Embed Size (px)

Citation preview

News U Can Use

4th July2014

The Week that was…

28th June to 4th July

Indian Economy India's annual infrastructure sector output growth slowed to 2.3% in May from 4.2% in the

previous month, weighed down by declines in the production of crude oil, natural gas,

petroleum and steel.

India's fiscal deficit in the first two months of the financial year touched Rs 2.41 lakh cr, or

45.6% of the full-year target.

India’s retail inflation for industrial workers remained almost flat at 7.02% in May compared

to 7.08% in April mainly due to lower price of petrol.

RBI data shows India attracted $37.8 bn foreign investment between January and March;

India's total external debt stood at $440.6 bn at the end of March, up 7.6% from the end of

March 2013.

India’s HSBC manufacturing PMI rose marginally from 51.4 in May to 51.5 in June, while

services PMI rose to a 17-month peak of 54.4 in June from a reading of 50.2 in May.

World Bank’s India director Onno Ruhl says inflation is still uncomfortably high in the country

and that the new government should avoid fiscal slippage as it seeks to revive the economy.

Rating agency S&P's says implementing the proposed regime to resolve problems of

distressed financial institutions in India will test political will as it needs drastic changes in

laws and regulations.

Rating agency Fitch says India's economic growth will accelerate to 5.5% this financial year

and 6.5% in FY16 due to the clear mandate received by the government.

Source: Crisil Weekly Market Update

Indian Debt Market G-sec yields eased during the week as geopolitical concerns in Iraq eased and global crude

oil prices came down, which saw investors and traders built GSec positions ahead of the

budget week. The ten year benchmark closed the week at 8.66% as against 8.75% in the

previous week.

Sentiment was also boosted by news flow around a possible reallocation of FII government

debt investment limits from the currently underutilized portion in the segment reserved for

long term investors to the almost fully utilized general FII limit segment. If this increase in

limit materializes, it can attract greater FII inflows, especially if the measures in the budget

play out as anticipated.

Fall in crude oil prices and hope of better monsoons going forward also aided the positive

sentiments in the market.

Liquidity in the system was very easy during the week with overnight rates trading below the

repo rate most part of the week.

Source: RBI,RMF Estimates

Indian Debt Market In G-sec auction, RBI auctioned G-Sec (Rs 15000 cr) in following four securities namely –

8.35% GS 2022 (Rs 3,000 cr), 8.60% GS 2028 (Rs 7,000 cr), 9.20% GS 2030 (Rs 3,000 cr)

and 9.23% GS 2043 (Rs 2,000 cr) with cut-off yield of 8.70%, 8.57%, 8.69% and 8.68%

respectively. There was no devolvement in any of the securities.

In T-bill auction, RBI auctioned 91 days T-bills (Rs 8000 cr) and 180 days T-bills (Rs 6000

cr) with cut-off yield of 8.52% (Previous : 8.56%) and 8.68% (Previous : 8.64% )

respectively.

This week, RBI will auction 91 days T-bill (Rs 9000 cr) and 364 days T-bill (Rs 6000 cr) on

July 9, 2014.

Source: RBI,RMF Estimates

Indian Commodities Market

Crude oil prices retreated in the week as fears over supply disruption by Iraq eased; prices

ended at $104.06 a barrel on the NYMEX on July 3, compared with $105.84 a barrel on

June 26.

US crude oil inventories fell 3.2mn barrels to 384.9mn barrels for the week ended June 27.

Source: Crisil Weekly Market Update

Indian Government

India inks pacts with China to build industrial parks and attract Chinese investment, share

flood data of the Brahmaputra river, and establish a framework for regular interactions

between the two nations’ administrative officials.

India refuses to sign the trade facilitation pact with the World Trade Organization; pushes for

finding a long term solution to the food security issue in the country.

Government plans solar and wind power projects in deserts, entailing an investment of over

Rs 2 lakh cr by 2022.

Foreign Investment and Promotion Board clears six FDI proposals with estimated

investments of Rs 551 cr.

