Embed Size (px)

Citation preview

• This presentation is only directed towards investment professionals, and the fund(s) are only available to them. Any person who do not have professional experience in matters relating to investments should not rely on this information.

• Historical returns are no guarantee for future returns. Future returns will depend, inter alia, on market developments, the fund manager’s skill, the fund’s risk profile and subscription and management fees. The return may become negative as a result of negative price developments.

• Pareto Forvaltning seeks to the best of its ability to ensure that all information given is correct, however, makes reservations regarding possible errors and omissions. Statements in the report may reflect the portfolio managers’ viewpoint at a given time, and this viewpoint may be changed without prior notice. The distribution of this information may be restricted by law in certain jurisdictions and this information is not intended for distribution to any person or entity in such jurisdiction.

• This presentation should not be perceived as an offer or recommendation to buy or sell financial instruments. Pareto Forvaltning does not assume responsibility for direct or indirect loss or expenses incurred through use or understanding of the presentation.

• Subscription and redemption fees are not taken into account in the historical performance given for our funds, this could affect the return adversely.

• Unless otherwise stated, the performance information given does not take into account any tax that may be incumbent on the product and / or customer. The tax treatment of the funds depends on the personal circumstances of each client and can be subject to future changes.

• Expectations of future performance should not be used as a reliable indicator of future performance. Such expectations do not take into account the effects of inflation and taxes, which will have a negative impact in real terms.

• In preparing this document we have relied upon and assumed, without independent verification, the accuracy and completeness of all information available from public sources or which was provided to us or otherwise reviewed by us. The information contained in this document has been taken from sources deemed to be reliable. We do not represent that such information is accurate or complete and it should not be relied on as such. Any opinions expressed herein reflect our judgment at this date, all of which are accordingly subject to change. Pareto Forvaltning AS accepts no liability whatsoever for any direct, indirect or consequential loss arising from the use of this document or its contents.

• The fund's KIID, prospectus, annual and semi-annual reports are available from www.paretoforvaltning.no/Rapporter (choose En for reports in English). For KIID documents in Swedish and German go to Customer information.

• Financial information and information about management and control is available from https://www.paretoforvaltning.no/Kundeinformasjon (choose En; General information; Pillar 3).

• Reference to Pareto Global Corporate Bond, means a fund under establishment, subject to CSSF approval, under the Luxembourg umbrella Pareto SICAV.

• Employees of Pareto Forvaltning AS have holdings in the fund(s) described herein.

• Pareto asset management is used as a description, the company name is Pareto Forvaltning AS.

• The source is Pareto Forvaltning unless otherwise stated. Read more about us, our products and risks associated with financial instruments on our website www.paretoforvaltning.no.

• Pareto Forvaltning has signed the United Nations-supported Principles of Responsible Investments (PRI) that include general guidelines for social responsibilities. Read more about PRI and the six principles here: http://www.unpri.org/about-pri/the-six-principles/

Disclaimer | 2

Variable net bias Long/Short Equity funds

Nordic Alpha - $ 150m – Sep 2003

– UCITS version 60m

– Offshore 90m

Nordic Omega - $ 30m – Dec 2005

– Only offshore

– Same investment approach as Nordic Alpha, but focus on small-caps

3

The Nordic economies

Population 27m

GDP $ 1700bn (43k p.c., all above Germany and the UK)

High level of education and R&D

Strong fiscal balances

Good demographics

Flexible labour markets

Open economies = continuous competitive pressures

Total market cap $ 1600bn

Highest density of top-return on capital companies

| 4

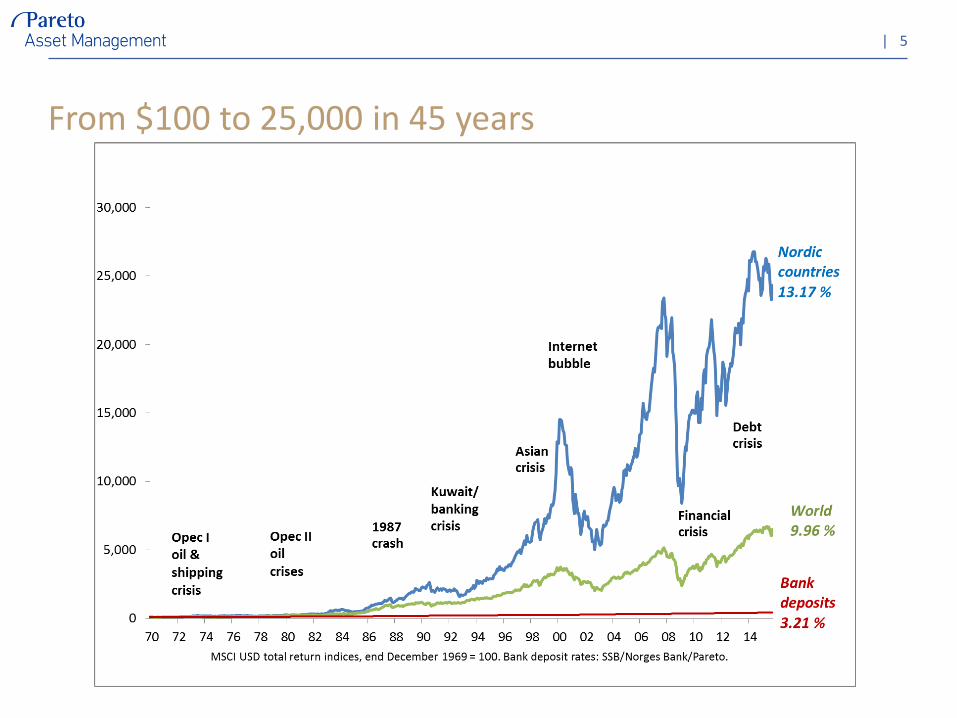

From $100 to 25,000 in 45 years

| 5

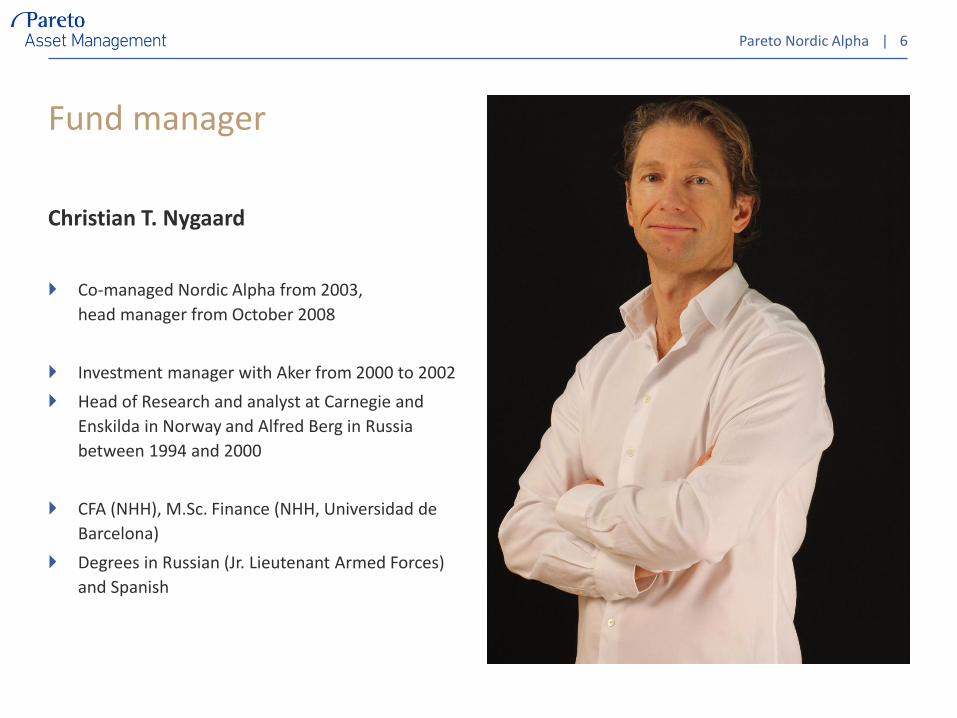

Fund manager

Christian T. Nygaard

Co-managed Nordic Alpha from 2003,

head manager from October 2008

Investment manager with Aker from 2000 to 2002

Head of Research and analyst at Carnegie and

Enskilda in Norway and Alfred Berg in Russia

between 1994 and 2000

CFA (NHH), M.Sc. Finance (NHH, Universidad de

Barcelona)

