Embed Size (px)

Citation preview

Networks in Finance and Marketing I

Prof. Dr. Daning Hu Department of Informatics University of Zurich Nov 26th, 2012

2

Outline n Introduction: Networks in Finance n Stock Correlation Networks

n Stock Ownership Networks

n Board Director Networks

n Bank Networks

n Ref Book: The Network Challenge: Strategy, Profit, and Risk in an Interlinked World, Paul R. Kleindorfer, Yoram J Wind, Robert E. Gunther

Introduction: Networks in Finance n Networks that are based on relationships in Finance domain:

¨ Stock correlations ¨ Stock ownerships ¨ Board of Directors ¨ Inter-bank Market/Transactions/Payments ¨ NOT Network in economics (e.g., supply chain networks)

n The most complex system is human behavior! In financial markets, stock price movements are largely influenced by behaviors of different trading parties (human beings).

n Econophysics aims to understand the trading behaviors by modeling the price statistical properties of a stock through a model of agents trading it.

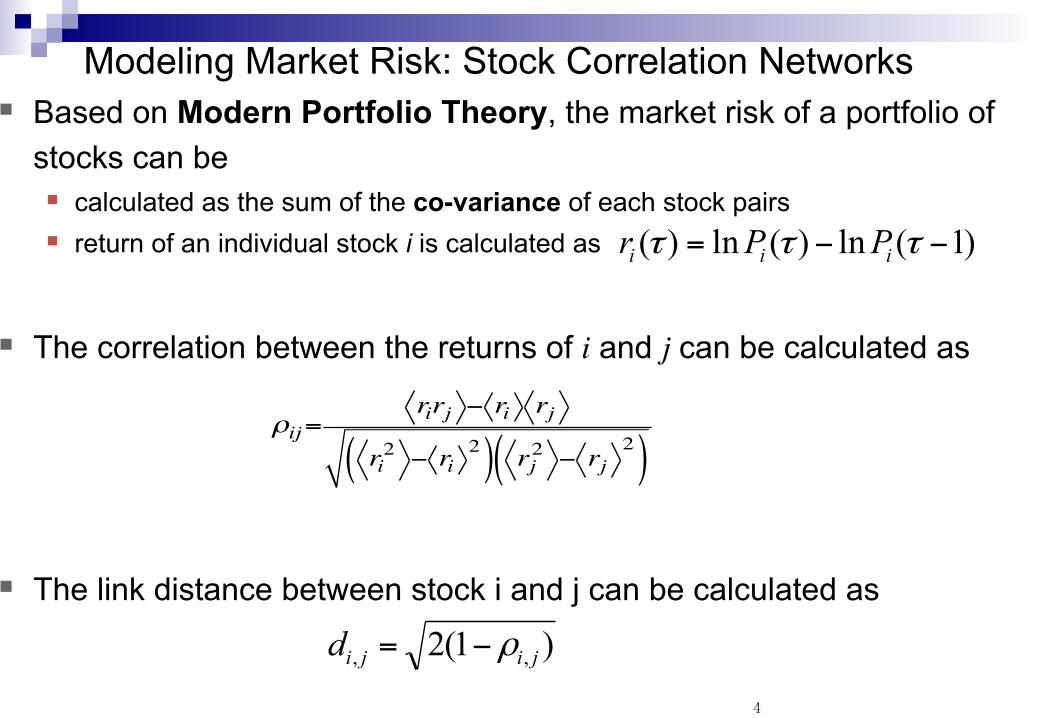

Modeling Market Risk: Stock Correlation Networks § Based on Modern Portfolio Theory, the market risk of a portfolio of

stocks can be § calculated as the sum of the co-variance of each stock pairs § return of an individual stock i is calculated as

§ The correlation between the returns of i and j can be calculated as

§ The link distance between stock i and j can be calculated as

4

ρij=rirj − ri rj

ri2 − ri

2( ) rj2 − rj

2( )

)1(ln)(ln)( −−= τττ iii PPr

)1(2 ,, jijid ρ−=

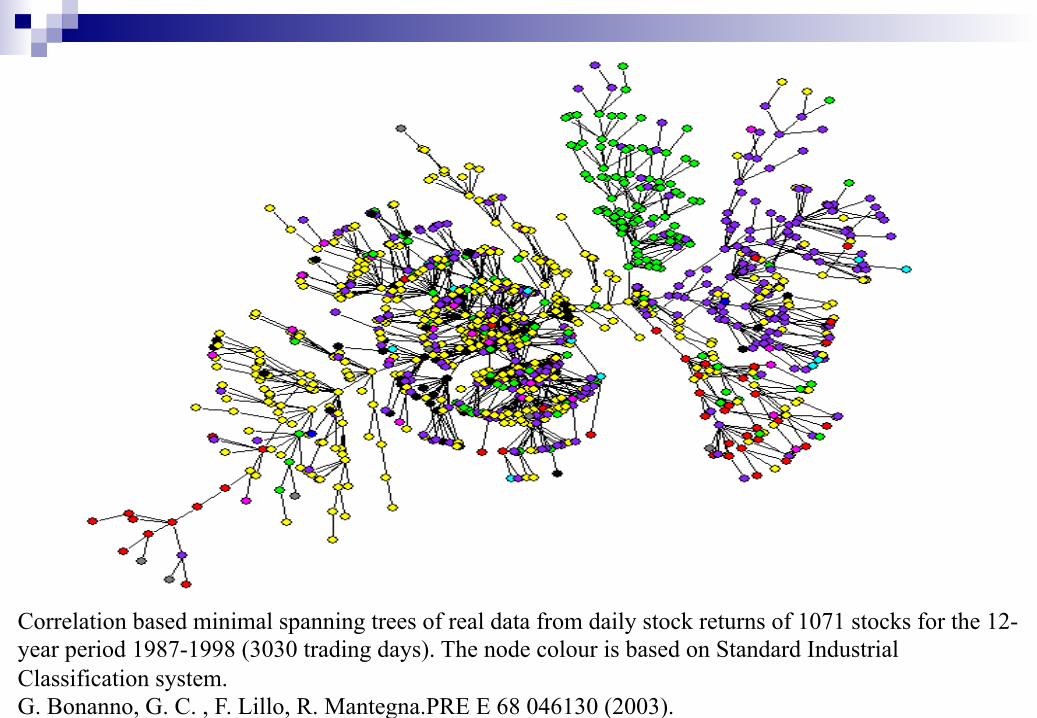

Correlation based minimal spanning trees of real data from daily stock returns of 1071 stocks for the 12-year period 1987-1998 (3030 trading days). The node colour is based on Standard Industrial Classification system. G. Bonanno, G. C. , F. Lillo, R. Mantegna.PRE E 68 046130 (2003).

