Embed Size (px)

Citation preview

MOODYS.COM

9 AUGUST 2012

NEWS & ANALYSIS Corporates 2 » BHP Billiton's Impairment Charge Is Credit Negative » KEPCO's Electric Tariff Hike Is Credit Negative for Korean

Manufacturers

Infrastructure 5 » Traffic Declines Are Credit Negative for European Toll Roads » China's Toll-Free Holidays Are Credit Negative for Shenzhen

International

Banks 7 » Raising Capital Requirements Is Credit Positive for Azerbaijan

Banks » Chinese Asset-Backed Issuance Disintermediates Banks, a Credit

Negative » Philippines Encourages Bank Consolidation, a Credit Positive » Aozora Bank's Repayment of Government's Preferred Shares Is

Credit Negative

US Public Finance 14 » Higher Medicare Reimbursements Are Positive for Not-for-Profit

Hospitals » Michigan's Emergency Loan Program Is Credit Positive for

Struggling Municipalities

CREDIT IN DEPTH Latin American Corporates 17

Latin American exporters would be hurt by a reduction in demand from the EU, with commodities producers the most vulnerable, and steel and pulp and paper particularly exposed. Companies would also face a knock-on effect from China, which is both a major exporter to the EU and a significant importer from Latin America. Those companies with the most revenue exposure to Europe include Fibria Celulose S.A., Magnesita Refratarios S.A. and Camposol S.A. Those with significant China exposure include Corporacion Nacional del Cobre de Chile, Corporacion Pesquera Inca S.A.C. and Asociación de Cooperativas Argentinas.

RECENTLY IN CREDIT OUTLOOK

» Articles in last Monday’s Credit Outlook 21 » Go to last Monday’s Credit Outlook

Click here for Weekly Market Outlook, our sister publication containing Moody’s Analytics’ review of market activity, financial predictions, and the dates of upcoming economic releases.

NEWS & ANALYSIS Credit implications of current events

2 MOODY’S CREDIT OUTLOOK 9 AUGUST 2012

Corporates

BHP Billiton’s Impairment Charge Is Credit Negative

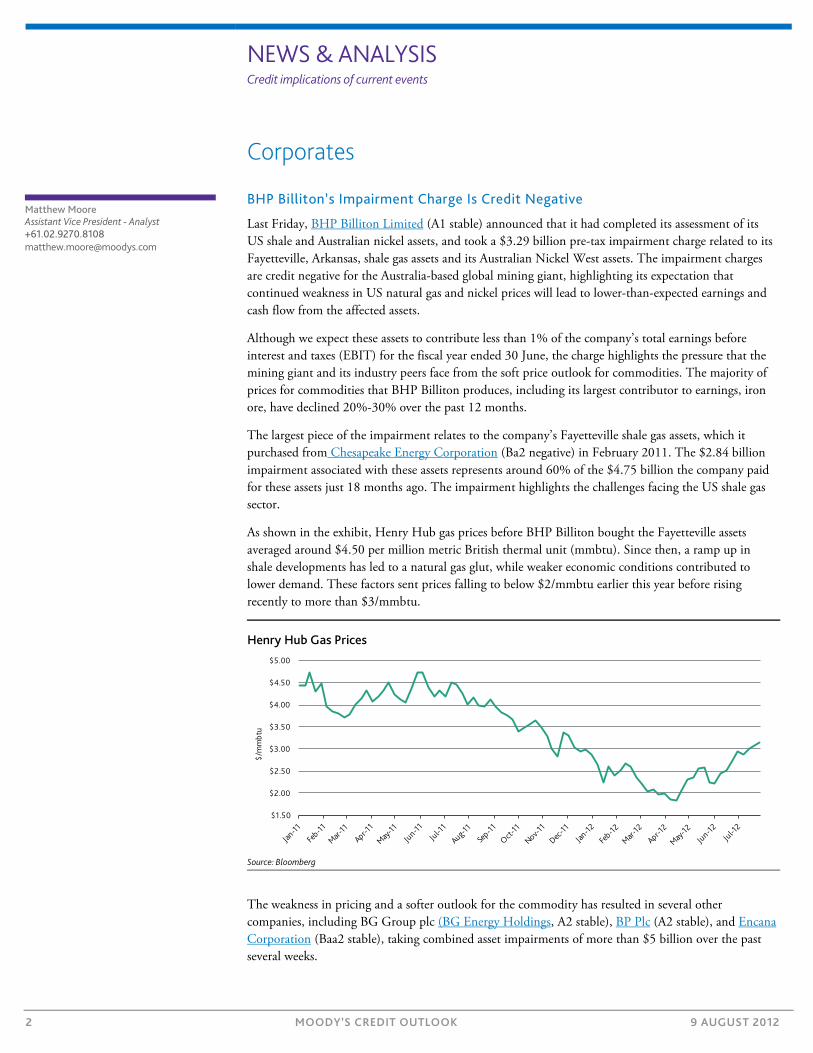

Last Friday, BHP Billiton Limited (A1 stable) announced that it had completed its assessment of its US shale and Australian nickel assets, and took a $3.29 billion pre-tax impairment charge related to its Fayetteville, Arkansas, shale gas assets and its Australian Nickel West assets. The impairment charges are credit negative for the Australia-based global mining giant, highlighting its expectation that continued weakness in US natural gas and nickel prices will lead to lower-than-expected earnings and cash flow from the affected assets.

Although we expect these assets to contribute less than 1% of the company’s total earnings before interest and taxes (EBIT) for the fiscal year ended 30 June, the charge highlights the pressure that the mining giant and its industry peers face from the soft price outlook for commodities. The majority of prices for commodities that BHP Billiton produces, including its largest contributor to earnings, iron ore, have declined 20%-30% over the past 12 months.

The largest piece of the impairment relates to the company’s Fayetteville shale gas assets, which it purchased from Chesapeake Energy Corporation

As shown in the exhibit, Henry Hub gas prices before BHP Billiton bought the Fayetteville assets averaged around $4.50 per million metric British thermal unit (mmbtu). Since then, a ramp up in shale developments has led to a natural gas glut, while weaker economic conditions contributed to lower demand. These factors sent prices falling to below $2/mmbtu earlier this year before rising recently to more than $3/mmbtu.

(Ba2 negative) in February 2011. The $2.84 billion impairment associated with these assets represents around 60% of the $4.75 billion the company paid for these assets just 18 months ago. The impairment highlights the challenges facing the US shale gas sector.

Henry Hub Gas Prices

Source: Bloomberg

The weakness in pricing and a softer outlook for the commodity has resulted in several other companies, including BG Group plc (BG Energy Holdings, A2 stable), BP Plc (A2 stable), and Encana Corporation (Baa2 stable), taking combined asset impairments of more than $5 billion over the past several weeks.

$1.50

$2.00

$2.50

$3.00

$3.50

$4.00

$4.50

$5.00

$/m

mbt

u

Matthew Moore Assistant Vice President - Analyst +61.02.9270.8108 [email protected]

NEWS & ANALYSIS Credit implications of current events

3 MOODY’S CREDIT OUTLOOK 9 AUGUST 2012

BHP Billiton’s decision to focus on developing the more liquids-rich US shale gas regions it acquired as part of its $15.1 billion purchase of Petrohawk Energy Corporation (Baa3 stable) in August 2011 also influenced its decision to write down the Fayetteville assets. As a result of this shift and strong pricing for liquids, Petrohawk assets were not affected by the company’s review.

Despite the impairment, we expect the BHP Billiton’s Petroleum division to continue to be a significant positive contributor to the company’s credit profile and a key differentiating factor when comparing the company with other major mining houses. The company’s second-largest contributor to earnings, the Petroleum division’s performance will continue to be underpinned by its significant oil and liquids production and its international gas assets.

The remaining $450 million of the impairment relates to the company’s Australian nickel assets, which have faced considerable margin pressure owing to large declines in nickel prices and continuing cost pressures in Western Australia. Nickel has been one of the worst performing metals, declining by more than 30% over the past 12 months.

NEWS & ANALYSIS Credit implications of current events

4 MOODY’S CREDIT OUTLOOK 9 AUGUST 2012

KEPCO’s Electric Tariff Hike Is Credit Negative for Korean Manufacturers

Last Monday, Korea Electric Power Corporation (KEPCO, A1 stable) electricity tariff rates for industrial users rose 6%. The increase follows a 6.1% rate hike in August 2011 and a 6.5% rate hike in December 2011. The increase is credit negative for Korea’s manufacturers.

