Embed Size (px)

Citation preview

Net Present Value and

Other Investment Criteria

Topics Covered

Net Present Value

Other Investment Criteria

Mutually Exclusive Projects

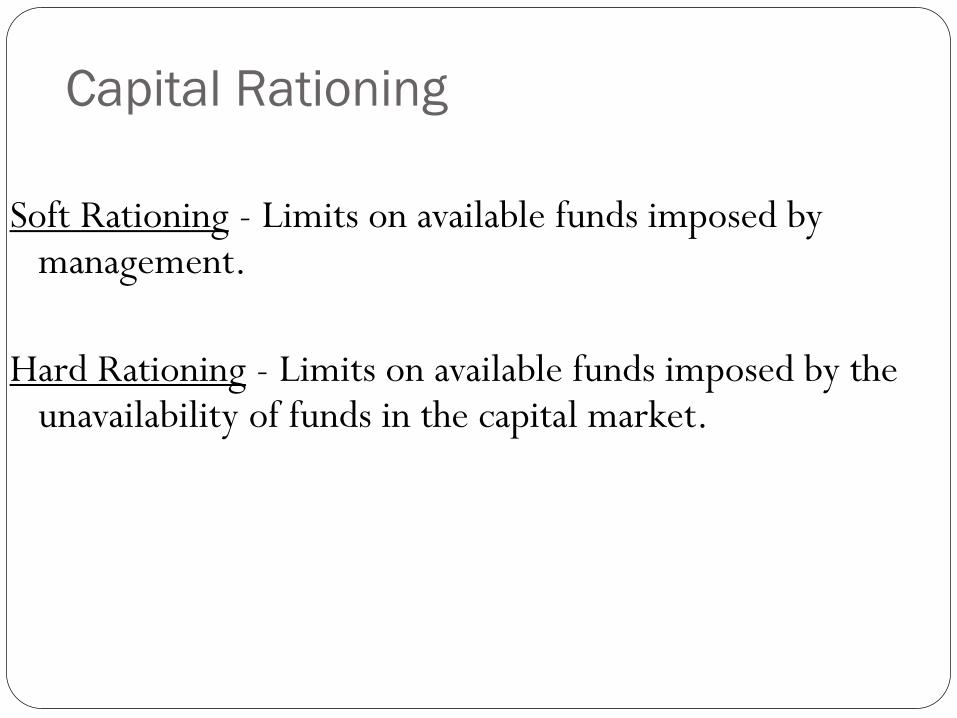

Capital Rationing

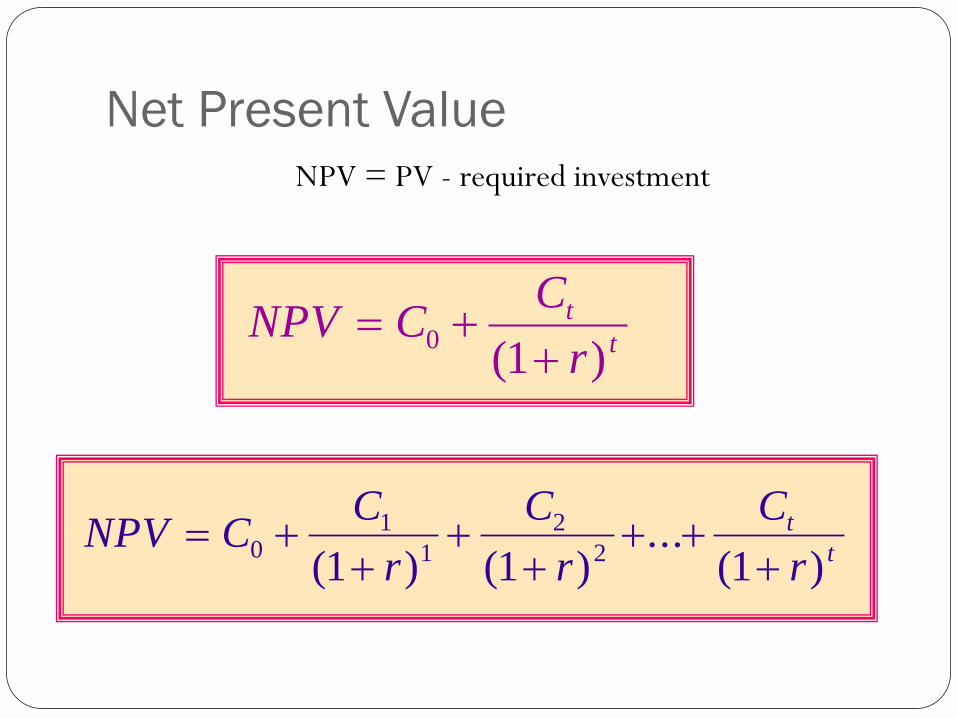

Net Present Value

Net Present Value - Present value of cash

flows minus initial investments.

Opportunity Cost of Capital - Expected rate

of return given up by investing in a project

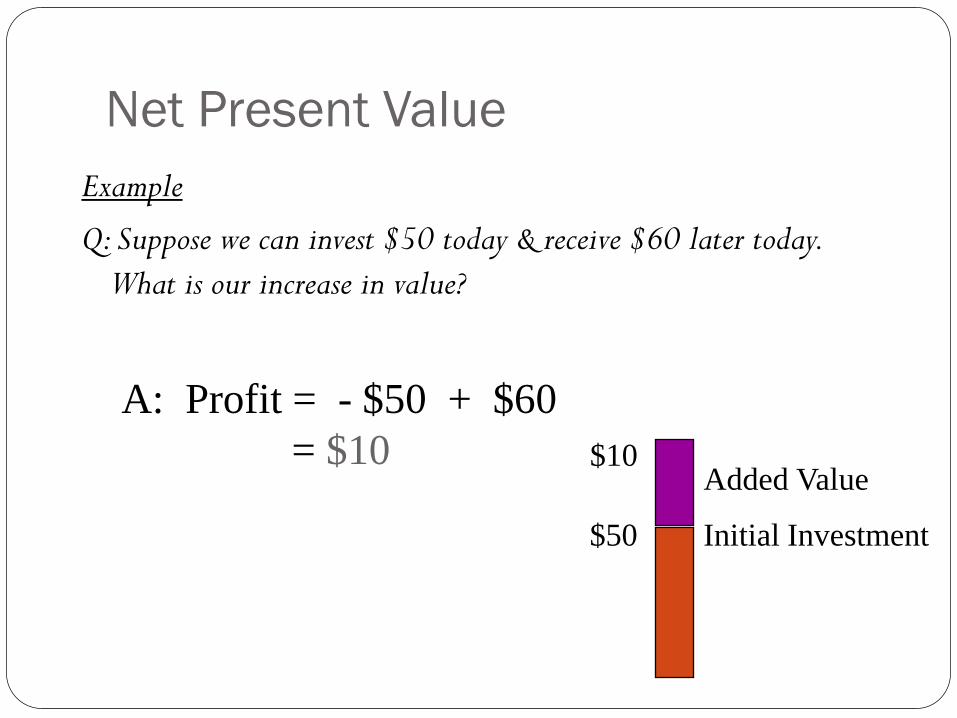

Net Present Value

Example

Q: Suppose we can invest $50 today & receive $60 later today.

What is our increase in value?

Initial Investment

Added Value

$50

$10

A: Profit = - $50 + $60

= $10

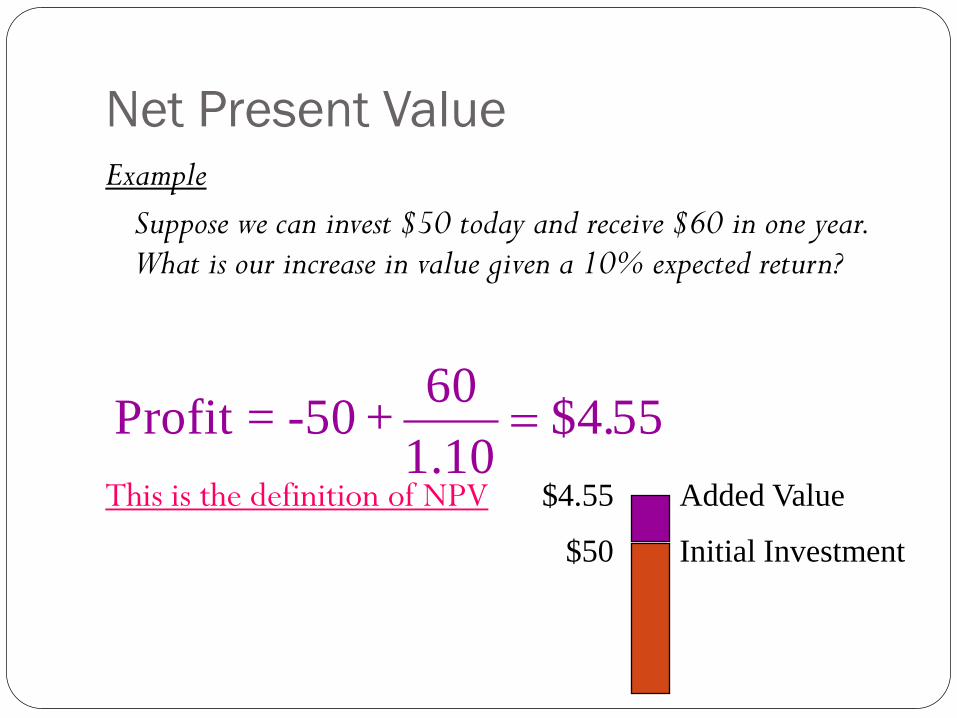

Net Present Value Example

Suppose we can invest $50 today and receive $60 in one year. What is our increase in value given a 10% expected return?

This is the definition of NPV

Profit = -50 +60

1.10 $4.55

Initial Investment

Added Value

$50

$4.55

Net Present Value

NPV = PV - required investment

NPV CC

r

t

t

0

1( )

NPV CC

r

C

r

C

r

t

t

0

1

1

2

21 1 1( ) ( )...

( )

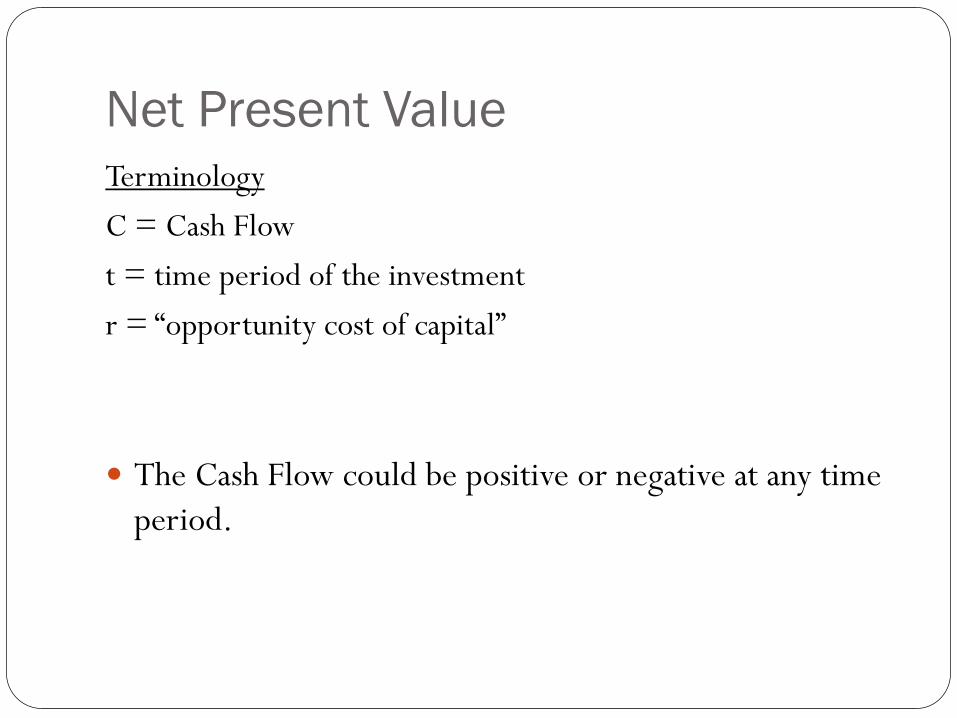

Net Present Value

Terminology

C = Cash Flow

t = time period of the investment

r = “opportunity cost of capital”

The Cash Flow could be positive or negative at any time

period.

