic Financial & Grants Management Terminology

North Central Regional Training August 20-23, 2013

7

See Activity 1

North Central Regional Training August 20-23, 2013

8

Effective Financial Management

North Central Regional Training August 20-23, 2013

9

Key Characteristics of Organizations with Highly Effective Financial Management

Written and followed policies and procedures Qualified and trained financial staff Effective communications Succession planning and cross-training Self-assessment and continuous improvement Active, knowledgeable and informed Board and

finance committee

North Central Regional Training August 20-23, 2013

10

Regulations & Requirements

North Central Regional Training August 20-23, 2013

11

Nat’l & Community Svc. Act of 1990

Serve America Act

Code of Federal Regulations (CFR)

OMB Circulars (part of CFR)

State & Local Regulations

Notice Of Funding Opportunity

Notice of Grant Award

Proposal & Budget

Grant ProvisionsCertifications and Assurances

North Central Regional Training August 20-23, 2013

12

Grant GuidelinesFederal

Grant GuidelinesEducational Institutions

States, Local, Indian Tribal Governments

Non-Profits Hospitals

Administrative Requirements

§ 45 CFR 2543§ 2 CFR 215

(formerly A-110)

§ 45 CFR 2541 OMB A-102

§ 45 CFR 2543§ 2 CFR 215 (formerly A-110)

§ 45 CFR 2543§ 2 CFR 215 (formerly A-110)

Cost Principles § 2 CFR 220 (formerly A-21)

§ 2 CFR 225 (formerly A-87)

§ 2 CFR 230 (formerly A-122)

§ 45 CFR 74 (HHS regulations)

Audit Requirements OMB A-133 OMB A-133 OMB A-133 OMB A-133

Notes:CFR = Code of Federal Regulations = Organization is subject to A-133 if it expends more than $500,000 of Federal funds in its fiscal year

Locate Grants Management Circulars: www.whitehouse.gov/omb/grants_circulars/

North Central Regional Training August 20-23, 2013

13

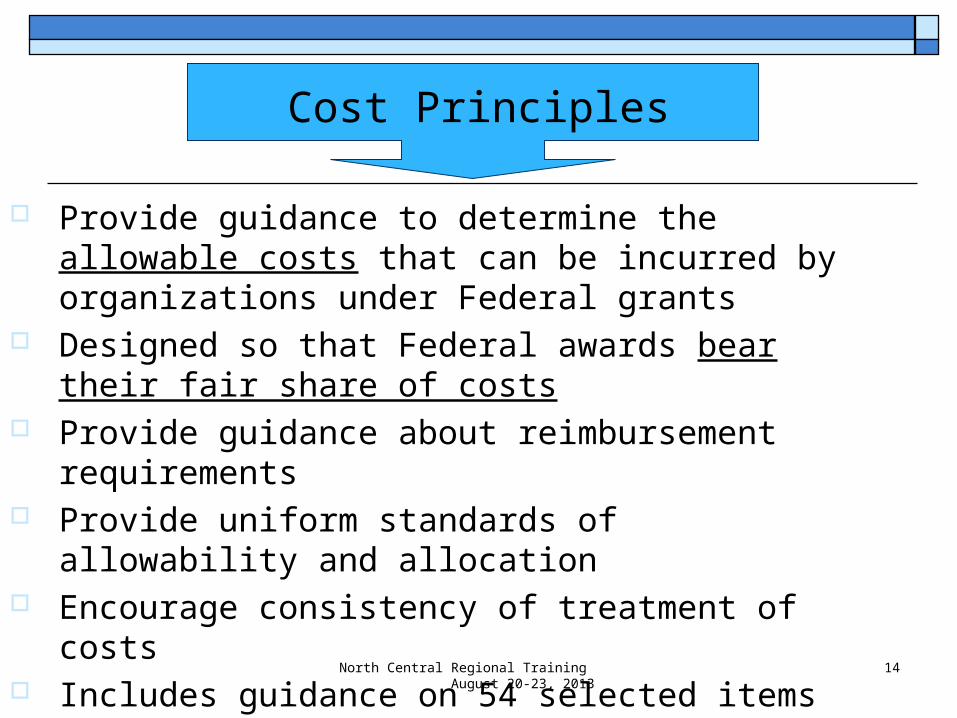

Basics of OMB Circulars Cost Principles

Allowable & Unallowable Costs Indirect Costs

Administrative Requirements Accounting System Documentation requirements

A-133 requirements

North Central Regional Training August 20-23, 2013

14

Provide guidance to determine the allowable costs that can be incurred by organizations under Federal grants