Government hikes price of non-subsidised cooking gas (LPG) by Rs 16.50 per cylinder and

that of jet fuel by over 0.5%.

Government estimates that the hike in the price of non-subsidized cooking gas will impact

less than 1% customers, as most do not use the quota of 12 subsidized cylinders per year.

Government extends the validity period of industrial licence to three years with a provision

for further extension of two years to improve ease of doing business in India.

Government hikes minimum export price (MeP) on onions to $500 a tonne fom $300 a

tonne to arrest rise in domestic prices of the edible bulb.

Government defers the upward revision of prices for domestic LPG and kerosene in some

states by a month.

Source: Crisil Weekly Market Update

Indian Government

Government inks a $500mn loan agreement with the World Bank for National Highways Inter-

connectivity Improvement Project.

Government agrees to extend the benefits of special economic zones (SEZ) and National

Investment and Manufacturing Zones (NIMZ) to the proposed industrial parks which would be

developed in collaboration with China.

French government proposes giving India a 1bn euro credit line to fund sustainable

development projects.

India makes a fresh request to Switzerland seeking bank details and names of Indians having

unaccounted money in Swiss banks.

The Project Monitoring Group under the Cabinet Secretariat decides to digitise all

applications for clearances relating to forest, environment and others by March 2015.

Government to auction unutilised investment limits in government debt worth Rs 5516 cr to

foreign investors on July 1.

Finance Ministry mulls doubling the exemption limit for investments by individuals in financial

instruments to Rs 2 lakh to boost household savings.

Coal Ministry rejects the power ministry's plea to allow medium and short-term electricity

purchase agreements to secure fuel linkages.

Source: Crisil Weekly Market Update

Indian Government

India and Bangladesh governments approve setting up of four more border haats along the

Indo-Bangla border in Meghalaya with an aim of increasing bilateral trade and improve living

conditions of border residents.

Food Ministry seeks approval to end the subsidy for raw sugar exports one year earlier as it

is being availed only by a few sugar mills.

Government plans to use the cable television service providers as franchisee network to

increase broadband penetration.

Panel headed by Former PMEAC chief C Rangarajan submits report on Tendulkar

Committee methodology for estimating poverty to Planning Commission.

Union ministry of power agrees to allocate an additional 177 Mw of power from NTPC's

Jajjar power plant to Andhra Pradesh.

Government proposes setting up a special economic zone for the Indian chemical industry

in Myanmar and Iran.

Government plans to revise the Real Estate Regulatory Bill, 2013, aiming to have increased

participation from the private sector.

Source: Crisil Weekly Market Update

Regulatory updates in India

RBI directs banks to give data about wilful defaulters every month or more frequently to the

credit information companies from the beginning of 2015.

RBI restores the limit on Indian corporates’ overseas direct investments under the automatic

route to 400% of networth, compared with the earlier limit of 100%.

RBI keeps the lending rate ceiling for micro finance companies unchanged at 27.75% for the

July to September quarter.

RBI switches to using an electronic bond trading platform to manage cash levels in the debt

market.

RBI to conduct a 4-day term reverse repo variable rate auction for a notified amount of Rs

20,000 cr on July 3.

RBI deputy governor R Gandhi says the banking regulator plans to issue guidelines for on-

tap and differentiated banking licenses later this year.

SEBI and other regulators plan to put in place a Common Reporting Standard (CRS) for all

financial institutions to facilitate an automatic exchange of suspicious trades and other

information through a global pool.

SEBI says investors with inactive accounts - with zero balance and no trades for a year - will

now get their physical annual account statements upon request from the second year.

Source: Crisil Weekly Market Update

Regulatory updates in India

A circular issued by SEBI says Indian financial institutions operating out of the US can now

register with the American tax authorities before December 31, 2014 as per the Foreign

Account Tax Compliance Act (FATCA).

SEBI imposes cumulative fines of Rs 76 cr on Taksheel Solutions and 15 other entities in a

case related to alleged irregularities in the company's IPO.

SEBI grants three months more time to bring supervisory and monitoring framework

pertaining to issuance and processing of Delivery Instruction Slips into force, taking into

account the grievances of depository participants.

