Embed Size (px)

Citation preview

New European Markets –

Baltic operations How to navigate in a recessionary environment

Valdis SiksnisCountry Senior Executive, Nordea Latvia branch

2

Nordea -

the leading bank in the Nordic and Baltic Sea region

RussiaRussia

Branches 51Customers 40,000Total lending EUR 2.5bnMarket rank Top 35

Branches 51Customers 40,000Total lending EUR 2.5bnMarket rank Top 35

LatviaLatvia

Branches 21Customers 68,000Total lending EUR 2.7bnMarket rank 4

Branches 21Customers 68,000Total lending EUR 2.7bnMarket rank 4

LithuaniaLithuania

Branches 17Customers 92,000Total lending EUR 2.0bnMarket rank 4

Branches 17Customers 92,000Total lending EUR 2.0bnMarket rank 4

EstoniaEstonia

Branches 19Customers 73,000Total lending EUR 2.0bnMarket rank 4

Branches 19Customers 73,000Total lending EUR 2.0bnMarket rank 4

DenmarkDenmark

Branches 384Customers 1,544,000Total lending EUR 65bnMarket rank 2

Branches 384Customers 1,544,000Total lending EUR 65bnMarket rank 2

NorwayNorway

Branches 124Customers 753,000Total lending EUR 40bnMarket rank 2

Branches 124Customers 753,000Total lending EUR 40bnMarket rank 2

FinlandFinland

Branches 345Customers 3,000,000Total lending EUR 51bnMarket rank 1

Branches 345Customers 3,000,000Total lending EUR 51bnMarket rank 1

PolandPoland

Branches 96Customers 1,169,000*Total lending EUR 3.5bnMarket rank 13

Branches 96Customers 1,169,000*Total lending EUR 3.5bnMarket rank 13

SwedenSweden

Branches 282Customers 3,473,000Total lending EUR 65bnMarket rank 2-3

Branches 282Customers 3,473,000Total lending EUR 65bnMarket rank 2-3

European Private Banking

European Private Banking

Customers 11,000Total AUM EUR 8bnMarket rank 1 Nordic in Luxembourg

Customers 11,000Total AUM EUR 8bnMarket rank 1 Nordic in Luxembourg

•Incl. Polish Life customers• Assets before eliminations

3

Moderated risk exposure in New European Markets –

increased profitability

An important component in the Nordea long-term strategy

Organic growth strategy has created a solid position in five East European countries

Value creation through profitable organic growth – maintained moderate risk profile

Revenues from New European Markets accounts for approx. 5% of Nordea Group revenues

New European Markets total income, EURm

68

8394

121110

Q3/07 Q4/07 Q1/08 Q2/08 Q3/08

4

Household strategy Based on strong competencies

Private Banking Corporate strategy Selective investments

Existing Nordic customers and new customersSelected global and European business lines

New European Markets

Next level of efficiency to support sustainable growth

Free up resources across the value chain - developing channels, customer service concepts and further streamline processes and IT-systems

Invest in product development, IT-systems and -infrastructure

Strengthen position in relationship-driven customer segments

Support the relationship banking strategy by a focused product strategy

Further differentiate service levels among and within customer segments

Enhance accessibility for all customers and secure efficient servicing - in particular of non-relationship banking customers

Continue to leverage positions within shipping & wealth management

Continue the profitable, risk-balanced growth

Prepare for a closer integration with the rest of the Group

The Nordea organic growth strategy –

4 Pillars

5

Selective investments in New European Markets

Cautious growth in Baltic countriesHarvest from investments – unchanged branch network 2009

Development of new customer segments (e.g. Private Banking)

Organic growth strategy in Poland according to plan - 36 new branches opened the first 9 months 2008

Average break-even after 9 months

Nordea – strong brand name and reputation

Nordea’s growth plan in Russia based on experiences from Poland and the Baltic countries and the full capacity of the Group

6

Key focus

on…

Superior and profitable growth in all segments where we choose to compete:

