Embed Size (px)

Citation preview

Walden C. Rhines

Next Steps for the Indian

Semiconductor Industry

Chairman and CEO

February 3, 2014

www.mentor.com © 2014 Mentor Graphics Corp. Company Confidential

SEMICONDUCTOR INDUSTRY

STRUCTURE

www.mentor.com © 2014 Mentor Graphics Corp. Company Confidential

Top 50 Semiconductor Companies, 2012 13 are fabless

— Qualcomm #4 — Broadcom #11 — AMD #13 — Nvidia #16

4 are foundries — TSMC #3 — UMC #20 — GlobalFoundries #15

Headquarter locations — 23 US 46% — 10 Japan 20% — 6 Taiwan 12% — 6 Europe 12% — 2 South Korea 4% — 2 China 4% — 1 Singapore 2%

WCR, IESA Vision Summit, February 2014 3

( )

( )

www.mentor.com © 2014 Mentor Graphics Corp. Company Confidential

6.1% 6.7% 7.1%

9.0%

12.0% 13.0%

14.2% 15.0%

16.7%

18.3% 18.7%

20.0%

24.9% 24.1%

25.0%

28.5% 29.0%

0%

15%

30%

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Fabless IC Sales (% of total IC Revenue)

Fabless Market Gaining in Overall Market

Source: IC Insights, 2014

WCR, IESA Vision Summit, February 2014 4

www.mentor.com © 2014 Mentor Graphics Corp. Company Confidential

$7.3 $7.3

$9.9

$17.0 $15.1 $16.8

$21.3

$28.7

$34.5

$41.1 $43.8 $43.8

$49.4

$63.5 $66.4

$72.6

$78.1

0

40

80

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Fabless IC Revenue ($ Billions)

Fabless IC Revenue Continues to Grow

Source: IC Insights, 2014

WCR, IESA Vision Summit, February 2014 5

www.mentor.com © 2014 Mentor Graphics Corp. Company Confidential

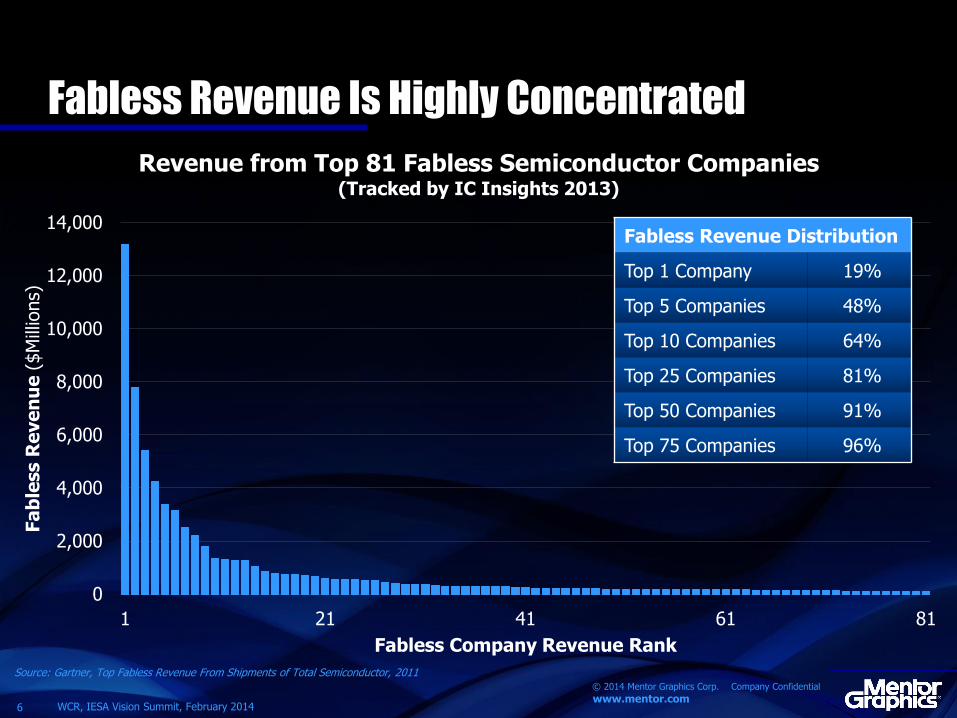

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

1 21 41 61 81

Fa

ble

ss R

eve

nu

e (

$M

illio

ns)

