Embed Size (px)

Citation preview

New U.S. Reporting Requirements for Foreign-Owned Disregarded Entities

Presented to STEP Miami

Carlos A. Somoza and Maria Toledo Kaufman Rossin January 26, 2017

2

Agenda

– Reporting under IRC Section 6038A

– Federal tax treatment of domestic LLCs

– Final Regulations issued December 13, 2016 • Form 5472 filing requirement

• Record-keeping requirement

• Examples

• Penalties

• Effective date – Questions

REPORTING UNDER IRC SECTION 6038A

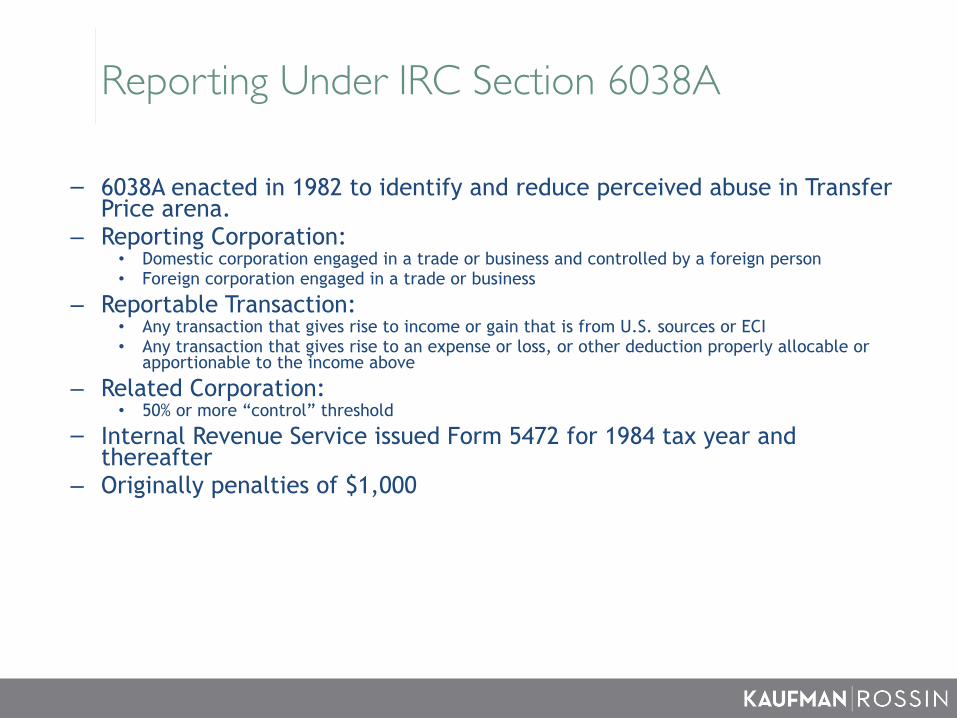

Reporting Under IRC Section 6038A

– 6038A enacted in 1982 to identify and reduce perceived abuse in Transfer Price arena.

– Reporting Corporation: • Domestic corporation engaged in a trade or business and controlled by a foreign person • Foreign corporation engaged in a trade or business

– Reportable Transaction: • Any transaction that gives rise to income or gain that is from U.S. sources or ECI • Any transaction that gives rise to an expense or loss, or other deduction properly allocable or

apportionable to the income above – Related Corporation:

• 50% or more “control” threshold

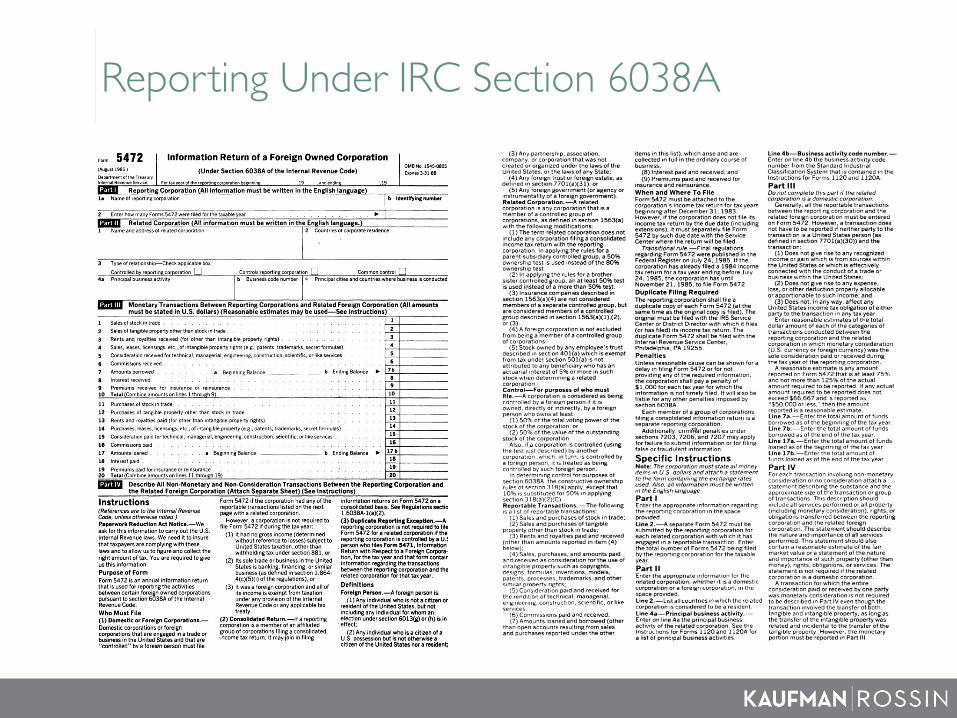

– Internal Revenue Service issued Form 5472 for 1984 tax year and thereafter

– Originally penalties of $1,000

Reporting Under IRC Section 6038A

FEDERAL TAX TREATMENT OF DOMESTIC LLCS

Federal Tax Treatment of Foreign-Owned Domestic LLC

– Treatment of Business Entities:

• Two or more members: Corporation or Partnership • One member: Corporation or Disregarded

– Default Treatment of Limited Liability Company:

• Two or more members: Partnership

• One member: Disregarded

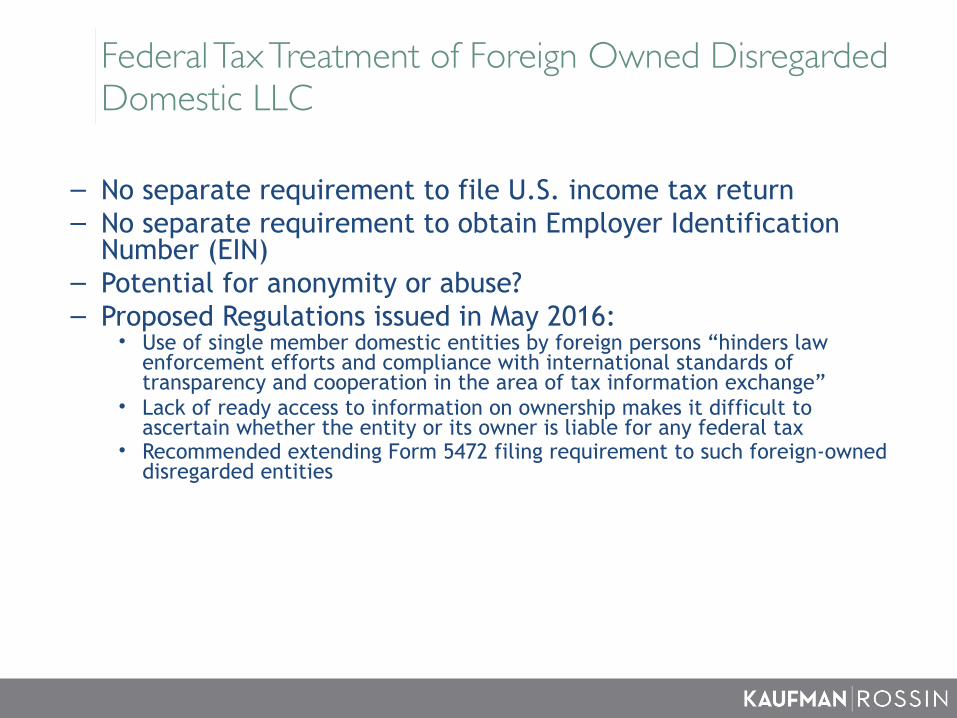

Federal Tax Treatment of Foreign Owned Disregarded Domestic LLC

– No separate requirement to file U.S. income tax return

– No separate requirement to obtain Employer Identification Number (EIN)

– Potential for anonymity or abuse?

– Proposed Regulations issued in May 2016:

• Use of single member domestic entities by foreign persons “hinders law enforcement efforts and compliance with international standards of transparency and cooperation in the area of tax information exchange”

• Lack of ready access to information on ownership makes it difficult to ascertain whether the entity or its owner is liable for any federal tax

• Recommended extending Form 5472 filing requirement to such foreign-owned disregarded entities

FINAL REGULATIONS

Final Regulations

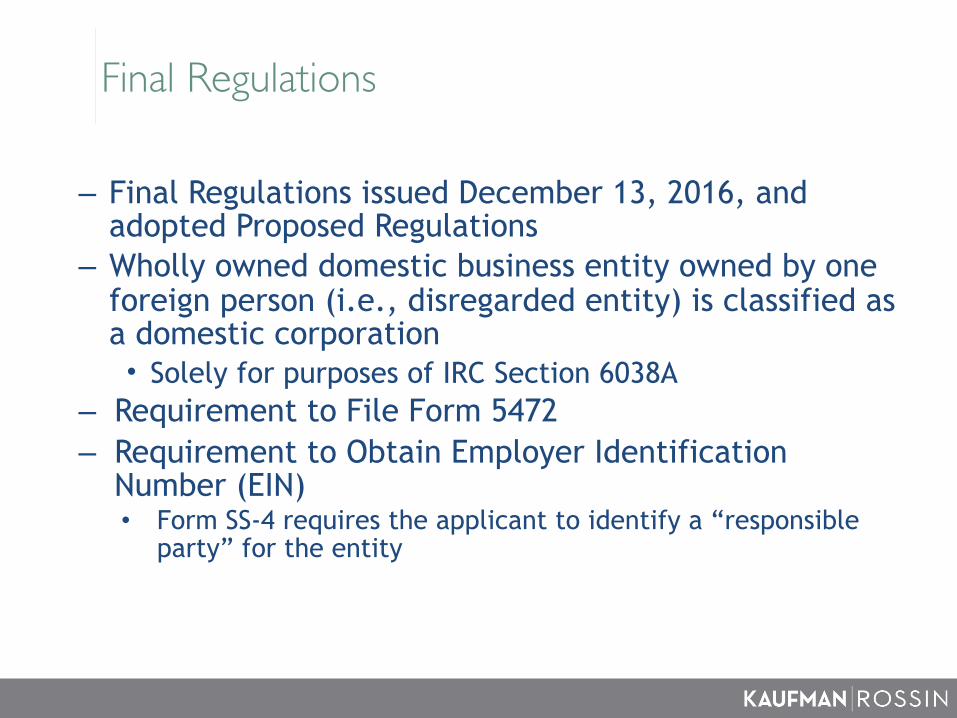

– Final Regulations issued December 13, 2016, and adopted Proposed Regulations

– Wholly owned domestic business entity owned by one foreign person (i.e., disregarded entity) is classified as a domestic corporation

• Solely for purposes of IRC Section 6038A – Requirement to File Form 5472

– Requirement to Obtain Employer Identification Number (EIN)

• Form SS-4 requires the applicant to identify a “responsible party” for the entity

What Is a Reportable Transaction?