Securities Appellate Tribunal upholds penalty of Rs 11 cr imposed by SEBI on Reliance

Petroinvestments last year for insider trading.

According to AMFI data, mutual funds’ assets under management rose to Rs 9.85 lakh cr in

the first quarter of current fiscal, compared with Rs 9.05 lakh cr in the previous quarter.

Industry body AMFI says total asset base of mutual funds could reach Rs 20 lakh cr in the

next 4-5 years from about Rs 9.85 lakh cr currently.

Retirement fund body EPFO launches online registration facility for employers, a move that

will help firms get employers' code within a day.

Source: Crisil Weekly Market Update

Regulatory updates in India

Telecom Disputes Settlement & Appellate Tribunal (TDSAT) quashed a penalty of Rs 72 cr

imposed on RCom for delayed submission of customer acquisition forms in the Madhya

Pradesh circle for 2011-12.

Comptroller & Auditor General of India (CAG) rejects telecom department’s stand allowing

Reliance Jio to offer voice services using broadband spectrum.

Oil regulator PNGRB extends the bid deadline for licences to retail CNG and piped cooking

gas in 14 cities, including Bengaluru and Pune, by one month to August 11.

Supreme Court asks SEBI to come up with safeguards to verify the transparency in the sale

of properties of the Sahara Group, meant to secure funds for the release of its chairman

Subrata Roy from prison.

Supreme Court orders BSES Yamuna Pvt Ltd to pay its outstanding dues for the first 6

months of 2014 to power generating and transmission companies before July 15.

Supreme Court dismisses a petition challenging the former government's decision in 2012 to

sell its stake in Hindustan Zinc Ltd (HZL) to Vedanta Group.

Source: Crisil Weekly Market Update

International Markets US non-farm payrolls rose by a seasonally adjusted 288,000 in June following an upwardly

revised 224,000 in May; the unemployment rate ticked down to a five-and-a-half year low of

6.1% in June from 6.3% in May.

US Pending Home Sales rose 6.1% in May to 103.9, compared to April’s upwardly revised

reading of 97.9.

US manufacturing PMI increased to 57.3 in June, the highest in more than four years, from

56.4 a month earlier.

US Institute for Supply Management (ISM) index of national factory activity came in at 55.3

in June, almost unchanged from May's 55.4 reading.

US industry-wide auto sales rose 1.2% to 1.4mn in June, pushing the annualized selling rate

to 16.98mn.

US ADP report says private sector employers added 281,000 jobs in June, compared to

179,000 jobs in May.

US trade deficit narrowed 5.6% in May to $44.4 bn after hitting a two-year high of $47 bn in

April.

US ISM non-manufacturing PMI edged down to 56 in June from 56.3 in May.

US Services PMI hit 61 in June, the highest final reading since the survey began in October

2009, compared with May's final reading of 58.1.

US composite PMI hit 61 in June, a record high for a final reading, versus 58.4 in May. Source: Crisil Weekly Market Update

International Markets US factory orders fell 0.5% in May as compared to an increase of 0.8% in April.

US Initial claims for state unemployment benefits rose by 2,000 to a seasonally adjusted

315,000 for the week ended June 28.

US Chicago purchasing managers’ index slumped to a seasonally adjusted 62.6 in June

from a reading of 65.5 in May.

The European Central Bank leaves its main interest rate unchanged at a record low of

0.15%, holding off fresh policy action while it waits for stimulus measures announced last

month to take effect.

Euro zone’s manufacturing Purchasing Managers' Index (PMI) fell to 51.8 in June from

May's 52.2, its lowest since November.

Euro zone’s services PMI fell to 52.8 in June from 53.2 in May.

Euro zone’s composite PMI came in at 52.8 in June, down from May’s 53.5.

Euro zone’s retail sales showed no growth in May following a revised fall of 0.2% in April.

Euro zone’s jobless rate remained at 11.6% in May following a downwardly revised rate of

11.7% in April.

Eurozone flash estimate of annual inflation came in at 0.5% in June, same as the level of

inflation in May.

