Embed Size (px)

Citation preview

ABVABVc

NYSE

No Boundaries to GrowthNo Boundaries to GrowthJune 2005

2ABVABVc

NYSE

ContentsNo Boundaries to Growth

AmBev Overview

2004, A Crucial Year

Culture, Values and Pillars

Growth Opportunities

1Q 2005, A Good Start

3ABVABVc

NYSE

2004 Highlights

109MM HL of beverages sold

US$1,551 million EBITDA (R$4,537 million)

37.8% EBITDA margin

Operations in 13 countries

Dominant position in Brazil, Argentina, Bolivia, Paraguayand Uruguay

Skol (leader in the Brazilian market) is the world’s thirdlargest selling brand

AmBev is PepsiCo’s largest bottller outside the US

~US$15 billion market cap

AmBev Overview

4ABVABVc

NYSE

TimelineAmBev Overview

Brahma Turnaround

AmBevCreation

Quinsa/AmBev

LatamExpansion

FromPatagoniato Alaska

89 99 02 03 04

5ABVABVc

NYSE

1989~99 – Turnaround of Brahma brewerAmBev Overview

Brahma NYSE listing (1996)Volume CAGR of 5.6%EBITDA CAGR of 30.9%

Cost Reduction, Production Expertise& Marketing Know-How

First steps abroad (1994)

Skol and Brahma brands established as the leaders in BrazilMarket share stable at 50.0%

Beer Brazil generated +95.0% of consolidated EBITDA

EBITDA margin expansion of 1,910bps

DownsizingDistribution network restructuringBrahma #1 & Skol Goes Down Roundlymarketing campaigns

6ABVABVc

NYSE

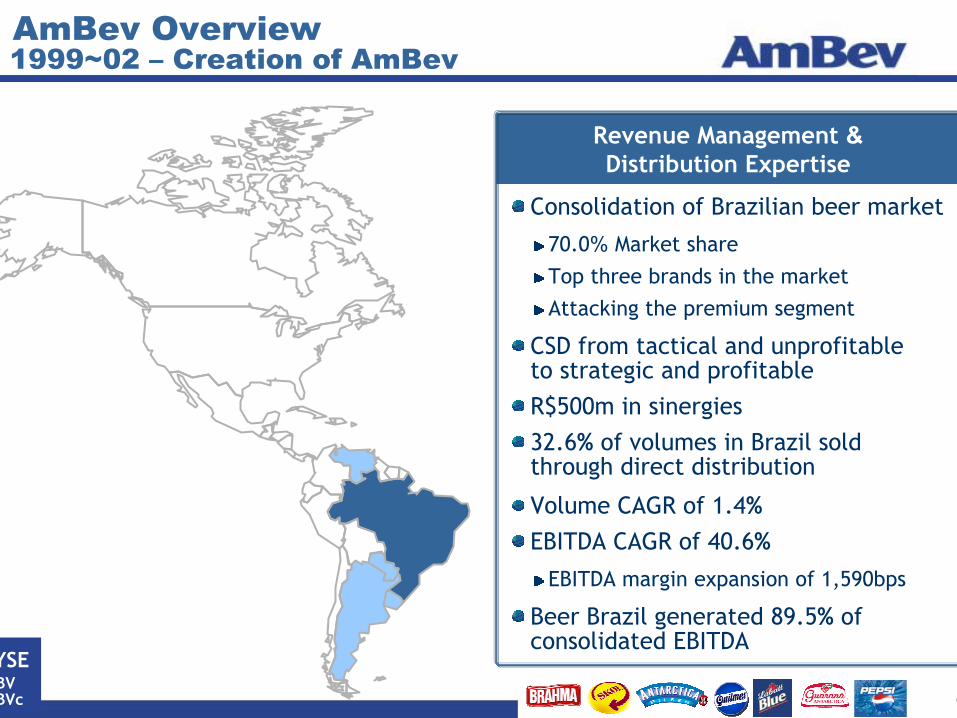

1999~02 – Creation of AmBevAmBev Overview

EBITDA margin expansion of 1,590bps

Revenue Management &Distribution Expertise

Consolidation of Brazilian beer market

70.0% Market shareTop three brands in the marketAttacking the premium segment

Volume CAGR of 1.4%EBITDA CAGR of 40.6%

Beer Brazil generated 89.5% of consolidated EBITDA

CSD from tactical and unprofitableto strategic and profitableR$500m in sinergies32.6% of volumes in Brazil soldthrough direct distribution

