Embed Size (px)

Citation preview

The Next Billions:Unleashing Business Potential in

Untapped Markets

COMMITTED TO IMPROVING THE STATE

OF THE WORLD

Prepared in collaboration with The Boston Consulting Group

World Economic ForumJanuary 2009

The views expressed in this publication do not necessarily reflect those of the World Economic Forum.

World Economic Forum91-93 route de la CapiteCH-1223 Cologny/GenevaSwitzerlandTel.: +41 (0)22 869 1212Fax: +41 (0)22 786 2744E-mail: [email protected]

© 2009 World Economic ForumAll rights reserved.No part of this publication may be reproduced or transmitted in any form or by any means, including photocopying andrecording, or by any information storage and retrieval system.

All photographs by Brent Stirton, courtesy of Getty Images,except for those on page 13 and page 29.

REF: 150109

Contents

Preface 4

Executive Summary 5

Chapter 1 – New Potential: Improving Lives and Opening Markets 8

Chapter 2 – New Markets: Opportunities and Challenges 10

Chapter 3 – New Perspectives: Challenging Deep-seated Beliefs 14

3.1 Affording Access Rather than Ownership 14

3.2 Monetizing Hidden Assets 16

3.3 Bridging the Gap in Public Goods through Private Enterprise 18

3.4 Scaling Out versus Scaling Up 19

3.5 Governing through Influence Rather than Authority 21

Chapter 4 – New Approaches: Design Principles for Success 24

4.1 Create Life-enhancing Offerings 24

4.2 Reconfigure the Product Supply Chain 26

4.3 Educate through Marketing and Communication 28

4.4 Collaborate to form Non-traditional Partnerships 29

4.5 Unshackle the Organization to Help New Business Models Succeed 32

Chapter 5 – New Alliances: Priorities for Stakeholders 33

Terminology 36

References 37

Appendix 1: Methodology for Estimating Populations and Incomes 39

Appendix 2: Case Study Selection Process 41

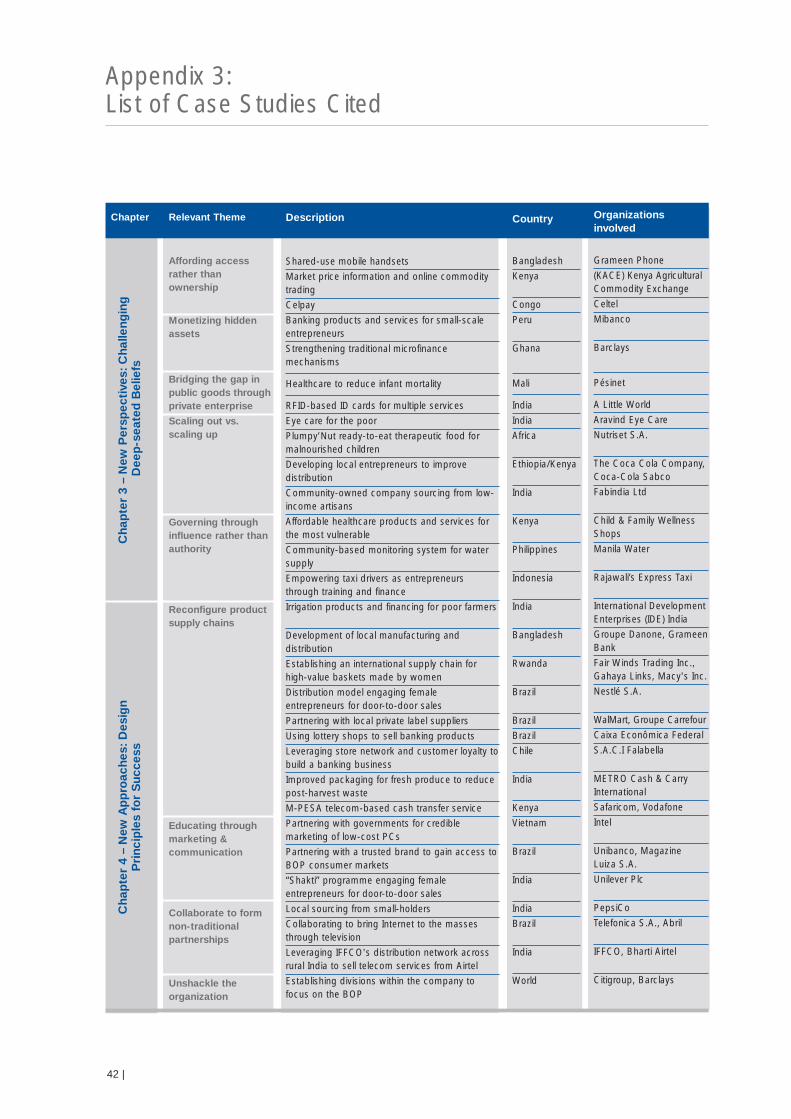

Appendix 3 – List of Case Studies Cited 42

The World Economic Forum is pleased to presentthis report on innovative approaches through whichcompanies across a broad range of industries cantap the economic potential of the “base of thepyramid” (BOP), generating sustainable economicgrowth while improving the livelihoods of the poor.

As part of its mission to facilitate “entrepreneurshipin the global public interest,” the Forum serves as aplatform for leaders to define and catalyse business-led and multi-stakeholder solutions to fostersustainable economic development. Over the pastfour years, the Consumer Industries community ofthe Forum has championed a series of activities,focused on improving food production and incomesin poor communities. The group has focused oncommercially viable business models that offer vitalproducts, services and business linkages relevant tothe food value chain – not only in the agriculture,food and beverage sectors but in retail and consumer,finance, telecom, energy and logistics as well.

This report was undertaken with support from theBill & Melinda Gates Foundation, with the goal ofdefining commercially viable business strategies thatcan help reduce poverty and hunger. It is based ona broad research survey plus three cross-industry,multi-stakeholder roundtables conducted in LatinAmerica, Africa and Asia during 2008. The researchsurvey included review of 60 reports and collectionof 200 case studies from primary and secondarysources. The roundtables provided ground-levelinsights from practitioners – ranging from multinationaland regional companies to social entrepreneurs –who are pioneering these business models on theground. The project team also drew on the priorwork of numerous thought leaders in this arena.

The business strategies outlined in this report form partof a rapidly-evolving frontier of BOP business initiativesworldwide. Undertaken by global and local companies– often in partnership with other organizations – theyrepresent the highly dynamic business innovationbeing applied in fast-growing BOP markets.

This report presents a set of new insights and designprinciples which can help companies tap theeconomic potential of BOP markets in ways thatserve both commercial and societal goals. It offers anarray of examples illustrating successful approaches;and recommends actions both companies and otherstakeholders can take to successfully develop andbroaden such initiatives. The report is being publishedjointly with a companion volume, “The Next Billions:Business Strategies to Enhance Food Value Chainsand Empower the Poor,” applying these concepts tothe food value chain, which comprises the largestshare of BOP income and spending.

This project was undertaken by the World EconomicForum in partnership with The Boston ConsultingGroup. Lisa Dreier led the initiative at the Forumtogether with Jennifer Baarn and Pial Islam, withinput from Helena Leurent, Sarita Nayyar and RickSamans. We thank The Boston Consulting Group forits work, led by Arvind Subramanian, AnandRaghuraman and Nimisha Jain with Neetu Vasanta,S. Rajagopal and Marije van Mens.

The report reflects the input, discussion and review ofa number of Forum partners and experts, to whom weare greatly indebted. Reviewers of this report include:Andrew Aulisi of the World Resources Institute (WRI),Susan Morgan of BT, Richard Rogers of the Bill &Melinda Gates Foundation, Willa Shalit of Fair WindsTrading Inc. in collaboration with Macy’s, Chris Shea ofGeneral Mills, and David Spielman of the InternationalFood Policy Research Institute (IFPRI). Jane Nelsonof Harvard University, Francisco Noguera of the WorldResources Institute and Mirjam Schoening of the SchwabFoundation for Social Entrepreneurship also servedas independent reviewers of the case study selections.

The economic and food crises of 2008 haveunderscored the need for sustainable models foreconomic growth which strengthen the livelihoods ofthe poorest. The strategies outlined in this reportoffer a pathway for business to develop suchmodels, in partnership with other stakeholders.

Preface

4 |

Richard SamansManaging DirectorWorld Economic Forum

Sarita NayyarSenior Director, Consumer IndustriesWorld Economic Forum

Companies around the world are increasing theirengagement in emerging markets, yet many remainfocused on the high-income populations in thosecountries. In fact, the world’s low-income population(the so-called “base of the pyramid”, or BOP)represents considerable productive andentrepreneurial potential, as well as untappeddemand for products and services. Yet, challengesin the business operating environment often limit thesuccess of standard business models in the BOPmarket. Companies that manage to overcome thesechallenges can generate both commercial benefitand sustainable livelihoods for the poor.

Success requires creative, new approaches tosourcing and distribution, product design andpartnerships. This report presents an overview of theopportunity at the BOP, outlines strategies that anumber of companies have adopted to generateboth commercial and social benefit in this market,and suggests design principles that companies andpartners can use when devising their own approaches.

The Opportunity

Globally, 3.7 billion people are largely excluded fromformal markets. This group, earning US$ 8a per dayor less, comprises the “base of the pyramid” (BOP)in terms of income levels. With an annual income ofUS$ 2.3 trillion a year that has grown at 8% inrecent years, this market represents a substantialgrowth opportunity.

While it is highly diversified, much of the BOPrepresents a fast-growing consumer market, anunderutilized productive sector, and a source ofuntapped entrepreneurial energy. Engaging the “nextbillions” at the BOP as producers, consumers andentrepreneurs is therefore key to both reducingpoverty and driving broader economic growth.

Historically, challenges in the operating environmenthave deterred companies from engaging in thismarket. As a result, people at the BOP remainbeneath the radar of most conventional businessmodels, often forced to rely on informal markets andsubstandard products. Companies that find new

ways to overcome constraints and tap opportunitiescan gain insights, market share and customer orsupplier loyalty, and will secure a strong position inthis growing market.

Successful business models can substantallyimprove BOP incomes and livelihoods, improvingaccess to essential goods and services whilecatalyzing economic multipliers and reducinginequality. Therefore, the BOP market offers ameeting ground where corporate economic benefitand social impact can be achieved together.

