Embed Size (px)

Citation preview

No Money Down FinancingNo Money Down Financing

Find out how to buy a house with 0.00% down

payment.

IntroductionIntroduction

We would like to walk you through some recently announced programs that will enable you to buy a home with 0.00% down payment.

We understand that there are many potential homeowners who have a good solid income, good credit but have not been able to save the money for a down payment.

IntroductionIntroductionJust last year I met a client who had been

renting the same townhouse for 25 years. If that client could add up all the rent they paid, they could have owned that home in half that time.

As homes increase in value year over year, the longer one waits to enter the market, the larger the down payment they needed to purchase a home. Some people just can’t save that amount of money.

IntroductionIntroduction

Lets stop and look, at how much you are paying to rent over 5 years.

An average 3 bedroom apartment/ townhouse in Burlington cost $1600.00 per month.

$1600 X 12 months = $19,200 X 5 years $96,000 (not including inflation)

IntroductionIntroduction

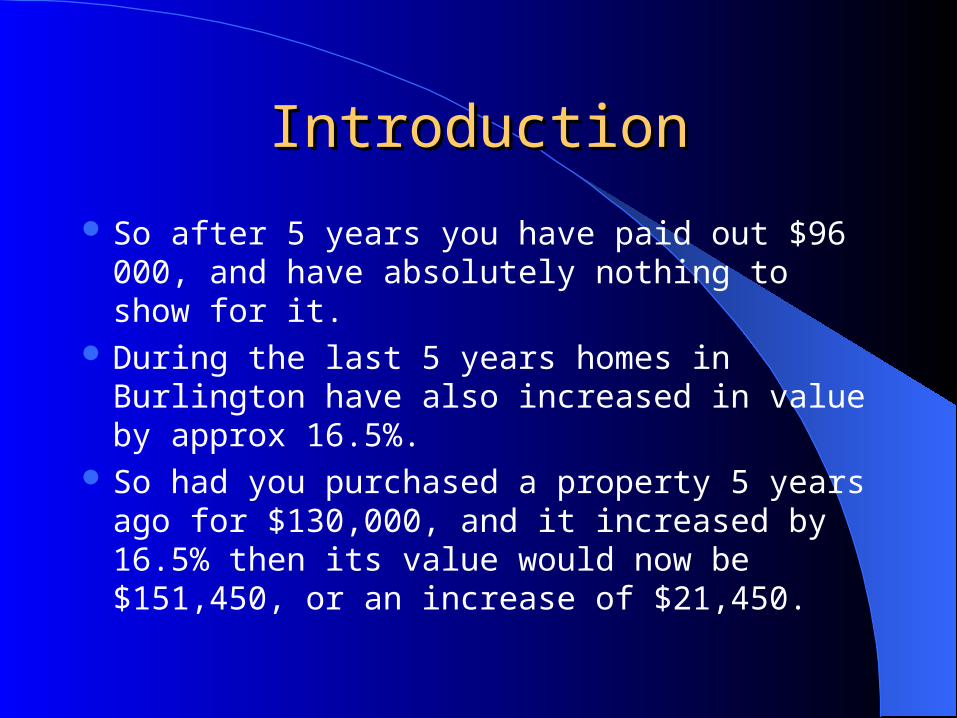

So after 5 years you have paid out $96 000, and have absolutely nothing to show for it.

During the last 5 years homes in Burlington have also increased in value by approx 16.5%.

So had you purchased a property 5 years ago for $130,000, and it increased by 16.5% then its value would now be $151,450, or an increase of $21,450.

