Embed Size (px)

Citation preview

New IRS Regulations on Repair vs. Capitalization

Presenters: Philip A. MannJeffrey D. Hiatt

May 2012

Who we are

We are a large independent provider of Cost Segregation and Energy Studies to small, local and regional CPA firms across the US – over 300 CPAs TRUST us to handle their client’s needs

We have prepared over 7,500 Studies since 1996

Our studies include preparation and signing of Form 3115 (almost 3,000 prepared)

www.costsegs.com

Philip A. Mann6400 Sheridan DriveSuite 230Williamsville, NY 14221

Phone: 716-633-9840Toll-Free: 877-633-9840

Fax: 716-633-9469Cell: 716-308-4868

email: [email protected]

Philip A. Mann, CPA Managing Director of MS Consultants,

LLC

Former Audit Partner in a regional firm

Started doing cost segregation studies 17 years ago

Began energy consulting in 2005

© MS Consultants, LLC 2010

Jeffrey D. Hiatt

Heads up the New England office

87 Lafayette Rd. Suite 11

Hampton Falls, NH 03844

Toll Free: 888.989.0054Phone: 508.878.4846Fax: 603.926.2811

Email: [email protected]

Repair vs. Capitalization

Let’s go back to the old rules.

In Summary

Improvements must be capitalized, while repairs must be deducted. After that it gets complicated

“Some items are clearly capital and other items are clearly expense, but between the two extremes a point is approached at which it is difficult

to determine whether the expenditure is capital or expense”

‐ Libby & Blouin, LTD., 4 BTA 910 (1926)

The Old rules‐con’t

The Old rules‐con’t

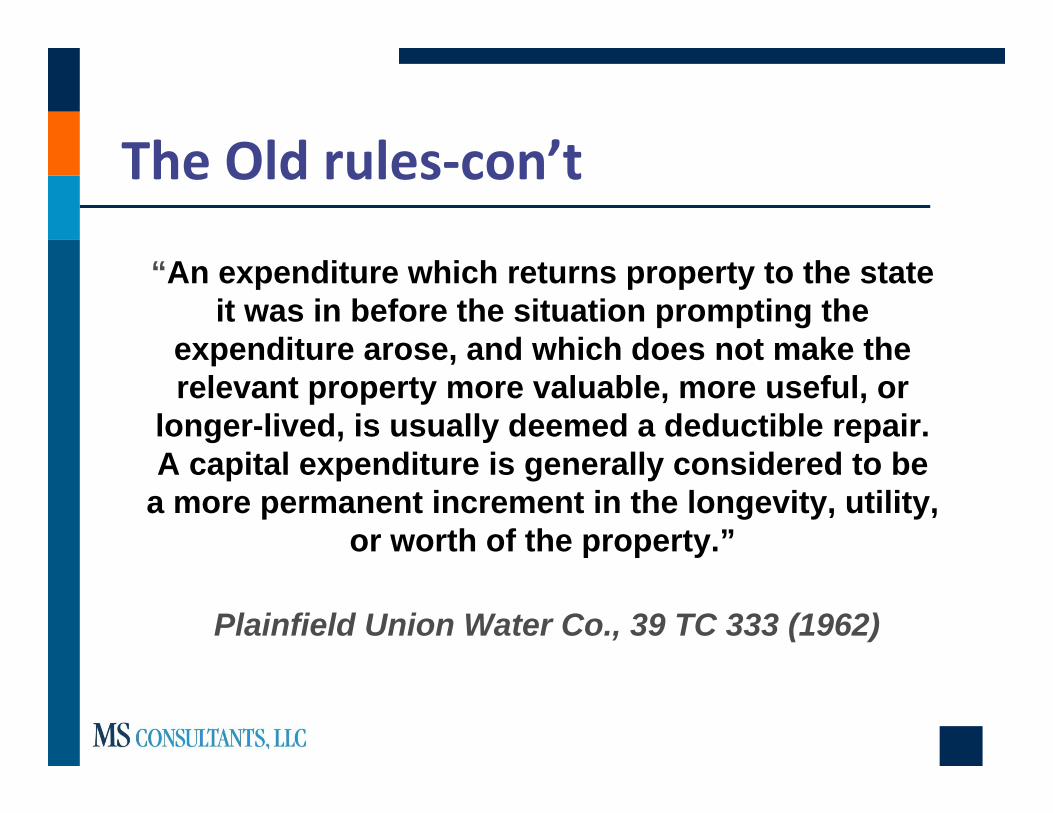

“An expenditure which returns property to the state it was in before the situation prompting the

expenditure arose, and which does not make the relevant property more valuable, more useful, or

longer-lived, is usually deemed a deductible repair. A capital expenditure is generally considered to be

a more permanent increment in the longevity, utility, or worth of the property.”

Plainfield Union Water Co., 39 TC 333 (1962)

The Old Rules, con’t

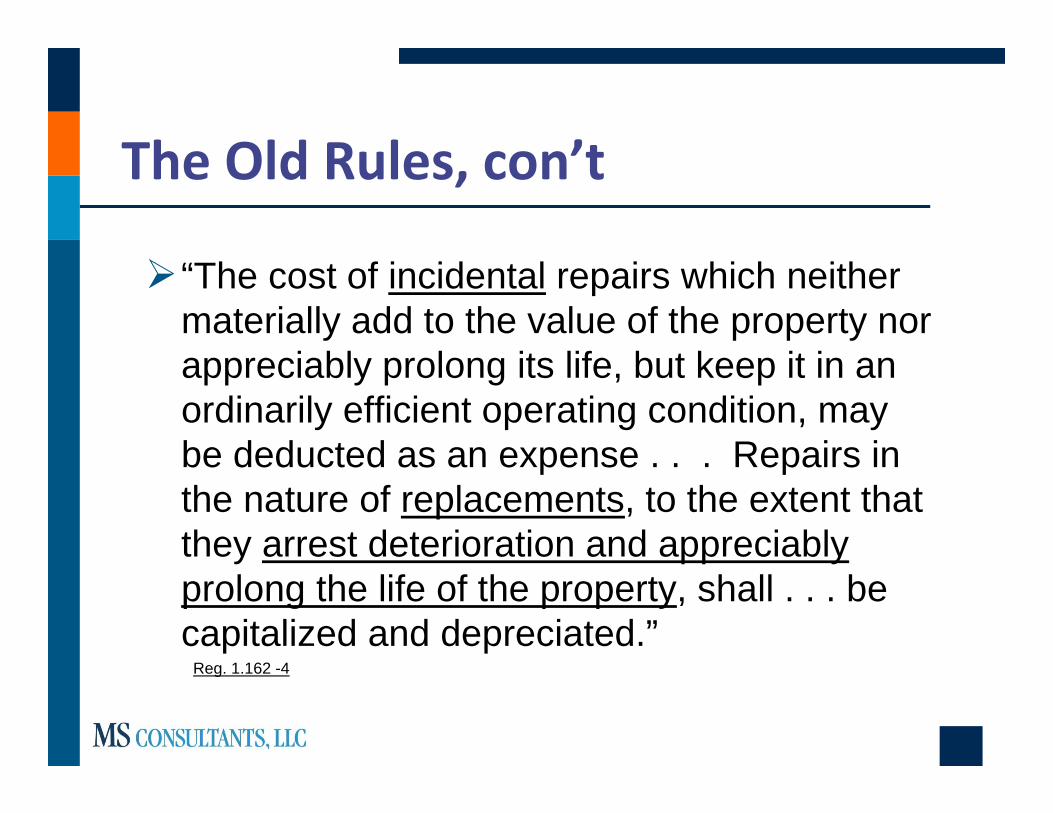

“The cost of incidental repairs which neither materially add to the value of the property nor appreciably prolong its life, but keep it in an ordinarily efficient operating condition, may be deducted as an expense . . . Repairs in the nature of replacements, to the extent that they arrest deterioration and appreciably prolong the life of the property, shall . . . be capitalized and depreciated.”

Reg. 1.162 -4

The Old Rules, con’t

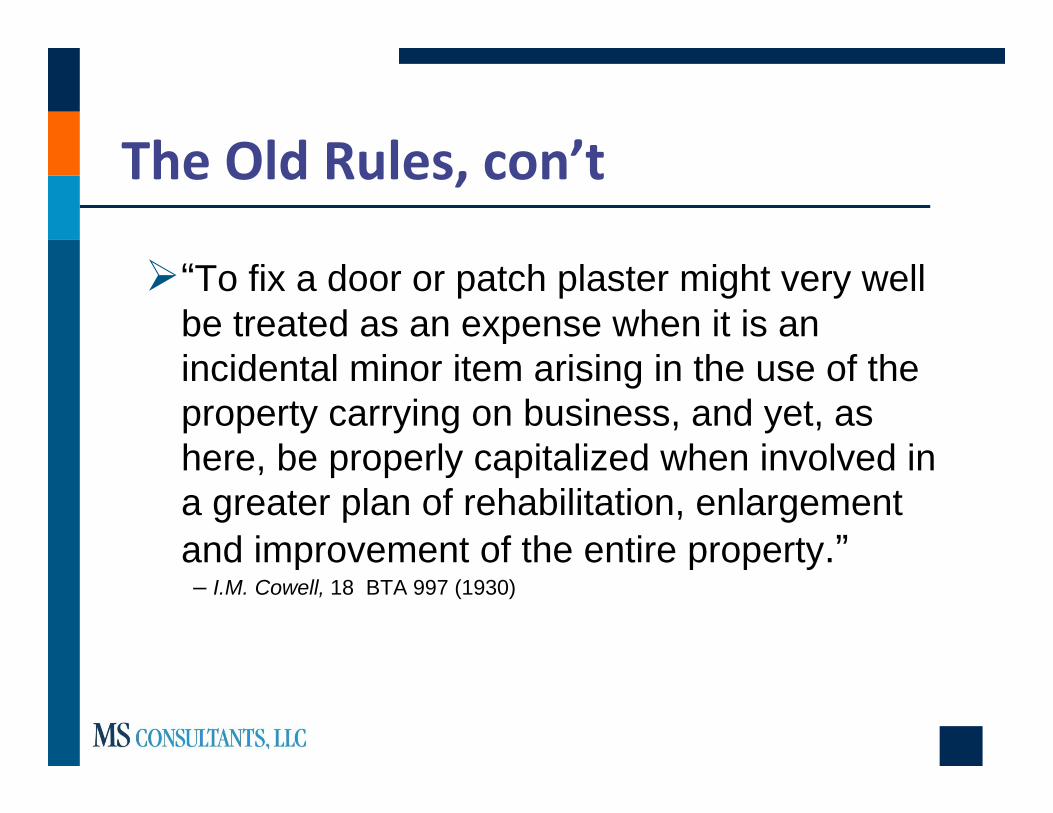

“To fix a door or patch plaster might very well be treated as an expense when it is an incidental minor item arising in the use of the property carrying on business, and yet, as here, be properly capitalized when involved in a greater plan of rehabilitation, enlargement and improvement of the entire property.” – I.M. Cowell, 18 BTA 997 (1930)

The Old Rules‐What is Capitalized?