Understanding the BOP

Within the BOP group, income levels vary. About 1.1billion earn US$ 2-8 per day and – while stillconsidered poor – are beginning to generate significantdiscretionary income. In the mid-range, 1.6 billionearn between US$ 1-2 per day, spending largely onessentials. One billion people live in extreme poverty,earning under US$ 1 per day, and often struggle tomeet basic needs (all figures in PPP$). People atthese income levels are found worldwide, largely inAsia, Africa and Latin America, with 60% of the BOPconcentrated in India and China.

The first step for companies seeking to engage thenext billions as producers and consumers is toovercome traditional stereotypes and mindsetsabout who they are and what they can accomplish.Although their needs are diverse and vary by culture,people at the BOP share several characteristics thatcompanies need to understand to do business withthem effectively:• Financial constraints: Low and fluctuating

incomes, and limited access to credit orinsurance, drive the BOP to be smart shoppersand risk-averse investors.

• Life challenges: Domestic constraints, difficultliving conditions, and high prices for oftensubstandard products or services are among thedaily challenges at the BOP.

• New Customers: BOP consumers lackinformation on many commercial products, andtherefore rely more heavily on trusted sources ordemonstrations to make buying decisions.

• Quality Standards: BOP consumers and workersconduct their lives with dignity and demand bothrespect and quality from service providers andemployers.

Executive Summary

| 5

a The US$ 8/day income threshold is in Purchasing PowerParity (PPP) dollars, and was defined by the WorldResources Institute report, The Next 4 Billions.

Adopting New Perspectives

Once a company understands the BOP market onits own terms, it must look beyond its traditionalbusiness approaches and – in collaboration withgovernments and local organizations – developinnovative new models suited to BOP needs andcapabilities. Companies can reframe the problemsencountered in BOP markets, finding ways toleverage them into business opportunities. Suchnew perspectives include the following:Affording access rather than ownership:Companies should consider how they can shift froma “selling” mode to one that deploys products foruse without requiring ownership. The focus shouldbe on the community rather than individuals.

Monetizing hidden assets: BOP communitiescontain “hidden assets” such as undocumentedcapital, community and personal resources, andunderutilized assets. Companies can seek out suchassets within communities and work to leveragetheir value.

Bridging the gap in public goods throughprivate enterprise: To overcome both hard andsoft infrastructure constraints, businesses canpartner with other organizations to implementinnovative solutions that benefit everyone.

Scaling out versus scaling up: Standardproduction models are often ineffective at the BOP.Centralized, large-scale production can increasecosts and fail to meet localized needs in BOPmarkets. Instead, businesses should combinescaling out with scaling up. Scaling out involvesleveraging local assets – manufacturing,entrepreneurs, producers – to adapt and replicatebusiness models according to local conditions.

Governing through influence rather thanauthority: Flexibility and decentralization are crucialfor adapting to local changes and controlling costs.Companies can reduce the need for costlymonitoring by aligning the interests of the employeeswith those of the company.

Design Principles for SuccessfulBusiness Models

Companies can translate new perspectives on theBOP into new business models. In seeking todevelop effective business models, companies candraw upon five design principles outlined below.

Create life-enhancing offerings: Develop offeringsthat improve the livelihoods of the BOP by pricing fortheir budgets, tailoring products to address localconstraints, and developing environmentallysustainable approaches.

Reconfigure the product supply chain: Create acost-efficient distribution system by sourcing fromlocal producers, leveraging existing local distributionchannels, and finding creative ways to overcomeinfrastructure constraints.

Educate through marketing communication:Design marketing programs that contain educationalas well as persuasive messages about productbenefits. Leverage trusted people, institutions andbrands to build consumer loyalty.

Collaborate in non-traditional partnerships: Tolower costs and broaden distribution, partner withlocal producers and consumers, as well as othercompanies. Invest in local talent and createincentives that encourage self-governance.

Unshackle the organization: Design corporateorganizational structures – including metrics,incentives and accountability systems – to support,measure and reward long-term success in businessinitiatives targeting the BOP

6 |

New Alliances: Priorities forStakeholders

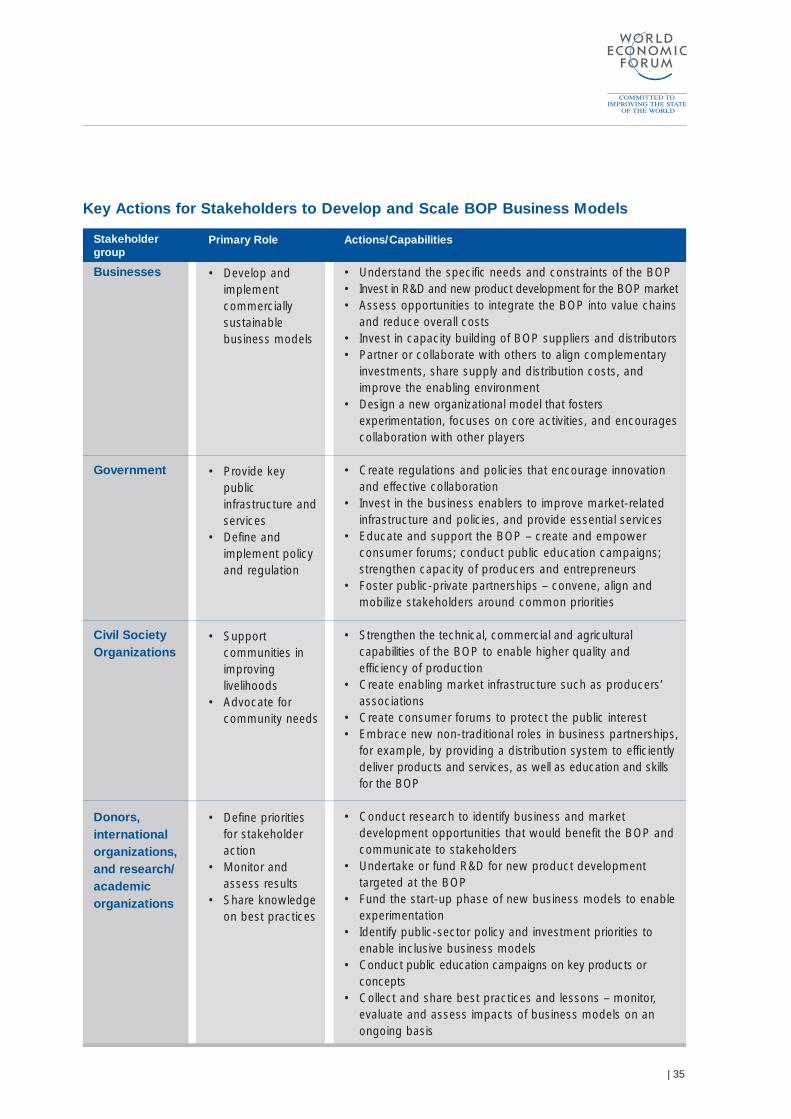

The innovative approaches described in this reportcan form the foundation of new growth opportunitiesfor companies that are bold enough to experiment.However, success in BOP markets often requirescollaboration with other companies or stakeholders.Such partners bring key capacities to enable orsupport BOP business models throughcomplementary action.

• Governments can strengthen policy and taxincentives for BOP business engagement.Examples in the telecom and agriculture sectorshave shown how policy reform can catalyzeincreased local investment and service provision.

• Companies can collaborate across industries andamong stakeholders to leverage shared resourcesand capabilities. Partnering with NGOs, donorsand governments can combine organizationalcapacities in ways that benefit all.

• All stakeholders can work to identify viablebusiness models, monitor and evaluate theirimpacts, and share learnings to acceleratemomentum. Raising the visibility of successfulBOP business initiatives can catalyze learning andbroader adoption by companies.

Over the next decade, even in the face of globaleconomic challenges, the base of the pyramid islikely to be a source of continued economic growth.Companies can establish a footprint in this growingmarket, while also investing in the communities thatwill lead and drive its expansion. The net result willsubstantially improve livelihoods, while generatingeconomic growth for companies and communitiesalike.

| 7

Nearly 3.7 billion people – more than half the world’spopulation – live on less than US$ 8b a day[1-4]and havebeen largely excluded from formal markets. They areoften referred to as the “Base of the Pyramid” (BOP).The lowest third of this group, in terms of income, stilllives below subsistence level and requires support toescape poverty. Those at the top of this segment –about a billion people – are beginning to generatesignificant discretionary income. Although they exhibitconsiderable productive and entrepreneurial potential,as well as demand for products and services, mostcompanies view them as risky, costly and unprofitableto serve. As a result, the BOP market remains beneaththe radar of most conventional business models, andmany at the BOP are forced to rely on informalmarkets and substandard products.

There are compelling reasons to focus on the nextwave of consumers, producers and entrepreneurs thatare found within the BOP. Bringing them into formalmarkets will expand and stabilize their incomes andimprove access to basic needs like education,healthcare and financial services, among others. It canalso trigger economic multipliers, easing socialtensions and reducing inequality.

What’s more, the approximately US$ 2.3 trillionc ayear that the BOP spends (an amount that has beenrapidly increasing) presents a substantial opportunityfor growth and competitive advantage to companiesthat are able to access it[1-4]. Although the needs ofthe BOP are diverse and vary by country andculture, once businesses have discovered successfulways to work with the BOP in one market, they cantransfer the process of innovation to other markets.

Early movers into the market of the next billions willgain many advantages: by being first to develop newofferings and establish innovative delivery channels,they will be in a position to gather valuable insights,gain greater market share, reach deeper into theBOP and attract the loyalty of consumers andproducers as incomes grow and needs expand.Therefore, the next billions offer a meeting groundwhere corporate economic benefit and social impactcan come together.

Chapter 1 – New Potential: Improving Lives and Opening Markets

8 |

• Nearly 3.7 billion people across emerging economies occupy the base of the pyramid (BOP); they earnless than US$ 8 a day (2002 PPP$) and remain largely excluded from formal markets

• Within this group is a sizable segment of potential consumers, producers and entrepreneurs who could beengaged by companies profitably with new business models – they are the “Next Billions”

• The first step for companies seeking to engage the poor as producers and consumers will be to overcometraditional stereotypes and mindsets about who they are and what they can accomplish

• Companies that are first to overcome the inherent challenges of this segment with sustainable businessmodels will gain a competitive advantage, while improving the lives and livelihoods of this large population

The “BOP” and the “Next Billions”“Base of the pyramid” (BOP) is a collectivereference to 3.7 billion people populating thelowest income strata in the world. The incomethreshold for this group is US$ 3,000 per personper year (in 2002 PPP$), or roughly US$ 8 perperson per day.

