Embed Size (px)

Citation preview

Creating and Protecting Ownership and Economic Opportunity | www.self-help.org

NEW MARKETS TAX CREDITS BORROWER ELIGIBILITY • APRIL 5, 2017

Creating and Protecting Ownership and Economic Opportunity | www.self-help.org 2

National CDFI with a mission to create ownership and economic opportunity for all

Affiliated orgs: Self-Help Ventures Fund, Self-Help Credit Union, Self-Help Federal Credit Union, Center for Responsible Lending

Business lines: commercial loans, home loans, retail services, real estate development, policy research

46 locations in North Carolina, California, Florida and Chicago, Self-Help has made $7 billion in loans: 25% in rural areas, 71% in designated low-income areas and 70% to communities of color.

Self-Help Overview

Creating and Protecting Ownership and Economic Opportunity | www.self-help.org

NMTC LENDER

3

SHVF has received $328 million in NMTC allocation over 6 rounds

$411 million deployed through revolving loan pools, or 125% of our allocation funded to date

160 NMTC loans across 18 states, 20% in non-metro areas

Borrowers 58% nonprofit or coop; 41% led by people of color

Self-Help NMTC Lending

Creating and Protecting Ownership and Economic Opportunity | www.self-help.org

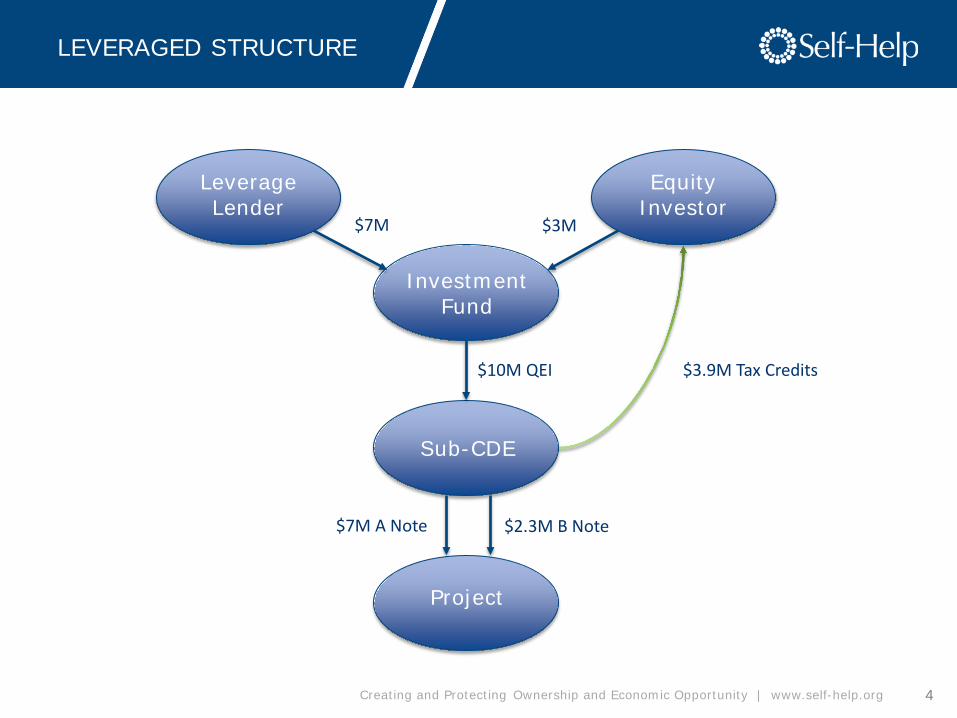

LEVERAGED STRUCTURE

4

Leverage Lender

Equity Investor

Investment Fund

Sub-CDE

Project

$7M $3M

$10M QEI

$2.3M B Note

$3.9M Tax Credits

$7M A Note

Creating and Protecting Ownership and Economic Opportunity | www.self-help.org

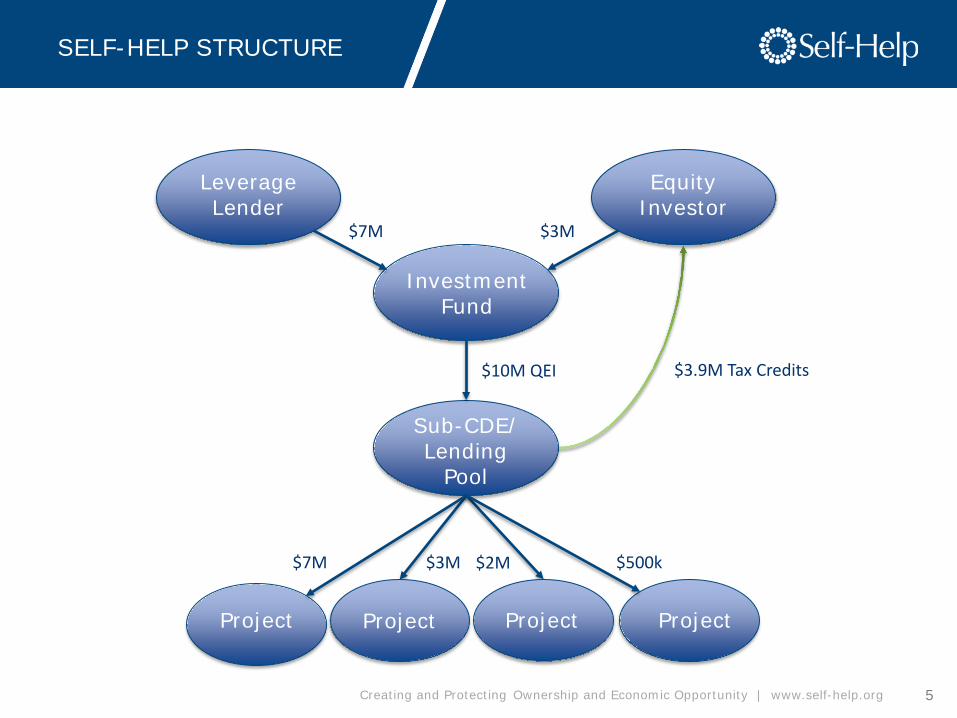

SELF-HELP STRUCTURE

5

Leverage Lender

Equity Investor

Investment Fund

Sub-CDE/ Lending

Pool

Project Project

$10M QEI

$7M $3M

$7M $3M $500k

Project Project Project

$2M

$3.9M Tax Credits

Creating and Protecting Ownership and Economic Opportunity | www.self-help.org

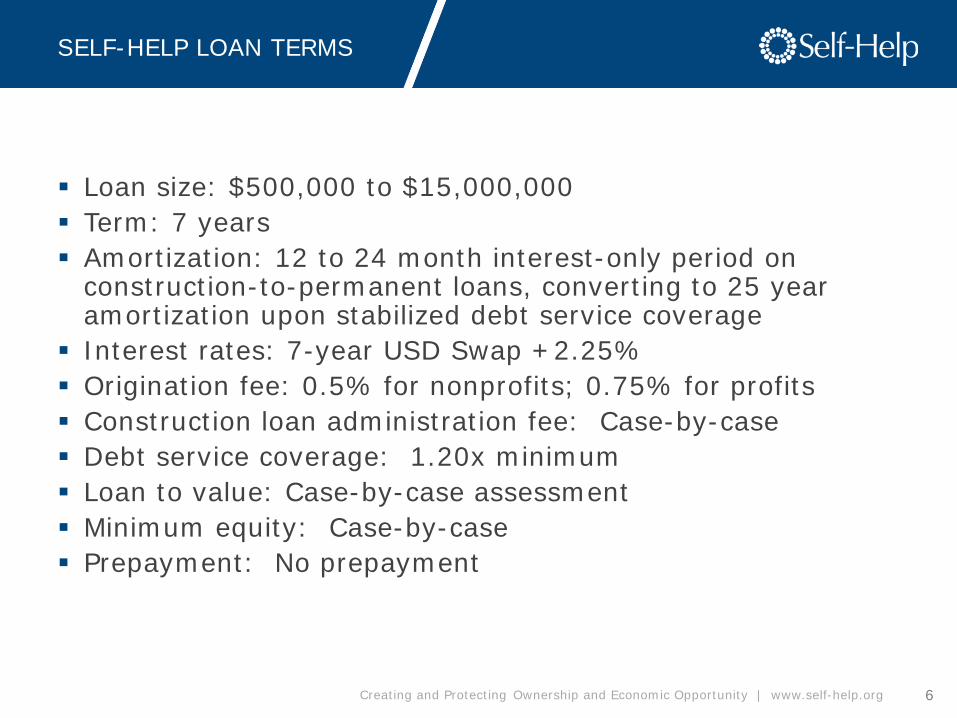

SELF-HELP LOAN TERMS

6

Loan size: $500,000 to $15,000,000 Term: 7 years Amortization: 12 to 24 month interest-only period on

construction-to-permanent loans, converting to 25 year amortization upon stabilized debt service coverage