Had you bought 5 years agoHad you bought 5 years ago

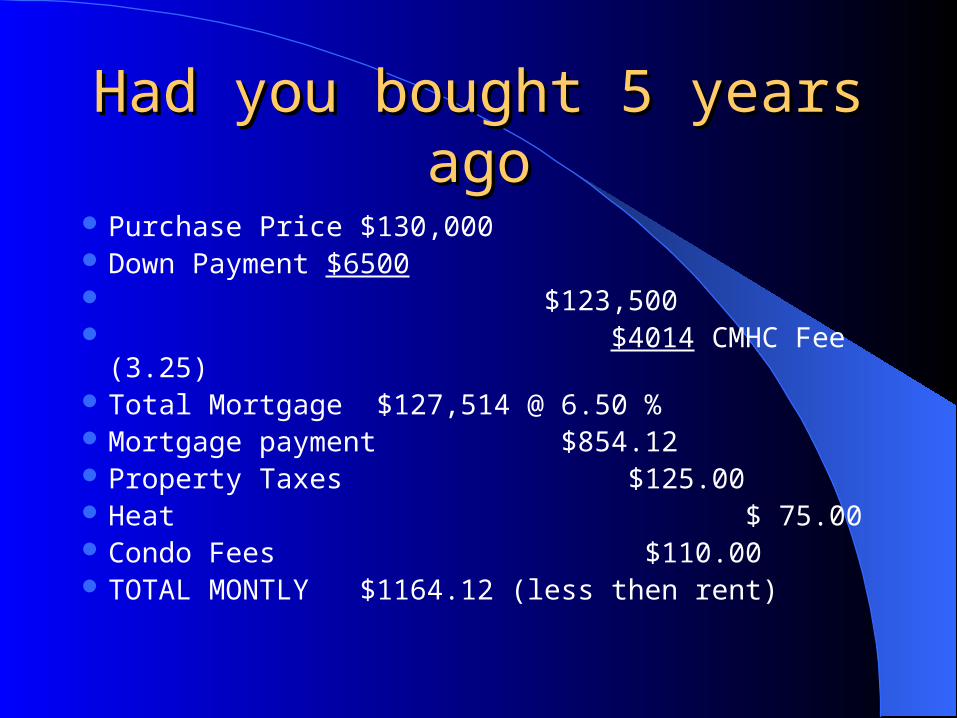

Purchase Price $130,000 Down Payment $6500 $123,500 $4014 CMHC Fee (3.25) Total Mortgage $127,514 @ 6.50 % Mortgage payment $854.12 Property Taxes $125.00 Heat $ 75.00 Condo Fees $110.00 TOTAL MONTLY $1164.12 (less then rent)

Had you bought 5 years agoHad you bought 5 years ago

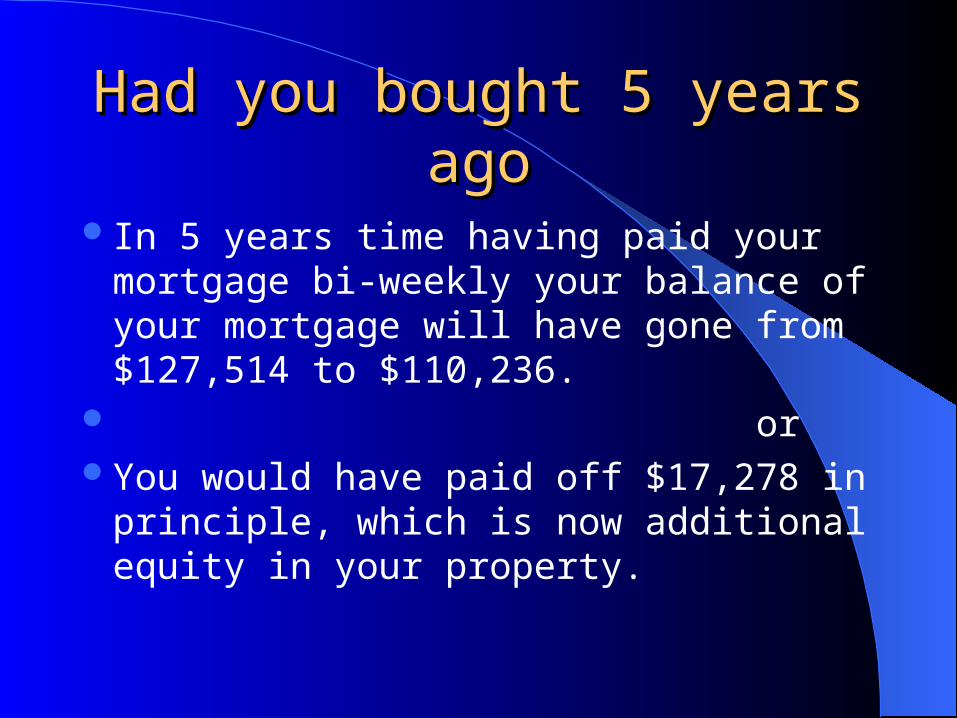

In 5 years time having paid your mortgage bi-weekly your balance of your mortgage will have gone from $127,514 to $110,236.

or You would have paid off $17,278 in

principle, which is now additional equity in your property.

