Embed Size (px)

Citation preview

News from:

Sweden• Citi launches new Fiduciary

Services business

International• Suspensions of CIS redemptions

Europe• Update on European regulation

United Kingdom • New regulatory structure

• FSA Risk Outlooks

• FSA Business Plan

• Revised Remuneration Code

Ireland• Fitness and probity standards

Luxembourg• Infrastructure funds

news & viewseuropean

second edition 2011

2 | European News & Views | Second Edition 2011

Contributors

Europe

Amanda J Hale

Head of UK Fiduciary Technical

Tel: +44 (0) 20 7508 0178

Ireland

Ian McCarthy

Senior Fiduciary Monitoring Officer

Tel: +353 1 622 1012

Luxembourg

Jean-Christian Six

Partner

Allen & Overy Luxembourg

Tel: +352 444 455 710

United Kingdom

Amanda J Hale

Head of UK Fiduciary Technical

Tel: +44 (0) 20 7508 0178

Selina Staines

Fiduciary Technical Analyst, UK

Tel: +44 (0) 20 7500 9741

Charlotte Hill

Financial Services Partner

Tel: +44 (0) 20 7809 2169

European News & Views | Second Edition 2011 | (i)

Contents

Introduction

By David Morrison 01

Sweden

Land of the Midnight Sun 02

International

Principles on suspensions of redemptions in Collective Investment Schemes 06

Europe

Positional update on European regulation 10

United Kingdom

A new approach to financial regulation: building a stronger system 14

Retail Conduct Risk Outlook and Prudential Risk Outlook arise out of Financial

Services Authority (FSA) restructure 16

The FSA Business Plan 2011/2012 22

Casting the net wider: the FSA’s revised Remuneration Code and its impact on asset managers 25

Ireland

The Central Bank of Ireland raises the bar in fitness and probity standards 28

Luxembourg

Luxembourg regulated infrastructure funds 31

Glossary 36

(ii) | European News & Views | Second Edition 2011

European News & Views | Second Edition 2011 | 1

Introduction

Hello and welcome! We are very

pleased to present our latest edition

of European News & Views, one that

provides you with the same incisive

commentary you know and trust on

the regulatory developments that are

shaping the fiduciary landscape across

EMEA, but with a renewed voice.

We begin our journey in “The Land

of the Midnight Sun” in honour

of our newly launched Fiduciary

Services business in Stockholm. With

a very skilled labour force, extensive

welfare benefits, first-rate internal

and external communications,

high-tech capitalism and an advanced

distribution system, Sweden certainly

offers an attractive standard of

living. It is a favourable place to

do business, as Swedish retail and

institutional investors, who have an

appetite for risk and who enjoy an

equities culture, will no doubt attest

to. Stockholm is sure to add a new

dimension to our strong fiduciary

coverage across EMEA.

From Stockholm, we move on to

open-ended collective investment

schemes and IOSCO’s published

consultation report on suspensions

of redemptions. With an overview

of IOSCO’s principles applicable to

the suspensions process — from how

to avoid a suspension through to

situations where suspension becomes

necessary — we ask if IOSCO’s

standards can be seen as minimum

best practice in the absence of

regulatory guidance.

On regulatory guidance in general,

we survey the profusion of regulation

that has hit the UK financial services

space. Supervisory reforms, “too-

big-to-fail” rules, market-wide

consultations, investment and retail

directives — including a helpful

timeline of the key initiatives

affecting the asset management

industry across Europe

“A New Approach to Financial

Regulation” takes a look at how the

UK government is working towards

sustainable growth in a programme of

reform driven by international efforts

and progression within the EU.

With the coming restructuring of

the FSA, we turn to the authority’s

decision to publish a Prudential Risk

Outlook and a Retail Conduct Risk

Outlook, examining how the former

aims to yield an understanding of the

overall macroeconomic and financial

trends in the UK financial system and

how the latter aims to increase risk

awareness and lead the authority’s

supervisory focus.

The FSA’s move to a new

organisational structure will be a

milestone event. So we give pause to

the FSA Business Plan, which focuses

on how the FSA intends to manage

the transition, touching on high-level

aims, work programme and priorities,

and other deliverables that will be of

interest to stakeholders.

Remaining with our UK focus,

Charlotte Hill, Partner, Stephenson

Harwood, gives us a welcome

rundown of the impact of the

FSA’s Remuneration Code on asset

managers, giving us an appreciation

of which firms and employees are

likely to be affected, what the key

issues are, how firms will be expected

to apply the Code, supervision

and enforcement, and steps to

implementation.

We include an article on how “Ireland

Raises the Bar in Fitness and Probity

Standards”, following the Central

Bank of Ireland’s recent consultation

paper on amendments to the Fit and

Proper Regime, which will come into

effect on 1 September 2011.

Finally, Jean-Christian Six, Partner,

Allen & Overy Luxembourg,

presents his interesting article on

regulated infrastructure funds,

placing Luxembourg as the likely

domicile of choice in Europe for the

establishment of such funds, which

are already seen by many institutional

investors as attractive for their

portfolio-enhancing qualities.

We hope you enjoy this edition of

European News & Views, and we very

much welcome your comments and

suggestions on anything of interest to

you in these engaging articles.

David MorrisonDirector and Head of Fiduciary Services, EMEA

2 | European News & Views | Second Edition 2011

Land of the Midnight Sun

The royal Swedish capital of Stockholm,

frequently referred to as one of the

world’s most beautiful cities, was built

over eight centuries and constitutes the

most populated area in Scandinavia.

Its strategic location on 14 islands on

the south-central east coast of Sweden

at the mouth of Lake Mälaren, by

the Stockholm archipelago, has been

historically important. It is home to

the national Swedish government, the

Riksdag (parliament) and the official

residence of the Swedish monarch and

prime minister. Stockholm is Sweden’s

financial centre. Major Swedish banks,

such as Swedbank, Handelsbanken and

Skandinaviska Enskilda Banken, are

headquartered in Stockholm, as are the

major insurance companies Skandia and

Trygg-Hansa. Stockholm is also home

to Sweden’s foremost stock exchange,

the Stockholm Stock Exchange

(Stockholmsbörsen). Additionally, about

45% of Swedish companies with more

than 200 employees are headquartered

in Stockholm.1

Goteborg (otherwise known as

Gothenburg), Sweden’s second largest

city, is a city of commerce, culture and

entertainment, one influenced by its

proximity to the sea. Its port has come

to be the largest harbour in Scandinavia.

Apart from trade, the second pillar

of Gothenburg has traditionally been

manufacturing. Major companies

operating plants in the area include

SKF, Volvo (the largest employer in

Gothenburg) and Ericsson.

Banking and finance are also important

trades, as are the event and tourist

industries.2

Malmö, which is Sweden’s third largest

city, is traditionally an old shipbuilding

and industrial centre. The city has

undergone a metamorphosis in recent

years since its economic integration with

Denmark, which was brought about by the

construction of the Oresund Bridge. The

bridge connects Sweden and Denmark

and is the longest road and rail bridge in

Europe. Almost 10% of the population of

Malmö works in Copenhagen, Denmark, as

a result. Malmö has built an international

reputation for being a creative,

progressive and environmentally aware

city, and has received international awards

such as Eco City and Fair Trade City.

Some other interesting facts about

Sweden are:

• Sweden is one of the largest countries

in Europe.3

• The Nobel Prizes were founded by the

Swedish inventor and entrepreneur

Alfred Nobel, who also invented

dynamite in 1866.4

• Swedish inventions include the

pacemaker, the ball bearing, the

safety match, the adjustable wrench,

the working zipper and the Tetra Pak

carton.5

• With Ericsson headquartered in

Stockholm, Sweden is a global

leader in mobile telecommunications

technology.

• Sweden has one of the highest

standards of living worldwide.

This is closely linked to trade

— many multinational companies

have their roots in Sweden, among

them, Volvo, AstraZeneca, ABB, IKEA,

Ericsson, Electrolux, H&M and Absolut.

Cutting-edge companies such as

Skype and Spotify were also founded

in Sweden.6

• Sweden is also the Land of the

Midnight Sun.7 In the summer, the

regions north of the Arctic Circle

enjoy between one and two months of

sunlight, which is a very long period

of constant daylight. In winter, the

Northern Lights can be seen, caused

by electrically charged particles being

thrust into the earth’s magnetic field at

great speed, propelled by solar winds.8

A short history of Sweden 10

Fourteen thousand years ago, Sweden

was covered by a thick ice cap. As the

ice cap melted, humankind began to

inhabit the area. Its first known dwelling

place, found in the south of the country,

dates from around 12,000 BCE.

