Embed Size (px)

Citation preview

NEW ISSUES - BOOK-ENTRY ONLY RATINGS: Moody’s: “Aa2” S&P: “AA” Fitch: “AA-”

(See “RATINGS” herein)

In the opinion of Hawkins Delafield & Wood LLP, Bond Counsel to the State of California (the “State”), under existing statutes and court decisions and assuming continuing compliance with certain tax covenants, (i) interest on the Offered Veterans G.O. Bonds (as defined below) is excluded from gross income for Federal income tax purposes pursuant to Section 103 of the Internal Revenue Code of 1986, as amended (the “Federal Tax Code”); (ii) interest on the Series CK Bonds (as defined below) is not treated as a preference item in calculating the alternative minimum tax imposed on individuals and corporations under the Federal Tax Code; such interest, however, is included in the adjusted current earnings of certain corporations for purposes of calculating the alternative minimum tax imposed on such corporations; (iii) interest on the Series CL Bonds (as defined below) is not treated as a preference item in calculating the alternative minimum tax imposed on individuals and corporations under the Federal Tax Code and is not included in the adjusted current earnings of corporations for purposes of calculating the alternative minimum tax; and (iv) interest on the Series CM Bonds (as defined below) is treated as a preference item in calculating the alternative minimum tax imposed on individuals and corporations under the Federal Tax Code. In the opinion of Bond Counsel to the State, under State law, interest on the Offered Veterans G.O. Bonds is exempt from State personal income taxes. See “TAX MATTERS.”

$445,700,000STATE OF CALIFORNIA

VETERANS GENERAL OBLIGATION BONDS

$152,295,000Series CK (Non-AMT)

$128,610,000Series CL (Non-AMT)

$164,795,000Series CM (AMT)

Dated: Date of Delivery Due: As shown on the inside cover page

This offering consists of the State of California Veterans General Obligation Bonds, Series CK (the “Series CK Bonds”), the State of California Veterans General Obligation Bonds, Series CL (the “Series CL Bonds”), and the State of California Veterans General Obligation Bonds, Series CM (the “Series CM Bonds”) as described and listed above (collectively, the “Offered Veterans G.O. Bonds”) authorized by the voters of the State. The Offered Veterans G.O. Bonds will mature in the years and bear interest at the rates set forth on the inside cover page hereof.

Interest is payable on June 1 and December 1 of each year, commencing December 1, 2015. The Offered Veterans G.O. Bonds may be purchased in book‑entry form only, in the principal amount of $5,000 or any integral multiple thereof. See APPENDIX C – “DTC AND THE BOOK‑ENTRY SYSTEM.” The Offered Veterans G.O. Bonds are subject to redemption prior to maturity. See “THE OFFERED VETERANS G.O. BONDS – Redemption.”

The Offered Veterans G.O. Bonds are general obligations of the State to which the full faith and credit of the State is pledged. Debt service on the Offered Veterans G.O. Bonds is payable first from moneys required under the California Military and Veterans Code (the “Veterans Code”) to be transferred from the Veterans’ Farm and Home Building Fund of 1943 (the “1943 Fund”) to the Veterans’ Bonds Payment Fund (as defined herein) and second, if the moneys transferred from the 1943 Fund to the Veterans’ Bonds Payment Fund are less than debt service then due and payable, the balance is payable from the General Fund of the State (the “General Fund”). The principal of and interest on all State general obligation bonds, including the Offered Veterans G.O. Bonds (as described above), are payable from moneys in the General Fund, subject under State law only to the prior application of such moneys to the support of the public school system and public institutions of higher education. The 1943 Fund is required to transfer to the General Fund, as soon as it becomes available, an amount equal to the amount paid by the General Fund, if any, together with interest thereon from the remittance date until paid, at the same rate of interest as borne by the applicable Veterans G.O. Bonds (as defined herein), compounded semiannually. The Veterans Code does not grant any lien on the 1943 Fund or the moneys therein to the holders of any Veterans G.O. Bonds (including the Offered Veterans G.O. Bonds). See “AUTHORIZATION OF AND SECURITY FOR THE OFFERED VETERANS G.O. BONDS.”

This cover page contains certain information for quick reference only. It is not a summary of the security or terms of the Offered Veterans G.O. Bonds. Investors are advised to read the entire Official Statement to obtain information essential to the making of an informed investment decision.

MATURITIES, PRINCIPAL AMOUNTS, INTEREST RATES, PRICES OR YIELDS AND CUSIPS(See inside front cover)

The Offered Veterans G.O. Bonds are offered when, as and if issued and received by the Underwriters, subject to certain conditions, including the receipt of certain legal opinions of the Honorable Kamala D. Harris, Attorney General of the State of California, and of Hawkins Delafield & Wood LLP, Bond Counsel to the State. In connection with the issuance of the Offered Veterans G.O. Bonds, Polsinelli LLP is serving as Disclosure Counsel to the State, and Orrick, Herrington & Sutcliffe LLP and Stradling Yocca Carlson & Rauth, a Professional Corporation, are serving as Co-Disclosure Counsel to the State regarding APPEnDIX A. Certain matters will be passed upon for the Underwriters by their counsel, Sidley Austin LLP. Montague DeRose and Associates, LLC is serving as Financial Advisor to the State. The Offered Veterans G.O. Bonds will be available for delivery through the facilities of The Depository Trust Company on or about October 29, 2015.

Honorable John ChiangTreasurer of the State of California

BofA Merrill Lynch(Joint Senior Manager)

Academy Securities, Inc.(Joint Senior Manager)

Drexel Hamilton LLC(Co-Senior Manager)

Mischler Financial Group, Inc.(Co-Senior Manager)

FTN Financial Capital Markets Goldman, Sachs & Co.Great Pacific Securities Morgan Stanley

RH Investment Corporation Stern Brothers & Co.Stifel Nicolaus & Co., Inc. Wulff, Hansen & Co.

Official Statement Dated: October 8, 2015.

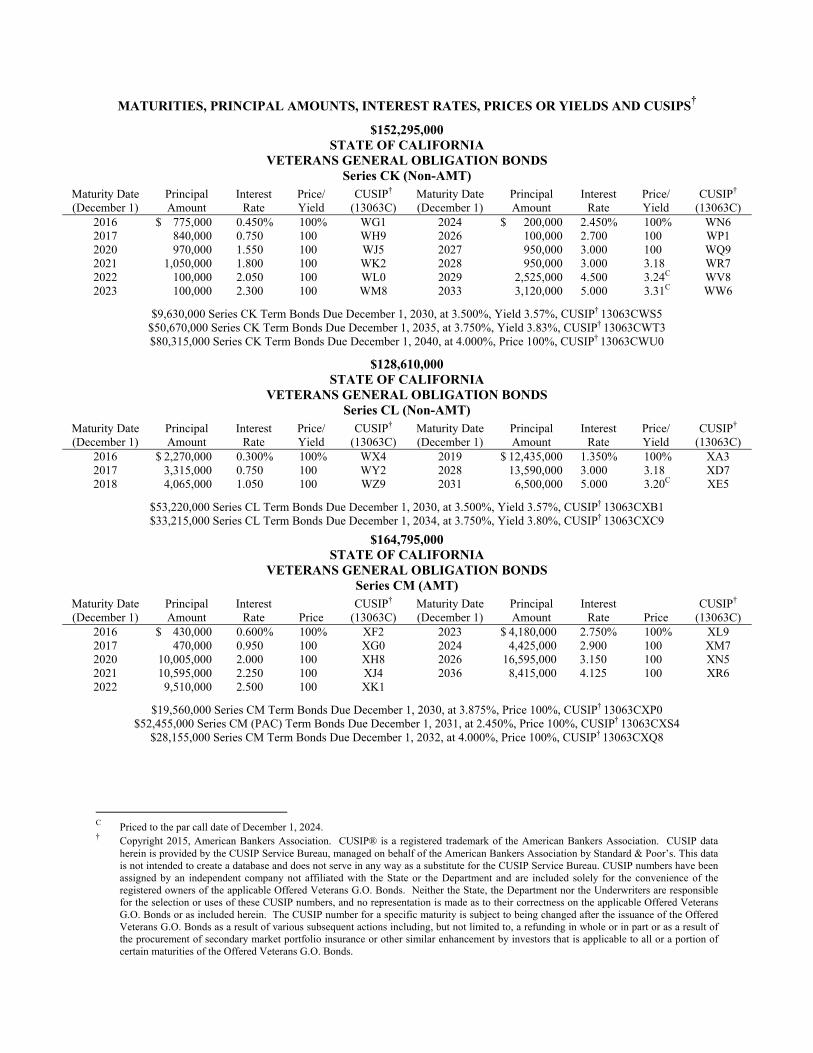

MATURITIES, PRINCIPAL AMOUNTS, INTEREST RATES, PRICES OR YIELDS AND CUSIPS†

$152,295,000 STATE OF CALIFORNIA

VETERANS GENERAL OBLIGATION BONDS Series CK (Non-AMT)

Maturity Date (December 1)

Principal Amount

Interest Rate

Price/ Yield

CUSIP† (13063C)

Maturity Date(December 1)

Principal Amount

Interest Rate

Price/ Yield

CUSIP† (13063C)

2016 $ 775,000 0.450% 100% WG1 2024 $ 200,000 2.450% 100% WN6 2017 840,000 0.750 100 WH9 2026 100,000 2.700 100 WP1 2020 970,000 1.550 100 WJ5 2027 950,000 3.000 100 WQ9 2021 1,050,000 1.800 100 WK2 2028 950,000 3.000 3.18 WR7 2022 100,000 2.050 100 WL0 2029 2,525,000 4.500 3.24C WV8 2023 100,000 2.300 100 WM8 2033 3,120,000 5.000 3.31C WW6

$9,630,000 Series CK Term Bonds Due December 1, 2030, at 3.500%, Yield 3.57%, CUSIP† 13063CWS5 $50,670,000 Series CK Term Bonds Due December 1, 2035, at 3.750%, Yield 3.83%, CUSIP† 13063CWT3 $80,315,000 Series CK Term Bonds Due December 1, 2040, at 4.000%, Price 100%, CUSIP† 13063CWU0

$128,610,000 STATE OF CALIFORNIA

VETERANS GENERAL OBLIGATION BONDS Series CL (Non-AMT)

Maturity Date (December 1)

Principal Amount

Interest Rate

Price/ Yield

CUSIP† (13063C)

Maturity Date(December 1)

Principal Amount

Interest Rate

Price/ Yield

CUSIP† (13063C)

2016 $ 2,270,000 0.300% 100% WX4 2019 $ 12,435,000 1.350% 100% XA3 2017 3,315,000 0.750 100 WY2 2028 13,590,000 3.000 3.18 XD7 2018 4,065,000 1.050 100 WZ9 2031 6,500,000 5.000 3.20C XE5

$53,220,000 Series CL Term Bonds Due December 1, 2030, at 3.500%, Yield 3.57%, CUSIP† 13063CXB1

$33,215,000 Series CL Term Bonds Due December 1, 2034, at 3.750%, Yield 3.80%, CUSIP† 13063CXC9

$164,795,000 STATE OF CALIFORNIA

VETERANS GENERAL OBLIGATION BONDS Series CM (AMT)

Maturity Date (December 1)

Principal Amount

Interest Rate Price

CUSIP† (13063C)

Maturity Date(December 1)

Principal Amount

Interest Rate Price

CUSIP† (13063C)

2016 $ 430,000 0.600% 100% XF2 2023 $ 4,180,000 2.750% 100% XL9 2017 470,000 0.950 100 XG0 2024 4,425,000 2.900 100 XM7 2020 10,005,000 2.000 100 XH8 2026 16,595,000 3.150 100 XN5 2021 10,595,000 2.250 100 XJ4 2036 8,415,000 4.125 100 XR6 2022 9,510,000 2.500 100 XK1

$19,560,000 Series CM Term Bonds Due December 1, 2030, at 3.875%, Price 100%, CUSIP† 13063CXP0

$52,455,000 Series CM (PAC) Term Bonds Due December 1, 2031, at 2.450%, Price 100%, CUSIP† 13063CXS4

$28,155,000 Series CM Term Bonds Due December 1, 2032, at 4.000%, Price 100%, CUSIP† 13063CXQ8

C Priced to the par call date of December 1, 2024. † Copyright 2015, American Bankers Association. CUSIP® is a registered trademark of the American Bankers Association. CUSIP data

herein is provided by the CUSIP Service Bureau, managed on behalf of the American Bankers Association by Standard & Poor’s. This data is not intended to create a database and does not serve in any way as a substitute for the CUSIP Service Bureau. CUSIP numbers have been assigned by an independent company not affiliated with the State or the Department and are included solely for the convenience of the registered owners of the applicable Offered Veterans G.O. Bonds. Neither the State, the Department nor the Underwriters are responsible for the selection or uses of these CUSIP numbers, and no representation is made as to their correctness on the applicable Offered Veterans G.O. Bonds or as included herein. The CUSIP number for a specific maturity is subject to being changed after the issuance of the Offered Veterans G.O. Bonds as a result of various subsequent actions including, but not limited to, a refunding in whole or in part or as a result of the procurement of secondary market portfolio insurance or other similar enhancement by investors that is applicable to all or a portion of certain maturities of the Offered Veterans G.O. Bonds.

No dealer, broker, salesperson or other person has been authorized by the State, the Department or the Underwriters to give any information or to make any representations with respect to the State or the Department or the Offered Veterans G.O. Bonds other than those contained in this Official Statement and, if given or made, such other information or representations must not be relied upon as having been authorized by any of the foregoing.

This Official Statement, including any supplement or amendment hereto, is intended to be deposited with, and may be obtained from the Municipal Securities Rulemaking Board (“MSRB”) through the Electronic Municipal Market Access (“EMMA”) website of the MSRB, currently located at http://emma.msrb.org. The information contained on such website is not part of this Official Statement and is not incorporated herein.

This Official Statement is not to be construed as a contract with the purchasers of the Offered Veterans G.O. Bonds.

The Underwriters have provided the following sentence for inclusion in this Official Statement. The Underwriters have reviewed the information in this Official Statement in accordance with, and as a part of, their responsibilities to investors under the Federal securities laws as applied to the facts and circumstances of this transaction, but the Underwriters do not guarantee the accuracy or completeness of such information.

