Embed Size (px)

Citation preview

MOODYS.COM

16 JANUARY 2014

NEWS & ANALYSIS Corporates 2

» Elliott Management’s Proposal to Boost Shareholder Returns Is Credit Negative for Juniper Networks

» Sears’ Holiday Woes Accelerate Its Cash Burn, a Credit Negative

» Road King’s China Toll Road Acquisition Is Credit Negative

» Antam Will Suffer from the Indonesian Export Ban of Mineral Ores

Banks 6

» Chile’s New Bankruptcy Law Is Credit Positive for Banks

» Capital Relief for German Mutualist Banking Groups on Intra-Group Stakes and Lending Is Credit Positive

» Belarus’ Capital Injections into Banks Are Credit Positive

» Vietnam Relaxes Bank Foreign Ownership Rules, a Credit Positive for Domestic Lenders

Insurers 16 » Preliminary US Healthcare Exchange Demographics Are Credit

Negative for Health Insurers

Asset Managers and Money Market Funds 18 » Systemically Important Designation for Asset Managers and

Funds Is Credit Positive

Sovereigns 21

» US Federal Budget Deficit Shrinks at Faster Pace, a Credit Positive

US Public Finance 23 » California’s Proposed Budget Would Significantly Improve

School and Community College Districts’ Liquidity

» FEMA Contribution to Nassau County, New York, Sewage Plant Repairs Is Positive for the County

RECENTLY IN CREDIT OUTLOOK

» Articles in Last Monday’s Credit Outlook 26 » Go to Last Monday’s Credit Outlook

Click here for Weekly Market Outlook, our sister publication containing Moody’s Analytics’ review of market activity, financial predictions, and the dates of upcoming economic releases.

NEWS & ANALYSIS Credit implications of current events

2 MOODY’S CREDIT OUTLOOK 16 JANUARY 2014

Corporates

Elliott Management’s Proposal to Boost Shareholder Returns Is Credit Negative for Juniper Networks

On Monday, New York-based hedge fund Elliott Management disclosed that it had accumulated a 6.2% stake in Juniper Networks, Inc. (Baa2 stable) and that it had urged the network infrastructure company to return cash to shareholders, reduce costs and adopt other initiatives to “drive long-term shareholder value.” Although Elliott’s proposals include some positive credit elements, such as calling for a more disciplined cost structure, full implementation of the plan would be credit negative for Juniper because it would increase financial leverage, reduce domestic liquidity and limit the company’s ability to make acquisitions or invest in existing businesses.

In a filing with the US Securities and Exchange Commission, Elliott recommended that Juniper buy back as much as $3.5 billion of its common stock, or 29% of its $12 billion market capitalization; initiate a 50-cent-a-share common dividend that would amount to an annual payout of about $200 million; streamline its security and switching product portfolio, which accounts for 25% of total revenue; and cut operating expenses by at least $200 million annually.

Juniper would have to borrow $2.15 billion and use $1.35 billion of its domestic cash to repurchase common stock in two installments: $1.5 billion immediately and through an accelerated share repurchase program, and another $1 billion one year from now. If Juniper were able to reduce operating costs by $200 million immediately, adjusted debt/EBITDA would increase to 2.7x (or 3.4x without cost reductions) from 1.6x as of 30 September 2013. We have noted previously that leverage above 2.0x would pressure Juniper’s credit rating.

Juniper maintains $1.7 billion, or 41%, of its total cash domestically. Elliott’s proposal would require Juniper to use an estimated $390 million of domestic cash to pay common dividends, in addition to the $1.35 billion it would allocate for share buybacks over two years. The dividend payment would equal approximately 25% of our projection for discretionary cash flow in 2014, comparable to the 25% average among dividend-paying technology firms. Assuming that Juniper generates about 75% of its cash flow from operations less capital expenditures domestically, domestic liquidity would fall to less than $700 million a year from now, considerably below the $1 billion level needed to stave off pressure on Juniper’s credit rating.

Elliott also contends that Juniper’s research and development (R&D) budget remains bloated relative to key peers on the basis of percentage of sales, R&D per employee and average salary per software engineer. If Juniper were to reduce R&D as a percentage of sales to a broad peer average of 11% from 21%, it would achieve $420 million in annual savings. Although the company’s R&D spending is elevated, especially when compared with Cisco Systems Inc.’s (A1 stable) R&D expenditures of 12% of sales, it would be challenging for Juniper to reduce it materially in the face of the company’s smaller scale and architectural changes in the networking sector, including the slow but growing deployment of software-defined networking offerings by enterprise and service provider customers.

Richard J. Lane Senior Vice President +1.212.553.7863 [email protected]

NEWS & ANALYSIS Credit implications of current events

3 MOODY’S CREDIT OUTLOOK 16 JANUARY 2014

Sears’ Holiday Woes Accelerate Its Cash Burn, a Credit Negative Last Thursday, Sears Holdings Corp. (Caa1 stable) provided a dismal holiday season update, disclosing that comparable-store sales in its domestic businesses (Sears and Kmart) declined 7.4% quarter-to-date through 6 January 2014. The company also said it expected domestic adjusted EBITDA to be between negative $80 million and $20 million in the fiscal fourth quarter ending 1 February, versus $365 million a year earlier. For the full year, the company expects domestic adjusted EBITDA to range between negative $308 million and negative $408 million, versus $557 million last year. Following these revisions, we lowered Sears’ corporate family rating to Caa1 from B3 on Friday.

These results are credit negative because they indicate that Sears’ initiatives to improve performance are not resonating with consumers and that the negative trends are accelerating. Comparable-store sales at its Sears Domestic’s stores fell 9.2% in the fourth quarter to date, compared with a decline of 2.4% for the first nine months of 2013. Importantly, Sears Domestic has called out weakness in its home appliance businesses throughout 2013, while competitors such as The Home Depot, Inc. (A2 stable) reported positive trends in home appliances, which points to market-share erosion for Sears.

This weak performance is also accelerating Sears’ cash burn. We now expect Sears’ cash burn (including capital expenditures, cash interest and required pension contributions) for the fiscal year ending 1 February 2014 to be in excess of $1.2 billion, compared with around $300 million a year earlier. We expect the cash burn for the fiscal year ending in January 2015 to remain well above $1 billion.

Although the company’s cash burn is meaningful and rising, Sears’ liquidity remains good. To raise cash, the company is considering strategic alternatives for its Sears Auto Center business, has filed a registration statement with the US Securities and Exchange Commission for a possible spinoff of its Lands’ End business and continues to work with the board and management of Sears Canada to increase the value of Sears Holdings’ 51% stake in Sears Canada.

The company disclosed that as of 4 January it had approximately $1.0 billion of cash in the US and Canada and $1.8 billion available under its domestic revolving credit facilities. The company also has sizable real estate holdings, including more than 700 Sears and Kmart locations in the US, a substantial majority of which are unpledged. Moreover, Sears has no significant debt maturities until approximately $2.24 billion of bank and bond debt that comes due in 2018. The company has ample liquidity despite its high cash burn, although this cannot continue indefinitely.

Scott Tuhy Vice President - Senior Credit Officer +1.212.553.3703 [email protected]

NEWS & ANALYSIS Credit implications of current events

4 MOODY’S CREDIT OUTLOOK 16 JANUARY 2014

Road King’s China Toll Road Acquisition Is Credit Negative Last Thursday, Road King Infrastructure Limited (B1 positive) said it had acquired a 49% equity interest in the operating rights of the Machao Expressway in China’s Anhui Province for RMB271 million. The acquisition is credit negative because it will increase the company’s debt and reduce its interest coverage during the next six to 12 months.

In addition to the acquisition cost, Road King or Anhui Machao Expressway Co., Ltd. (unrated), a project company that owns the expressway, will likely incur debt to cover about RMB500 million of the expressway’s construction costs. The expressway began operating at the end of 2013, and was wholly owned by Anhui Transportation Investment Group Co., Ltd (unrated), a state-owned enterprise, before Road King acquired its equity interest.

We estimate that Road King’s debt will increase by 9%-10% as a result of the transaction. Its adjusted debt/capitalization ratio, including the pro rated debt of its existing jointly controlled entities, will increase to 55%-56% from 53.2% as of 30 June 2013. The company’s adjusted interest coverage will weaken to around 2.4x from 2.6x. Road King will consume internal cash of about RMB121 million to pay the unpaid amount of the tender offer for the equity interests immediately after relevant government departments approve the transaction.

Because the road is new, we expect it will be two to three years before the expressway generates meaningful cash flow for Road King. As a result, Road King’s interest coverage from its toll road income will weaken amid higher adjusted interest expenses.

However, Road King has an adequate cash buffer to cover the acquisition. Its cash balance of HKD6.4 billion (around RMB5 billion) at the end of June 2013 and operating cash flows will be adequate to cover its short-term debt of HKD5.55 billion (around RMB4.3 billion), outstanding land payments for its property business and the acquisition costs. Furthermore, given Road King’s good track record of operating toll roads, we believe the execution risk of the new acquisition is low.

Established in 1994, Road King is a Hong Kong-listed company with investments in toll roads and property development projects in China. It is the only property developer with significant investments in toll roads among the Chinese property companies we rate.

In recent years, Road King’s property business has outpaced its toll-road business, with the segment’s profit growing at a compound annual growth rate of 23% to HKD725 million in 2012 from HKD482 million in 2010. By comparison, the toll-road business’ compound annual growth rate rose 7% over the same period to HKD166 million.

Franco Leung Assistant Vice President - Analyst +852.3758.1521 [email protected]

NEWS & ANALYSIS Credit implications of current events

5 MOODY’S CREDIT OUTLOOK 16 JANUARY 2014

Antam Will Suffer from the Indonesian Export Ban of Mineral Ores Last Sunday, the ban on the export of Indonesia’s mineral ores went into effect. The ban is credit negative for state-owned PT Aneka Tambang (Persero) Tbk (Antam, Ba3 review for downgrade), Indonesia’s second-largest nickel ore and ferronickel exporter, because it prevents the company from shipping its nickel and bauxite ore to overseas customers, thereby hurting profitability. On Tuesday, we put Antam’s ratings on review for downgrade.

Based on the current version of the ban, we expect Antam’s EBIT/interest to fall below 4.0x from 4.8x as of 30 September 2013, and its retained cash flow/debt ratio to drop below 20% from 72.9% over the same period. Antam’s large cash balance of more than $300 million at 30 September 2013 and the flexibility in the timing of its capital spending will help it weather the effects of the ban. We will reassess the Indonesian government’s support that we have incorporated into Antam’s Ba3 rating because Antam has not benefited from exemptions from the ban that the government granted to other miners.