Net Present Value

Net Present Value Rule

Managers increase shareholders’ wealth by accepting all

projects that are worth more than they cost.

Therefore, they should accept all projects with a positive net

present value.

Net Present Value

Example

You have the opportunity to purchase an

office building. You have a tenant lined up

that will generate $16,000 per year in

cash flows for three years. At the end of

three years you anticipate selling the

building for $450,000. How much would

you be willing to pay for the building?

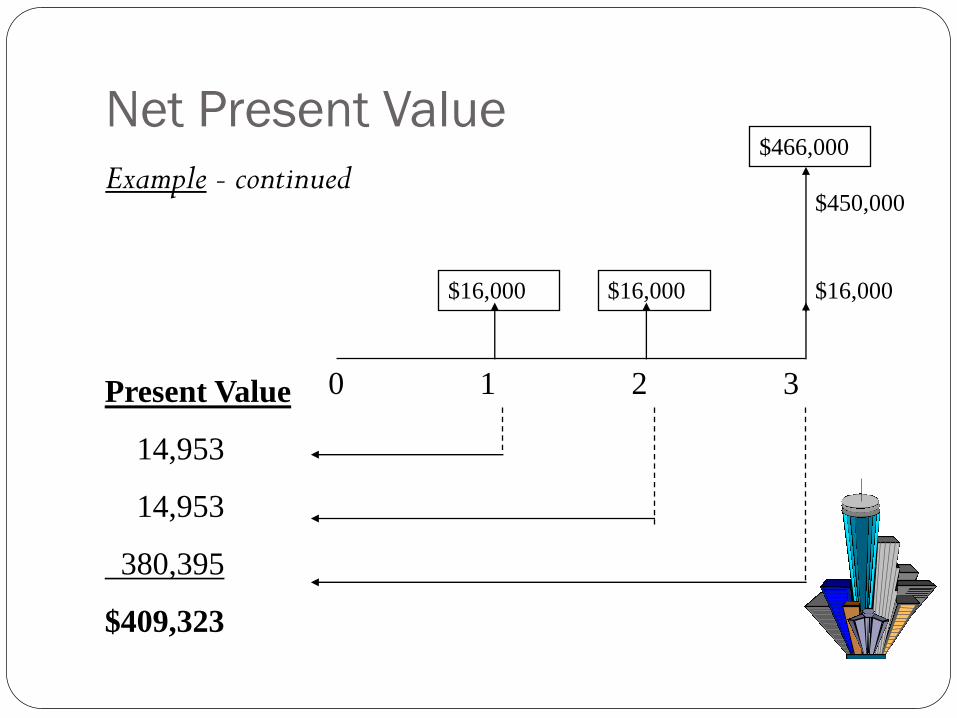

Net Present Value

Example - continued

$16,000 $16,000 $16,000

$450,000

$466,000

0 1 2 3 Present Value

14,953

14,953

380,395

$409,323

Net Present Value

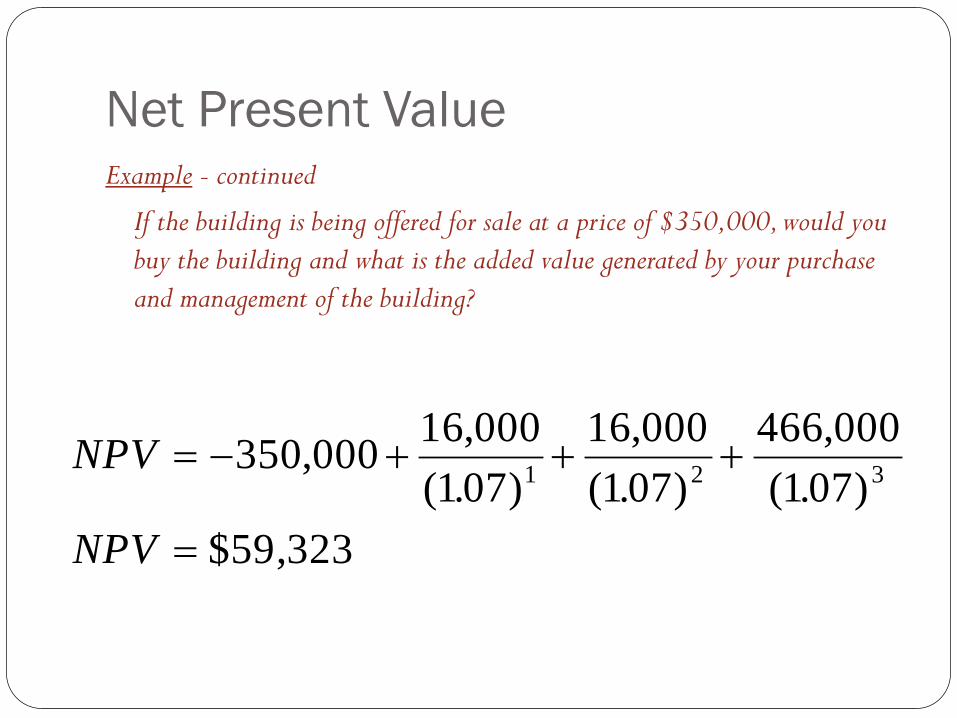

Example - continued

If the building is being offered for

sale at a price of $350,000,

would you buy the building and

what is the added value generated

by your purchase and management

of the building?

Net Present Value Example - continued

If the building is being offered for sale at a price of $350,000, would you

buy the building and what is the added value generated by your purchase

and management of the building?

NPV

NPV

350 00016 000

107

16 000

107

466 000

107

323

1 2 3,

,

( . )

,

( . )

,

( . )

$59,

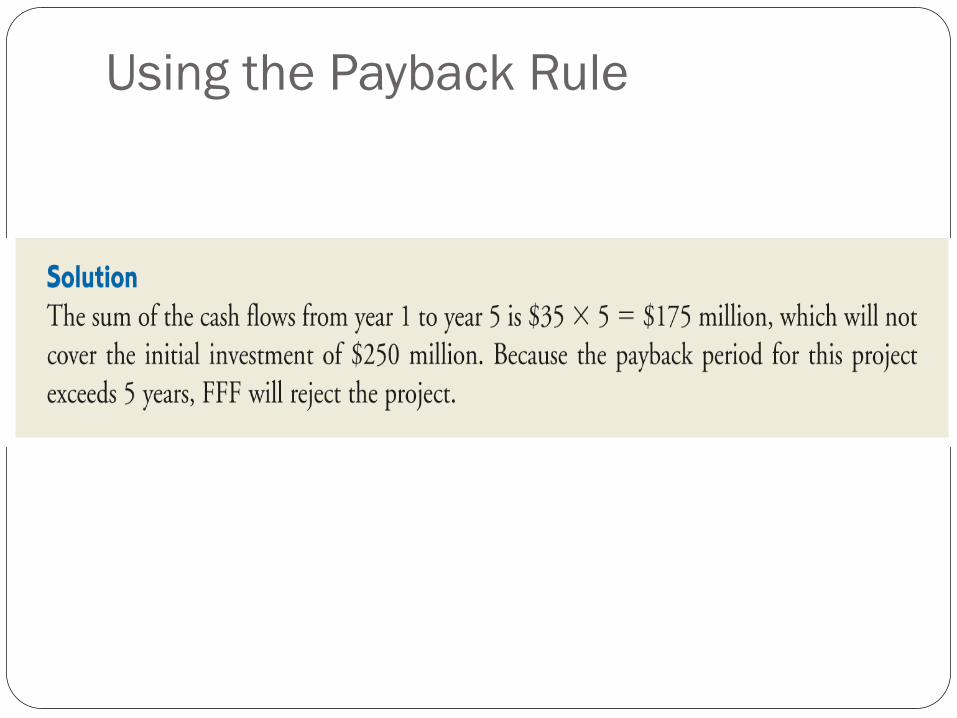

Payback Method

Payback Period - Time until cash flows recover the initial

investment of the project.

The payback rule specifies that a project be accepted if its

payback period is less than the specified cutoff period.

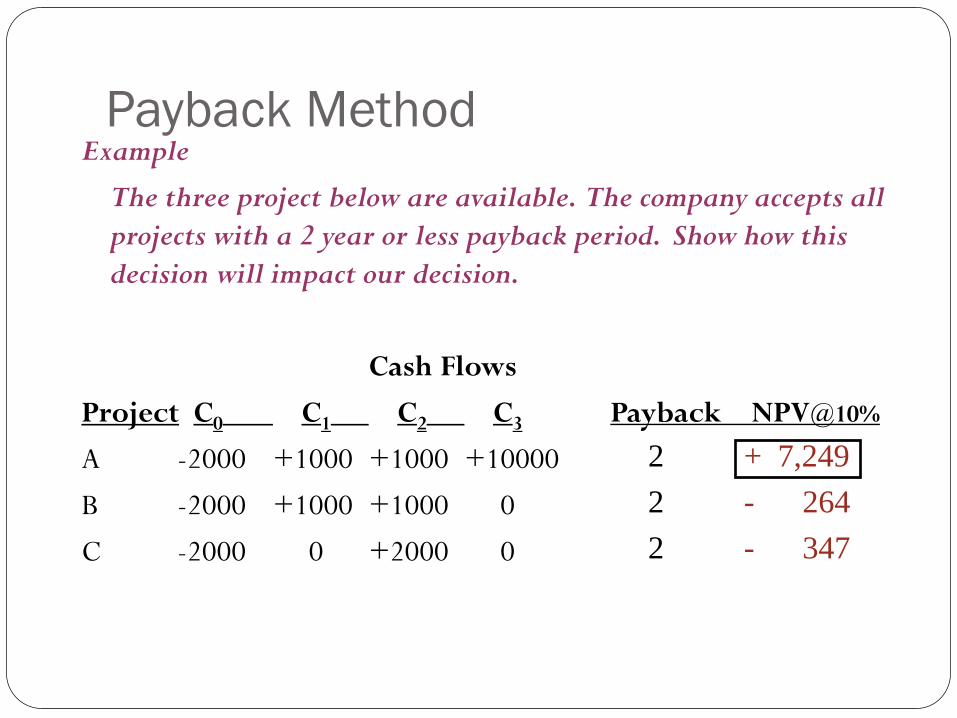

Payback Method Example

The three project below are available. The company accepts all

projects with a 2 year or less payback period. Show how this

decision will impact our decision.