Fabless Company Revenue Rank

Revenue from Top 81 Fabless Semiconductor Companies (Tracked by IC Insights 2013)

Fabless Revenue Is Highly Concentrated

Fabless Revenue Distribution

Top 1 Company 19%

Top 5 Companies 48%

Top 10 Companies 64%

Top 25 Companies 81%

Top 50 Companies 91%

Top 75 Companies 96%

Source: Gartner, Top Fabless Revenue From Shipments of Total Semiconductor, 2011

WCR, IESA Vision Summit, February 2014 6

Fabless Revenue Distribution

Top 1 Company 19%

Top 5 Companies 48%

Top 10 Companies 64%

Top 25 Companies 81%

Top 50 Companies 91%

Top 75 Companies 96%

www.mentor.com © 2014 Mentor Graphics Corp. Company Confidential

Leading Fabless Companies Specialize and

Average ~22 Years since Formation

Fabless Company

Years in Business (Founded)

Headquarters 2012 Rev. ($M)

Technology

Qualcomm 29 (1985) US 13,177 Wireless/CDMA

Broadcom 23 (1991) US 7,793 Wireless/Broadband

AMD 45 (1969) US 5,422 MPU

Nvidia 21 (1993) US 4,229 GPU

MediaTek 17 (1997) Taiwan 3,366 Wireless/Storage

Marvell 19 (1995) US 3,157 MPU/DSP

LSI Corp. 33 (1981) US 2,506 Storage/Networking

Xilinx 30 (1984) US 2,196 FPGA

Altera 31 (1983) US 1,783 FPGA

Avago 9 (2005) Singapore 1,349 Wireless/Wired Infrastructure

HiSilicon 23/10 (1991/2004) China 1,285 Networking/Digital Media

Mstar 12 (2002) Taiwan 1,272 Wireless/Multimedia

Novatek 17 (1997) Taiwan 1,256 Display/Multimedia

CSR 16 (1998) Europe 1,025 GPS/Wireless

Realtek 27 (1987) Taiwan 836 Networking/Peripheral

Dialog 33 (1981) Europe 774 Wireless/Power Mgmt

Himax 13 (2001) Taiwan 738 Display/Multimedia

Spreadtrum 13 (2001) China 725 Wireless

Cirrus Logic 30 (1984) US 714 Broadband/Storage

Source: IC Insights, March 2013 update

WCR, IESA Vision Summit, February 2014 7

www.mentor.com © 2014 Mentor Graphics Corp. Company Confidential

Global Recessions (IMF)

$2,571 $2,399

$1,607 $1,635 $1,832

$1,675 $1,829

$1,987

$1,510

$777 $983 $941 $981

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

VC

Fu

nd

ing

Ra

ise

d (

$M

illio

n)

Worldwide Fabless Semiconductor Companies

Venture Capital Raised by Year

Average $1,725

Average $920

Average $2,485

Source: Global Semiconductor Alliance (GSA) , IMF & Mentor Graphics Analysis

WCR, IESA Vision Summit, February 2014 8

www.mentor.com © 2014 Mentor Graphics Corp. Company Confidential

Total Number of “Fabless Companies”

(GSA Estimate)

50

500

750

850

950

1,100

1,250 1,300

1,350 1,400

1,300 1,300

1,200

1,100

1,010 1,011

1996 1998 2000 2002 2004 2006 2008 2010 2012

Source: GSA Portal, Industry Data 1/10/2012, http://www.gsaglobal.org/resources/industrydata/facts.asp

WCR, IESA Vision Summit, February 2014 9

www.mentor.com © 2014 Mentor Graphics Corp. Company Confidential

The Continuum

Sub-System SoC Supplier Core IP System

Model: IDM Foundry Fabless SIP Design

Services

Design Fabricate

Sell (branded)