Within this group are the “next billions” – a largegroup of consumers, producers andentrepreneurs who can be profitably engaged orserved by business, albeit with new andinnovative approaches. Within this report, theterm “next billions” refers to the members of theBOP whom business has the opportunity toengage in the near term.

b In 2002 PPP$.c In 2008 US dollars. All figures with regards to incomes and

spends are in 2008 US dollars, unless stated otherwise.

| 9

Accessing the next billions does present challenges– but companies can overcome these by lookingbeyond traditional business models. In this report,the term “business model” encompasses both theproduct or service offering, as well as the operationaland financial arrangements that go into generatingreturns from a particular activity. Business modelinnovation involves significant changes in two ormore components of the business model thattogether redefine a company’s position in the marketand create superior value.

To achieve business model innovation, organizationsmust first cultivate a more nuanced understanding ofthe BOP – how they live and what they need toimprove their livelihoods. Second, they need to lookat economic levers that limit operations in this market,including the regulatory and policy environment, anddefine strategies for overcoming those obstacles.

A number of companies are starting to adoptsuccessful models that extend their reach into thesemarkets. They are developing technologies,products, and services that meet local needs. Theyare discovering local capacity for supply anddistribution networks. They are expanding access tofinance for consumers, producers andentrepreneurs. And they are partnering with eachother, as well as with governments and civil societyorganizations (including both public and local

community organizations), to implement newbusiness models. These “inclusive” interventions arecatalysing significant improvement in the livelihoodsof the BOP, creating a virtuous cycle of growingincomes and purchasing power within theircommunities.

Although this opportunity is attractive for manyindustries, some have made more headway thanothers. Packaged goods companies, for instance,have realized substantial progress in deepeningdistribution, and telecommunication players havebeen able to reduce hardware, service andcollection costs. By describing current challenges,highlighting pioneering efforts and distilling principlesfor success, this report offers a cross-industryperspective demonstrating that it is possible todevelop inclusive, profitable and scalable businessmodels to engage with the BOP.

Chapter 2 takes a deep dive into the lives of theBOP – to understand who they are, how they copewith their constraints, and what they will need in theyears ahead. Chapter 3 expands on newperspectives that could help companies break out ofexisting mindsets and develop new approaches.Chapter 4 provides practical design principles forcreating successful new business models. Chapter 5recommends a way forward to broaden the scope ofbusiness engagement at the BOP.

Chapter 2 – New Markets: Opportunities and Challenges

10 |

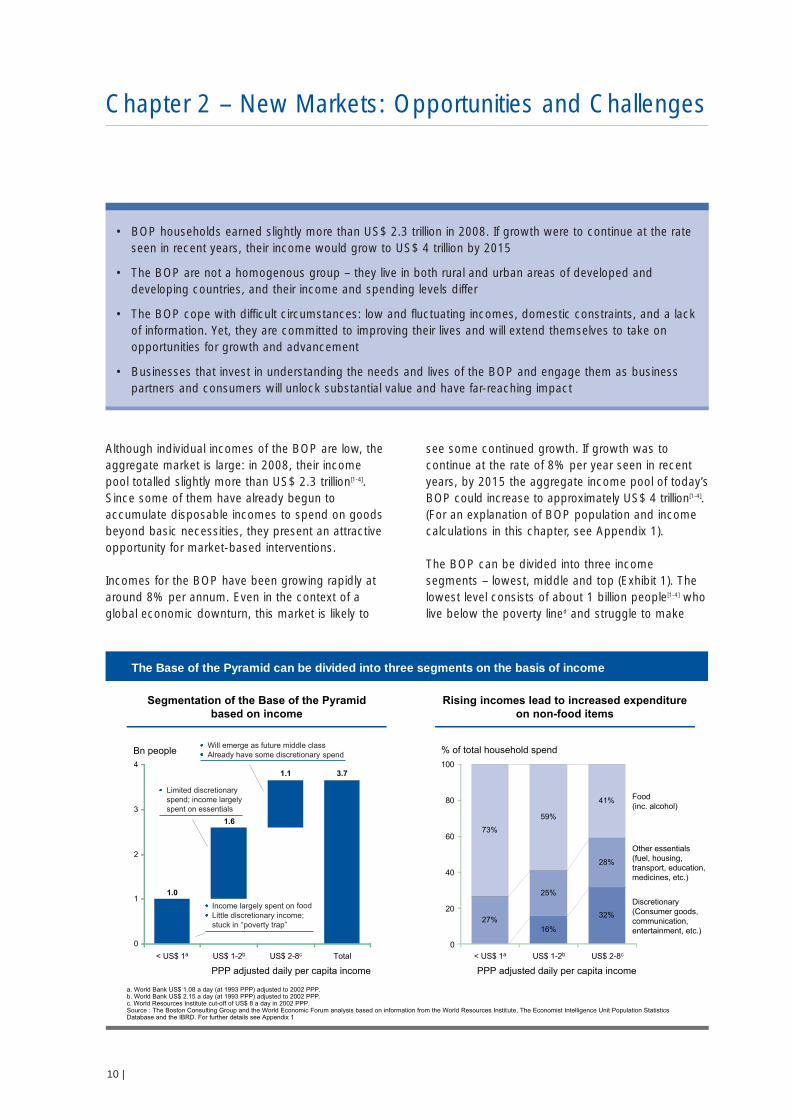

Although individual incomes of the BOP are low, theaggregate market is large: in 2008, their incomepool totalled slightly more than US$ 2.3 trillion[1-4].Since some of them have already begun toaccumulate disposable incomes to spend on goodsbeyond basic necessities, they present an attractiveopportunity for market-based interventions.

Incomes for the BOP have been growing rapidly ataround 8% per annum. Even in the context of aglobal economic downturn, this market is likely to

see some continued growth. If growth was tocontinue at the rate of 8% per year seen in recentyears, by 2015 the aggregate income pool of today’sBOP could increase to approximately US$ 4 trillion[1-4].(For an explanation of BOP population and incomecalculations in this chapter, see Appendix 1).

The BOP can be divided into three incomesegments – lowest, middle and top (Exhibit 1). Thelowest level consists of about 1 billion people[1-4] wholive below the poverty lined and struggle to make

• BOP households earned slightly more than US$ 2.3 trillion in 2008. If growth were to continue at the rateseen in recent years, their income would grow to US$ 4 trillion by 2015

• The BOP are not a homogenous group – they live in both rural and urban areas of developed anddeveloping countries, and their income and spending levels differ

• The BOP cope with difficult circumstances: low and fluctuating incomes, domestic constraints, and a lackof information. Yet, they are committed to improving their lives and will extend themselves to take onopportunities for growth and advancement

• Businesses that invest in understanding the needs and lives of the BOP and engage them as businesspartners and consumers will unlock substantial value and have far-reaching impact

The Base of the Pyramid can be divided into three segments on the basis of income

Segmentation of the Base of the Pyramidbased on income

Segmentation of the Base of the Pyramidbased on income

Rising incomes lead to increased expenditureon non-food items

Rising incomes lead to increased expenditureon non-food items

16%

32%27%

25%

28%

73%

59%

41%

< US$ 1a US$ 1-2b US$ 2-8c

Food(inc. alcohol)

Other essentials(fuel, housing, transport, education,medicines, etc.)

Discretionary(Consumer goods,communication,entertainment, etc.)

PPP adjusted daily per capita income

0

100

20

40

60

80

% of total household spend

3.71.1

1.6

1.0

0

1

2

3

4

< US$ 1a US$ 1-2b US$ 2-8c

PPP adjusted daily per capita income

Bn people

Total

a. World Bank US$ 1.08 a day (at 1993 PPP) adjusted to 2002 PPP.b. World Bank US$ 2.15 a day (at 1993 PPP) adjusted to 2002 PPP.c. World Resources Institute cut-off of US$ 8 a day in 2002 PPP.Source : The Boston Consulting Group and the World Economic Forum analysis based on information from the World Resources Institute, The Economist Intelligence Unit Population StatisticsDatabase and the IBRD. For further details see Appendix 1

| 11

ends meet. The middle segment constitutes thelargest group, with approximately 1.6 billion people[1-4].Although they have little discretionary spendingpower, they are generally able to support their basicneeds and will require intervention only to improvethe level and consistency of their existing incomes.

The top segment – which comprises around 1.1billion people[1-4] – has sufficient disposable incometo purchase nonessential products, yet they receivelittle attention from most businesses, because theirincomes are still relatively low and tend to fluctuate.This group may be easiest to engage with, sincethey have surplus incomes and already spend ondiscretionary items. However, engaging the lower-income ranges of the BOP is also feasible andimportant. If businesses and organizations help toincrease capacity and income among all ranks of theBOP, they will foster broad-based growth throughoutthe market.

In many countries, women undertake most of thefarm labour, as well as food collection or purchasingand preparation. Yet, women often have less accessto information, credit and services than men do,which constrains their capacity as producers andconsumers. Companies could pay special attentionto women as an underserved segment and addresstheir needs, preferences and constraints in thedesign of products and services. For example,micro-farm equipment can be designed to beaffordable and require less intense manual labour,and food products can be targeted to householdnutritional needs. Since women reinvest most oftheir income into the family, they are a powerfulavenue for value creation at the household andcommunity level 5. Companies that recognize andinvest in this opportunity could help strengthencommunity-level productivity and enhance long-termmarket growth.

Where do the BOP live?