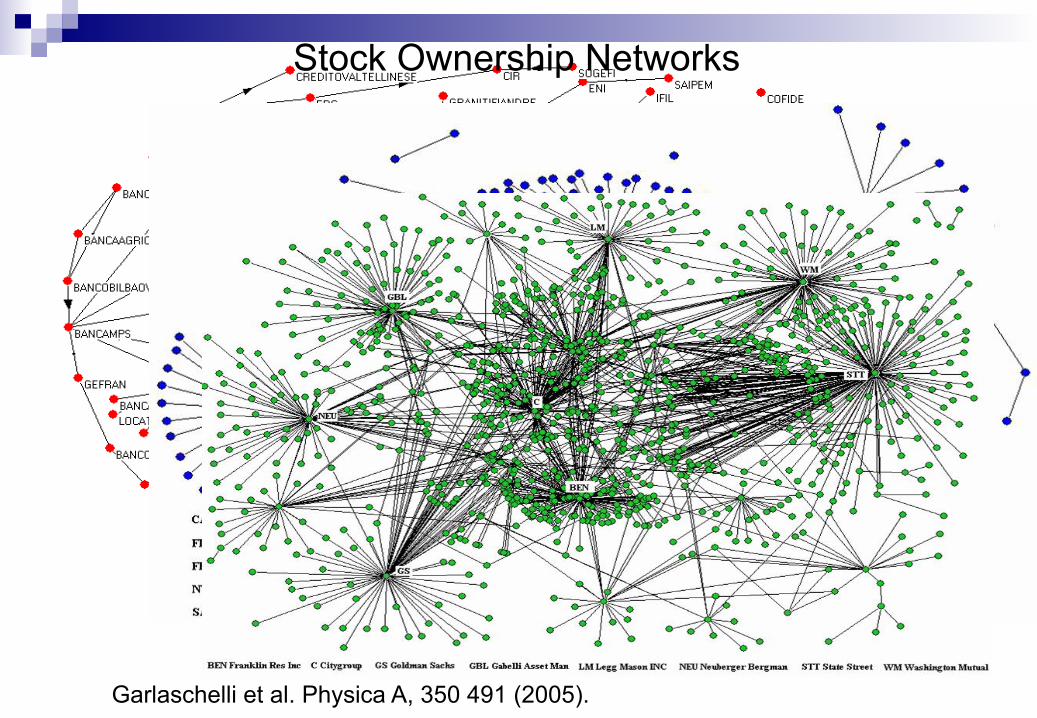

Garlaschelli et al. Physica A, 350 491 (2005).

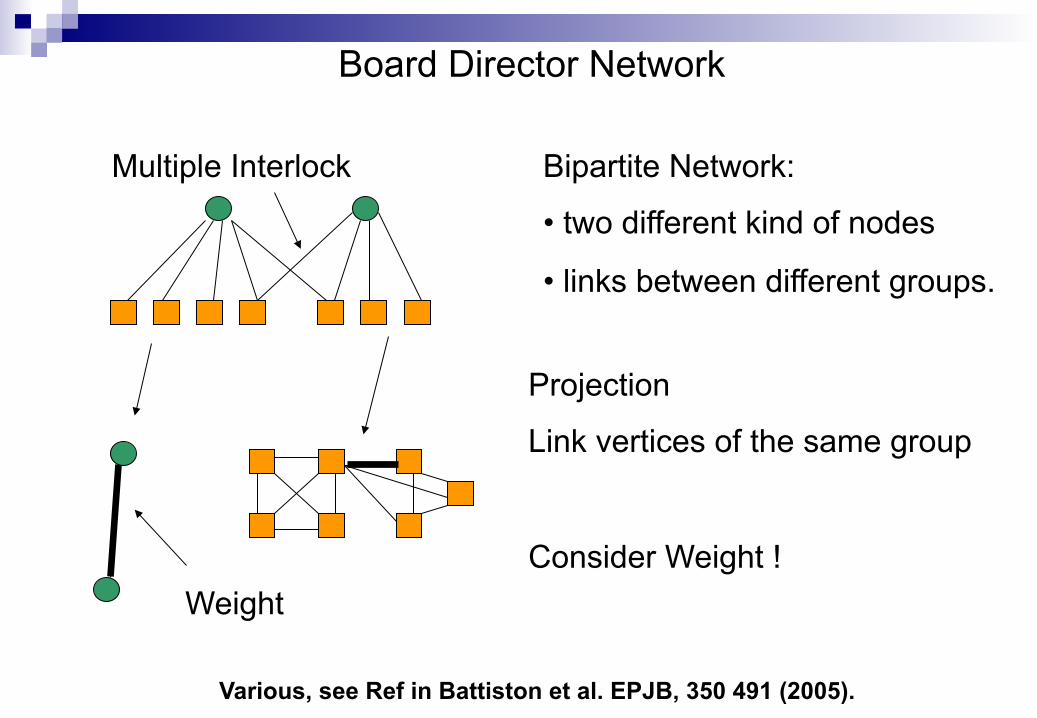

Stock Ownership Networks

Bipartite Network:

• two different kind of nodes

• links between different groups.

Projection

Link vertices of the same group

Consider Weight !

Multiple Interlock

Weight

Various, see Ref in Battiston et al. EPJB, 350 491 (2005).

Board Director Network

De Masi et al. In preparation.

