Embed Size (px)

Citation preview

Nicholson Financial Services,Inc.David S. NicholsonFinancial Advisor89 Access RoadSte. CNorwood, MA 02062781-255-1101866-668-1101david@nicholsonfs.comwww.nicholsonfs.com

Winter/Spring 2013Bubbles

Four Retirement Planning Mistakes to Avoid

Compounding Can Add Fuel to Your Portfolio

I refinanced my mortgage loan last year. CanI deduct any of the costs associated withrefinancing the loan?

Nicholson Financial ServicesDid You Know...?Bubbles

See disclaimer on final page

Although 2012 ended with a bit of a"fizzle" due to the fear of the impending"fiscal cliff," the markets had a good yearcoming back from a soft 2011. The S&P500 finished 2012 up 16% while theDJIA posted a +10.24% and the Russell2000 a +16.4%. The internationalindexes fared better as well. Ironically,the concerns over the "fiscal cliff" lastedonly one day into the new year. Ourelected officials found a way to dosomething they haven't done much inrecent history - compromise. The firsttwo months of 2013 have shown strongpositive moves in the equity markets aswell. Going forward, I believe that we willsee more political compromise. If so, thegradual economic recovery, low interestrate environment, and favorablevaluations may lead to another strongyear for stocks.

Nicholson Financial Services, Inc. is anindependent firm.

The word "bubbles" still makes me laugh. If youhave seen Finding Nemo then you know what Iam talking about. Anyone who has had childrenin the past 10 years has probably seen thatmovie many, many times as I have. Those arenot the type of bubbles we are going to talkabout here though. Our focus is on economicbubbles. Over the past 15 years, our economyhas seen the impact of two major economicbubbles bursting, and I believe we are nowwitnessing the potential for another.

In the late 1990's, stocks had a historic run ofincredibly strong returns, in spite of valuations.By 2000, equities were very overpriced. Therewas a lot of conjecture at the time by analysts,economists and investors that the paradigmhad shifted. Many thought stocks would toleratehigher valuations going forward and that thingswere "different this time." They weren't. The"equity valuation bubble" burst from 2000 to2002 as a multi-year bear market returnedstocks to more modest valuation levels. Duringthat time, the Federal Reserve (the Fed)lowered interest rates significantly to spureconomic growth. This, combined with relaxingpolicies in the mortgage industry and otherfactors, contributed to the next bubble -housing.

The popping housing bubble was one ofseveral main factors that lead to the globalfinancial crisis in 2008. That crisis was reallymore of a "credit crisis" than anything else. Inthe fall of 2008, the credit markets froze almostcompletely, leading to a domino effect on otherasset classes. In particular, stocks were hit veryhard as many institutions sold their holdings toraise cash. I have discussed those events inthese missives numerous times over the pastfew years, particularly in 2009 & 2010. In orderto keep our economy out of a depression,encourage business investing and spur on aneconomic recovery, the Federal Reserve cutinterest rates to all-time lows. Rates literallycan't go any lower. This environment is, in myopinion, as much of an anomaly as the early1980's when rates were higher than 15%. Thatsaid, I believe this low rate environment hascaused a rapidly expanding bubble in bonds.

Bond prices have an inverse relationship tointerest rates. This means that when the Fedlowers rates, bond prices typically go up andvisa versa. Considering that rates are thelowest they have been in history, it would followthat overall bond prices are the highest inhistory as well. As a result of the 2008 crisis,the S&P 500 averaged roughly -1% per yearfrom 2000 to 2009. Over the same time frame,long-term US Treasury bonds averaged betterthan 7.5% per year. Considering that manyinvestors primarily use past performance tomake their investments decisions (something Iadvise against) and the "flight to safety" after2008, it is not surprising that billions havepoured into bond funds in the past 4 years.