Degrees in Russian (Jr. Lieutenant Armed Forces)

and Spanish

| 6Pareto Nordic Alpha

Award nominations

| 7

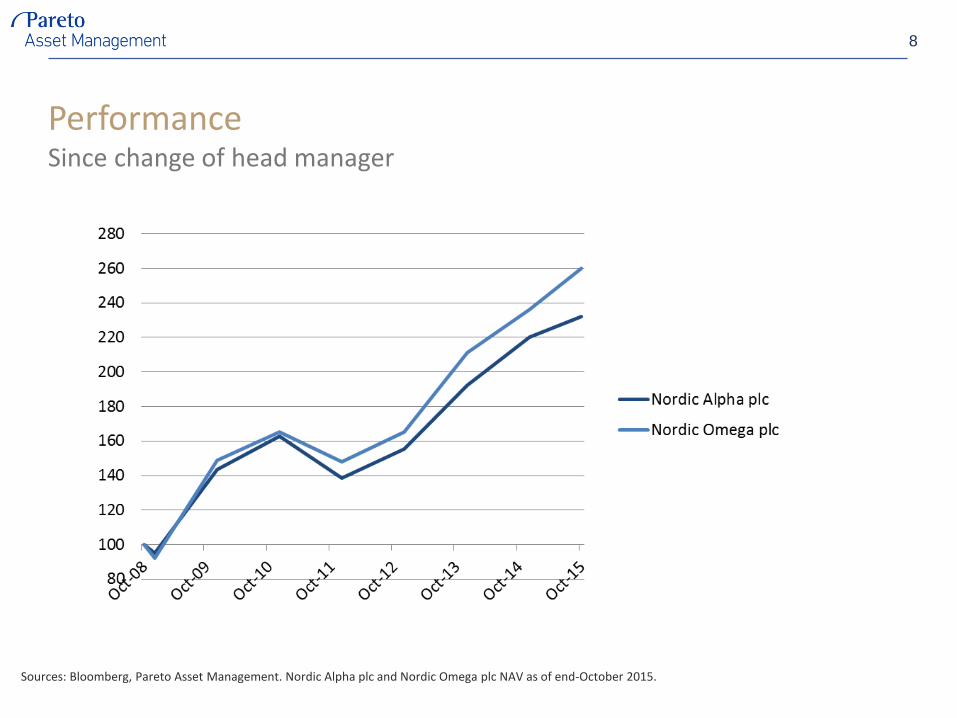

Performance

8

Sources: Bloomberg, Pareto Asset Management. Nordic Alpha plc and Nordic Omega plc NAV as of end-October 2015.

Since change of head manager

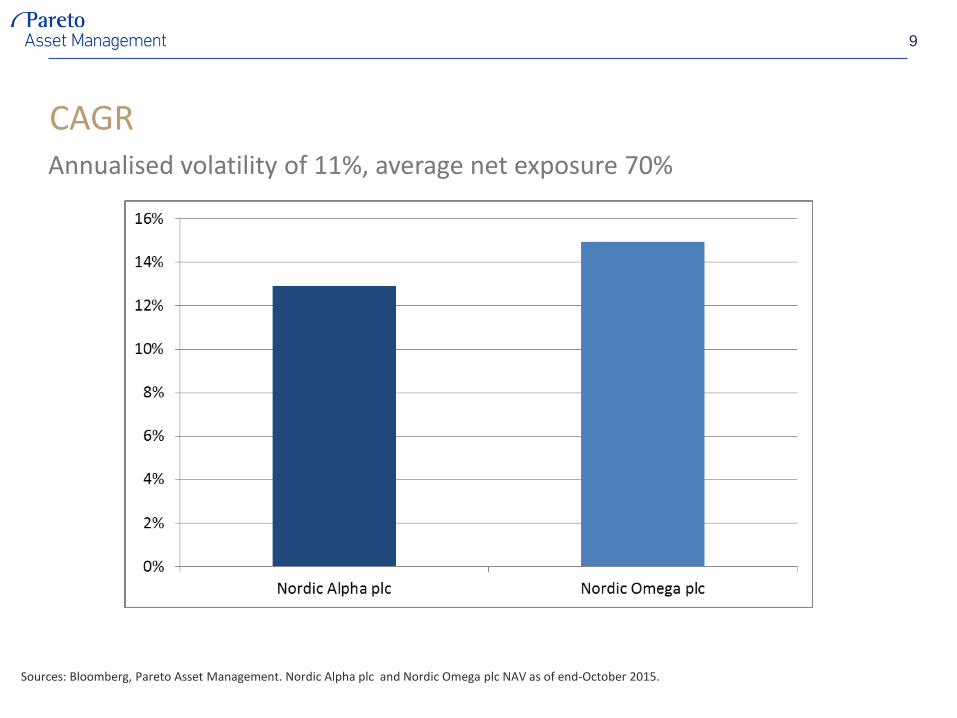

CAGRAnnualised volatility of 11%, average net exposure 70%

9

Sources: Bloomberg, Pareto Asset Management. Nordic Alpha plc and Nordic Omega plc NAV as of end-October 2015.

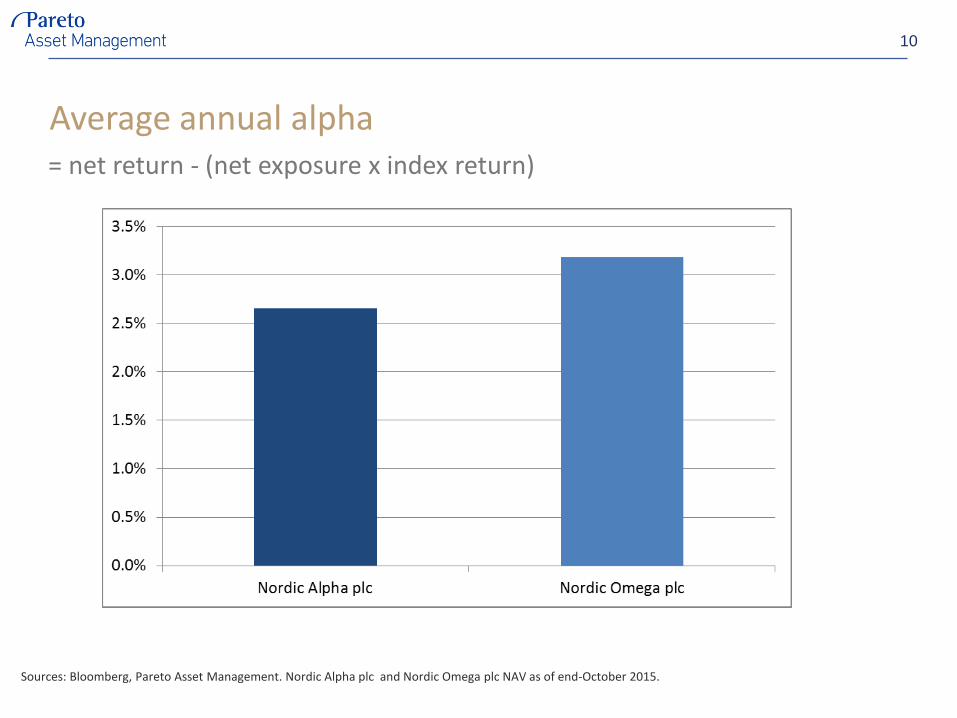

Average annual alpha= net return - (net exposure x index return)

10

Sources: Bloomberg, Pareto Asset Management. Nordic Alpha plc and Nordic Omega plc NAV as of end-October 2015.

