Embed Size (px)

Citation preview

New Georgian tax code

Revised inbound investment framework

www.pwc.com

PwC

Agenda

1.What is the game plan?

2.Withholding tax on non-residents

3.FIZ framework remains uncertain

4.Transfer pricing

5.Thin capitalisation

6.Closing remarks

2

PwC

What is the game plan?

3

1

PwC

Limited explanation from government on changes

Purposes of the new code:

• Using the best international tax practices, EU directives

IN LINE WITH THE WORLD‘S BEST PRACTICES:

• Terminology used fully in line with OECD standards

• Transfer Pricing

• International cargo

• Associated entities

Mi

nistry

of

Fi

nance

presentation

on

New

Tax

Code

(3

June

2010)

4

PwC

Limited engagement of international business

All consultation was done in Georgian.

Timeframes were too short to allow non-Georgians to participate:

• Two weeks were provided for comments on the draft tax code.

• Process for consulting on secondary legislation is only slightly slower.

A lot of “international best practice” got lost in translation …

5

PwC

The new framework

The government has promoted Georgia as a favourable tax jurisdiction.

Key components were:

• 15% corporate tax rate.

• decreasing withholding tax on payments to non-residents.

• elimination of withholding tax on interest and dividends by 2012.

The new tax code:

• Increases withholding tax on non-residents.

• Potentially makes it more difficult to obtain treaty relief.

• Introduces new transfer pricing and thin capitalisation rules (these carry high compliance costs and are aimed at revenue collection).

6

PwC

Withholding tax on non-residents

7

2

PwC

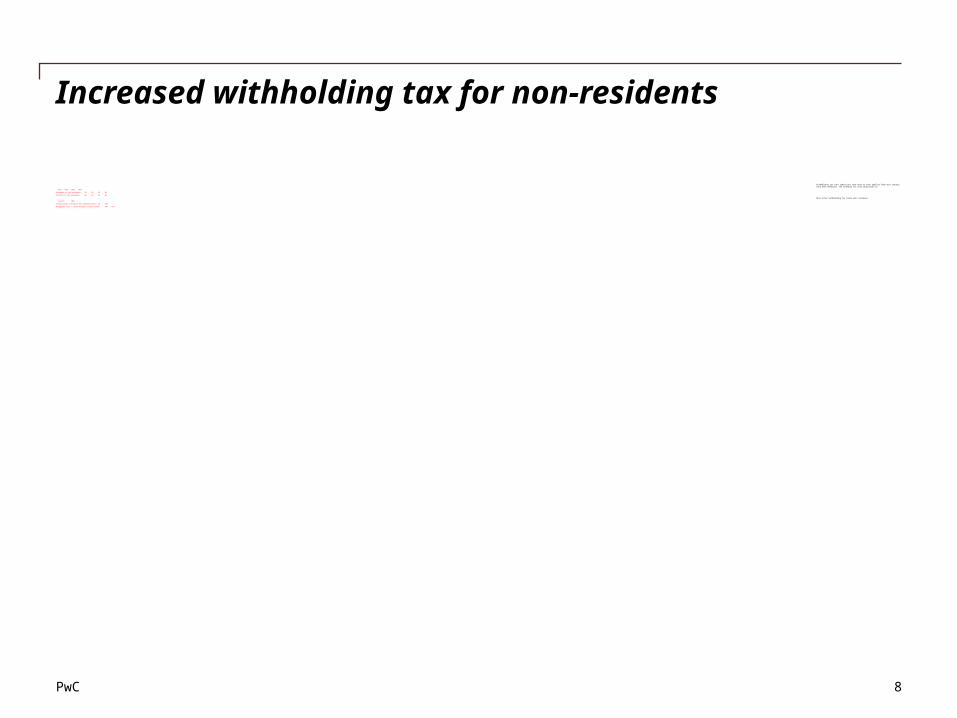

Increased withholding tax for non-residents

Withholding tax rate reductions that were to have applied from next January have been deferred. The schedule for rate reductions is:

2011 2012 2013 2014

Dividends to non-residents 5% 5% 3% 0%

Interest to non-residents 5% 5% 5% 0%

Most other withholding tax rates will increase:

Current 2011

International transport and communications 4% 10%

Management fees / other Georgian-source income 10% 15%

8

PwC

Tax treaties become more important

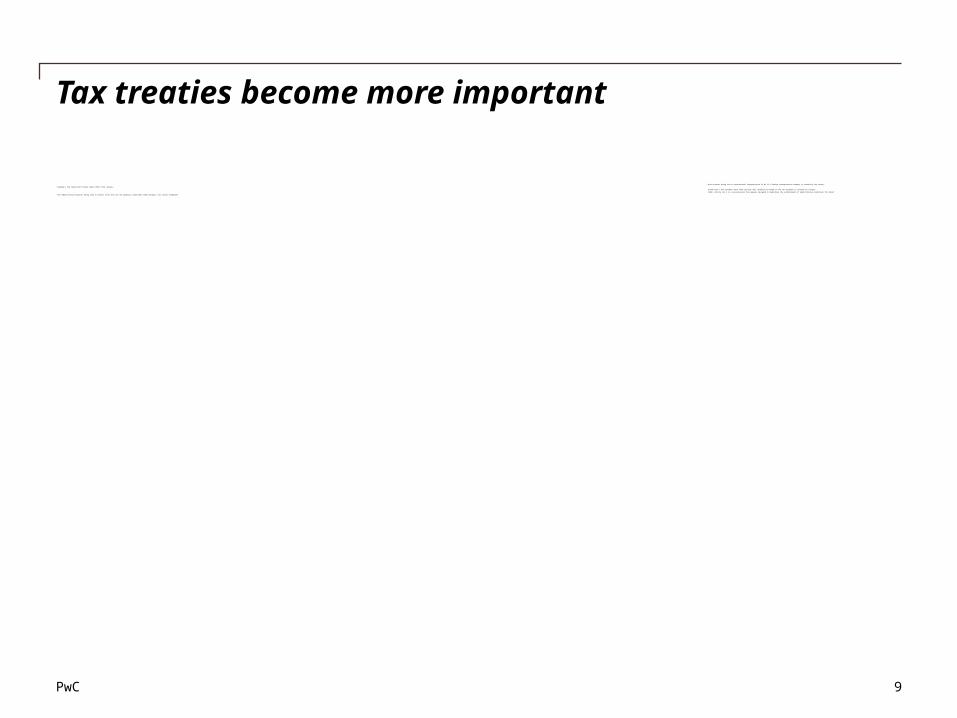

Most treaties bring tax on international transportation to 0% if a foreign transportation company is covered by the treaty.

• Georgia’s new treaty with Turkey takes effect from January.

Income that a non-resident earns from services will normally be exempt if the non-resident is covered by a treaty.

ISSUE: Article 125.1 is a new provision that appears designed to legitimise the establishment of administrative conditions for relief.

• Are administrative barriers being used to collect taxes that are not properly collectable under Georgia’s tax treaty framework?

9

PwC

FIZ framework remains uncertain

10

3

PwC

FIZ rules clarified …

The new tax code suggests:

• A Free Industrial Zone (FIZ) is supposed to operate as a tax-free zone (except personal taxes paid by employees).

• An International Enterprise (IE) is a registered entity operating within a FIZ, and is exempt from profit tax.

• A Free Warehouse Enterprise (FWE) may locate inside or outside a FIZ:

- FWE may store and sell foreign goods or re-export Georgian goods.

- FWE is exempt from profit tax on profits from re-export.

11

PwC

… but problems remain

Who may an IE transact with? An IE may not:

• Supply goods or services outside a FIZ.

• Supply goods or services within a FIZ other than to an IE (is a foreign customer an IE?).

• Receive non-permitted services from non-IE.

• Receive goods included on a negative list from a non-IE.

The Law on Free Industrial Zones does not contemplate such restrictions.

There are no special rules for services received by an IE, so it appears that services provided by a Georgian company would be subject to normal 18% VAT. An IE is VAT exempt, so this is a real cost of business.