Sweden

The Innovation Union Scorecard says “Sweden is the most innovative country in the EU.” 9

Sweden is separated in the west from Norway by the Scandinavian Mountains and shares the Gulf of Bothnia to the north

of the Baltic Sea with Finland. The southern part of the country is chiefly agricultural, forests covering an increasing

percentage of the land the further north you go. With its intense green countryside, impenetrable forests, little red

cottages atop remote islands and famously clear blue waters, Sweden’s pastoral beauty is distinctive.

European News & Views | Second Edition 2011 | 3

Sweden

In its earliest history, the Swedish

population lived by hunting and fishing.

However, during the early Iron Age the

population of Sweden became settled

and agriculture came to form the basis

of the economy and society.

It was not until the 1890s that industry

began to grow. Between 1900 and 1930,

Sweden transformed into one

of Europe’s leading industrial nations.

In 1995, Sweden became a member

of the European Union (EU). Sweden has

held the EU presidency on two occasions:

from 1 January to 30 June 2001 and from

30 June to 31 December 2009.

As you may be aware, it was under

the Swedish EU presidency that

technical discussions started around the

first Alternative Investment

Fund Managers Directive (AIFMD),

and the first official publication of

the AIFMD compromise text.12

Sweden’s economy

The World Economic Forum 2010

competitiveness index ranks Sweden as

the second most competitive economy

behind Switzerland, and the long-run

prospects for growth remain favourable.13

Looking forward to 2015, the Economist

Intelligence Unit Limited (EIU) has

reported some of the following

expectations for the Swedish economy: 14

• An increase in competition and the

sale of state holdings in enterprise.

The government will also try to

increase incentives to work but will

not introduce any radical reforms of

the labour market.

• With public debt and the general

government deficit low, there is an

urgent need for fiscal tightening. The

EIU has forecast that the balance will

improve from an estimated deficit of

1.5% of GDP in 2010 to a surplus of

1.8% by 2015.

• Monetary policy is expected to be

gradually tightened with the benchmark

repo rate rising to under 4% by the

latter part of the forecast period.

• From an estimated 5.3% in 2010,

growth is expected to slow on a

quarterly basis in 2011 (although

annual growth will be strong, owing

to carryover effects in 2010). This

will be followed by a pick-up to around

2.4% in 2012-15.

“Aided by peace and neutrality for the whole of the 20th century, Sweden has achieved an enviable standard of living under a mixed system of high-tech capitalism and extensive welfare benefits. It has a modern distribution system, excellent internal and external communications, and a skilled labour force.” 11

4 | European News & Views | Second Edition 2011

• Inflation (EU harmonised measure)

is expected to rise from an average

of 1.9% in 2009 and 2010 to over

2% throughout 2011-15, owing

to continued growth, falling

unemployment and upward

pressure on wages.

Importantly, the EIU has reported that

Swedish banks are well prepared for

Basel III as they are well capitalised

by international standards and

currently able to fund their operations

themselves through the financial

markets. So, even under the new

regulatory framework proposed by

the Basel Committee on Banking

Supervision (Basel III), Swedish

banks have already begun the process

of raising capital levels to meet the

new regulations.

A focus on mutual funds

The “Cerulli Quantitative Update:

Global Markets 2010” on Sweden

reported that Swedish investors, in

general, have an appetite for risk

and enjoy an equity culture. This

is demonstrated by the fact that

equity funds had positive net inflows

throughout 2009, despite the fact that

the Swedish equity market, in line with

global markets, was not fruitful for

investors at the start of that year.

Equity funds continue to dominate

in Sweden and are back at the levels

seen before the crash in 2008,

when falling markets took the equity

exposure to low levels. The bar graph

below shows that the Swedish remain

dedicated equity investors and are

not afraid to take on risk in their

investment portfolios, as seen by the

level of interest in emerging market

equity funds. 15

Top players in the mutual funds space

There were only two foreign players

among the top ten mutual fund

managers in Sweden in 2009; both

had close ties to the local market. One

was Norway’s Storebrand; the other,

Old Mutual, which owns Skandia, the

Swedish insurer.

When provided with the opportunity,

Swedish retail and institutional

investors have been open to investing

in foreign fund groups, as seen on

platforms such as Nordnet and Avanza.

At the time of the Cerulli Associates

report, distribution was dominated by

banks and unit-linked platforms. 16

The below table provides a list of the

largest Swedish asset managers.

Market regulation

Companies who operate business

in the Swedish financial sector

are authorised and supervised by

the Swedish Financial Supervisory

Authority, Finansinspektionen (FI).

The main rules applicable to

the Swedish securities markets

are defined by the Financial

Markets Act (2007:528) (Lag om

Vardepappersmarknaden [LVM]), and

the Financial Trading Act (1991:980)

(Lag om handel med finansiella

instrument [LHFI]). In addition to the

LVM and the LHFI, there are a number

of Acts that cover reporting duties,

insider rules, takeover rules and

money-laundering regulations. 17

The LVM came into force in 2007 and

through its adoption Sweden became

compliant with the Markets in Financial

Instruments Directive (MiFID). The LVM

contains fundamental rules for the

organisation of a securities business,

such as capital requirements and

portfolio risk diversification rules.

The LVM also sets out requirements for

obtaining a licence to conduct securities

business. Any company planning to offer

services on the securities market in

Sweden needs to obtain a licence from

the FI. The application procedures are

described in the LVM. 18

Sweden

Rank Manager

2009

AUM (SEK bn)

Market Share (%)

1 Swedbank AB 443.4 34.6

2 SEB 146.1 11.4

3 Svenska Handelsbanken 125.6 9.8

4 Nordea AB 94.7 7.4

5 Sjunde AP-fondens 92.6 7.2

6 Lansforsakringsbolagen 65.8 5.1

7 AMF Pension 52.4 4.1

8 Storebrand SPAR A/S 47.9 3.7

9 Old Mutual 43.9 3.4

10 Hagstromer & Qviberg AB 25.6 2.0

Others 143.7 11.2

Mutual fund total 1,281.7 100.0

70%

60%

50%

40%

30%

20%

10%

0%2005

Balanced Bond Equity Money Market Others

2006 2007 2008 2009

European News & Views | Second Edition 2011 | 5

At present, there are two securities

exchanges in Sweden, the OMX Nordic

Exchange Stockholm (OMX) and the

Nordic Growth Market. The OMX is the

largest securities exchange in the Baltic

region and offers trade in shares, money-

market instruments and derivatives. 19

Investment funds specifically are

captured by the Swedish Investment

Funds Act (SFS 2004:46) (SIFA). It

covers, among other things:

• Authorisation obligations

• Capital requirements

• Branch and cross-border operations

• Depositaries

• Management of investment funds

• Fund rules

• Report and accounts requirements, etc.

Depositary bank activities

Pursuant to SIFA, each investment

fund shall have a depositary

(Förvaringsinstitut). SIFA defines the

Förvaringsinstitut as a bank or other

credit institution that holds assets in

custody in an investment fund and

administers deposits into, and payments

from, the fund. The Förvaringsinstitut

shall maintain its registered office in

Sweden or, where the Förvaringsinstitut

is a branch established in Sweden, in

another state within the European

Economic Area (EEA).

The duties of the Förvaringsinstitut,

according to SIFA, chapter 3, are

outlined below:

• Implement decisions of the

management company provided that

they do not violate the provisions of

SIFA or the fund rules.

• Take receipt and hold in custody the

property of the fund.

• Ensure the sale and redemption

of the fund’s units is conducted in

accordance with the provisions of

SIFA and the fund rules.

• Ensure the value of the fund’s units

is calculated in accordance with the

provisions of SIFA and the fund rules.

• Ensure the assets of the fund are

transferred to the depositary

without delay.

• Ensure the assets of the fund are

used in accordance with provisions

of SIFA and the fund rules.

Additional guidance regarding depositary

responsibilities is provided by the FI

through complementary ordinances,

regulations and the fund market

handbook (Investeringsfonder — en

vägledning), for example, in its Guidelines

on Depositary Bank Outsourcing. 20

Conclusion

This article provides just the hint of

a flavour of the country. You might

say “the tip of the iceberg”. Which

is rather fitting given the nature of

certain parts of the country’s climate.

By many accounts, though, Sweden

is not only known to be a favourable

country in which to live but a favourable

place in which to conduct business. (Just

a few of the headlines that captivate this

ethos are featured in this article.)