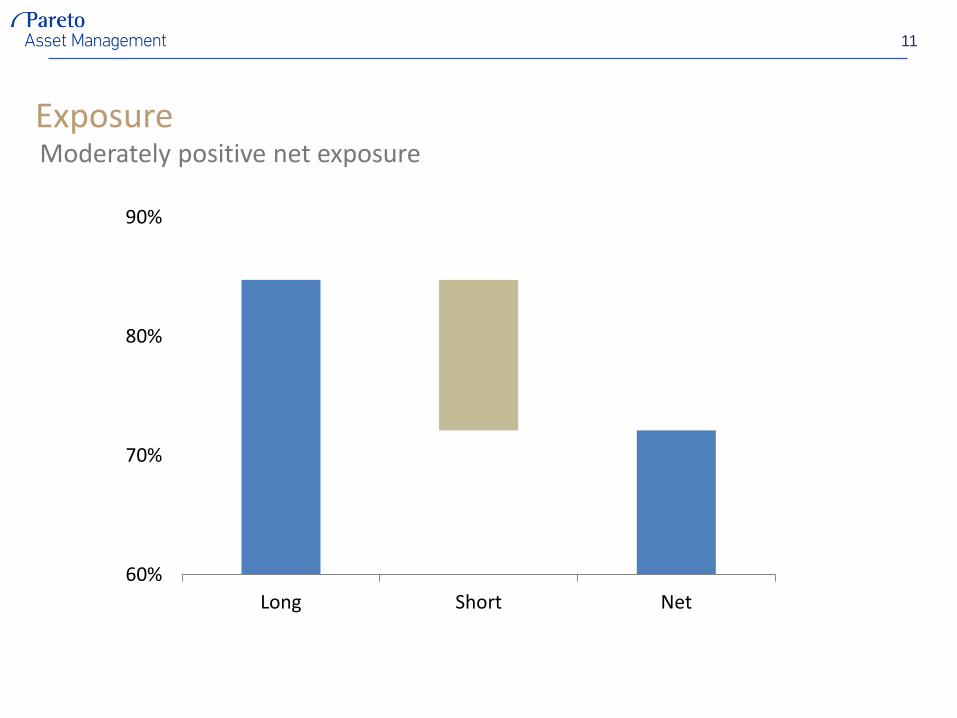

Exposure

11

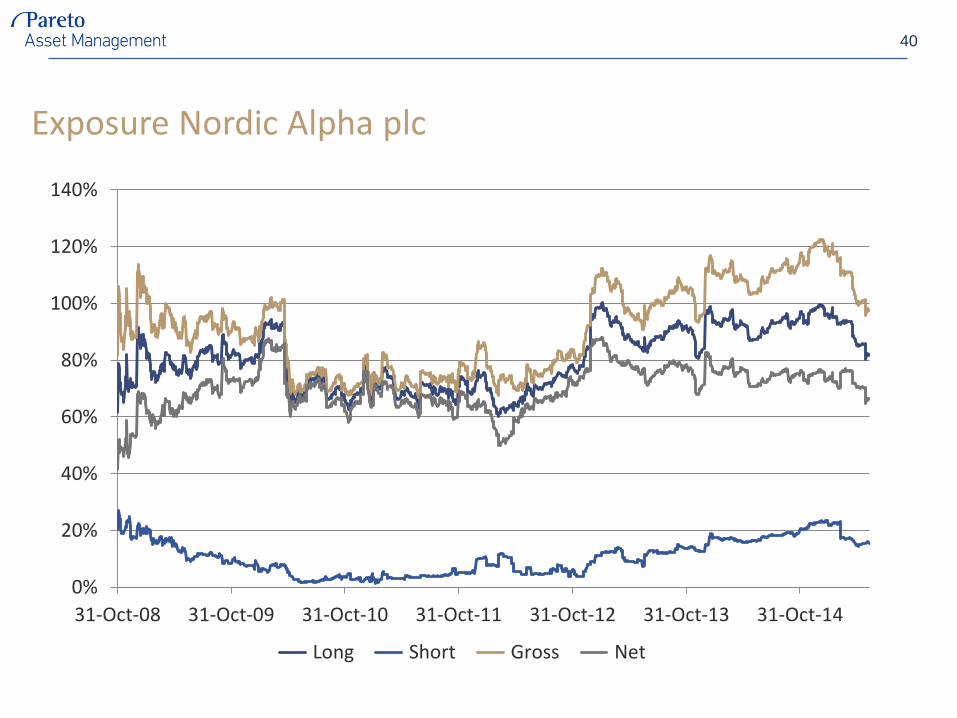

Moderately positive net exposure

60%

70%

80%

90%

Long Short Net

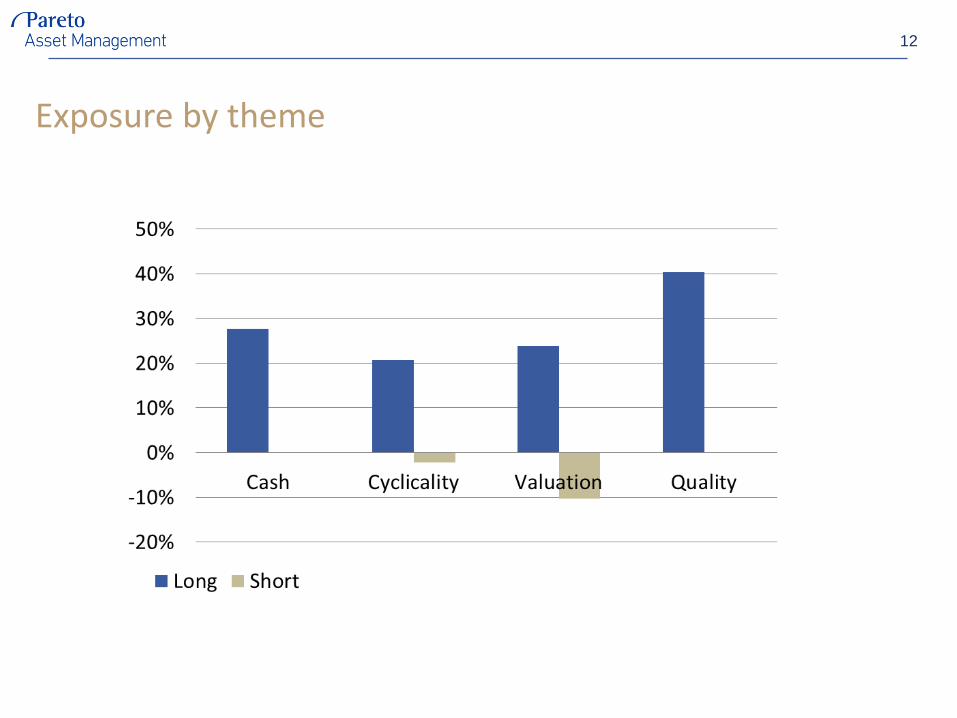

Exposure by theme

12

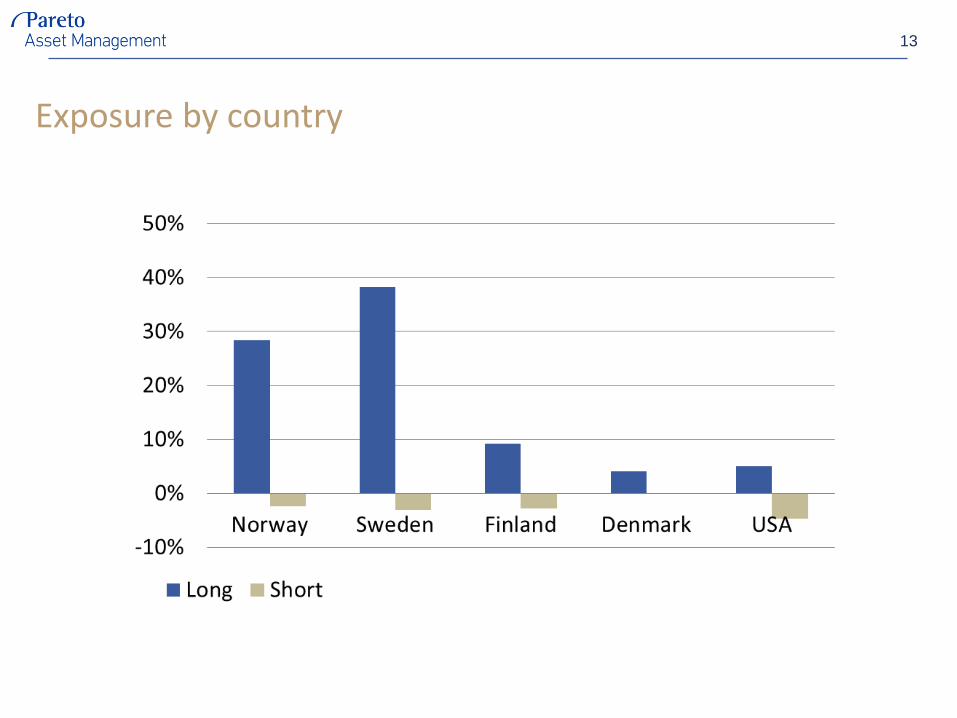

Exposure by country

13

Investment Style

Deep in-house company analysis, focus on stock selection

Aligning bottom-up stock selection with top-down market direction view

Low turnover (0.5/y)