12

PwC

Transfer pricing

13

4

PwC

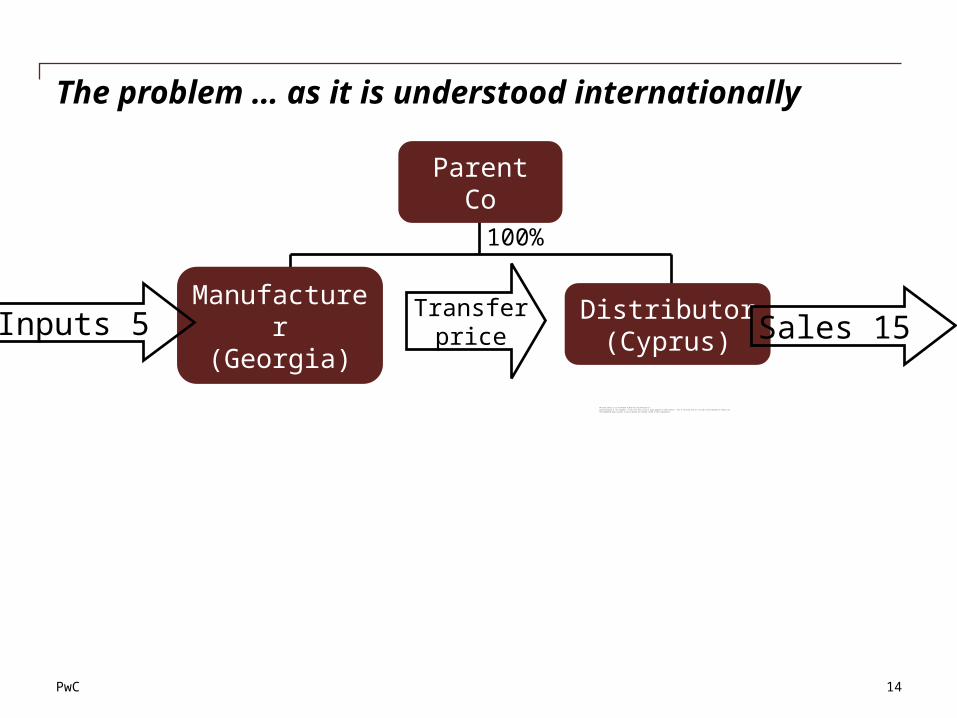

The problem … as it is understood internationally

The total profit is 15, but Parent Co does not care who earns it.

Transfer pricing is “tax avoidance” in the sense that it uses a legal approach to shift profits. This is the label that the tax code and the Ministry of Finance use.

The fundamental policy concern is how to measure the economic income in each jurisdiction.

14

100%

Parent Co

Manufacturer(Georgia)

Distributor(Cyprus)

TransferpriceInputs 5 Sales 15

PwC

Transfer pricing mechanicsWhat does it mean in practical terms?

Concern: Related parties are not subject to market conditions when they set their prices.

Solution: Benchmark transactions between unrelated parties to determine how related parties would act without common control.

Key concepts:

• “Functional analysis” - understanding how companies operate to know what drives value creation and prices.

• “Comparability.”

15

PwC

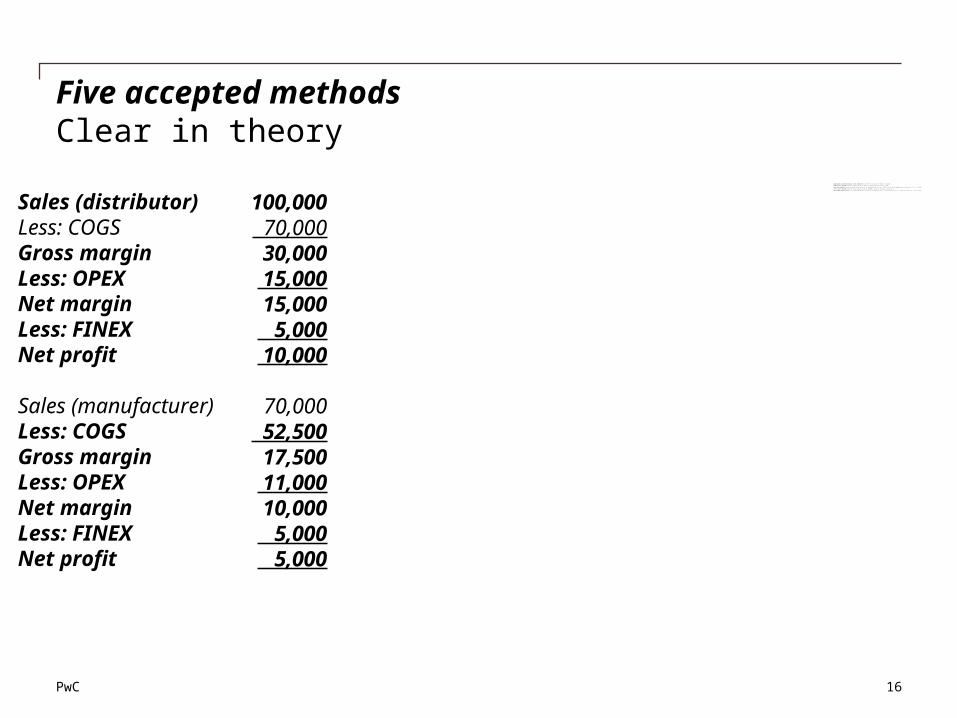

Five accepted methodsClear in theory

16

Comparable uncontrolled price (CUP) method focuses directly on price of product (70,000).