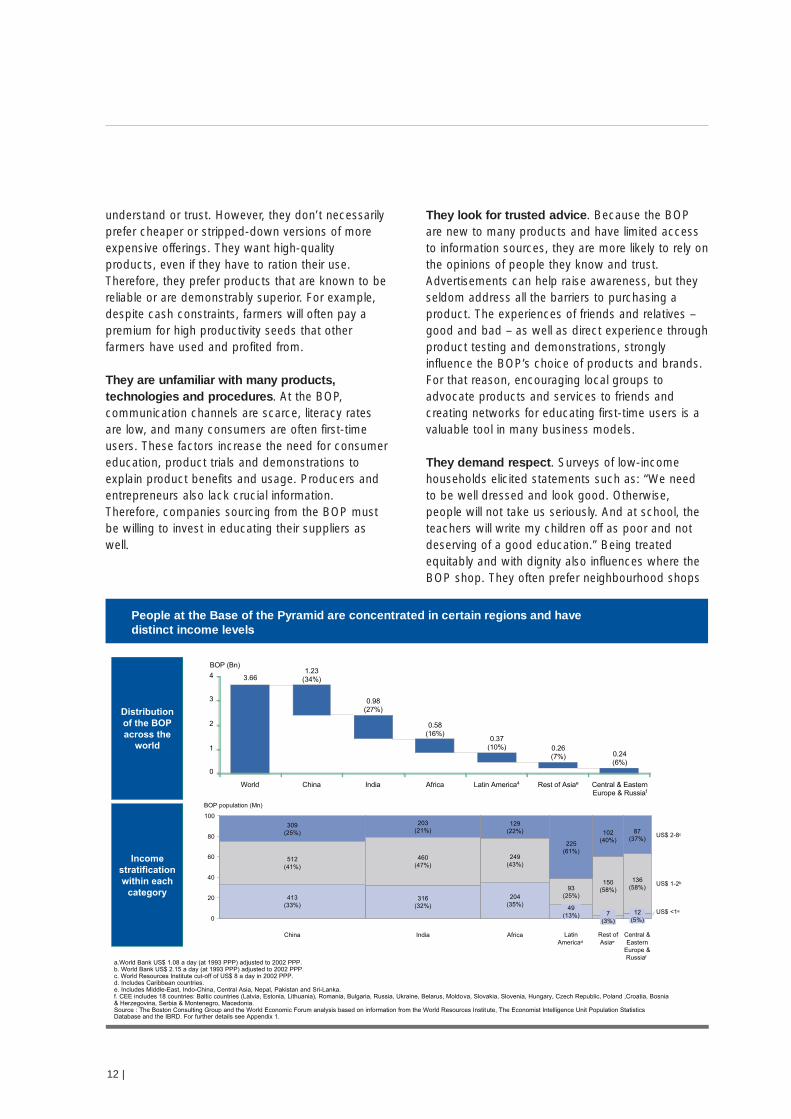

People living at the BOP can be found all over theworld, yet they are particularly concentrated in a fewareas. India and China alone account for 60%. Asia,Africa and Latin America together account for 94%of the total BOP population[1-4]. Africa has the highestshare of the poorest segment – only 65% of Africa’sBOP population is above the World Bank’s US$ 1 aday poverty line, compared with more than 86% inLatin America (Exhibit 2). The majority of the BOPlive in rural areas (68% globally)[2], which adds to thecomplexity and costs of reaching them.

Some salient characteristicsAlthough it is difficult to generalize about a group asvaried as the BOP, it is important to understand thecharacteristics that distinguish them from other groups.

They manage low and fluctuating incomes. Theburden of low incomes is compounded by the factthat income streams for BOP households areunpredictable. As customers, therefore, they resistlarge up-front outlays and recurring expenses in theform of instalments. In addition, most lack access toaffordable credit which would enable essentialpurchases or business investments. Therefore,companies might look for ways to align their pricesand financing for consumers with incomes that ebband flow. They might also design financial incentivesthat provide a stable income and encourageentrepreneurship when engaging with the BOP asproducers.

They cope with domestic constraints anddifficult living conditions. The living spaces of BOPhouseholds are typically quite small. Furthermore,conveniences that more affluent households take forgranted – such as uninterrupted electricity and cleanrunning water – have yet to reach many BOPhouseholds. These conditions impose constraints onboth the type of products that the BOP can produceand consume and their level of productivity.Companies engaging with the poor could strive todeliver business and product solutions that addressthese constraints.

They are smart shoppers and investors. Sinceevery cent counts for low-income households, theyare unlikely to spend money on products they don’t

d World Bank US$ 1.08 a day poverty line in 1993 PPP,which translates into US$1. 34 in 2002 PPP.

understand or trust. However, they don’t necessarilyprefer cheaper or stripped-down versions of moreexpensive offerings. They want high-qualityproducts, even if they have to ration their use.Therefore, they prefer products that are known to bereliable or are demonstrably superior. For example,despite cash constraints, farmers will often pay apremium for high productivity seeds that otherfarmers have used and profited from.

They are unfamiliar with many products,technologies and procedures. At the BOP,communication channels are scarce, literacy ratesare low, and many consumers are often first-timeusers. These factors increase the need for consumereducation, product trials and demonstrations toexplain product benefits and usage. Producers andentrepreneurs also lack crucial information.Therefore, companies sourcing from the BOP mustbe willing to invest in educating their suppliers aswell.

They look for trusted advice. Because the BOPare new to many products and have limited accessto information sources, they are more likely to rely onthe opinions of people they know and trust.Advertisements can help raise awareness, but theyseldom address all the barriers to purchasing aproduct. The experiences of friends and relatives –good and bad – as well as direct experience throughproduct testing and demonstrations, stronglyinfluence the BOP’s choice of products and brands.For that reason, encouraging local groups toadvocate products and services to friends andcreating networks for educating first-time users is avaluable tool in many business models.

They demand respect. Surveys of low-incomehouseholds elicited statements such as: “We needto be well dressed and look good. Otherwise,people will not take us seriously. And at school, theteachers will write my children off as poor and notdeserving of a good education.” Being treatedequitably and with dignity also influences where theBOP shop. They often prefer neighbourhood shops

12 |

People at the Base of the Pyramid are concentrated in certain regions and have distinct income levels

3.66

0

1

2

3

4

World

1.23(34%)

China

0.98(27%)

India

0.58(16%)

Africa

0.37(10%)

Latin America4

0.26(7%)

Rest of Asiae

0.24(6%)

Central & EasternEurope & Russiaf

BOP (Bn)

512(41%)

413(33%)

309(25%)

China

203(21%)

460(47%)

93(25%)

49(13%)

LatinAmericad

102(40%)

150(58%)

7(3%)

Rest ofAsiae

87(37%)

136(58%)

12(5%)

Central &Eastern

Europe &Russiaf

US$ 2-8c

US$ 1-2b

Africa

0

100

20

40

60

80

BOP population (Mn)

225(61%)

204(35%)

249(43%)

129(22%)

India

316(32%)

US$ <1a

Distributionof the BOPacross the

world

Incomestratificationwithin each

category

a.World Bank US$ 1.08 a day (at 1993 PPP) adjusted to 2002 PPP.b. World Bank US$ 2.15 a day (at 1993 PPP) adjusted to 2002 PPP.c. World Resources Institute cut-off of US$ 8 a day in 2002 PPP.d. Includes Caribbean countries.e. Includes Middle-East, Indo-China, Central Asia, Nepal, Pakistan and Sri-Lanka.f. CEE includes 18 countries: Baltic countries (Latvia, Estonia, Lithuania), Romania, Bulgaria, Russia, Ukraine, Belarus, Moldova, Slovakia, Slovenia, Hungary, Czech Republic, Poland ,Croatia, Bosnia& Herzegovina, Serbia & Montenegro, Macedonia.Source : The Boston Consulting Group and the World Economic Forum analysis based on information from the World Resources Institute, The Economist Intelligence Unit Population StatisticsDatabase and the IBRD. For further details see Appendix 1.

– which are familiar and offer personalized service –over supermarkets, which may require more traveltime and seem intimidating. Companies shouldconsider such sensitivities and treat the BOP –whether as consumers or employees – with respect.

They face disadvantages in the market. BecauseBOP consumers’ spending power is limited, and thecosts to reach them are high, they tend to be servedby inefficient supply chains. That often results in theirpaying higher prices for inferior goods, compared towealthier members of their societies – an inequityoften referred to as the “BOP penalty”. This costdynamic presents a tremendous opportunity fororganizations and businesses to offer better qualityand more affordable options to the poor. Butrealizing that opportunity will require uprootingentrenched stereotypes and being open to newways of engaging with this segment.

| 13

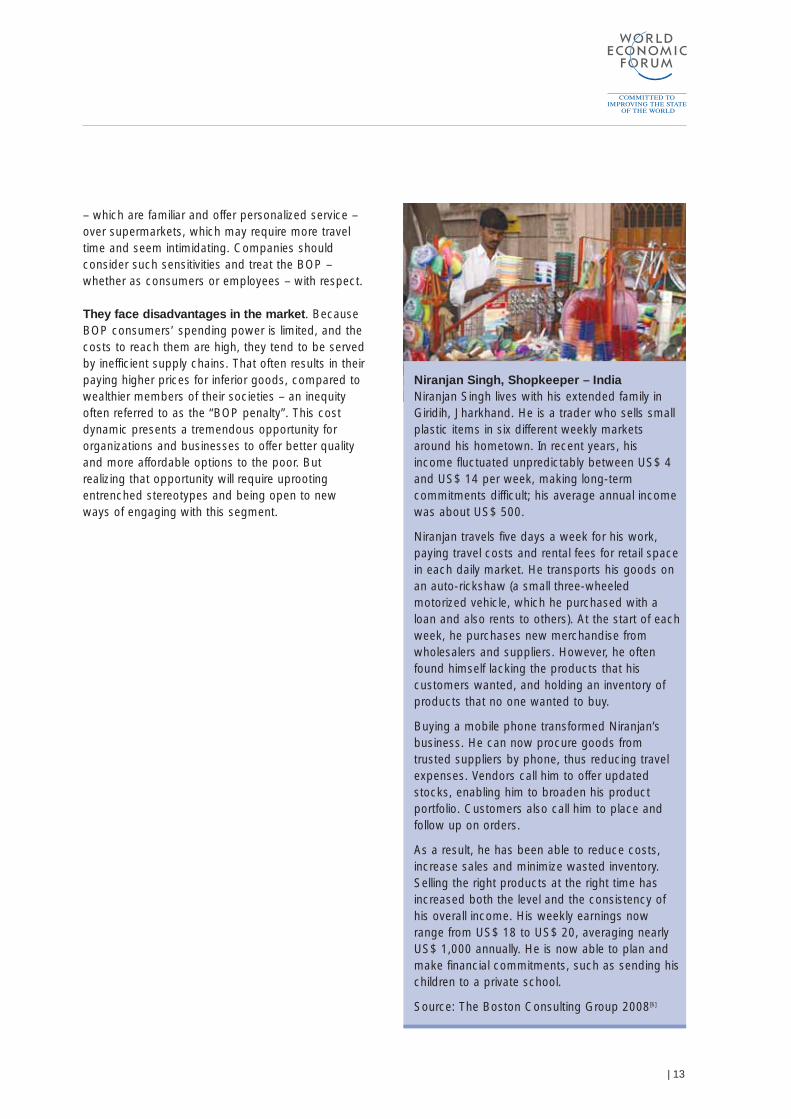

Niranjan Singh, Shopkeeper – India Niranjan Singh lives with his extended family inGiridih, Jharkhand. He is a trader who sells smallplastic items in six different weekly marketsaround his hometown. In recent years, hisincome fluctuated unpredictably between US$ 4and US$ 14 per week, making long-termcommitments difficult; his average annual incomewas about US$ 500.