Renting vs BuyingRenting vs Buying

If you rent for 5 years and payout $96,000, you still have nothing

Renting vs BuyingRenting vs Buying

However if you had bought 5 years ago….Your home has increase in value by

$21,450So you now own a house worth $151,450 With a mortgage balance of $110,236 Your Equity $ 41,214Plus the ability to have your home continue

to increase in value for years to come.

You can’t afford not to buy. You can’t afford not to buy.

So as you can see over 5 years buying could create in excess of $40,000 in equity.

So why have you not purchased a house??

NO DOWN PAYMENT !!!!!!!!!

How can I buy a home.How can I buy a home.

We now have 2 separate programs that will enable you to buy a house and you will only have to come up with the closing costs, legal fees of approx $1200 and Land Transfer tax, of approx $1025, (based on a $130,000 purchase price). A total of $2225.

If you have paid first and last months rent and your rent is $1200, now you only need an additional $1000.00.

How can I buy a home.How can I buy a home.

Now you must understand that if you had the down payment, the income, and the good credit history, then you could basically use any lender to approve your mortgage, at full discounted rates.

Therefore the lenders who are giving you the ability to buy without a down payment are taking a greater risk, and will therefore charge a higher rate.

PROGRAM #1PROGRAM #1

I have a lender who will now give you 5% cash back, if you take a 5 Year mortgage at posted rates.

Now please note that the 5% cash back CAN’T be used to directly fund the down payment. CMHC and GE Capital have a very strict policy against this.

PROGRAM #1PROGRAM #1

If you have a family member who is willing to “gift” you the 5% down payment, (they must also provide you a letter confirming that the amount is actually a gift and does not require repayment.). Once the house closes you receive the 5% cash back.

Now what you do with that cash is your business.

PROGRAM #1PROGRAM #1

Some people may be concerned with having to pay the higher interest rate over the 5 years, lets look at what this increased rate will actually cost you.

These are sample rates only……

PROGRAM #1PROGRAM #1

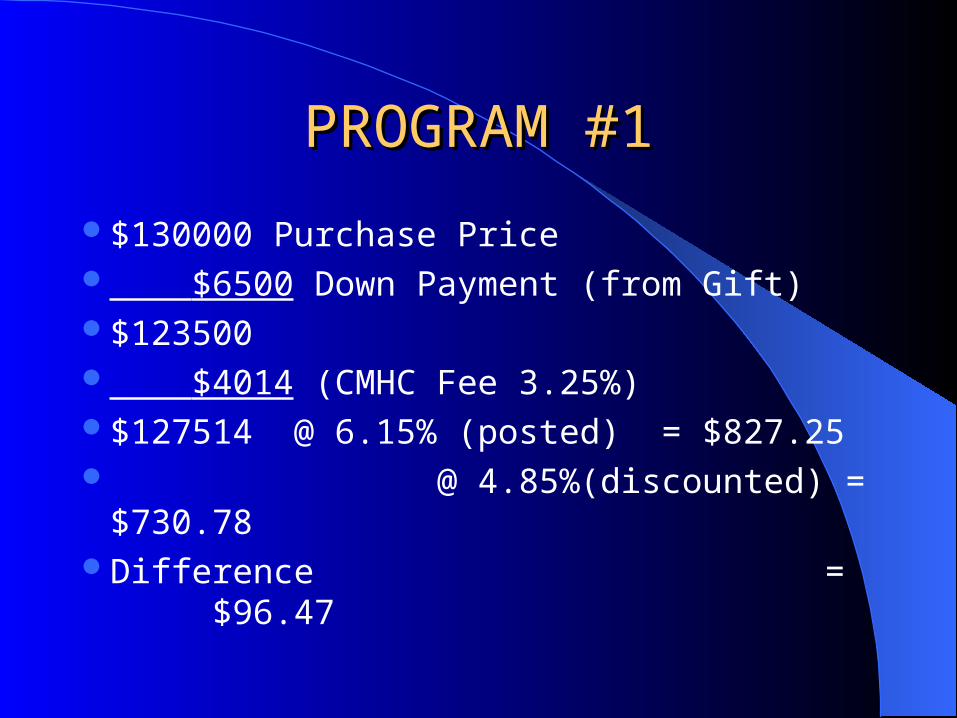

$130000 Purchase Price $6500 Down Payment (from Gift)$123500 $4014 (CMHC Fee 3.25%) $127514 @ 6.15% (posted) = $827.25 @ 4.85%(discounted) = $730.78Difference = $96.47

