Embed Size (px)

Citation preview

1 Taking control of the future tpa-global.com

November 15, 2017

New transfer pricing regulations in Polandin force since January 1st, 2017

Marta Klepacz and Agnieszka Krzyżaniak

2 Taking control of the future tpa-global.com

Presenters

Agnieszka KrzyżaniakManager in Transfer Pricing Group, MDDPtel. (+48) (22) 320 48 64|[email protected]

Marta KlepaczTransfer Pricing Senior Consultant, MDDPtel. (+48) (22) 376 52 86|[email protected]

3 Taking control of the future tpa-global.com

Breaking TP news in Poland…

A Ministry of Finance has set up new Department for Transfer Pricing and Valuation responsible for:• forming the Ministry of Finance’s policy in the

area of transfer pricing• preparation of proposals of system solutions• development of guidelines for taxpayers and

ensure uniform application and interpretation of regulations

• database for transfer pricinganalysis / valuation

18th of September published final Regulation of the Minister of Finance of the information to be included in transfer pricing documentation

National Revenue Administration (NRA) plans to create Transfer Pricing Forum

• a platform for discussion about transfer pricing between tax administration andbusiness, the world of science and NGOs

• constant discussion platform – meeting at least 2 times per year

Preliminary draft budget act for 2018 yearpredicts increase of income taxes, includingtransfer pricing from tax collection system

4 Taking control of the future tpa-global.com

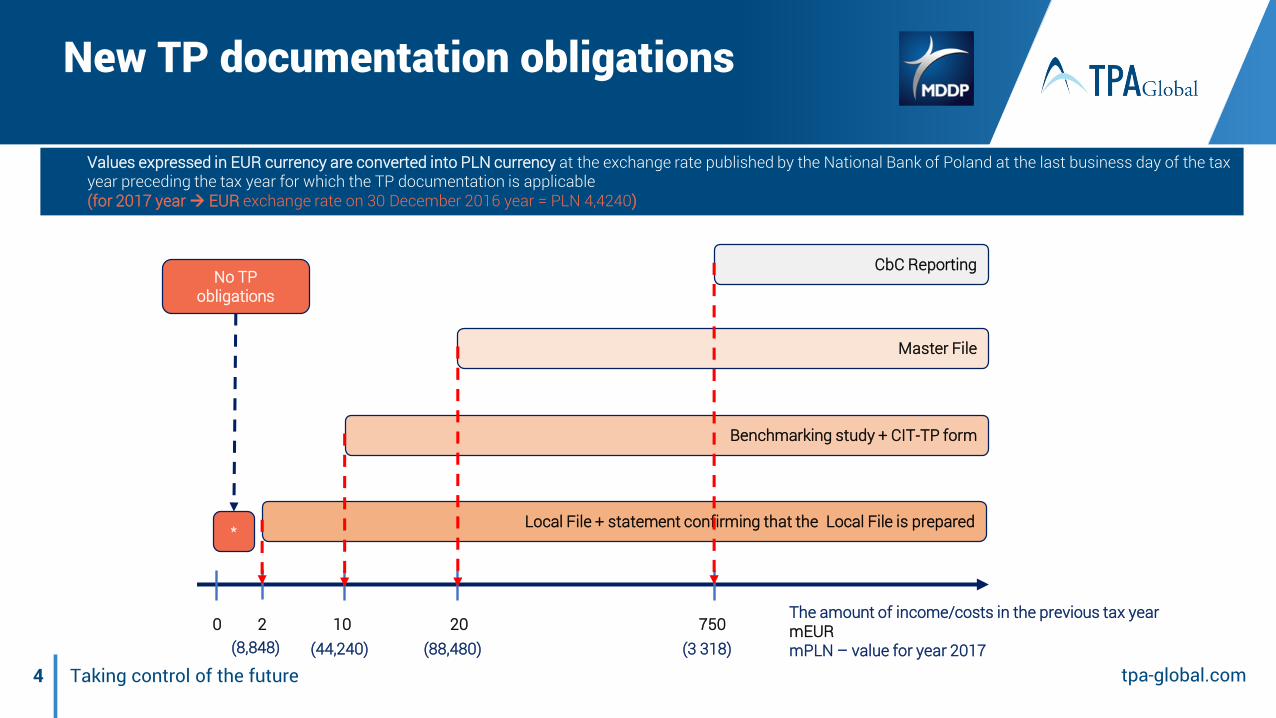

New TP documentation obligations

Values expressed in EUR currency are converted into PLN currency at the exchange rate published by the National Bank of Poland at the last business day of the tax year preceding the tax year for which the TP documentation is applicable(for 2017 year EUR exchange rate on 30 December 2016 year = PLN 4,4240)

