Embed Size (px)

Citation preview

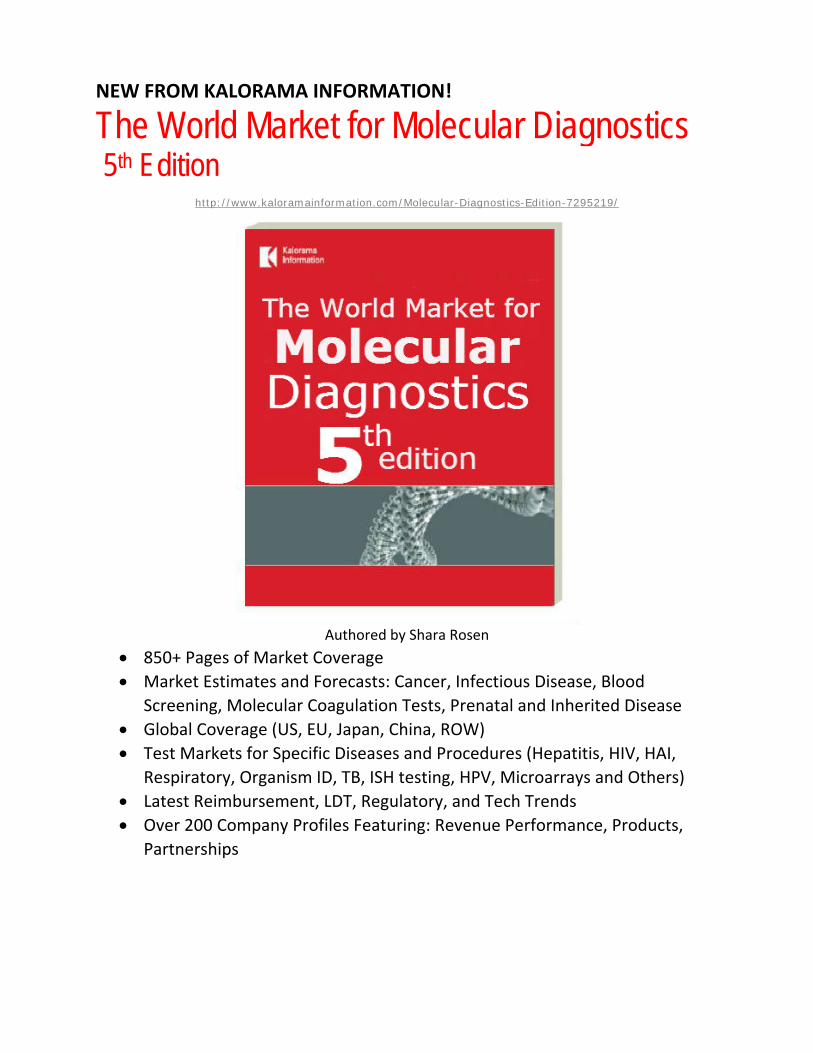

NEW FROM KALORAMA INFORMATION!

The World Market for Molecular Diagnostics 5th Edition

http://www.kaloramainformation.com/Molecular-Diagnostics-Edition-7295219/

Authored by Shara Rosen

• 850+ Pages of Market Coverage • Market Estimates and Forecasts: Cancer, Infectious Disease, Blood

Screening, Molecular Coagulation Tests, Prenatal and Inherited Disease • Global Coverage (US, EU, Japan, China, ROW) • Test Markets for Specific Diseases and Procedures (Hepatitis, HIV, HAI,

Respiratory, Organism ID, TB, ISH testing, HPV, Microarrays and Others) • Latest Reimbursement, LDT, Regulatory, and Tech Trends • Over 200 Company Profiles Featuring: Revenue Performance, Products,

Partnerships

OVER 200 Company Profiles The Intense Competitor Focus In This Report Includes:

What Major Diagnostic Companies are Doing In Molecular DX

Abbott Diagnostics Alere

ARKRAY Beckman Coulter Inc./Danaher Becton, Dickinson and Company

bioMérieux Inc. Bio‐Rad Laboratories Inc. Gen‐Probe Inc./Hologic

Hologic, Inc. Instrumentation Laboratory Ortho Clinical Diagnostics

QIAGEN N.V. Roche Diagnostics

Siemens Healthcare Diagnostics Sysmex Corporation

Thermo Fisher Scientific Inc.

Status of Molecular Diagnostic Focused Companies Alacris Theranostics GmbH

Astra Biotech GmbH Autogenomics Inc.

Biocartis SA Biofortuna Ltd.

Biotype Diagnostic GmbH BlueGnome DiaGenic ASA DiagnoCure

ELITech Group EraGen Biosciences Inc.

Genetic Technologies Limited GenMark Diagnostics Inc.

Helicos BioSciences IRIS International, Inc. Luminex Corporation

Meridian Bioscience, Inc. Nanosphere, Inc.

Sony DADC Biosciences TrimGen Genetic Technology

TrovaGene, Inc.

New Innovators To Watch! Ahram Biosystems, Inc. Allegro Diagnostics Corp. Amoy Diagnostics Co. Ltd.

Anagnostics Bioanalysis GmbH

Applied BioCode, Inc. ArcticDx Inc.

Ariosa Diagnostics Axela Inc.

BioHelix Corporation BioNanomatrix/ BioNano Genomics

BJS Biotechnologies DiagCor Bioscience Inc. Ltd. DxTerity Diagnostics Inc.

Epistem plc Exiqon A/S Exonhit

GeneNews Limited Genome Diagnostics BV

Genomica S.A.U. Genorama Ltd. GnuBIO, Inc.

Great Basin Corporation Health Discovery Corporation

IncellDx, Inc. Insight Genetics IntegenX Inc.

Linkage Biosciences, Inc. Med BioGene, Inc.

Multiplicom NABsys, Inc.

Nanostring Technologies, Inc. NIPD Genetics Ltd OptiGene Ltd

Orion Genomics Oxford Gene Technology

PrimeraDx Rheonix Inc.

Skyline Diagnostics B.V. Spartan Bioscience Inc. Stratos Genomics Inc. VolitionRx Limited

WaferGen Biosystems, Inc.

And Many Other Companies…

http://www.kaloramainformation.com/Molecular-Diagnostics-Edition-7295219/

World Market for Molecular Diagnostics

5th

Kalorama InformationA division of MarketResearch.com

38 East 29th Street Sixth FloorNew York, New York 10016

212.807.2660 t800.298.5603 t212.807.2676 f

www.kaloramainformation.com

Copyright © 2013 Kalorama Information Reproduction without prior written permission, in any media now in existence or hereafter developed,

in whole or in any part, is strictly prohibited.

