Embed Size (px)

DESCRIPTION

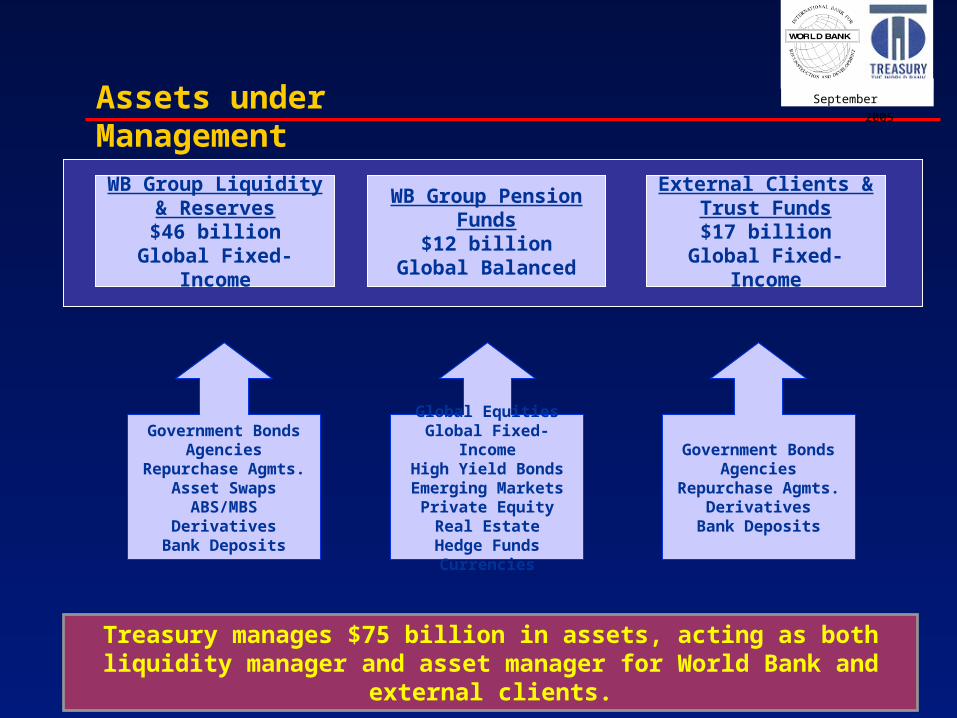

New Directions in Strategic Asset Allocation. International Conference on the Investment of Social Security Funds September 27-28, 2005 Merida, Mexico. Sudhir Rajkumar Head of Pension Asset Advisory Services World Bank Treasury [email protected]. Assets under Management. - PowerPoint PPT Presentation

Citation preview

1

September

2005

New Directions in Strategic Asset Allocation

International Conferenceon the

Investment of Social Security Funds

September 27-28, 2005Merida, Mexico

Sudhir RajkumarHead of Pension Asset Advisory Services

World Bank [email protected]

2

September

2005

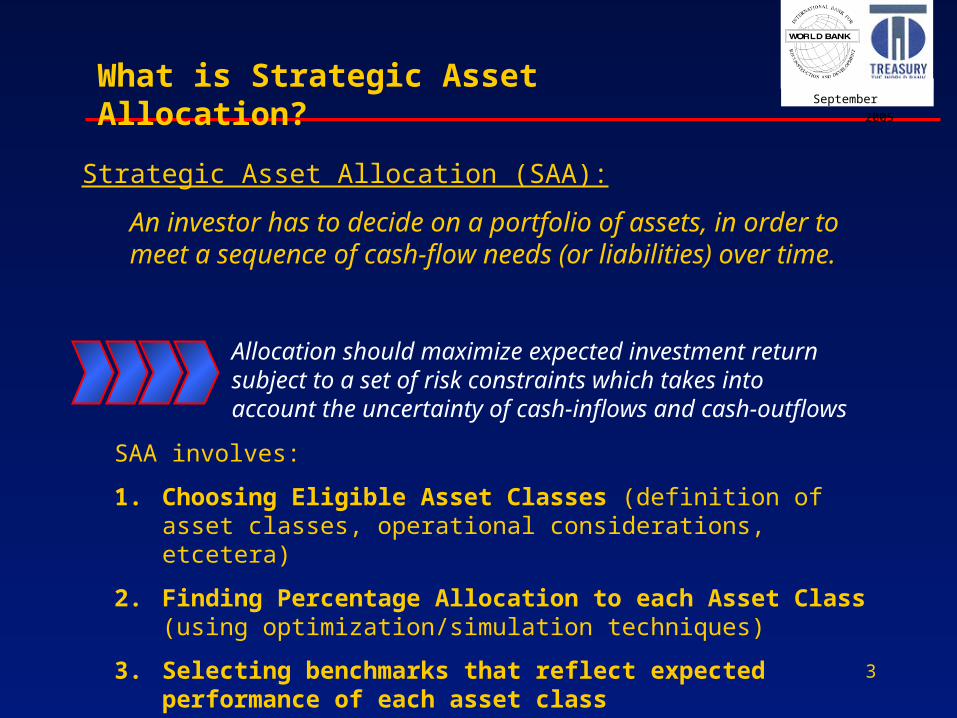

WB Group Liquidity & Reserves$46 billion

Global Fixed-Income

WB Group Pension Funds

$12 billionGlobal Balanced

External Clients & Trust Funds$17 billion

Global Fixed-Income

Government BondsAgencies

Repurchase Agmts.Asset Swaps

ABS/MBSDerivatives

Bank Deposits

Global EquitiesGlobal Fixed-Income

High Yield BondsEmerging Markets

Private EquityReal Estate

Hedge FundsCurrencies

Government BondsAgencies

Repurchase Agmts.Derivatives

Bank Deposits

Assets under Management

Treasury manages $75 billion in assets, acting as both liquidity manager and asset manager for World Bank and external clients.

3

September

2005

Strategic Asset Allocation (SAA):

An investor has to decide on a portfolio of assets, in order to meet a sequence of cash-flow needs (or liabilities) over time.

SAA involves:

1. Choosing Eligible Asset Classes (definition of asset classes, operational considerations, etcetera)

2. Finding Percentage Allocation to each Asset Class (using optimization/simulation techniques)

3. Selecting benchmarks that reflect expected performance of each asset class

Allocation should maximize expected investment return subject to a set of risk constraints which takes into account the uncertainty of cash-inflows and cash-outflows

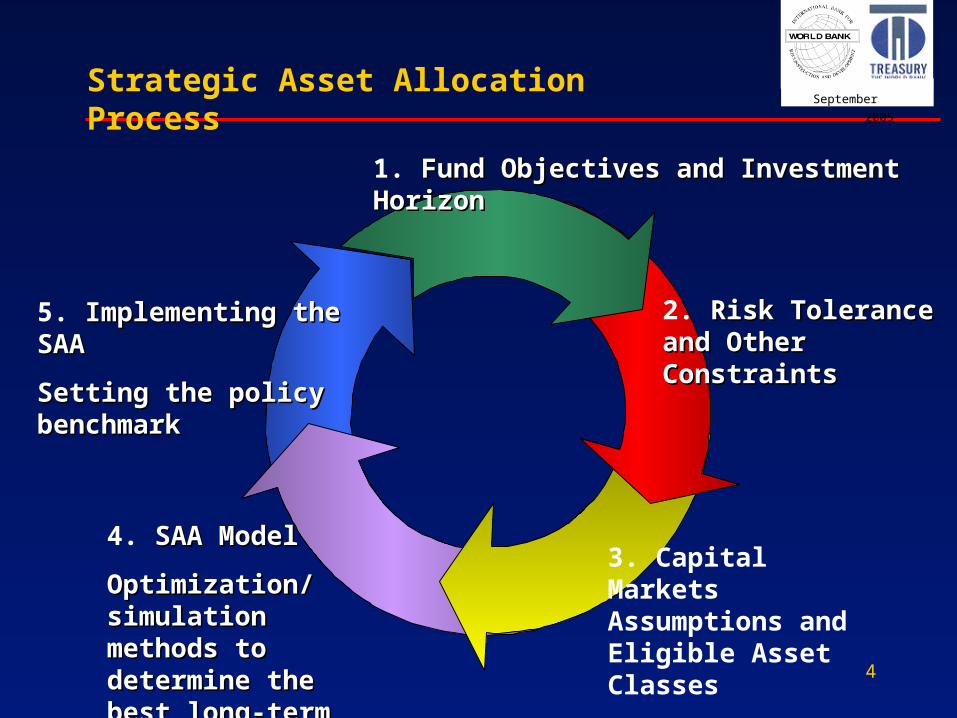

What is Strategic Asset Allocation?