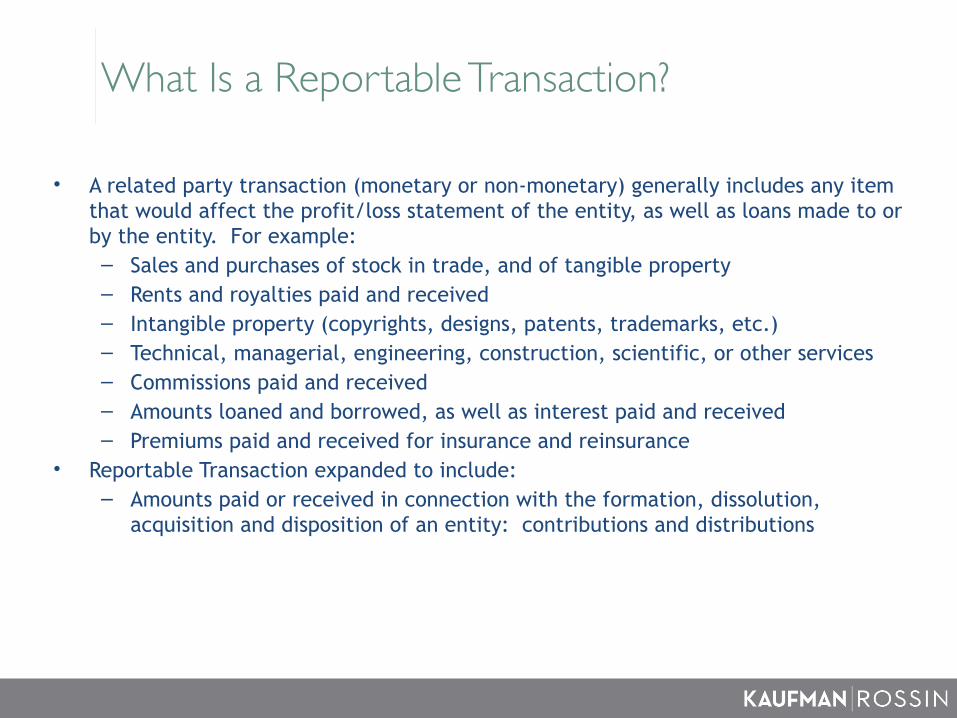

• A related party transaction (monetary or non-monetary) generally includes any item that would affect the profit/loss statement of the entity, as well as loans made to or by the entity. For example: – Sales and purchases of stock in trade, and of tangible property – Rents and royalties paid and received – Intangible property (copyrights, designs, patents, trademarks, etc.) – Technical, managerial, engineering, construction, scientific, or other services – Commissions paid and received – Amounts loaned and borrowed, as well as interest paid and received – Premiums paid and received for insurance and reinsurance

• Reportable Transaction expanded to include: – Amounts paid or received in connection with the formation, dissolution,

acquisition and disposition of an entity: contributions and distributions

What Is a Related Party?

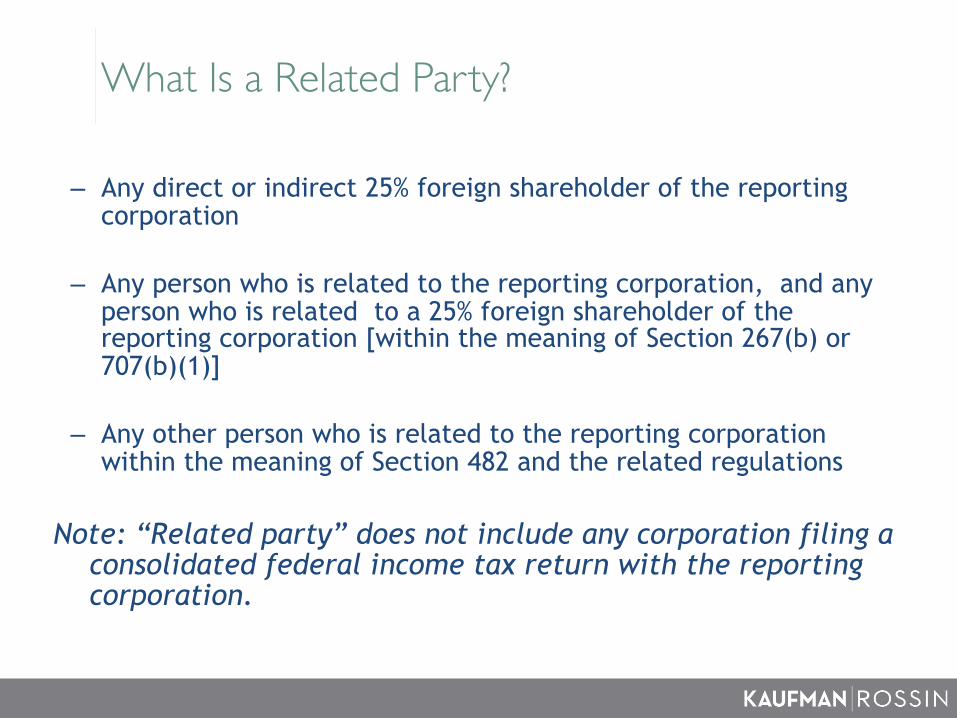

– Any direct or indirect 25% foreign shareholder of the reporting corporation

– Any person who is related to the reporting corporation, and any person who is related to a 25% foreign shareholder of the reporting corporation [within the meaning of Section 267(b) or 707(b)(1)]

– Any other person who is related to the reporting corporation within the meaning of Section 482 and the related regulations

Note: “Related party” does not include any corporation filing a consolidated federal income tax return with the reporting corporation.