IN CONNECTION WITH THIS OFFERING, THE UNDERWRITERS MAY OVERALLOT OR EFFECT TRANSACTIONS WHICH STABILIZE OR MAINTAIN THE MARKET PRICES OF THE OFFERED VETERANS G.O. BONDS AT LEVELS ABOVE THAT WHICH MIGHT OTHERWISE PREVAIL IN THE OPEN MARKET. SUCH STABILIZING, IF COMMENCED, MAY BE DISCONTINUED AT ANY TIME. THE UNDERWRITERS MAY OFFER AND SELL THE OFFERED VETERANS G.O. BONDS TO CERTAIN DEALERS, INSTITUTIONAL INVESTORS AND OTHERS AT PRICES LOWER THAN THE PRICES OR YIELDS STATED ON THE INSIDE FRONT COVER PAGE HEREOF, AND SAID PRICES OR YIELDS MAY BE CHANGED FROM TIME TO TIME BY THE UNDERWRITERS.

THE OFFERED VETERANS G.O. BONDS WILL NOT BE REGISTERED UNDER THE SECURITIES ACT OF 1933, AS AMENDED, IN RELIANCE UPON AN EXEMPTION CONTAINED IN SUCH ACT. THE OFFERED VETERANS G.O. BONDS HAVE NOT BEEN REGISTERED OR QUALIFIED UNDER THE SECURITIES LAWS OF ANY STATE. THE OFFERED VETERANS G.O. BONDS HAVE NOT BEEN RECOMMENDED BY ANY FEDERAL OR STATE SECURITIES COMMISSION OR REGULATORY AUTHORITY, AND THE FOREGOING AUTHORITIES HAVE NEITHER REVIEWED NOR CONFIRMED THE ACCURACY OF THIS OFFICIAL STATEMENT.

TABLE OF CONTENTS Page Page

INTRODUCTION ................................................................... 1 Description of the Offered Veterans G.O. Bonds ............. 1 Security for and Sources of Payment of Veterans G.O.

Bonds ....................................................................... 1 Redemption ...................................................................... 2 Financial Condition of the State General Fund ................ 2 Information Related to the Official Statement .................. 3 Plan of Finance ................................................................. 4 Tax Matters ...................................................................... 5 Continuing Disclosure ...................................................... 5

AUTHORIZATION OF AND SECURITY FOR THE OFFERED VETERANS G.O. BONDS ................................... 6

Authorization ................................................................... 6 Security for and Sources of Payment of Veterans G.O.

Bonds ....................................................................... 6 The 1943 Fund ................................................................. 8 Remedies .......................................................................... 8

THE OFFERED VETERANS G.O. BONDS .......................... 9 General ............................................................................. 9 Identification and Authorization of the Offered

Veterans G.O. Bonds .............................................. 10 Redemption .................................................................... 10 Notice of Redemption .................................................... 21

TAX MATTERS .................................................................... 21 Federal Tax Matters ....................................................... 21 State Tax Matters ........................................................... 25 Miscellaneous ................................................................. 25

LEGAL MATTERS ............................................................... 26 LITIGATION ......................................................................... 26 UNDERWRITING ................................................................. 27 FINANCIAL STATEMENTS OF THE STATE ................... 27 REPORT OF INDEPENDENT AUDITORS AND FINANCIAL STATEMENTS OF THE PROGRAM ............ 27 RATINGS .............................................................................. 28 FINANCIAL ADVISOR ....................................................... 28 ADDITIONAL INFORMATION .......................................... 28 APPENDIX A THE STATE OF CALIFORNIA ............. A-1

APPENDIX B THE DEPARTMENT OF VETERANS AFFAIRS OF THE STATE OF CALIFORNIA, THE PROGRAM AND THE 1943 FUND ................................... B-1 INTRODUCTION ............................................................... B-1

Forward-Looking Statements ....................................... B-1 THE DEPARTMENT .......................................................... B-1

General ......................................................................... B-1 Governance of the Department ..................................... B-1 Administration of the Department ................................ B-2

THE PROGRAM ................................................................. B-4 History.......................................................................... B-4 General ......................................................................... B-4 Program Financing ....................................................... B-5 Certain Statutory Requirements ................................... B-5 Allocation of Lendable Moneys ................................... B-8 Administration of the Program ..................................... B-9 Contracts of Purchase ................................................. B-10 Mobile Homes Contracts of Purchase ........................ B-23

Home Improvement Contracts of Purchase ................ B-24 Construction Contracts of Purchase ........................... B-25 Pooled Self-Insurance Fund ....................................... B-25 USDVA Guaranty Program; Loan Insurance ............. B-26 Property Insurance ..................................................... B-29 Life and Disability Insurance ..................................... B-32 Legislative Protection of Veterans ............................. B-34 External Reviews of the Program ............................... B-35

THE 1943 FUND ............................................................... B-36 General ....................................................................... B-36 Selected Financial Data of the 1943 Fund and the

Program and Department’s Discussion .............. B-38 Department’s Discussion of Financial Data ............... B-41 Program Features Designed to Mitigate Market

Downturns .......................................................... B-48 Department Outlook ................................................... B-49 Investments of the 1943 Fund .................................... B-49 Excess Revenues ........................................................ B-50 Maintenance of Fund Parity ....................................... B-51

EXHIBIT 1 REPORT OF INDEPENDENT AUDITORS AND FINANCIAL STATEMENTS –VETERANS’ FARM AND HOME PURCHASE PROGRAM OF THE DEPARTMENT OF VETERANS AFFAIRS, STATE OF CALIFORNIA (VETERANS FARM AND HOME BUILDING FUND OF 1943, VETERANS DEBENTURE REVENUE FUND AND POOLED SELF-INSURANCE FUND) FOR THE FISCAL YEARS ENDED JUNE 30, 2015 AND 2014 .............................................B – Exhibit 1 - 1

EXHIBIT 2 CERTAIN DEPARTMENT FINANCIAL INFORMATION AND OPERATING DATA ..................................B – Exhibit 2 - 1

APPENDIX C DTC AND THE BOOK-ENTRY SYSTEM

APPENDIX D FORMS OF CONTINUING DISCLOSURE CERTIFICATES

APPENDIX E CERTAIN FEDERAL TAX CODE REQUIREMENTS

APPENDIX F PROPOSED FORM OF LEGAL OPINION OF ATTORNEY GENERAL

APPENDIX G PROPOSED FORM OF LEGAL OPINION OF BOND COUNSEL TO THE STATE

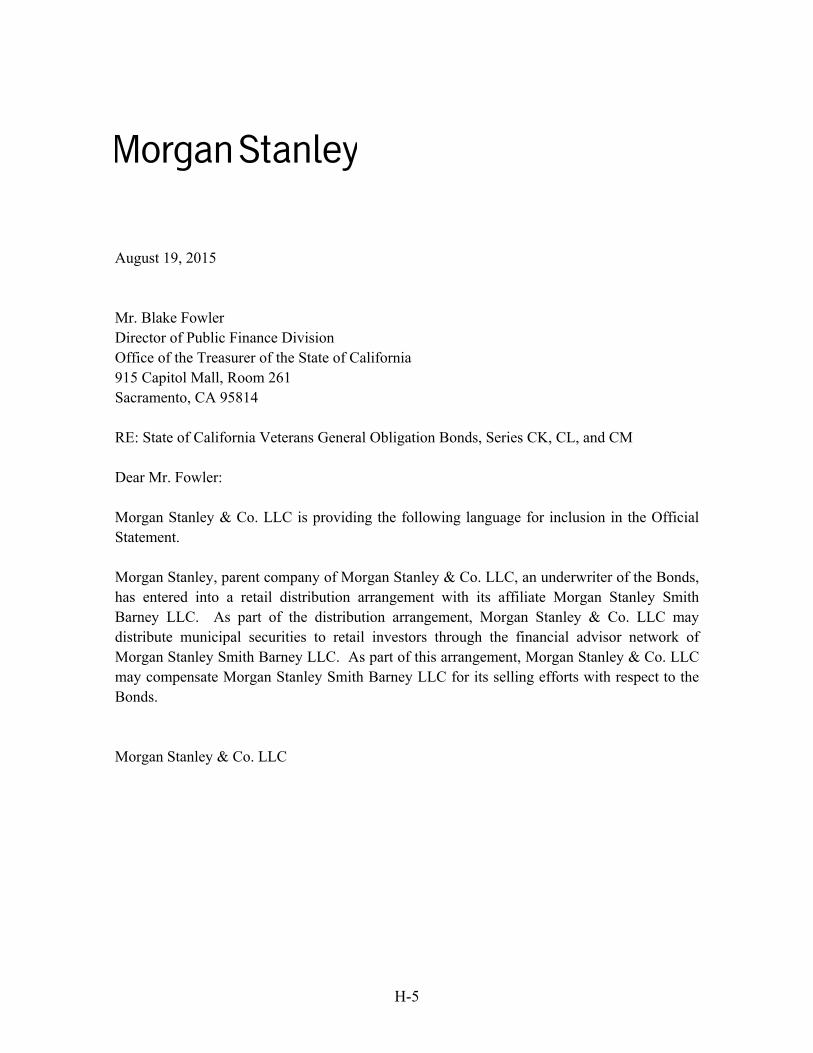

APPENDIX H LETTERS FROM CERTAIN UNDERWRITERS

APPENDIX I AUDITED BASIC FINANCIAL STATEMENTS OF THE STATE FOR THE FISCAL YEAR ENDED JUNE 30, 2014

1

OFFICIAL STATEMENT

$445,700,000 STATE OF CALIFORNIA

VETERANS GENERAL OBLIGATION BONDS $152,295,000

Series CK (Non-AMT) $128,610,000

Series CL (Non-AMT) $164,795,000

Series CM (AMT)

INTRODUCTION

This Introduction contains only a brief summary of the terms of the State of California Veterans General Obligation Bonds, Series CK (the “Series CK Bonds”); Veterans General Obligation Bonds, Series CL (the “Series CL Bonds”); and Veterans General Obligation Bonds, Series CM (the “Series CM Bonds,” and together with the Series CK Bonds and the Series CL Bonds, the “Offered Veterans G.O. Bonds”) and a brief description of this Official Statement. A full review should be made of the entire Official Statement, including Appendices. Summaries of provisions of the Constitution and laws of the State of California (the “State”) or any other documents referred to in this Official Statement do not purport to be complete and such summaries are qualified in their entirety by references to the respective complete provisions.

Description of the Offered Veterans G.O. Bonds

The issuance of veterans general obligation bonds and commercial paper notes (“Veterans G.O. Bonds”) is authorized by various general obligation bond acts, as amended (collectively, the “Bond Acts”) approved by the voters of the State and by resolutions of the Veterans’ Finance Committee of 1943 (the “Veterans’ Finance Committee”). The Offered Veterans G.O. Bonds are authorized by specific Bond Acts to finance or to refinance obligations that were issued to provide funds for the financing of contracts (“Contracts of Purchase”) for the purchase of homes and farms for California military veterans under the Farm and Home Purchase Program (the “Program”) of the Department of Veterans Affairs of the State (the “Department”). See “—Plan of Finance” below.

The Offered Veterans G.O. Bonds will be registered in the name of a nominee of The Depository Trust Company, New York, New York (“DTC”) which will act as securities depository for the Offered Veterans G.O. Bonds. Beneficial interests in the Offered Veterans G.O. Bonds may be purchased in book-entry form only, in denominations of $5,000 or any integral multiple thereof. The Offered Veterans G.O. Bonds will be dated the date of their delivery (the “Dated Date”) and will mature on the respective dates and in the respective amounts set forth on the inside cover page hereof. Interest on the Offered Veterans G.O. Bonds will accrue from the Dated Date at the respective rates shown on the inside cover page of this Official Statement, will be payable on June 1 and December 1 in each year (each, an “Interest Payment Date”) commencing December 1, 2015, and will be calculated on the basis of a 360-day year comprised of twelve 30-day months. See APPENDIX C – “DTC AND THE BOOK-ENTRY SYSTEM.”

Security for and Sources of Payment of Veterans G.O. Bonds

The Offered Veterans G.O. Bonds are general obligations of the State to which the full faith and credit of the State is pledged. The Military and Veterans Code (the “Veterans Code”) requires that, with respect to Veterans G.O. Bonds, on the dates when funds are to be remitted to

2

bondholders for the payment of debt service on such Veterans G.O. Bonds, there shall be transferred to a revolving special fund in the State Treasury (the “Veterans’ Bonds Payment Fund”) to pay the debt service on such Veterans G.O. Bonds, all of the money in the Veterans’ Farm and Home Building Fund of 1943 (the “1943 Fund”) (but not in excess of the amount of debt service then due and payable). Debt service on the Offered Veterans G.O. Bonds is payable first from moneys required under the Veterans Code to be transferred from the 1943 Fund to the Veterans’ Bonds Payment Fund and second, if the moneys transferred from the 1943 Fund to the Veterans’ Bonds Payment Fund are less than debt service then due and payable, the balance is payable from the General Fund of the State (the “General Fund”). The principal of and interest on all State general obligation bonds, including the Offered Veterans G.O. Bonds (as described above), are payable from moneys in the General Fund, subject under State law only to the prior application of such moneys to the support of the public school system and public institutions of higher education. The 1943 Fund is required to transfer to the General Fund, as soon as it becomes available, an amount equal to the amount paid by the General Fund, if any, together with interest thereon from the remittance date until paid, at the same rate of interest as borne by the applicable Veterans G.O. Bonds, compounded semiannually. The Veterans Code does not grant any lien on the 1943 Fund or the moneys therein to the holders of any Veterans G.O. Bonds (including the Offered Veterans G.O. Bonds). Each Bond Act authorizing the Offered Veterans G.O. Bonds provides that the State shall collect annually, in the same manner and at the same time as it collects other State revenues, a sum of money, in addition to the ordinary revenues of the State, sufficient to pay the principal of and interest on the respective Offered Veterans G.O. Bonds authorized under such Bond Act. See “AUTHORIZATION OF AND SECURITY FOR THE OFFERED VETERANS G.O. BONDS,” APPENDIX A – “THE STATE OF CALIFORNIA – STATE FINANCES – REVENUES, EXPENDITURES AND RESERVES – The General Fund” and “—STATE INDEBTEDNESS AND OTHER OBLIGATIONS – Capital Facilities Financing – General Obligation Bonds.” See also APPENDIX B – “THE DEPARTMENT OF VETERANS AFFAIRS OF THE STATE OF CALIFORNIA, THE PROGRAM AND THE 1943 FUND” for a discussion of the Department, the Program and the 1943 Fund.

Redemption

The Offered Veterans G.O. Bonds are subject to special redemption from Unexpended Proceeds (as defined below) and special redemption from Excess Revenues (as defined below) prior to maturity, as described below. In addition, certain Offered Veterans G.O. Bonds are subject to optional redemption, sinking fund redemption, and special mandatory redemption, prior to maturity, as described below. See “THE OFFERED VETERANS G.O. BONDS – Redemption.”

