Embed Size (px)

Citation preview

Network ConvergencePolicy in China

July 2012

Introduction

In China, the regulation and development of telecom/internet networks and broadcasting networks remained largely separate until 2010

3-network convergence trials, now underway, will have major impact on how China’s IT infrastructure develops

Outcome of China’s final choices for convergence will impact global equipment vendors, systems and applications developers, and content providers

Key Points

China may merge regulators or require cross-investment to break regulatory and competitive log jam

Key obstacles to convergence in China are political rather than technical

Broadcasting and telecom regulators locked in long-standing turf war over convergence

Telecom operators currently enjoy multiple advantages over cable companies in terms of convergence-readiness

Reaching TV screens key to reaching the masses

Convergence in China

Key obstacles to convergence are more political, less technical

• Power struggle between telecom and broadcasting regulators

• Cable TV network not yet ready as nationwide integrated interactive platform

• Cable network still 2~3 years from ready to compete with telecom network

• Telecom operators curbed by State Council policy

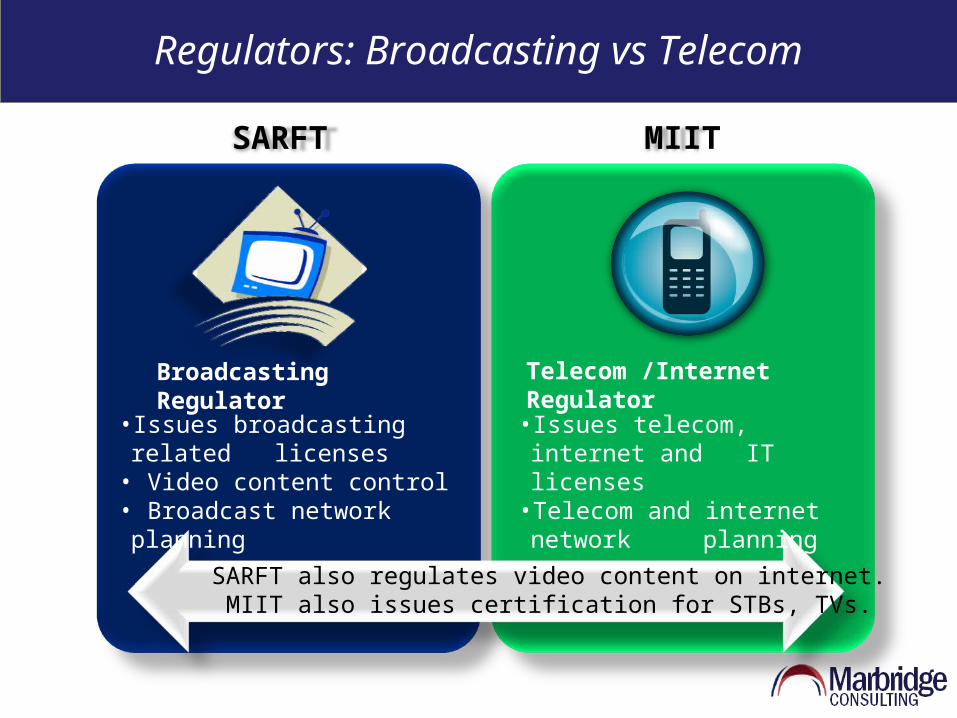

Regulators: Broadcasting vs Telecom

SARFT also regulates video content on internet. MIIT also issues certification for STBs, TVs.

