Embed Size (px)

Citation preview

New York University Salomon Center

Leonard N. Stern School of Business

Special Report On

Defaults and Returns in the High-Yield Bond and Distressed Debt

Market:

The Year 2009 in Review and Outlook

By

Edward I. Altman

with

Brenda J. Karlin

February 08, 2010

February 08, 2010 Altman High-Yield Bond Default and Return Report

2

Contents

Executive Summary ....................................................................................................................................... 3

Defaults, Default Rates, and Recoveries ........................................................................................................ 4

Bankruptcies .................................................................................................................................................. 8

Industry Defaults .......................................................................................................................................... 10

Age of Defaults ............................................................................................................................................ 11

Fallen Angel Defaults .................................................................................................................................. 12

Default Losses and Recoveries .................................................................................................................... 14

Distressed Exchanges................................................................................................................................... 17

Liquidation Recoveries ................................................................................................................................ 21

Forecast Recovery Versus Actual ................................................................................................................ 24

Related Recovery Statistics .......................................................................................................................... 25

Mortality Rates and Losses .......................................................................................................................... 29

Returns and Spreads ..................................................................................................................................... 30

New Issues and Other Changes in the High-Yield Market .......................................................................... 33

Credit Quality and Trends in New Issuance ................................................................................................ 33

Proportion and Size of the Distressed and Defaulted Public and Private Debt Markets .............................. 34

Forecasting Default Rates and Recoveries ................................................................................................... 37

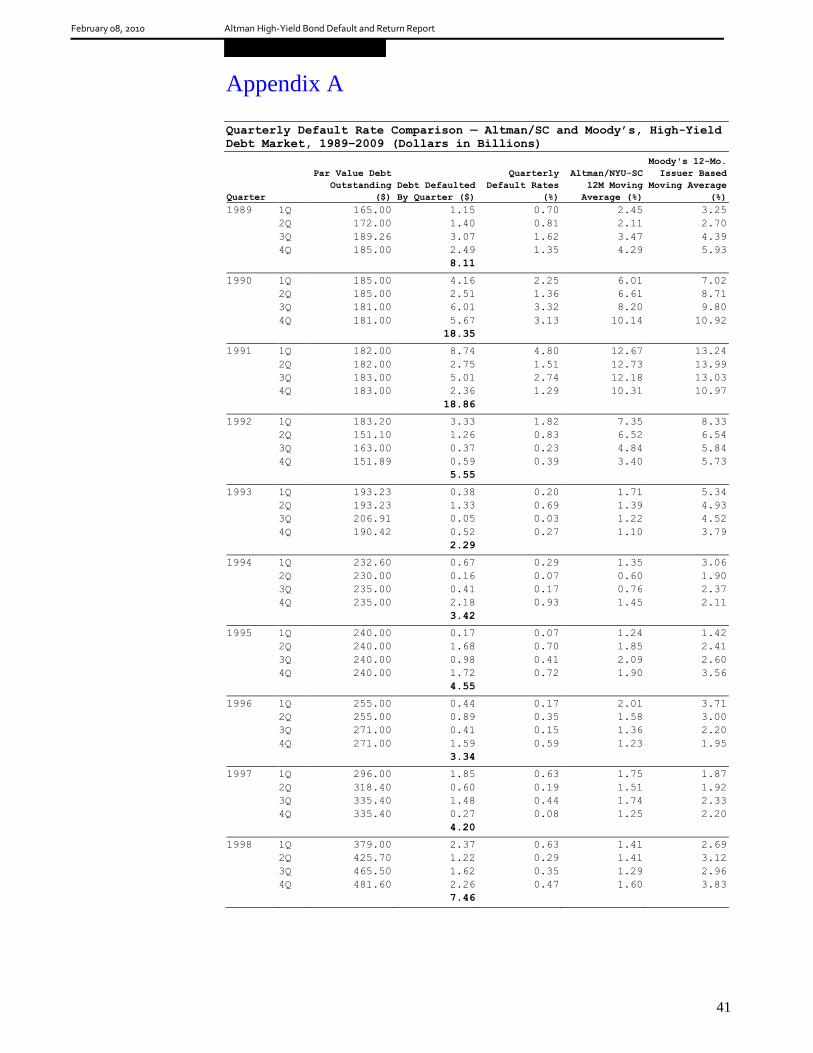

Appendix A: Quarterly Default Rate Comparison ....................................................................................... 41

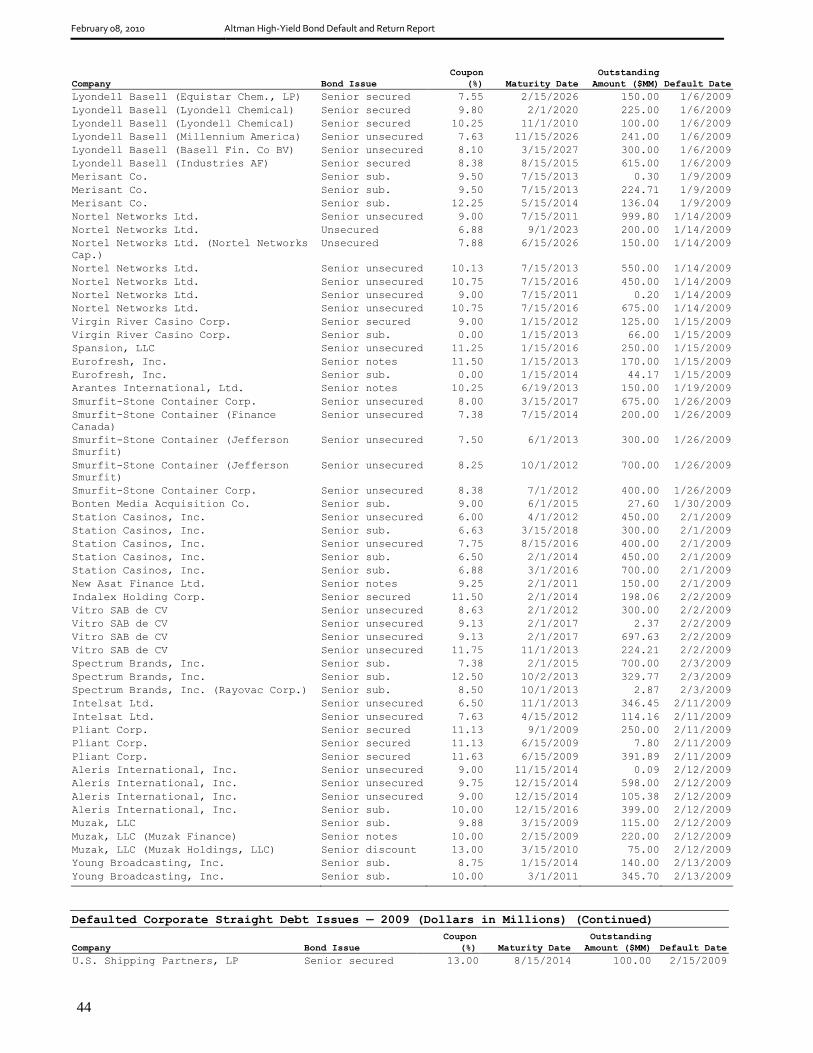

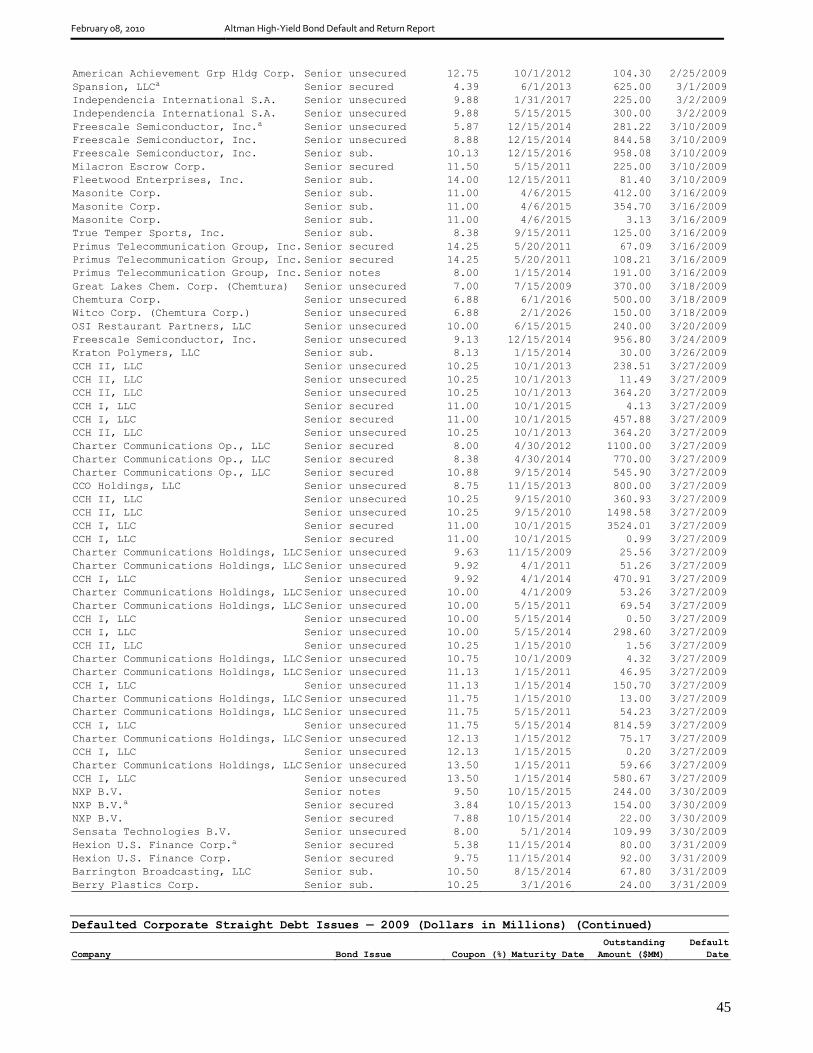

Appendix B: Defaulted Corporate Straight Debt Issues .............................................................................. 43

Appendix C: Distressed Exchanges ............................................................................................................. 51

Appendix D: Leveraged Loan Defaults ....................................................................................................... 52

Appendix E: Chapter 11 Filings by Liability Size ....................................................................................... 54

Appendix F: Defaults by Industry ................................................................................................................ 58

Appendix G: 2009 Emergences from Default .............................................................................................. 61

Acknowledgments

Dr. Altman is the Max L. Heine Professor of Finance and Director of the Credit and Debt

Markets Research Program at the NYU Salomon Center, Leonard N. Stern School of Business

and a consultant to Paulson & Co. Brenda Karlin is a Research Associate at the NYU Salomon

Center. We appreciate the assistance of Vallabh Muralikrishnan and Hemant Sharma of the NYU

Salomon Center and the several market makers who provided us with price quotations. We offer a

special thanks to the various rating agencies, Daniel Sweeney and Johnathan Blau of Credit

Suisse, Steven Miller of S&P LCD, Kerry Mastroianni of New Generation Research and Daniel

Kamensky of Paulson & Co..