4

September

2005

1. Fund Objectives and Investment HorizonFund Objectives and Investment Horizon

2. Risk Tolerance and Risk Tolerance and Other ConstraintsOther Constraints

3. Capital Markets Assumptions and Eligible Asset Classes

4. SAA ModelSAA Model

Optimization/Optimization/simulation simulation methods to methods to determine the determine the best long-term best long-term allocationallocation

5. Implementing the Implementing the SAASAA

Setting the policy Setting the policy benchmarkbenchmark

Strategic Asset Allocation Process

September

2005

5

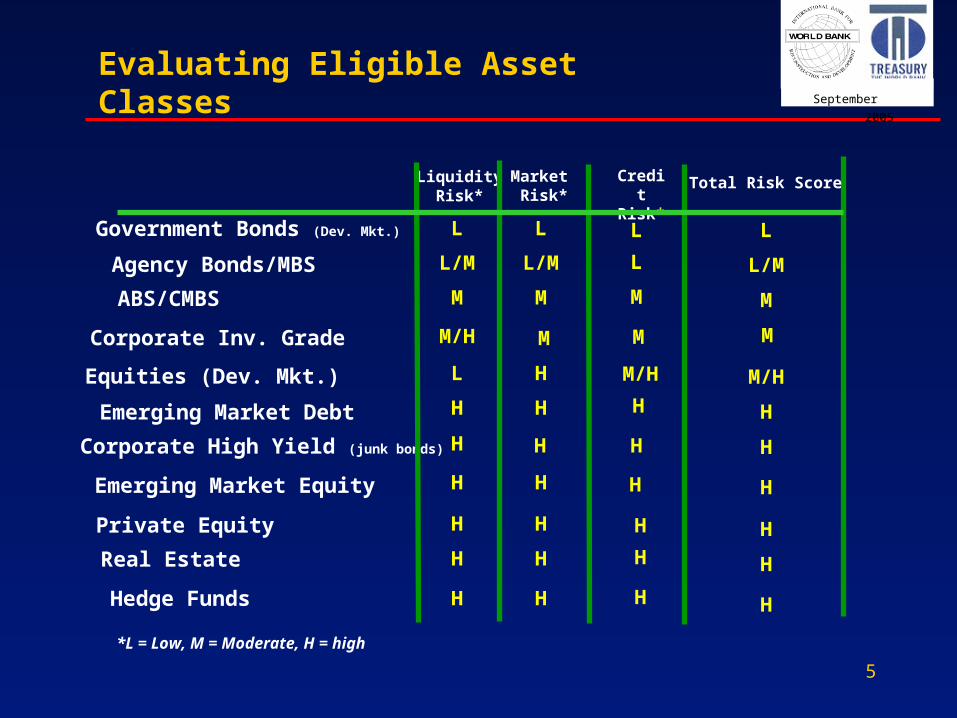

Evaluating Eligible Asset Classes

LiquidityRisk*

Corporate Inv. Grade

Agency Bonds/MBS

ABS/CMBS

Government Bonds (Dev. Mkt.)

Emerging Market Equity

Emerging Market Debt

Corporate High Yield (junk bonds)

Equities (Dev. Mkt.)

Hedge Funds

Private Equity

Real Estate

L

L/M

M

M/H

L

H

H

H

H

H

H

Market Risk*

L

L/M

M

M

H

H

H

H

H

H

Credit Risk*

Total Risk Score

L

L/M

M

M

M/H

H

H

H

H

H

H

*L = Low, M = Moderate, H = high

H

L

L

M

M

M/H

H

H

H

H

H

H

6

September

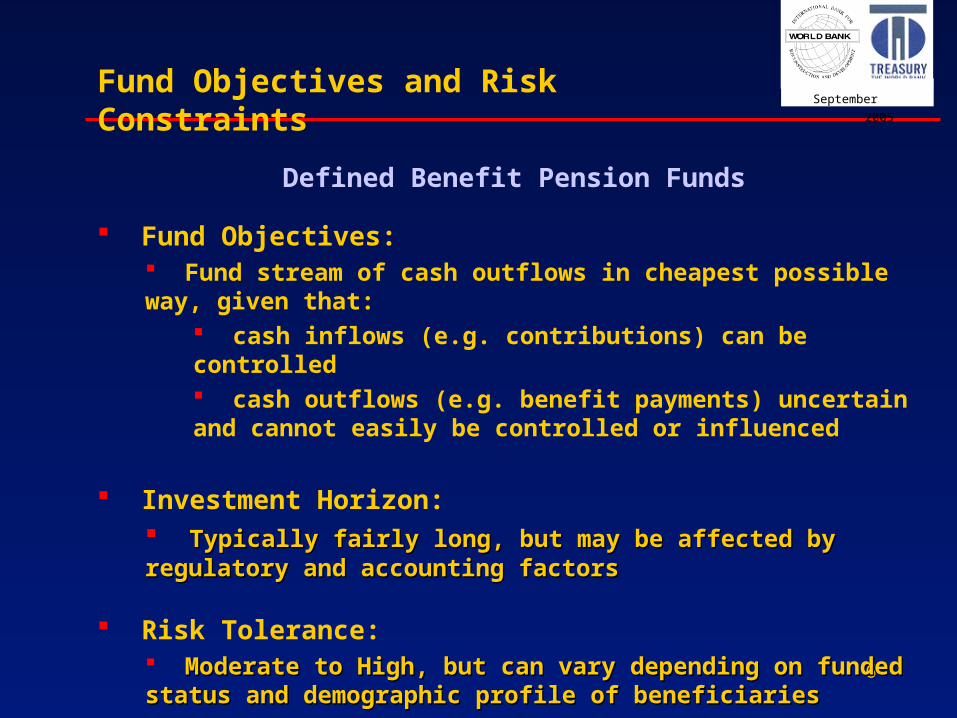

2005Fund Objectives and Risk Constraints

Defined Benefit Pension Funds

Fund Objectives: Fund stream of cash outflows in cheapest possible way, given that:

cash inflows (e.g. contributions) can be controlled cash outflows (e.g. benefit payments) uncertain and cannot easily be controlled or influenced

Investment Horizon: Typically fairly long, but may be affected by regulatory and Typically fairly long, but may be affected by regulatory and accounting factorsaccounting factors

Risk Tolerance:

Moderate to High, but can vary depending on funded status and Moderate to High, but can vary depending on funded status and demographic profile of beneficiariesdemographic profile of beneficiaries