Since March 2009, stocks have generallyoutperformed bonds by a wide margin. Yet,after the stock market low that month, moremoney has gone into bond funds than stockfunds in every month that followed, save for 3.THREE! Bonds can go no higher from interestrate cuts and now face downside pressure aswe get closer to the inevitable interest rate hikefrom the Fed. The question is not "if" the ratehike will occur, but when. The Fed says theywill likely start raising rates in 2015, but it couldcertainly be sooner if economic growth, andinflation, start to heat up. A rising interest rateenvironment coupled with bondsunderperforming other asset classes like stocksand potentially real estate could lead to a massexodus from long-term bonds. To put it anotherway, the bond bubble would pop.

It is my opinion that 1) short-term bonds stilloffer "safety" but at the sacrifice of return and 2)long-term bonds have built in more interest raterisk than at any point in recorded history. It isunlikely that this bubble bursting will have thekind of negative impact on our economy thatthe last two bubbles did. Many institutions andsavvy investors already know about it and willlikely take precautions. My concern is for theaverage investor who doesn't see it coming.This is especially true for retirees who investedin long-term bonds seeking higher yields. Theyneed to be aware of the possible risks in theirportfolios.

Page 1 of 4

Four Retirement Planning Mistakes to AvoidWe all recognize the importance of planningand saving for retirement, but too many of usfall victim to one or more common mistakes.Here are four easily avoidable mistakes thatcould prevent you from reaching yourretirement goals.

1. Putting off planning and savingBecause retirement may be many years away,it's easy to put off planning for it. The longeryou wait, however, the harder it is to make upthe difference later. That's because the sooneryou start saving, the more time yourinvestments have to grow.

The chart below shows how much you couldsave by age 65 if you contribute $3,000annually, starting at ages 20 ($679,500), 35($254,400), and 45 ($120,000). As you cansee, a few years can make a big difference inhow much you'll accumulate.

Note: Assumes 6% annual growth, no tax, andreinvestment of all earnings. This is ahypothetical example and is not intended toreflect the actual performance of anyinvestment.

Don't make the mistake of promising yourselfthat you'll start saving for retirement as soon asyou've bought a house or that new car, or afteryou've fully financed your child's education--it'simportant that you start saving as much as youcan, as soon as you can.

2. Underestimating how muchretirement income you'll needOne of the biggest retirement planningmistakes you can make is to underestimate theamount you'll need to accumulate by the timeyou retire. It's often repeated that you'll need70% to 80% of your preretirement income afteryou retire. However, depending on your lifestyleand individual circumstances, it's notinconceivable that you may need to replace100% or more of your preretirement income.

With the future of Social Security uncertain, andfewer and fewer people covered by traditionalpension plans these days, your individualsavings are more important than ever. Keep inmind that because people are living longer,

healthier lives, your retirement dollars mayneed to last a long time. The average65-year-old American can currently expect tolive another 19.2 years (Source: National VitalStatistics Report, Volume 60, Number 4,January 2012). However, that's theaverage--many can expect to live longer, somemuch longer, lives.

In order to estimate how much you'll need toaccumulate, you'll need to estimate theexpenses you're likely to incur in retirement. Doyou intend to travel? Will your mortgage be paidoff? Might you have significant health-careexpenses not covered by insurance orMedicare? Try thinking about your currentexpenses, and how they might change betweennow and the time you retire.

3. Ignoring tax-favored retirement plansProbably the best way to accumulate funds forretirement is to take advantage of IRAs andemployer retirement plans like 401(k)s, 403(b)s,and 457(b)s. The reason these plans are soimportant is that they combine the power ofcompounding with the benefit of tax deferred(and in some cases, tax free) growth. For mostpeople, it makes sense to maximizecontributions to these plans, whether it's on apre-tax or after-tax (Roth) basis.

If your employer's plan has matchingcontributions, make sure you contribute at leastenough to get the full company match. It'sessentially free money. (Some plans mayrequire that you work a certain number of yearsbefore you're vested in (i.e., before you own)employer matching contributions. Check withyour plan administrator.)

4. Investing too conservativelyWhen you retire, you'll have to rely on youraccumulated assets for income. To ensure aconsistent and reliable flow of income for therest of your lifetime, you must provide somesafety for your principal. It's common forindividuals approaching retirement to shift aportion of their investment portfolio to moresecure income-producing investments, likebonds.

