Embed Size (px)

Citation preview

Deutsche Asset& Wealth Management

Client logopositioning

New Trends in the Global ETF IndustryMarco MontanariHead of Passive Asset Management, Asia [email protected]

Deutsche Asset& Wealth Management

ETF Market Growth

Deutsche Asset& Wealth Management

Marco MontanariNew Trends in the Global ETF Industry

Datum 2010 DB Blue template

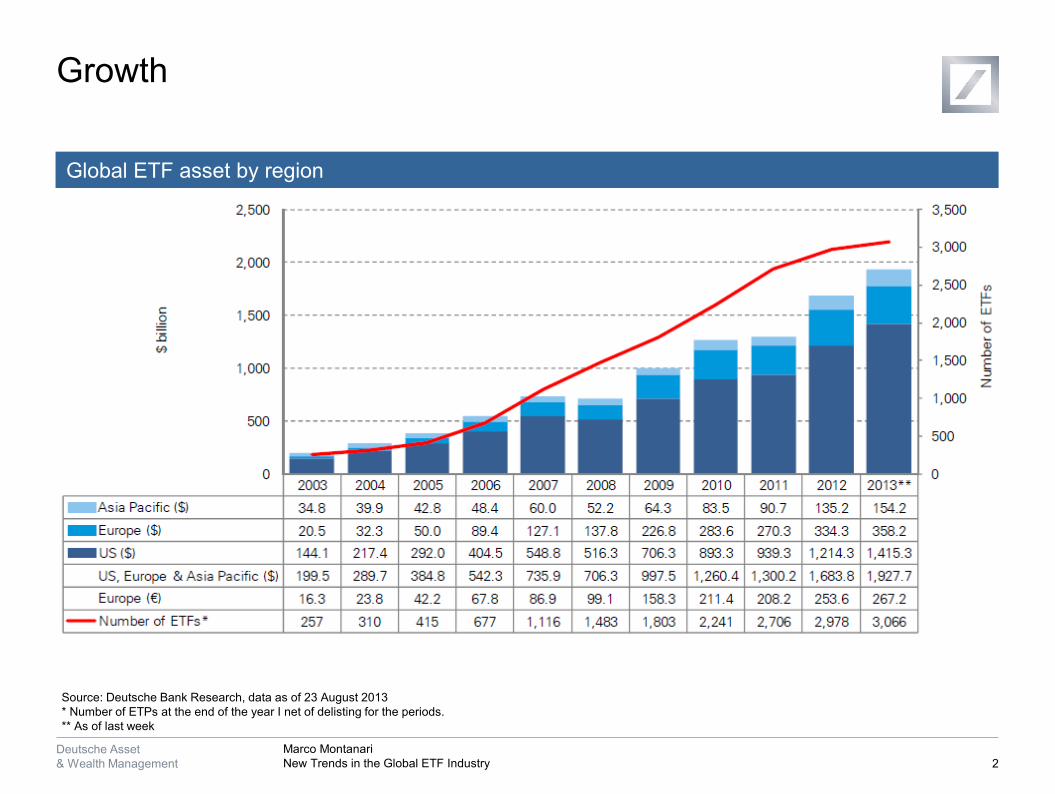

Growth

2

Source: Deutsche Bank Research, data as of 23 August 2013* Number of ETPs at the end of the year I net of delisting for the periods.** As of last week