Euro zone’s producer price index eased down by a seasonally adjusted 0.1% in May, after

inching down 0.1% in April. Source: Crisil Weekly Market Update

International Markets UK’s manufacturing PMI improved to a seasonally adjusted 57.5 in June from a reading of

57.0 in May.

China’s official Purchasing Managers' Index (PMI) came in at 51 in June, above the 50.8

reading in May.

China’s HSBC Manufacturing PMI reading for June rebounded to 50.7, up from 49.4 in May.

China's official non-manufacturing PMI dropped to 55 in June from a six-month high of 55.5

in May.

China’s HSBC services PMI rose to 53.1 in June from 50.7 in May.

China's composite PMI came in at 52.4 in June, up from 50.2 in the previous month.

Japan’s industrial production rose a seasonally adjusted 0.5% in May following a 2.8% drop

in April.

The Bank of Japan's quarterly "tankan" survey shows that the headline index for big

manufacturers' sentiment fell by 5 points from three months earlier to 12 in June.

Japan’s final manufacturing Purchasing Managers Index (PMI) reading rose to a seasonally

adjusted 51.5 in June, higher than 49.9 in May.

BNP Paribas agrees to pay nearly $9bn to resolve criminal allegations that it processed

transactions for clients in Sudan and other blacklisted countries in violation of US trade

sanctions.

General Motors recalls 8.2 mn vehicles due to a fault in ignition switches.

Source: Crisil Weekly Market Update

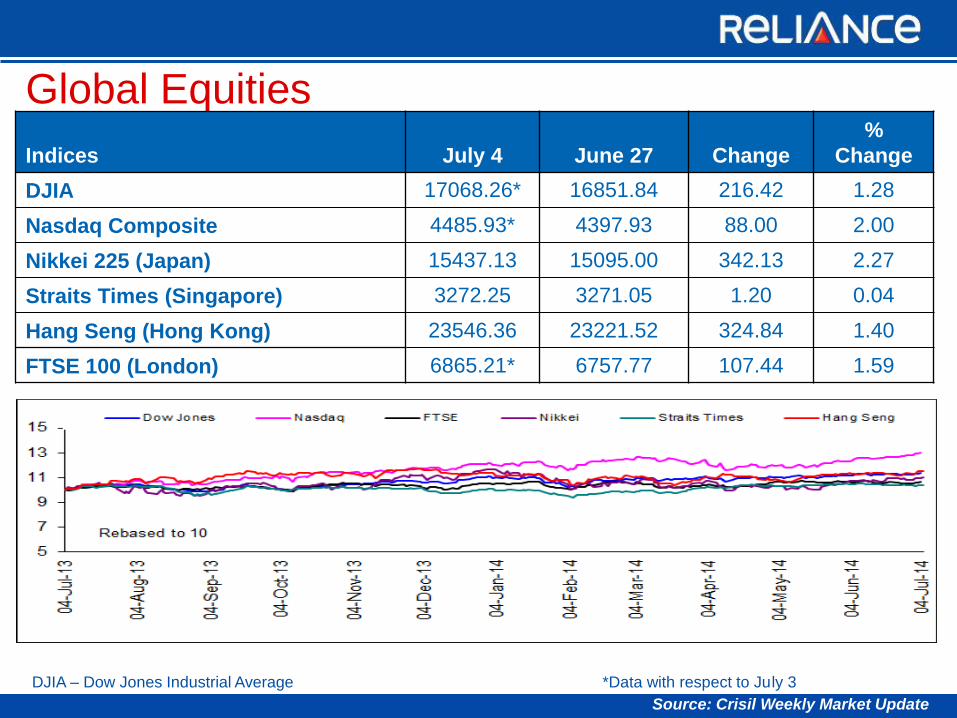

Global Equities

Indices July 4 June 27 Change

%

Change

DJIA 17068.26* 16851.84 216.42 1.28

Nasdaq Composite 4485.93* 4397.93 88.00 2.00

Nikkei 225 (Japan) 15437.13 15095.00 342.13 2.27

Straits Times (Singapore) 3272.25 3271.05 1.20 0.04

Hang Seng (Hong Kong) 23546.36 23221.52 324.84 1.40

FTSE 100 (London) 6865.21* 6757.77 107.44 1.59

DJIA – Dow Jones Industrial Average *Data with respect to July 3

Source: Crisil Weekly Market Update

Global Equities Key global indices advanced in the week ended July 3/4, with Japan’s Nikkei index gaining

the most – up 2.3%.