7

September

2005Fund Objectives and Risk Constraints

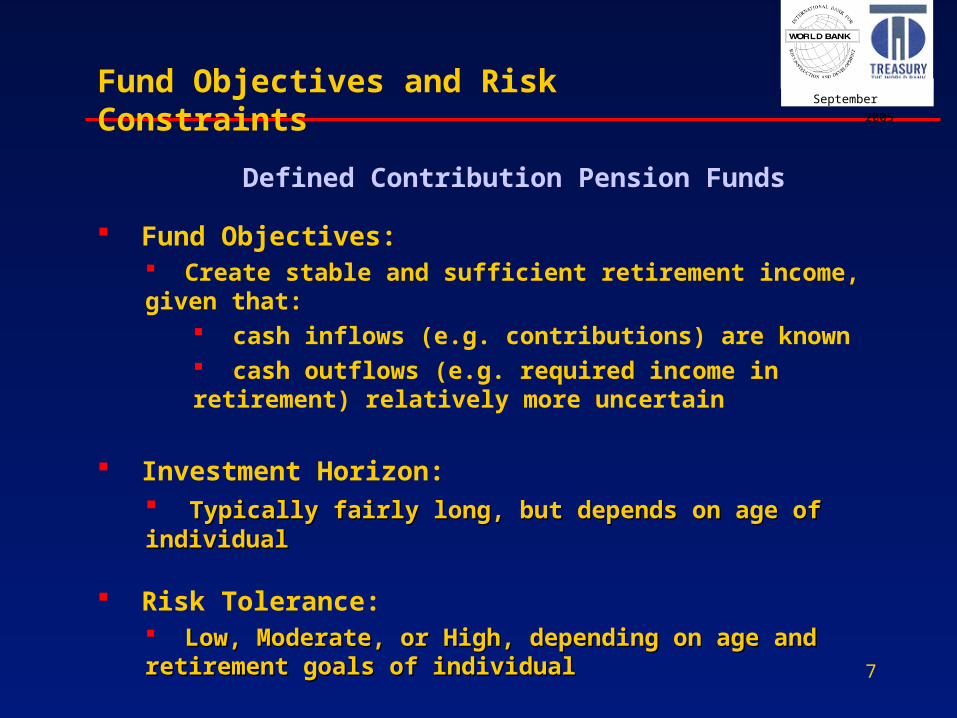

Defined Contribution Pension Funds

Fund Objectives: Create stable and sufficient retirement income, given that:

cash inflows (e.g. contributions) are known cash outflows (e.g. required income in retirement) relatively more uncertain

Investment Horizon: Typically fairly long, but depends on age of individualTypically fairly long, but depends on age of individual

Risk Tolerance:

Low, Moderate, or High, depending on age and retirement goals of Low, Moderate, or High, depending on age and retirement goals of individualindividual

8

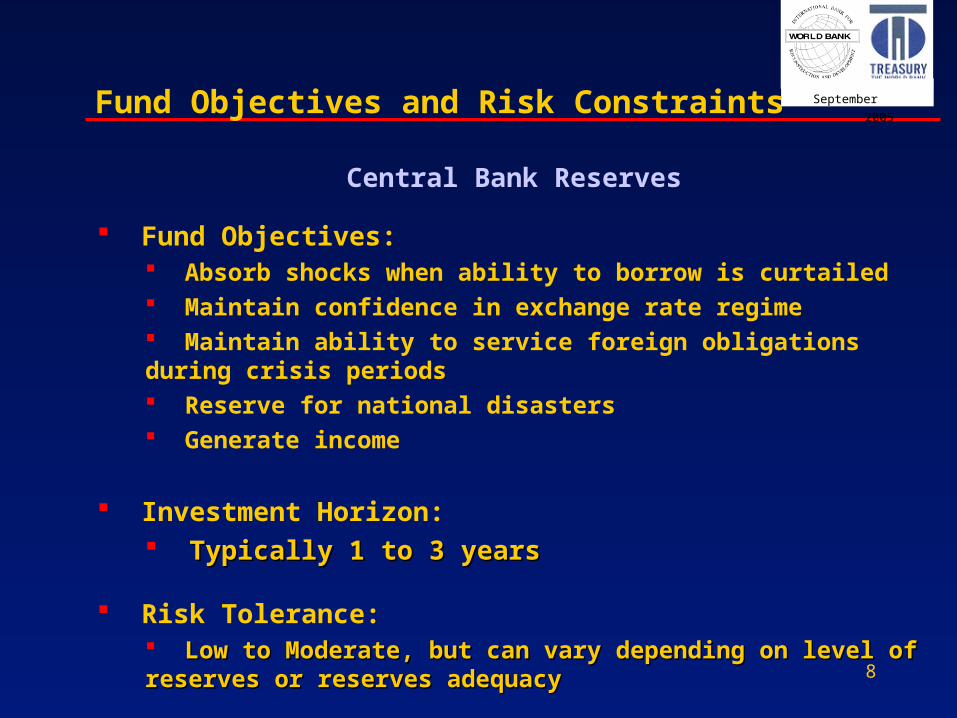

September

2005Fund Objectives and Risk Constraints

Central Bank Reserves

Fund Objectives: Absorb shocks when ability to borrow is curtailed Maintain confidence in exchange rate regime Maintain ability to service foreign obligations during crisis periods Reserve for national disasters Generate income

Investment Horizon: Typically 1 to 3 yearsTypically 1 to 3 years

Risk Tolerance:

Low to Moderate, but can vary depending on level of reserves or Low to Moderate, but can vary depending on level of reserves or reserves adequacyreserves adequacy

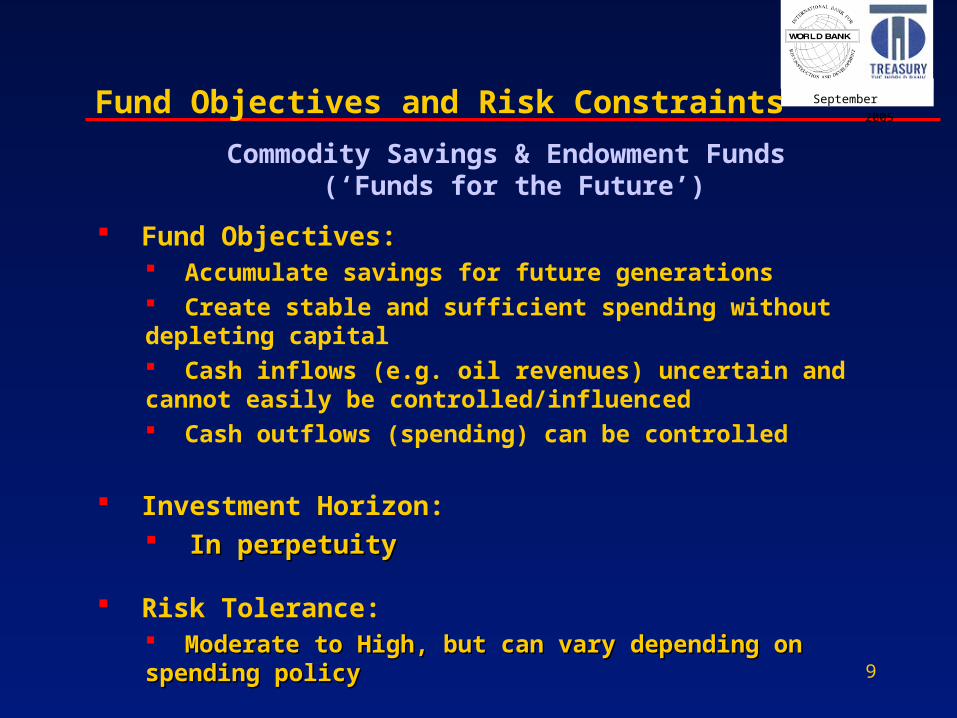

9

September

2005Fund Objectives and Risk Constraints

Commodity Savings & Endowment Funds (‘Funds for the Future’)

Fund Objectives: Accumulate savings for future generations Create stable and sufficient spending without depleting capital Cash inflows (e.g. oil revenues) uncertain and cannot easily be controlled/influenced Cash outflows (spending) can be controlled

Investment Horizon: In perpetuityIn perpetuity

Risk Tolerance:

Moderate to High, but can vary depending on spending policyModerate to High, but can vary depending on spending policy