Financial Condition of the State General Fund

The following paragraphs present an extremely abbreviated summary of certain fiscal issues relating to the State, all of which are described in more detail in APPENDIX A. All cross references under this heading are to sections of APPENDIX A—“THE STATE OF CALIFORNIA.” Capitalized terms used under “—Financial Condition of the State General Fund” and not defined in the forepart to this Official Statement have the meanings ascribed to them in APPENDIX A. Investors should review the whole of APPENDIX A.

3

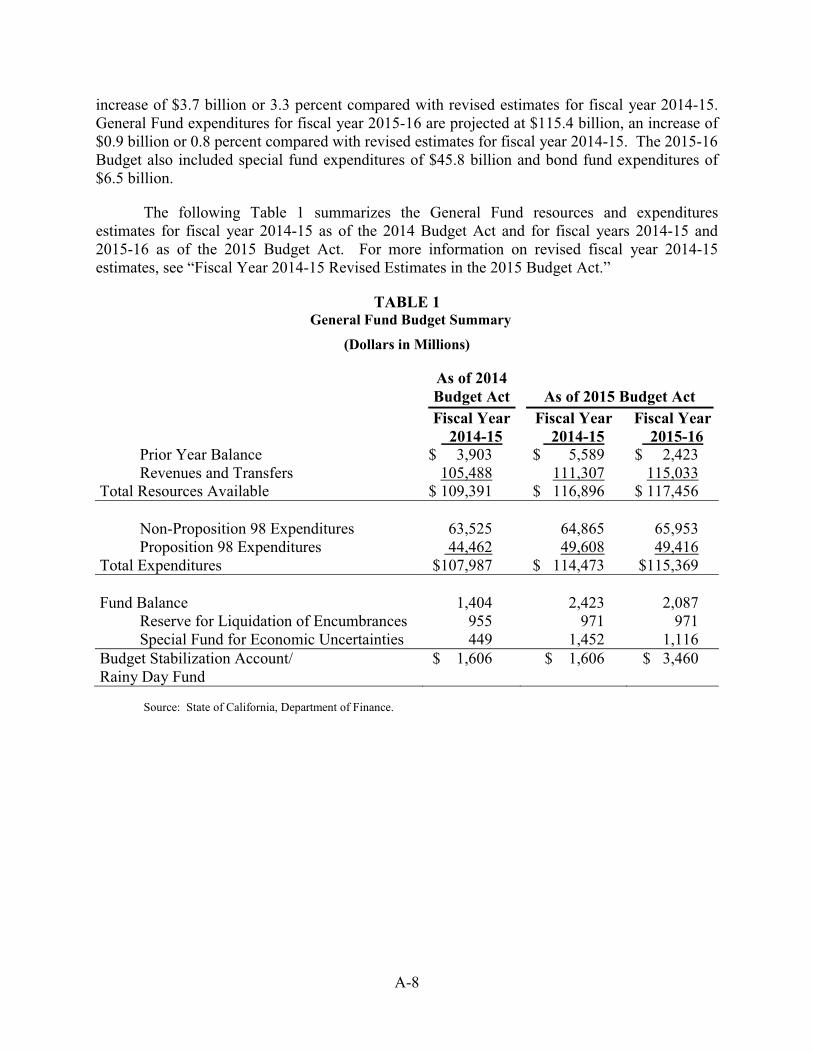

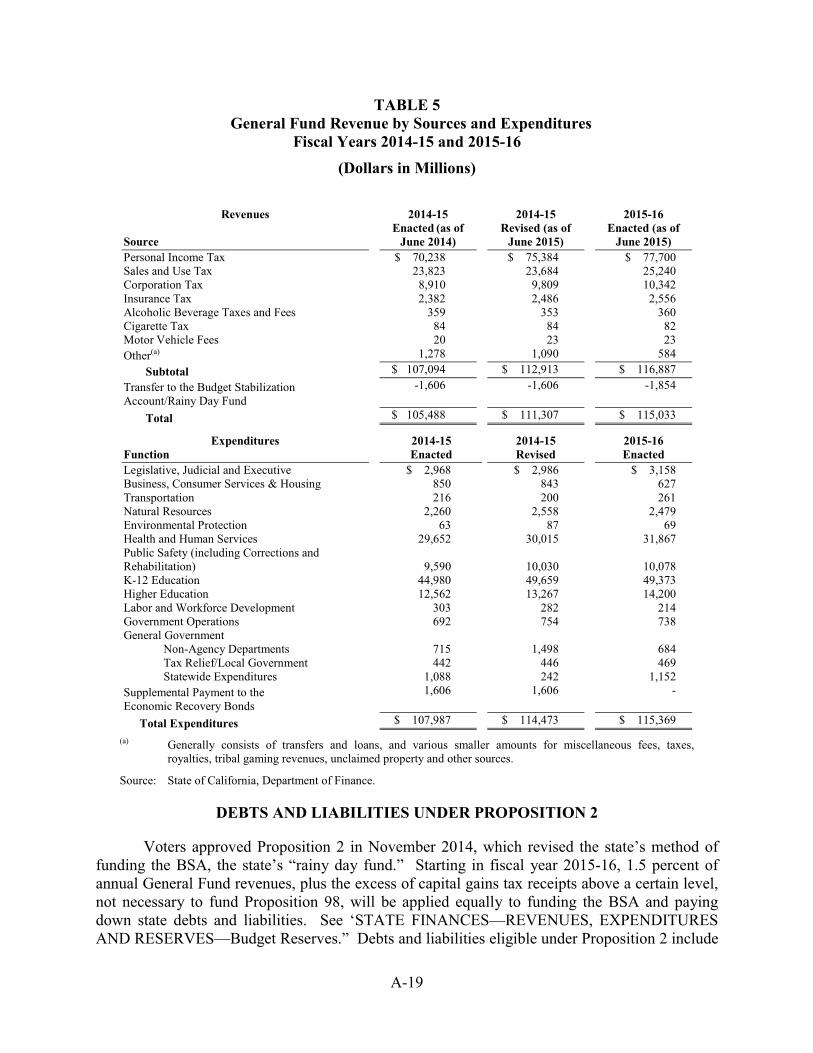

The State’s fiscal health has significantly improved since the end of the severe recession in 2009. Voters approved Proposition 30 in November 2012, providing increased revenues through December 31, 2018. Voters also approved Proposition 2 in November 2014, which directs specified revenues towards increasing reserves in the Budget Stabilization Account (“BSA”), the State’s rainy day fund, and paying down specified debts. See “DEBTS AND LIABILITIES UNDER PROPOSITION 2” and “STATE FINANCES – REVENUES, EXPENDITURES AND RESERVES—Budget Reserves—Budget Stabilization Account.” In recent years, the State has paid off billions of dollars of budgetary borrowings, debts and deferrals which were accumulated in order to balance budgets during the previous recession and years prior.

By the end of fiscal year 2015-16, the BSA is projected to have a balance of $3.5 billion. Under the Proposition 2 requirements, the 2015 Budget Act directs an additional $1.9 billion to pay off loans from special funds, pay down past liabilities from Proposition 98, and help the University of California reduce its employee pension unfunded liability.

In addition, the 2015-16 Budget repays the remaining $1 billion in budgetary deferrals to schools and community colleges, discharges the last of the $15 billion in Economic Recovery Bonds that were issued to cover budget deficits from as far back as 2002, repays local governments $765 million in mandated reimbursements, and reduces outstanding mandate liabilities owed to schools and community colleges by $3.8 billion.

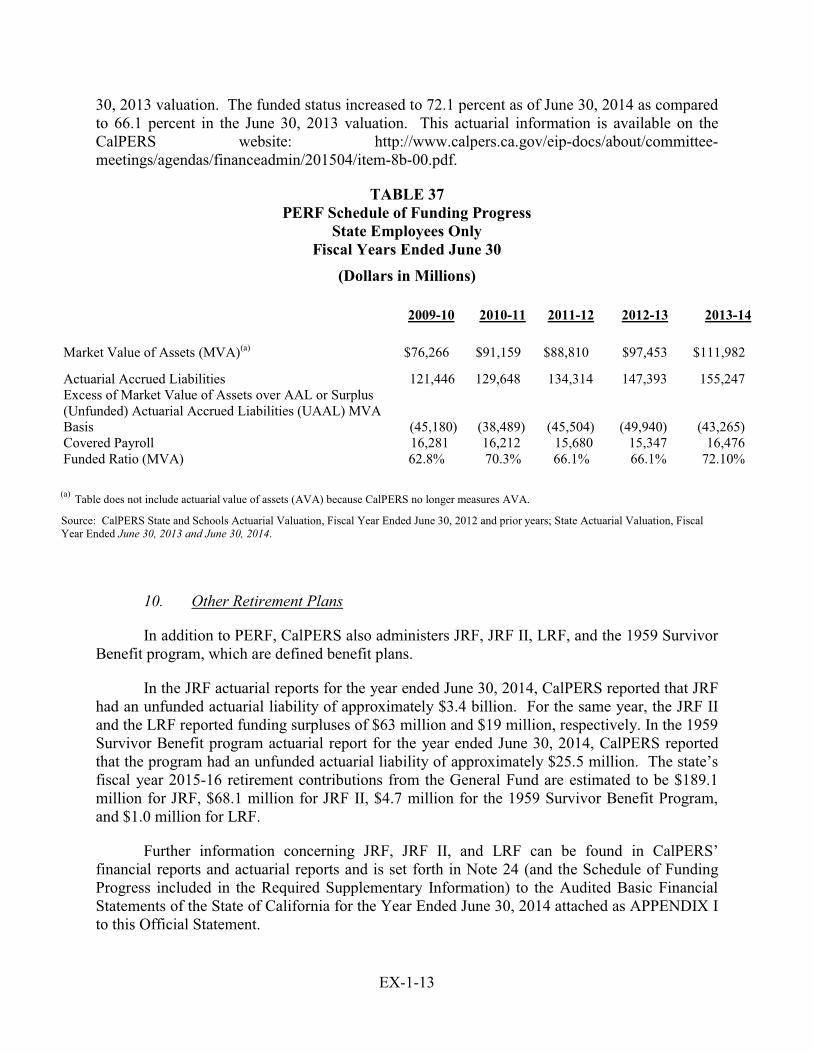

Despite the recent significant budgetary improvements, there remain a number of budget risks that threaten the State’s financial condition, including the significant unfunded liabilities of the two main retirement systems managed by State entities, the California Public Employees’ Retirement System (“CalPERS”) and the California State Teachers’ Retirement System (“CalSTRS”). In recent years, the State has committed to significant increases in annual payments to these systems to reduce the unfunded liabilities. The State also has a significant unfunded liability with respect to other post-employment benefits. See “CURRENT STATE BUDGET—Budget Risks” and “STATE FINANCES—OTHER ELEMENTS—Pension Systems” and “—Retiree Health Care Costs.”

In addition, the State’s revenues (particularly the personal income tax) can be volatile and correlate to overall economic conditions. See “STATE FINANCES – REVENUES, EXPENDITURES AND RESERVES—Sources of Tax Revenue.” Under Proposition 2, upswings in personal income taxes derived from capital gains will be deposited in the BSA and used to pay off certain of the State’s debts and liabilities. However, during the last recession the State experienced a significant economic downturn and State tax revenues declined precipitously, resulting in budget deficits in the tens of billions of dollars. There can be no assurances that the State will not face fiscal stress and cash pressures again, or that other changes in the State or national economies will not materially adversely affect the financial condition of the State.

Information Related to the Official Statement

All financial and other information presented or incorporated by reference in this Official Statement has been provided by, respectively, the State or the Department from its records, except for information expressly attributed to other sources. The presentation of historical information, including tables of receipts from taxes and other revenues, is intended to show recent historical information and is not intended to indicate future or continuing trends in the

4

financial position or other affairs of, respectively, the State or the Department. No representation is made that past experience, as it might be shown by such financial and other information, will necessarily continue or be repeated in the future. Certain statements included or incorporated by reference in this Official Statement constitute “forward-looking statements.” Such statements are generally identifiable by the terminology used such as “plan,” “expect,” “estimate,” “budget” or other similar words. The achievement of certain results or other expectations contained in such forward-looking statements involve known and unknown risks, uncertainties and other factors that may cause actual results, performance or achievements attained to be materially different from any future results, performance or achievements expressed or implied by such forward-looking statements. Any statements made in this Official Statement involving matters of opinion, whether expressly stated or not, are set forth as such and not as representations of fact.

The information set forth in this Official Statement has been obtained from official sources that are believed to be reliable, but such information is not guaranteed as to accuracy or completeness. Estimates and opinions are included and should not be interpreted as statements of fact. Summaries of documents do not purport to be complete statements of their provisions and such summaries are qualified by references to the entire contents of the summarized documents. The information and expressions of opinion herein are subject to change without notice, and neither the delivery of this Official Statement nor any sale made by use of this Official Statement shall, under any circumstances, create any implication that there has been no change in the affairs of the State or the Department since the date hereof.

A wide variety of other information, including financial information, concerning the State and the Department is available from State agencies, State agency publications and State agency websites. Such information includes websites operated by the Department, the State Department of Finance, the State Controller’s Office and the State Treasurer’s Office. Any such information that is inconsistent with the information set forth in this Official Statement should be disregarded. No such information is a part of or incorporated into this Official Statement, except as expressly noted.

The information in APPENDIX C – “DTC AND THE BOOK-ENTRY SYSTEM” regarding DTC and its book-entry system has been furnished by DTC and no representation is made by the State or the Department as to the accuracy or completeness of such information.

This Official Statement does not constitute an offer to sell the Offered Veterans G.O. Bonds or the solicitation of an offer to buy, nor shall there be any sale of the Offered Veterans G.O. Bonds, by any person in any state or other jurisdiction to any person to whom it is unlawful to make such offer, solicitation or sale in such state or jurisdiction.

Plan of Finance

Under the Program, the Department acquires residential property to be sold to eligible veterans under Contracts of Purchase between the Department and such veterans. Such acquisition is financed principally with the proceeds of Veterans G.O. Bonds and the Revenue Bonds (as defined below) and from other moneys available in the 1943 Fund. The Offered Veterans G.O. Bonds are being issued for the purposes of (i) reimbursing the Department for existing Contracts of Purchase previously funded by the 1943 Fund, (ii) funding Contracts of Purchase to be originated in the future, (iii) refunding certain outstanding Veterans G.O. Bonds, and (iv) paying certain costs of issuance of the Offered Veterans G.O. Bonds. The Contracts of

5

Purchase financed with proceeds of the Series CL Bonds (the “Series CL Contracts of Purchase”), and the Contracts of Purchase financed with proceeds of the Veterans G.O. Bonds being refunded with proceeds of the Series CK Bonds and the Series CM Bonds that are reallocated for Federal Tax Code purposes to such Offered Veterans G.O. Bonds (the “Series CK and Series CM Reallocated Contracts of Purchase”), are collectively referred to herein as the “Offered Veterans G.O. Bonds Contracts of Purchase.” See EXHIBIT 2 to APPENDIX B – “CERTAIN DEPARTMENT FINANCIAL INFORMATION AND OPERATING DATA – Amounts Expected to be Available to Fund Contracts of Purchase and Related Investments” for information regarding the amount of money currently available and also expected to be made available to finance new Contracts of Purchase following the issuance of the Offered Veterans G.O. Bonds.