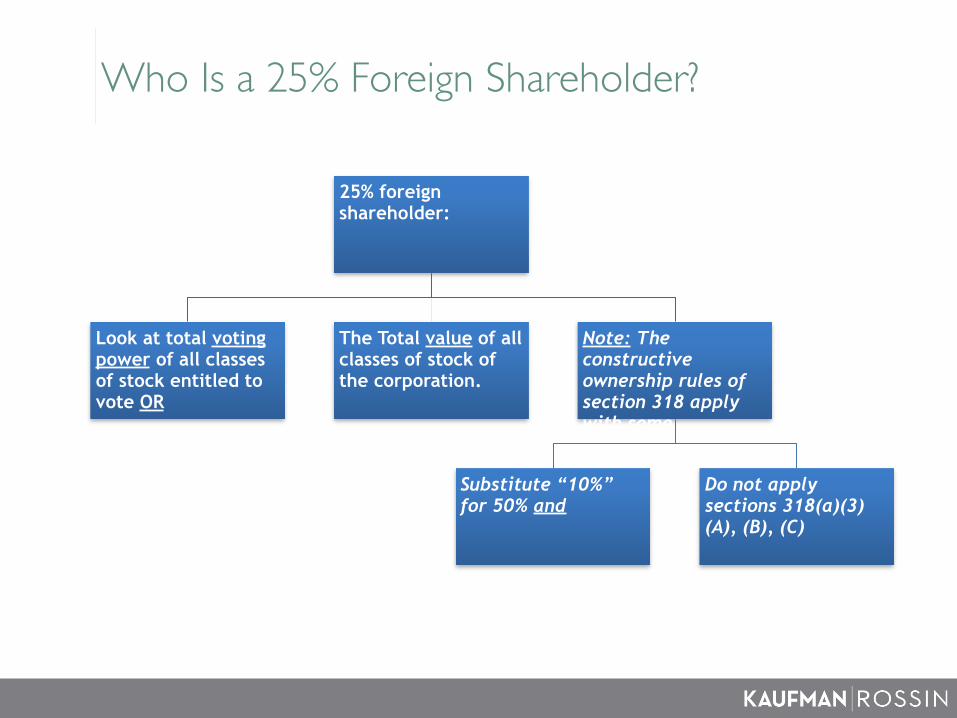

Who Is a 25% Foreign Shareholder?

25% foreign shareholder:

Look at total voting power of all classes of stock entitled to vote OR

The Total value of all classes of stock of the corporation.

Note: The constructive ownership rules of section 318 apply with some modifications:

Substitute “10%” for 50% and

Do not apply sections 318(a)(3)(A), (B), (C)

