Embed Size (px)

Citation preview

2000796-424

NGA coverage: what is affordable?

Analysys Mason event – The Next Generation of European Regulation

21 October 2014 • Rupert Wood

2000796-424

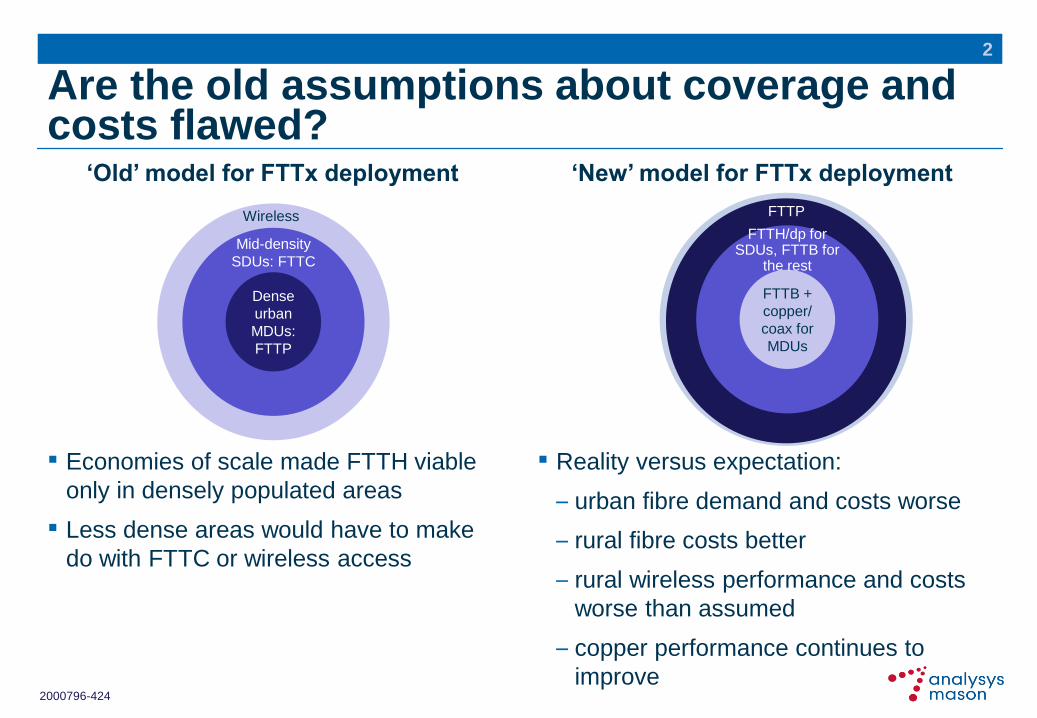

Are the old assumptions about coverage and costs flawed?

▪ Economies of scale made FTTH viable

only in densely populated areas

▪ Less dense areas would have to make

do with FTTC or wireless access

2

▪ Reality versus expectation:

– urban fibre demand and costs worse

– rural fibre costs better

– rural wireless performance and costs

worse than assumed

– copper performance continues to

improve

‘Old’ model for FTTx deployment ‘New’ model for FTTx deployment

Dense

urban

MDUs:

FTTP

Mid-density

SDUs: FTTC

Wireless

FTTB +

copper/

coax for

MDUs

FTTH/dp for SDUs, FTTB for

the rest

FTTP

2000796-424

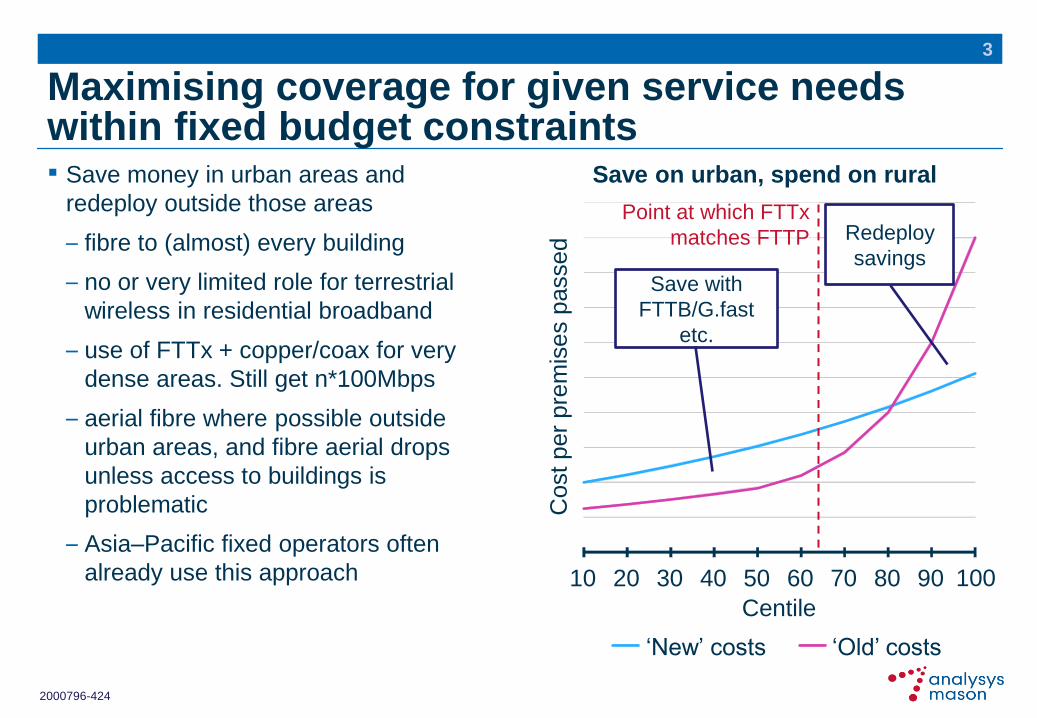

Maximising coverage for given service needs within fixed budget constraints ▪ Save money in urban areas and

redeploy outside those areas

– fibre to (almost) every building

– no or very limited role for terrestrial

wireless in residential broadband

– use of FTTx + copper/coax for very

dense areas. Still get n*100Mbps

– aerial fibre where possible outside

urban areas, and fibre aerial drops

unless access to buildings is

problematic

– Asia–Pacific fixed operators often

already use this approach

3

Save on urban, spend on rural

10 20 30 40 50 60 70 80 90 100 C

ost

per

pre

mis

es p

assed

Centile

‘New’ costs ‘Old’ costs

Save with

FTTB/G.fast

etc.