Tax Matters

In the opinion of Hawkins Delafield & Wood LLP, Bond Counsel to the State, under existing statutes and court decisions and assuming continuing compliance with certain tax covenants described in such opinion, (i) interest on the Offered Veterans G.O. Bonds is excluded from gross income for Federal income tax purposes pursuant to Section 103 of the Internal Revenue Code of 1986, as amended (the “Federal Tax Code”); (ii) interest on the Series CK Bonds is not treated as a preference item in calculating the alternative minimum tax imposed on individuals and corporations under the Federal Tax Code; such interest, however, is included in the adjusted current earnings of certain corporations for purposes of calculating the alternative minimum tax imposed on such corporations; (iii) interest on the Series CL Bonds is not treated as a preference item in calculating the alternative minimum tax imposed on individuals and corporations under the Federal Tax Code and is not included in the adjusted current earnings of corporations for purposes of calculating the alternative minimum tax; and (iv) interest on the Series CM Bonds is treated as a preference item in calculating the alternative minimum tax imposed on individuals and corporations under the Federal Tax Code. In the opinion of Bond Counsel to the State, under State law, interest on the Offered Veterans G.O. Bonds is exempt from State personal income taxes. See “TAX MATTERS” below, APPENDIX E – “CERTAIN

FEDERAL TAX CODE REQUIREMENTS” and APPENDIX G – “PROPOSED FORM OF

LEGAL OPINION OF BOND COUNSEL TO THE STATE.”

Continuing Disclosure

The State Treasurer will agree on behalf of the State to provide annually certain financial information and operating data relating to the State by not later than April 1 of each year in which any Offered Veterans G.O. Bonds are outstanding (the “State’s Annual Report”), commencing with the report to be filed on or before April 1, 2016, containing 2014-2015 Fiscal Year financial information, and to provide notice of the occurrence of certain enumerated events.

The Department Secretary will agree to provide annually certain financial information and operating data relating to the Program by not later than April 1 of each year in which any Offered Veterans G.O. Bonds are outstanding (the “Department’s Annual Report”), commencing with the report to be filed on or before April 1, 2016, containing the 2014-2015 fiscal year financial information.

The specific nature of the information to be contained in the State’s Annual Report, the Department’s Annual Report and the notices of events and certain other terms of the continuing

6

disclosure obligations are set forth in APPENDIX D—“FORMS OF CONTINUING DISCLOSURE CERTIFICATES.” The State Treasurer has adopted policies and procedures designed to ensure compliance with its continuing disclosure undertakings. The Department has policies and procedures designed to ensure compliance with its continuing disclosure undertakings.

Certain prior annual reports of the State Treasurer, certain prior reports of financial information and operating data relating to the Program, and other reports and notices are available from the Electronic Municipal Market Access (“EMMA”) website (www.emma.msrb.org) operated by the Municipal Securities Rulemaking Board (“MSRB”) or on such other website as may be designated by MSRB or the Securities and Exchange Commission. The information contained on any such website is not part of this Official Statement and is not incorporated herein.

AUTHORIZATION OF AND SECURITY FOR THE OFFERED VETERANS G.O. BONDS

Authorization

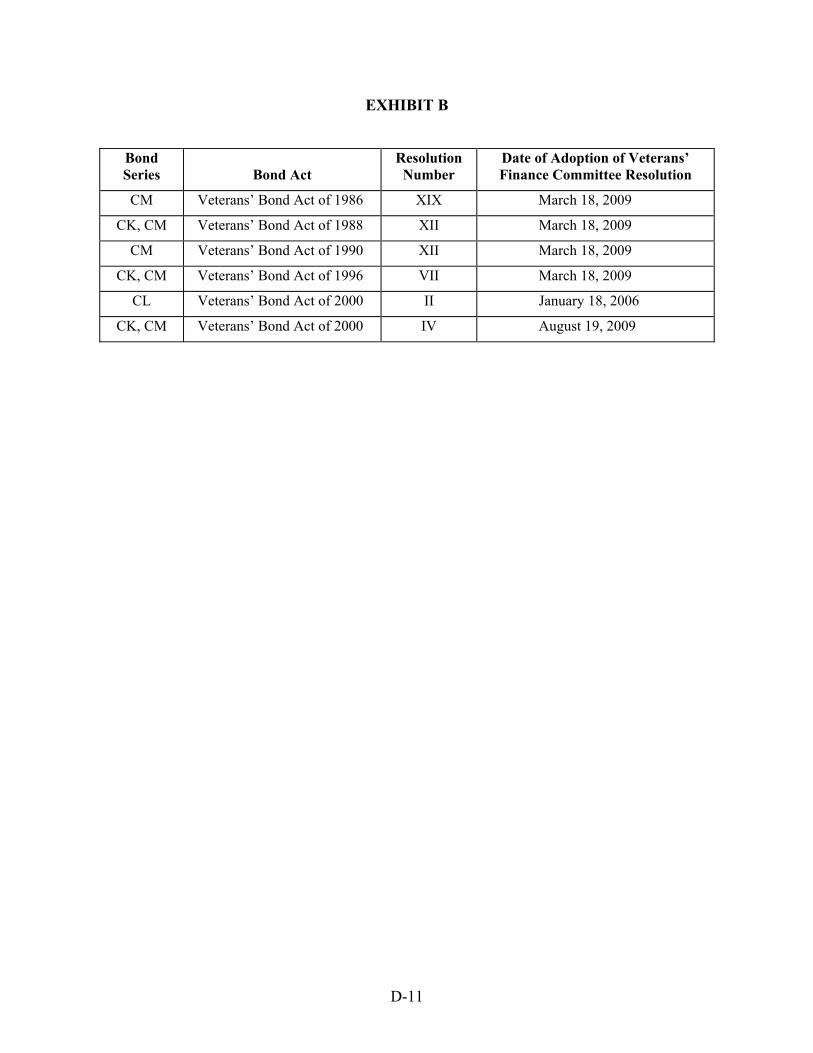

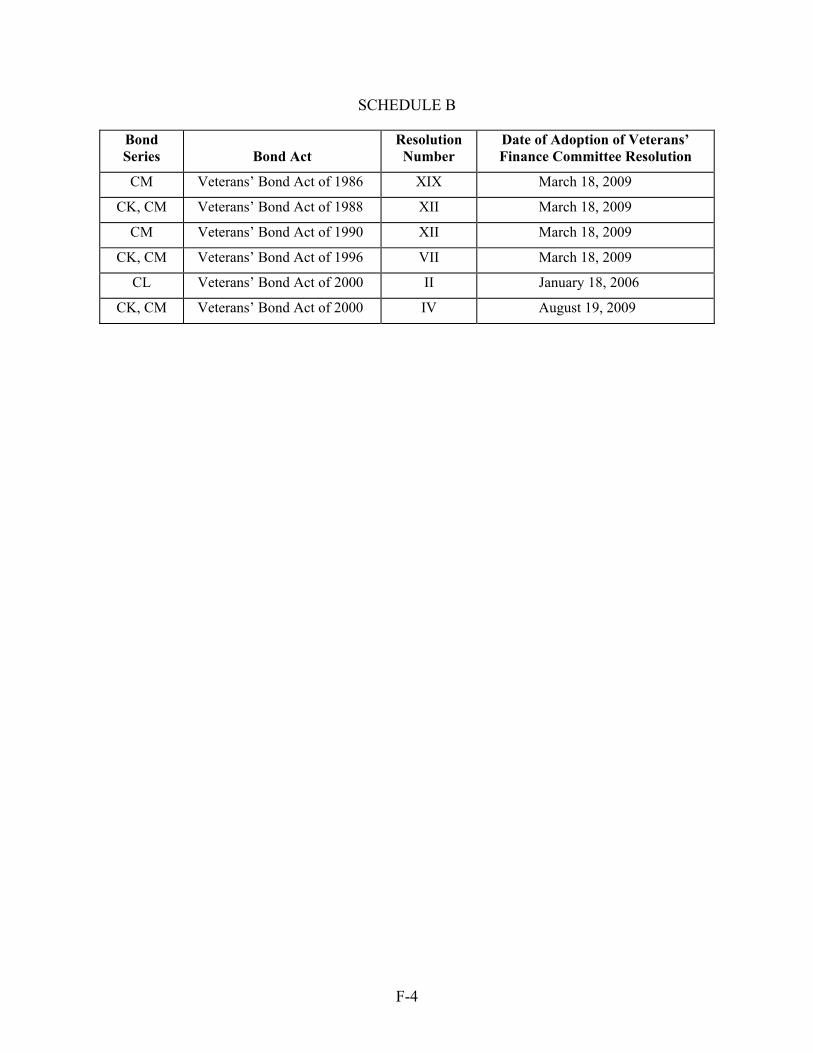

The issuance of Veterans G.O. Bonds is authorized by Bond Acts approved by the voters of the State and by resolutions of the Veterans’ Finance Committee. The State General Obligation Bond Law (the “Law”), which is set forth in Chapter 4 (commencing with Section 16720) of Part 3 of Division 4 of Title 2 of the California Government Code as incorporated by reference into each Bond Act, provides for the authorization, sale, issuance, use of proceeds, repayment and refunding of State general obligation bonds, including Veterans G.O. Bonds. The Offered Veterans G.O. Bonds are authorized under the specific Bond Acts identified under “THE OFFERED VETERANS G.O. BONDS – Identification and Authorization of the Offered Veterans G.O. Bonds” and by resolutions adopted by the Veterans’ Finance Committee (collectively, the “Resolutions”).

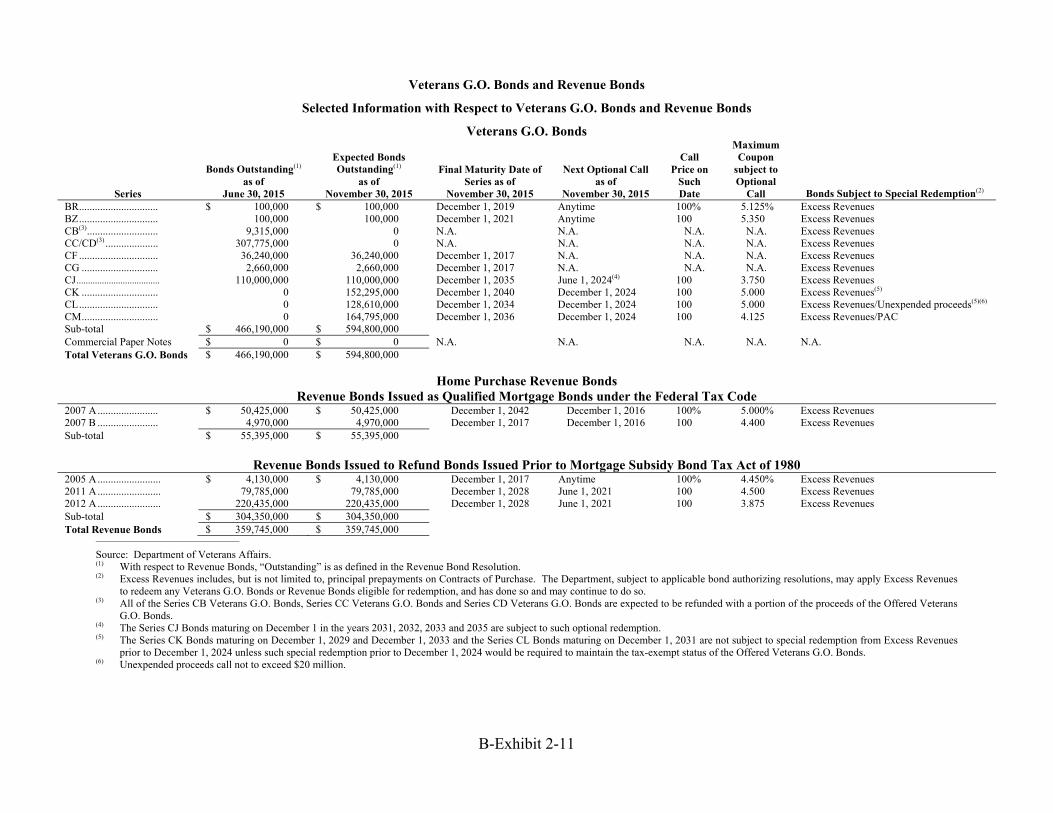

As of July 1, 2015, $428,610,000 of Veterans G.O. Bonds are authorized but not issued, there were outstanding approximately $466,190,000 aggregate principal amount of Veterans G.O. Bonds and there were no outstanding commercial paper notes. See APPENDIX B – “THE DEPARTMENT OF VETERANS AFFAIRS OF THE STATE OF CALIFORNIA, THE PROGRAM AND THE 1943 FUND,” including EXHIBIT 2 to APPENDIX B – “CERTAIN DEPARTMENT FINANCIAL INFORMATION AND OPERATING DATA – Veterans G.O. Bonds and Revenue Bonds.”

Security for and Sources of Payment of Veterans G.O. Bonds

Veterans G.O. Bonds are general obligations of the State. The Veterans Code establishes in the State Treasury the Veterans’ Bonds Payment Fund, a revolving special fund, and requires that on the dates when funds are to be remitted to bondholders for the payment of debt service on Veterans G.O. Bonds, there shall be transferred to the Veterans’ Bonds Payment Fund to pay the debt service on such Veterans G.O. Bonds all of the money in the 1943 Fund (but not in excess of the amount of debt service then due and payable). Debt service on Veterans G.O. Bonds is payable first from the moneys required under the Veterans Code to be transferred from the 1943 Fund to the Veterans’ Bonds Payment Fund and second, if the moneys transferred from the 1943 Fund to the Veterans’ Bonds Payment Fund are less than debt service then due and payable, the balance is payable from the General Fund. The principal of and interest on all State general

7

obligation bonds are payable from moneys in the General Fund, subject under State law only to the prior application of such moneys to the support of the public school system and public institutions of higher education. The 1943 Fund is required to transfer to the General Fund, as soon as it becomes available, an amount equal to the amount paid by the General Fund, if any, together with interest thereon from the remittance date until paid at the same rate of interest as borne by the applicable Veterans G.O. Bonds, compounded semiannually. The Veterans Code does not grant any lien on the 1943 Fund or the moneys therein to the holders of any Veterans G.O. Bonds. The 1943 Fund has always made its payments in a timely manner and in an amount sufficient such that the required debt service payments on Veterans G.O. Bonds have been paid.