So, why the interest in Sweden specifically?

As you will have seen from the

introduction of this edition of European

News & Views, due to client demand,

Citi has just launched a new Swedish

fiduciary business in Stockholm.

This new addition to Citi’s fiduciary

product will further provide clients

with significant coverage across the

EMEA region, ensuring high-quality,

consistent and single-point access to

Citi’s award-winning fiduciary team.

If you have any questions regarding

the launch of our new branch in

Stockholm, please do not hesitate to

contact us.

1 www.stockholmbusinessregion.se/en/, accessed on 1 April 2011.

2 www.ne.se/g%C3%B6teborg/999778 (Swedish National Encyclopaedia), accessed on 1 April 2011.

3 www.sweden.se/eng/Home/Lifestyle/Facts/Sweden-in-brief/, accessed on 1 April 2011.

4 www.nobelprize.org/alfred_nobel/biographical/articles/life-work/index.html, accessed on 30 March 2011.

5 www.sweden.se/eng/Home/Education/Research/Facts/Innovation/, accessed on 1 April 2011.

6 www.sweden.se/eng/Home/Society/Facts/This-is-Sweden/, accessed on 1 April 2011.

7 www.sweden.se/eng/Home/Work/Life_in_Sweden/Climate_nature/Seasons/, accessed on 1 April 2011.

8 www.sweden.se/upload/Sweden_se/english/slides/Flash/Sweden_Swedes_20_Speakers_notes.pdf, accessed on 1 April 2011.

9 “Innovation Union Scorecard: Sweden is the Most Innovative Country in the EU,” 3 February 2011, www.investsweden.se, accessed on 1 April 2011.

10 www.sweden.se/eng/Home/Lifestyle/Facts/History-of-Sweden/, accessed on 1 April 2011.

11 ”Sweden: Economy Overview”, Ina Dimireva, 14 November 2009, www.eubusiness.com/europe/sweden, accessed on 1 April 2011.

12 Issued on 12 October 2009. All AIFMD compromise proposals are available on the Council’s website (www.consilium.europa.eu) by performing a search under the applicable interinstitutional file reference, 2009/0064(COD).

13 www.weforum.org/issues/global-competitiveness (World Economic Forum Global Competitiveness Report), accessed on 1 April 2011.

14 Economist Intelligence Unit Limited Country Report on Sweden, March 2011.

15 Cerulli Quantitative Update: Global Markets 2010, Sweden.

16 Exhibit 1 Largest 10 Swedish Mutual Fund Managers, 2007-2009 (sources: Lipper FMI, Cerulli Associates).

17 www.iflr1000.com/LegislationGuide/132/Securities-market-regulation-an-overview.html, accessed on 1 April 2011.

18 www.iflr1000.com/pdfs/Directories/1/Sweden_2009.pdf, 1 April 2011.

19 www.nasdaqomx.com/listingcenter/nordicmarket/rulesand regulations/, accessed on 1 April 2011.

20 Förvaringsinstitut och delegering — en vägledning.

Sweden

6 | European News & Views | Second Edition 2011

Risks and consequences

IOSCO considers some of the risks

and consequences deriving from the

suspension of redemption rights in an

investment fund in terms of:

• The direct impact on the investor:

if the risks inherent to investing

into a fund are not adequately

disclosed to investors, retail

or institutional, redemption

suspensions could cause serious

consequences to financial

markets. Suspensions carried out

in unsatisfactory conditions may

lead to the unequal treatment of

investors, for example, should some

investors in the fund be made aware

of the planned suspension, before

it becomes effective.

• Confidence and reputation:

suspending redemptions in a

sizeable investment fund may have

consequences that go far beyond its

investors, and may eventually lead

to wider macroeconomic or market-

wide implications. As the decision

to suspend subscription rights has

an adverse impact on investors’

confidence, it is possible that a

poor information/disclosure policy

eventually has a wider effect on the

financial industry and a general loss

of investors trust. Additionally, the

reputation of the fund manager/

promoter may be seriously

impacted and could generate issues

in the long term, particularly after

the suspension limitations have

been lifted.

• Market impact: the recognition

of a suspension in one or more

investment funds could lead to

investors performing withdrawals

in other investment funds. These

actions may cause liquidity issues

in the funds concerned, and they

may be forced to sell their assets.

Under particular market or sector

conditions, a forced sale may add

pressure to an already stressed

market and lead to further declines

in prices, possibly ending in a

vicious-circle scenario.

• The impact on counterparties:

an investment fund with liquidity

issues due to significant or

extraordinary withdrawals may

find itself in difficulties in meeting

other payment obligations (e.g.

margin calls). Liquidity problems

due to large redemptions may also

have an impact on funds’ market

counterparties.

IOSCO principles

IOSCO’s guidelines include principles

applicable to the “suspensions

process” in a chronological order,

from how to avoid a suspension

through to situations where

suspension becomes the only option.

A. Management of liquidity risk

Principle 1: “The responsible entity

should ensure that the degree of

liquidity of the open-ended CIS it

manages allows it in general to

meet redemption obligations and

other liabilities.”

Principles on Suspensions of Redemptions in Collective Investment Schemes

The redemption of units is a fundamental right of investors in open-ended collective investment schemes (CISs). It is on

the basis of this right that the technical committee of the International Organisation of Securities Commissions (IOSCO)

has published a consultation report on principles on suspensions of redemptions in CISs. IOSCO’s guidelines are issued on

a consultation basis and are open for comments until 30 May 2011. 1

International

European News & Views | Second Edition 2011 | 7

International

An open-ended fund should be

managed in a way that allows it to

meet redemption obligations and

other liabilities. This can be achieved

either by holding very liquid assets as

a fixed percentage (often determined

by laws or regulations) or by using a

principle-based approach.

IOSCO considers that although

the borrowing of cash can be used

to facilitate redemption requests,

“the routine use of borrowing is

not an appropriate way to manage

the CIS liquidity risk.” Besides

the consideration of redemption

obligations, the liquidity of the CIS

must be appropriate to deal with other

liabilities or payment commitments

that may, for example, result from

margin calls or collateral requirements

for derivatives positions.

Principle 2: “Before and during any

investment, the responsible entity

should consider the liquidity of the

types of instruments and assets

and its consistency with the overall

liquidity profile of the open-ended

CIS. For this purpose, the responsible

entity should establish, implement

and maintain an appropriate liquidity

management policy and process.”

In considering this principle, and

to meet redemption obligations

and liabilities, the responsible

entity should establish, implement

and maintain an appropriate

and proportionate liquidity risk

management policy and process.

B. Ex-ante disclosures to investors

Investors should be made aware

of the risk of the suspension of

redemptions, prior to their investment

in an open-ended CIS. Therefore, as

a minimum, the fund’s constitutional

documents and/or prospectus should

clearly disclose that redemptions

may be suspended in exceptional

circumstances. However, IOSCO

considers it unpractical to define the

term “exceptional circumstances” and

considers that examples of what might

constitute “exceptional circumstances”

should be provided instead.

C. Criteria and reasons for

the suspension

Principle 3: “Suspensions of

redemptions by the responsible entity

may be justified only in exceptional

circumstances provided such

suspension is in the best interest of

all unitholders within the CIS or if the

suspension is required by law.”

According to the consultation report,

the decision to suspend is a two-

step approach. The first relates to

exceptional circumstances.

Exceptional circumstances are generally

temporary situations, occur rarely and

should be such that a fair and robust

valuation, and orderly sale, of the fund’s

assets are not possible. Besides valuation,

suspensions might also be justified if

it is not possible to sell assets other

than at fire sale prices in order to meet

redemption requests. The consultation

report provides possible reasons for the

suspension of redemptions, but does

not provide a non-exhaustive list. Such

examples may include:

• Market failures, exchange closures:

markets may be affected by

unexpected events that impact

the functioning of exchanges or

the regular course of transactions.

Unexpected events can also be

related to political, economic, military,

monetary or other emergencies.

“An open-ended fund should be managed in a way that allows it to meet redemption obligations and other liabilities. This can be achieved either by holding very liquid assets as a fixed percentage (often determined by laws or regulations) or by using a principle-based approach.”

8 | European News & Views | Second Edition 2011

• Operational issues: unpredictable

operational problems and technical

failures can temporarily hamper

transactions, or affect the valuation

of the assets — this includes

operational issues affecting a fund’s

service providers.

• Liquidity issues: a suspension

arising as a result of poor liquidity

management in a fund is not

acceptable, in IOSCO’s view.