Designed so that Federal awards bear their fair share of costs

Provide guidance about reimbursement requirements Provide uniform standards of allowability and

allocation Encourage consistency of treatment of costs Includes guidance on 54 selected items of cost

Cost Principles

Allowable, Reasonable & Allocable Allowable –A cost within award limitations consistent,

documented, reasonable & allocable Reasonable - A cost that does not exceed what a

prudent person would do under the circumstances at the time the decision

Allocable - Treated consistently with other costs incurred for the same purpose in like circumstances and benefits the award and can be distributed proportionally to the benefits received

North Central Regional Training August 20-23, 2013

15

North Central Regional Training August 20-23, 2013

16

Provide consistency and uniformity among Federal agencies in the management of grants and cooperative agreements

Require all Federal agencies to issue a grants management common rule to adopt government-wide terms and conditions

Federal Grant Guidelines

Educational Institutions

States, Local, Indian Tribal Governments

Non-Profits Hospitals

Administrative Requirements

§ 45 CFR 2543§ 2 CFR 215

(formerly A-110)

§ 45 CFR 2541 OMB A-102

§ 45 CFR 2543§ 2 CFR 215 (formerly A-110)

§ 45 CFR 2543§ 2 CFR 215 (formerly A-110)

Administrative Requirements

North Central Regional Training August 20-23, 2013

17

Provide the standards for obtaining consistency and uniformity among Federal agencies for the audit of organizations expending Federal funds

Apply to all organizations that expend $500,000 or more of Federal funds in that organization’s fiscal year

A-133 Audit Requirements

North Central Regional Training August 20-23, 2013

18

Accounting Systems

North Central Regional Training August 20-23, 2013

19

Efficient Accounting System Requirements Distinguish grant verses non-grant related expenses Identify costs by program year & budget category Differentiate between direct and indirect costs Account for each award/grant separately Record in-kind contribution as both revenue & expense Provide management with financial reports at both the

summary or detailed levels that will compare outlays with budget amounts

Correlate financial reports submitted to CNCS directly to accounting information and supporting documents

Accounting System that properly segregates funds

North Central Regional Training August 20-23, 2013

20

Department of Education Grant

CNCS Grant

Ford Foundation Grant

Accounting System

Grant 1

Grant 2

Grant 3

NOT

North Central Regional Training August 20-23, 2013

21

Policies & Procedures

North Central Regional Training August 20-23, 2013

22

Policies & Procedures Policies and procedures are a set of written documents

that describe an organization's policies for operation – “what is to be done” the procedures necessary to fulfill the policies – “how it is to be

completed” All staff must be familiar with these documents Documents must be kept up-to-date Documents should explain the rationale and include

principal transactions and completed forms Documents must incorporate Federal and CNCS grant

regulations and provisionsSee Handout 2

North Central Regional Training August 20-23, 2013

23

Internal Controls

North Central Regional Training August 20-23, 2013

24

Why Have Internal Controls? Improve accountability to constituents

CNCS, trustees, funders, public Help organization achieve performance & budget

targets Improve reliability of financial reporting Improve compliance with laws & regulations Prevent loss of resources & public assets Prevent loss of public trust Reduce legal liability

Who is Responsible? Everyone within the organization has some role in internal controls Roles vary depending upon level of responsibility:

Executives establish the presence of integrity, ethics, competence and a positive control environment

Directors and department heads have oversight responsibility for internal controls within their units

Managers and supervisory personnel are responsible for executing control policies and procedures at the detail level within their specific unit

Each individual within a unit is to be cognizant of proper internal control procedures associated with their specific job responsibilities

North Central Regional Training August 20-23, 2013

25

A Good Control Environment Includes Positive “atmosphere” in the work environment Existence of a code of conduct and code of ethics Written job descriptions Timely/appropriate communications with Board Written policies to hire, train, promote and compensate

employees Safeguards for employees related to whistle-blowing A clear chain of command Clear, written delegations of authority & responsibilities