PROGRAM #1PROGRAM #1

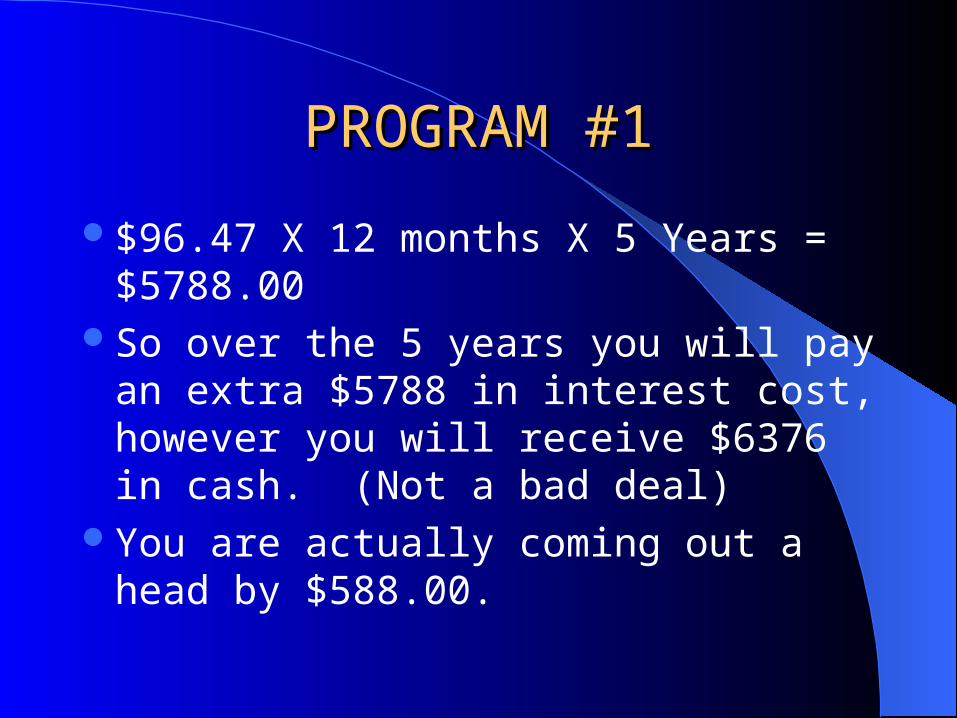

$96.47 X 12 months X 5 Years = $5788.00So over the 5 years you will pay an extra

$5788 in interest cost, however you will receive $6376 in cash. (Not a bad deal)

You are actually coming out a head by $588.00.

PROGRAM #1PROGRAM #1

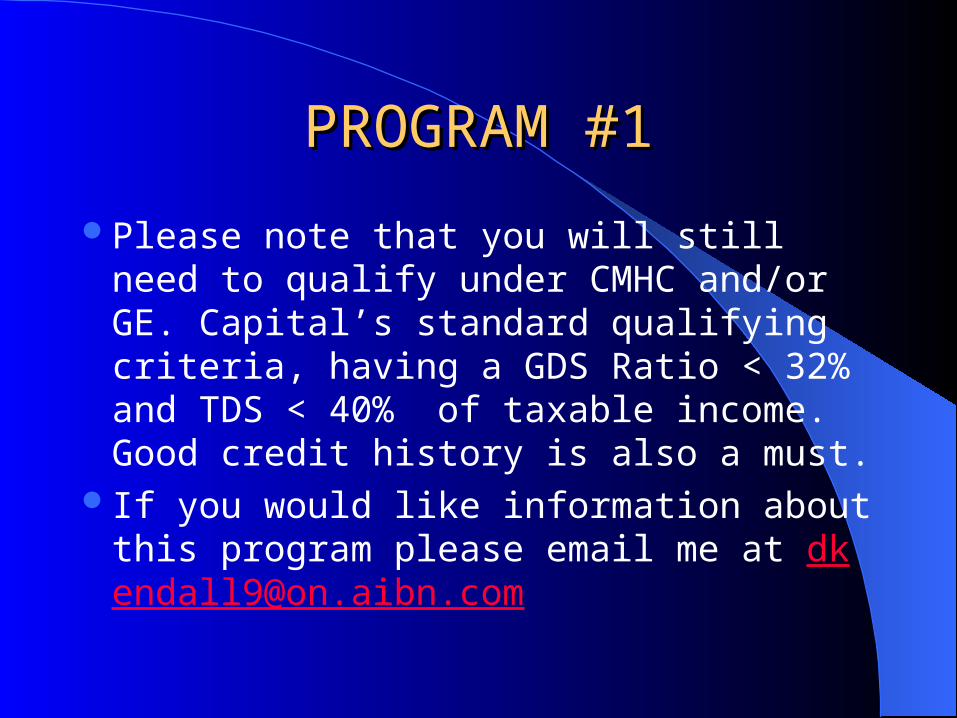

Please note that you will still need to qualify under CMHC and/or GE. Capital’s standard qualifying criteria, having a GDS Ratio < 32% and TDS < 40% of taxable income. Good credit history is also a must.

