Embed Size (px)

Citation preview

NEW JERSEY HUMAN SERVICES:COST PRINCIPLES & ACCOUNTING FOR ALLOCATION OF COSTS & INDIRECT/GENERAL & ADMINISTRATIVE COSTS Presented By:

Joseph J. Scudese, CPA, CGFM, CFE, PSA, Partner

WithumSmith+Brown, PC ▪ Certified Public Accountants and Consultants ▪ BE IN A POSITION OF STRENGTH1

withum.com

COST PRINCIPLESCOST PRINCIPLES

State of New Jersey, Department of Human State of New Jersey, Department of Human Services, Contract Reimbursement Manual (“CRM”)

Section 4 – Principles for Determining Costsp g(MUST read for allowability of Program Costs)

WithumSmith+Brown, PC ▪ Certified Public Accountants and Consultants ▪ BE IN A POSITION OF STRENGTH2

withum.com

COST PRINCIPLESCOST PRINCIPLESBasic Elements of the Cost Principles:

R bl d All bilit (CRM S t 4 2)• Reasonableness and Allocability (CRM Sect. 4.2)

Reasonableness – “A cost is reasonable if, in it is nature or amount, it does not exceed that which would be incurred by an ordinary prudent y y pperson….”

So who is this “prudent person”?“The model of all legal behavior and always exercises due care ” The model of all legal behavior and always exercises due care.

In addition CRM 4.2: “The action of the prudent person would take in the circumstances, considering responsibilities to the public at large, the

t id l li t h h ld government, provider agency employees, clients, shareholders or members, and the fulfillment of the purposes for which the provider agency was organized.”

WithumSmith+Brown, PC ▪ Certified Public Accountants and Consultants ▪ BE IN A POSITION OF STRENGTH3

withum.com

COST PRINCIPLESCOST PRINCIPLES

Allocability – A cost is allocable if:Allocability A cost is allocable if:1. Incurred for the contract.

2. It benefits the contract & other non-contract activities & is distributed in a reasonableactivities & is distributed in a reasonableproportion to the benefits received.

3. Is necessary to the operation of the Agency.

WithumSmith+Brown, PC ▪ Certified Public Accountants and Consultants ▪ BE IN A POSITION OF STRENGTH4

withum.com

COST PRINCIPLESCOST PRINCIPLES

Allowable Items of Cost:

• Compensation for Personal Services Charges to contracts, whether treated as direct or indirect costs, are determined and supported as required in this Section.required in this Section.

(Be careful about “accrued vacation pay” more than 52 weeks of compensation – cannot be charged to the contract.)

WithumSmith+Brown, PC ▪ Certified Public Accountants and Consultants ▪ BE IN A POSITION OF STRENGTH5

withum.com

COST PRINCIPLESCOST PRINCIPLES

• Incentive Compensation – Allowable, but:Incentive Compensation Allowable, but: Is part of overall compensation (Refer to

Policy Circular P2.01-Section 5.16 “Salary o cy C cu a .0 Sec o 5. 6 Sa a y Compensation Limitations”)

Paid or accrued pursuant to:p1. An agreement with the employee2. Established written plan 2. Established written plan

WithumSmith+Brown, PC ▪ Certified Public Accountants and Consultants ▪ BE IN A POSITION OF STRENGTH6