The Veterans Code states that moneys in the Veterans’ Bonds Payment Fund are (i) required to be used solely to pay debt service when due on Veterans G.O. Bonds, (ii) not considered “surplus money” for the purposes of the California Government Code and (iii) prohibited from being borrowed by, or transferred to, the General Fund or to the General Cash Revolving Fund.

Each of the Bond Acts provides that the State will collect annually in the same manner and at the same time as it collects other State revenues, an amount sufficient to pay principal of and interest on the Veterans G.O. Bonds authorized under such Bond Act in that year. Each of the Bond Acts also contain a continuing appropriation from the General Fund of the sum annually necessary to pay the principal of and the interest on the Veterans G.O. Bonds authorized under such Bond Act as they become due and payable. No further appropriation by the State Legislature is required to pay the principal of and interest on Veterans G.O. Bonds. Under the State Constitution, the appropriation from the General Fund to pay the principal of and interest on Veterans G.O. Bonds as set forth in the related Bond Act cannot be repealed until the principal of and interest on such Veterans G.O. Bonds are paid and discharged.

Each of the Bond Acts provides that the Veterans G.O. Bonds issued thereunder constitute valid and legally binding general obligations of the State, and the full faith and credit of the State is pledged for the punctual payment of the principal of, and interest on, the Veterans G.O. Bonds, as the principal and interest become due and payable. The pledge of the full faith and credit of the State alone does not create a lien on any particular moneys in the General Fund or any other assets of the State, but is an undertaking by the State to be irrevocably obligated in good faith to use its taxing powers as may be required for the full and prompt payment of the principal of and interest on all State general obligation bonds, including the Veterans G.O. Bonds to the extent that the moneys transferred from the 1943 Fund to the Veterans’ Bonds Payment Fund are less than debt service then due and payable. The only provision of the State Constitution that creates a higher priority for any State fiscal obligation is a provision directing that from all State revenues, there will first be set apart the moneys to be applied by the State for the support of the public school system and public institutions of higher education. In the past when cash resources in the General Fund have been constrained, State officials have worked within their powers granted by State law to manage cash resources to ensure that payments to schools and universities and for general obligation debt service would be made. On any debt service payment date, all State general obligation bonds, including the Veterans G.O. Bonds, have an equal claim on moneys in the General Fund on that date for payment of debt service. See APPENDIX A – “THE STATE OF CALIFORNIA – STATE INDEBTEDNESS AND OTHER OBLIGATIONS – Capital Facilities Financing – General Obligation Bonds.”

8

The 1943 Fund

The Department’s principal fund for the Program is the 1943 Fund. As more particularly described herein, the moneys in the 1943 Fund are used to pay the amount of required debt service to the Veterans’ Bonds Payment Fund, for payment of principal and interest on Veterans G.O. Bonds, and if necessary, are used to reimburse the General Fund for any amounts paid from the General Fund for debt service on the Veterans G.O. Bonds, including to pay interest thereon to the General Fund from the date of remittance from the General Fund until paid at the same rate of interest as borne by the applicable Veterans G.O. Bonds, compounded semiannually.

The Department also issues Home Purchase Revenue Bonds (the “Revenue Bonds”) the debt service on which is payable from the 1943 Fund, pursuant to the Veterans’ Revenue Debenture Act of 1970, as amended (the “Act”), a Resolution of Issuance for Department of Veterans Affairs of the State of California Home Purchase Revenue Bonds, adopted March 19, 1980, as amended and supplemented (the “Revenue Bond Resolution”), and separate authorizing resolutions. Revenue Bonds issued by the Department are special obligations of the Department payable solely from, and secured by a pledge of, an undivided interest in the assets of the 1943 Fund (other than proceeds of Veterans G.O. Bonds or any amounts in any rebate account) and any reserve accounts established for the benefit of Revenue Bonds. The Act provides that this undivided interest in the assets of the 1943 Fund of holders of the Revenue Bonds is secondary and subordinate to any interest or right in the assets of the 1943 Fund of the people of the State and of the holders of the Veterans G.O. Bonds. If the transfers required to be made to the Veterans’ Bonds Payment Fund for payment of debt service on Veterans G.O. Bonds have been made, no holder or beneficial owner of Veterans G.O. Bonds has any right to restrict disbursements by the Department from the 1943 Fund for any lawful purpose, including payment of debt service on or redemptions and purchases of Revenue Bonds. The 1943 Fund is required to reimburse the General Fund for any debt service payments on the Veterans G.O. Bonds paid by the General Fund to the extent of any shortfalls in transfers from the 1943 Fund to the Veterans’ Bonds Payment Fund, including to pay interest thereon to the General Fund as described herein, before the 1943 Fund may make payments on Revenue Bonds (although payments on Revenue Bonds may be made from amounts on deposit in any reserve accounts established for the benefit of Revenue Bonds and, if any, in the loan loss account held in the Veterans Debenture Revenue Fund). As of July 1, 2015, there were approximately $359,745,000 aggregate principal amount of Revenue Bonds outstanding.

For additional information, see APPENDIX B – “THE DEPARTMENT OF VETERANS AFFAIRS OF THE STATE OF CALIFORNIA, THE PROGRAM AND THE 1943 FUND – THE 1943 FUND.”

Remedies

Under each Resolution it is an event of default of the State to fail to pay or to fail to cause to be paid, when due, principal of or interest or premium on any Offered Veterans G.O. Bond issued pursuant thereto or to declare a moratorium on the payment of or to repudiate any Offered Veterans G.O. Bond authorized under such Resolution.

The Resolutions do not contain any provision providing for the acceleration of the Offered Veterans G.O. Bonds authorized thereunder. Each Resolution states with regard to the Offered Veterans G.O. Bonds authorized by such Resolution that in the case that one or more events of default occurs, then, and in every such case, the registered Bondholder is entitled to

9

proceed to protect and enforce such registered Bondholder’s rights by such appropriate judicial proceeding as such registered Bondholder deems most effectual to protect and enforce any such right, whether by mandamus or other suit or proceeding at law or in equity, for the specific performance of any covenant or agreement contained in such Resolution, or in aid of the exercise of any power granted in such Resolution, or to enforce any other legal or equitable right vested in the Bondholders by such Resolution or by law, as more specifically set forth in such Resolution authorizing the applicable Offered Veterans G.O. Bonds pursuant to the respective Bond Act. Beneficial owners of the Offered Veterans G.O. Bonds (the “Beneficial Owners”) cannot protect and enforce such rights except through the registered Bondholder. See “THE OFFERED VETERANS G.O. BONDS – General” and APPENDIX C – “DTC AND THE BOOK–ENTRY SYSTEM.”

Since the State has never failed to make a debt service payment on any general obligation bond, including any Veterans G.O. Bonds, when due, the exact steps which would be taken, or the remedies available to Bondholders, have never been tested. There are no cross-default provisions among general obligation bonds, including any Veterans G.O. Bonds, so any default with respect to any particular issue of bonds would not provide any remedy to holders of other bonds which are not affected. Neither the State nor the Department is eligible to file for protection under the Federal bankruptcy laws.

THE OFFERED VETERANS G.O. BONDS

General

The Offered Veterans G.O. Bonds will be registered in the name of the nominee of DTC, which will act as securities depository for the Offered Veterans G.O. Bonds. Beneficial interests in the Offered Veterans G.O. Bonds may be purchased in book-entry form only, in denominations of $5,000 or any integral multiple thereof. See APPENDIX C – “DTC AND THE BOOK-ENTRY SYSTEM.”

Principal and interest are payable directly to DTC. Upon receipt of payments of principal and interest, it is the responsibility of DTC to in turn remit such principal and interest to the Direct Participants in DTC for disbursement to the Beneficial Owners of the Offered Veterans G.O. Bonds. None of the State Treasurer, the Department nor the Underwriters can give any assurances that DTC will distribute to Direct Participants, or that Participants or others will distribute to the Beneficial Owners, payment of principal of and interest on the Offered Veterans G.O. Bonds or any redemption or other notices or that they will do so on a timely basis or will serve and act in the manner described in this Official Statement. None of the State Treasurer, the Department nor the Underwriters is responsible or liable for the failure of DTC or any Direct Participant or Indirect Participant to make any payments or give any notice to a Beneficial Owner with respect to the Offered Veterans G.O. Bonds or for any error or delay relating thereto.

The Offered Veterans G.O. Bonds will be dated the Dated Date and will mature on the respective dates and in the respective amounts set forth on the inside cover page hereof. Interest on the Offered Veterans G.O. Bonds will accrue from the Dated Date at the respective rates shown on the inside cover page of this Official Statement. Interest on the Offered Veterans G.O. Bonds is payable on each Interest Payment Date commencing December 1, 2015 and shall be calculated on the basis of a 360-day year comprised of twelve 30-day months. The record date for the payment of interest on the Offered Veterans G.O. Bonds is the close of business on the

10

15th day of the month immediately preceding an Interest Payment Date, whether or not the record date falls on a business day.

The information in APPENDIX C—“DTC AND THE BOOK-ENTRY SYSTEM” regarding DTC and its book-entry system has been furnished by DTC and no representation is made by the State, the Department or the Underwriters as to the accuracy or completeness of such information.

Identification and Authorization of the Offered Veterans G.O. Bonds

The Offered Veterans G.O. Bonds are being issued pursuant to the Bond Acts described below.

Authorization

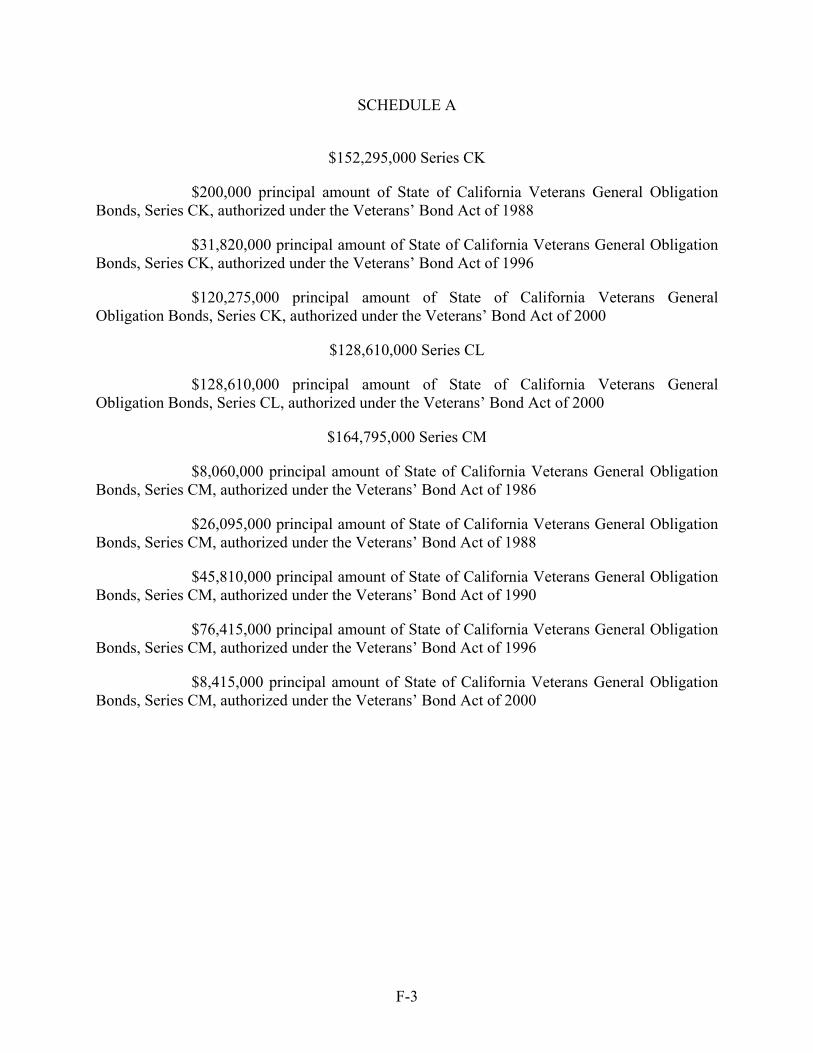

$200,000 principal amount of Series CK Bonds, authorized under the Veterans’ Bond Act of 1988;

$31,820,000 principal amount of Series CK Bonds, authorized under the Veterans’ Bond Act of 1996;

$120,275,000 principal amount of Series CK Bonds, authorized under the Veterans’ Bond Act of 2000;

$128,610,000 principal amount of Series CL Bonds, authorized under the Veterans’ Bond Act of 2000;

$8,060,000 principal amount of Series CM Bonds, authorized under the Veterans’ Bond Act of 1986;

$26,095,000 principal amount of Series CM Bonds, authorized under the Veterans’ Bond Act of 1988;

$45,810,000 principal amount of Series CM Bonds, authorized under the Veterans’ Bond Act of 1990;

$76,415,000 principal amount of Series CM Bonds, authorized under the Veterans’ Bond Act of 1996; and

$8,415,000 principal amount of Series CM Bonds, authorized under the Veterans’ Bond Act of 2000.

