Embed Size (px)

Citation preview

Circulated By EmailVolume - IV | May 2020

Vadodara Branch of Western India Regional Council ofThe Institute of Chartered Accountants of India

The Institute of Chartered Accountants of India(Setup by an Act of Parliament)

Editorial Team

CA. Krunal Brahmbhatt 78748 11551Chairman

CA. Vinod Pahilwani 98980 78176Vice-Chairman

CA. Manoj Sahu 90990 94500Secretary

CA. Rikin Patel 88667 09509Treasurer

CA. Vishal Doshi 98240 59901Ex-officio

CA. Hitesh Agrawal 99980 28737IP - Chairman

CA. Rahul Agrawal 97233 10418Committee Member

CA. Dhruvik Parikh 99795 39966Committee Member

CA. Krunal Brahmbhatt CA. Dhruvik Parikh

CA. Nayan Kothari CA. Rahul Parikh

CA. Hitesh Thakkar CA. Rachit Sheth

CA. Chinmay Naik CA. Janki Gohil

CA. Sakshi Somani CA. Neel Shah

CA. Sahil Rao

Managing Committee

Contents

Friends presently we are in a phase of different than routine which will give usenormous experience of life and lets cheers this the way it is.

"Every great dream begins with a dreamer. Always remember, you have within youthe strength, the patience, and the passion to reach for the stars to change the world.

Our all chartered accountants are leader and born to contribute to the society now it’stime to take the lead in society by our profession and lets be the front runner in eachfield like research, politics making, contribution to society, economy etc.

Friends presently we are facing problem rather I can say it’s a disaster on earth.Presently what we are facing is something different that our generation never beenfelt or gone through such situation. There are many questions on intention behindthis .Whether it is manipulated /planned or unintentional act. Now whatever hasbeen happened was happened now it’s time to analyze impact of COVID-19 on Indianeconomy and how this disaster we can convert in to an opportunity. We shouldappreciate the efforts of our government and all political parties who are working forthe betterment of country as a one entity and we are lucky enough to have stalwartand most influential personality in this scenario on whom population of India relyupon and act upon . i.e our prime minister Shri Narendra Modi Ji .we are almostsuccessful to control corona situation in India because of joint effort of each civilian.This is the situation where we can find that lots of NGO, Police department, doctorsand volunteers are working on their toe to fight with this disaster. Friends I am surethat india will shine and come out with this disaster very soon. Now question is thatwhat should we do after COVID -19 effects?? Friends at this juncture doctors, police,system, NGO has been done with their responsibility and its time to take over chargeby professionals like Chartered Accountants, Cost accountants, Economist,company secretaries, Industrialist and different business association along witheconomic system of India. Now our think tank has to come out with how we canboost our economy and we can contribute to the country. Friends why this is theperfect time to take this initiative? History says that when there is disaster on country,each citizen is working for the humanity and for the country because emotionalsentiments and patriotism is at its pick point to work for the same goal. One of e.g forthis sentiments is that there is scenario in country is that all national companies/organization and NGOs of india came forward to support the nation and this is thebest time to convert this emotion into consumption of domestic product and useswadeshi but system has to ensure that product should be of such a quality that canbeat international quality. Standard of developed country is something different thendeveloping country now we need to change upscale standard of quality for ourcountry in each segment. Friends our country has empanel of opportunity tocompete with Chinese market which is ruling the global economy. modiji is havingvision to convert our economy from 1 trillion to 5 trillion and this is perfect time toconvert disaster into an opportunity by adapting Chinese model with improvisedstandard. There are various sectors that global market is dependent on china andnow its time to convert this situation of COVID -19 in favor of India and open suchavenues in India to capture global market but for that our system has to work jointlywith entrepreneur along with giving support to MSME sector to stabilize Indianeconomy with rapid growth.

Lets contribute to the nation.

Regards,

CA. Krunal BrahmbhattChairman

Chairman Communication Forthcoming Events 2Pg 0

Judicial Decisions on 0Pg 2Indirect Taxes

Time Limit for taking The ITC & Pg 03Ledger Restrictions - An Analysis

Financial Instruments Part-1 Pg 09

Covid-19 Corporate Governance Pg 13

Due Date Calendar Pg 14

Vadodara Branch of WIRC of ICAI

Volume - III April 2020

02

Branch Events

Day & Date : Saturday, 02.05.2020

Time : 05.00 pm to 07.00 pm

Fees : FEES: Rs. 50 + GST for ICAI Members

Payment link : http://www.baroda-icai.org/ ProgramDetails.aspx?ProgID=483

Webinar on Corporate Governance Jointly with FGI

Contributed by : CA Anirudh Sonpal.can be reached at [email protected]

Judicial Decisionson Indirect Taxes

concern may be having statutory dues. No right ofaudience is given in the resolution proceedings tothe operational creditors viz. the Central Govt. orthe State Govt. as the case may be.’

[Ultratech Nathdwara Cement Ltd (formerly BinaniCement Ltd) – Rajasthan HC]

II. INTERESTON DELAYED REFUND

The Honourable High Court refused to review itsearlier order wherein interest @ 9% was ordered tobe allowed on refund. The revenue authority hadfiled a review application on the ground that thestatute provides for interest @ 6% u/s 56 of theCGST Act,2017. The Honourable High Courtdismissed the civil review application filed by therevenue authorities.

[Saraf Natural Stone – Gujarat HC]

[Willowood Chemicals Pvt Ltd – Gujarat HC]

III. DETENTION OF GOODS & VEHICLE

3.1 When the vehicle was intercepted from the14.01.2020, the person in-charge of theconveyance was in fact carrying the requisitedocuments, which he was supposed to carry in thecourse of transportation of the goods. As regardsthe discrepancy found in the course of inspection,the only observation made by the authoritiesconcerned is that the valuation does not seem tohave been properly conducted. The HonourableHigh Court observed that ‘If at all if this, accordingto the respondents, is contrary to the law, theauthorities are supposed to draw an appropriateproceeding under the law;

the Inspecting Authorities for the allegeddiscrepancy could have only intimated theAssessing Authority for initiating appropriateproceedings. What is more relevant to take note ofis the fact that the details in the invoice bill as wellas in the e-way bill matched the products found inthe vehicle at the time of inspection except for theprice of sale.’ While allowing the petition, theHonourable High Court held that that undervaluation of a good in the invoice cannot be aground for detention of the goods and vehicle for aproceeding to be drawn under Section 129 of theCGST Act, 2017 read with Rule 138 of the CGSTRules, 2017

[K.P. Sugandh Ltd – Chhattisgarh HC]

3.2 The goods, being transported to a godown forexhibition purpose, were detained on the groundthat the godown could not have been registered asan additional place. The Petitioner had taken astand that the dispute of registration can be

Topic Speaker

Corporate Governance post COVID 19 VadodaraCA. Vishal Doshi,Followed by Q & A Session (5 mins)

Current Pandemic – Corporate Culture Mr. Bhagirat Merchant,& ShrimadBhagvad Gita Mumbai

Followed by Q & A Session (15 mins)

Woman Independent Director – MumbaiCA. Priti Savla,Opportunity and ChallengesFollowed by Q & A Session (5 mins)

I. DEMAND

Tax demands were raised against the petitioner forthe period before it took over a company in theproceedings under the Insolvency BankruptcyCode, 2016, which was also approved by the NCLT.The resolution plan approved had also factored thedues of excise duty and service tax that existed atthe relevant time. Despite the resolution planhaving attained finality and having been executed,the respondents herein have raised numerousdemands from the petitioner for the period fromApril 2012 to June 2017 and interest up to25.7.2017. Having made the full and final paymentas proposed by the resolution professional, thepetitioner addressed a letter dated 26.11.2018 tothe respondents informing them of the payment ofdues as admitted by the CIRP and reminded themthat all remaining claims and proceedings stoodextinguished in terms of the resolution plan. TheHonourable High Court quashed and struck downthe additional demands of the revenue authoritiesand observed that ‘once the offer of the resolutionapplicant is accepted and the resolution plan isapproved by the appropriate authority, the same isbinding on all concerned to whom the industry

Time : 05.00 to 05.25 pm

Time : 05.30 to 06.15 pm

Time : 06.30 to 06.55 pm

Vadodara Branch of WIRC of ICAI

Volume - III April 2020

03

decided by the adjudication officer and not by theofficer detaining the goods. While the HonourableHigh Court had granted extension for the hearing,the revenue authorities issued notices for demandof tax and penalty without hearing the assessee.While disposing the petition by granting anopportunity of personal haring and representation,the Honourable High Court also observed that ‘incases of this nature, elementary cannons of naturaljustice and fairness would require that the partyshould be personally heard by the decision makere i t h e r i n p e r s o n o r t h ro u g h a u t h o r i s e drepresentative/ counsel, if any, and thereafter aconsidered decision is taken thereon, instead ofdriving the affected party like the present petitionerhaving to approach this Court and then litigate thematter on account of violation of natural justice.’