Wall Street stocks ended the week at new record highs primarily on the back of encouraging

sets of domestic economic data including government and private sector jobs reports,

pending home sales, manufacturing and auto sales.

Further gains were witnessed, especially on the Nasdaq, supported by rally in technology

shares.

Some gains were however capped following weak second-quarter forecast from DuPont Co,

and after General Motors announced another massive auto recall.

Britain’s FTSE added 1.6% during the week on stock specific buying, especially in mining

shares which rose on the back of upbeat manufacturing data from China.

The benchmark got further support after housing shares rallied on positive brokerage

comments about the sector.

Some gains were however cut short on intermittent profit booking.

Hong Kong’s Hang Seng index rose 1.4% in the week primarily boosted by robust

manufacturing activity data from China and the US.

Sentiments strengthened further following encouraging jobs data from the US.

Japan’s Nikkei index rose 2.3% in the week as the exporters’ heavy benchmark benefitted

from a weak yen and upbeat China factory activity data.

Source: Crisil Weekly Market Update

Global Equities Sentiments were boosted further on tracking positive jobs data from the US.

Singapore’s Straits Times index ended flat in the week as investors stayed on the sidelines

for most parts of the week ahead of the US jobs data and the European Central Bank (ECB)

meet.

Source: Crisil Weekly Market Update

Global Debt US treasury prices ended lower in the week ended July 3 after the release of positive

domestic economic indicators.

Bond prices fell after reports showed that the US non-farm payrolls rose by a seasonally

adjusted 288,000 in June following an upwardly revised 224,000 in May; the unemployment

rate slipped to a five-and-a-half year low of 6.1% in June from 6.3% in May.

Encouraging US private sector jobs data also dented the safe-haven appeal of the US debt.

US ADP report says private sector employers added 281,000 jobs in June, compared

to 179,000 jobs in May.

Bond prices were also pulled down by the strong manufacturing activity data from US and

China:

US manufacturing PMI increased to 57.3 in June, the highest in more than four years,

from 56.4 a month earlier.

China’s official Purchasing Managers' Index (PMI) came in at 51 in June, above the

50.8 reading in May.

Bond prices declined after the National Association of Realtors said that the US pending

home sales surged 6.1% to 103.9 in May, registering the highest month-on-month gain in

four years.

Intermittent gains in the equity market also weighed down on the US treasuries.

Source: Crisil Weekly Market Update

Global Debt Losses were however capped on month-end buying and after the data showed that the US

Institute for Supply Management (ISM) dipped to 56 in June from 56.3 in May.

The yield on the 10 year benchmark bond rose sharply to 2.65% on July 3 from 2.53% on

June 26.

The US Federal Reserve bought $1.03 bn of treasuries maturing August 2039- August 2043

on Monday as part of its economic stimulus program.

On weekly debt holding front, foreign central banks' investment in US Treasuries and

agency debt at the Federal Reserve rose by $11 bn to $3.30 trillion in the week ended July

2.

Source: Crisil Weekly Market Update

USA

Wall Street stocks ended the week at new record highs, with Dow Jones and Nasdaq

gaining 1.3% and 2%, respectively.

Markets recorded stellar gains primarily on the back of encouraging sets of domestic

economic data including government and private sector jobs reports, pending home sales,

manufacturing and auto sales.

US non-farm payrolls rose by a seasonally adjusted 288,000 in June following an

upwardly revised 224,000 in May; the unemployment rate ticked down to a five-and-a-

half year low of 6.1% in June from 6.3% in May.

US ADP report says private sector employers added 281,000 jobs in June, compared

to 179,000 jobs in May.