Nordic and international corporates

Best local corporates in attractive segments

Municipalities and state entities

Employees of corporate customers

Higher income earners

Young people with high potential income

Innovative multichannel distribution and a high level use of e-services

Full product assortment and standardized customer concepts with successful track record and procedures approved by the Nordea Group

7

Macroeconomic situation and trends

8

Will get worse before things will start to improve

Source: Nordea Markets

9

External imbalances have started to improve

Inflation peaked during the summer

10

Unemployment set to rise

Wage pressures easing (at least in Estonia and Latvia)

Source: Nordea Markets

11

Business development and market position in Baltics

12

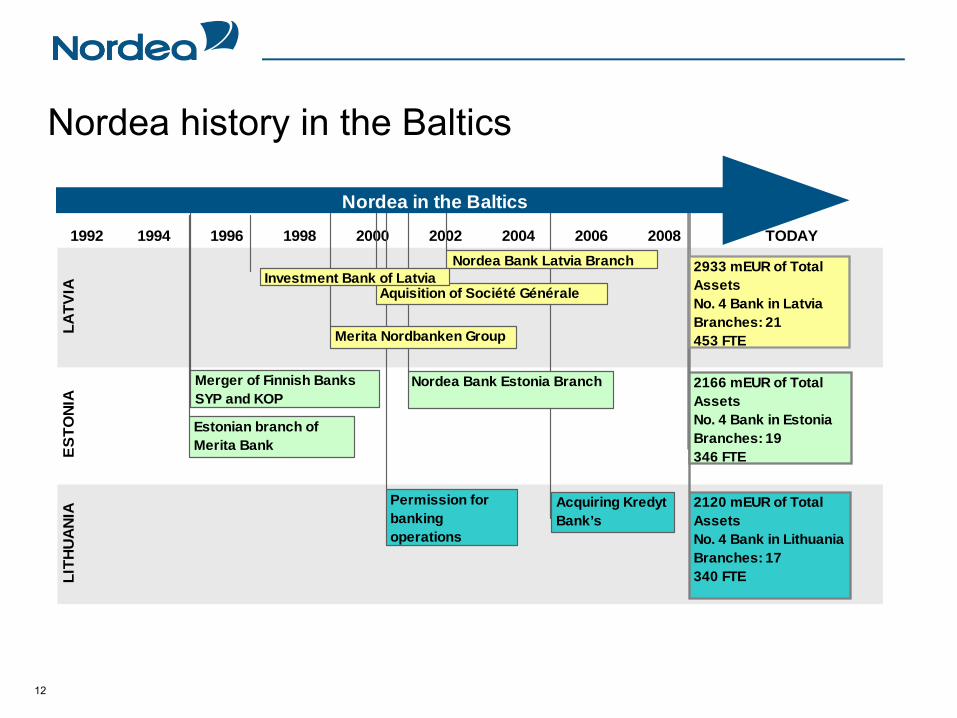

TODAY

LATV

IAES

TONI

ALI

THUA

NIA

1992 20081994 1996 1998 2000 2002 2004 2006

Acquiring Kredyt Bank’s

Nordea Bank Latvia Branch

2120 mEUR of Total AssetsNo. 4 Bank in Lithuania Branches: 17 340 FTE

2166 mEUR of Total AssetsNo. 4 Bank in Estonia Branches: 19 346 FTE

2933 mEUR of Total AssetsNo. 4 Bank in LatviaBranches: 21 453 FTE

Nordea Bank Estonia Branch Merger of Finnish Banks SYP and KOP

Permission for banking operations

Aquisition of Société Générale

Merita Nordbanken Group

Estonian branch of Merita Bank

Nordea in the Baltics

Investment Bank of Latvia

Nordea history in the Baltics

13

Market rank by total assets end June 2008

0

2000

4000

6000

8000

10000

12000

Han

saba

nk

SEB

Nor

dea

Sam

po

EKR

E

BIG

ÄRIP

SBM

mio

EU

R

26,29%32,98%22,54%25,20%

9,19%24,56%

-1,65%

4,22%

Latvia5.2%

-3.8% -2.1%

18.9% 3.4%

-7.5% -1.4% 6.6%-5.0% -15.7% -10.3%

13.8%0

1000000

2000000

3000000

4000000

5000000

6000000

7000000

8000000

Han

saba

nka

Par

ex b

anka

SEB

ban

ka

Nor

dea

DnB

NO

RD

Rie

tum

uB

anka

Aizk

rauk

les

bank

aLa

tvija

sH

ipotēk

u un

zem

esU

niC

redi

tB

ank

Latv

ijas

Krā

jban

ka

Nor