[Ahnas Mohammed – Kerala HC]

IV. LEVY

The Appellant club was collecting membershipsubscription and admission fees from themembers to be expended for the meetings andother petty administrative expenses and wereparked in the Administration Account. TheAppellate AAR ruled that such contributions werenot liable to GST on the grounds that the appellantwas not carrying on any business and there was noinherent supply for any consideration since therewas no particular service or benefit to themembers, and on the ground of mutuality.

[Rotary Club of Mumbai Nariman Point –Maharashtra Appellate AAR]

Contributed by : CA. Abhay Desaican be reached at [email protected]

Time Limit for takingThe ITC & Ledger

Restrictions - An Analysis

1. The basic design of GST postulates that the inputtax credit (“ITC”) shall be seamlessly granted to theregistered businesses to avoid the cascadingeffect of tax and also to ensure that the entire taxburden is transparently transferred to the endconsumer. Said design also found mention in theStatement of Objects and Reasons accompaniedin the CGST Bill, 2017 when it was introduced in theParliament. Paragraph 4 of the said Statementspecifically records that the design of GST is toallow seamless transfer of ITC from one stage to

another in the chain of value addition which wouldalso incentivize tax compliance. Therefore I submitthat any restrictions imposed in curtailing the saidseamless flow of ITC would have to be looked atminutely and an interpretation favoring theobjective behind the implementation of GST shouldbe adopted. With these words in the present articlewe shall deal with two such restrictions about ITC.One (Sec. 16(4)) deals with t ime-relatedrestrictions and the other (Rule 86A) deals with theutilization related restrictions of the balanceavailable in the electronic credit ledger. It may benoted that the reference in the present article is ofthe provisions of the CGST Act, 2017 but the sameshall also be construed as a reference to the similarprovisions under the SGST Act(s), 2017 unlessstated otherwise.

Time-related restrictions u/s 16(4)

2. Before analyzing the provisions contained u/s16(4) of the CGST Act, 2017 it is worthwhile to firstreproduce the concerned provisions for readyreference:

“Sec. 16(4) A registered person shall not be entitledto take input tax credit in respect of any invoice ordebit note for supply of goods or services or bothafter the due date of furnishing of the return undersection 39 for the month of September following theend of financial year to which such invoice or invoicerelating to such debit note pertains or furnishing ofthe relevant annual return, whichever is earlier.”

3. Subsequently vide CGST (Second Removal ofDifficulties) Order, 2018 dated 31-12-2018following proviso has been added:

“Provided that the registered person shall be entitledto take input tax credit after the due date offurnishing of the return under section 39 for themonth of September, 2018 till the due date offurnishing of the return under the said section for themonth of March, 2019 in respect of any invoice orinvoice relating to such debit note for supply ofgoods or services or both made during the financialyear 2017-18, the details of which have beenuploaded by the supplier under sub-section (1) ofsection 37 till the due date for furnishing the detailsunder sub-section (1) of said section for the monthof March, 2019.”

4. A conjoint reading of the original provision alongwith the subsequently added proviso would providethat the registered person cannot take the ITC inrespect of an invoice or a debit note pertaining to aninvoice after the due date for furnishing the returnu/s 39 for September from the end of the FY towhich the invoice pertains or the filing of the annual

Vadodara Branch of WIRC of ICAI

Volume - III April 2020

04

return, whichever is earlier. However, as anexception for FY 2017-18, being the first year ofGST, proviso provides that ITC can be taken evenafter the normal cut-off date but till the due date forfurnishing the return for March 2019 provided thedetails of invoices related to the said ITC have beenuploaded by the concerned suppliers in GSTR – 1till the due date of filing GSTR – 1 for March 2019. Itmay also be noted that Sec. 16(4) also standsamended vide Finance Act, 2020 to the effect thatthe said restriction in respect of a debit note shallbe considered from the year in which such debitnote is issued and not the year in which the invoicerelating to such debit note was issued. However asthe said amendment is yet to be notified the sameis not discussed in the present article in detail.

5. Ordinarily a prudent registered person is expectedto take the ITC within the time restrictionscontained u/s 16(4) to avoid any litigation. In otherwords as an illustration ITC for the invoicepertaining to FY 2019-20 should be taken by theearliest of the two cut-off dates which will be20.10.2020 (i.e. due date for September GSTR –3B) as an annual return will be filed only after thesaid date.

6. Now the purpose of the present article is toexamine the contentions which one can make if theITC is sought to be taken after the above-stated cut-off date. We shall divide the contentions into twobroad categories. The first category shall deal withwhether such time-related restrictions can beimposed and the second category shall deal withthe stage of the entire process of taking the ITC atwhich the said restrictions will be applied. Beforediscussing the same please note that restrictionscontained u/s 16(4) do not apply to ITC of IGST paidon import of goods as the said restrictions onlycover ITC related to the tax in respect of theinvoice/debit note.

7. Now the first fundamental aspect deals withwhether such time-related restrictions can beimposed or not. In this regard fol lowingcontentions can be examined by the readers to saythat such time-related restrictions may not belegally valid:

I. It can be contended that Sec. 16(2) of the CGSTAct, 2017 starts with a non-obstante clause tothe effect that notwithstanding anythingcontained in the entire Sec. 16, a registeredperson shall be entitled to ITC if he satisfies thefour conditions given therein (viz. possessingr e q u i s i t e d o c u m e n t s , r e c e i p t o fgoods/services, tax paid by the supplier to the

Government and filing of the return by therecipient). Therefore I submit that as Sec. 16(2)starts with a non-obstante clause overriding allother provisions of Sec. 16 including Sec. 16(4)it can be contended that as long as all theconditions u/s 16(2) are satisfied which do nothave any time-related restrictions, ITC cannotbe restricted.

II. Despite the non-obstante clause in Sec. 16(2)one may contend that as the said provisiondeals with the entitlement of ITC whereas Sec.16(4) deals with the taking of the ITC, and asboth operate in separate domains they willcontinue to apply. In other words a registeredperson may be entitled to ITC u/s 16(2) on thesatisfaction of the four conditions but wouldnot be able to take the said ITC if he crosses thetime restrictions contained u/s 16(4). Now oneof the conditions for a registered person to beentitled to ITC u/s 16(2) is that he must havefurnished the return u/s 39. The process ofavailing the ITC, as we shall see later, happensin the records maintained under the law and thesaid amount is then credited in the electroniccredit ledger by way of the reflection of thesame in the return filed u/s 39. Therefore Isubmit that Sec. 16(2) not only provides for theconditions to become entitled to ITC but alsoprovides for the condition to get the availed ITCreflected in the electronic credit ledger by wayof filing of the return. Once the said propositionis found valid, given the non-obstante clause inSec. 16(2) overriding all other provisions of Sec.16, Sec. 16(4) cannot curtail the taking of thesaid already entitled ITC and validly reflected inthe electronic credit ledger.

III. The amendment in Rule 61(5) by categorizingGSTR – 3B as a return u/s 39 and therefore tosay that the restrictions contained u/s 16(4)shall apply must be seen in light of why the saidrestrictions have been provided and originallylinked the same with GSTR – 3 and not GSTR –3B. Rule 4(iv) of GST Settlement of FundsRules, 2017 provides that the GSTN must senda report of the ITC remaining unutilized (to beread as unavailed in the context) because ofrestrictions u/s 16(4) so that the said moneycan be apportioned between the Centre and theStates (same for unavailed CGST as well asSGST). Said report would be generated fromthe exact amount of ITC not availed whichwould have been available only in the GSTR – 1,2 & 3 system wherein a supplier would havereported a B2B transaction in GSTR – 1

Vadodara Branch of WIRC of ICAI

Volume - III April 2020

05

whereas the recipient would not have matchedthe same and intimated the ITC claim in theportal by filing GSTR – 2. In the GSTR – 3Bregime due to the absence of matching andhence not knowing the exact amount ofunavailed ITC, Sec. 17(2A) came to be insertedin the IGST Act, 2017 vide IGST (Amdt.) Act,2018 to provide for the ad hoc apportionmentof the monies lying in the IGST credit ledgers.Therefore I submit that the original reference toGSTR – 3 in Sec. 16(4) was based on the entiremechanism of matching and apportionment ofthe monies of the unavailed ITC. Now GSTR –3B being only a summary return (ref para 8.6.6.of the 17th GST Council Meeting Minutes)cannot take the place of GSTR – 3 for Sec. 16(4)given the above discussion. Hence it can becontended that a retrospective amendment inRule 61(5) to make GSTR – 3B a return u/s 39cannot be read while interpreting Sec. 16(4)and hence the last date to avail the ITC would bethe date of filing of the annual return. Thiswould also be in line with the principle that in anenvironment where periodically only summaryreturns in the form of GSTR 3B are to be filedwithout matching, last opportunity for availingthe ITC at the time of finalizing the annual returnworking especially when the unavailed ITCstands already reflected in GSTR 2A has to bepermitted.