Therefore, suspensions as a result

of lack of liquidity should be the

last resort in cases where, despite

appropriate liquidity management

processes, the fund has to face

unforeseeable liquidity issues.

• Poor management: it may be

reasonable to suspend redemptions

when facing operational or iquidity

issues, if caused by poor management

rather than by unpredictable

circumstances, if this is in the interest

of investors. In such cases, IOSCO

considers the competent regulatory

authorities should take measures

against those responsible for poor

management practices.

The second relates to the best

interests of investors, as the fair and

equal treatment of incoming, ongoing

and outgoing investors must be a

consideration.

D. Decision to suspend

Principle 4: “The responsible entity

should have the operational capability

to suspend redemptions in an orderly

and efficient manner.”

Principle 5: “The decision by the

responsible entity to suspend

redemptions, in particular the reasons

for the suspension and the planned

actions, should be appropriately:

a) documented; b) communicated

to competent authorities and other

relevant parties; c) communicated

to unitholders.”

Principle 6: “During the suspension

of the redemptions, the responsible

entity should generally not accept

new subscriptions. Subscriptions

cannot be accepted if reliable,

meaningful and robust valuation of

the assets is not possible.”

Principle 7: “The suspension

should be regularly reviewed by the

responsible entity. The responsible

entity should take all necessary steps

in order to resume normal operations

as soon as possible, having regard to

the best interest of unitholders.”

Principle 8: “The responsible

entity should keep the competent

authority and unitholders informed

throughout the period of the

suspension. The decision to resume

normal operations should also be

communicated immediately.”

In terms of implementing processes

in advance, the decision to suspend

redemptions should be enforced in

an orderly and efficient manner.

This implies that the parties

responsible for the relevant operational

tasks should have the capabilities to

perform their roles. Processes and

procedures should exist to react

immediately in cases of circumstances

requiring dealing suspensions. Such

processes and procedures should

include interactions and communication

channels and notification procedures

with relevant third parties (e.g.

depositary, intermediaries, distributors

and regulatory authorities). Detailed

communication plans should exist,

devising the most effective

communication strategy targeting

investors, including processes

for dealing with investor queries

or complaints.

Should the case be that a suspension

is required, or is being considered,

the entities responsible for taking

the decision to suspend should make

sure all relevant parties (depositary,

external legal counsel and regulatory

authority) have been engaged and

notified as required (approval may be

required in some jurisdictions). Any

alternative course of action should

be considered and discounted, and

the suspension should be temporary

and consistent with disclosures made

to investors.

The decision to suspend redemptions

should be appropriately documented,

communicated to the regulatory

authorities and to other relevant

parties, and communicated to

concerned unitholders. When a

suspension event actually arises,

the responsible entity should

thoroughly analyse the situation

that might even require involvement

from external legal counsel.

A suspension of redemptions

should also imply a suspension

of subscriptions. However, IOSCO

considers that there may be cases

where, if a reliable NAV can still

be calculated, subscriptions could

be accepted. But any prospective

investor should be clearly informed

about the redemptions suspension in

a clear and comprehensive manner

and be given the chance to cancel the

subscription order.

The decision to suspend redemptions

should be formally reviewed on an

ongoing basis during the suspension

period. The acceptable length of

the suspension depends on the

circumstances and particular reasons

for the suspension and on applicable

laws and regulations. Under no

circumstances should the suspension

of redemptions remain in force for

a prolonged period. All alternatives

should be investigated to allow

investors access to their money,

including liquidation and/or the

establishment of side pockets.

Regular updates should be provided

to all concerned parties, during the

International

European News & Views | Second Edition 2011 | 9

suspension period. Any decision to

resume normal operations should be

communicated immediately to the

competent regulatory authority and

to unitholders.

E. Alternative measures

IOSCO identifies three examples

of alternative measures to the

suspension of redemptions, applicable

in extraordinary circumstances.

• Gating mechanism: by using a

gate, the entity responsible for the

management of the open-ended

fund limits the redemption amounts

to a specific proportion, on any one

redemption day. All redemption

orders are (if applicable)

proportionally reduced to ensure

equal treatment of investors. When

such safeguards are introduced,

these should be clearly disclosed in

the prospectus or other constitutive

documents of the fund, and

maximum transparency should be

applied at all times. It should be

noted that only some regulatory

regimes of certain jurisdictions

allow for gates. You should refer

to the full consultation report for

further details.

• Side pockets: a side pocket is

created when specific assets in a

fund’s portfolio are ring-fenced and

segregated from the rest of the

fund’s portfolio. A side pocket is

usually not actively managed, and

the assets it contains are liquidated

by seeking the best timing and

market opportunities. Again, note

should be taken of the fact that

only some jurisdictions

allow the creation of side pockets.

Refer to the full consultation report

for further details.

• Discount: a few jurisdictions allow

for a discount to be applied on

the redemption price determined

on the basis of the NAV in the

case of stressed markets or an

unusual and significant number of

redemptions. This methodology

requires maximum care to address

transparency and discretion issues.

A discount should be applied only

if the reasons for its application

are properly disclosed in the

prospectus, and should be applied

consistently to all redemptions

completed on the same day.

Conclusions

IOSCO standards are highly regarded

by regulatory authorities in general.

They are also often referred to by the

European Commission in its legislative

proposals. Although they do not have

any binding force, they should always

be regarded as minimum best practice

in the absence of clear or specific

regulatory guidance.

International

1 Consultation Report on Principles on Suspensions of Redemptions in Collective Investment Schemes, CR01/11, March 2011.

“The decision to suspend redemptions should be appropriately documented, communicated to the regulatory authorities and to other relevant parties, and communicated to concerned unitholders. When a suspension event actually arises, the responsible entity should thoroughly analyse the situation that might even require involvement from external legal counsel.”

10 | European News & Views | Second Edition 2011

Europe

Positional update on European regulation

In response to the financial crisis and

the threat of economic instability, an

abundance of regulation has hit the

UK financial services industry. This

is something that we have discussed

in other articles in this edition of

European News & Views. And we

have seen how this has been driven

at international and European levels,

with the EU in particular continuing

to develop its agenda for regulatory

reform. But not all initiatives for reform

have been driven by the financial crisis.

In fact, there are a number of reviews

of existing EU legislation taking

place. The following table provides a

snapshot of the current position of key

initiatives currently affecting the asset

management industry across Europe.

If you would like further information

on anything listed below, please

contact [email protected].

Supervisory structure

EU Financial Supervisory Reform

Macro: New European Systemic Risk Board (ESRB)

• Regulations have been published in the European Commission’s Official Journal.

Micro: New European Supervisory Authorities (ESAs)

• Regulations have been published in the European Commission’s Official Journal.

• Chairpersons and executive directors have been confirmed.

• Stakeholder groups have been established for the European Banking Authority (EBA) and European Insurance and Occupational Pensions Authority (EIOPA).

• European Securities and Markets Authority (ESMA) stakeholder group formation currently in progress.

• The ESAs became operational from 1 January 2011.

UK Financial Supervisory Reform

Macro: Financial Policy Committee (FPC) to be established in Bank of England

• HM Treasury issued a consultation paper on 17 February 2011.

• The consultation closed on 14 April 2011.

• The government is expected to publish a white paper, including a draft bill for pre-legislative scrutiny, in spring 2011.

• The FSA split into four main business units in April 2011.

• Government legislation is expected to be introduced before summer 2011.

• Final bill to receive royal assent in summer 2012.

European News & Views | Second Edition 2011 | 11

Europe

Markets

European Markets Infrastructure Regulation (EMIR)

European Commission proposal for a regulation on the European Parliament and of the Council on OTC derivatives, central counterparties and trade repositories

• The proposed regulation was published on 15 September 2010.

• The EU Parliament and EU Council are currently negotiating on the text and final agreement is expected in July 2011.

• Subject to negotiation, regulations will come into force 20 days after publication in the European Commission’s Official Journal.

EU Securities Law

Securities Law Directive (SLD)

• The European Commission published a consultation paper (set of principles) on 5 November 2010.

• The consultation closed on 1 January 2011.

• Responses to the European Commission’s consultation were published on 3 March 2011.

• The European Commission is expected to issue a legislative proposal in Q2 2011.

EU Central Securities Depositaries

European Commission consultation on Central Securities Depositories (CSDs) and on the harmonisation of certain aspects of securities settlement in the European Union

• The European Commission published a consultation paper 13 January 2011.

• The consultation closed on 1 March 2011.