The latest increase is significantly lower than the double-digit hike that KEPCO had originally sought.1 Nonetheless, it will still have a negative effect on the profitability of Korean manufacturers, especially heavy users such as those in the steel, chemicals and semiconductor industries. Electric arc furnace-based steel producers pay about 7% for electricity in their cost of goods.

Among our rated Korean corporates, Hyundai Steel Co.

The effect of the higher electricity costs for Hyundai Steel’s domestic rival,

(Baa3 negative) will be hardest hit by the higher costs. Based on its 2011 income statement, the new tariff will decrease operating income by 3%. But we expect the actual effect of the price hike on the company to be smaller because of its ability to pass on part of the higher tariff to customers given its dominant market position in the domestic long steel sector (i.e., sections and reinforced bars).

POSCO (A3 review for downgrade), will be less than 1% of its operating income, because of its blast furnace-centered operations, which consume less electricity than electric arc furnaces. In addition, the company has a high self-sufficiency (around 70%) of electricity, based on its energy-efficient steel-making plants.

In addition, industrial consumers are likely to face further tariff hikes in the next one to two years. KEPCO will continue to seek ways to raise tariffs for industrial users, as the company has incurred losses providing power to this segment. In the first quarter this year, KEPCO reported a net loss of KRW513 billion. Its net loss for 2011 was a massive KRW3.2 trillion.

Korean manufacturers have historically benefited from the government’s export-oriented policies, which have included low power tariffs for the sector. Compared with those in other developed countries, Korea’s electricity tariff for industrial use was only 62% of the average of 20 member countries of the Organisation for Economic Co-operation and Development in 2010. It was also 62.5% lower than that of Japan, 52% lower than the UK, and 14.5% lower than the US.

However, such benign policies could change, given the persistent tightness in the country’s power supply, the considerable deterioration in KEPCO’s financial profile, and the growing outcry from the public over the preferential tariffs given to manufacturers.

1 See Korea’s Limit on Power Tariff Increase Is Credit Negative for KEPCO, 23 July 2012.

Chris Park Vice President - Senior Credit Officer +852.3758.1366 [email protected]

NEWS & ANALYSIS Credit implications of current events

5 MOODY’S CREDIT OUTLOOK 9 AUGUST 2012

Infrastructure

Traffic Declines Are Credit Negative for European Toll Roads

Last Thursday, Italian toll road operator Atlantia S.P.A.

In the past, high inflation, which benefits the revenue line of operators through the indexation of toll rates, and cost-cutting measures have largely offset the effect of lower traffic volumes. However, maintaining profitability is likely to prove challenging for the toll road operators most affected by continued traffic declines.

(Baa1 negative) disclosed an 8% drop in traffic across its main network for the first half of 2012, the latest in a series of dramatic and credit negative traffic declines throughout the toll roads of the West European periphery. Traffic declines are credit negative for European toll road operators as they are the major determinant of revenue.

Among the companies reporting lower first-half traffic, Portugal’s Brisa Concessao Rodoviaria S.A. (Ba2 negative) saw the sharpest decline at 15.3%, followed by Spain’s Abertis Infraestructuras, S.A. (unrated) at 9.1%, and Atlantia’s Italian counterpart, SIAS - Società Iniziative Autostradali e Servizi S.p.A. (Baa2 negative) at 8.1%. French toll roads, which connect various European destinations and thereby have an element of diversity, fared better in the first half of the year. Nonetheless, compared with the prior year, traffic fell by 1.6% for Societe des Autoroutes Paris-Rhin-Rhone-APRR (Baa3 stable), 1.9% for Autoroutes du Sud de la France (ASF) (Baa1 stable) and 2.9% for SANEF S.A.

The decline in heavy-goods vehicle traffic was most severe, affected by declining production across Europe as businesses responded to the economic slowdown by scaling down their orders. As manufacturing output fell, so did heavy-goods vehicle volumes. Truck volumes remain around 10% below the levels seen before the start of the financial crisis in 2007.

(Baa1 negative).

High fuel prices have also affected car traffic volumes. Light-goods vehicle traffic dropped around 8% on Atlantia’s and SIAS’s networks in Italy, where fuel prices were an average of 20% higher than in the first half of 2011. As the recessionary developments continue and unemployment rises, we expect a further decline in disposable income, which will weigh on commuter traffic and discretionary travel.

We expect continuing economic weakness to affect traffic levels across the sector. The latest traffic data is evidence of increasing divergence in the performance of European toll road operators, with those in peripheral economies hit more severely by their government’s austerity measures, the declining wealth of road users, and not being transcontinental through-routes.

Joanna Fic Assistant Vice President - Analyst +44.20.7772.5571 [email protected]

NEWS & ANALYSIS Credit implications of current events

6 MOODY’S CREDIT OUTLOOK 9 AUGUST 2012

China’s Toll-Free Holidays Are Credit Negative for Shenzhen International Last Thursday, China’s State Council announced its approval of a Ministry of Transport policy proposal to waive toll fees for passenger cars with seven or fewer seats during four important national holidays, making road travel toll-free approximately 20 days every year. The holidays include the Spring Festival, Tomb Sweeping Festival, Labour Day and National Day as well as their subsequent days. All toll roads in China will be affected with the exception of airport expressways, over which local authorities have discretion. The policy is credit negative for Shenzhen International Holdings Limited (Baa3 stable).

Shenzhen International invests in and operates 17 toll roads in China. We estimate that its toll income will decline approximately 3%-5%, or about HKD170 million per year. This, coupled with a less favorable economic environment this year, will significantly slow the company’s year-on-year growth in toll road revenues to low-single digits from 11.6% in 2011.

The toll-free policy will induce more traffic than usual on Shenzhen International’s highways, which are heavily used by local commuters between the Shenzhen municipality and neighboring regions including Hong Kong. Management will have challenges monitoring and controlling traffic volume and will incur higher operating costs during affected holidays. As a result, we expect a modest drop in profit margins for the company’s toll roads.

The announced policy further indicates that the concession and regulatory framework for toll-road operators is less transparent in China than in developed countries for setting tariffs and protecting against events outside of the control of the concessionaire.

In the past decade, there has been no tariff increase for Shenzhen International because toll road operators are already more profitable than other industry sectors in China. The central government authorities, including the State Council and Ministry of Transport, have been studying policy changes including a gradual reduction of toll fees for toll roads, as in this case. In our view, adverse policy changes will be gradually implemented, but their scope will be limited and the negative effect is likely to be mitigated by long-term traffic growth.

Jiming Zou Analyst +852.3758.1343 [email protected]

Nan Nan Associate Analyst +852.3758.1459 [email protected]

NEWS & ANALYSIS Credit implications of current events

7 MOODY’S CREDIT OUTLOOK 9 AUGUST 2012

Banks

Raising Capital Requirements Is Credit Positive for Azerbaijan Banks

Last Friday, the Central Bank of Azerbaijan (CBA) announced that it will raise the minimum capital thresholds for banks operating in Azerbaijan to AZN50 million ($63.7 million) as of 1 January 2014 from the current AZN10 million ($12.7 million). The measure, which will affect existing and new banks, is credit positive for the Azerbaijan banking sector because it will foster consolidation, leading to increased competition for larger banks.

We do not expect the new measure to significantly boost the banking system’s capitalization because we believe very few smaller banks will be able to secure capital injections from their shareholders, and most banks will opt for consolidation or liquidation instead. Because these smaller banks are generally weak institutions, their consolidation or liquidation will improve the stability of the banking system.

Based on year-end 2011 capital levels, only 11 of the system’s 43 banks had sufficient capital to meet the new requirements (see exhibit). Those 11 banks are only 25% of all banks operating in Azerbaijan, but they hold more than 70% of total banking assets.

Azerbaijan Banks Capital Distribution at Year-End 2011

Source: Central Bank of Azerbaijan

Among the other 32 banks, which had less than AZN50 million of capital, we estimate that only 13 medium size banks (21% of banking system assets) will be able to meet the new capital requirements via internal capital generation and capital injections from their shareholders or by consolidating. As a result, the new requirements will likely encourage most of those banks to consolidate, creating stronger financial institutions that will be in a better position to compete with large banks.