Global ETF asset by region

Deutsche Asset& Wealth Management

Marco MontanariNew Trends in the Global ETF Industry

Datum 2010 DB Blue template

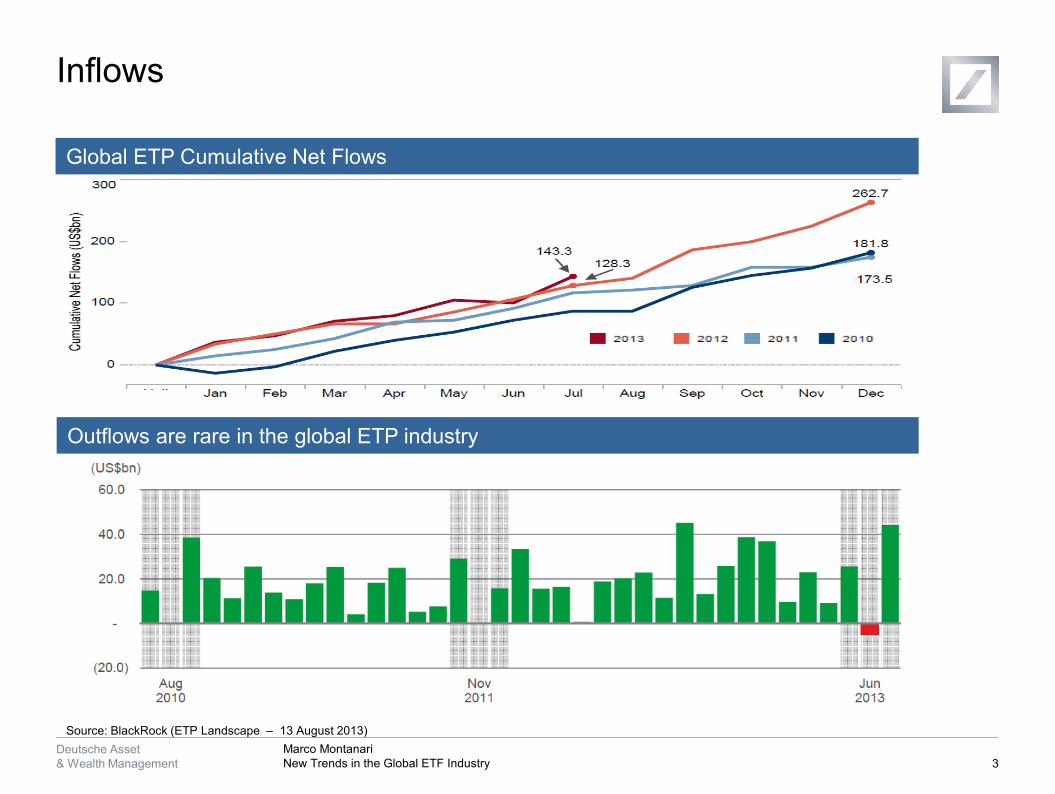

Inflows

3

Source: BlackRock (ETP Landscape – 13 August 2013)

Global ETP Cumulative Net Flows

Outflows are rare in the global ETP industry

Marco MontanariNew Trends in the Global ETF Industry

Deutsche Asset& Wealth Management

9/9/2013 4:52:54 PM 2010 DB Blue template

4

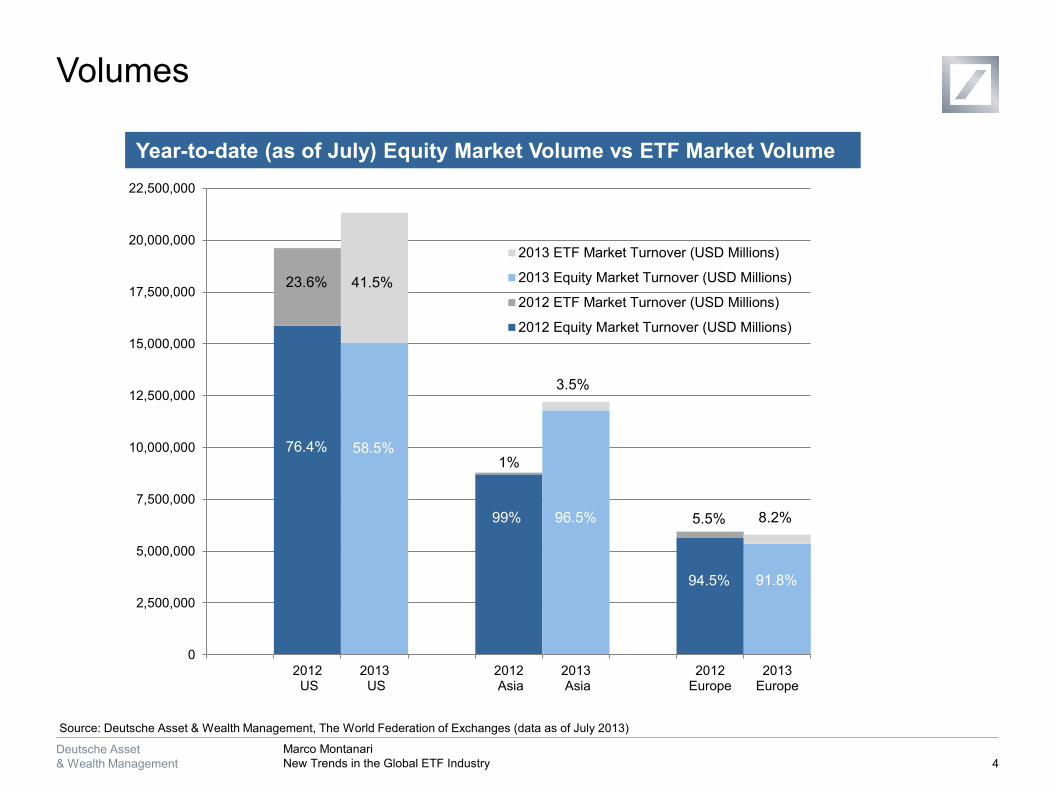

Volumes

Source: Deutsche Asset & Wealth Management, The World Federation of Exchanges (data as of July 2013)