Resale price method focuses on margin based on sales to third parties (30,000/10

0,000 = 30%)

Cost plus method focuses on margin based on costs to third parties (17,500/70,

000 = 25%), and is often expressed as a mark-up (17,500/52,

500 = 331/3%).

Profit split method allocates total operating profit (25,000), based on relative contribution.

Net margin method compares net operating profit to that of independent firms. May use sales (15,000/10

0,000 = 15%) cost (10,000/52,

500 = 19%), assets.

Sales (distributor)Less: COGSGross marginLess: OPEXNet marginLess: FINEXNet profit

Sales (manufacturer)Less: COGSGross marginLess: OPEXNet marginLess: FINEXNet profit

100,000 70,00030,000 15,00015,000 5,000 10,000

70,000 52,50017,500 11,00010,000 5,000 5,000

PwC

Challenging in practice

Example 1: A European multinational in the steel industry sold various classes of steel among its affiliates. Prices were set with regard to the spot price of steel at the time of each sale. Question: What method was used to confirm that the multinational had used arm’s length prices?

Example 2: Two contract manufacturers produce widgets. The first takes title to inventory, but has an arrangement that requires payment only when the finished product is shipped. The second does not take title to inventory:

Sales COGS Opex Profit GP% Net profit

Company 1 2,000 1,000 500 500 50% 25%

Company 2 500 0 250 250 100% 50%

17

PwC

The Georgian model

The law recognises the five OECD methods, consistent with “international best practice.” However, some questions are not answered:

• Why is the government concerned about transfer pricing?

• Will the authorities recognise corresponding adjustments?

• What are the practical implications of Georgia applying a 20% threshold for determining control, compared to the normal 50%?

• The international “arm’s length principle” lost something in translation, and the law focuses on the form, rather than outcome, of arrangements. Will the authorities respect the transactions as they are structured by taxpayers (international best practice)?

18

PwC

Documentation dilemmaDo independent comparables exist in a small market?

Taxpayers must submit documentation (including economic analysis) to demonstrate compliance with the arm’s length principle.

A typical study and economic analysis involves using independent data as an objective standard to validate pricing, and entails:

• Complete a functional analysis to understand what economic factors drive the business.

• Select a pricing method. This will be influenced by drivers of the business AND the quality and extent of available data.

• Apply the method. This involves refining the data to improve the comparability of independent firms.

• Write up the results to explain judgments made in the review process and the results were interpreted.

There are no special penalties for non-compliance.

19

PwC

Conclusions

The full implications will not be clear until after the Ministry of Finance issues administrative guidance on the new rules.

Some thoughts we hope the authorities will heed:

• A possible title for a study: “Adjustments required to create economic comparability of sales of two cubic foot microwave ovens (with rotisserie) in Zaire with three cubic foot microwave ovens (without rotisserie) in Bahrain.”

• Chevron headlines in Tax Management Transfer Pricing Report:

- 7 July 1993: “Chevron Not Required To Label 1.3 Million Pages In §6503(k) Case”

- 18 Aug 1993: “Chevron, IRS Told To Narrow Differences on Documents”

20

PwC

Thin capitalisation

21

5

PwC

Rules in a nutshell

Interest expense may be disallowed on any debt in excess of three times its capital:

• Capital is essentially Assets less Liabilities, but no guidance is provided on how assets are valued.

• Liabilities are only those on which interest is paid, and exclude loans from the government or international organizations.

The rules do not apply to:

• Financial institutions.

• Entities that have gross income of less than GEL 200,000.

• Entities with interest expense that is less than 20% of their taxable income before deducting that interest expense.

22

PwC

What is tax evasion in Georgia?

Article 123.7: The rules only apply if prosecutors of the Ministry of Finance prove that thin capitalization was used for tax evasion.

• What does this mean exactly?

• Georgian language does not distinguish between avoidance and evasion. In New Zealand:

- If I give up my job to live on a beach, I reduce my tax liability and avoid tax. However, my purpose is to change my lifestyle, so no action is taken.