Cash Flows

Project C0 C1 C2 C3 Payback NPV@10%

A -2000 +1000 +1000 +10000

B -2000 +1000 +1000 0

C -2000 0 +2000 0

+ 7,249

- 264

- 347

2

2

2

Using the Payback Rule

Using the Payback Rule

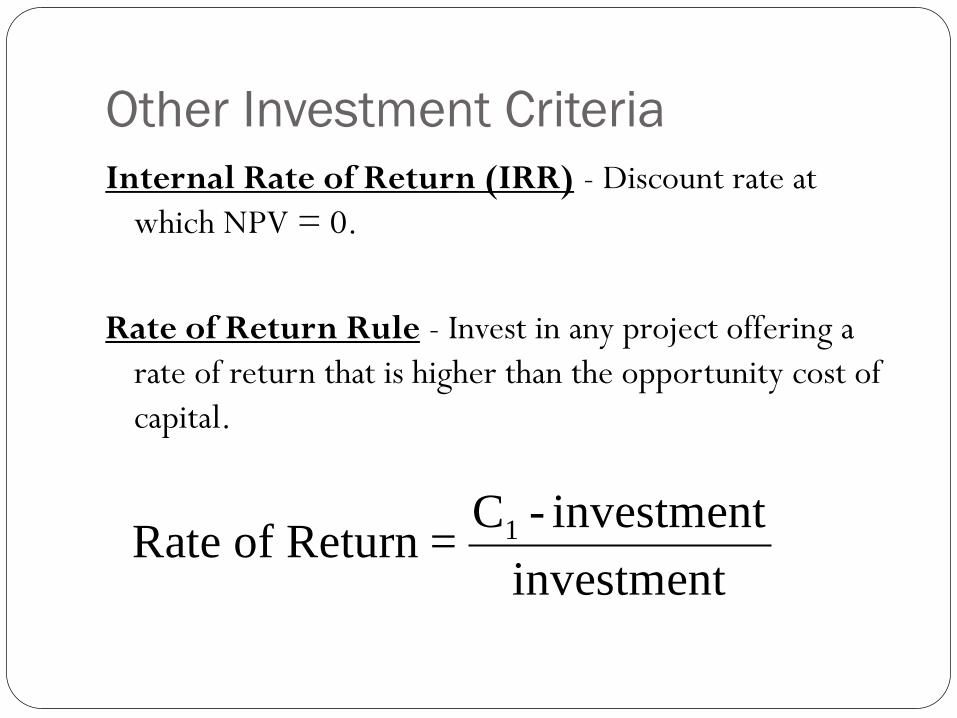

Other Investment Criteria

Internal Rate of Return (IRR) - Discount rate at

which NPV = 0.

Rate of Return Rule - Invest in any project offering a

rate of return that is higher than the opportunity cost of

capital.

Rate of Return =C - investment

investment

1

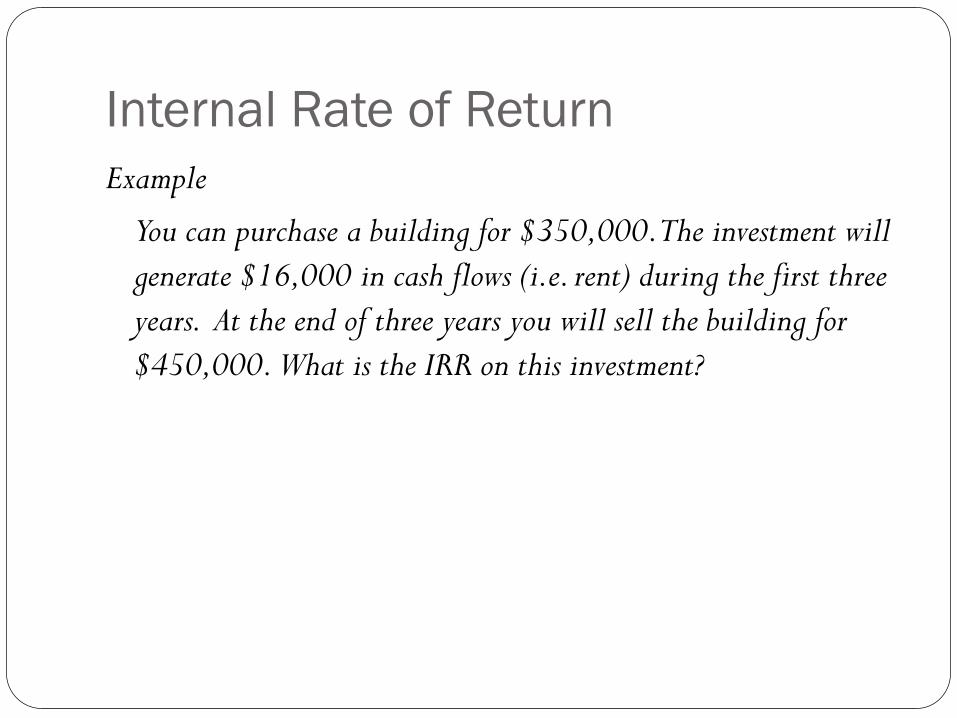

Internal Rate of Return

Example

You can purchase a building for $350,000. The investment will

generate $16,000 in cash flows (i.e. rent) during the first three

years. At the end of three years you will sell the building for

$450,000. What is the IRR on this investment?

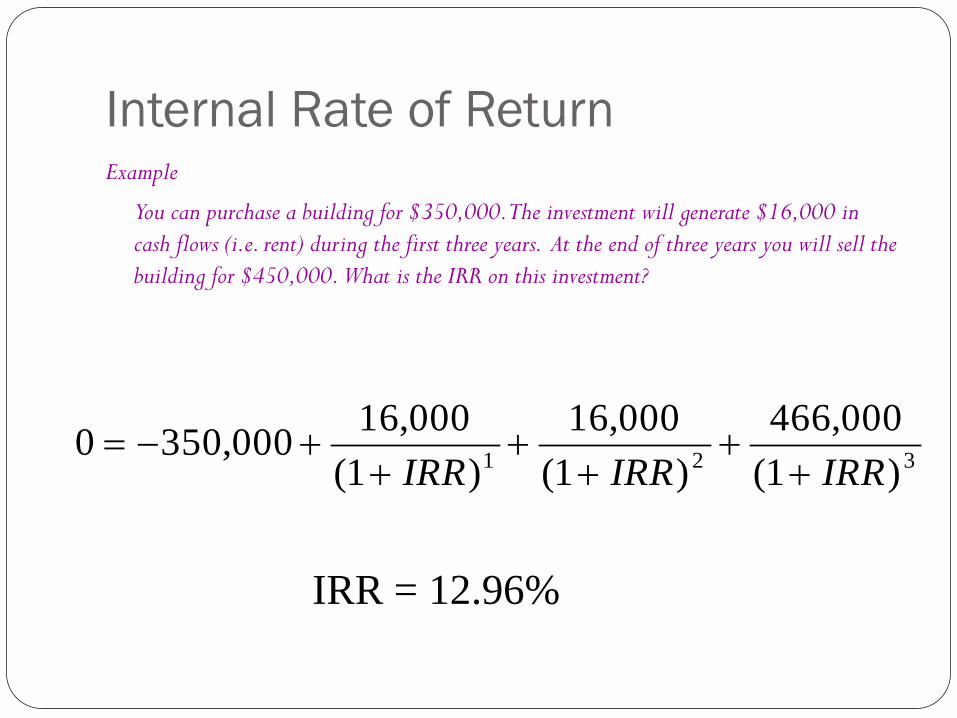

Internal Rate of Return Example

You can purchase a building for $350,000. The investment will generate $16,000 in

cash flows (i.e. rent) during the first three years. At the end of three years you will sell the

building for $450,000. What is the IRR on this investment?

0 350 00016 000

1

16 000

1

466 000

11 2 3

,

,

( )

,

( )

,

( )IRR IRR IRR

IRR = 12.96%

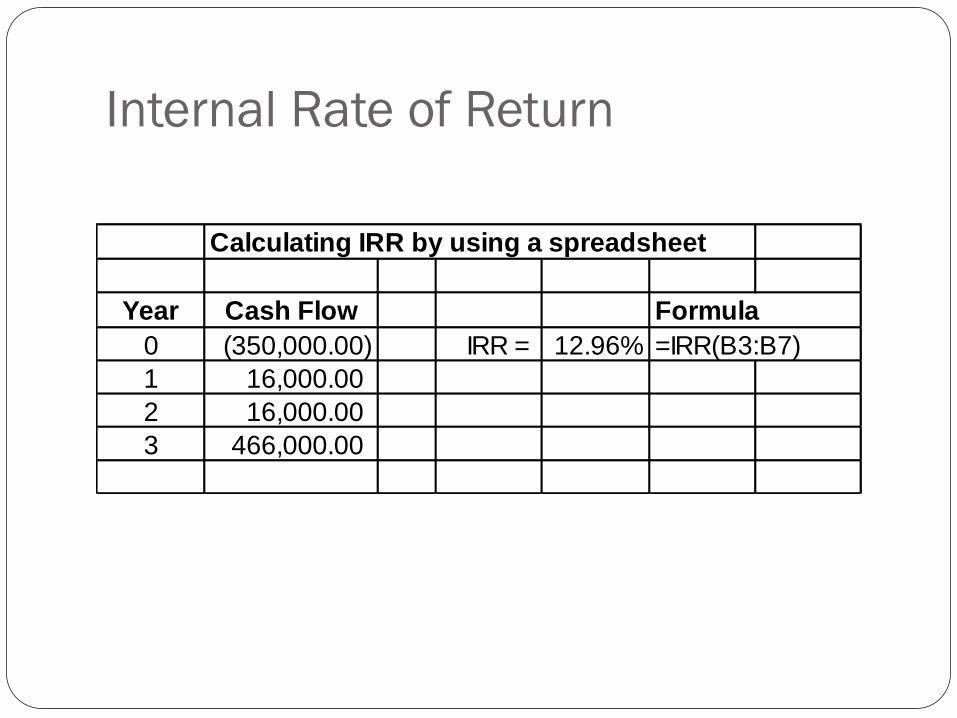

Internal Rate of Return

Calculating IRR by using a spreadsheet

Year Cash Flow Formula

0 (350,000.00) IRR = 12.96% =IRR(B3:B7)