The implementation of the ban was required by Indonesia’s 2009 Mineral and Coal Mining Law, which sought to encourage miners to build smelters in Indonesia that would enhance the value of unprocessed ores, helping labour absorption within Indonesia and providing incremental revenues to the government.

Full details on the implementation of the ban have yet to emerge. On Saturday, one day before the ban took effect, the Indonesian government agreed last-minute to carve-outs that we expect will grant temporary exemptions to copper, manganese, zinc, lead and iron concentrate exporters until 2017. However, the ban on nickel ore went through as planned. Before the ban, Indonesia was a primary source of nickel and bauxite for Chinese aluminium and stainless steel producers.

Sales of unprocessed nickel ore constitute roughly 33% of Antam’s revenue, with the balance coming primarily from ferronickel, gold and silver. All nickel ore sales were generated through exports, so the ban deprives the company of around $300 million in sales. Although the loss of revenue occurs immediately, Antam needs more clarity to adjust its cost base, leaving it exposed to ongoing losses as long as these uncertainties exist.

Ahead of the ban, Antam built a new $490 million chemical grade alumina plant in Tayan, which the company expects will be ready for commercial production in April. The new facility will alleviate some of the top-line pressure in 2014 given that the company expects the facility’s annualized sales to be $200 million. Antam is also building a new ferronickel plant in East Halmahera with a capacity of 27,000 metric tonnes per year that it expects to be commercially viable in 2016. As a comparison, Antam produced 14,293 metric tonnes of ferronickel in the nine months to 30 September 2013.

Brian Grieser Vice President - Senior Analyst +65.6398.3713 [email protected]

Vincent Tordo Associate Analyst +65.6398.8331 [email protected]

NEWS & ANALYSIS Credit implications of current events

6 MOODY’S CREDIT OUTLOOK 16 JANUARY 2014

Banks

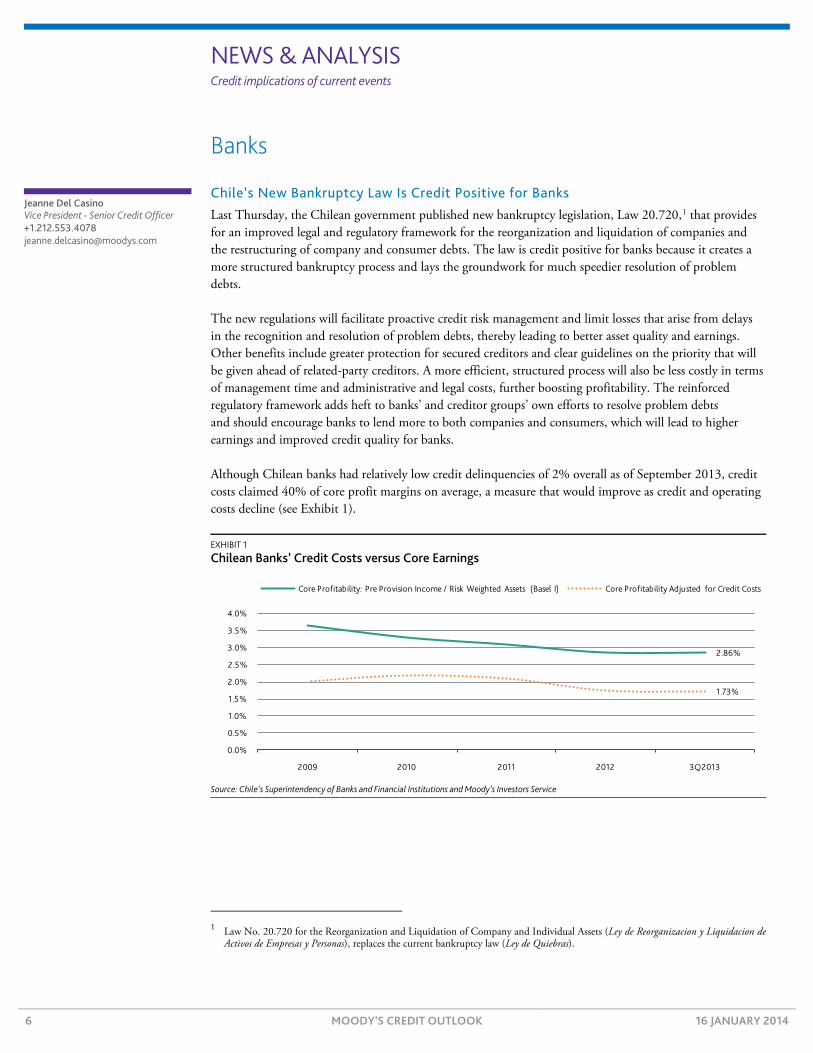

Chile’s New Bankruptcy Law Is Credit Positive for Banks Last Thursday, the Chilean government published new bankruptcy legislation, Law 20.720,1 that provides for an improved legal and regulatory framework for the reorganization and liquidation of companies and the restructuring of company and consumer debts. The law is credit positive for banks because it creates a more structured bankruptcy process and lays the groundwork for much speedier resolution of problem debts.

The new regulations will facilitate proactive credit risk management and limit losses that arise from delays in the recognition and resolution of problem debts, thereby leading to better asset quality and earnings. Other benefits include greater protection for secured creditors and clear guidelines on the priority that will be given ahead of related-party creditors. A more efficient, structured process will also be less costly in terms of management time and administrative and legal costs, further boosting profitability. The reinforced regulatory framework adds heft to banks’ and creditor groups’ own efforts to resolve problem debts and should encourage banks to lend more to both companies and consumers, which will lead to higher earnings and improved credit quality for banks.

Although Chilean banks had relatively low credit delinquencies of 2% overall as of September 2013, credit costs claimed 40% of core profit margins on average, a measure that would improve as credit and operating costs decline (see Exhibit 1).

EXHIBIT 1

Chilean Banks’ Credit Costs versus Core Earnings

Source: Chile’s Superintendency of Banks and Financial Institutions and Moody’s Investors Service

1 Law No. 20.720 for the Reorganization and Liquidation of Company and Individual Assets (Ley de Reorganizacion y Liquidacion de

Activos de Empresas y Personas), replaces the current bankruptcy law (Ley de Quiebras).

2.86%

1.73%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

2009 2010 2011 2012 3Q2013

Core Profitability: Pre Provision Income / Risk Weighted Assets (Basel I) Core Profitability Adjusted for Credit Costs

Jeanne Del Casino Vice President - Senior Credit Officer +1.212.553.4078 [email protected]

NEWS & ANALYSIS Credit implications of current events

7 MOODY’S CREDIT OUTLOOK 16 JANUARY 2014

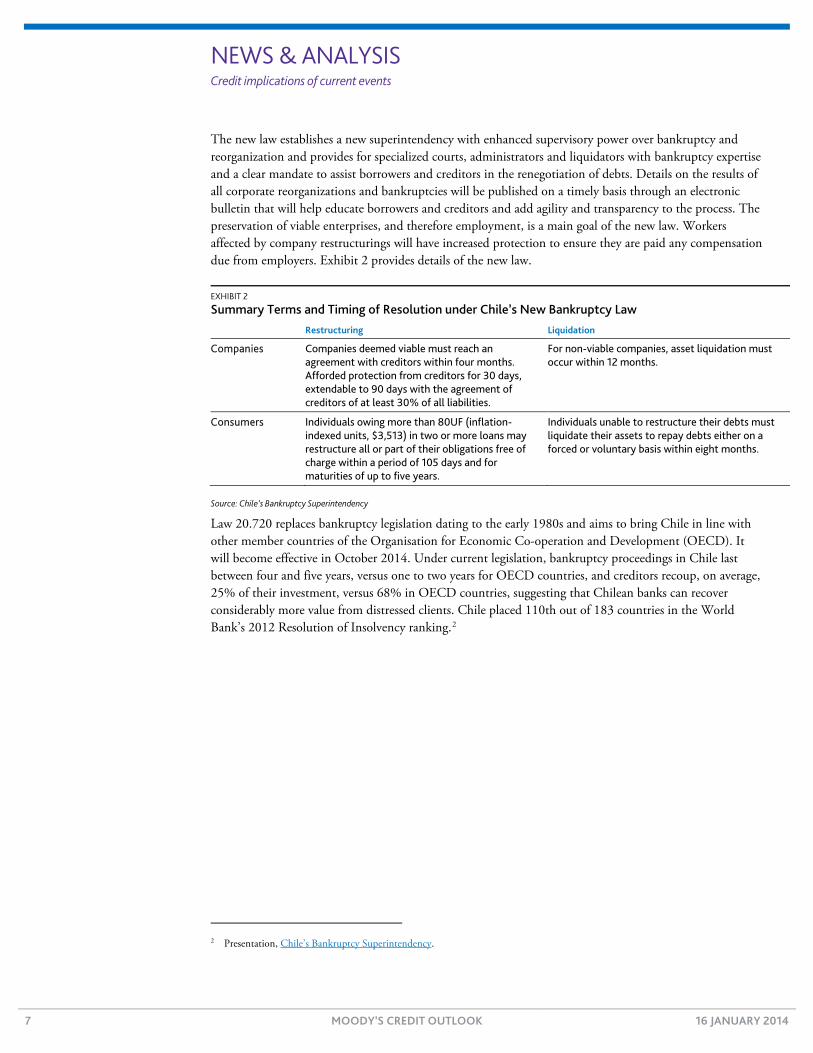

The new law establishes a new superintendency with enhanced supervisory power over bankruptcy and reorganization and provides for specialized courts, administrators and liquidators with bankruptcy expertise and a clear mandate to assist borrowers and creditors in the renegotiation of debts. Details on the results of all corporate reorganizations and bankruptcies will be published on a timely basis through an electronic bulletin that will help educate borrowers and creditors and add agility and transparency to the process. The preservation of viable enterprises, and therefore employment, is a main goal of the new law. Workers affected by company restructurings will have increased protection to ensure they are paid any compensation due from employers. Exhibit 2 provides details of the new law.

EXHIBIT 2

Summary Terms and Timing of Resolution under Chile’s New Bankruptcy Law Restructuring Liquidation

Companies Companies deemed viable must reach an agreement with creditors within four months. Afforded protection from creditors for 30 days, extendable to 90 days with the agreement of creditors of at least 30% of all liabilities.

For non-viable companies, asset liquidation must occur within 12 months.