February 08, 2010 Altman High-Yield Bond Default and Return Report

3

From a default and performance perspective, the year 2009 proved to be a year

of incredible contrasts for investors in high yield bonds, with a record amount

of defaults ($123.8 billion) occurring, surpassing the previous record in 2002

($96.8 billion). However, absolute returns and returns versus 10-yr Treasuries

were at their highest historical levels, new issuance increased more than three-

fold in a one-year period, and only 15% of high-yield bonds outstanding were

classified as distressed by year-end, compared to 82% one year earlier.

In several ways, 2009 was reminiscent of 1991 when the default rate also

topped 10 percent, yet absolute and relative returns (43.23% and 26.05%)

registered record high levels (to that point). In both years, investors had

expected much worse conditions in the subsequent year, and required yield

spreads at the start of each year were at record-high levels.

The default rate rose to 10.74%, the highest annual default rate since 2002, and

the second highest default rate in our entire time series. The fourth-quarter 2009

default rate was 2.59%, increasing from the third-quarter 2009, but at a lower

level than one year earlier (2.90%).

Default losses on high-yield bonds came in at 7.30%, based on a weighted

average recovery rate of 36.1% just after default, slightly below the historical

average. The weighted average recovery on bankruptcy and payment defaults

was somewhat lower at 34.6%, compared to 42.7% for distressed exchange

default recoveries.

Returns on high-yield bonds reached historically high levels, ending the year at

55.19% (Citi Index). The excess return versus 10-yr US Treasuries was 65.11%,

more than double the previous record high of 29.37% in 2003. Yield-to-

maturity spreads versus 10-yr US Treasuries decreased to 5.13% by year-end

2009, 1,218bp lower than year-end 2008, but in-line with the historical average

of 5.23%. Defaulted bonds and bank loans also did extremely well, with a

combined return of 56.0%.

The distressed ratio of bonds yielding more than 1,000bp above the risk-free

rate decreased dramatically to 15.3% as of the end of 2009, from 26.8% three

months earlier and an astonishing 82.0% at year-end 2008. This metric has

decreased steadily over the ensuing thirteen months.

Estimates of the face value size of the distressed and defaulted debt markets

decreased significantly to $1.61 trillion, as of December 31, 2009, down more

than 50% from $3.59 trillion one year earlier. This decrease is attributable to the

dramatic drop in the distressed ratio. The market value estimate also decreased

to approximately $1.01 trillion.

Based on our mortality rate methodology and new issuance in the last ten years,

stratified by original bond rating, the Altman forecast for the high-yield bond

market’s default rate in 2009 was 7.98%, and based on several different models

was 13.6%, compared to an actual default rate of 10.74%. This year, based on

four different methodologies, the 2010 forecasts range from 3.86% (distressed

ratio method) to 14.00% (recession scenarios method), with the consensus

average rate of 6.70%, if the economy ―double-dips‖ into a recession or never

emerges from the current downturn, and 4.27% if it does not.

February 08, 2010 Altman High-Yield Bond Default and Return Report

4

Defaults, Default Rates, and Recoveries

The high-yield bond default rate in 2009 soared to levels unprecedented over the past

seven years. 2009 witnessed the second highest dollar denominated default rate in

our time series (from 1971), lower only than the rate realized in 2002. The rate

increased from 4.65% at year-end 2008 to 10.74% for all of 2009. Defaults include

straight corporate bonds whose firms went bankrupt, missed an interest payment and

did not cure it within the grace or forbearance period, or completed a distressed

exchange. The 2009 rate is based on a mid-year market size of $1.153 trillion, up by

$62 billion from a year earlier. In all, $123.8 billion of defaults, the largest dollar

amount ever, was recorded in 2009 (Figure 1), surpassing 2002 by $27 billion. Note

in Figure 1 that the historical weighted-average annual default rate is 4.55% over the

39 year period (1971-2009). This weighted-average rate is up considerably compared

to 3.94% at the end of 2008. Our weights are based on the par value of high-yield

bonds outstanding in each year. The arithmetic annual average default rate climbed

to 3.33% from 3.14% one year earlier.

In the fourth quarter of 2009, the default rate was 2.59%, larger than one quarter earlier

(0.83%), but lower than both the first two quarters of 2009 as well as the fourth quarter

of 2008 (Figure 2 and Appendix A). Two-thirds of the dollar amount of defaults in the

fourth quarter was related to the bankruptcy filing by CIT Group. Indeed, had this

default not occurred, the quarterly default rate would have been a mere 0.74%, the

lowest since the third-quarter 2008, indicating a slow-down in the rapid pace of defaults

which has plagued the market in the past year. Eighteen issuers defaulted in the fourth

quarter on 76 issues. The most sizeable defaults during the year were CIT, defaulting on

over $22 billion of outstanding bonds, Charter Communications, defaulting on almost

$13 billion, and General Motors, which defaulted on over $10 billion. Abitibi Bowater,

Ford Motor, Harrah’s, Nortel, and R.H. Donnelley each defaulted on outstanding bonds

of more than $3 billion. In all, 119 issuers constituting 405 issues defaulted in 2009

(Appendix B), considerably greater than the 63 issuers and 154 issues that defaulted in

2008. The average dollar amount of defaulting bonds per defaulting issuer in 2009 was

$1.04 billion, compared to $796 million in 2008, and $288 million in 2007. Lehman

Brothers is not included in the 2008 statistics since its bonds were not rated non-

investment grade before defaulting.

In our default statistics, we include those bonds from distressed exchanges actually

tendered. For example, in the Ford Motor Co. exchange, $3.35 billion of bonds were

exchanged of the $8.2 billion outstanding and subject to the exchange offer. In 2009,

there were a record 53 distressed exchanges, involving 45 companies, comprising

$22.9 billion of defaults (18.5% of the total). See Appendix C for the list of 2009

distressed exchanges and later our discussion of these restructurings.

In 2009, S&P and Moody’s issuer-denominated default rates were 10.93% and

13.22%, respectively. Moody’s 16.50% dollar-denominated default rate was greater

than its issuer-denominated rate, as is usually the case in a stressed year. Fitch’s

dollar-denominated default rate for 2009 was 13.70%.

The issuer-based default rate for the last 12 months in the US leveraged loan market

was 8.07% (Figure 3), and 9.61% based on amount of issuance, according to S&P’s

LCD compilations. This is in contrast to the significantly smaller rates of 4.35% and

February 08, 2010 Altman High-Yield Bond Default and Return Report

5

3.75%, respectively, at the end of 2008. Sixty-four leveraged loan issuers defaulted

in 2008 (Appendix D), compared to forty-one in 2008. According to our comparison

between high-yield bond defaults (Appendix B) and leveraged loan defaults

(Appendix D), 27 firms had both bonds and leveraged loans default in 2009.

Since the U.S. economy went into a recession in December 2007, and technically

was still in recession in 2009, both 2008 and 2009 are included as recession years.

Whereas the default rate began increasing two years, or so, before the start of the two

prior recessions, this time the increase in default rates coincided with the beginning

(Figure 4). In all five prior recessions since 1972, it is clear that the default rates

peaked near the end, or soon after the recession. Since 2010’s economic outlook is

highly uncertain, our default rate forecast will be based on both recession and non-

recession scenarios.

February 08, 2010 Altman High-Yield Bond Default and Return Report

6

Figure 1. Historical Default Rates — Straight Bonds Only, Not

Including Defaulted Issues From Par Value Outstanding, 1971–2009

(Dollars in Millions)

Par Value

Year

Outstandinga

($) Defaults ($)

Default Rates

(%)

2009 1,152,952 123,824 10.740

2008 1,091,000 50,763 4.653

2007 1,075,400 5,473 0.509

2006 993,600 7,559 0.761

2005 1,073,000 36,209 3.375

2004 933,100 11,657 1.249

2003 825,000 38,451 4.661

2002 757,000 96,858 12.795

2001 649,000 63,609 9.801

2000 597,200 30,295 5.073

1999 567,400 23,532 4.147

1998 465,500 7,464 1.603

1997 335,400 4,200 1.252

1996 271,000 3,336 1.231

1995 240,000 4,551 1.896

1994 235,000 3,418 1.454

1993 206,907 2,287 1.105

1992 163,000 5,545 3.402

1991 183,600 18,862 10.273

1990 181,000 18,354 10.140

1989 189,258 8,110 4.285

1988 148,187 3,944 2.662

1987 129,557 7,486 5.778

1986 90,243 3,156 3.497

1985 58,088 992 1.708

1984 40,939 344 0.840

1983 27,492 301 1.095

1982 18,109 577 3.186

1981 17,115 27 0.158

1980 14,935 224 1.500

1979 10,356 20 0.193

1978 8,946 119 1.330

1977 8,157 381 4.671

1976 7,735 30 0.388

1975 7,471 204 2.731

1974 10,894 123 1.129

1973 7,824 49 0.626

1972 6,928 193 2.786

1971 6,602 82 1.242

Standard

Deviation (%)

Arithmetic Average

Default Rate

1971 to 2009 3.331 3.224

1978 to 2009 3.636 3.422

1985 to 2009 4.322 3.548

Weighted Average

Default Rateb

1971 to 2009 4.550

1978 to 2009 4.561

1985 to 2009 4.598

Median Annual Default

Rate

1971 to 2009 1.896

a As of midyear.

b Weighted by par value of amount outstanding for each year.

Source: NYU Salomon Center.

February 08, 2010 Altman High-Yield Bond Default and Return Report

7

Figure 2. Quarterly and the Four-Quarter Moving Average Default Rate

1989–2009

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

198919901991199219931994199519961997199819992000200120022003200420052006200720082009

Qu

arte

rly

Def

ault

Rat

e

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

4 -

Qu

arte

r M

ovin

g A

vera

ge

Quarterly

Moving

Source: NYU Salomon Center.

Figure 3. S&P Leveraged Loan Index 12-Month Moving Average Default

Rate 1998–2009 (Number of Issuers)

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00%

9.00%

Dec-98

Jun-99

Dec-99

Jun-00

Dec-00

Jun-01

Dec-01

Jun-02

Dec-02

Jun-03

Dec-03

Jun-04

Dec-04

Jun-05

Dec-05

Jun-06

Dec-06

Jun-07

Dec-07

Jun-08

Dec-08

Jun-09

Dec-09

Source: Standard & Poor’s LCD.

Figure 4. Historical Default Rates and Recession Periods in the US

High-Yield Bond Market, 1972–2009

Periods of Recession: 11/73–3/75, 1/80–7/80, 7/81–11/82, 7/90–3/91, 4/01–12/01, 12/07–

12/09 (still continuing as of 12/09).

Sources: Figure 1 of this report and National Bureau of Economic Research.