SARFT MIIT

Broadcasting Regulator Telecom /Internet Regulator

• Issues broadcasting related licenses

• Video content control • Broadcast network planning

• Issues telecom, internet and IT licenses

• Telecom and internet network planning

SARFT protects cable operators under “safeguarding government mouthpiece” rubric

MIIT has repeatedly lost to SARFT in struggle for power in convergence

Convergence Key Battleground in Long-standing Turf War between SARFT, MIIT

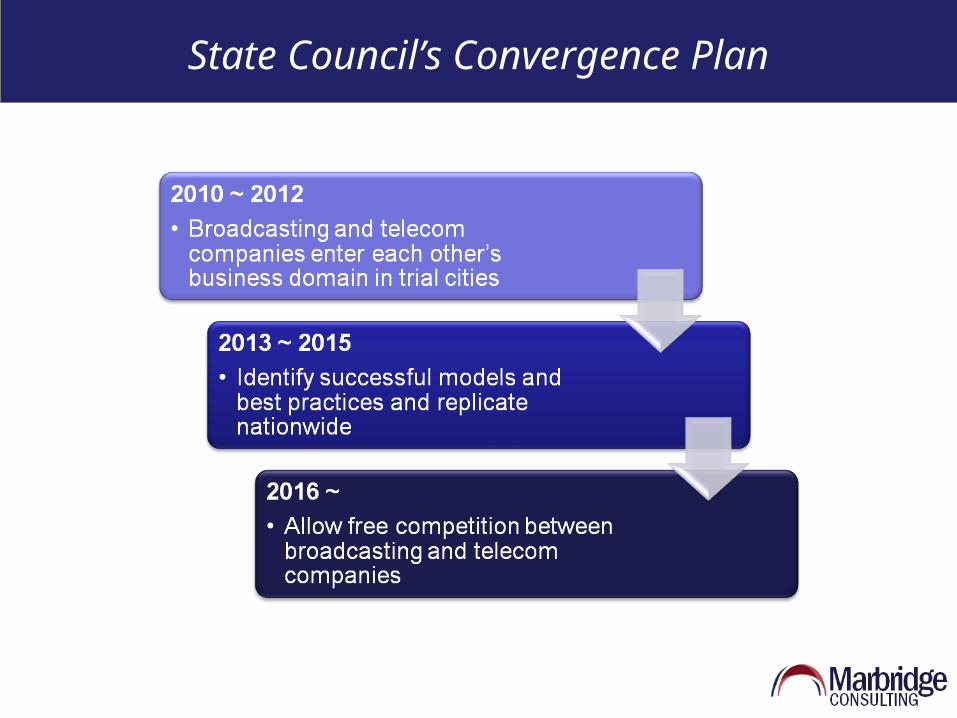

State Council’s Convergence Plan

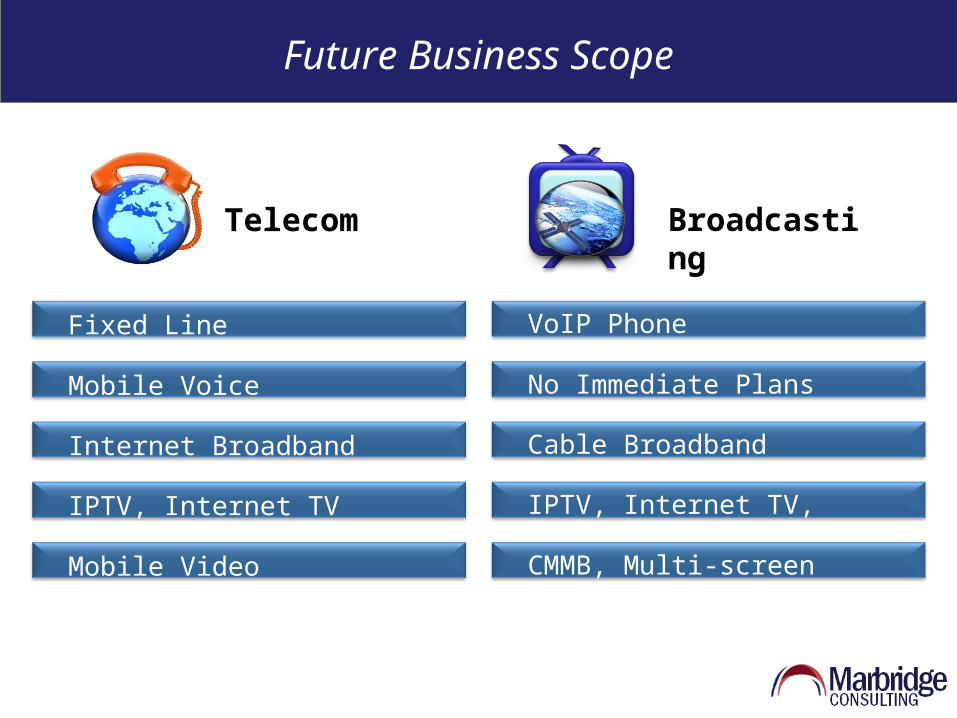

Future Business Scope

Fixed Line VoIP Phone

Mobile Voice No Immediate Plans