US Pending Home Sales rose 6.1% in May to 103.9, compared to April’s upwardly

revised reading of 97.9.

US manufacturing PMI increased to 57.3 in June, the highest in more than four years,

from 56.4 a month earlier.

US industry-wide auto sales rose 1.2% to 1.4mn in June, pushing the annualized

selling rate to 16.98mn.

Further gains were witnessed, especially on the Nasdaq, supported by rally in technology

shares.

Source: Crisil Weekly Market Update

USA

Some gains were however capped following weak second-quarter forecast from DuPont Co,

and after General Motors announced another massive auto recall.

Wariness ahead of the announcement of monthly payrolls data also checked some gains

from the markets.

Source: Crisil Weekly Market Update

UK

Britain’s FTSE added 1.6% during the week on stock specific buying.

The benchmark started off the week on a positive note after housing shares rallied on

upbeat brokerage comments about the sector.

A rally in mining shares on the back of upbeat manufacturing data from China, coupled with

buying interest in banking and auto shares, further added to the upward momentum of the

market.

Some gains were however cut short on intermittent profit booking.

Source: Crisil Weekly Market Update

ASIA

Hong Kong’s Hang Seng index rose 1.4% in the week ended July 4 following upbeat

domestic cues.

Market was primarily boosted by upbeat manufacturing activity data from China and the US.

China’s official Purchasing Managers' Index (PMI) came in at 51 in June, above the

50.8 reading in May.

China’s HSBC Manufacturing PMI reading for June rebounded to 50.7, up from 49.4 in

May.

Sentiments strengthened further following encouraging jobs data from the US.

Further gains were however restrained due to intermittent profit booking by investors.

Japan’s Nikkei index rose 2.3% in the week ended July 4 and emerged as the topmost

gainer among key indices analyzed.

The exporters’ heavy benchmark advanced earlier, benefitting from a weak yen and upbeat

China factory activity data

Investors shrugged off weak Bank of Japan tankan survey numbers.

The Bank of Japan's quarterly "tankan" survey shows that the headline index for big

manufacturers' sentiment fell by 5 points from three months earlier to 12 in June.

Sentiments were boosted further on tracking upbeat jobs data from the US.

Some gains were however chipped off on sporadic profit booking.

Source: Crisil Weekly Market Update

ASIA

Singapore’s Straits Times index ended flat in the week ended July 4 amid weak market

activity.

Investors stayed on the sidelines for most parts of the week ahead of the US jobs data and

the European Central Bank (ECB) meet.

Sentiments however strengthened a bit on tracking encouraging US private sector jobs data.

Source: Crisil Weekly Market Update

Indian Futures and Options Market Review

Nifty Futures

The Nifty near month contract (July 31, 2014) closed up with 30.90 point

premium to the spot index on July 4, 2014.

Over the week ended July 4, the Nifty spot index surged 3.23% on rising

optimism that the domestic government would unveil a fiscally prudent budget

due next week and positive global cues.

The other Nifty future contracts, viz., August contract ended at 7824 points (up

243 points over the week) and September contract ended at 7865 points (up

248 points over the week).

Overall, Nifty futures saw a weekly trading volume of Rs 38,675 cr arising out of

around 10 lakhs contracts with an open interest of nearly 152 lakhs.

Source: Crisil Weekly Market Update

Indian Futures and Options Market Review

Nifty Options

Nifty 8000 call witnessed the highest open interest of 114 lakh on July 4 and also saw the

highest increase in open interest of 27 lakhs over the week.

Nifty 8000 call also garnered the higher number of contracts over the week at 9 lakhs.

For put options, Nifty 7500 put witnessed the highest open interest of 56 lakh on July 4

and also saw the highest increase in open interest of 21 lakhs over the week.

Nifty 7500 put also garnered highest number of contracts over the week at 7 lakhs.

Overall, options saw 79 lakh contracts getting traded at a notional value of Rs 3,04,475 cr

during the week.