Interest rates: 7-year USD Swap +2.25% Origination fee: 0.5% for nonprofits; 0.75% for profits Construction loan administration fee: Case-by-case Debt service coverage: 1.20x minimum Loan to value: Case-by-case assessment Minimum equity: Case-by-case Prepayment: No prepayment

Creating and Protecting Ownership and Economic Opportunity | www.self-help.org

NMTC LOAN EXAMPLE

7

Eastern Carolina Organics (ECO)

Creating and Protecting Ownership and Economic Opportunity | www.self-help.org

NMTC LOAN EXAMPLE

8

ECO is a women-led farmer owned cooperative produce distributor with seasonal cash flows

• Required 95% LTV to renovate 26,000 s.f. warehouse facility on a brownfield site as larger more centrally located home for ECO and 4 other sustainability-related business tenants

• In 2012, SHVF made a $1.24M NMTC loan in principal repaid from previous loans; 10 year loan, 4 years of NMTC subsidy and prepayment prohibition

• But for: ECO could not secure standard bank debt and needed additional subsidy to cash flow

Borrower Need

Creating and Protecting Ownership and Economic Opportunity | www.self-help.org

NMTC LOAN EXAMPLE

9

Promotes local-regional farm system, promotes organic growing

Creates a “food hub” for aligned businesses, including

Transformed a brownfield in a severely distressed neighborhood providing a larger, more centrally located home for ECO and 4 other sustainability-related business tenants

Provided 8 quality jobs to local residents. ECO covers 100% of health and dental premiums for full-time employees and provides 0% loans to families facing health crises.

ECO also delivers 80% of sales proceeds back to growers, a much higher percentage than is typical in the industry, which has the multiplier effect of supporting better jobs for farmers and their employees.

Community Impact

Creating and Protecting Ownership and Economic Opportunity | www.self-help.org

NMTC BORROWER

10

Began to develop, hold, and self-manage commercial real estate in 1991, with a focus on community revitalization in NC downtowns

SHVF has invested $73 million to redevelop more than 1.3 million square feet of office and retail space in 16 locations throughout North Carolina and Washington DC.

6 are NMTC projects; 10 are HTC projects.

Self-Help Commercial Real Estate Development

Creating and Protecting Ownership and Economic Opportunity | www.self-help.org

S-H AS BORROWER

11

Kent Corner

Creating and Protecting Ownership and Economic Opportunity | www.self-help.org

S-H AS BORROWER

12

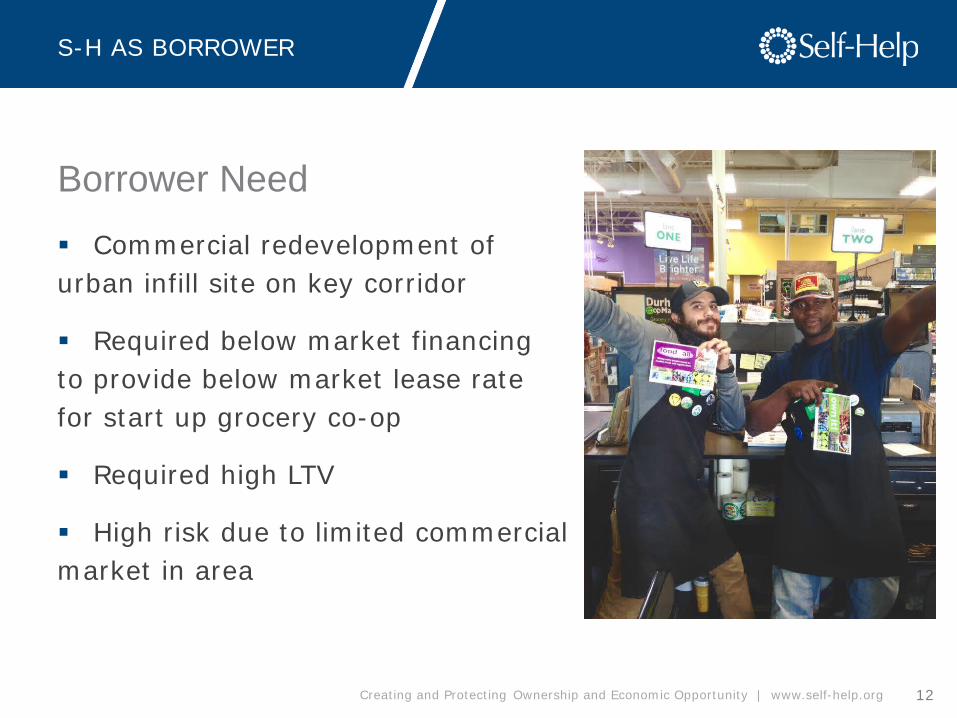

Commercial redevelopment of urban infill site on key corridor

Required below market financing to provide below market lease rate for start up grocery co-op