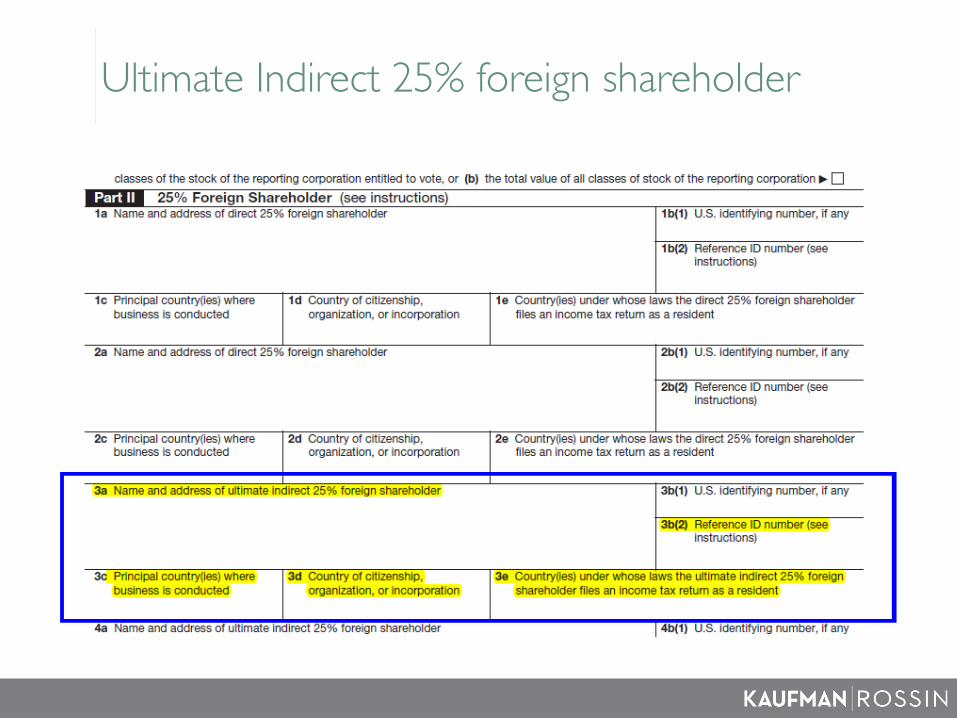

Ultimate Indirect 25% foreign shareholder

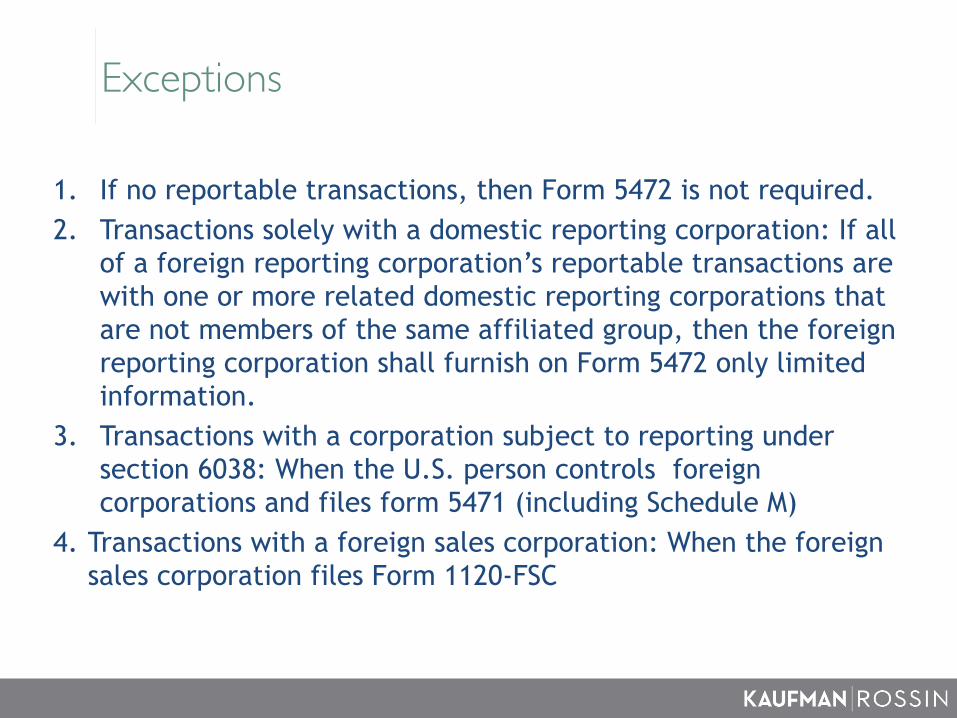

Exceptions

1. If no reportable transactions, then Form 5472 is not required. 2. Transactions solely with a domestic reporting corporation: If all

of a foreign reporting corporation’s reportable transactions are with one or more related domestic reporting corporations that are not members of the same affiliated group, then the foreign reporting corporation shall furnish on Form 5472 only limited information.

3. Transactions with a corporation subject to reporting under section 6038: When the U.S. person controls foreign corporations and files form 5471 (including Schedule M)

4. Transactions with a foreign sales corporation: When the foreign sales corporation files Form 1120-FSC

Exceptions

• The Final Regulations disqualify domestic disregarded entities from certain Form 5472 filing exceptions available to U.S. corporations, including: 1. Where the owner is a foreign corporation reported on Form

5471 and the reportable transaction is duly reported, and 2. Where the foreign corporation qualifies as a foreign sales

corporation for the taxable year and files a Form 1120-FSC.

When and Where to File

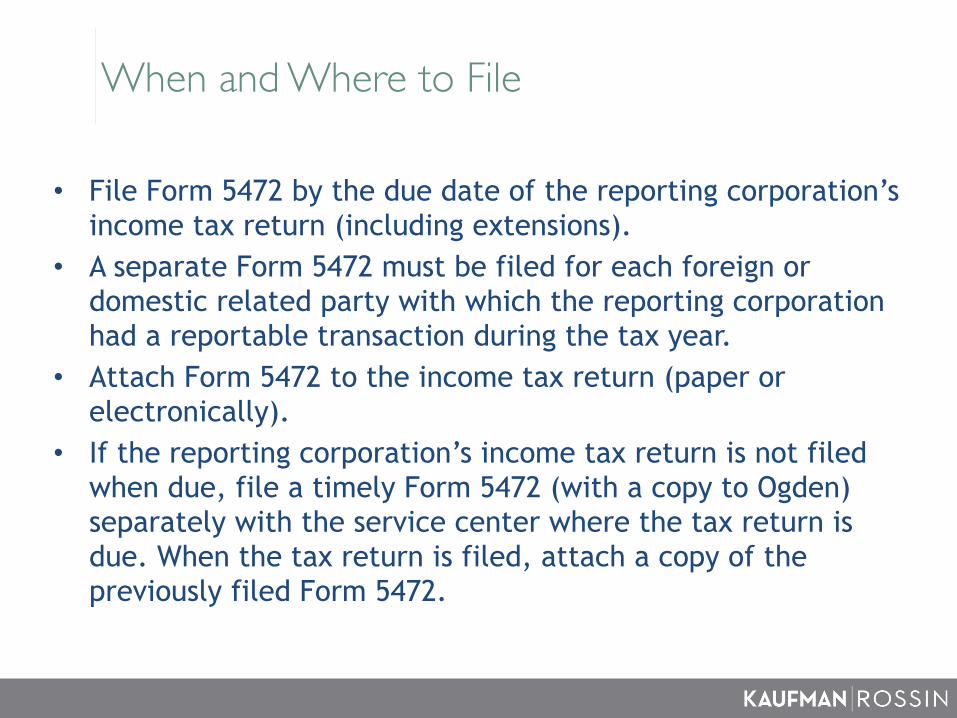

• File Form 5472 by the due date of the reporting corporation’s income tax return (including extensions).

• A separate Form 5472 must be filed for each foreign or domestic related party with which the reporting corporation had a reportable transaction during the tax year.

• Attach Form 5472 to the income tax return (paper or electronically).

• If the reporting corporation’s income tax return is not filed when due, file a timely Form 5472 (with a copy to Ogden) separately with the service center where the tax return is due. When the tax return is filed, attach a copy of the previously filed Form 5472.

Record Maintenance Requirements

• The reporting corporation is required to keep permanent books and records sufficient to establish the correct U.S. tax treatment of any transactions with related parties, including information, documents and records of the foreign owner that may be relevant. – Original entry records, general ledgers, order books, contracts and invoices – Income statements for all related parties – Any documents relating to the setting of prices, such as correspondence, memoranda,

and contracts – Filings by related parties with foreign governments – A corporate road map, showing equity ownership and control among related parties – Records of loans, provisions of services, and other non-sales transactions

The regulations require that the records be maintained by product or industry group.