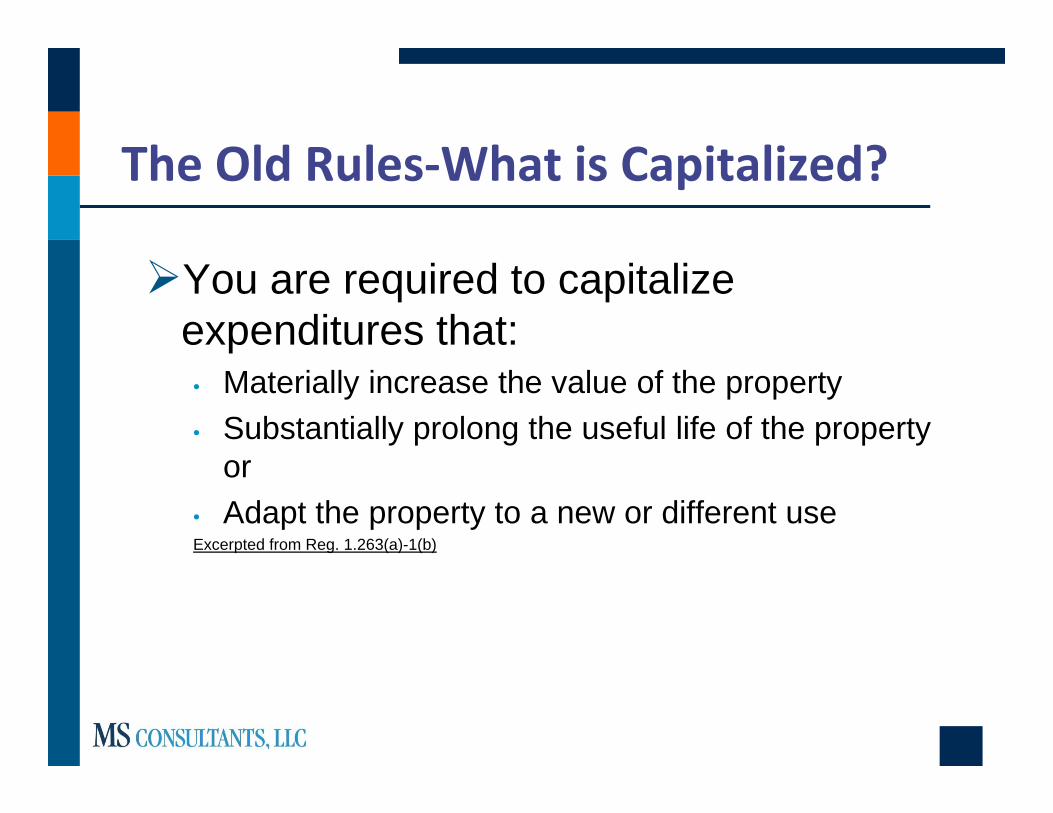

You are required to capitalize expenditures that:

• Materially increase the value of the property • Substantially prolong the useful life of the property

or • Adapt the property to a new or different useExcerpted from Reg. 1.263(a)-1(b)

And remember you cannot write off the structural component being replaced (If you own the building)

You cannot write off the structural component being replaced (If you own the building)“Congress did not intend a retirement of a structural component of the building to be a disposition requiring recognition of gain or loss. Thus, if the roof wears out . . cost recovery continues over the remaining recovery period. If the roof is replaced, the unadjusted basis of the new roof is recovered over a new recovery period beginning in the month it is placed in service."

Joint Committee on Taxation Staff, General Explanation of the Economic Recovery Act of 1981

Tenant lease abandonments

IRS Sec. 168(i)(8)(B) If an improvement which is made by the landlord for a

lessee is disposed of or removed by the landlord at the end of a lease, the remaining tax basis of those assets disposed of shall be treated as an abandonment for tax purposes.

This 1996 law change was to provide landlords with similar results as tenants who abandon improvements when leases are abandoned

Tenant lease abandonmentsExample New tenant takes over existing space, and will pay for

their own buildout. As part of the buildout, they demo 100% of the existing

ceiling tiles, lighting, and some of the drywall and office doors.

Cost of the above 39 year structural items is $80,000, and were placed in service (by purchasing the building) 5 years ago.

LANDLORD’S TAX SAVINGS = remaining basis $70,000 x 40% tax rate = $28,000!

Then Came the Recent CasesJ.L. Smith

Taxpayer expenses new cells for aluminum smelting operations. Cells are part of 800 cell system

IRS wins- each cell is unit of property

Recent Court Cases, con’tIngram Industries

Taxpayer expenses new engines and overhauls for tugboats

Taxpayer wins-Tugboat is unit of property

Recent Court Cases, con’tFEDERAL EXPRESS CORP., DC-TN, 2003-2 USTC “When, as in the case at bar, a repair is made to a

discrete component part of a larger item of property, the court must determine whether to apply the Repair Regulations to the component part or to the larger item of property. Otherwise stated, the court must identify which “unit of property” is being “repaired” and whether the repair materially adds to the value or appreciably prolongs the life of that unit of property.”

Taxpayer wins-Plane is unit of property

Recent Court Cases, con’tFEDERAL EXPRESS CORP., DC-TN, 2003-2 USTC, Con’t Four Factor Test to Determine the Proper Unit of Property

1) As a matter of taxpayer or industry practice, is the component (smaller unit) treated or purchased separately from the building (larger unit)?

2) Is the individual component and the building co-extensive? “If an engine is not “regularly and periodically” replaced over the life of the aircraft, then the useful life of the engine is coextensive with the life of the property that it powers.”

3) Can the smaller unit and larger unit function without each other? i.e., Functional Interdependence is important

4) Must the smaller unit be removed from the larger unit for maintenance to occur?

What has happened since Fed Ex?

In 2004, The IRS requested comments:“The Service and the Treasury Department want to

provide clear, consistent and administrative rules that will reduce the uncertainty and controversy in this area . . .”

In 2006 the Treasury issued their first set of proposed regulations. These were withdrawn in 2008 and replaced with a new set of proposed regs. Under the 2008 Prop. Reg. 1.263(a)-3(d)(2)(ii) - Buildings and their structural components as defined under Sec. 1.48-1(e) are a single unit of property.

What has happened since Fed Ex?

Many taxpayers began filing Form 3115 “Change in Accounting Method” before the proposed regulations become final. Due to the large amount of Form 3115s being filed, the IRS formed a task committee to best determine how to handle this issue.

And on August 27th, the IRS decided to help taxpayers

What has happened since Fed Ex?

Rev. Proc. 2009-39• Automatic Approval• Due with Tax Return• No Filing Fee• For tax years ending on or after December

31, 2008

Repair vs. Capitalization Under the Old Rules

Write off the remaining tax basis of items that were capitalized that should have been expensed as a repair instead (with Form 3115 automatic approval):

Roofs Garage Doors Parking Lots HVAC Outside Painting/Powerwashing Hot Water Heaters

New IRS Regulations on Repair vs. Capitalization

On December 23, 2011, the IRS issued the long-awaited Repair vs. Capitalization regulations that will have significant impacts on a wide range of industries. These new rules, effective for the tax years beginning in 2012, are far-reaching and will probably affect all of your taxpayers who own businesses or real estate.

New IRS Regulations on Repair vs. Capitalization

New regs are 250 pages

The New Regulations

Changes to IRS Code Sec 162(a) and 263(a)

effective for tax years beginning in 2012 –taxpayers must comply.

To comply with the new rules – in many circumstances will need to file Form 3115 “Change in Accounting Method”

Provisions in the New Regulations

1. New Capitalization Standards2. Unit of Property (UOP) has Changed3. 9 Structural Components of the Building4. Write off of Structural Components5. Remodeling Expenditures (Plan of Rehabilitation Doctrine)6. Creation of “routine maintenance safe labor for non-

building assets”7. New rules on “Materials & Supplies” (M&S)8. “Official” de minimis rule9. Facilitation Expenses must be capitalized10. Repairs/Improvements to non-building assets11. Other changes to the rules

New capitalization standards‐(1)

BETTERMENT of the Unit of Property

RESTORATION of the Unit of Property

ADAPTS the Unit of Property to a new or different use.

