Embed Size (px)

Citation preview

Steve Wanklin

Non people costs optimization

2 Copyright © Capgemini 2013. All Rights Reserved

Analyst Day 2013 I June 19-20

New Services to Differentiate & Accelerate the Infra Strategy

ITS IOS

2013 2011

2015

Establish Basis for Future

Business Evolution

Service Management (Industrialisation)

Streamline the Legacy

Service Integration (Rolls Royce, State of

Texas)

Service Aggregation (BMC, RSA)

Service Orchestration

(BMC, RSA)

1

2

3

3 Copyright © Capgemini 2013. All Rights Reserved

Analyst Day 2013 I June 19-20

Infra Approach to Industrialization

Bid & Solution • Service Catalogue • Price Benchmarks • Global Team

Transition • PM Community • DVI Incentive • Sales to Delivery Handover

Delivery • Global Delivery Network • Unit Costing Target • DVI Improvement

Industrialization

Drive significant costs out of non-labour cost base and enable major change in labour support costs

Total Cost of Ownership (TCO)

Deployment of standard tools for Service Management and Systems Management

Systems & Tools

Security

Analyst Day 2013 I June 19-20

Deployment of standard tools for Security Management

4 Copyright © Capgemini 2013. All Rights Reserved

Analyst Day 2013 I June 19-20

Co-opetition Partner-Aligned

Competition Agnostic-Player

Integrated stacks Vertical alignment

Asset light

Industrialised & automated Highly converged estate High-touch/high-value

“Invest for the future” “Impact on SBU”

Strategic investments

GTM Opportunities Shared risks & shared rewards “Appropriate” commitments “Don’t sell the crown jewels”

Traditional platforms Lateral focus

Asset intensive

Highly customized “one-offs” Fragmented/diverse technologies High-touch/low-value

“Buy for the here and now” “Impact on me”

BAU procurement

Where we have been • Historically, our cost of delivering Infrastructure

Services had been high and there had been limited degree of standardization in the management of our estate.

Where we want to be • The move away from traditional operating

models towards more complex relationships and alliances with strategic suppliers, and even competitors.

• Relationships based on co-investing and co-innovating.

Partnering for Success – Business Pioneer

5 Copyright © Capgemini 2013. All Rights Reserved

Analyst Day 2013 I June 19-20

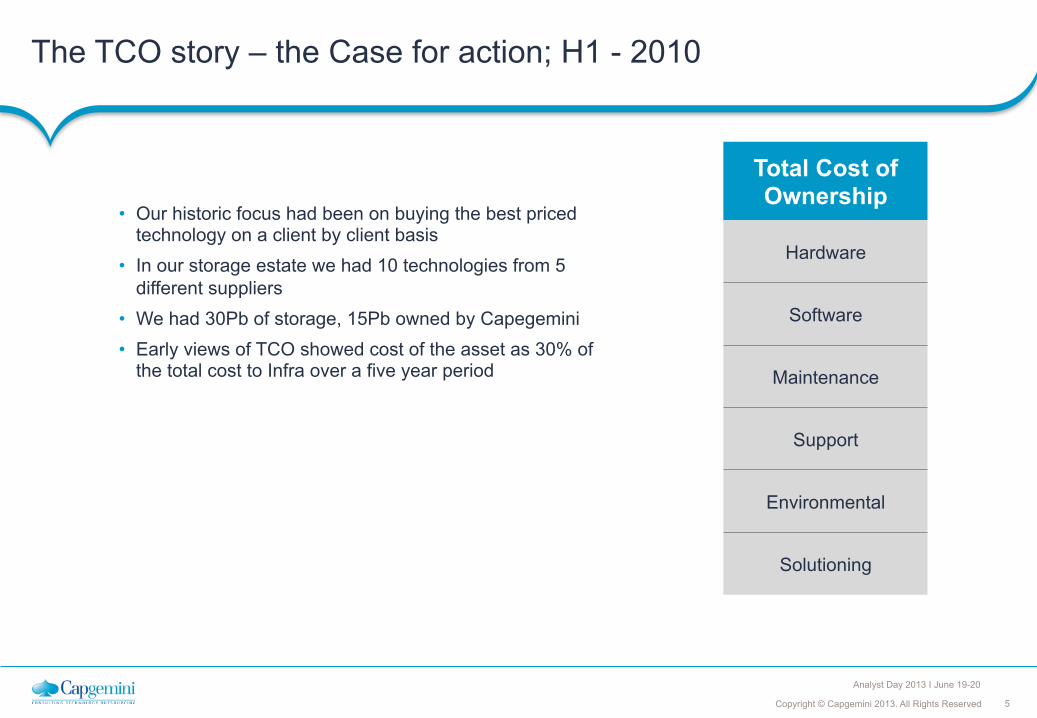

• Our historic focus had been on buying the best priced technology on a client by client basis