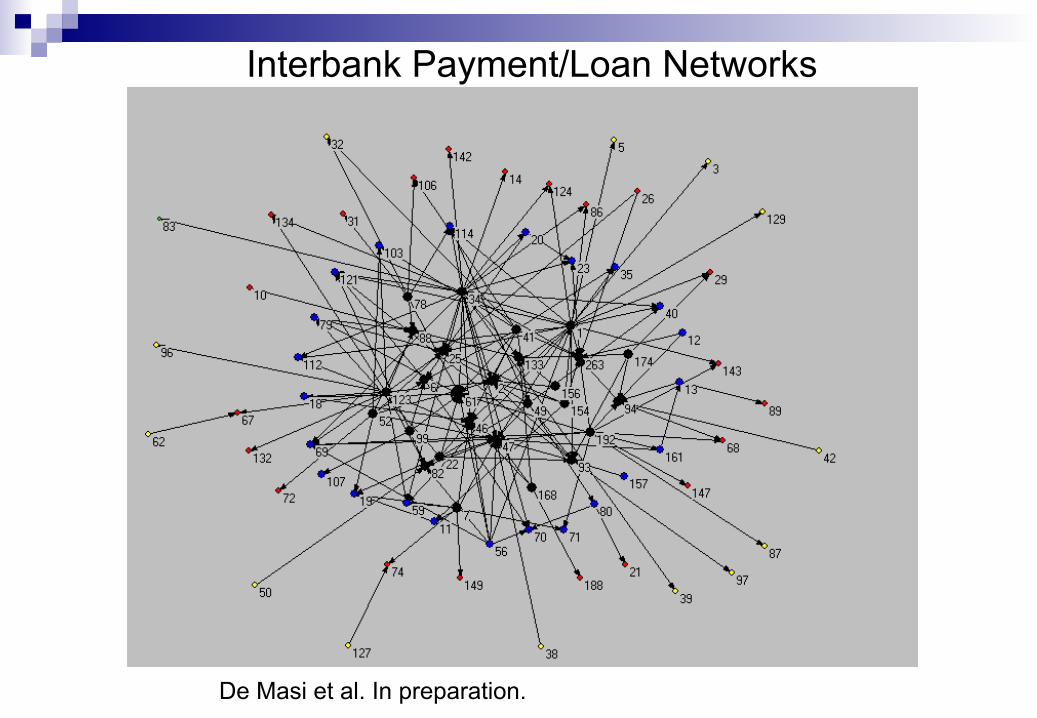

Interbank Payment/Loan Networks

Financial Network Analysis n Financial Networks Analysis can help

¨ In distinguishing behaviors of different markets

¨ In visualizing important features as the chain of control

¨ In testing the validity of market models

n Many of these financial networks are scale-free networks. Thus different network models can be tested against such empirical financial networks.

Case I: The Small-World of Investing n Social Networks on Information Transfer in Stock Market

¨ connections between mutual fund managers and corporate board members via shared education networks.

¨ academic institutions attended for both undergraduate and graduate degrees as our network measure

n The major findings are

¨ portfolio managers place larger bets on firms they are connected to through their network

¨ perform significantly better on these holdings relative to their non-connected holdings. (7.8% per year)

¨ positive returns concentrated on news announcements

Correlated risk exposures in banks’ financial asset portfolios:

Interbank payments A B C

X Z Y

Banks

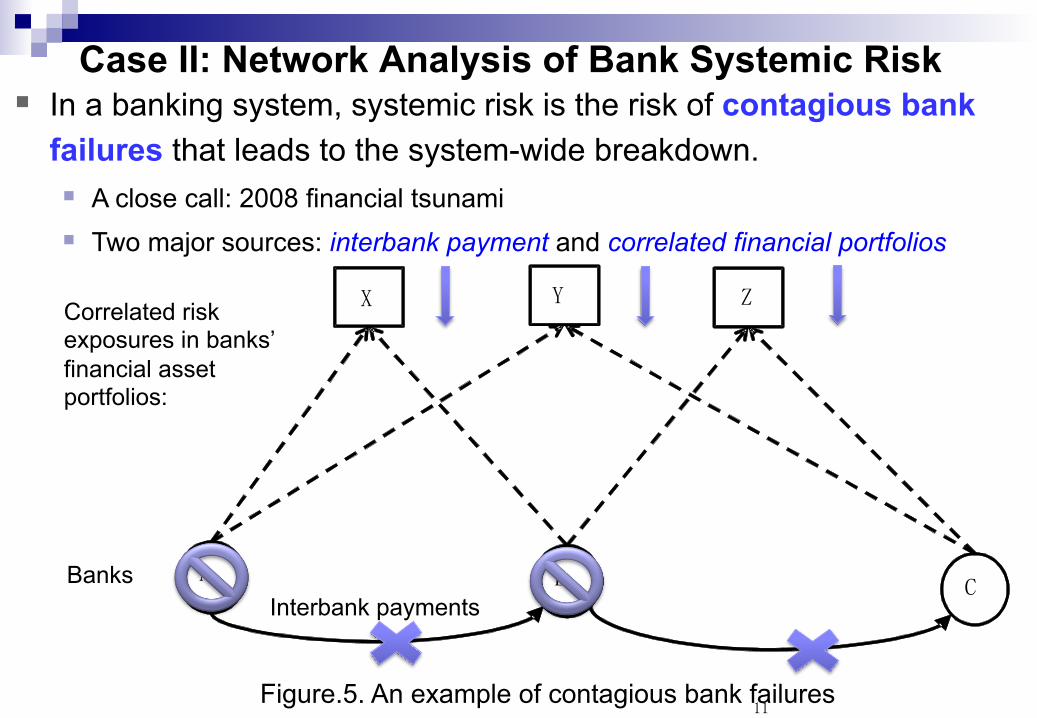

Case II: Network Analysis of Bank Systemic Risk

11

§ In a banking system, systemic risk is the risk of contagious bank failures that leads to the system-wide breakdown. § A close call: 2008 financial tsunami § Two major sources: interbank payment and correlated financial portfolios