Niranjan travels five days a week for his work,paying travel costs and rental fees for retail spacein each daily market. He transports his goods onan auto-rickshaw (a small three-wheeledmotorized vehicle, which he purchased with aloan and also rents to others). At the start of eachweek, he purchases new merchandise fromwholesalers and suppliers. However, he oftenfound himself lacking the products that hiscustomers wanted, and holding an inventory ofproducts that no one wanted to buy.

Buying a mobile phone transformed Niranjan’sbusiness. He can now procure goods fromtrusted suppliers by phone, thus reducing travelexpenses. Vendors call him to offer updatedstocks, enabling him to broaden his productportfolio. Customers also call him to place andfollow up on orders.

As a result, he has been able to reduce costs,increase sales and minimize wasted inventory.Selling the right products at the right time hasincreased both the level and the consistency ofhis overall income. His weekly earnings nowrange from US$ 18 to US$ 20, averaging nearlyUS$ 1,000 annually. He is now able to plan andmake financial commitments, such as sending hischildren to a private school.

Source: The Boston Consulting Group 2008[6]

The BOP have not been completely ignored. Somecompanies have made profitable forays into thismarket by adapting their offers, creating smallerpackages, or finding innovative ways to cut costsand prices. Yet, such efforts have only scratched thesurface of untapped opportunities in the BOPeconomy. The most successful companies havegone farther by rethinking stereotypes andfundamentally altering their business models on thebasis of deep insight into the lives of the BOP.

Much of the conventional wisdom about businessoperations in emerging economies stands in the wayof further growth and opportunity among the BOP.This chapter presents five ways of reframing theproblems that have challenged conventionalsolutions:

• Affording access rather than ownership• Monetizing hidden assets• Bridging the gap in public goods through private

enterprise • Scaling out versus scaling up• Governing through influence rather than authority

These new perspectives can help organizationstransform perceived problems into profitableopportunities for years to come. Not all of them willbe applicable in all cases. Organizations mustconsider where to apply them and how to achievethe best balance between conventional thinking andnew perspectives.

3.1 Affording Access Rather thanOwnership

A person doesn’t have to own a product in order tobenefit from it – he or she just has to use it. Yet,companies tend to measure a product’s marketpotential in terms of the number of people who canafford to buy it. Given the relatively low and volatileincomes of the BOP, this mindset severely restrictsthe perceived potential of these markets. Iforganizations think about “who can use the product”rather than “who can buy it,” they will find a muchlarger and potentially profitable opportunity.

Reframing this problem requires new kinds ofmetrics to measure market potential and affordability.What if companies were to measure “access” totheir products rather than ownership? Such accesscould be provided through a shared-usage model orthrough an entrepreneur who “leases” the product tocustomers. This way of thinking has opened upvaluable markets for a number of companies.

In Bangladesh, for example, Grameen Telecomequipped village women with mobile handsets and,for a small fee, the women make the handsetsavailable to others for both incoming and outgoingcalls. Over time, many of these customers havebought their own mobile handsets – often choosinga Grameen phone; since it is the brand they havebecome familiar with and have grown to trust. As a

Chapter 3 – New Perspectives: Challenging Deep-seated Beliefs

14 |

• Much of the conventional wisdom about business operations in emerging economies stands in the way offurther growth and opportunity among the BOP

• By adopting new perspectives, companies will be able to view the next billions through a prism ofopportunity

• Organizations will need to think about “who can use the product” rather than “who can buy it”; to unleash“hidden potential” in the form of undocumented capital and underutilized potential; to collaborate with thegovernment to bridge gaps in public goods; to balance scaling up (through centralization) with scaling out(through localization); and to actively align incentives to manage various alliances

• These new approaches can help organizations transform perceived problems into profitable opportunitiesfor years to come

result, the mobile phone sector in Bangladesh hasbeen growing rapidly: from only 200,000 subscribersin 2001 to more than 42 million at the end of May,2008. Nearly half of those 42 million subscribers useGrameen Phone. At the same time, numerouswomen have become entrepreneurs and improvedtheir incomes, thereby reducing poverty andexpanding opportunities. Other organizations aroundthe world have adopted and extended the Grameenshared-access model for mobile phone usage,including offering additional services[7]. The Celtelcase cited in Box 1 is one such example.

Kenya Agricultural Commodity Exchange (KACE)and Safaricom Ltd combined the shared-accessmodel with a new application that offers a valuableinformation service to farmers and traders. Theservice provides information on the prices of specificcommodities via SMS messages – by typing in“beans”, or “maize”, for example, to find the goingprice in the capital. As a result, farmers can accessvital pricing information to target their sales to thebest buyers, and improve their negotiating positionwith traders and middlemen. It costs only 15shillings (20 cents) per use, and the costs can beshared among the farmers[8].

To challenge conventional wisdom about productownership, consider the following questions:• “How can a company change from a “selling”

mode to one that “deploys” products for usewithout requiring ownership?

• How would this new approach affect itsrevenues?

• Does such an approach change how thecompany thinks about realizing further value fromexisting assets and customers?

• What new business models might this newapproach require?”

| 15

Emerging Rules for Success • Focus on the features that will have a high

impact on the livelihoods of the target market. • Design an offer that makes it possible for them

to access those features, even if it meansgoing beyond the boundaries of currentbusiness models

• Assess the economic viability at group orcommunity levels, rather than at an individualcustomer or producer level

• Construct an offer that benefits large groups ofconsumers or producers and permits poolingof revenue streams so that the company isprotected from an individual consumer’svolatile income

3.2 Monetizing Hidden Assets

There is a wealth of potential capital residing withinBOP communities, but these assets are oftenhidden from formal markets[10]. The term “assets”refers to a broad array of resources that cangenerate economic value. This includesundocumented capital, which is capital thatindividuals have used historically or traditionally, butfor which they do not have formal ownership rights.Undocumented capital could include property forwhich a family has tenancy rights but no legal title;or unincorporated businesses that aren’t funded bya bank or other traditional investors. The secondtype of capital is personal and community resourcesthat can be leveraged to enable businesstransactions, produce or sell goods. It includes thecollective power of a community, which is ofteninformally used for contract enforcement. Even agood personal reputation – a prized asset thatallows access to local credit – could be considereda source of capital. The third kind of capital is

underutilized assets, such as civil societyorganizations and small and medium enterprises(SMEs). Many of these entities already have strongnetworks within the community and a deepknowledge of where their untapped sources of valueare. It also includes people with entrepreneurial orother skills that have yet to be developed.

Leveraging the economic value of these hidden ass•ets can potentially unlock significant market growth.Indeed, the aggregate value of such capital ispotentially enormous. Consider the money thatMexican immigrants earn in the United States andsend back to families in Mexico through informalremittance channels, or the extraordinarily highinterest rates charged by village money lenders inIndia for low-income people with no access toformal credit. Companies should look beyond theofficial models to learn how local communities bringcapital into the system “unofficially”, and seek toleverage that capital to catalyse further valuecreation.

16 |

Celtel International is a leading pan-African mobilecommunications group, with operations in 15African countries. Celtel entered the DemocraticRepublic of Congo (DRC) market in 2000, revised itsbusiness models and adopted numerous changesto achieve commercial success. The key innovationwas enabling shared usage. Celtel encouraged theuse of family-shared handsets and handsetsmanaged by “Mamans GSM” (women who renthandsets for the price of airtime plus 100 or 500Congolese Francs (US$ 0.23-1.17), depending onthe region. The business provides an excellentlivelihood for Mamans GSM, contributing as muchas half of the household income, and it also bringsbenefits to the entire village through access tocommunication and information.

Celtel’s services have helped farmers and small-scale entrepreneurs to reduce the cost of travel, getinformation about the price of goods to buy and to

sell, and assess security and road conditions. It alsocreated jobs, trained local technicians and a salesforce and built a pool of professionals withinternational standards. As a result, families getinformation on basic health and education services.Celtel has attracted more than 2 million customersin DRC’s 25 provinces. Celtel earns more percustomer in the Congo than it does in moredeveloped markets, in part because of the lowpenetration of landlines (10,000 for a population of54.8 million in 2002) and mobile phones (10,000subscribers). Celtel offers a vivid example of howconstraints in infrastructure and security can be adriver of innovation rather than a barrier to doingbusiness.

Source: United Nations Development Programme,2008[9]

Box 1 – Celtel and Celplay, Democratic Republic of Congo: Giving Farmers and Entrepreneurs Vital Information

In fact, mobilizing the community is a good entrypoint for identifying hidden assets, since the BOPmaintain strong community ties. For that reason,companies have integrated local communityentrepreneurs into their value chains, in addition toserving them as customers. Not only does thisbroaden the customer base for these companies, itcan also generate higher profits, since the localentrepreneurs are willing to pay more for resourcesthey had no access to previously. Lastly, it removesmarket inefficiencies and thus creates an economicmultiplier. For example, Mibanco (Banco de laMicroempresa S.A.) in Peru has loaned more thanUS$ 1.6 billion in amounts ranging from US$ 100 toUS$ 1,500 to low-income households and theirmicro and small enterprises. Mibanco’s innovationwas to design special banking products to be usedfor the purposes of housing, agriculture, workingcapital, and other necessities. To ensure that theloans would be paid back, they instituted personalincentives, such as awards and public recognition.As a result, they were able to offer credit to peoplewho never had access to the formal banking systemin Peru[11].