Consumers Individuals owing more than 80UF (inflation-indexed units, $3,513) in two or more loans may restructure all or part of their obligations free of charge within a period of 105 days and for maturities of up to five years.

Individuals unable to restructure their debts must liquidate their assets to repay debts either on a forced or voluntary basis within eight months.

Source: Chile’s Bankruptcy Superintendency

Law 20.720 replaces bankruptcy legislation dating to the early 1980s and aims to bring Chile in line with other member countries of the Organisation for Economic Co-operation and Development (OECD). It will become effective in October 2014. Under current legislation, bankruptcy proceedings in Chile last between four and five years, versus one to two years for OECD countries, and creditors recoup, on average, 25% of their investment, versus 68% in OECD countries, suggesting that Chilean banks can recover considerably more value from distressed clients. Chile placed 110th out of 183 countries in the World Bank’s 2012 Resolution of Insolvency ranking.2

2 Presentation, Chile’s Bankruptcy Superintendency.

NEWS & ANALYSIS Credit implications of current events

8 MOODY’S CREDIT OUTLOOK 16 JANUARY 2014

Capital Relief for German Mutualist Banking Groups on Intra-Group Stakes and Lending Is Credit Positive Last Thursday, German newspaper Frankfurter Allgemeine Zeitung reported that German bank regulator Bundesanstalt fuer Finanzdienstleistungsaufsicht (BaFin) granted mutualist groups in Germany an exemption from certain capital deductions attributable to intra-group stake holdings and from risk weights on intra-group exposures.

Although BaFin’s move will lift some of the pressure on individual member banks to raise capital ratios under Basel III, the regulator’s decision is credit positive for Germany’s mutualist groups. The decision takes into consideration several financial factors, such as the flexible allocation of capital and liquidity, that support the groups’ cohesion and ability to continue their commitment of mutual support.

BaFin made use of an option under the Capital Requirement Regulation (CRR)3 that took effect 1 January and which allows national regulators to consider certain capital requirements at the group level of mutualist groups rather than at the entity level.

With its decision, BaFin acknowledges the effectiveness of the cross-sector support schemes. The beneficiaries will be public-sector Sparkassen-Finanzgruppe (Aa2 stable, C+/a2 stable4) and the German cooperative banking association, FinanzGruppe Volksbanken und Raiffeisenbanken (BVR, unrated).

Continuation of the zero risk weight on intra-group exposures will support funding for the weaker, mostly wholesale-funded member banks. If BaFin had decided to introduce risk weights for exposures within these groups, it would have excluded the weakest member banks from access to group liquidity, exposing them to higher funding risks and leaving the stronger members with excess liquidity.

For some of the weaker, lower-rated Landesbanken, which are still recovering from distress during the banking crisis, the indirect benefits of cross-sector cohesion remain important. The zero risk weight therefore remains a stabilising factor for these groups and the financial system as a whole.

With their cohesion remaining strong, BaFin’s endorsement of their effective support schemes and certain capital requirements monitored at the group level,5 we assess the strength of the mutualist groups based on their average financial profile, rather than based on their weakest link. We also think the regulator’s decision will not impair the comparability of capital resources with those of its peers, given that the treatment closely resembles that of Europe’s larger, legally integrated banking groups.

Sparkassen-Finanzgruppe and the BVR are in many ways comparable to private banking groups owing to their common strategy and business culture, largely unified operations and shared brand names. Their comprehensive financial product suites, which include mutual funds and insurance products, and their technology needs mostly rely on specialised entities they own within their groups.

3 Capital Requirement Regulation article 49, 3.(a) 4 Ratings shown in this report are the bank’s deposit rating, its standalone bank financial strength rating/baseline credit assessment

and the corresponding rating outlooks. 5 The mutualist groups must regularly give evidence of their compliance with the minimum capital requirements under Basel III on a

consolidated or aggregated basis, whereby they will calculate available capital on a net basis, which eliminates the multiple use of elements eligible for the calculation of own funds.

Katharina Barten Vice President - Senior Credit Officer +49.69.707.30.765 [email protected]

Carola Schuler Managing Director +49.69.707.30.766 [email protected]

NEWS & ANALYSIS Credit implications of current events

9 MOODY’S CREDIT OUTLOOK 16 JANUARY 2014

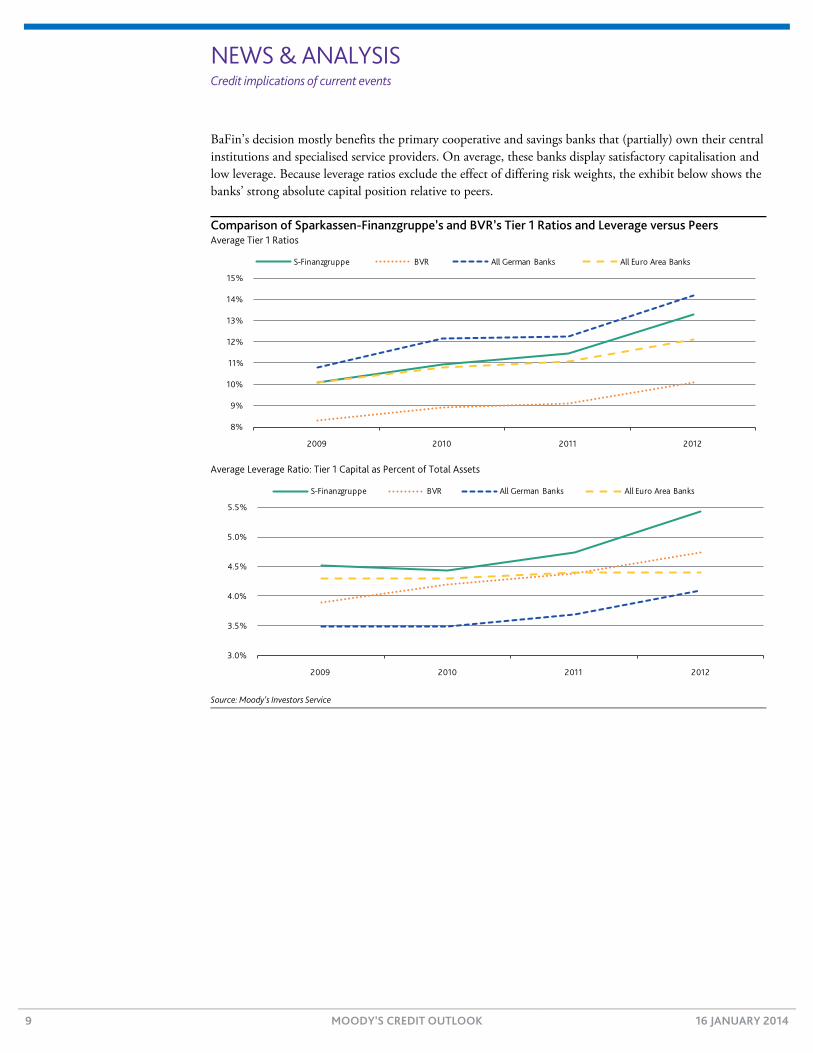

BaFin’s decision mostly benefits the primary cooperative and savings banks that (partially) own their central institutions and specialised service providers. On average, these banks display satisfactory capitalisation and low leverage. Because leverage ratios exclude the effect of differing risk weights, the exhibit below shows the banks’ strong absolute capital position relative to peers.

Comparison of Sparkassen-Finanzgruppe’s and BVR’s Tier 1 Ratios and Leverage versus Peers Average Tier 1 Ratios

Average Leverage Ratio: Tier 1 Capital as Percent of Total Assets

Source: Moody’s Investors Service

8%

9%

10%

11%

12%

13%

14%

15%

2009 2010 2011 2012

S-Finanzgruppe BVR All German Banks All Euro Area Banks

3.0%

3.5%

4.0%

4.5%

5.0%

5.5%

2009 2010 2011 2012

S-Finanzgruppe BVR All German Banks All Euro Area Banks

NEWS & ANALYSIS Credit implications of current events

10 MOODY’S CREDIT OUTLOOK 16 JANUARY 2014

Belarus’ Capital Injections into Banks Are Credit Positive

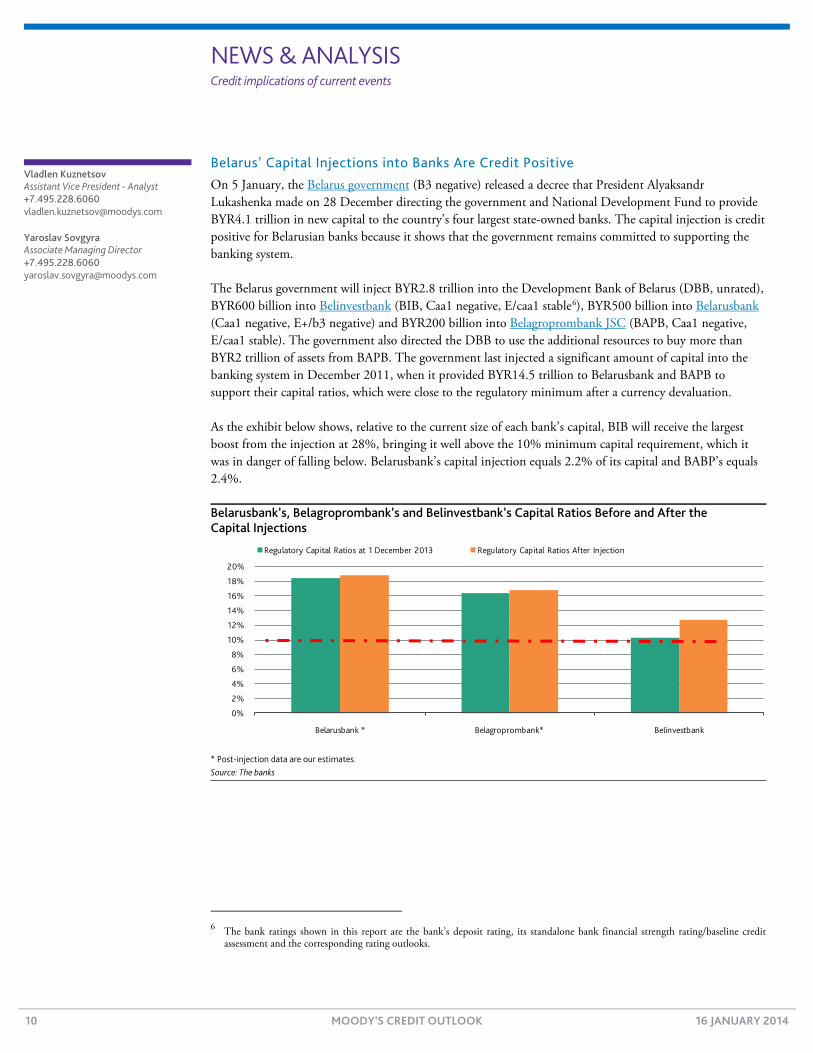

On 5 January, the Belarus government (B3 negative) released a decree that President Alyaksandr Lukashenka made on 28 December directing the government and National Development Fund to provide BYR4.1 trillion in new capital to the country’s four largest state-owned banks. The capital injection is credit positive for Belarusian banks because it shows that the government remains committed to supporting the banking system.