THE WORLD MARKET FOR MOLECULAR DIAGNOSTICS, 5TH EDITION

A KALORAMA INFORMATION MARKET INTELLIGENCE REPORT

The World Market for Molecular Diagnostics has been prepared by Kalorama Information. We serve business and industrial clients in the United States and abroad with a complete line of information services and research publications.

Kalorama Information Market Intelligence Reports are specifically designed to aid the action-oriented executive by providing a thorough presentation of essential data and concise analysis.

Author: Shara Rosen Publication Date: January 2013

Copyright © 2013 Kalorama Information

Reproduction without prior written permission, in any media now in existence or hereafter developed, in whole or in any part, is strictly prohibited.

T A B L E O F C O N T E N T S

CHAPTER ONE: EXECUTIVE SUMMARY ..........................................................1 Introduction ......................................................................................................................... 1

Scope and Methodology ...................................................................................................... 4

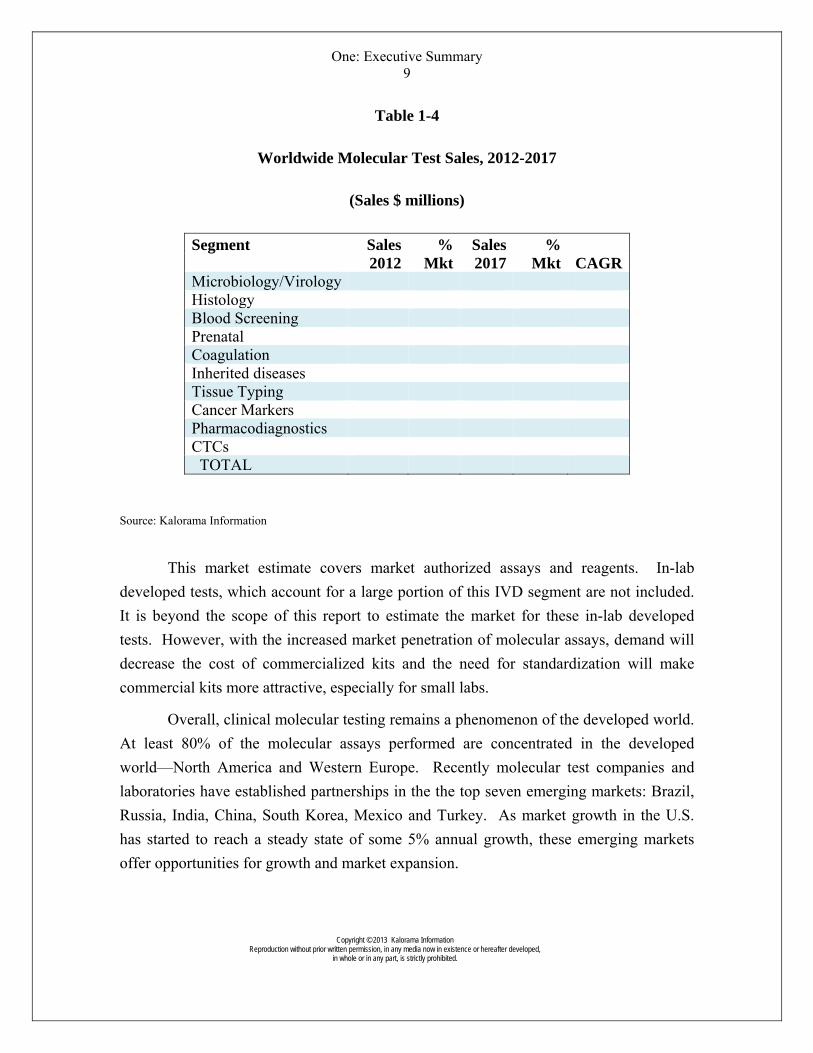

Size and Growth of the Market ......................................................................................... 7

Market Trends .................................................................................................................. 11

CHAPTER TWO: INTRODUCTION .....................................................................15 Background ....................................................................................................................... 15

Developments since 2000 ............................................................................................... 16 New Platforms ................................................................................................................ 18 Test Quality Control ....................................................................................................... 24

Building a Strong Future .................................................................................................. 27 The Service Industry Makes Gains ................................................................................. 27 The $1000 Genome ......................................................................................................... 30 Information Technology and “Apps” ............................................................................. 32 Miniaturization and Multiplexed Assays ........................................................................ 35 Integrated Sample–to-Results Testing ............................................................................ 37 Mass Spectrometry ......................................................................................................... 38

Tests and Technologies in 2012 ........................................................................................ 42

CHAPTER THREE: THE COMMERCIALIZATION CONUNDRUM .............49 Background ....................................................................................................................... 49

Commercialization of Molecular Tests ........................................................................... 51

Regulatory Issues and Molecular Assays ........................................................................ 54

Patent Litigation Abounds ............................................................................................... 57 Consumer, Payer and Physician Acceptance .................................................................. 61 Clinical Molecular Test Reimbursement Coding in The U.S. ........................................ 64

CHAPTER FOUR: SEQUENCING – HYPE AND REALITY ............................69 Background ....................................................................................................................... 69

Companies and Technologies ......................................................................................... 71 PCR Not Ready To Take the Back Seat ......................................................................... 80 Pathogen sequencing ...................................................................................................... 86 Prenatal Fetal Chromosomal Analysis ............................................................................ 87

CHAPTER FIVE: MARKET ANALYSIS: WORLD MARKETS .......................91 Background ....................................................................................................................... 91

Market Estimate and Forecast by Region ...................................................................... 92

Copyright © 2013 Kalorama Information

Reproduction without prior written permission, in any media now in existence or hereafter developed, in whole or in any part, is strictly prohibited.