Source: Crisil Weekly Market Update

Indian Futures and Options Market Review

Week ended

July 4, 2014

Turnover

Rs. Cr. % to Total

Index Futures 56,026 9.76

Index Options 318,219 55.44

Stock Futures 155,222 27.04

Stock Options 44,522 7.76

Total 573,988 100.00

Put Call Ratio 0.82 (4 July) 0.85 (27 June)

Stock Futures and Options –

NSE witnessed 38 lakh contracts in stock futures valued at Rs 1,55,222 cr while stock options saw volumes of 11 lakh contracts valued at Rs 44,522 cr during the week ended July 4, 2014.

NSE F&O Turnover –

Overall turnover on NSE's derivatives segment stood at Rs 5.74 lakh cr (146 lakh contracts) during the week ended July 4 vs Rs 13.73 lakh cr (362 lakh contracts) in the previous week.

Put Call ratio fell slightly to 0.82 on July 4 from 0.85 on June 27.

Source: Crisil Weekly Market Update

Indian Futures and Options Market Review

Source - SEBI

FII Segment

On July 3 (last available SEBI data), foreign institutional investors' open interest stood at Rs 1, 22,987 cr (32 lakh contracts). The details of FII derivatives trades for the period June 27 – July 3 are as follows: -

Week Ended

July 3, 2014

Buy Sell Buy % Sell %

No. of

contracts

Amt in Rs

Cr

No. of

contracts

Amt in Rs

Cr

No. of

contracts Amt in Rs Cr

No. of

contracts

Amt in Rs

Cr

Index

Futures 168597 6474 171022 6561 11.13 11.23 11.53 11.58

Index

Options 802852 30522 746684 28489 53.00 52.94 50.33 50.29

Stock

Futures 382578 14492 406571 15466 25.26 25.14 27.41 27.30

Stock

Options 160818 6161 159237 6131 10.62 10.69 10.73 10.82

Total 1514845 57648.09 1483514 56648 100.00 100.00 100.00 100.00

Source: Crisil Weekly Market Update

The Week Ahead…

7th July to 11th July 2014

The Week Ahead Day Event

Monday, July 7

Euro-Zone Sentix Investor Confidence, July

Japan’s Trade Balance, May

Japan’s Leading Index, May

Japan’s Coincident Index, May

Tuesday, July 8

US Consumer Credit, May

UK NIESR GDP Estimate, June

UK Industrial Production, May

China’s Consumer Price Index, June

China’s Producer Price Index, June

Japan’s Eco Watchers Survey: Current/Outlook, June

India's Railway Budget 2014-15

Wednesday, July 9

US Federal Open Markets Committee meeting Minutes

US Crude Oil Inventories, July 5

UK RICS House Price Balance, June

Japan’s Machine Tool Orders, June

Japan’s Tertiary Index, May

India's Economic Survey 2014-15

Thursday, July 10

US Wholesale Inventories, May

US Initial Jobless Claims, July 5

European Central Bank’s Monthly Report

Bank of England Monetary Policy Review

UK Visible Trade Balance, May

China’s Trade Balance, June

China’s New Yuan Loans, June

Japan’s Consumer Confidence Index, June

India’s Union Budget 2014-15

Friday, July 11

US Treasury Budget, June

India’s Index of Industrial Production, May

India’s Forex Reserves, July 4

Indian Debt Market Outlook

This week, the G-Sec market is expected to take cues from the budget to be presented on

10th July & concerns arising out of geo political tensions in Iraq .

Liquidity is expected to tighten on indirect tax outflows. .

Corporate bond market is expected to take cues from G-sec market and primary issuances.

Source: RBI,RMF Estimates

Indian Debt Markets

The maturities of duration

funds have increased due to

increased exposure in gsecs

as positive sentiments build

up in market ahead of the

budget.

The maturities of liquid and

liquid plus funds reflects cash

movement in the portfolio.