1 16,000.00

2 16,000.00

3 466,000.00

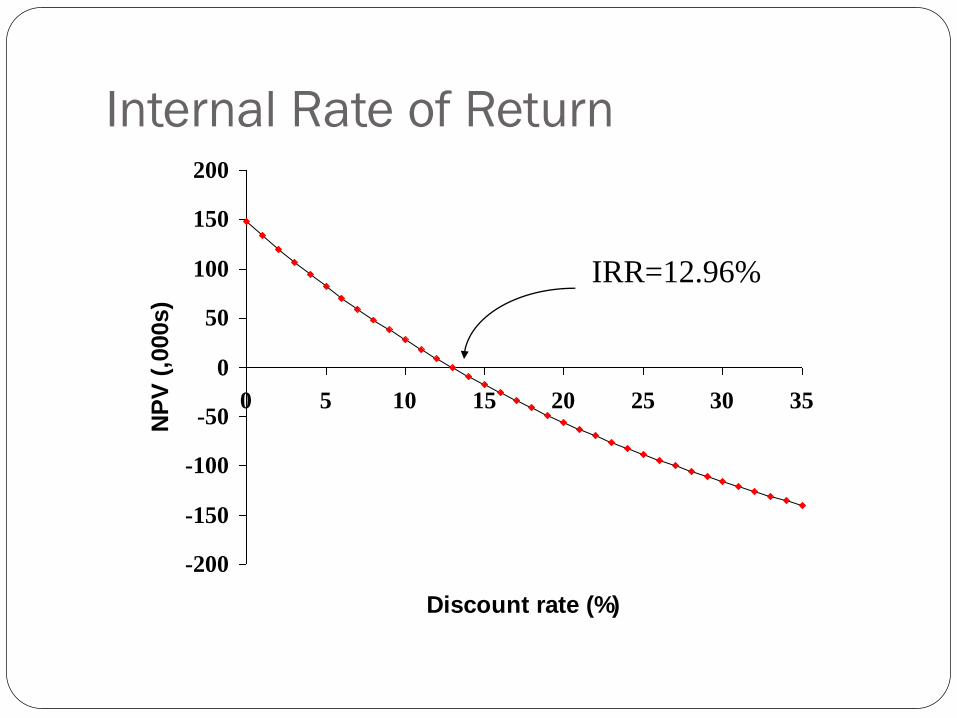

Internal Rate of Return

-200

-150

-100

-50

0

50

100

150

200

0 5 10 15 20 25 30 35

Discount rate (%)

NP

V (

,000s)

IRR=12.96%

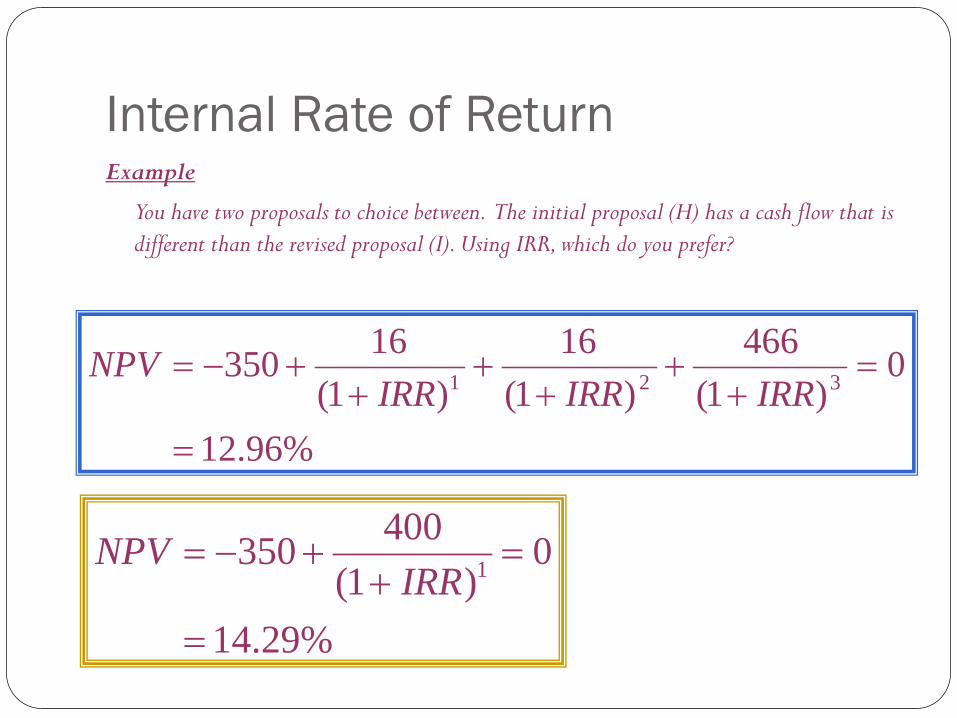

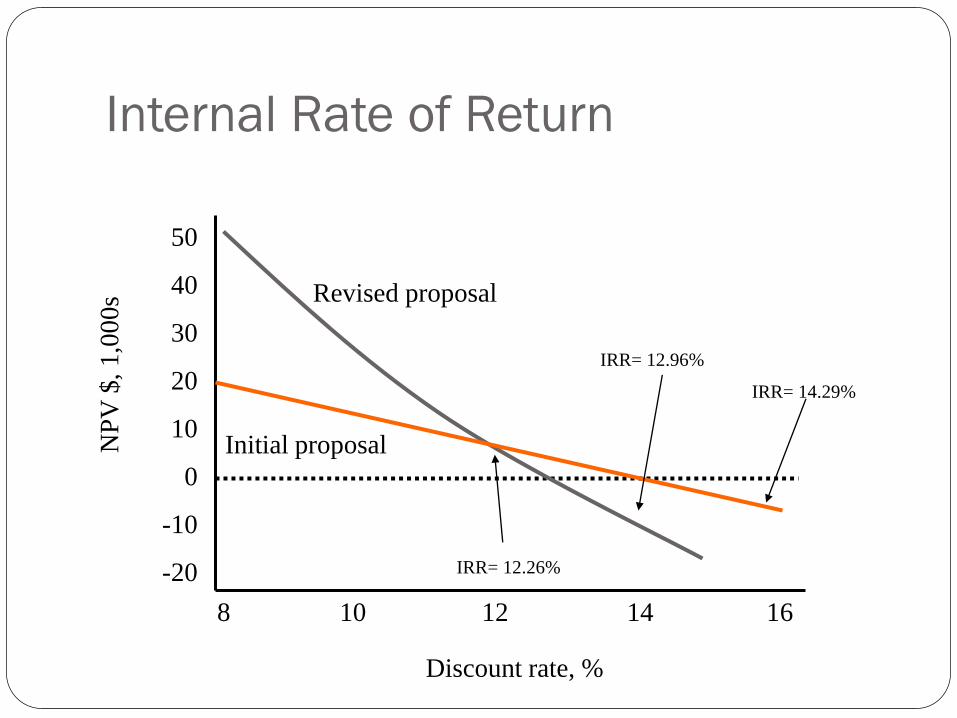

Internal Rate of Return Example

You have two proposals to choice between. The initial proposal (H) has a cash flow that is

different than the revised proposal (I). Using IRR, which do you prefer?

%29.14

0)1(

400350

1

IRR

NPV

%96.12

0)1(

466

)1(

16

)1(

16350

321

IRRIRRIRR

NPV

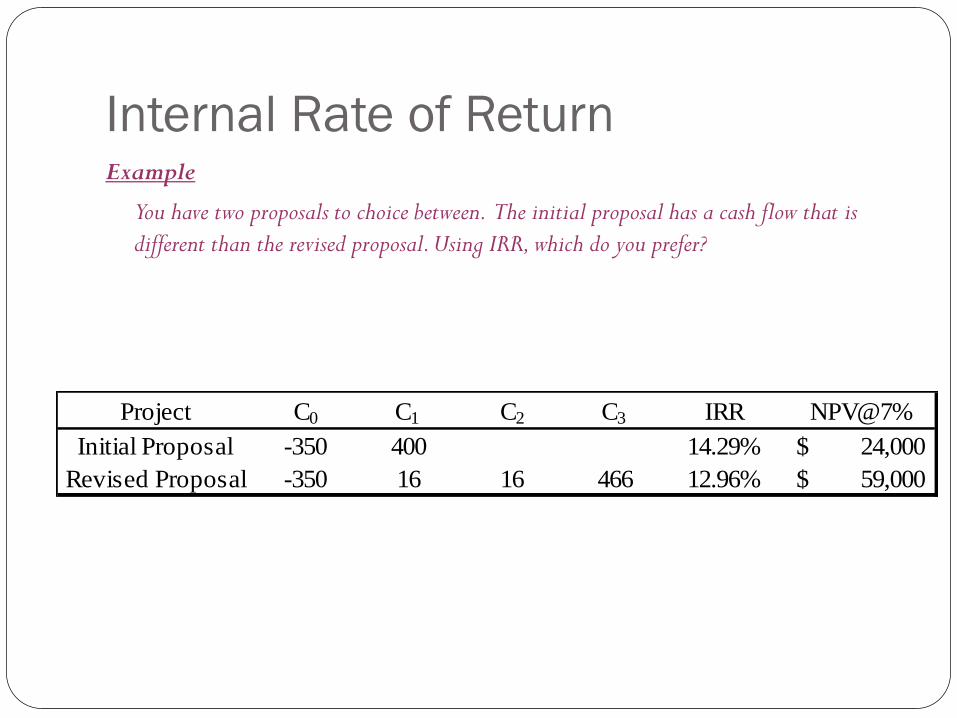

Internal Rate of Return Example

You have two proposals to choice between. The initial proposal has a cash flow that is

different than the revised proposal. Using IRR, which do you prefer?

Project C0 C1 C2 C3 IRR NPV@7%

Initial Proposal -350 400 14.29% 24,000$

Revised Proposal -350 16 16 466 12.96% 59,000$

Internal Rate of Return

50

40

30

20

10

0

-10

-20

NP

V $

, 1,0

00s

Discount rate, %

8 10 12 14 16

Revised proposal

Initial proposal

IRR= 14.29%

IRR= 12.96%

IRR= 12.26%

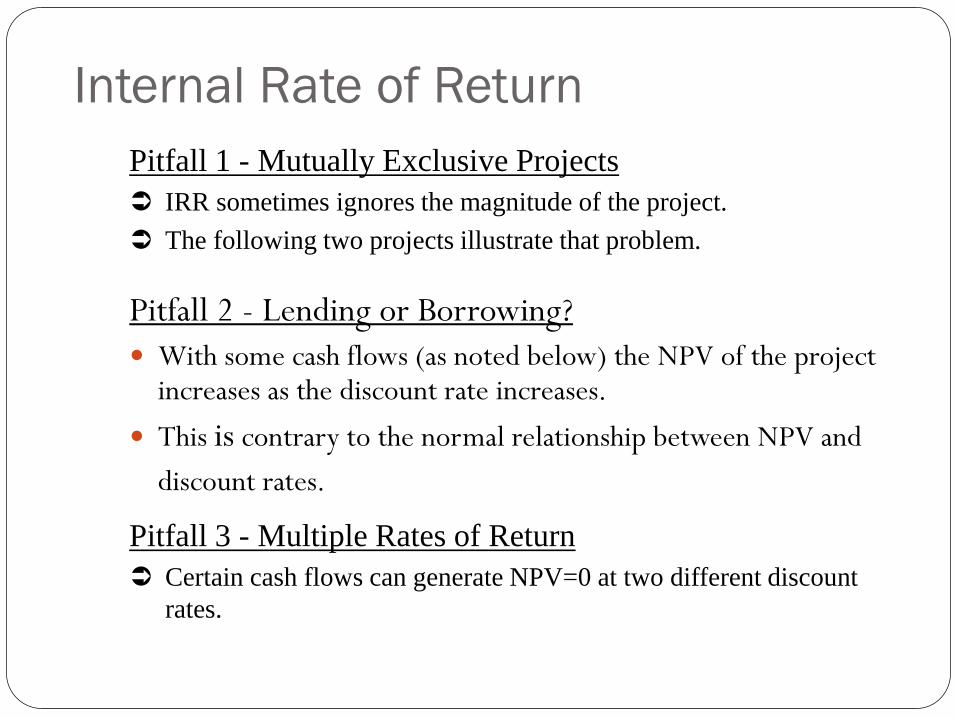

Internal Rate of Return

Pitfall 2 - Lending or Borrowing?