• Responses to the European Commission’s consultation were published on 9 March 2011.

• The European Commission is expected to issue a legislative proposal in June 2011.

“Too big to fail”

UK Investment Bank Resolution Regime

Special Administration Regime (SAR)

• The Investment Bank Special Administration Regulations 2011 and The Investment Bank (Amendment of Definition) Order 2011 was published and entered into force on 8 February 2011.

• HM Treasury is expected to introduce insolvency rules to accompany Regulations in 2011.

• The FSA is expected to consult early in 2011 on proposals to ensure firms prepare their own managed recovery and resolution plan policy.

EU Investor Compensation

Investor Compensation Schemes Directive (ICSD)

• The European Commission issued a proposal for an amending Directive on 12 July 2010.

• The EU Parliament’s Economic and Monetary Affairs Committee (ECON) approved a report on the Commission’s proposal on 13 April 2011.

• The EU Parliament and EU Council are currently negotiating on the text and final agreement is expected in June 2011.

• Member States are expected to transpose the legislation into final rules in 2012.

12 | European News & Views | Second Edition 2011

Europe

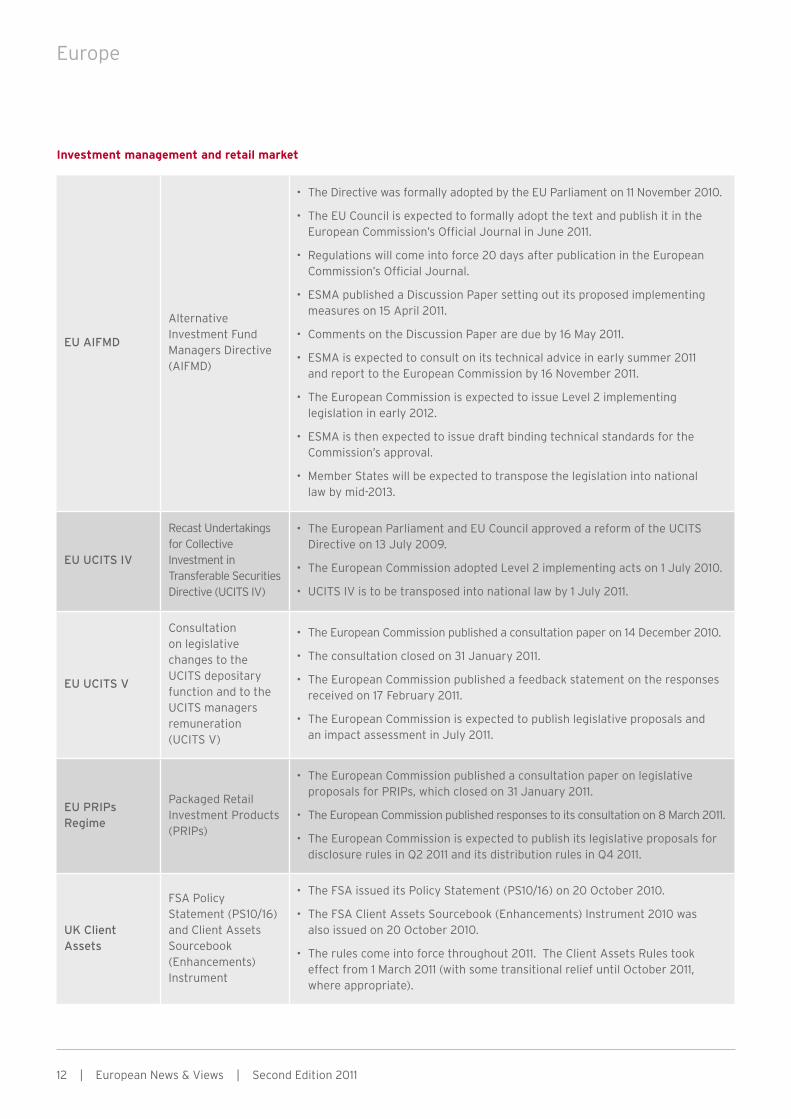

Investment management and retail market

EU AIFMD

Alternative Investment Fund Managers Directive (AIFMD)

• The Directive was formally adopted by the EU Parliament on 11 November 2010.

• The EU Council is expected to formally adopt the text and publish it in the European Commission’s Official Journal in June 2011.

• Regulations will come into force 20 days after publication in the European Commission’s Official Journal.

• ESMA published a Discussion Paper setting out its proposed implementing measures on 15 April 2011.

• Comments on the Discussion Paper are due by 16 May 2011.

• ESMA is expected to consult on its technical advice in early summer 2011 and report to the European Commission by 16 November 2011.

• The European Commission is expected to issue Level 2 implementing legislation in early 2012.

• ESMA is then expected to issue draft binding technical standards for the Commission’s approval.

• Member States will be expected to transpose the legislation into national law by mid-2013.

EU UCITS IV

Recast Undertakings for Collective Investment in Transferable Securities Directive (UCITS IV)

• The European Parliament and EU Council approved a reform of the UCITS Directive on 13 July 2009.

• The European Commission adopted Level 2 implementing acts on 1 July 2010.

• UCITS IV is to be transposed into national law by 1 July 2011.

EU UCITS V

Consultation on legislative changes to the UCITS depositary function and to the UCITS managers remuneration (UCITS V)

• The European Commission published a consultation paper on 14 December 2010.

• The consultation closed on 31 January 2011.

• The European Commission published a feedback statement on the responses received on 17 February 2011.

• The European Commission is expected to publish legislative proposals and an impact assessment in July 2011.

EU PRIPs Regime

Packaged Retail Investment Products (PRIPs)

• The European Commission published a consultation paper on legislative proposals for PRIPs, which closed on 31 January 2011.

• The European Commission published responses to its consultation on 8 March 2011.

• The European Commission is expected to publish its legislative proposals for disclosure rules in Q2 2011 and its distribution rules in Q4 2011.

UK Client Assets

FSA Policy Statement (PS10/16) and Client Assets Sourcebook (Enhancements) Instrument

• The FSA issued its Policy Statement (PS10/16) on 20 October 2010.

• The FSA Client Assets Sourcebook (Enhancements) Instrument 2010 was also issued on 20 October 2010.

• The rules come into force throughout 2011. The Client Assets Rules took effect from 1 March 2011 (with some transitional relief until October 2011, where appropriate).

European News & Views | Second Edition 2011 | 13

Europe

Others

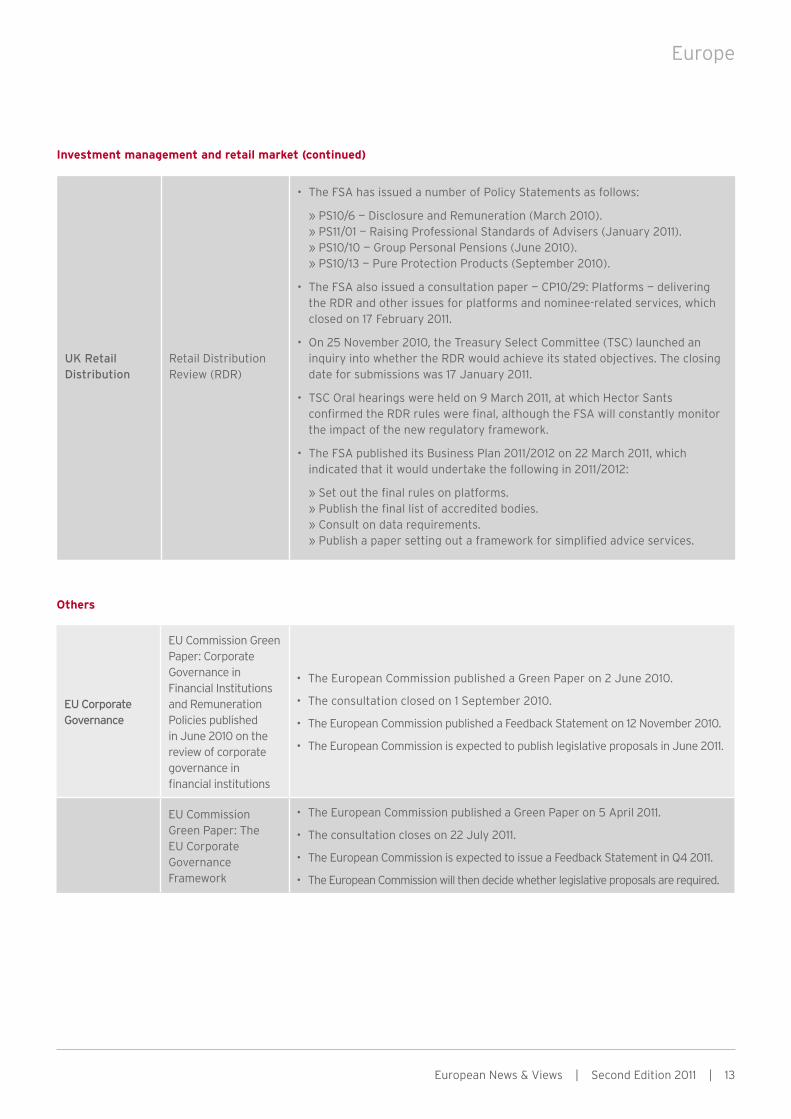

EU Corporate Governance

EU Commission Green Paper: Corporate Governance in Financial Institutions and Remuneration Policies published in June 2010 on the review of corporate governance in financial institutions

• The European Commission published a Green Paper on 2 June 2010.