North Central Regional Training August 20-23, 2013

26

A Good Control Environment Includes (cont’d)

Written policies, procedures and processes Adequate review process for financial

transactions, financial reports, budgets, etc. Adequate cash management procedures (e.g.,

monthly bank reconciliations by supervisory personnel)

System to track participants’ & employees’ activities

System to follow up on problems to ensure resolution

North Central Regional Training August 20-23, 2013

27

North Central Regional Training August 20-23, 2013

28

Prohibited Activities

Prohibited Activities While charging time to the AmeriCorps

program, accumulating service or training hours, or otherwise performing activities supported by the AmeriCorps program or the Corporation, staff and members may not engage in specific activities. (see 45 CFR § 2520.65)

North Central Regional Training August 20-23, 2013

29

See Handout 3

North Central Regional Training August 20-23, 2013

30

Documenting Expenses

Documenting Expenses

AllowableAllocable

ReasonableConsistently Applied

North Central Regional Training August 20-23, 2013

31

Document, Document, Document

Documentation BasicsWhy Retain Documentation? To track incoming information

To review information

To provide historical evidence

To provide evidence of accomplishments

To prepare for an audit

North Central Regional Training August 20-23, 2013

32

See Handout 4

Establish a written record retention policy

Electronic Storage of Records- AmeriCorps Member Records

The electronic storage procedures and system must Provide for the safe-keeping and security of the records, including:

Sufficient prevention of unauthorized alterations or erasures of records Effective security measures to ensure only authorized persons have

access to records Adequate measures designed to prevent physical damage to records A system providing for back-up and recovery of records

Provide for the easy retrieval of records in a timely fashion, including: Storage of the records in a physically accessible location Clear and accurate labeling of all records Storage of the records in a usable, readable format

Where there is a requirement for a signature on a record, electronically stored records must include an image of the original signature Records without signatures, when required, are considered incomplete

North Central Regional Training August 20-23, 2013

33

North Central Regional Training August 20-23, 2013

34

Signed timesheets with supervisory approval Quarterly payroll returns (941) Payroll register Personnel file with salary/wage information Employment contract Cancelled checks Direct deposit schedule

Key Documentation Issue

34

Salary

See Handout 5

North Central Regional Training August 20-23, 2013

35

Match

Project CostsThe total allowable budget or expenditures incurred to operate the program and accomplish its objectives is divided into 2 sections:

North Central Regional Training August 20-23, 2013

36

Federal Share

Grantee Share

aka: match

Portion of total expenditures not paid for with CNCS funds

Portion of budget or total expenditures paid for with CNCS funds

Federal and Grantee Share funds must be treated consistently

Contributions received by cash, check, electronic funds transfer, credit card, or payroll deduction

CashContributions

In-KindContributions

Sources of Match

Value of non-cash contributions May be in the form of real property,

equipment, supplies, services, and other expendable property

Approved Budget Match Amount and Sources of MatchSources of Match Changed Significantly Contact your Grants Officer

North Central Regional Training August 20-23, 2013

37

Finding Match SourcesCash:

Donations Leases, sale of

goods/services Local governments State appropriations Foundation grants or

corporate contributions

In-Kind Contributions:

Value of donated services and/or donated goods

Labor space vehicles

training supplies equipment services

North Central Regional Training August 20-23, 2013

38

Senior Corps: Unclaimed volunteer reimbursements (i.e., mileage, meals,

physicals) cannot be counted as match

Using Other Federal Funds as Match Budgeting

Discuss your intent to use other Federal funds to match a CNCS grant with the other agency before submitting your application

AmeriCorps – Serve America Act of 2009 requires grantees and subgrantees to report the amounts and sources of Federal funds used to carry out programs Report this on spreadsheet provided by CNCS October 2012 – report on eGrants FFR may be possible

Document in your records whether in-kind contribution that obtained with Federal funds

North Central Regional Training August 20-23, 2013

39

Acceptable Match is . . . Cash and in-kind contributions are accepted as part of the grantee’s cost sharing or matching when contributions meet all of the following criteria:

Are verifiable from the grantee's records Are necessary and reasonable for proper and efficient accomplishment

of project or program objectives Are allowable under the applicable OMB cost principles Are not paid by the Federal Government under another award, except

where authorized by Federal statute to be used for cost sharing or matching

Are provided for in the approved budget (allowable under program guidelines)