IV. Without prejudice to the above contention, itmay be noted that GSTR – 3B initially was not areturn u/s 39. Time limits stipulated u/s 16(4)only applies in the context of a return u/s 39. It isonly by way of CGST (Sixth Amendment) Rules,2019 notified vide Notification No. 49/2019 –Central Tax dated 09.10.2019 that with aretrospective effect Rule 61(5) was amended toprovide that GSTR – 3B is a return u/s 39.Therefore we submit that the vested rightcreated before the date of the said amendmentto avail the ITC (wherein the restrictions werenot linked to GSTR – 3B but to GSTR -3 whichnow stands annulled) cannot be taken back.Support for the said proposition can be takenfrom the Hon’ble Supreme Court decisions inthe case of Dai Ichi Karkaria Ltd. 1999 (112)E.L.T. 353 (S.C.) and Eicher Motors Ltd. 1999(106) E.L.T. 3 (S.C.).

V. Consider a situation wherein a registeredperson intends to avail the ITC within thestipulated time frame but is prevented fromavailing the same as he does not havesufficient funds to pay the net liability in cash

and file the return. As per the current design ofthe GSTN portal, GSTR – 3B cannot be filed inwhich ITC has been reflected unless the net taxamount for the given tax period is also paid.This is contrary to the legal provisions as in Sec.39 merely links return filing due date with thepayment due date but nowhere provides thatthe return can be filed only after making thepayment. It is also a settled principle that lawmust excuse an impossible duty. Support canbe drawn from the decision of Hon’ble SupremeCourt in the case of Cochin State Power & LightCorporation Ltd. v. The State of Kerala AIR 1965SC 1688 wherein it has been held that “theperformance of this impossible duty must beexcused following the maxim, lex non cogitatead impossible (the law does not compel thedoing of impossibilities)". Therefore time-related restrictions cannot apply in suchsituations.

VI. It can also be contended that Article 300A of theConstitution provides that no person shall bedeprived of his property save by the authority oflaw. It has been held that the said authority oflaw needs to be reasonable (see K.T PlantationPvt. Ltd. Vs. State of Karnataka (2011) 9 SCC 1).As submitted above, GST is a destination-based value-added tax system wherein all theentities in the chain of transactions till the finaldestination are called to pay tax after adjustingthe ITC which is as good as the advance taxpaid. Hence ITC is a property of the concernedregistered person and the said property cannotbe denied by way of not allowing the creditmerely due to time-related procedurallimitations. This is more relevant especiallywhen the GST is a new law and enoughconfusion prevails in the mind of the taxpayeras well as the department (evident from AAR)coupled with the fact that already time hasbeen extended for FY 2017-18.

VII. The above contentions would equally applywhen it comes to claiming ITC based on self-invoice prepared u/s 31(3)(f) of the CGST Act,2017 in case of the tax payable under RCM forsupplies received from unregistered suppliers.This is because the entire mechanism ofproviding the time limits has been inserted toidentify the unavailed ITC reported in GSTR –1/2 but not claimed in GSTR – 2 (which is nowsuspended). Now for the reporting of the self-invoice the same was required to be done inGSTR – 2. In absence of the same, we cancontend that the mechanism of apportionment

Vadodara Branch of WIRC of ICAI

Volume - III April 2020

06

of revenue concerning unavailed ITC asenvisaged u/s 16(4) would fail even in thisscenario (moreover in case of RCM the tax ispaid by the same registered person whointends to avail the ITC and hence the questionof apportionment would not arise as opposedto forward charge). Hence the said time-relatedrestrictions would not apply. Further as alsostated before, Sec. 16(2) overrides Sec. 16(4)and in the absence of time limits in Sec. 16(2),ITC should be available even if the same isclaimed beyond the stipulated time.

VIII. It is also submitted that the restrictionscontained u/s 16(4) is for the invoice “for thesupply” of goods/services whereas the self-invoice prepared by the recipient u/s 31(3)(f) fordischarging the tax under RCM is an invoiceprepared “for the receipt” of goods/services. Itmust be noted that the recipient whiledischarging the tax under RCM do not becomethe deemed supplier. Further the provisoinserted u/s 16(4) for FY 2017-18 permittingthe taking of ITC beyond the normal time limitsprovides for the condition that the details of therelevant invoice should be reported by thevendor in GSTR – 1. Hence invoices the detailsof which are reportable in GSTR – 1 (invoice forsupplies) are only sought to be covered u/s16(4). Therefore it can be said that therestrictions would not apply to cases where ITCis related to self-invoice details of which are notreportable in GSTR – 1 (only invoice numbersare to be mentioned) but are reportable in GSTR– 2. Without prejudice, it can also be contendedas explained later, that the restriction containedu/s 16(4) even if applied would apply only quathe year in which the self-invoice is preparedand not qua the year in which the underlyingsupplies would have been received.

IX. We may also state that the Hon’ble SupremeCourt decision in the case of Osram Surya P. Ltdvs Commissioner of Central Excise (2002) 122TAXMAN 0583 did not rule on the legal validityof the time-related restriction of six months foravailing MODVAT credit (as it was not thequestion before the Court) but only consideredthe issue as to whether the same can apply toinvoices issued before the imposition of thesaid restriction or not. We also observe that thedecision of the Hon'ble Supreme Court in thecase of ALD Automotive Pvt. Ltd. v. CTO 2018(364) ELT 3 (SC) wherein the validity of time-related restrictions contained u/s 19 of theTNVAT Act, 2006 was upheld is clearly

distinguishable from the present case based onthe language used as well as the context asdiscussed in the contentions above.

8. Now we shall discuss the second fundamentalaspect as to at what stage shall the said restrictionapply in the entire process of claiming the ITC.

9. Sec. 16(1) inter alia provides that a registeredperson is “entitled to take” the credit of the taxcharged on any supply of goods or services or bothwhich are used or intended to be used in the courseor furtherance of business. It further provides thatthe said amount of ITC shall be credited to theelectronic credit ledger of the given person.Therefore at this stage we can conclude that thestage of “taking the credit” is different from thestage in which the said amount is credited in theelectronic credit ledger.

10. Further Rule 36(2) of the CGST Rules, 2017provides that a registered person can avail the ITConly if the document (e.g. tax invoice) available forclaiming such credit contains all the necessaryparticulars and the said information is furnished bythe registered person in GSTR – 2. Sec. 35(1)(d) ofthe CGST Act, 2017 provides that a registeredperson shall be required to maintain the record ofthe ITC availed. Hence it would appear that the actof taking the credit in the records to be maintainedby way of ensuring that the documents contain thenecessary particulars and the same are submittedin form GSTR – 2 is a precursor to the reflection ofthe said ITC in the electronic credit ledger on aprovisional basis by filing GSTR – 3. Now in theabsence of GSTR – 2 we can say that a registeredperson can avail the credit as soon as thedocument containing the relevant particulars aremade available. This also brings us to Sec. 16(2)which clearly deals with the entitlement of ITC andnot the taking of the said ITC. Said provisionsprovide for the satisfaction of four conditions (viz.possession of relevant documents, receipt ofgoods/services, tax paid by the suppliers to theGovernment and return filed u/s 39). Now out of thesaid four conditions it cannot be said that all mustbe satisfied before the stage of taking the ITC. Thisis because the actual payment condition and thereturn filing condition can be satisfied only after thetaking of the ITC as otherwise no registered personcan avail and utilize the ITC of the preceding taxperiod unless he files the return first and the tax ispaid by the concerned suppliers. This cannot be theintention of Sec. 16(2). The same is also apparentas discussed above from the fact that Sec. 16(2)only deals with the conditions for entitlement of ITCand not for taking of the ITC. Therefore I submit that

Vadodara Branch of WIRC of ICAI

Volume - III April 2020

07

only first two conditions (viz. possession ofdocument already part of Rule 36(2) and receipt ofgoods/services (in certain situations even therequirement of receipt can be satisfied post facto))needs to be fulfilled before availing the ITC in therecords maintained and the other two can be metpost such availment. Said conclusion also getssupport from the fact that the filing of return hasbeen made as a condition to become entitled to ITCu/s 16(2) and not for taking the ITC. Hence wesubmit that on receipt of the goods/services foruse in the business and on possession of therelevant documents, ITC can be availed in therecords maintained u/s 35.