Human resources, which include the large pools ofpeople who might become producers orentrepreneurs with adequate training, are anotherform of hidden assets. Yet, conventional methods ofdeveloping their skills and collecting the goods theyproduce in distant villages are expensive. Anotherdeterrent is the reluctance of many businesses toinvest in training when the benefits might be sharedby competitors. For example, companies often needraw materials from farmers in a particular region, butthey avoid sourcing from them because theproducts are often poor in quality. Although thecompany and the farmers would both benefit if thecompany would help to improve the quality ofproduce, the company is reluctant to make suchinvestments because it has no way of ensuring thatthe farmers won’t begin selling to other companiesas well.

Uncovering hidden community resources will requirecompanies to collaborate with other organizationsand possibly even competitors to share communityskills, knowledge and training. But the benefits ofgaining a more skilled, productive and accessibleworkforce often justify the effort and cost.

The potential for companies to unlock hidden assetsby collaborating with local communities andintegrating new models with their current ways ofdoing business is substantial. To challengeconventional wisdom about capital assets, considerthe following questions:• What hidden assets does the target community

have, and how does the community leverage theirvalue?

• How could the hidden capital that exists ininformal arrangements be brought into formalsystems?

| 17

Emerging Rules for Success • Tap local knowledge residing in informal

networks for sources of hidden assets in thecommunity

• Identify local partners with the best access tocommunity information

• Identify gaps in current roles, construct anoffer that bridges those gaps, and provideeconomically attractive incentives for partners

• Provide local producers with the expertise andtools they need to meet company standards

18 |

3.3 Bridging the Gap in Public Goodsthrough Private Enterprise

Developing nations face major infrastructure gaps.Organizations that set out to engage low-incomegroups as customers or producers are oftenconstrained by the lack of basic infrastructure theytake for granted when serving current massmarkets. This greatly increases the costs ofengaging with the poor, designing products forthem, and collaborating with them for the purposesof production and sourcing. The missinginfrastructure can include “hard” infrastructure, suchas roads, warehousing, logistics facilities and publicutilities for water and electricity.

It can also include “soft” infrastructure, such asproducer organizations, educational and trainingprogrammes, and basic information on consumers,including individual identification and credit historiesthat allow companies to target them for specificproducts and services.

Hard and soft infrastructures enable market activityand value creation, and they are largely consideredthe responsibility of the public sector (such asgovernments or development agencies). Organizationsthat seek to do business with the BOP overcome

infrastructure constraints in two ways: they can formactive partnerships with the public sector to improvethe circumstance of the BOP, or they can findinnovative ways – often in collaboration with others –to bridge the gap in public goods.

Consider the example of Pésinet Health Care, whichfunded an innovative initiative to reduce infant mortalityin Mali. Instead of setting up clinics in rural locations,the company trained qualified local representativesto perform basic check-ups and communicate theinformation electronically to doctors in the cities.Patients visited doctors only when they neededhands-on attention. That made the service moreaffordable for patients and helped to reduce thecountry’s infant mortality rate. For the programme tobecome self-financing, the company needed to achieveeconomies of scale that required treating 1,200 to1,500 children. The costs of the project were recoveredby revenues generated by subscription charges,which were US$ 1.05 a month per child andincluded visits to the doctor and basic medicines. Ina similar project rolled out in Saint-Louis, Senegal,the infant mortality rate fell from 120 per thousand toonly 8 per thousand. The new model has madebasic healthcare more accessible to low-incomepeople and, because it generates sufficient revenuesin subscriptions, its operations are sustainable[13], [14].

The majority of Ghanaians, especially the poor, donot have access to banks, credit unions or similarfinancial institutions. However, the need for bothsavings and access to credit is most urgent amongthis section of the population. Indeed, the situationhas led many people, including small enterprisesand traders, to turn to informal mechanisms suchas Susu collectors and moneylenders to meet theirfinancial needs. Susu, or daily deposit collection, isa traditional and informal financial institution in WestAfrica, and there are about 4,000 Susu collectors inGhana. As part of Barclays Microbanking, BarclaysBank Ghana is embarking on an unconventionalinitiative to connect modern finance with informalfinancial systems, such as Susu collection in Ghana.The business dimension for Barclays is centred on

creating value for money by helping the smalltraders focus and sharpen their financialmanagement skills. In the long run, the bankbenefits by encouraging more traders to appreciatethe habit of saving and, therefore, channel theirsavings to the bank through the Susu collectors.The provision of credit to the Susu collectors forpassing on as loans to the market women allowsthe small traders access to funds to invest in theirbusinesses. That helps to diversify and increasetheir sources of income. Barclays was thus able tobring Ghana’s informal financial systems into formalchannels.

Source: Harvard Corporate Social ResponsibilityInitiative, 2007[12]

Box 2 – Barclays Micro Banking, Ghana: Diversifying by Partnering with Susu Collectors

Another obstacle companies face is a lack ofinformation about the choices and constraints in thedaily lives of the BOP. Indeed, some companies evenfind it difficult to identify which groups of consumersbelong to this segment. Government data is ofteninaccurate or nonexistent, and many workers lackofficial salary records. This can be a particularchallenge for banks. By insisting on official records,banks lose not only potential customers, but alsothe opportunity to catalyse growth and reducepoverty by providing essential financial services.

Organizations could work towards improving financialinformation systems through tools such as creditbureaus and smart cards. Better, more accurate waysof identifying low-income consumers and determiningtheir qualifications and needs could be achievedthrough a consortium of companies that stand tobenefit from this effort, rather than a stand-aloneorganization. For example, A Little World, a technologycompany based in Mumbai, India, launched a projectin which a consortium of six banks providebiometrics-based identification cards and RFIDsmart cards and near-field-communication mobilephones to people without bank accounts. Not onlyhas the consortium made it possible to offer bankingservices without the expense of building branches, ithas also built some invaluable soft infrastructure inthe form of credit information that can be used bymany other industries over time to accurately identifyand track their customers. That allows companies toexpand their boundaries and partner with companiesin other industries to share investments and returns[15].

Private intervention can support the creation of publicgoods – not just for philanthropic reasons, but alsoto ensure long-term profitability in low-income markets.Interventions in the public domain by many companiesaround the world have demonstrated that they canadd value for customers as well as producers. Tochallenge conventional wisdom about investing inpublic goods, consider the following questions: • Will investing in a public good that also benefits

competitors actually improve near-term profits?• Who will decide how much each partner will gain

from opportunities and how much each could invest? • How can the organization create an open

partnership model to facilitate entry and exit ofpartners over time?

3.4 Scaling Out versus Scaling Up

To serve customers efficiently, companies often workto reduce the unit costs of products and achieveeconomies of scale through centralized productionin large factories. But this model has two problemswhen it comes to the low-income market. First, itincreases the costs of serving and sourcing(warehousing and distribution) since producers andcustomers live far from central factories. Second,centralized factories often produce standardizedproducts for global or regional markets, which isoften not what low-income consumers need orwant. The BOP’s requirements for locally-targetedproducts often cannot be met with standard low-cost production models. Companies therefore needto rethink strategies or scaling in this market.

What’s more, companies often attach hierarchicalstructure to large-scale operations. As they seek to“scale up” an innovation, they standardize structuresin the forms of decision rules, measurement

| 19

Emerging Rules for Success • Invest in both hard and soft infrastructure as

needed to execute the new business model. • Consider partnering with competitors and

players in other industries and government• Consider the cost of bridging infrastructure

gaps as part of an overall capital expense andvalue the investment according to its life-timeworth, rather than its immediate returns

• Be open and willing to explore a variety of“unconventional” revenue streams, but bring inpartners rather than doing it alone

systems, and organizational models. While thesecan boost efficiency in large-scale standardizedmarkets, they can also limit innovation – a keyquality for success in diversified BOP markets.Companies should instead seek to replicateinnovation, constantly adapting it along the way, inorder to expand their market and offer a newpathway to growth.

One of the problems with large-scale sourcing andproduction schemes is that they are designed forhigh-density areas. The traditional concept ofeconomies of scale often fails when it comes toserving the low-income markets. Although demandand supply in this market is potentially very large inthe aggregate, these consumers buy and sell locallybecause they live primarily in small, scatteredgroups. The alternative to scaling up is to scale out:create experiments that can be adapted and rolledout to increasing numbers of markets. That involvesthe low-income people as producers anddistributors, as well as consumers, and it minimizesoverhead.

Yet, scaling up and scaling out are not mutuallyexclusive. Instead, organizations need to balancescaling up (through centralization) with scaling out(through localization) to achieve the rightcombination of low costs and customized solutions.To accomplish this, organizations could deconstructtheir value chains and for each step consider thetrade-off between centralization and localization. The

resulting model could reduce costs and enhancecustomer appeal, reach, and credibility.

Aravind Eye Care in India exemplifies such a modelin using metrics in initial examinations to triagepatient needs. Its staff of local entrepreneursexamines patients at low-cost community centres,which are located in remote towns and villages.Basic examination, screening and preliminarydiagnostic procedures can be carried out by theseentrepreneurs with minimum training. Casesrequiring consultation with an expert are dealt withby e-mailing patient-exam reports to doctors incities. These doctors are highly trained and form acostly resource in the treatment chain. Only patientsthat need hands-on treatment are referred on toselect hospitals. Each small community centre isself-sustaining, because it uses local resources andinexpensive basic instruments. The organization hasgrown by leaps and bounds and that has givenmany more people access to good eye-careservices. It has also made Aravind a huge success.A recent study conducted by a hospital showed thatafter treatment, 85% of the men and 58% of thewomen who had lost their jobs due to sightimpairment were reintegrated into the workforce[16].Rethinking business models can create considerablebenefits not only for companies, but also forindividuals. By starting with a few trials, thenreplicating the innovation and adapting it along theway, companies can eventually reach marketssufficiently large to ensure profits.

20 |

The lack of organized supply chains in India resultsin extremely low price realizations for individualweavers and artisans. Fabindia started as awholesale export company in 1960 and has sinceestablished itself as a major player in the Indianretail market, with 17 community-owned companiesas its associate companies. These companies havetheir own warehouses, contributing to the efficiencyof Fabindia's supply chain. Their principal buyer isFabindia, which positions itself as an ethnic-chicstore for a variety of products, particularly garments.Fabindia focuses on retail, wholesale exports, andinstitutional sales to corporations, resorts and

hotels. Fabindia had US$ 80 million in sales in 2007and plans to establish growth to 250 stores over thenext four years. Artisans Micro Finance Pvt Ltdowns 49% of Fabindia, while 20,000 artisanshareholders own 26%, with private investors andemployees making up the final 25%. As acommunity-owned company, the value of theartisans’ shares increase as the company’s stockrises. Some artisans have doubled their share value,which they can use as collateral for loans.