0

2,500,000

5,000,000

7,500,000

10,000,000

12,500,000

15,000,000

17,500,000

20,000,000

22,500,000

2012 US

2013 US

2012 Asia

2013 Asia

2012Europe

2013Europe

2013 ETF Market Turnover (USD Millions)

2013 Equity Market Turnover (USD Millions)

2012 ETF Market Turnover (USD Millions)

2012 Equity Market Turnover (USD Millions)

41.5%

58.5%76.4%

96.5%99%

1%

3.5%

8.2%

94.5%

5.5%

23.6%

91.8%

Year-to-date (as of July) Equity Market Volume vs ETF Market Volume

Deutsche Asset& Wealth Management

Marco MontanariNew Trends in the Global ETF Industry

Datum 2010 DB Blue template

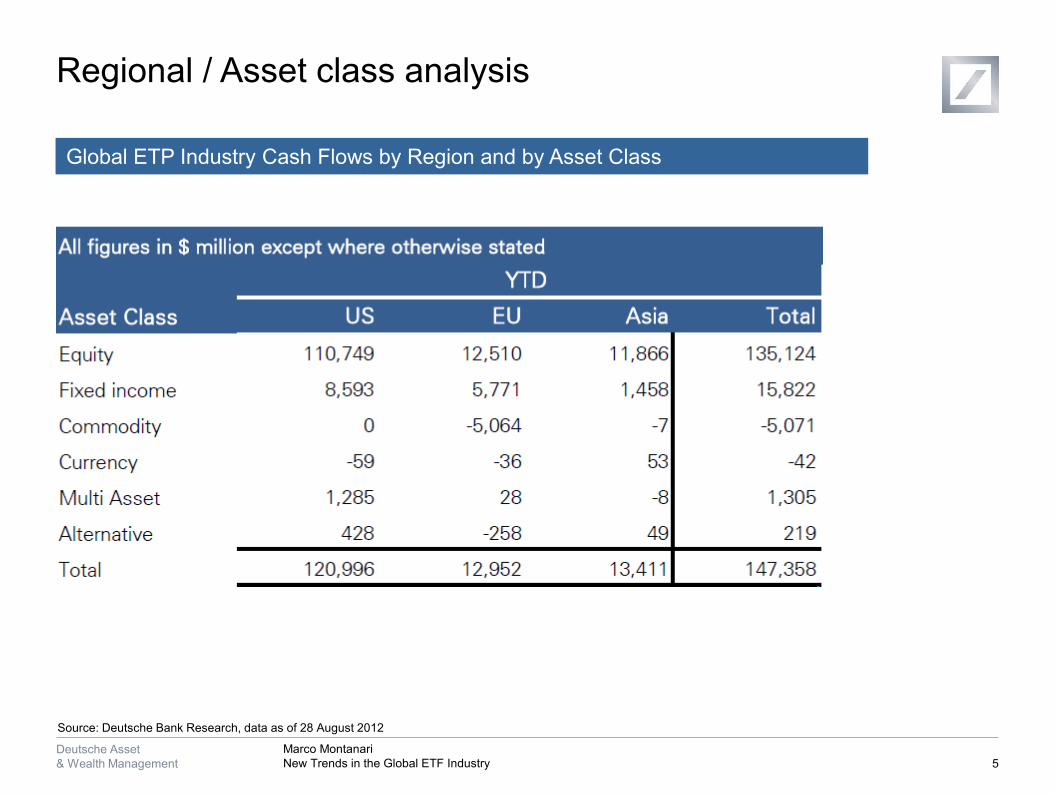

Regional / Asset class analysis

5

Source: Deutsche Bank Research, data as of 28 August 2012

Global ETP Industry Cash Flows by Region and by Asset Class

Marco MontanariNew Trends in the Global ETF Industry

Deutsche Asset& Wealth Management

9/9/2013 4:52:54 PM 2010 DB Blue template

6

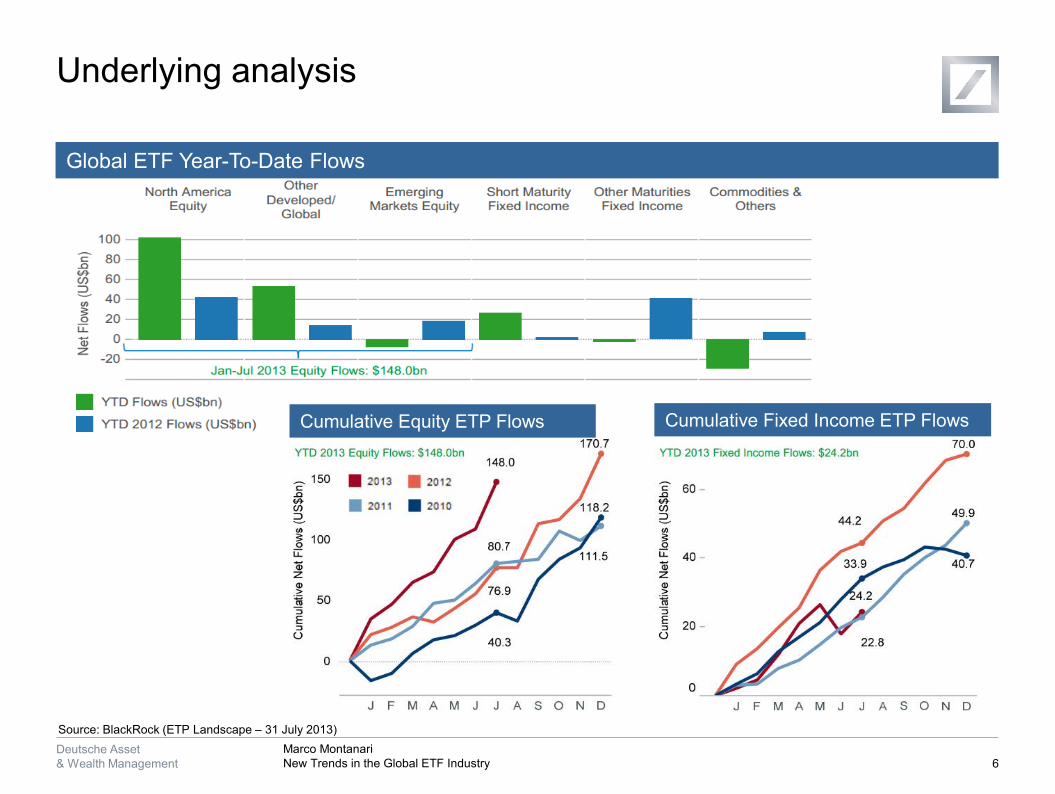

Underlying analysis

Source: BlackRock (ETP Landscape – 31 July 2013)