If you would like information about this program please email me at [email protected]

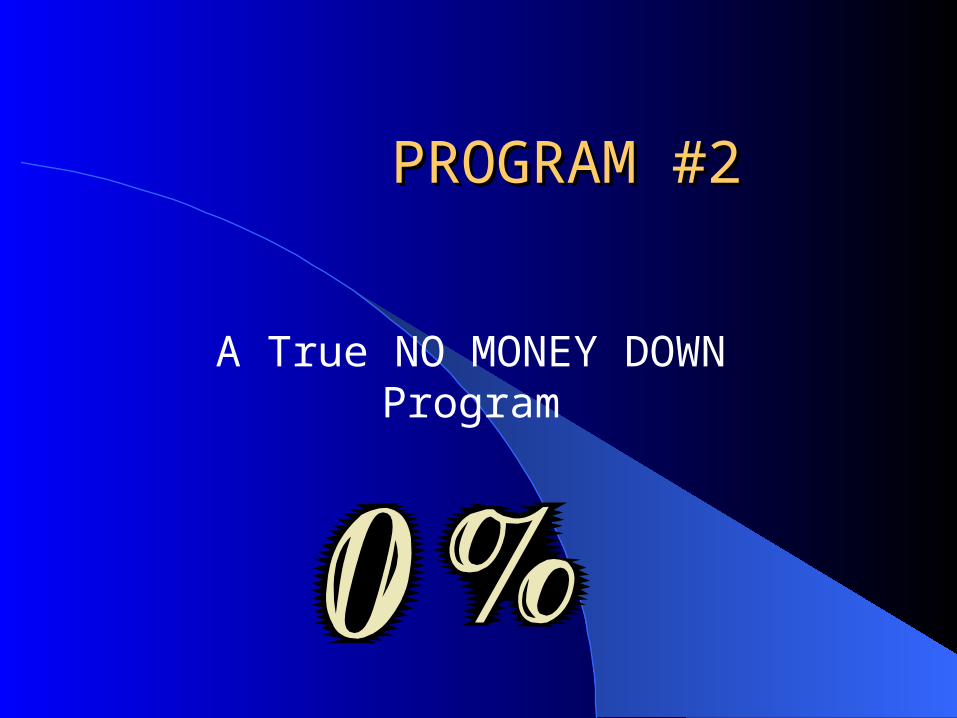

PROGRAM #2 PROGRAM #2

A True NO MONEY DOWN Program

Program #2Program #2

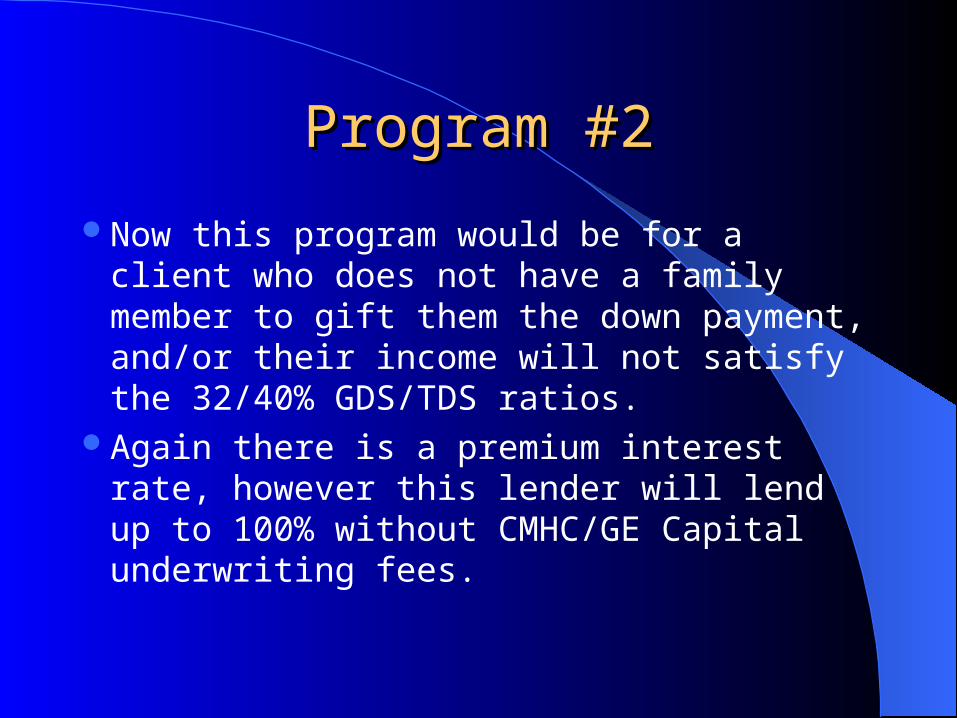

Now this program would be for a client who does not have a family member to gift them the down payment, and/or their income will not satisfy the 32/40% GDS/TDS ratios.

Again there is a premium interest rate, however this lender will lend up to 100% without CMHC/GE Capital underwriting fees.

Program #2Program #2

With taking CMHC/GE Capital out of the equation you are immediately saving the 3.25% CMHC/GE Capital underwriting fee.

This will save you $4014.00 ( Based on $130,000 purchase price with 5% down)

That is the good news…..

Program #2Program #2

Now please keep in mind, in order for a lending institution to lend 100% without CMHC or GE Capital underwriting, all as a first mortgage, they are taking a substantially higher risk with this type of financing.