Redemption

Optional Redemption

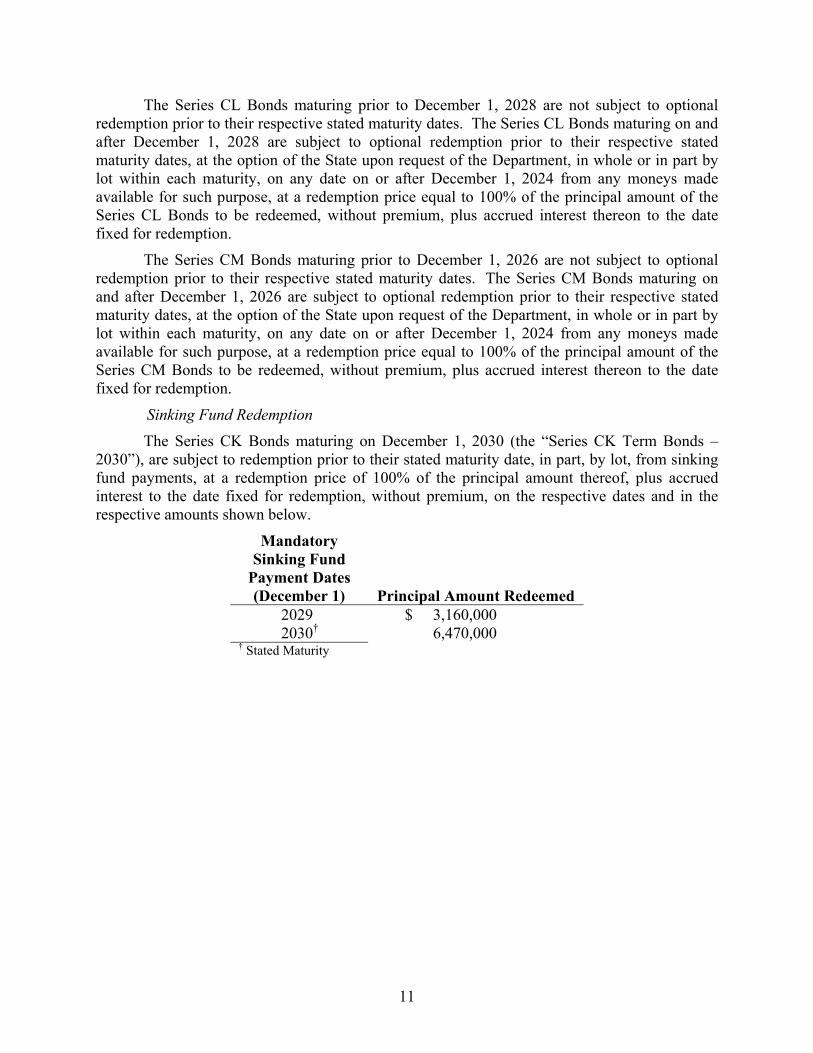

The Series CK Bonds maturing prior to December 1, 2026 are not subject to optional redemption prior to their respective stated maturity dates. The Series CK Bonds maturing on and after December 1, 2026 are subject to optional redemption prior to their respective stated maturity dates, at the option of the State upon request of the Department, in whole or in part by lot within each maturity, on any date on or after December 1, 2024 from any moneys made available for such purpose, at a redemption price equal to 100% of the principal amount of the Series CK Bonds to be redeemed, without premium, plus accrued interest thereon to the date fixed for redemption.

11

The Series CL Bonds maturing prior to December 1, 2028 are not subject to optional redemption prior to their respective stated maturity dates. The Series CL Bonds maturing on and after December 1, 2028 are subject to optional redemption prior to their respective stated maturity dates, at the option of the State upon request of the Department, in whole or in part by lot within each maturity, on any date on or after December 1, 2024 from any moneys made available for such purpose, at a redemption price equal to 100% of the principal amount of the Series CL Bonds to be redeemed, without premium, plus accrued interest thereon to the date fixed for redemption.

The Series CM Bonds maturing prior to December 1, 2026 are not subject to optional redemption prior to their respective stated maturity dates. The Series CM Bonds maturing on and after December 1, 2026 are subject to optional redemption prior to their respective stated maturity dates, at the option of the State upon request of the Department, in whole or in part by lot within each maturity, on any date on or after December 1, 2024 from any moneys made available for such purpose, at a redemption price equal to 100% of the principal amount of the Series CM Bonds to be redeemed, without premium, plus accrued interest thereon to the date fixed for redemption.

Sinking Fund Redemption

The Series CK Bonds maturing on December 1, 2030 (the “Series CK Term Bonds – 2030”), are subject to redemption prior to their stated maturity date, in part, by lot, from sinking fund payments, at a redemption price of 100% of the principal amount thereof, plus accrued interest to the date fixed for redemption, without premium, on the respective dates and in the respective amounts shown below.

Mandatory Sinking Fund

Payment Dates (December 1) Principal Amount Redeemed

2029 $ 3,160,000 2030† 6,470,000

† Stated Maturity

12

The Series CK Bonds maturing on December 1, 2035 (the “Series CK Term Bonds – 2035”), are subject to redemption prior to their stated maturity date, in part, by lot, from sinking fund payments, at a redemption price of 100% of the principal amount thereof, plus accrued interest to the date fixed for redemption, without premium, on the respective dates and in the respective amounts shown below.

Mandatory Sinking Fund

Payment Dates (December 1) Principal Amount Redeemed

2031 $ 6,760,000 2032 7,070,000 2033 9,585,000 2034 13,310,000 2035† 13,945,000

† Stated Maturity

The Series CK Bonds maturing on December 1, 2040 (the “Series CK Term Bonds – 2040”), are subject to redemption prior to their stated maturity date, in part, by lot, from sinking fund payments, at a redemption price of 100% of the principal amount thereof, plus accrued interest to the date fixed for redemption, without premium, on the respective dates and in the respective amounts shown below.

Mandatory Sinking Fund

Payment Dates (December 1) Principal Amount Redeemed

2036 $ 14,610,000 2037 15,300,000 2038 16,025,000 2039 16,790,000 2040† 17,590,000

† Stated Maturity

The Series CL Bonds maturing on December 1, 2030 (the “Series CL Term Bonds – 2030”), are subject to redemption prior to their stated maturity date, in part, by lot, from sinking fund payments, at a redemption price of 100% of the principal amount thereof, plus accrued interest to the date fixed for redemption, without premium, on the respective dates and in the respective amounts shown below.

Mandatory Sinking Fund

Payment Dates (December 1) Principal Amount Redeemed

2029 $ 27,415,000 2030† 25,805,000

† Stated Maturity

13

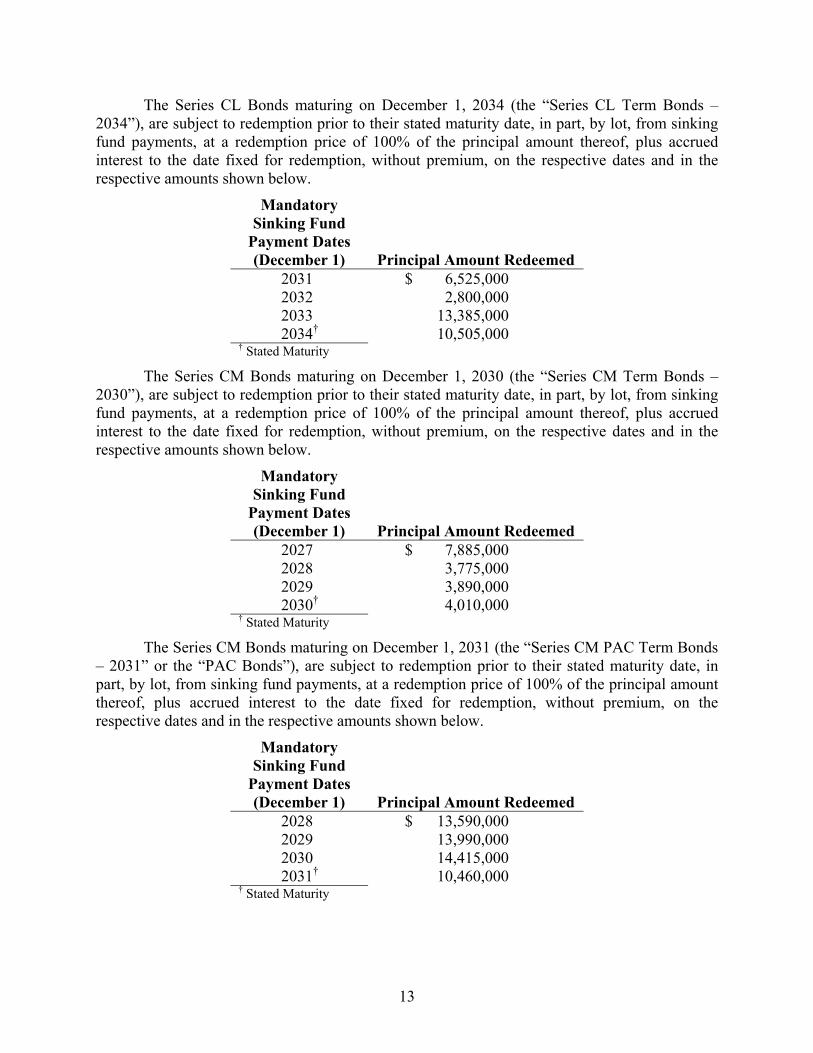

The Series CL Bonds maturing on December 1, 2034 (the “Series CL Term Bonds – 2034”), are subject to redemption prior to their stated maturity date, in part, by lot, from sinking fund payments, at a redemption price of 100% of the principal amount thereof, plus accrued interest to the date fixed for redemption, without premium, on the respective dates and in the respective amounts shown below.

Mandatory Sinking Fund

Payment Dates (December 1) Principal Amount Redeemed

2031 $ 6,525,000 2032 2,800,000 2033 13,385,000 2034† 10,505,000

† Stated Maturity

The Series CM Bonds maturing on December 1, 2030 (the “Series CM Term Bonds – 2030”), are subject to redemption prior to their stated maturity date, in part, by lot, from sinking fund payments, at a redemption price of 100% of the principal amount thereof, plus accrued interest to the date fixed for redemption, without premium, on the respective dates and in the respective amounts shown below.

Mandatory Sinking Fund

Payment Dates (December 1) Principal Amount Redeemed

2027 $ 7,885,000 2028 3,775,000 2029 3,890,000 2030† 4,010,000

† Stated Maturity

The Series CM Bonds maturing on December 1, 2031 (the “Series CM PAC Term Bonds – 2031” or the “PAC Bonds”), are subject to redemption prior to their stated maturity date, in part, by lot, from sinking fund payments, at a redemption price of 100% of the principal amount thereof, plus accrued interest to the date fixed for redemption, without premium, on the respective dates and in the respective amounts shown below.

Mandatory Sinking Fund

Payment Dates (December 1) Principal Amount Redeemed

2028 $ 13,590,000 2029 13,990,000 2030 14,415,000 2031† 10,460,000

† Stated Maturity

14

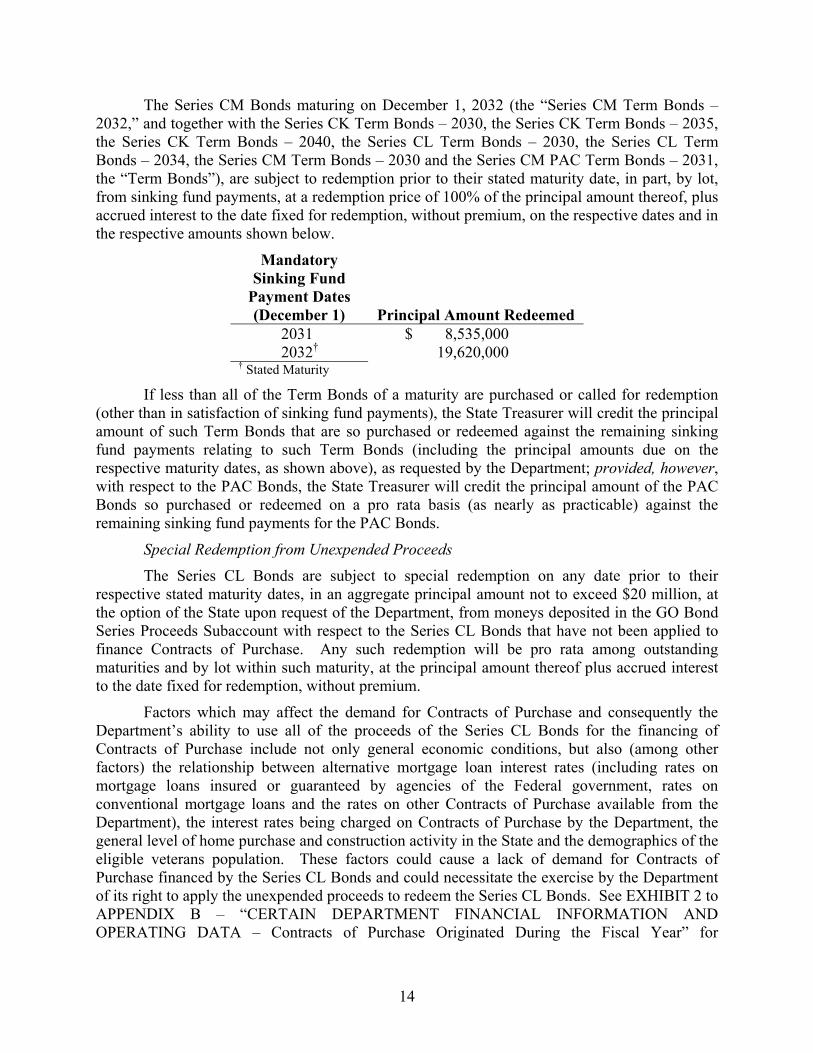

The Series CM Bonds maturing on December 1, 2032 (the “Series CM Term Bonds – 2032,” and together with the Series CK Term Bonds – 2030, the Series CK Term Bonds – 2035, the Series CK Term Bonds – 2040, the Series CL Term Bonds – 2030, the Series CL Term Bonds – 2034, the Series CM Term Bonds – 2030 and the Series CM PAC Term Bonds – 2031, the “Term Bonds”), are subject to redemption prior to their stated maturity date, in part, by lot, from sinking fund payments, at a redemption price of 100% of the principal amount thereof, plus accrued interest to the date fixed for redemption, without premium, on the respective dates and in the respective amounts shown below.

Mandatory Sinking Fund

Payment Dates (December 1) Principal Amount Redeemed

2031 $ 8,535,000 2032† 19,620,000

† Stated Maturity

If less than all of the Term Bonds of a maturity are purchased or called for redemption (other than in satisfaction of sinking fund payments), the State Treasurer will credit the principal amount of such Term Bonds that are so purchased or redeemed against the remaining sinking fund payments relating to such Term Bonds (including the principal amounts due on the respective maturity dates, as shown above), as requested by the Department; provided, however, with respect to the PAC Bonds, the State Treasurer will credit the principal amount of the PAC Bonds so purchased or redeemed on a pro rata basis (as nearly as practicable) against the remaining sinking fund payments for the PAC Bonds.

Special Redemption from Unexpended Proceeds

The Series CL Bonds are subject to special redemption on any date prior to their respective stated maturity dates, in an aggregate principal amount not to exceed $20 million, at the option of the State upon request of the Department, from moneys deposited in the GO Bond Series Proceeds Subaccount with respect to the Series CL Bonds that have not been applied to finance Contracts of Purchase. Any such redemption will be pro rata among outstanding maturities and by lot within such maturity, at the principal amount thereof plus accrued interest to the date fixed for redemption, without premium.