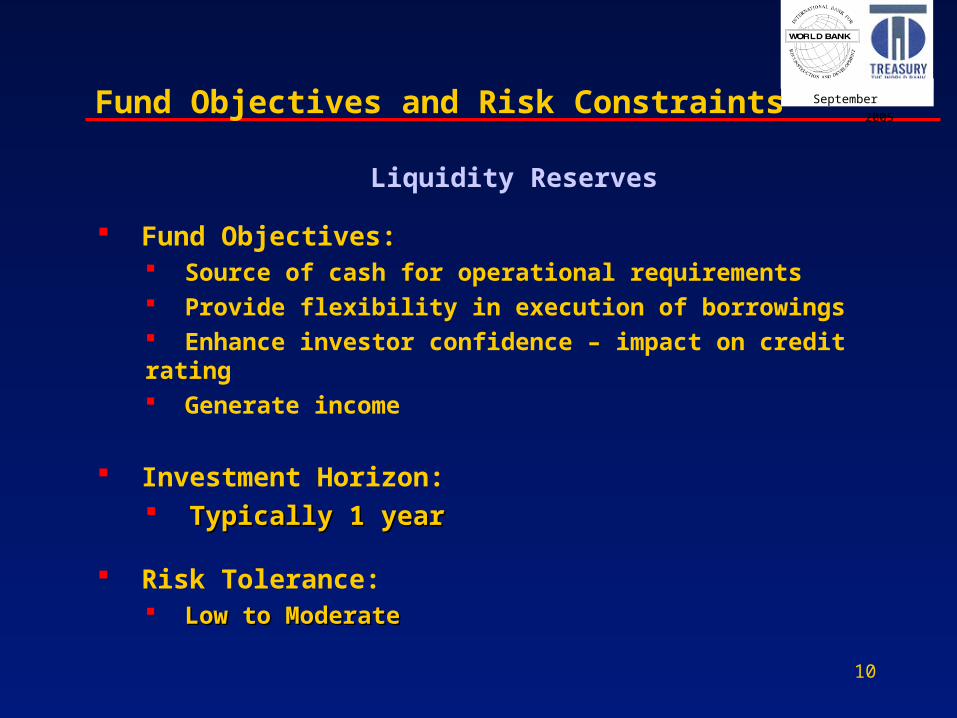

10

September

2005Fund Objectives and Risk Constraints

Liquidity Reserves

Fund Objectives: Source of cash for operational requirements Provide flexibility in execution of borrowings Enhance investor confidence – impact on credit rating Generate income

Investment Horizon: Typically 1 yearTypically 1 year

Risk Tolerance:

Low to ModerateLow to Moderate

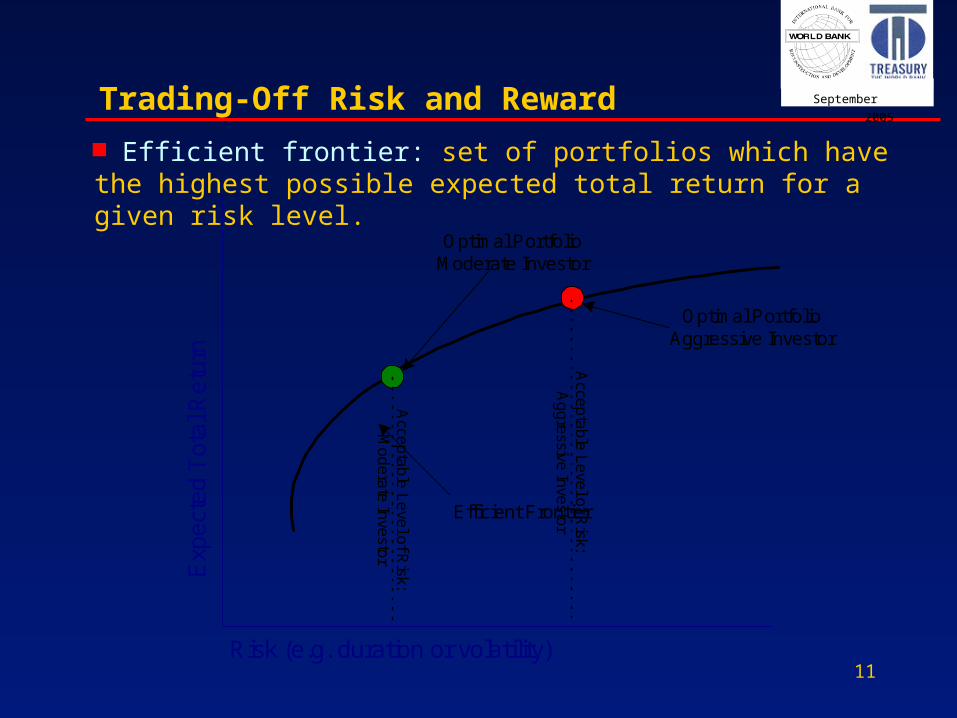

11

September

2005

Exp

ecte

d T

otal

Ret

urn

Risk (e.g. duration or volatility)

Efficient Frontier

Optimal PortfolioModerate Investor

Optimal PortfolioAggressive Investor

Acce

pta

ble

Le

vel o

f Risk:

Ag

gressive

Investor

Acce

pta

ble

Le

vel o

f Risk:

Mo

de

rate

Inve

stor

Trading-Off Risk and Reward

Efficient frontier: set of portfolios which have the highest possible expected total return for a given risk level.

12

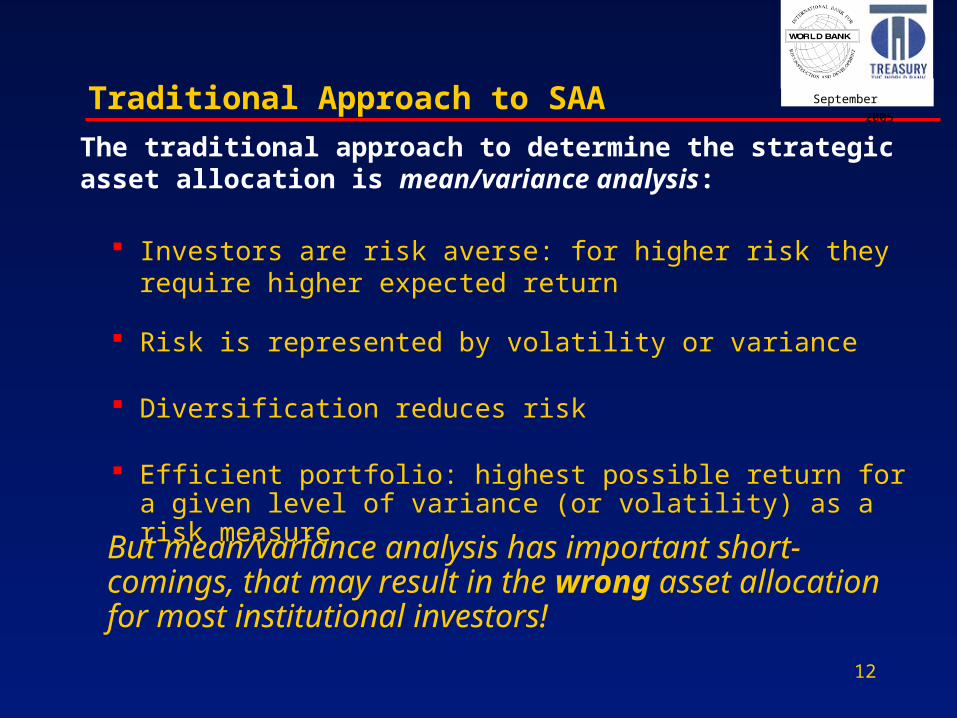

September

2005Traditional Approach to SAA

Investors are risk averse: for higher risk they require higher expected return

Risk is represented by volatility or variance

Diversification reduces risk

Efficient portfolio: highest possible return for a given level of variance (or volatility) as a risk measure

The traditional approach to determine the strategic asset allocation is mean/variance analysis:

But mean/variance analysis has important short-comings, that may result in the wrong asset allocation for most institutional investors!

