Embed Size (px)

Citation preview

Ninth AnnualDomestic Tax Conference8 May 2014 | Chicago

Best practices inworldwide compliance

Case studies and lessons learned

Page 3

IRS Circular 230 disclosure

Any US tax advice contained herein was not intended orwritten to be used, and cannot be used, for the purpose ofavoiding penalties that may be imposed under the InternalRevenue Code or applicable state or local tax lawprovisions.

These slides are for educational purposes onlyand are not intended, and should not be relied upon, asaccounting advice.

Page 4

► EY refers to the global organization, and may refer to one or more,of the member firms of Ernst & Young Global Limited, each of whichis a separate legal entity. Ernst & Young LLP is a client-serving memberfirm of Ernst & Young Global Limited located in the US.

► This presentation is © 2014 Ernst & Young LLP. All rights reserved.No part of this document may be reproduced, transmitted or otherwisedistributed in any form or by any means, electronic or mechanical,including by photocopying, facsimile transmission, recording, rekeying,or using any information storage and retrieval system, without writtenpermission from Ernst & Young LLP. Any reproduction, transmission ordistribution of this form or any of the material herein is prohibited and isin violation of US and international law. Ernst & Young LLP expresslydisclaims any liability in connection with use of this presentation or itscontents by any third party.

► Views expressed in this presentation are not necessarily those ofErnst & Young LLP.

Disclaimer

Page 5

Today’s presenters

Elizabeth Summers, NIKEMatthew Duncan, Ernst & Young LLP

Tom Knoeller, Ernst & Young LLPCheryl Belles, Ernst & Young LLP – Moderator

Page 6

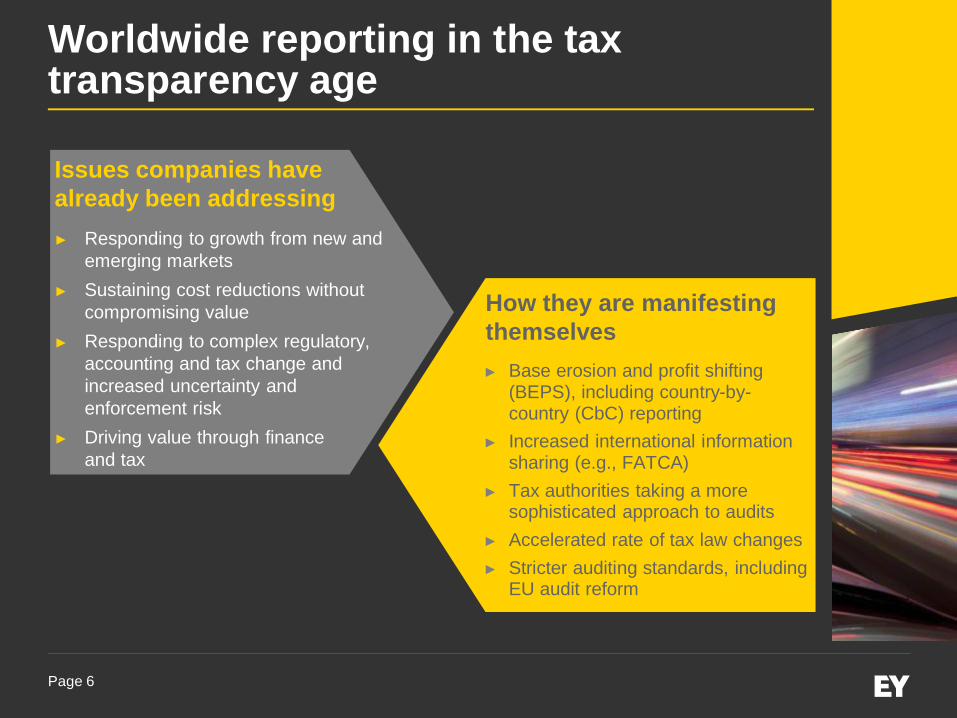

Worldwide reporting in the taxtransparency age

How they are manifestingthemselves► Base erosion and profit shifting

(BEPS), including country-by-country (CbC) reporting

► Increased international informationsharing (e.g., FATCA)

► Tax authorities taking a moresophisticated approach to audits

► Accelerated rate of tax law changes► Stricter auditing standards, including

EU audit reform

Issues companies havealready been addressing► Responding to growth from new and

emerging markets► Sustaining cost reductions without

compromising value► Responding to complex regulatory,

accounting and tax change andincreased uncertainty andenforcement risk

► Driving value through financeand tax

Page 7

Timeline of CbC reporting conceptdevelopment

► June 2013 — G8 leaders call on OECD to develop a template for CbCreporting to tax authorities

► July 2013 — OECD BEPS Action Plan — Action 13 transfer pricingdocumentation, including CbC template