With some cash flows (as noted below) the NPV of the project increases as the discount rate increases.

This is contrary to the normal relationship between NPV and

discount rates.

Pitfall 1 - Mutually Exclusive Projects

IRR sometimes ignores the magnitude of the project.

The following two projects illustrate that problem.

Pitfall 3 - Multiple Rates of Return

Certain cash flows can generate NPV=0 at two different discount

rates.

Copyright © 2007 Pearson Addison-Wesley. All

rights reserved.

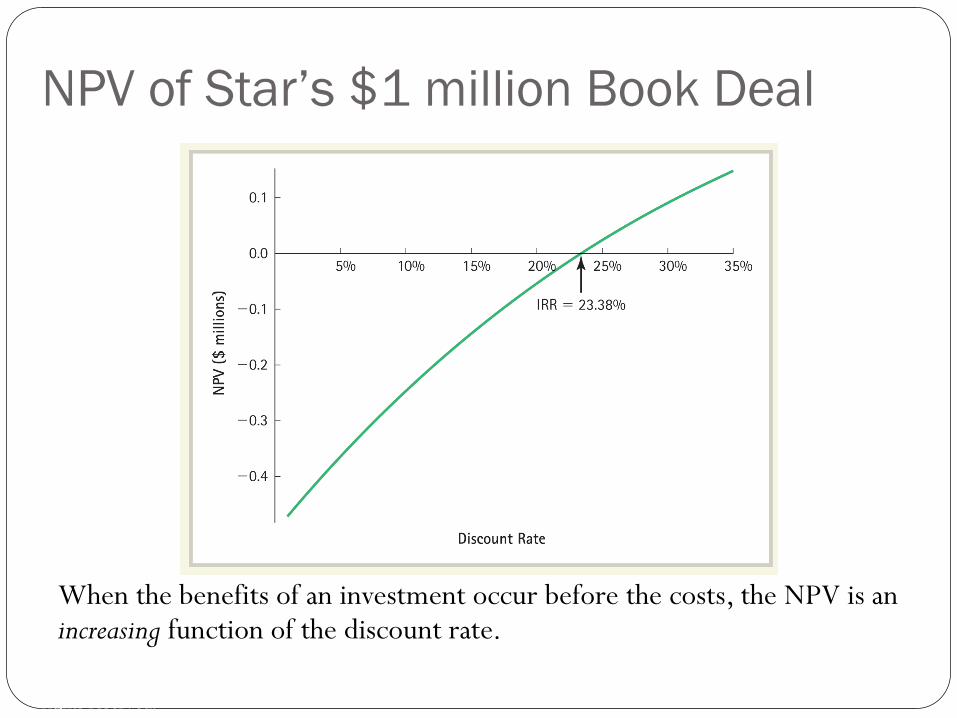

NPV of Star’s $1 million Book Deal

When the benefits of an investment occur before the costs, the NPV is an increasing function of the discount rate.

Copyright © 2007 Pearson Addison-Wesley. All

rights reserved.

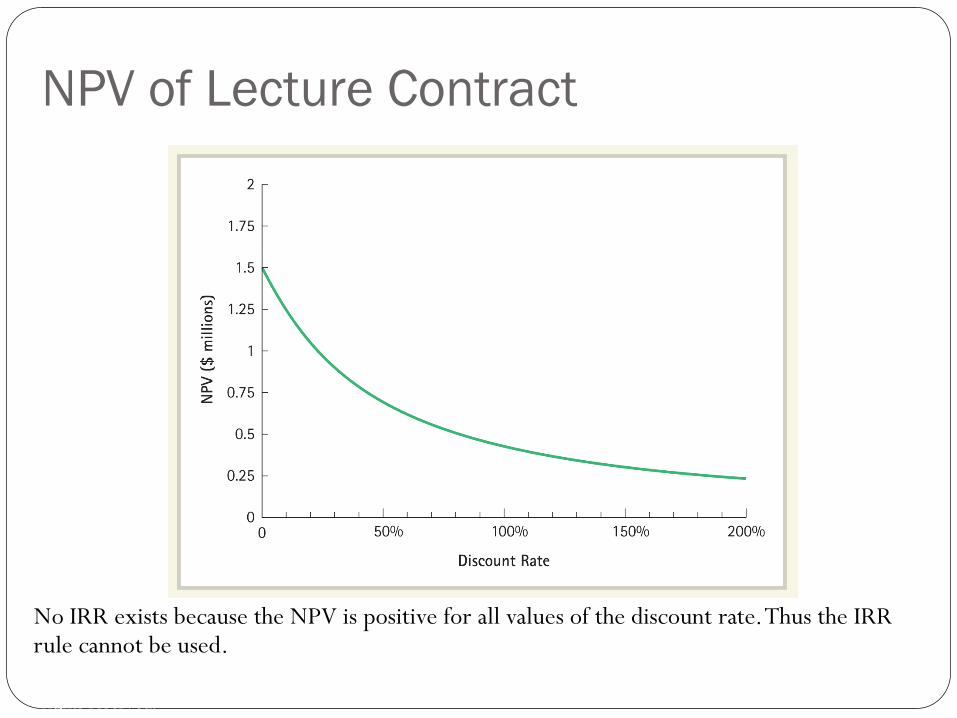

NPV of Lecture Contract

No IRR exists because the NPV is positive for all values of the discount rate. Thus the IRR rule cannot be used.

Copyright © 2007 Pearson Addison-Wesley. All

rights reserved.

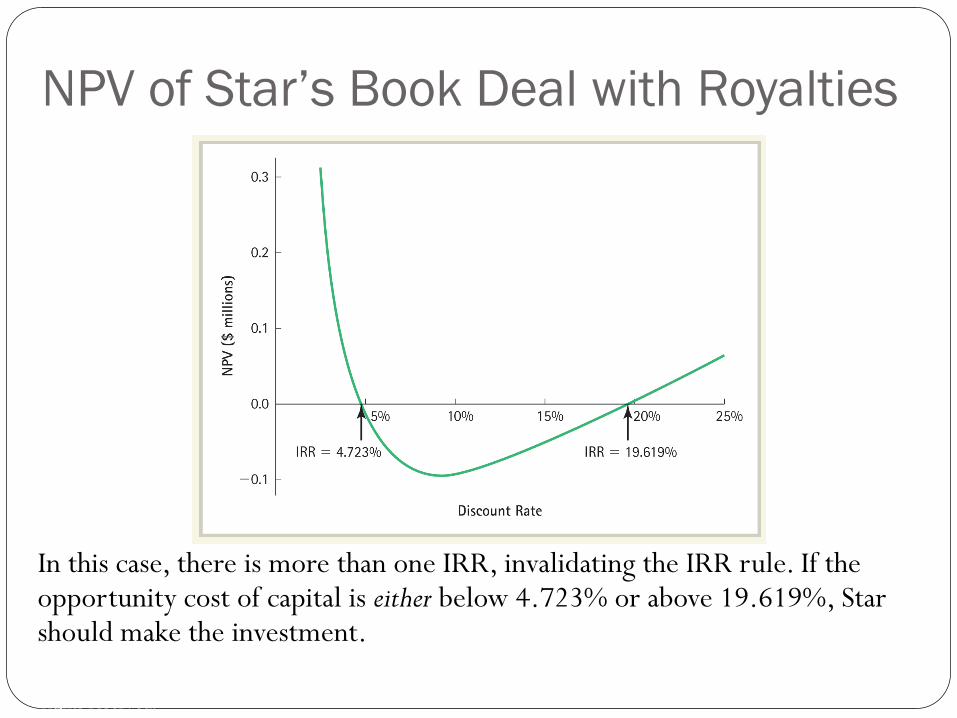

NPV of Star’s Book Deal with Royalties

In this case, there is more than one IRR, invalidating the IRR rule. If the opportunity cost of capital is either below 4.723% or above 19.619%, Star should make the investment.

Project Interactions

When you need to choose between mutually exclusive

projects, the decision rule is simple. Calculate the NPV of

each project, and, from those options that have a positive

NPV, choose the one whose NPV is highest.

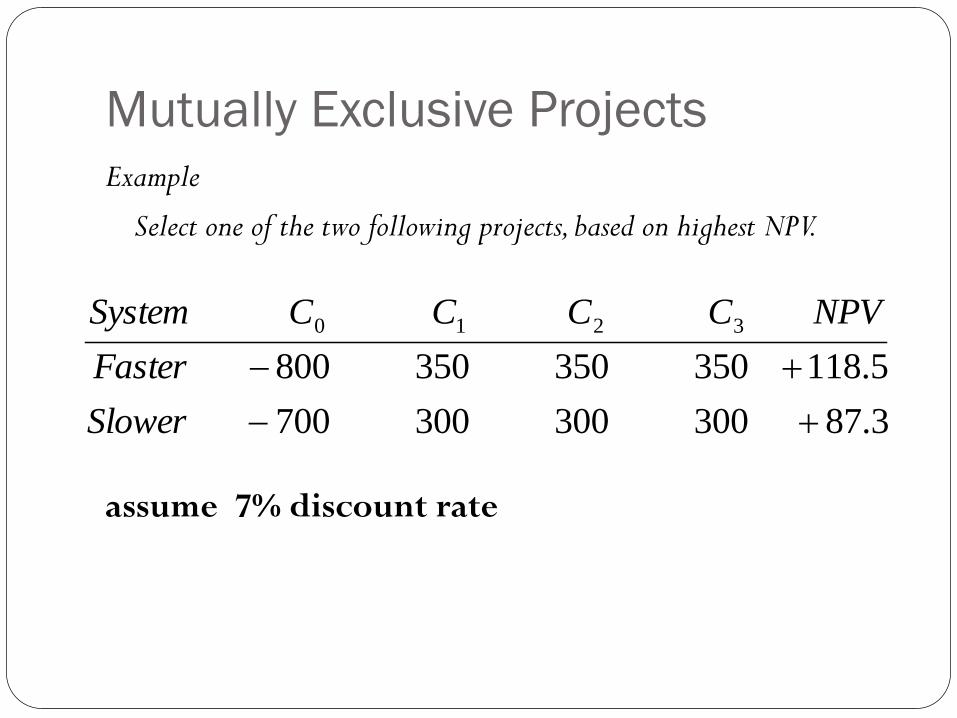

Mutually Exclusive Projects

Example

Select one of the two following projects, based on highest NPV.

assume 7% discount rate

3.87300300300700

5.118350350350800

3210

Slower

Faster

NPVCCCCSystem

Investment Timing

Sometimes you have the ability to defer an investment and

select a time that is more ideal at which to make the

investment decision. A common example involves a tree

farm. You may defer the harvesting of trees. By doing so,

you defer the receipt of the cash flow, yet increase the cash

flow.

Investment Timing

Example

You may purchase a computer anytime within the next five years.

While the computer will save your company money, the cost of

computers continues to decline. If your cost of capital is 10%

and given the data listed below, when should you purchase the

computer?