2 10 20 750

Local File + statement confirming that the Local File is prepared

Benchmarking study + CIT-TP form

Master File

CbC Reporting

*

The amount of income/costs in the previous tax yearmEURmPLN – value for year 2017

No TP obligations

0(8,848) (44,240) (88,480) (3 318)

5 Taking control of the future tpa-global.com

Statutory TP deadlines – from FY 2017

Submission of CIT – 8

statement in Poland

Approval of the financial

statement + 10 days

✓ Master File ****✓ Local File* and benchmarkingstudies***

✓ CIT – TP form✓ Statement confirming that Local file is

prepared✓ Local File**

31 Mar. 2018

2017 2018

31st Dec.2016 31st Mar. 2017 31st Dec. 2018

LEGEND:Assumptions: Calendar year = Tax year* Without financial data description (Article 9a par. 2b, point 3 of Corporate Income Tax Act)** Supplementation of the description of the financial data (Article 9a par. 2b, point 3 in Corporate Income Tax Act)*** Exceeding EUR 10 m of revenues/ costs in the previous year**** Exceeding EUR 20 m of revenues / costs in the previous year

6 Taking control of the future tpa-global.com

TP documentation obligation –transaction limits

• Revenues / costs < EUR 2m – no obligations related to transfer pricing documentation

• Revenues / costs > EUR 2 m – TP documentation obligations

Transaction thresholds:Revenues <EUR 2-20 m >• from 50k EUR (increased by 5k EUR for every 1 m

EUR of revenues over 2 m EUR) Revenues <EUR 20-100 m>• from EUR 140k (increased by EUR 45k for every EUR

10 m revenues over EUR 20 m) Rvenues > EUR 100 m • EUR 500k.

Transaction limits(since 1 January 2017 year)

• EUR 100k - the value of the transaction does not exceed 20% of the capital share of the party to the transactions

• EUR 30k – provision of services, sale, share of intangible assets

• EUR 50k – other types of transactions

• EUR 20k – transactions with entities from tax heavens

Transaction limits(till 31 December 2016 year)

7 Taking control of the future tpa-global.com

Transaction thresholds from FY 2017

50 55 60 65 70 75 80 85 90 95 100 105 110 115 120 125 130 135 140

185

230

275

320

365

410

455

500

0

100

200

300

400

500

600

2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 30 40 50 60 70 80 90 100Tran

sact

ion

thre

shol

d fo

r the

tax

year

[kEU

R]

Revenues of the taxpayer for the year preceding the tax year [mEUR]