High concentration (appr. 25 positions)

14

Stock selection – QualitySuperior position, growth and capital return at reasonable price

| 15

Stock selection – Quality

Market position – #1 (all companies)

Market share – 31% (#2 player 19%)

Organic growth Q3 – 9%

ROCE 2015 – 17%

EV/EBIT 2015 – 13.5 (discount to Nordic market at 14.8)

Three biggest position owned on average for 7 years with return CAGR of 29%

Median characteristics for our companies

| 16

Stock selection – Quality

38% market share in passive safety (air bags, seat belts)

25% market share in active safety (cameras, radars)

8% organic growth in Q3 vs global car volumes flat

26% ROCE (16e), 41% pre-r&d

EV/EBIT (16e) 11

Total return over 4 years at 209% (CAGR 33%)

1.3m people die in traffic every year

Case – Autoliv – leader in car safety

| 17

Stock selection – Valuation

Opportunities arise with degree of popularity and external shocks

Mean-reverting valuation

| 18

Stock selection – Valuation

Short company in the leisure industry

– ROE of 10% (0-15% last 20y)

– Peak Price/Book multiple of 2.6

– Net debt/EBITDA 4x

– Negative acc. free cash flow last 10 years

– Negative return so far

Cases

| 19

Stock selection – Valuation

Stora Enso

– Mr. Market: «A doomed paper company»

– No! Paper is 20% of CE with 10% ROCE

– Great capital allocation to high-returning pulp and packaging

– 20% of EV in forests

– Total return over 3 years at 93% (CAGR 25%)

Cases

| 20

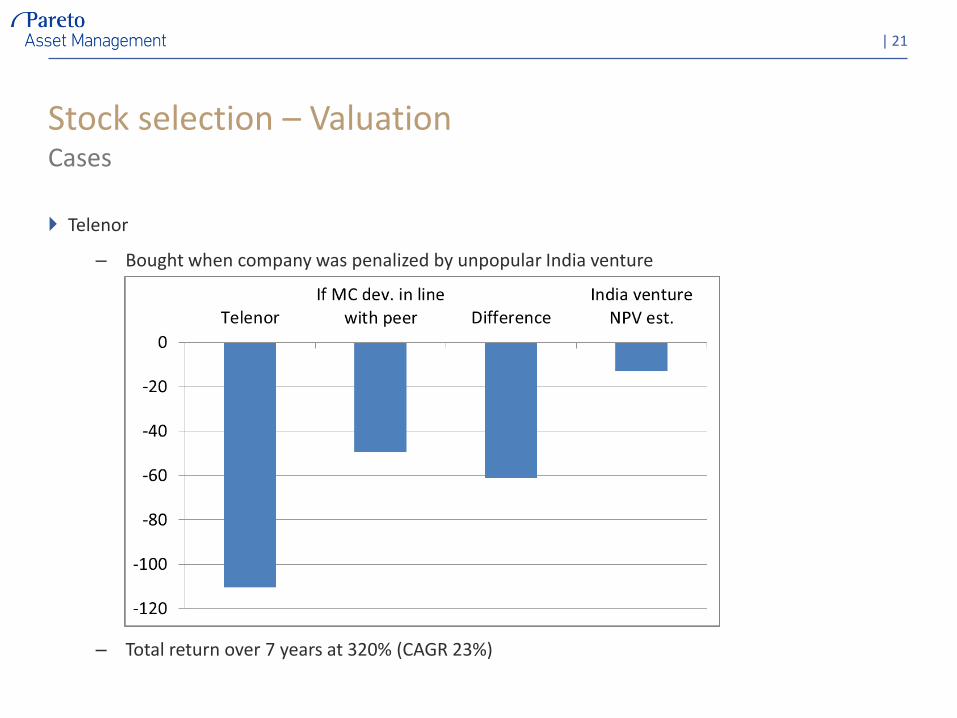

Stock selection – Valuation

Telenor

– Bought when company was penalized by unpopular India venture

– Total return over 7 years at 320% (CAGR 23%)

Cases

| 21

Stock selection – Cyclicality

Companies tend to expand in good times and vice versa, collectively creating boom and bust cycles

Median for the companies we own – ROE ¼ and Price/Book ½ of peak last 15 years

Mean-reverting profitability of cyclical companies

| 22

Stock selection – Cyclicality

Sales flat for 10 years

EBIT margin from 3 to 4%

– Including 1pp average margin headwind per year from higher steel and plastics costs

– And 1pp per year in costs for closing factories

Headwind is about to turn to tailwind

White goods volumes in Europe (1/3 of sales) flat since 2005

EV/EBIT (16e) at 20% discount to market

Case – Electrolux – 10 years of headwinds from costs and volume

| 23

Net exposure management

Anemic demand growth– No pull from China– Cheap money impact on demand in OECD largely behind us– Fiscal policy tool box is empty

Cost of capital will stay lower for longer– Inflation is dead– Central banks stay soft to stimulate demand

Both support the case for our Quality theme (2/3 of our net long)