7ABVABVc

NYSE

2002~03 – Quinsa-AmBev business combinationAmBev Overview

Beer and CSD together94.4 million HL of beverages soldin 2003Beer Brazil generated 81.4% ofconsolidated EBITDA

Scale & Best Practices

2003 pro forma EBITDA growth of108.0% in the Southern Cone regionMore sinergies and fasterimplementation

Leading brewer in Argentina, Bolívia, Paraguay and Uruguay

Consolidation of the Southern Cone beer market

8ABVABVc

NYSE

2003~04 – Expansion throughout LatamAmBev Overview

Four new operations in theNorth of Latin America

Growth

Significant market share gain

Best practices standardized

EBITDA margin expansion of 1,400 bps to 29.3% in theBrazilian Soft Drinks business

43.7% of volumes in Brazil soldthrough direct distribution

Beer Brazil generated 63.9% ofconsolidated EBITDA

Revenue pool equivalent to~US$3 bn per yearLeverage of Pepsi distribution system

9ABVABVc

NYSE

2004 – The American Beverage CompanyAmBev Overview

Cost reduction through benchmarking

Cross licensing agreements with InBev

Best Practices & Sinergies

Merger of Labatt’s operationsinto AmBev

One of the highest net sales/hl

Growth in a mature market

~30% of pro forma consolidatedEBITDA generated in hard currency

Significant potential for earnings growth

Investment grade rating granted by S&PImproved balance sheet

Beer Brazil generated 63.9% ofconsolidated EBITDA

10ABVABVc

NYSE

2004 Highlights

109MM HL of beverages sold

US$1,551 million EBITDA (R$4,537 million)

37.8% EBITDA margin

Operations in 13 countries

Dominant position in Brazil, Argentina, Bolivia, Paraguayand Uruguay

Skol (leader in the Brazilian market) is the world’s thirdlargest selling brand

AmBev is PepsiCo’s largest bottller outside the US

~US$15 billion market cap

AmBev Overview

11ABVABVc

NYSE

62%

63%

64%

65%

66%

67%

68%

69%

70%

71%

jan/01 jan/02 jan/03 jan/04 jan/05

Dominance reaffirmed in Brazil

Our culture has been the key driver to both maximizing opportunities and quickly

rebounding from trouble

2004, A Crucial Year

Sucess achieved throughdisciplined operations

Market shareback at 68.2%

DiagnosisDiagnosis

LearningsLearnings

ActionsActions

TargetRange

12ABVABVc

NYSE

How we reach our goalsCulture, Values and Pillars

People & Culture

Top Line Growth

Top Line Growth

Excellence in

Distribution

Excellence in

Distribution

Permanent Cost

Reduction

Permanent Cost

ReductionFinancial DisciplineFinancial Discipline

Strategic Pillars

Revenues

(-) COGS

(-) Oper. Exp.

(=) Oper. Profit

PayoutLeverage

Capital Structure

13ABVABVc

NYSE

Talented people, strong culture drive the businessCulture, Values and Pillars

Strong commitment with recruiting, training and developing leaders

“Talents are developed at home”Best peopleBest people

30% to 90% of total compensation linkedto aggressive operating targetsOwnersOwners

220 top executives hold 1.8 billion non voting shares(3,3% of the company)AlignmentAlignment

14ABVABVc

NYSE

“Hands On” Managerial ModelCulture, Values and Pillars

3 Yr Strat Plan+

1 Yr Budget

3 Yr Strat Plan+

1 Yr Budget

Detailed TargetCascading

Detailed TargetCascading

DisciplinedPerformance

Review

DisciplinedPerformance

Review

RESULTS!!