13

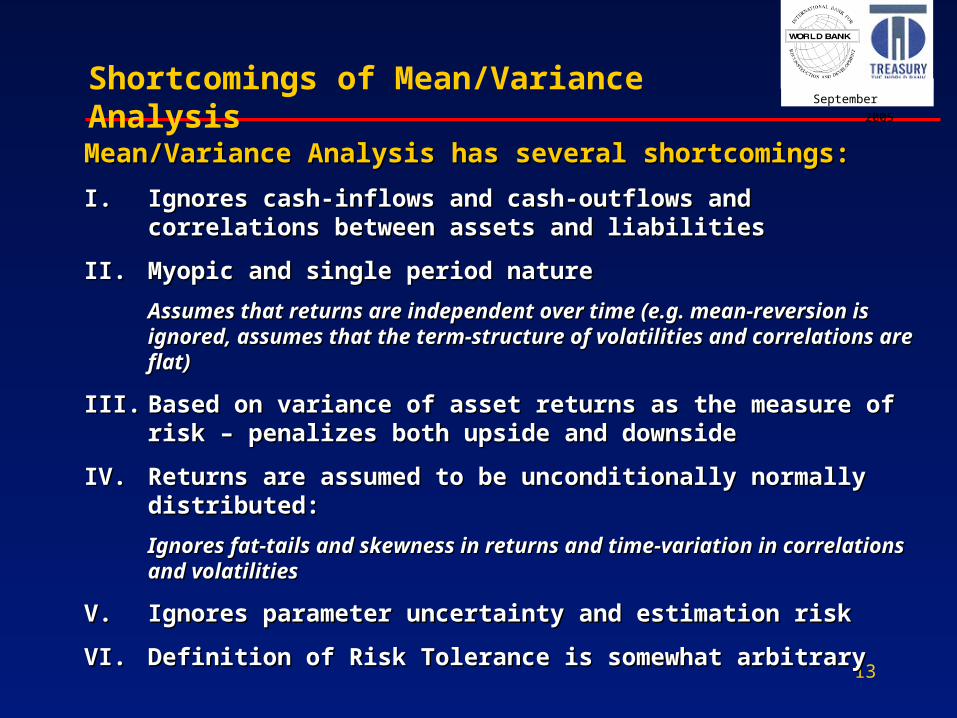

September

2005Shortcomings of Mean/Variance Analysis

Mean/Variance Analysis has several shortcomings:Mean/Variance Analysis has several shortcomings:

I.I. Ignores cash-inflows and cash-outflows and correlations between Ignores cash-inflows and cash-outflows and correlations between assets and liabilitiesassets and liabilities

II.II. Myopic and single period natureMyopic and single period nature

Assumes that returns are independent over time (e.g. mean-reversion is Assumes that returns are independent over time (e.g. mean-reversion is ignored, assumes that the term-structure of volatilities and correlations are ignored, assumes that the term-structure of volatilities and correlations are flat)flat)

III.III. Based on variance of asset returns as the measure of risk – Based on variance of asset returns as the measure of risk – penalizes both upside and downsidepenalizes both upside and downside

IV.IV. Returns are assumed to be unconditionally normally distributed:Returns are assumed to be unconditionally normally distributed:

Ignores fat-tails and skewness in returns and time-variation in correlations Ignores fat-tails and skewness in returns and time-variation in correlations and volatilitiesand volatilities

V.V. Ignores parameter uncertainty and estimation riskIgnores parameter uncertainty and estimation risk

VI.VI. Definition of Risk Tolerance is somewhat arbitraryDefinition of Risk Tolerance is somewhat arbitrary

14

September

2005

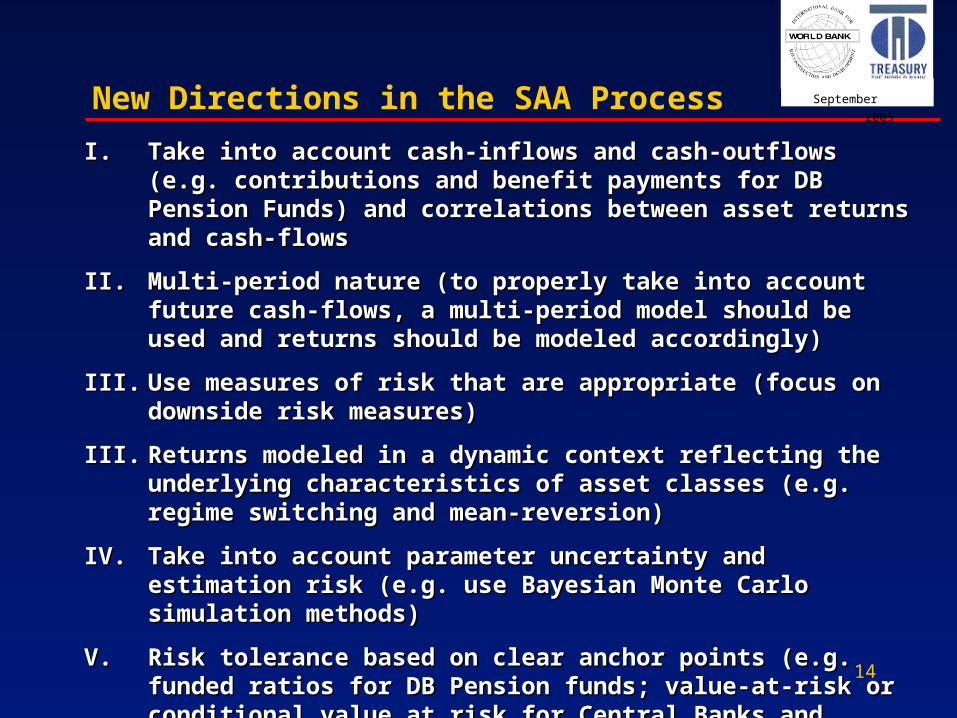

I.I. Take into account cash-inflows and cash-outflows (e.g. Take into account cash-inflows and cash-outflows (e.g. contributions and benefit payments for DB Pension Funds) and contributions and benefit payments for DB Pension Funds) and correlations between asset returns and cash-flowscorrelations between asset returns and cash-flows

II.II. Multi-period nature (to properly take into account future cash-Multi-period nature (to properly take into account future cash-flows, a multi-period model should be used and returns should be flows, a multi-period model should be used and returns should be modeled accordingly)modeled accordingly)

III.III. Use measures of risk that are appropriate (focus on downside risk Use measures of risk that are appropriate (focus on downside risk measures)measures)

III.III. Returns modeled in a dynamic context reflecting the underlying Returns modeled in a dynamic context reflecting the underlying characteristics of asset classes (e.g. regime switching and mean-characteristics of asset classes (e.g. regime switching and mean-reversion)reversion)

IV.IV. Take into account parameter uncertainty and estimation risk (e.g. Take into account parameter uncertainty and estimation risk (e.g. use Bayesian Monte Carlo simulation methods)use Bayesian Monte Carlo simulation methods)

V.V. Risk tolerance based on clear anchor points (e.g. funded ratios for Risk tolerance based on clear anchor points (e.g. funded ratios for DB Pension funds; value-at-risk or conditional value at risk for DB Pension funds; value-at-risk or conditional value at risk for Central Banks and liquidity reserves; spending-at-risk for Central Banks and liquidity reserves; spending-at-risk for endowments)endowments)