The United States .............................................................................................................. 97 RUO/IUO Issues ............................................................................................................. 98 The Patient Protection and Affordable Care Act ............................................................ 98 Accountable Care Organizations .................................................................................. 100

Europe .............................................................................................................................. 101 IVD Directive Update ................................................................................................... 105

China ................................................................................................................................ 107

India ................................................................................................................................. 110

CHAPTER SIX: THE MARKET FOR BLOOD MARKERS IN CANCER .....113 Overview .......................................................................................................................... 113

Methylation Patterns ..................................................................................................... 113 Other Tests .................................................................................................................... 114

Blood Molecular Test Market and Forecasts ............................................................... 115 LDTs ............................................................................................................................. 115 Radiotherapy Testing .................................................................................................... 116

CHAPTER SEVEN: THE MARKET FOR MOLECULAR ASSAYS IN HEMATOLOGY......................................................................................................121

Flow Cytometry ............................................................................................................... 122

CHAPTER EIGHT: THE MARKET FOR MOLECULAR ASSAYS IN COAGULATION AND CARDIAC CARE ...........................................................127

Thrombophilia SNPs ...................................................................................................... 127 MTHFR ........................................................................................................................ 128 Factor V ........................................................................................................................ 128 CYP4V2 ........................................................................................................................ 128 Market and Forecast ..................................................................................................... 129 Coagulation Molecular Research Projects .................................................................... 129

Pharmacodiagnostics ...................................................................................................... 130 Market for PGx testing ................................................................................................. 133 Plavix Testing ............................................................................................................... 134

CHAPTER NINE: HISTOLOGY AND CYTOLOGY ........................................137 Overview .......................................................................................................................... 137

in situ hybridization ........................................................................................................ 140

HPV Testing .................................................................................................................... 144 Tissue Microarrays ....................................................................................................... 148 Circulating Tumor Cells ............................................................................................... 150 Chromosome Analysis .................................................................................................. 155 Pharmacodiagnostic Histology ..................................................................................... 158

Copyright © 2013 Kalorama Information

Reproduction without prior written permission, in any media now in existence or hereafter developed, in whole or in any part, is strictly prohibited.

CHAPTER TEN: MICROBIOLOGY AND VIROLOGY ..................................165 Overview .......................................................................................................................... 165

Microbiology Market and Forecast ............................................................................... 166 Role of ID Testing in the Molecular Diagnostics Market ............................................. 167 Markets for Specific Infectious Disease Tests .............................................................. 168

Genome Sequencing ........................................................................................................ 170 Roche, Illumina and Life .............................................................................................. 171 Other Systems ............................................................................................................... 171

Mass Spectrometry ......................................................................................................... 173 Major Companies .......................................................................................................... 174 Market Estimate ............................................................................................................ 175

Blood Culture .................................................................................................................. 176 HIV ............................................................................................................................... 179 Market and Forecast ..................................................................................................... 179

Hepatitis ........................................................................................................................... 182 Market and Forecast ..................................................................................................... 182 Sexually Transmitted Diseases (STDs) ........................................................................ 184 Hospital Acquired Infections (HAIs) ............................................................................ 187 Market and Forecast ..................................................................................................... 190 Respiratory Tract Infections ......................................................................................... 191

Tuberculosis ..................................................................................................................... 195 Market and Forecast ..................................................................................................... 196

Fungal Infections ............................................................................................................. 200

CHAPTER ELEVEN: THE MARKET FOR MOLECULAR ASSAYS IN BLOOD TRANSFUSION MEDICINE .................................................................................203

Blood Pathogen Screening .............................................................................................. 204 Market and Forecast ..................................................................................................... 204

Blood Typing ................................................................................................................... 208 Molecular Blood Typing ............................................................................................... 211

CHAPTER TWELVE: THE MARKET FOR MOLECULAR ASSAYS IN ORGAN TRANSPLANT MANAGEMENT .........................................................................213

HLA Typing ..................................................................................................................... 213 Stem Therapy Matching ............................................................................................... 214 HLA Market and Forecast ............................................................................................ 216

Copyright © 2013 Kalorama Information

Reproduction without prior written permission, in any media now in existence or hereafter developed, in whole or in any part, is strictly prohibited.

CHAPTER THIRTEEN: THE MARKET FOR MOLECULAR ASSAYS IN PRENATAL AND NEONATAL TESTING .........................................................219

Overview .......................................................................................................................... 219

Market and Forecast ....................................................................................................... 221

FISH testing ..................................................................................................................... 222 Other Developments ..................................................................................................... 224

Neonatal Testing .............................................................................................................. 230

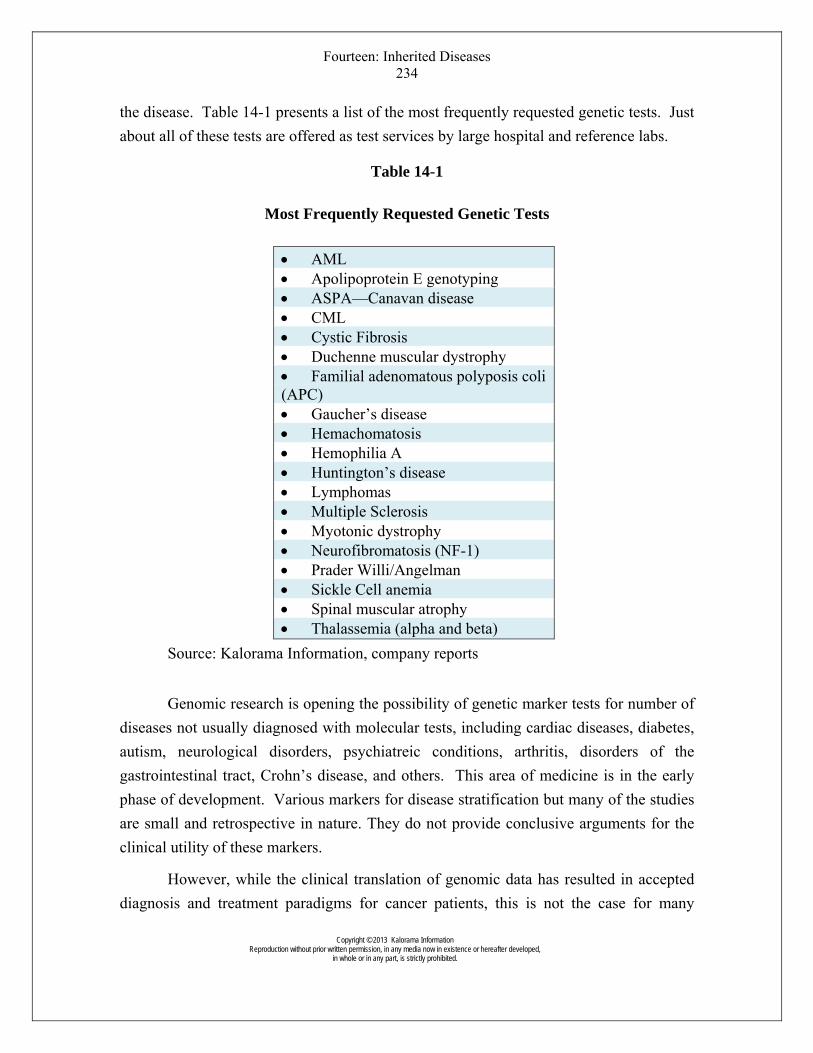

CHAPTER FOURTEEN: THE MARKET FOR MOLECULAR ASSAYS FOR INHERITED DISEASES ........................................................................................233