| 24

Bottom-up meets top-down

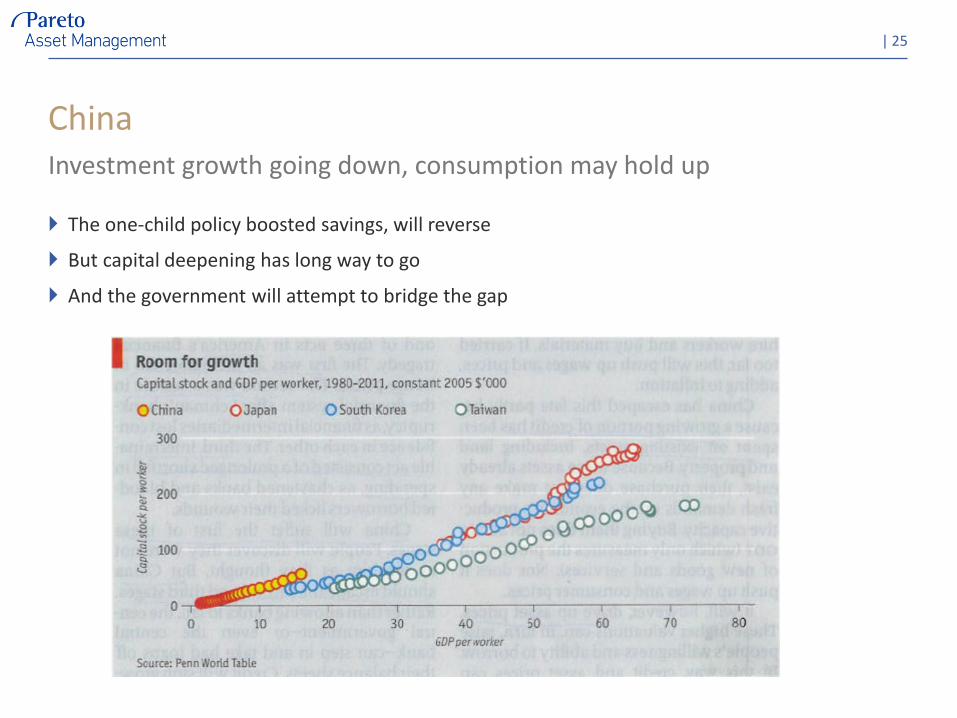

China

The one-child policy boosted savings, will reverse

But capital deepening has long way to go

And the government will attempt to bridge the gap

| 25

Investment growth going down, consumption may hold up

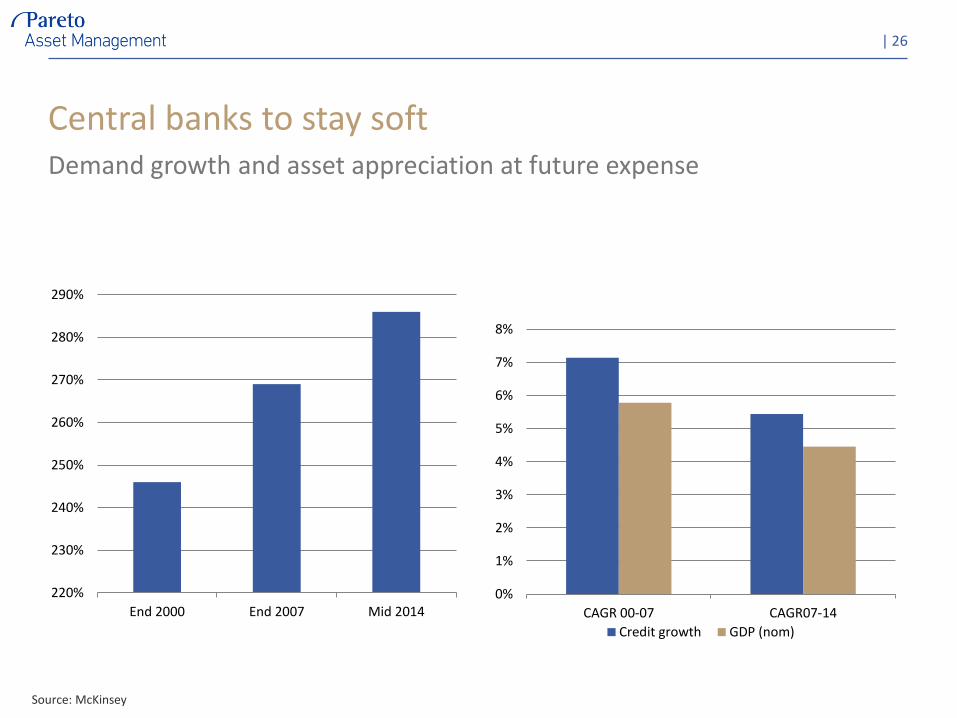

Central banks to stay soft

| 26

Source: McKinsey

220%

230%

240%

250%

260%

270%

280%

290%

End 2000 End 2007 Mid 20140%

1%

2%

3%

4%

5%

6%

7%

8%

CAGR 00-07 CAGR07-14

Credit growth GDP (nom)

Demand growth and asset appreciation at future expense

The cost of capital will stay low

More flexible labour market

High unemployment

Better price transparency for consumers

New capital-efficient business models

Sharing (cars in use 5% of time)

Higher asset turnover

Need to keep credit growth going

Saving the EMU

| 27

Net exposure management

Macro and earnings estimates equal current conditions, so they are in aggregate useless– and subject to large revisions

Consequently, aggregate P/E and EV/EBIT are useless

Price/Book measures the value of the production and earnings capacity

| 28

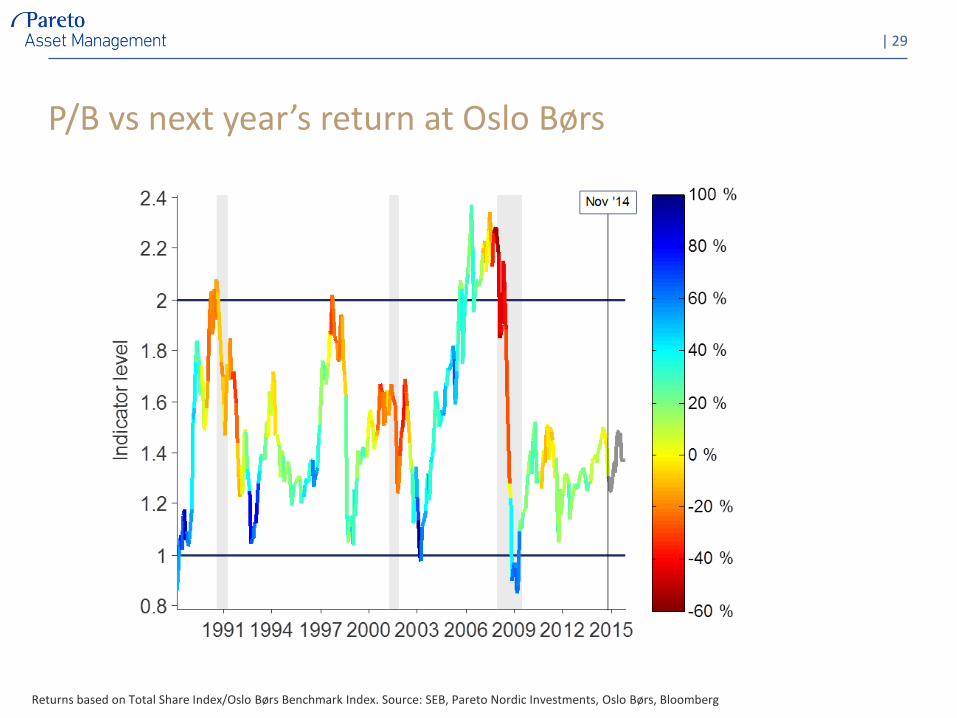

Valuation

P/B vs next year’s return at Oslo Børs

| 29

Returns based on Total Share Index/Oslo Børs Benchmark Index. Source: SEB, Pareto Nordic Investments, Oslo Børs, Bloomberg