Global ETF Year-To-Date Flows

Cumulative Equity ETP Flows Cumulative Fixed Income ETP Flows

Deutsche Asset& Wealth Management

Marco MontanariNew Trends in the Global ETF Industry

Datum 2010 DB Blue template

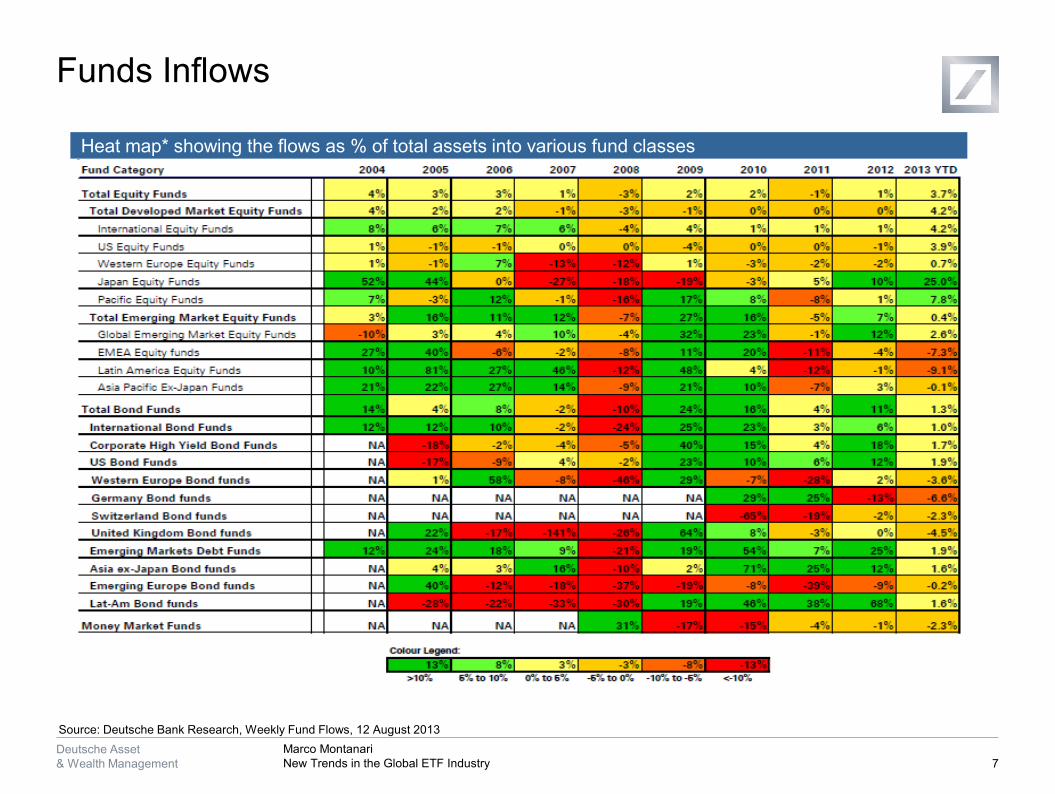

Funds Inflows

7

Source: Deutsche Bank Research, Weekly Fund Flows, 12 August 2013

Heat map* showing the flows as % of total assets into various fund classes

Deutsche Asset& Wealth Management

Key Trends

Marco MontanariNew Trends in the Global ETF Industry

Deutsche Asset& Wealth Management

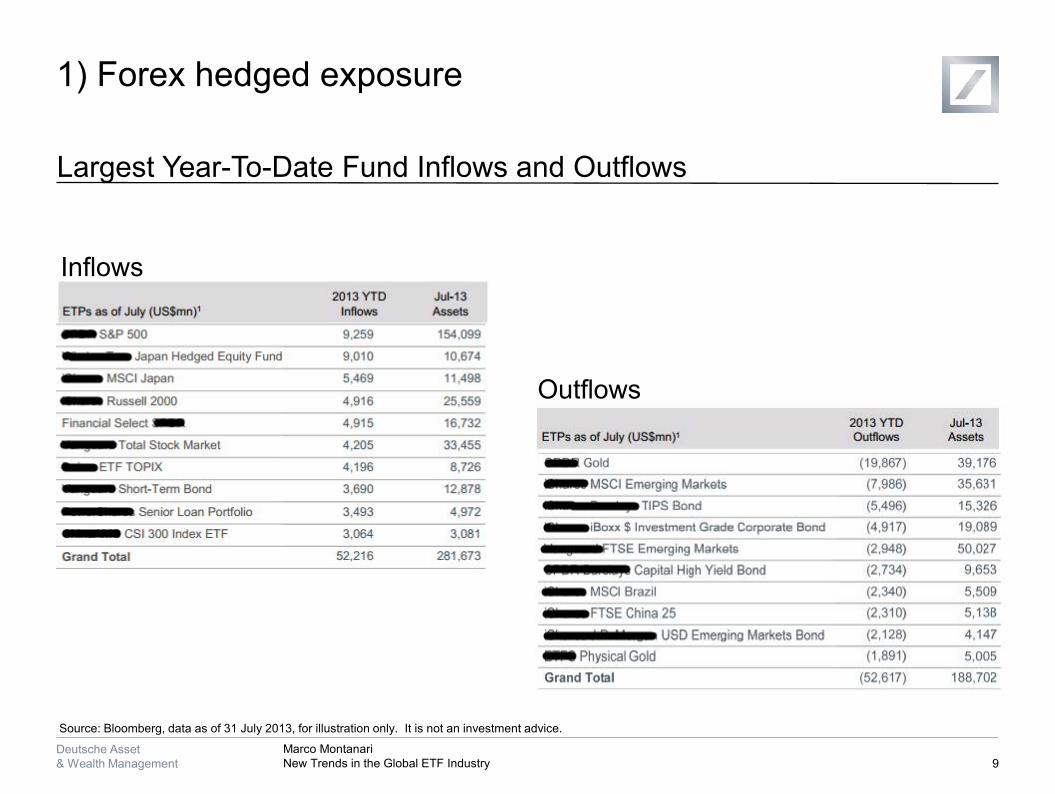

1) Forex hedged exposure

9/9/2013 4:52:54 PM 2010 DB Blue template

9

Largest Year-To-Date Fund Inflows and Outflows

Inflows

Outflows

Source: Bloomberg, data as of 31 July 2013, for illustration only. It is not an investment advice.