Arthritis ........................................................................................................................... 239

Gastrointestinal Conditions ........................................................................................... 241

Diabetes ............................................................................................................................ 242

Cardiovascular Disease................................................................................................... 246

Alzheimer’s Disease ........................................................................................................ 249

Parkinson’s Disease ........................................................................................................ 251

Psychiatric Disorders ...................................................................................................... 253

Autism .............................................................................................................................. 259

CHAPTER FIFTEEN: CONCLUSIONS AND STRATEGIC IMPLICATIONS – 2012 AND BEYOND ................................................................................................261

Expectations and Realities .............................................................................................. 261

Four Issues That Will Impact Market Success ............................................................. 263

CHAPTER SIXTEEN: COMPETITIVE ANALYSIS .........................................265 Companies and Vendors to Watch ................................................................................ 265

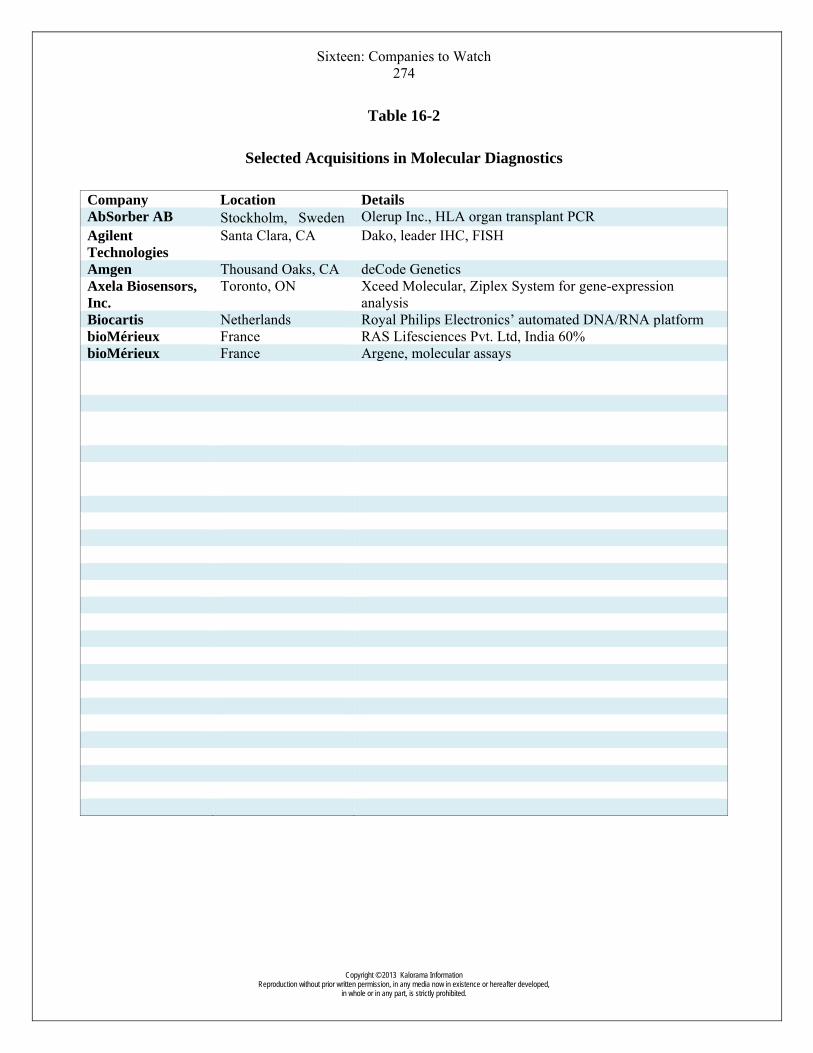

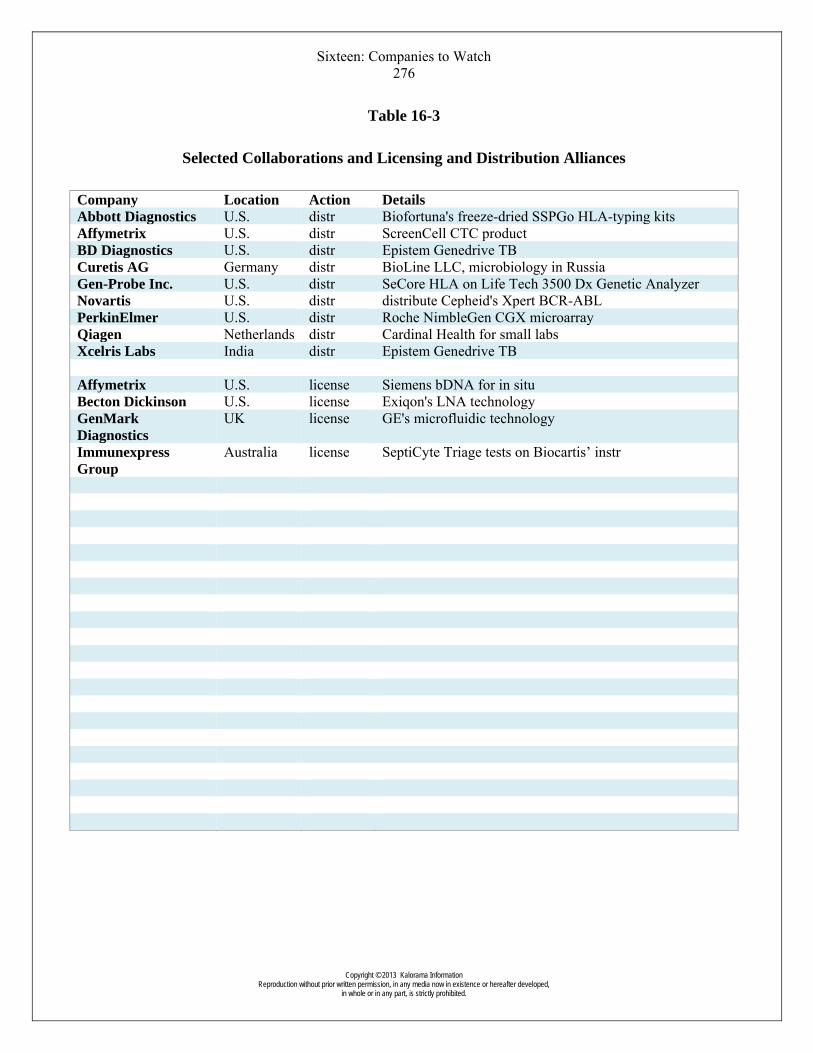

Acquisitions, Alliances and Collaborations .................................................................. 272