The remaining 19 small banks, which comprised only 6% of total system’s assets at year-end 2011, will find it difficult to raise additional capital via consolidation or external capital contribution. As a result, we expect them to be liquidated if they are not acquired by larger banks. Liquidation of small banks would result in a more stable banking system since they are generally non-transparent financial

11

4

9

19

73% 9% 12%6% 0%

10%

20%

30%

40%

50%

60%

70%

80%

0

2

4

6

8

10

12

14

16

18

20

>=AZN 50 million >=AZN 40 -<50 million >=AZN20 -<40 million <AZN 20 million

Number of Banks -left axis Percent Total Banking Assets - right axis

Capital

Will likely be liquidated

Will likely consolidate

Meet new requirements

Lev Dorf Analyst +7.495.228.6056 [email protected]

Yaroslav Sovgyra Associate Managing Director +7.495.228.6076 [email protected]

NEWS & ANALYSIS Credit implications of current events

8 MOODY’S CREDIT OUTLOOK 9 AUGUST 2012

institutions with weak financial fundamentals, high risk-taking, high shares of related-party lending and limited franchises.

With a weighted average Tier 1 capital ratio of 13% at year-end 2011,2 most banks in Azerbaijan have sufficient capital to absorb losses expected under our central scenario and we do not expect any material changes in capitalisation levels as a result of consolidation.

2 Please see Azerbaijan: Banking System Outlook, 31 July 2012

NEWS & ANALYSIS Credit implications of current events

9 MOODY’S CREDIT OUTLOOK 9 AUGUST 2012

Chinese Asset-Backed Issuance Disintermediates Banks, a Credit Negative

On Tuesday, three Chinese local government infrastructure firms became the first batch of companies to issue asset-backed notes (ABNs) in China following the National Association of Financial Market Institutional Investors releasing new guidance on 3 August that allows non-financial institutions to issue ABNs. The three firms, Shanghai Pudong Road & Bridge Construction Co. (unrated), Ningbo Urban Construction Investment Holding Co., Ltd. (unrated), and Nanjing Public Holdings (Group) Co. (unrated), will offer up to RMB2.5 billion in ABN with maturities from one to five years in private placements, with 4.88%-5.85% interest rates that are lower than benchmark loan rates. This is a credit negative development for Chinese banks that illustrates, and adds to, a trend toward financial disintermediation in China.

More companies in China are seeking direct funding from capital markets. According to the second-quarter Monetary Policy Execution Report published on 2 August by the People’s Bank of China, corporate bond issuance in the first half of 2012 had strong year-over-year growth of 37%, and about 10.6% of total financing came from the corporate bond market, up 2.1 percentage points from the same period in 2011.

Whereas large, strong corporations are responsible for the robust growth in corporate bond issuance so far, we believe the ABN market opening will provide an additional funding channel for corporations with lower credit ratings but with assets that have strong cash flows. All this indicates that banks will see their strongest traditional customers increasingly turn to non-bank channels to meet their funding needs, potentially reducing banks’ loan volume and yields in this credit category. This raises the risk that banks will be forced to adjust their loan portfolios and enter new areas such as small and medium size enterprise lending or emerging industries. Because Chinese banks are less familiar with these sectors, risk management and pricing will be challenging.

The newly open ABN market raises the risk of structural subordination for existing bank loans, given that cash flows originated from the underlying assets will be restricted to service only the ABN. This will decrease cash flow available to service existing bank loans. And because assets being used to back ABNs are generally those with more stable cash flows and better quality, in the case of default, banks could be subordinated or have no claim rights on the securitized assets, leaving them with recourse only to assets of lower quality. In addition, because ABN issuers will not divert their entire issuance proceeds to pay down existing bank loans, their overall leverage will likely increase, creating a weakening borrower profile for banks.

Given ABN guidance largely targets the corporate sector, we expect its effects will be more pronounced among banks with a higher focus on corporate lending, namely China Development Bank (Aa3 positive), Bank of Communication (A3 stable; D+/ba1 stable),3 China CITIC Bank (Baa2 stable; D/ba2 stable), and Shanghai Pudong Development Bank (Baa3 stable; D/ba2 stable). The ABN guidance states that underlying assets can be assets with predictable cash flows, property rights, or a mix of both. We believe assets in transportation and logistics, power generation and supply and public utilities, and infrastructure projects are most likely to back ABN issuance owing to their relatively predictable cash flows, at least in the beginning phase of this market development.

3 The bank ratings shown in this report are the bank’s deposit rating, its standalone bank financial strength rating/baseline

credit assessment and the corresponding rating outlooks.

Katie Chen Associate Analyst +86.10.6319.6569 [email protected]

NEWS & ANALYSIS Credit implications of current events

10 MOODY’S CREDIT OUTLOOK 9 AUGUST 2012

Although the issuer’s liquidity and funding options improve with ABN issuance, which could, in turn, strengthen their capacity to service their bank loans, and banks can gain fee income by providing underwriting services for these securities, an overall increase in corporate leverage and structural subordination for existing bank loans outweigh these positive factors.

NEWS & ANALYSIS Credit implications of current events

11 MOODY’S CREDIT OUTLOOK 9 AUGUST 2012

Philippines Encourages Bank Consolidation, a Credit Positive

Last Thursday, the central bank of the Philippines, Bangko Sentral ng Pilipinas (BSP), and the Philippine Deposit Insurance Corporation (PDIC) took new steps to encourage consolidation among rural banks. The new steps add several enhancements to a program launched in August 2010 to encourage bank mergers and acquisitions and are credit positive for Philippine banks.

Compared with the original program, Strengthening Program for Rural Banks (SPRB), the enhanced program, “SPRB Plus,” now allows the following:

» Universal and commercial banks, thrift banks, rural banks and non-bank corporations can participate as eligible investors and benefit from the program incentives. (The original program only allowed rural banks to acquire other rural banks.)

» Eligible investors can collect licensing fee waivers for additional branches they open.4

SPRB Plus, which will run from 2 August until 31 December 2013, and can be extended by the regulators, allows larger universal and commercial banks to add to their branch networks in certain coveted Metro Manila areas, where these banks are currently restricted from opening new branches until July 2014. Among our rated banks, those restricted from opening branches in Metro Manila are shown in the exhibit below. In addition, this program also provides an opportunity for larger banks to diversify their operations in the rural market in a cost-effective manner.

Our Rated Philippines Banks

Name Long-Term Bank Foreign Currency Deposit Rating Standalone Credit Strength

Allied Banking Corporation Ba3 positive E+/b1 positive

BDO UNIBANK, INC. * Ba2 positive D/ba2 stable

Bank of the Philippine Islands * Ba2 positive D/ba2 stable

Land Bank of the Philippines Ba2 positive D-/ba3 stable

Metropolitan Bank and Trust Company * Ba2 positive D/ba2 stable

Philippine National Bank Ba2 stable E+/b1 positive

Rizal Commercial Banking Corporation Ba2 stable D-/ba3 stable

United Coconut Planters Bank B2 stable E/caa1 stable

* Currently restricted until July 2014 from opening new branches in certain areas of Metro Manila Source: Moody's ratings as of 8 August 2012

Under the enhanced program, BSP will grant branch licenses in these restricted areas to universal, commercial or thrift banks that make an acquisition, provided that they satisfy BSP’s pre-condition of having strong financial fundamentals and sound banking practices. The granting of a license depends on the acquirer bringing the acquired banks’ risk-based capital adequacy ratio to 10%. An additional branch license will be granted to banks for every three rural banks they acquire. Without these incentives, branch licensing fees for universal and commercial banks amount to PHP20 million per branch.

4 See details here.

Simon Chen, CFA Analyst +65.6398.8305 [email protected]

NEWS & ANALYSIS Credit implications of current events

12 MOODY’S CREDIT OUTLOOK 9 AUGUST 2012

We believe that the enhanced program, which expands the investor pool from only rural banks previously to now also include universal and commercial and thrift banks, will increase the pace of consolidation in an overcrowded Philippine banking system.5

Specifically, we expect the enhancement to lead to more universal and commercial banks acquiring financially weaker rural banks, which we see as a necessary step for the industry to strengthen its overall financial health, efficiency, and corporate governance. Rural banks in general have poorer credit fundamentals than the banking system average, particularly in asset quality and liquidity.6

5 At the end of March 2012, a total of 723 banks operated in the Philippines. Of that total, 574 were rural banks that

constituted an estimated 2% of banking system assets, 38 universal/commercial banks representing 89%, 71 thrift banks representing 8%, and 40 cooperative banks representing 1%.