Internet Broadband Cable Broadband

IPTV, Internet TV IPTV, Internet TV, Cable TV

Mobile Video CMMB, Multi-screen

Telecom Broadcasting

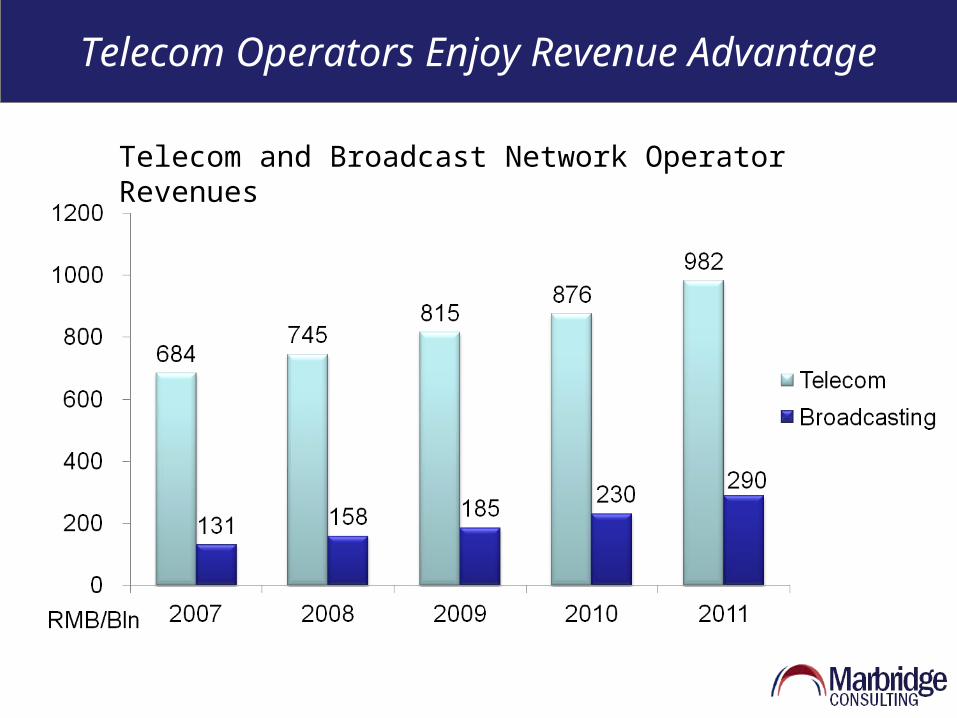

Telecom operators currently better positioned for convergence than cable companies

Telecom Operators Enjoy Revenue Advantage

Telecom and Broadcast Network Operator Revenues

• Telecom operators fully commercialized• Broadcasting companies propaganda focused

• Telecom networks have nationwide scale• Cable networks localized, fragmented

Telecom Operators More Commercialized and Consolidated

Broadcasting Companies Enjoy Control of Video Content Production and Distribution