Conform to other grant provisions or OMB Circulars

North Central Regional Training August 20-23, 2013

40

Administrative Requirements

Exception: Volunteer Match

Do not count as match - The value of direct community services

performed by volunteers

Do count as match -

Services that contribute to organizational functions

Count services such as accounting, legal, training of staff or participants that are elements of the grantee’s cost allocation plan

North Central Regional Training August 20-23, 2013

41

Recording In-Kind Contributions Maintain adequate documentation to support amounts

claimed as match Maintain same documentation for both CNCS Federal share

and for grantee’s share Documentation must meet same standards as other

expenditures within organization Record donation and valuation of item in detail Enter into the General Ledger as income and expenditure

Failure to enter match contributions into general ledger requires a formal explanatory policy and separate spread sheet accountability of receipt and use

North Central Regional Training August 20-23, 2013

42

See Handout 6

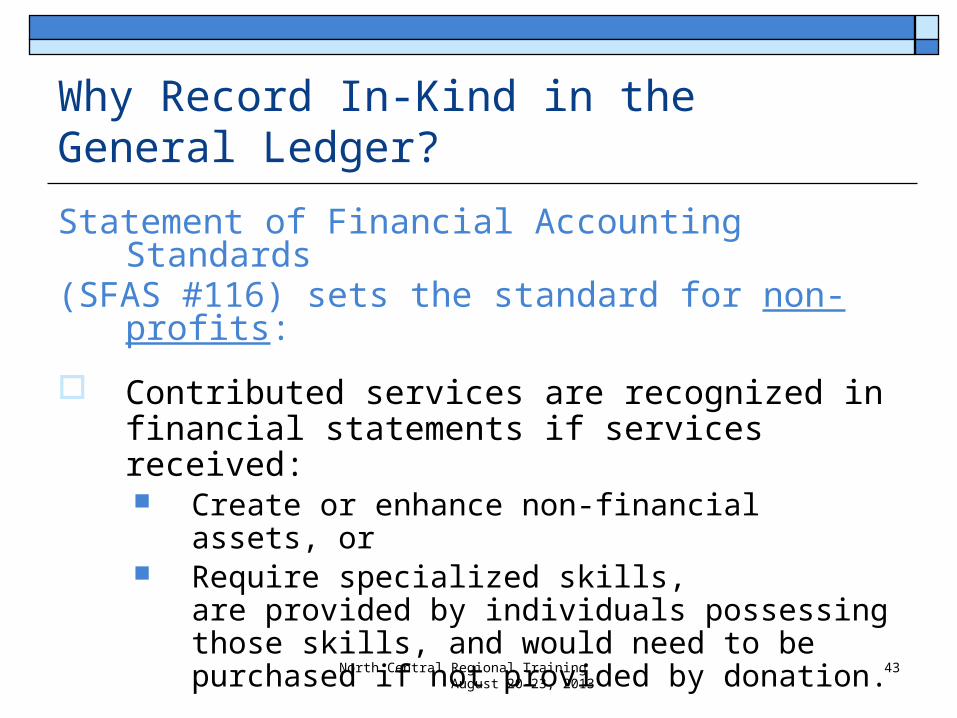

Statement of Financial Accounting Standards (SFAS #116) sets the standard for non-profits:

Contributed services are recognized in financial statements if services received: Create or enhance non-financial assets, or Require specialized skills, are provided by

individuals possessing those skills, and would need to be purchased if not provided by donation.

Why Record In-Kind in the General Ledger?

North Central Regional Training August 20-23, 2013

43

Enter into the General Ledger as income and expenditure:

Example:A local paint store donates a professional paint sprayer with a fair market value of $550.00

$550.00 – 7250 In-Kind Expense Account (debit) $550.00 – 5250 In-Kind Income Account (credit)

Recording In-Kind Contributions

North Central Regional Training August 20-23, 2013

44

Use fair market price Consider what it would cost to obtain similar goods or

services The donor must provide the value of the donation Review the donation letter or form to ensure the value is

reasonable

Valuing In-Kind Contributions

The IRS defines fair market value as the price that item would sell for

on the open market

North Central Regional Training August 20-23, 2013

45

1. Document the basis for determining value of personal services, material, equipment, building, and land

2. Obtain written acknowledgement from the donor to include: Name and signature of donor Date and location of donation Detailed description of contributed item or service Estimated value of contribution, how value was determined,

who made the determination Whether the contribution was obtained with Federal funds