withum.com

COST PRINCIPLES

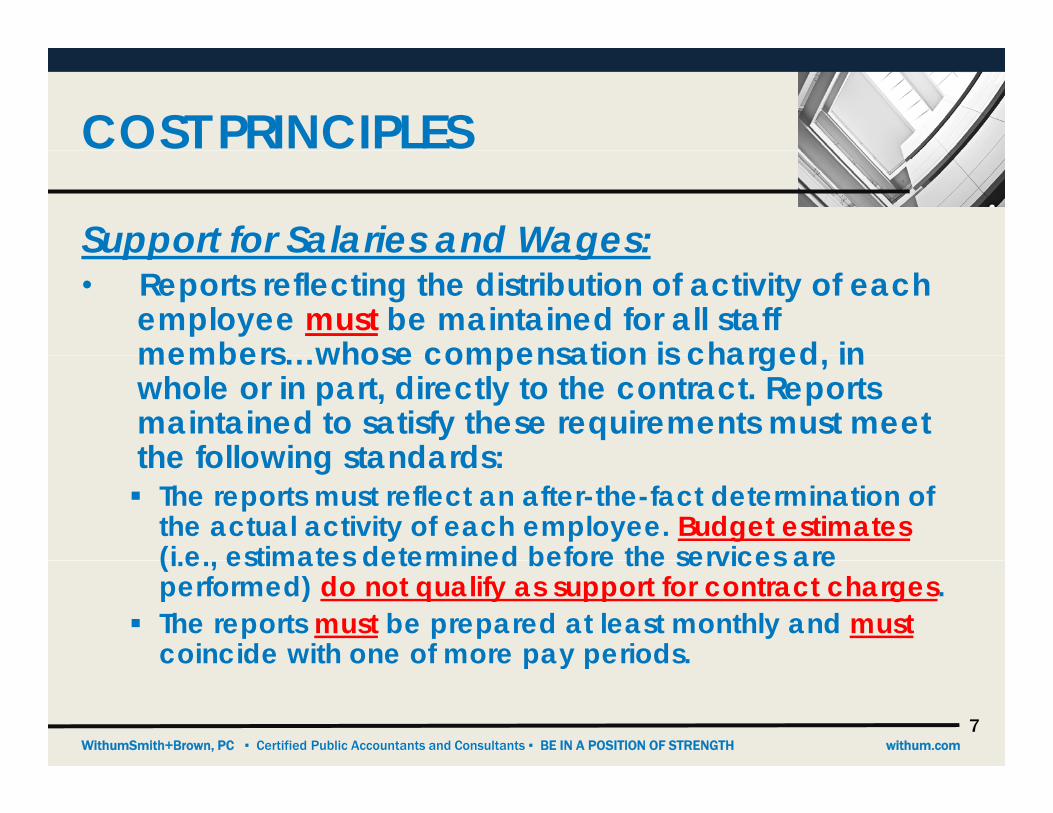

Support for Salaries and Wages:S pp S g• Reports reflecting the distribution of activity of each

employee must be maintained for all staff members whose compensation is charged in members…whose compensation is charged, in whole or in part, directly to the contract. Reports maintained to satisfy these requirements must meet the following standards:the following standards: The reports must reflect an after-the-fact determination of

the actual activity of each employee. Budget estimates(i e estimates determined before the services are (i.e., estimates determined before the services are performed) do not qualify as support for contract charges.

The reports must be prepared at least monthly and mustcoincide with one of more pay periods.

WithumSmith+Brown, PC ▪ Certified Public Accountants and Consultants ▪ BE IN A POSITION OF STRENGTH7

withum.com

coincide with one of more pay periods.