Redeploy

savings

Point at which FTTx

matches FTTP

2000796-424

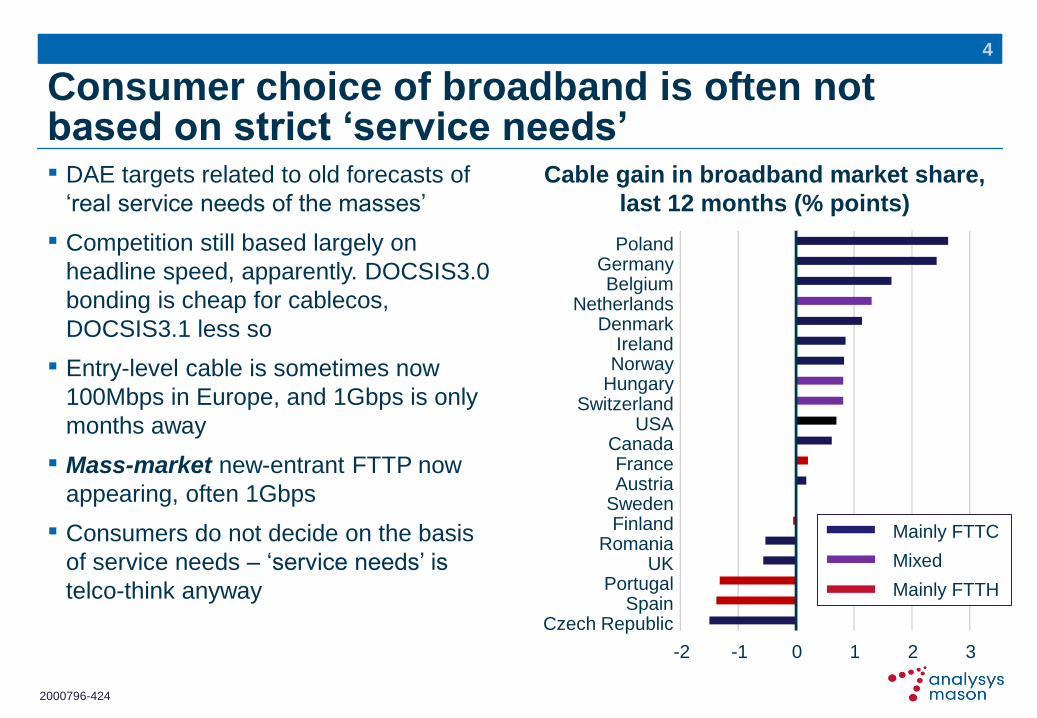

Consumer choice of broadband is often not based on strict ‘service needs’ ▪ DAE targets related to old forecasts of

‘real service needs of the masses’

▪ Competition still based largely on

headline speed, apparently. DOCSIS3.0

bonding is cheap for cablecos,

DOCSIS3.1 less so

▪ Entry-level cable is sometimes now

100Mbps in Europe, and 1Gbps is only

months away

▪ Mass-market new-entrant FTTP now

appearing, often 1Gbps

▪ Consumers do not decide on the basis

of service needs – ‘service needs’ is

telco-think anyway

4

Cable gain in broadband market share,

last 12 months (% points)

-2 -1 0 1 2 3

Czech Republic Spain

Portugal UK

Romania Finland

Sweden Austria France

Canada USA

Switzerland Hungary Norway Ireland

Denmark Netherlands

Belgium Germany

Poland

Mainly FTTC

Mixed

Mainly FTTH

2000796-424

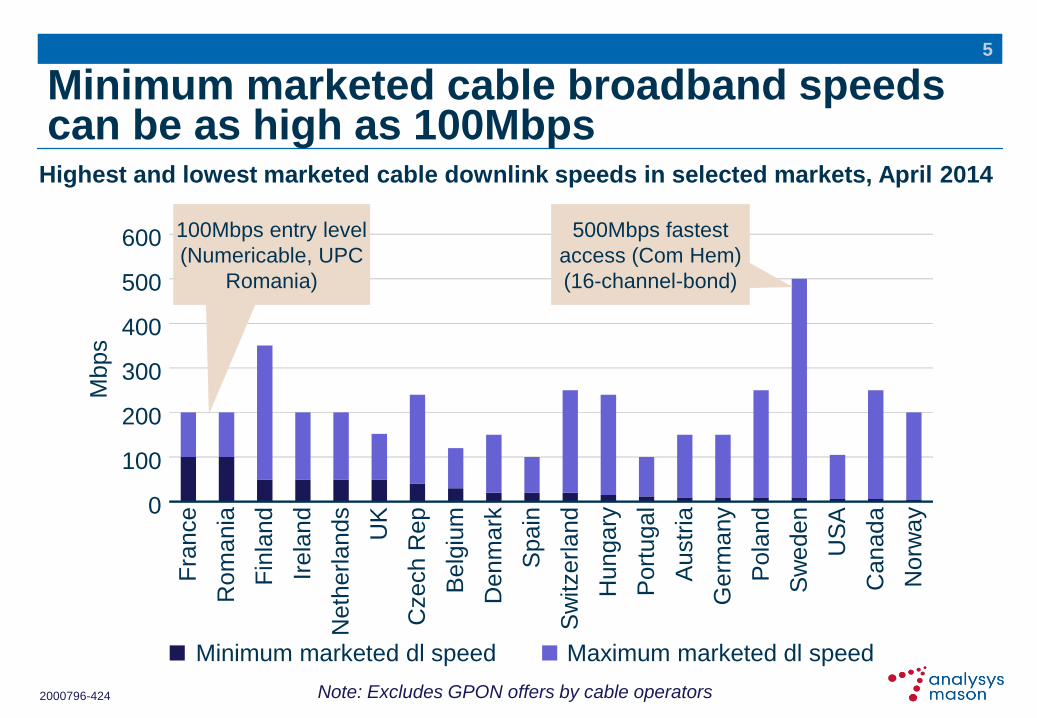

Minimum marketed cable broadband speeds can be as high as 100Mbps

5

Highest and lowest marketed cable downlink speeds in selected markets, April 2014