11. Now once the said ITC is availed in the records itwas to be provisionally credited in the electroniccredit ledger as per Sec. 41 for matching which wasto be undertaken by the GSTN portal as per Sec. 42& 43. Once the ITC matched the provisional creditwould get converted into final credit. Therefore Isubmit that the process of reflection of the said ITCin GSTR – 3B, and in the absence of matching, isonly a second step post the availment of ITC in therecords to get the availed amount credited in thee lect ron ic cred i t ledger for subsequentutilization/refund. One can also draw support fromthe Hon’ble Apex Court decisions in the case ofChandrapur Magnet Wires (P) Ltd. V. CCE 1996 (8)ELT (SC) and CCE VS. Bombay Dyeing & Mfg. Co.Ltd. 2007 (215) ELT 3 (SC) as well as Hon’bleGujarat High Court decision in the case of CCE Vs.Ashima Dyecot Ltd. 2008 (232) ELT 580 (Guj)wherein it has been held that debit in the CENVATrecords posts the credit in the said records shallt a n t a m o u n t t o n o n - a v a i l m e n t o f t h eMODVAT/CENVAT credits and therefore inabsence of any subsequent debit in the saidregister, the credit in the register would tantamountto the availment of the said credits. We also rely onthe decision of Hon’ble CESTAT in the case of CCEv. Ford India Ltd. 2012 (284) E.L.T. 202 (Tri. -Chennai) wherein it has been held the date ofavailment of CENVAT credit would be the date onwhich entries are made in RG – 23 Part – I record. Inthe said decision it was also observed that theSupreme Court decision in the case of OsramSurya Pvt. Ltd. (supra) did not deal with the issue asto when it can be said that the credit has beenavailed. Hence we can conclude that the ITCavailment first happens in the records maintainedby the taxpayer and the return filing process ismerely a reflection of the said ITC for credit in theelectronic credit ledger to al low for theutilization/refund.

12. Once the above proposition is adopted, Sec. 16(4)provides for the restrictions for the taking of the ITCand not the reflection of the same in GSTR – 3B forgetting the said amount credited in the electroniccredit ledger. Thus it can be said that as long as theregistered person has availed the ITC in the booksof accounts (which will be a record u/s 35 as far asITC availment is concerned) before the cut-off dateprescribed u/s 16(4), the same can be said to be inorder.

13. For ITC of the tax payable under RCM on thesupplies received from unregistered suppliers itcan be contended that Sec. 16(4) even if it applieswould apply qua the year in which the self-invoice isissued and not qua the year in which the underlyingsupplies would have been received. A delay inraising the self-invoice may have certain otherconsequences in terms of penalties for violation oftime of supply provisions however the samecannot be inferred to the effect that the delayedself-invoice would relate to the actual date of thereceipt of goods/services. This is because thetime-related restriction u/s 16(4) has a nexus withthe date of the document and not the date of theactual receipt of goods/services. Had it been so thesaid provision would have linked the restrictionwith the actual receipt date of goods/services andnot the date of the document. Therefore it can becontended that the ITC of the self-invoice even ifmade in FY 2019-20 for the underlying supplyreceived in FY 2017-18 would remain ITC of FY2019-20 and accordingly Sec. 16(4), if at all, wouldapply.

Hence we conclude that the time-relatedrestrictions imposed u/s 16(4) is not that simple tointerpret and take a position. All the abovecontentions must be examined in detail beforemaking any decision.

Rule 86A – Blocking of the Electronic Credit Ledger

14. Rule 86A came to be inserted vide Notf no. 75/2019– CT dt 26.12.2019. Said Rule in a nutshell grantspower to restrict the utilization of the balance lyingin the electronic credit ledger in cer taincircumstances. Before discussing the said Rule, itis important to understand whether the provisionsof the Act enable the Government to prescribe sucha Rule.

15. Generic rulemaking power contained u/s 164 of theCGST Act, 2017 can be exercised only for carryingout the provisions of the Act. Hence there must be aprovision in the Act that authorizes or provides forthe formation of any rule. Sec. 49(4) of the CGSTAct, 2017 provides that the amount available in the

Vadodara Branch of WIRC of ICAI

Volume - III April 2020

08

electronic credit ledger may be used for makingany payment towards output tax in such mannerand subject to such conditions and within suchtime as may be prescribed. Therefore the authoritygranted by the Act to the Executive by way of adelegated legislation concerning the utilization ofthe amount available is limited to the manner andsubject to such conditions as prescribed. Now thecomplete ban on the utilization of the said balanceis not concerning any manner of utilization. Hencewe need to only consider whether the powergranted to prescribe conditions for utilization of thesaid balance can be said to also grant the power torestrict in toto?

16. The power granted by Sec. 49(4) is only to prescribethe procedural conditions enabling the utilization ofthe balance and cannot be interpreted to restrict itsutilization of the ITC duly availed following the law.Therefore on this ground itself it can be contendedthat Rule 86A is going beyond the provisions of theAct and is thus ultra vires.

17. Presuming that the power to prescribe theconditions would also include the power to restrict,it must however be seen as to whether the exerciseof said power results in an excessive delegation ornot. This is because excessive delegation is notpermissible and the rule made by exercising thesame would not be valid. Hon’ble Supreme Court inthe leading case on the subject of VasantlalMaganbhai Sanjanwala vs The State Of Bombay1961 SCR (1) 341 has held that the delegation by anAct can be proper only if the same is done by settingthe proper framework and guidance within whichthe delegated authority can exercise the power.Improper exercise of a vague and arbitrary power tochange the policy of the Act (in the present casewithout challenging the availment of ITC byfollowing the principles of natural justice in theform of SCN but straight away blocking theutilization of the balance) would be a case ofexcessive delegation not permitted in law. Hence inthe present case exercise of rulemaking power tochange the policy of the Act (which nowherepermits for the blockage of electronic creditledgers) would be a case of excessive delegationand hence even on this ground it can be contendedthat the Rule 86A is not just and proper.

18. Having discussed the validity of the new Rule weshall now go into the detailed discussion of the Ruleitself presuming it to be valid. Before discussing thecircumstances in which the power to restrict theutilization of the balance available in the electroniccredit ledger can be invoked it is worthwhile first todiscuss the vital aspect dealing with the conditions

related to the reason to believe to be satisfied forinvocation of the said Rule. The relevant part ofRule 86A for our discussion reads as under:

“Rule 86A(1) The Commissioner or an officerauthorised by him in this behalf, not below the rankof an Assistant Commissioner, having reasons tobelieve that credit of input tax available in theelectronic credit ledger has been fraudulentlyavailed or is ineligible inasmuch as – may, forreasons to be recorded in writing, not allow debit ofan amount equivalent to such credit in electroniccredit ledger for discharge of any liability undersection 49 or for claim of any refund of anyunutilised amount”

19. Above Rule, therefore, provides that the officerexercising the power should have “reasons tobelieve” that the case in question falls in the givencircumstances (which are discussed later) andsaid reasons are to be recorded in writing.

20. Hon’ble Supreme Court in the case of Union OfIndia vs Mohan Lal Capoor & Others 1974 SCR (1)797 (SC) has held that reasons are the linksbetween the mater ia ls on which cer tainconclusions are based and the actual conclusions.They disclose how the mind is applied to thesubject matter for a decision whether it is purelyadministrative or quasi-judicial. They should reveala rational nexus between the facts considered andthe conclusions reached. Therefore the reasonsleading to the exercise of the power granted by theRule must be based on rational nexus and not onany conjecture or surmises. The reasons recordedmust be relevant and germane to the content andscope of the power conferred by the statute andmust show a reasonable nexus between the factsconsidered and satisfaction reached (P.K.Chowdhury and others v. Union of India and others(MP) 1976 MPLJ 690 (MP)).

21. Further Hon’ble Supreme Court in the case ofAjantha Industries And Ors vs Central Board OfDirect Taxes 1976 SCR (2) 884 (SC) has held thatthe requirement of recording the reasons as amatter of principle of natural justice would alsoencompass the requirement of communicatingsuch reasons to the taxpayer to enable the taxpayerwho is prejudicially affected to challenge thedecision.

22. Therefore I submit that the requirement ofrecording the reasons would also encompass therequirement of communicating such reasons tothe taxpayer whose electronic credit ledger issought to be blocked. An unreasonable exercise ofthe power can be challenged in the Courts.

