Embed Size (px)

Citation preview

New Regime of Service Tax

Presented By

CA. S K Mishra

IntroductionIntroduction• Service tax was introduced in the year 1994 through

Chapter V of Finance Act 1994 by then Finance minister of India, Dr. Manmohan Singh.

• Service tax , as the name suggests, is a tax on Services. It is a tax levied on the transaction of certain services specified by the Central Government under the Finance Act, 1994.

• Till 30.06.2012, 119 services were taxable.

• There is nothing called Service tax Act.

IntroductionIntroduction• Service sector has been growing phenomenally all over the world,

though it may very in degree & magnitude among the various countries.

• The service tax when introduced in 1994, taxed only three services, namely stock brokers, general insurer and telephone services.

• When introduced, even the policy maker would have never thought that one day it will be the major revenue earner for the Govt. kitty.

• In today’s context, the growth of an economy is evaluated in terms of the growth & spread of the service tax too.

• Services constitutes more than 60% of India’s GDP at present.

• During the F.Y 1994-95, only Rs.410 crores were collected, which has been grown to over Rs.80,000/- crores during F.Y 2011-12.

Authority to levy service taxAuthority to levy service tax

Vide Entry 97 of Schedule VII of the Constitution of India, the Central Government levies Service tax through Chapter V of the Finance Act, 1994.

Administration & Collection of service tax is done by Central

Excise Department.

Rate of Service taxRate of Service taxThe effective rate of Service Tax at present ( w.e.f 01.04.2012 ) is 12.36% on the value of the taxable service. It comprises of Service Tax @12% payable on the “Gross value of taxable service”, Education Cess @ 2% on the service tax amount, and Secondary and Higher Education Cess @ 1% on the service tax amount.

Who is liable to pay Service taxWho is liable to pay Service tax• Normally, the ‘person’ who provides the taxable service

on receipt of service charges is responsible for paying the Service Tax to the Government (Sec.68 (1) of the Act).

• However in respect of services covered under reverse charge category, the service recipient is required to pay service tax.

• With the introduction of Point of taxation Rule 2011, service tax liability arises if service is provided & invoice is raised , though the amount is paid latter.

What is Reverse ChargeWhat is Reverse Charge• Service tax being an Indirect tax akin to Excise duty or VAT it

is payable by the Service providers who in turn collect the same from recipient.

• But Govt. has notified certain services where in service recipient is required to deposit the service tax. This is what called reverse charge.

• The burden to DEPOSIT service tax shifted from service provider to recipient.

• Liability to pay service tax is both on service provider as well as on recipient ( PARTIAL REVERSE CHARGE)

• Liabilities of both the service provider and service receiver are independent of each other.

• Small scale benefit available only to the service provider, if entitled.

• Service tax liability on the part of service recipient arises even if a very nominal amount is paid.

Services covered under reverse Services covered under reverse charge categorycharge category

• Transportation of Goods by Road• Hiring of any motor vehicle designed to carry

passenger• Supply of manpower for any purpose including

security/detective agency service• Works contract service• Service provided by Advocate• Service provided by arbitral tribunal• Support service provided by Govt or local

authorities

TaxabilityTaxability

• Service tax is levied @12.36% on the value of all services, other than those services specified in the negative list , provided or agreed to be provided in the taxable territories.

• Taxable Territories = India – J & K

Major Changes in Service Tax law Major Changes in Service Tax law by Finance Act 2012by Finance Act 2012

• Rate change from 10% to 12%

• Introduction of Negative list concept in service tax (Exempted service).

• Scope of Reverse charge category services widened.

• Introduction of Partial reverse charge

Consequence of Changes in service tax lawConsequence of Changes in service tax law

• Mandatory registration under service tax for Service recipient.

• Service recipient is now required to deposit service tax FOR REVERSE CHARGE CATEGORY SERVICES.

• Additional financial burden on service recipient.

• Additional statutory compliance for service recipient.

• Huge revenue for Govt.

Service tax liability under reverse Service tax liability under reverse charge categorycharge category

Sl. No.