Note: Excludes GPON offers by cable operators

Fra

nce

Rom

ania

Fin

land

Irela

nd

Neth

erlands

UK

Czech R

ep

Belg

ium

Denm

ark

Spain

Sw

itze

rland

Hungary

Port

ugal

Austr

ia

Germ

any

Pola

nd

Sw

eden

US

A

Canada

Norw

ay

Minimum marketed dl speed Maximum marketed dl speed

0

100

200

300

400

500

600

Mbps

500Mbps fastest

access (Com Hem)

(16-channel-bond)

100Mbps entry level

(Numericable, UPC

Romania)

2000796-424

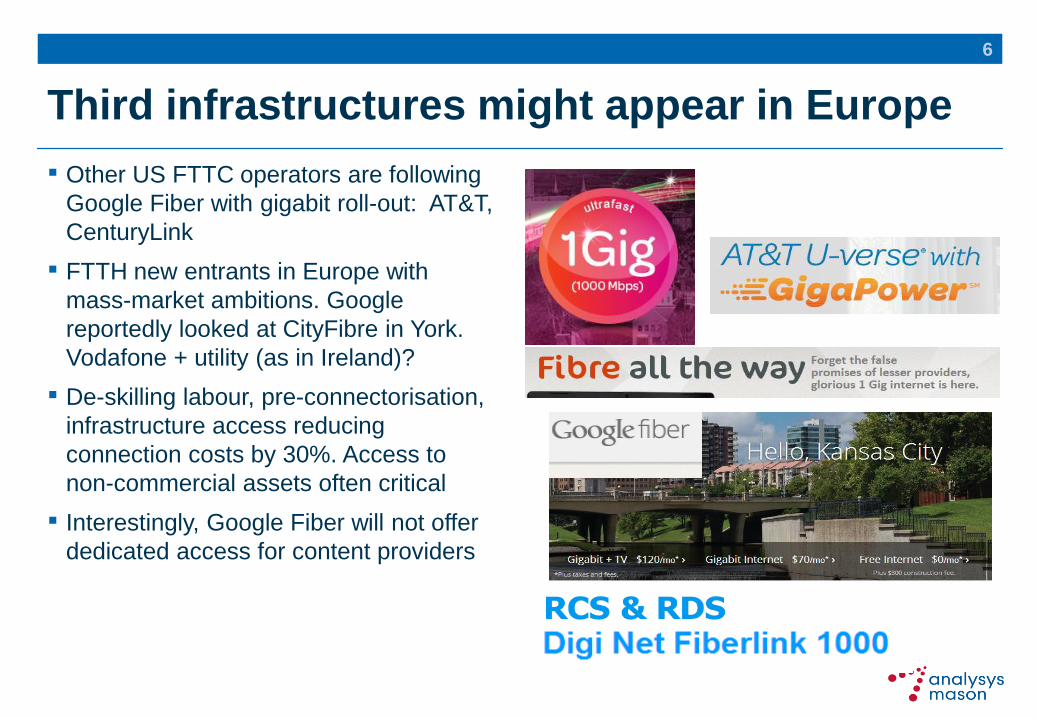

Third infrastructures might appear in Europe

▪ Other US FTTC operators are following

Google Fiber with gigabit roll-out: AT&T,

CenturyLink

▪ FTTH new entrants in Europe with

mass-market ambitions. Google

reportedly looked at CityFibre in York.

Vodafone + utility (as in Ireland)?

▪ De-skilling labour, pre-connectorisation,

infrastructure access reducing

connection costs by 30%. Access to

non-commercial assets often critical

▪ Interestingly, Google Fiber will not offer

dedicated access for content providers

6

2000796-424

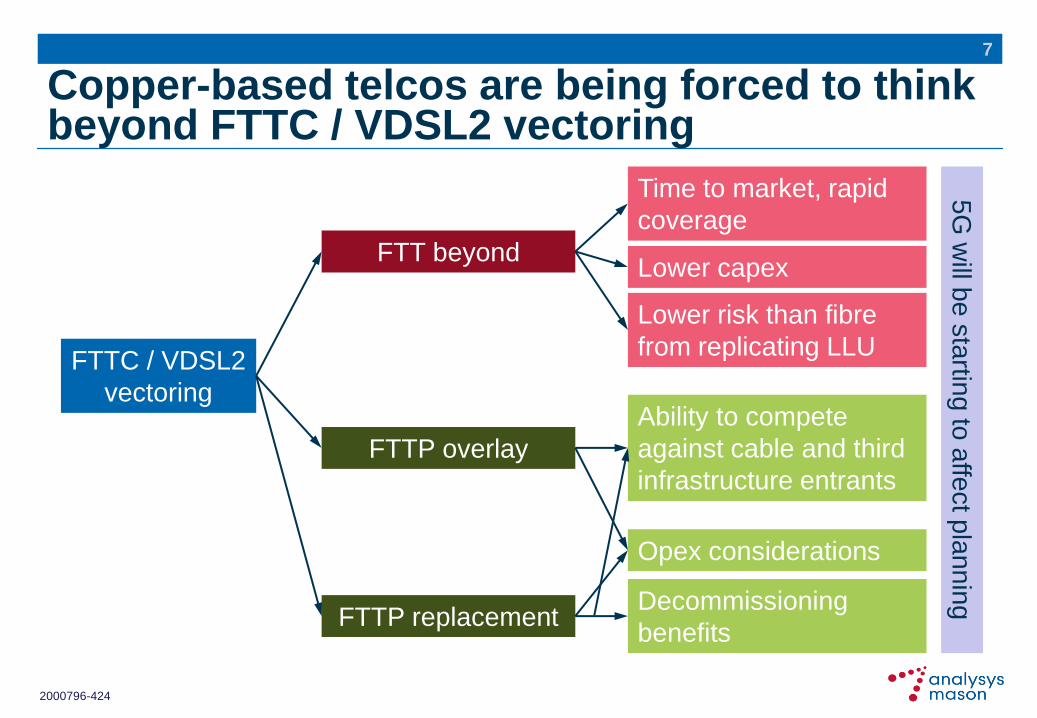

Copper-based telcos are being forced to think beyond FTTC / VDSL2 vectoring

7

FTTC / VDSL2

vectoring

FTT beyond

FTTP overlay

FTTP replacement

Time to market, rapid

coverage

Ability to compete

against cable and third

infrastructure entrants

Opex considerations

Lower capex

Lower risk than fibre

from replicating LLU

Decommissioning

benefits

5G

will b

e s

tartin

g to

affe

ct p

lan

nin

g

2000796-424

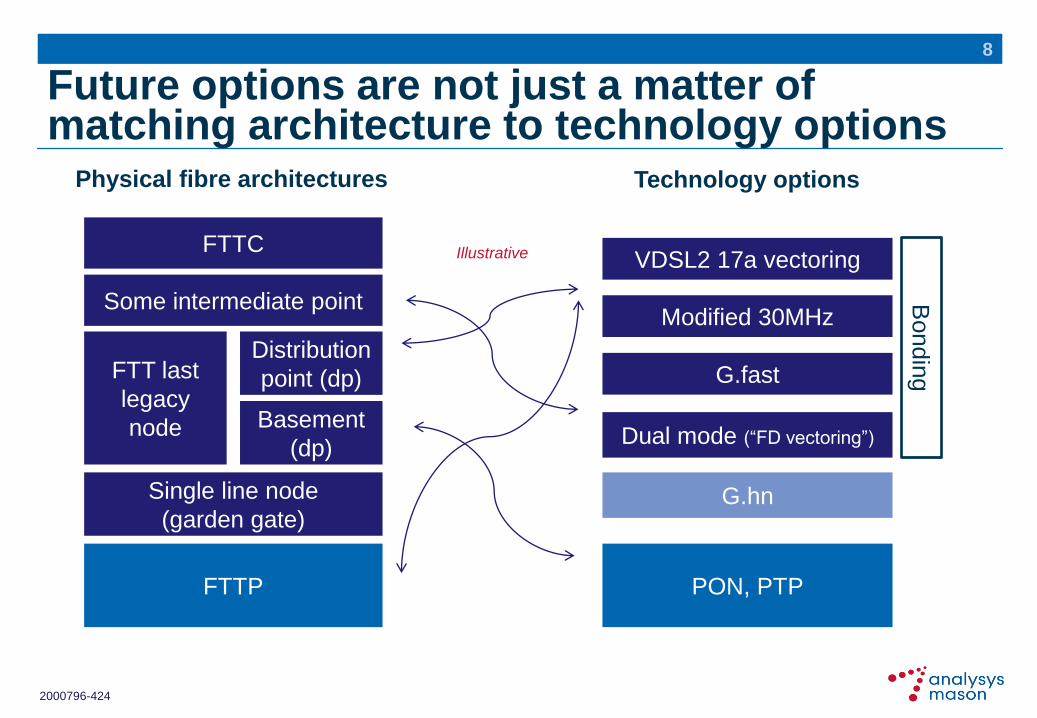

Future options are not just a matter of matching architecture to technology options

8

Physical fibre architectures Technology options

FTTC

Distribution

point (dp) FTT last

legacy

node Basement

(dp)

Single line node

(garden gate)

FTTP

VDSL2 17a vectoring

Modified 30MHz

G.fast

PON, PTP

Bondin

g

Illustrative

Dual mode (“FD vectoring”)

G.hn

Some intermediate point

2000796-424

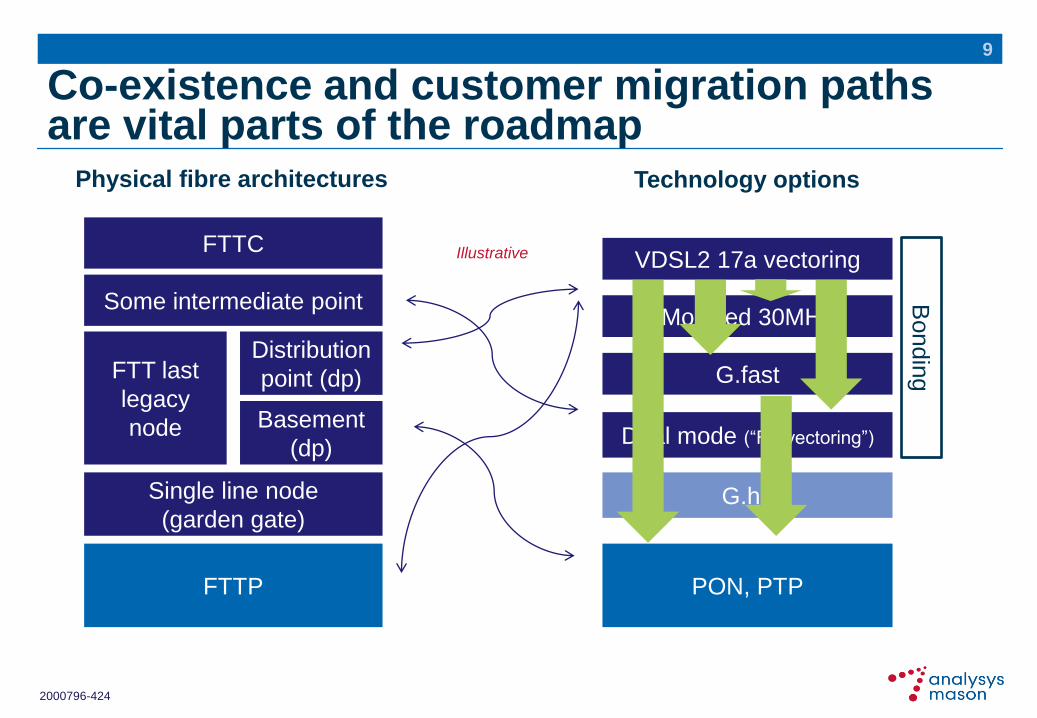

Co-existence and customer migration paths are vital parts of the roadmap

9

Physical fibre architectures Technology options

FTTC

Distribution

point (dp) FTT last

legacy

node Basement

(dp)

Single line node

(garden gate)

FTTP

VDSL2 17a vectoring

Modified 30MHz

G.fast

PON, PTP

Bondin

g

Illustrative

Dual mode (“FD vectoring”)

G.hn

Some intermediate point

2000796-424

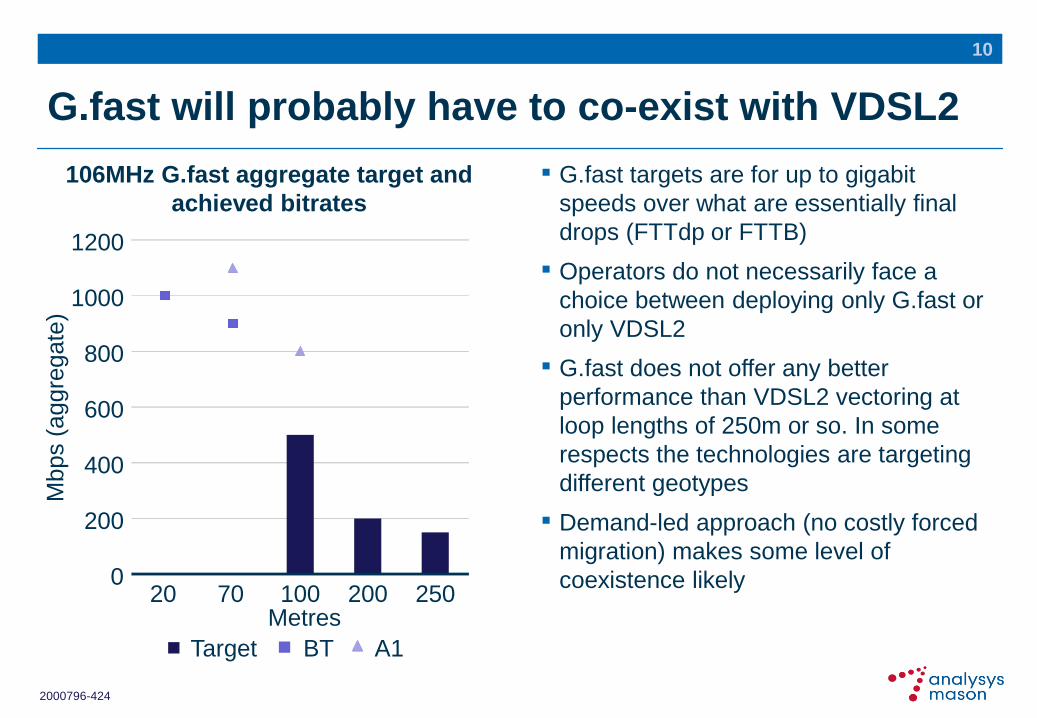

G.fast will probably have to co-exist with VDSL2

▪ G.fast targets are for up to gigabit

speeds over what are essentially final

drops (FTTdp or FTTB)

▪ Operators do not necessarily face a

choice between deploying only G.fast or

only VDSL2

▪ G.fast does not offer any better

performance than VDSL2 vectoring at

loop lengths of 250m or so. In some

respects the technologies are targeting

different geotypes

▪ Demand-led approach (no costly forced

migration) makes some level of

coexistence likely

10

106MHz G.fast aggregate target and

achieved bitrates

20 70 100 200 250 0

200

400

600

800

1000

1200

Mbps (

aggre

gate

)

Metres

Target BT A1

2000796-424

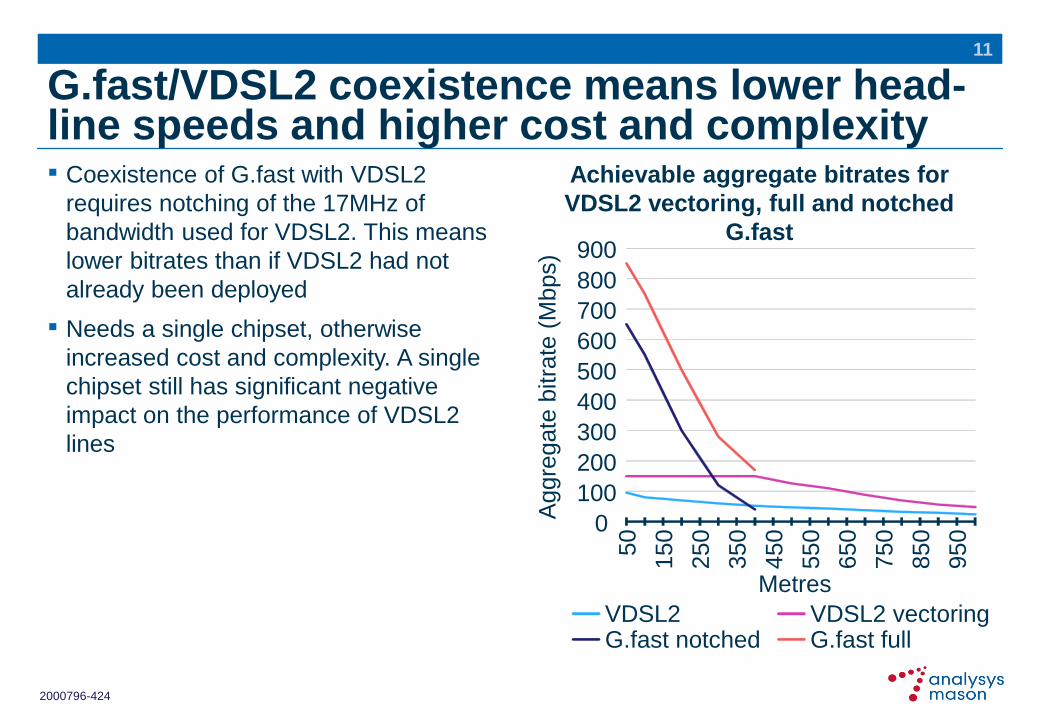

G.fast/VDSL2 coexistence means lower head-line speeds and higher cost and complexity ▪ Coexistence of G.fast with VDSL2

requires notching of the 17MHz of

bandwidth used for VDSL2. This means

lower bitrates than if VDSL2 had not

already been deployed

▪ Needs a single chipset, otherwise

increased cost and complexity. A single

chipset still has significant negative

impact on the performance of VDSL2

lines

11

Achievable aggregate bitrates for

VDSL2 vectoring, full and notched

G.fast

50

150

250

350

450

550

650

750

850

950 0

100

200

300

400

500

600

700

800

900

Aggre

gate

bitra

te (

Mbps)

Metres

VDSL2 VDSL2 vectoring G.fast notched G.fast full

2000796-424

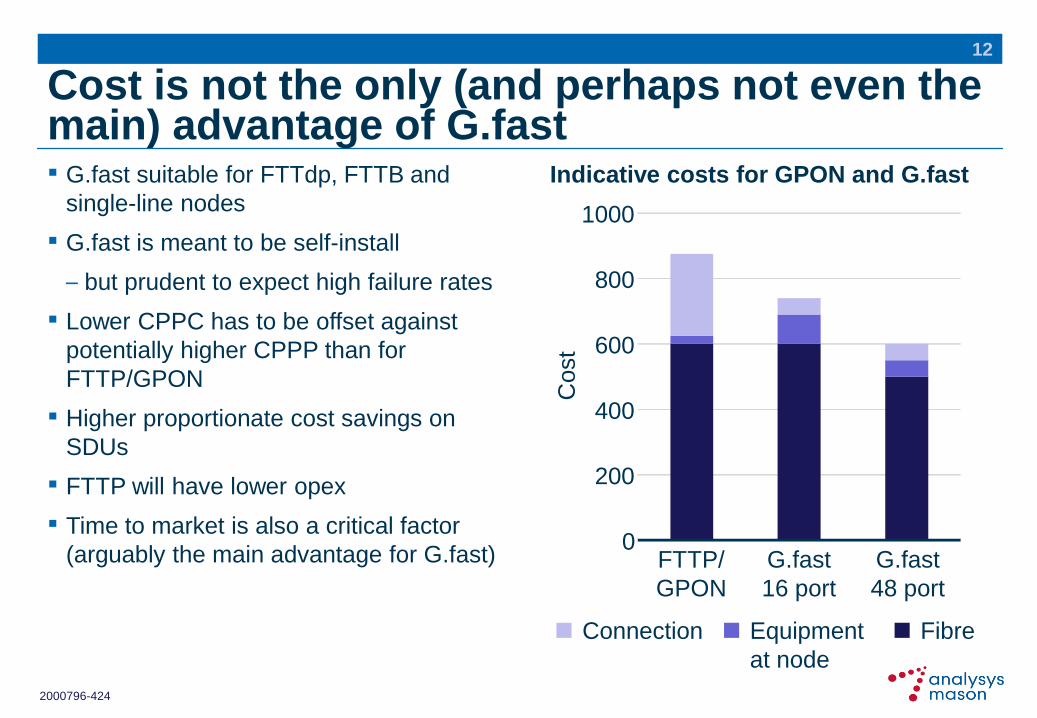

Cost is not the only (and perhaps not even the main) advantage of G.fast ▪ G.fast suitable for FTTdp, FTTB and

single-line nodes

▪ G.fast is meant to be self-install

– but prudent to expect high failure rates

▪ Lower CPPC has to be offset against

potentially higher CPPP than for

FTTP/GPON

▪ Higher proportionate cost savings on

SDUs

▪ FTTP will have lower opex

▪ Time to market is also a critical factor

(arguably the main advantage for G.fast)

12

Indicative costs for GPON and G.fast

0

200

400

600

800

1000

FTTP/

GPON

G.fast

16 port

G.fast

48 port C

ost

Connection Equipment

at node

Fibre

2000796-424

Intermediate solutions are being developed

Modified 30MHz

▪ Leverages existing 30a band plans

(rarely used outside APAC) while

allowing vectored 17a and 30a VDSL2

to coexist in the same binder

▪ No bitrate loss on longer loops, but 30a

bitrates on shorter loops

▪ Can be used anywhere with

FTTC/VDSL2 vectoring now – i.e. any

cabinet

▪ Improvements out to 550m loops

▪ Tone spacing would need to be

changed. ITU would need to

standardise, changes to local ANFPs.

Mid to late 2015 for commercial products

13

Dual-mode (“FD vectoring”)

▪ Like a mobile FD-TD hybrid, notched G.fast

bonds with existing VDSL2 vectoring

▪ No new standards required

▪ More expensive, less scalable (for now)

than modified 30MHz, but potentially

superior performance

Approximate achievable speeds of

modified 30MHz and VDSL2

0

50

100

150

200

250

300

350

50

15

0

25

0

35

0

45

0

55

0

65

0

75

0

85

0

95

0

Aggre

gate

bitra

te

(Mb

ps)

Metres

VDSL2

VDSL2 vectoring

Modified 30MHz

2000796-424

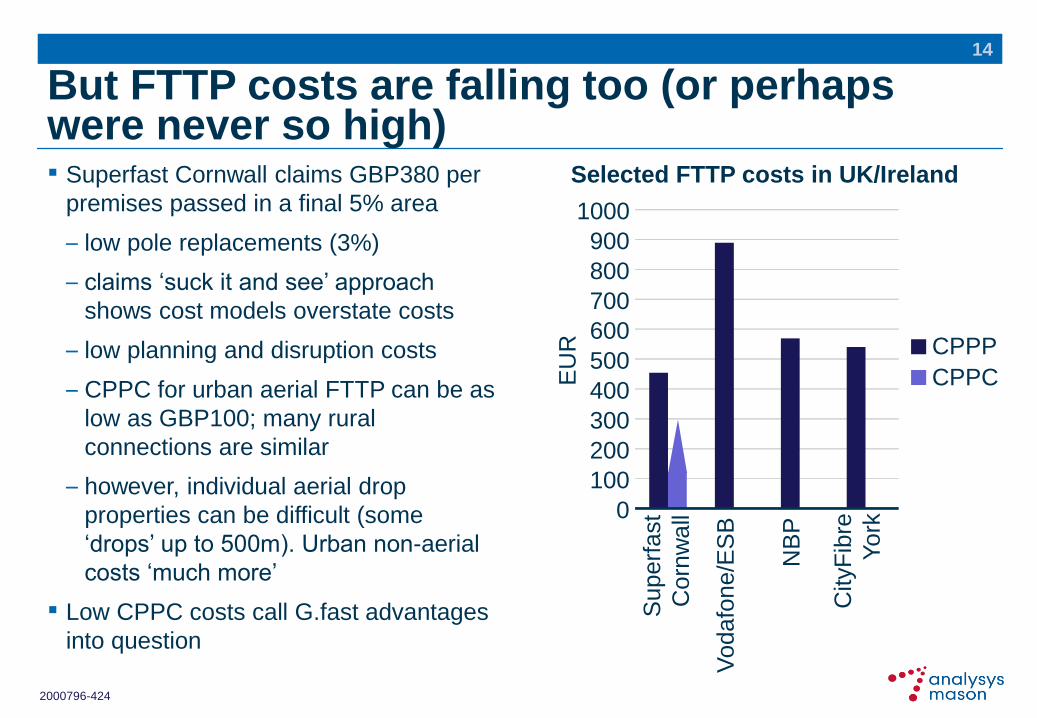

But FTTP costs are falling too (or perhaps were never so high) ▪ Superfast Cornwall claims GBP380 per

premises passed in a final 5% area

– low pole replacements (3%)

– claims ‘suck it and see’ approach

shows cost models overstate costs

– low planning and disruption costs

– CPPC for urban aerial FTTP can be as

low as GBP100; many rural

connections are similar

– however, individual aerial drop

properties can be difficult (some

‘drops’ up to 500m). Urban non-aerial

costs ‘much more’

▪ Low CPPC costs call G.fast advantages

into question

14

Selected FTTP costs in UK/Ireland

0

100

200

300

400

500

600

700

800

900

1000

Superf

ast

Corn

wall

Vodafo

ne/E

SB

NB

P

CityF

ibre

York

EU

R

CPPP

CPPC

2000796-424

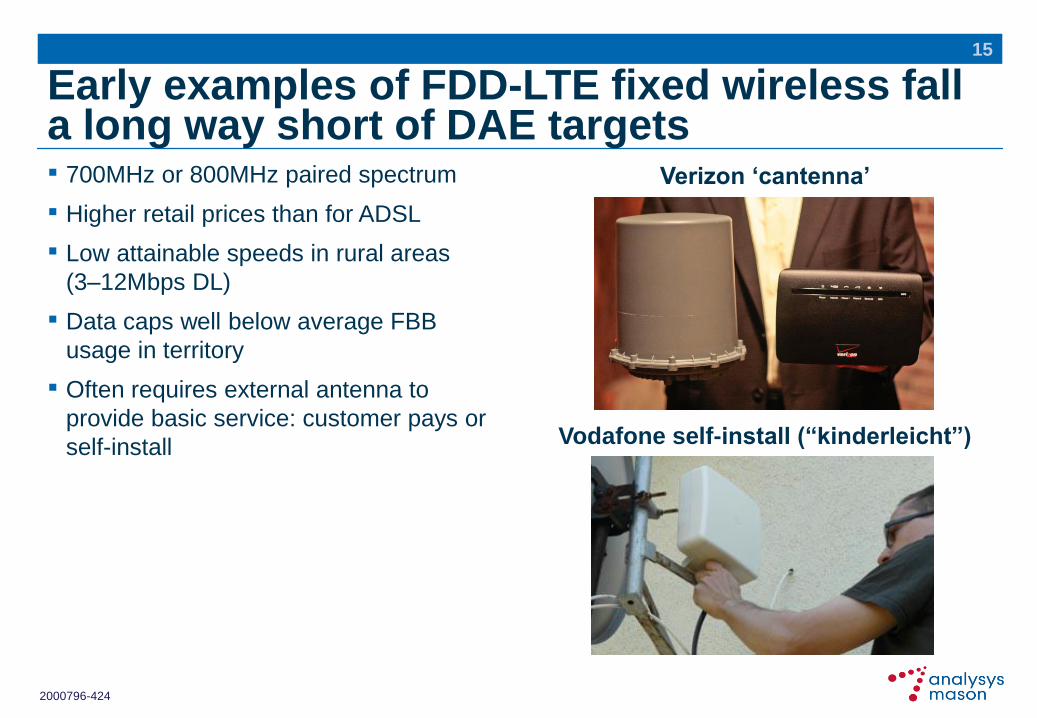

Early examples of FDD-LTE fixed wireless fall a long way short of DAE targets ▪ 700MHz or 800MHz paired spectrum

▪ Higher retail prices than for ADSL

▪ Low attainable speeds in rural areas

(3–12Mbps DL)

▪ Data caps well below average FBB

usage in territory

▪ Often requires external antenna to

provide basic service: customer pays or

self-install

15

Verizon ‘cantenna’

Vodafone self-install (“kinderleicht”)

2000796-424

Active network sharing is becoming common but spectrum pooling is not

▪ Very few examples of full spectrum

pooling in the world (PCCW/3 in Hong

Kong), and none for rural areas

▪ Carrier aggregation with pooled

spectrum improves spectral efficiency a

little

▪ Spectrum sharing will in any case

happen when MNOs are ready to use

licence-exempt secondary-use spectrum

▪ Desirability of maintaining service

differentiation

16

▪ There is no spectrum ‘quick fix’ for deep

rural broadband

▪ Suitability of pooled spectrum bands for

FWA is critical. 800MHz bands alone are

insufficient for fixed wireless. 700MHz

bands are critical, but will probably not

be enough

▪ Fixed-line usage is still vastly higher

than mobile (96% of consumer data

traffic in Europe)