New Directions in the SAA Process

15

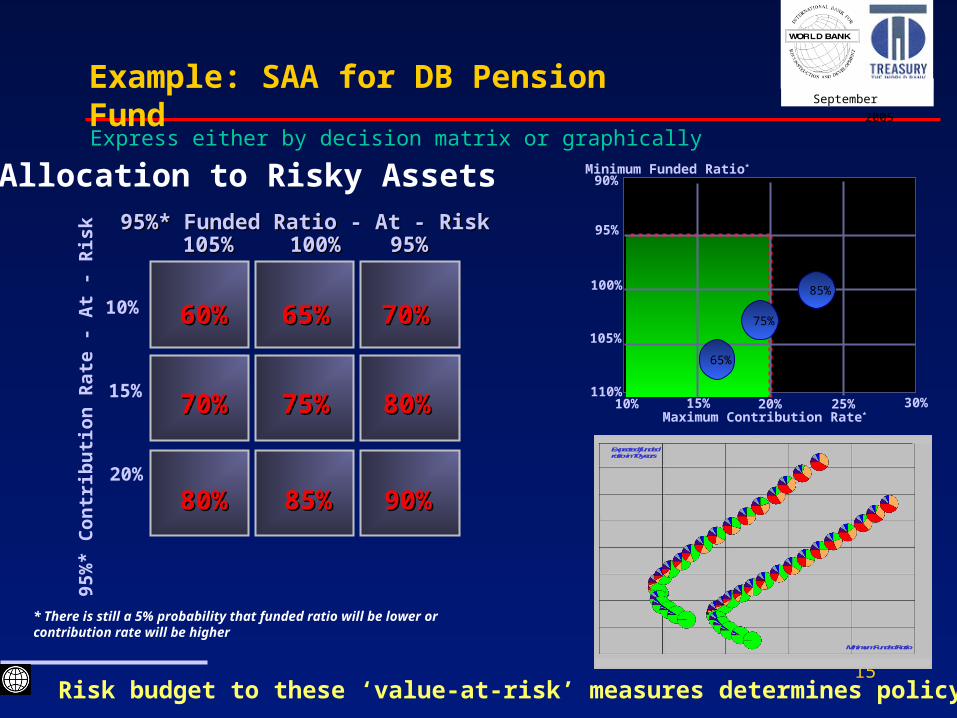

September

2005Example: SAA for DB Pension Fund

60%60% 70%70%65%65%

70%70% 80%80%75%75%

80%80% 90%90%85%85%

105%105% 95%95%100%100%95%* Funded Ratio - At - Risk95%* Funded Ratio - At - Risk

10%

20%

15%

95%

* C

on

trib

uti

on

Rat

e -

At

- R

isk

Risk budget to these ‘value-at-risk’ measures determines policy allocation

* There is still a 5% probability that funded ratio will be lower or contribution rate will be higher

Maximum Contribution Rate*

Minimum Funded Ratio*

110%10%

100%

90%

20% 30%15% 25%

105%

95%

65%

85%

75%

Express either by decision matrix or graphically

Expected funded ratio in 10 years

Minimum Funded Ratio

Expected funded ratio in 10 years

Minimum Funded Ratio

Allocation to Risky Assets

16

September

2005

Setting Realistic Expected Return Assumptions

Modeling Risk: Downside Risk Approaches

Modeling Future Returns

New Directions……

17

September

2005

Setting Realistic Return Expectations:

Asset allocation optimizations are extremely sensitive to expected return assumptions. How do we ensure realistic expectations?

• Should we use long-term historical returns?• Should we use equilibrium expected returns?• What are the drivers of actual returns?• Should expected returns be valuation-independent (‘no

view’ approach) or do valuations matter?• How often do you review expected return assumptions?

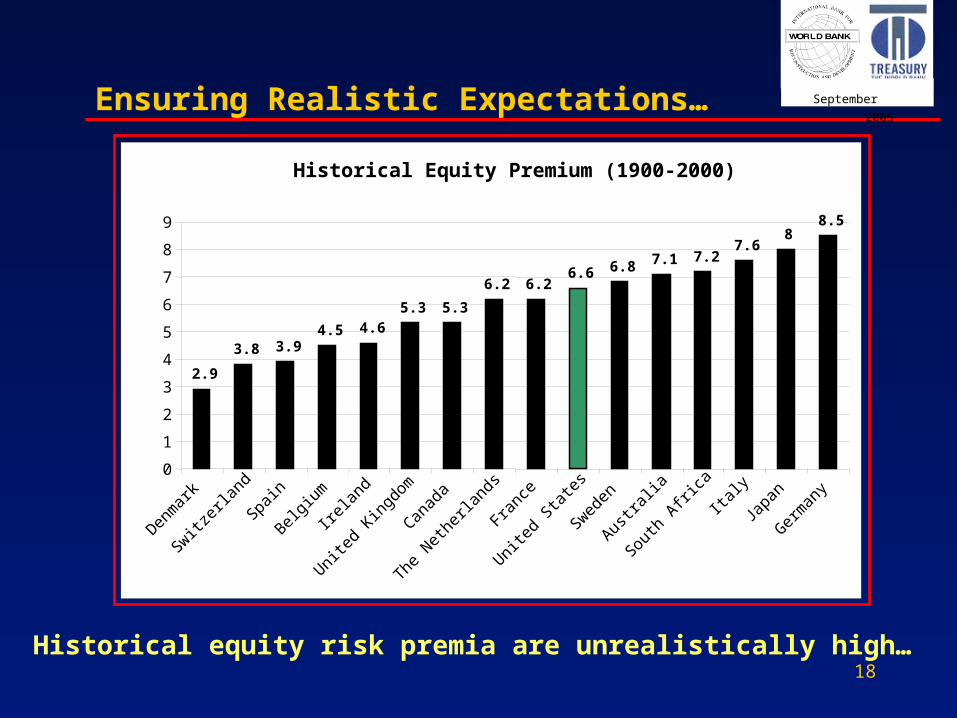

Ensuring Realistic Expectations…

18

September

2005

Historical Equity Premium (1900-2000)

2.9

3.8 3.94.5 4.6

5.3 5.3

6.2 6.26.6 6.8 7.1 7.2

7.68

8.5

0

1

2

3

4

5

6

7

8

9

Denm

ark

Switzer

land

Spain

Belgium

Irelan

d

United

King

dom

Canad

a

The N

ethe

rland

s

Franc

e

United

Sta

tes

Sweden

Austra

lia

South

Afri

caIta

ly

Japa

n

Germ

any

Historical equity risk premia are unrealistically high…

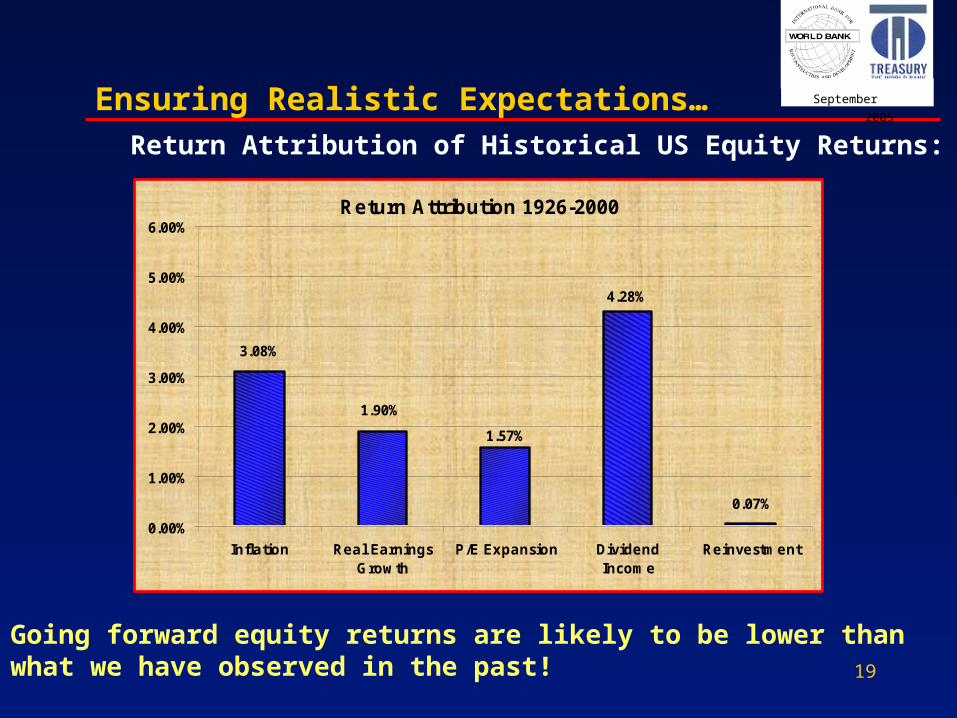

Ensuring Realistic Expectations…

19

September

2005

Return Attribution 1926-2000

3.08%

1.90%

1.57%

4.28%

0.07%

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

Inflation Real EarningsGrowth

P/E Expansion DividendIncome

Reinvestment

Ensuring Realistic Expectations…

Going forward equity returns are likely to be lower than what we have observed in the past!