The Belarus government will inject BYR2.8 trillion into the Development Bank of Belarus (DBB, unrated), BYR600 billion into Belinvestbank (BIB, Caa1 negative, E/caa1 stable6), BYR500 billion into Belarusbank (Caa1 negative, E+/b3 negative) and BYR200 billion into Belagroprombank JSC (BAPB, Caa1 negative, E/caa1 stable). The government also directed the DBB to use the additional resources to buy more than BYR2 trillion of assets from BAPB. The government last injected a significant amount of capital into the banking system in December 2011, when it provided BYR14.5 trillion to Belarusbank and BAPB to support their capital ratios, which were close to the regulatory minimum after a currency devaluation.

As the exhibit below shows, relative to the current size of each bank’s capital, BIB will receive the largest boost from the injection at 28%, bringing it well above the 10% minimum capital requirement, which it was in danger of falling below. Belarusbank’s capital injection equals 2.2% of its capital and BABP’s equals 2.4%.

Belarusbank’s, Belagroprombank’s and Belinvestbank’s Capital Ratios Before and After the Capital Injections

* Post-injection data are our estimates. Source: The banks

6 The bank ratings shown in this report are the bank’s deposit rating, its standalone bank financial strength rating/baseline credit

assessment and the corresponding rating outlooks.

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

Belarusbank * Belagroprombank* Belinvestbank

Regulatory Capital Ratios at 1 December 2013 Regulatory Capital Ratios After Injection

Vladlen Kuznetsov Assistant Vice President - Analyst +7.495.228.6060 [email protected]

Yaroslav Sovgyra Associate Managing Director +7.495.228.6060 [email protected]

NEWS & ANALYSIS Credit implications of current events

11 MOODY’S CREDIT OUTLOOK 16 JANUARY 2014

The DBB’s latest recapitalization, along with a swap of risky assets with BAPB, is an indication that the government is taking steps to release the banking sector from having to participate in certain high-risk government programs in favor of financing these programs solely through the DBB. The government has undertaken certain reforms, including creating the DBB in 2011, to assume the underwriting of loans for the most risky government programs. These reforms were a pre-condition for the approval of financing from the Russia-led EurAsian Economic Community. Since then, Belarusbank and BAPB have transferred approximately $1 billion in loans to the DBB.

In this context, BAPB’s capital injection is significantly credit positive. Although its capital will only rise 2.4% from the injection, the asset swap with the DBB will allow BAPB to replace more of its higher-risk assets with safer government bonds and cash. Of the BYR2 trillion in assets, the DBB will pay BYR1 trillion of cash for its own bonds, and BYR1 trillion in government bonds for long-term loans. Each of these equals 11% of BAPB’s capital, for a total effect of 22% of BAPB’s capital.

The effect on the DBB’s creditworthiness is mixed. On the one hand, it will benefit significantly from the 54% increase in capital, but it will also add high-risk assets and the capital injection may allow it to do more risky lending in the future.

NEWS & ANALYSIS Credit implications of current events

12 MOODY’S CREDIT OUTLOOK 16 JANUARY 2014

Vietnam Relaxes Bank Foreign Ownership Rules, a Credit Positive for Domestic Lenders Last Monday, the law firm of Allens in a note to clients shared its interpretation of a government decree on foreign ownership of banks published on 3 January. Although the headline change introduced by Decree 01/2014/ND-CP focused on an increase in the foreign ownership limit in banks to 30% from 20% as of 20 February, Allens’ read of the decree’s likely application is that Vietnam has effectively abolished the upper limit on foreign investments in domestic banks, subject to special conditions.

The relaxation of ownership rules is credit positive for Vietnamese banks because it gives foreign shareholders the flexibility to increase their stake. This, in turn, would attract new foreign capital and improve banks’ loss-absorption capacity, which is currently weak owing to the large overhang of problem loans. However, we are skeptical about the extent to which an increase to 30% from 20% will attract broad-based interest given that investors would not achieve control over a bank. This is what makes Allens’ interpretation of the possible majority participation in the future – should it materialize – an even more positive development because such greater flexibility in the ownership regime would likely attract a greater number of investors and capital for the benefiting banks.

If majority foreign ownership were allowed, we estimate that the “special case” status would be more likely for the nine undisclosed banks that have been earmarked for restructuring by the Vietnamese government in a report released in 2012. We also think the special conditions could extend to larger banks in which foreign shareholders already control 15%-20%, because problem loans are plaguing larger banks as well. Foreign investors have almost fully utilized the previous 20% cap, so the higher limit should stimulate additional foreign direct investments into the sector.

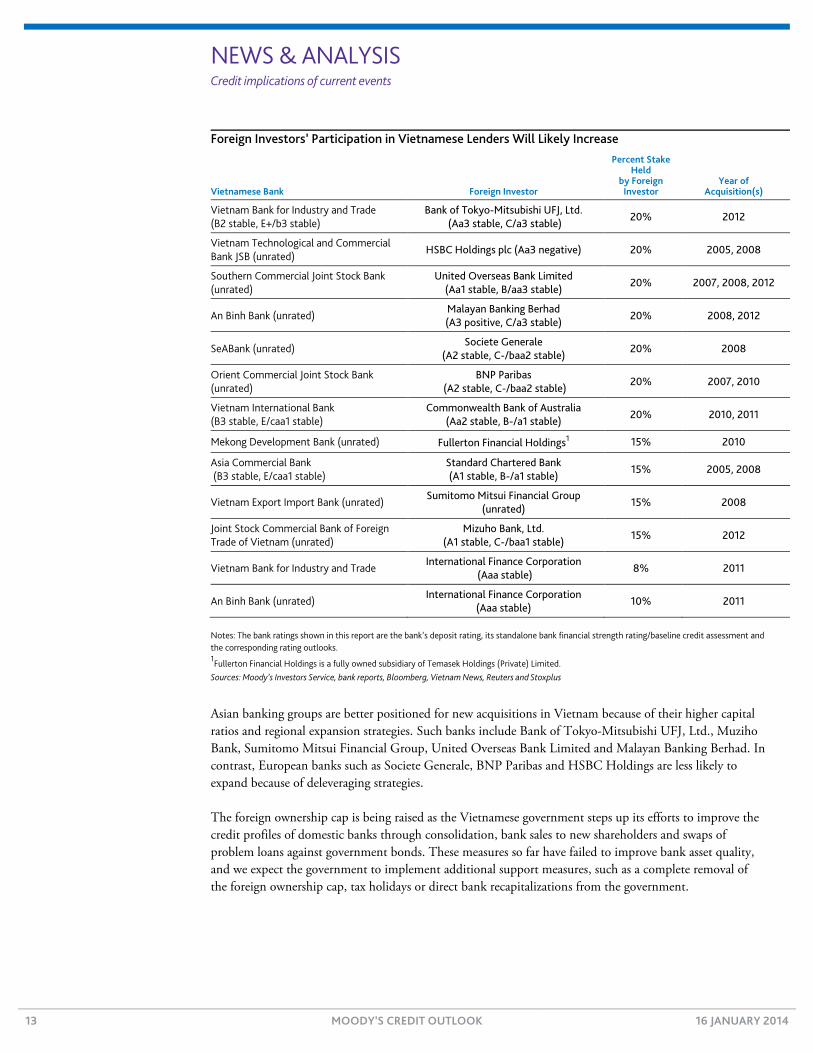

Foreign banking groups that already have stakes in Vietnamese banks (see exhibit below) are more likely to be the first investors to own majority interests in local lenders, followed by investors in low price-to-earnings stocks. Still, new equity investments into Vietnamese banks will be moderate because domestic banks lost some of their appeal after the 2008-10 credit boom. Moreover, banks globally are adjusting their capital structures to Basel III rules, so larger investments in non-consolidated subsidiaries will pressure Tier 1 capital ratios at the parent level.7

7 Minority interest greater than 20% results in deductions from parent’s common equity Tier 1 capital.

Eugene Tarzimanov Vice President - Senior Credit Officer +65.6398.8329 [email protected]

Gene Fang Vice President - Senior Analyst +65.6398.8311 [email protected]

NEWS & ANALYSIS Credit implications of current events

13 MOODY’S CREDIT OUTLOOK 16 JANUARY 2014

Foreign Investors’ Participation in Vietnamese Lenders Will Likely Increase

Vietnamese Bank Foreign Investor

Percent Stake Held

by Foreign Investor

Year of Acquisition(s)

Vietnam Bank for Industry and Trade (B2 stable, E+/b3 stable)

Bank of Tokyo-Mitsubishi UFJ, Ltd. (Aa3 stable, C/a3 stable)

20% 2012

Vietnam Technological and Commercial Bank JSB (unrated)

HSBC Holdings plc (Aa3 negative) 20% 2005, 2008

Southern Commercial Joint Stock Bank (unrated)

United Overseas Bank Limited (Aa1 stable, B/aa3 stable)

20% 2007, 2008, 2012

An Binh Bank (unrated) Malayan Banking Berhad (A3 positive, C/a3 stable)

20% 2008, 2012

SeABank (unrated) Societe Generale

(A2 stable, C-/baa2 stable) 20% 2008

Orient Commercial Joint Stock Bank (unrated)

BNP Paribas (A2 stable, C-/baa2 stable)

20% 2007, 2010

Vietnam International Bank (B3 stable, E/caa1 stable)

Commonwealth Bank of Australia (Aa2 stable, B-/a1 stable)

20% 2010, 2011

Mekong Development Bank (unrated) Fullerton Financial Holdings1 15% 2010

Asia Commercial Bank (B3 stable, E/caa1 stable)

Standard Chartered Bank (A1 stable, B-/a1 stable)

15% 2005, 2008

Vietnam Export Import Bank (unrated) Sumitomo Mitsui Financial Group

(unrated) 15% 2008

Joint Stock Commercial Bank of Foreign Trade of Vietnam (unrated)

Mizuho Bank, Ltd. (A1 stable, C-/baa1 stable)

15% 2012

Vietnam Bank for Industry and Trade International Finance Corporation

(Aaa stable) 8% 2011

An Binh Bank (unrated) International Finance Corporation

(Aaa stable) 10% 2011

Notes: The bank ratings shown in this report are the bank’s deposit rating, its standalone bank financial strength rating/baseline credit assessment and the corresponding rating outlooks. 1Fullerton Financial Holdings is a fully owned subsidiary of Temasek Holdings (Private) Limited. Sources: Moody’s Investors Service, bank reports, Bloomberg, Vietnam News, Reuters and Stoxplus

Asian banking groups are better positioned for new acquisitions in Vietnam because of their higher capital ratios and regional expansion strategies. Such banks include Bank of Tokyo-Mitsubishi UFJ, Ltd., Muziho Bank, Sumitomo Mitsui Financial Group, United Overseas Bank Limited and Malayan Banking Berhad. In contrast, European banks such as Societe Generale, BNP Paribas and HSBC Holdings are less likely to expand because of deleveraging strategies.