6 As of third-quarter 2011, rural banks’ NPL ratio was 10.4%, compared with 3.3% for the overall banking system, while their NPL coverage ratio was 60% versus the system’s 135%, and their loan-to-deposit ratio was 98% versus 62% for the system.

NEWS & ANALYSIS Credit implications of current events

13 MOODY’S CREDIT OUTLOOK 9 AUGUST 2012

Aozora Bank’s Repayment of Japanese Government’s Preferred Shares Is Credit Negative

Last Thursday, Aozora Bank, Ltd. (Baa2 stable; D+/ba1 stable)7 announced that it is near an agreement with major stakeholders on a comprehensive plan to fully repay “over time” approximately ¥180 billion to the government of Japan (Aa3 stable), which supported the bank by purchasing preferred shares in October 2000. Full repayment is credit negative for Aozora because without the government’s preferred shares, the bank’s Tier 1 capital ratio will decline to approximately 13% from 19.37% at the end of March.

The approach of the 3 October mandatory conversion date for the bulk of the government’s outstanding preferred shares to common shares prompted the announcement. Converting the preferred shares to common shares would dilute the bank’s other shareholders and give the government voting rights, limiting management’s flexibility. Aozora currently does not have sufficient retained earnings to repay the government in full and any plan that facilitates full repayment necessitates a change in its capital structure, which needs shareholder approval. Given the single largest shareholder owned 54.8% of the voting rights at the end of March, once a repayment and capital plan that’s acceptable to the regulators and the major shareholder is reached, a challenge by minority shareholders will be difficult. Details of the proposed capital plan are not yet available, but any plan that causes capital to decline by the full amount of the government’s preferred shares is credit negative.

Aozora’s high Tier 1 capital ratio and high quality of capital are credit strengths. Given its limited domestic franchise and higher funding costs relative to its peers, the bank has a higher risk appetite than its peers. However, we regard capital as sufficient to support a business model of relatively higher risk and higher return. Recently, the bank has taken fewer risks and refocused on domestic lending. In addition, liquidity has improved and funding costs have fallen to 0.58% in fiscal 2011, ended 31 March 2011, from 1.18% in fiscal 2008. Despite strategic changes, the bank continues to face challenges in building a core franchise that will deliver stable returns, and it still shows a relatively higher risk appetite than its peers.

Following the full repayment of the government’s preferred shares, the regulator will have less sway over the strategic direction of the bank, making it more difficult for management to resist shareholder pressure to increase returns, an additional credit negative.

7 The ratings shown are Aozora Bank’s deposit rating, its standalone bank financial strength rating/baseline credit assessment

and the corresponding rating outlooks.

Kyosuke Kaji Assistant Vice President - Analyst +81.3.5408.4031 [email protected]

Graeme Knowd Associate Managing Director +81.3.5408.4149 [email protected]

NEWS & ANALYSIS Credit implications of current events

14 MOODY’S CREDIT OUTLOOK 9 AUGUST 2012

Public Finance

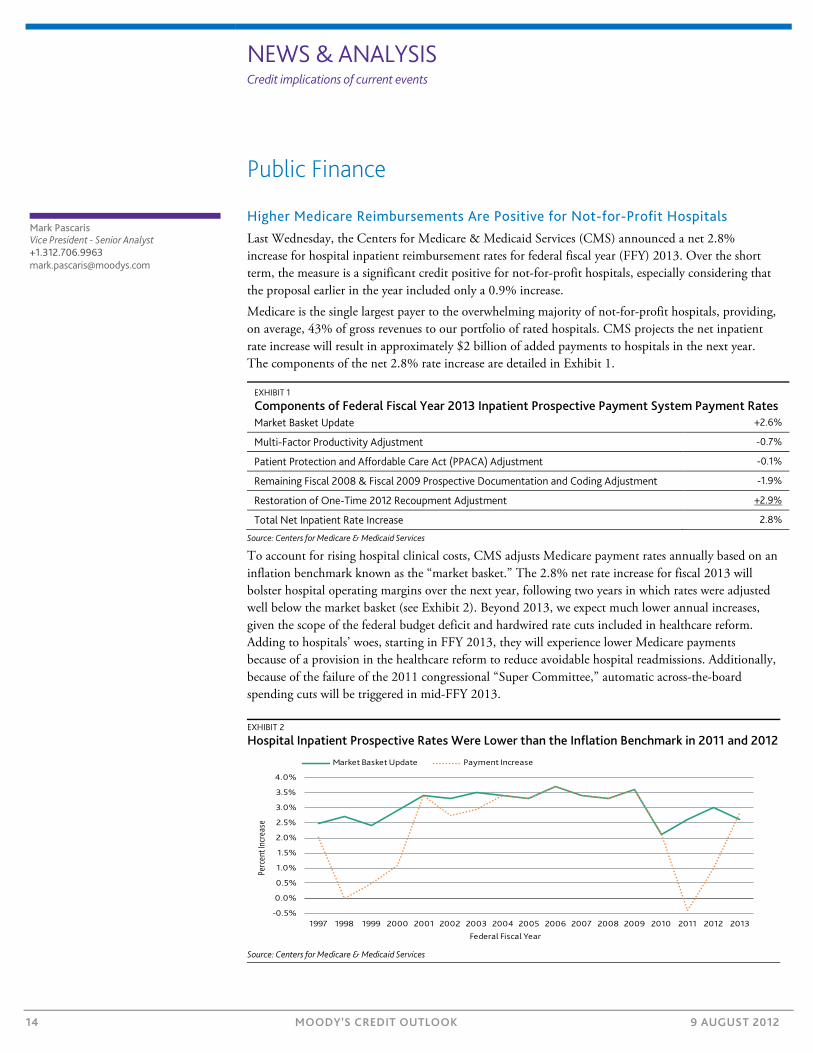

Higher Medicare Reimbursements Are Positive for Not-for-Profit Hospitals Last Wednesday, the Centers for Medicare & Medicaid Services (CMS) announced a net 2.8% increase for hospital inpatient reimbursement rates for federal fiscal year (FFY) 2013. Over the short term, the measure is a significant credit positive for not-for-profit hospitals, especially considering that the proposal earlier in the year included only a 0.9% increase.

Medicare is the single largest payer to the overwhelming majority of not-for-profit hospitals, providing, on average, 43% of gross revenues to our portfolio of rated hospitals. CMS projects the net inpatient rate increase will result in approximately $2 billion of added payments to hospitals in the next year. The components of the net 2.8% rate increase are detailed in Exhibit 1.

EXHIBIT 1

Components of Federal Fiscal Year 2013 Inpatient Prospective Payment System Payment Rates Market Basket Update +2.6%

Multi-Factor Productivity Adjustment -0.7%

Patient Protection and Affordable Care Act (PPACA) Adjustment -0.1%

Remaining Fiscal 2008 & Fiscal 2009 Prospective Documentation and Coding Adjustment -1.9%

Restoration of One-Time 2012 Recoupment Adjustment +2.9%

Total Net Inpatient Rate Increase 2.8%

Source: Centers for Medicare & Medicaid Services

To account for rising hospital clinical costs, CMS adjusts Medicare payment rates annually based on an inflation benchmark known as the “market basket.” The 2.8% net rate increase for fiscal 2013 will bolster hospital operating margins over the next year, following two years in which rates were adjusted well below the market basket (see Exhibit 2). Beyond 2013, we expect much lower annual increases, given the scope of the federal budget deficit and hardwired rate cuts included in healthcare reform. Adding to hospitals’ woes, starting in FFY 2013, they will experience lower Medicare payments because of a provision in the healthcare reform to reduce avoidable hospital readmissions. Additionally, because of the failure of the 2011 congressional “Super Committee,” automatic across-the-board spending cuts will be triggered in mid-FFY 2013.