Figure.5. An example of contagious bank failures

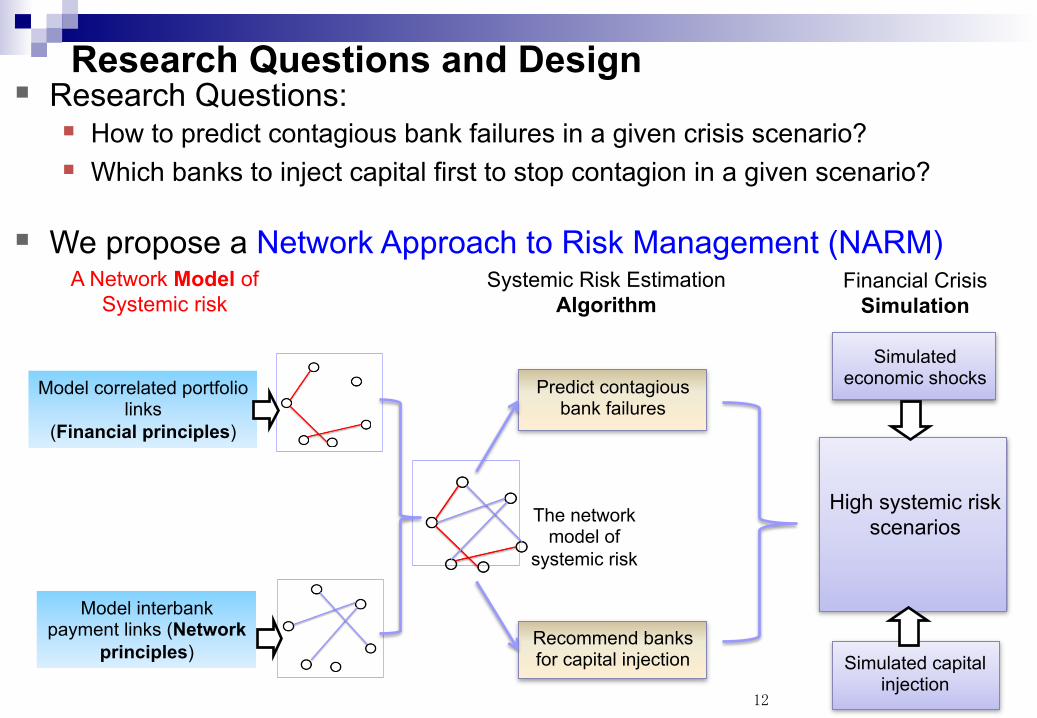

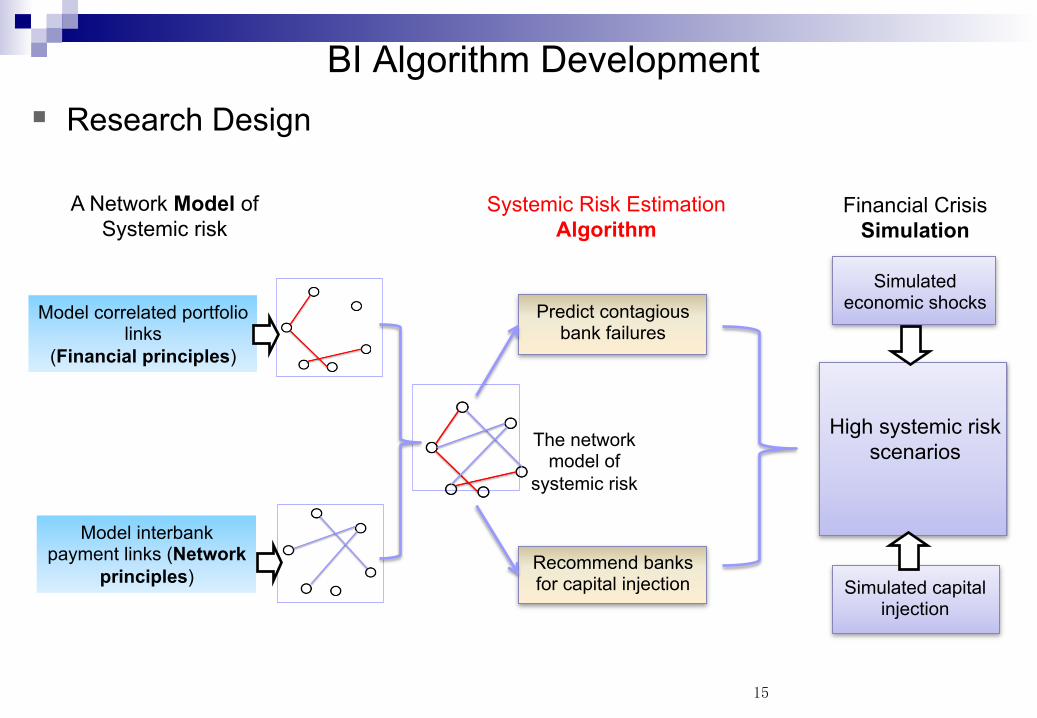

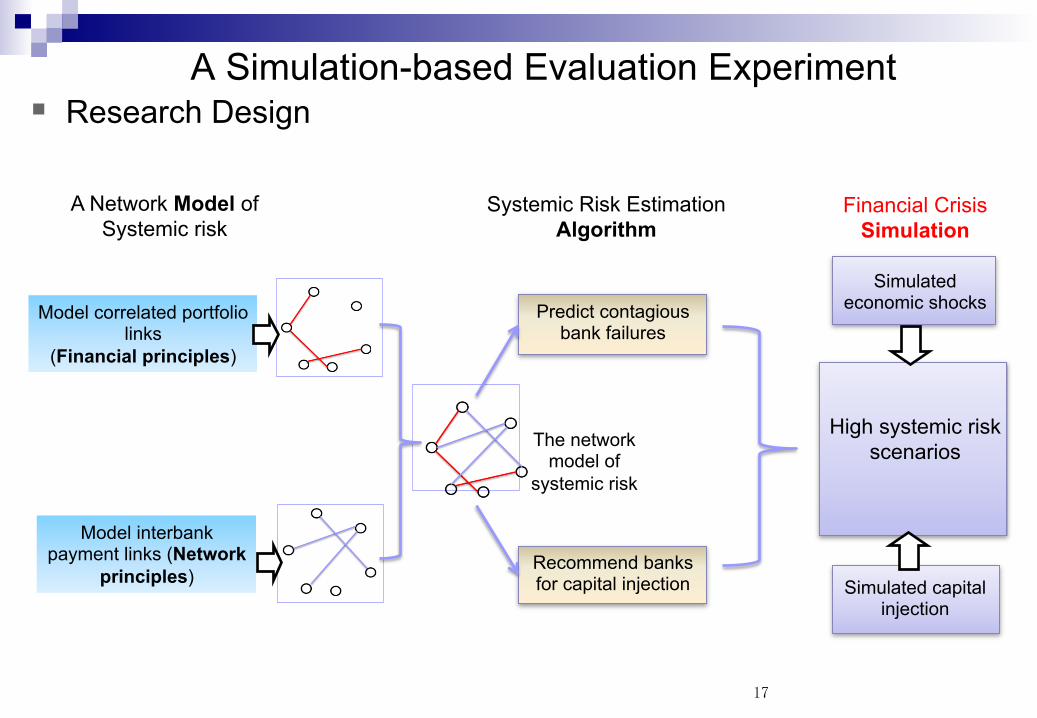

Research Questions and Design § Research Questions:

§ How to predict contagious bank failures in a given crisis scenario? § Which banks to inject capital first to stop contagion in a given scenario?