Examples

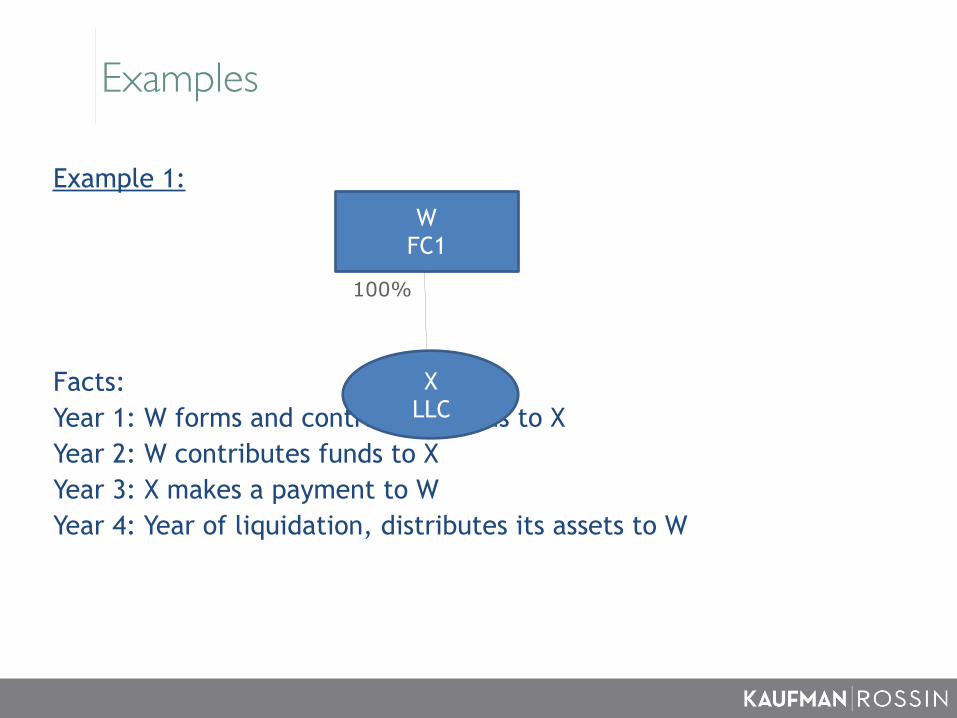

Example 1:

100%

Facts: Year 1: W forms and contributes funds to X Year 2: W contributes funds to X Year 3: X makes a payment to W Year 4: Year of liquidation, distributes its assets to W

W FC1

X LLC

Examples

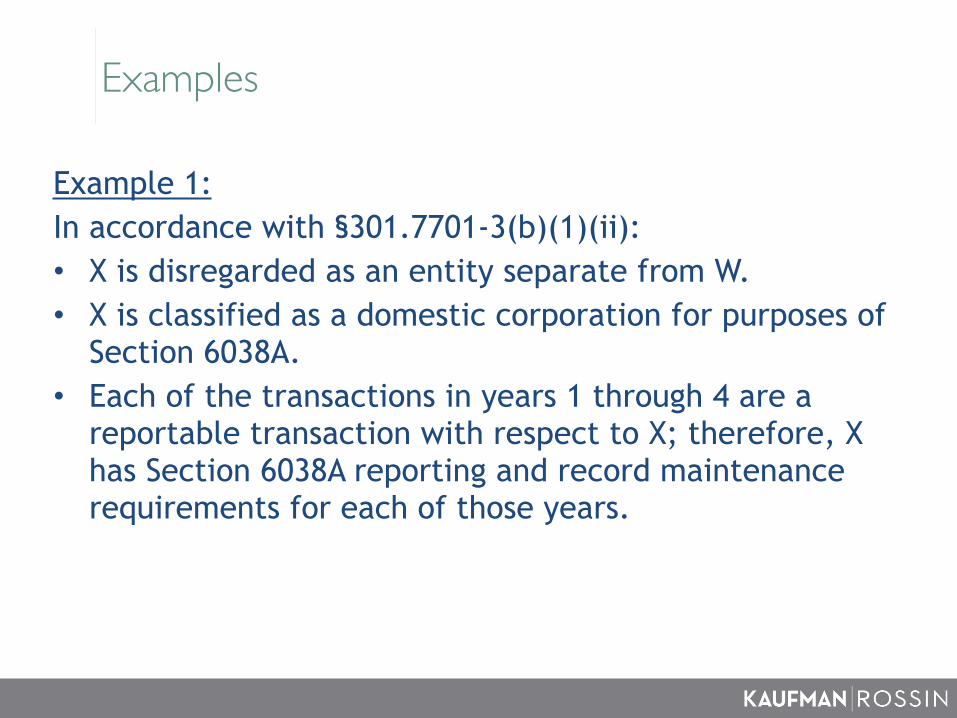

Example 1: In accordance with §301.7701-3(b)(1)(ii): • X is disregarded as an entity separate from W. • X is classified as a domestic corporation for purposes of

Section 6038A. • Each of the transactions in years 1 through 4 are a

reportable transaction with respect to X; therefore, X has Section 6038A reporting and record maintenance requirements for each of those years.