Marco MontanariNew Trends in the Global ETF Industry

Deutsche Asset& Wealth Management

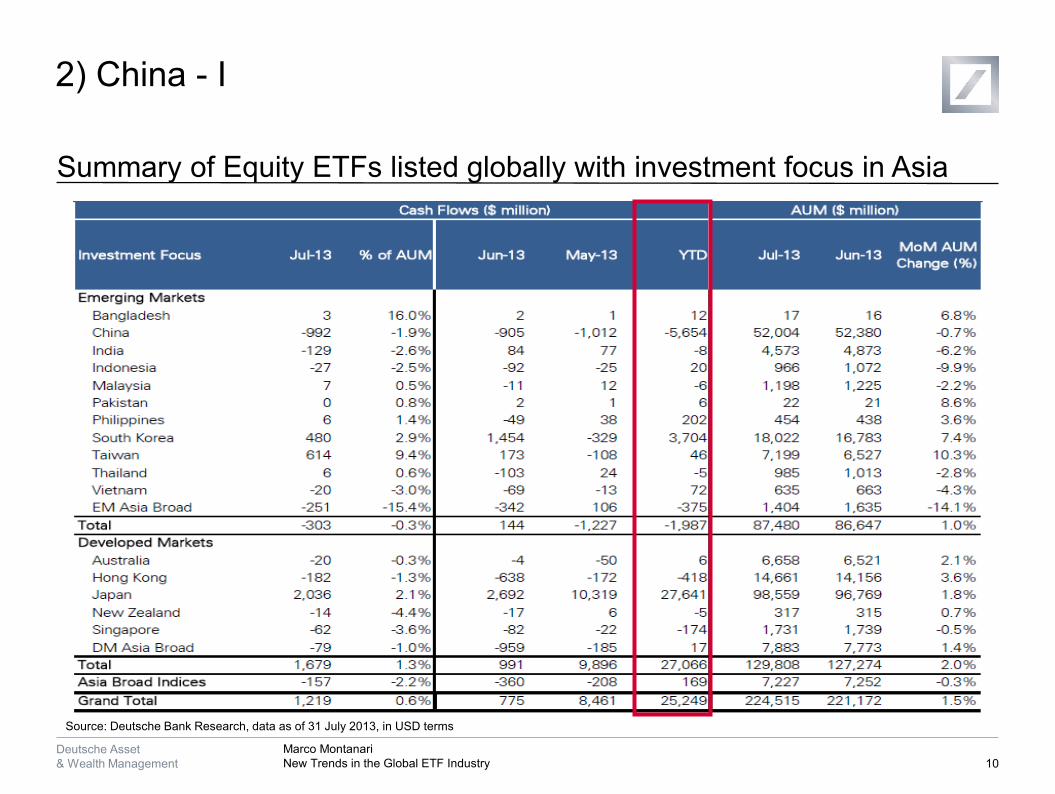

2) China - I

9/9/2013 4:52:54 PM 2010 DB Blue template

10

Summary of Equity ETFs listed globally with investment focus in Asia

Source: Deutsche Bank Research, data as of 31 July 2013, in USD terms

Marco MontanariNew Trends in the Global ETF Industry

Deutsche Asset& Wealth Management

2) China - II

9/9/2013 4:52:54 PM 2010 DB Blue template

11

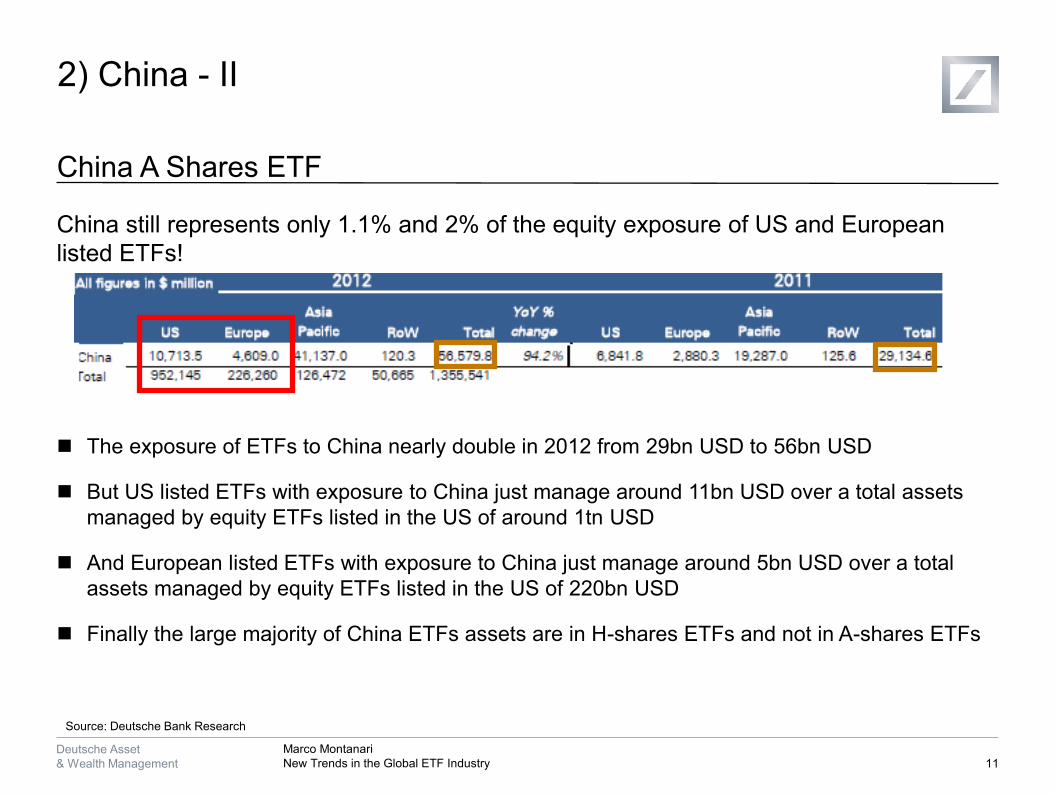

China A Shares ETF

China still represents only 1.1% and 2% of the equity exposure of US and European listed ETFs!

The exposure of ETFs to China nearly double in 2012 from 29bn USD to 56bn USD

But US listed ETFs with exposure to China just manage around 11bn USD over a total assets managed by equity ETFs listed in the US of around 1tn USD