Source: RBI,RMF Estimates

Particulars 27-Jun-14 04-Jul-14

Change

(bps)

10 year Gsec yield (%) 8.75 8.65 -0.10

Scheme Maturity (years) Change

G-sec Fund 11.68 12.09 0.41

Income Fund 10.69 11.01 0.32

Short Term Fund 2.62 2.66 0.04

MIP 8.09 6.31 -1.78

Dynamic Bond Fund 9.84 10.34 0.50

Liquid Schemes Maturity (days) Change

Floating Rate Fund 170.00 161.95 -8.05

Money Managers Fund 100.00 93.88 -6.12

Liquidity Fund 38.00 37.19 -0.81

Medium Term Fund 267.00 233.39 -33.61

Treasury Plan 42.00 35.20 -6.80

Cash Plan 47.00 45.07 -1.93

Product Labeling

Reliance Gilt Securities

Fund

· income over long term.

· investment in Government securities.

· low risk. (BLUE)

Reliance Income Fund · income over long term.

· investment in debt and money market instruments

· low risk. (BLUE)

Reliance Short Term

Fund

·income over short term.

· investment in debt and money market instruments, with the scheme would have maximum

weighted average duration between 0.75-2.75 years

· low risk. (BLUE)

Reliance Monthly

Income Plan

· regular income and capital growth over long term.

· investment in debt & money market instruments and equities & equity related securities

· medium risk. (YELLOW)

Reliance Dynamic Bond

Fund

· income over long term.

· investment in debt and money market instruments

· low risk. (BLUE)

Reliance Corporate

Bond Fund

-Income over Medium Term

-Investment predominantly in corporate bonds of various maturities and across ratings that

would include all debt securities issued by entities such as Banks, Public Sector Undertakings,

Municipal Corporations, bodies corporate, companies etc·

-low risk. (BLUE)

This product is suitable for investors who are seeking*:

*Investors should consult their financial advisers if in doubt about whether the product is suitable for them.

Product Labeling This product is suitable for investors who are seeking*:

*Investors should consult their financial advisers if in doubt about whether the product is suitable for them.

Reliance Floating

Rate Fund – Short

Term Plan

·income over short term.

· investment predominantly in floating rate and money market instruments with tenure exceeding

3 months but up to a maturity of 3 years and fixed rate debt securities

· low risk. (BLUE)

Reliance Money

Manager Fund

·income over short term.

· investment in debt and money market instruments

· low risk. (BLUE)

Reliance Liquidity Fund ·income over short term.

· investment in debt and money market instruments

· low risk. (BLUE)

Reliance Medium Term

Fund

·income over short term.

· investment in debt and money market instruments with tenure not exceeding 3 years.

· low risk. (BLUE)

Reliance Liquid Fund –

Treasury Plan

·income over short term.

· investment in debt and money market instruments

· low risk. (BLUE)

Reliance Liquid Fund –

Cash Plan

·income over short term.

· investment in debt and money market instruments

· low risk. (BLUE)

Product Labeling Disclaimer

Note: Risk may be represented as:

(BLUE) investors

understand that their

principal will be at low

risk

(YELLOW) investors

understand that their

principal will be at

medium risk

(BROWN) investors

understand that their

principal will be at high

risk

Information's provided here are meant for general reading purpose only and is not meant to

serve as a professional guide for the readers. This document has been prepared on the

basis of publicly available information, internally developed data and other sources believed

to be reliable. The Sponsor, The Investment Manager, The Trustee or any of their respective

directors, employees, affiliates or representatives do not assume any responsibility for, or

warrant the accuracy, completeness, adequacy and reliability of such information. Whilst no

action has been solicited based upon the information provided herein, due care has been

taken to ensure that the facts are accurate and opinions given fair and reasonable. This

information is not intended to be an offer or solicitation for the purchase or sale of any

financial product or instrument. Recipients of this information should rely on information/data

arising out of their own investigations. Readers are advised to seek independent

professional advice and arrive at an informed investment decision before making any

investments. None of The Sponsor, The Investment Manager, The Trustee, their respective

directors, employees, affiliates or representatives shall be liable for any direct, indirect,

special, incidental, consequential, punitive or exemplary damages, including lost profits

arising in any way from the information contained in this material.

Mutual Fund investments are subject to market risks, read all scheme

related documents carefully.

Thank you