Looking Beyond Borders ................................................................................................ 277

CHAPTER SEVENTEEN: COMPANY PROFILES: TOP TIER IVD COMPANIES’ MOLECULAR BUSINESSES .....................................................279

Abbott Diagnostics .......................................................................................................... 280 Recent Revenue History ............................................................................................... 280 HLA .............................................................................................................................. 281 Molecular Histology ..................................................................................................... 281 Companion Tests .......................................................................................................... 282

Copyright © 2013 Kalorama Information

Reproduction without prior written permission, in any media now in existence or hereafter developed, in whole or in any part, is strictly prohibited.

Molecular Diagnostics .................................................................................................. 283 Infectious Diseases - Molecular .................................................................................... 286 IntelligentMDx Alliance ............................................................................................... 287 PLEX-ID ....................................................................................................................... 288

Alere ................................................................................................................................. 290 Recent Revenue History ............................................................................................... 290 ARKRAY ..................................................................................................................... 293

Beckman Coulter Inc./Danaher ......................... ........................................................... 294 Recent Revenue History ............................................................................................... 294 Instrumentation ............................................................................................................. 295

Becton, Dickinson and Company (BD) ......................................................................... 297 Recent Revenue History ............................................................................................... 297 The BD MAX Enterprise .............................................................................................. 298 Viper System ................................................................................................................ 300 Molecular Microbiology ............................................................................................... 300 BD GeneOhm ............................................................................................................... 301 Histology ...................................................................................................................... 301 Oncology, etc. ............................................................................................................... 302

bioMérieux Inc. ............................................................................................................... 304 Recent Revenue History ............................................................................................... 304 Molecular Oncology ..................................................................................................... 305 The Biocartis Program .................................................................................................. 306 Molecular Microbiology ............................................................................................... 307 NucliSENS .................................................................................................................... 307 Product Development ................................................................................................... 308

Bio-Rad Laboratories Inc. .............................................................................................. 309 Recent Revenue History ............................................................................................... 309

Gen-Probe Inc. ................................................................................................................ 311 Recent Revenue History ............................................................................................... 311 Product development .................................................................................................... 312 Expansion ..................................................................................................................... 313 Prostate Cancer ............................................................................................................. 314 STDs ............................................................................................................................. 315 Panther System ............................................................................................................. 315 HPV .............................................................................................................................. 316 Transplant/HLA testing ................................................................................................ 317 Infectious Diseases ....................................................................................................... 318 Blood Bank ................................................................................................................... 318

Hologic, Inc. ..................................................................................................................... 320 Recent Revenue History ............................................................................................... 320

Instrumentation Laboratory (IL) .................................................................................. 323 Recent Revenue History ............................................................................................... 323

Ortho Clinical Diagnostics ............................................................................................. 324 Recent Revenue History ............................................................................................... 324

Copyright © 2013 Kalorama Information

Reproduction without prior written permission, in any media now in existence or hereafter developed, in whole or in any part, is strictly prohibited.

QIAGEN N.V. .................................................................................................................. 325 Recent Revenue History ............................................................................................... 325 Market Expansion ......................................................................................................... 327 Histology ...................................................................................................................... 329 Infectious diseases ........................................................................................................ 329 Rotor-Gene ................................................................................................................... 330 Oncology/Personalized Medicine ................................................................................. 331 TB ................................................................................................................................. 334 HPV .............................................................................................................................. 335 HLA .............................................................................................................................. 336 Automation for the Future ............................................................................................ 336 Women’s Health ........................................................................................................... 337 Point of Care ................................................................................................................. 338 Sequencing .................................................................................................................... 340

Roche Diagnostics ........................................................................................................... 342 Recent Revenue History ............................................................................................... 342 Miscellaneous ............................................................................................................... 344 Viral Load ..................................................................................................................... 345 STDs ............................................................................................................................. 346 Companion Tests .......................................................................................................... 347 Sample Preparation ....................................................................................................... 350 Tissue Diagnostics ........................................................................................................ 350 Blood Bank ................................................................................................................... 351 Sequencing .................................................................................................................... 352 Microarrays ................................................................................................................... 354

Siemens Healthcare Diagnostics .................................................................................... 355 Recent Revenue History ............................................................................................... 355 Histology ...................................................................................................................... 356 Molecular ...................................................................................................................... 356 Sequencing .................................................................................................................... 357 Companion Tests .......................................................................................................... 358

Sysmex Corporation ....................................................................................................... 359 Recent Revenue History ............................................................................................... 359

Thermo Fisher Scientific Inc. ......................................................................................... 361 Recent Revenue History ............................................................................................... 361 Allergy .......................................................................................................................... 363

CHAPTER EIGHTEEN: COMPANY PROFILES: MAJOR MOLECULAR TEST COMPANIES ...........................................................................................................365

Affymetrix, Inc. ............................................................................................................... 366 Histology ...................................................................................................................... 369 Whole Genome Analysis .............................................................................................. 371

Agilent Technologies Inc. ............................................................................................... 373 Research Products ......................................................................................................... 375

Copyright © 2013 Kalorama Information

Reproduction without prior written permission, in any media now in existence or hereafter developed, in whole or in any part, is strictly prohibited.