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

72 74 76 78 80 82 84 86 88 90 92 94 96 98 00 02 04 06 08

February 08, 2010 Altman High-Yield Bond Default and Return Report

8

Bankruptcies

As can be seen in Figure 5, the amount of total liabilities for Chapter 11 bankruptcies

in 2009 was $604.0 billion, based on 234 filings. Where total liabilities exceeded

$100 million, the total liabilities for filings in 2009 are larger than any prior year,

except for last ($720.8 billion), which included the Lehman Brothers’ filing. General

Motors Corp. was the largest bankruptcy filing in 2009, with $172.8 billion in

liabilities. Without Lehman, this past year’s liabilities in bankruptcy would have

exceeded 2008 by almost $500 billion, and would be greater than the previous peak

in 2002 by almost $250 billion.

Appendix E lists this year’s large Chapter 11 bankruptcies. Our bankruptcy list

includes a large number of LBOs. So far this year, there were 74 bankrupt LBOs (six

in which the PE firm had only a minority interest), 25 more than the 49 of such

filings for all of 2008.1

Figure 5. Total Filings and Liabilitiesa of Public Companies Filing

for Chapter 11 Protection, 1989–2009

$0

$100

$200

$300

$400

$500

$600

$700

$800

89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 (Excl. LEH

)

08 (Incl. LEH

)

2009

$ B

illi

on

0

40

80

120

160

200

240

280

Pre- Petition Liabilities, in $ billions (left axis)

Number of Filings (right axis)

2009

234 filings and liabilities of

$604.0 billion

2008

Excluding Lehman

Brothers

145 filings and

liabilities of

$107.8 billion

Including Lehman

Brothers

146 filings and

liabilities of $720.8

billion

a Minimum $100 million in liabilities.

Sources: Appendix E from the NYU Salomon Center Bankruptcy Filings Database.

The number of billion-dollar bankruptcies in 2009 increased two-fold from 21, last

year, to 43, higher than the 41 recorded in 2002, the prior record year. The majority

of the larger bankruptcies were in the auto/motor carrier, financial services,

communications, and construction/real estate sectors (Appendix D).

According to New Generation Research, the number of public companies filings was

207 (Figure 6). The average of total liabilities for all 234 bankruptcy filings in 2009

was $2.6 billion, down from $4.9 billion one year earlier. The latter figure would

have been just 0.7 billion without Lehman.

1 List compiled by E. Griffith, published on www.pehub.com.

February 08, 2010 Altman High-Yield Bond Default and Return Report

9

Figure 6. Historical Bankruptcy Filings 1980–2008

Year Total Filingsa

Total Filingsb

(>$100

Million)

Total Filings

(≥$1 Billion)

Total

Liabilitiesb

($ MN)

(>100 Million)

Average

Liabilitiesb

($ MN)

(>100 Million)

1980 62 4 0 746.0 186.5

1981 74 6 1 3960.0 660.0

1982 84 12 3 7113.0 592.8

1983 89 14 3 13674.0 976.7

1984 121 12 0 3440.0 286.7

1985 149 14 2 8605.2 614.7

1986 149 11 3 9335.4 850.5

1987 112 12 1 25421.0 2118.4

1988 122 14 2 6905.0 493.2

1989 135 22 10 33538.9 1524.5

1990 115 35 10 41115.1 1174.7

1991 123 51 11 81157.9 1591.3

1992 91 37 14 64224.1 1735.8

1993 86 37 4 17701.1 478.4

1994 70 24 1 8396.0 349.8

1995 85 32 7 27153.0 848.5

1996 86 32 0 11687.0 365.2

1997 83 36 5 18865.9 524.1

1998 122 56 6 32038.3 572.1

1999 145 109 19 70957.1 651.0

2000 179 136 23 98895.8 727.2

2001 263 169 38 228604.1 1352.7

2002 220 135 41 336611.7 2493.4

2003 172 102 26 115171.8 1129.1

2004 92 44 11 39549.7 898.9

2005 86 34 10 141525.2 4162.5

2006 66 32 4 22321.6 697.6

2007 78 38 8 72642.7 1911.7

2008 136 147 21 721009.8 4904.8

2009 207 234 43 603992.3 2581.2

Total 3602 1641 327 2,866,382.3 1,746.7

a Represents both Chapter 7 and 11 public company filings (Source: New Generation

Research). b

Filings of all companies, including private firms, with Total Liabilities

greater than $100 million (Source: NYU Salomon Center Bankruptcy Filings Database). c

Filings with Total Liabilities greater than $1 billion (Source: NYU Salomon Center

Bankruptcy Filings Database).

In Figure 7, we compare the date of default with the Chapter 11 filing date for firms

that defaulted on bonds and also went bankrupt going back to 1981. Based on 833

observations from the NYU Salomon Center Master Default and Bankruptcy

Databases, both events occurred on the same date in 408 instances (49%). In the

remaining 51% of the cases, the lag between the default date and bankruptcy date

varied considerably, with decreasing levels as the two dates became further separated

from each other. Of course, some defaulting issuers never formally file for

bankruptcy as their problems are settled out of court or the default comes as a result

of a distressed exchange, and they do not file for bankruptcy in subsequent years

(many do, however – see our discussion at a later point).

February 08, 2010 Altman High-Yield Bond Default and Return Report

10

Figure 7. Time Differential Between Default and Bankruptcy Filinga

(1981–2009)

0%

10%

20%

30%

40%

50%

60%

0 2 4 6 8 10 12 14 16 18 20 22 24 26 28 29 31 33 35

Number of Months Lag

% o

f the

Tot

al O

bser

vatio

ns

*Based on 833 observations

Source: NYU Salomon Center Default and Bankruptcy Filings Databases

(408)

a

Based on 833 observations.

Source: NYU Salomon Center Default and Bankruptcy Filings Databases.

Industry Defaults

Figure 8 lists the number of high-yield bond defaults by industry. Of the total 119

defaulting issuers in 2009, general manufacturers, communications and media,

leisure and entertainment, and real estate/construction were industries in which a

total of 78 firms defaulted. Nine issuers defaulted in the auto/motor carrier sector,

eight in energy, and seven in both financial services and transportation. The

remaining ten defaulting issuers were spread over various industries. Appendix E

presents a more detailed breakdown of all 119 defaulting issuers.

Figure 9 shows high-yield corporate bond defaults across industries per dollar

amount since 1990. Communications and media ―lead‖ the 2009 totals, due primarily

to the Charter Communications and R.H. Donnelley defaults. As in the past, we

observe that the communications and media sector far outdistanced all other sectors

in the dollar amount of defaulting issues over the last 19 years, primarily the result of

the telecom meltdown during 2000–02, as well as 2009’s defaults due to large-scale

bankruptcies.

February 08, 2010 Altman High-Yield Bond Default and Return Report

11

Figure 8. Corporate Bond Defaults by Industry (Number of Companies)

Industry 1970–89 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 Total

Auto/Motor

Carrier

6 3 1 1 1 4 3 8 9 36

Conglomerates 5 1 3 3 1 1 1 15

Energy 35 4 2 3 1 1 13 1 8 9 1 1 4 8 91

Financial

Services

21 7 14 3 2 1 2 1 2 6 1 6 4 5 6 2 3 2 5 7 100

Leisure/Entertai

nment

9 8 2 4 3 4 3 1 5 5 8 9 6 5 6 3 10 12 103

General

Manufacturing

26 5 8 8 7 3 8 6 7 6 16 23 43 22 13 17 12 6 7 10 35 288

Health Care 4 2 1 1 1 2 2 8 6 3 4 3 2 1 1 41

Miscellaneous

Industries

16 4 4 3 1 1 1 3 3 16 34 38 25 16 6 1 4 3 4 5 188

Real

Estate/Construct

ion

14 7 5 1 2 1 2 1 4 6 4 3 2 1 6 11 70

REIT 12 1 1 14

Retailing 10 6 15 6 4 5 6 3 6 6 12 7 12 5 5 3 2 2 3 5 5 128

Comm. & Media 17 3 4 1 1 3 2 2 1 6 11 8 39 26 21 6 3 2 4 10 20 190

Transportation

(Non Auto)

9 1 2 2 2 1 8 5 7 7 6 2 5 1 7 65

Utilities 2 1 1 1 1 0 0 6

Total 186 47 62 34 22 19 28 15 29 37 98 107 156 112 86 39 34 23 19 63 119 1,335

Source: NYU Salomon Center.

Figure 9. Corporate Bond Defaults by Industry (Dollars in Millions)

Industry 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 Total

Auto/Motor

Carrier

468 90 215 300 100 430 120 3,737 285 280 3,573 2,692 1,382 16,872 30,544

Conglomerates 100 690 275 1,065

Energy 60 103 600 75 100 3,812 217 4,200 4,085 11,857 8,895 50 1,511 1,993 37,558

Financial

Services

928 696 536 78 687 700 66 689 375 1,968 5,062 3,803 1,079 110 541 156 26,973 29,274 73,721

Leisure/

Entertainment

498 1,191 159 138 435 293 245 1,100 2,891 3,437 21,242 633 1,286 6,861 715 6,022 10,395 57,541

General

Manufacturing

2,675 3,695 488 118 616 641 123 247 2,092 2,507 3,138 2,455 2,108 225 1,396 1,486 2,379 3,747 25,766 55,902

Health Care 18 1,120 75 125 2,214 1,715 692 115 3,843 360 520 150 10,947

Miscellaneous

Industries

1,968 4,911 1,378 1,056 317 1,286 832 461 1,290 7,615 8,352 9,715 5,594 4,494 1,977 569 409 1,396 1,505 1,787 56,912

Real Estate/

Construction

2,605 417 113 49 75 190 258 383 385 252 1,110 1,088 77 1,783 174 2,158 4,803 15,921

Retailing 4,443 2,937 1,489 18 2,814 395 164 2,504 1,241 2,052 3,081 1,586 4,092 877 749 1,059 332 363 1,412 1,015 32,623

Communications

& Media

460 286 1,549 2,980 5,983 34,827 47,953 7,603 2,551 150 1,496 765 5,904 30,954 143,461

Transportation

(Non Auto)

1,028 1,452 301 562 1,125 310 2,890 1,430 4,711 2,086 2,421 12,376 272 964 31,928

Utilities 1,452 617 85 275 202 75 1,150 1,417

5,273

Total 14,631 18,021 4,883 1,926 3,723 4,536 3,465 4,200 6,994 23,440 29,976 68,934 96,673 36,764 11,657 35,954 7,559 5,473 50,763 123,824 552,801

Source: NYU Salomon Center.

Age of Defaults

Figure 10 shows the age distribution of defaults in 2009 and for the period 1991–

2009. It appears normal that the number of defaults is low in the first year after

issuance. What typically follows is an increase in default rates in years two through

four. Indeed, 2009 essentially mirrors the cumulative default proportions over 1991–

2009, in terms of marginally increasing default frequencies in years one through

three, slightly lower rates in years four and five versus three. There was a somewhat

interesting increase in six-year-old issues and a disproportionately large cohort

February 08, 2010 Altman High-Yield Bond Default and Return Report

12

(15%) of bonds issued ten or more years prior to default. Many bonds that were ten

years or older that defaulted in 2009 were originally investment-grade issues. Again,

as in 2008, a small proportion (5%) defaulted during the first year after issuance. The

historical average is 8%.