The foreign ownership cap is being raised as the Vietnamese government steps up its efforts to improve the credit profiles of domestic banks through consolidation, bank sales to new shareholders and swaps of problem loans against government bonds. These measures so far have failed to improve bank asset quality, and we expect the government to implement additional support measures, such as a complete removal of the foreign ownership cap, tax holidays or direct bank recapitalizations from the government.

NEWS & ANALYSIS Credit implications of current events

14 MOODY’S CREDIT OUTLOOK 16 JANUARY 2014

Insurers

Preliminary US Healthcare Exchange Demographics Are Credit Negative for Health Insurers On Monday, the US Department of Health and Human Services (HHS) released data showing that initial enrollment on the healthcare exchanges is skewed toward an older and therefore less healthy population. For health insurers, a risk pool consisting of a higher-than-expected mix of older individuals would create challenges resulting not only in higher medical costs and downward earnings pressure in 2014, but also upward pressure for premiums in 2015. Neither outcome bodes well for a vibrant insurance exchange, which insurers had been counting on for increased revenues and income. Both WellPoint, Inc. (Baa2 stable) and Health Net, Inc. (Ba3 positive), having participated fairly aggressively in the exchanges, are more exposed to a potential adverse earnings development.

The enrollment statistics show that only 24% of those who have enrolled in the exchange for private healthcare insurance are in the critical 18-34-year-old age group, well short of the 40% target based on the proportion of eligible people in this age group. The way the exchange products are structured and priced, a sizable portion of these healthy individuals must enroll so their lower claim costs can subsidize the higher anticipated claim costs of less healthy individuals.

The Obama administration remains hopeful that more young people will sign up for healthcare insurance in the remaining months before the end of the open enrollment period on 31 March 2014. The administration points to similar results in the Massachusetts healthcare plan several years ago, which experienced a higher enrollment of young individuals closer to the open enrollment deadline. Taking no chances, the administration is planning a major marketing effort aimed at this age group over the next several weeks.

Despite the Obama administration’s optimism, we continue to have doubts about the enrollment outlook based on the economics of the situation for those not receiving a government-provided subsidy to offset premiums. The economics for healthy young individuals do not provide much incentive for them to sign up. For those not eligible for a subsidy, a low-cost plan on the insurance exchange will cost more than $100 per month and will carry a high deductible of several thousand dollars. On the other hand, the penalty for not having health insurance during 2014 is minimal (for an individual, it is limited to the greater of $95 or 1% of income).

We see two other challenges related to those in the 18-34-year-old age group that may be problematic for health insurers. The first is the health status of those who have signed up; we suspect that the enrollees may very well be the least healthy of the 18-34-year-old age group, or those who have a specific need for health insurance coverage in the coming year (e.g., young couples with intentions of using maternity benefits). If this is the case, this group would not provide the financial support insurers need to cover the higher medical costs of the older enrollees.

Steve Zaharuk Senior Vice President +1.212.553.1634 [email protected]

NEWS & ANALYSIS Credit implications of current events

15 MOODY’S CREDIT OUTLOOK 16 JANUARY 2014

The second challenge relates to the percentage within the 18-34-year-old group that cancel their policies after a few months. Since insurers are relying on a full year of premiums from this age group to support claims from older individuals, the potential for a large number of these “young invincibles” cancelling their policies during the year is a risk for insurers. The probability of cancellation may be higher for those who purchased a policy as a result of a marketing push rather than a perceived need. Although these individuals may have been convinced of the value of a comprehensive health insurance package, the monthly premium requirement, along with a lack of need to obtain medical care, may cause them to reevaluate.

NEWS & ANALYSIS Credit implications of current events

16 MOODY’S CREDIT OUTLOOK 16 JANUARY 2014

Asset Managers

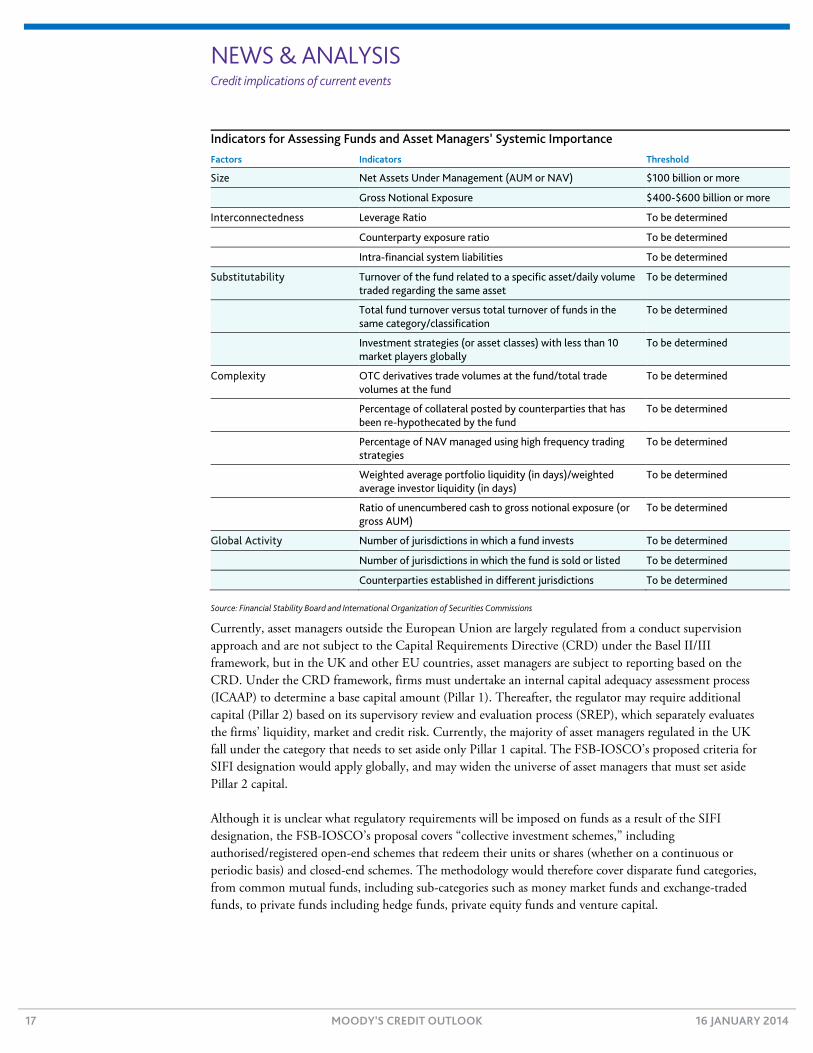

Systemically Important Designation for Asset Managers and Funds Is Credit Positive Last Wednesday, the Financial Stability Board (FSB) and the International Organization of Securities Commissions (IOSCO) published their consultative document on a proposed methodology for identifying non-bank, non-insurer global systematically important financial institutions (SIFIs),8 including investment funds and asset managers.

This is a step toward tighter regulation of shadow banking,9 and if implemented by national regulators, large funds and asset managers could face bank-style supervisory regimes. Although such a designation will likely lead to an increased cost of capital for such firms through higher required capital, more stringent reporting requirements and amplified risk assessment procedures,10 we expect the SIFI designation to strengthen the creditworthiness of those entities.

An institution will be designated a SIFI if its distress or disorderly failure would cause significant disruption to the global financial system and economic activity across jurisdictions, owing to its size, complexity and systemic interconnectedness (see exhibit). The FSB is focusing on size to set the materiality thresholds for determining the assessment pools for SIFIs. For investment funds, the threshold is set at $100 billion in net assets under management. In the case of hedge funds, an alternative threshold will be set at $400-$600 billion in gross notional exposure. In addition to size, the FSB is seeking public comment on setting additional materiality thresholds based on global activities.

8 FSB-IOSCO, Consultative Document: Assessment Methodologies for Identifying Non-Bank Non-Insurer Global Systemically

Important Financial Institutions, 8 January 2014. 9 Financial Stability Board, Strengthening Oversight and Regulation of Shadow Banking, 29 August 2013. 10 The Bank of England addresses the economic effect of CRD IV on investment firms in its consultation paper, Strengthening capital

standards: implementing CRD IV, August 2013, which concludes that investment firms will face higher capital requirements under CRD IV. The Investment Management Association estimated the cost to the investment industry of additional regulatory reporting requirements in its report, “The Real Cost of Regulation,” October 2011.

Soo Shin Kobberstad Vice President - Senior Analyst +44.20.7772.5214 [email protected]

Vanessa Robert Vice President - Senior Credit Officer +33.1.53.30.10.23 [email protected]

NEWS & ANALYSIS Credit implications of current events

17 MOODY’S CREDIT OUTLOOK 16 JANUARY 2014

Indicators for Assessing Funds and Asset Managers’ Systemic Importance Factors Indicators Threshold

Size Net Assets Under Management (AUM or NAV) $100 billion or more

Gross Notional Exposure $400-$600 billion or more

Interconnectedness Leverage Ratio To be determined

Counterparty exposure ratio To be determined

Intra-financial system liabilities To be determined

Substitutability Turnover of the fund related to a specific asset/daily volume traded regarding the same asset

To be determined

Total fund turnover versus total turnover of funds in the same category/classification

To be determined

Investment strategies (or asset classes) with less than 10 market players globally

To be determined

Complexity OTC derivatives trade volumes at the fund/total trade volumes at the fund

To be determined

Percentage of collateral posted by counterparties that has been re-hypothecated by the fund

To be determined

Percentage of NAV managed using high frequency trading strategies

To be determined

Weighted average portfolio liquidity (in days)/weighted average investor liquidity (in days)

To be determined

Ratio of unencumbered cash to gross notional exposure (or gross AUM)

To be determined

Global Activity Number of jurisdictions in which a fund invests To be determined

Number of jurisdictions in which the fund is sold or listed To be determined

Counterparties established in different jurisdictions To be determined

Source: Financial Stability Board and International Organization of Securities Commissions

Currently, asset managers outside the European Union are largely regulated from a conduct supervision approach and are not subject to the Capital Requirements Directive (CRD) under the Basel II/III framework, but in the UK and other EU countries, asset managers are subject to reporting based on the CRD. Under the CRD framework, firms must undertake an internal capital adequacy assessment process (ICAAP) to determine a base capital amount (Pillar 1). Thereafter, the regulator may require additional capital (Pillar 2) based on its supervisory review and evaluation process (SREP), which separately evaluates the firms’ liquidity, market and credit risk. Currently, the majority of asset managers regulated in the UK fall under the category that needs to set aside only Pillar 1 capital. The FSB-IOSCO’s proposed criteria for SIFI designation would apply globally, and may widen the universe of asset managers that must set aside Pillar 2 capital.