Engineers for Hire

Acti

vit

y

IP SoC Wafer

Narrow Fabless Definitions Broad

WCR, IESA Vision Summit, February 2014 10

www.mentor.com © 2014 Mentor Graphics Corp. Company Confidential

Total Semiconductor Companies - GSA — 1284 Companies — 1011 Fabless — 273 IDMs

IC Insights — 133 Companies

The Fabless Universe

WCR, ISA Vision Summit, 2014 12

www.mentor.com © 2014 Mentor Graphics Corp. Company Confidential

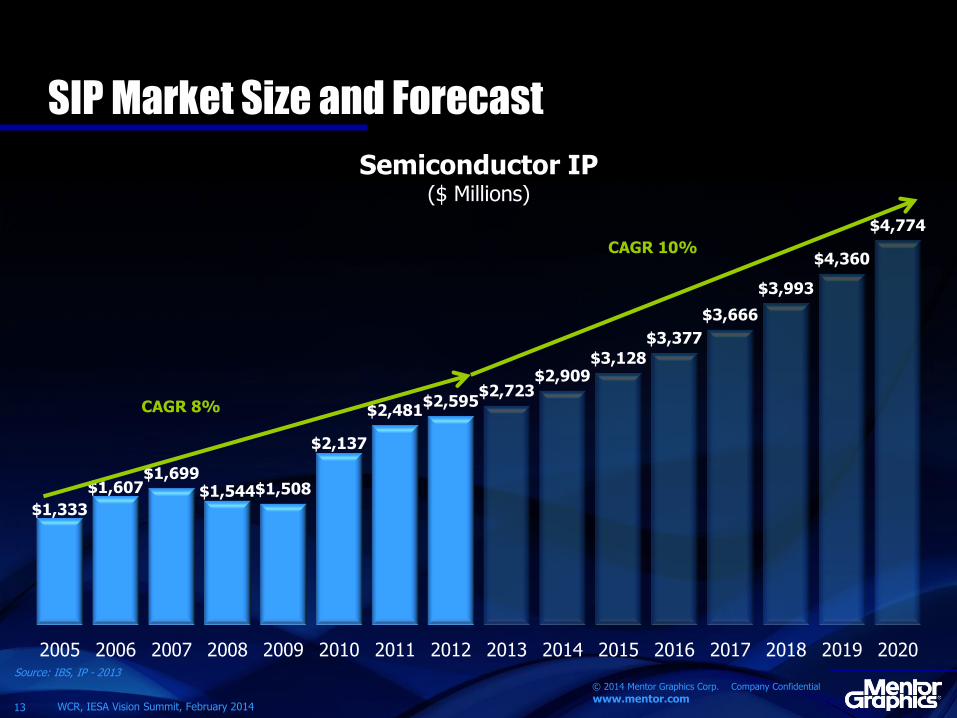

$1,333

$1,607 $1,699

$1,544 $1,508

$2,137

$2,481 $2,595

$2,723 $2,909

$3,128

$3,377

$3,666

$3,993

$4,360

$4,774

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Semiconductor IP ($ Millions)

SIP Market Size and Forecast

CAGR 8%

CAGR 10%

Source: IBS, IP - 2013

WCR, IESA Vision Summit, February 2014 13

www.mentor.com © 2014 Mentor Graphics Corp. Company Confidential

0

250

500

750

1,000

1 2 3 4 5 6 7 8 9 10 11 12

Fabless Company Revenue Rank

Revenue from Top 12 Semiconductor IP Companies ($ Millions)

SIP Revenue Distribution

Source: IBS, IP - 2013

WCR, IESA Vision Summit, February 2014 14

IP Revenue Distribution

Top 1 Company 34%

Top 5 Companies 73%

Top 10 Companies 87%

www.mentor.com © 2014 Mentor Graphics Corp. Company Confidential

0

250

500

750

1,000

1 2 3 4 5 6 7 8 9 10 11

Fabless Company Revenue Rank

Revenue from Top 12 Semiconductor IP Companies ($ Millions)

SIP Revenue Distribution

Source: IBS, IP - 2013

WCR, IESA Vision Summit, February 2014 15

www.mentor.com © 2014 Mentor Graphics Corp. Company Confidential

Leading SIP Players Specialize and Average

~22 Years in Business (Same as Fabless)

Fabless Company

Years in Business (Founded)

Headquarters 2012 Rev.