Description of services Liability of service

provider (%)

Liability of service

recipient (%)

01 Transportation of goods by road Nil 100

02 Hiring of any motor vehicle designed to carry passenger

(on abated value) Nil 100

03 Hiring of any motor vehicle designed to carry passenger

(on Full value) 60 40

04 Supply of Manpower for any purpose including security services.

25 75

Service tax liability under reverse Service tax liability under reverse charge categorycharge category

Sl. No. Description of services Liability of service provider (%)

Liability of service recipient (%)

05 Works contract services 50 50

06 Services provided by advocate

Nil 100

07 Service provided by Govt. or local authority.

Nil 100

08 Support service provided by arbitral tribunal

Nil 100

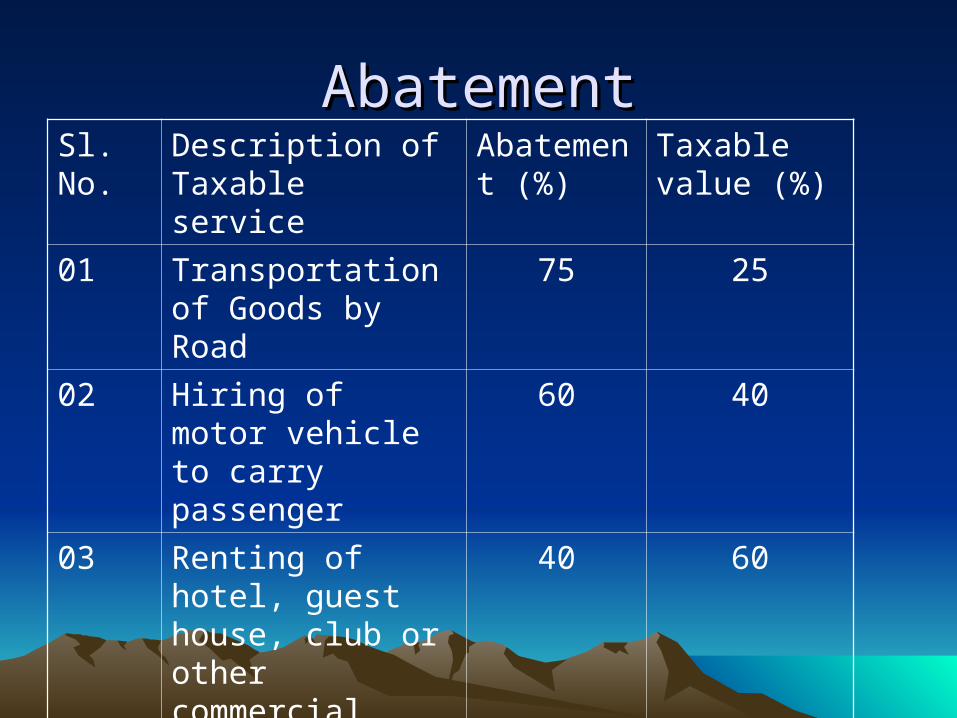

AbatementAbatementSl. No.

Description of Taxable service

Abatement (%)

Taxable value (%)

01 Transportation of Goods by Road

75 25

02 Hiring of motor vehicle to carry passenger

60 40

03 Renting of hotel, guest house, club or other commercial place for residential or lodging

40 60

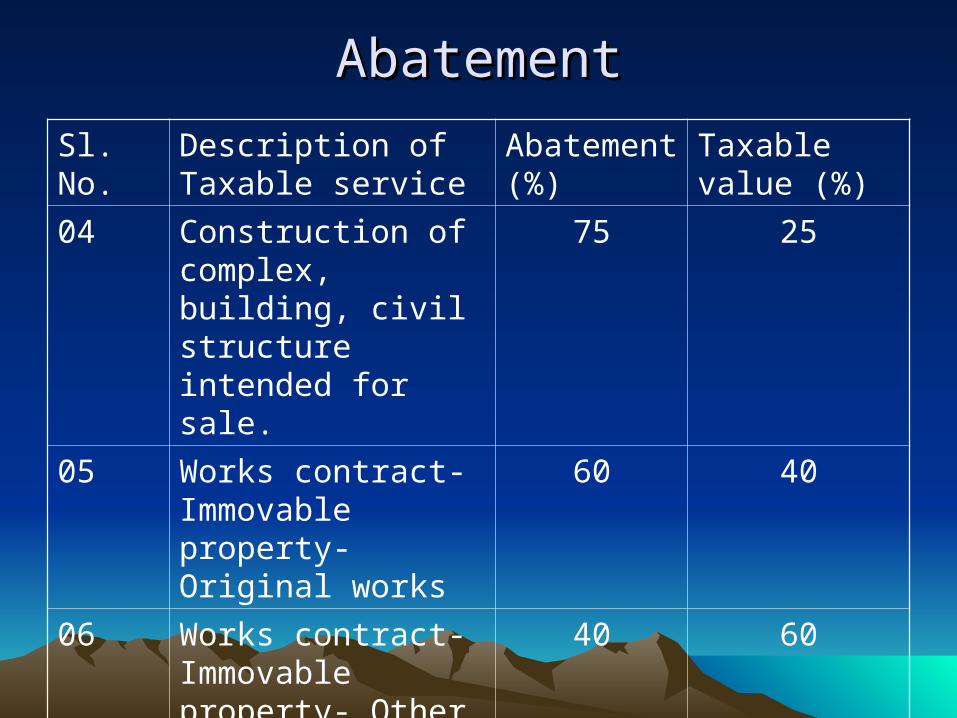

AbatementAbatement

Sl. No. Description of Taxable service

Abatement (%)