Source: Word Press, 2008[19]

Box 3 – Fabindia, India: Bringing Customers to Indian Artists and Indian Arts and Crafts to the World

In traditional large-scale production models, everythingfrom procurement to production, processing,packaging and marketing is standardized. That worksefficiently when companies can use establishedchannels for supply and sourcing, and they aretargeting middle- and high-income consumers.However, production costs increase when demandis broadly dispersed and volumes vary, as is the caseat the BOP. In these settings, localized productioncentres can be a more effective approach. TheFrench company Nutriset S.A., which manufacturesPlumpy’Nut, a fortified food for extremelymalnourished children, has adopted such a strategy.The company sought to lower manufacturing anddelivery costs, allow flexible production schedules,and maintain high quality standards by introducing atailored licensing system. It outsources production tolocal franchisees, some of which operate as mini-manufacturing units, in Malawi, Niger, Ethiopia and theDemocratic Republic of Congo, and plans expansionto other regions. Nutriset works intensively withfranchisees on quality control and monitoring. Thismakes it possible for local production to significantlyreduce delivery costs, while creating jobs andcapacity[17].

Although the pursuit of economies of scale has beena central tenet of conventional business models for along time, the means to achieve it are different forBOP markets, where scale is often betterunderstood and evaluated at the micro, rather thanthe macro, level. To challenge the conventionalwisdom of economies of scale, consider thefollowing questions:• Where should the company scale up and where

should it scale out? • Can the company balance both kinds of scale

simultaneously? • How will the company adopt a decentralized

system, encourage innovation, and still ensureproduct quality and effective management?

3.5 Governing through InfluenceRather than Authority

As companies grow, the natural inclination is to exertmore control on decision-making and tightenmonitoring and audit systems. Yet, at the BOP,information gathering and control has to happenthrough collaboration and with local partners. Giventhe wide dispersion of villages and communities inemerging marketse, it is crucial to retain a high degreeof flexibility and decentralization, in order to adapt tolocal changes and control costs. To reduce theoverall costs of monitoring when enlisting the BOPas consumers and co-producers, companies mustfirst align their goals with the community’s interestsand then introduce local checkpoints. Organizationsthat have managed to link their interests to those oftheir local partners have found that they can delivermore value at significantly lower cost. This is alsotrue for partnerships with different organizations.

| 21

Emerging Rules for Success • Design products and processes for micro

markets and evaluate them accordingly• Leverage what has been learned from other

local initiatives rather than create over-archingstructures for monitoring. Maintaindecentralized governance and implementation

e For the purposes of this report, an emerging market is onewhose social and business activities are in the process ofindustrialization.

When considering doing business with BOPcommunities, companies are often concerned aboutthe substantial monitoring costs that might berequired to ensure compliance with qualitystandards. A better approach is to reduce the needfor monitoring by aligning the interests of theemployees with those of the company so thatemployees are motivated to deliver better results.This can be achieved by developing sharedaspirations and values, leveraging incentives such asprofits so that employees benefit when theorganization benefits. In order for this to work,however, companies will need to rethink theirbusiness models and current shareholders will needto relinquish some rights in exchange for broadeningthe range of benefits.

One organization that has succeeded with such apartnership approach is Child and Family WellnessShops in Kenya. They have adopted a franchisemodel to deliver healthcare, and offered the nurseswho run their local clinics shares in the company.That motivates the nurse-owners to provide highquality healthcare and reach out to the communitywith information and education. Not only hasproviding nurses with better remuneration improvedhealth in the community, it has also helped to retain

local talent, which addresses the problem of “braindrain” – the outmigration of skilled professionals –that affects many developing countries[20].

Even after aligning with the interests of local partners,companies will still need to ensure that standards,payments and other requirements are met. Somecompanies appoint an “aggregator”, who serves as apoint of contact for accountability and fee collectionfrom the community. For instance, rather than tryingto collect money from individual customers in avillage for using its services, a company couldconsolidate payments using a commission-basedlocal entrepreneur who collects payments fromindividuals, thereby reducing the collection costs forthe company and ensuring timely payments.

Some companies partner with communities for thepurposes of governance. That’s what the ManilaWater Company Inc. did when it established acommunity-based collection programme for waterconsumption. To assess and collect fees, it installeda “mother” meter for the whole community, whichwas responsible for jointly paying the bill. Thecommunity now employs local checkers to ensureindividual payment, which saves the company fromhaving to employ additional resources. As a result,the programme has become a source of localemployment, generating more than 10,000 jobssince it started operations in 1997[21].

Besides working with local players, businesses canpartner with other organizations to create and shareassets. But these organizations should be viewedmore as a network of peers, rather than vendors.One of the main challenges with such arrangementsis the establishment of clear governance standards.Often partnerships have broken down because thepartners didn’t share common goals. Even whenaspirations and values are shared, the partnershipmust still create an open architecture for organizationsto enter and exit on the basis of their capacity tooperate in the market. For example, if there is anarrangement among financial sector companies tocreate a common customer-credit database, each ofthe players ought to be able to contribute andbenefit. There should be clear guidelines for howvarious organizations will participate and how theircontribution will be valued, if they choose to exit.

22 |

There is authoritative power in the social forces thatbind communities together, and the key to successamong the BOP is to tap into it. Companies thathave aligned the interests of communities, and thenallowed individuals and other partner organizationsto manage them, have unlocked great potential,while reducing the overhead costs of monitoring. The key to making partnerships work lies in aligning

the interests of all stakeholders towards a commongoal. That calls for viewing community members aspartners, not just salaried employees. To ensurequality control, companies can engage managers atthe community level and design incentives for thecommunities to manage themselves. To challengeconventional wisdom about governance, considerthe following questions: • What partners – with whom the company might

share responsibilities and profits – can help itachieve its goals? Will the organization be willingto relinquish its power in order to lowermonitoring costs?

• How can the company align incentives toreinforce accountability and trust with thecommunity?

• How can the company establish cleargovernance standards and an open architecturewhere partners can enter and exit freely?

• How will the company value their contributionsdespite its focus on long-term profits?

| 23

Emerging Rules for Success • Align incentives to create “natural” monitoring

mechanisms and structure the programme sothat there is a clear economic benefit for thebusiness partners to follow agreed-uponguidelines

• Create entrepreneurs rather than employeesand provide flexibility and a high degree ofautonomy in decision-making

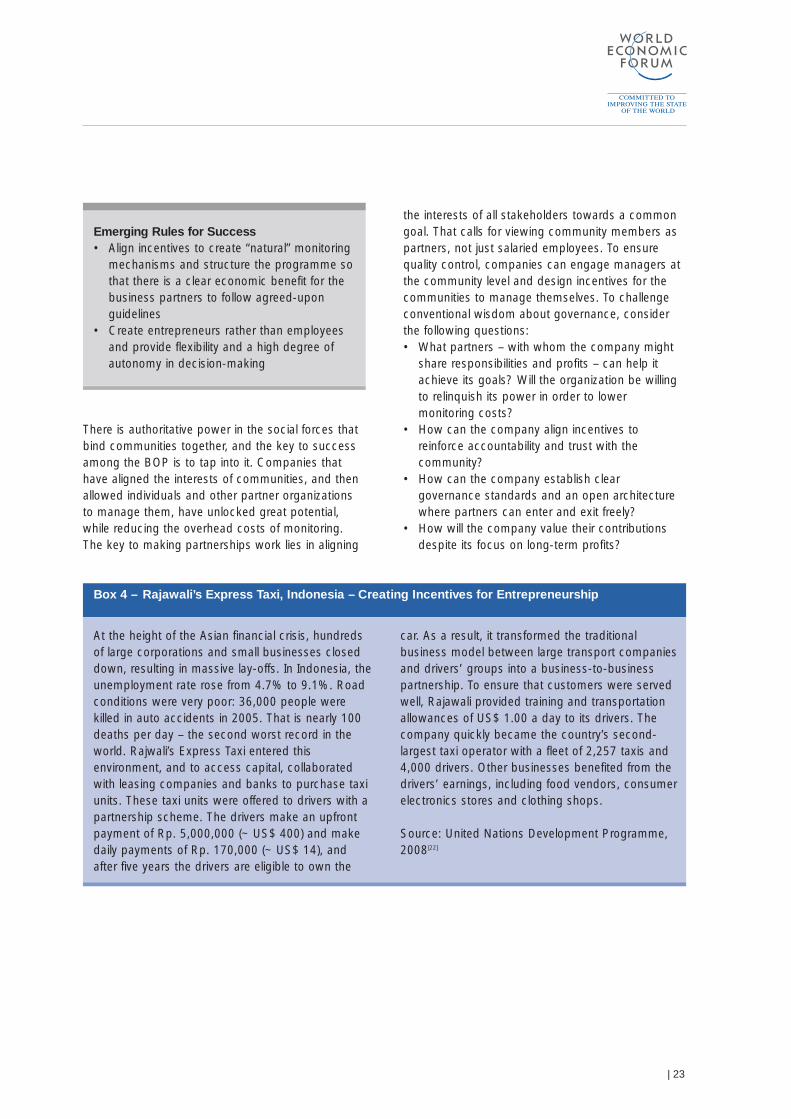

At the height of the Asian financial crisis, hundredsof large corporations and small businesses closeddown, resulting in massive lay-offs. In Indonesia, theunemployment rate rose from 4.7% to 9.1%. Roadconditions were very poor: 36,000 people werekilled in auto accidents in 2005. That is nearly 100deaths per day – the second worst record in theworld. Rajwali’s Express Taxi entered thisenvironment, and to access capital, collaboratedwith leasing companies and banks to purchase taxiunits. These taxi units were offered to drivers with apartnership scheme. The drivers make an upfrontpayment of Rp. 5,000,000 (~ US$ 400) and makedaily payments of Rp. 170,000 (~ US$ 14), andafter five years the drivers are eligible to own the

car. As a result, it transformed the traditionalbusiness model between large transport companiesand drivers’ groups into a business-to-businesspartnership. To ensure that customers were servedwell, Rajawali provided training and transportationallowances of US$ 1.00 a day to its drivers. Thecompany quickly became the country’s second-largest taxi operator with a fleet of 2,257 taxis and4,000 drivers. Other businesses benefited from thedrivers’ earnings, including food vendors, consumerelectronics stores and clothing shops.