Vadodara Branch of WIRC of ICAI

Volume - III April 2020

09

23. Lastly let us consider the circumstances which canpermit the exercise of the given power. It may benoted that Rule 86A can be invoked only if ITCavailable in the electronic credit ledger has been“fraudulently availed or is ineligible” in the givencircumstances. Hence I submit that thecircumstances discussed below would not ipsofacto authorize invocation of the rule unless it hasbeen established that the ITC in the given situationshas been fraudulently availed or is ineligible. This isbecause as we shall see later one of thecircumstances which enable the invocation of theRule is that the tax in respect of which ITC has beenavailed has not been paid by the concernedsuppliers. Now merely non-payment of tax by thesuppliers in an otherwise genuine transaction willnot make the said ITC as “fraudulently availed orineligible”. Therefore I submit that the test of ITCbeing “fraudulently availed or ineligible” shall haveto be satisfied before the invocation of the Rule.

24. Now five circumstances have been provided underwhich the Rule can be invoked if the ITC has been“fraudulently availed or is ineligible” in the givencircumstances. Circumstances are as under:

25. Before we conclude we also submit that as per Rule86A(3) the restriction imposed shall cease to haveeffect after the expiry of a period of one year fromthe date of imposing such restriction.

26. Based on the above discussions we can concludethat the power granted by Rule 86A needs to beexercised by the department with caution and anyundue or unreasonable exercise can be challengedin the Courts for appropriate relief.

Standards dealing with financial instruments under IndAS:

Under Ind AS, three Standards deal with accounting forfinancial instruments.

� Ind AS 32 Financial Instruments: Presentationdeals with the presentation and classification offinancial instruments as financial liabilities orequity and sets out the requirements regardingoffset of financial assets and financial liabilities inthe balance sheet.

� Ind AS 107 Financial Instruments: Disclosures setsout the disclosures requirements in respect offinancial instruments.

� Ind AS 109 Financial Instruments containsguidance on the recognition, derecognition,classification and measurement of financialinstruments, including impairment and hedgeaccounting.

Scope:

IND AS 109 establishes principles for the accounting forfinancial asset or financial liability. This Standardapplies to all types of entities and financial instruments

Clause

(a)(i)

(a)(ii)

(b)

Circumstances

the credit of input tax has beenavailed on the strength of taxinvoices or debit notes or anyother document prescribedunder rule 36 -

(i) issued by a registeredperson who has been foundnon-existent or not to beconducting any business froma n y p l a c e f o r w h i c hregistration has been obtainedor

without receipt of goods orservices or both

the credit of input tax has beenavailed on the strength of taxinvoices or debit notes or anyother document prescribedunder rule 36 in respect of anysupply, the tax charged inrespect of which has not beenpaid to the Government

Remarks

It must be shown from thefacts that the supplier isn o n - e x i s t e n t o r n o tconducting business fromhis registered place.

It must be shown from factsthat goods or services havenot been received and ITChas been availed.

As discussed earlier merenon-payment of tax by thesuppliers cannot disentitlethe ITC in an otherwisegenuine transaction. Courtsin the pre-GST era have readdown the actual paymentcondition and applied onlyin non-genuine cases.Therefore as mere non-payment cannot make theITC ineligible we are of theview that said clause can beinvoked only if it has beenfound that the transactionwas not genuine.

Clause

(c)

(d)

Circumstances

the registered person availingthe credit of input tax has beenfound non-existent or not to beconducting any business froma n y p l a c e f o r w h i c hregistration has been obtained

the registered person availingany credit of input tax is not inpossession of a tax invoice ordeb i t note or any otherdocument prescribed underrule 36

Remarks

The taxpayer whose creditledger is sought to beblocked should be found tobe non-existent or notconducting business fromthe registered place ofbusiness.

It must be shown that thegiven documents are notavailable in respect of whichITC has been availed.

Contributed by : CA. Rohit Parekhcan be reached at [email protected]

Financial InstrumentsPart-1

Vadodara Branch of WIRC of ICAI

Volume - III April 2020

10

other than –

� Investments in equity shares of subsidiaryassociate or Joint venture - covered in Ind AS 110,Ind AS 28 and Ind AS 27.

� Rights and obligations under lease to which Ind AS116 applies.

� Employers' rights and obligations arisingfrom employee benefit plans, Ind AS 19 applies.

� Financial Instruments issued by the entity thatmeets the definition of an equity instrument. Ind AS32 specifies its classification, however thisstandard applies to entity holding this instrument.

� Rights and Obligations arising out of InsuranceContracts. Ind AS 104 applies.

� Forward Contracts to buy or sell an acquiree,between an acquirer and a selling shareholder in abusiness combination, to which Ind AS 103applies.

� Financial Instruments, contracts and obligationsunder share-based payment transactions to whichInd AS 102 applies.

� Rights to payments to reimburse the entity forexpenditure that is required to make to settle aliability that it recognises as a provision during thecurrent or earlier period, in accordance with Ind AS37.

� Rights and obligations within the scope of Ind AS115 that are financial instruments, except forthose that Ind AS 115 specifies are accounted forin accordance with this standard.

� Loan commitments other than following to whichthis standard apply-

- Loan commitments that entity designates asfinancial liability through Profit or loss(FVTPL).

- Loan commitments that can be settled net incash or by delivering or issuing other financialinstrument (Derivative).

However, impairment and derecognition of loancommitments will be done as per this standard, even iffor loan commitments which are not falling within thisstan

Definition:

The definition of a financial instrument is broad. Afinancial instrument is defined as any contract that givesrise to a of one entity and afinancial asset financialliability equity instrumentor of another entity.

Examples of financial instruments are Trade receivablesand payables, bank loans and overdrafts, issued debt,equity and preference shares, investments in securities(e.g. shares and bonds), and various derivatives. In

addition, some contracts to buy or sell non-financialitems that would not meet the definition of financialinstruments are specifically brought within the scope ofthe financial instruments Standards on the basis thatthey behave and are used in a similar way to financialinstruments.

Financial Assets:

A financial asset is any asset that is:

� cash;

� an equity instrument of another entity;

� a contractual right:

- to receive cash or another financial asset fromanother entity; or

- to exchange financial assets or financialliabilities with another entity under conditionsthat are potentially favourable to the entity; or

� a contract that will or may be settled inthe entity’s own equity instruments and is:

- a non-derivative for which the entity is ormay be obliged to receive a variable number ofthe entity’s own equity instruments; or

- a derivative that will or may be settledother than by the exchange of a fixed amountof cash or another financial asset for a fixednumber of the entity’s own equity instruments.

Examples of financial assets are investments in equityinstruments, investments in debt instruments, tradereceivables, cash and cash equivalents, derivativefinancial assets.

Financial Liabilities:

A financial liability is any liability that is:

� a contractual obligation

- to deliver cash or another financial asset toanother entity; or

- to exchange financial assets or financialliabilities with another entity under conditionsthat are potentially unfavourable to the entity; or

� a contract that will or may be settled inthe entity’s own equity instruments and is:

- a non-derivative for which the entity is ormay be obliged to deliver a variable number ofthe entity’s own equity instruments; or

- a derivative that will or may be settledother than by the exchange of a fixed amountof cash or another financial asset for a fixednumber of the entity’s own equity instruments.

Equity Instrument:

An equity instrument is any contract that evidences a

Vadodara Branch of WIRC of ICAI

Volume - III April 2020

11

residual interest in the assets of an entity after deductingall of its liabilities.

The presentation by the issuer of a financial instrumentor its component parts as liability or equity is determinedbased on principles of classification contained in Ind AS32.

Recognition & Dercognition

Financial assets and financial liabilities - Initialrecognition:

An entity should recognise a financial asset or a financialliability in its balance sheet when, and only when, theentity becomes party to the contractual provisions of theinstrument and also classify the same according tomeasurement basis.

Examples of initial recognition of arrangements asfinancial assets and financial liabilities are:

� Unconditional receivables and payables arerecognised as assets or liabilities when the entitybecomes a party to the contract and, as aconsequence, has a legal right to receive or a legalobligation to pay cash.

� Issued debt is recognised as a liability when theentity that issues it becomes a party to thecontractual terms of the debt and, consequently,has a legal obligation to pay cash to the debt holder.

� A derivative is recognised as an asset or a liabilityon the commitment date, rather than on the date onwhich settlement takes place. At inception, the fairvalues of the right and obligation created by thederivative may be equal in which case, the fair valueof the derivative will be zero.

Arrangements that are not recognised as financialassets and financial liabilities are:

� Planned future transactions, no matter how likely,are not assets and liabilities because the entity hasnot become a party to a contract.

� Derivative contracts to buy or sell non-financialitems that are scoped out of Ind AS 109 are notrecognised as financial assets and financialliabilities because they are executory contracts.

� Assets to be acquired and liabilities to be incurredas a result of a firm commitment to purchase or sellgoods or services are generally not recognised untilat least one of the parties has performed under theagreement.