Figure 10. Distribution of Years to Default From Original Issuance Date (By Year of

Default), 1991–2009

1991 1992 1993/1994 1995 1996/1997 1998 1999 2000 2001

Years

to No. of % of No. of % of No. of % of No. of % of No. of % of No. of % of No. of % of No. of % of No. of % of

Default Issues Total Issues Total Issues Total Issues Total Issues Total Issues Total Issues Total Issues Total Issues Total

1 0 0 0 0 3 8 1 3 7 14 2 6 32 26 19 10 40 12

2 18 13 0 0 6 16 9 28 7 14 5 15 37 30 51 28 69 21

3 26 19 7 13 5 14 7 22 7 14 10 30 15 12 56 31 87 26

4 29 21 10 19 2 5 3 9 17 36 3 9 14 11 14 8 65 19

5 35 26 8 15 4 11 1 3 4 8 10 30 7 6 13 7 27 8

6 10 7 12 22 8 22 2 6 5 10 2 6 8 6 5 3 14 4

7 4 3 5 9 7 19 2 6 0 0 1 3 10 8 12 7 21 6

8 10 7 4 7 0 0 2 6 0 0 0 0 2 2 4 2 5 1

9 3 2 0 0 0 0 4 13 0 0 0 0 0 0 3 2 4 1

10+ 2 1 8 15 2 5 1 3 2 4 0 0 0 0 6 3 3 1

Total 137 100 54 100 37 100 32 100 49 100 33 100 125 100 183 100 335 100

2002 2003 2004 2005 2006 2007 2008 2009 1991–2009

Years

to

No. of

% of

No. of

% of

No. of

% of

No. of

% of

No. of

% of

No. of

% of

No. of

% of

No. of

% of

No. of

% of

Default Issues Total Issues Total Issues Total Issues Total Issues Total Issues Total Issues Total Issues Total Issues Total

1 29 8 18 9 8 10 16 9 2 4 1 3 9 6 20 5 207 8

2 51 15 30 15 7 9 13 7 4 8 1 3 18 12 39 10 365 15

3 61 18 26 13 8 10 9 6 6 12 6 17 34 22 65 16 435 18

4 56 16 23 11 6 8 22 12 5 10 9 26 30 19 61 15 369 15

5 45 13 40 20 10 13 14 8 4 8 3 9 20 13 51 13 296 12

6 21 6 20 10 16 21 17 9 9 17 4 11 10 6 58 14 221 9

7 8 2 25 12 9 12 13 7 6 12 2 6 9 6 15 4 149 6

8 7 2 3 1 6 8 11 6 7 13 5 14 6 4 18 4 90 4

9 12 3 5 2 1 1 5 3 6 12 1 3 7 5 16 4 67 3

10+ 54 16 13 6 6 8 64 34 3 6 3 9 11 7 62 15 240 10

Total 344 100 203 100 77 100 184 100 52 100 35 100 154 100 405 100 2,439 100

Source: NYU Salomon Center.

Fallen Angel Defaults

Twenty-three issuers (19% of the total in 2009) were responsible for 129 (32% of the

total) defaulting issues that were investment grade at some time prior to default. This

results in a fallen-angel issuer default rate of 8.07%, considerably higher than the

historical average of 3.88% (Figure 11). The fallen-angel default rate for 1985–2009

is slightly below the historical average annual rate for original issue defaults in the

high-yield bond market (4.60%). This differential (3.88% vs. 4.60%), however, is not

statistically significant due to a relatively high standard deviation of around 260bp

per year between the two rates. Figure 12 shows the fallen angel proportion of

defaults from 1977 to the present. In 2009, 32% of defaulted issues were originally

rated investment grade, somewhat above the historical average of 27%.

February 08, 2010 Altman High-Yield Bond Default and Return Report

13

Figure 11. Fallen Angels Versus Original(S&P)Issue and All High

Yield Default Ratesa (In Percent)

Year

Fallen Angel

Average

12-Mo. Default

Rate

Original Issue

Speculative Grade

Default Rates

All Speculative

Grade Bond

Default Rates

Altman Dollar

Weighted Annual

Default Rates

2009 8.07 11.89 10.93 10.74

2008 3.07 4.34 4.02 4.60

2007 0.86 1.00 0.97 0.51

2006 1.40 1.23 1.26 0.76

2005 2.74 3.70 2.48 3.37

2004 0.83 2.65 2.23 1.25

2003 5.88 5.46 5.53 4.66

2002 6.59 8.55 8.32 12.79

2001 8.46 10.14 10.99 9.81

2000 7.01 7.10 7.03 5.07

1999 4.01 5.10 4.62 4.15

1998 3.31 2.75 2.23 1.60

1997 2.04 2.10 1.71 1.25

1996 1.38 2.00 1.71 1.23

1995 0.25 3.90 3.07 1.90

1994 0.00 2.31 1.70 1.45

1993 1.72 1.99 1.79 1.10

1992 4.50 5.48 5.45 3.40

1991 7.53 10.86 11.66 10.27

1990 5.77 8.30 8.20 10.14

1989 3.74 4.93 5.33 4.29

1988 4.25 3.39 3.95 2.66

1987 4.36 2.92 2.41 5.78

1986 2.46 6.29 4.78 3.50

1985 6.77 4.06 3.24 1.71

Arithmetic Average

3.88 4.90 4.62 4.32

Standard Deviation

2.51 2.99 3.15 3.55

a All S&P issuer based except for Altman rates.

Sources: NYU Salomon Center and S&P.

February 08, 2010 Altman High-Yield Bond Default and Return Report

14

Figure 12. Fallen Angel Defaulted Issues by Original Rating, 1977-

2009

Year Total No. Defaulted Issuesa

Originally Rated Investment

Grade (%)

2009 405 32

2008 154 31

2007 35 11

2006 52 13

2005 184 49

2004 79 19

2003 203 33

2002 322 39

2001 258 14

2000 142 16

1999 87 13

1998 39 31

1997 20 0

1996 24 13

1995 29 10

1994 16 0

1993 24 0

1992 59 25

1991 163 27

1990 117 16

1989 66 18

1988 64 42

1987 31 39

1986 55 15

1985 26 4

1984 14 21

1983 7 43

1982 20 55

1981 1 0

1980 4 25

1979 1 0

1978 1 100

1977 2 100

Total 2,704 27%

a Where we could find an original rating from either S&P or Moody's.

Sources: Moody's, NYU Salomon Center, and S&P.

Default Losses and Recoveries

The weighted-average recovery rate (based on market prices just after defaults) on

high-yield bond defaults in 2009 remained below the historic average of 44.8% to

end the year at 36.1%. This is lower than the recovery rate of 42.5% in 2008, and is

the lowest rate since 2002. The default loss rate in 2009, without an adjustment for

fallen angels and including the loss of 0.438% (43.8bp) from lost coupons, was

approximately 730.0bp (Figure 13). If we remove fallen angel defaults (129 issues)

the loss would have been 1,009.2bp on original issue high-yield bonds.

Unlike the prior two quarters, the recovery rate on fallen angels was higher than on

original non-investment grade bonds demonstrating a return to the norm. This was

the result of the CIT defaults, which recovered roughly 65%, diluting the effect of

the GM default earlier in the year, which had recovered only about 10%. Over the

32-year period from 1978 to 2009, the arithmetic average annual loss rate on high-

yield bond defaults is 2.45%, 3.09% on a weighted-average basis (Figure 14).

February 08, 2010 Altman High-Yield Bond Default and Return Report

15

Figure 13. 2009 Default Loss Rate

Unadjusted for

Fallen Angels

(%)

Only Fallen

Angels (%)

All Except

Fallen Angels

(%)

Price Adjusted

for

Fallen Angels

(%)

Background Data

Average Default Rate 10.740 8.070 13.644 11.462

Average Price At Defaulta 36.133 43.224 30.784 35.655

Average Price At Downgradeb 81.04

Average Recovery 36.133 53.337 30.784 39.614

Average Loss Of Principal 63.867 46.663 69.216 60.386

Average Coupon Payment 8.163 5.856 9.504 8.076

Default Loss Computation

Default Rate 10.740 8.070 13.644 11.462

X Loss Of Principal 63.867 46.663 69.216 60.386

Default Loss of Principal 6.859 3.766 9.443 6.921

Default Rate 10.740 8.070 13.644 11.462

X Loss of 1/2 Coupon 4.082 2.928 4.752 4.038

Default Loss of Coupon 0.438 0.236 0.648 0.463

Default Loss of Principal

and Coupon

7.297 4.002 10.092 7.384

a If default date price is not available, end-of-month price is used.

b Downgrade to non-

investment grade. Note: Average Default Rate of “Only Fallen Angels” is based on number

of issuers.

Sources: NYU Salomon Center and various dealer quotes.

February 08, 2010 Altman High-Yield Bond Default and Return Report

16

Figure 14. Default Rates and Losses,a 1978–2009 (Dollars in Millions)

Year

Par Value

Outstandinga

($)

Par Value

of Default

($)

Default

Rate (%)

Weighted

Price After

Default ($)

Weighted

Coupon (%)

Default Loss

(%)b

2009 1,152,952 123,824 10.74 36.1 8.16 7.30

2008 1,091,000 50,763 4.65 42.5 8.23 2.83

2007 1,075,400 5,473 0.51 66.6 9.64 0.19

2006 993,600 7,559 0.76 65.3 9.33 0.30

2005 1,073,000 36,209 3.37 61.1 8.61 1.46

2004 933,100 11,657 1.25 57.7 10.30 0.59

2003 825,000 38,451 4.66 45.5 9.55 2.76

2002 757,000 96,858 12.79 25.3 9.37 10.15

2001 649,000 63,609 9.80 25.5 9.18 7.76

2000 597,200 30,295 5.07 26.4 8.54 3.95

1999 567,400 23,532 4.15 27.9 10.55 3.21

1998 465,500 7,464 1.60 35.9 9.46 1.10

1997 335,400 4,200 1.25 54.2 11.87 0.65

1996 271,000 3,336 1.23 51.9 8.92 0.65

1995 240,000 4,551 1.90 40.6 11.83 1.24

1994 235,000 3,418 1.45 39.4 10.25 0.96

1993 206,907 2,287 1.11 56.6 12.98 0.56

1992 163,000 5,545 3.40 50.1 12.32 1.91

1991 183,600 18,862 10.27 36.0 11.59 7.16

1990 181,000 18,354 10.14 23.4 12.94 8.42

1989 189,258 8,110 4.29 38.3 13.40 2.93

1988 148,187 3,944 2.66 43.6 11.91 1.66

1987 129,557 7,486 5.78 75.9 12.07 1.74

1986 90,243 3,156 3.50 34.5 10.61 2.48

1985 58,088 992 1.71 45.9 13.69 1.04

1984 40,939 344 0.84 48.6 12.23 0.48

1983 27,492 301 1.09 55.7 10.11 0.54

1982 18,109 577 3.19 38.6 9.61 2.11

1981 17,115 27 0.16 72.0 15.75 0.15

1980 14,935 224 1.50 21.1 8.43 1.25

1979 10,356 20 0.19 31.0 10.63 0.14

1978 8,946 119 1.33 60.0 8.38 0.59

Arithmetic Average 1978–2009 3.64 44.79 10.64 2.45

Weighted Average 1978–2009 4.56 3.09

a Excludes defaulted issues.

b Default loss rate adjusted for fallen angels is 9.3% in

2002, 1.82% in 2003, 0.59% in 2004, 1.56% in 2005, 0.039% in 2006, 0.20% in 2007, 3.42%

in 2008, and 7.38% in 2009.