► July 2013 — OECD White Paper on Transfer Pricing Documentation► October 2013 — OECD Memorandum on Transfer Pricing Documentation

and Country by Country Reporting► January 2014 — OECD Discussion Draft on Transfer Pricing Documentation

and CbC Reporting — proposed template released► February 2014 — More than 1,200 pages of comments submitted to OECD► March and May 2014 — Consultations on Discussion Draft► May 2014 — OECD Working Party expected to finish work on the template► June–July 2014 — OECD expected to approve template for release► By September 2014 — OECD expected to release recommended

CbC reporting template

Page 8

Proposed CbC reporting templateProposed CbC reporting templateC

ount

ry

Con

stitu

ente

ntiti

esor

gani

zed

inth

eco

untr

y

Plac

eof

effe

ctiv

em

anag

emen

t

Impo

rtan

tbus

ines

sac

tivity

code

(s)

Rev

enue

s

Earn

ings

befo

rein

com

eta

x

Income tax paid(on cash basis)

Tota

lwith

hold

ing

tax

paid

Stat

edca

pita

land

accu

mul

ated

earn

ings

Num

ber

ofem

ploy

ees

Tota

lem

ploy

eeex

pens

e

Tang

ible

asse

tsot

her

than

cash

and

cash

equi

vale

nts

Roy

altie

spa

idto

cons

titue

nten

titie

s

Roy

altie

sre

ceiv

edfr

omco

nstit

uent

entit

ies

Inte

rest

paid

toco

nstit

uent

entit

ies

Inte

rest

rece

ived

from

cons

titue

nten

titie

s

Serv

ice

fees

paid

toco

nstit

uent

entit

ies

Serv

ice

fees

rece

ived

from

cons

titue

nten

titie

s

(a) Tocountry oforganization

(b) Toall othercountries

1.

2.

3.

4.

Total:

1.

2.

3.

4.

Total:

1.

2.

3.

4.

Total:

Page 9

Tax controversy risk

92% of the largest companies think that global disclosure and transparencyrequirements will continue to grow in the next two years.

69% of the largest companies report that they feel tax audits have become moreaggressive in the last two years.

68% of the largest companies report that they feel tax authorities globally haveincreased their focus on cross-border transactions in the last two years.

Leading enterprise sources of tax risk in order of prevalence:► Insufficient resources to cover tax function activities: 75%► Insufficient internal communication: 64%► A lack of processes or technology: 57%

* EY 2014 Global Controversy Survey covering 830 tax and finance executives in 25 markets

Page 10

How are jurisdictions altering their corporateincome tax base in 2014?

*Based upon an EY survey of 61 jurisdictions

Page 11

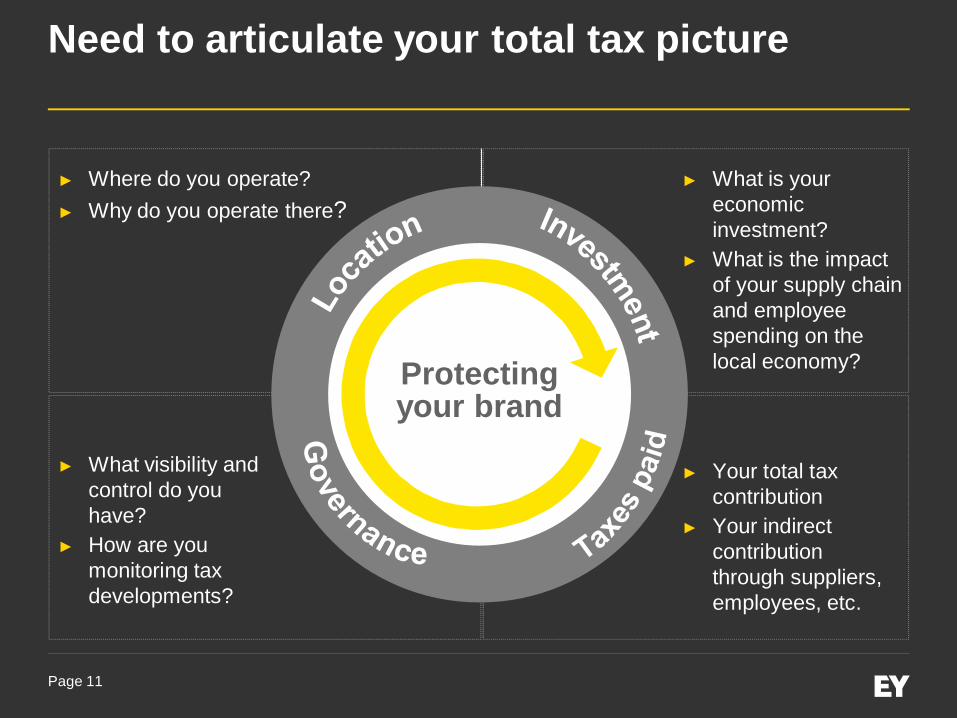

Need to articulate your total tax picture

► What is youreconomicinvestment?