Maintain control over all video content to TV terminals

Produce bulk of domestic film and TV programming

• SARFT issues IPTV, Internet TV licenses only to broadcasting firms

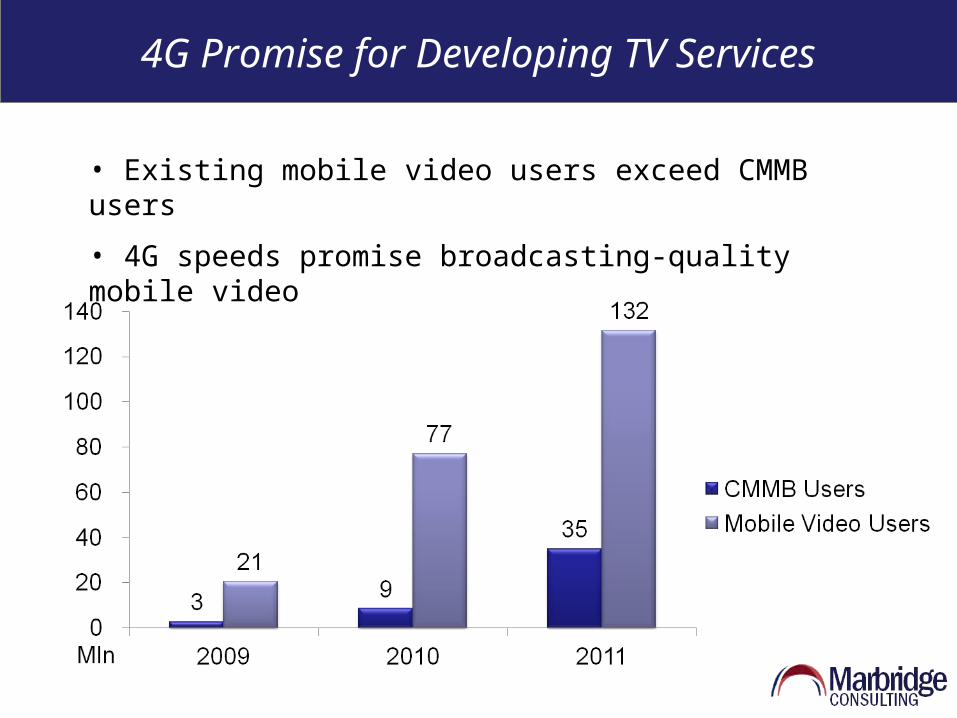

4G Promise for Developing TV Services

• Existing mobile video users exceed CMMB users

• 4G speeds promise broadcasting-quality mobile video

4G Impact on Convergence Limited in Short Term

Key obstacles to broad 4G commercialization in China

• Limited TD-LTE chips and terminals

• China Telecom, Unicom first need to recoup 3G capex

• MIIT wants slow transition to 4G to keep competitive balance

4G?

Reaching TV Screens Key to Reaching the Masses

• Why TV?

- 97% TV penetration vs. 38% Internet penetration (by 2011)