Taxable value (%)

04 Construction of complex, building, civil structure intended for sale.

75 25

05 Works contract- Immovable property- Original works

60 40

06 Works contract- Immovable property- Other works (finishing, repair etc)

40 60

AbatementAbatement

Sl. No. Description of Taxable service

Abatement (%)

Taxable value (%)

07 Works contract- Movable property- Repair & maintenance

30 70

08 Transport of passenger by Air

60 40

09 Transport of goods by Rail

70 30

What is Negative ListWhat is Negative List

• Till 30.06.2012 , the definition of Service tax was inclusive in nature.

• It means only those services were taxable which are specified in Sec 65 of Finance Act 1994 as amended from time to time.

• But with the introduction of concept of Negative list, barring the 39 services, all other services are now taxable w.e.f 01.07.2012.

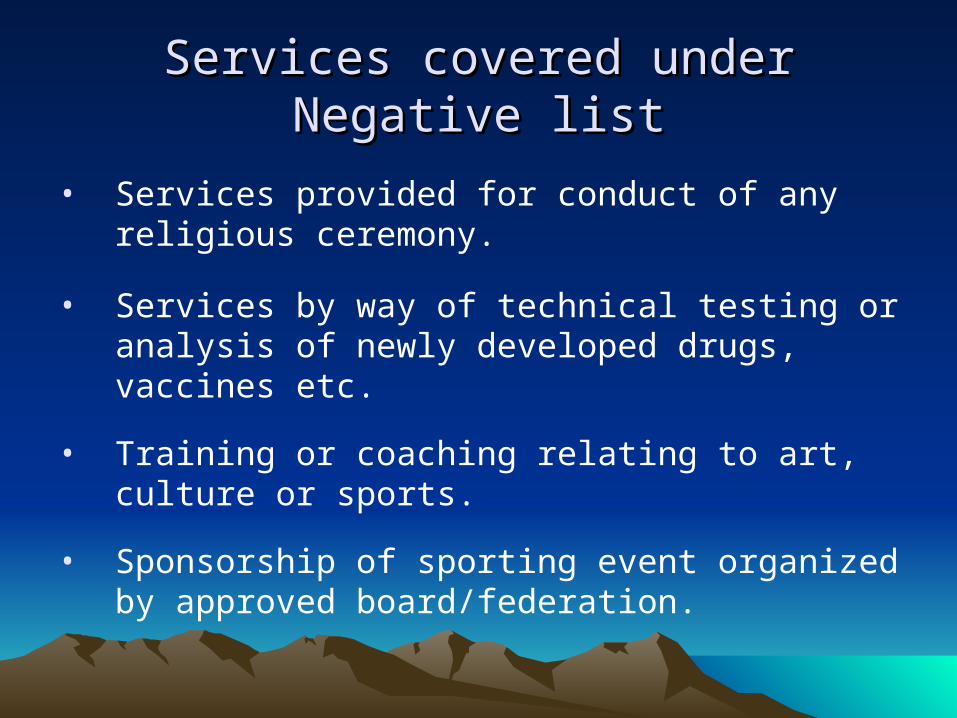

Services covered under Negative listServices covered under Negative list

• Services provided for conduct of any religious ceremony.

• Services by way of technical testing or analysis of newly developed drugs, vaccines etc.

• Training or coaching relating to art, culture or sports.

• Sponsorship of sporting event organized by approved board/federation.