• The consultation closed on 1 September 2010.

• The European Commission published a Feedback Statement on 12 November 2010.

• The European Commission is expected to publish legislative proposals in June 2011.

EU Commission Green Paper: The EU Corporate Governance Framework

• The European Commission published a Green Paper on 5 April 2011.

• The consultation closes on 22 July 2011.

• The European Commission is expected to issue a Feedback Statement in Q4 2011.

• The European Commission will then decide whether legislative proposals are required.

UK Retail Distribution

Retail Distribution Review (RDR)

• The FSA has issued a number of Policy Statements as follows:

» PS10/6 — Disclosure and Remuneration (March 2010). » PS11/01 — Raising Professional Standards of Advisers (January 2011). » PS10/10 — Group Personal Pensions (June 2010). » PS10/13 — Pure Protection Products (September 2010).

• The FSA also issued a consultation paper — CP10/29: Platforms — delivering the RDR and other issues for platforms and nominee-related services, which closed on 17 February 2011.

• On 25 November 2010, the Treasury Select Committee (TSC) launched an inquiry into whether the RDR would achieve its stated objectives. The closing date for submissions was 17 January 2011.

• TSC Oral hearings were held on 9 March 2011, at which Hector Sants confirmed the RDR rules were final, although the FSA will constantly monitor the impact of the new regulatory framework.

• The FSA published its Business Plan 2011/2012 on 22 March 2011, which indicated that it would undertake the following in 2011/2012:

» Set out the final rules on platforms. » Publish the final list of accredited bodies. » Consult on data requirements. » Publish a paper setting out a framework for simplified advice services.

Investment management and retail market (continued)

14 | European News & Views | Second Edition 2011

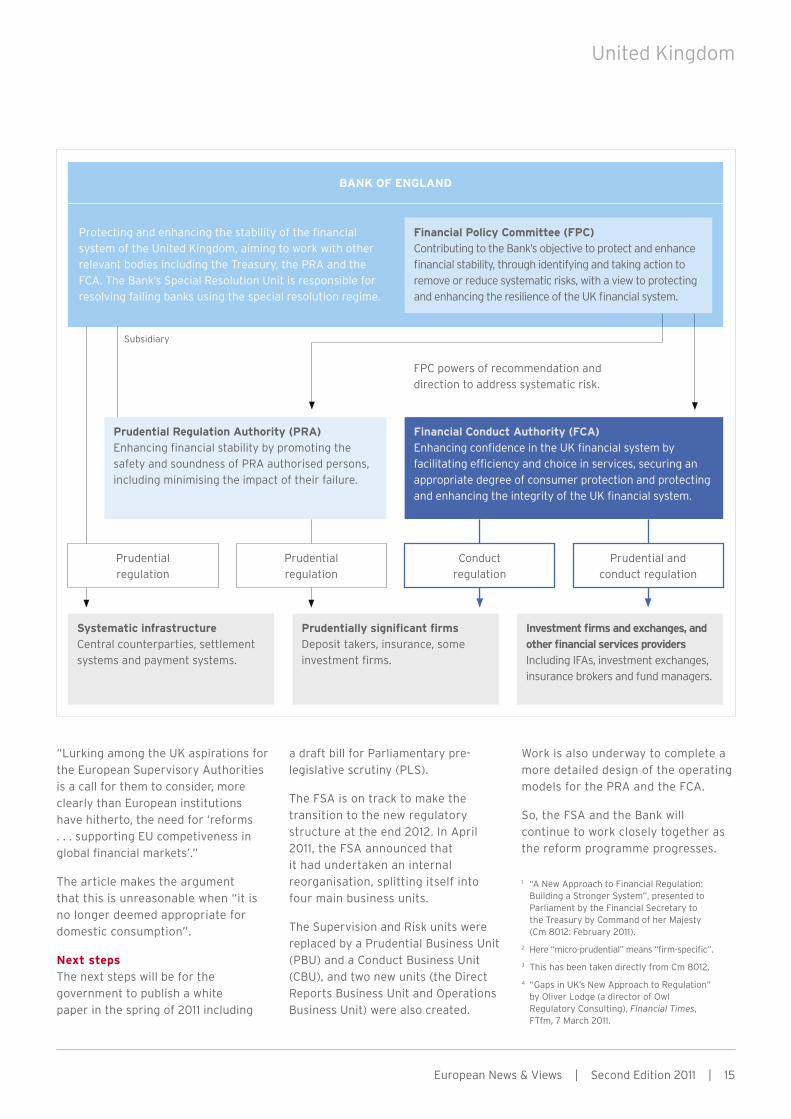

A new approach to financial regulation: building a stronger system

Supported by the Bank of England

(the Bank) and the Financial Services

Authority (FSA), the government

has played a leading role in the

international programme of reform

that is being taken forward by the

Financial Stability Board (FSB),

the International Monetary Fund

(IMF) and the Basel Committee on

Banking Supervision, and within

the European Union.

The government has also established

the Independent Banking Commission

(IBC), chaired by Sir John Vickers,

to consider the structure of the UK

banking market.

Reforms focus on three key

institutional changes:

• A new Financial Policy Committee

(FPC) to be established within

the Bank, with responsibility for

“macro-prudential” regulation, or

regulation of stability and resilience

of the financial system as a whole.

• The “micro-prudential” regulation

of financial institutions that

manage significant risks on their

balance sheets will be carried out

by an operationally independent

subsidiary of the Bank, the Prudential

Regulation Authority (PRA). 2

• The responsibility for conduct

of business regulation will be

transferred to a new specialist

regulator responsible for conduct

issues across the entire spectrum of

financial services. The government

has now finalised the name of this

body, which has had the working

title “Consumer Protection and

Markets Authority” (CPMA), as the

Financial Conduct Authority (FCA).

Under this framework, the Treasury,

the Bank and the FSA will be

collectively responsible for financial

stability. The diagram opposite

depicts the roles of the bodies within

the new regulatory architecture. 3

The government has made it clear

that there will be a fundamental

change in the way that the new

regulatory authorities carry out

their functions. The intention is to

deliver a more judgment-led, focused

and effective regulation of the

financial sector. The reforms

will be implemented through

primary legislation amending the

Financial Services and Markets

Act 2000 (FSMA).

Since the Treasury consultation was

published, a press release issued

on the UK Parliament’s website

(entitled, “Committee Launches

Inquiry into the Accountability of

the Bank of England”) discusses the

fact that on the 3 February 2011, the

Treasury Committee reported on the

government’s proposals for financial

regulation. It commended the Bank’s

engagement with Parliament over the

Monetary Policy Committee. As the

government’s proposals will extend the

responsibilities of the Bank to include

monitoring financial stability and taking

action against threats to that stability,

the Treasury Committee is launching an

inquiry into the Bank to give the issue

the attention it deserves.

Some of the key questions will be

to determine:

• What kind of decisions should be

made by each body within the Bank.

• To whom the Bank should be

accountable.

• What resources the Bank will need

to carry out its functions.

An article in FTfm, dated 7 March

2011, talks about the Treasury’s

proposals: 4

“Keen observers (aka the anoraks)

will be familiar with the government’s

determination to drop the legislative

obligation, previously binding on

the regulators, always to consider

the impact of their actions on the

competiveness of the industry . . .

It is interesting, then, to see the

cultivation of competition emerge

as a key statement in the objectives

of the unborn FCA.”