COST PRINCIPLESCOST PRINCIPLES

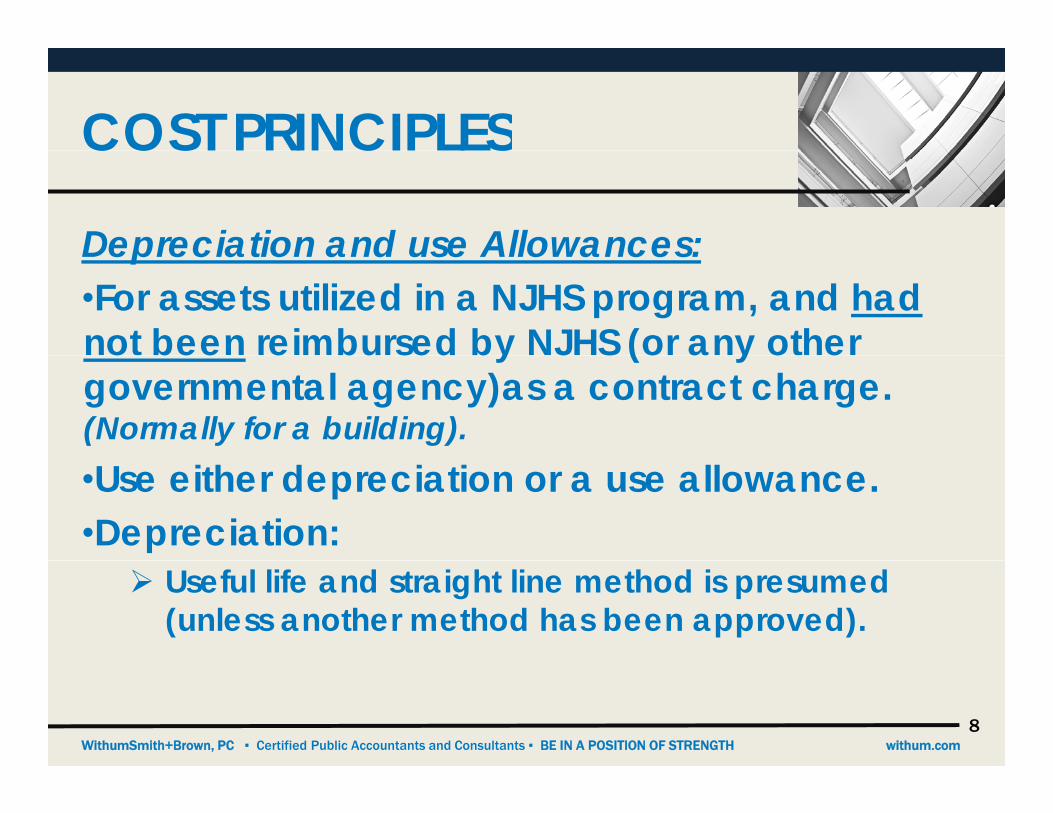

Depreciation and use Allowances:Depreciation and use Allowances:•For assets utilized in a NJHS program, and hadnot been reimbursed by NJHS (or any other o bee e bu sed by J S (o a y o e governmental agency)as a contract charge. (Normally for a building).•Use either depreciation or a use allowance.•Depreciation: Useful life and straight line method is presumed

(unless another method has been approved).

WithumSmith+Brown, PC ▪ Certified Public Accountants and Consultants ▪ BE IN A POSITION OF STRENGTH8

withum.com

COST PRINCIPLESCOST PRINCIPLES

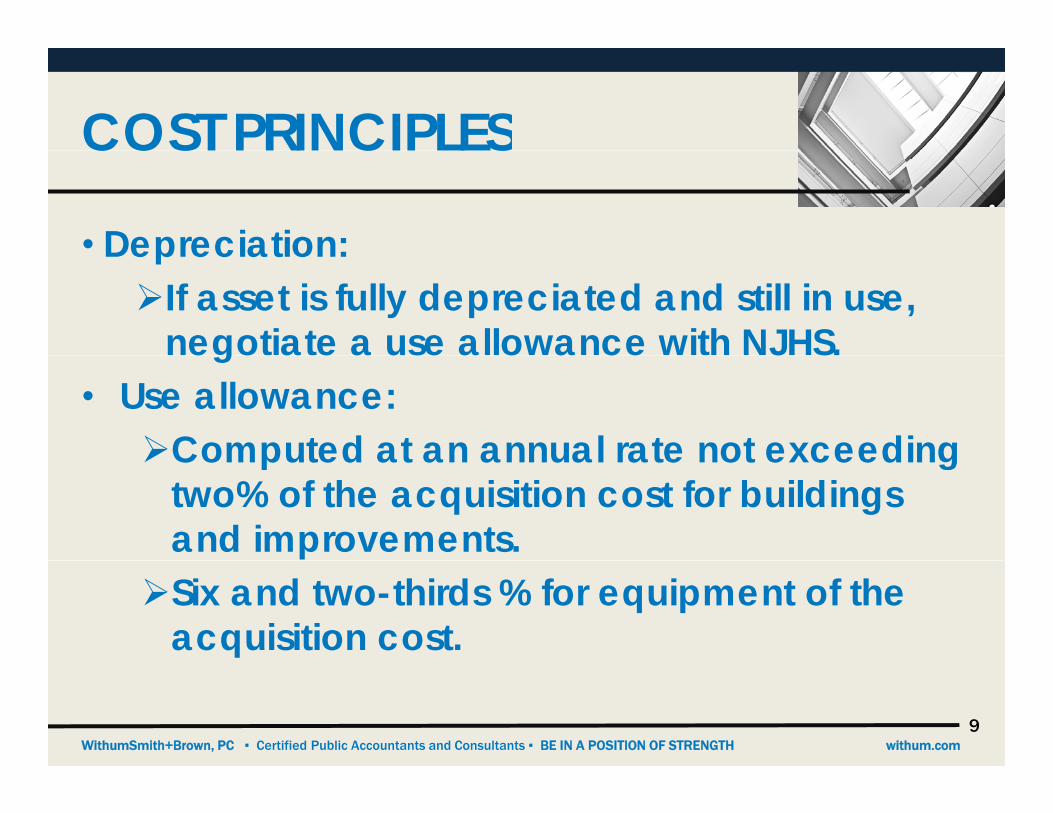

• Depreciation:Depreciation:If asset is fully depreciated and still in use,

negotiate a use allowance with NJHS.ego a e a use a o a ce J S.• Use allowance: Computed at an annual rate not exceeding Computed at an annual rate not exceeding

two% of the acquisition cost for buildings and improvements. Six and two-thirds % for equipment of the

acquisition cost.

WithumSmith+Brown, PC ▪ Certified Public Accountants and Consultants ▪ BE IN A POSITION OF STRENGTH9

withum.com

COST PRINCIPLESCOST PRINCIPLES

• Rental Costs – “Rental costs under less-than-Rental Costs Rental costs under less thanarm’s length leases are allowable only up to the amount that would be allowed had title to the property vested in the provider agency.”