New capitalization standards‐(1)‐con’t

Old rules verse the new rules OLD

• Materially increase the value of the property • Substantially prolong the useful life of the property or • Adapt the property to a new or different use

New Betterment Restoration Adapt the property to new or different use

New capitalization standards(1)‐con’t

BETTERMENT of the Unit of PropertyAmeliorate a material condition or defect at

the time of acquisition or production – not having previous knowledge of the defect is not an excuseResult in a material additionMaterially increases the quality, capacity,

efficiency or strength of the UOP

New capitalization standards(1)‐con’t

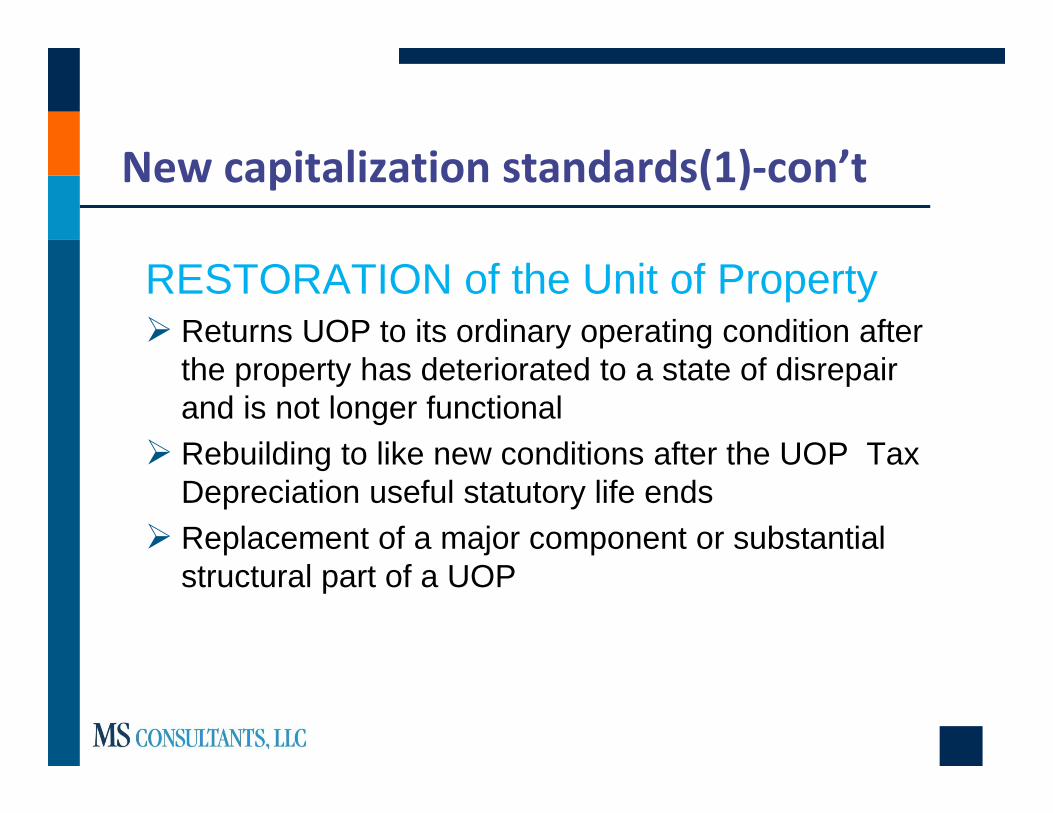

RESTORATION of the Unit of Property Returns UOP to its ordinary operating condition after

the property has deteriorated to a state of disrepair and is not longer functional

Rebuilding to like new conditions after the UOP Tax Depreciation useful statutory life ends

Replacement of a major component or substantial structural part of a UOP

New capitalization standards‐(1)‐con’t

Adapts the property to a new or different use Same as the old rules Change an office to a retail store

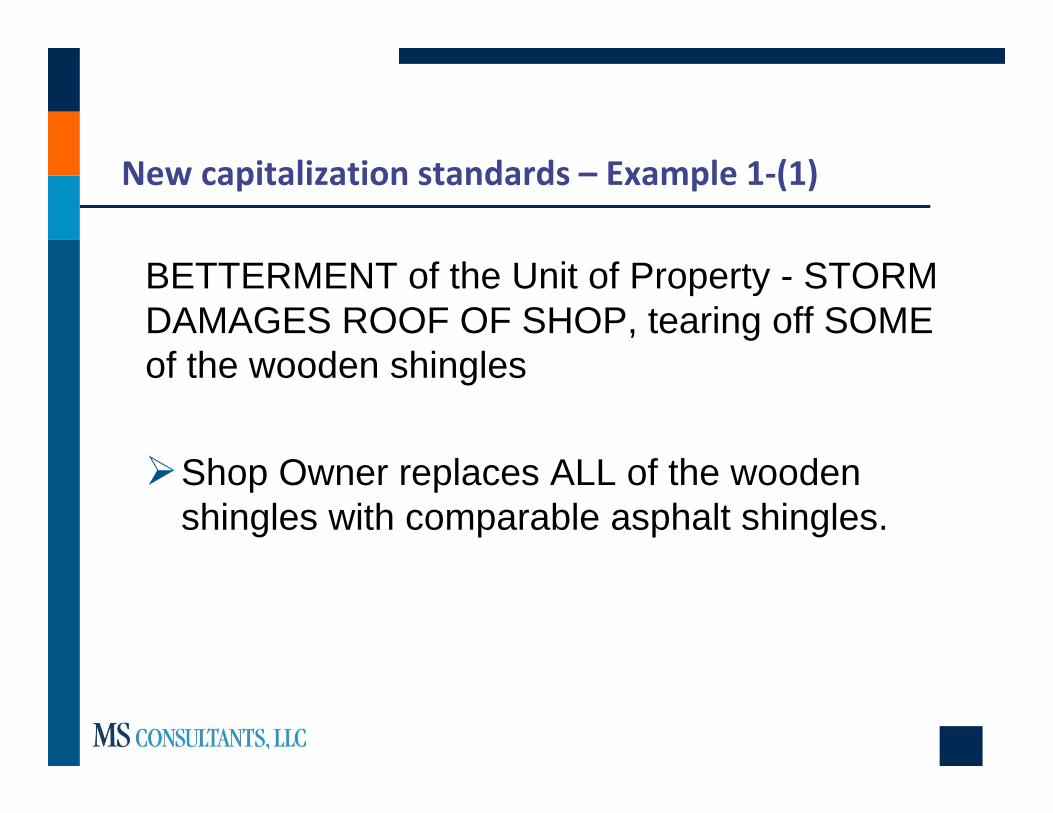

New capitalization standards – Example 1‐(1)

BETTERMENT of the Unit of Property - STORM DAMAGES ROOF OF SHOP, tearing off SOME of the wooden shingles

Shop Owner replaces ALL of the wooden shingles with comparable asphalt shingles.

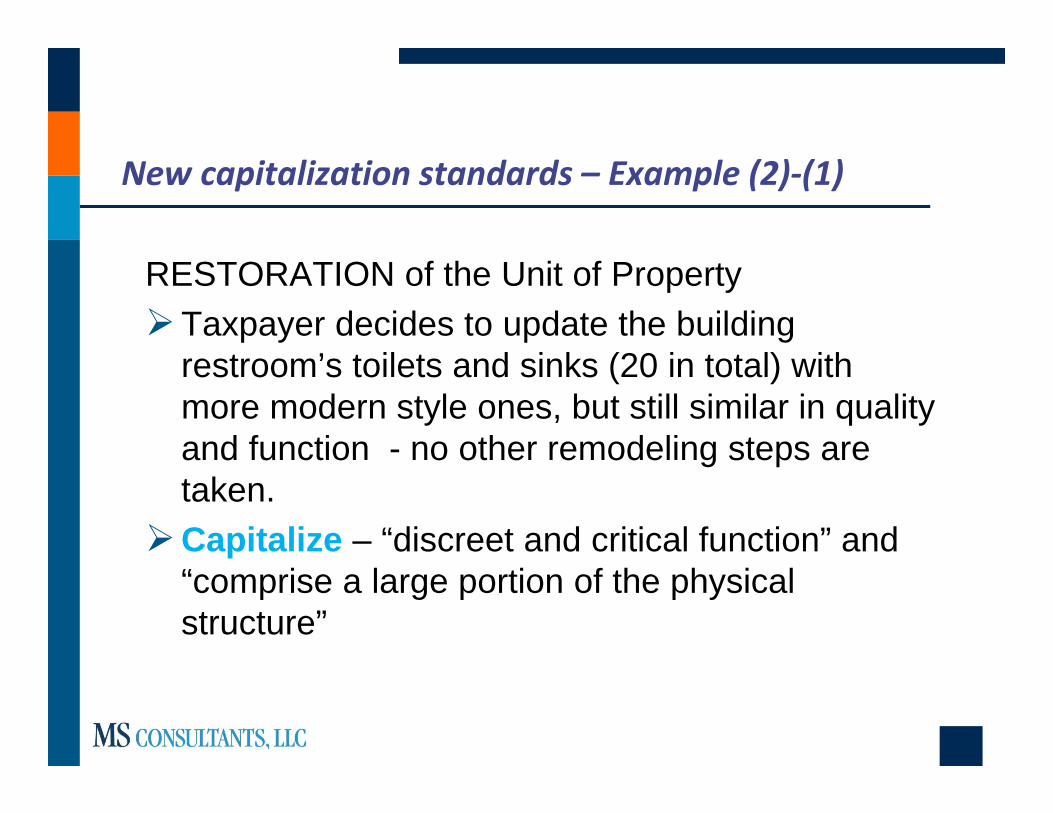

New capitalization standards – Example (2)‐(1)

RESTORATION of the Unit of PropertyTaxpayer decides to update the building

restroom’s toilets and sinks (20 in total) with more modern style ones, but still similar in quality and function - no other remodeling steps are taken.