► What is the impactof your supply chainand employeespending on thelocal economy?

► Where do you operate?► Why do you operate there?

► Your total taxcontribution

► Your indirectcontributionthrough suppliers,employees, etc.

► What visibility andcontrol do youhave?

► How are youmonitoring taxdevelopments?

Protectingyour brand

Page 12

Defining global compliance and reporting(GCR)

GCR comprises the key elements of a company’s finance and taxprocesses that prepare statutory financial and tax filings as required incountries around the world.

Record-to-report and GCR

Record andprocess

transactions

Legal entityfinancial

accounting

Taxaccounting

andprovisions

Statutoryreportingand legal

entitycompliance

Corporateincome taxcompliance

Transferpricing

Tax planningand

controversymanagement

Governance and control

Indirect taxcompliance

Page 13

Case study: NIKE

Page 14

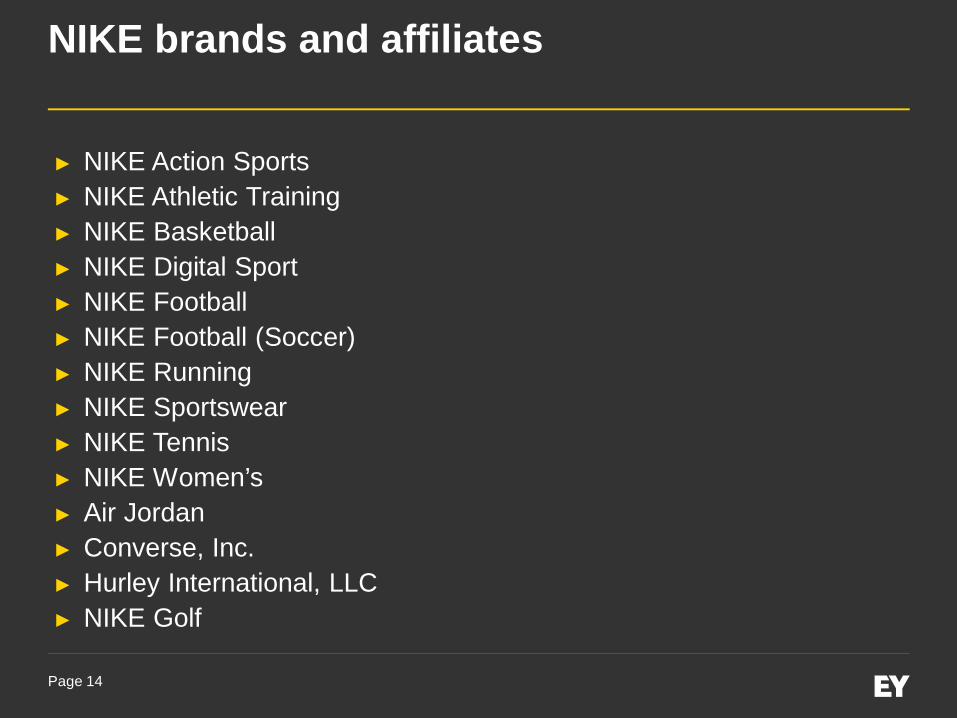

NIKE brands and affiliates

► NIKE Action Sports► NIKE Athletic Training► NIKE Basketball► NIKE Digital Sport► NIKE Football► NIKE Football (Soccer)► NIKE Running► NIKE Sportswear► NIKE Tennis► NIKE Women’s► Air Jordan► Converse, Inc.► Hurley International, LLC► NIKE Golf