*** Keep a copy of the receipt in your files ***

Documenting In-Kind Contributions

If audited, a grantee may be required to provide supporting documentation of ALL donations, if not available during the audit

North Central Regional Training August 20-23, 2013

46

See Handout 7

Sample: In-Kind Contribution Form

North Central Regional Training August 20-23, 2013

Does your In-Kind

Form have all this

information?

47

North Central Regional Training August 20-23, 2013

48

Financial Reporting

North Central Regional Training August 20-23, 2013

49

Key Elements of Financial Reporting Prepare all financial reports with information

from the organization’s accounting system Review and reconcile the information to ensure

accuracy prior to report submission Ensure files have the proper documentation to

support all information reported in financial reports

Submit all reports on time

Program Income Defined as “gross income received by the grantee . . .

directly generated by a grant supported activity, or earned only as the result of the grant agreement during the grant period”

There are 2 alternatives to using program income: Additive – added to funds committed to the program and used

to further program objectives Deductive – deducted from total allowable costs of the

program to determine the net allowable costs for which the CNCS share is based

Consult grant terms and conditions to determine deductive or additive alternative

North Central Regional Training August 20-23, 2013

50

North Central Regional Training August 20-23, 2013

51

Budgeting

Budget Narrative Preparation Review your program/projects goals and objectives Estimate the resources needed to achieve

program/project goal, for example: Participants – members, volunteers Staff positions Space, utilities, supplies, telephone Medical and liability insurance Uniforms and training Transportation Evaluations

North Central Regional Training August 20-23, 2013

52

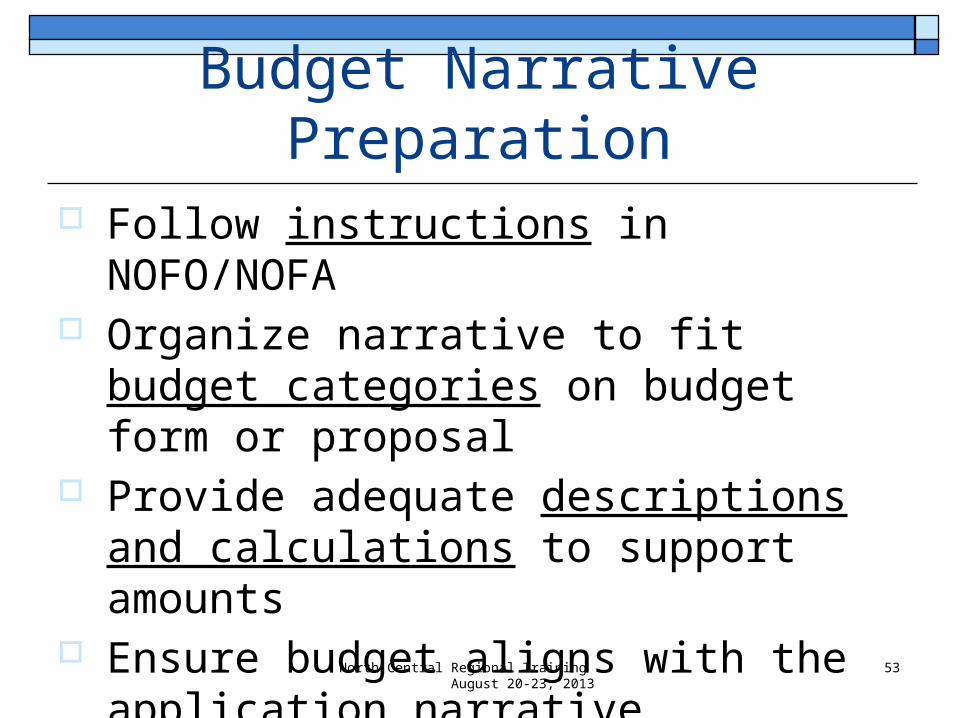

Budget Narrative Preparation Follow instructions in NOFO/NOFA Organize narrative to fit budget categories