Capitalize – “discreet and critical function” and “comprise a large portion of the physical structure”

New capitalization standards –(1)‐cont

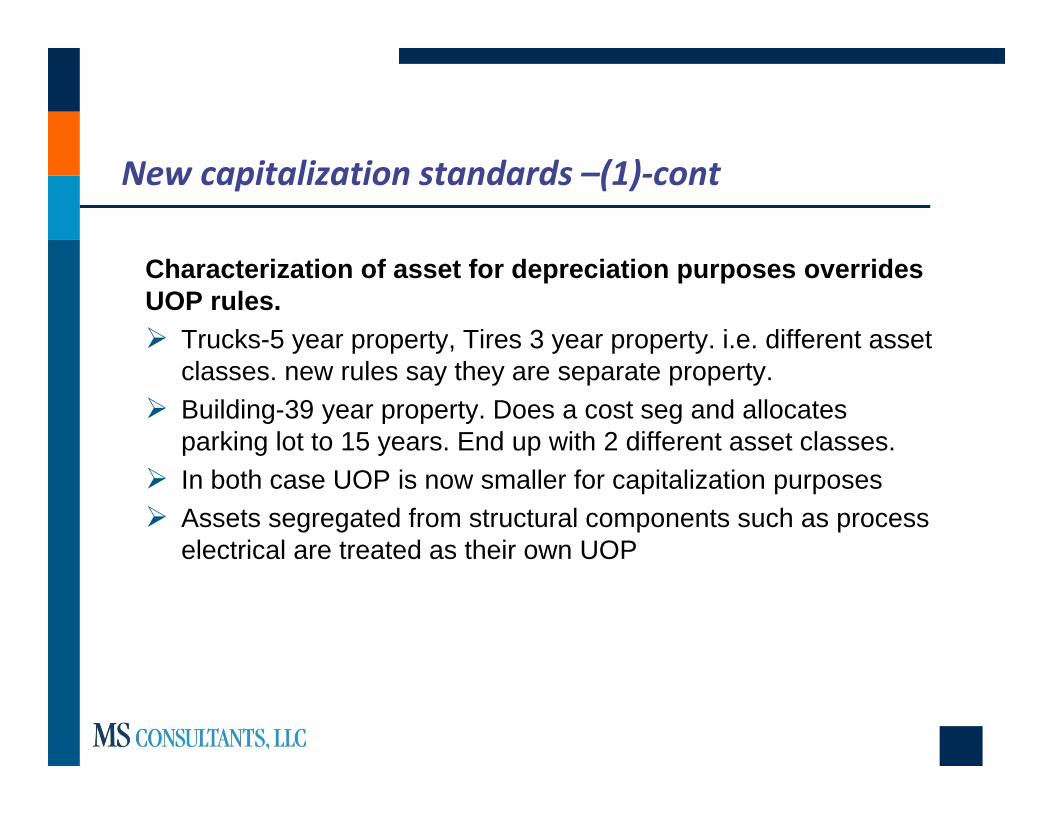

Characterization of asset for depreciation purposes overrides UOP rules. Trucks-5 year property, Tires 3 year property. i.e. different asset

classes. new rules say they are separate property. Building-39 year property. Does a cost seg and allocates

parking lot to 15 years. End up with 2 different asset classes. In both case UOP is now smaller for capitalization purposes Assets segregated from structural components such as process

electrical are treated as their own UOP

The Unit of Property has changed‐(2)

Unit of Property (UOP) test for Real Estate will now be applied to 9 individual Structural Components of the property, not the building as a whole – the UOP we measure against just became smaller!

The Unit of Property has changed‐(2)‐con’t

UOP for assets other than buildings. In general, for real or personal property that isn't classified as a building by the temp regs. all the components that are functionally interdependent comprise a single UOP. Components of property are functionally interdependent if the placing in service of one component by the taxpayer is dependent on the placing in service of the other component by the taxpayer.

The Unit of Property has changed‐(2)‐con’t

UOP for buildings. In general, each building and its structural components are one UOP — “the building.” And amounts are treated as paid for an improvement to a building if they improve: (1) the building structure; or (2) any designated building system.

The Unit of Property has changed‐(2)‐con’t

What is a building structure? A building structure consists of a building and its structural components as defined at Reg. § 1.48-1(e).

Thus, if a business taxpayer restores a building structure, for example, it replaces the entire roof, the expense is treated as an improvement to the single UOP consisting of the building. Similarly, if the taxpayer makes a betterment to a building system, such as an improvement to the heating, ventilation, and air conditioning (HVAC) system, then the expense also constitutes an improvement to the building UOP. (T.D. 9564)

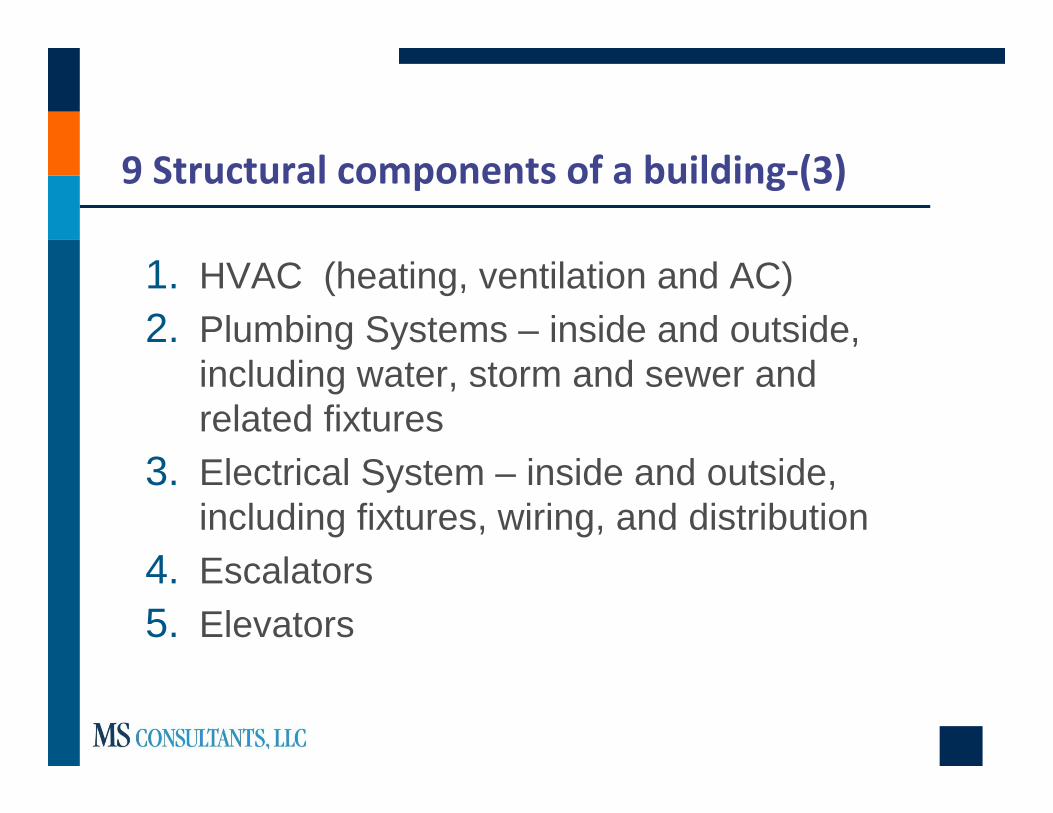

What is a building system? This new term consists of the following nine structural components. Each of them (including their sub-components) is a building system that is separate from the building structure, and to which the improvement rules must be separately applied:

9 Structural components of a building‐(3)

1. HVAC (heating, ventilation and AC)2. Plumbing Systems – inside and outside,

including water, storm and sewer and related fixtures

3. Electrical System – inside and outside, including fixtures, wiring, and distribution

4. Escalators5. Elevators

9 Structural components of a building–(3)‐con’t

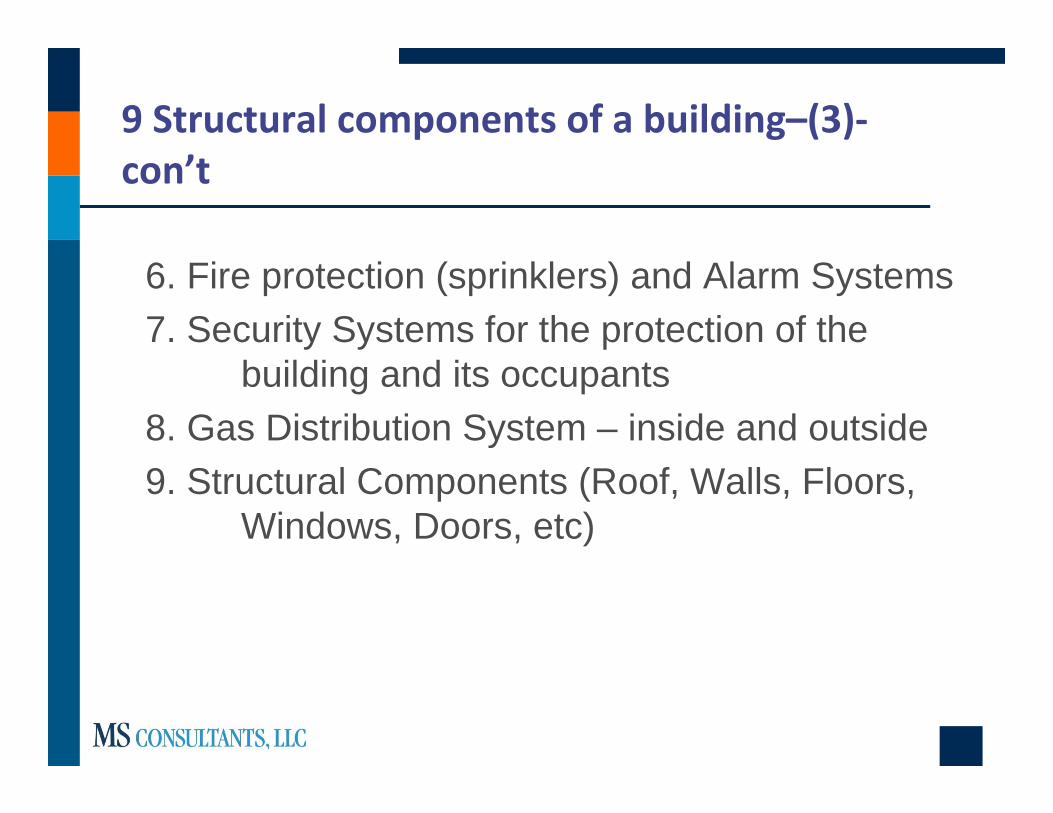

6. Fire protection (sprinklers) and Alarm Systems7. Security Systems for the protection of the

building and its occupants8. Gas Distribution System – inside and outside9. Structural Components (Roof, Walls, Floors,