Involvement of the whole senior management

Multi-functional approach

3,000 individual goals + 15,000 collective goals

Monthly performance reviews

Targets are to be achieved, not revised

Corporate targets broken down into detailed operating goals

Commitment built across the whole organization

Action plans required when forecasts indicateunderperformance (“red light”)

In 13 out of 15 years AmBev / Brahma deliveredon stretched targets

15ABVABVc

NYSE

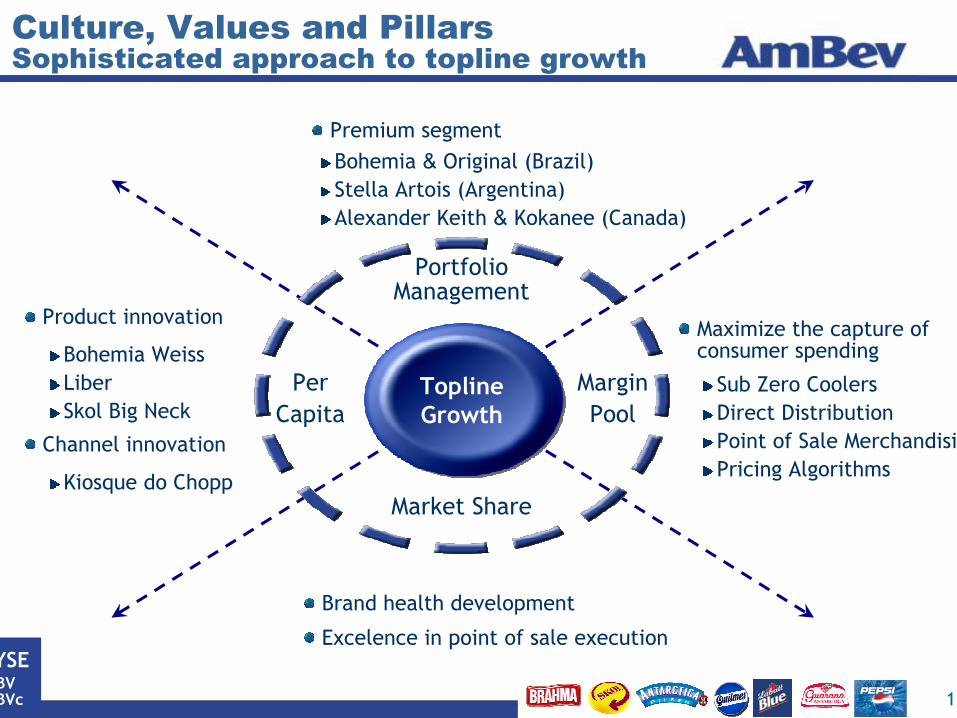

Sophisticated approach to topline growth

Brand health development

Excelence in point of sale execution

Culture, Values and Pillars

Channel innovation

Product innovation

Bohemia WeissLiberSkol Big Neck

Kiosque do Chopp

Sub Zero CoolersDirect DistributionPoint of Sale MerchandisingPricing Algorithms

Maximize the capture of consumer spending

ToplineGrowth

PortfolioManagement

MarginPool

Market Share

PerCapita

Premium segmentBohemia & Original (Brazil)Stella Artois (Argentina)Alexander Keith & Kokanee (Canada)