vik

Ban

ka

Dan

ske

Ban

k

tEUR

0

1000

2000

3000

4000

5000

6000

7000

8000

SE

B

Han

saba

nk

DnB

NO

RD

Nor

dea

Dan

ske

Ban

k

Sno

ras

Ban

k

Ūki

o B

ank

Šia

ulių

Ban

k

Par

ex B

ank

HV

B

Med

ical

Ban

k

mio

EU

R

1,4%

0,8%8,6%30,0%

1,4%

19,1%

5,1%9,0%5,1%

-3,0% 9,6 %

Estonia

Lithuania

14

Maintained low cost base and further leverage of investments

LithuaniaLithuania

Branches 17Customers 92,000Total lending EUR 2.0bnMarket rank 4

Branches 17Customers 92,000Total lending EUR 2.0bnMarket rank 4

EstoniaEstonia

Branches 19Customers 73,000Total lending EUR 2.0bnMarket rank 4

Branches 19Customers 73,000Total lending EUR 2.0bnMarket rank 4

LatviaLatvia

Branches 22Customers 68,000Total lending EUR 2.7bnMarket rank 4

Branches 22Customers 68,000Total lending EUR 2.7bnMarket rank 4

Development of new customer segments (e.g. Private Banking)

Sales focus on cash management, daily services and savings products

Portfolio quality above market average

Branches 2005

FTE 2005 Branches 2008

FTE 2008

Estonia 11 203 20 346

Latvia 12 215 21 469

Lithuania 10 147 19 315

Prepared for new market situation in Baltic countries

15

Baltic total Latvia Estonia LithuaniaEUR

m Q3/08 Q3/07 Q3/08 Q3/07 Q3/08 Q3/07 Q3/08 Q3/07Total income 105 76 50 37 29 24 26 15Total expenses 42 33 18 14 13 11 11 8Profit before loan losses 61 42 32 23 15 12 14 7

Operating profit 54 42 29 23 14 12 11 7

Increased profitability in Baltic operations

76

105

4254

Q307 Q308

Total income Total expenses Operating profit

EURm

16

Gradually slowing growth ratesGrowth total lending, %

50 49

38

145

65

78

52

9

35

2005 2006 2007 Q308/Q307 Q308/Q208

Total market Nordea

Growth in total lending, EURbn

8,6

10,711,6

7,2

2,7

0,9

2,4 2,5

0,60,6

2005 2006 2007 Q308/Q307 Q308/Q208

Total market Nordea

Nordea accounts for approx 20% of new lending in Q3 – slowing growth rate

Increase mainly explained by new lending to existing customers and to Nordic corporates