§ We propose a Network Approach to Risk Management (NARM)

12

A Network Model of Systemic risk

Systemic Risk Estimation Algorithm

Model correlated portfolio links

(Financial principles)

Model interbank payment links (Network

principles)

Financial Crisis Simulation

Simulated economic shocks

Simulated capital injection

High systemic risk scenarios

Predict contagious bank failures

Recommend banks for capital injection

The network model of

systemic risk

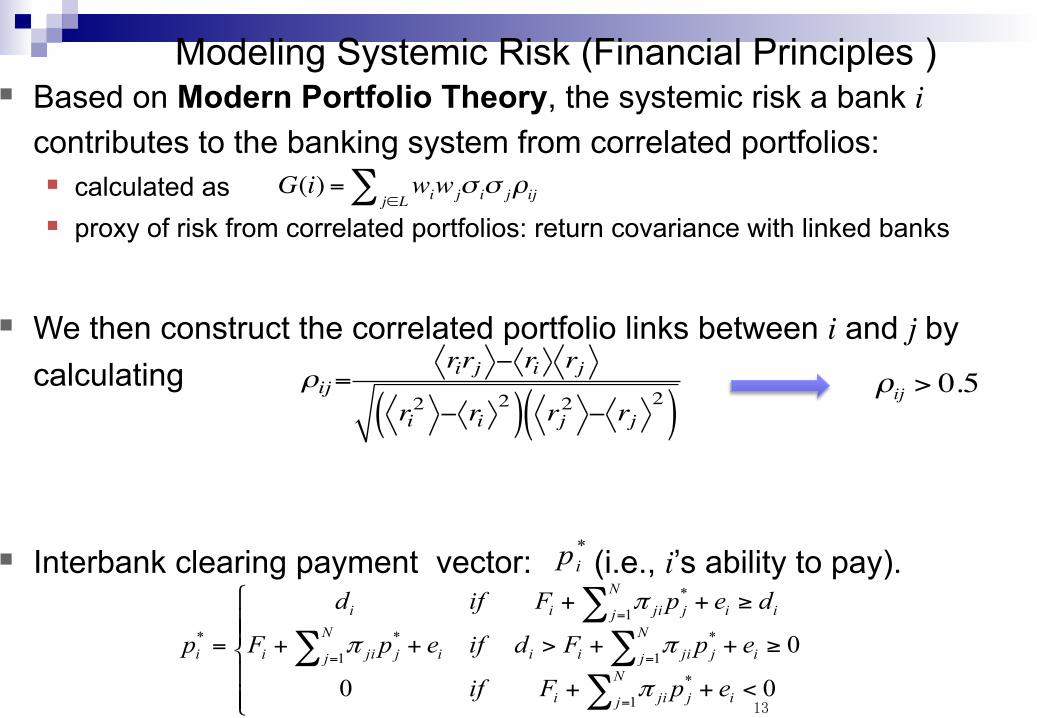

Modeling Systemic Risk (Financial Principles ) § Based on Modern Portfolio Theory, the systemic risk a bank i

contributes to the banking system from correlated portfolios: § calculated as § proxy of risk from correlated portfolios: return covariance with linked banks

§ We then construct the correlated portfolio links between i and j by calculating

§ Interbank clearing payment vector: (i.e., i’s ability to pay).

13

*ip

⎪⎪⎩

⎪⎪⎨

⎧

<++

≥++>++

≥++

=

∑∑∑

∑

=

==

=

N

j ijjii

N

j ijjiiiN

j ijjii

N

j iijjiii

i

epFif

epFdifepF

depFifd

p

1*

1*

1*

1*

*

00

0

π

ππ

π

G(i) = wiwjσ iσ jρijj∈L∑

ρij=rirj − ri rj

ri2 − ri

2( ) rj2 − rj

2( )ρij > 0.5

14

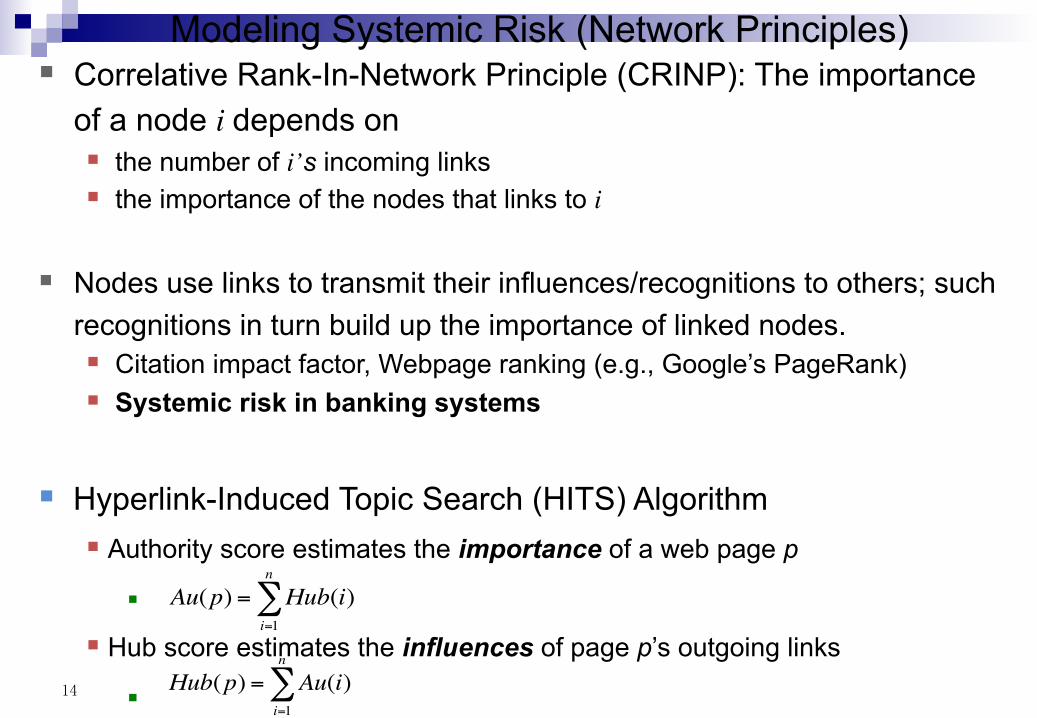

§ Correlative Rank-In-Network Principle (CRINP): The importance of a node i depends on § the number of i’s incoming links § the importance of the nodes that links to i