• Unallowable Items of Cost (Section 4.7 of CRM) Unallowable as a direct cost and as a

di t/G l d i i t ti C tIndirect/General & Administrative Cost.

WithumSmith+Brown, PC ▪ Certified Public Accountants and Consultants ▪ BE IN A POSITION OF STRENGTH10

withum.com

COST PRINCIPLESCOST PRINCIPLES

So how to make sure that you adhere to the So how to make sure that you adhere to the requirements of Contract Reimbursement Manual?

Have someone, either on the program side or in p gthe accounting department, that is well versed in the CRM and that person signs off on the

ll bilit f t t dit allowability of contract expenditures.

WithumSmith+Brown, PC ▪ Certified Public Accountants and Consultants ▪ BE IN A POSITION OF STRENGTH11

withum.com

ALLOCATION OF COSTSALLOCATION OF COSTS

THE DOWNFALL OF MOST THE DOWNFALL OF MOST OC O S S?ALLOCATION PLANS IS?

WithumSmith+Brown, PC ▪ Certified Public Accountants and Consultants ▪ BE IN A POSITION OF STRENGTH12

withum.com

ALLOCATION OF COSTSALLOCATION OF COSTS

USING THE ALLOCATION BASES/PERCENTAGES USING THE ALLOCATION BASES/PERCENTAGES THAT WERE SPECIFIED IN THE BUDGET!!

THAT WAS AN ESTIMATE!!!!

NOT AFTER THE FACT DOCUMENTATIONNOT AFTER-THE-FACT DOCUMENTATION

WithumSmith+Brown, PC ▪ Certified Public Accountants and Consultants ▪ BE IN A POSITION OF STRENGTH13

withum.com

ALLOCATION OF COSTSALLOCATION OF COSTS

70%70%WithumSmith+Brown, PC ▪ Certified Public Accountants and Consultants ▪ BE IN A POSITION OF STRENGTH

14withum.com

DIRECT COSTS TO BE ALLOCATEDALLOCATED• Costs that traditionally require special Costs that traditionally require special

accounting methodology and associated adequate supporting documentation: Personnel Costs:

► Salaries and Wages (BIGGEST problem)Fringe benefits (Usually based on % of S&W)► Fringe benefits (Usually based on % of S&W)

Non-Personnel Costs:► Facility Costs► Other non-personnel costs (not assigned to the

indirect/general and administrative cost pool)

WithumSmith+Brown, PC ▪ Certified Public Accountants and Consultants ▪ BE IN A POSITION OF STRENGTH15

withum.com

DIRECT COSTS TO BE ALLOCATEDALLOCATEDFor all costs to be allocated, the Agency should , g yhave a written plan that specifies the methodology utilized in the allocation of the costs for each cost to be allocated So for costs for each cost to be allocated. So for instance, as an example, i.e.:Salaries and wages are allocated based upon time g p

sheets prepared for each employee which specify the hours worked by activity for each day during the payroll period.p y p

Rent and other facility costs are allocated upon the square footage attributable to each program’s activity and the space occupied by employee

WithumSmith+Brown, PC ▪ Certified Public Accountants and Consultants ▪ BE IN A POSITION OF STRENGTH16

withum.com

activity and the space occupied by employee.

SUPPORT FOR ALLOCATIONS

• Why do we need to support the allocations?Why do we need to support the allocations? “Necessary and reasonable” “Allocable to the award” Allocable to the award “Actually incurred”

WithumSmith+Brown, PC ▪ Certified Public Accountants and Consultants ▪ BE IN A POSITION OF STRENGTH17

withum.com

SUPPORT FOR ALLOCATIONS

No matter what allocation methodology that you utilize, gy ythe first thing you should do is prepare a written document that delineates/explains the various methods the agency has in place to allocate costs. This g y pdocument would contain, as a minimum, what is the basis of allocation for:1. Salaries and wages and fringe benefits.1. Salaries and wages and fringe benefits.2. Non-personnel costs.3. General & Administrative Costs.This document will become a permanent part of your accounting procedures and would only be updated at such a point when an allocation basis would change.

WithumSmith+Brown, PC ▪ Certified Public Accountants and Consultants ▪ BE IN A POSITION OF STRENGTH18

withum.com

p g

SALARY AND WAGE ALLOCATIONSALLOCATIONSSupport for Salaries and Wages:S pp S g• Reports reflecting the distribution of activity of each

employee must be maintained for all staff members whose compensation is charged in whole members…whose compensation is charged, in whole or in part, directly to the contract. Reports maintained to satisfy these requirements must meet the following standards:standards: The reports must reflect an after-the-fact determination of

the actual activity of each employee. Budget estimates(i e estimates determined before the services are (i.e., estimates determined before the services are performed) do not qualify as support for contract charges.