8 Taking control of the future tpa-global.com

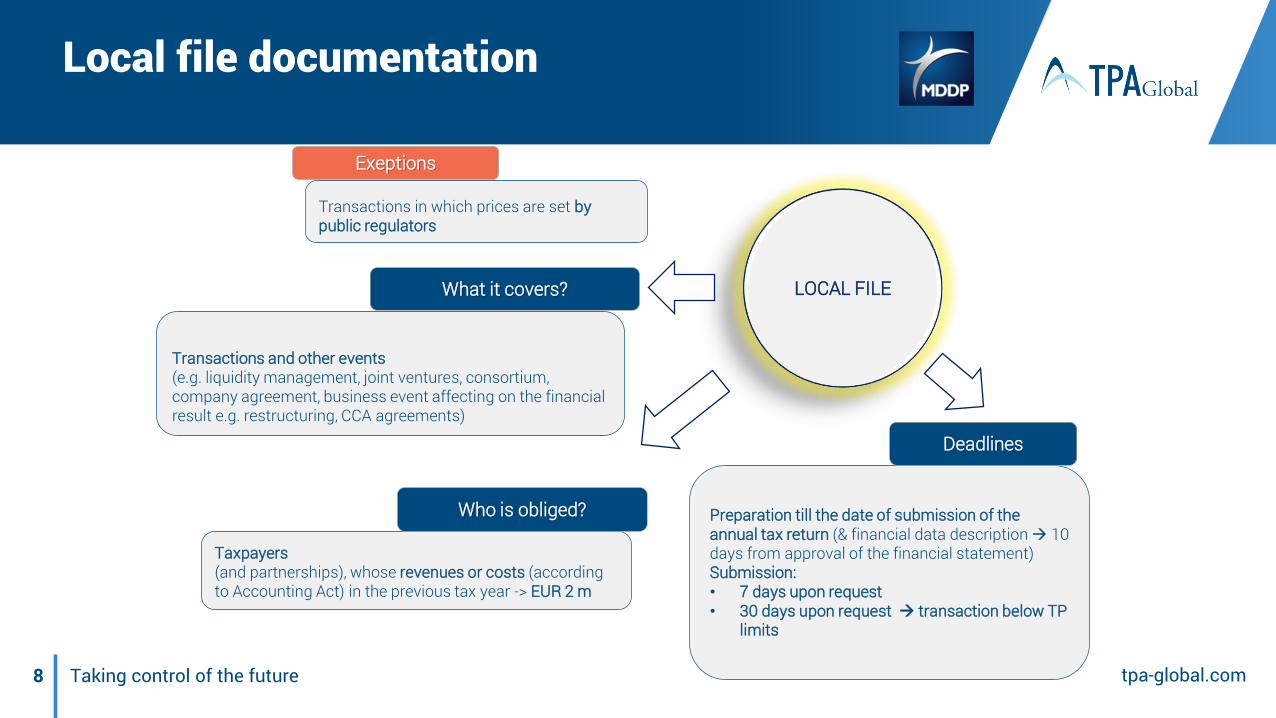

Local file documentation

Preparation till the date of submission of the annual tax return (& financial data description 10 days from approval of the financial statement)Submission: • 7 days upon request • 30 days upon request transaction below TP

limits

Taxpayers(and partnerships), whose revenues or costs (according to Accounting Act) in the previous tax year -> EUR 2 m

Who is obliged?

LOCAL FILE

Transactions and other events (e.g. liquidity management, joint ventures, consortium, company agreement, business event affecting on the financial result e.g. restructuring, CCA agreements)

What it covers?