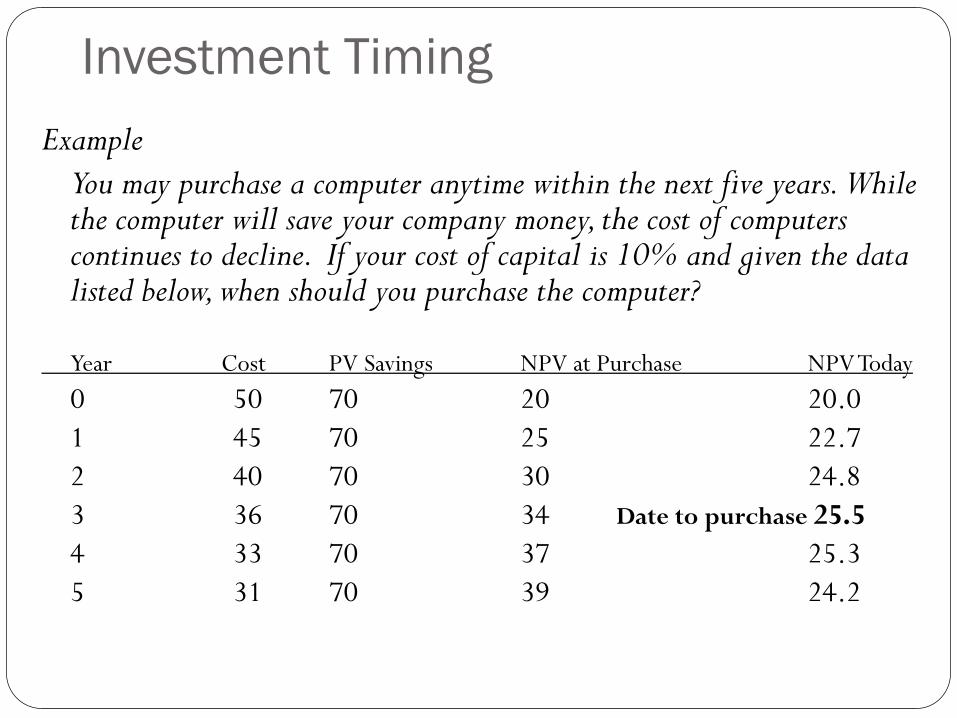

Investment Timing

Example

You may purchase a computer anytime within the next five years. While the computer will save your company money, the cost of computers continues to decline. If your cost of capital is 10% and given the data listed below, when should you purchase the computer?

Year Cost PV Savings NPV at Purchase NPV Today

0 50 70 20 20.0

1 45 70 25 22.7

2 40 70 30 24.8

3 36 70 34 Date to purchase 25.5

4 33 70 37 25.3

5 31 70 39 24.2

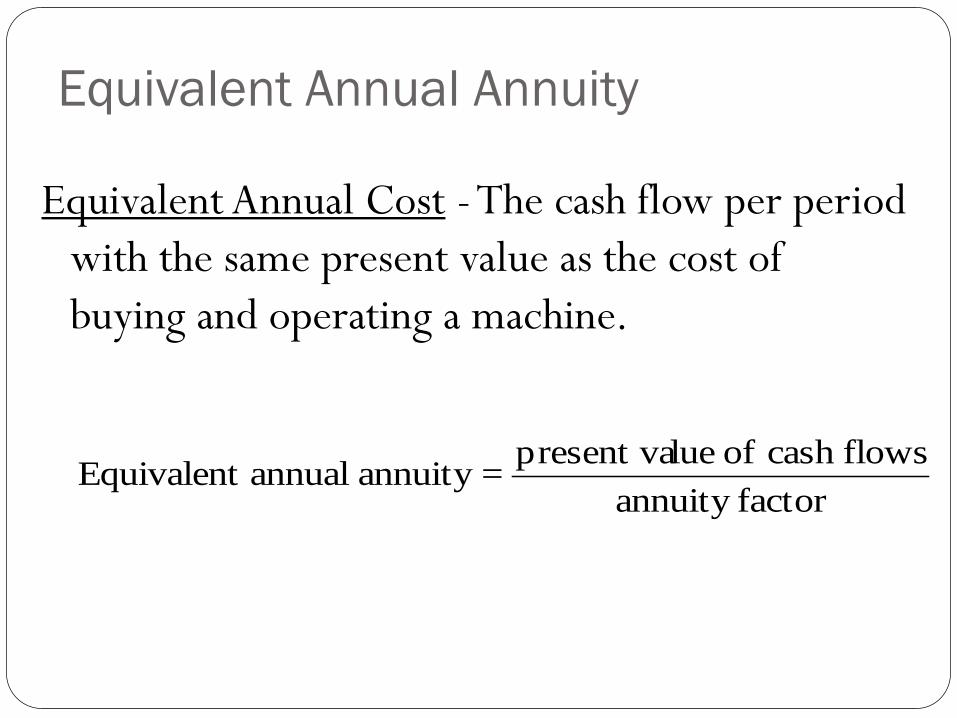

Equivalent Annual Annuity

Equivalent Annual Cost - The cash flow per period

with the same present value as the cost of

buying and operating a machine.

factorannuity

flowscash of luepresent va=annuity annual Equivalent

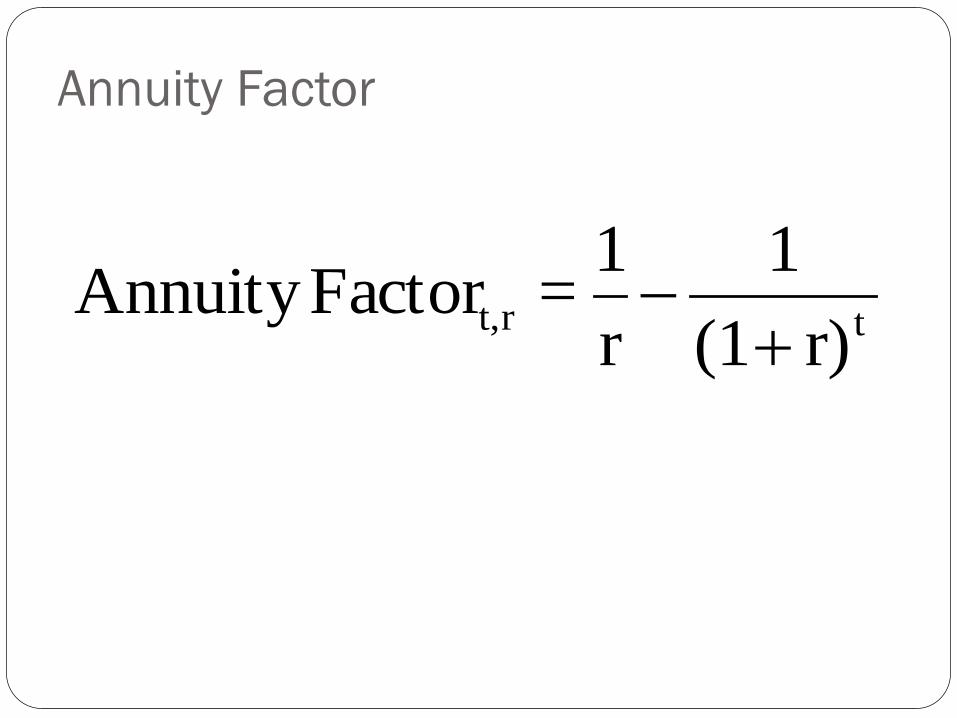

Annuity Factor

trt,r)(1

1

r

1=FactorAnnuity

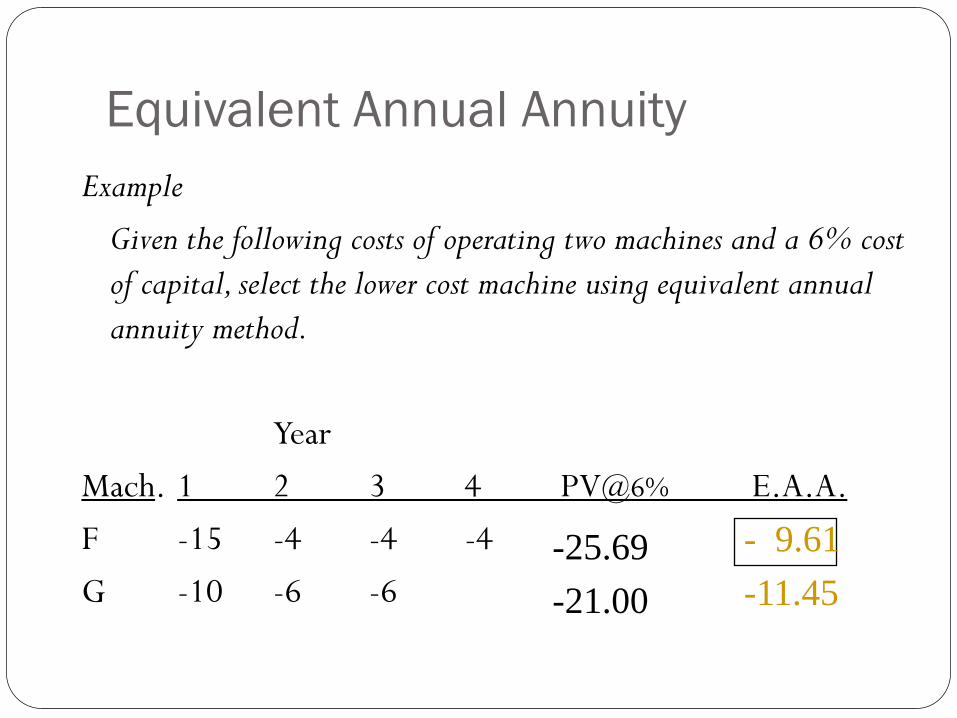

Equivalent Annual Annuity

Example

Given the following costs of operating two machines and a 6% cost

of capital, select the lower cost machine using equivalent annual

annuity method.

Year

Mach. 1 2 3 4 PV@6% E.A.A.

F -15 -4 -4 -4

G -10 -6 -6 -25.69

-21.00

- 9.61

-11.45

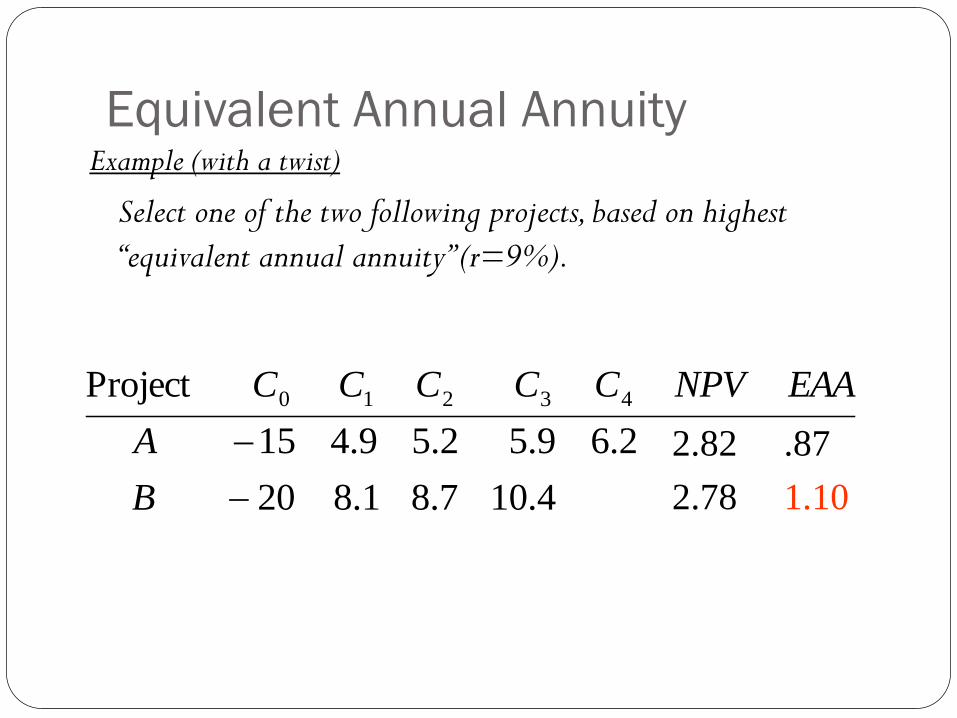

Equivalent Annual Annuity Example (with a twist)

Select one of the two following projects, based on highest

“equivalent annual annuity” (r=9%).