Source: NYU Salomon Center.

Figure 15 lists the average recovery rate by seniority for 1978–2009. The recoveries

on all seniorities were significantly lower than the historical norms. In 2009, 29 of

the defaulting issues were senior secured, with an average recovery rate of 43.70%,

compared to a historical average of 57.8% (57.4% median). This is higher than the

third-quarter recovery of 38.74%, primarily due to a Nortek, Inc. senior secured

default of $750 million with a recovery rate of 101%. Two hundred twenty-six of the

issues were senior unsecured with an average recovery rate of 37.2%, compared to a

historical average of 37.7% (45.6% median). This rate was largely affected by the

low recovery rates of several large, defaulting issuers, including Abitibi Bowater,

General Motors, and Charter Communications.

There were 31 issues that were senior subordinated with an average recovery of

24.1%, compared to a historical average of 30.6% (32.7% median). Four were

subordinated with an average recovery of 12.6%, compared to a historical average of

30.9% (29.7% median). Seven were issued as either discount or zero coupon notes

with an average recovery of 16.8% compared to a historical average of 25.4%

(18.2% median). One hundred eight issues could not be priced. The historic 31-year

February 08, 2010 Altman High-Yield Bond Default and Return Report

17

median for all high-yield bond defaults stayed constant at 41.8%, while the

arithmetic average dropped slightly to 37.6%. These latter statistics are based on a

sample of over 2,500 defaults.

Figure 15. Weighted Average Recovery Rates on Defaulted Debt by Seniority per $100 Face

Amount, 1978–2009

Senior Secured Senior Unsecured

Senior

Subordinated Subordinated

Discount and

Zero Coupon

All

Seniorities

Default

Year No. % $ No. % $ No. % $ No. % $ No. % $ No. $

2009 29 10 43.70 226 76 37.22 31 10 24.06 4 1 12.57 7 2 16.84 297 36.13

2008 18 14 30.52 79 63 49.56 23 18 30.25 4 3 21.09 1 1 2.71 125 42.52

2007 10 36 87.24 10 36 47.70 6 21 63.98 2 7 46.53 0 0 0.00 28 66.65

2006 9 18 90.60 26 52 60.90 8 16 50.24 1 2 60.33 6 12 78.31 50 65.32

2005 67 54 76.50 44 36 45.88 7 6 32.67 0 0 0.00 5 4 74.21 123 61.10

2004 27 39 63.67 33 48 56.77 2 3 37.44 0 0 0.00 7 10 43.06 69 57.72

2003 57 28 53.51 108 53 45.40 29 14 35.98 1 0 38.00 8 4 32.27 203 45.58

2002 37 11 52.81 254 75 21.82 21 6 32.79 0 0 0.00 28 8 26.47 340 25.30

2001 9 3 40.95 187 67 28.84 48 17 18.37 0 0 0.00 37 13 15.05 281 25.62

2000 13 8 39.58 47 29 25.40 61 37 25.96 26 16 26.62 17 10 23.61 164 26.74

1999 14 11 26.90 60 47 42.54 40 31 23.56 2 2 13.88 11 9 17.30 127 27.90

1998 6 18 70.38 21 62 39.57 6 18 17.54 0 0 0.00 1 3 17.00 34 40.46

1997 4 16 74.90 12 48 70.94 6 24 31.89 1 4 60.00 2 8 19.00 25 57.61

1996 4 17 59.08 4 17 50.11 9 38 48.99 4 17 44.23 3 13 11.99 24 45.44

1995 5 15 44.64 9 27 50.50 17 52 39.01 1 3 20.00 1 3 17.50 33 41.77

1994 5 23 48.66 8 36 51.14 5 23 19.81 3 14 37.04 1 5 5.00 22 39.44

1993 2 6 55.75 7 22 33.38 10 31 51.50 9 28 28.38 4 13 31.75 32 38.83

1992 15 22 59.85 8 12 35.61 17 25 58.20 22 33 49.13 5 7 19.82 67 50.03

1991 4 3 44.12 69 44 55.84 37 24 31.91 38 24 24.30 9 6 27.89 157 40.67

1990 12 10 32.18 31 27 29.02 38 33 25.01 24 21 18.83 11 9 15.63 116 24.66

1989 9 12 82.69 16 21 53.70 21 28 19.60 30 39 23.95 76 35.97

1988 13 21 67.96 19 31 41.99 10 16 30.70 20 32 35.27 62 43.45

1987 4 13 90.68 17 55 72.02 6 19 56.24 4 13 35.25 31 66.63

1986 8 14 48.32 11 20 37.72 7 13 35.20 30 54 33.39 56 36.60

1985 2 7 74.25 3 11 34.81 7 26 36.18 15 56 41.45 27 41.78

1984 4 29 53.42 1 7 50.50 2 14 65.88 7 50 44.68 14 50.62

1983 1 13 71.00 3 38 67.72 4 50 41.79 8 55.17

1982 16 80 39.31 4 20 32.91 20 38.03

1981 1 100 72.00 1 72.00

1980 2 50 26.71 2 50 16.63 4 21.67

1979 1 100 31.00 1 31.00

1978 1 100 60.00 1 60.00

Total/Avg

.

389 15 57.82 1332 51 37.75 474 18 30.58 259 10 30.85 164 6 25.45 2,618 36.72

Median 57.42 45.64 32.73 29.69 18.25 41.77

Standard

Deva

18.21 13.35 14.17 17.46 20.37 13.89

a Standard deviations are calculated based on the yearly averages.

Sources: NYU Salomon Center from various dealer quotes.

Distressed Exchanges

Distressed exchanges usually represent a firm’s desperate attempt to avoid a formal

bankruptcy filing or a payment default on outstanding debt. They were particularly

―popular‖ in 2008 and 2009 as the successful outcome of Chapter 11 reorganizations

became very uncertain in a difficult D.I.P. and exit financing Chapter 11

environment. It is also possible, however, that a proposed distressed exchange could

represent a firm’s strategy to extract concessions from creditors when the firm has

little likelihood of failing, despite a stressed macroeconomic environment.

Distressed exchanges take several forms including a debt for debt, cash for debt,

equity for debt exchange, and various other forms that might include multiple new

February 08, 2010 Altman High-Yield Bond Default and Return Report

18

securities in exchange for the more immediate problem security. Over the last two

years, debt for debt exchanges were popular (61 of the 197 exchanged issues), as

well as cash for debt (57) and debt + cash for debt (58). Surprisingly, only 16

involved all or partial equity exchanges, perhaps a reflection of the reluctance on the

part of creditors to accept such a minority claim when the debtor is so weak.

Distressed exchanges (DEs) in 2009 accounted for about 37.8% of the defaulted

issuers (45 out of 119), but only 18.5% of the defaulted dollar amount. From 1984

through 2009, DEs accounted for about 10.6% of all defaulting issuers and 11.9% of

all defaulted dollar amounts (Figure 16). Despite the record number of DEs in 2009,

the pace at which DEs were being sought as a restructuring alternative seems to have

slowed toward the end of the year, as there was no significant exchange offer yet to

be completed.

Figure 16 indicates the ―popular‖ re-emergence of DEs over the last 24 months

compared to the last 25 years. Indeed, during this period, approximately 51% (59 of

116) of all DEs took place, and there is no guarantee that a DE will, in fact, save the

company from a subsequent bankruptcy. As we have compiled in a recent study,

about 46% of all DEs up to 2007 resulted in a subsequent Chapter 11 or Chapter 7

bankruptcy filing and 30% of the DE firms were acquired. The data would appear to

indicate a DE is oftentimes just a short-term fix (see Altman & Karlin, 20092). Note

that we have not tracked the eventual fate of the distressed exchanges in 2008 and

2009 since those firms have not had a significant enough post-exchange period for

our statistics to be relevant.

2 The Re-emergence of Distressed Exchanges in Corporate Restructurings, E. Altman and B. Karlin, NYU Salomon Center Working

Paper, 2009 (see E. Altman’s website) and published in The Journal of Credit Risk, Summer 2009.

February 08, 2010 Altman High-Yield Bond Default and Return Report

19

Figure 16. High Yield Bond Distressed Exchange (D/E) Default and Recovery Statistics,

1984–2009

Year

D/E

Defaults

($)

Total

Defaults ($)

D/E

Defaults

(%)

to Total

$

D/E

Defaults

(No. of

Issuers)

Total

Defaults

(No. of

Issuers)

D/E

Defaults

(%) to

Total No.

of Issuers

D/E

Recovery

Ratea

All

Default

Recovery

Ratea

Difference

Between D/E

& All

Default

Recovery

Rate

2009 22,905.90 123.823.79 18.5 45 119 37.8 42.68 36.13 6.55

2008 30,329.42 50,763.26 59.7 14 64 21.9 52.41 42.50 9.91

2007 146.83 5,473.00 2.7 1 19 5.3 85.17 66.65 18.52

2006 0.00 7,559.00 0.0 0 0 0 NA NA NA

2005 0.00 36,209.00 0.0 0 0 0 NA NA NA

2004 537.88 11,657.00 4.6 5 39 12.8 58.05 57.72 0.33

2003 1,034.94 38,451.00 2.7 7 86 8.1 78.52 45.58 32.94

2002 764.80 96,858.00 0.8 3 112 2.7 61.22 25.30 35.92

2001 1,267.60 63,609.00 2.0 5 156 3.2 33.12 25.62 7.50

2000 50.00 30,295.00 0.2 1 107 0.9 77.00 26.74 50.26

1999 2,118.40 23,532.00 9.0 6 98 6.1 65.39 27.90 37.49

1998 461.10 7,464.00 6.2 2 37 5.4 17.34 40.46 (23.12)

1997 0.00 4,200.00 0.0 0 0 0.0 NA NA NA

1996 0.00 3,336.00 0.0 0 0 0.0 NA NA NA

1995 0.00 4,551.00 0.0 0 0 0.0 NA NA NA

1994 0.00 3,418.00 0.0 0 0 0.0 NA NA NA

1993 0.00 2,287.00 0.0 0 0 0.0 NA NA NA

1992 0.00 5,545.00 0.0 0 0 0.0 NA NA NA

1991 76.00 18,862.00 0.4 1 62 1.6 31.30 40.67 (9.37)

1990 1,044.00 18,354.00 5.7 7 47 14.9 43.15 24.66 18.49

1989 548.90 8,110.00 6.8 7 26 26.9 44.53 35.97 8.56

1988 390.30 3,944.00 9.9 3 24 12.5 28.40 43.45 (15.05)

1987 33.60 7,486.00 0.4 2 15 13.3 40.70 66.63 (25.93)

1986 114.80 3,156.00 3.6 4 23 17.4 47.68 36.60 11.08

1985 323.30 992.00 32.6 2 19 10.5 55.04 41.78 13.26

1984 100.10 344.00 29.1 1 12 8.3 44.12 50.62 (6.50)

Totals/Averages $69,154.04 $580,279.05 11.9% 116 1099 10.6% 51.81b 42.00b 9.82

a Weighted-average recovery rates for each year.

b Arithmetic average of the weighted-average annual recovery rates;

only those years with DEs counted. The arithmetic average of each individual DE (116) for the entire sample period

was 48.24% and the average for the non-DE defaults (983 observations) was 36.72%.