§ Nodes use links to transmit their influences/recognitions to others; such recognitions in turn build up the importance of linked nodes. § Citation impact factor, Webpage ranking (e.g., Google’s PageRank) § Systemic risk in banking systems

§ Hyperlink-Induced Topic Search (HITS) Algorithm § Authority score estimates the importance of a web page p

§

§ Hub score estimates the influences of page p’s outgoing links

§

Au(p) = Hub(i)i=1

n

∑

Hub(p) = Au(i)i=1

n

∑

Modeling Systemic Risk (Network Principles)

BI Algorithm Development

15

§ Research Design

15

A Network Model of Systemic risk

Systemic Risk Estimation Algorithm

Model correlated portfolio links

(Financial principles)

Model interbank payment links (Network

principles)

Financial Crisis Simulation

Simulated economic shocks

Simulated capital injection

High systemic risk scenarios

Predict contagious bank failures

Recommend banks for capital injection

The network model of

systemic risk

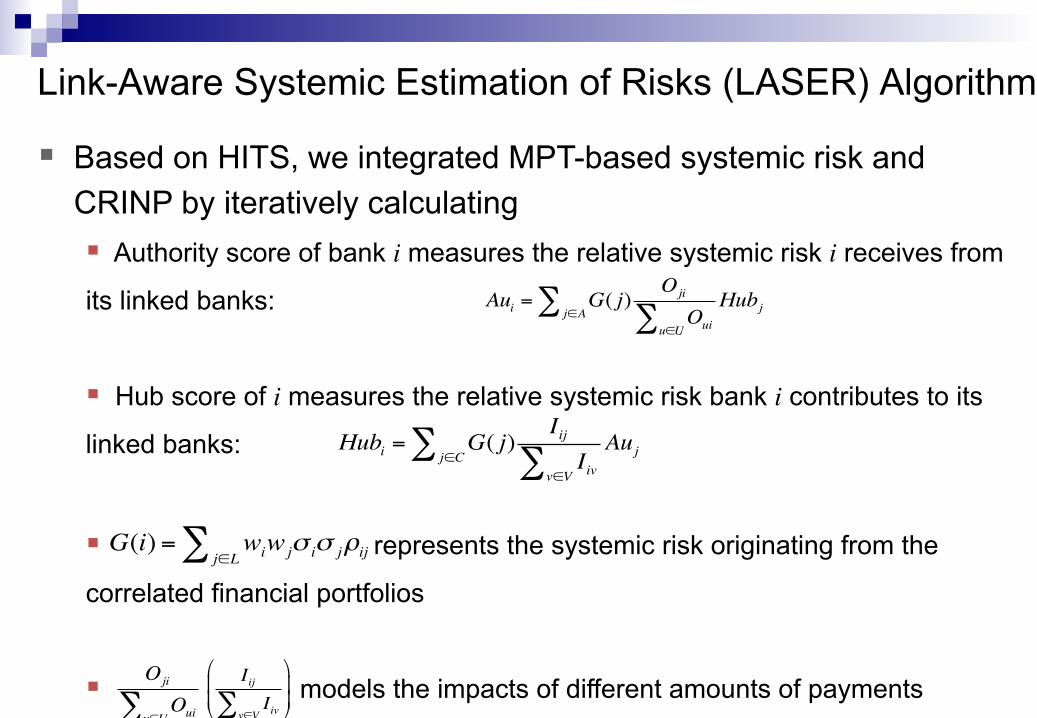

Link-Aware Systemic Estimation of Risks (LASER) Algorithm

16

§ Based on HITS, we integrated MPT-based systemic risk and CRINP by iteratively calculating § Authority score of bank i measures the relative systemic risk i receives from

its linked banks:

§ Hub score of i measures the relative systemic risk bank i contributes to its

linked banks:

§ represents the systemic risk originating from the

correlated financial portfolios

§ models the impacts of different amounts of payments

Aui = G( j)Oji

Ouiu∈U∑Hubjj∈A∑

Hubi = G( j)IijIivv∈V∑Aujj∈C∑

G(i) = wiwjσ iσ jρijj∈L∑

Oji

Ouiu∈U∑IijIivv∈V∑

#

$

%%

&

'

((

A Simulation-based Evaluation Experiment

17

§ Research Design

17

A Network Model of Systemic risk

Systemic Risk Estimation Algorithm

Model correlated portfolio links

(Financial principles)

Model interbank payment links (Network

principles)

Financial Crisis Simulation

Simulated economic shocks

Simulated capital injection

High systemic risk scenarios

Predict contagious bank failures

Recommend banks for capital injection

The network model of

systemic risk

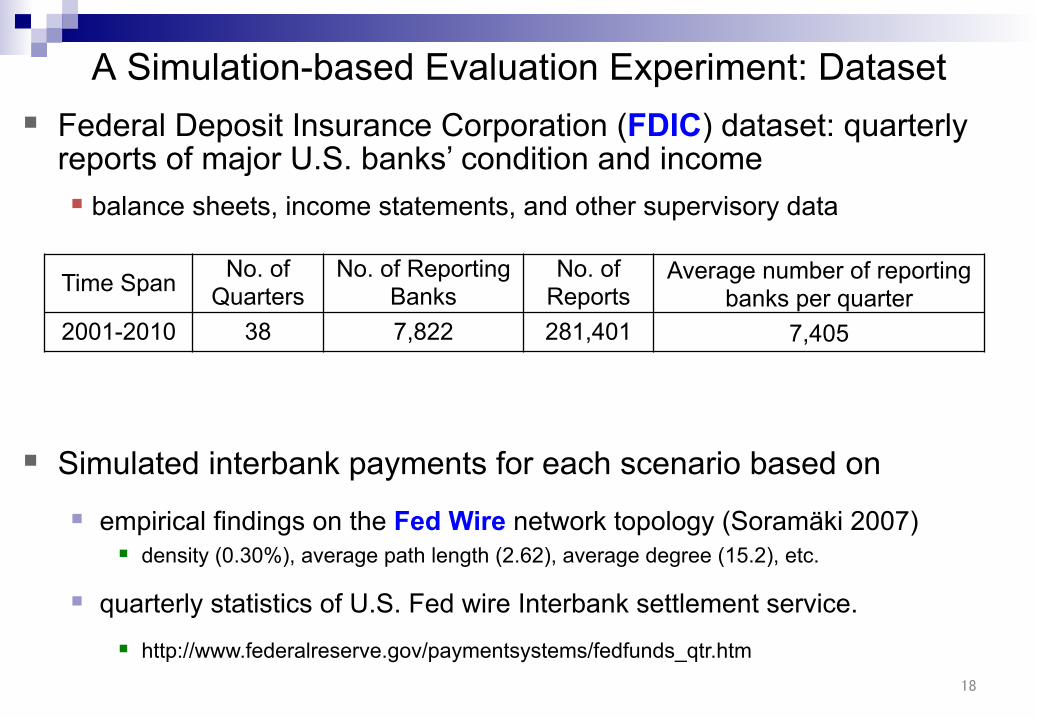

A Simulation-based Evaluation Experiment: Dataset § Federal Deposit Insurance Corporation (FDIC) dataset: quarterly

reports of major U.S. banks’ condition and income § balance sheets, income statements, and other supervisory data

§ Simulated interbank payments for each scenario based on

§ empirical findings on the Fed Wire network topology (Soramäki 2007) § density (0.30%), average path length (2.62), average degree (15.2), etc.