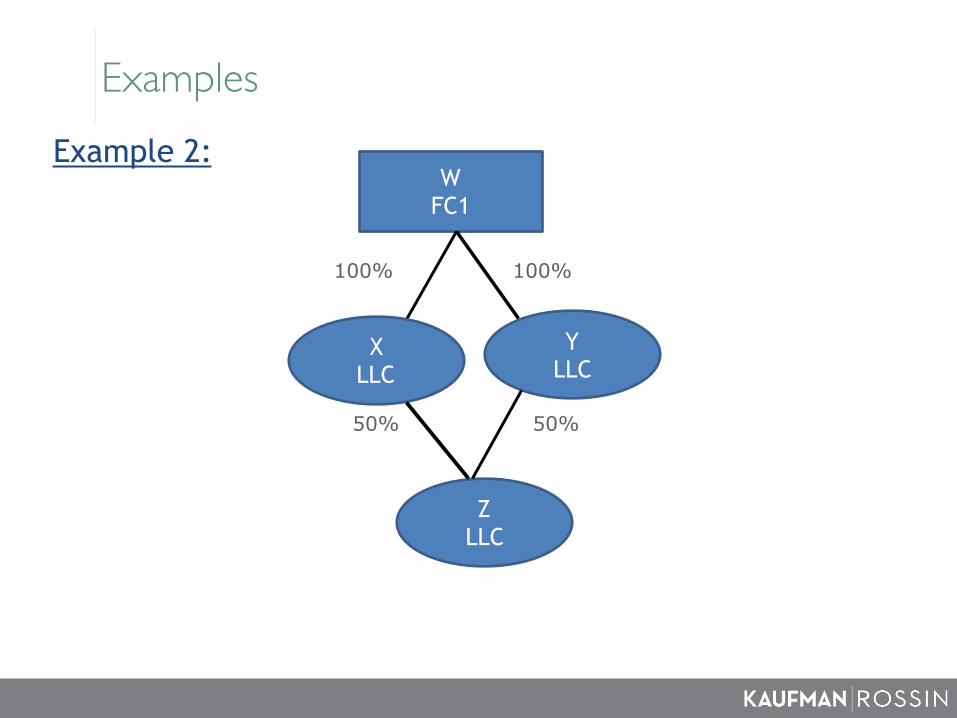

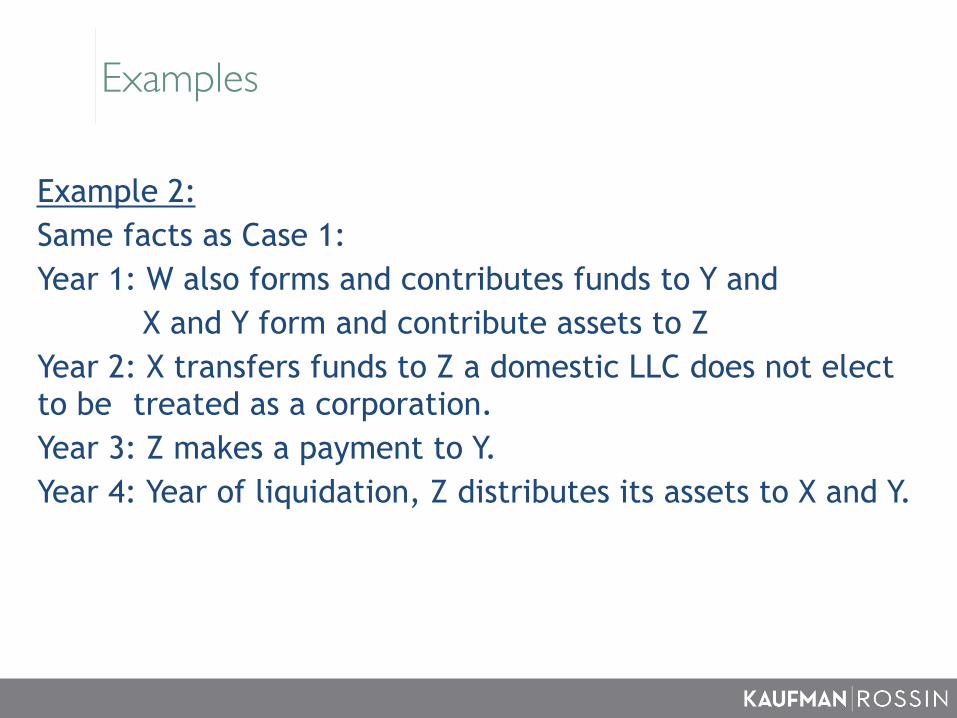

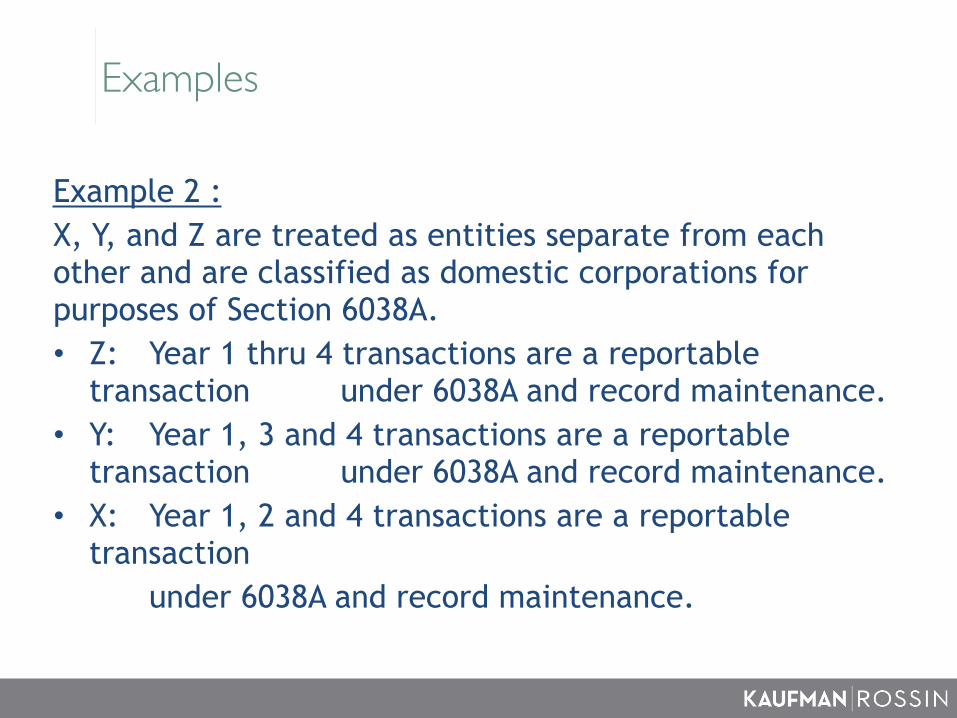

ExamplesExample 2:

100% 100%

50% 50%

W FC1

Y LLC

X LLC

Z LLC

Examples

Example 2: Same facts as Case 1: Year 1: W also forms and contributes funds to Y and X and Y form and contribute assets to Z Year 2: X transfers funds to Z a domestic LLC does not elect to be treated as a corporation. Year 3: Z makes a payment to Y. Year 4: Year of liquidation, Z distributes its assets to X and Y.