Source: NYU Salomon Center.

Recovery Rates on Distressed Exchanges

Because DEs are not as dramatic a reflection of a firm’s distressed status as a

bankruptcy or nonpayment of cash interest on debt, one might expect the

recovery rate on DE defaults to be higher than other, more serious distressed

situations. Of course, one reason for the larger recoveries in DEs is lenders need

to be offered a ―premium‖ in order to be persuaded to participate in the

exchange.

Figure 16 shows the arithmetic average recovery rate on all DE defaults was 51.8%

for 1984–2009, compared to 42.0% for all defaults, and 36.7% for all non-DE

defaults. In 2008, DEs recovered 52.2%, while non-DE defaults recovered only

27.1%. As the 2009 recovery rate on DEs equaled 42.7% versus 36.1% on all

defaults, the spread has widened significantly since earlier this year, particularly the

first quarter, when the recovery on all defaults was higher than on DEs.

In Figure 17, we calculate a difference in means test between the arithmetic average

recovery rate (48.2%) on the 116 DE issuers (269 issues) during 1984–2009 and the

average recovery rate on all non-DE defaults (36.7%) of the same period. We found

that given the above, the DE recovery rate is significantly higher (t = 7.49) at the 1%

confidence level. It is not surprising that bondholders will choose, in many instances,

to accept a recovery with certainty from a DE, rather than take the chance of holding

February 08, 2010 Altman High-Yield Bond Default and Return Report

20

out for an uncertain — and likely lower — recovery in bankruptcy (see below). Our

results do not include data for situations where a DE offer is rejected.

Figure 17. Difference in Means Test Between Recovery Rates: All

Nondistressed Exchange Defaults Versus Distressed Exchanges (D/E),

1984–2009

All Defaults Excluding D/E

(Issues)

Distressed Exchange

(Issues)

Sample Size 2239 269

Mean Recovery Rate 36.72 48.24

Standard Deviation 25.95 23.59

Variance 673.63 556.27

t-testa 7.48755

a

Sources: NYU Salomon Center, and authors’ compilation.

In Figure 18, we calculate a difference in means test between the weighted average

recovery rate on the announcement date of a DE versus the completion date for both

2008 and 2009. Of the 42 defaulted issues in 2008 due to a DE, in which prices were

available for both the announcement and completion dates, the weighted average

recovery was approximately 13 percentage points higher on the completion date.

Though completion date recoveries also proved to be higher in 2009, they were much

less so, with only a 4.9% difference in pricing between the two dates. So, the prices

of the distressed exchange bonds were significantly higher at the completion of the

exchange than when it was first announced based on the 2008 sample, but the

difference was much less significant in the 2009 cohort. Overall, the completion date

price was higher than the announcement date in 79 of the 148 issues, just over 50%

(53.4%) of the cases.

Figure 18. Distressed Exchange Weighted Average Recovery Rates:

Announcement Date versus Completion Date, 2008–2009

Year

# of

Observations Announcement Date

Completion

Date Difference t-test

2008 42 42.68 55.64 (12.97) 2.69469a

2009 106 36.51 41.41 (4.91) 1.44079b

a Significant at the .01 level. b Significant at the .10 level.

Source: NYU Salomon Center.

February 08, 2010 Altman High-Yield Bond Default and Return Report

21

Liquidation Recoveries

As we, (Altman & Karlin (2009)3), and others have discussed, the recent credit crisis

has heightened the risk that a Chapter 11 filing could result in a failed reorganization,

ultimately culminating in a liquidation of assets and subsequent payment of proceeds

to creditors. As noted earlier, the reduced availability of either debtor-in-possession

(D.I.P.) or exit financing makes a successful reorganization less likely. Even under

more normal conditions, firms may have little or no prospect of generating sufficient

cash flows to cover even a reduced debt burden and, in essence, the liquidation value

of the enterprise is deemed greater than the going-concern value. Given these

prospects, a key question for major stakeholders, particularly creditors, is the likely

recovery given liquidation, and how that value compares with the debt price just after

the filing of the initial Chapter 11. These are the questions we will now examine.

Liquidating Chapter 7’s versus Chapter 11’s4

Liquidations after an initial Chapter 11 filing can take two main forms – either a

conversion to Chapter 7 or a liquidating Chapter 11. The primary differences

between these two forms may affect the expected recovery for creditors from the

estate based on the revenues, timing, costs, and the administration of the liquidation

process. The liquidating Chapter 11 is more popular with some debtors because the

business continues with the incumbent board and management remaining as the

―debtor-in-possession‖ to manage the liquidation, as opposed to the court appointed

Trustee in a Chapter 7. The latter has the task of liquidating the estate as

expeditiously as possible, with limited powers to operate the business.

To illustrate some differences, in a Chapter 11 case, commercial real property leases

may be assumed or rejected up to 210 days (120 days with a possible 90 day

extension) after the initial filing, while in a Chapter 7 they must be assumed or

rejected within 60 days. Thus, a Chapter 7 Trustee is more likely to expedite a sale

process and not explore alternative options to maximize value. The Trustee is usually

paid a percentage (not to exceed 3%) of the total amount dispersed. As such, creditor

distributions will be reduced by the fee, although the proceeds are likely to come

earlier than in a liquidating Chapter 11.

On the other hand, since a committee of unsecured creditors is usually not appointed

in a Chapter 7, this process is not burdened by the delay of having all decisions

reviewed by the committee as well as the need to negotiate with the unsecured

creditors to garner their votes for liquidation without the threat of objections and

lawsuits – not to mention the likely cost of these objections and delays usually borne

by the estate. Another potentially significant cost of the Chapter 11 process is the

professional fees incurred by all constituencies in drafting and reviewing the plan

and disclosure statement, as well as for hearings and objections. A further expense of

the Chapter 11 process is the payment in full, in cash, of any administrative and

priority claims before any funds are distributed to creditors.

3E. Altman and B. Karlin (2009), ―Defaults and Returns in the High Yield Bond Market: The Year 2008 in Review and Outlook‖,

NYU Salomon Center Special Report, February.

4 Thanks to Daniel Kamensky of Paulson & Co. for his helpful comments on the differences between these two processes.

February 08, 2010 Altman High-Yield Bond Default and Return Report

22

In essence, the creditors need to weigh the benefits of greater control of the process

under the Chapter 11 liquidation versus the additional time and expenses. Many

creditors, however, are not experienced enough to do this tradeoff analysis. While a

proceeding under Chapter 11 may involve more costs and delays, limited power to

consider alternatives in a Chapter 7 will oftentimes swing the decision in favor of the

Chapter 11 liquidation, thereby making it more popular, especially when creditors

are more sophisticated and more is at stake.

Indeed, our research shows that over the 20-year period 1990-2009, 92 relatively

large companies with publicly held bonds outstanding liquidated under Chapter 11,

while just 28 companies converted first to a Chapter 7 and then liquidated (about a

3.3:1 ratio). If we expand our sample to include all Chapter 11 filings, regardless if

publicly held bonds were outstanding, the number of Chapter 11 liquidations

increases to 351 vs. 298 Chapter 7 conversions (a 1.2:1 ratio) over the same 20-year

period.5 So, it appears that larger firms with more complex capital structures prefer

the Liquidating Chapter 11 alternative more frequently than do all debtors in

bankruptcy. Figure 19 shows the frequency of Chapter 11 liquidations and Chapter 7

conversions, by year, over the period 1990-2009, with a further distinction being

whether or not the firms had publicly traded bonds outstanding.

Figure 19. Chapter 11 Liquidations versus Chapter 7 Conversions, By

Year and Whether Publicly Owned Bonds Were Outstanding (Number of

Firms), 1990–2009

Year

All Chapter 11

Liquidations

All Chapter 7

Conversions

Chapter 11

Liquidations

w/Bonds Outstanding

Chapter 7

Conversions w/Bonds

Outstanding

2009 20 22 5 2

2008 22 18 3 3

2007 17 9 5 0

2006 19 16 4 2

2005 25 13 7 1

2004 49 12 11 1

2003 66 27 14 4

2002 34 42 9 5

2001 17 33 7 5

2000 25 19 10 4

1999 11 16 2 1

1998 5 12 1 0

1997 4 10 1 0

1996 9 6 3 0

1995 3 9 1 0

1994 9 5 4 0

1993 6 9 1 0

1992 7 8 2 0

1991 1 8 1 0

1990 2 4 1 0

Total 351 298 92 28

Sources: New Generation Research (Boston) and NYU Salomon Center Default Database.

Recoveries

Several key questions are critical for existing creditors and potential distressed debt

investors when a company defaults and files for the right to reorganize under Chapter

5 Thanks to New Generation Research, Boston, MA, for the relevant data accumulations. Data in the first ten years in our time series

(1990-1999) are less certain, especially the Chapter 7 conversions.

February 08, 2010 Altman High-Yield Bond Default and Return Report

23

11. First, and foremost, is whether or not the price of debt securities will increase

during and after the reorganization. Key to that conclusion is the likelihood that the

firm will emerge from bankruptcy as a going concern, and whether the old debt

securities will be exchanged for valuable new debt, equity claims, cash, or a

combination of the aforementioned. Most studies, including Altman and Eberhart

(1994)6 and Keisman (2004)

7, have shown that the average rate of return between the

initial default and the subsequent price at the time of emergence from the

reorganization results in an annualized return between low single digits and 20%-

30%, depending upon the seniority and the sample period. Generally, senior debt

securities do best with significant positive annual returns of 20-30%.

If the company is not able to successfully reorganize, positive returns in the post-

bankruptcy period are less likely since values will no longer be based on a going-

concern concept. Regardless of the outcome, distressed investors usually assume a

―floor‖ value given a downside scenario, and, certainly, liquidation qualifies as an

extremely negative scenario. Also worth noting is the opportunity cost of lost

potential returns given the sale of the securities at default and investment of the

proceeds in alternative securities instead of holding onto the debt. For example,

Altman and Eberhart assumed that the appropriate ―opportunity cost‖ was the return

on an investment in a portfolio of high-yield, junk-bond securities.