17

Credit risk management

18

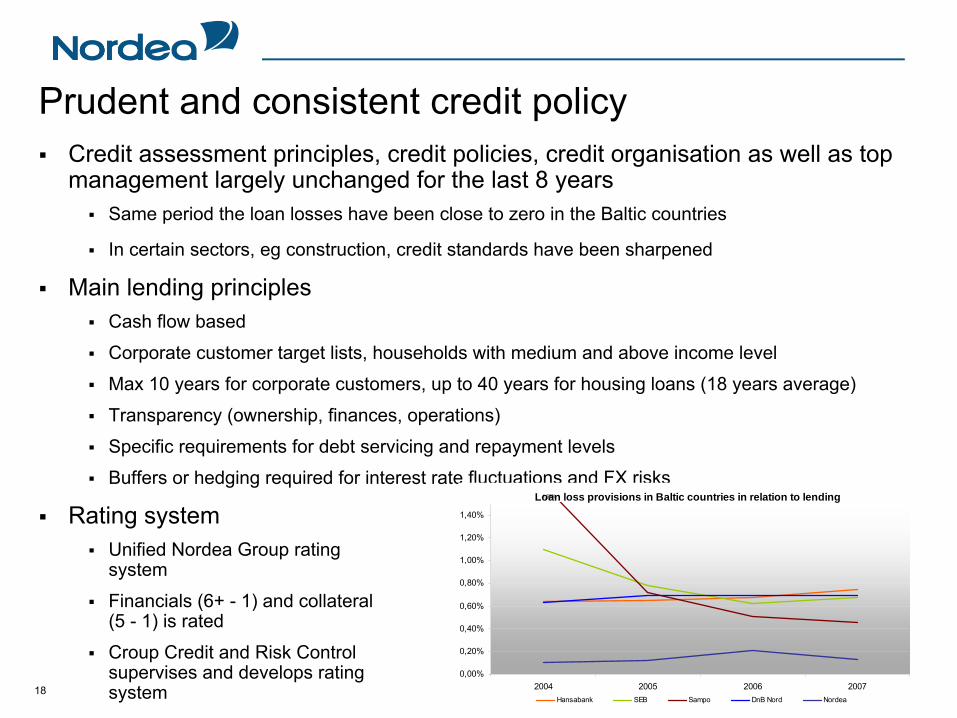

Prudent and consistent credit policyCredit assessment principles, credit policies, credit organisation as well as top management largely unchanged for the last 8 years

Same period the loan losses have been close to zero in the Baltic countries

In certain sectors, eg construction, credit standards have been sharpened

Main lending principlesCash flow based

Corporate customer target lists, households with medium and above income level

Max 10 years for corporate customers, up to 40 years for housing loans (18 years average)

Transparency (ownership, finances, operations)