Unfortunately, safety comes at the price ofreduced growth potential and the risk of erosionof value due to inflation. Safety at the expenseof growth can be a critical mistake for thosetrying to build an adequate retirement nest egg.On the other hand, if you invest too heavily ingrowth investments, your risk is heightened. Afinancial professional can help you strike areasonable balance between safety andgrowth.

Because retirement may bemany years away, it's easyto put off planning for it.The longer you wait,however, the harder it is tomake up the difference later.That's because the sooneryou start saving, the moretime your investments haveto grow.

Page 2 of 4, see disclaimer on final page

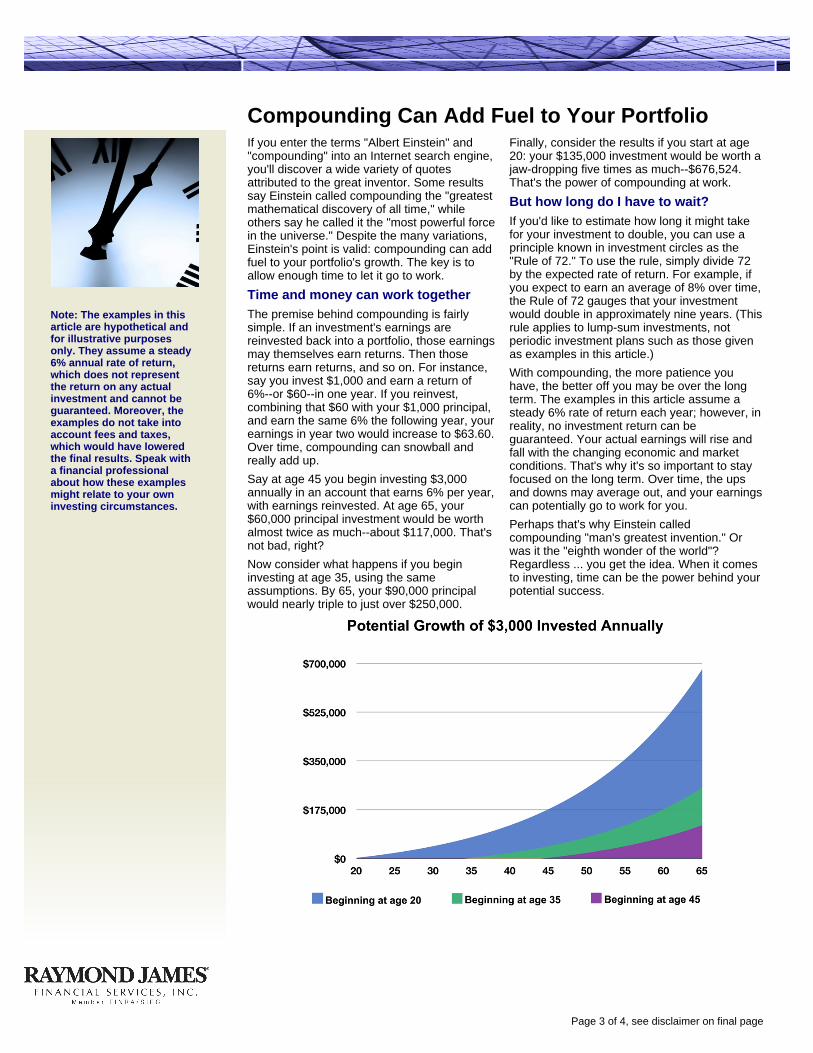

Compounding Can Add Fuel to Your PortfolioIf you enter the terms "Albert Einstein" and"compounding" into an Internet search engine,you'll discover a wide variety of quotesattributed to the great inventor. Some resultssay Einstein called compounding the "greatestmathematical discovery of all time," whileothers say he called it the "most powerful forcein the universe." Despite the many variations,Einstein's point is valid: compounding can addfuel to your portfolio's growth. The key is toallow enough time to let it go to work.

Time and money can work togetherThe premise behind compounding is fairlysimple. If an investment's earnings arereinvested back into a portfolio, those earningsmay themselves earn returns. Then thosereturns earn returns, and so on. For instance,say you invest $1,000 and earn a return of6%--or $60--in one year. If you reinvest,combining that $60 with your $1,000 principal,and earn the same 6% the following year, yourearnings in year two would increase to $63.60.Over time, compounding can snowball andreally add up.