Source: United Nations Development Programme,2008[22]

Box 4 – Rajawali’s Express Taxi, Indonesia – Creating Incentives for Entrepreneurship

The BOP often find themselves having to makedifficult compromises: their incomes are limited, yetthey desire products and services that are suited totheir needs; they require information, yet they havedifficulty accessing it; they live in scattered townsand rural villages, yet they must deliver their waresto distant markets. Companies first need to invest indeveloping a comprehensive understanding of theBOP and the constraints they face. The next step isto create new business models that break thesecompromises and give low-income people asustainable foothold in a market that allows them tothrive.

This chapter addresses what it will take to convertthe BOP into the next billions. It presents a set ofdesign principles for developing new businessmodels that are based on an analysis of more than200 case studies and numerous discussions withcompanies planning on or currently engaging withthe next billions as consumers, producers orentrepreneurs. The design principles are structuredalong four parts of a typical business model: productinnovation, supply chains, marketing andpartnerships. They apply specifically to thecircumstances of the next billions and togetherpresent a framework for innovation. The fiveprinciples, seen in Exhibit 3, are: 1. Create life-enhancing offerings2. Reconfigure the product supply chain 3. Educate through marketing and communication4. Collaborate to form non-traditional partnerships5. Unshackle the organization.

The chapter concludes with a discussion of howcompanies can help new business models succeedby unshackling the organization. It should be noted,

however, that these principles are given assuggestions rather than prescriptive solutions. Thereis no silver bullet in this market. Organizations willneed to be prepared to consider many kinds ofinnovations on several fronts.

4.1 Create Life-enhancing Offerings

Life-enhancing means offering products and servicesthat improve livelihoods and trigger the economicmultipliers that allow the next billions to overcometheir constraints. Rather than offer the sameproducts they sell in the mass markets of developedeconomies, companies need to adapt their productsand prices to the specific needs of the next billions.

Chapter 4 – New Approaches: Design Principles for Success

24 |

• Companies will need to innovate their business models targeted to the BOP to unlock their potential as the“next billions” who can be engaged by business

• Companies need to redesign their offers, their product supply chain arrangements and their marketing andcommunication to profitably engage with the next billions

• Collaboration with other companies, government, civil society organizations and especially poorcommunities themselves is critical to improve economics, enhance offers and fill gaps

Framework for innovation: Design principles for success

Unshackledorganization

Educationalmarketing andcommunication

Reconfigured

product supply

chainsLife

-enh

anci

ng

offe

rings

Creativecollaboration

A farmer in a rural area, for example, may want arugged mobile handset with a data feed thatprovides wholesale prices at nearby markets,whereas a day labourer in a city may care moreabout how the handset looks and feels and its abilityto take pictures. Therefore, mobile operators andhandset manufacturers need to design products andservices that deliver both aspirational and pragmaticvalue. Research suggests the following practicalguidelines:

Price for the budgets of the next billions.Because the next billions have low incomes and littlesavings, large up-front purchases are often out oftheir reach. For many products, pricing will involvesome consideration of credit terms. Producers andretailers of large-ticket items, such as durablegoods, for example, could offer financing tailored tothe next billions’ budgets in order to increase sales.Service providers, such as mobile operators, could“fit the pocket” of consumers by lowering rechargeamounts, offering flexible terms, and encouragingfree or low-cost trial use.

One of the best ways to make products available isto offer less expensive and smaller packages. Forexample, a BOP customer may need a small loanfor a one-time purchase of inputs for a businessoperation or for an emergency. Yet, manyinstitutionalized credit offerings are expensive andavailable only for large amounts. With a minimalinvestment in restructuring, a financial institutionmight offer small-size loans with flexible repaymentterms. Since families tend to pool their funds forexpensive purchases, certain products shouldappeal to all family members. One possibility wouldbe prepaid family plans for mobile handsets becausefamily members tend to share them.

Tailor products to address local constraintsand emphasize quality. Developing low-costproducts shouldn’t mean sacrificing quality. In fact,because the BOP can’t afford products that breakdown, they will often pay a premium for quality theycan trust – even if they have to use credit or tradedown to less expensive products in othercategories. Some companies have demonstratedsuccessful examples of assuring quality for locallytailored products and in turn earning the loyalty ofthe consumers. Take the example of InternationalDevelopment Enterprises India (IDE India) which is a

| 25

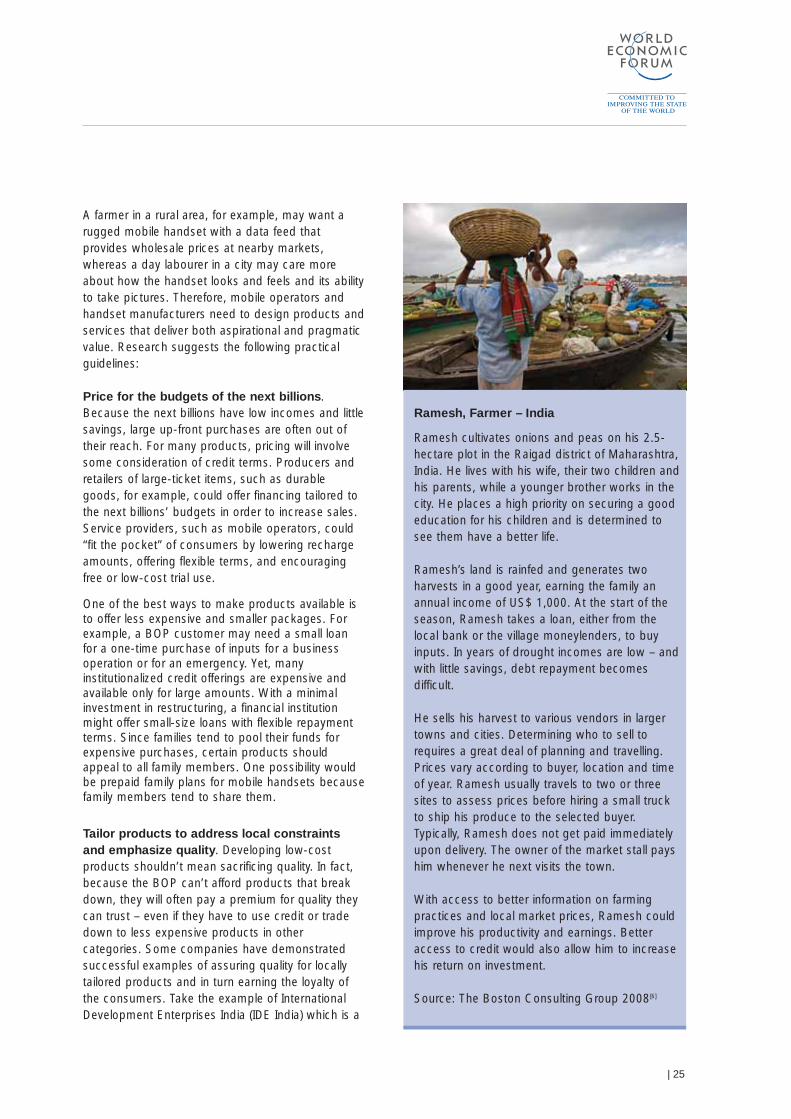

Ramesh, Farmer – India

Ramesh cultivates onions and peas on his 2.5-hectare plot in the Raigad district of Maharashtra,India. He lives with his wife, their two children andhis parents, while a younger brother works in thecity. He places a high priority on securing a goodeducation for his children and is determined tosee them have a better life.

Ramesh’s land is rainfed and generates twoharvests in a good year, earning the family anannual income of US$ 1,000. At the start of theseason, Ramesh takes a loan, either from thelocal bank or the village moneylenders, to buyinputs. In years of drought incomes are low – andwith little savings, debt repayment becomesdifficult.

He sells his harvest to various vendors in largertowns and cities. Determining who to sell torequires a great deal of planning and travelling.Prices vary according to buyer, location and timeof year. Ramesh usually travels to two or threesites to assess prices before hiring a small truckto ship his produce to the selected buyer.Typically, Ramesh does not get paid immediatelyupon delivery. The owner of the market stall payshim whenever he next visits the town.

With access to better information on farmingpractices and local market prices, Ramesh couldimprove his productivity and earnings. Betteraccess to credit would also allow him to increasehis return on investment.

Source: The Boston Consulting Group 2008[6]

social enterprise that engages actively with small-scale farmers by supplying manually operatedtreadle pumps. As uninterrupted power supply israrely available to these small landholders, theycould not use electrical pumps. IDE India designedpumps which required no power supply and enabledfarmers to trade up from manual methods ofdrawing and transporting water to the treadlepumps. In order to keep retail prices low, productmanufacturing is outsourced to local manufacturers,who follow a stringent quality assurance programmeand participate in IDE India’s warranty scheme. Theenterprise has also facilitated partnerships in servicehubs that provide processing facilities and allow forintermediary sales of produce. This provided broad-based support to farmers and convinced them topay money for the product as its easy to use and ofhigh quality. IDE India has successfully helpedfarmers to increase their productivity and in manycases they have doubled their income, often withintwo years of purchase[23].

Develop environmentally sustainableapproaches. Raising the income and consumptionlevel of the BOP will place immense pressure onalready-stretched resources such as land, water,energy and ecosystems. Therefore companiesshould explore economically sustainable solutionsthat have a minimal impact on the environment.Products and services offered to low-incomepopulations should aim for innovative and eco-friendly methods of production and consumption.Goods marketed to the next billions should utilizepackaging that minimizes environmentally harmfulwastes. Farming techniques and inputs should bedeveloped to address environmental concerns whilealso enhancing farmers’ incomes.

4.2 Reconfigure the Product SupplyChain

Of the BOP, 68% reside in rural areas, wherephysical access – for both distribution and sourcing– is a challenge. Even in urban areas, distributionrequires a network of micro-traders. Companiesoften wrestle with tradeoffs between cost, coverageand control. Distribution networks need to reachdisparate neighbourhoods and villages, whileremaining viable at low volumes and prices.Manufacturers need to ensure that they haveadequate oversight of pricing, stocking, and servicethroughout the distribution chain to fulfil qualityrequirements. The following recommendations couldguide the design of effective distribution networks: