Embed Size (px)

Citation preview

Newsletter

August 2016

In This IssueTrending

Topics

Due Date

Chart

Notifications

& Circulars

Seminars and

CoursesAbout Us

In This Issue

Trending Topics 03

“On Tap” licensing Coming Soon for universal banks

Wait, GST is not a reality yet: It still has to cover seven

grueling steps

Mutual funds Are ratings the real indicators?

Instruments of investments in FDI

Due Date Chart 12

Notifications and Circulars 14

Seminars and Courses 18

Seminar

Batches for Professional Courses

About Us 23

Contact Us 26

2

TRENDING TOPICS

In This IssueTrending

Topics

Due Date

Chart

Notifications

& Circulars

Seminars and

CoursesAbout Us

“On Tap” licensing Coming

Soon for universal banks

4

Background

With just over a month left for his term

coming to end at Mint Road, outgoing

Reserve Bank of India (RBI) governor

Raghuram Rajan has taken one of the key

reform steps in the country’s banking sector

by announcing final norms for ‘on tap

licensing’ or continuous licensing. In simple

words, this means bank licensing process will

no longer be a once-in-a-decade affair. It will

be an ongoing process. From this point

onwards, any eligible banking aspirant,

individual or entity, can walk to the central

bank with an application to start a full service

bank at any point. They don’t need to wait for

specific announcement from the RBI or

government on a brief window for bank

licensing like that happened in 1993, 2001

and later in 2013.

Detailed Analysis

In the first round, RBI gave ten permits, while

two each in the second and third round.

These include Kotak Mahindra and Yes Bank

(2004) and later IDFC and Bandhan. Since

1990s, some of the private banks which got

license, lost their race in the tough

competition. They got eventually merged with

other banks. A few examples are Bank of

Rajasthan, Times Bank and Bank of Madura.

With on-tap licensing comes in, the RBI,

under Rajan, has initiated the biggest

overhaul in India’s banking structure, after

readying the structure for differentiated

banking regime with the issuance of small

finance banks and payments bank licenses.

If one sees the monetary policy structure

reforms too along with this, Rajan’s

governorship has witnessed an era of big

reforms in India’s banking industry.

But, the big highlight of ‘on-tap licensing’ norm is

that corporate biggies are out of the race

already. The central bank’s final guidelines

clearly say that ‘large industrial houses are

excluded as eligible entities but are permitted to

invest in the banks up to 10 percent’. This line

immediately pours ice-cold water on the plans of

corporate tycoons, who wants to wear the cap of

a banker. The apex bank’s move is

understandable since it has never favoured big

corporations setting up banks since banks

primarily deal with public money. Hence, the RBI

doesn’t want to take chances of private

corporations misusing that money for related

party lending.

Having said that the RBI has permitted business

houses to invest up to 10 percent in the new

banks. The question here is can RBI ensure few

corporations that do not act in concert to take

indirect control of a bank. Also, the RBI permits

the existing non-banking financial companies

(NBFCs) that are ‘controlled by residents’ and

have a successful track record for at least 10

years applying for license. So are individuals /

professionals who are ‘residents’ and have 10

years of experience in banking and finance.

Also, private groups ‘owned and controlled by

residents’ and have a successful track record for

at least 10 years.

In This IssueTrending

Topics

Due Date

Chart

Notifications

& Circulars

Seminars and

CoursesAbout Us

In This IssueTrending

Topics

Due Date

Chart

Notifications

& Circulars

Seminars and

CoursesAbout Us

Such entities, with total assets of Rs 5,000 crore

or more and non-financial business of the group

not accounting for more than 40 percent of total

income, can apply. The minimum entry capital

set is Rs 500 crore. In short, the RBI primarily

wants good NBFCs convert to full-service

banks. A private group can apply if it is primarily

into financial services business with good track

record of a decade. The stringent norms would

mean that only very few eligible candidates can

throw their hat in the ring. Not surprising given

the central bank always had an aversion to

corporations setting up banks.

In the last round, from the 25 candidates applied

for full service bank licenses, only two got the

final permit — IDFC and Bandhan. The others

too can try their luck once the new regulation

comes into place. For the yet-to-be banked in

the hinterland of the country, this is good news

since more banks would mean more

competition, more reach that would lower the

cost of services. The RBI has made it clear that

new banks under the ‘on-tap’ licensing mode

cannot ignore the rural areas of the country by

stipulating that at least 25 per cent of their

branches should be in unbanked rural centers

(population up to 9,999 as per the latest census)

and they shall comply with the priority sector

lending targets and sub-targets as applicable to

the existing domestic scheduled commercial

banks.

Under the priority sector lending rules, a bank

needs to lend at least 40 percent of their

loans to economically weaker sections.

Financial inclusion has been a big challenge

for Indian banking sector even after decades

of nationalization of banks. The new set of

universal banks and the small finance,

payments banks will change this scene. But,

all depends on how many licenses the central

bank chooses to give.

With the RBI now opening the door for all

eligible aspirants on a continuous basis, one

gets an impression that so many new banks

will now come to the picture. But that is

unlikely given the stringent riders the RBI has

set and the central bank’s aversion for too

many banks. But, as mentioned earlier, the

key takeaway from the guideline is that no big

corporate house should dream of becoming a

bank now, unless they can outsmart the

regulator by acting in concert with interested

parties.

FirstPost.com

5

GST not a reality yet: Still has

to cover seven grueling steps

6

Background

The Rajya Sabha clearance to the GST Bill,

touted as the biggest tax reform since India's

Independence, lifted market mood on

Thursday, but only briefly. The bill is set to

improve the government's revenue and help

it achieve better transmission of prices. It is

expected that certain goods, such as capital

goods, would become cheaper by 12-14 per

cent, increasing demand for them, raising

investment and, thus, economic growth.

However, the landmark legislation still needs

to clear some more hurdles before the bill

becomes a law, enforceable by the April 1,

2017 deadline.

The Way Forward

We list out the next key steps for the same:

The bill will now be sent to the Lok Sabha,

which has already passed the bill but will

have to discuss and ratify the

amendments made in the Rajya Sabha.

The BJP has majority in the Lower House

and thus a quick clearance is a given. In

case the amendments are not cleared, the

bill will go to parliamentary committee,

though the chances are slim.

One the amendments are cleared, the bill

will go to state assemblies for clearance.

At least 50% of the states (15 states) must

approve the legislation. Only Tamil Nadu

looks tough at the moment, as the

AIADMK MPs skipped the voting in the

Upper House. The BJP is in power in 13

states, while JD-U - another strong backer

of the GST legislation - is in power in

Bihar. The Congress-ruled states too are

likely to clear it.

The legislation will then go to the President,

whose signature will turn it into a law ahead of

its rollout by the deadline of April 1, 2017.

The next step will be the formation of the GST

Council. This council will have representatives

from both the Centre and states. All this will

be made within 60 days of the enactment of

the bill. It will decide the revenue neutral rate

(RNR), the rate at which there will be no loss

in aggregate central and state tax revenue.

The RNR will then get converted into a three-

slab GST rate structure, depending on

exemptions. Essential commodities will be

charged at low rates offset by higher 'sin'

taxes on goods considered to be luxuries. A

so-called standard or GST rate will be the

middle slab and will apply to most goods and

services. The single GST rate will be split

between and central and state GST. The split

shares will be decided by the GST Council.

Three more laws will need to be passed: laws

on the Central GST, integrated GST and 29

separate state GST legislations (SGST).

While the first two laws will be cleared by

Parliament, the third law will be cleared by the

respective state assemblies.

The Economic Times

In This IssueTrending

Topics

Due Date

Chart

Notifications

& Circulars

Seminars and

CoursesAbout Us

Mutual funds Are ratings the

real indicators?Background

When it comes to investing, most of us believe

in lady luck, intuitions and fate. Successful

investing is not based on destiny; it involves a

right blend of logic, research, discipline and

planning. Investing for returns is directly

proportional to the risk tolerance of the

individual. Based on the risk appetite, there

are several investment vehicles available in the

market to the investors. One of the most

popular investment vehicles in India is mutual

funds. Mutual funds are diversified, and tend to

lower your risk. It lets you invest small amounts

of money, which are monitored by qualified

professionals who use the invested sum to

create a portfolio based on pre-defined goals.

Mutual fund investing guidelines

that can help

Among mutual fund ratings, the most popular

one is the Morningstar Risk Rating. The

mutual fund ratings are generally graded on a

scale of one star to five stars, one being the

poorest and five being the best. These ratings

have been in vogue for more than a decade

Among mutual fund ratings, the most popular

one is the Morningstar Risk Rating. The

mutual fund ratings are generally graded on

a scale of one star to five stars, one being

the poorest and five being the best. These

ratings have been in vogue for more than a

decade and are an indicator of the fund’s

performance and consistency. Also known as

star ratings, it is designed to help investors to

arrive at purchase decisions for their

portfolios. Mutual fund ratings can make or

break the success of a mutual fund. With the

rating business blossoming to a million dollar

industry, the impact to the end investor

cannot be ignored. While mutual fund ratings

can help in arriving at an informed decision

making, there are some points that need

extra consideration. Read on to understand

them better:

1. Higher ratings doesn’t always

guarantee higher returns

In the mutual fund investment scenario, a

fund with higher ratings can be illusive.

Analysis of other factors in the mutual fund

such as – its performance trend, immediate

7

In This IssueTrending

Topics

Due Date

Chart

Notifications

& Circulars

Seminars and

CoursesAbout Us

future returns, investment strategy, its relative

risk strategy and its indicative performance in

bull and bear market conditions is vital. A

balanced decision taken after consideration of

the variables makes the portfolio more

comprehensive and sound.

2. Goal alignment and portfolio

Align the portfolio based on the time identified

goals. For short term goals or financial

requirements, equity investments might not

guarantee returns. Majority of the investors

assume that mutual funds are only about

investing in equities and therefore end up

investing higher amounts in equity funds.

Though such funds may be rated 5 stars, they

tend to be more volatile and erratic in fetching

returns and are not the best bid for short term

set of goals.

3. Fund strategy

The key to investing in mutual funds is to

discern the strategy of the fund. When we buy

or invest in a fund, we should understand what

it does, and articulate its entry and exit

strategy. This enables in evaluation of fund’s

performance and to build a portfolio of funds

that work together. Each mutual fund category

adopts a different strategy. The performance of

a fund is also dependent on the role of the

fund manager. The strategy adopted by the

fund manager needs careful understanding -

such as de-concentration of funds by dis

investing large cap funds and increased fund

flow into mid cap funds, stoppage in cash calls

etc. Use diligence in deciding between large/

small-cap equity/short-term/ long-term bond.

4. Availability of the fund manager

The exit of the fund manager does not always

signal red. Different mutual fund houses have

varied investing cultures, and with the right

institutional processes, the absence or

unavailability of a fund manager does not carry

a huge impact to the end investor. In case of a

change in the fund manager it would be more

In This IssueTrending

Topics

Due Date

Chart

Notifications

& Circulars

Seminars and

CoursesAbout Us

prudent to keep the fund on a watch list for a

couple of quarters and compare its

performance rather than exiting immediately.

There have also been instances were a fund

has been downgraded due to the exit of its

fund manager who solely managed the affairs

and the past performance and star ratings get

skewed.

5. Rating comparisons across time

horizons

Ratings are awarded to the fund schemes,

based on the performance of the portfolio for a

specified period of time. The number of years

the fund has been in existence and the stars

earned is a performance indicator of the fund.

Hence, comparison needs to be made on the

basis of both factors, as a 5 star rated fund

which is 10 years old is more consistent in

returns than a 5 star rated, 3 year old fund.

There is no one investment plan that is fool

proof. It requires informed decision making

through research and structured planning.

“Destiny is not a matter of chance; it is a

matter of choice. It is not a thing to be waited

for; it is a thing to be achieved.” - William

Jennings Bryan.

Mutual fund investing is not matter to be left in

the hands of destiny; it is the result of

conscious choice. With the right decisions it

can make money work for you.

Caclubindia.com

Instruments of Investments in

Foreign Direct Investment (FDI)

Equity Shares

The Indian Company can issue equity shares

in accordance with the provisions of the

Companies Act, as applicable, shall include

equity shares that have been partly paid,

subject to pricing guidelines/valuation norms

prescribed under FEMA Regulations

Preference Shares

The Indian Company can issue Fully,

compulsorily & mandatorily convertible

preference shares subject to pricing

guidelines/valuation norms prescribed under

FEMA Regulations. Preference shares shall

be required to be fully paid, and should be

mandatorily and fully convertible.

Debenture

Condition

The Indian Company can issue above

mentioned securities subject to pricing

guidelines/valuation norms prescribed under

FEMA Regulations.

Price Guidelines

The price/conversion formula of convertible

capital instruments should be determined

upfront at the time of issue of the

instruments.

The price at the time of conversion should

not in any case be lower than the fair value

worked out, at the time of issuance of such

instruments, in accordance with the extant

FEMA regulations.

Warrant: Fully, compulsorily and

mandatorily convertible Warrant.

Further, ‘warrant’ includes Share Warrant

issued by an Indian Company in accordance

to provisions of the Companies Act, 2013

subject to terms and conditions as stipulated

by the Reserve Bank of India in this behalf,

from time to time.

A. When Company will determine the price

or conversion formula of convertible

Instrument?

The Company will determine the price or

conversion formula of convertible Instrument

at the time of issue of the instruments.

B. Whether price can be lower than the fair

value worked out at the time of issuance of

such instrument?

The price at the time of conversion should not

in any case be lower than the fair value

worked out, at the time of issuance of such

instruments.

In This IssueTrending

Topics

Due Date

Chart

Notifications

& Circulars

Seminars and

CoursesAbout Us

12

In This IssueTrending

Topics

Due Date

Chart

Notifications

& Circulars

Seminars and

CoursesAbout Us

10

C. Whether Optionality clauses are allowed

to holder of Equity/ Preference shares and

debentures?

Yes, Optionality clauses are allowed in equity

shares, fully, compulsorily and mandatorily

convertible debentures and fully, compulsorily

and mandatorily convertible preference shares

under FDI scheme, subject to the following

conditions:

Condition: There is a minimum lock-in period

of one year which shall be effective from the

date of allotment of such capital instruments.

After the lock-in period and subject to FDI

Policy provisions, if any, the non-resident

investor exercising option/right shall be eligible

to exit without any assured return, as per

pricing/valuation guidelines issued by RBI from

time to time.

D. Whether Indian Company can issue Non-

Convertible/ optionally convertible/ Partly

Convertible Preference Shares/ Debentures

to Foreign Investors under FDI?

No, Indian Company can’t issue Non-

Convertible/ optionally convertible or Partly

Convertible Preference Shares or Debentures

to Foreign Investors under FDI.

If Company will issue the same and received

the fund will be consider as Debt. Accordingly

all norms applicable for ECBs relating to eligible

borrowers, recognized lenders, amount and

maturity, end-use stipulations, etc. shall apply.

DRs and FCCBs

The inward remittance received by the Indian

company vides issuance of DRs and FCCBs

are treated as FDI and counted towards FDI.

Conditions:

i. FCCBs/DRs may be issued in accordance

with the Scheme for issue of Foreign

Currency Convertible Bonds and Ordinary

Shares (Through Depository Receipt

Mechanism) Scheme, 1993 and DR

Scheme 2014 respectively, as per the

guidelines issued by the Government of

India there under from time to time.

ii. DRs are foreign currency denominated

instruments issued by a foreign

Depository in a permissible jurisdiction

against a pool of permissible securities

issued or transferred to that foreign

depository and deposited with a

domestic custodian.

iii. A person can issue DRs, if it is eligible to

issue eligible instruments to person

resident outside India under Schedules

1, 2, 2A, 3, 5 and 8 of Notification No.

FEMA 20/2000-RB dated May 3, 2000,

as amended from time to time.

iv. The aggregate of eligible securities

which may be issued or transferred to

foreign depositories, along with eligible

securities already held by persons

resident outside India, shall not exceed

the limit on foreign holding of such

eligible securities under the relevant

regulations framed under FEMA, 1999.

v. The pricing of eligible securities to be

issued or transferred to a foreign

depository for the purpose of issuing

depository receipts should not be at a

price less than the price applicable to a

corresponding mode of issue or transfer

of such securities to domestic investors

under the relevant regulations framed

under FEMA, 1999.

vi. In terms of Notification No. FEMA.20/

2000-RB dated May 3, 2000 as amended

from time to time, a person will be eligible

to issue or transfer eligible securities to a

foreign depository, for the purpose of

converting the securities so purchased

into depository receipts in terms of

Depository Receipts Scheme, 2014 and

guidelines issued by the Government of

India there under from time to time.

vii. The issue of depository receipts as per

DR Scheme 2014 shall be reported to the

Reserve Bank by the domestic custodian

as per the reporting guidelines for DR

Scheme 2014.

ADR & GDR

Two-way Fungibility Scheme

i. A limited two-way Fungibility scheme has

been put in place by the Government of

India for ADRs/GDRs.

ii. Under this Scheme, a stock broker in

India, registered with SEBI, can purchase

shares of an Indian company from the

market for conversion into ADRs/GDRs

based on instructions received from

overseas investors.

11

In This IssueTrending

Topics

Due Date

Chart

Notifications

& Circulars

Seminars and

CoursesAbout Us

iii. Re-issuance of ADRs/GDRs would be

permitted to the extent of ADRs/GDRs

which have been redeemed into

underlying shares and sold in the Indian

market.

Sponsored ADR/GDR issue

i. An Indian company can also sponsor an

issue of ADR/GDR.

ii. Under this mechanism, the company

offers its resident shareholders a choice to

submit their shares back to the company

so that on the basis of such shares,

ADRs/GDRs can be issued abroad.

iii. The proceeds of the ADR/GDR issue are

remitted back to India and distributed

among the resident investors who had

offered their Rupee denominated shares

for conversion.

iv. These proceeds can be kept in Resident

Foreign Currency (Domestic) accounts in

India by the resident shareholders who

have tendered such shares for conversion

into ADRs/GDRs.

Caclubindia.com

DUE DATE CHART

In This IssueTrending

Topics

Due Date

Chart

Notifications

& Circulars

Seminars and

CoursesAbout Us

13

In This IssueTrending

Topics

Due Date

Chart

Notifications

& Circulars

Seminars and

CoursesAbout Us

DUE DATE CHART (August 2016)

Due Date Category Particulars Form/Challan/Site

06-Aug-16

Central Excise

Payment

Payment for the month July

2016 (Non SSI)www.aces.gov.in

Service TaxPayment for the month July

2016 (For Companies) www.aces.gov.in

07-Aug-16TDS/ TCS

Payment

TDS Payment for the month

July 2016Challan 281

10-Aug-16Central Excise

Return

Return for the month July 2016

for All Assessee (Non SSI)www.aces.gov.in

15-Aug-16 Provident Fund

Payment for the Month

July 2016www.epfindia.com

Declaration of new Employees

for the month July 2016Form No. 11

21-Aug-16Employee State

Insurance (ESI)

Payment for the month

July 2016www.esic.in

25-Aug-16 Provident FundReturn for the month

July 2016 www.epfindia.com

30-Aug-16 ESIC Return of contributions www.epfindia.com

NOTIFICATIONS

AND CIRCULARS

In This IssueTrending

Topics

Due Date

Chart

Notifications

& Circulars

Seminars and

CoursesAbout Us

In This IssueTrending

Topics

Due Date

Chart

Notifications

& Circulars

Seminars and

CoursesAbout Us

Notification/ Circular Reference No.

Exemption from TDS to Securitization Trust on

Income received from activity of Securitization

Notification No. 46/2016,

dated 1706-2016

Exemption from TDS on specified payments made to

banks etc.

The Central Government deriving power under section

197A(1F) has notified that no deduction of tax shall be

made on the payments of the nature specified below, in

case such payment is made by a person to a bank listed

in the Second Schedule to the Reserve Bank of India Act,

1934, excluding a foreign bank, or to any payment

systems company authorized by the Reserve Bank of

India under Section 4(2) of the Payment and Settlement

Systems Act, 2007.

Notification No. 47/2016,

dated 17-062016

Relaxation from deduction of tax at higher rate under

section 206AA

Notification No 53/2016,

dated 24-06-2016

Information contained in valid declarations under the

Income Declaration Scheme, 2016 to be kept

Confidential

Notification No 56/2016,

dated 06-072016

Clarifications on the Income Declaration Scheme,

2016 via issue of FAQs

Circular No. 24/2016,

Dated 27-06-2016 and

Circular No 25/2016,

Dated 30-062016

Threshold Limit of tax audit under section 44AB and

section 44AD

Section 44AB of the Income-tax Act makes it obligatory

for every person carrying on business to get his accounts

of any previous year audited if his total sales, turnover or

gross receipts exceed Rs. 1 Crore. However, if an eligible

person opts for presumptive taxation scheme as per

section 44AD(1), he shall not be required to get his

accounts audited if the total turnover/ gross receipts of the

relevant previous year does not exceed two crore rupees.

Press Release,

dated 20-06-2016

Relaxation of time schedule for making payments

under the Income Declaration Scheme 2016

Press Release,

dated 14-07-2016

Direct Tax Law

15 Source: ICAI e-Journal

In This IssueTrending

Topics

Due Date

Chart

Notifications

& Circulars

Seminars and

CoursesAbout Us

16 Source: ICAI e-Journal

Indirect Tax LawNotification/ Circular Reference No.

Services Provided prior to 31st May 2016 exempt

from Krishi Kalyan Cess (KKC)

Notification No. 35/2016-

ST dated June 23, 2016

Transportation of goods by a vessel from outside

India upto the customs station in India prior to

31st May 2016 exempt from Service Tax

Notification No. 36/

2016-Service Tax,

Dated: June 23, 2016

Sale of goods at Duty Free Shops in Indian Currency

Central Government vide Circular No. 31/2016-

CUSTOMS, Dated: July 6, 2016 has provided that the

passengers are now permitted to purchase goods at duty

free shops in Indian rupees up to an amount not

exceeding Rs.25,000 as against earlier limit of Rs.5,000.

Circular No. 31/2016-

CUSTOMS,Dated: July

06, 2016

Procedure for accounting storage etc. for Duty Free

Shops

Central Government vide Circular No. 32/2016-

CUSTOMS, Dated: July 13, 2016 has prescribed a

system of accounting of receipt, storage, operations and

removal of goods with regard to Duty Free Shops.

Circular No. 32/2016-

CUSTOMS, Dated: July

13, 2016

Amendment in Import of Goods at Concessional Rate

for manufacture of excisable goods rules

Notification No. 100/

2016-Customs (NT),

Dated: July 14, 2016

Recovery of confirmed demands during the pendency

of stay application

Circular No.

1035/23/2016-CX

dated July 4, 2016

Honnavar port in Karnataka appointed for unloading

of imported goods and loading of export goods

Notification No. 97/2016-

CUSTOMS (NT), Dated:

July 8, 2016

Time limit for taking Registration under Central

Excise by Jewellers

Circular No.

1033/21/2016-CX

dated July 1, 2016

Procedure for supply of bunker fuels to Indian

vessels carrying containerized cargo

Notification No. 31/2016-

Central Excise (N.T.),

Dated: July 4, 2016

In This IssueTrending

Topics

Due Date

Chart

Notifications

& Circulars

Seminars and

CoursesAbout Us

17

Others (MCA/ SEBI/ RBI)Notification/ Circular Reference No.

Companies (cost records and audit) Amendment

Rules, 2016

The amendments deal with aspects like definition of cost

audit report, certifications before appointment of cost

auditor, provisions for removal of cost auditor, filing of

returns with ROC etc. The amendments also deal with

applicability of cost records and audit to certain industries.

For complete text of the notification, please refer the link:

http://www.mca.gov.in/Ministry/pdf/Rules_15072016.pdf

MCA notification no.

G.S.R(E) dated

14th July 2016

Revised Formats for Financial Results and

Implementation of Ind-AS by Listed Entities

The circular specifies formats for declaration of

Unaudited/Audited quarterly financial results by the listed

companies. It also lays down detailed guidelines with

respect to Implementation of Ind-AS during the first year

i.e. financial year 2016-2017 and various other

clarifications on issues with regard to Ind-AS

implementation. For complete text of the circular, please

refer the link:

http://www.sebi.gov.in/cms/sebi_data/attachdocs/1467712

561526.pdf

SEBI circular no.

CIR/CFD/FAC/62/2016

dated 5th July 2016

Implementation of Indian Accounting Standards

(Ind AS)

RBI has directed that Banks shall refer to the Report of

the Working Group on “Implementation of Ind AS by

Banks in India”. The Proforma Ind AS Financial

Statements shall include the Balance Sheet including

Statement of Changes in Equity, Profit and Loss Account

and Notes. The circular also lays down the various

disclosure requirements for significant accounting policies

and the approach on exemptions under Ind AS 101 First

Time Adoption of Indian Accounting Standards. For

complete text of the circular, please refer the link:

https://rbi.org.in/Scripts/NotificationUser.aspx?Id=10456&

Mode=0

Source: ICAI e-Journal

SEMINARS AND

COURSES

In This IssueTrending

Topics

Due Date

Chart

Notifications

& Circulars

Seminars and

CoursesAbout Us

In This IssueTrending

Topics

Due Date

Chart

Notifications

& Circulars

Seminars and

CoursesAbout Us

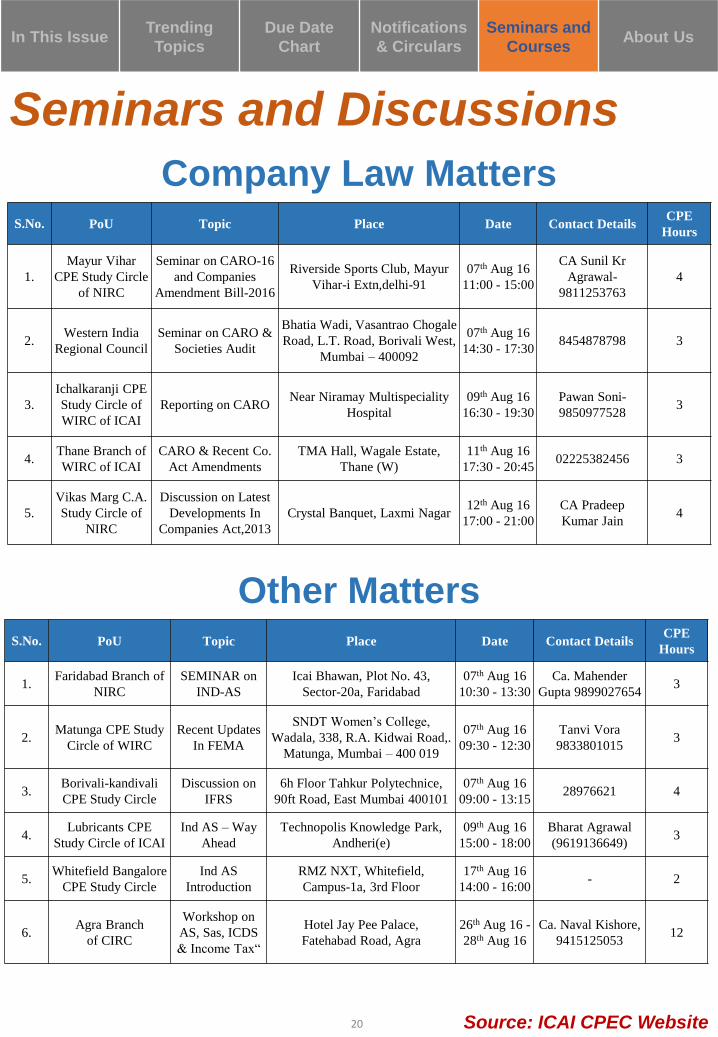

Seminars and Discussions

Taxation Matters

19 Source: ICAI CPEC Website

S.No. PoU Topic Place Date Contact DetailsCPE

Hours

1.

Urban Estate

CPE Study Circle

of Faridabad

Service Tax And

Foreign Trade Policy

Hotel Delite, Neelam Bata

Road, Faridabad

07th Aug 16

10:00 - 13:00

CA Manoj Gupta

(M) 9810182124, 3

2.

Laxmi Nagar

CPE Study Circle

of NIRC

GST (Goods And

Service Tax)

Lagan Banquet Hall. Nirman

Vihar, Near Metro Station,

Delhi 110092.

07th Aug 16

12:15 - 14:15

CA Mukesh

Kumar Singh4

3.

VIP Road CAs

Study Circle of

EIRC

GST Model Law –

The Way Ahead

220, Bangur Avenue, Block-a,

Ground Floor, Kolkata-700055

07th Aug 16

10:00 - 13:00

Ca. Rahul Rungta

93310398623

4.Nashik Branch of

WIRC

Workshop on Tax &

Corporate Audit

Nashik Branch of WIRC of

ICAI, ICAI Bhawan, Ashoka

Marg, Nashik

07th Aug 16

10:00 - 17:30

0253 2236107/

22360126

5.

Joshi Road CPE

Study Circle of

NIRC

Commodity Code,

Vat, Service Tax, Gst

Hotel Swati Dx, Opp Jassa Ram

Hospital, Gurdwara Road, Karol

Bagh, New Delhi – 110005

08th Aug 16

17:00 - 22:00

Ca Shravan Suri,

98730231135

6.Palghat Branch

of SIRCNRI Taxation

Icai Bhawan, Indrani Nagar,

Chunnambuthara

08th Aug 16

17:30 - 20:30Ca Arun A 3

7.

ACAE CAs

Study Circle of

EIRC

Practical Issues In E-

filling of TDS Returns

And IT Returns

6, Lyons Range, 3rd Floor, Unit-

2, Kolkata-700001

08th Aug 16

17:00 - 20:00- 3

8.

East End CA

Study Circle of

NIRC

Seminar on The

Concept of “TAX

AUDIT & GST”

Scope Minar,auditorium,back

Side of V3S Mall,laxmi

Nagar,delhi-110092

09th Aug 16

17:30 - 21:30- 4

9.Bangalore

Branch of SIRC

HUF -Latest Tax

Issues

Bangalore Branch of SIRC of

ICAI

10th Aug 16

18:00 - 20:00

Ms.Geethanjali D

080-305635132

10.Trichur Branch

of SIRC

Seminar on Goods

and Service Tax

Icai Bhawan, Alum Vettu

Vazhi Chiyyaram

13th Aug 16

09:30 - 12:300487-2253400 6

11.

Masjid Bunder

CPE Study Circle

of WIRC

Taxation Impact on

LLP

Roman Vision Banquet

Hall,99/101, 3rd Floor, Above

Vijay Transport, Mumbai - 09

18th Aug 16

17:30 - 20:30

Pratik Doshi

98705609503

12.

MII Powai Lake

CPE Study Circle

of ICAI

MVAT Updates &

Sales Tax Amnesty

Scheme 2016

MTNL-CETTM, Technology

Street, Hiranandani Gardens,

Powai, Mumbai– 400076

20th Aug 16

15:00 - 18:00

CA Santosh

Agarwal

9930367339

3

In This IssueTrending

Topics

Due Date

Chart

Notifications

& Circulars

Seminars and

CoursesAbout Us

20 Source: ICAI CPEC Website

Other Matters

Seminars and Discussions

Company Law MattersS.No. PoU Topic Place Date Contact Details

CPE

Hours

1.