Windows, Doors, etc)

9 Structural components of a building‐(3)‐con’t

Same rules apply to tenants, even though they do not own the building

Write off of Structural Components‐(4)

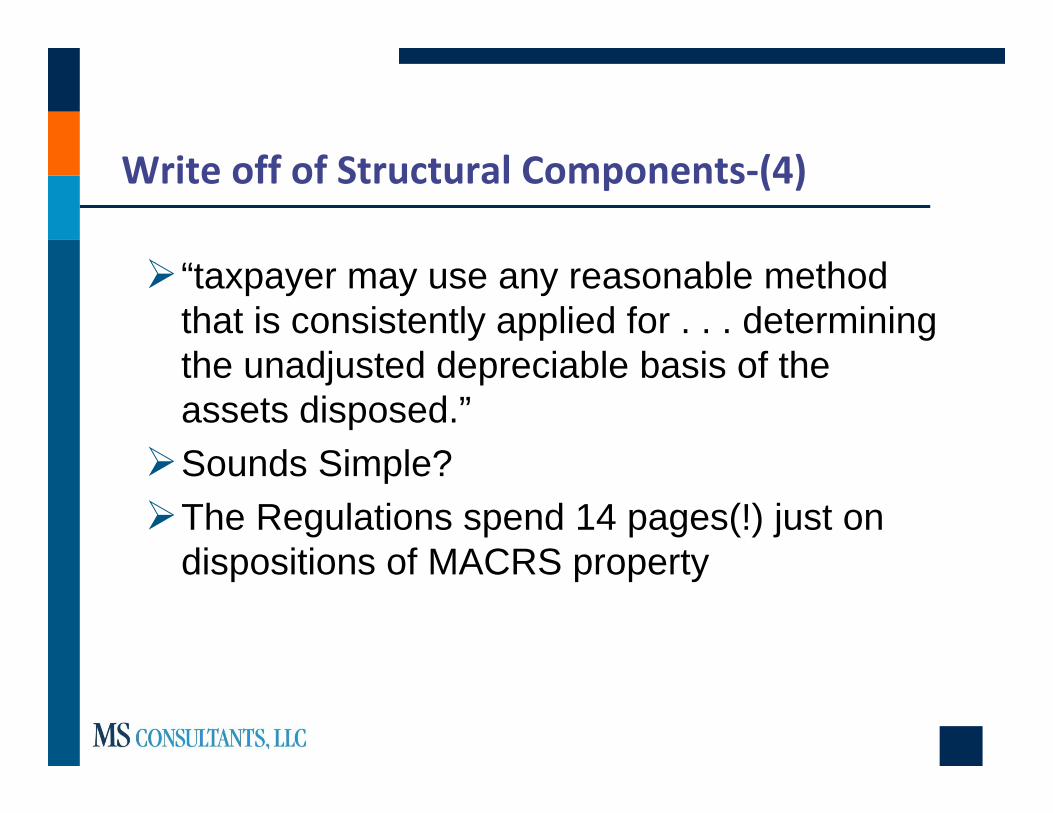

“taxpayer may use any reasonable method that is consistently applied for . . . determining the unadjusted depreciable basis of the assets disposed.”Sounds Simple?The Regulations spend 14 pages(!) just on

dispositions of MACRS property

Write off of Structural Components‐(4)‐con’t

Identify the item being replaced – without construction records or a cost seg study to support your position?

Regs specifically state that the asset disposed of cannot be larger than the UOP – for example, how much of the original “roof” was replaced? Can you identify the original HVAC units that were replaced?

IRS does state that you are not required to write off the old asset.

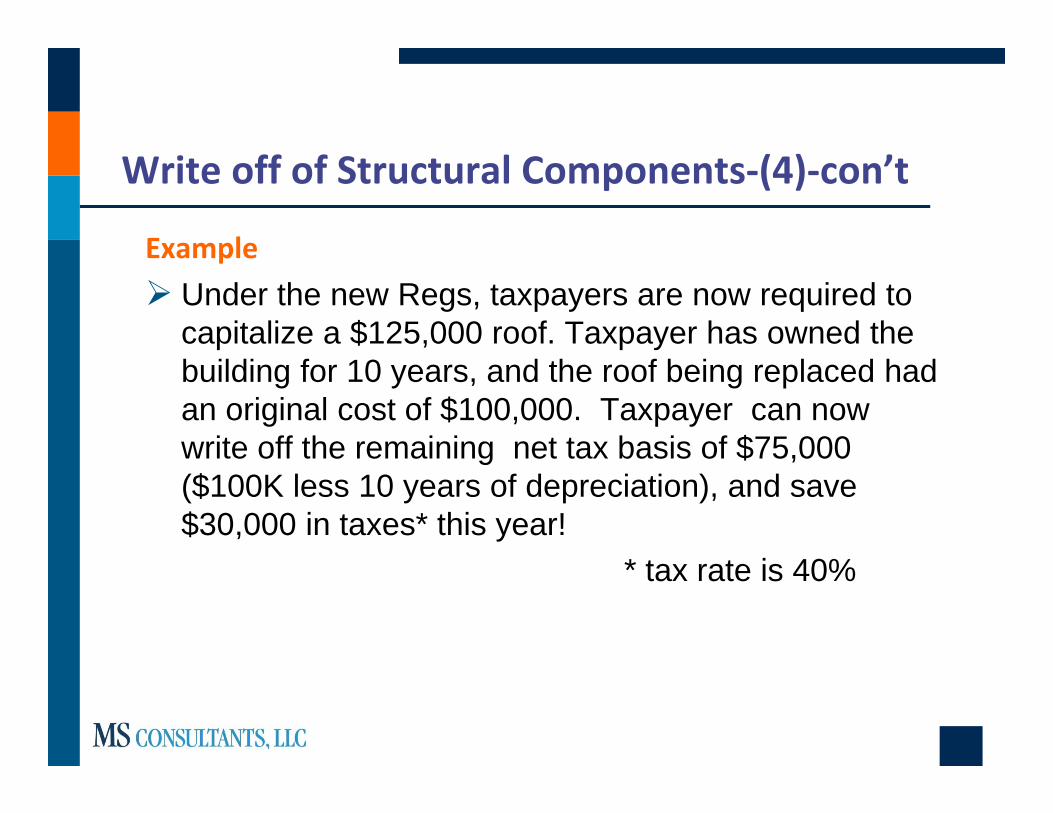

Write off of Structural Components‐(4)‐con’t

Example Under the new Regs, taxpayers are now required to

capitalize a $125,000 roof. Taxpayer has owned the building for 10 years, and the roof being replaced had an original cost of $100,000. Taxpayer can now write off the remaining net tax basis of $75,000 ($100K less 10 years of depreciation), and save $30,000 in taxes* this year!

* tax rate is 40%

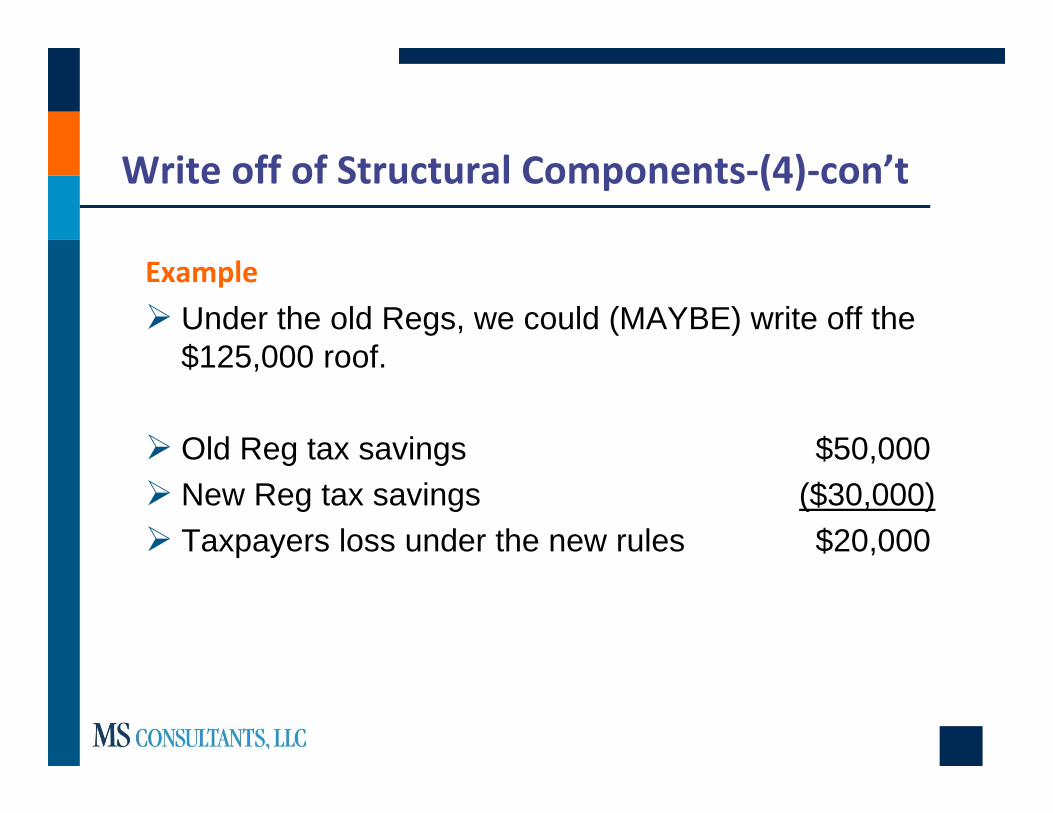

Write off of Structural Components‐(4)‐con’t

Example Under the old Regs, we could (MAYBE) write off the

$125,000 roof.