Return Attribution of Historical US Equity Returns:

20

September

2005

Accurately capturing risks of investment portfolios:

Variance of asset returns penalizes both the upside and downside equally, but what if we care more about downside risk?

• Likelihood versus magnitude of losses• Risk at the end of the investment horizon versus risk

during the investment horizon

Modeling Risk

21

September

2005

Risk of 10 Percent Loss: 20% Probability

75

80

85

90

95

100

105

110

115

120

0 1 2 3 4

Risk of 10 Percent Loss: 20% Probability

75

80

85

90

95

100

105

110

115

120

0 1 2 3 4

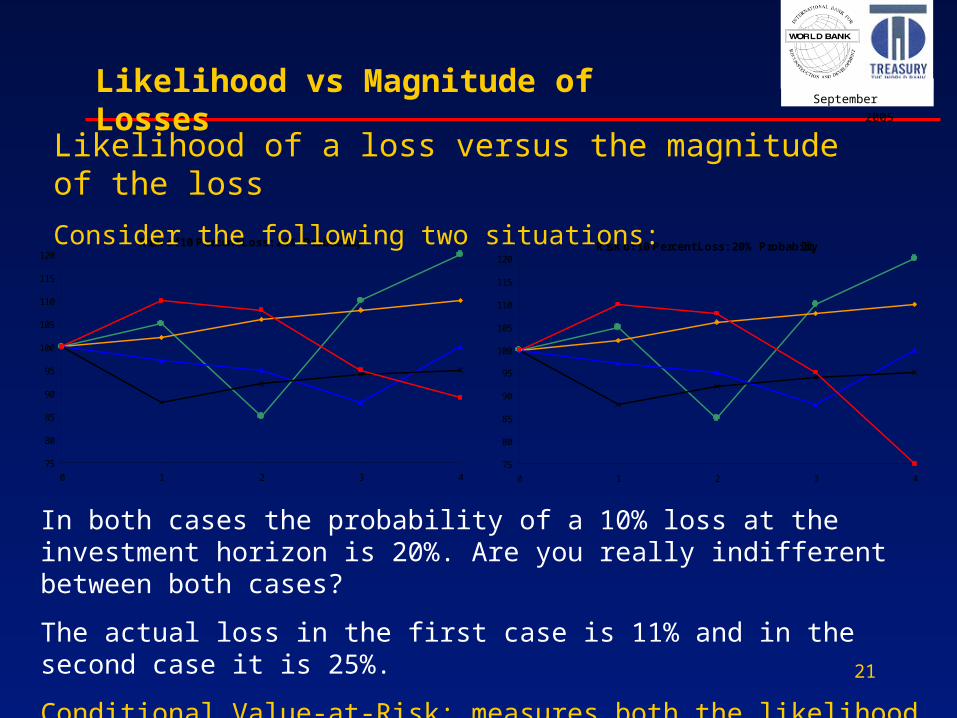

Likelihood of a loss versus the magnitude of the loss

Consider the following two situations:

In both cases the probability of a 10% loss at the investment horizon is 20%. Are you really indifferent between both cases?

The actual loss in the first case is 11% and in the second case it is 25%.

Conditional Value-at-Risk: measures both the likelihood and the magnitude of losses

Likelihood vs Magnitude of Losses

22

September

2005

Risk of 10 Percent Loss: Ending Wealth versus Interim Wealth

75

80

85

90

95

100

105

110

115

120

0 1 2 3 4

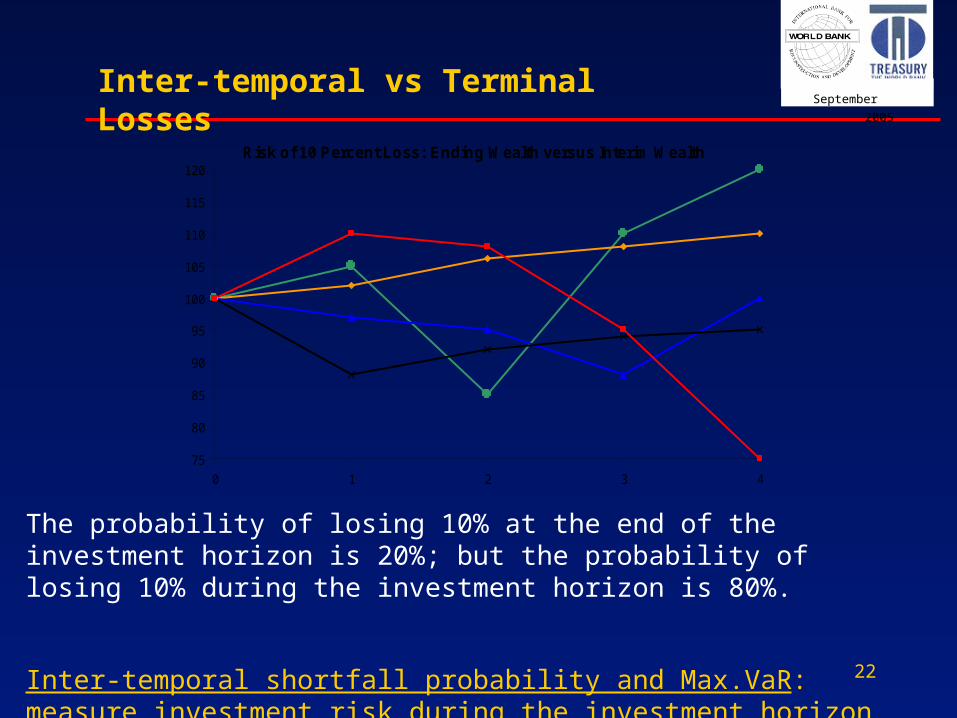

The probability of losing 10% at the end of the investment horizon is 20%; but the probability of losing 10% during the investment horizon is 80%.

Inter-temporal shortfall probability and Max.VaR: measure investment risk during the investment horizon and not only at the end

Inter-temporal vs Terminal Losses

23

September

2005

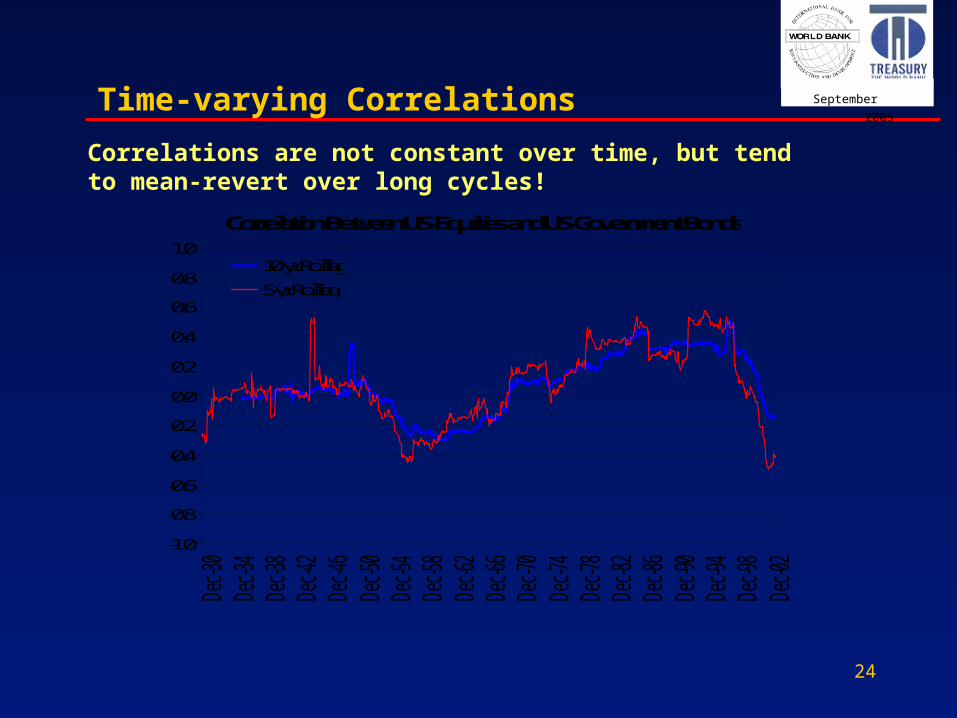

Modeling the dynamics of asset returns

How do we realistically model the dynamics and characteristics of asset returns?