4.107.81.820

2.69.52.59.415

Project 43210

B

A

EAANPVCCCCC

2.82

2.78

.87

1.10

Capital Rationing

Capital Rationing - Limit set on the amount of funds available for investment. The act of placing restrictions on the amount of new investments or projects undertaken by a company. This is accomplished by imposing a higher cost of capital for investment consideration or by setting a ceiling on the specific sections of the budget.

Companies may want to implement capital rationing in situations where past returns of investment were lower than expected.

Capital Rationing

ABC Corp. has a cost of capital of 10% but that the company has undertaken too many projects, many of which are incomplete. This causes the company's actual return on investment to drop well below the 10% level. As a result, management decides to place a cap on the number of new projects by raising the cost of capital for these new projects to 15%. Starting fewer new projects would give the company more time and resources to complete existing projects.

Capital Rationing

Soft Rationing - Limits on available funds imposed by management.

Hard Rationing - Limits on available funds imposed by the unavailability of funds in the capital market.

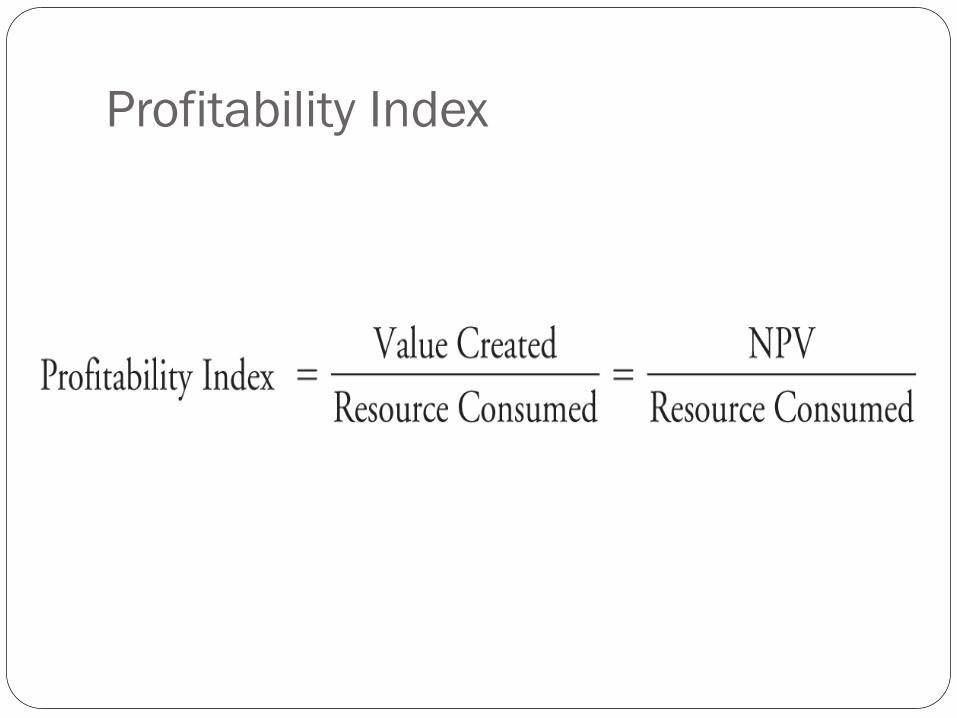

Profitability Index

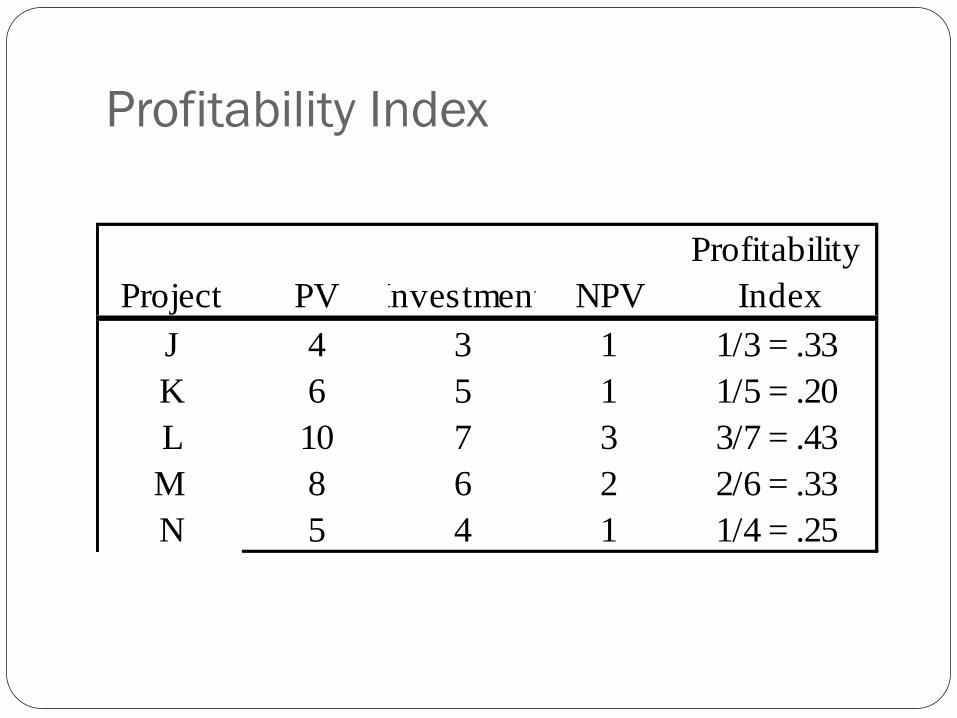

Profitability Index

Profitability

Project PV Investment NPV Index

J 4 3 1 1/3 = .33

K 6 5 1 1/5 = .20

L 10 7 3 3/7 = .43

M 8 6 2 2/6 = .33

N 5 4 1 1/4 = .25

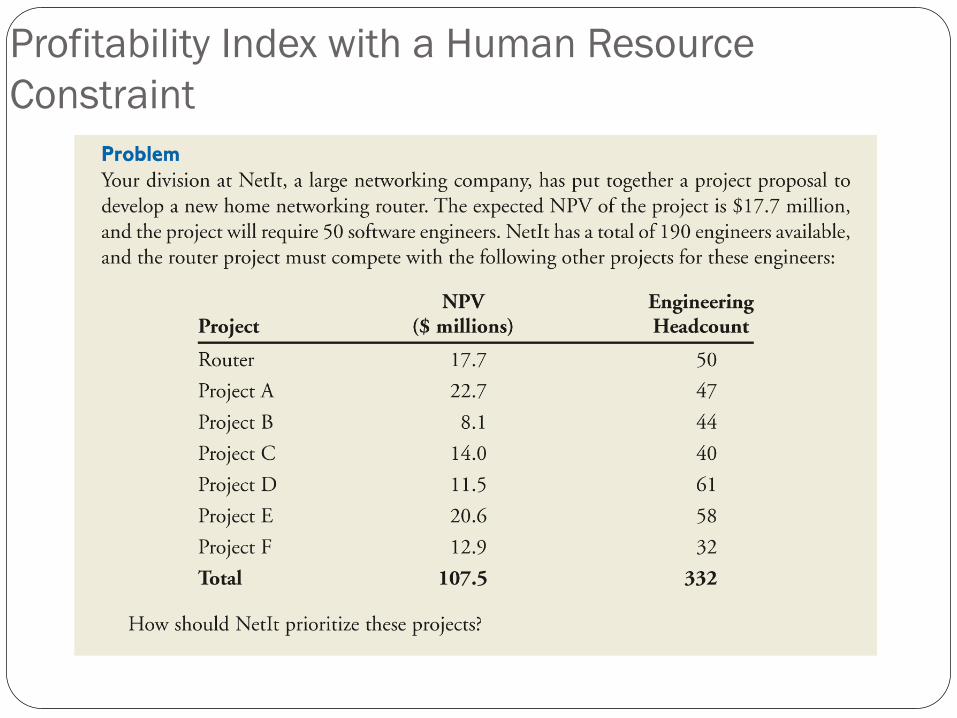

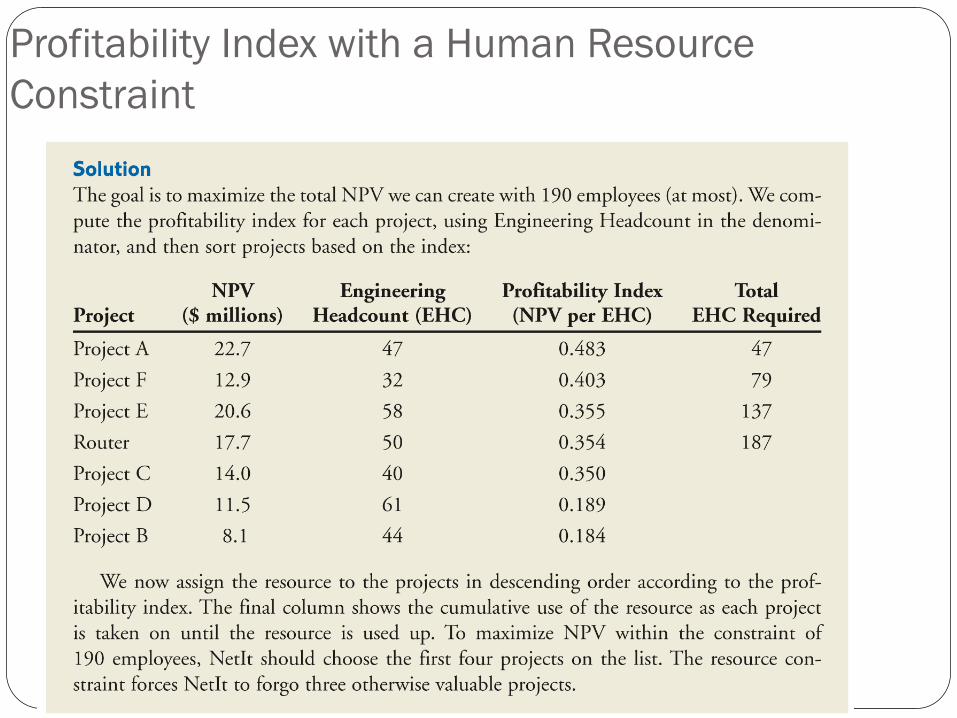

Profitability Index with a Human Resource

Constraint

Profitability Index with a Human Resource

Constraint

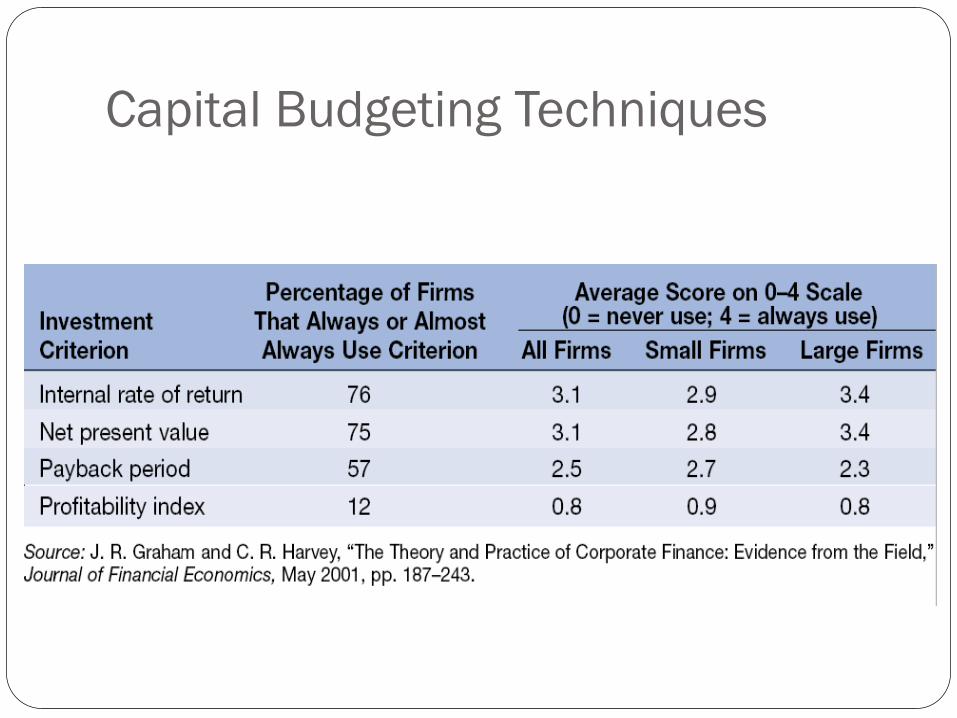

Capital Budgeting Techniques

EVA in Period n (When Capital Lasts

Forever)

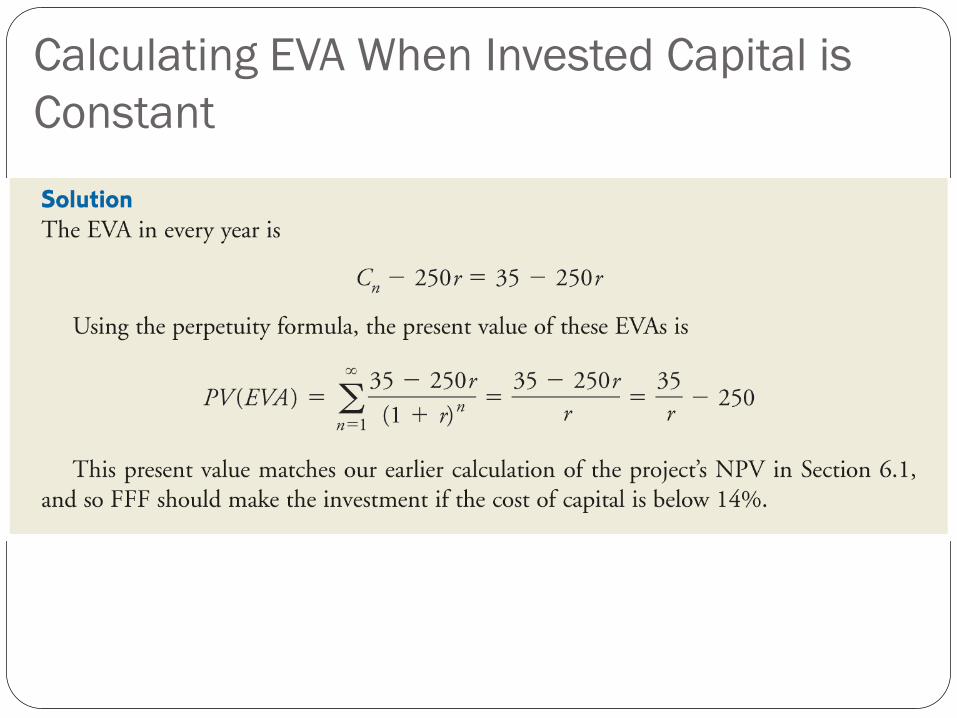

Calculating EVA When Invested Capital is

Constant

Calculating EVA When Invested Capital is

Constant

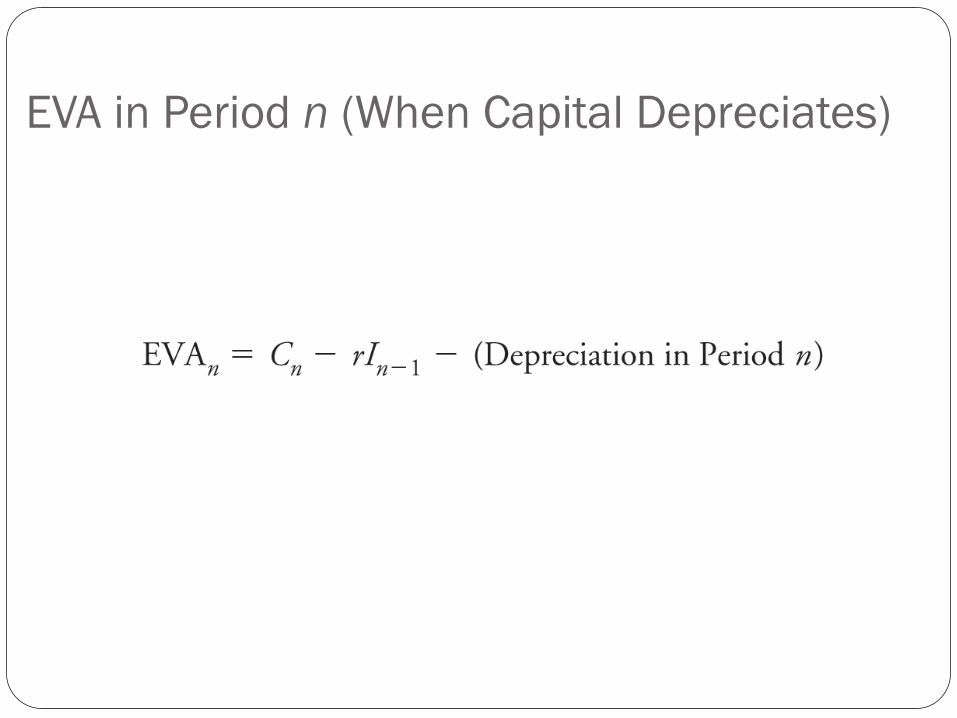

EVA in Period n (When Capital Depreciates)

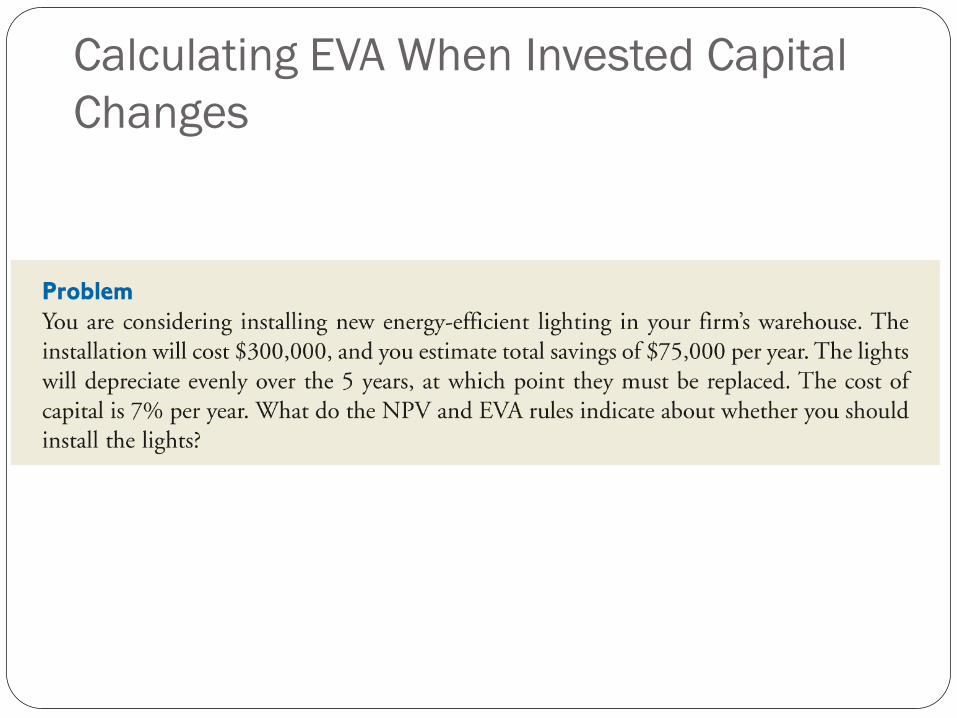

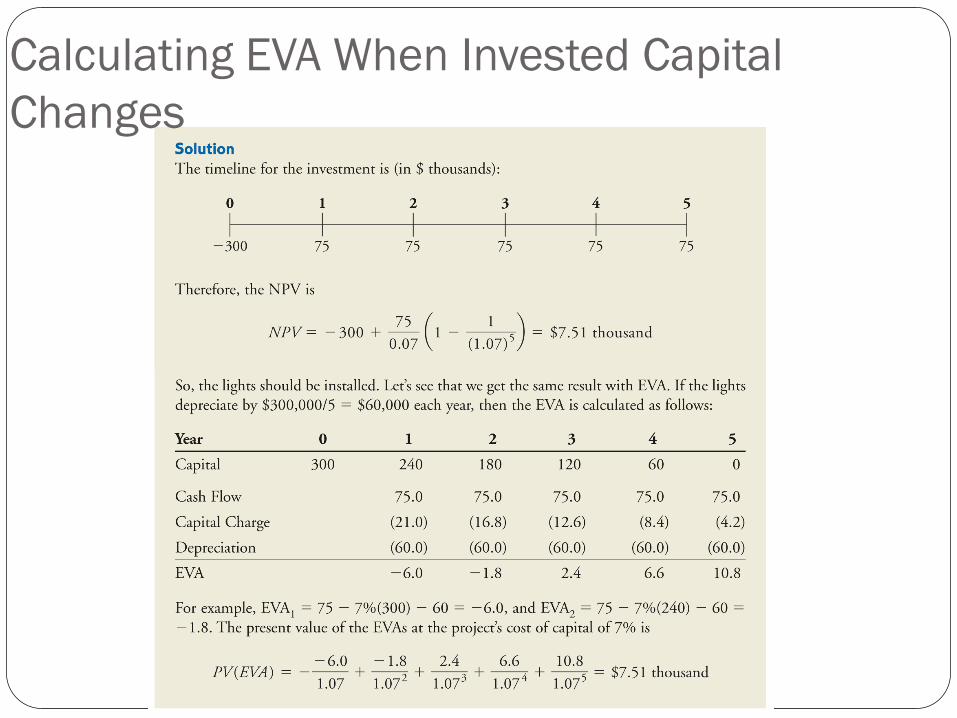

Calculating EVA When Invested Capital

Changes

Calculating EVA When Invested Capital

Changes