Although it is unclear what regulatory requirements will be imposed on funds as a result of the SIFI designation, the FSB-IOSCO’s proposal covers “collective investment schemes,” including authorised/registered open-end schemes that redeem their units or shares (whether on a continuous or periodic basis) and closed-end schemes. The methodology would therefore cover disparate fund categories, from common mutual funds, including sub-categories such as money market funds and exchange-traded funds, to private funds including hedge funds, private equity funds and venture capital.

NEWS & ANALYSIS Credit implications of current events

18 MOODY’S CREDIT OUTLOOK 16 JANUARY 2014

Currently, regulated investment funds or collective investment schemes, such as undertakings for collective investment in transferable securities (UCITS), are generally exempt from CRD. It is not clear whether funds will be subject to capital requirements or only to disclosure requirements (Pillar 3) to publish detailed risk assessment of the fund. In June 2013, IOSCO published its Principles for the Regulation of Exchange Traded Funds, which placed significant importance on better disclosure requirements.

Although more stringent risk assessments, capital requirements and greater transparency are credit positive for investors in large, complex asset managers and investment funds, operational and cost burdens will clearly increase for firms that meet the SIFI criteria, especially during the initial implementation period. Of the range of entities that may receive the SIFI designation, the bigger firms are more likely to withstand the higher costs. This may lead to an unintended consequence of distorted competitiveness in favour of the larger players in the SIFI league. Those SIFIs just at the cusp of the SIFI threshold may scale down in size or strategy. As a result, the market may become fragmented, with very large players at one end of the spectrum, and small funds on the other.

NEWS & ANALYSIS Credit implications of current events

19 MOODY’S CREDIT OUTLOOK 16 JANUARY 2014

Sovereigns

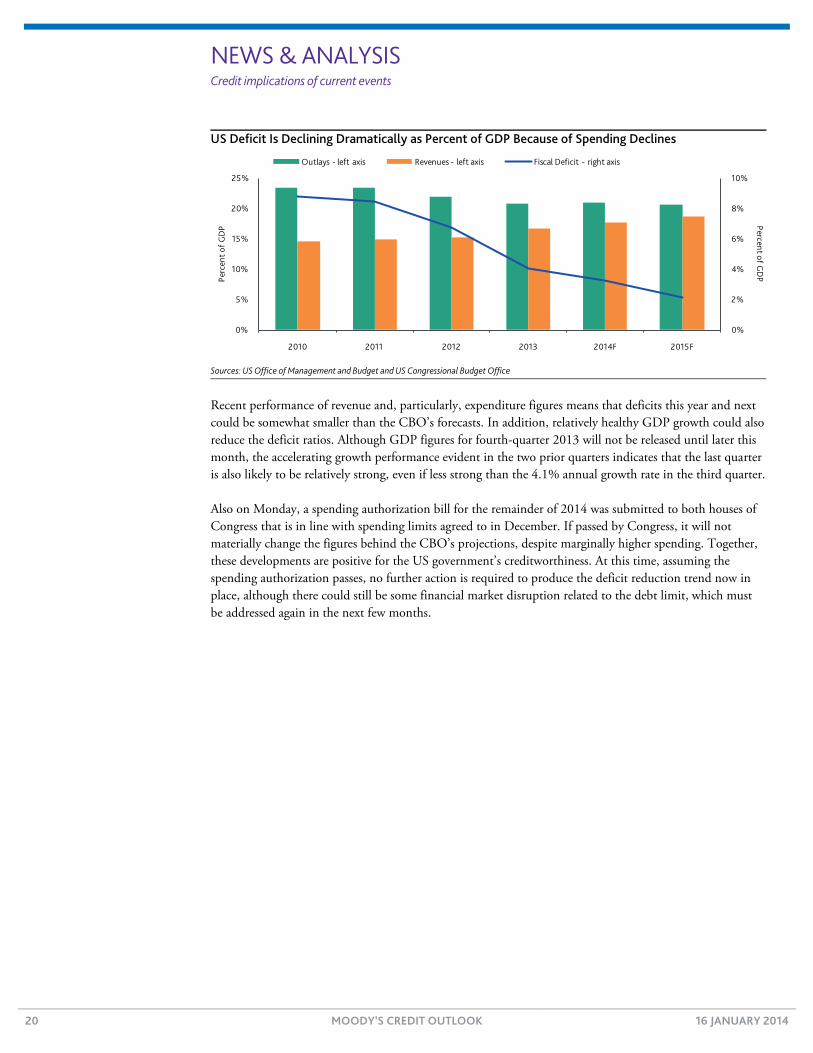

US Federal Budget Deficit Shrinks at Faster Pace, a Credit Positive On Monday, the US Treasury released its monthly statement for December, which covers the first quarter of the 2014 fiscal year and indicates that the federal deficit is falling more quickly than the government expected, a credit positive development for the US government (Aaa stable). Furthermore, because GDP growth has been accelerating, the deficit as a percent of GDP is likely to be declining even more quickly. The spending agreement reached in Congress on Monday evening, if implemented, would maintain this trend.

During the fourth quarter of calendar 2013, which is the first quarter of the federal fiscal year 2014, total revenues rose 8.0% from a year earlier. The biggest drivers of the revenue rise were social insurance and retirement taxes, most importantly social security, which rose by about one quarter as a result of the higher tax rate that became effective at the beginning of 2013. Total social insurance and retirement taxes account for nearly one third of federal revenues. At the same time, individual income taxes, which make up almost half of total revenues, declined slightly from the year-earlier period. Corporate income taxes, much smaller at only about 10% of the total, showed a strong 10.8% increase because of robust corporate profits.

Meanwhile, federal expenditures recorded a 7.8% drop, although this was partly the result of the accounting treatment of transfers from Fannie Mae and Freddie Mac to the Treasury. Such transfers, which were more than $30 billion during the quarter, are counted by the Treasury as negative expenditures. However, even after adjusting for this factor, other expenditures fell at a rate of about 4%. Sequestration meant that the decline was seen in many categories of spending, although the Department of Health and Human Services and the Social Security Administration saw some increase in their outlays, large portions of which are not affected by sequestration. It is notable that interest payments paid by the Treasury fell despite the stock of debt being larger. The Treasury was able to reduce its interest payments because interest rates remained very low and it could refinance more expensive debt issued in past years with lower-yielding securities.

These trends in revenues and outlays together reduced the budget deficit during the quarter by 41% from the comparable year-earlier period. As shown in the exhibit, the Congressional Budget Office (CBO) had projected a drop in the deficit for the 2014 fiscal year to 3.3% of GDP from 3.9% (projected earlier, but now 4.1%) in 2013 and 6.8% in 2012. For 2015, the CBO’s projected deficit is 2.1%.

Steven Hess Senior Vice President +1.212.553.4741 [email protected]

NEWS & ANALYSIS Credit implications of current events

20 MOODY’S CREDIT OUTLOOK 16 JANUARY 2014

US Deficit Is Declining Dramatically as Percent of GDP Because of Spending Declines

Sources: US Office of Management and Budget and US Congressional Budget Office

Recent performance of revenue and, particularly, expenditure figures means that deficits this year and next could be somewhat smaller than the CBO’s forecasts. In addition, relatively healthy GDP growth could also reduce the deficit ratios. Although GDP figures for fourth-quarter 2013 will not be released until later this month, the accelerating growth performance evident in the two prior quarters indicates that the last quarter is also likely to be relatively strong, even if less strong than the 4.1% annual growth rate in the third quarter.

Also on Monday, a spending authorization bill for the remainder of 2014 was submitted to both houses of Congress that is in line with spending limits agreed to in December. If passed by Congress, it will not materially change the figures behind the CBO’s projections, despite marginally higher spending. Together, these developments are positive for the US government’s creditworthiness. At this time, assuming the spending authorization passes, no further action is required to produce the deficit reduction trend now in place, although there could still be some financial market disruption related to the debt limit, which must be addressed again in the next few months.

0%

2%

4%

6%

8%

10%

0%

5%

10%

15%

20%

25%

2010 2011 2012 2013 2014F 2015F

Percent of GD

PPerc

ent o

f GD

P

Outlays - left axis Revenues - left axis Fiscal Deficit - right axis

NEWS & ANALYSIS Credit implications of current events

21 MOODY’S CREDIT OUTLOOK 16 JANUARY 2014

US Public Finance

California’s Proposed Budget Would Significantly Improve School and Community College Districts’ Liquidity Last Thursday, California (A1 stable) Governor Jerry Brown released his proposed 2014-15 state budget, which includes the elimination of a $6.2 billion backlog of deferred state aid payments and adds $4.8 billion in new funding for school and community college districts. The budget plan is credit positive for the districts because it materially improves their liquidity, makes them less reliant on short-term borrowing and bolsters cash reserves.

The state delayed an increasingly larger amount of aid payments to districts during and after the recession. Under the 2013-14 state budget, only about half of the outstanding $6.2 billion in “deferrals” (delayed payments of state funding to districts) were to be paid in fiscal 2014-15, with the remaining $2.9 billion in fiscal 2015-16. The new proposal eliminates all outstanding deferrals in July 2014 without creating any future ones. The 2014-15 proposed budget would also increase new funding by 8% to $4.8 billion for school and community college districts.