($M) Technology

ARM Holdings 23 (1990) UK 881.7 MPU Cores

Synopsys Including Virage Logic

27 (1986) US 403.6 Broad Portfolio of Cores

Rambus 23 (1990) US 234.1 Memory

Tessera 23 (1990) US 207.3 Chip Scale Packaging

Imagination Technologies

28 (1985) UK 182.9 Mobile Graphic/

Digital Radio

WiLAN 21 (1992) Canada 88.0 Wired & Wireless

MIPS Technologies Acquired by Imagination 2013

29 (1984) US 82.2 MPU Cores

Cadence 25 (1988) US 72.0 Broad Portfolio of IP

Ceva 11 (2002) US/Israel 53.7 DSP Cores

Silicon Image 18 (1995) US 48.9 Wired & Wireless

Faraday Technology 20 (1993) Taiwan 22.5 Broad Portfolio of Cores

MoSys 22 (1991) US 6.1 Memory & I/O

Source: IBS, IP - 2013

WCR, IESA Vision Summit, February 2014 16

www.mentor.com © 2014 Mentor Graphics Corp. Company Confidential

Tape-outs at advanced nodes are growing

Increasing Percent of Tape-outs at Leading Edge

0

4,000

8,000

12,000

16,000

2008 2009 2010 2011 2012 2013F

By Line Width 2009 2010 2011 2012F 2013F

≥38nm but <55nm 578 845 1,130 1,235 1,309

≥27nm but <38nm 19 76 330 455 596

<27nm 7 61 112 204

TOTAL 12,799 12,958 12,727 12,354 12,136

Source: VLSI Research, October 2012

Design Completions by Line Width

Source: VLSI Research, October 2012

WCR, IESA Vision Summit, February 2014 17

<27nm ≥27nm but<38nm

≥38nm but<55nm

≥55nm but<75nm

≥120nm but<160nm

≥160nm but<200nm

≥200nm but<300nm ≥300nm but<500nm

≥500nm

≥75nm but<120nm

www.mentor.com © 2014 Mentor Graphics Corp. Company Confidential

But Large Opportunities in Older Technologies

0

400

800

1,200

1,600

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

<27nm

32nm

45nm

65nm

130nm

180nm

≥250nm

90nm

43

% o

f P

rod

ucti

on

Wafer Starts KWPW

Source: VLSI Research, December 2012

WCR, IESA Vision Summit, February 2014 18

www.mentor.com © 2014 Mentor Graphics Corp. Company Confidential

“In the next 10 years, as many as 100 billion objects could be tied together to form a

“central nervous system” for the planet and support highly intelligent web-based systems...”

Internet of Things Will Transform the

Semiconductor Industry

WCR, ISA Vision Summit, 2014 20

Source: IC Insights, “IC Market Drivers 2014.” Chart from Cisco, “The Internet of Things: How the Next Evolution of the Internet is Changing Everything,” Dave Evans 2011

www.mentor.com © 2014 Mentor Graphics Corp. Company Confidential

Internet of Things Will Transform the

Semiconductor Industry

WCR, IESA Vision Summit, February 2014 21

Source: Cisco, April 2011

www.mentor.com © 2014 Mentor Graphics Corp. Company Confidential

Company Count

Product Revenue >20%

within specific SIA category

Gross Margin

Average

Gross Margin

Median

Foundry 3 41% 20%

Discrete 7 34% 32%

Memory 6 18% 16%

ASSP 28 48% 50%

Analog 11 51% 54%

Micro Component 8 57% 47%

FPGA 3 66% 65%

Total Database 56 48% 50%

Semiconductor Gross Margin by Category 2012

Average (Weighted Average)

22

Source: Semiconductor Companies (Largest semiconductor companies with published financial metrics available for required reporting periods)

WCR, IESA Vision Summit, February 2014 22

www.mentor.com © 2014 Mentor Graphics Corp. Company Confidential

Product Differentiation

— Process AND design differentiation

— Moderate volume application niches

— Higher design effort per square mm of silicon

— More “art” than digital design

— Lack of multi-sourcing of functions

Infrastructure

— Application support

Product Differentiation Alone Makes Switching

Analog/Mixed-Signal Suppliers Difficult

23 WCR, IESA Vision Summit, February 2014 23

www.mentor.com © 2014 Mentor Graphics Corp. Company Confidential

Change in Strategy toward Differentiation

Gradually Raises GPM%

0%

20%

40%

60%

80%

100%

1980 1985 1990 1995 2000 2005 2010

Gro

ss M

arg

in %

“National Semiconductor

is an analog company…” 2004 Annual Report

National acquires Microprocessor Manufacturer Cyrix

August 1997

National is acquired by Texas Instruments

Linear Technology

Maxim

Analog Devices

National Semiconductor

Source: Company financial reports

WCR, IESA Vision Summit, February 2014 24

www.mentor.com © 2014 Mentor Graphics Corp. Company Confidential

INDIA’S EVOLVING IMPORTANCE TO THE

FUTURE OF THE FABLESS

SEMICONDUCTOR INDUSTRY

www.mentor.com © 2014 Mentor Graphics Corp. Company Confidential

India Is in the Top 5 Semiconductor Design

Locations Worldwide

Source: India Semiconductor Association “Study on semiconductor design, embedded software and services industry” April 2011