APPENDIX

| 30

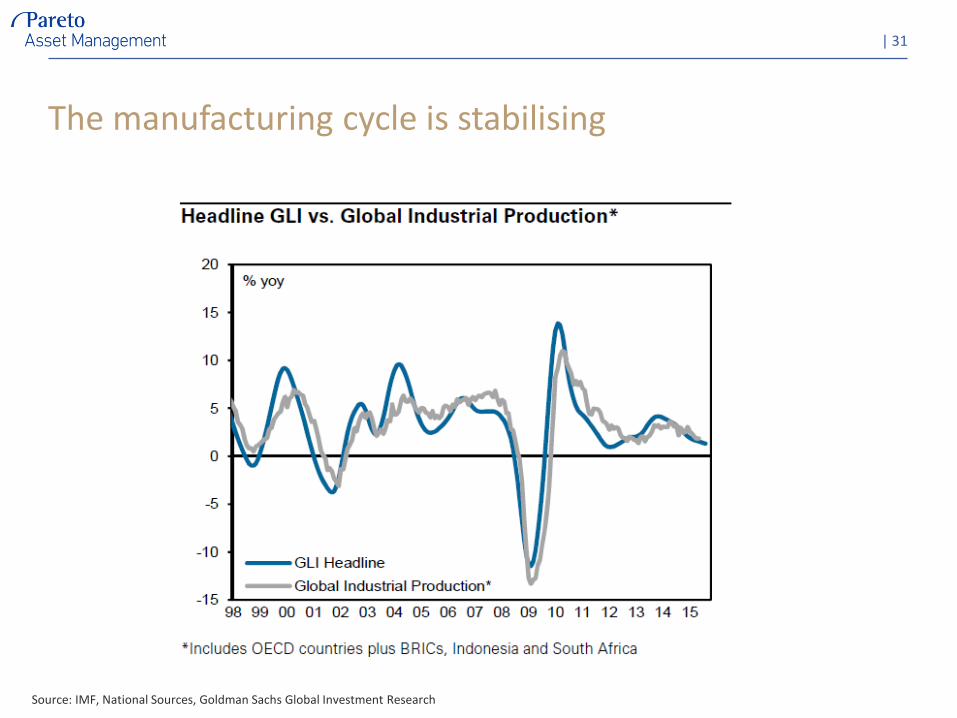

The manufacturing cycle is stabilising

| 31

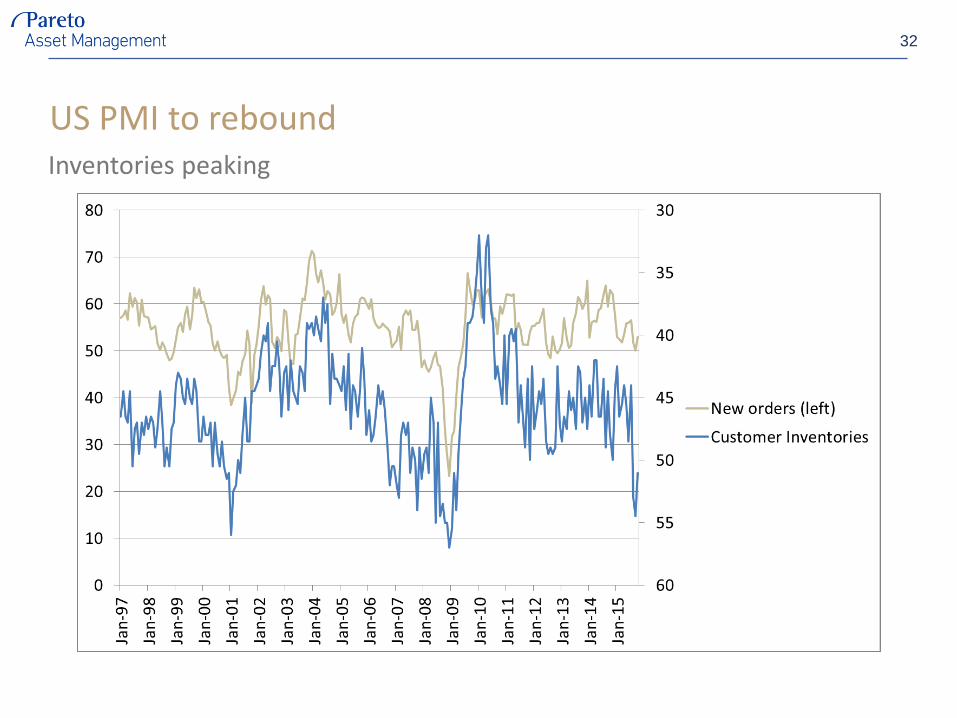

Source: IMF, National Sources, Goldman Sachs Global Investment Research

US PMI to reboundInventories peaking

32

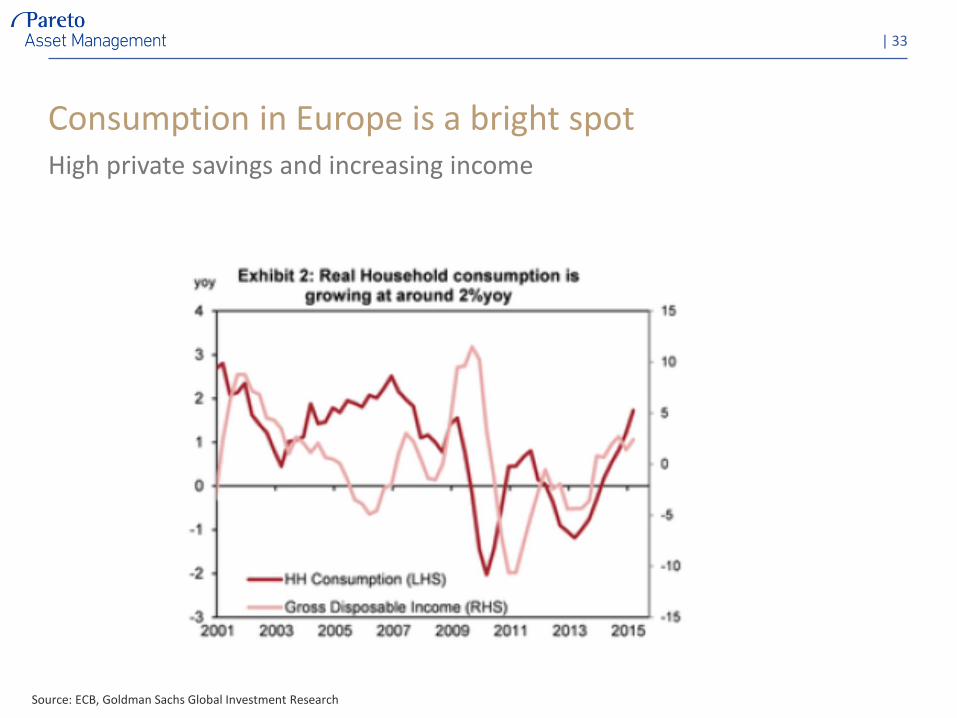

Consumption in Europe is a bright spot

| 33

High private savings and increasing income

Source: ECB, Goldman Sachs Global Investment Research

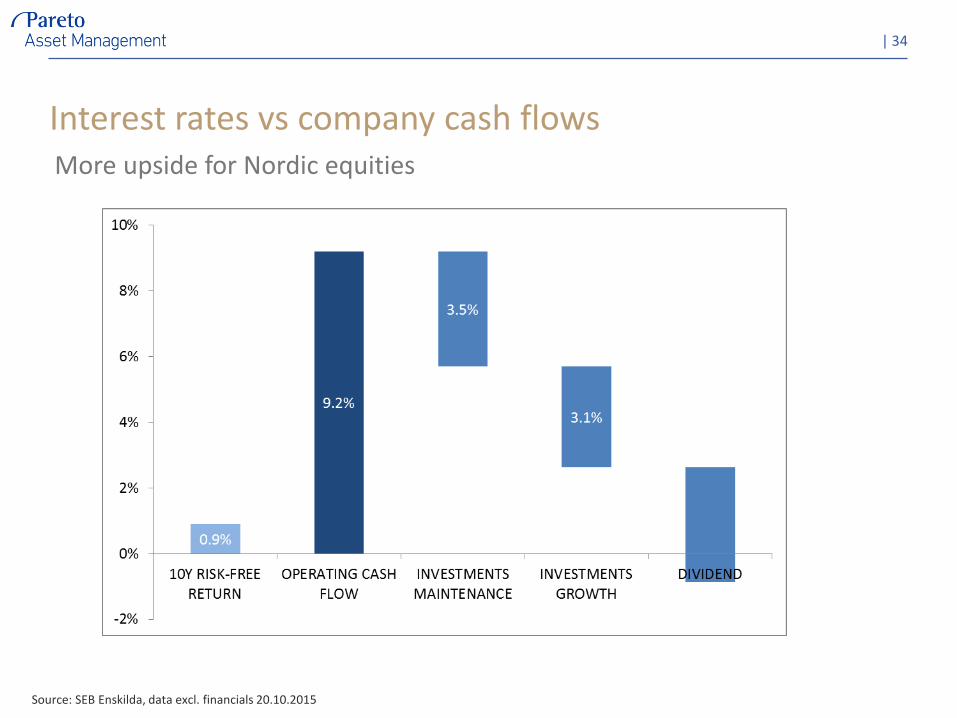

Interest rates vs company cash flowsMore upside for Nordic equities

| 34

Source: SEB Enskilda, data excl. financials 20.10.2015

3,2%

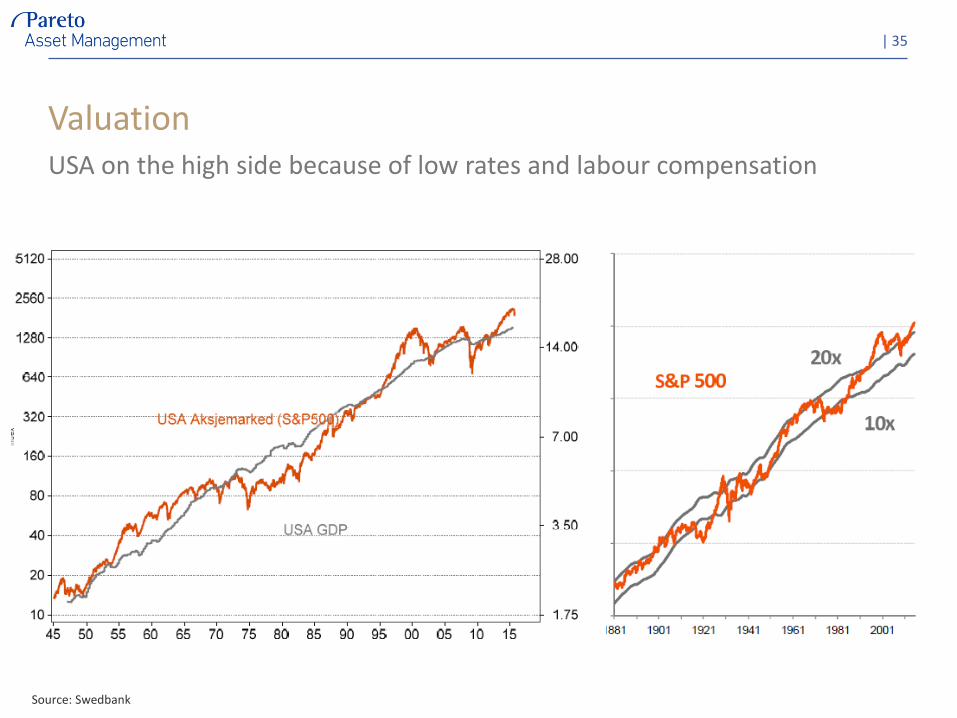

Valuation

| 35

Source: Swedbank

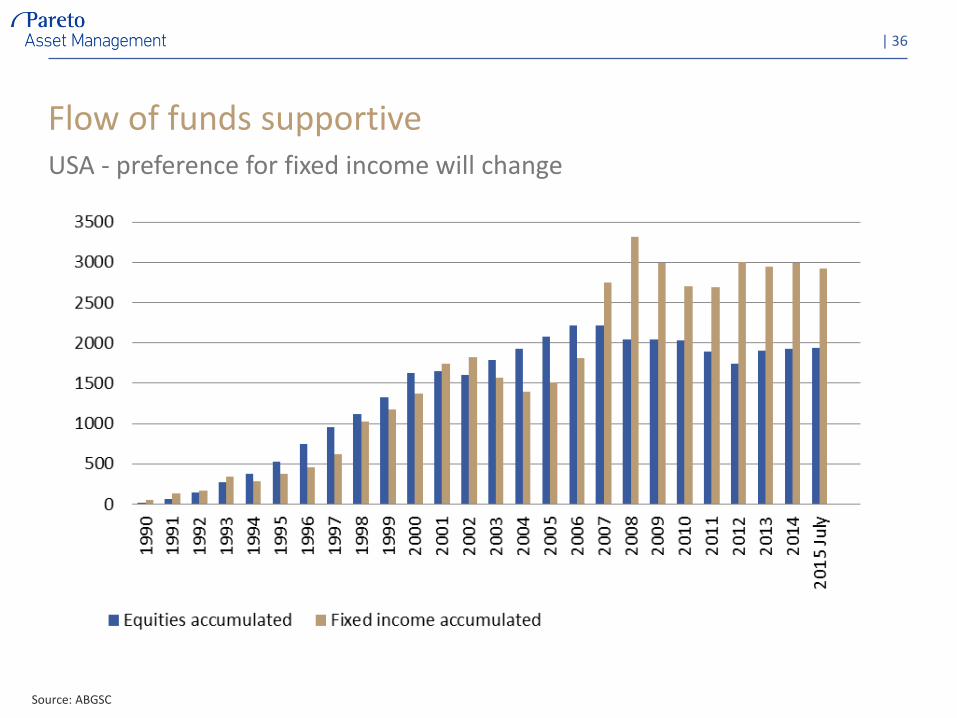

USA on the high side because of low rates and labour compensation

Flow of funds supportive

| 36

Source: ABGSC

USA - preference for fixed income will change

Other positive factors

Consumer surplus not in GDP

– What would you pay for this?

Energy will still get cheaper

More efficient logistics and capital employed

– Corporate margins at an all-time high, but asset turn grows 2.5% annually– Three years of asset turn growth neutralises 1pp margin decline