Say at age 45 you begin investing $3,000annually in an account that earns 6% per year,with earnings reinvested. At age 65, your$60,000 principal investment would be worthalmost twice as much--about $117,000. That'snot bad, right?

Now consider what happens if you begininvesting at age 35, using the sameassumptions. By 65, your $90,000 principalwould nearly triple to just over $250,000.

Finally, consider the results if you start at age20: your $135,000 investment would be worth ajaw-dropping five times as much--$676,524.That's the power of compounding at work.

But how long do I have to wait?If you'd like to estimate how long it might takefor your investment to double, you can use aprinciple known in investment circles as the"Rule of 72." To use the rule, simply divide 72by the expected rate of return. For example, ifyou expect to earn an average of 8% over time,the Rule of 72 gauges that your investmentwould double in approximately nine years. (Thisrule applies to lump-sum investments, notperiodic investment plans such as those givenas examples in this article.)

With compounding, the more patience youhave, the better off you may be over the longterm. The examples in this article assume asteady 6% rate of return each year; however, inreality, no investment return can beguaranteed. Your actual earnings will rise andfall with the changing economic and marketconditions. That's why it's so important to stayfocused on the long term. Over time, the upsand downs may average out, and your earningscan potentially go to work for you.

Perhaps that's why Einstein calledcompounding "man's greatest invention." Orwas it the "eighth wonder of the world"?Regardless ... you get the idea. When it comesto investing, time can be the power behind yourpotential success.

Note: The examples in thisarticle are hypothetical andfor illustrative purposesonly. They assume a steady6% annual rate of return,which does not representthe return on any actualinvestment and cannot beguaranteed. Moreover, theexamples do not take intoaccount fees and taxes,which would have loweredthe final results. Speak witha financial professionalabout how these examplesmight relate to your owninvesting circumstances.

Page 3 of 4, see disclaimer on final page

Nicholson FinancialServices, Inc.David S. NicholsonFinancial Advisor89 Access RoadSte. CNorwood, MA 02062781-255-1101866-668-1101david@nicholsonfs.comwww.nicholsonfs.com

Prepared by Broadridge Investor Communication Solutions, Inc. Copyright 2013

This information, developed by anindependent third party, has been obtainedfrom sources considered to be reliable, butRaymond James Financial Services, Inc.does not guarantee that the foregoingmaterial is accurate or complete. Thisinformation is not a complete summary orstatement of all available data necessary formaking an investment decision and does notconstitute a recommendation. Theinformation contained in this report does notpurport to be a complete description of thesecurities, markets, or developments referredto in this material. This information is notintended as a solicitation or an offer to buy orsell any security referred to herein.Investments mentioned may not be suitablefor all investors. The material is general innature. Past performance may not beindicative of future results. Raymond JamesFinancial Services, Inc. does not provideadvice on tax, legal or mortgage issues.These matters should be discussed with theappropriate professional.

Securities offered through Raymond JamesFinancial Services, Inc., memberFINRA/SIPC, an independent broker/dealer,and are not insured by FDIC, NCUA or anyother government agency, are not deposits orobligations of the financial institution, are notguaranteed by the financial institution, andare subject to risks, including the possibleloss of principal.