Mayur Vihar

CPE Study Circle

of NIRC

Seminar on CARO-16

and Companies

Amendment Bill-2016

Riverside Sports Club, Mayur

Vihar-i Extn,delhi-91

07th Aug 16

11:00 - 15:00

CA Sunil Kr

Agrawal-

9811253763

4

2.Western India

Regional Council

Seminar on CARO &

Societies Audit

Bhatia Wadi, Vasantrao Chogale

Road, L.T. Road, Borivali West,

Mumbai – 400092

07th Aug 16

14:30 - 17:308454878798 3

3.

Ichalkaranji CPE

Study Circle of

WIRC of ICAI

Reporting on CARONear Niramay Multispeciality

Hospital

09th Aug 16

16:30 - 19:30

Pawan Soni-

98509775283

4.Thane Branch of

WIRC of ICAI

CARO & Recent Co.

Act Amendments

TMA Hall, Wagale Estate,

Thane (W)

11th Aug 16

17:30 - 20:4502225382456 3

5.

Vikas Marg C.A.

Study Circle of

NIRC

Discussion on Latest

Developments In

Companies Act,2013

Crystal Banquet, Laxmi Nagar12th Aug 16

17:00 - 21:00

CA Pradeep

Kumar Jain4

S.No. PoU Topic Place Date Contact DetailsCPE

Hours

1.Faridabad Branch of

NIRC

SEMINAR on

IND-AS

Icai Bhawan, Plot No. 43,

Sector-20a, Faridabad

07th Aug 16

10:30 - 13:30

Ca. Mahender

Gupta 98990276543

2.Matunga CPE Study

Circle of WIRC

Recent Updates

In FEMA

SNDT Women’s College,

Wadala, 338, R.A. Kidwai Road,.

Matunga, Mumbai – 400 019

07th Aug 16

09:30 - 12:30

Tanvi Vora

98338010153

3.Borivali-kandivali

CPE Study Circle

Discussion on

IFRS

6h Floor Tahkur Polytechnice,

90ft Road, East Mumbai 400101

07th Aug 16

09:00 - 13:1528976621 4

4.Lubricants CPE

Study Circle of ICAI

Ind AS – Way

Ahead

Technopolis Knowledge Park,

Andheri(e)

09th Aug 16

15:00 - 18:00

Bharat Agrawal

(9619136649)3

5.Whitefield Bangalore

CPE Study Circle

Ind AS

Introduction

RMZ NXT, Whitefield,

Campus-1a, 3rd Floor

17th Aug 16

14:00 - 16:00- 2

6.Agra Branch

of CIRC

Workshop on

AS, Sas, ICDS

& Income Tax“

Hotel Jay Pee Palace,

Fatehabad Road, Agra

26th Aug 16 -

28th Aug 16

Ca. Naval Kishore,

941512505312

In This IssueTrending

Topics

Due Date

Chart

Notifications

& Circulars

Seminars and

CoursesAbout Us

21

Batches for Upcoming

Courses

International Financial Reporting (IFRS)

Methodology: The participants are required to

devote time in self-study and case studies.

Participants may be grouped for preparing the

case study, Self-study, case study and

Evaluation Test for successful completion of the

course.

Duration of the Course: Class-room Study of

60 Hours - 12 days Course Saturday & Sunday

(9:30 AM to 5:30 PM)

Evaluation Test: IFRS Certification Course

exam is conducted on second Sunday of March,

June, September and December.

Examination Dates - Year 2016

Quarter 1 - March 13, 2016 (N.A.)

Quarter 2 - June 12, 2016 (N.A.)

Quarter 3 - September 11, 2016

Quarter 4 - December 11, 2016

Certificate on completion of the Course:

A certificate will be awarded to the participants

after attending and satisfactorily completing the

course and passing the certification exam.

Minimum No. of Seats: 30

CPE Hours: 60 Hours (60 Structured)

ICAI Webstie

The International Financial Reporting Standards

(IFRS) issued by International Accounting

Standards Board (IASB) are gaining recognition

as Global Reporting Standards. The Council of

the Institute of Chartered Accountants of India,

while appreciating the emerging diversities and

complexities in the world of accounting and the

need for knowledge of IFRS in relation to the

convergence of the Indian Accounting

Standards with IFRS, has decided to launch a

Certificate Course on International Financial

Reporting Standards for its members. The

objective of this Course is to enhance the

knowledge as well as to provide benefit to the

members in the global service market.

The Course aims at providing:

• Introduction of the concepts of IFRS

• Dissemination of knowledge on IFRS;

• Comparison of IFRS with existing Indian

Accounting Standards;

• Issues in relation to IFRS;

• Conversion of Financial Statements prepared

on the basis of Indian GAAP to IFRS based

financial statements.

Apart from the comprehensive theoretical

aspects, this course, the first of its kind in India,

will sharpen the expertise and excellence of our

members through multiple case studies across

the industry and service sector.

Fees: Rs 30,000

Eligibility for the Course: Members of ICAI

The fees can be paid either by a Demand draft,

Pay Order or through online mode. The demand

draft/ pay order shall be drawn in favour of the

"Secretary, The Institute of Chartered

Accountants of India, payable at New Delhi."

Certificate Course on Forex

and Treasury Management

Course Duration

Classes will be for Eight days. (Weekends only)

Saturday and Sunday (10.00 a.m. to 5.00 p.m.)