Ind AS 109 requires that a financial asset (except forcertain trade receivables) or a financial liability should bemeasured at initial recognition at its fair value plus orminus, transaction costs that are directly attributable tothe acquisition or issue of the financial asset or thefinancial liability. However, the financial assets or

financial liabilities subsequently measured at FVTPL, donot include such transaction costs. Trade receivablesthat do not contain a significant financing component(determined in accordance with Ind AS 115 Revenuefrom Contracts with Customers) are initially measuredat their transaction price and not at fair value.

In case the fair value of a financial instrument at initialrecognition differs from the transaction price, an entityshall:-

- Record the financial instrument at fair value; thedifference between fair value and transaction pricewould be “day 1 gain or loss” only if that fair value isevidenced by a Level 1 input or based on a valuationtechnique that uses only data from observablemarkets.

- In all other cases, the financial instrument will berecorded at fair value adjusted to defer thedifference between the transaction price and thefair value. After initial recognition, this deferral shallbe recognised as a gain or loss only to the extentthat it arises from a change in a factor (includingtime) that market participants would take intoaccount.

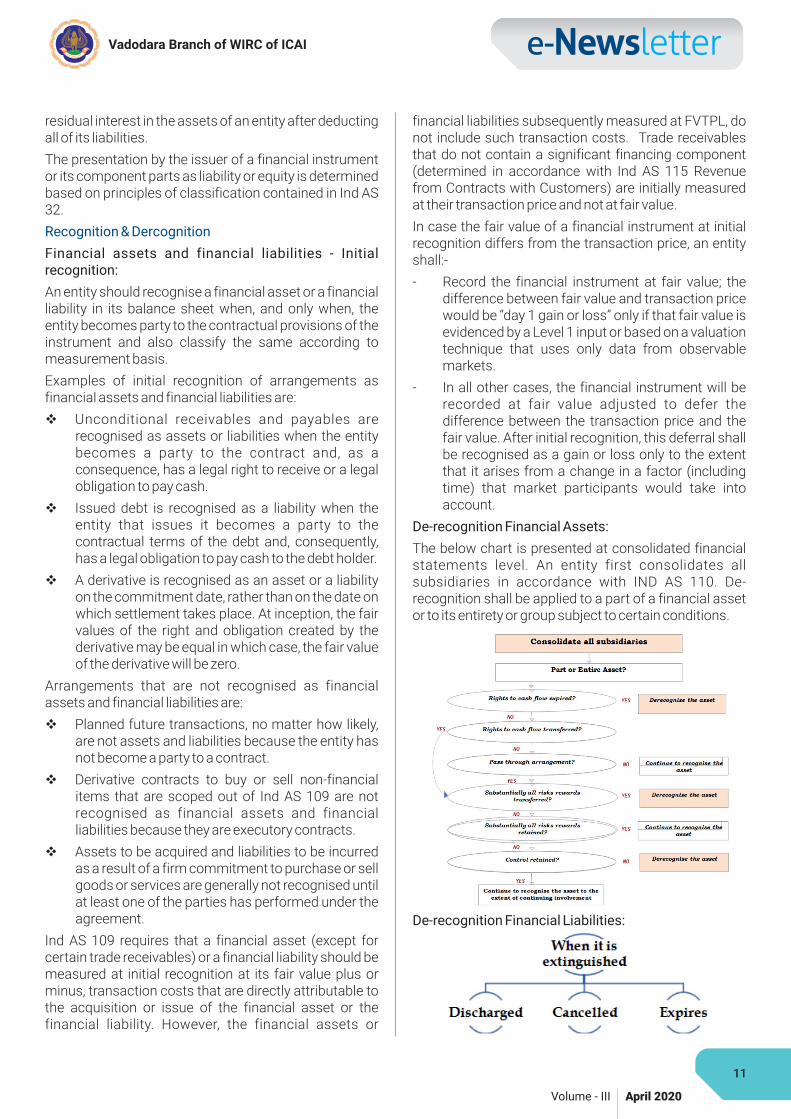

De-recognition Financial Assets:

The below chart is presented at consolidated financialstatements level. An entity first consolidates allsubsidiaries in accordance with IND AS 110. De-recognition shall be applied to a part of a financial assetor to its entirety or group subject to certain conditions.

De-recognition Financial Liabilities:

Vadodara Branch of WIRC of ICAI

Volume - III April 2020

12

Financial assets - Classification:

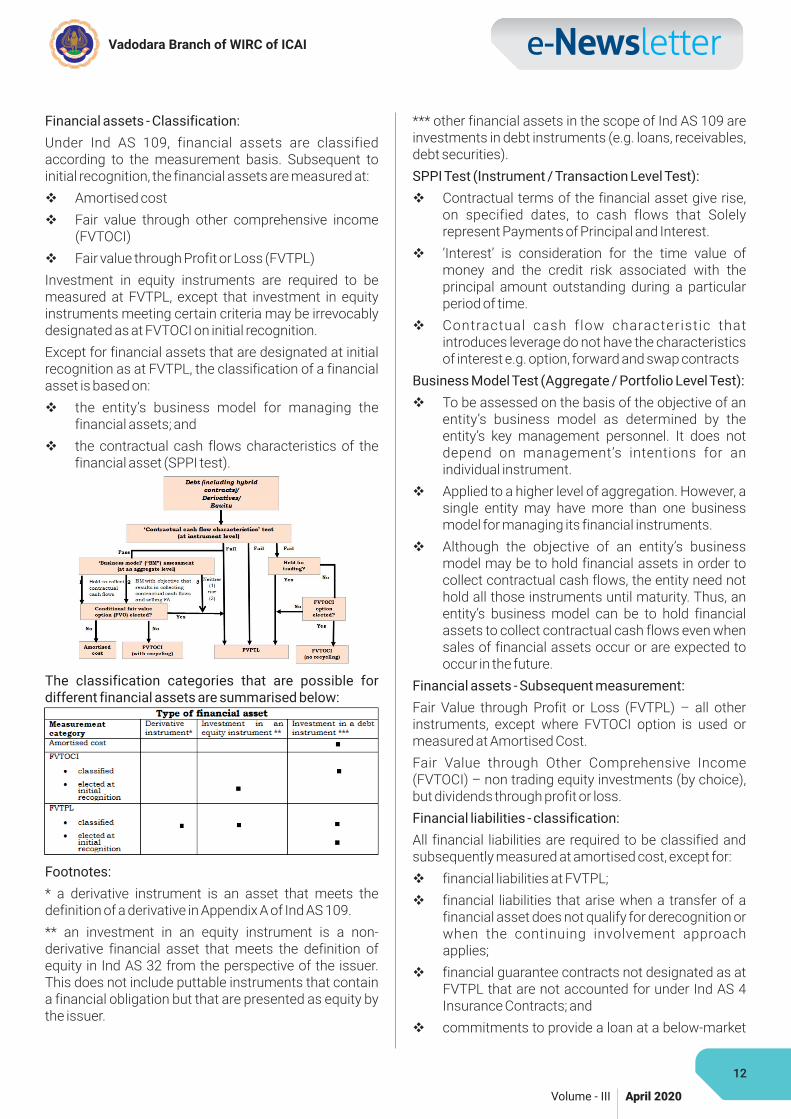

Under Ind AS 109, financial assets are classifiedaccording to the measurement basis. Subsequent toinitial recognition, the financial assets are measured at:

� Amortised cost

� Fair value through other comprehensive income(FVTOCI)

� Fair value through Profit or Loss (FVTPL)

Investment in equity instruments are required to bemeasured at FVTPL, except that investment in equityinstruments meeting certain criteria may be irrevocablydesignated as at FVTOCI on initial recognition.

Except for financial assets that are designated at initialrecognition as at FVTPL, the classification of a financialasset is based on:

� the entity’s business model for managing thefinancial assets; and

� the contractual cash flows characteristics of thefinancial asset (SPPI test).

The classification categories that are possible fordifferent financial assets are summarised below:

Footnotes:

* a derivative instrument is an asset that meets thedefinition of a derivative in Appendix A of Ind AS 109.

** an investment in an equity instrument is a non-derivative financial asset that meets the definition ofequity in Ind AS 32 from the perspective of the issuer.This does not include puttable instruments that containa financial obligation but that are presented as equity bythe issuer.

*** other financial assets in the scope of Ind AS 109 areinvestments in debt instruments (e.g. loans, receivables,debt securities).

SPPI Test (Instrument / Transaction Level Test):

� Contractual terms of the financial asset give rise,on specified dates, to cash flows that Solelyrepresent Payments of Principal and Interest.

� ‘Interest’ is consideration for the time value ofmoney and the credit risk associated with theprincipal amount outstanding during a particularperiod of time.