WCR, IESA Vision Summit, February 2014 26

www.mentor.com © 2014 Mentor Graphics Corp. Company Confidential

India’s Fabless Company Sample

- GSA and IESA Members

Source: GSA Directory and IESA membership, 2014

WCR, IESA Vision Summit, February 2014 28

www.mentor.com © 2014 Mentor Graphics Corp. Company Confidential

India Is Already a Leading Source of SIP

US, 43.0%

India, 5.3%

UK, 5.3%

Germany, 4.7%

Israel, 4.7%

Canda, 4.3%

France, 4.1%

Taiwan, 4.1%

China, 3.9%

Japan, 3.1%

Others, 17.3%

SIP Company Headquarters Distribution by Country

486 SIP Suppliers

Note: Not corrected for those companies that have a bulk of their resources in India with small headquarter operations in other regions Source: Design & Reuse Portal Silicon IP Vendors, 2014

WCR, IESA Vision Summit, February 2014 31

www.mentor.com © 2014 Mentor Graphics Corp. Company Confidential

Evolving from Design Services to

Fabless Powerhouse

1985 initially offered contract R&D services

1988 company launched it’s first product

1991 Qualcomm went public and revolutionized the wireless communications industry

First CDMA Demonstration

WCR, IESA Vision Summit, February 2014 32

www.mentor.com © 2014 Mentor Graphics Corp. Company Confidential

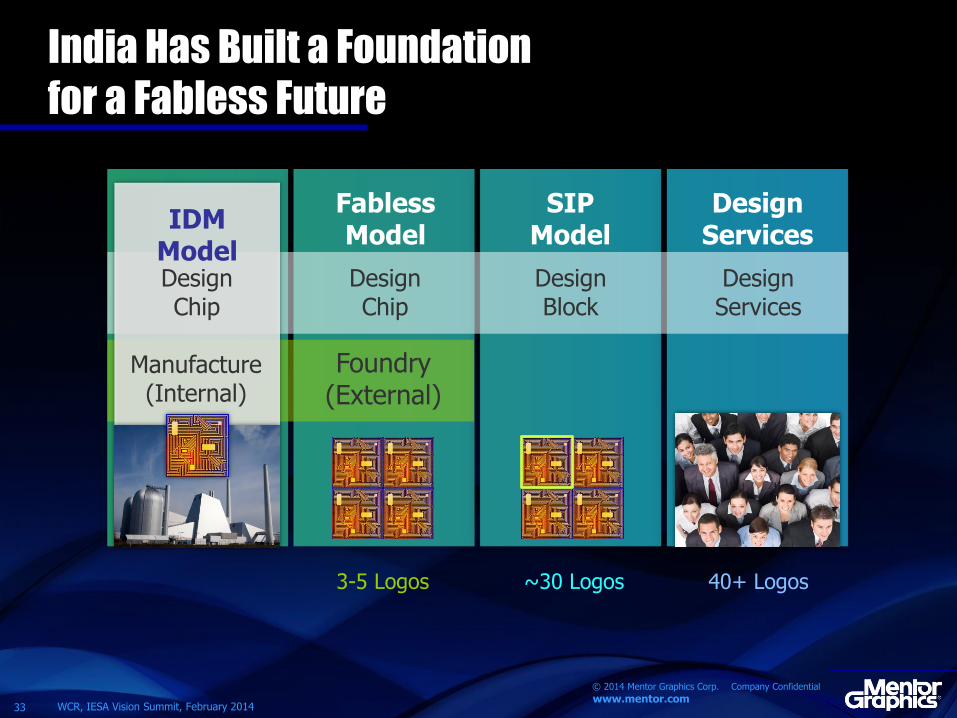

IDM Model Design Chip

Manufacture (Internal)

Fabless Model

SIP Model

Design Services

Design Chip

Design Block

Design Services

India Has Built a Foundation

for a Fabless Future

3-5 Logos ~30 Logos 40+ Logos

WCR, IESA Vision Summit, February 2014 33

Foundry (External)

www.mentor.com © 2014 Mentor Graphics Corp. Company Confidential

FOUNDATION FOR FUTURE

SEMICONDUCTOR GROWTH

www.mentor.com © 2014 Mentor Graphics Corp. Company Confidential

World’s Economic Center of Gravity

Has Moved East

Source: “Urban World: Cities and the rise of the consuming class,” McKinsey & Company, June 2012

WCR, IESA Vision Summit, February 2014 35

AD 1 to 2025

www.mentor.com © 2014 Mentor Graphics Corp. Company Confidential

Worldwide leadership with the most influential design teams in the world

India Has a Strong Foundation

WCR, IESA Vision Summit, February 2014 36

www.mentor.com © 2014 Mentor Graphics Corp. Company Confidential

1,031 Multinational Corporation

R&D Centers in India

Source: Attrition, Hiring and Salary Increase Study, Zinnov, November 2013 http://www.slideshare.net/zinnov/cb-final-deck-media-nov14

WCR, IESA Vision Summit, February 2014 37

www.mentor.com © 2014 Mentor Graphics Corp. Company Confidential

Most Attractive Outsourcing Countries

Source: SourcingLine https://www.sourcingline.com/top-outsourcing-countries

WCR, IESA Vision Summit, February 2014 38

www.mentor.com © 2014 Mentor Graphics Corp. Company Confidential

WCR, IESA Vision Summit, February 2014 39

18 of the top 20 U.S. semiconductor companies have design centers in India

20 European corporations set up engineering R&D centers in India within the last year

Engineering and R&D Activity in India

Source: “Fab opportunity,” The Hindu, November 1, 2013 “European MNCs Keen To Open Their R&D Centers In India,” EFYTimes, May 3, 2013 NASSCOM

www.mentor.com © 2014 Mentor Graphics Corp. Company Confidential

Worldwide leadership with the most influential design teams in the world

Richest pool of creative engineering resources and educational institutions in the world

India Has a Strong Foundation

WCR, IESA Vision Summit, February 2014 40

www.mentor.com © 2014 Mentor Graphics Corp. Company Confidential

2013 Joint Entrance Examination (JEE) statistics

JEE Main exam: ~1.25 million candidates

JEE Advanced: only 150,000 eligible

Qualified: 21,110 students

Called for Interview: 14,336

Available Seats: 9,885 at 17 IITs

IIT Top Ten: included two women for first time

Electronic Designers in India

Are Talented and Competitive

Source: http://education.oneindia.in/news/2013/06/24/iit-jee-advanced-2013-result-analysis-005513.html Pictures from Livemint, April 28, 2013; “Maths “tough” at IIT-JEE”, The Hindu, April 12, 2010; “IIT-JEE 2012 Results Declared,” IBNLive, May 18, 2012

WCR, IESA Vision Summit, February 2014 42

www.mentor.com © 2014 Mentor Graphics Corp. Company Confidential

Experience Level Increasing, But Still a Young and

Creative Workforce

32% 35% 34% 24%

47% 40% 42%

50%

17% 20% 18% 22%

4% 4% 6% 4%

2009 2010 2011 2012

Average R&D Employee Experience

14+ yrs

8-14 yrs

4-8 yrs

0-4 yrs

Source: Attrition, Hiring and Salary Increase Study, Zinnov, November 2013 http://www.slideshare.net/zinnov/cb-final-deck-media-nov14

WCR, IESA Vision Summit, February 2014 43

www.mentor.com © 2014 Mentor Graphics Corp. Company Confidential

Worldwide leadership with the most influential design teams in the world

Richest pool of creative engineering resources and educational institutions in the world

Growing pool of angel investors — In India — Also in the West with strong connections to India

India Has a Strong Foundation

WCR, IESA Vision Summit, February 2014 44

www.mentor.com © 2014 Mentor Graphics Corp. Company Confidential

Top 5 Destination for Foreign Investment

“India has experienced rapid economic gains for a decade

and has a young, large and fast-growing population.

In 2012, the country saw

$25.5 Billion in FDI inflows

with investors still anticipating

enormous potential.”