Examples

Example 2 : X, Y, and Z are treated as entities separate from each other and are classified as domestic corporations for purposes of Section 6038A. • Z: Year 1 thru 4 transactions are a reportable

transaction under 6038A and record maintenance. • Y: Year 1, 3 and 4 transactions are a reportable

transaction under 6038A and record maintenance. • X: Year 1, 2 and 4 transactions are a reportable

transaction under 6038A and record maintenance.

Penalties

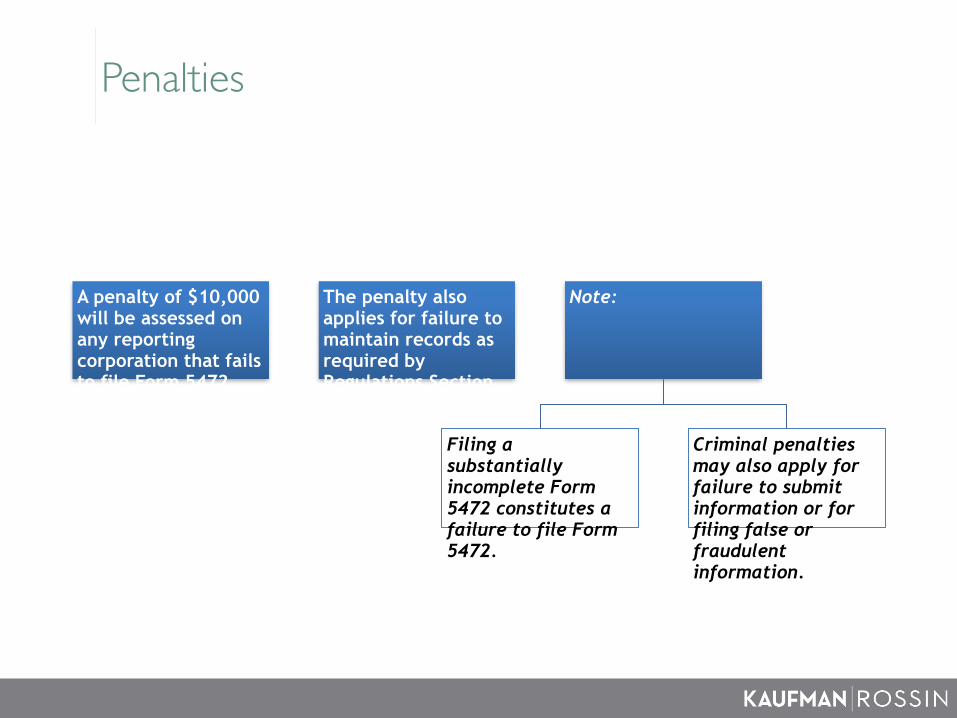

A penalty of $10,000 will be assessed on any reporting corporation that fails to file Form 5472 when due.

The penalty also applies for failure to maintain records as required by Regulations Section 1.6038A-3.

Note:

Filing a substantially incomplete Form 5472 constitutes a failure to file Form 5472.

Criminal penalties may also apply for failure to submit information or for filing false or fraudulent information.

Effective Date

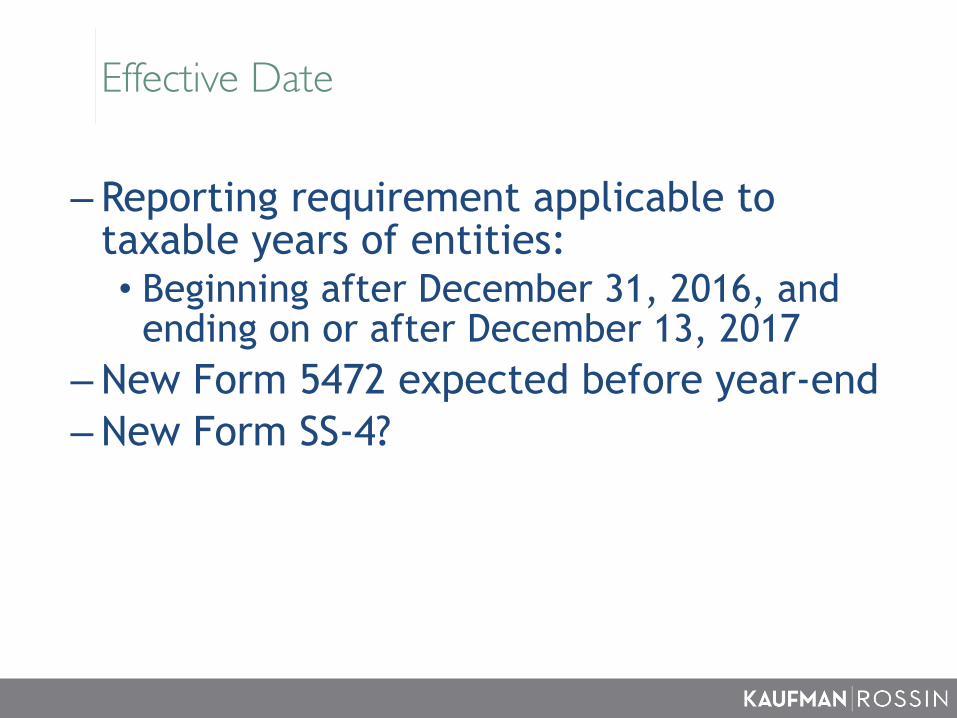

– Reporting requirement applicable to taxable years of entities:

• Beginning after December 31, 2016, and ending on or after December 13, 2017

–New Form 5472 expected before year-end –New Form SS-4?

New Form 5472?

Questions?

IRS Circular 230 Disclosure: The IRS requires that we inform you that any tax advice given in this document is an informal opinion for discussion purposes only. The advice is not intended to be used for the purpose of avoiding tax penalties and it cannot be used for that purpose. We are available for formal consultations and written tax opinions at your request.

Principal, International Tax [email protected] 305.857.6849

International Tax Manager [email protected] 305.850.5134

Carlos A. Somoza, J.D., LL.M.

Maria Toledo, CPA

Contact Us