Asuragen, Inc. .................................................................................................................. 377 Oncology ...................................................................................................................... 377 Inherited Diseases ......................................................................................................... 380 Controls ........................................................................................................................ 381 Sample Collection ......................................................................................................... 381 Sequencing .................................................................................................................... 382

Beijing Genome Institute (BGI) ..................................................................................... 384 BGI Projects.................................................................................................................. 385

BioFire Diagnostics, Inc. ................................................................................................. 387 Respiratory Panel .......................................................................................................... 388 Environmental Testing .................................................................................................. 390

Caliper Life Sciences ....................................................................................................... 391 Clinical Diagnostics ...................................................................................................... 391 Sequencing .................................................................................................................... 393 Life Sciences ................................................................................................................. 395

Celera Diagnostics ........................................................................................................... 396

Cepheid ............................................................................................................................ 399 Market Expansion ......................................................................................................... 400 HAI ............................................................................................................................... 401 Personalized Medicine .................................................................................................. 402 TB ................................................................................................................................. 403 Infectious Diseases ....................................................................................................... 404

Eiken Chemical Co., Ltd ................................................................................................ 404

Enzo Biochem Inc. .......................................................................................................... 408 ColonSentry .................................................................................................................. 409 Alliances ....................................................................................................................... 410 IP Protection ................................................................................................................. 411

Epigenomics AG .............................................................................................................. 412

Fluidigm Corporation ..................................................................................................... 415 Prenatal ......................................................................................................................... 417

Illumina Inc. .................................................................................................................... 419 BeadXpress ................................................................................................................... 420 Sequencing .................................................................................................................... 422 Cytogenetics ................................................................................................................. 423 Sample Prep .................................................................................................................. 424 PCR ............................................................................................................................... 424 CLIA Lab Service ......................................................................................................... 425

Ipsogen SA ....................................................................................................................... 426

Life Technologies ............................................................................................................ 429 Ion Torrent Systems ...................................................................................................... 432 Personalized Medicine .................................................................................................. 434 PCR ............................................................................................................................... 436 Arrays ........................................................................................................................... 437

Copyright © 2013 Kalorama Information

Reproduction without prior written permission, in any media now in existence or hereafter developed, in whole or in any part, is strictly prohibited.

IVD Company Deals ..................................................................................................... 437 Life and Quidel develop diagnostics on the 7500 Fast Dx ........................................... 439 Sepsis ............................................................................................................................ 440 HIV ............................................................................................................................... 440 Informatics .................................................................................................................... 441 International Presence ................................................................................................... 441

Novartis Diagnostics ....................................................................................................... 443 Blood Bank ................................................................................................................... 443 International Programs .................................................................................................. 445 Blood Typing ................................................................................................................ 446 Molecular IVDs ............................................................................................................ 446 Companion Tests .......................................................................................................... 447

PerkinElmer, Inc. ............................................................................................................ 449 Prenatal and Neonatal Screening .................................................................................. 450 Personalized Medicine .................................................................................................. 452 Molecular and Sequencing Diagnostics ........................................................................ 453 Test Services ................................................................................................................. 454 Human Health Research ............................................................................................... 455

RainDance Technologies, Inc. ........................................................................................ 456 Product Development ................................................................................................... 457

Seegene, Inc. .................................................................................................................... 461 Instrumentation ............................................................................................................. 464

Transgenomic, Inc. .......................................................................................................... 465 Lab Services.................................................................................................................. 466 Diagnostic Tools Division ............................................................................................ 468 CTCs ............................................................................................................................. 470 Sequencing .................................................................................................................... 471

CHAPTER NINETEEN: MARKET PARTICIPANTS...................................................................................473

Alacris Theranostics GmbH ........................................................................................... 473

Astra Biotech GmbH ...................................................................................................... 474

Autogenomics Inc. ........................................................................................................... 476

Biocartis SA ..................................................................................................................... 477

Biofortuna Ltd. ................................................................................................................ 480

Biotype Diagnostic GmbH .............................................................................................. 481

BlueGnome ...................................................................................................................... 482

DiaGenic ASA .................................................................................................................. 485

DiagnoCure ...................................................................................................................... 487

ELITech Group ............................................................................................................... 488

EraGen Biosciences Inc. ................................................................................................. 490

Copyright © 2013 Kalorama Information

Reproduction without prior written permission, in any media now in existence or hereafter developed, in whole or in any part, is strictly prohibited.

Genetic Technologies Limited ........................................................................................ 491

Victoria, Australia ........................................................................................................... 491

www.gtglabs.com ............................................................................................................. 491

GenMark Diagnostics Inc. .............................................................................................. 492

Helicos BioSciences ......................................................................................................... 494

IRIS International, Inc. .................................................................................................. 495 Cytology ....................................................................................................................... 497

Luminex Corporation ..................................................................................................... 497 IVD Expansion ............................................................................................................. 499 Cystic Fibrosis .............................................................................................................. 501 MAGPIX Multiplexing ................................................................................................. 502

Meridian Bioscience, Inc. ............................................................................................... 502 Bioline .......................................................................................................................... 504

Nanosphere, Inc. .............................................................................................................. 505 Infectious Diseases ....................................................................................................... 507 Hospital Acquired Infections ........................................................................................ 507

Sony DADC Biosciences ................................................................................................. 509 Cell Sorting ................................................................................................................... 510 Mass Spectrometry ....................................................................................................... 511

TrimGen Genetic Technology ........................................................................................ 512

TrovaGene, Inc. ............................................................................................................... 513 Prenatal ......................................................................................................................... 515

CHAPTER TWENTY: PROMISING COMPANIES ..........................................517 Ahram Biosystems, Inc. .................................................................................................. 517

Allegro Diagnostics Corp................................................................................................ 518

Amoy Diagnostics Co. Ltd. ............................................................................................. 519

Anagnostics Bioanalysis GmbH ..................................................................................... 520 Sample Preparation ....................................................................................................... 522

Applied BioCode, Inc. ..................................................................................................... 522

ArcticDx Inc. ................................................................................................................... 524

Ariosa Diagnostics ........................................................................................................... 526

Axela Inc. ......................................................................................................................... 526

BioHelix Corporation ..................................................................................................... 528

BioNanomatrix/ BioNano Genomics ............................................................................. 530

BJS Biotechnologies ........................................................................................................ 531

DiagCor Bioscience Inc. Ltd. ......................................................................................... 532

Copyright © 2013 Kalorama Information

Reproduction without prior written permission, in any media now in existence or hereafter developed, in whole or in any part, is strictly prohibited.