The reports must be prepared at least monthly and mustcoincide with one of more pay periods.

WithumSmith+Brown, PC ▪ Certified Public Accountants and Consultants ▪ BE IN A POSITION OF STRENGTH19

withum.com

coincide with one of more pay periods.

SALARY AND WAGE ALLOCATIONSALLOCATIONSWhy so much emphasis of the allocation and Why so much emphasis of the allocation and support for salaries and wages? In most instances the largest $$$$$. Basis of other allocations (fringe benefits and many

non-personnel costs).B d i th t titi d Based upon experience the area most entities do not “adequately document.”

WithumSmith+Brown, PC ▪ Certified Public Accountants and Consultants ▪ BE IN A POSITION OF STRENGTH20

withum.com

SALARY AND WAGE ALLOCATIONSALLOCATIONS• Allocations within and without the NJHS contract must

adhere to Contract Reimbursement Manual.• Employees that are generally considered

administrative personnel, those salaries generally are administrative personnel, those salaries generally are 100% classified as General and Administrative (“G&A”) expenses.

• Can a G&A employee have a direct cost for salaries • Can a G&A employee have a direct cost for salaries and wages? Maybe, but it has to be documented on the time record the direct service performed. (For example the G&A employee performed a “direct example the G&A employee performed a direct program service” and not in a supervisory or administrative role).

WithumSmith+Brown, PC ▪ Certified Public Accountants and Consultants ▪ BE IN A POSITION OF STRENGTH21

withum.com

SALARY AND WAGE ALLOCATIONSALLOCATIONSYou could for example:You could for example:1. If the individual is a Program Coordinator or

Manager then you could use the number of a age e you cou d use e u be o clients for each program as a % of the total clients served.

2. If the number of clients does not work for a reasonable allocation then you could use the t t l di t l i f th i total direct salaries for the various programs.

WithumSmith+Brown, PC ▪ Certified Public Accountants and Consultants ▪ BE IN A POSITION OF STRENGTH22

withum.com

SALARIES AND WAGES -ALLOCATIONALLOCATIONSo how do we start, prepare the following:• Prepare a written document that explains how you are allocating

salaries and wages. What employees will satisfy the requirement by time and effort reporting on a time sheet, and what employees are allocate on some other basis (these are the employees that are allocate on some other basis (these are the employees that have one job function but they are allocated to two or more activities, therefore they cannot delineate their time on a time sheet, need to determine another method of allocation).

• Prepare a “Employee Designation Schedule” on each employee to determine if they need to have a document to support the allocation of their salary. (See next page for a suggested format).Th h l h d t h th i ti ll t d • Then have employees who need to have their time allocated prepare a time sheet that designates hours worked by each program activity.

WithumSmith+Brown, PC ▪ Certified Public Accountants and Consultants ▪ BE IN A POSITION OF STRENGTH23

withum.com

SALARIES AND WAGES -ALLOCATIONALLOCATION

Name ofEmployee Job Position

G&AEmployee Fulltime Part‐Time

NotAllocated

Allocated ‐TimeSheet

Allocated ‐OtherBasis

Susan Worth Executive Director X X X

James Friendly Program Coordinator X X

Jill Lang Counselor X X

WithumSmith+Brown, PC ▪ Certified Public Accountants and Consultants ▪ BE IN A POSITION OF STRENGTH24

withum.com

SALARIES AND WAGES –ALLOCATION ALLOCATION Sample Time Sheet:p

Time and Effort Reporting - 9/1/11 to 9/15/11

9/1/2011 9/2/2011 9/5/2011 9/6/2011 9/7/2011 9/8/2011 9/9/2011 TotalNJHS-DAS 4 7 1/2 2 3 8 24 1/2Project Mobile 4 1/2 6 5 15 1/2

Employee: James Friendly

Project Mobile 4 1/2 6 5 15 1/2Holiday 8 8Vacation 8 8

8 8 8 8 8 8 8 56

9/10/2011 9/11/2011 9/12/2011 9/13/2011 9/14/2011 9/15/2011 TotalNJHS DAS 3 1/2 4 5 6 2 20 1/2NJHS-DAS 3 1/2 4 5 6 2 20 1/2Project Mobile 4 1/2 4 3 2 8 6 27 1/2

8 8 8 8 8 8 48Totals 16 16 16 16 16 16 8 104

Summary NJHS DAS 45NJHS-DAS 45Project Mobile 43Holiday 8Vacation 8

104

E l Si t S i Si t

WithumSmith+Brown, PC ▪ Certified Public Accountants and Consultants ▪ BE IN A POSITION OF STRENGTH25

withum.com

Employee Signature_________________________ Supervisory Signature________________________

SALARIES AND WAGES –ALLOCATION ALLOCATION So what is the allocation % for James Friendly? So what is the allocation % for James Friendly?