Deadlines

Transactions in which prices are set by public regulators

Exeptions

9 Taking control of the future tpa-global.com

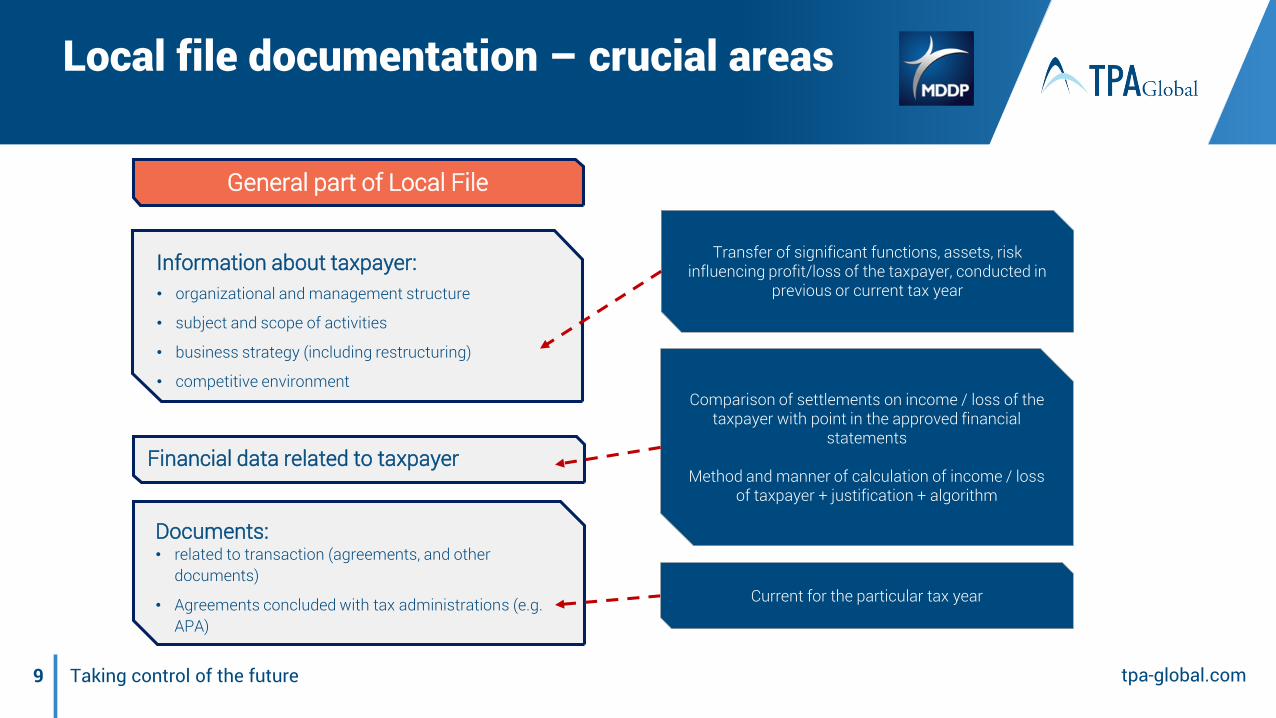

Local file documentation – crucial areas

Financial data related to taxpayer

Information about taxpayer:• organizational and management structure

• subject and scope of activities

• business strategy (including restructuring)

• competitive environment

Documents:• related to transaction (agreements, and other

documents)

• Agreements concluded with tax administrations (e.g. APA)

Transfer of significant functions, assets, risk influencing profit/loss of the taxpayer, conducted in

previous or current tax year

Comparison of settlements on income / loss of the taxpayer with point in the approved financial

statements

Method and manner of calculation of income / loss of taxpayer + justification + algorithm

Current for the particular tax year

General part of Local File

1 0 Taking control of the future

Local file documentation– crucial areas

Description of IC-transaction or other event:• Type and subject of the transaction

• Financial data related to the transaction

• Identification data of parties

• Description of the transaction

• Method and the manner of calculating income / loss of taxpayer + justification + algorithm

Benchmarking analysis*

Separate functional analysis for each type of activity

Balance sheet and off-balance sheet assets

Human capitalFunctional profile

Actual data at the beginning or at the end of the tax year

Transaction value resulting from:- issued / received invoices / contracts

- received / transferred payments

Impact of settlements on income / loss of the taxpayer

Justification for TP adjustments

*Justification for lack of information indicated in the TP Regulation

Annual or multi-annual data

What is the description of comparability?

Comparable data, data sources

Transactional part of Local File

1 1 Taking control of the future tpa-global.com

Benchmarking analysis

*Source: BEPS Action 13 Country-by-Country Reporting; Handbook on Effective Tax Risk Assessment

Preparation and submission:together with Local File documentation

Taxpayers(and partners of partnership), whose revenues or costs (according to Accounting Act) in the previous tax year exceeded > EUR 10 m

Who is obliged?BENCHMARKING

ANALYSIS

Deadlines

Transactions in which prices are set by public regulators

Exeptions

An element of Local File, which is justification for the arm's length prices. Can be prepared in two variants: internal or external comparison.In any of two above variants can’t be applied, a description of the compliance of the terms of the transaction with the market conditions should be applied

What is it?

1 2 Taking control of the future tpa-global.com

Benchmarking analysis- cont.

BENCHMARK ANALYSIS

External comparison - comparison of prices used in the analyzed transaction with prices used by independent entities on the market carrying out activity comparable to the taxpayer

External comparison

• primarily including Polish entities, if available• the content of the benchmarking analysis report should address

all Polish regulations• updated once in three years

Problems with using group benchmarking analysis

Internal comparison - comparison of prices used in the analyzed transaction with prices used by the taxpayer in similar transactions with independent entities

Internal comparison

1 3 Taking control of the future tpa-global.com

CIT-TP / PIT-TP

by the date of submission of the annual tax return

Taxpayers(and partners of partnership), whose income or costs (according to Accounting Act) in the current tax year exceed -> EUR 10 m

Who is obliged?

CIT-TP/PIT-TP

Deadlines

A separate simplified statement on transactions and other events between related entitiesSubmitted as the attachment to the tax return.

What is it?

The statement enables tax authorities to type tax payers and the transactions to be subject of the potential tax control in the field of transfer pricing

The purpose of the introduction

1 4 Taking control of the future tpa-global.com

Simplified statement on transactions and other occurrences between related entities (CIT-TP)

The main issues:

• more then 140 items to fill• the information is divided into 6 main

categories:A. Data identifying the taxpayerB. Identification of taxpayers’ TP

relationships with related partiesC. Information about related entitiesD. Main taxpayer's business activity and

functional profileE. RestructuringsF. Related party transactions or other events

(divided into 6 subcategories)