DxTerity Diagnostics Inc. ............................................................................................... 533

Epistem plc ...................................................................................................................... 534

Exiqon A/S ....................................................................................................................... 535

Exonhit ............................................................................................................................. 536

GeneNews Limited .......................................................................................................... 537

Genome Diagnostics BV (GenDx) .................................................................................. 539

Genomica S.A.U. ............................................................................................................. 540

Genorama Ltd. ................................................................................................................ 541

Great Basin Corporation ................................................................................................ 543

Health Discovery Corporation (HDC) .......................................................................... 544

IncellDx, Inc. .................................................................................................................... 545

Insight Genetics ............................................................................................................... 547

IntegenX Inc. ................................................................................................................... 549 Sample Transport .......................................................................................................... 551

Linkage Biosciences, Inc. ................................................................................................ 551

Med BioGene, Inc. (MBI) ............................................................................................... 552

Multiplicom ..................................................................................................................... 554

NABsys, Inc. .................................................................................................................... 555

Nanostring Technologies, Inc. ........................................................................................ 556

NIPD Genetics Ltd .......................................................................................................... 558

OptiGene Ltd ................................................................................................................... 559

Orion Genomics .............................................................................................................. 561

Oxford Gene Technology (OGT) ................................................................................... 562

PrimeraDx ....................................................................................................................... 564

Rheonix Inc. ..................................................................................................................... 565

Skyline Diagnostics B.V. ................................................................................................. 567

Spartan Bioscience Inc. .................................................................................................. 569

Stratos Genomics Inc. ..................................................................................................... 571

VolitionRx Limited ......................................................................................................... 572

WaferGen Biosystems, Inc. ............................................................................................ 573

Copyright © 2013 Kalorama Information

Reproduction without prior written permission, in any media now in existence or hereafter developed, in whole or in any part, is strictly prohibited.

CHAPTER TWENTY ONE: MOLECULAR NEWCOMERS ...........................575 DiaSorin S.p.A. ................................................................................................................ 575

Fujirebio Diagnostics, Inc. .............................................................................................. 577

GE Healthcare ................................................................................................................. 579 Cell Imaging ................................................................................................................. 581 Molecular Sequencing .................................................................................................. 582

Phadia AB ........................................................................................................................ 583

Quidel Corporation ......................................................................................................... 585 Alliances ....................................................................................................................... 587

Randox Laboratories Ltd. .............................................................................................. 588

TOSOH Corporation ...................................................................................................... 589

Transasia Bio-Medicals Ltd. .......................................................................................... 590

CHAPTER TWENTY TWO: TEST PLATFORM INNOVATIONS ................593 Advanced Liquid Logic, Inc. (ALL) .............................................................................. 593

Aquila Diagnostic Systems ............................................................................................. 595

Canon U.S. Life Sciences (CLS) ..................................................................................... 595

DNA Medicine Institute (DMI) ...................................................................................... 596

Espira, Inc. ....................................................................................................................... 597

Genia Technologies Inc. .................................................................................................. 598

Genisphere ....................................................................................................................... 599

Lumora Ltd. .................................................................................................................... 600

Michigan State University .............................................................................................. 601

NobleGen Biosciences ..................................................................................................... 602

Oxford Nanopore Technologies Ltd. ............................................................................. 603

QuantuMDx Group Limited .......................................................................................... 603

SensiQ Technologies, Inc. ............................................................................................... 605

Thermal Gradient, Inc. ................................................................................................... 606

Vela Diagnostics (VelaDx) .............................................................................................. 606

CHAPTER TWENTY THREE: SAMPLE PREPARATION SUPPLIERS ......609 Arcxis Biotechnologies .................................................................................................... 609

Argylla Technologies LLC ............................................................................................. 610

Biomatrica, Inc. ............................................................................................................... 611

Fluoresentric, Inc. ........................................................................................................... 614

Copyright © 2013 Kalorama Information

Reproduction without prior written permission, in any media now in existence or hereafter developed, in whole or in any part, is strictly prohibited.

New England Biolabs, Inc. (NEB) .................................................................................. 615

NorDiag ............................................................................................................................ 616

Norgen Biotek Corp. ....................................................................................................... 617

Phthisis Diagnostics ........................................................................................................ 618

PreAnalytiX GmbH ........................................................................................................ 619

QIAGEN N.V. .................................................................................................................. 620

Streck ............................................................................................................................... 622

ZyGEM Corp. Ltd. ......................................................................................................... 623

CHAPTER TWENTY FOUR: COMPANY PROFILES: INFORMATION TECHNOLOGY SPECIALISTS ...........................................................................625

Access Genetics ................................................................................................................ 625

CLC bio ............................................................................................................................ 626

CollabRx, Inc. .................................................................................................................. 629

Definiens ........................................................................................................................... 632

DNA Direct ...................................................................................................................... 634

DIYGenomics .................................................................................................................. 634

GenoSpace, LLC ............................................................................................................. 637

HolGenTech Inc. ............................................................................................................. 637

Ingenuity Systems ........................................................................................................... 640

MediSapiens Ltd. ............................................................................................................ 642

NextBio ............................................................................................................................. 643

Personalis ......................................................................................................................... 643

Portable Genomics .......................................................................................................... 644

Sciclips .............................................................................................................................. 645

Selventa ............................................................................................................................ 646

Sophic Systems Alliance ................................................................................................. 647

Wellpoint Inc. .................................................................................................................. 647

CHAPTER TWENTY FIVE: MICROBIOLOGY SPECIALISTS ..................649 Advanced Biological Laboratories (ABL) ..................................................................... 649

AdvanDx, Inc. .................................................................................................................. 651

Akonni Biosystems Inc. .................................................................................................. 653 Sample Preparation ....................................................................................................... 654 Test Systems ................................................................................................................. 655

Copyright © 2013 Kalorama Information

Reproduction without prior written permission, in any media now in existence or hereafter developed, in whole or in any part, is strictly prohibited.

Biomagnetics Diagnostics Corporation ......................................................................... 658

BlackBio S.L. ................................................................................................................... 660

Bruker BioSciences Corporation ................................................................................... 660

CapitalBio Corporation .................................................................................................. 663

Ceeram S.A.S. .................................................................................................................. 666

Cooperative Diagnostics, LLC ....................................................................................... 667

Curetis AG ....................................................................................................................... 668

Enigma Diagnostics Limited .......................................................................................... 669

Focus Diagnostics, Inc. ................................................................................................... 672

GenoID Ltd. ..................................................................................................................... 674

Great Basin Scientific, Inc. ............................................................................................. 675

Hain Lifescience GmbH.................................................................................................. 676

HiberGene Diagnostics Ltd ............................................................................................ 678

Ibis Biosciences ................................................................................................................ 679

iCubate Incorporated ..................................................................................................... 680

Immunexpress Group ..................................................................................................... 681

InDevR ............................................................................................................................. 682

Ingen Biosciences SA ...................................................................................................... 683

Intelligent Medical Devices, Inc. (IMDx) ...................................................................... 684

IQuum Inc. ....................................................................................................................... 686

Miacom Diagnostics GmbH ........................................................................................... 687

MicroPhage, Inc. ............................................................................................................. 688

Mobidiag Ltd ................................................................................................................... 690

Molecular Detection Inc. (MDI) .................................................................................... 690

Molzym GmbH & Co. KG ............................................................................................. 692

Myconostica ..................................................................................................................... 693

nanoMR Inc. .................................................................................................................... 694

NetBio ............................................................................................................................... 696

PathGEN Dx Pte. Ltd. .................................................................................................... 696

PathoGene ........................................................................................................................ 697

Pathogenica ...................................................................................................................... 698

SIRS-Lab ......................................................................................................................... 701

T2 Biosystems .................................................................................................................. 702

Copyright © 2013 Kalorama Information

Reproduction without prior written permission, in any media now in existence or hereafter developed, in whole or in any part, is strictly prohibited.