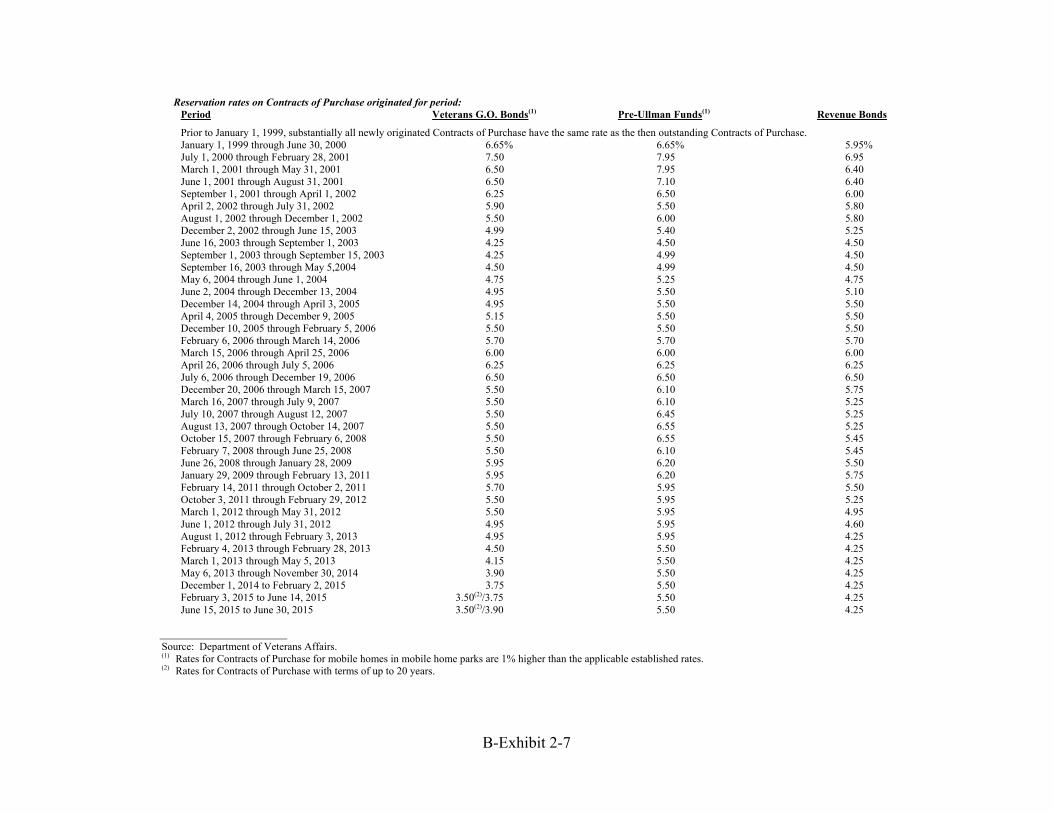

Factors which may affect the demand for Contracts of Purchase and consequently the Department’s ability to use all of the proceeds of the Series CL Bonds for the financing of Contracts of Purchase include not only general economic conditions, but also (among other factors) the relationship between alternative mortgage loan interest rates (including rates on mortgage loans insured or guaranteed by agencies of the Federal government, rates on conventional mortgage loans and the rates on other Contracts of Purchase available from the Department), the interest rates being charged on Contracts of Purchase by the Department, the general level of home purchase and construction activity in the State and the demographics of the eligible veterans population. These factors could cause a lack of demand for Contracts of Purchase financed by the Series CL Bonds and could necessitate the exercise by the Department of its right to apply the unexpended proceeds to redeem the Series CL Bonds. See EXHIBIT 2 to APPENDIX B – “CERTAIN DEPARTMENT FINANCIAL INFORMATION AND OPERATING DATA – Contracts of Purchase Originated During the Fiscal Year” for

15

information regarding the recent rate of originations of Contracts of Purchase, and “— Selected Principal Flows with respect to Contracts of Purchase Funded by both Veterans G.O. Bonds and Revenue Bonds” for the interest rates on Contracts of Purchase originated since January 1, 1990. For additional information, see APPENDIX B – “THE DEPARTMENT OF VETERANS AFFAIRS OF THE STATE OF CALIFORNIA, THE PROGRAM AND THE 1943 FUND – THE PROGRAM – Interest Rates.”

From time to time moneys may be or become available through the issuance of Veterans G.O. Bonds and Revenue Bonds and from other moneys available in the 1943 Fund to finance Contracts of Purchase. Since the Department has full discretion, subject to eligibility requirements and the requirements of the Federal Tax Code, in applying the proceeds of all of these bonds and other available moneys in the 1943 Fund to finance the Program, the proceeds of prior and future, if any, Veterans G.O. Bonds and Revenue Bonds and other available moneys in the 1943 Fund may be used to finance Contracts of Purchase before proceeds of the Series CL Bonds are so used. See APPENDIX B – “THE DEPARTMENT OF VETERANS AFFAIRS OF THE STATE OF CALIFORNIA, THE PROGRAM AND THE 1943 FUND – THE PROGRAM – Qualifying Veteran Status” for information regarding eligibility requirements for different moneys made available by the Department and EXHIBIT 2 to APPENDIX B – “CERTAIN DEPARTMENT FINANCIAL INFORMATION AND OPERATING DATA – Amounts Expected to be Available to Fund Contracts of Purchase and Related Investments” for information regarding the amount of money currently available and expected to become available to finance Contracts of Purchase upon the issuance of the Offered Veterans G.O. Bonds.

Special Redemption from Excess Revenues

The Offered Veterans G.O. Bonds are subject to special redemption on any date prior to their respective stated maturity dates, at the option of the State upon request of the Department, from Excess Revenues (as defined below) derived from any Veterans G.O. Bonds or any Revenue Bonds, except that, as described below under “—Special Mandatory Redemption of PAC Bonds,” certain Prepayments (as defined below) on the Offered Veterans G.O. Bonds Contracts of Purchase must be applied to redeem only the PAC Bonds, and the principal amount of the PAC Bonds redeemed from Prepayments and other Excess Revenues is limited; and, provided, however, that the Series CK Bonds maturing on December 1, 2029 and December 1, 2033 and the Series CL Bonds maturing on December 1, 2031 are not subject to special redemption from Excess Revenues prior to December 1, 2024 unless such special redemption prior to December 1, 2024 would be required to maintain the tax-exempt status of the Offered Veterans G.O. Bonds. Any such special redemption from Excess Revenues may be in whole or in part and of any maturity at the option of the State upon a request of the Department and by lot within such maturity, at the principal amount thereof plus accrued interest to the date fixed for redemption, without premium. “Prepayments” means all moneys received in connection with Contracts of Purchase other than interest and scheduled repayments of principal. Prepayments on Contracts of Purchase include, but are not limited to, principal prepayments, prepayment premiums or prepayment penalties, hazard insurance payments, payments in respect of partial or complete condemnation and recoveries on defaulted Contracts of Purchase.

“Excess Revenues” means, as of any date of calculation, the amount of all Revenues (as defined below) held in the revenue account established under the Revenue Bond Resolution in excess of Accrued Debt Service (as defined below). “Revenues” means all moneys received by

16

or on behalf of the Department representing (i) principal and interest payments on the Contracts of Purchase including all prepayments representing the same and all prepayment premiums or penalties received by or on behalf of the Department with respect to the Contracts of Purchase, (ii) interest earnings received on the investment of amounts to the extent deposited in the revenue account established under the Revenue Bond Resolution, (iii) amounts transferred to the revenue account from the bond reserve account or the loan loss account established under the Revenue Bond Resolution, and (iv) any other amounts payable by parties executing Contracts of Purchase or private participants in the Program or related to recoveries on defaulted Contracts of Purchase, including origination and commitment fees, servicing acquisition fees, liquidation proceeds, and insurance proceeds, except to the extent not included as “Revenues” pursuant to the provisions of any resolution authorizing the issuance of a series of Revenue Bonds. “Accrued Debt Service” means, as of any date of determination and, as the context requires, with respect to all Revenue Bonds and Veterans G.O. Bonds (including the Offered Veterans G.O. Bonds), the sum of: (i) the aggregate amount of scheduled interest and principal (except to the extent principal is otherwise to be redeemed pursuant to clause (ii) or (iii) below) to become due after such date but on or before the end of the current debt service year, less the product of (x) the number of whole months remaining in the current debt service year and (y) the Monthly Debt Service Requirement; (ii) the redemption price of bonds for which notice of redemption has been issued, provided such redemption price is to be paid from amounts on deposit in the revenue account created under the Revenue Bond Resolution; and (iii) the redemption price of bonds that the Department will be obligated to redeem prior to the end of the next succeeding debt service year under the terms of any resolution governing Revenue Bonds or Veterans G.O. Bonds, to the extent that such obligation arises on account of amounts on deposit in the revenue account created under the Revenue Bond Resolution. “Monthly Debt Service Requirement” means, as of any date of determination, one-twelfth of the aggregate amount of scheduled interest and principal to become due during the debt service year in which such date falls, as computed on the first day of such debt service year.

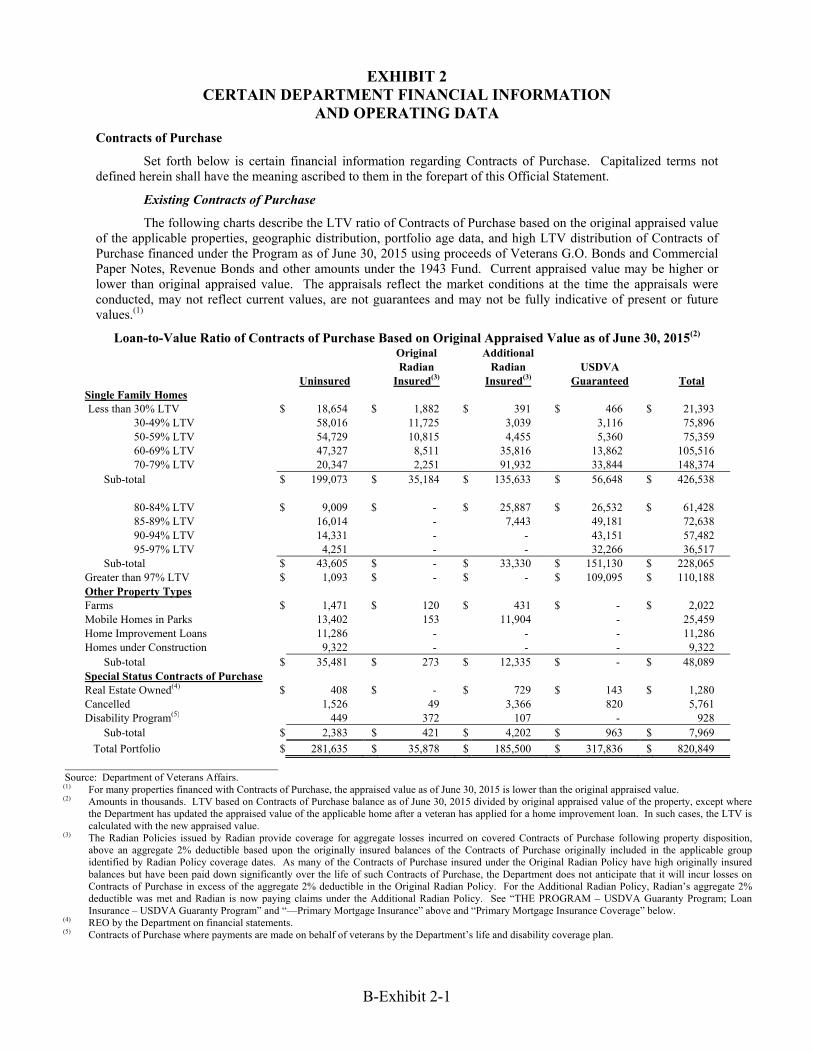

Excess Revenues can include Prepayments and repayments on Contracts of Purchase, investment earnings, and Revenues which had been set aside to be recycled into new Contracts of Purchase. All payments on Contracts of Purchase are deposited in the 1943 Fund and applied to pay debt service on the Veterans G.O. Bonds and Revenue Bonds (including mandatory redemptions of Veterans G.O. Bonds and Revenue Bonds), to finance Contracts of Purchase, to pay Program and Department expenses, and to pay certain insurance claims. The Department, subject to applicable bond authorizing resolutions, may apply Excess Revenues to redeem any Veterans G.O. Bonds or Revenue Bonds eligible for redemption. The Department’s decision to apply Excess Revenues to redeem bonds, to finance Contracts of Purchase, or for any other permitted purpose depends on many factors, including but not limited to applicable bond authorizing resolution requirements, demand for Contracts of Purchase, debt service cost savings, investment earnings, and Federal Tax Code requirements. See APPENDIX B – “THE DEPARTMENT OF VETERANS AFFAIRS OF THE STATE OF CALIFORNIA, THE PROGRAM AND THE 1943 FUND – THE 1943 FUND – Excess Revenues.” See also EXHIBIT 2 to APPENDIX B – “CERTAIN DEPARTMENT FINANCIAL INFORMATION AND OPERATING DATA – Existing Contracts of Purchase – Loan-to-Value Ratio of Contracts of Purchase Based on Original Appraised Value as of June 30, 2015” and “– Amounts Expected to be Available to Fund Contracts of Purchase and Related Investments.”

17

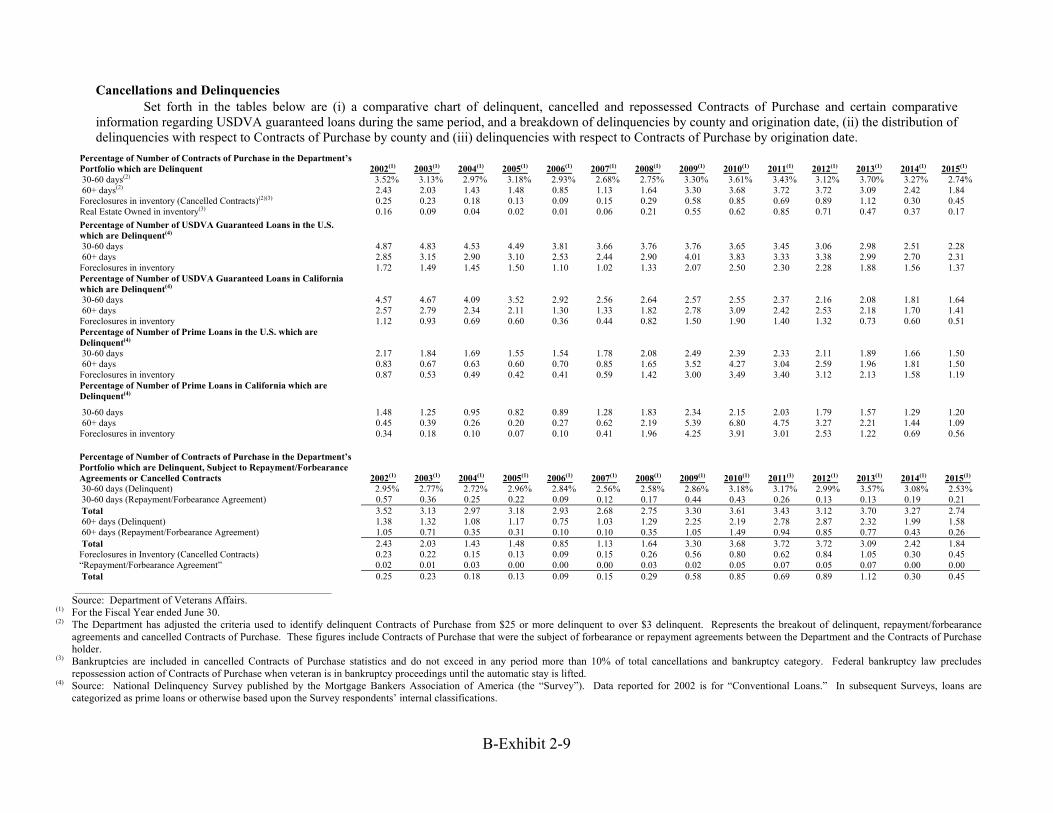

The Department’s actual past prepayment experience for existing Contracts of Purchase is set forth in EXHIBIT 2 to APPENDIX B – “CERTAIN DEPARTMENT FINANCIAL INFORMATION AND OPERATING DATA – Contracts of Purchase Origination and Principal Repayment Experience.”