| 37

Source: ABGSC

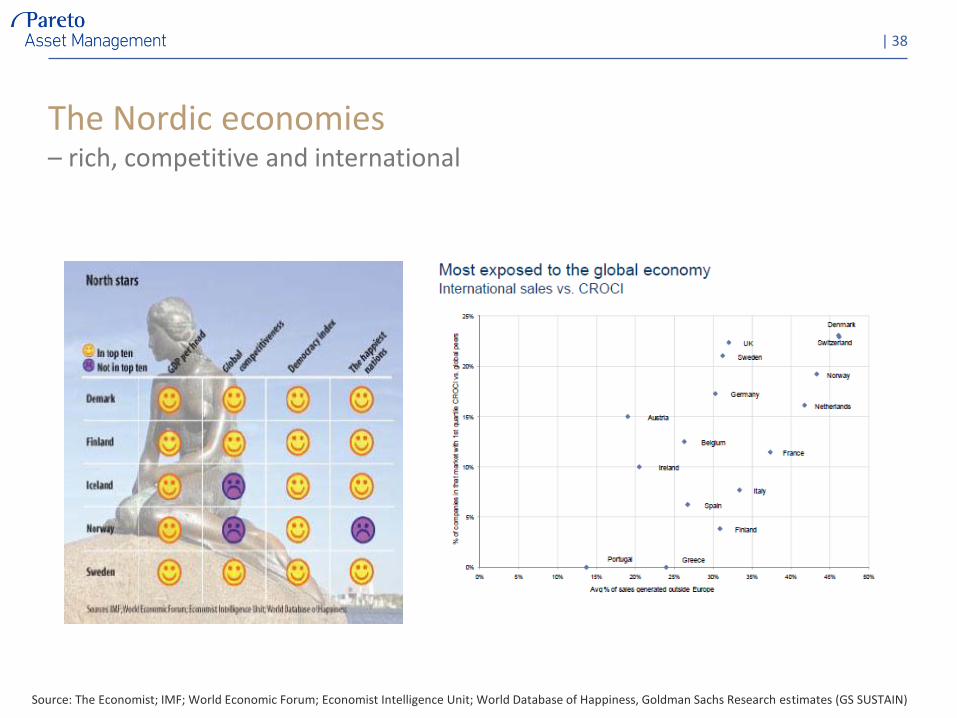

The Nordic economies– rich, competitive and international

| 38

Source: The Economist; IMF; World Economic Forum; Economist Intelligence Unit; World Database of Happiness, Goldman Sachs Research estimates (GS SUSTAIN)

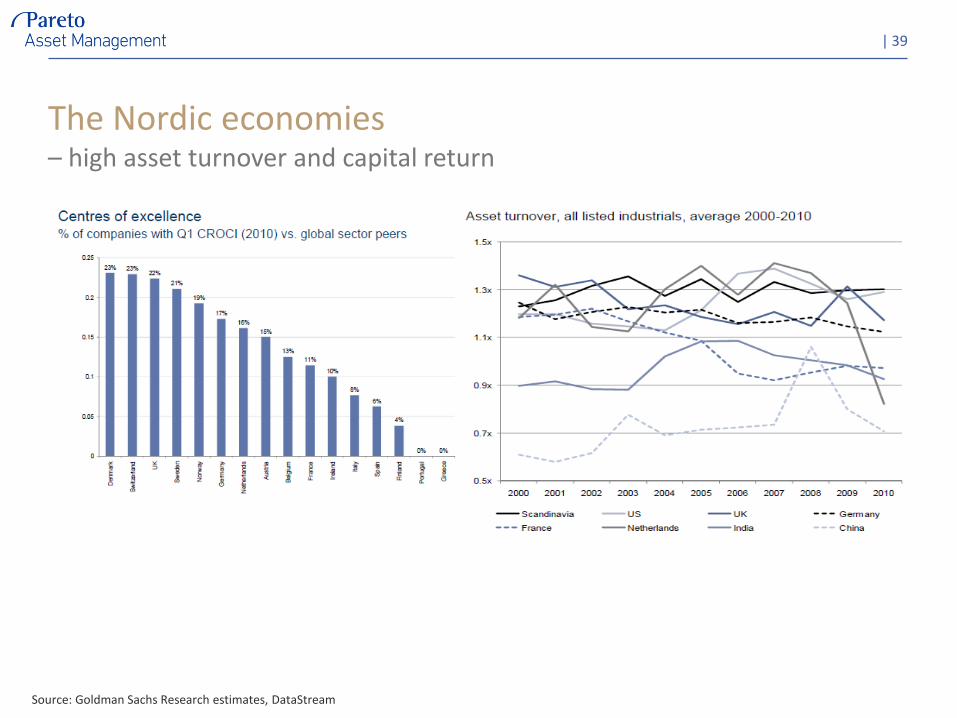

The Nordic economies– high asset turnover and capital return

| 39

Source: Goldman Sachs Research estimates, DataStream

Exposure Nordic Alpha plc

40

0%

20%

40%

60%

80%

100%

120%

140%

31-Oct-08 31-Oct-09 31-Oct-10 31-Oct-11 31-Oct-12 31-Oct-13 31-Oct-14

Long Short Gross Net

The short side

Regardless of market view

Selective stock selection across all three vectors

Pair trades

Possible hedging with current positive market view

EMU break-up

– Telecom and utilities in countries with weak current account and debt position

Monetary policy impact breaks down

– But long in companies with credible organic growth, construction, gold miners

China’s investment boom is mature

– Commodities and capital goods

When negative market view

High beta (materials, capital goods, consumer discretionary)