16ABVABVc

NYSE

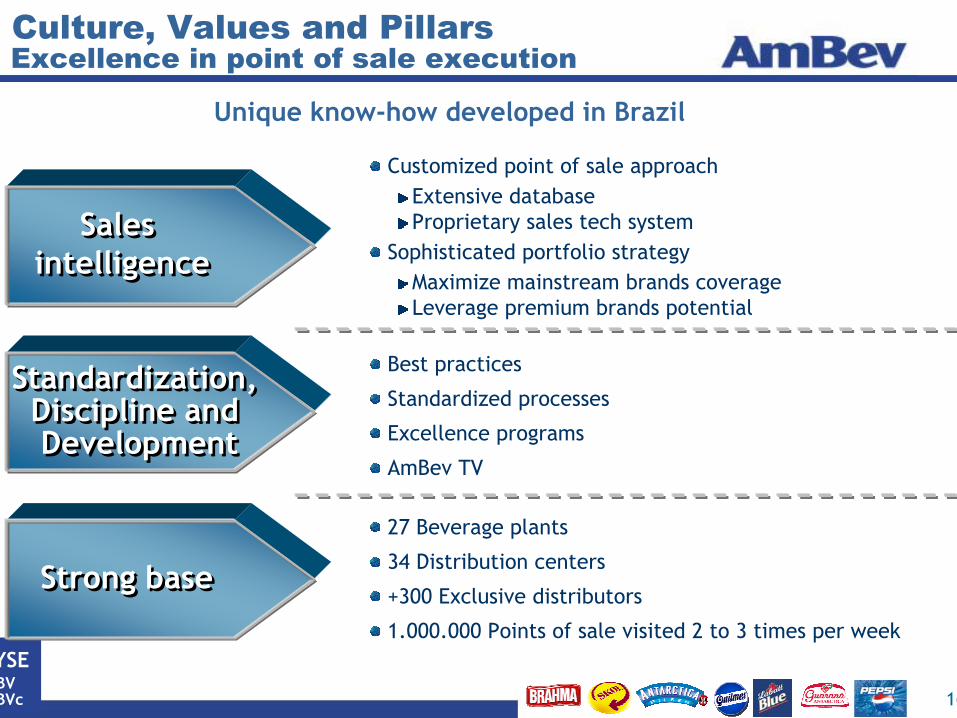

Excellence in point of sale execution

Unique know-how developed in Brazil

Culture, Values and Pillars

Best practices

Standardized processes

Excellence programs

AmBev TV

Standardization, Discipline and Development

Standardization, Discipline and Development

Customized point of sale approach

Sales intelligence

Sales intelligence

Maximize mainstream brands coverageLeverage premium brands potential

Extensive databaseProprietary sales tech system

Sophisticated portfolio strategy

Strong baseStrong base

27 Beverage plants

34 Distribution centers

+300 Exclusive distributors

1.000.000 Points of sale visited 2 to 3 times per week

17ABVABVc

NYSE

Obsessive cost reduction CultureCulture, Values and Pillars

Actual COGS N+1

Management challenge

Hyp. COGS N+1

Commodities

Exchange rate

Inflation

COGS N

“To Be Beaten” approach

Zero tolerance with unnecessaryexpenditures

Detailed mapping of cost andconsumption drivers

Top-down cost reduction targets

ZBB targets eliminatory for bonus payment

Zero Base Budget (ZBB)

18ABVABVc

NYSE

178292 337

502

998

1.327

7 11

247356 313

1.607

1999 2000 2001 2002 2003 2004

Maximizing shareholder returns

Share buyback programs Dividends

R$ Million R$ Million

Culture, Values and Pillars

Payout(% on Net Income)

114%

33%

55%

Stronger Balance Sheet minimizing cash balance requirementBenefiting from Interest on Own Capital (IOC) tax deductibilityResulting in higher dividend yied

1999 2000 2001 2002 2003 2004

19ABVABVc

NYSE

Significant improvement in taxbreak provided by IOC

Well executed tax planning

0%

10%

20%

30%

40%

50%

60%

1Q03 2Q03 3Q03 4Q03 1Q04 2Q04 3Q04 4Q04 1Q05

Effective Income Tax RateEffective Income Tax Rate before GoodwillNominal Rate

Effective Tax Rate beforeGoodwill below 34%

39,0 40,8 35,9 35,7 33,4

71,3

129,6

73,8

37,0

1Q03 2Q03 3Q03 4Q03 1Q04 2Q04 3Q04 4Q04 1Q05

R$ Million

Culture, Values and Pillars

20ABVABVc

NYSE

16,9 16,1 18,9 19,426,1

39,0

50,9

70,9

81,0 83,128,6%

24,7% 23,8%21,1%

27,8% 28,7%30,5%

37,0%35,4%

37,8%

0,0

20,0

40,0

60,0

80,0

100,0

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

0,0%

5,0%

10,0%

15,0%

20,0%

25,0%

30,0%

35,0%

40,0%

EBITDA per share EBITDA margin

Consistent track record

R$

CAGR: 19,4%

Culture, Values and Pillars

21ABVABVc

NYSE

Best positioned for long term growth

Young and seasoned management team

Growth Opportunities

Leader in Brazil and in the Southern Cone

Solid growth platform in the North of Latin America

Revenue pool larger than US$3 bn per year

Significant potential to earnings growth in Canada

Stronger and smarter after 2003 hit

Good macroeconomic perspectives – GDP, income and employment

Price and Share

US$60m in annual cost reduction identified

Still more of the same (ZBB, Direct Distribution, Margin Pool)

22ABVABVc

NYSE

1Q05 EBITDA Breakdown2005, A Good Start

399

78

67

544

Brazil North America* HILA Total*US$ Million

25.2% 39.3%32.5%45.9%EBITDAmarginEBITDAmargin

41.6% 49.6%24.7%56.6%GrowthGrowth

* Pro forma basis

23ABVABVc

NYSE

No Boundaries to Growth

ABVABVcABVABVc

NYSENYSEAMBV4AMBV3AMBV4AMBV3

BovespaBovespa