— A.T Kearney

Source: ATKearney Foreign Direct Investment Confidence Index, 2013

WCR, IESA Vision Summit, February 2014 45

Redraw? 1.77

1.77

1.81

1.83

1.83

1.85

1.86

1.97

2.02

2.09

Singapore

Mexico

UK

Germany

Australia

India

Canada

Brazil

China

United States

2013 FDI Confidence Index® Top 25

www.mentor.com © 2014 Mentor Graphics Corp. Company Confidential

0

110

220

$0

$500

$1,000

$1,500

$2,000

2006 2007 2008 2009 2010 2011 2012

Ro

un

ds o

f Fu

nd

ing

Am

ou

nt

Ra

ise

d (

US $

Mill

ion)

Amount Raised (US$ M) Number of Rounds

Key India VC Statistics

Source: Dow Jones VentureSource, 2013

WCR, IESA Vision Summit, February 2014 46

www.mentor.com © 2014 Mentor Graphics Corp. Company Confidential

CLOSING

THE PRODUCT DEFINITION GAP

www.mentor.com © 2014 Mentor Graphics Corp. Company Confidential

Key Ingredients to Generate a

Thriving Infrastructure

Involvement and expertise with end equipment

Only when Indian engineers are exposed to the full system, top down, can they see where the opportunities to innovate lie along the entire design chain.

EE Times Asia 1/12/2009 http://www.eetasia.com/ART_8800559411_480200_NT_2c623a76.HTM

WCR, IESA Vision Summit, February 2014 48

www.mentor.com © 2014 Mentor Graphics Corp. Company Confidential

Product Marketing

Customer Marketing & Purchasing

“Wants list”

Management Sales

Superb Product Definition Requires

Elimination of Functional Barriers

Product Development Customer

Innovative Product Architecture

True understanding of needs vs. wants

Key developers

Innovative Product Architecture

Corporate “bag of tricks”

Key developers

WCR, IESA Vision Summit, February 2014 49

www.mentor.com © 2014 Mentor Graphics Corp. Company Confidential

Foreign “Flagged” Indian Companies

Produced Early Successes – Some Examples

Companies Focus Highlights

Beceem Communications

HQ — Santa Clara, CA • Design Center: Bangalore, India • Founded: 2003 • Employees: 193+

Mobile Broadband

• $43.7 million revenue in 2009 • 22 US patents & 59 pending and 11 provisional patent applications • Acquired by Broadcom for $316 million in 2010

Redpine Signals

HQ — San Jose, CA • Design Center: Hyderabad, India • Founded: 2001 • Employees: 50+

Wireless Networking

• 100+ patents, patent filings & disclosures on OFDM/MIMO • 2012 Top 100 Global Award Winner • 2013 Best Application of Energy Harvesting award at the IDTechEx

Energy Harvesting & Storage Conference

HelloSoft

HQ — Sunnyvale, CA • Design Center: Hyderabad, India • Founded: 1997 • Employees: 50+

RISC-only VOIP

• Acquired by Imagination Technologies for $47 million • 30+ patents related to IP-based communication • Named one of Top 100 Technology Companies …Silicon India in

2007 • Selected as a Technology Pioneer …World Economic Forum in 2007

WCR, IESA Vision Summit, February 2014 50

Source: RealInnovation.com “Outsourcing: Product Innovation from India: by Zinnov http://www.realinnovation.com/content/c070219a.asp

www.mentor.com © 2014 Mentor Graphics Corp. Company Confidential

Evolution of the Beceem Model

Bridge the gap between the system architects and the designers in India

Do it virtually

Move operations to India

system architect

designers

WCR, IESA Vision Summit, February 2014 51

www.mentor.com © 2014 Mentor Graphics Corp. Company Confidential

Conceived and developed in India

Virtual stimulus

Test bench acceleration

Embedded SW co-development and verification

2x performance; 2x capacity

1/4 power per gate

1/3 footprint per gate

When Users and Tool Developers

Work in Close Proximity…

system architect

designers

WCR, IESA Vision Summit, February 2014 52

www.mentor.com © 2014 Mentor Graphics Corp. Company Confidential

Virtual Peripherals

Test Bench Acceleration

“Out-of-the-Box” Architectural Innovations

Revolutionize Design Verification

Simulation Acceleration

Assertions

Functional Coverage

Low Power

Physical Peripherals

Fast, Accurate Design Compile

Accelerated SW Execution

Total Hardware Debug Visibility

Comprehensive Software Debug

WCR, IESA Vision Summit, February 2014 53

www.mentor.com © 2014 Mentor Graphics Corp. Company Confidential

Lasting Differentiation Requires Infrastructure

Contract Design

SIP

Chips

Systems

Extend to more areas!! • Contract development • SIP • Full chips • Electronic systems