EXHIBIT 2

Hospital Inpatient Prospective Rates Were Lower than the Inflation Benchmark in 2011 and 2012

Source: Centers for Medicare & Medicaid Services

-0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Perc

ent I

ncre

ase

Federal Fiscal Year

Market Basket Update Payment Increase

Mark Pascaris Vice President - Senior Analyst +1.312.706.9963 [email protected]

NEWS & ANALYSIS Credit implications of current events

15 MOODY’S CREDIT OUTLOOK 9 AUGUST 2012

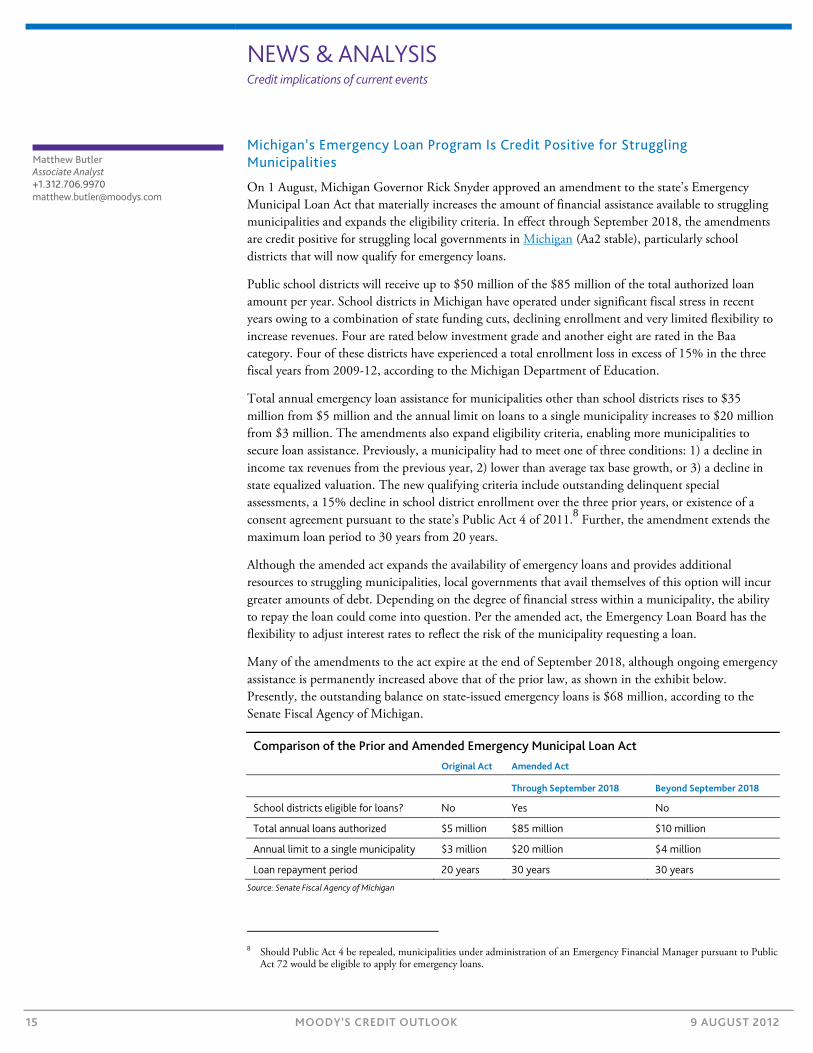

Michigan’s Emergency Loan Program Is Credit Positive for Struggling Municipalities

On 1 August, Michigan Governor Rick Snyder approved an amendment to the state’s Emergency Municipal Loan Act that materially increases the amount of financial assistance available to struggling municipalities and expands the eligibility criteria. In effect through September 2018, the amendments are credit positive for struggling local governments in Michigan (Aa2 stable), particularly school districts that will now qualify for emergency loans.

Public school districts will receive up to $50 million of the $85 million of the total authorized loan amount per year. School districts in Michigan have operated under significant fiscal stress in recent years owing to a combination of state funding cuts, declining enrollment and very limited flexibility to increase revenues. Four are rated below investment grade and another eight are rated in the Baa category. Four of these districts have experienced a total enrollment loss in excess of 15% in the three fiscal years from 2009-12, according to the Michigan Department of Education.

Total annual emergency loan assistance for municipalities other than school districts rises to $35 million from $5 million and the annual limit on loans to a single municipality increases to $20 million from $3 million. The amendments also expand eligibility criteria, enabling more municipalities to secure loan assistance. Previously, a municipality had to meet one of three conditions: 1) a decline in income tax revenues from the previous year, 2) lower than average tax base growth, or 3) a decline in state equalized valuation. The new qualifying criteria include outstanding delinquent special assessments, a 15% decline in school district enrollment over the three prior years, or existence of a consent agreement pursuant to the state’s Public Act 4 of 2011.8 Further, the amendment extends the maximum loan period to 30 years from 20 years.

Although the amended act expands the availability of emergency loans and provides additional resources to struggling municipalities, local governments that avail themselves of this option will incur greater amounts of debt. Depending on the degree of financial stress within a municipality, the ability to repay the loan could come into question. Per the amended act, the Emergency Loan Board has the flexibility to adjust interest rates to reflect the risk of the municipality requesting a loan.

Many of the amendments to the act expire at the end of September 2018, although ongoing emergency assistance is permanently increased above that of the prior law, as shown in the exhibit below. Presently, the outstanding balance on state-issued emergency loans is $68 million, according to the Senate Fiscal Agency of Michigan.

Comparison of the Prior and Amended Emergency Municipal Loan Act

Original Act Amended Act

Through September 2018 Beyond September 2018

School districts eligible for loans? No Yes No

Total annual loans authorized $5 million $85 million $10 million

Annual limit to a single municipality $3 million $20 million $4 million

Loan repayment period 20 years 30 years 30 years

Source: Senate Fiscal Agency of Michigan

8 Should Public Act 4 be repealed, municipalities under administration of an Emergency Financial Manager pursuant to Public

Act 72 would be eligible to apply for emergency loans.

Matthew Butler Associate Analyst +1.312.706.9970 [email protected]

CREDIT IN DEPTH Detailed analysis of an important topic

16 MOODY’S CREDIT OUTLOOK 9 AUGUST 2012

EU Recession Presents Risk for Latin America Commodities Producers – Potential for Knock-On Effect in China

» A recession in the EU would hurt Latin American exporters. Deepening concern about the health of European Union economies has implications for Latin America, which is a significant exporter to the region. Latin American exporters would be hurt by a reduction in demand from the EU and also face a knock-on effect in China. Recession in the EU would exacerbate the slowdown in China, which is both a major exporter to the EU and a significant importer from Latin America.

» Commodities producers would be most vulnerable. Latin American commodities exporters would be more vulnerable to weakness in the EU than producers of finished goods. Industries including steel and pulp and paper would be particularly exposed. Commodities exporters would be hurt the most because they are vulnerable to short-term price declines arising from reduced demand. Over the long term, however, Latin American commodities producers remain well positioned to benefit from their exposure to China, which remains a dynamic and fast-growing economy despite the recent slowdown.

» The greatest risk comes from direct exposure to Europe. Companies at greatest risk are those that generate significant export revenue in Europe and have less opportunity to offset this weakness by diverting exports to China, which will remain a significant importer despite its recent slowdown in growth. Companies that trade within the Americas are less exposed, although they would be affected to the extent that recession in the EU led to a general weakening of Latin American economies.

» Companies that are most exposed. Latin American companies with the most revenue exposure to Europe include Fibria Celulose S.A. (Ba1 stable), Magnesita Refratarios S.A. (B1 stable) and Camposol S.A. (B3 stable). Those with significant China exposure include Corporacion Nacional del Cobre de Chile (A1 stable) , Corporacion Pesquera Inca S.A.C. (B2 positive) and Asociación de Cooperativas Argentinas (B2 stable).

Latin American companies vulnerable to EU recession

The export-driven economies of Latin America are highly sensitive to macroeconomic shifts among their major trading partners, all of which are grappling with economic turbulence. The US, by far the largest destination for Latin American goods, continues in a slow-growth mode, European Union economies are weakening, and China is seeing a slowdown. Right now the deepest concerns center on Europe.

A recession in the European Union would be credit negative for many Latin American exporters of commodities like iron ore and soybeans, which have enjoyed strong growth in global demand in recent years. But not all companies in Latin America would be affected equally. The degree of exposure for each company depends on what it produces and where it sells its products.