Is it based upon the 104 hours or not?Is it based upon the 104 hours or not?

WithumSmith+Brown, PC ▪ Certified Public Accountants and Consultants ▪ BE IN A POSITION OF STRENGTH26

withum.com

SALARIES AND WAGES –ALLOCATION ALLOCATION No, it is based upon 88 hours (45 + 43). The , p 88 ( 5 3)vacation and holiday do not factor in on the computation (allocations are based upon hoursworked) Therefore 51% (45/88) of the salaries worked). Therefore, 51% (45/88) of the salaries and wages for this pay period will be allocated to DAS and 49% (43/88) to Project Mobile.( / ) j

What happens if James was on vacation for a whole pay period, how do we allocate the salaries for that pay period?

WithumSmith+Brown, PC ▪ Certified Public Accountants and Consultants ▪ BE IN A POSITION OF STRENGTH27

withum.com

SALARIES AND WAGES –ALLOCATION ALLOCATION The allocation for that pay period should be The allocation for that pay period should be based upon the average allocation of prior pay periods.

WithumSmith+Brown, PC ▪ Certified Public Accountants and Consultants ▪ BE IN A POSITION OF STRENGTH28

withum.com

SALARIES AND WAGES -ALLOCATIONALLOCATIONSo what about those employees that need to be allocated, p ybut due to their job position (they only perform one job function), however their salaries are allocated to different activates and their salary is therefore paid out of two different y pgrants or contracts.

One method to allocate is after all emplo ee salaries that • One method to allocate is after all employee salaries that are directly 100% chargeable & employee salaries that were allocated by the time & effort reporting, then

ll t th i i l ( ) b d th allocate the remaining employee(s) based upon the percentage of salaries for each activity to the total of all salaries and wages. (This would not include G&A salaries).

WithumSmith+Brown, PC ▪ Certified Public Accountants and Consultants ▪ BE IN A POSITION OF STRENGTH29

withum.com

SALARIES AND WAGES -ALLOCATIONALLOCATIONWhat about other allocation methods:• You could use the number of clients for a

particular program activity as a % of the total clients served for all program servicesclients served for all program services.

(Just make sure than the units of service are (Just make sure than the units of service are comparable between the programs. If one unit of service for a program is a daily encounter and the other unit of service is by hours provided then the other unit of service is by hours provided, then the units would not be appropriate, since the service delivery in hours would/could be drastically different)

WithumSmith+Brown, PC ▪ Certified Public Accountants and Consultants ▪ BE IN A POSITION OF STRENGTH30

withum.com

different).

SALARIES AND WAGES -ALLOCATIONALLOCATIONFinal thought:gWhat if the Agency utilizes an electronic timekeeping system. Is this adequate?

Probably not, since it would only tract/record the employee coming to work, taking a break from work and going to lunch and then leaving at the work and going to lunch, and then leaving at the end of the day. It would not reflect the hours worked on more than one program/project. Therefore for all employees that need to document Therefore, for all employees that need to document his or her time on a particular activity/project they would have to prepare a written paper time sheet to record their hours for each progam/project

WithumSmith+Brown, PC ▪ Certified Public Accountants and Consultants ▪ BE IN A POSITION OF STRENGTH31

withum.com

record their hours for each progam/project.

SALARIES AND WAGES -ALLOCATIONALLOCATIONAs a tip of advice, for those Not-For-Profits, if you As a tip of advice, for those Not For Profits, if you receive Federal grants/contracts (either directly or as a pass-through), you must still have adequate time and effort reporting. This is a requirement of Office of Management and B d t Ci l A 122 Att h t B It 8 Budget Circular A-122, Attachment B, Item 8, Section M, which has the exact documentation requirements as the Contract Reimbursement requirements as the Contract Reimbursement Manual.

WithumSmith+Brown, PC ▪ Certified Public Accountants and Consultants ▪ BE IN A POSITION OF STRENGTH32

withum.com

OTHER DIRECT COST ALLOCATIONSALLOCATIONS• All non-personnel costs that can be charged All non personnel costs that can be charged

directly to a program, project or activity will be charged so.