- If my purpose in doing something is to reduce tax, it is struck down. However, no action is taken if tax savings are incidental to a real business purpose.

- Evasion relies on fraud or hiding facts to reduce a tax liability.

23

PwC

The draft regulations paint a scary picture …

A major issue in the new code is the increase in delegated legislation.

• Essentially, Parliament has abrogated responsibility for enacting law to the MoF, which also administers that law.

• This is not international best practice.

Draft thin capitalisation instructions have been prepared:

• The draft does not address the unanswered questions in the law:

- What are “assets”?

- What is “tax evasion”?

• The law defines debt to be a liability of any form on which an interest is paid, except loans received from the government and international financial institutions. The draft instruction defines debt to include interest-free loans.

24

PwC

Closing remarks

25

6

PwC

The new code is generally a step in the right direction …

Relative to developed countries, Georgia’s performance is less than optimal but relative to where its tax system was before the Rose Revolution, its success has been remarkable. Administrative capacity – in line with wider state capacity – has been strengthened, tax receipts are massively up, and increasingly – are being used to advance fledging policy agendas.

If “the public finances are one of the best starting points for an investigation of society, especially though not exclusively of its political life,” then what we see in the Georgia taxation system, although imperfect at times, mirrors, some of the finer aspirations of the post-2003 political elite.

Conclusions in Transparency Internationalreport on the Georgian tax system (May 2010)

26

… but some of the signals are discomforting.

T h i s p u b l i c a t i o n h a s b e e n p re p a re d fo r g e n e ra l g u i d a n c e o n ma tte rs o f i n te re s t o n l y, a n d d o e s n o t c o n s t i t u te p ro f e s s i o n a l a d v i c e . Y o u s h o u l d n o t a c t u p o n t h e i n fo rma t i o n c o n ta i n e d i n th i s p u b l i c a t i o n w i th o u t o b ta i n i n g s p e c i f i c p ro fe s s i o n a l a d v i c e . No re p re s e n t a t i o n o r wa rra n ty (e x p re s s o r i mp l i e d ) i s g i v e n a s to th e a c c u ra c y o r c o mp l e te n e s s o f th e i n fo rma t i o n c o n ta i n e d i n t h i s p u b l i c a t i o n , a n d , to th e e x t e n t p e rmi t te d b y l a w, P ri c e wa te rh o u s e Co o p e rs Ce n tra l A s i a a n d Ca u c a s u s B. V, Ge o rg i a n b ra n c h , i t s me mb e rs , e mp l o y e e s a n d a g e n ts d o n o t a c c e p t o r a s s u me a n y l i a b i l i ty, re s p o n s i b i l i ty o r d u ty o f c a re fo r a n y c o n s e q u e n c e s o f y o u o r a n y o n e e l s e a c t i n g , o r re f ra i n i n g t o a c t , i n re l i a n c e o n t h e i n f o rma t i o n c o n t a i n e d i n th i s p u b l i c a t i o n o r f o r a n y d e c i s i o n b a s e d o n i t .

© 2 0 1 0 Pr i c e wa te rh o u s e Co o p e rs Ce n tra l As i a a n d Ca u c a s u s B .V , Ge o rg i a n b ra n c h . Al l ri g h ts re s e rv e d . In th i s d o c u me n t, “PwC” re fe r s to P ri c e wa te rh o u s e Co o p e rs Ce n tra l As i a a n d Ca u c a s u s B .V ., wh i c h i s a me mb e r f i rm o f P ri c e wa te rh o u s e Co o p e rs In te rn a t i o n a l L i mi t e d , e a c h me mb e r f i rm o f wh i c h i s a s e p a ra te l e g a l e n t i ty.

![Untitled-1 [kgm.ge]kgm.ge/res/docs/ENGL.pdf · KAKHURI BRANDY GVINIS D GEORGIAN MARANI C" ACH A CHACHA FROM GEORGIAN GRAPE C" ACHA Georgian Brandy is a traditional Georgian strong](https://img.pdfslide.us/doc/110x75/5fc65d9b8079666720597242/untitled-1-kgmgekgmgeresdocsenglpdf-kakhuri-brandy-gvinis-d-georgian-marani.jpg)

![SELLING INBOUND: TRANSFORM YOUR REP'S INBOUND SELLING SKILLS [INBOUND 2014]](https://img.pdfslide.us/doc/110x75/55d54cf8bb61ebdb228b46ca/selling-inbound-transform-your-reps-inbound-selling-skills-inbound.jpg)