Commodity producers would be more vulnerable than companies that manufacture finished goods because they are more vulnerable to price swings. Those that export more to the EU than to comparatively stronger China would also be more vulnerable. Companies that are entirely focused on the Latin American market or that limit most of their trade to the Americas would be less vulnerable.

There is considerable uncertainty about the depth and duration of a recession in Europe. The optimism that followed the June 17 Greek election, which handed power to political parties that support the EU bailout and austerity measures, did little to alleviate the pressures on EU sovereigns and banks and it did not remove the potential for a significant shock to the global financial system arising from the debt crisis.

Marianna Waltz, CFA Vice President - Senior Analyst +55.11. 3043.7309 [email protected]

Barbara Mattos Assistant Vice President – Analyst +55.11.3043.7357 [email protected]

CREDIT IN DEPTH Detailed analysis of an important topic

17 MOODY’S CREDIT OUTLOOK 9 AUGUST 2012

We currently expect a mild recession in the euro area economy in 2012. The baseline forecast from Moody’s Macroeconomic Board calls for euro area GDP to be flat to down 1% this year and to grow 0.5%-1.5% in 2013. That would represent a slowdown from GDP growth of 1.5% in 2011 and 2% in 2010, which followed a 4.4% contraction in 2009, according to Eurostat. There is downside risk to the Moody’s forecast, however, to the extent that the turbulence weakens European consumer and business confidence, which would cut further into consumption and business investment. In addition, austerity measures and deleveraging in the banking sector will continue to constrain growth.

EU’s place as Latin America’s second-largest export market on the wane

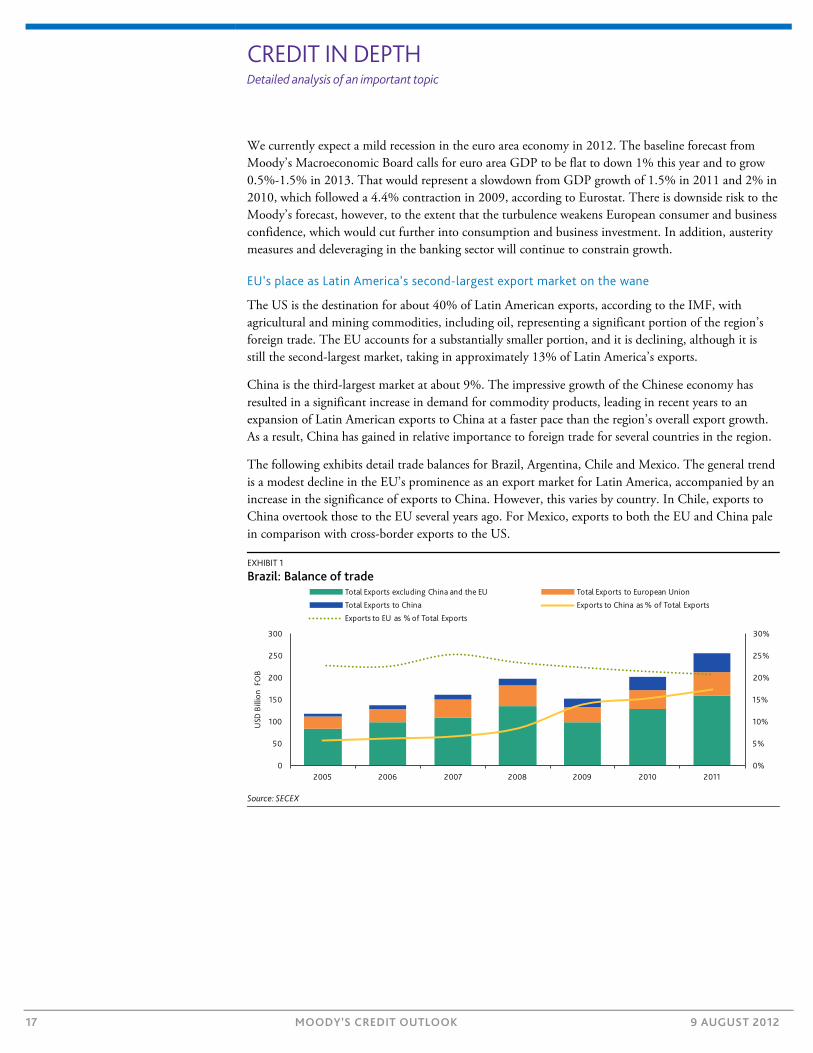

The US is the destination for about 40% of Latin American exports, according to the IMF, with agricultural and mining commodities, including oil, representing a significant portion of the region’s foreign trade. The EU accounts for a substantially smaller portion, and it is declining, although it is still the second-largest market, taking in approximately 13% of Latin America’s exports.

China is the third-largest market at about 9%. The impressive growth of the Chinese economy has resulted in a significant increase in demand for commodity products, leading in recent years to an expansion of Latin American exports to China at a faster pace than the region’s overall export growth. As a result, China has gained in relative importance to foreign trade for several countries in the region.

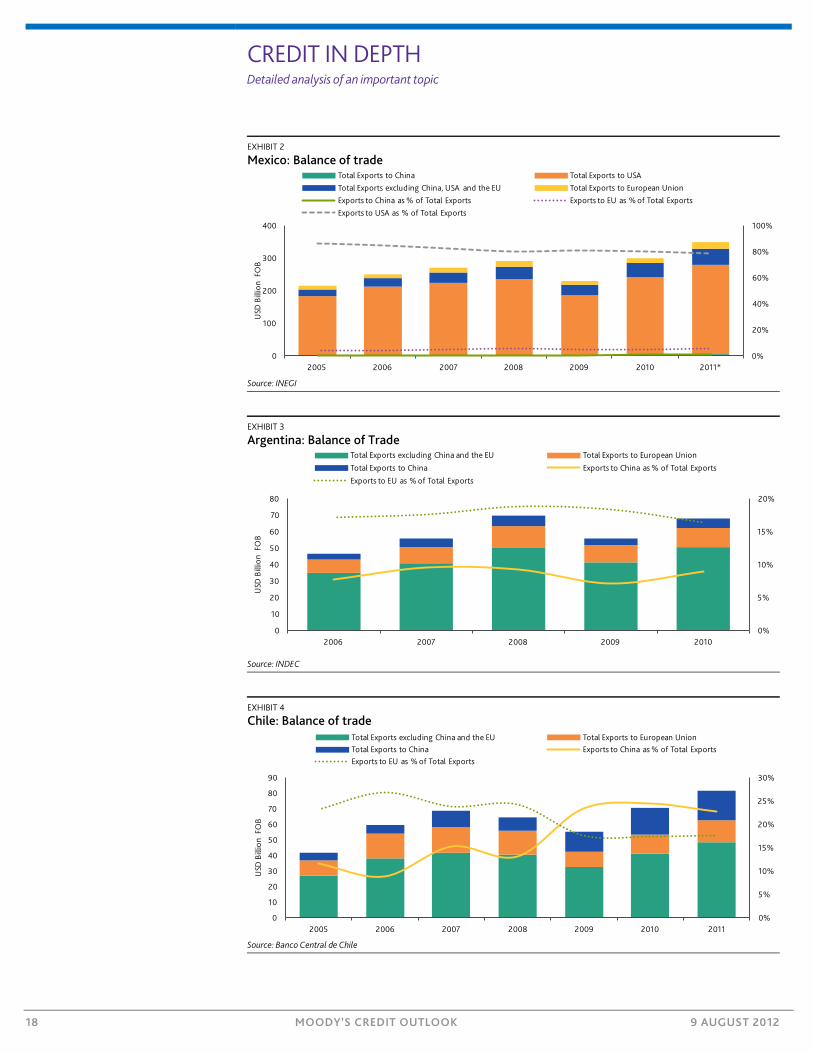

The following exhibits detail trade balances for Brazil, Argentina, Chile and Mexico. The general trend is a modest decline in the EU’s prominence as an export market for Latin America, accompanied by an increase in the significance of exports to China. However, this varies by country. In Chile, exports to China overtook those to the EU several years ago. For Mexico, exports to both the EU and China pale in comparison with cross-border exports to the US.