Required high LTV

High risk due to limited commercial market in area

Borrower Need

Creating and Protecting Ownership and Economic Opportunity | www.self-help.org

S-H AS BORROWER

13

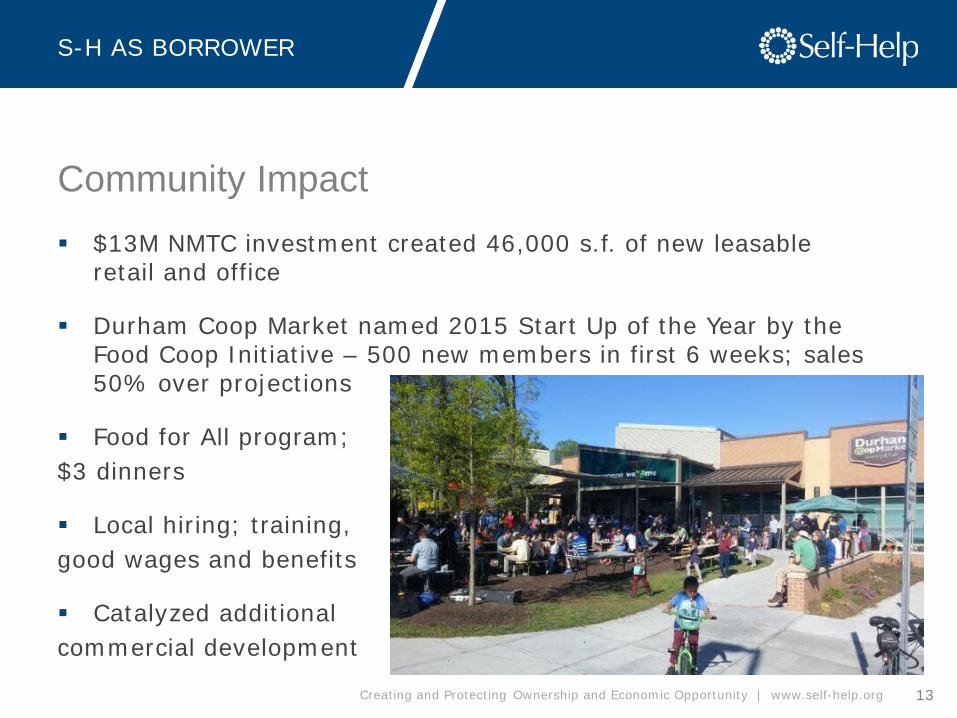

$13M NMTC investment created 46,000 s.f. of new leasable retail and office

Durham Coop Market named 2015 Start Up of the Year by the Food Coop Initiative – 500 new members in first 6 weeks; sales 50% over projections