Specific requirements for debt servicing and repayment levels

Buffers or hedging required for interest rate fluctuations and FX risks

Rating systemUnified Nordea Group rating system

Financials (6+ - 1) and collateral (5 - 1) is rated

Croup Credit and Risk Control supervises and develops rating system

Loan loss provisions in Baltic countries in relation to lending

0,00%

0,20%

0,40%

0,60%

0,80%

1,00%

1,20%

1,40%

2004 2005 2006 2007Hansabank SEB Sampo DnB Nord Nordea

1,68%

19

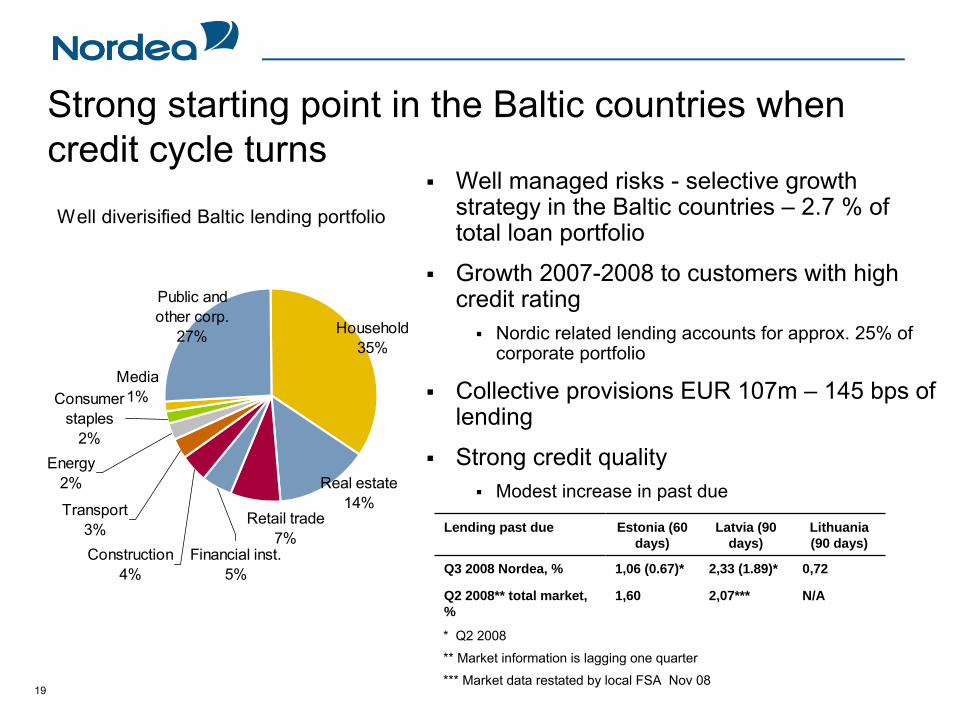

Strong starting point in the Baltic countries when credit cycle turns

Well managed risks - selective growth strategy in the Baltic countries – 2.7 % of total loan portfolio

Growth 2007-2008 to customers with high credit rating

Nordic related lending accounts for approx. 25% of corporate portfolio

Collective provisions EUR 107m – 145 bps of lending

Strong credit qualityModest increase in past due

Well diverisified Baltic lending portfolio

Public and other corp.

27%

Financial inst.5%

Consumer staples

2%Energy

2%

Transport3%

Media1%

Household35%

Real estate14%

Construction 4%

Retail trade7%

Lending past due Estonia (60 days)

Latvia (90 days)

Lithuania (90 days)

Q3 2008 Nordea, % 1,06 (0.67)* 2,33 (1.89)* 0,72

Q2 2008** total market, %

1,60 2,07*** N/A

* Q2 2008

** Market information is lagging one quarter

*** Market data restated by local FSA Nov 08

20

Insignificant individual loan losses Ytd September

Impaired loans of EUR 106m or 1.45% of total lending

Collective allowances for the Baltic countries amounting to EUR 107m

Loan losses remained at low levels

0

1

2

3

4

5

6

7

8

2007 Q108 Q208 Q3080

5

10

15

20

25

30

35

Total lending (lhs) Loan losses in basis points of total lending (rhs)