� Contractual cash flow characteristic thatintroduces leverage do not have the characteristicsof interest e.g. option, forward and swap contracts

Business Model Test (Aggregate / Portfolio Level Test):

� To be assessed on the basis of the objective of anentity’s business model as determined by theentity’s key management personnel. It does notdepend on management’s intentions for anindividual instrument.

� Applied to a higher level of aggregation. However, asingle entity may have more than one businessmodel for managing its financial instruments.

� Although the objective of an entity’s businessmodel may be to hold financial assets in order tocollect contractual cash flows, the entity need nothold all those instruments until maturity. Thus, anentity’s business model can be to hold financialassets to collect contractual cash flows even whensales of financial assets occur or are expected tooccur in the future.

Financial assets - Subsequent measurement:

Fair Value through Profit or Loss (FVTPL) – all otherinstruments, except where FVTOCI option is used ormeasured at Amortised Cost.

Fair Value through Other Comprehensive Income(FVTOCI) – non trading equity investments (by choice),but dividends through profit or loss.

Financial liabilities - classification:

All financial liabilities are required to be classified andsubsequently measured at amortised cost, except for:

� financial liabilities at FVTPL;

� financial liabilities that arise when a transfer of afinancial asset does not qualify for derecognition orwhen the continuing involvement approachapplies;

� financial guarantee contracts not designated as atFVTPL that are not accounted for under Ind AS 4Insurance Contracts; and

� commitments to provide a loan at a below-market

Vadodara Branch of WIRC of ICAI

Volume - III April 2020

13

interest rate.

Financial liabilities that are designated as hedged itemsare subject to the hedge accounting requirements.

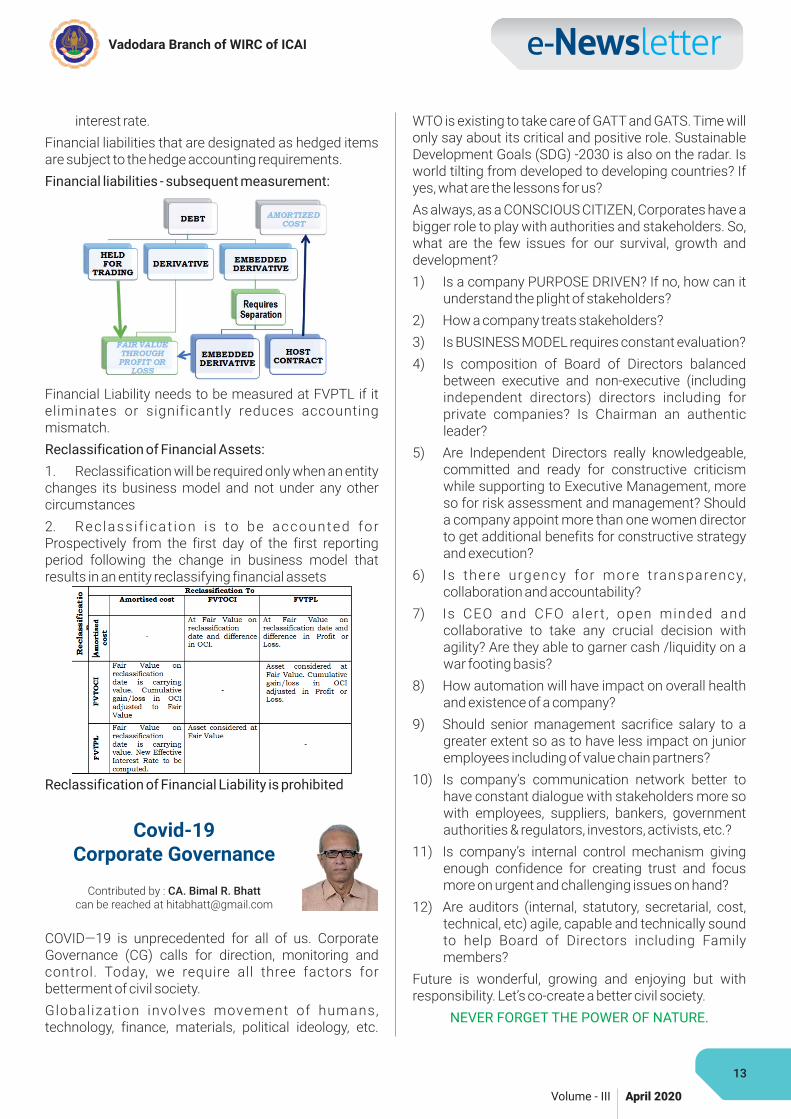

Financial liabilities - subsequent measurement:

Financial Liability needs to be measured at FVPTL if iteliminates or significantly reduces accountingmismatch.

Reclassification of Financial Assets:

1. Reclassification will be required only when an entitychanges its business model and not under any othercircumstances

2. Rec lass i f icat ion is to be accounted forProspectively from the first day of the first reportingperiod following the change in business model thatresults in an entity reclassifying financial assets

Reclassification of Financial Liability is prohibited

Contributed by : CA. Bimal R. Bhattcan be reached at [email protected]

Covid-19Corporate Governance

WTO is existing to take care of GATT and GATS. Time willonly say about its critical and positive role. SustainableDevelopment Goals (SDG) -2030 is also on the radar. Isworld tilting from developed to developing countries? Ifyes, what are the lessons for us?

As always, as a CONSCIOUS CITIZEN, Corporates have abigger role to play with authorities and stakeholders. So,what are the few issues for our survival, growth anddevelopment?

1) Is a company PURPOSE DRIVEN? If no, how can itunderstand the plight of stakeholders?

2) How a company treats stakeholders?

3) Is BUSINESS MODEL requires constant evaluation?

4) Is composition of Board of Directors balancedbetween executive and non-executive (includingindependent directors) directors including forprivate companies? Is Chairman an authenticleader?

5) Are Independent Directors really knowledgeable,committed and ready for constructive criticismwhile supporting to Executive Management, moreso for risk assessment and management? Shoulda company appoint more than one women directorto get additional benefits for constructive strategyand execution?

6) Is there urgency for more transparency,collaboration and accountability?

7) Is CEO and CFO aler t , open minded andcollaborative to take any crucial decision withagility? Are they able to garner cash /liquidity on awar footing basis?

8) How automation will have impact on overall healthand existence of a company?

9) Should senior management sacrifice salary to agreater extent so as to have less impact on junioremployees including of value chain partners?

10) Is company’s communication network better tohave constant dialogue with stakeholders more sowith employees, suppliers, bankers, governmentauthorities & regulators, investors, activists, etc.?

11) Is company’s internal control mechanism givingenough confidence for creating trust and focusmore on urgent and challenging issues on hand?

12) Are auditors (internal, statutory, secretarial, cost,technical, etc) agile, capable and technically soundto help Board of Directors including Familymembers?

Future is wonderful, growing and enjoying but withresponsibility. Let’s co-create a better civil society.

NEVER FORGET THE POWER OF NATURE.

COVID—19 is unprecedented for all of us. CorporateGovernance (CG) calls for direction, monitoring andcontrol. Today, we require all three factors forbetterment of civil society.

Globalization involves movement of humans,technology, finance, materials, political ideology, etc.

Vadodara Branch of WIRC of ICAI

Volume - III April 2020

14

Due Date CalendarContributed by : CA. Himesh D. Gajjarcan be reached at [email protected]