EXHIBIT 1

Brazil: Balance of trade

Source: SECEX

0%

5%

10%

15%

20%

25%

30%

0

50

100

150

200

250

300

2005 2006 2007 2008 2009 2010 2011

USD

Bill

ion

FO

B

Total Exports excluding China and the EU Total Exports to European Union

Total Exports to China Exports to China as % of Total Exports

Exports to EU as % of Total Exports

CREDIT IN DEPTH Detailed analysis of an important topic

18 MOODY’S CREDIT OUTLOOK 9 AUGUST 2012

EXHIBIT 2

Mexico: Balance of trade

Source: INEGI

EXHIBIT 3

Argentina: Balance of Trade

Source: INDEC

EXHIBIT 4

Chile: Balance of trade

Source: Banco Central de Chile

0%

20%

40%

60%

80%

100%

0

100

200

300

400

2005 2006 2007 2008 2009 2010 2011*

USD

Bill

ion

FO

B

Total Exports to China Total Exports to USATotal Exports excluding China, USA and the EU Total Exports to European UnionExports to China as % of Total Exports Exports to EU as % of Total ExportsExports to USA as % of Total Exports

0%

5%

10%

15%

20%

0

10

20

30

40

50

60

70

80

2006 2007 2008 2009 2010

USD

Bill

ion

FO

B

Total Exports excluding China and the EU Total Exports to European Union

Total Exports to China Exports to China as % of Total Exports

Exports to EU as % of Total Exports

0%

5%

10%

15%

20%

25%

30%

0

10

20

30

40

50

60

70

80

90

2005 2006 2007 2008 2009 2010 2011

USD

Bill

ion

FO

B

Total Exports excluding China and the EU Total Exports to European UnionTotal Exports to China Exports to China as % of Total ExportsExports to EU as % of Total Exports

CREDIT IN DEPTH Detailed analysis of an important topic

19 MOODY’S CREDIT OUTLOOK 9 AUGUST 2012

EXHIBIT 5

Brazil, Argentina, Chile and Mexico: Balance of trade

Source: INEGI, Banco Central de Chile, INDEC and SECEX.

EU slowdown could affect China as well

A recession in the EU would further weaken its demand for Latin American exports. But some impact of weakening in the EU could come through a knock-on effect in China. China was the largest exporter to the EU in 2011, accounting for about 17% of EU imports, according to Eurostat. Consequently, a slowdown in Europe stands to reduce the region’s demand for Chinese goods; in turn, that would reduce Chinese demand for Latin American commodities.

Right now, we forecast a soft landing for China. Moody’s baseline scenario is 7.5%-8.5% GDP growth in both 2012 and 2013, down from 9.2% in 2011. At such growth rates, the Chinese economy will remain dynamic and will still be among the world’s fastest-growing economies. As such, even as it slows it will continue to provide an important buffer for Latin American exporters exposed to weakness in Europe. Latin American producers of globally traded commodities such as copper, market pulp and iron ore still should be able to redirect exports to China, as well as other growing economies such as India and Russia.

Commodities exporters with large EU exposure are most vulnerable

A slowdown in Europe and China would not affect all Latin American companies equally. Commodities exporters would be more exposed in the near term than exporters of manufactured goods. Commodities exporters are more vulnerable to short-term price declines that result from reduced commodities demand. A one-two punch of reduced sales volumes and lower prices could hurt commodity exporters’ cash flows and potentially lead to higher leverage or weaker liquidity.

Some offsetting factors for commodities exporters is the fact that some Latin American producers are intrinsically low cost producers compared to peers in their segments, such as iron ore and steel, as well as pulp and paper. Such competitive advantage should shield them from the downturn to some degree, as higher cost competitors may be forced to shut down their capacity in the event of a more prolonged downturn. Secondly, weaker local currencies would typically stimulates exports as they become more competitive in international markets and would, to a certain extent counterbalance potential pressures coming from weakening demand over exporters. Lastly, commodities exporters have the ability to divert their products to other markets, whereas this is more difficult for makers of manufactured goods that are more subject to differences in tastes and needs from one market to the next.

0%

2%

4%

6%

8%

10%

12%

14%

16%

0

100

200

300

400

500

600

700

2006 2007 2008 2009 2010

USD

Bill

ion

FO

B

Total Exports excluding China and the EU Total Exports to European Union

Total Exports to China Exports to China as % of Total Exports

Exports to EU as % of Total Exports

CREDIT IN DEPTH Detailed analysis of an important topic

20 MOODY’S CREDIT OUTLOOK 9 AUGUST 2012

After any short-term price volatility, we would expect Latin America’s commodities producers to still be well placed to benefit from China’s longer-term growth prospects. China is likely to rebound from any EU-induced economic slowdown well before the EU puts its debt and banking problems behind it. Therefore, Latin American commodities producers with more exposure to China than Europe are likely to better weather the fallout from an EU recession and its broader crisis.

The least exposed Latin American companies are either domestically focused or conduct most of their trade within the Americas. With no trade links to Europe and China, companies such as restaurant operator Arcos Dorados Holdings Inc. (Ba2 stable), Brazilian homebuilders such as PDG Realty S.A. Empreend. e Participacoes (Ba2 stable), Cyrela Brazil Realty S.A. (Ba2 stable) and Even Construtora e Incorporadora S.A., among other homebuilders, retailer Cencosud S.A. (Baa3 stable) as well as Latin American telecoms, such as NET Serviços de Comunicação S.A. (Baa3 positive) and America Móvil S.A.B. de C.V. (A2, stable)will not face a direct impact on demand. However, to the extent that lower demand for Latin American goods from China and Europe leads to a weakening of Latin American economies, the domestically focused companies could see some fallout in terms of reduced demand from Latin American consumers.

Developments in Europe and potential deceleration in China are likely to be key factors affecting future ratings trends in the region. We have seen a negative ratings drift in Latin America in recent quarters, with downgrades exceeding upgrades.9 This is affecting cyclical sectors in particular, including commodities exporters in areas like pulp and paper and steel. The balance between positive and negative rating outlooks and rating reviews in Latin America has turned decidedly negative, suggesting a continuation of the negative rating trend. There were 16 ratings in Latin America with a negative outlook or under review for downgrade as of May 31, compared with six ratings with a positive outlook or under review for an upgrade. The last time this ratio skewed positive was the first quarter of 2011.

Please click here to read name-by-name analyses of 90 Latin American companies’ exposure to the European Union and China. The full report includes a six page table detailing the companies’ industry, primary location in Latin America, and percent of sales to the EU and China.

9 See Credit Trends in Brazil, 8 June 2012, Credit Trends in Mexico, 11 June 2012 and Credit Trends in Argentina, 11

June 2012.

RECENTLY IN CREDIT OUTLOOK Select any article below to go to last Monday’s Credit Outlook on moodys.com

21 MOODY’S CREDIT OUTLOOK 9 AUGUST 2012

NEWS & ANALYSIS Corporates 2 » Court Ruling Is Credit Positive for Hewlett-Packard, Negative for Oracle » Devon’s Joint Venture with Sumitomo Is Credit Positive » Valero’s Retail Separation Plan Increases Financial Risk, a Credit Negative » Allegiant Travel’s Addition of Airbus Aircraft Is Credit Positive » New Congo Mining License Is Credit Positive for ENRC » China’s Five-Year Natural Gas Plan Would Help Gas Distributors » Macau’s Casinos Bet on Full House, Despite Shrinking Revenues » Crown’s Casino Expansion Plans in Australia Are Credit Negative

Infrastructure 11 » Intercontinental Exchange’s Energy Markets Transition Is Credit

Negative for Power Producers » CELPA Wins Large Tariff Increase, a Credit Positive » UK Competition Commission’s Decision Is Credit Positive for

Phoenix Natural Gas

Banks 14 » Trading Losses at Knight and UBS Are Credit Negative for Bondholders » Danish Banks Pay to Place Deposits with the Central Bank, a

Credit Negative » Commerzbank’s Withdrawal from Ukraine Is Credit Negative for

Forum Bank » Chinese Regulator’s Criticism of Banks' Compliance Reporting

Highlights Risk » Indonesian Banks Mobilize Their Recap Bonds to Gain Liquidity, a

Credit Positive

Asset Managers and Money Market Funds 20 » Resurgence of US Closed-End Fund IPOs Is Credit Positive for Managers » US Treasury Prepares for Negative Interest Rates, a Credit

Negative for Money Market Funds

Sovereigns 24 » Myanmar Moves Toward Rejoining International Financial System,

a Credit Positive » Fiji Restores Credit-Positive Diplomatic Ties with Australia and

New Zealand

US Public Finance 26 » California Risks Losing Hundreds of Millions of Dollars from

Facebook’s Plunging Share Price » Georgia Voters Spurn Proposed Tax, a Credit Negative for Atlanta

and Eight Other Regions » Massachusetts Bill Limiting Healthcare Spending Is Credit Negative

for Hospitals

Securitization 29 » Increase in For-Profit College Dropouts Hurts Student Loan

Securitizations

Accounting 31 » Loosening US Framework for Private Company Financial Reporting

Is Negative for Investors

RATINGS & RESEARCH Rating Changes 33

Last week we downgraded Walgreen, Bermuda Commercial Bank, DSK Bank, First Horizon National, First Tennessee Bank, Forum Bank, Raiffeisenbank (Bulgaria) EAD, and 258 Italian ABS and RMBS, and upgraded several Uruguayan banks, among other rating actions.