1 5 Taking control of the future tpa-global.com

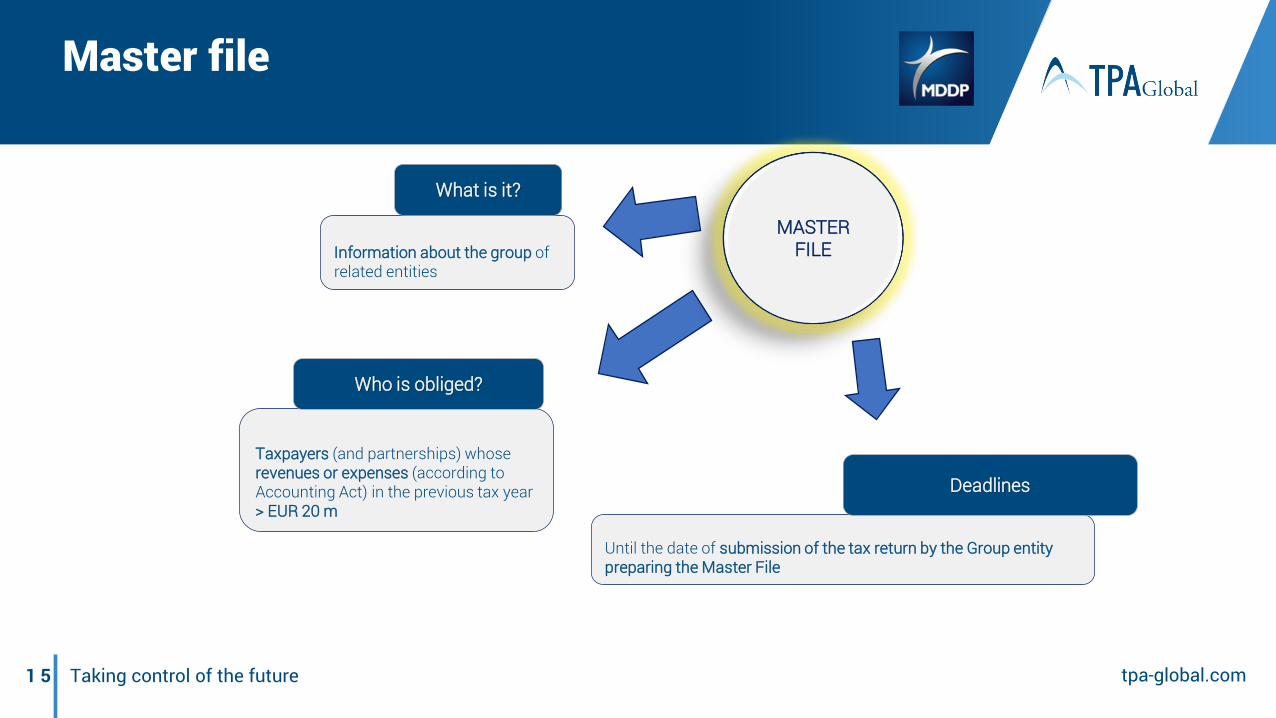

Master file

Taxpayers (and partnerships) whose revenues or expenses (according to Accounting Act) in the previous tax year> EUR 20 m

Who is obliged?

Information about the group of related entities

Until the date of submission of the tax return by the Group entity preparing the Master File

What is it?

Deadlines

MASTER FILE

1 6 Taking control of the future tpa-global.com

Master file - crucial areas

Information about entity

• Entity obliedto prepare?

• Date of submissionof its taxreturn

Groupdescription

• Organizationalstructure

Transfer Pricing policy

• Services

• Intangibleassets

• Financingactivities

• Other

Group activity• Main activities

• Geographicmarkets

• Business factors

• Significantvalue-addedchains

• Restructuringevents

Description of intangible

assets

• Possession

• Creation

• Developing

• Exploitation

• Changesduring the year

Financing

• Financial situation

• Externalfinancing

• List of significantexternal loansand credits

Advance pricing agreement

• Other CIT agreements outside Poland

1 7 Taking control of the future tpa-global.com

Electronic(model template - not available online yet)

Country-by-Country reporting according to Polish regulations

Capital Groups:Consolidated revenues in the previous financial year> EUR 750 m

Who is obliged?

Information about a group of related entities

Information about:- the global allocation of profit in the group- the amount of taxes paid in each country- location and type of economic activity

What is it?

What covers?

The cash penalty imposed by the Head of the NRA in the amount ofPLN 1 m

Sanctions?The main entity in the Group or other entity appointed within the group to submit a CBC report

Who submits?

To the Head of the NRA

To whom the form should be submitted?