Old Reg tax savings $50,000 New Reg tax savings ($30,000) Taxpayers loss under the new rules $20,000

Remodeling Expenditures – (5)

Goodbye Plan of Rehabilitation Doctrine

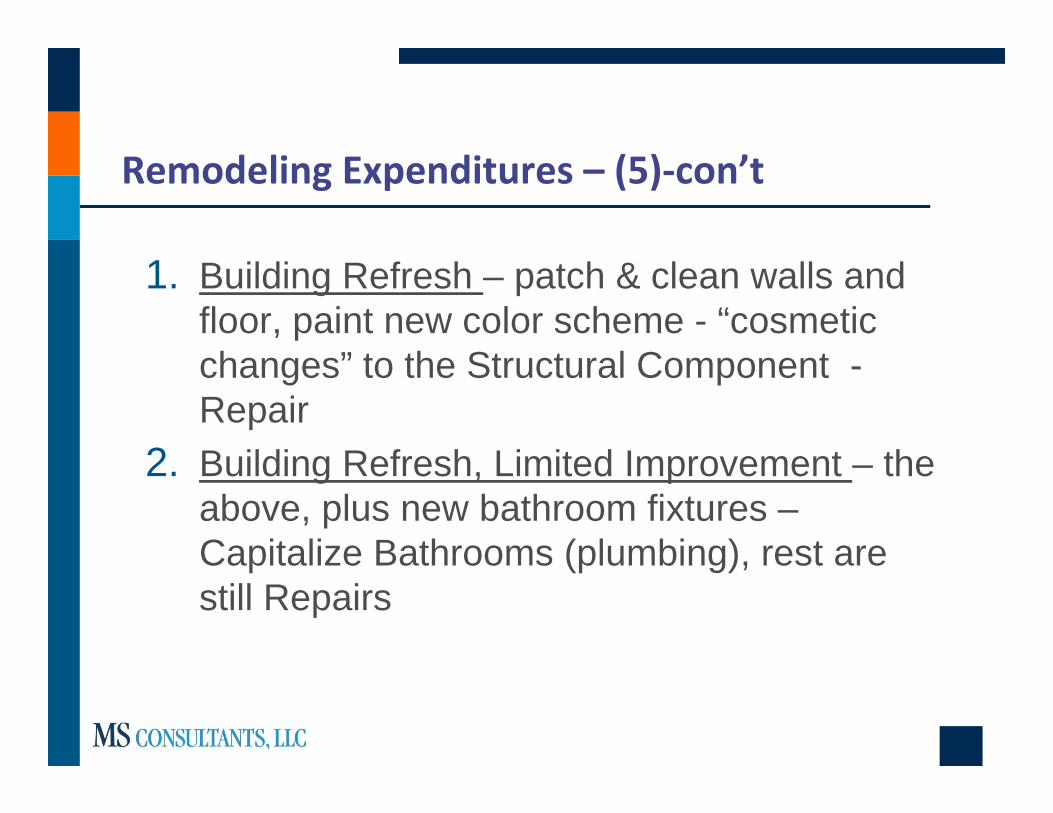

Remodeling Expenditures – (5)‐con’t

1. Building Refresh – patch & clean walls and floor, paint new color scheme - “cosmetic changes” to the Structural Component -Repair

2. Building Refresh, Limited Improvement – the above, plus new bathroom fixtures –Capitalize Bathrooms (plumbing), rest are still Repairs

Remodeling Expenditures‐(5)‐con’t

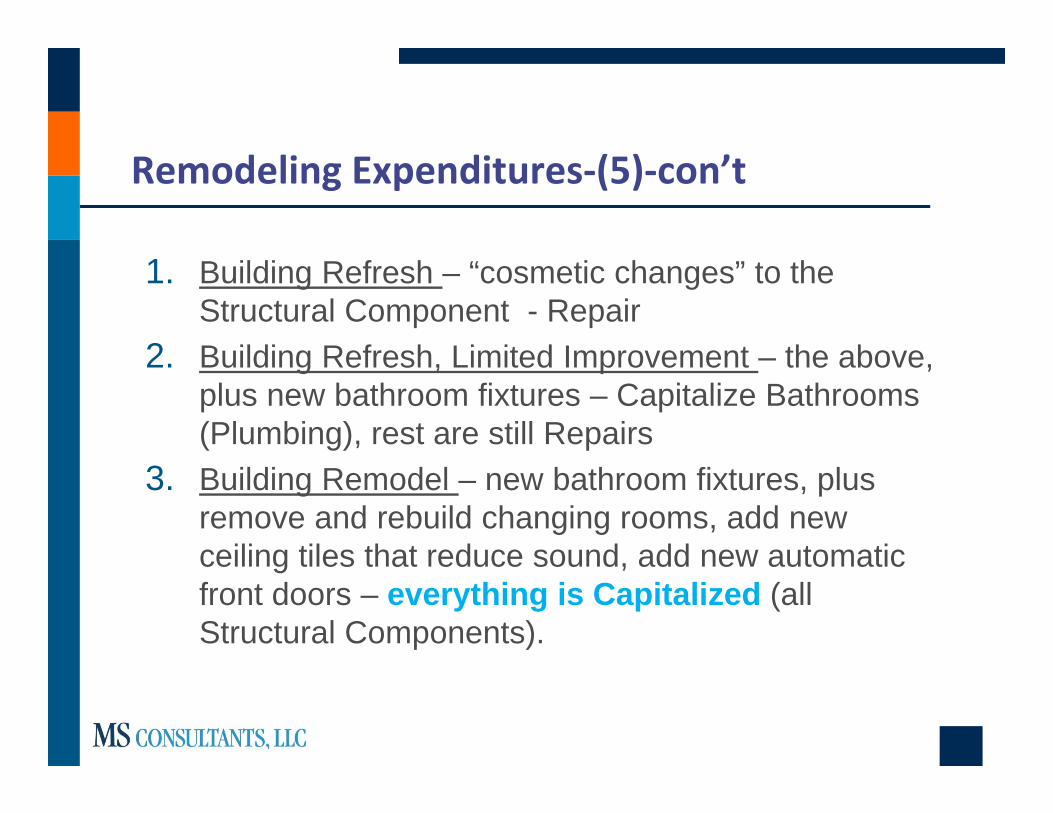

1. Building Refresh – “cosmetic changes” to the Structural Component - Repair

2. Building Refresh, Limited Improvement – the above, plus new bathroom fixtures – Capitalize Bathrooms (Plumbing), rest are still Repairs

3. Building Remodel – new bathroom fixtures, plus remove and rebuild changing rooms, add new ceiling tiles that reduce sound, add new automatic front doors – everything is Capitalized (all Structural Components).

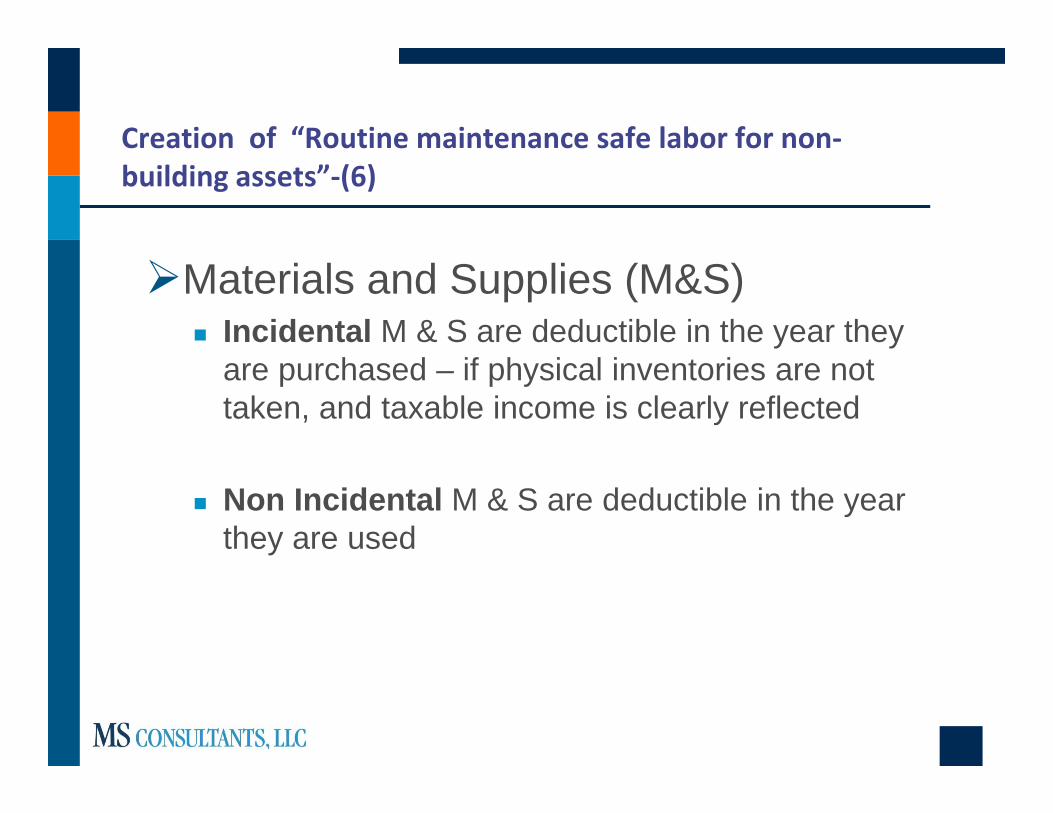

Creation of “Routine maintenance safe labor for non‐building assets”‐(6)