- Priority and price: TV or STB first, then PC

• 3 ways to get to TV: Cable DTV, IPTV, and Internet TV

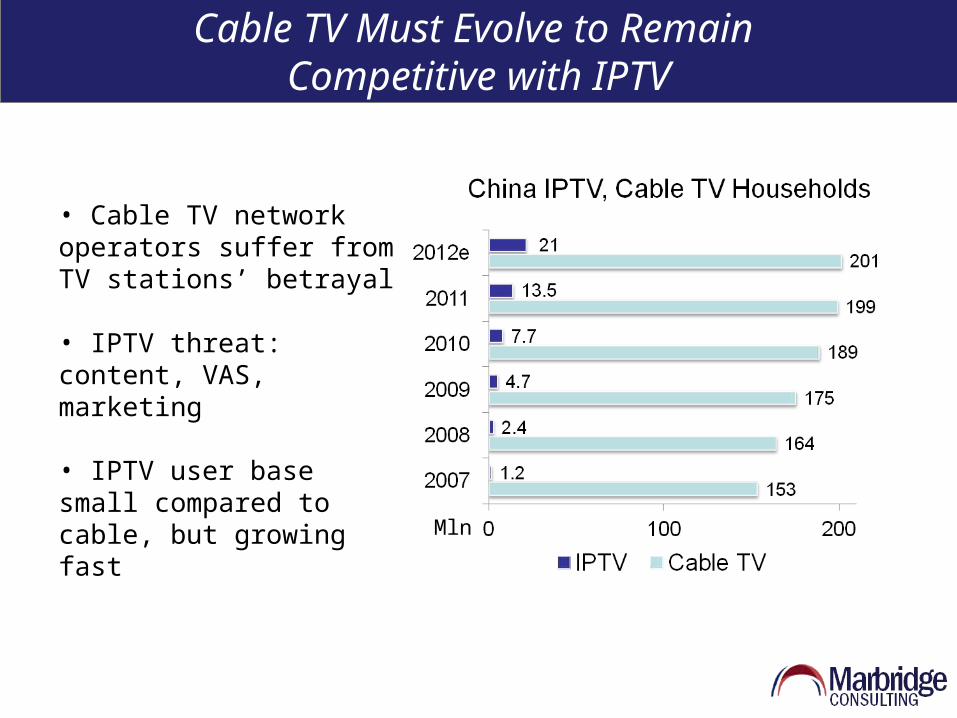

Cable TV Must Evolve to Remain Competitive with IPTV

• Cable TV network operators suffer from TV stations’ betrayal

• IPTV threat: content, VAS, marketing

• IPTV user base small compared to cable, but growing fast

Mln

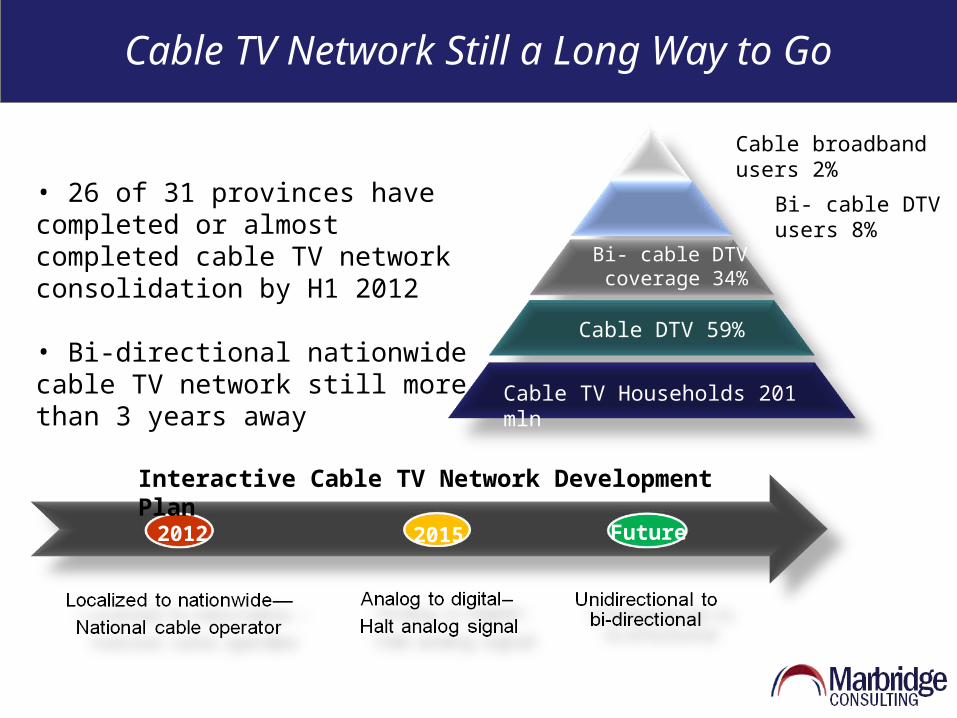

2012 2015 Future

Interactive Cable TV Network Development Plan

Cable TV Network Still a Long Way to Go

• 26 of 31 provinces have completed or almost completed cable TV network consolidation by H1 2012