Attendance

Compulsory 75% attendance is required.

Professional Credit

The participants to this course will be given 30

CPE Hrs after successful completion of the

course.

Course Fees

Rs. 17,500/-* per member for the complete

course. The fees also includes examination fee

for the first attempt. The candidate who does

not appear or fails to clear the examination is

required to pay an examination fee of Rs.

2,000/- in the subsequent attempt. The fees can

be paid vide DD/Cheque in favour of “The

Secretary, The Institute of Chartered

Accountants of India” Payable at New Delhi.

Course fee can also be paid online through ICAI

Payment portal.

ICAI Webstie

In This IssueTrending

Topics

Due Date

Chart

Notifications

& Circulars

Seminars and

CoursesAbout Us

About the Course

The Committee on Financial Market and

Investors’ Protection (CFMIP) is one of the

Non-Standing Committees of the ICAI which

conducts Certificate Course on Forex and

Treasury Management (FXTM) for professional

development of members in this field. This

course covers foreign exchange market,

money market, bond market operations and

related financial products. It therefore analyses

the international finance environment within

which banks, other intermediaries and

companies operate and how it affects their

operations in treasury. Sound treasury

management utilizes the right financial

products and tools for minimizing risk. The

course examines alternative strategies and

techniques that can be employed to manage

the risks associated with international business

transactions and other treasury operations. It

also provides an overview of the structure and

key functions of the treasury.

Eligibility

Only the Members of ICAI and the Students of

the Institute who have passed the CA Final

Examination are eligible to pursue this course.

ABOUT US

In This IssueTrending

Topics

Due Date

Chart

Notifications

& Circulars

Seminars and

CoursesAbout Us

S.P. Chopra & Co. is a professional services firm established in

1949; Ranking amongst the top 20 firms in India

11 full time partners and staff strength of over 100

Offices in New Delhi, Mumbai, Canada and Dubai

Our firm offers Accounting, Assurance and Consultancy as its core business

lines for domestic and global businesses of medium to large size.

We have been empanelled with Reserve Bank of India, Royal Audit

Authority of Bhutan, United Nations and World Bank. We are also a

member of the Prime Global (an independent association of more than

350 accounting firms all over the World).

24

In This IssueTrending

Topics

Due Date

Chart

Notifications

& Circulars

Seminars and

CoursesAbout Us

25

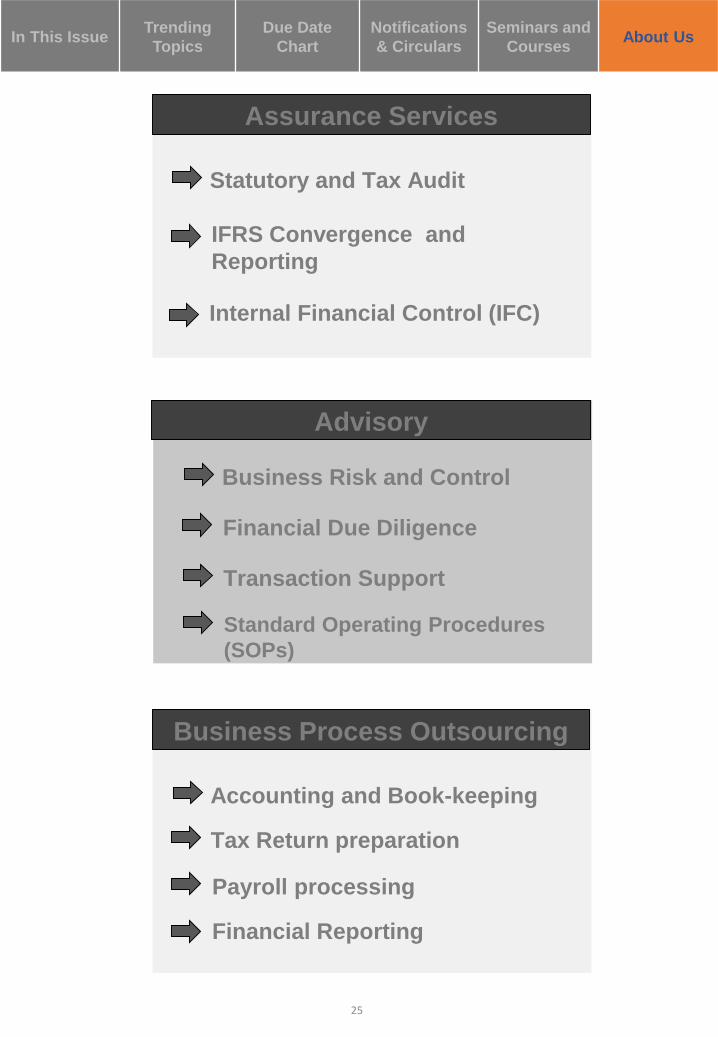

Business Process Outsourcing

Accounting and Book-keeping

Tax Return preparation

Payroll processing

Financial Reporting

Advisory

Business Risk and Control

Standard Operating Procedures

(SOPs)

Financial Due Diligence

Transaction Support

Assurance Services

Statutory and Tax Audit

IFRS Convergence and

Reporting

Internal Financial Control (IFC)

In This IssueTrending

Topics

Due Date

Chart

Notifications

& Circulars

Seminars and

CoursesAbout Us

26

Mob: 9899110300