Food for All program; $3 dinners

Local hiring; training, good wages and benefits

Catalyzed additional commercial development

Community Impact

Creating and Protecting Ownership and Economic Opportunity | www.self-help.org

ELIGIBILITY

14

Geography

Project

Borrower

3 Levels of Evaluation

Creating and Protecting Ownership and Economic Opportunity | www.self-help.org

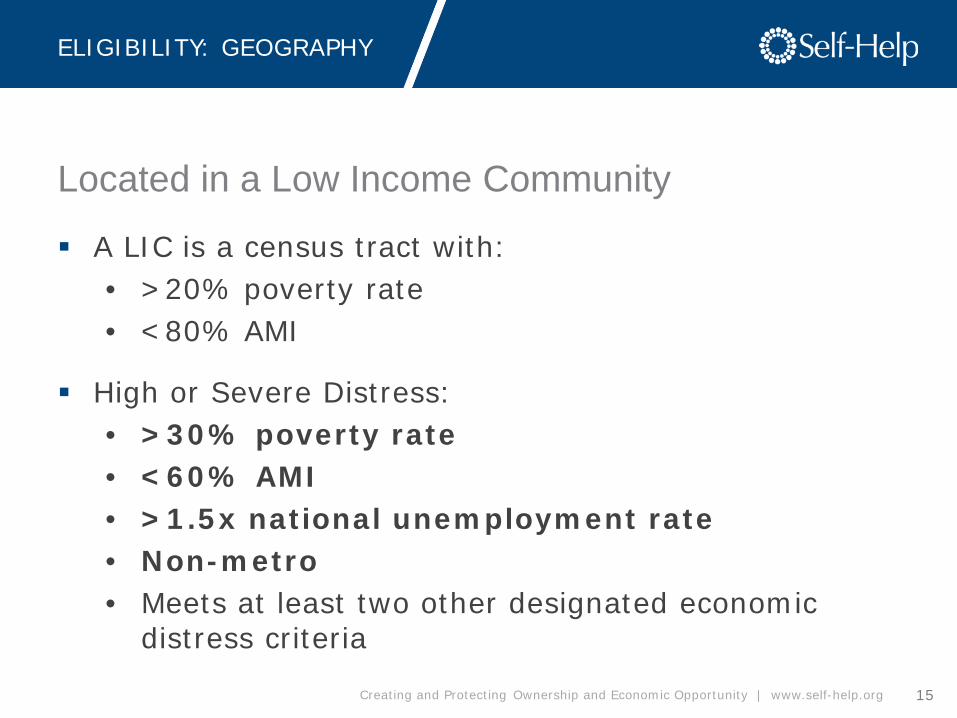

ELIGIBILITY: GEOGRAPHY

15

A LIC is a census tract with: • >20% poverty rate • <80% AMI

High or Severe Distress: • >30% poverty rate • <60% AMI • >1.5x national unemployment rate • Non-metro • Meets at least two other designated economic

distress criteria

Located in a Low Income Community

Creating and Protecting Ownership and Economic Opportunity | www.self-help.org

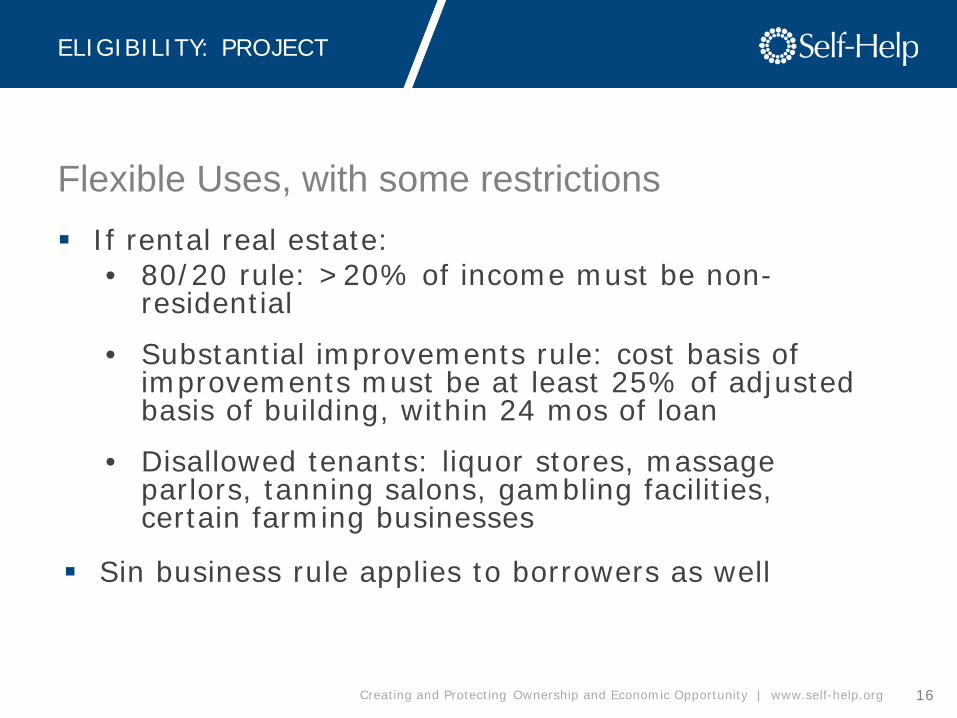

ELIGIBILITY: PROJECT

16

If rental real estate: • 80/20 rule: >20% of income must be non-

residential

• Substantial improvements rule: cost basis of improvements must be at least 25% of adjusted basis of building, within 24 mos of loan

• Disallowed tenants: liquor stores, massage parlors, tanning salons, gambling facilities, certain farming businesses