And European listed ETFs with exposure to China just manage around 5bn USD over a total assets managed by equity ETFs listed in the US of 220bn USD

Finally the large majority of China ETFs assets are in H-shares ETFs and not in A-shares ETFs

Source: Deutsche Bank Research

Marco MontanariNew Trends in the Global ETF Industry

Deutsche Asset& Wealth Management

3) Fixed Income

9/9/2013 4:52:54 PM 2010 DB Blue template

12

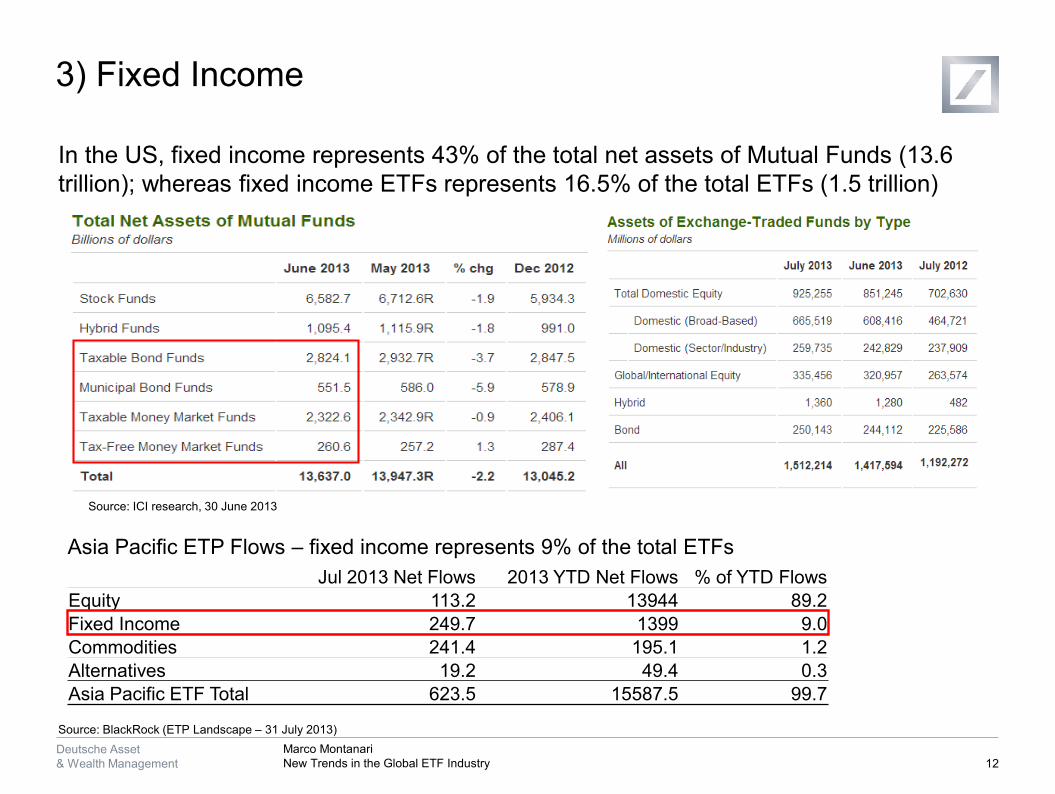

In the US, fixed income represents 43% of the total net assets of Mutual Funds (13.6 trillion); whereas fixed income ETFs represents 16.5% of the total ETFs (1.5 trillion)

Source: ICI research, 30 June 2013

Jul 2013 Net Flows 2013 YTD Net Flows % of YTD FlowsEquity 113.2 13944 89.2Fixed Income 249.7 1399 9.0Commodities 241.4 195.1 1.2Alternatives 19.2 49.4 0.3Asia Pacific ETF Total 623.5 15587.5 99.7