The article also goes on to uncover a

second surprise from the consultation:

United Kingdom

In February 2011, HM Treasury (the Treasury) consulted on a new approach to financial regulation. The consultation paper

was entitled “Building a Stronger System”. 1 In it, the government asserts its commitment to restoring the UK economy to

sustainable, long-term growth, and to recognising the crucial role of the financial sector.

“Under this framework, the Treasury, the Bank and the FSA will be collectively responsible for financial stability.”

European News & Views | Second Edition 2011 | 15

United Kingdom

“Lurking among the UK aspirations for

the European Supervisory Authorities

is a call for them to consider, more

clearly than European institutions

have hitherto, the need for ‘reforms

. . . supporting EU competiveness in

global financial markets’.”

The article makes the argument

that this is unreasonable when “it is

no longer deemed appropriate for

domestic consumption”.

Next steps

The next steps will be for the

government to publish a white

paper in the spring of 2011 including

a draft bill for Parliamentary pre-

legislative scrutiny (PLS).

The FSA is on track to make the

transition to the new regulatory

structure at the end 2012. In April

2011, the FSA announced that

it had undertaken an internal

reorganisation, splitting itself into

four main business units.

The Supervision and Risk units were

replaced by a Prudential Business Unit

(PBU) and a Conduct Business Unit

(CBU), and two new units (the Direct

Reports Business Unit and Operations

Business Unit) were also created.

Work is also underway to complete a

more detailed design of the operating

models for the PRA and the FCA.

So, the FSA and the Bank will

continue to work closely together as

the reform programme progresses.

1 “A New Approach to Financial Regulation: Building a Stronger System”, presented to Parliament by the Financial Secretary to the Treasury by Command of her Majesty (Cm 8012: February 2011).

2 Here “micro-prudential” means “firm-specific”.

3 This has been taken directly from Cm 8012.

4 “Gaps in UK’s New Approach to Regulation” by Oliver Lodge (a director of Owl Regulatory Consulting), Financial Times, FTfm, 7 March 2011.

Protecting and enhancing the stability of the financial

system of the United Kingdom, aiming to work with other

relevant bodies including the Treasury, the PRA and the

FCA. The Bank’s Special Resolution Unit is responsible for

resolving failing banks using the special resolution regime.

Financial Policy Committee (FPC)

Contributing to the Bank’s objective to protect and enhance

financial stability, through identifying and taking action to

remove or reduce systematic risks, with a view to protecting

and enhancing the resilience of the UK financial system.

Financial Conduct Authority (FCA)

Enhancing confidence in the UK financial system by

facilitating efficiency and choice in services, securing an

appropriate degree of consumer protection and protecting

and enhancing the integrity of the UK financial system.

FPC powers of recommendation and

direction to address systematic risk.

Systematic infrastructure

Central counterparties, settlement

systems and payment systems.

Investment firms and exchanges, and

other financial services providers

Including IFAs, investment exchanges,

insurance brokers and fund managers.

Prudentially significant firms

Deposit takers, insurance, some

investment firms.

Prudential

regulation

Prudential

regulation

Prudential and

conduct regulation

Conduct

regulation

BANK OF ENGLAND

Subsidiary

Prudential Regulation Authority (PRA)

Enhancing financial stability by promoting the

safety and soundness of PRA authorised persons,

including minimising the impact of their failure.

16 | European News & Views | Second Edition 2011

Retail Conduct Risk Outlook and Prudential Risk Outlook arise out of Financial Services Authority (FSA) restructure

In response to the recent financial crisis

and the threat to economic stability,

a plethora of new regulation — set to

continue over the coming months — has

hit the financial services industry.

Against this backdrop, the FSA is

concerned that firms’ assessment and

reaction to the challenges brought on

by new initiatives and regulatory change

could create additional risks to the

detriment of consumers.

In March 2010, the FSA launched its

enhanced Consumer Protection Strategy,

which included a commitment to the

earlier identification of retail conduct

risks. The other initiatives included:

• A more intensive supervision of the

conduct of large retail firms.

• An increased focus on product

intervention, which is further detailed

in the FSA’s Product Intervention

Discussion Paper (published in

January 2011) and covered in our

January Regulatory Update.

• A greater use of enforcement and

other regulatory tools for dealing

with poor conduct.

The FSA’s RCRO 2011

As the FSA aims to see fewer risks

resulting in consumer detriment

across the industry, the RCRO,

published on 28 February 2011,

presents the FSA’s view of current,

emerging and potential risks

arising from firms’ conduct in their

relationship with consumers. It aims

to increase risk awareness and inform

the FSA’s supervisory focus.

The RCRO is divided into two

main sections, “Chapter A — The

Environment” and “Chapter B — The

United Kingdom

This year the FSA has decided to publish two documents (rather than its historical Financial Risk Outlook): the

Prudential Risk Outlook (PRO) and the Retail Conduct Risk Outlook (RCRO). These better fit the coming restructuring

of the FSA into the Prudential Regulation Authority (PRA) and the Financial Conduct Authority (FCA) and reflect the

FSA’s focus on prudential and conduct issues.1 Together, they will help inform how the FSA sets its priorities and deploys

its resources over the next twelve months.2

European News & Views | Second Edition 2011 | 17

United Kingdom

Risks”. The key points of relevance to

asset managers from each of these

sections are detailed below.

Chapter A — The Environment

Consumers and financial services firms

face an uncertain macroeconomic

environment. Many households remain

vulnerable to further macroeconomic

shocks, such as higher unemployment

or interest rates. This section discusses

the key macroeconomic trends that are

of most relevance to consumers.

Asset management and the economy

Crucial to the demand for financial

services is how consumers choose to

allocate their income. Interestingly,

the rate of saving has increased

significantly since before the financial

crisis. In addition, following a period of

disinvestment in financial assets in 2007

and 2008, investment into equity and

pension funds started to increase. In

fact, the UK asset management sector

experienced a record year for retail

investment in 2009 with net retail sales

of GBP25.8 billion. This strong trend

continued in 2010, when net retail sales

showed an inflow of approximately

GBP24 billion.

The RCRO analysis suggests that, due to

the low-interest-rate environment, the

search for yield and capital protection

has driven consumers’ investment

decisions. This is reflected by the

growth of investment in bond funds,

absolute return funds, passive funds

and exchange-traded funds. This trend

is expected to continue for some time.

However, the FSA is concerned that, as

a result, consumers may be attracted to

the higher returns offered by higher risk

products without fully understanding

the impact.

For example, asset managers are

continuing to develop more complex

investment strategies and promoting

these funds to retail investors. Absolute

return funds are one such example.

While they may all use the same sector

name, they use a wide range of often

complex investment strategies across

multiple asset classes. Consumers may

have difficulty in distinguishing between

these different products or in assessing

the level of risk that is being taken to

achieve returns.

There has also been a long-term trend

towards growth in funds being managed

passively (passive funds), which has

recently manifested in the growth of

exchange-traded funds (ETFs). This,

coupled with the changes to adviser

remuneration as a result of the Retail

Distribution Review (RDR), may lead to

advisers increasingly recommending

passive funds. The FSA raises its

concern that consumers may not

understand the difference between

product types in terms of investment

strategy, tax status and risk.

Regulatory background and outlook

This section summarises some of

the main regulatory initiatives that

are currently affecting the asset

management industry.

Retail Distribution Review (RDR)

The rules for implementing the RDR will

come into effect at the end of 2012. The

proposals aim to ensure that:

• Consumers are offered a transparent

and fair charging system for the

advice they receive.

• Consumers are clear about the

service they receive.

• Consumers receive advice from

highly respected professionals.

• Advisory firms become more stable

and better able to meet their

liabilities.

The new rules will apply to any individual

advising on products and services

regardless of the type of firm for which

they work. Therefore, advisers within

banks, asset managers, life insurers, sole

traders, partnerships, stockbrokers, IFAs

or financial advice firms will be subject

to the same regulatory environment.

The RDR introduces minimum

qualification requirements for advisers.

Therefore, it is important for firms to

ensure that their plans for achieving

these qualification requirements are

well under way.

Packaged Retail Investment

Products (PRIPs)

A new EU regime for PRIPs, which

is expected to have complementary

elements to the RDR, is likely to be

implemented in 2012 or 2013. The aim of

the regime is to harmonise the standards

of consumer protection applicable to

substitutable retail products sold by

different sectors of the financial services

industry, including fund managers. The

FSA is working with the Commission in

developing these proposals.