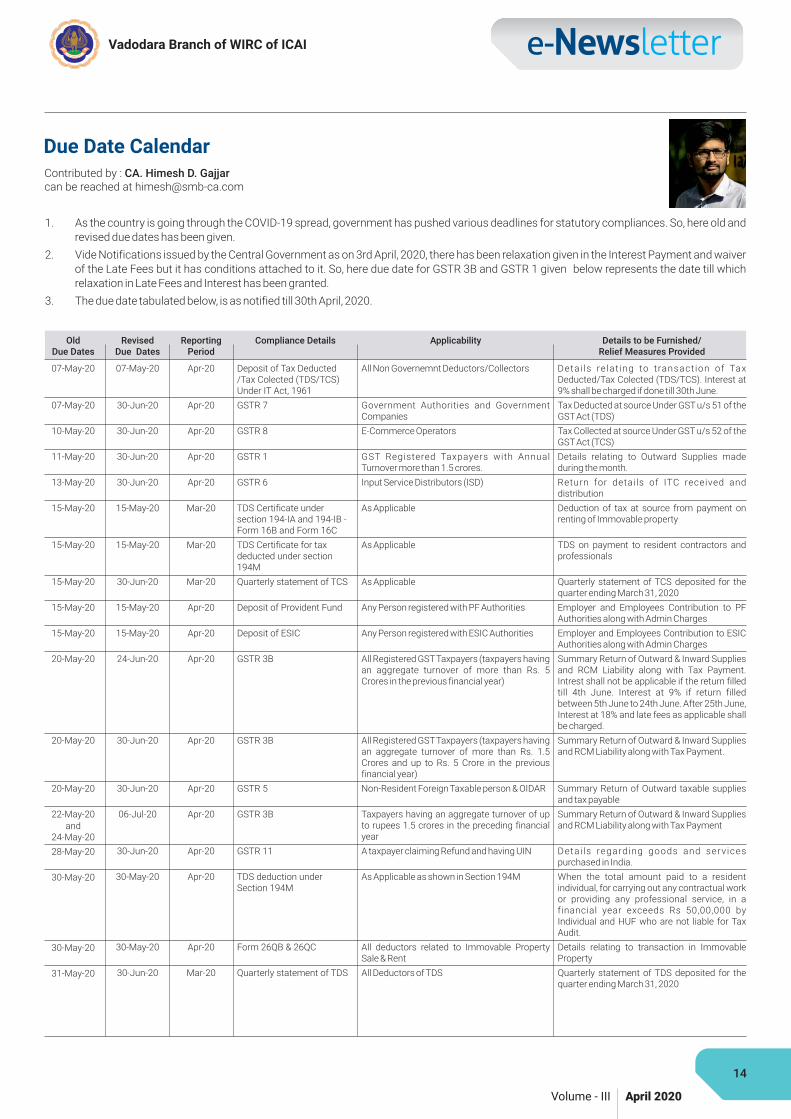

1. As the country is going through the COVID-19 spread, government has pushed various deadlines for statutory compliances. So, here old andrevised due dates has been given.

2. Vide Notifications issued by the Central Government as on 3rd April, 2020, there has been relaxation given in the Interest Payment and waiverof the Late Fees but it has conditions attached to it. So, here due date for GSTR 3B and GSTR 1 given below represents the date till whichrelaxation in Late Fees and Interest has been granted.

3. The due date tabulated below, is as notified till 30th April, 2020.

OldDue Dates

07-May-20

07-May-20

10-May-20

11-May-20

13-May-20

15-May-20

15-May-20

15-May-20

15-May-20

15-May-20

20-May-20

20-May-20

20-May-20

22-May-20and

24-May-20

28-May-20

30-May-20

30-May-20

31-May-20

RevisedDue Dates

07-May-20

30-Jun-20

30-Jun-20

30-Jun-20

30-Jun-20

15-May-20

15-May-20

30-Jun-20

15-May-20

15-May-20

24-Jun-20

30-Jun-20

30-Jun-20

06-Jul-20

30-Jun-20

30-May-20

30-May-20

30-Jun-20

ReportingPeriod

Apr-20

Apr-20

Apr-20

Apr-20

Apr-20

Mar-20

Mar-20

Mar-20

Apr-20

Apr-20

Apr-20

Apr-20

Apr-20

Apr-20

Apr-20

Apr-20

Apr-20

Mar-20

Compliance Details

Deposit of Tax Deducted/Tax Colected (TDS/TCS)Under IT Act, 1961

GSTR 7

GSTR 8

GSTR 1

GSTR 6

TDS Certificate undersection 194-IA and 194-IB -Form 16B and Form 16C

TDS Certificate for taxdeducted under section194M

Quarterly statement of TCS

Deposit of Provident Fund

Deposit of ESIC

GSTR 3B

GSTR 3B

GSTR 5

GSTR 3B

GSTR 11

TDS deduction underSection 194M

Form 26QB & 26QC

Quarterly statement of TDS

Applicability

All Non Governemnt Deductors/Collectors

Government Authorities and GovernmentCompanies

E-Commerce Operators

GST Registered Taxpayers with AnnualTurnover more than 1.5 crores.

Input Service Distributors (ISD)

As Applicable

As Applicable

As Applicable

Any Person registered with PF Authorities

Any Person registered with ESIC Authorities

All Registered GSTTaxpayers (taxpayers havingan aggregate turnover of more than Rs. 5Crores in the previous financial year)

All Registered GSTTaxpayers (taxpayers havingan aggregate turnover of more than Rs. 1.5Crores and up to Rs. 5 Crore in the previousfinancial year)

Non-Resident Foreign Taxable person & OIDAR

Taxpayers having an aggregate turnover of upto rupees 1.5 crores in the preceding financialyear

A taxpayer claiming Refund and having UIN

As Applicable as shown in Section 194M

All deductors related to Immovable PropertySale & Rent

All Deductors of TDS

Details to be Furnished/Relief Measures Provided

Detai ls re lat ing to transact ion of TaxDeducted/Tax Colected (TDS/TCS). Interest at9% shall be charged if done till 30th June.

Tax Deducted at source Under GST u/s 51 of theGST Act (TDS)

Tax Collected at source Under GST u/s 52 of theGST Act (TCS)

Details relating to Outward Supplies madeduring the month.

Return for details of ITC received anddistribution

Deduction of tax at source from payment onrenting of Immovable property

TDS on payment to resident contractors andprofessionals

Quarterly statement of TCS deposited for thequarter ending March 31, 2020

Employer and Employees Contribution to PFAuthorities along with Admin Charges

Employer and Employees Contribution to ESICAuthorities along with Admin Charges

Summary Return of Outward & Inward Suppliesand RCM Liability along with Tax Payment.Intrest shall not be applicable if the return filledtill 4th June. Interest at 9% if return filledbetween 5th June to 24th June. After 25th June,Interest at 18% and late fees as applicable shallbe charged.

Summary Return of Outward & Inward Suppliesand RCM Liability along with Tax Payment.

Summary Return of Outward taxable suppliesand tax payable

Summary Return of Outward & Inward Suppliesand RCM Liability along with Tax Payment

Detai ls regarding goods and servicespurchased in India.

When the total amount paid to a residentindividual, for carrying out any contractual workor providing any professional service, in afinancial year exceeds Rs 50,00,000 byIndividual and HUF who are not liable for TaxAudit.

Details relating to transaction in ImmovableProperty

Quarterly statement of TDS deposited for thequarter ending March 31, 2020

Vadodara Branch of WIRC of ICAI

DISCLAIMER : The ICAI and the Vadodara Branch of WIRC of ICAI is not in any way responsible for the result of any action taken on the basis of the advertisement published in theNewsletter. The members, however, may bear in mind the provisions of the Code of Ethics while responding to the advertisements. The views and opinion expressed or implied inthe Newsletter are those of the authors / contributors and do not necessarily reflect those of Vadodara Branch. Unsolicited matters are sent at the owner's risk and the publisheraccepts no liability for loss or damage. Material in this publication may not be reproduced, whether in part or in whole, without the consent of Vadodara Branch. Members arerequested to kindly send material of professional interest to The same may be published in the newsletter subject to availability [email protected]/[email protected] & editorial editing.

Vadodara Branch of WIRC ofThe Institute of Chartered Accountants of India

www.baroda-icai.org WIRC : www.wirc-icai.org ICAI: www.icai.orgl l

Half Page (1 Color) 5,500

ADVERTISEMENTS : The tariff for advertising given below are duly approved by the Managing Committee of the Vadodara Branch. Advertisements are received directly by theBranch and no advertising agency has been appointed for this purpose. This Newsletter is circulated without any charges to its members and otherSUBSCRIPTION RATES :important categories of recipients as per ICAI Advisory on Newsletters. Subscription rate is Rs. 20/- per issue for others. : on behalf ofPUBLISHED BY CA. Krunal BrahmbhattVadodara Branch of WIRC of ICAI “ICAI Bhawan”, Kalali-Tandalja Road, Atladra, Vadodara - 390 012PUBLISHED AT

Designed by Multiprints, 30/B, Gandhi Oil Mill Compound, Near BIDC, Gorwa, Vadodara - 390 016. Ph.: 0265-228 5592

“ICAI Bhawan”, Kalali-Tandalja Road, Atladra,Vadodara - 390 012. +91 265 268 0593Telefax :

M: 85110 77115 / 0265 268 1115 (DCO)

8,500

THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIAICAI Bhawan, Post Box No. 7100, Indraprastha Marg,New Delhi - 110 002.

+91 (11) 3989 3989 | [email protected].: E-mail:www.icai.orgWeb:

WESTERN INDIA REGIONAL COUNCILICAI Tower, Plot no C-40, G Block, Opp MCA Ground,Bandra Kurla Complex, Bandra (E), Mumbai - 400 051

+022 - 3367 1400 / 3367 1500 | [email protected].: Email:www.wirc-icai.orgWeb:

Back Cover (4 color) 16,500 Inside Front/Back Cover (4 color) Full Page (1 Color)

* Discount - 3 to 6 issue of 10%, 7 to 12 issue 15% * Circulated to more than Chartered Accountants2200ADVERTISEMENT RATE :

11,000

Volume - III April 2020

15