We have analyzed a sample of bonds from companies that filed for reorganization

under Chapter 11 and eventually liquidated under a Chapter 7 conversion or a

liquidating Chapter 11. The number of Chapter 7 conversions or Chapter 11

liquidations over the 20-year period 1990-2009 for firms with publicly held bonds

outstanding, for which we had prices at the time of filing, is 87, with 141 individual

issues. Of these, we were able to trace the price of the bonds just prior to liquidation

on 72 of these issues (42 firms, see Figure 20). The average price of the 72 issues at

the time of the initial filing was $20.18 of par value, compared to an average price of

just $13.22 upon liquidation. The difference of just less than seven percentage points

is extremely significant (t-test = 7.1). The average price of the 141 issues upon filing

is essentially the same ($20.65) as the smaller sample of 72 ($20.18) that we were

able to find prices for both at the time of filing and at liquidation. Of the 72

securities, all but 12 (six firms) had a lower price at liquidation than at the time of the

initial filing.

The negative performance of liquidating companies is far more clear for those firms

that converted to a Chapter 7 than those liquidating under a Chapter 11, and the

security prices of the Chapter 7 firms were also considerably lower at the time of the

initial filing. This implies that those firms that eventually liquidate under a Chapter 7

conversion are in far worse shape with fewer reorganization prospects than those

who eventually do liquidate, but under a Chapter 11 process. For example, the

average price of the 15 bonds of Chapter 7 companies at the time of filing is $8.19

compared to just $1.91 upon conversion to Chapter 7 (t = 2.94). The comparable

statistics for the 57 Chapter 11 liquidations were $23.93 and $16.76, respectively.

6 E. Altman and A. Eberhart (1994), ―Do Seniority Provisions Protect Bondholders’ Investments?‖, Journal of Portfolio

Management, Summer.

7 D. Keisman (2004), ―Ultimate Recovery Rates on Bank Loan and Bond Defaults‖, Loss Stats, S&P (NY).

February 08, 2010 Altman High-Yield Bond Default and Return Report

24

While the difference in means prices ($7.17) of the latter is not trivial, the mean

difference is barely significant at the 10% level.

Finally, it is clear that the market understood that those companies that eventually

liquidated were in significantly poorer condition than the average company that

defaults. Indeed, the average price of corporate bonds at the time of default,

approximately $36.78, is significantly higher than the average price ($20.65) of our

141-issue sample that eventually resulted in liquidation. Still, not surprisingly,

despite this relatively low price at filing, the portfolio of liquidating issuers did

poorly between the filing and liquidation dates, indicating that the market

overestimated the prices at the time of filing. This would most likely be due to the

perceived upside potential if the firm eventually overcomes its adversity and either

emerges from the reorganization as a going concern or is sold in a 363 sale or total

enterprise transaction.9

Figure 20. Recovery Rates (Wgt. Prices) on Bonds of Companies That

Filed a Chapter 11 Petition and Later Converted to a Chapter 7 or a

Liquidating Chapter 11, 1990–2009

No. of Bonds

Wgt. Avg. Price at

Filing (F) Chapter 11

Wgt. Avg. Price at

Liquidation (L) t-test

All Liquidations

(Std. Deviation)

72 $20.18

(17.69)

$13.22

(28.83)

1.75c

Chapter 11 Liquidations

(Std. Deviation)

57 $23.93

(19.49)

$16.76

(30.90)

1.48c

Chapter 7

Conversion/Liquidations

(Std. Deviation)

15

$8.19

(7.40)

$1.91

(3.69)

2.94b

a

b Significant at the .01 level. c Significant at the .10 level.

Source: Author Compilation from data supplied from New Generation Research (Boston) and the NYU Salomon Center (NY) Default

Database.

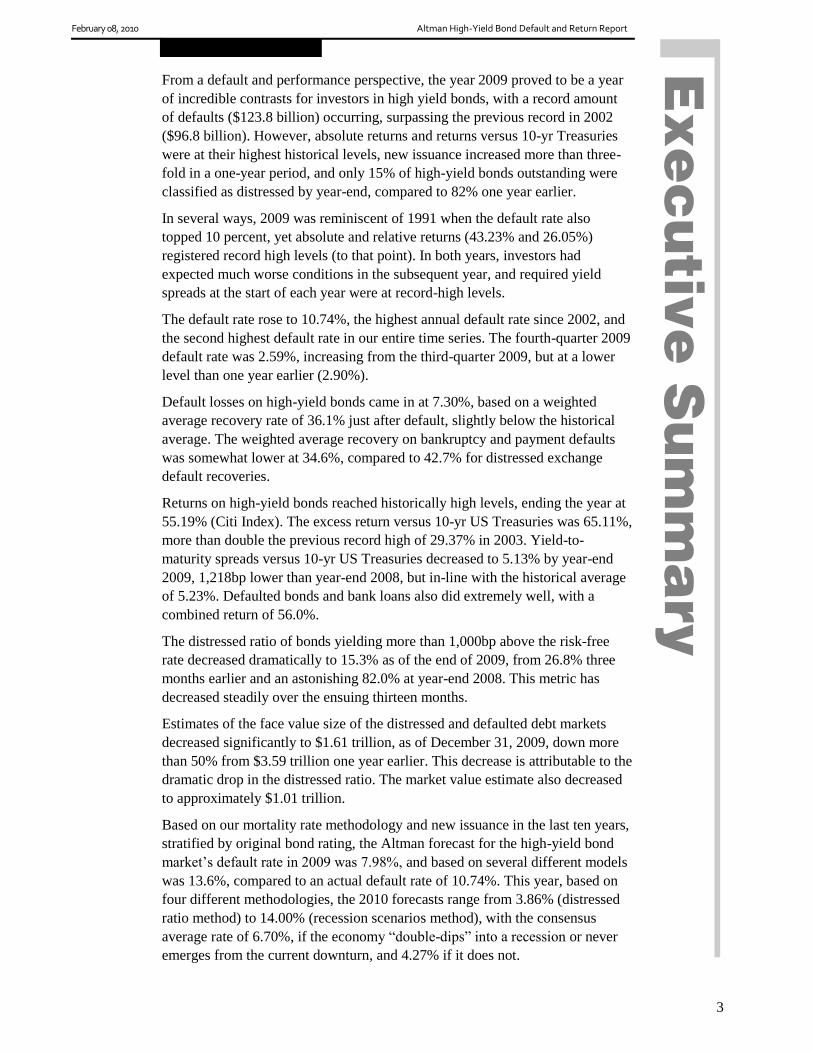

Forecast Recovery Versus Actual

The 2009 weighted-average recovery rate of 36.1% was above our linear or non-

linear regression default/recovery rate forecasting models’ predictions (Figure 21).10

We would have expected the average recovery rate to be closer to the 26%-29%

range, based upon the model used. As noted earlier, the weighted-average recovery

rate was impacted positively (i.e. considerably higher recoveries) by the CIT and

Charter Communications filings.

8 Based on over 2,600 defaulted bond observations for the period 1978-2009 (Figure 15, earlier).

9 We have not assessed the ultimate value of the bonds given a 363 or total enterprise sale.

10 ―The Link Between Default and Recovery Rates: Theory, Empirical Results and Implications,‖ Altman, Brady, Resti and Sironi,

Journal of Business, November 2005.

XF XL

t =

+

t =

√ Var XF Var XL

NF NL

February 08, 2010 Altman High-Yield Bond Default and Return Report

25

Figure 21. Recovery Rate/Default Rate Association, Dollar Weighted

Average Recovery Rates to Dollar Weighted Average Default Rates,

1982–2009

2005

2004

2003

20022001

20001999

1998

19971996

19951994

1993

1992

1991

1990

1989

1988

1987

1986

1985

1984

1983

1982

20062007

2008

2009

y = -2.3137x + 0.5029

R2 = 0.5361

y = -0.1069Ln(x) + 0.0297

R2 = 0.6287

y = 30.255x2 - 6.0594x + 0.5671

R2 = 0.6151

y = 0.1457x-0.2801

R2 = 0.6531

10%

20%

30%

40%

50%

60%

70%

0% 2% 4% 6% 8% 10% 12% 14%

Rec

ove

ry R

ate

Recovery Rate/Default Rate AssociationDollar Weighted Average Recovery Rates to Dollar Weighted Average Default Rates

(1982-2009)

Regression equations are based on data from 1982–2003, with later years data points

inserted to show the model’s effectiveness.

Sources: “The Link Between Default and Recovery Rates: Theory, Empirical Results and

Implications,” Altman, Brady, Resti, and Sironi, Journal of Business, November 2005, and

NYU Salomon Center.

Related Recovery Statistics

The recovery rate (based on price just after default) on corporate high-yield bond

defaults has a fairly high variance in terms of the wide spectrum of possible outcomes,

with a standard deviation of about 25%. Figure 22 shows the frequency distribution of

individual issue recovery rates on over 2,500 corporate bond defaults of all seniorities

since 1971. Note that the modal value is only in the 10–20% range, even though our

historical average recovery rate range is 35–40%.

Figure 22. Corporate Bond Default Recovery Rate Frequency (Based on

Number of Issues 1971–2009)

0

100

200

300

400

500

600

0-10 10-20 20-30 30-40 40-50 50-60 60-70 70-80 80-90 90-100 >100

Recovery Rate Range (%)

Freq

uenc

y

Number of Observations = 2,547.

Source: NYU Salomon Center Default Database.

February 08, 2010 Altman High-Yield Bond Default and Return Report

26

Figure 23 shows the average price at default based on the number of years after

issuance. Although we observe some aging effect with the recovery rate increasing as

the years to default increases, there is not a great deal of difference between the first

and fifth years (32–38%) or between the sixth through ninth years (40–42%). The latter

period is more likely to comprise fallen angel defaults than the former. We note years

seven through nine showed a decrease in recoveries in 2009, compared to 2008,

returning to more normal values.

Figure 23. Average Price at Default by Number of Years After

Issuance (1971–2009)

Years to Default No. of Observations Average Price ($)

1 179 33.44

2 381 34.11

3 472 32.39

4 386 37.68

5 304 37.83

6 261 42.40

7 164 41.79

8 96 42.07

9 63 40.15

10 198 35.06

All 2,504 36.64

Source: NYU Salomon Center.

Figure 24 shows the recovery rate by original rating for the entire corporate bond

default database over the last 39 years. As expected, the higher the original rating,

the greater the average recovery rate, but only in the investment-grade original rating

range — that is, among fallen angels. Once below BBB, the weighted-average

recovery rate varies narrowly, 34–38%. However, we observe the median recovery

rates follow a continuous drop, as the original rating falls, except between the B and

CCC original ratings (both 29%).

Figure 24. Average Price after Default by Original Bond Rating,

1971-2009

Rating

No. of

Observatio

ns

Average

Price ($)

Weighted

Price ($)

Median

Price ($)

Std.