Page 15

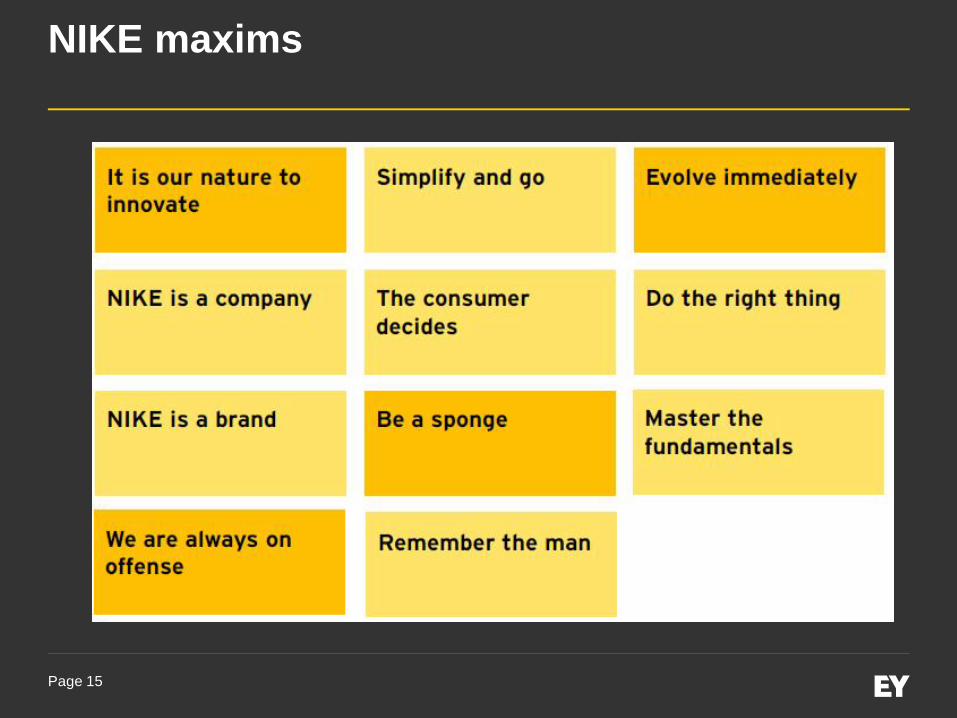

NIKE maxims

Page 16

GCR objectives

► Achieve full visibility to the status of tax filings, includingproactive identification and resolution of potential issuesor risky tax positions

► Improved timeliness of filings► Centralized access to tax filings, entity information and

engagement information► Improved connection to local developments –

controversy, regulatory developments and localbusiness changes

► Visibility and control over scope and fees► Improved discussions on tax planning opportunities

Page 17

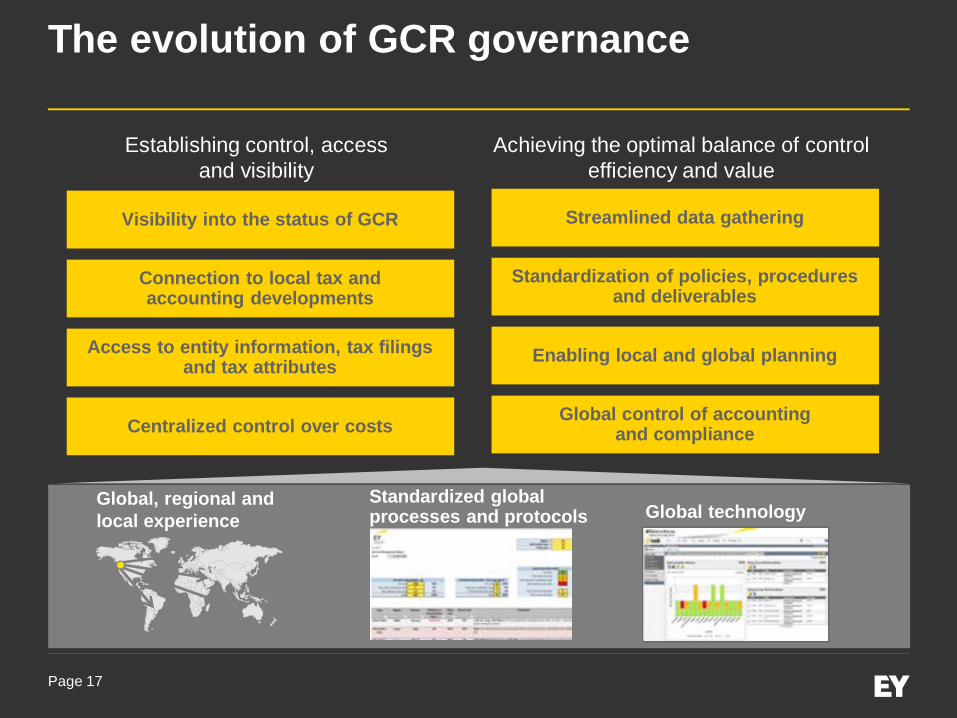

The evolution of GCR governance

Global technologyGlobal, regional andlocal experience

Standardized globalprocesses and protocols

Visibility into the status of GCR

Connection to local tax andaccounting developments

Access to entity information, tax filingsand tax attributes

Centralized control over costs

Establishing control, accessand visibility

Streamlined data gathering

Standardization of policies, proceduresand deliverables

Enabling local and global planning

Global control of accountingand compliance

Achieving the optimal balance of controlefficiency and value

Page 18

A path to move forward

Practical considerations to developing an approach to achieve a GCRprocess within your organization

Who Stakeholders

What Extent of processes (e.g., accounting, compliance, controversy)Budget considerations

When Timing considerations aligned with organizational initiativesWhere Implementation across portions or the entire organization

Page 19

Next steps

JUST DO IT.

Page 20

Questions and answers

Page 21

Thankyou!

Ninth AnnualDomestic Tax Conference8 May 2014 | Chicago