• After the above there generally will be non-personnel costs that are still open and need to be accounted for. These non-personnel costs should fall into two categories:

t1. Program costs2. General and Administrative Costs (G&A)

WithumSmith+Brown, PC ▪ Certified Public Accountants and Consultants ▪ BE IN A POSITION OF STRENGTH33

withum.com

OTHER DIRECT COST ALLOCATIONSALLOCATIONSFor program costs that are not charged directly to a For program costs that are not charged directly to a program, project or activity you will then have to determine the most reasonable basis to allocate. Wh t b i d t d t i th itt Whatever basis you need to document in the written plan previously discussed. One method to allocate these remaining direct program costs would utilize, these remaining direct program costs would utilize, as a basis, the salaries and wages already recorded to each program, project or activity as a

f i i ipercentage of total direct salaries and wages. This method is the most widely utilized/recognized acceptable allocation methodology

WithumSmith+Brown, PC ▪ Certified Public Accountants and Consultants ▪ BE IN A POSITION OF STRENGTH34

withum.com

acceptable allocation methodology.

OTHER DIRECT COST ALLOCATIONSALLOCATIONSThis method would follow the following accounting g gfor salaries and wages (S&W) for each program, project or activity:1. All direct employee S&W charged 100%.p y g %2. All allocated S&W based upon a time sheet (or

other allocation basis) that delineates that employees time and effort.employees time and effort.

After the above is completed you would take the total of the S&W for each program/activity as a percentage of the total salaries and wagespercentage of the total salaries and wages.Those percentages would then be applied to each non-personnel cost to be allocated.

WithumSmith+Brown, PC ▪ Certified Public Accountants and Consultants ▪ BE IN A POSITION OF STRENGTH35

withum.com

FACILITY COST ALLOCATIONS

• Facility Costs – most times based upon square Facility Costs most times based upon square footage.

• Remember the “common areas” are included e e be e co o a eas a e c uded in the square footage allocation. (Based upon the previously calculated allocated amount).

• Allocation of facility costs based upon FTE. Be careful, may not be an appropriate basis of

ll ti ( h l th allocation. (Does each employee occupy the same square footage office space?)

WithumSmith+Brown, PC ▪ Certified Public Accountants and Consultants ▪ BE IN A POSITION OF STRENGTH36

withum.com

OTHER DIRECT COST ALLOCATIONSALLOCATIONS• Other allocation bases:Other allocation bases: Clients Served – be cognizant of comparability of

“service hours” for all services provided. Number of computer keystrokes. Food costs – number of meals served.

WithumSmith+Brown, PC ▪ Certified Public Accountants and Consultants ▪ BE IN A POSITION OF STRENGTH37

withum.com

GENERAL AND ADMINISTRATIVE EXPENSESADMINISTRATIVE EXPENSES

• Why do we have Indirect/General & Why do we have Indirect/General & Administrative (“G&A”)costs?Not practical or almost impossible to allocate direct

costs.Federal, State or Local governments normally

require itrequire it.Management needs to understand how much G&A

they incur in operating their program services. y p g p g(Many governmental agencies, potential donors, etc. look to this G&A rate as a barometer of how an agency expends “public dollars ”)

WithumSmith+Brown, PC ▪ Certified Public Accountants and Consultants ▪ BE IN A POSITION OF STRENGTH38

withum.com

agency expends public dollars. )

GENERAL AND ADMINISTRATIVE EXPENSESADMINISTRATIVE EXPENSESThe requirements related to General & The requirements related to General & Administrative Expenses (G&A) are delineated in the NJHS Contract Reimbursement Manual (CRM), Section 4.3 under the heading Indirect Costs. (In regard to this accounting for costs, G&A and Indirect Costs are interchangeable terminologies) Indirect Costs are interchangeable terminologies).

WithumSmith+Brown, PC ▪ Certified Public Accountants and Consultants ▪ BE IN A POSITION OF STRENGTH39

withum.com

GENERAL AND ADMINISTRATIVE EXPENSESADMINISTRATIVE EXPENSESSome Key points in the CRM are:Some Key points in the CRM are:• “An indirect cost is one which, because of its

incurrence for common or joint objectives, is not readily subject to treatment as a direct cost.”

• “The overall objective is to allocate the indirect costs of the provider agency to its major activities or cost of the provider agency to its major activities or cost objectives in a reasonable proportion to the benefits provided.”

• “Indirect costs shall be accumulated by logical cost groupings with due consideration accorded to the reasons for incurring costs.”

WithumSmith+Brown, PC ▪ Certified Public Accountants and Consultants ▪ BE IN A POSITION OF STRENGTH40

withum.com

reasons for incurring costs.

GENERAL AND ADMINISTRATIVE EXPENSESADMINISTRATIVE EXPENSESSome Key points in the CRM are (Cont.):S y p C (C )• “When reporting costs, the provider agency must

meet the following minimum requirements”:1 “The statistical base used to allocate each cost center must 1. The statistical base used to allocate each cost center must measure as accurately as possible the service rendered by that center to other cost centers.”2. “The statistics used must be auditable and maintained on a 2. The statistics used must be auditable and maintained on a continuous basis.”