UCITS IV

The new UCITS IV rules, which come

into force from 1 July 2011, except

for the transitional rules for the KIID,

make a number of technical changes

to the current UCITS regulations. Of

particular relevance to consumers is the

replacement of simplified prospectuses

with a key investor information document

(KIID), including a new synthetic risk

and reward indicator. This means that

firms will need to present information

about UCITS funds to consumers in a

different format. The FSA suggests that

there is a possibility that consumers may

be discouraged from buying products

that are classified as higher risk, even

where they might best meet their needs.

Consequently, firms may need to improve

the quality of their marketing and sales

advice to explain the risks and benefits of

their products and invest in systems and

controls to ensure that their KIIDs meet

the requirements of the directive.

Prudential measures with possible

effects on conduct

Prudential measures can affect the

behaviour of firms in a way that

may indirectly affect consumers.

For example, the Basel III framework,

published on 16 December 2010 by the

18 | European News & Views | Second Edition 2011

EU Commission, set out the following

micro-prudential and macro-prudential

reforms for internationally active banks:

• Higher and better quality capital.

• Better risk coverage.

• The introduction of a leverage ratio

as a backdrop to the risk-based

requirement.

• Measures to promote the build-up

of capital that can be drawn down in

periods of stress.

• The introduction of global liquidity

standards.

This culminated in a Policy Statement

(PS) from the FSA (PS09/16) in October

2009. The PS develops an enhanced

prudential framework for firms and

aims to improve their ability to monitor

their liquidity risk and reduce the risk of

failure. This should enhance consumer

protection and, in turn, help to build

greater confidence in the financial

system as a whole. (We cover the

Prudential Risk Outlook [PRO] later in

this article, which provides further detail

on macroeconomic and financial trends.)

Chapter B – The Risks

This section of the RCRO describes the

retail conduct risks that the FSA believes

require particular attention by firms

and in terms of supervisory focus. The

identified risks have been considered

under three categories:

1. Current issues: risks that have

already crystallised, with poor

firm conduct already resulting in

customer detriment.

2. Emerging risks: risks where the

FSA already has evidence of

poor conduct in firms but little

or no evidence yet of widespread

consumer detriment, although the

FSA believes the issue could grow.

3. Potential concerns: risks that may

emerge in the future, given the

possible impact of environmental

factors and firm behaviour.

The following are of particular relevance

to asset managers.

Current issues

The sale and marketing of structured

investment products

The interest in structured investment

products remains high in the current

environment. However, consumers

investing in these products are

exposed to a number of risks, such as

counterparty risk, inflation risk and

market risk. The varying features of

these products can be difficult for

consumers to understand. Therefore,

the quality of the design, marketing and

distribution of structured investments

is of paramount importance. The FSA

suggests that firms should ensure that

they are promoted in a way that is fair,

clear and not misleading, and that they

meet the needs, circumstances and

objectives of each individual investor.

Emerging risks

The increasing popularity of complex

investment products

ETFs — In addition to the risks outlined

earlier, many of the funds underlying

ETFs listed in London are domiciled in

other jurisdictions, usually Luxembourg

and Ireland. Consequently, those ETFs

are primarily supervised and covered

by the relevant investor protection

and compensation schemes of their

country of domicile, which may differ

from the protections offered in the UK.

Therefore, there is a risk that retail

investors may not always be aware of

these differences where they exist.

The FSA has heightened their

supervisory vigilance in this area

and will intervene where they

believe the sale of complex ETFs

or other exchange-traded products

is contributing to poor consumer

outcomes.

Pensions — With the long-term trend

of declining defined benefit pension

schemes, consumers are becoming

increasingly dependent on annuity

income and other private investment

to fund their retirement. In its 2010

Financial Risk Outlook, the FSA

reported that the financial crisis had

materially impacted the value of

investments held by consumers close

to retirement. The FSA is concerned

that such consumers will be vulnerable

to those products that offer potentially

greater returns but that are not suited

to individual circumstances or are

higher risk than appreciated or desired.

Therefore, ensuring that consumers

understand the level of risk, capital

protection, costs and likely impact on

investment return is essential.

Unauthorised Collective Investment

Schemes (UCIS) — The FSA is becoming

increasingly concerned over the sale of

UCIS to consumers. The risks associated

with such funds are not always easy

for advisers and consumers to

understand. In addition, the governance

arrangements and financial structure

of the schemes may themselves cause

risks for investors. For example, many

UCIS may not be subject to investment

and borrowing restrictions, which aim to

ensure a prudent spread of risk and, as

a result, are generally considered to be

higher risk.

Transition to the implementation of

the RDR — The FSA is concerned firms

making changes to their business

models may seek to maximise their

recurring revenue stream before the

RDR is implemented. This could be

by: attempting to acquire a larger

market share, which could result

in unnecessary churn in the retail

investment market and excessive

costs for consumers; building up their

book to increase the attractiveness

of the firm, particularly should they

be planning to leave the market and

sell their business; or increasing the

amount of trail commission on their

United Kingdom

European News & Views | Second Edition 2011 | 19

books. As a consequence, the FSA

has heightened their supervisory

vigilance in this area and will continue

to intervene where it believes high

commission levels may be contributing

to poor consumer outcomes.

Platforms — In the third quarter

of 2010, platforms administered

approximately GBP135 billion in IFA

assets. In addition, approximately

50% of all new retail fund investment

business was placed through platforms.

While platforms can bring benefits to

consumers, they also bring a number of

risks. In March 2010, the FSA published

the findings of its thematic review, which

assessed the quality of advice when

recommending investments held on

platforms. The key risks identified were:

• Poor quality of advice in relation to

investments.

• A lack of review of oversight and risk

management procedures.

• Inadequate management of conflicts

of interest.

• Poor standards of disclosure of

information on charges and

ongoing services.

In November 2010, the FSA published a

consultation paper on platforms (CP10/29)

to ensure that platform services would be

fully aligned with the standards required

by the RDR after January 2013. The main

proposals included:

• Preventing product providers from

making payments that advisers

could use to disguise the charge the

customer is paying for advice.

• Ensuring platforms allow their

customers to transfer their

investments elsewhere without

having to cash them in first.

• Requiring platforms to be upfront

about the income they receive from

fund managers or product providers.

• Ensuring that customers who invest

in funds through platforms are

provided with information about

the fund from fund managers and

maintain their voting rights.

The FSA plans to continue monitoring

developments in this market and will

consider whether further regulatory

action is required. The FSA suggests

that firms should ensure that they

only place investments on a platform

where it is considered to be in the

best interests of clients and should

ensure that the oversight and risk

management arrangements of

their business are fit for purpose,

particularly when making changes to

their business model.

Firms’ reward policies and practices

— The FSA is concerned that, in the

current environment in particular,

firms may consider using their reward

policies to achieve specific strategic

targets, which could influence staff

behaviour and pose risks to the

delivery of fair consumer outcomes or

to the effectiveness of controls that

would otherwise mitigate these risks.

As a result, the FSA expects firms

to ensure that they comply with the

revised Remuneration Code. This seeks

to ensure that remuneration policies,

practices and procedures for firms are

consistent with, and promote, effective

risk management and include measures

to avoid conflicts of interest.3

Potential concerns

Business model changes

following the RDR

As already discussed, the RDR may

require asset management firms

to alter their business models — for

example, by changing their charging

structures or launching new share

classes to support the rules on

charging. The way in which funds

are distributed will also undoubtedly

change — for example, some financial

advice firms and advisers are planning

to leave the market because of

the RDR (the FSA estimates that

adviser numbers will reduce by 11%).

Therefore, product providers will have

to identify new strategies to get their

products to market. Some of these

changes may lead to new areas of risk

for consumers.

Next steps

With the RDR on the horizon, business

model change will inevitably require

firms to adopt new processes and the

FSA has outlined that it will be vital for

firms to ensure that their systems and

controls, including the competence

of employees, keep pace with these

changes. The FSA plans to work with

the industry to ensure these risks

are minimised.

Firms should ensure that any

marketing material and sales advice

clearly explains the risks and benefits

of each product and is clear, fair

and not misleading. In particular,

firms should ensure that their KIIDs

meet the requirements of the

UCITS IV Directive.

UCITS IV contains a number of new

rules regarding risk management. By

ensuring that they have a robust risk

United Kingdom

“In the third quarter of 2010, platforms administered approximately GBP135 billion in IFA assets. In addition, approximately 50% of all new retail fund investment business was placed through platforms.”

20 | European News & Views | Second Edition 2011

management framework and process

in place, firms can make great steps

in mitigating many of the risks

outlined in this article.

As always, disclosure and transparency

underpin the strategic objectives of