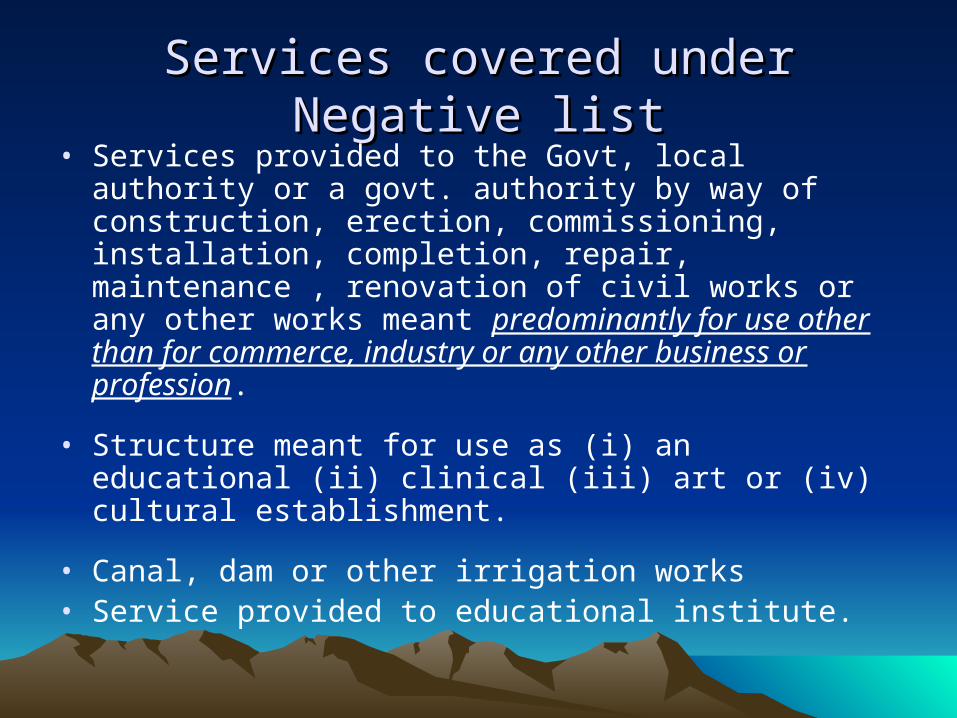

Services covered under Negative listServices covered under Negative list• Services provided to the Govt, local authority or a govt.

authority by way of construction, erection, commissioning, installation, completion, repair, maintenance , renovation of civil works or any other works meant predominantly for use other than for commerce, industry or any other business or profession.

• Structure meant for use as (i) an educational (ii) clinical (iii) art or (iv) cultural establishment.

• Canal, dam or other irrigation works• Service provided to educational institute.

Services covered under Negative listServices covered under Negative list• Services provided by way of construction,

erection, commissioning, installation, completion, repair, maintenance , renovation of Road, bridge, tunnel or terminal for use by general public.

• Structure meant for funeral, burial or cremation of deceased.

• Services provided by way of construction, erection, commissioning, installation, completion, repair, maintenance , renovation of

Airport, port, railways or metro.

Services covered under Negative listServices covered under Negative list

• Post harvest storage infrastructure for agricultural produce such as cold storage etc.

• Services by way of collecting or providing news by an independent journalist, PTI.

• Services by way of renting of a hotel, guest house, club or commercial places for residential or lodging purpose charging below Rs.1000 per day.

• Services provide in relation to serving of food or beverage by a restaurant or mess ( non air -conditioned)

Services covered under Negative listServices covered under Negative list

• Services provided by goods transport agency for transportation of fruits, vegetables, egg, milk, food grain or pulses.

• Amount charged for transportation by single goods carriage is less than Rs.1500. (Multiple Rs.750).

• Transportation of passenger by air terminating at North eastern region or by a contract carriage for transportation of passenger excluding tourism and by Rope way, tram way

• Vehicle parking for general public.

Hiring of VehicleHiring of Vehicle• Prior to 01.07.2012, service tax on hiring of

vehicle was responsibility of vehicle owner.

• Now the same has been covered under reverse charge category. As such liability to deposit service tax is on service recipient .

• Service tax payable by service receipient comes to Value*0.4*12.36 =Value*4.944%.

R & M Contract (Only labour)R & M Contract (Only labour)• R & M contract such as R &M of office,

guest house etc. is management or maintenance service and not covered under Reverse charge category.

• Though R & M contract as R & M of Guest house, office, hospital, electrical installation involves only labour, it can not be construed as Manpower Supply.

• Therefore service tax liability is on the part of service provider.

R & M Contract/ Works contractR & M Contract/ Works contract(Both labour & Material)(Both labour & Material)

• The R & M may be either for movable assets or for Immovable asset.

• Covered under partial reverse charge category.• Service tax liability both for service provider as well as

service receipient.

• If the labour component can not be separated, it will be treated as works contract.

• Abatement will apply.• Immovable property : Original works 40% (taxable value)• : Other works 60% (taxable value)• Movable property : 70% ( taxable value)

Thank U