§ quarterly statistics of U.S. Fed wire Interbank settlement service.

§ http://www.federalreserve.gov/paymentsystems/fedfunds_qtr.htm 18

Time Span No. of Quarters

No. of Reporting Banks

No. of Reports

Average number of reporting banks per quarter

2001-2010 38 7,822 281,401 7,405

19

0%10%20%30%40%50%60%70%80%90%

100%

0 0.5 1 1.5 2 2.5 3 3.5 4 4.5 5

Ave

rage

Ban

k Fa

ilure

Rat

e γ

Shock Rate β

Average Bank Failure Rates of Generated Scenarios at Different Shock Rates

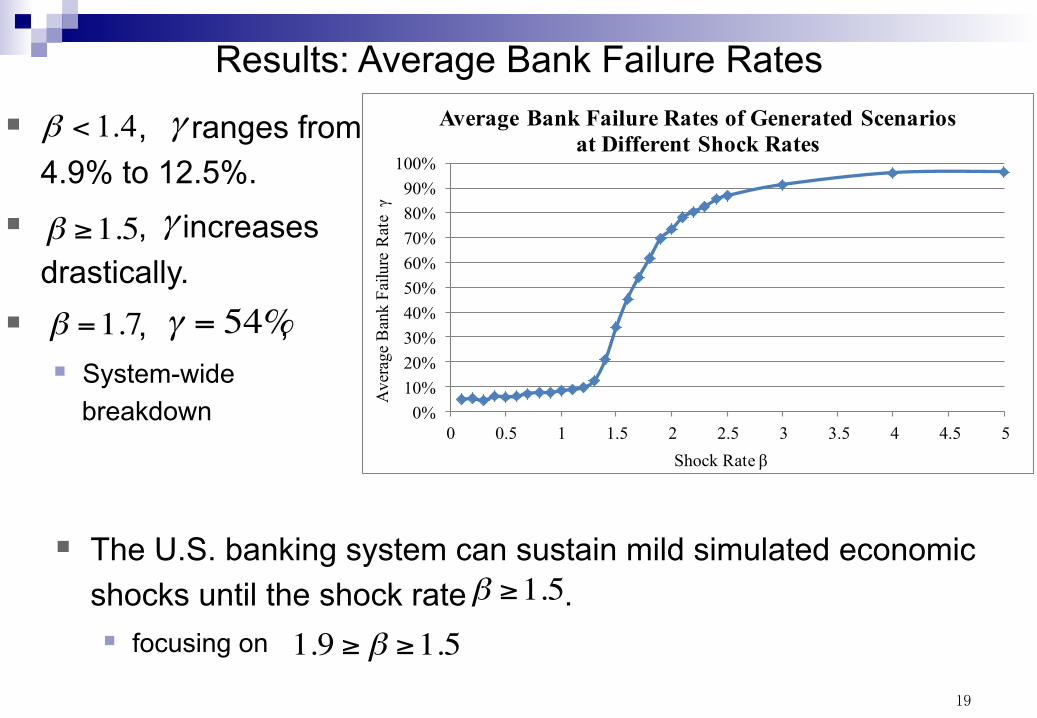

Results: Average Bank Failure Rates

§ , ranges from 4.9% to 12.5%.

§ , increases drastically.

§ , , § System-wide

breakdown

4.1<β γ

β ≥1.5 γ

β =1.7 γ = 54%

§ The U.S. banking system can sustain mild simulated economic shocks until the shock rate . § focusing on

β ≥1.5

1.9 ≥ β ≥1.5

20

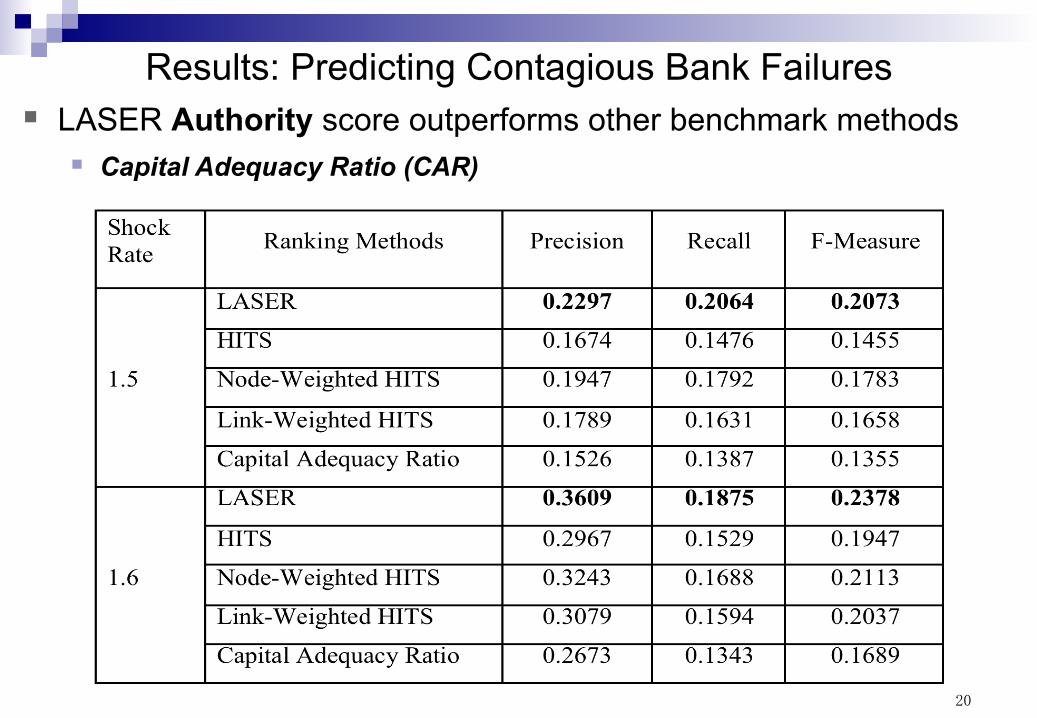

Results: Predicting Contagious Bank Failures § LASER Authority score outperforms other benchmark methods