Districts that are heavily reliant on state aid, generally those with lower wealth and property tax values, were most affected by the deferrals and would benefit the most from the governor’s proposal. The largest affected districts include Los Angeles Unified School District (Aa2 stable), Long Beach Unified School District (Aa2) and Fresno Unified School District (Aa3 negative). Other districts with larger portions of their general funding coming from property taxes will receive little or no benefit from the early deferral payments.

The governor’s plan to eliminate all aid deferrals will strengthen districts’ liquidity compared with our earlier expectations and could be the beginning of several years of on-time payments. Furthermore, we expect school and community college districts to be significantly less dependent on short-term borrowing and have healthier cash reserves.

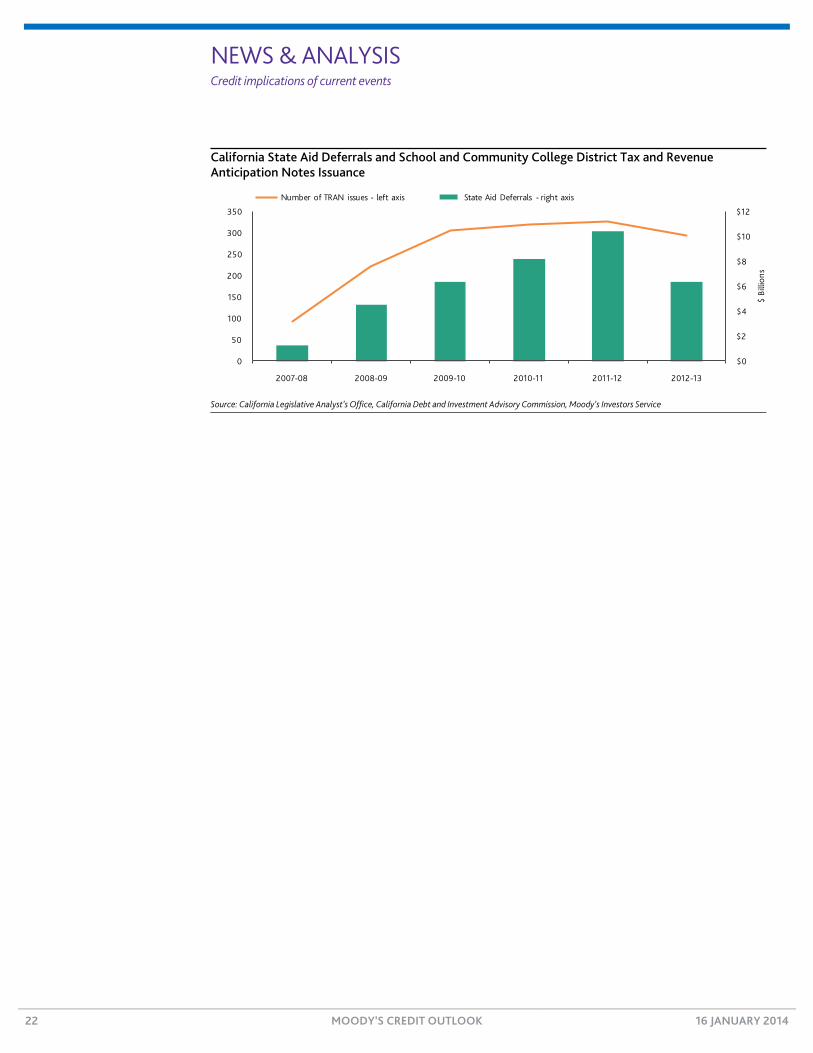

The state government deferred state aid payments during the recession to avoid permanent cuts to school and community college districts. As the state would pay off prior-year deferrals, it created new ones and began developing a large backlog of payments. At the height of deferrals in fiscal 2011-12, the state owed districts $10.2 billion, 22% of annual state aid.

To make up for delayed state aid, school and community college districts increasingly relied on borrowing in the short-term market via tax and revenue anticipation notes (TRANs) for cash flow needs (see exhibit). Districts issued nearly 330 TRANs in fiscal 2011-12, versus about 90 in 2007-08 – a more than 250% increase. Districts with a heavy reliance on state aid for annual funding experienced significant liquidity challenges and were the most reliant on TRANs.

Eric Harper Analyst +1.415.274.1753 [email protected]

NEWS & ANALYSIS Credit implications of current events

22 MOODY’S CREDIT OUTLOOK 16 JANUARY 2014

California State Aid Deferrals and School and Community College District Tax and Revenue Anticipation Notes Issuance

Source: California Legislative Analyst’s Office, California Debt and Investment Advisory Commission, Moody’s Investors Service

$0

$2

$4

$6

$8

$10

$12

0

50

100

150

200

250

300

350

2007-08 2008-09 2009-10 2010-11 2011-12 2012-13

$ Bi

llion

s

Number of TRAN issues - left axis State Aid Deferrals - right axis

NEWS & ANALYSIS Credit implications of current events

23 MOODY’S CREDIT OUTLOOK 16 JANUARY 2014

FEMA Contribution to Nassau County, New York, Sewage Plant Repairs Is Positive for the County On Saturday, New York Governor Andrew Cuomo announced that the US Federal Emergency Management Agency (FEMA) had approved at least $730 million to repair and rebuild a Nassau County, New York (A2 stable), sewage treatment plant damaged by Superstorm Sandy. The announcement is credit positive for Nassau County because the subsidy reduces the need for a debt issuance that would have increased the financially constrained county’s outstanding debt by 27%.

The Bay Park Sewage Treatment Plant serves approximately 550,000 residents, or 41% of the county’s population, and treats 58 million gallons of sewage daily. Superstorm Sandy destroyed the facility’s electrical grid and shut down the plant for two days. The county estimates that necessary repairs and upgrades for the facility will cost approximately $850 million. The county had planned to finance these capital investments through a combination of state loans and long-term financing. Until now, however, the federal government had not committed to a specific share of the construction costs. FEMA’s $730 million commitment is the agency’s largest award to date for Sandy-related repairs to any local government but New York City.

Over the past decade, Nassau County has relied heavily on both short- and long-term borrowing to fund its operations. The county has taken measures to reduce expenditures under the oversight of the Nassau County Interim Finance Authority (NIFA, sales tax rated Aa1 stable), a state-appointed control board, and has had some success in reducing headcount. However, the county has limited ability to reduce its annual debt service, which remains highest in the state.

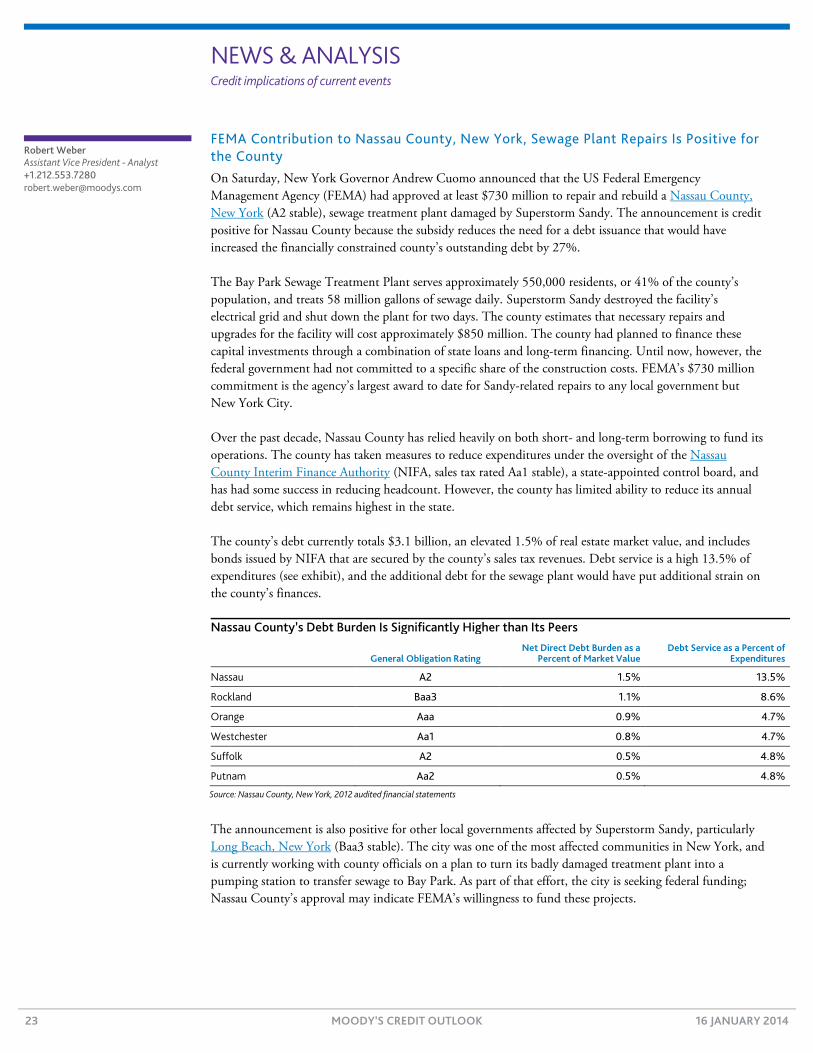

The county’s debt currently totals $3.1 billion, an elevated 1.5% of real estate market value, and includes bonds issued by NIFA that are secured by the county’s sales tax revenues. Debt service is a high 13.5% of expenditures (see exhibit), and the additional debt for the sewage plant would have put additional strain on the county’s finances.

Nassau County’s Debt Burden Is Significantly Higher than Its Peers

General Obligation Rating Net Direct Debt Burden as a

Percent of Market Value Debt Service as a Percent of

Expenditures

Nassau A2 1.5% 13.5%

Rockland Baa3 1.1% 8.6%

Orange Aaa 0.9% 4.7%

Westchester Aa1 0.8% 4.7%

Suffolk A2 0.5% 4.8%

Putnam Aa2 0.5% 4.8%

Source: Nassau County, New York, 2012 audited financial statements

The announcement is also positive for other local governments affected by Superstorm Sandy, particularly Long Beach, New York (Baa3 stable). The city was one of the most affected communities in New York, and is currently working with county officials on a plan to turn its badly damaged treatment plant into a pumping station to transfer sewage to Bay Park. As part of that effort, the city is seeking federal funding; Nassau County’s approval may indicate FEMA’s willingness to fund these projects.