Key Questions:

I. What distribution for returns do we use?normal, lognormal, fat-tailed and skewed distribution, extreme value theory

II. Do we assume constant or time-varying parameters?

III. How do we deal with parameter uncertainty, length of the sample period, and parameter mis-estimation?

Modeling the Future

24

September

2005

Correlation Between US Equities and US Government Bonds

-1.0

-0.8

-0.6

-0.4

-0.2

0.0

0.2

0.4

0.6

0.8

1.0

Dec

-30

Dec

-34

Dec

-38

Dec

-42

Dec

-46

Dec

-50

Dec

-54

Dec

-58

Dec

-62

Dec

-66

Dec

-70

Dec

-74

Dec

-78

Dec

-82

Dec

-86

Dec

-90

Dec

-94

Dec

-98

Dec

-02

10-yr Rolling

5-yr Rolling

Correlations are not constant over time, but tend to mean-revert over long cycles!

Time-varying Correlations

25

September

2005

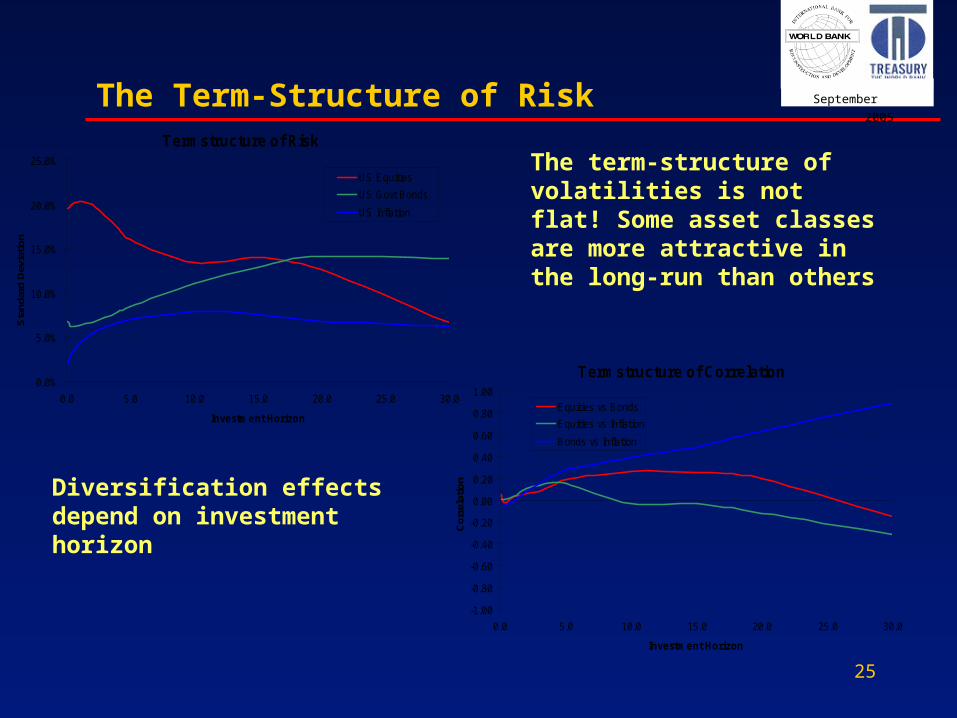

Termstructure of Risk

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

0.0 5.0 10.0 15.0 20.0 25.0 30.0

Investment Horizon

Sta

ndar

d D

evia

tion

US Equities

US Govt Bonds

US Inflation

Termstructure of Correlation

-1.00

-0.80

-0.60

-0.40

-0.20

0.00

0.20

0.40

0.60

0.80

1.00

0.0 5.0 10.0 15.0 20.0 25.0 30.0

Investment Horizon

Co

rrel

atio

n

Equities vs Bonds

Equities vs Inflation

Bonds vs Inflation

The term-structure of volatilities is not flat! Some asset classes are more attractive in the long-run than others

Diversification effects depend on investment horizon

The Term-Structure of Risk

26

September

2005

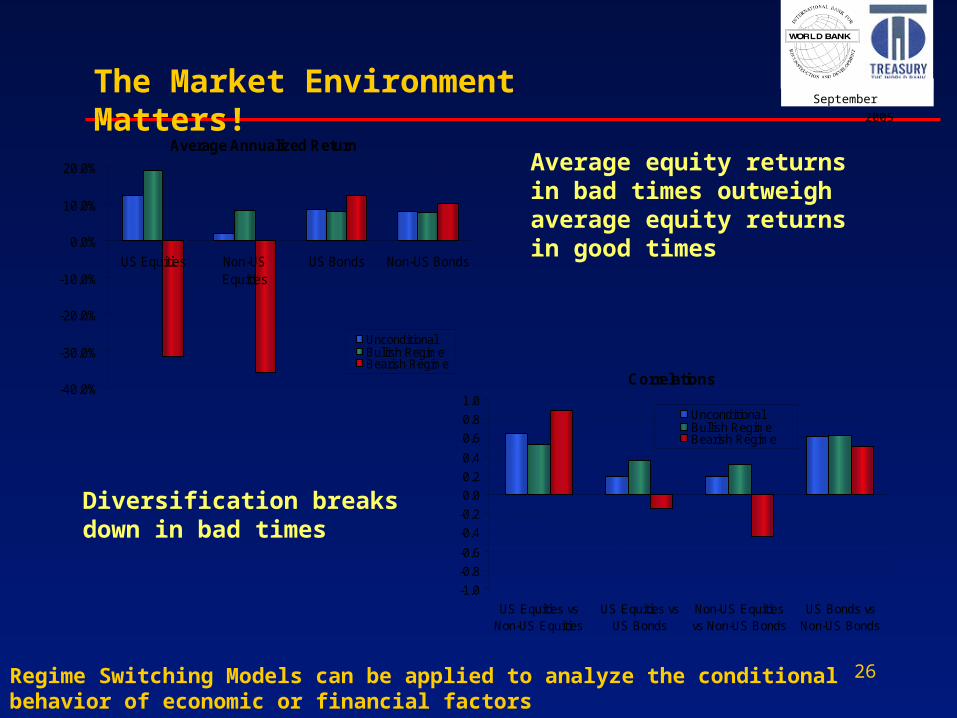

Average Annualized Return

-40.0%

-30.0%

-20.0%

-10.0%

0.0%

10.0%

20.0%

US Equities Non-USEquities

US Bonds Non-US Bonds

UnconditionalBullish RegimeBearish Regime

The Market Environment Matters!

Average equity returns in bad times outweigh average equity returns in good times

Correlations

-1.0

-0.8

-0.6

-0.4

-0.2

0.0

0.2

0.4

0.6

0.8

1.0

US Equities vsNon-US Equities

US Equities vsUS Bonds

Non-US Equitiesvs Non-US Bonds

US Bonds vsNon-US Bonds

UnconditionalBullish RegimeBearish Regime

Diversification breaks down in bad times

Regime Switching Models can be applied to analyze the conditional behavior of economic or financial factors