For certain qualified mortgage bonds (which include Revenue Bonds, but exclude Veterans G.O. Bonds) issued or to be issued after 1988, the Federal Tax Code prohibits the use of repayments (including prepayments) of principal of Contracts of Purchase financed with the proceeds of an issue of such bonds to make additional Contracts of Purchase after 10 years from the date of issuance of such bonds (or the date of issuance of original bonds in the case of refundings), after which date such amounts must be used to redeem such bonds of the issue, except for a $250,000 de minimis amount. See “APPENDIX E – CERTAIN FEDERAL TAX CODE REQUIREMENTS – Other Requirements Imposed by the Federal Tax Code – Required Redemptions.”

The Federal Tax Code requires a payment to the United States from certain veterans whose Contracts of Purchase are originated after December 31, 1990 with the proceeds of qualified mortgage bonds. Since such requirement remains in effect with respect to any Contracts of Purchase originated after December 31, 1990 with proceeds of certain Revenue Bonds, for a period ending nine years after the execution of such Contracts of Purchase, the Department is unable to predict what effect, if any, such requirement will have on the origination or prepayment of Contracts of Purchase to which such provision applies.

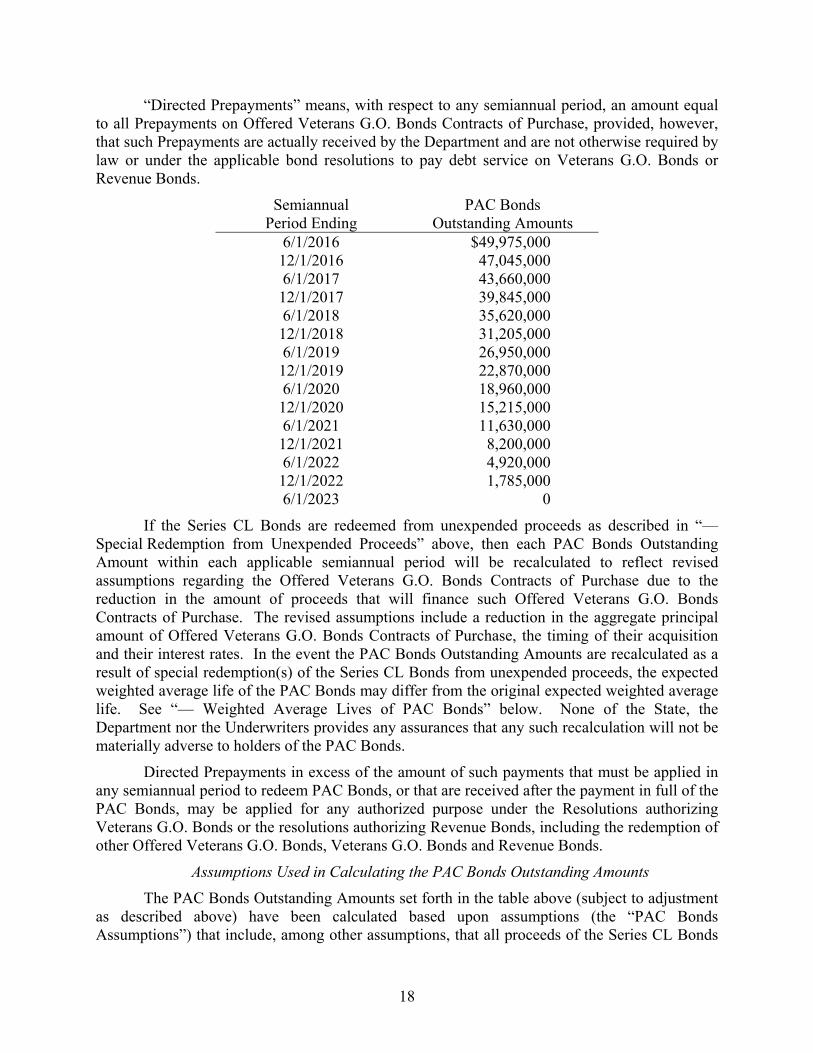

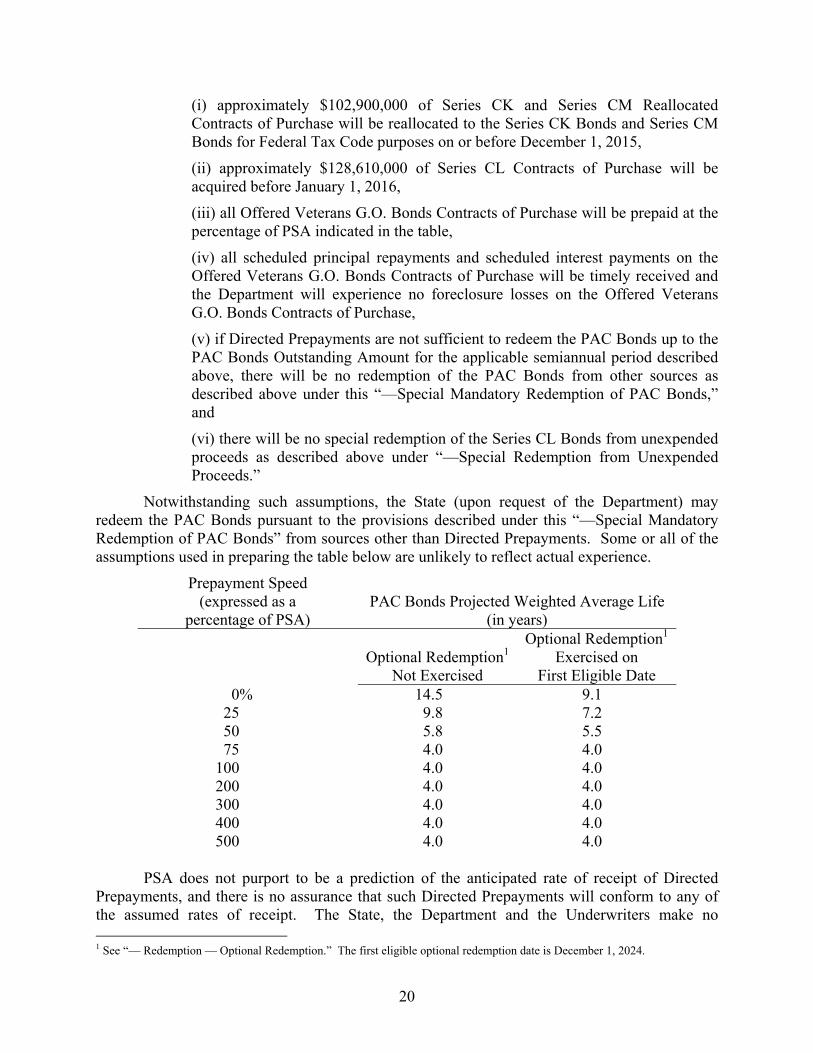

Special Mandatory Redemption of PAC Bonds

The PAC Bonds are subject to special mandatory redemption from Directed Prepayments (as defined below) at a redemption price of 100% of the principal amount thereof, plus accrued interest to the date fixed for redemption. Such mandatory redemptions may occur on any date but, to the extent that there are Directed Prepayments, must occur at least once during each semiannual period ending on a June 1 or December 1, commencing with the period ending June 1, 2016. Such redemptions may be made, at the option of the State as requested by the Department, from sources other than Directed Prepayments to the extent Directed Prepayments are not sufficient to satisfy the mandatory redemption. Any such redemption from Directed Prepayments or other sources must not result in the aggregate principal amount of the PAC Bonds outstanding following such redemption to be less than the related PAC Bonds Outstanding Amount for the related semiannual period as set forth in the table below. The PAC Bonds Outstanding Amounts set forth in the table below may be adjusted as described below due to a redemption of Series CL Bonds from unexpended proceeds as described under “—Special Redemption from Unexpended Proceeds” above (as so adjusted, the “Applicable Outstanding Amount”).

18

“Directed Prepayments” means, with respect to any semiannual period, an amount equal to all Prepayments on Offered Veterans G.O. Bonds Contracts of Purchase, provided, however, that such Prepayments are actually received by the Department and are not otherwise required by law or under the applicable bond resolutions to pay debt service on Veterans G.O. Bonds or Revenue Bonds.

Semiannual Period Ending

PAC Bonds Outstanding Amounts

6/1/2016 $49,975,000 12/1/2016 47,045,000 6/1/2017 43,660,000 12/1/2017 39,845,000 6/1/2018 35,620,000 12/1/2018 31,205,000 6/1/2019 26,950,000 12/1/2019 22,870,000 6/1/2020 18,960,000 12/1/2020 15,215,000 6/1/2021 11,630,000 12/1/2021 8,200,000 6/1/2022 4,920,000 12/1/2022 1,785,000 6/1/2023 0

If the Series CL Bonds are redeemed from unexpended proceeds as described in “—Special Redemption from Unexpended Proceeds” above, then each PAC Bonds Outstanding Amount within each applicable semiannual period will be recalculated to reflect revised assumptions regarding the Offered Veterans G.O. Bonds Contracts of Purchase due to the reduction in the amount of proceeds that will finance such Offered Veterans G.O. Bonds Contracts of Purchase. The revised assumptions include a reduction in the aggregate principal amount of Offered Veterans G.O. Bonds Contracts of Purchase, the timing of their acquisition and their interest rates. In the event the PAC Bonds Outstanding Amounts are recalculated as a result of special redemption(s) of the Series CL Bonds from unexpended proceeds, the expected weighted average life of the PAC Bonds may differ from the original expected weighted average life. See “— Weighted Average Lives of PAC Bonds” below. None of the State, the Department nor the Underwriters provides any assurances that any such recalculation will not be materially adverse to holders of the PAC Bonds.

Directed Prepayments in excess of the amount of such payments that must be applied in any semiannual period to redeem PAC Bonds, or that are received after the payment in full of the PAC Bonds, may be applied for any authorized purpose under the Resolutions authorizing Veterans G.O. Bonds or the resolutions authorizing Revenue Bonds, including the redemption of other Offered Veterans G.O. Bonds, Veterans G.O. Bonds and Revenue Bonds.

Assumptions Used in Calculating the PAC Bonds Outstanding Amounts

The PAC Bonds Outstanding Amounts set forth in the table above (subject to adjustment as described above) have been calculated based upon assumptions (the “PAC Bonds Assumptions”) that include, among other assumptions, that all proceeds of the Series CL Bonds

19

available to purchase Contracts of Purchase are utilized for such purchases (as described further below), and that the Directed Prepayments are received at a rate equal to 75% of Securities Industry and Financial Markets Association (“SIFMA”) (formerly the Public Securities Association) standard prepayment model for 30-year mortgage loans (“PSA”), as further described below. Since Prepayments on Contracts of Purchase cannot be predicted, the actual principal amount of and characteristics of the Offered Veterans G.O. Bonds Contracts of Purchase may differ from such assumptions.

The PAC Bonds Assumptions, including those regarding the expected rate of receipt of Directed Prepayments, may differ from the assumptions contained in the Cash Flow Statement (as described in APPENDIX B) required under the Revenue Bond Resolution to be delivered in connection with the issuance of the Offered Veterans G.O. Bonds. The State, the Department and the Underwriters make no representation that actual experience will conform to the PAC Bonds Assumptions. Age and interest rates of Contracts of Purchase are factors that can affect the speeds at which Contracts of Purchase are prepaid.

PSA Model

Prepayments on mortgage loans, including obligations such as the Contracts of Purchase, are commonly measured relative to a prepayment standard or model. The model represents an assumed monthly rate of prepayment of the then-outstanding principal balance of a pool of new 30-year mortgage loans, and does not purport to be either a historical description of the prepayment experience of any pool of mortgage loans or a prediction of the anticipated rate of prepayment of any pool of mortgage loans, including the Offered Veterans G.O. Bonds Contracts of Purchase.

One hundred percent PSA assumes prepayment rates of 0.2 percent per year of the then-unpaid principal balance of such pool of mortgage loans in the first month of the life of such mortgage loans and an additional 0.2 percent per year in each month thereafter (for example, 0.4 percent per year in the second month) until the 30th month. Beginning in the 30th month and in each month thereafter during the life of the mortgage loans in such pool, 100 percent PSA assumes a constant prepayment rate of the mortgage loans in such pool of six percent per year. Multiples will be calculated from this prepayment rate sequence; e.g., 200 percent PSA assumes prepayment rates will be 0.4 percent per year in month one, 0.8 percent per year in month two, reaching 12 percent per year in the 30th month and remaining constant at 12 percent per year thereafter.

Weighted Average Lives of PAC Bonds

The weighted average life of a bond refers to the average of the length of time that will elapse from the date of issuance of such bond to the date each installment of principal is paid, weighted by the amount of such installment. The weighted average life of the PAC Bonds will be influenced by, among other factors, the rate at which Prepayments on Offered Veterans G.O. Bonds Contracts of Purchase are received.

Set forth in the following table are the projected weighted average lives (in years) of the PAC Bonds based upon various rates of receipt of Directed Prepayments expressed as percentages of PSA. The State and the Department have made no projections as to the weighted average lives of the PAC Bonds at rates of receipt of Directed Prepayments exceeding 500% of PSA. The table below assumes for each rate of receipt of Directed Prepayments that, inter alia:

20