EURbn bps

21

Nordea Latvian operations

22

Loan growth mainly in corporate segment

0

200

400

600

800

1 000

1 200

1 400

1 600

1 800

2 000

1.kv2005

2.kv2005

3.kv2005

4.kv2005

1.kv2006

2.kv2006

3.kv2006

4.kv2006

1.kv2007

2.kv2007

3.kv2007

4.kv2007

1.kv2008

2.kv2008

3.kv2008

Corporate loans Household loans

EURm

23

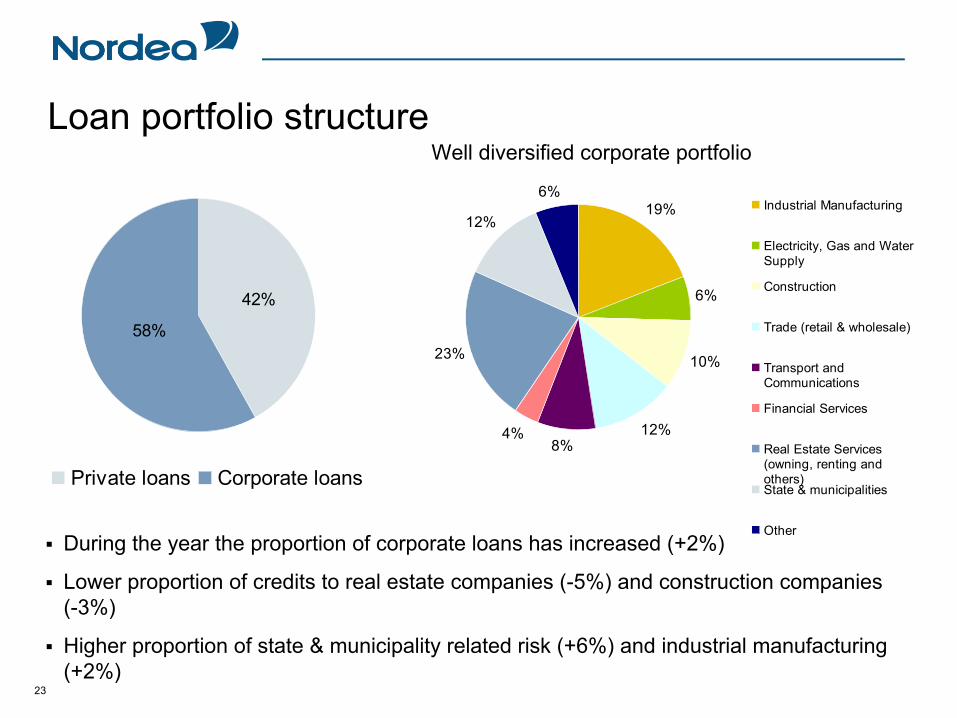

Loan portfolio structure

58%

42%

Private loans Corporate loans

19%

6%

10%

12%8%

4%

23%

12%

6%Industrial Manufacturing

Electricity, Gas and WaterSupply

Construction

Trade (retail & wholesale)

Transport andCommunications

Financial Services

Real Estate Services(owning, renting andothers)State & municipalities

Other During the year the proportion of corporate loans has increased (+2%)

Lower proportion of credits to real estate companies (-5%) and construction companies (-3%)

Higher proportion of state & municipality related risk (+6%) and industrial manufacturing (+2%)

Well diversified corporate portfolio

24

Deposits increases in both Corporate and Household segment

Resident deposit market has been decreasing

Nordea perceived as “safe harbour” – substantial increase of current account balance and deposit volumes during last 5 weeks

0

50

100

150

200

250

300

350

1.kv 2005 3.kv 2005 1.kv 2006 3.kv 2006 1.kv 2007 3.kv 2007 1.kv 2008 3.kv 2008

Corporate deposits Household deposits

EURm

25

Market shares

Large volume of non-resident deposits in the market influences Nordea market share

Deposit market share increase, “house bank”relationships top sales priority

4%5%6%7%8%9%

10%11%12%13%

Q12003

Q32003

Q12004

Q32004

Q12005

Q32005

Q12006

Q32006

Q12007

Q32007

Q12008

Q32008

Corporate loans Household loans

12.2%

11.3%

4.4%

3.2%

1,5%

2,0%

2,5%

3,0%

3,5%

4,0%

4,5%

5,0%

Q12003

Q32003

Q12004

Q32004

Q12005

Q32005

Q12006

Q32006

Q12007

Q32007

Q12008

Q32008

Corporate deposits Household deposits

26

Loan loss provisions

0

500

1 000

1 500

2 000

2 500

3 000

3 500

2002 2003 2004 2005 2006 2007 20080,00%

0,05%

0,10%

0,15%

0,20%

0,25%

Net Loan Losses and provisions Net Loans Losses and provisions from Total Portfolio

2002 2003 2004 2005 2006 2007 2008Loans 128 005 310 144 466 747 749 468 1 207 127 2 211 316 2 859 229Off-balance sheet items 10 610 33 739 40 875 122 365 116 153 165 498 183 089Loan Portfolio Total 138 616 343 883 507 622 871 833 1 323 280 2 376 814 3 042 318Net Loan Losses and provisions 285 2 758 115 213 426 2 874Net Loan Losses and provisions from Total Portfolio 0,21% 0,00% 0,15% 0,01% 0,02% 0,02% 0,09%