But not needing a second mortgage means you are not paying 14 –15% rates or additional processing fees.

Program #2Program #2

Their interest rate is at the 5 year “posted” rate. Their current 5 Year rate is 6.15* Before you start saying these rates are too high,

finish this presentation. But “No Processing Fees” They are also very specific about what type of

applicant they are willing to consider. * rates subject to change without notice

Program #2Program #2

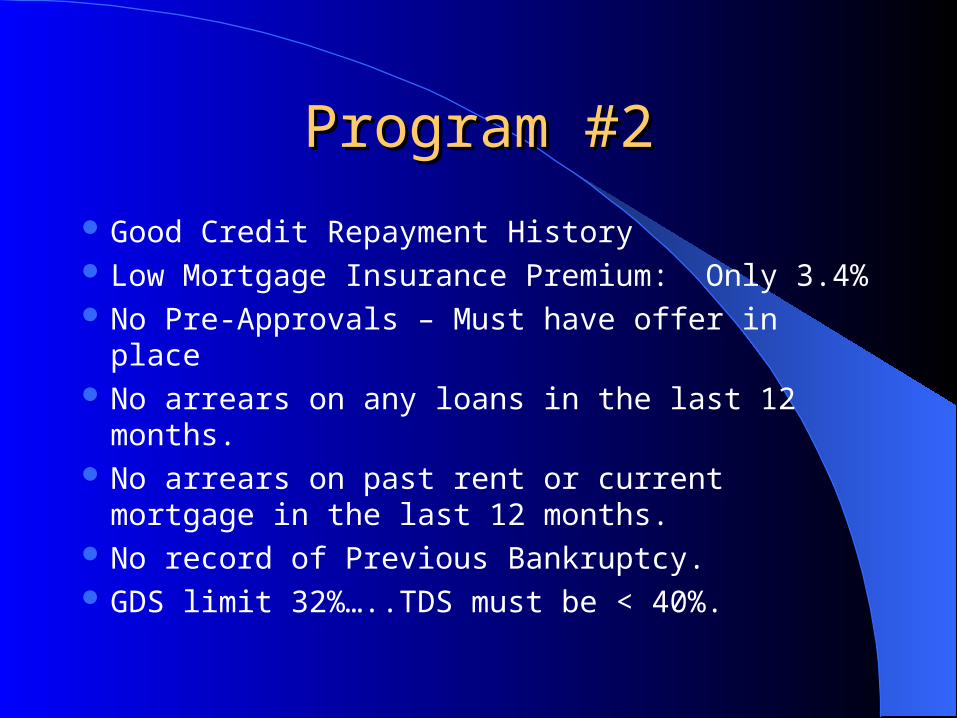

Good Credit Repayment History Low Mortgage Insurance Premium: Only 3.4% No Pre-Approvals – Must have offer in place No arrears on any loans in the last 12 months. No arrears on past rent or current mortgage in the

last 12 months. No record of Previous Bankruptcy. GDS limit 32%…..TDS must be < 40%.