Materials and Supplies (M&S) Incidental M & S are deductible in the year they

are purchased – if physical inventories are not taken, and taxable income is clearly reflected

Non Incidental M & S are deductible in the year they are used

New Rules on Materials & Supplies‐(7)‐con’t

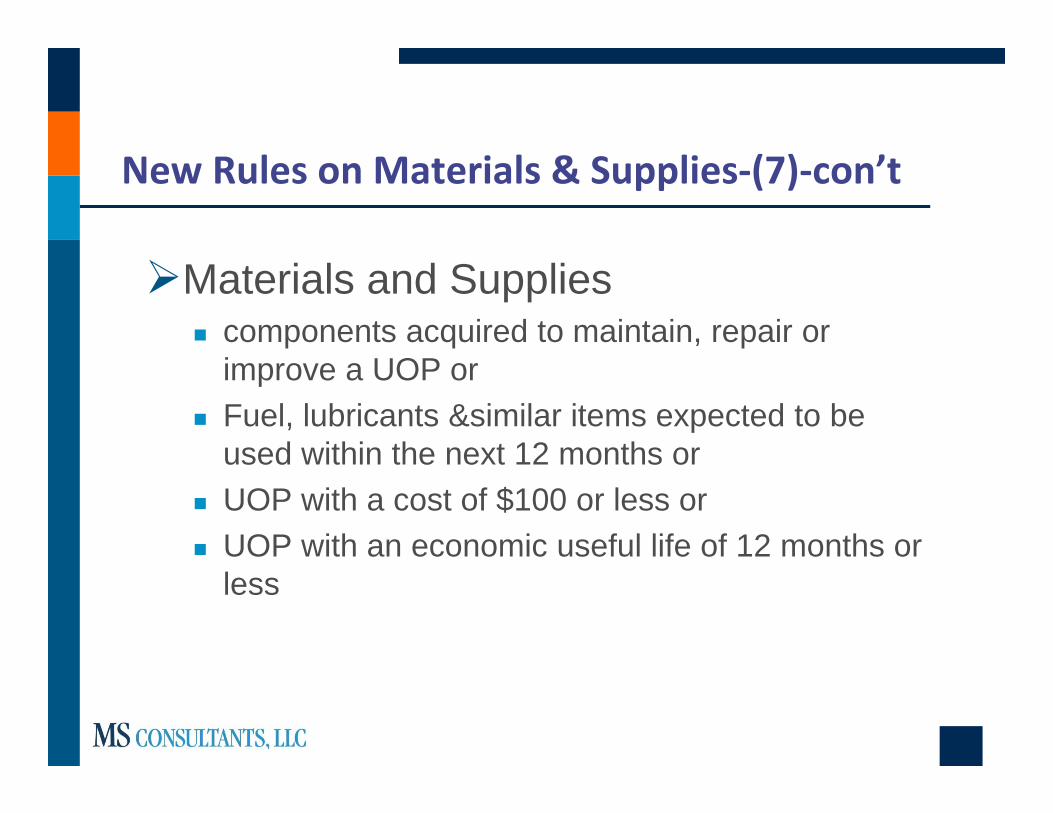

Materials and Supplies components acquired to maintain, repair or

improve a UOP or Fuel, lubricants &similar items expected to be

used within the next 12 months or UOP with a cost of $100 or less or UOP with an economic useful life of 12 months or

less

New Rules on Materials & Supplies‐(7)‐con’t

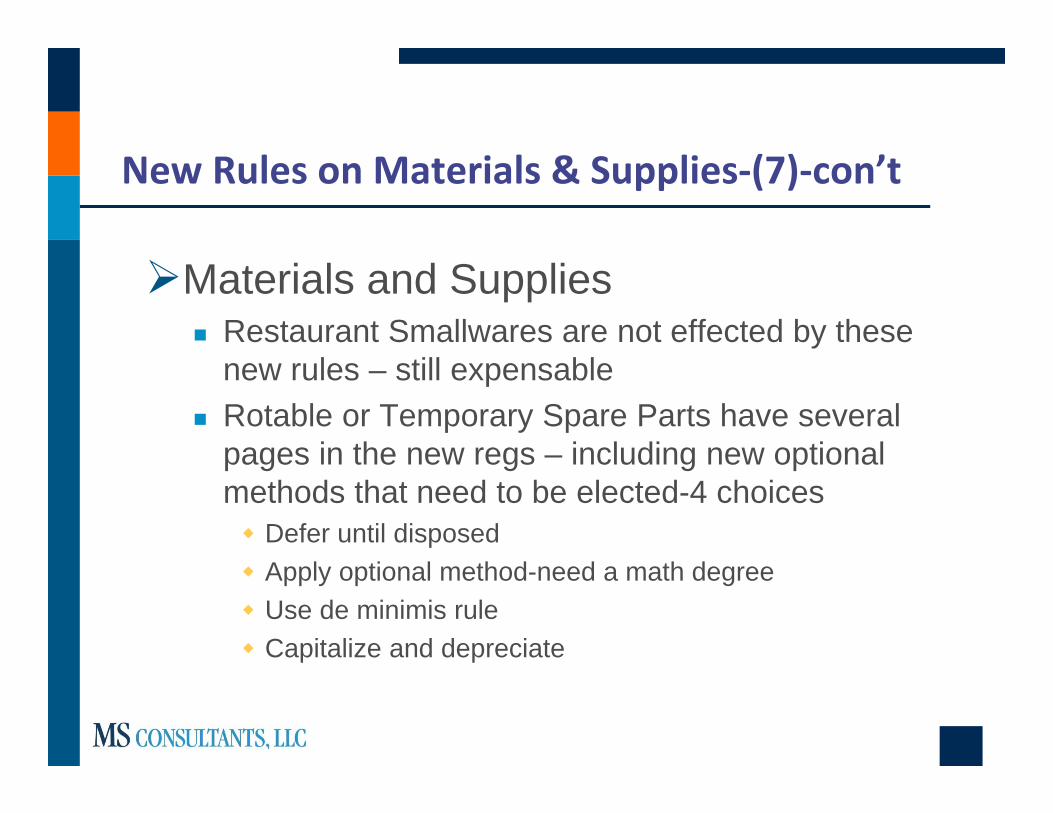

Materials and Supplies Restaurant Smallwares are not effected by these

new rules – still expensable Rotable or Temporary Spare Parts have several

pages in the new regs – including new optional methods that need to be elected-4 choices Defer until disposed Apply optional method-need a math degree Use de minimis rule Capitalize and depreciate

“Official” de minimis rule‐(8)

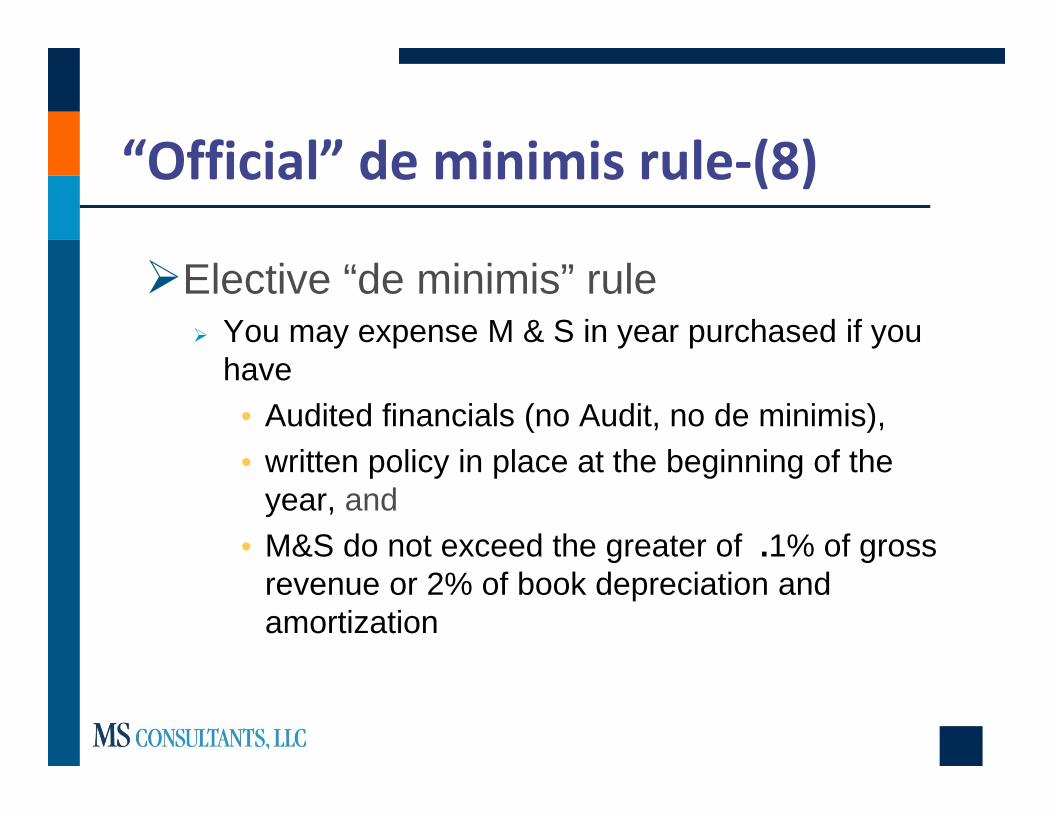

Elective “de minimis” rule You may expense M & S in year purchased if you

have• Audited financials (no Audit, no de minimis), • written policy in place at the beginning of the