§ Capital Adequacy Ratio (CAR)

21

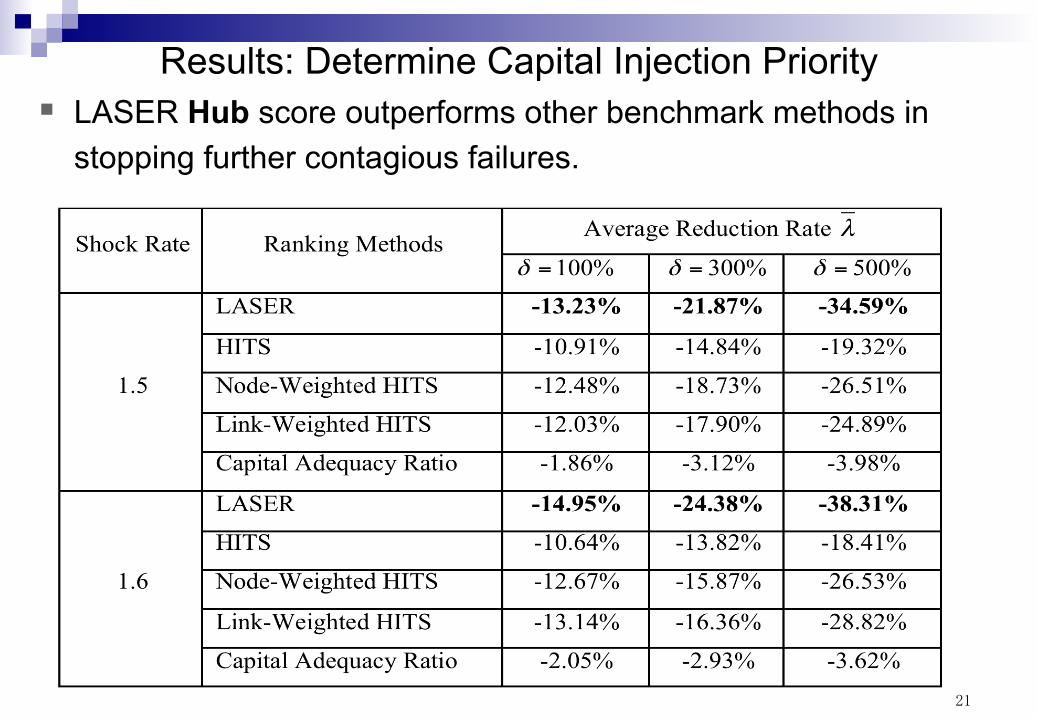

Results: Determine Capital Injection Priority § LASER Hub score outperforms other benchmark methods in

stopping further contagious failures.

22

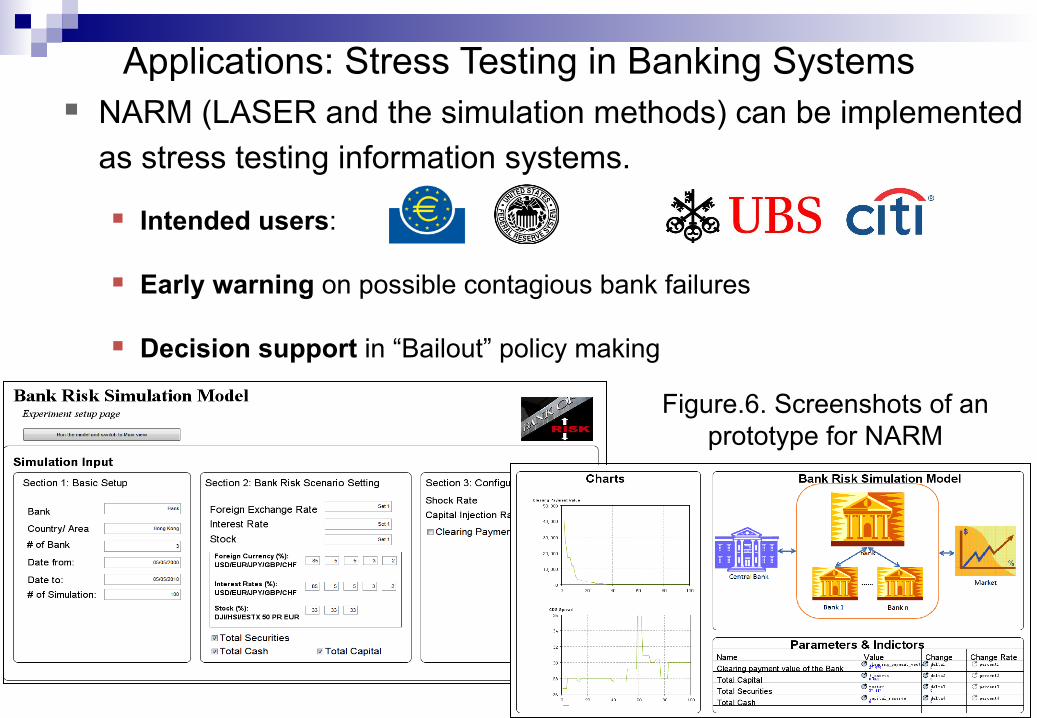

Applications: Stress Testing in Banking Systems § NARM (LASER and the simulation methods) can be implemented

as stress testing information systems.

§ Intended users:

§ Early warning on possible contagious bank failures

§ Decision support in “Bailout” policy making

Figure.6. Screenshots of an prototype for NARM

![iNTHECHANCERYCOURTFORDAVIDSONCOUNTY,TENNESSEE, …inthechancerycourtfordavidsoncounty,tennessee, atnashville i l terryr.clayton, 1 i i ‘ petitioner, ‘ ] i.. '] w_ _ fl vs. ] no.09—1801~11]](https://img.pdfslide.us/doc/110x75/60bc75f8c00a2768f44f0d43/inthechancerycourtfordavidsoncountytennessee-inthechancerycourtfordavidsoncountytennessee.jpg)