• “Both the direct costs and indirect costs shall exclude capital expenditures and unallowable costs.” capital expenditures and unallowable costs. (Remember to include unallowable costs on your Report of Expenditures as a cost activity.)

WithumSmith+Brown, PC ▪ Certified Public Accountants and Consultants ▪ BE IN A POSITION OF STRENGTH41

withum.com

GENERAL AND ADMINISTRATIVE EXPENSESADMINISTRATIVE EXPENSESSome Key points in the CRM are (Cont.):Some Key points in the CRM are (Cont.):• “The distribution base may be total direct costs

(excluding capital expenditures), direct salaries, or other base which results in an equitable distribution.”

WithumSmith+Brown, PC ▪ Certified Public Accountants and Consultants ▪ BE IN A POSITION OF STRENGTH42

withum.com

GENERAL AND ADMINISTRATIVE EXPENSES ADMINISTRATIVE EXPENSES • The allocation of G&A expenses on NJHS’s The allocation of G&A expenses on NJHS s

contract: G&A should capture all the G&A expenses of the

Agency, not just the G&A of the program. If management personnel, normally 100% in G&A,

performs direct service then that portion of their performs direct service, then that portion of their compensation should be directly charged to the program’s direct expenses. (Time sheet must reflect the hours attributable to that direct service.)

You should have a written plan as to how the G&A was derived and the plan basis

WithumSmith+Brown, PC ▪ Certified Public Accountants and Consultants ▪ BE IN A POSITION OF STRENGTH43

withum.com

was derived and the plan basis.

GENERAL AND ADMINISTRATIVE EXPENSES ADMINISTRATIVE EXPENSES • When allocating G&A expenses, allocation When allocating G&A expenses, allocation

could be based upon:1. Total direct salaries and wages for each activity as

a % of total direct salaries and wages costs for all activities (Including all funded NJHS programs, non-funded programs [“Unallowable] fund raising non funded programs [ Unallowable], fund raising. etc.).

2. Total Direct Costs. This would include ALL the total direct costs for each activity as a % of total direct costs for all activities, exclusive of equipment/renovations costs.

WithumSmith+Brown, PC ▪ Certified Public Accountants and Consultants ▪ BE IN A POSITION OF STRENGTH44

withum.com

equ p e / e o a o s cos s.

GENERAL AND ADMINISTRATIVE EXPENSES ADMINISTRATIVE EXPENSES How does an entity start to prepare their How does an entity start to prepare their G&A/indirect costs calculation? General ledger needs to capture General and

Administrative costs. Analysis of G&A costs to determine if the costs

contain any “unallowable costs” per the CRM contain any unallowable costs per the CRM regulations. (Cannot “back door” unallowable costs.)

Make sure that ALL of the operations of the entity receive their fair share of the indirect costs.

WithumSmith+Brown, PC ▪ Certified Public Accountants and Consultants ▪ BE IN A POSITION OF STRENGTH45

withum.com

GENERAL AND ADMINISTRATIVE EXPENSES ADMINISTRATIVE EXPENSES • Determine what the G&A/indirect cost base Determine what the G&A/indirect cost base

will be. Salaries and Wages Total direct costs, exclusive of

equipment/renovations.

• Prepare a calculation.

WithumSmith+Brown, PC ▪ Certified Public Accountants and Consultants ▪ BE IN A POSITION OF STRENGTH46

withum.com

ALLOCATION OF COSTSALLOCATION OF COSTS

Other “Tips of Advice”:O p1. Prepare a written document that explains the

process and the methodologies the entity utilizes in the allocation of costs (This would include how the allocation of costs. (This would include how each type of cost is allocated, the basis of the allocation and the appropriate support.)

2 M t ith t ff th t ill b i l d d/ ff t d 2. Meet with staff that will be involved and/or affected by the allocation of cost. May be necessary to explain to certain staff why that individual needs to

“ d t il d” ti h t d prepare a “more detailed” time sheet, as opposed to another employee who does not have to delineate his or her time.

WithumSmith+Brown, PC ▪ Certified Public Accountants and Consultants ▪ BE IN A POSITION OF STRENGTH47

withum.com

CONTACT INFORMATIONCONTACT INFORMATION

Joseph J. ScudesepWithumSmith+Brown, PCOne Spring StreetNew Brunswick, NJ [email protected]

WithumSmith+Brown, PC ▪ Certified Public Accountants and Consultants ▪ BE IN A POSITION OF STRENGTH48

withum.com