on budget form or proposal Provide adequate descriptions and

calculations to support amounts Ensure budget aligns with the application

narrative

North Central Regional Training August 20-23, 2013

53

Budget Narrative Preparation Allocate costs based on a consistent and

documented cost allocation plan. Examples include: Level of effort: percentage of time spent on activity X

salary Rent: total CNCS program space ÷ total host agency

space Expenses: percentage of expenses for program

versus total organization’s expenses

North Central Regional Training August 20-23, 2013

54

Key Budgeting Tips Check to ensure that required match is met Be strategic when allocating funds to CNCS or

grantee share, some costs can be met with in-kind donations

Be aware of budget changes that require amendments

Identify In-kind donations prior to creating the budget

North Central Regional Training August 20-23, 2013

55

Budget ManagementGrantees must obtain prior approval from CNCS for: Subgrants or contracts not included in approved application and

budget Specific costs described in the Cost Principles

For example: overtime pay, rearrangement and alteration costs, and pre-award costs

Purchases of equipment over $5,000 using grant funds, unless specified in the approved application and budget

Cumulative or aggregate budget line items that amount to 10% or more of the total budget

North Central Regional Training August 20-23, 2013

56

1. Do not assume approvals have been granted unless documented 2. Approval required by the OGM or FFMC

North Central Regional Training August 20-23, 2013

57

Close Out

Overview of the Close Out ProcessGrantee Responsibility: Complete grant close out within 90 days of the end

of the project period Seek a no-cost extension from the OGM or FFMC

for activities that will extend beyond the project period end dates As a subgrantee, you must go through your

Commission, Parent, or other primary organization Senior Corps no-cost extensions are rarity

Must request 90 days prior to end of 3 year grant endNorth Central Regional Training

August 20-23, 201358

Grantee ResponsibilitiesComplete the following steps: Pay outstanding obligations Closeout sub-grants Submit close out documents as necessary Enter final Federal Financial Report (FFR) in eGrants Return unobligated funds Ensure all final amounts are equal

FFR in eGrants FFR in Payment Management System (PMS) Drawdown in PMS

North Central Regional Training August 20-23, 2013

59

Reconciling the Grant Reconcile all expenditures and draw downs, so

that funds expended are equal to funds disbursed and advanced

If these reports do not reflect the same expenditure amounts the Corporation cannot close your grant until you make adjustments

North Central Regional Training August 20-23, 2013

60

FinalDrawdown FFR

Subsequent Audit CNCS retains right to conduct a

subsequent audit or other review of a grant—close out does not change this right

Notice of audit may extend the three year record retention requirement

North Central Regional Training August 20-23, 2013

61

Retaining Records

Retain all records for three years from submission of the final FFR

Requirement is included in the CNCS Regulations

North Central Regional Training August 20-23, 2013

62

North Central Regional Training August 20-23, 2013

63

Highlights: Program Responsibility Overall compliance with CNCS and program

specific regulations Training, monitoring and oversight of

subgrantee or participant compliance Accurate, timely and complete program and

performance reporting Ensure key staff understand roles,

responsibility, understand each other’s priorities and work together

North Central Regional Training August 20-23, 2013

64

Highlights: Fiscal Responsibility Overall compliance with State and Federal

regulations Accurate, timely and complete financial

reporting Tracking of budget to actual expenses Ensure key staff understand roles,

responsibility, understand each other’s priorities and work together

North Central Regional Training August 20-23, 2013

65

Helpful LinksDescription Website Address

Corporation for National and Community Service

www.nationalservice.gov

A-133 Federal Audit Clearinghouse harvester.census.gov/sac/dissem/simpleqry.html

Excluded Parties List System www.epls.gov

Payment Management System at HHS

www.dpm.psc.gov

GuideStar www.guidestar.org

OMB Circulars www.whitehouse.gov/omb/circulars

CNCS eGrants Gateway egrants.cns.gov/espan/main/login.jsp

Questions?Open

Wrap Up

Evaluation

North Central Regional Training August 20-23, 2013

66

For More Information Contact your CNCS Grants Officer

E-mail or call your Grants Officer Visit the Resource Center

Online tools and training www.nationalserviceresources.org/financial-and-grants-management

North Central Regional Training August 20-23, 2013

67