27

Operating profit increased by 24%

2006 1-3 Kv. 2007 1-3 Kv. 2008 1-3Kv.Net interest income 12 958 22 493 31 524Comission Income 4 435 11 229 10 711Other income 3 421 3 082 7 425Total income 20 814 36 804 49 660Staff costs 4 913 5 497 8 651Administrative expenses 3 708 7 465 8 496Other costs 515 428 771Total costs 9 136 13 390 17 917Income-expenses 11 678 23 414 31 743Loan provisions 196 68 2 874Operational income 11 481 23 346 28 868C/I 43,9% 36,4% 36,1%

0

10 000

20 000

30 000

40 000

50 000

60 000

2006 1-3 Kv. 2007 1-3 Kv. 2008 1-3Kv.0,0%

5,0%

10,0%

15,0%

20,0%

25,0%

30,0%

35,0%

40,0%

45,0%

50,0%

Income Total expenses Operational profit C/I

2820082007

15

Nordea branch network in Latvia

22 branches

This year:2 new branches in Riga

2 branches expanded in Daugavpils and Liepāja

By the end of the year new branch in Ventspils

29

Profitability in banking sector decreasing –

Nordea an industry exception

Profit before tax (TEUR)

020 000

40 00060 000

80 000100 000120 000

140 000160 000

180 000200 000

Q12006

Q22006

Q32006

Q420006

Q12007

Q22007

Q32007

Q42007

Q12008

Q22008

Q32008

0,0%

2,0%

4,0%

6,0%

8,0%

10,0%

12,0%

14,0%

16,0%

Banking sector Nordea Nordea share of total pretax profit

30

Summary

Solid position in five East European countries

New European Markets an important component in the Nordea long-term strategy

Strong starting point in the Baltic countries when credit cycle turns

Prudent and consistent credit policy

Loan losses remained at low levels - past due lower than market average

Lower proportion of credits to real estate companies and construction companies in Latvian corporate portfolio

Profitability in Latvian banking sector decreasing – Nordea an industry exception

New European Markets –

Baltic operations How to navigate in a recessionary environment

Valdis SiksnisCountry Senior Executive, Nordea Latvia branch

32

Appendix

33

New European Markets 9 month results

Poland Latvia Estonia Lithuania RussiaEURm Ytd

08 Ytd

07 Ytd

08 Ytd

07 Ytd

08 Ytd

07 Ytd

08 Ytd

07 Ytd

08 Ytd

07

Total income 101 62 50 37 29 24 26 15 122 55

Total expenses 56 41 18 14 13 11 11 8 57 33

Profit before loan losses 44 21 32 23 15 12 14 7 65 23

Operating profit 45 21 29 23 14 12 11 7 65 21

Ytd

08 Ytd

07 Ytd

08 Ytd

07 Ytd

08 Ytd

07 Ytd

08 Ytd

07 Ytd

08 Ytd

07

Lending, bn 3.9 2.3 2.9 2.0 2.1 1.5 2.3 1.2 3.5 0.9

Deposits, bn 2.3 1.4 0.6 0.5 0.6 0.6 0.5 0.3 0.6 0.3

Number

of employees

(FTEs) 1 000 1 444 469 405 346 303 315 240 1 704 1 217

34

3rd quarter operating profit by markets

Banking Denmark

Banking Finland

Banking Norway

Banking Sweden

New European Markets

EURm Q308 Chg Q308 Chg Q308 Chg Q308 Chg Q308 Chg

Total income 464 8% 435 3% 252 25% 456 7% 120 76%

Total expenses -212 7% -193 7% -118 6% -242 9% -57 46%

Profit before loan losses 252 10% 242 0% 134 47% 214 5% 63 272%

Operating profit 220 -7% 223 -10% 130 34% 208 8% 58 93

Q308 Q307 Q308 Q307 Q308 Q307 Q308 Q307 Q308 Q307

RaRoCar, % 24 27 34 38 23 18 24 24 39 23

C/I ratio, % 46 46 44 43 47 55 53 52 48 67

Lending, bn 66.0 59.5 51.9 45.7 39.7 35.5 64.1 58.9 14.8 8.1

Deposits, bn 35.1 31.1 34.0 28.4 19.3 18.9 31.3 28.3 4.5 3.2

Number of employees (FTEs) 4 969 4 989 5 457 5 476 1 877 1 806 4 856 4 336 4 291 3 178