year, and • M&S do not exceed the greater of .1% of gross

revenue or 2% of book depreciation and amortization

“De Minimis” example

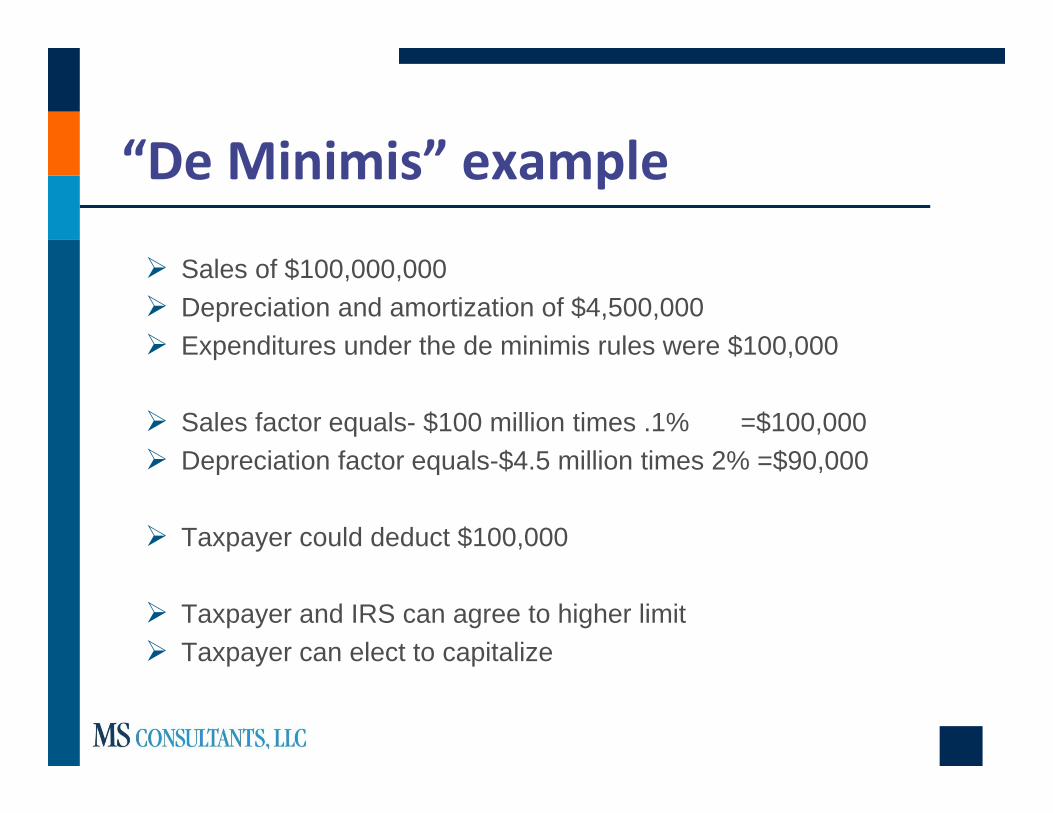

Sales of $100,000,000 Depreciation and amortization of $4,500,000 Expenditures under the de minimis rules were $100,000

Sales factor equals- $100 million times .1% =$100,000 Depreciation factor equals-$4.5 million times 2% =$90,000

Taxpayer could deduct $100,000

Taxpayer and IRS can agree to higher limit Taxpayer can elect to capitalize

“Official” de minimis rule‐(8)‐con’t

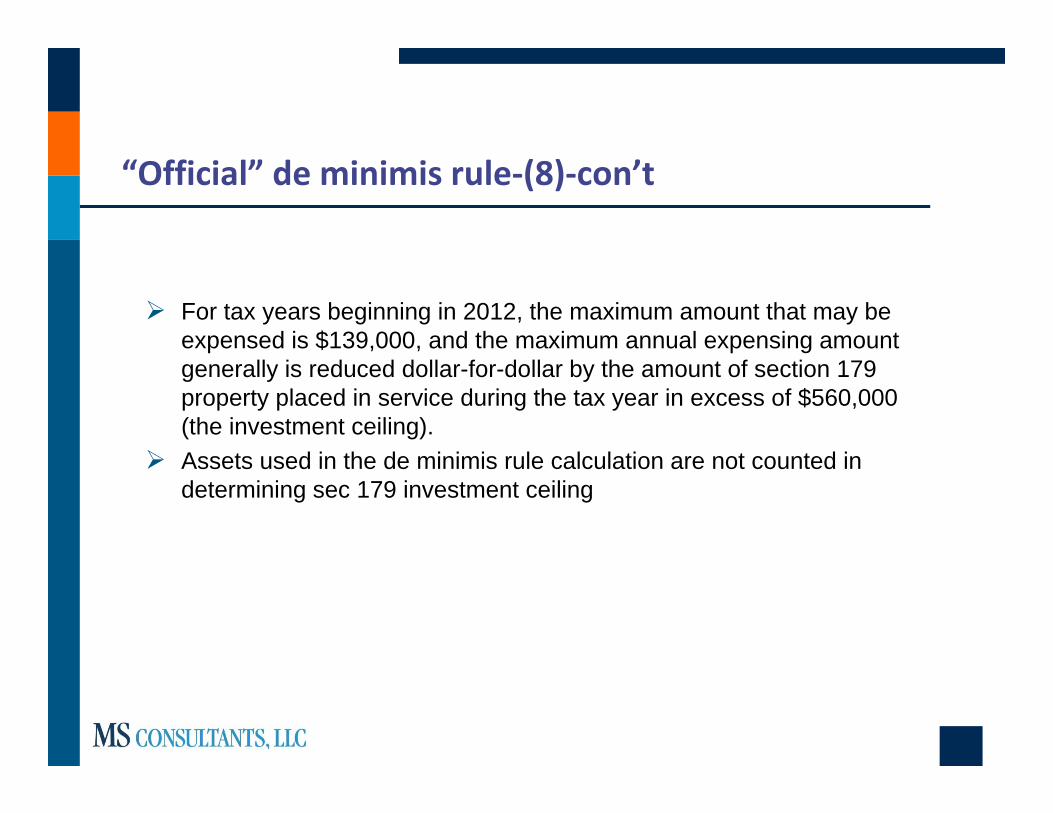

For tax years beginning in 2012, the maximum amount that may be expensed is $139,000, and the maximum annual expensing amount generally is reduced dollar-for-dollar by the amount of section 179 property placed in service during the tax year in excess of $560,000 (the investment ceiling).

Assets used in the de minimis rule calculation are not counted in determining sec 179 investment ceiling

Facilitative Expenses‐(9)

Facilitative costs include “inherently facilitative” expenses made up of 11 categories. These include the costs of items such as shipping, moving or appraising property, application fees, sales and transfer taxes, finder's fees, and architectural, engineering, environmental or inspection services related to specific properties, brokers' or appraisers' fees, and services provided by a qualified intermediary in a Code Sec. 1031 exchange.

Costs relating to activities performed in the process of determining whether to acquire real property and which real property to acquire generally aren't facilitative expenses and therefore may be currently deductible, unless they are “inherently facilitative” expenses.

Amounts paid for employee compensation or overhead can be expensed unless buying for resale under 263a.An election can be made to capitalize.

De minimis rules can be used.

Repairs/Improvements to Non‐Building Assets‐(10)

Same capitalization standards (Betterment, Restoration, New Use)

Routine Maintenance Safe Harbor – ongoing activity that a taxpayer expect to perform - more than once during the ADS taxable life of the UOP - to keep the UOP in ordinary and efficient operating condition (once again, cannot be applied to buildings)

Other Changes to the Rules‐(11)

Clarification that lessors and lessees must depreciate their improvements, and cannot amortize them over the life of the lease. You can even go back and fix.

Other Changes to the Rules‐(11)‐cont

A new rule requires taxpayers to capitalize repair-type expenses made to assets before they are placed in service.”

Buy a building in 2011 but do “repairs” before building is placed in-service in 2012

“Repairs” would be capitalized under new regs. Taxpayer should have placed building in-service

before doing repairs

Large Business & International Directive‐Internal Guidance

For taxpayers who adopted a method of accounting relating to the conversion of capitalized assets to repair expense under IRS sec 263(a)

Resulting from-Rev. Proc. 2009-39, 2009-38 IRB, 08/27/2009 Relates to taxpayers currently expensing items that need to be

capitalized under the new regulations. IRS will discontinue exams Taxpayer has 2 years under Revenue Procedures 2012-19 and 2012-

20 to change accounting method

Transition guidance Issued March 7, 2012

Rev Proc. 2012-19-changes to comply with all provisions except depreciation and dispositions

Rev Proc. 2012-20-changes to comply with depreciation and dispositions

Change is automatic 23 changes in total For tax years beginning on or after January 1, 2012 Cannot be early adopted Scope Limitations waived for 1st and 2nd years Taxpayers receive audit protection for prior years upon filing national

office copy of Form 3115-Ogden, Utah

What the IRS wanted to accomplish when the began rewriting the regs in 2004

“The Service and the Treasury Department want to provide clear,

consistent and administrative rules that will reduce the uncertainty and

controversy in this area . . .”

Did the IRS accomplish their goal?