Dev. ($)

Minimum

Price ($)

Maximum

Price ($)

AAA 14 82.55 92.87 95.00 21.92 32.00 106.13

AA 30 65.68 76.84 60.00 26.69 17.80 103.00

A 247 48.45 46.13 44.88 27.36 2.00 100.00

BBB 470 40.16 33.32 39.00 23.89 1.00 103.00

BB 272 38.51 34.71 36.00 23.49 1.00 107.75

B 1294 34.27 32.92 29.00 24.82 0.02 112.00

CCC 298 37.27 35.68 29.00 29.00 0.13 106.75

Total 2625 38.12 36.06 33.00 26.02 0.02 112.00

Source: NYU Salomon Center Default Database.

Earlier we showed that seniority makes a large difference in expected recoveries. It is

true that the likelihood is greater that an investment-grade bond at issuance will have

senior priority (secured or unsecured) than one would expect from noninvestment-

grade original issue bonds. Figure 25 shows the recovery rate by seniority,

contingent upon if the original issue was rated investment grade.

February 08, 2010 Altman High-Yield Bond Default and Return Report

27

Figure 25. Recovery Rates by Seniority and Original Rating, Corporate Bond Defaults (By

Issue, 1971–2009)

Seniority Original Rating

No. of

Issues

Mean Price

($)

Weighted

Price ($)

Median Price

($) STD

Minimum

Price ($)

Maximum

Price ($)

Senior Secured

Investment Grade

145 53.21 57.23 50.50 27.02 3.00 106.13

Non-Investment Grade

270 43.83 44.29 39.00 29.19 1.00 106.75

All 460 46.64 46.99 43.50 28.39 0.05 106.75

Senior Unsecured

Investment Grade

482 43.69 40.28 42.25 25.29 2.00 100.50

Non-Investment Grade

650 36.18 33.10 31.15 24.25 0.02 100.00

All 1243 39.95 36.70 35.00 24.99 0.02 100.50

Senior Subordinated

Investment Grade

16 37.10 34.29 27.31 27.48 1.00 83.75

Non-Investment Grade

432 32.74 29.32 27.37 24.31 0.13 107.75

All 476 32.14 29.30 27.00 24.30 0.13 107.75

Subordinated Investment Grade

21 22.52 6.43 10.00 27.59 2.00 103.00

Non-Investment Grade

204 32.54 29.64 28.92 22.68 1.00 112.00

All 238 31.45 21.97 28.42 23.05 1.00 112.00

Discount Investment Grade

1 13.63 13.63 13.63 13.63

Non-Investment Grade

103 27.48 26.29 17.31 25.16 0.42 102.50

All 130 26.84 26.31 18.00 23.51 0.42 102.50

Source: NYU Salomon Center Default Database.

From Figure 25, we see considerably higher recoveries between investment-grade

and noninvestment-grade bonds for senior secured (53.2% versus 43.8%) and senior

unsecured (43.7% versus 36.2%), less of a difference for the senior subordinated

class (37.1% versus 32.2%), and the reverse for the subordinated class. Likewise, as

seniority is reduced, we see a reduction in recoveries for the investment-grade issues,

but not much difference for the noninvestment-grade securities.

Finally, in Figure 26, we break down recoveries by seniority for different major

industrial sectors. The sectors are the same as itemized earlier when we observed the

incidence of defaults per industrial sectors (Figures 8 and 9). The overall weighted-

average recovery rates are highest for energy (51.9%), utilities (51.8%), and financial

services (47.6%), and lowest for general manufacturinge (29.9%), communications

(28.0%), and auto/motor carrier (25.7%). The rest vary between 32–45%.

February 08, 2010 Altman High-Yield Bond Default and Return Report

28

Figure 26. Recovery Rates by Industry and Seniority (1971–2009)

Industry Seniority

No. of

Issues

Mean Price

($)

Weighted

Price ($)

Median

Price ($) STD

Minimum Price

($)

Maximum

Price ($)

Auto/Motor Carrier Senior Secured 16 30.78 24.96 24.00 24.46 2.71 92.00

Senior Unsecured 74 30.09 26.37 23.91 22.86 4.00 93.60

Senior Sub 20 27.26 21.77 23.50 19.93 3.00 71.00

Subordinated 4 34.28 25.71 27.00 21.25 18.00 65.13

Senior Sub +Sub 24 28.43 22.21 25.00 19.85 3.00 71.00

All 114 29.84 25.75 25.00 22.31 2.71 93.60

Conglomerates Senior Unsecured 3 44.92 47.94 53.38 14.65 28.00 53.38

Senior Sub 1 71.00 71.00 71.00 71.00

Subordinated 2 11.50 15.19 11.50 9.19 5.00 18.00

Senior Sub +Sub 3 31.33 22.52 18.00 34.96 5.00 71.00

All 6 38.13 40.93 40.69 25.10 5.00 71.00

Energy Senior Secured 37 63.25 65.24 64.00 32.44 2.00 104.50

Senior Unsecured 86 44.76 44.99 43.50 21.90 6.75 86.38

Senior Sub 28 38.15 46.60 34.88 23.97 1.00 107.75

Subordinated 26 25.38 25.39 21.13 12.19 9.50 55.00

Discount 1 45.26 45.26 45.26 45.26

Senior Sub +Sub 54 32.00 42.22 27.50 20.11 1.00 107.75

All 178 44.73 51.86 38.94 26.20 1.00 107.75

Financial Services Senior Secured 16 34.44 27.34 23.94 24.31 14.00 94.00

Senior Unsecured 156 49.88 56.01 52.13 28.29 0.02 100.00

Senior

Subordinated

20 31.97 28.85 28.00 24.07 1.00 92.00

Subordinated 28 22.43 9.11 6.00 26.78 1.00 103.00

Senior Sub +Sub 48 26.41 13.05 23.00 25.86 1.00 103.00

All 220 43.63 47.65 39.25 29.14 0.02 103.00

Leisure & Senior Secured 37 50.69 55.86 52.50 25.98 0.05 106.00

Entertainment Senior Unsecured 44 37.66 30.66 27.86 26.79 3.75 100.00

Senior Sub 40 31.07 27.75 23.00 25.34 3.00 99.00

Subordinated 21 46.17 55.78 36.50 29.79 7.00 112.00

Discount 2 18.88 20.74 18.88 9.73 12.00 25.76

Senior Sub +Sub 61 36.27 33.60 29.00 27.67 3.00 112.00

All 144 40.16 38.02 35.00 27.40 0.05 112.00

General Mfg Senior Secured 78 40.75 41.26 39.22 25.64 1.75 106.75

Senior Unsecured 200 33.40 26.61 29.00 21.93 0.25 99.50

Senior Sub 142 31.69 29.04 27.75 23.84 0.75 106.00

Subordinated 65 34.95 27.99 32.00 21.15 2.00 90.88

Discount 12 17.90 27.17 8.72 23.25 0.75 66.50

Senior Sub +Sub 207 32.71 28.76 29.00 23.03 0.75 106.00

All 497 33.89 29.87 29.50 23.27 0.25 106.75

Healthcare Senior Secured 2 91.25 97.38 91.25 10.25 84.00 98.50

Senior Unsecured 12 46.90 49.61 55.50 15.38 8.75 56.00

Senior Sub 33 24.50 21.06 15.50 23.11 0.13 86.00

Subordinated 10 23.77 17.57 23.50 13.41 4.75 39.00

Discount 2 21.05 27.07 21.05 18.32 8.09 34.00

Senior Sub +Sub 43 24.33 20.50 18.00 21.11 0.13 86.00

All 59 31.08 31.72 29.00 24.27 0.13 98.50

Misc. Industries Senior Secured 31 44.24 46.49 43.50 27.26 5.00 93.50

Senior Unsecured 59 51.92 54.99 56.09 25.97 8.00 99.00

Senior Sub 33 35.16 36.40 27.81 26.28 1.00 96.00

Subordinated 8 38.67 17.59 34.07 23.53 4.00 88.00

Discount 5 4.37 4.27 4.03 2.79 0.75 8.00

Senior Sub +Sub 41 35.85 35.12 29.63 25.52 1.00 96.00

All 136 43.58 45.95 40.00 27.46 0.75 99.00

Real Estate Senior Secured 6 50.58 52.55 58.75 34.50 3.00 82.50

& Construction Senior Unsecured 56 47.05 39.70 44.25 22.15 6.00 100.50

Senior Sub 29 25.43 18.22 15.50 25.74 2.00 95.50

Subordinated 11 35.98 25.21 21.88 33.65 2.00 98.25

Discount 3 13.61 20.97 13.63 12.40 1.21 26.00

Senior Sub +Sub 40 28.33 19.37 17.69 28.08 2.00 98.25

All 105 39.16 32.00 32.25 26.84 1.21 100.50

February 08, 2010 Altman High-Yield Bond Default and Return Report

29

Figure 26. Recovery Rates by Industry and Seniority (1971–2009) (Continued)

Industry Seniority

No. of

Issues

Mean Price

($)

Weighted

Price ($)

Median

Price ($) STD

Minimum Price

($)

Maximum

Price ($)

Retailing Senior Secured 28 45.17 38.80 43.50 24.74 2.50 90.00

Senior Unsecured 154 45.20 45.10 43.50 20.38 0.23 98.50

Senior Sub 74 31.89 28.83 25.25 22.68 0.50 94.00

Subordinated 36 27.27 25.44 20.00 18.96 3.38 70.00

Discount 3 35.85 35.51 20.00 33.26 13.48 74.06

Senior Sub +Sub 110 30.38 28.11 23.00 21.55 0.50 94.00

All 295 39.57 36.24 40.00 22.44 0.23 98.50

Communications Senior Secured 61 37.53 36.70 32.00 31.83 1.00 99.00

& Media Senior Unsecured 299 30.43 26.12 24.00 22.74 1.00 95.75

Senior Sub 48 38.05 33.40 34.00 26.16 0.13 97.00

Subordinated 17 32.00 37.86 20.00 25.84 6.50 89.00

Discount 101 28.82 26.59 20.00 23.55 0.42 102.50

Senior Sub +Sub 65 36.47 33.77 30.00 26.01 0.13 97.00

All 526 31.69 28.05 24.00 24.63 0.13 102.50

Transport (Non-

auto)

Senior Secured 121 50.23 60.59 44.00 26.49 2.00 106.13

Senior Unsecured 73 29.39 27.65 24.00 19.05 6.00 99.00

Senior Sub 6 41.71 25.24 36.75 25.99 13.00 83.75

Subordinated 8 29.89 20.50 26.06 21.63 10.00 65.50

Senior Sub +Sub 14 34.96 22.14 33.63 23.42 10.00 83.75

All 208 41.89 44.74 34.25 25.82 2.00 106.13

Utilities Senior Secured 27 56.57 39.27 56.25 24.69 2.00 99.88

Senior Unsecured 27 78.34 65.03 84.00 18.34 28.88 98.63