35

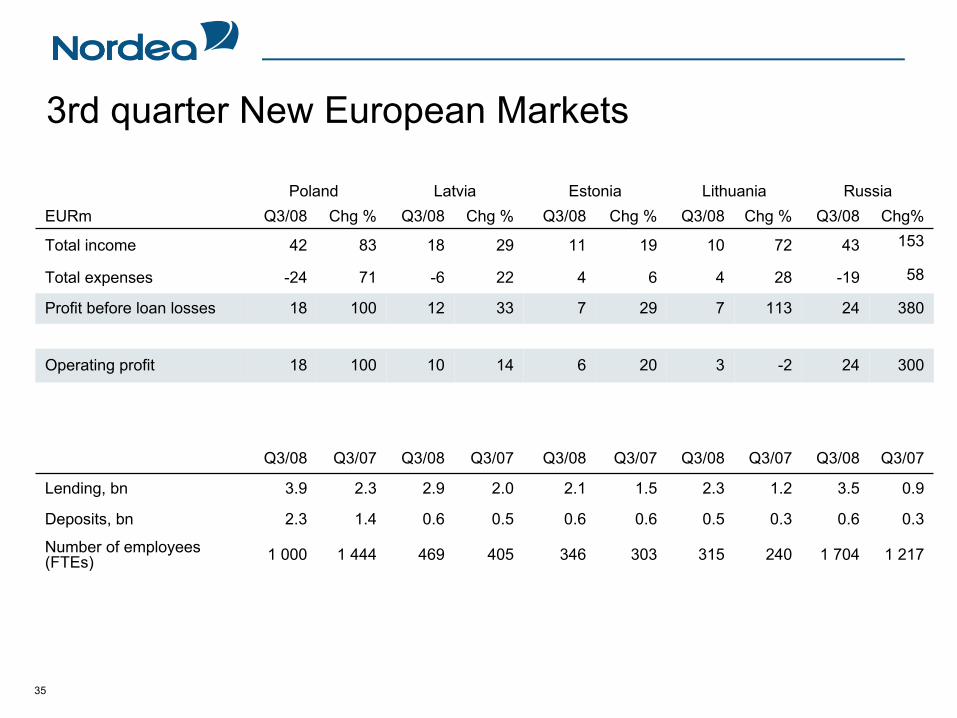

3rd quarter New European Markets

Poland Latvia Estonia Lithuania RussiaEURm Q3/08 Chg % Q3/08 Chg % Q3/08 Chg % Q3/08 Chg % Q3/08 Chg%

Total income 42 83 18 29 11 19 10 72 43 153

Total expenses -24 71 -6 22 4 6 4 28 -19 58

Profit before loan losses 18 100 12 33 7 29 7 113 24 380

Operating profit 18 100 10 14 6 20 3 -2 24 300

Q3/08 Q3/07 Q3/08 Q3/07 Q3/08 Q3/07 Q3/08 Q3/07 Q3/08 Q3/07

Lending, bn 3.9 2.3 2.9 2.0 2.1 1.5 2.3 1.2 3.5 0.9

Deposits, bn 2.3 1.4 0.6 0.5 0.6 0.6 0.5 0.3 0.6 0.3

Number

of employees

(FTEs) 1 000 1 444 469 405 346 303 315 240 1 704 1 217

![Object-oriented rapid prototyping / [by] Valdis Berzins](https://img.pdfslide.us/doc/110x75/61ec7f1fe7d16b283277bfb2/object-oriented-rapid-prototyping-by-valdis-berzins.jpg)