Research Highlights 40

Last week we published on packaging, Latin American corporates, US corporate pensions, US restaurants, US utilities, French banks, Greek banks, Danish banks, US banks, global insurers, US states' cash flow notes, US privatized military housing, US auto ABS, and Asia-Pacific structured finance, among other reports.

MOODYS.COM

Report: 144581

© 2012 Moody’s Investors Service, Inc. and/or its licensors and affiliates (collectively, “MOODY’S”). All rights reserved.

CREDIT RATINGS ISSUED BY MOODY'S INVESTORS SERVICE, INC. (MIS”) AND ITS AFFILIATES ARE MOODY’S CURRENT OPINIONS OF THE RELATIVE FUTURE CREDIT RISK OF ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES, AND CREDIT RATINGS AND RESEARCH PUBLICATIONS PUBLISHED BY MOODY’S (“MOODY’S PUBLICATIONS”) MAY INCLUDE MOODY’S CURRENT OPINIONS OF THE RELATIVE FUTURE CREDIT RISK OF ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES. MOODY’S DEFINES CREDIT RISK AS THE RISK THAT AN ENTITY MAY NOT MEET ITS CONTRACTUAL, FINANCIAL OBLIGATIONS AS THEY COME DUE AND ANY ESTIMATED FINANCIAL LOSS IN THE EVENT OF DEFAULT. CREDIT RATINGS DO NOT ADDRESS ANY OTHER RISK, INCLUDING BUT NOT LIMITED TO: LIQUIDITY RISK, MARKET VALUE RISK, OR PRICE VOLATILITY. CREDIT RATINGS AND MOODY’S OPINIONS INCLUDED IN MOODY’S PUBLICATIONS ARE NOT STATEMENTS OF CURRENT OR HISTORICAL FACT. CREDIT RATINGS AND MOODY’S PUBLICATIONS DO NOT CONSTITUTE OR PROVIDE INVESTMENT OR FINANCIAL ADVICE, AND CREDIT RATINGS AND MOODY’S PUBLICATIONS ARE NOT AND DO NOT PROVIDE RECOMMENDATIONS TO PURCHASE, SELL, OR HOLD PARTICULAR SECURITIES. NEITHER CREDIT RATINGS NOR MOODY’S PUBLICATIONS COMMENT ON THE SUITABILITY OF AN INVESTMENT FOR ANY PARTICULAR INVESTOR. MOODY’S ISSUES ITS CREDIT RATINGS AND PUBLISHES MOODY’S PUBLICATIONS WITH THE EXPECTATION AND UNDERSTANDING THAT EACH INVESTOR WILL MAKE ITS OWN STUDY AND EVALUATION OF EACH SECURITY THAT IS UNDER CONSIDERATION FOR PURCHASE, HOLDING, OR SALE.

ALL INFORMATION CONTAINED HEREIN IS PROTECTED BY LAW, INCLUDING BUT NOT LIMITED TO, COPYRIGHT LAW, AND NONE OF SUCH INFORMATION MAY BE COPIED OR OTHERWISE REPRODUCED, REPACKAGED, FURTHER TRANSMITTED, TRANSFERRED, DISSEMINATED, REDISTRIBUTED OR RESOLD, OR STORED FOR SUBSEQUENT USE FOR ANY SUCH PURPOSE, IN WHOLE OR IN PART, IN ANY FORM OR MANNER OR BY ANY MEANS WHATSOEVER, BY ANY PERSON WITHOUT MOODY’S PRIOR WRITTEN CONSENT.

All information contained herein is obtained by MOODY’S from sources believed by it to be accurate and reliable. Because of the possibility of human or mechanical error as well as other factors, however, all information contained herein is provided “AS IS” without warranty of any kind. MOODY'S adopts all necessary measures so that the information it uses in assigning a credit rating is of sufficient quality and from sources MOODY'S considers to be reliable including, when appropriate, independent third-party sources. However, MOODY’S is not an auditor and cannot in every instance independently verify or validate information received in the rating process. Under no circumstances shall MOODY’S have any liability to any person or entity for (a) any loss or damage in whole or in part caused by, resulting from, or relating to, any error (negligent or otherwise) or other circumstance or contingency within or outside the control of MOODY’S or any of its directors, officers, employees or agents in connection with the procurement, collection, compilation, analysis, interpretation, communication, publication or delivery of any such information, or (b) any direct, indirect, special, consequential, compensatory or incidental damages whatsoever (including without limitation, lost profits), even if MOODY’S is advised in advance of the possibility of such damages, resulting from the use of or inability to use, any such information. The ratings, financial reporting analysis, projections, and other observations, if any, constituting part of the information contained herein are, and must be construed solely as, statements of opinion and not statements of fact or recommendations to purchase, sell or hold any securities. Each user of the information contained herein must make its own study and evaluation of each security it may consider purchasing, holding or selling.

NO WARRANTY, EXPRESS OR IMPLIED, AS TO THE ACCURACY, TIMELINESS, COMPLETENESS, MERCHANTABILITY OR FITNESS FOR ANY PARTICULAR PURPOSE OF ANY SUCH RATING OR OTHER OPINION OR INFORMATION IS GIVEN OR MADE BY MOODY’S IN ANY FORM OR MANNER WHATSOEVER.

MIS, a wholly-owned credit rating agency subsidiary of Moody’s Corporation (“MCO”), hereby discloses that most issuers of debt securities (including corporate and municipal bonds, debentures, notes and commercial paper) and preferred stock rated by MIS have, prior to assignment of any rating, agreed to pay to MIS for appraisal and rating services rendered by it fees ranging from $1,500 to approximately $2,500,000. MCO and MIS also maintain policies and procedures to address the independence of MIS’s ratings and rating processes. Information regarding certain affiliations that may exist between directors of MCO and rated entities, and between entities who hold ratings from MIS and have also publicly reported to the SEC an ownership interest in MCO of more than 5%, is posted annually at www.moodys.com under the heading “Shareholder Relations — Corporate Governance — Director and Shareholder Affiliation Policy.”

Any publication into Australia of this document is by MOODY’S affiliate, Moody’s Investors Service Pty Limited ABN 61 003 399 657, which holds Australian Financial Services License no. 336969. This document is intended to be provided only to “wholesale clients” within the meaning of section 761G of the Corporations Act 2001. By continuing to access this document from within Australia, you represent to MOODY’S that you are, or are accessing the document as a representative of, a “wholesale client” and that neither you nor the entity you represent will directly or indirectly disseminate this document or its contents to “retail clients” within the meaning of section 761G of the Corporations Act 2001.

Notwithstanding the foregoing, credit ratings assigned on and after October 1, 2010 by Moody’s Japan K.K. (“MJKK”) are MJKK’s current opinions of the relative future credit risk of entities, credit commitments, or debt or debt-like securities. In such a case, “MIS” in the foregoing statements shall be deemed to be replaced with “MJKK”. MJKK is a wholly-owned credit rating agency subsidiary of Moody's Group Japan G.K., which is wholly owned by Moody’s Overseas Holdings Inc., a wholly-owned subsidiary of MCO.

This credit rating is an opinion as to the creditworthiness or a debt obligation of the issuer, not on the equity securities of the issuer or any form of security that is available to retail investors. It would be dangerous for retail investors to make any investment decision based on this credit rating. If in doubt you should contact your financial or other professional adviser.

EDITORS PRODUCTION ASSOCIATE Jay Sherman and Elisa Herr Alisa Llorens