• In our storage estate we had 10 technologies from 5 different suppliers

• We had 30Pb of storage, 15Pb owned by Capegemini • Early views of TCO showed cost of the asset as 30% of

the total cost to Infra over a five year period

Total Cost of Ownership

Hardware

Software

Maintenance

Support

Environmental

Solutioning

The TCO story – the Case for action; H1 - 2010

6 Copyright © Capgemini 2013. All Rights Reserved

Analyst Day 2013 I June 19-20

• We reviewed the storage estate with EMC and proposed; • Migration to two different EMC technologies VMAX and VNX

• 3 standard configurations Gold, Silver and Bronze to deliver service and cost differential

• We made a commitment to 25Pb of storage over five years • Prices based on this approach gave a circa 30% improvement

on existing purchase prices • EMC to become Capgemini’s 6th Strategic Partner

The TCO Story – the EMC Proposal

Total Cost of Ownership

Hardware

Software

Maintenance

Support

Environmental

Solutioning

7 Copyright © Capgemini 2013. All Rights Reserved

Analyst Day 2013 I June 19-20

• We have met the five year commitment in the first two years, in June 2013

• 80% of the Capgemini storage is now on an EMC platform • Plan is to have 80% managed by the Storage COE in

India by YE • COE support ratios have improved from 118Tb/FTE to 300TB/

FTE

• We have achieved a 60% reduction in the TCO of storage • This has helped build a cost base and a partnership that is

driving our success with new clients

Before: • 924 TB storage • 4,953 drives • Average drive size 186 GB • 122 m² space used • € 216k/year on power

After: • 936 TB storage • 896 drives • Average drive size 1,120 GB • 18 m² space used • € 41k/year on power

80% less hardware, space, power 60% less TCO (5years)

HGI Storage Data-centre details

The TCO Story – the EMC Proposal – Two Years Later

8 Copyright © Capgemini 2013. All Rights Reserved

Analyst Day 2013 I June 19-20

EMC HGI Deal

HP Bravo Deal

BMC ITSMaaS

Q3’11 Q1’12 Q2’12 2013

Ben

efits

Rea

lizat

ion

• Standardized storage and data protection

• Standardized x86 server architecture across Data Centres

• Migrate 200+ clients to new ITSMaaS solution

• ITBMaaS for standardized billing portal • Converged computing decision • Data Centre consolidation strategy

The Road Map

Questions

10 Copyright © Capgemini 2013. All Rights Reserved

Analyst Day 2013 I June 19-20

Industrialisation of Traditional Services Requires Acceleration

• Many clients with existing, single source outsourcing contracts want to multi-source, but struggle with integration

• Services integration involving traditional IT outsourcing (ITO) towers is on a collision course with emerging visions of cloud service orchestration (Forrester)

• The global market opportunity for SI deals is estimated at €5n

Disaggregation of Services

• The Infrastructure Services market evolution and the rise of new services have a price erosion effect that we estimate as 3 – 10%

• Up to 20% decrease on TCV for traditional services should be expected on renewals

• RIM addressable market size of ≈ €5bn growing by 25% YoY

Margin Pressure

• Buyer preference moving to on-demand, pay-per-use & “as a Service” models

• Traditional OS services are increasingly commoditized

• Security, data sovereignty and lack of integration are restricting Cloud uptake

• Targeted capture of 2% of €28bn cloud service market

Technology disruption

Infra response: Market leading “Service Integration” offer

Infra response: XRIM and Accelerated TCO agenda

Infra response: Service Aggregation and Service

Brokering plays

Service Orchestration

11 Copyright © Capgemini 2013. All Rights Reserved

Analyst Day 2013 I June 19-20

Target is to Reduce Costs across the End-to-end TCO Stack

• Reduced price-point on preferred product sets • Increased focus on fewer standards and suppliers • Transformation and displacement of higher cost

infrastructure • Newer technologies; de-duplication, virtual connect...

• Reduced price-point, and economies of scale • Global agreements, swap-outs & spares in place of fix

• Common solutions, reduce training and support costs • Focus on Centre of Excellence in GDC’s • Best-in-class delivery models

• Technology refresh benefits on footprint and power • Data centre design optimization

• Solution architects enabled to focus on the winning solution and less on the underlying technology supplier

TCO Management - approach to our Three Year Plan

Total Cost of Ownership

Hardware

Software

Maintenance

Support

Environmental

Solutioning

The information contained in this presentation is proprietary. © 2013 Capgemini. All rights reserved.

www.capgemini.com

About Capgemini With more than 125,000 people in 44 countries, Capgemini is one of the world’s foremost providers of consulting, technology and outsourcing services. The Group reported 2012 global revenues of EUR 10.3 billion. Together with its clients, Capgemini creates and delivers business and technology solutions that fit their needs and drive the results they want. A deeply multicultural organization, Capgemini has developed its own way of working, the Collaborative Business ExperienceTM, and draws on Rightshore®, its worldwide delivery model.

Rightshore® is a trademark belonging to Capgemini