Program #2Program #2

Again one might ask, how much higher is my payment going to be as a result of the higher mortgage rate.

We will use the same example$130,000 purchase price, with “No” money

down.

Program #2Program #2

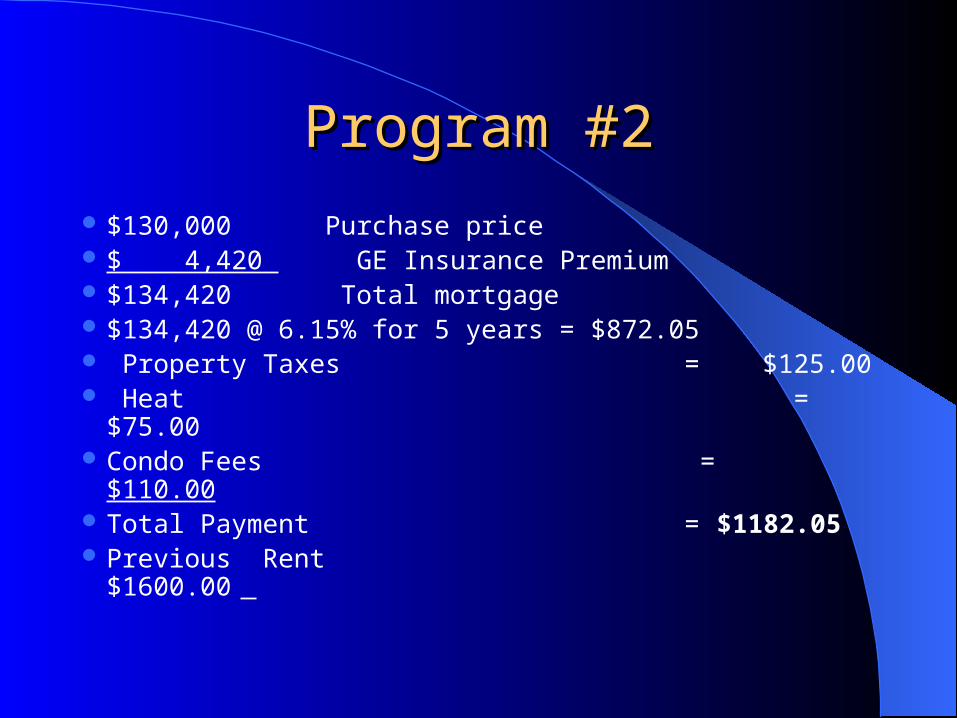

$130,000 Purchase price $ 4,420 GE Insurance Premium $134,420 Total mortgage $134,420 @ 6.15% for 5 years = $872.05 Property Taxes = $125.00 Heat = $75.00 Condo Fees = $110.00 Total Payment = $1182.05 Previous Rent $1600.00

Program #2Program #2

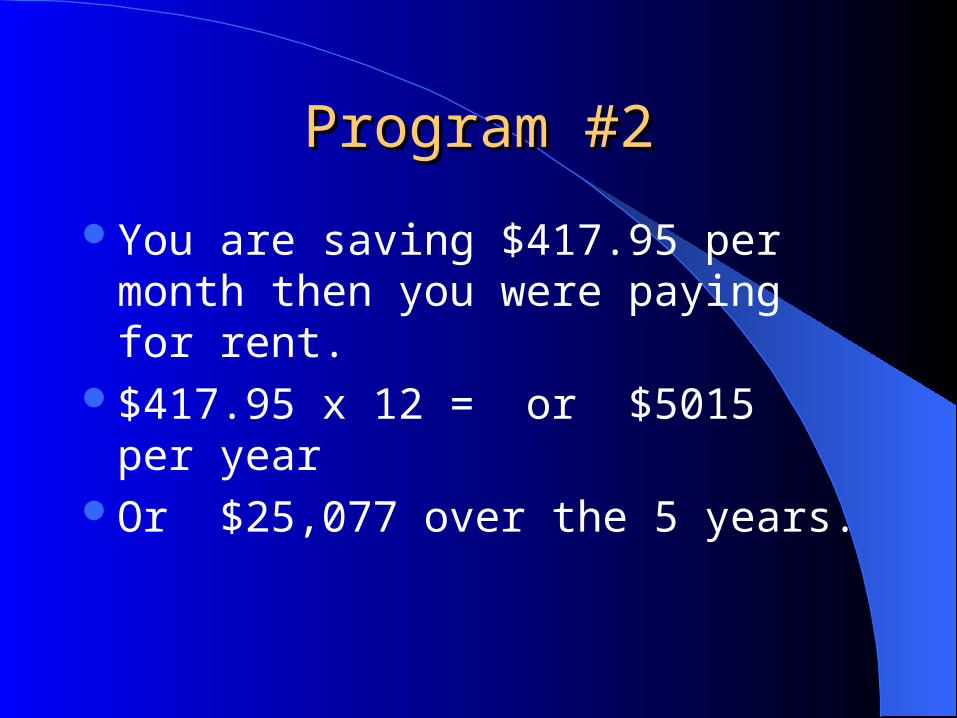

You are saving $417.95 per month then you were paying for rent.