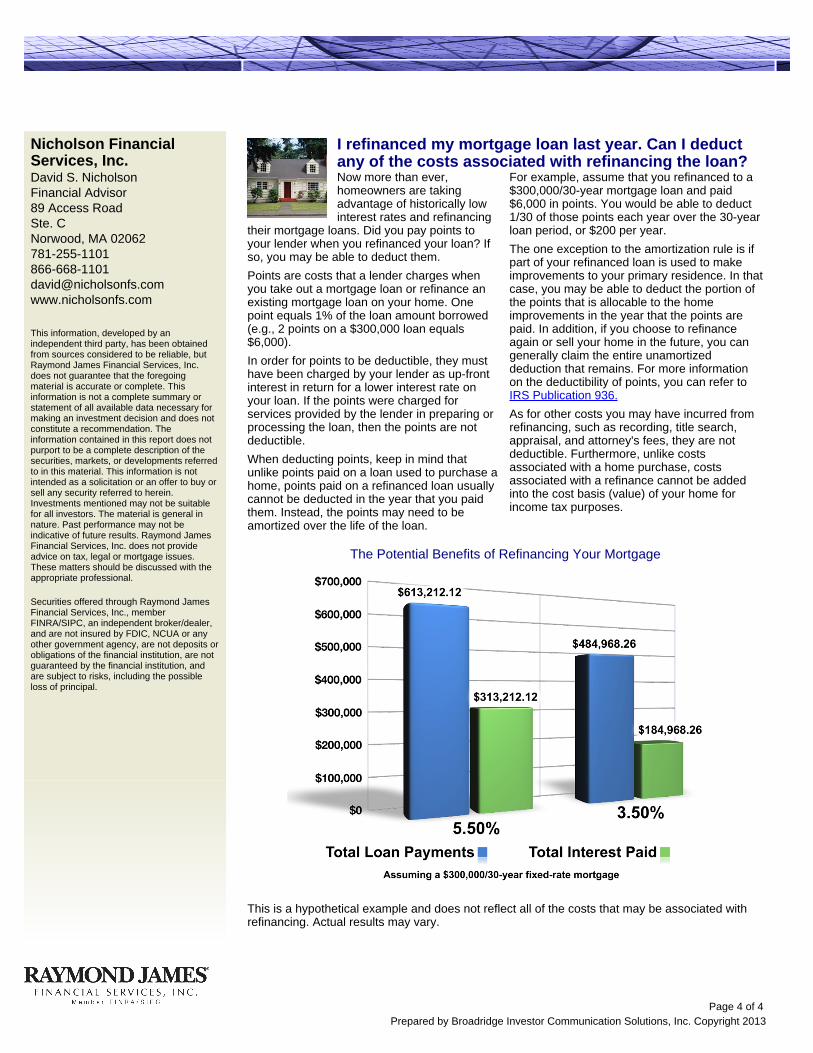

The Potential Benefits of Refinancing Your Mortgage

This is a hypothetical example and does not reflect all of the costs that may be associated withrefinancing. Actual results may vary.

I refinanced my mortgage loan last year. Can I deductany of the costs associated with refinancing the loan?Now more than ever,homeowners are takingadvantage of historically lowinterest rates and refinancing

their mortgage loans. Did you pay points toyour lender when you refinanced your loan? Ifso, you may be able to deduct them.

Points are costs that a lender charges whenyou take out a mortgage loan or refinance anexisting mortgage loan on your home. Onepoint equals 1% of the loan amount borrowed(e.g., 2 points on a $300,000 loan equals$6,000).

In order for points to be deductible, they musthave been charged by your lender as up-frontinterest in return for a lower interest rate onyour loan. If the points were charged forservices provided by the lender in preparing orprocessing the loan, then the points are notdeductible.

When deducting points, keep in mind thatunlike points paid on a loan used to purchase ahome, points paid on a refinanced loan usuallycannot be deducted in the year that you paidthem. Instead, the points may need to beamortized over the life of the loan.

For example, assume that you refinanced to a$300,000/30-year mortgage loan and paid$6,000 in points. You would be able to deduct1/30 of those points each year over the 30-yearloan period, or $200 per year.

The one exception to the amortization rule is ifpart of your refinanced loan is used to makeimprovements to your primary residence. In thatcase, you may be able to deduct the portion ofthe points that is allocable to the homeimprovements in the year that the points arepaid. In addition, if you choose to refinanceagain or sell your home in the future, you cangenerally claim the entire unamortizeddeduction that remains. For more informationon the deductibility of points, you can refer toIRS Publication 936.

As for other costs you may have incurred fromrefinancing, such as recording, title search,appraisal, and attorney's fees, they are notdeductible. Furthermore, unlike costsassociated with a home purchase, costsassociated with a refinance cannot be addedinto the cost basis (value) of your home forincome tax purposes.

Page 4 of 4