Robert Weber Assistant Vice President - Analyst +1.212.553.7280 [email protected]

RECENTLY IN CREDIT OUTLOOK Select any article below to go to last Monday’s Credit Outlook on moodys.com

24 MOODY’S CREDIT OUTLOOK 16 JANUARY 2014

NEWS & ANALYSIS Corporates 2

» EP Energy's IPO Is Credit Positive for EPE Holdings » CHC IPO Proceeds Will Reduce Debt and Boost Liquidity » Forest's Aptalis Deal Adds Diversity and EBITDA » SandRidge's Gulf Sale Increases Leverage » FedEx's Debt-Funded Stock Buybacks Are Credit Negative » Norske Skogindustrier Sells Remaining Brazilian Operations,

a Credit Positive

Banks 8

» U.S. Bancorp's Chicago Acquisition Highlights a Contrarian Approach to Branches

» Withdrawal of Public-Sector Deposits Is Credit Neutral for Puerto Rico’s Banks

» Greek Banks' Funding Pressures Ease with Declining Central Bank Funding and Higher Deposits

» Raiffeisen Bank International Plans to Increase Capital, a Credit Positive

» Chinese Banks' Disclosure of Systemic Importance Indicators Is Credit Positive

» China Tightens Control of Shadow Banking, a Credit Positive » China's Local Government Debt Is Credit Negative for Its

Banks » Hong Kong's Proposed Resolution Regime Is Credit Negative

for Bank and Insurer Bondholders » Taiwan Moves to Increase Banks’ General Provisions, a Credit

Positive » Proposed Reforms for India's Priority-Sector Lending Are

Credit Positive

Insurers 29 » Fairfax's Increased Investment in BlackBerry Is Credit

Negative » American Financial Group's Proposed Acquisition of Summit

Holdings Southeast Is Credit Negative » German Life Insurers May See Lower Maximum Guaranteed

Rate on 2015 Policies, a Credit Positive » Nippon Life's Premium Discount Is Credit Negative for

Japanese Life Insurers

Securitization 36 » China's Updated Risk Retention Rule Is Credit Positive for

Securitization Investors

RATINGS & RESEARCH Rating Changes 37

Last week we upgraded Hovanian Enterprises and downgraded Sears Holdings, Bahrain Islamic Bank, and Forethought Life Insurance, among other rating actions.

Research Highlights 42

Last week we published on global oil and natural gas, US speculative-grade liquidity, our Asian Liquidity Stress Index, Singapore Power Ltd’s Austrian investments, Japan and Korea banks, Brazil, US healthcare, Dutch RMBS, global ABCP and auto loan ABS, among other reports.

MOODYS.COM

Report: 162729

© 2014 Moody’s Corporation, Moody’s Investors Service, Inc., Moody’s Analytics, Inc. and/or their licensors and affiliates (collectively, “MOODY’S”). All rights reserved.

CREDIT RATINGS ISSUED BY MOODY'S INVESTORS SERVICE, INC. (“MIS”) AND ITS AFFILIATES ARE MOODY’S CURRENT OPINIONS OF THE RELATIVE FUTURE CREDIT RISK OF ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES, AND CREDIT RATINGS AND RESEARCH PUBLICATIONS PUBLISHED BY MOODY’S (“MOODY’S PUBLICATIONS”) MAY INCLUDE MOODY’S CURRENT OPINIONS OF THE RELATIVE FUTURE CREDIT RISK OF ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES. MOODY’S DEFINES CREDIT RISK AS THE RISK THAT AN ENTITY MAY NOT MEET ITS CONTRACTUAL, FINANCIAL OBLIGATIONS AS THEY COME DUE AND ANY ESTIMATED FINANCIAL LOSS IN THE EVENT OF DEFAULT. CREDIT RATINGS DO NOT ADDRESS ANY OTHER RISK, INCLUDING BUT NOT LIMITED TO: LIQUIDITY RISK, MARKET VALUE RISK, OR PRICE VOLATILITY. CREDIT RATINGS AND MOODY’S OPINIONS INCLUDED IN MOODY’S PUBLICATIONS ARE NOT STATEMENTS OF CURRENT OR HISTORICAL FACT. MOODY’S PUBLICATIONS MAY ALSO INCLUDE QUANTITATIVE MODEL-BASED ESTIMATES OF CREDIT RISK AND RELATED OPINIONS OR COMMENTARY PUBLISHED BY MOODY’S ANALYTICS, INC. CREDIT RATINGS AND MOODY’S PUBLICATIONS DO NOT CONSTITUTE OR PROVIDE INVESTMENT OR FINANCIAL ADVICE, AND CREDIT RATINGS AND MOODY’S PUBLICATIONS ARE NOT AND DO NOT PROVIDE RECOMMENDATIONS TO PURCHASE, SELL, OR HOLD PARTICULAR SECURITIES. NEITHER CREDIT RATINGS NOR MOODY’S PUBLICATIONS COMMENT ON THE SUITABILITY OF AN INVESTMENT FOR ANY PARTICULAR INVESTOR. MOODY’S ISSUES ITS CREDIT RATINGS AND PUBLISHES MOODY’S PUBLICATIONS WITH THE EXPECTATION AND UNDERSTANDING THAT EACH INVESTOR WILL, WITH DUE CARE, MAKE ITS OWN STUDY AND EVALUATION OF EACH SECURITY THAT IS UNDER CONSIDERATION FOR PURCHASE, HOLDING, OR SALE.

MOODY’S CREDIT RATINGS AND MOODY’S PUBLICATIONS ARE NOT INTENDED FOR USE BY RETAIL INVESTORS AND IT WOULD BE RECKLESS FOR RETAIL INVESTORS TO CONSIDER MOODY’S CREDIT RATINGS OR MOODY’S PUBLICATIONS IN MAKING ANY INVESTMENT DECISION. IF IN DOUBT YOU SHOULD CONTACT YOUR FINANCIAL OR OTHER PROFESSIONAL ADVISER.

ALL INFORMATION CONTAINED HEREIN IS PROTECTED BY LAW, INCLUDING BUT NOT LIMITED TO, COPYRIGHT LAW, AND NONE OF SUCH INFORMATION MAY BE COPIED OR OTHERWISE REPRODUCED, REPACKAGED, FURTHER TRANSMITTED, TRANSFERRED, DISSEMINATED, REDISTRIBUTED OR RESOLD, OR STORED FOR SUBSEQUENT USE FOR ANY SUCH PURPOSE, IN WHOLE OR IN PART, IN ANY FORM OR MANNER OR BY ANY MEANS WHATSOEVER, BY ANY PERSON WITHOUT MOODY’S PRIOR WRITTEN CONSENT.

All information contained herein is obtained by MOODY’S from sources believed by it to be accurate and reliable. Because of the possibility of human or mechanical error as well as other factors, however, all information contained herein is provided “AS IS” without warranty of any kind. MOODY'S adopts all necessary measures so that the information it uses in assigning a credit rating is of sufficient quality and from sources MOODY'S considers to be reliable including, when appropriate, independent third-party sources. However, MOODY’S is not an auditor and cannot in every instance independently verify or validate information received in the rating process or in preparing the Moody’s Publications.

To the extent permitted by law, MOODY’S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability to any person or entity for any indirect, special, consequential, or incidental losses or damages whatsoever arising from or in connection with the information contained herein or the use of or inability to use any such information, even if MOODY’S or any of its directors, officers, employees, agents, representatives, licensors or suppliers is advised in advance of the possibility of such losses or damages, including but not limited to: (a) any loss of present or prospective profits or (b) any loss or damage arising where the relevant financial instrument is not the subject of a particular credit rating assigned by MOODY’S.

To the extent permitted by law, MOODY’S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability for any direct or compensatory losses or damages caused to any person or entity, including but not limited to by any negligence (but excluding fraud, willful misconduct or any other type of liability that, for the avoidance of doubt, by law cannot be excluded) on the part of, or any contingency within or beyond the control of, MOODY’S or any of its directors, officers, employees, agents, representatives, licensors or suppliers, arising from or in connection with the information contained herein or the use of or inability to use any such information.

NO WARRANTY, EXPRESS OR IMPLIED, AS TO THE ACCURACY, TIMELINESS, COMPLETENESS, MERCHANTABILITY OR FITNESS FOR ANY PARTICULAR PURPOSE OF ANY SUCH RATING OR OTHER OPINION OR INFORMATION IS GIVEN OR MADE BY MOODY’S IN ANY FORM OR MANNER WHATSOEVER.

MIS, a wholly-owned credit rating agency subsidiary of Moody’s Corporation (“MCO”), hereby discloses that most issuers of debt securities (including corporate and municipal bonds, debentures, notes and commercial paper) and preferred stock rated by MIS have, prior to assignment of any rating, agreed to pay to MIS for appraisal and rating services rendered by it fees ranging from $1,500 to approximately $2,500,000. MCO and MIS also maintain policies and procedures to address the independence of MIS’s ratings and rating processes. Information regarding certain affiliations that may exist between directors of MCO and rated entities, and between entities who hold ratings from MIS and have also publicly reported to the SEC an ownership interest in MCO of more than 5%, is posted annually at www.moodys.com under the heading “Shareholder Relations — Corporate Governance — Director and Shareholder Affiliation Policy.”

For Australia only: Any publication into Australia of this document is pursuant to the Australian Financial Services License of MOODY’S affiliate, Moody’s Investors Service Pty Limited ABN 61 003 399 657AFSL 336969 and/or Moody’s Analytics Australia Pty Ltd ABN 94 105 136 972 AFSL 383569 (as applicable). This document is intended to be provided only to “wholesale clients” within the meaning of section 761G of the Corporations Act 2001. By continuing to access this document from within Australia, you represent to MOODY’S that you are, or are accessing the document as a representative of, a “wholesale client” and that neither you nor the entity you represent will directly or indirectly disseminate this document or its contents to “retail clients” within the meaning of section 761G of the Corporations Act 2001. MOODY’S credit rating is an opinion as to the creditworthiness of a debt obligation of the issuer, not on the equity securities of the issuer or any form of security that is available to retail clients. It would be dangerous for “retail clients” to make any investment decision based on MOODY’S credit rating. If in doubt you should contact your financial or other professional adviser.

EDITORS PRODUCTION ASSOCIATE News & Analysis: Jay Sherman and Elisa Herr

Amanda Kissoon

![2121 21 SPARCO BÅ3 21 C] -07 BA3 2103, (K 2103, 2107 ( c BA3 BA3 2101—07 2101 2102, 2103, 21 C 7 ( 21 C I BPT (I-LAO 21 C I BPT (I-LAO 7 BA3 ruo ruo NED EurcEx M3ÅT3-2 …](https://img.pdfslide.us/doc/110x75/610a4c5a32cfb84fad3ebd8c/2121-21-sparco-b3-21-c-07-ba3-2103-k-2103-2107-c-ba3-ba3-2101a07-2101.jpg)