CHAPTER TWENTY SIX: BLOOD BANK SPECIALISTS .............................705 AbSorber AB ................................................................................................................... 705

AXO Science .................................................................................................................... 706

GMS Biotech .................................................................................................................... 707

Grifols, S.A. ..................................................................................................................... 708

Immucor, Inc. .................................................................................................................. 710

Progenika Inc. ................................................................................................................. 711

CHAPTER TWENTY SEVEN: COMPANIES SPECILAIZING IN CIRCULATING TUMOR CELLS ........................................................................715

ApoCell, Inc. .................................................................................................................... 715

Biocept, Inc. ..................................................................................................................... 717

Clearbridge BioMedics ................................................................................................... 719

Cynvenio Biosystems, Inc. .............................................................................................. 720

On-Q-ity ........................................................................................................................... 721

RareCyte, Inc. .................................................................................................................. 723

ScreenCell ........................................................................................................................ 723

Veridex, LLC ................................................................................................................... 725

CHAPTER TWENTY EIGHT: COMPANY PROFILES: HISTOLOGY SPECIALISTS .........................................................................................................729

Advanced Cell Diagnostics ............................................................................................. 729

Biocare Medical, LLC .................................................................................................... 732

ChipDX, LLC .................................................................................................................. 733

Cymogen Dx, LLC .......................................................................................................... 734

Dako A/S .......................................................................................................................... 736 Alliances ....................................................................................................................... 738 Companion Diagnostics ................................................................................................ 739

Horizon Discovery Ltd.................................................................................................... 741

HTG Molecular Diagnostics ........................................................................................... 742 Automation ................................................................................................................... 744

Mitomics Inc. ................................................................................................................... 745

Norchip............................................................................................................................. 746

Copyright © 2013 Kalorama Information

Reproduction without prior written permission, in any media now in existence or hereafter developed, in whole or in any part, is strictly prohibited.

CHAPTER TWENTY NINE: COMPANY PROFILES: SELECTED TEST SERVICE PROVIDERS .........................................................................................753

23andMe ........................................................................................................................... 753

Agendia BV ...................................................................................................................... 756 Market Expansion ......................................................................................................... 758 Product News ................................................................................................................ 758

AltheaDx Diagnostics, Inc. ............................................................................................. 760

Ambry Genetics ............................................................................................................... 762

Aria Diagnostics, Inc. (formerly Ariosa Diagnostics) ................................................. 763

ARUP Laboratories ........................................................................................................ 764

AssureRx Health, Inc. ..................................................................................................... 766

Avesthagen Limited ........................................................................................................ 767

Bio-Reference Laboratories, Inc. (BRLI) ..................................................................... 767

bioTheranostics ............................................................................................................... 771

Bostwick Laboratories .................................................................................................... 773

CardioDx, Inc. ................................................................................................................. 774

Caris Life Sciences .......................................................................................................... 777

Castle Biosciences Inc. .................................................................................................... 779

CBLPath .......................................................................................................................... 780

Chronix Biomedical Inc. ................................................................................................. 781

Clarient Inc. ..................................................................................................................... 783

CombiMatrix Molecular Diagnostics, Inc. ................................................................... 787

Complete Genomics ........................................................................................................ 789

Crescendo Bioscience, Inc. ............................................................................................. 793

deCode genetics ehf ......................................................................................................... 794 Gene Variants ............................................................................................................... 796

DermaGenoma, Inc. ........................................................................................................ 798

Diagnósticos da América (DASA) .................................................................................. 799

Diatherix Laboratories Inc. ............................................................................................ 800

EXACT Sciences Corporation ....................................................................................... 801

Exosome Diagnostics ....................................................................................................... 803

Genelex Corporation ...................................................................................................... 806

Genetadi Biotech SL ....................................................................................................... 807

Genomic Health, Inc. ...................................................................................................... 808 Service Spin off ............................................................................................................ 811

Copyright © 2013 Kalorama Information

Reproduction without prior written permission, in any media now in existence or hereafter developed, in whole or in any part, is strictly prohibited.

Expansion ..................................................................................................................... 811 Sequencing .................................................................................................................... 812 Information Technology ............................................................................................... 813

Genoptix Medical Laboratory ....................................................................................... 814

GenoVive LLC ................................................................................................................ 815

Inostics GmbH ................................................................................................................. 817

IntegraGen SA ................................................................................................................. 818

Interleukin Genetics, Inc. ............................................................................................... 820

Knome, Inc. ...................................................................................................................... 822

Lab21 Limited ................................................................................................................. 824 Services ......................................................................................................................... 825 Products Division .......................................................................................................... 826 Expansion ..................................................................................................................... 827

Laboratory Corporation of America Holdings (LabCorp) ......................................... 829

LifeCodexx AG ................................................................................................................ 833

Lineagen Inc. ................................................................................................................... 834

Lumigenix ........................................................................................................................ 835

Mayo Medical Laboratories ........................................................................................... 836

MDxHealth SA (formerly Oncomethylome Sciences) ................................................. 838

Medical Diagnostic Laboratories L.L.C. (MDL) .......................................................... 840

Myriad Genetics, Inc....................................................................................................... 842 Alliances ....................................................................................................................... 843 Test Information ........................................................................................................... 845 Patent Issues.................................................................................................................. 846

Natera Inc. ....................................................................................................................... 848

Navigenics ........................................................................................................................ 849

NewGene .......................................................................................................................... 850

Pathway Genomics .......................................................................................................... 851

Pathwork Diagnostics ..................................................................................................... 853

PGXL Laboratories ........................................................................................................ 855

Precision Therapeutics ................................................................................................... 856

Prometheus Laboratories Inc. ....................................................................................... 859 Patent Issues.................................................................................................................. 861