Sin business rule applies to borrowers as well

Flexible Uses, with some restrictions

Creating and Protecting Ownership and Economic Opportunity | www.self-help.org

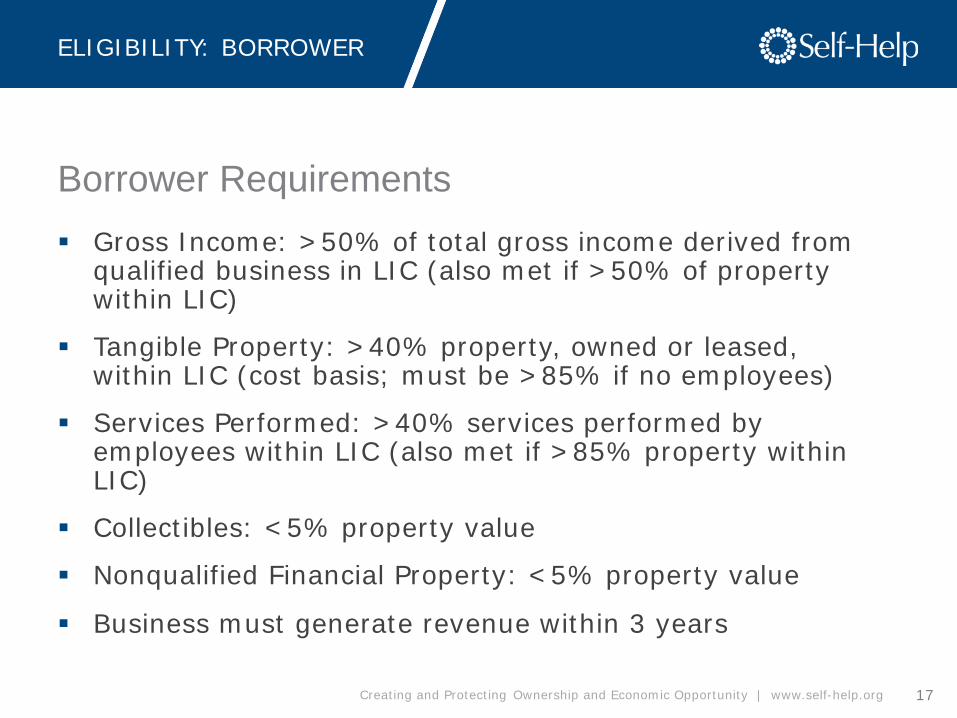

ELIGIBILITY: BORROWER

17

Gross Income: >50% of total gross income derived from qualified business in LIC (also met if >50% of property within LIC)

Tangible Property: >40% property, owned or leased, within LIC (cost basis; must be >85% if no employees)

Services Performed: >40% services performed by employees within LIC (also met if >85% property within LIC)

Collectibles: <5% property value

Nonqualified Financial Property: <5% property value

Business must generate revenue within 3 years

Borrower Requirements

Creating and Protecting Ownership and Economic Opportunity | www.self-help.org

ELIGIBILITY: EXPECTATIONS

18

A CDE must have a “reasonable expectation” that all eligibility requirements will continue to be met over NMTC compliance period

Most CDEs require annual certifications and reporting to document a borrower’s continued compliance

Reasonable Expectations Test

Creating and Protecting Ownership and Economic Opportunity | www.self-help.org

BECOME A BORROWER

19

Compelling, measurable community impact, measured in terms of: • jobs creation, quality, accessibility • providing goods and services where they were

lacking (education, health care, fresh food)

Ready to go • Other sources of funding are committed • Approvals are in place

Who gets to the top of the queue?

Creating and Protecting Ownership and Economic Opportunity | www.self-help.org

LINGO REVIEW

20

NMTC – New Markets Tax Credit

CDE – Community Development Entity is eligible to become a NMTC allocatee

QEI – Qualified Equity Investment triggers tax credit return

QLICI – Qualified Low Income Community Investment

QALICB – Qualified Active Low Income Community Business

Creating and Protecting Ownership and Economic Opportunity | www.self-help.org

CONTACTS

21

Amanda Frazier Wong NMTC Director 864-952-6320 [email protected] Eligibility & general NMTC program questions Steve Saltzman Senior Loan Officer 919-956-4620 [email protected] Charter Schools & Healthy Foods Loans Allison Moy Underwriter 919-956-4414 [email protected] Commercial Real Estate Loans Donnetta Collier Charlotte Area 704-409-5913 [email protected]