Asia Pacific ETP Flows – fixed income represents 9% of the total ETFs

Source: BlackRock (ETP Landscape – 31 July 2013)

Marco MontanariNew Trends in the Global ETF Industry

Deutsche Asset& Wealth Management

4) Smart / Enhanced / Beta+

9/9/2013 4:52:54 PM 2010 DB Blue template

13

ETF and index providers have recently tended to compete on fees as a means of increasing market share (overall in developed markets)

The satisfaction rate for indices is moderate for equity, at about 71%. Lower for bond indices. (EDHEC-Risk Asian Index Survey 2011 interviewing 127 institutional investors in Asia Pacific)

Indexation and smart beta are playing increasingly important roles in investors’ portfolios (Towers Watson 2012)

A number of institutional investors, including St James's Place, Wyoming Retirement System and CS are switching to MSCI Risk Premia Indices (MSCI 2012)

According to the head of systematic investment strategies at Swiss fund house Lombard Odier, smart beta will grow to represent one-third of global institutional equity allocations by 2018

Marco MontanariNew Trends in the Global ETF Industry

Deutsche Asset& Wealth Management

62% of the respondents will increase their investments in ETFs

64% of respondents will consider Asian-listed ETFs due to parallel trading hours to the respective Asian markets, compared to 47% last year

77% of the investors understand the market making role, up from 65% last year

Since last year the % of people not considering Asian-listed ETFs due to lower trading volume went down from 18% to 5%

42% of respondents confirmed they understand ETF’s liquidity is dependent on the underlying market liquidity, not just the liquidity of the ETF, up from 35% last year

Half of the respondents aware of US tax disadvantage and avoid US listed ETFs

Focus on Asia – Results of the 2013 Asian ETFs Survey sponsored by Deutsche Asset & Wealth Management ETFs for the third year in a row (involving 300 institutional, intermediaries and retail investors):

9/9/2013 4:52:54 PM 2010 DB Blue template

14

Marco MontanariNew Trends in the Global ETF Industry

Deutsche Asset& Wealth Management

Contact

9/9/2013 4:52:54 PM 2010 DB Blue template

15

Marco MontanariHead of Passive Asset Management, Asia Pacific

Email: [email protected]

Deutsche Asset& Wealth Management

Marco MontanariNew Trends in the Global ETF Industry

Datum 2010 DB Blue template

Important Information

© 2013 Deutsche Bank AG This presentation contains a short summary description of the above mentioned ETFs and is for discussion purposes only. A complete description of the funds is in the respective and most recent prospectus of the above mentioned ETFs. This presentation is not for distribution to, or for the attention of, US or Canadian persons. Without limitation, this presentation does not constitute an offer or a recommendation to enter into any transaction. When making an investment decision, you should rely solely on the final documentation and any prospectus relating to the transaction and not this summary. Investment strategies involve numerous risks. Prospective investors or counterparties should discuss with their professional tax, legal, accounting and other adviser(s) the effect of anytransaction they may enter into, including the possible risks and benefits of such transaction and should ensure that they fullyunderstand the transaction and have made an independent assessment of the appropriateness of such transaction in the light of their own objectives and circumstances. In no way should Deutsche Bank be deemed to be holding itself out as a financial adviser or a fiduciary of the recipient hereof. Deutsche Bank may make a market or trade in instruments economically related to fund units orderivatives mentioned herein, and/or have investment banking or other relationships with issuers of the relevant securities. Deutsche Bank actively manages various risks, and on occasion may deal in securities mentioned in this document or in related instrumentsduring the period between your receipt of this fact sheet and the award of any order. Whilst Deutsche Bank‘s trading or hedging activities are not intended to have any significant impact upon prices, its dealings could affect the prices you pay or receive for transactions in related securities or fund units. Deutsche Bank, and its current and future subsidiaries, parents, affiliates, divisions, officers, directors, agents and/or employees, disclaim all liability with respect to this document and the information herein, and are not liable for any errors or omissions, or for any damages howsoever arising from any reliance placed thereon, save as required by applicable laws and regulations. A full description of the terms and conditions of all sub-funds are included in the prospectus of and II. You can get the full and the simplified prospectus of each sub-fund of at , 49, avenue J.F. Kennedy, L-1855 Luxembourg, R.C.S. Luxembourg D-119 899.Deutsche Bank AG is authorised under German Banking Law (competent authority: BaFin – Federal Financial Supervising Authority) and is regulated by the Financial Services Authority for the conduct of investment business in the United Kingdom. The registered address of Deutsche Bank AG, London Branch, is Winchester House, 1 Great Winchester Street, London EC2N 2DB.

16