▪ If only higher frequency bands are

available, then infrastructure and CPE

costs (outdoor antennas) rise sharply

towards fixed-line levels

Pooling for rural fixed wireless

2000796-424

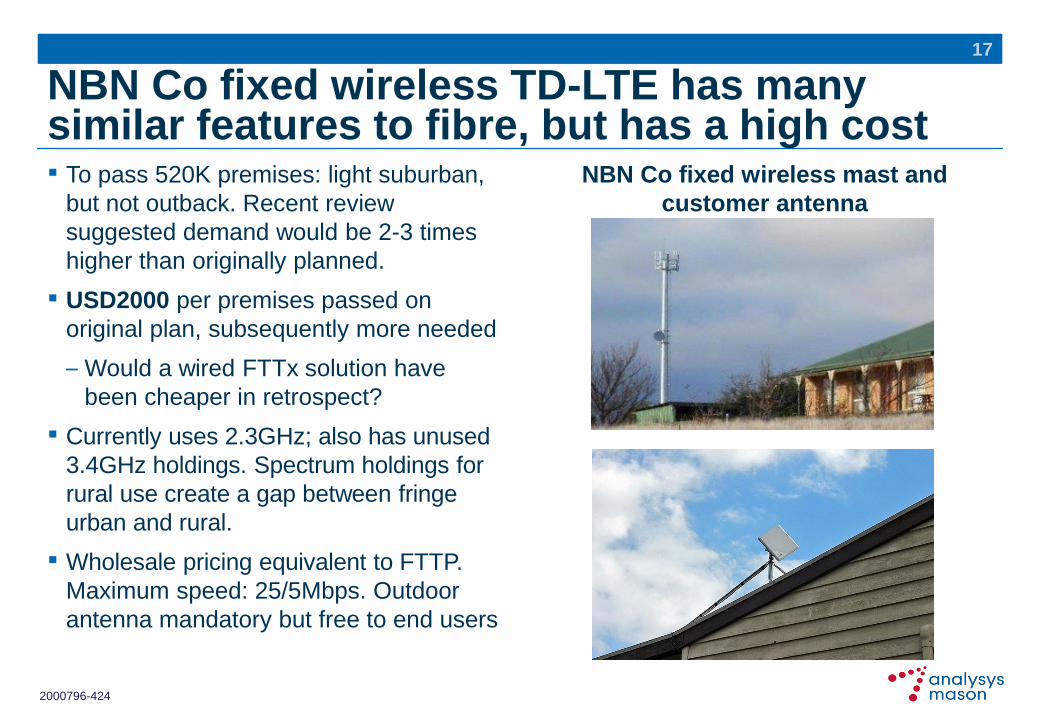

NBN Co fixed wireless TD-LTE has many similar features to fibre, but has a high cost ▪ To pass 520K premises: light suburban,

but not outback. Recent review

suggested demand would be 2-3 times

higher than originally planned.

▪ USD2000 per premises passed on

original plan, subsequently more needed

– Would a wired FTTx solution have

been cheaper in retrospect?

▪ Currently uses 2.3GHz; also has unused

3.4GHz holdings. Spectrum holdings for

rural use create a gap between fringe

urban and rural.

▪ Wholesale pricing equivalent to FTTP.

Maximum speed: 25/5Mbps. Outdoor

antenna mandatory but free to end users

17

NBN Co fixed wireless mast and

customer antenna

2000796-424

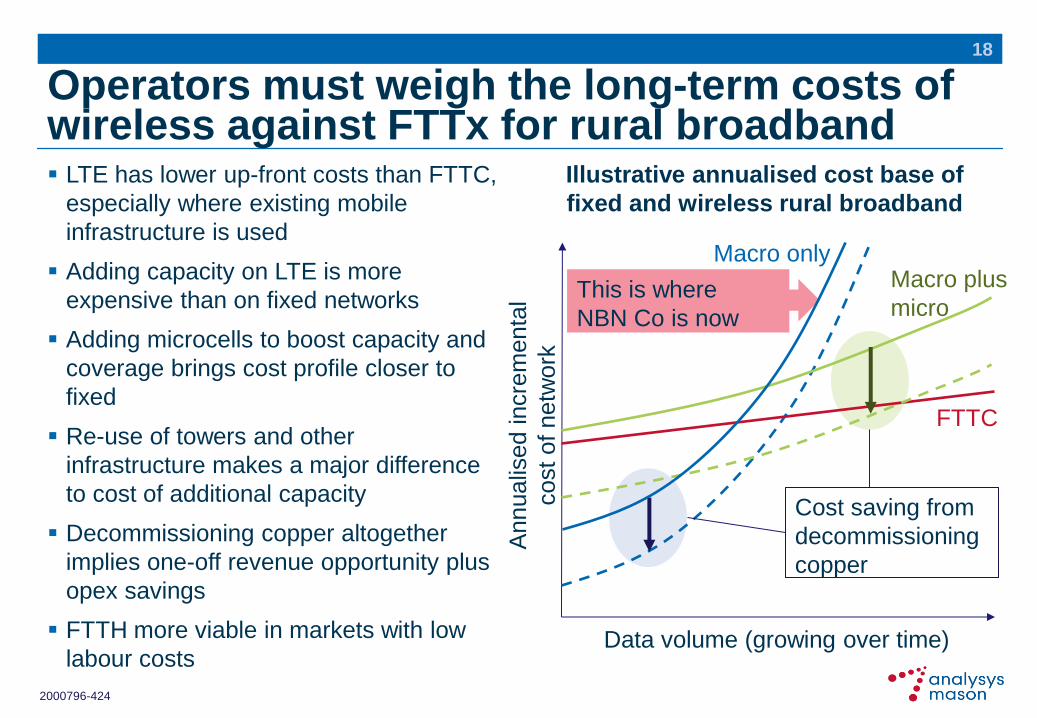

Operators must weigh the long-term costs of wireless against FTTx for rural broadband LTE has lower up-front costs than FTTC,

especially where existing mobile

infrastructure is used

Adding capacity on LTE is more

expensive than on fixed networks

Adding microcells to boost capacity and

coverage brings cost profile closer to

fixed

Re-use of towers and other

infrastructure makes a major difference

to cost of additional capacity

Decommissioning copper altogether

implies one-off revenue opportunity plus

opex savings

FTTH more viable in markets with low

labour costs

18

Illustrative annualised cost base of

fixed and wireless rural broadband

Data volume (growing over time)

Annualis

ed incre

menta

l

cost

of netw

ork

Macro only Macro plus

micro

FTTC

Cost saving from

decommissioning

copper

This is where

NBN Co is now

2000796-424

Conclusions

▪Operators could refocus away from urban to deliver a more-even,

and quicker-to-market, high bandwidth experience

▪ Improving service coverage of >100Mbps is achievable without

additional costs

▪FTTP may cost less in deep rural areas than imagined

▪Fixed wireless is not a cheap option – in fact it will probably cost

more in the long run

19

2000796-424

Contact details

20

Rupert Wood

Principal Analyst

Analysys Mason Limited

St Giles Court, 24 Castle Street

Cambridge CB3 0AJ, UK

Tel: +44 (0)1223 460600

Fax: +44 (0)1223 460866

www.analysysmason.com

Registered in England No. 5177472