| 41

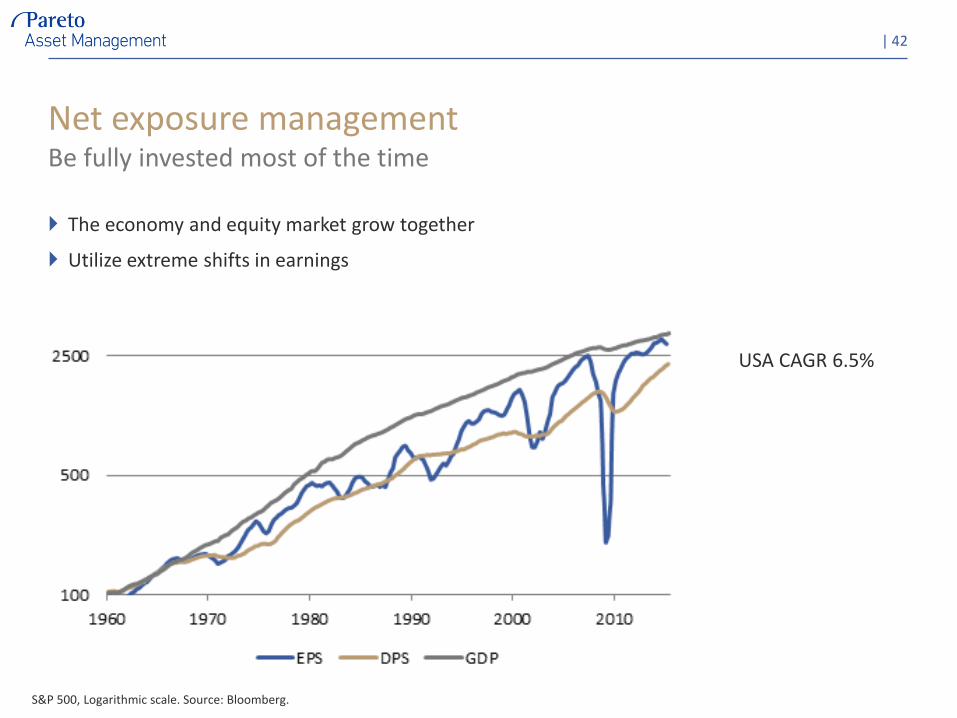

Net exposure management

The economy and equity market grow together

Utilize extreme shifts in earnings

Be fully invested most of the time

| 42

S&P 500, Logarithmic scale. Source: Bloomberg.

USA CAGR 6.5%

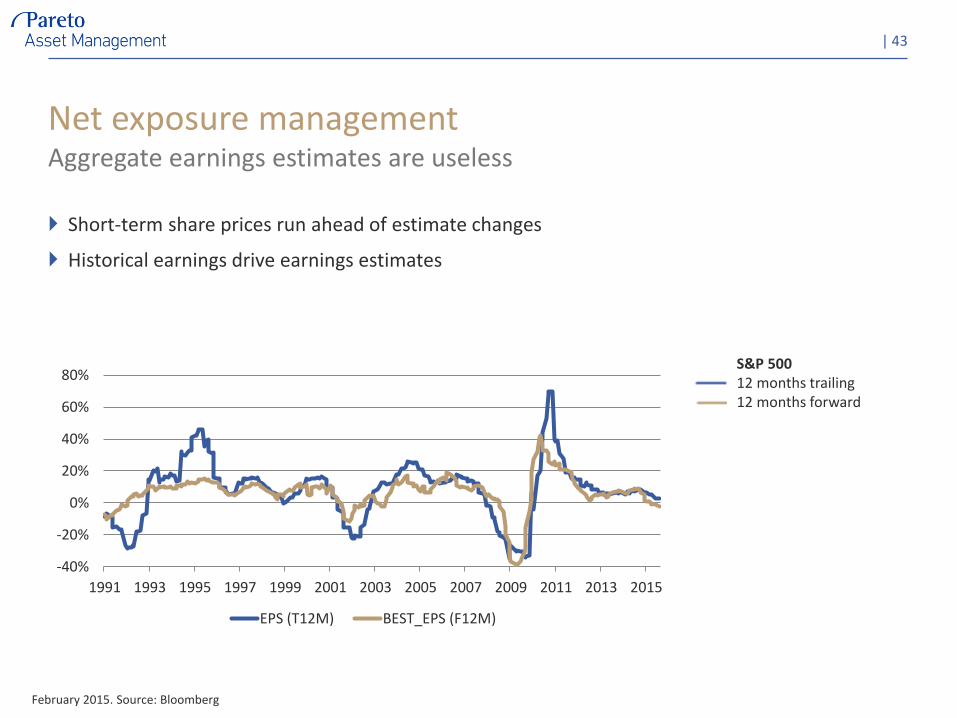

Net exposure management

Short-term share prices run ahead of estimate changes

Historical earnings drive earnings estimates

Aggregate earnings estimates are useless

| 43

February 2015. Source: Bloomberg

S&P 500 12 months trailing12 months forward

-40%

-20%

0%

20%

40%

60%

80%

1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015

EPS (T12M) BEST_EPS (F12M)

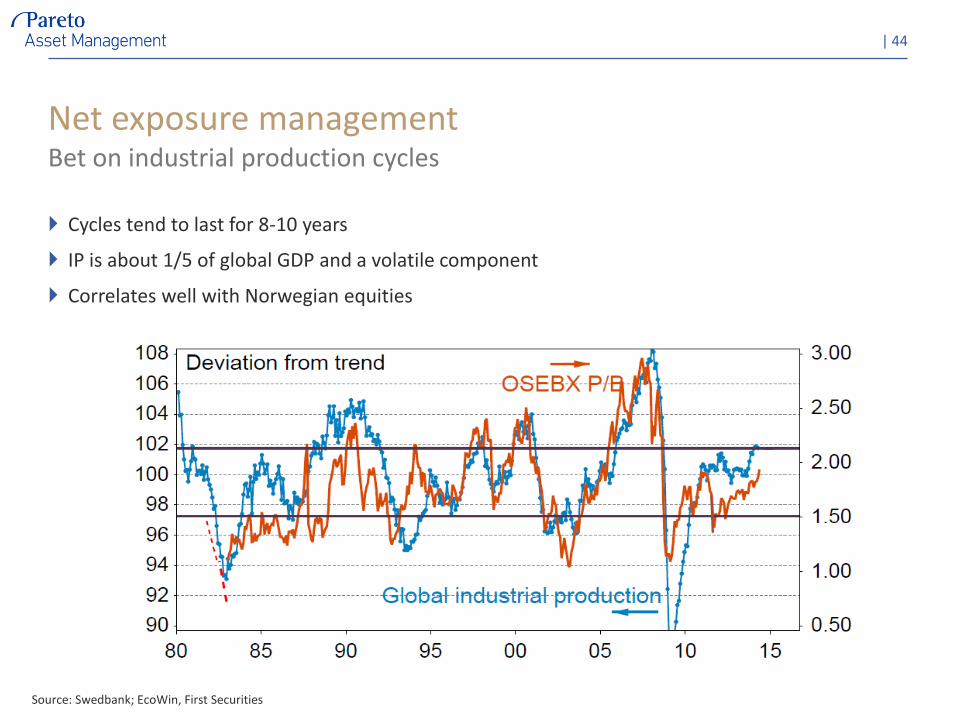

Net exposure management

Cycles tend to last for 8-10 years

IP is about 1/5 of global GDP and a volatile component

Correlates well with Norwegian equities

Bet on industrial production cycles

| 44

Source: Swedbank; EcoWin, First Securities

![[Nordic Built Challenge 17.12.2013] Trine Pertou Mach, Nordic Built: Nordic Built](https://img.pdfslide.us/doc/110x75/547174dcb4af9f980a8b4ad9/nordic-built-challenge-17122013-trine-pertou-mach-nordic-built-nordic-built.jpg)