$417.95 x 12 = or $5015 per yearOr $25,077 over the 5 years.

Program #2Program #2

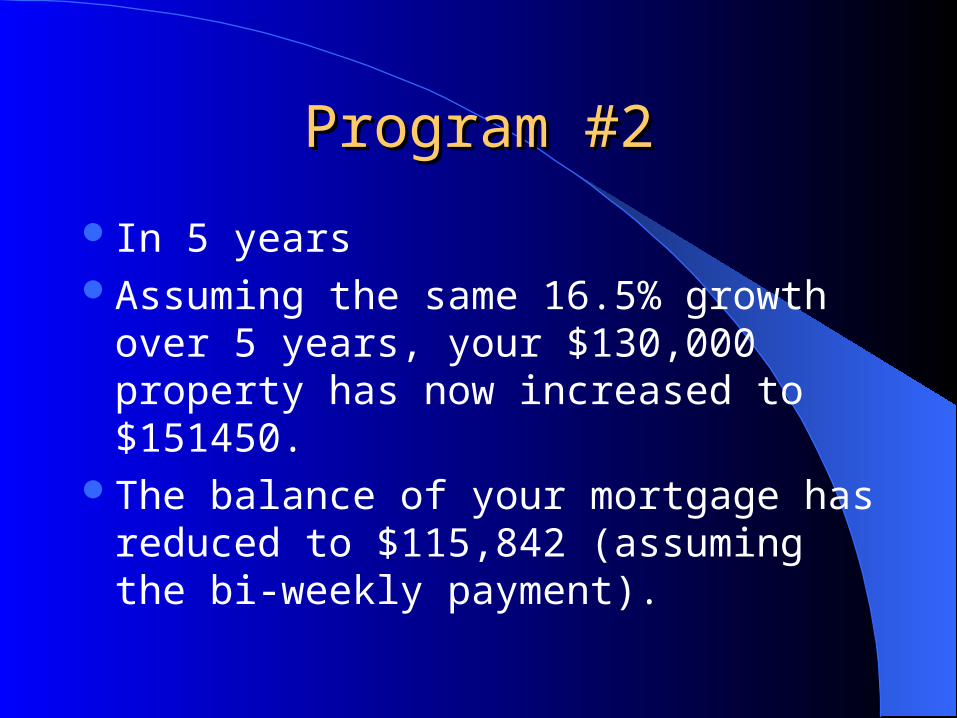

In 5 yearsAssuming the same 16.5% growth over 5

years, your $130,000 property has now increased to $151450.

The balance of your mortgage has reduced to $115,842 (assuming the bi-weekly payment).

Program #2Program #2

$151450 asset$114509

Mortgage

$35,608 Equity

Program #2Program #2

Again you now have $35,608 in equity, you saved the $4420 GE Capital Underwriting fee

More importantly you now own a house and after the 5 Years the lenders will be tripping over themselves offering you a mortgage to payout this mortgage at discounted rates.

Program #2Program #2

So you would be saving an extra $418 per month, and an opportunity to get you out of the rut of renting.

Why pay $72,000 over five years and have nothing to show for it .

Make homeownership a reality.

SummarySummary

I have given you options on how to effectively buy a home with no money down. If you have some money but not quite 5%, then I have additional options that I would like to share with you.

If you would like to speak with me about any of your financing needs please call 905-336-8448, ask for Dave Kendall, or email me at [email protected]

![Document of The World Bank...[ X ] Loan [ ] IDA Grant [ ] Guarantee [ ] Credit [ ] Grant [ ] Other Total Project Cost: 1473.90 Total Bank Financing: 500.00 Financing Gap: 0.00 . Financing](https://img.pdfslide.us/doc/110x75/602e30ca2723d660756cbe12/document-of-the-world-bank-x-loan-ida-grant-guarantee-credit.jpg)