WCR, IESA Vision Summit, February 2014 54

www.mentor.com © 2014 Mentor Graphics Corp. Company Confidential

Summary

While the number of new fabless startups has declined substantially in the West during the past decade, they are growing in India

India has key capabilities to stimulate growth of semiconductor companies — Design services companies — Design engineering expertise and innovation — Returning entrepreneurs — Educational system

Direct interaction with equipment/systems companies will complete the product development process

WCR, IESA Vision Summit, February 2014 55

www.mentor.com © 2014 Mentor Graphics Corp. Company Confidential

w w w . m e n t o r . c o m

www.mentor.com © 2014 Mentor Graphics Corp. Company Confidential

…[entrepreneurial business] in India has been held down for years..[due to] big problems with transport, infrastructure, government intervention at national and local level, swarming chaos and confusion in the streets, blatant poverty.

BBC News Business 6/26/2011

Time has come to demonstrate our leadership position by building our own capabilities in IC design, IC fabrication and design & manufacturing of electronics products”

Ajay Kumar 2/21/2011 Joint Secretary,

Dept. of Information Technology

India's portion of a $250 billion semiconductor market is marginal. It has only two fabless startups, its innovation record as measured by the number of patents granted is dismal, it suffers from a dearth of Ph.Ds and high attrition rates, what talent it does have is undisciplined and it let China dominate completely in systems manufacturing.

EE Times Asia 1/12/2009

I recall a discussion in mid-2005 where an industry expert mentioned that fabless was the way forward for the Indian industry! Between then and now, fabs were supposed to come up, but they failed. Nevertheless, one must not give up hope!

Pradeep Chakraborty’s Blog, April 7, 2011

Semiconductor Frustrations Abound

Original Slide

WCR, IESA Vision Summit, February 2014 66

www.mentor.com © 2014 Mentor Graphics Corp. Company Confidential

Semiconductor Frustrations Abound

Consumption of electronics in India is all set to cross $400 billion by 2020… threatening to cause a major balance of payments crisis by outpacing oil import bill. the country needs to build an ecosystem to avert such crisis.

The Hindu Business Line & J.A. Chowdary, The Indus Entrepreneurs TiE, 2012

India, where the demand for chips goes in billions both in revenue and shipment, needs companies [like Cosmic Circuits] to balance its trade deficit in electronics hardware. Its time for VLSI design service companies in India to get into own product development.

EE Herald, 2011

Approximately 95% of the software and hardware companies in India... base their businesses around outsourcing, while the remaining 5% are Indian-American owned high technology product development startups that are similar to those of Silicon Valley.

Go4 Funding “The Changing Landscape of Indian

Entrepreneurship and Angel Investments”

The proposed national policy… aims to address the huge gap between locally produced electronics and the domestic demand for electronics in India.

Jaswinder Ahuja, Cadence Design Systems India

Original Slide

WCR, IESA Vision Summit, February 2014 67

www.mentor.com © 2014 Mentor Graphics Corp. Company Confidential

Key Ingredients to Generate a Thriving Fabless

Infrastructure

1. Involvement and expertise with end equipment

2. Foster a culture that tolerates failure and minimizes bureaucratic barriers

3. Don’t apologize for being dependent upon multinational companies

Source: RealInnovation.com “Outsourcing: Product Innovation from India: by Zinnov http://www.realinnovation.com/content/c070219a.asp

Original Slide

WCR, IESA Vision Summit, February 2014 68

www.mentor.com © 2014 Mentor Graphics Corp. Company Confidential

1. Involvement and expertise with end equipment

2. Foster a culture that tolerates failure and minimizes bureaucratic barriers

3. Don’t apologize for being dependent upon multinational companies

4. Grow entrepreneurial connections between India and companies in the U.S., Europe and Asia

Key Ingredients to Generate a

Thriving Fabless Infrastructure

Original Slide

WCR, IESA Vision Summit, February 2014 69