• Bi-directional nationwide cable TV network still more than 3 years away

Bi- cable DTVusers 8%

Cable broadband users 2%

Cable TV Households 201 mln

Cable DTV 59%

Bi- cable DTV coverage 34%

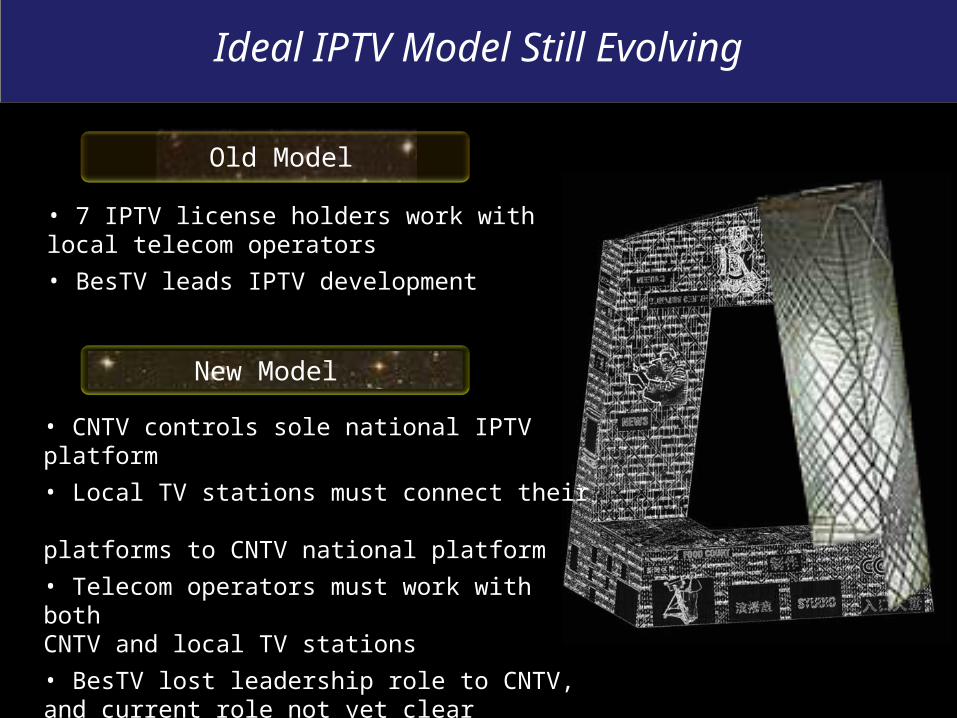

Ideal IPTV Model Still Evolving

• 7 IPTV license holders work with local telecom operators

• BesTV leads IPTV development

Old Model

New Model

• CNTV controls sole national IPTV platform

• Local TV stations must connect their platforms to CNTV national platform

• Telecom operators must work with both CNTV and local TV stations

• BesTV lost leadership role to CNTV, and current role not yet clear

Internet TV: Born an Original, May Die a Copy

• Internet TV originally had no operator, relied on pirated content; now 7operators and only legal content

• Internet TV lacks a clear, sustainable business model

• IPTV vs. Internet TV

- IPTV provides a dedicatedcontent line

- Internet TV doesn’t offer live broadcasts

Possible Solutions to Break Regulatory and Competitive Log Jam

• SARFT, MIIT to merge ? - Multi-screen technology complicating convergence turf battle and policy-making

• Cross-over investment

- China Mobile may invest in CMMB operator

- China Mobile may invest in national cable operator

- China Mobile to obtain fixed-line license

Global Impact of China’s Convergence Choices

Video Content

• Pace of converged network development key demand driver for domestic and foreign content

• Chinese content demand already influencing Hollywood global releases

Equipment, IT solutions

• Convergence drives demand for smart terminals creating opportunities for:

- Terminal makers

- CA providers

- Video/Audio codec developers

Conclusions

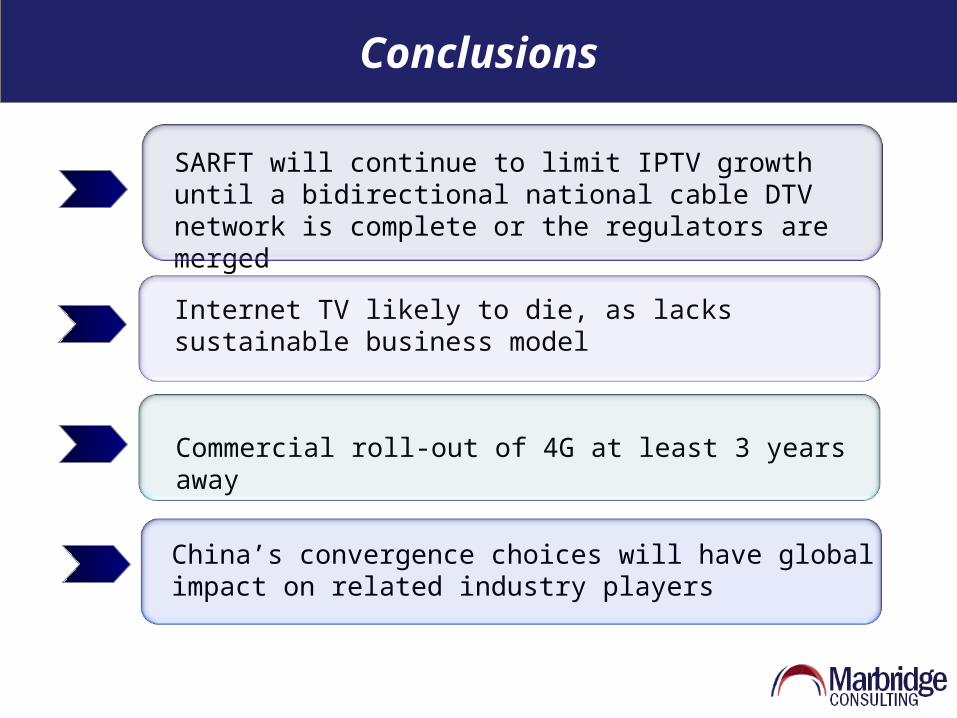

Commercial roll-out of 4G at least 3 years away

SARFT will continue to limit IPTV growth until a bidirectional national cable DTV network is complete or the regulators are merged

Internet TV likely to die, as lacks sustainable business model

China’s convergence choices will have global impact on related industry players

Tel: +86-10-8447-7374 Fax: +86-10-8447-7314 E-mail: [email protected]

www.marbridgeconsulting.com

THANK YOU