Form? CBC report

1 8 Taking control of the future tpa-global.com

CBC report – deadline for submitting*

* Assumption: fiscal year = calendar yearIf the financial year covers a different period, the deadlines for submitting the CBC report are respectively changing

2016 2017 2018

31st Dec. 20171st Jan. 2016 1st. Jan. 2017 31st Dec. 2018

12 months from the end of the financial year

Submission of the CBC report for FY 2017

Submission of the CBC reportFY 2016

by taxpayers with a financial yearbeginning January 1st, 2016 and

ending December 31st, 2016

Deadline

1 9 Taking control of the future tpa-global.com

Starting PointDetermine EBIT%

Key People FunctionsAllocation of EBIT%

CBC notification

19

Entities belonging to capital groups that are subject to the obligation to submit information about a group of entities (CBC report):- Polish entity being a participant of group of entities- PE ("plant") in Poland

Who is obliged?Notification about an obligation of CBC notificationsubmission

Interactive form in ePUAP platform (CBC-P) -submitted electronically or in writing form directly to the Head of the NRA

What is it?

Form?

The cash penalty imposed by the Head of the NRA in the amount ofPLN 1 m

Sanctions?

To the Head of the NRA

To whom submit?

CBC NOTIFICATION

2 0Taking control of the future

tpa-global.com

CBC notification - deadline for submission*

* Assumption: fiscal year = calendar yearIf the financial year covers a different period, the deadlines for submitting the CBC report are recpectively changing

2016 2017 2018

31st Dec. 20171st Jan. 2016 1st. Jan. 2017 31st Dec. 201831st Oct. 2017

Transitional period

Transitional period:Deadline for the first year -> 10 months after the end of the financial yearGeneral principle:Deadline -> last day of the financial year

Obligation to submit a CBC notificationfor FY 2017

(covering period January 1st, 2017 and ending December 31st, 2017

Obligation to submit a CBC notificationfor FY 2016

(by taxpayers with a financial year coveringperiod January 1st, 2016 and ending

December 31st, 2016)

Deadline

2 1 Taking control of the future tpa-global.com

Areas of interest of Polish tax authorities

AREAS OF INTEREST OF

TAX AUTHORITIES

Restructuring

Group financing transactions

Licenses feesespecially related to

transactions withentities from tax

havens

Intangible services particularly

management fees

Shared service centers

2 2 Taking control of the future tpa-global.com

Tax audits

22

In 2016 in comparison to 2015, the number of tax audits regarding transfer pricing issues increased by 36% (commenced) and 119% (ended).

Increasing number of transfer pricing tax audits is one of the most important task of the tax administration for next years.Compared to 2015, in the year 2016 the controlled taxpayers

made an estimation of their income by:

Reduction of losses in terms of tax optimization PLN 88 m in 2015 and PLN 2 330 m in 2016 (an increase of 2 500%!)

Reduction of losses - in transfer pricing area: PLN 5,3 m in 2015 to PLN 458,6 m in 2016 (an increase of 8 500%!)

Determination of tax liability on tax optimization: PLN 23,8 m in 2015 and PLN 779,7 m in 2016 (an increase of 3200%!)

Determination of tax liability in transfer pricing area: PLN 5,4 m in 2015 and PLN 166,1 m in 2016 (an increase of 2950%!)

2 3 Taking control of the future tpa-global.com

Summary of Polish transfer pricing legislation in force since January 1st, 2017

2 4 Taking control of the future tpa-global.com

Questions?

2 5 Taking control of the future

TPA Global provides international businesses with integrated and value-addedsolutions in improving financial performance, operational efficiency, strategicdevelopment and talent coaching through a cross-border and cross-discipline teamof professionals which identifies the right solutions for customers and targets;efficient and streamlined advisory and implementation processes which cutthrough operational complexities across functions and borders; and superiorcustomer service and support which proactively anticipate the evolving needs ofthe clients.

H.J.E. Wenckebachweg 210 . 1096 AS Amsterdam . The Netherlands . +31 (0)20 462 3530 . tpa-global.com

The views expressed and the information provided in this material are of general nature andis not intended to address the circumstances of any particular individual or entity. The abovecontent should neither be regarded as comprehensive nor sufficient for making decisions.No one should act on the information or views provided in this publication withoutappropriate professional advise. It should be noted that no assurance is given for any lossarising from any actions taken or to be taken or not taken by anyone based on thispublication.

© 2017 Transfer Pricing Associates Holding B.V. All Rights Reserved.

tpa-global.com